Embed Size (px)

Citation preview

February 28 - March 2, 2016

Oscar Landerretche M. Chairman of the Board

BMO CAPITAL MARKETS 25th GLOBAL METALS & MINING CONFERENCE

CODELCO: RECENT DEVELOPMENTS AND PERSPECTIVES

2 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

CODELCO HIGHLIGHTS

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 3

2015 Highlights

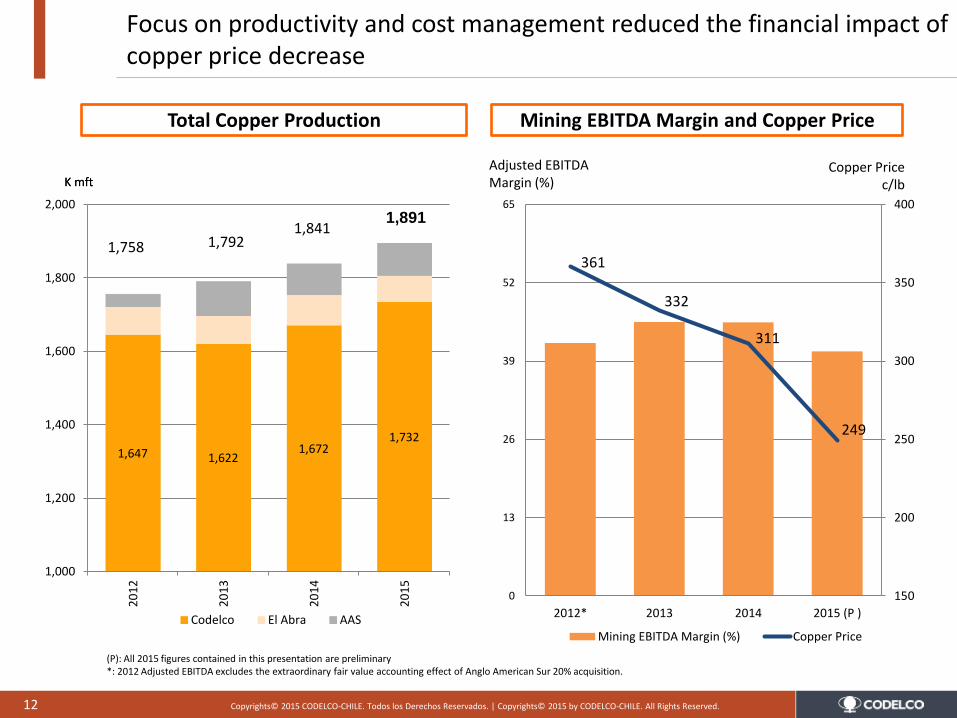

Copper Own Mine Production: increased by 3.6% in 2015 to 1,732 thousand tons, compared to 2014, especially due to the new production coming from Mina Ministro Hales. Total production achieved a historical record of 1,891 thousand tons.

Cost Reduction(P): C1 decreased 7.8% to 138.6 c/lb in 2015 compared to 2014, attributable to lower input prices and the intensification of the control cost program.

Financial Performance(P): Adjusted Mining EBITDA Margin reached 41%, despite the 20% drop in the average copper price in 2015 compared to 2014. (S&P A+, Moody’s A1)

Financing Program: In addition to the US$2 billion bond issuance in September, Codelco received US$600 million capital injection plus an approval to retain earnings for US$225 million, securing the financing for 2016.

Investment Program: During 2015 Codelco reduced its capex program by US$1 billion, without affecting the execution plan for the key projects under construction.

Safety(P): total global accident frequency and severity rates deceased by 30% and 39%, reaching 0.93* and 140**, respectively. No fatal accident.

(P): All 2015 figures contained in this presentation are preliminary * Lost Time Injuries/ Million Hours worked ** Lost days & days charged / Million Hours worked

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 4

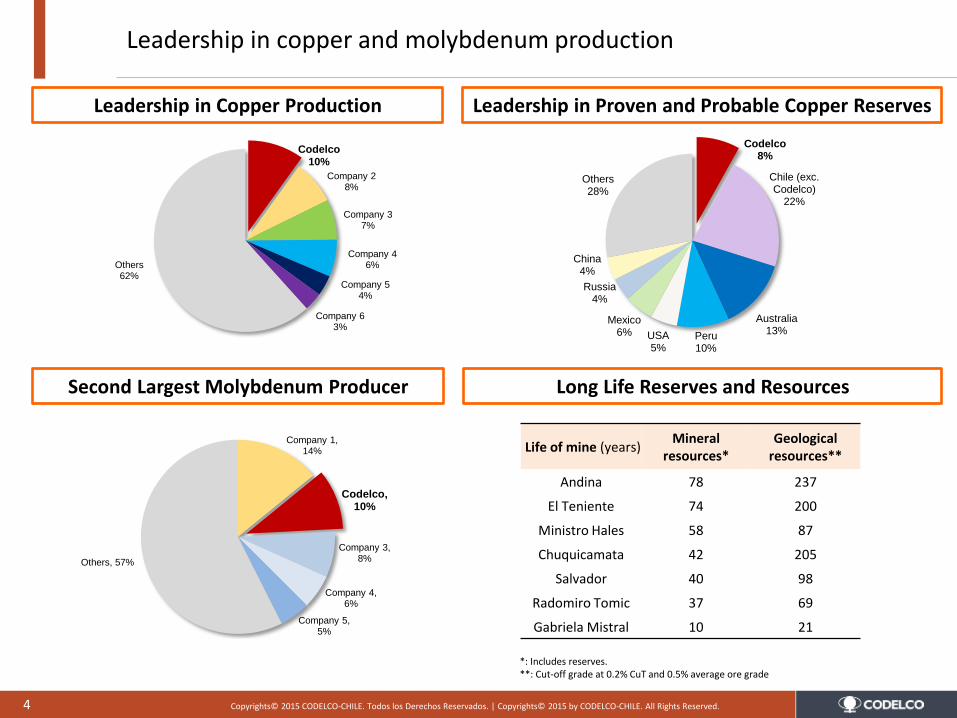

Leadership in copper and molybdenum production

Long Life Reserves and Resources

Leadership in Proven and Probable Copper Reserves Leadership in Copper Production

Second Largest Molybdenum Producer

Codelco 8%

Chile (exc. Codelco)

22%

Australia 13%

Peru 10%

USA 5%

Mexico 6%

Russia 4%

China 4%

Others 28%

Codelco 10%

Company 2 8%

Company 3 7%

Company 4 6%

Company 5 4%

Company 6 3%

Others 62%

Company 1, 14%

Codelco, 10%

Company 3, 8%

Company 4, 6%

Company 5, 5%

Others, 57%

Life of mine (years) Mineral

resources* Geological

resources**

Andina 78 237

El Teniente 74 200

Ministro Hales 58 87

Chuquicamata 42 205

Salvador 40 98

Radomiro Tomic 37 69

Gabriela Mistral 10 21

*: Includes reserves. **: Cut-off grade at 0.2% CuT and 0.5% average ore grade

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 5

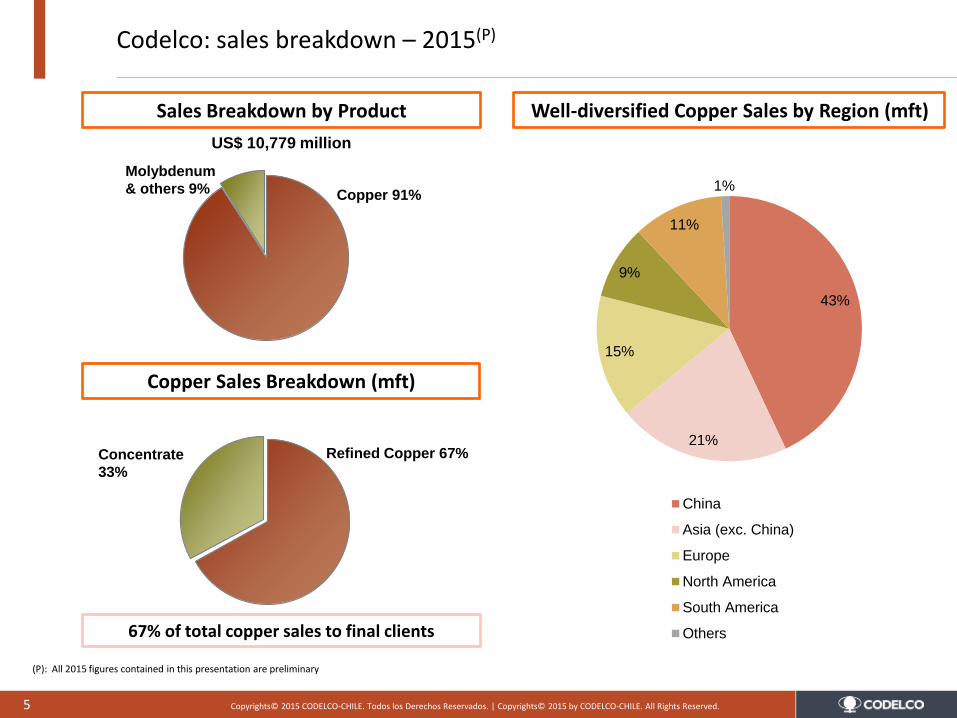

Codelco: sales breakdown – 2015(P)

Refined Copper 67% Concentrate

33%

Well-diversified Copper Sales by Region (mft)

Copper Sales Breakdown (mft)

Sales Breakdown by Product

43%

21%

15%

9%

11%

1%

China

Asia (exc. China)

Europe

North America

South America

Others67% of total copper sales to final clients

Copper 91%

Molybdenum

& others 9%

US$ 10,779 million

(P): All 2015 figures contained in this presentation are preliminary

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 6

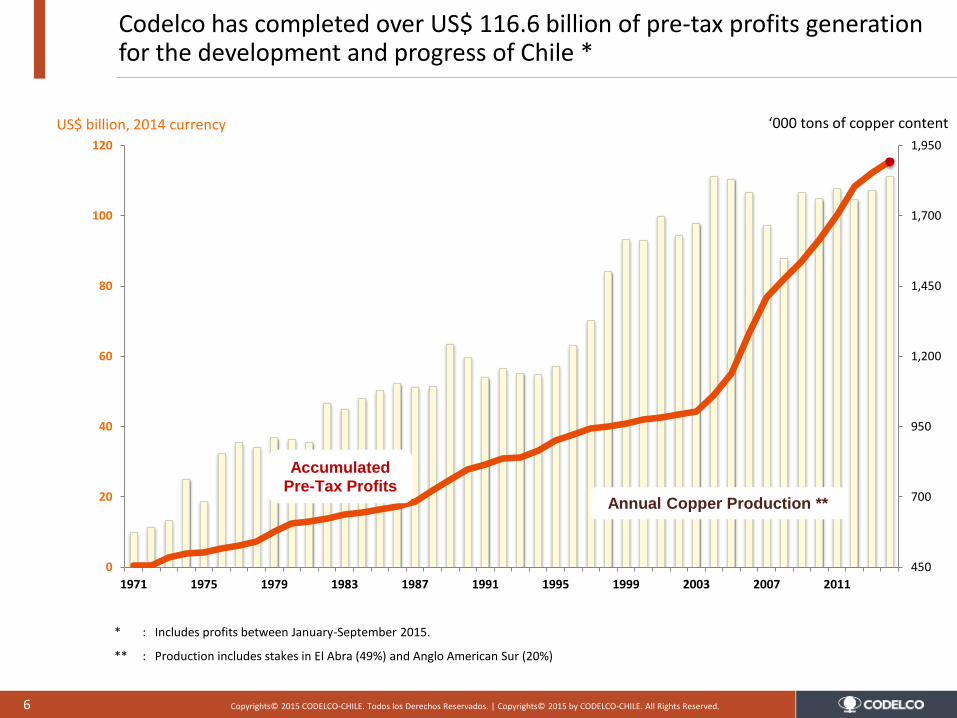

Codelco has completed over US$ 116.6 billion of pre-tax profits generation for the development and progress of Chile *

* : Includes profits between January-September 2015.

** : Production includes stakes in El Abra (49%) and Anglo American Sur (20%)

450

700

950

1,200

1,450

1,700

1,950

0

20

40

60

80

100

120

1971 1975 1979 1983 1987 1991 1995 1999 2003 2007 2011

Accumulated Pre-Tax Profits

Annual Copper Production **

US$ billion, 2014 currency ‘000 tons of copper content

7 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

COPPER MARKET

8 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

Copper price

c/lb

*: Year 2016 until February 15th.

50

100

150

200

250

300

350

400

450

500

2004 2006 2008 2010 2012 2014 2016

COPPER PRICE: 2004-2016*

Since 2011, the price of copper has shown a downward trend, which has intensified in recent times

• Increasing in world copper production has temporary turned the market into a surplus, in times of a slowdown and uncertainties on the Chinese economy growth.

• Increasing uncertainties in the world economy growth.

• Strong process of dollar appreciation.

• Important cost reductions from lower input prices, allow marginal producers to remain in business.

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 9

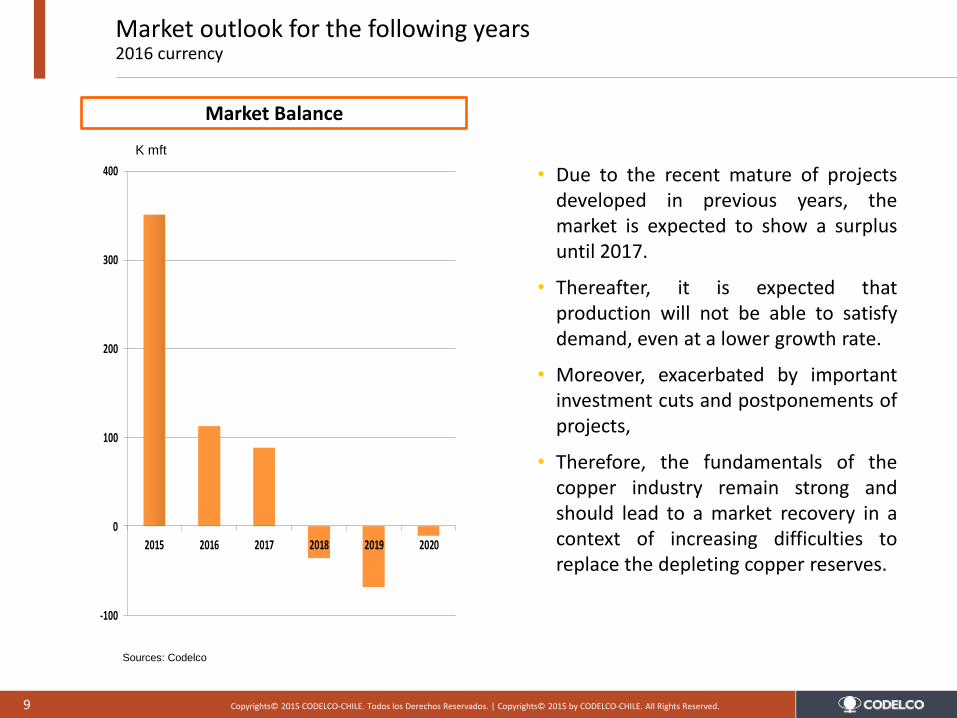

Market outlook for the following years 2016 currency

-100

0

100

200

300

400

2015 2016 2017 2018 2019 2020

Sources: Codelco

Market Balance

K mft

• Due to the recent mature of projects developed in previous years, the market is expected to show a surplus until 2017.

• Thereafter, it is expected that production will not be able to satisfy demand, even at a lower growth rate.

• Moreover, exacerbated by important investment cuts and postponements of projects,

• Therefore, the fundamentals of the copper industry remain strong and should lead to a market recovery in a context of increasing difficulties to replace the depleting copper reserves.

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 10

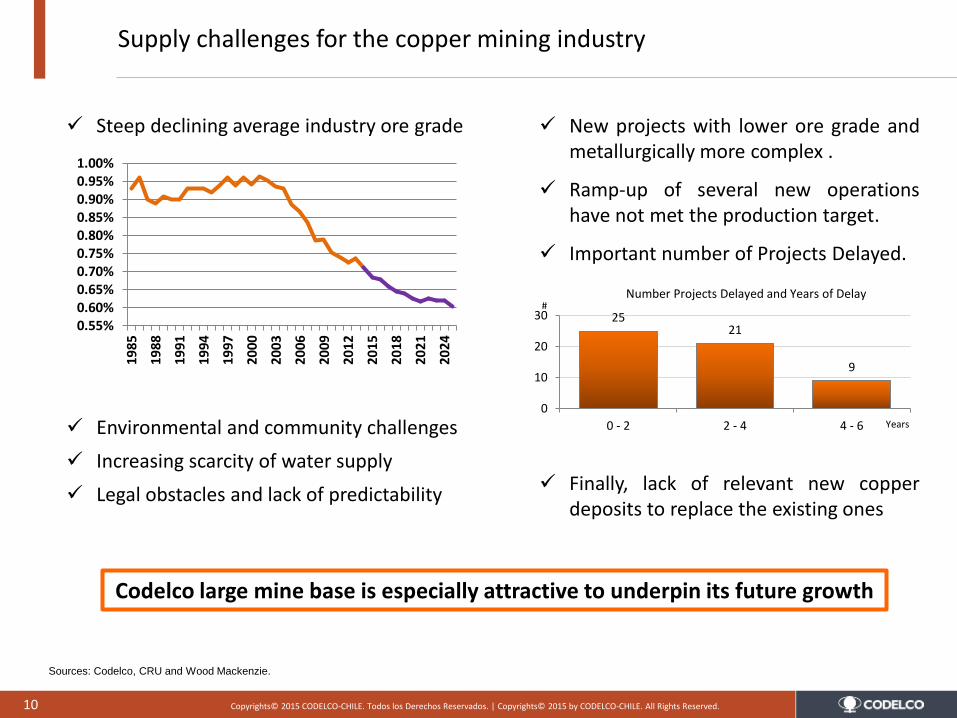

Steep declining average industry ore grade

Environmental and community challenges

Increasing scarcity of water supply

Legal obstacles and lack of predictability

New projects with lower ore grade and metallurgically more complex .

Ramp-up of several new operations have not met the production target.

Important number of Projects Delayed.

Finally, lack of relevant new copper deposits to replace the existing ones

Sources: Codelco, CRU and Wood Mackenzie.

Supply challenges for the copper mining industry

Number Projects Delayed and Years of Delay

0.55%0.60%0.65%0.70%0.75%0.80%0.85%0.90%0.95%1.00%

19

85

19

88

19

91

19

94

19

97

20

00

200

3

20

06

20

09

20

12

20

15

20

18

20

21

202

4

25 21

9

0

10

20

30

0 - 2 2 - 4 4 - 6

#

Years

Codelco large mine base is especially attractive to underpin its future growth

11 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

CODELCO’S OPERATING AND FINANCIAL REVIEW

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 12

Focus on productivity and cost management reduced the financial impact of copper price decrease

Adjusted EBITDA Margin (%)

Copper Price c/lb

(P): All 2015 figures contained in this presentation are preliminary *: 2012 Adjusted EBITDA excludes the extraordinary fair value accounting effect of Anglo American Sur 20% acquisition.

K mft

361

332

311

249

150

200

250

300

350

400

0

13

26

39

52

65

2012* 2013 2014 2015 (P )

Mining EBITDA Margin (%) Copper Price

K mft

1,647 1,622 1,672

1,732

1,000

1,200

1,400

1,600

1,800

2,000

20

12

20

13

20

14

20

15

Codelco El Abra AAS

1,758

1,891

1,792 1,841

Total Copper Production Mining EBITDA Margin and Copper Price

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 13

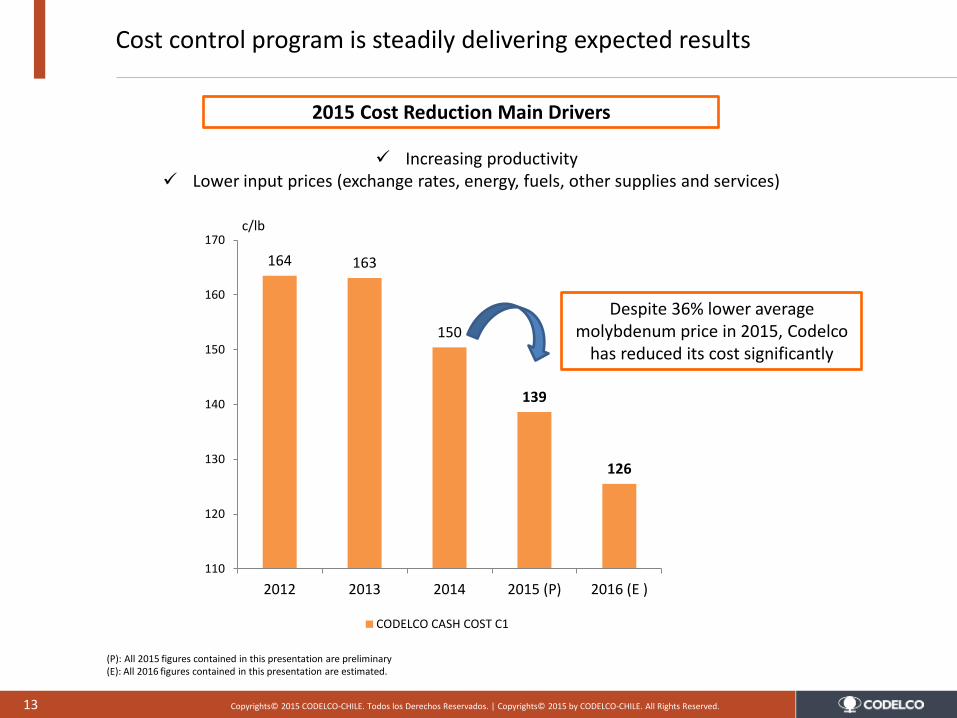

Cost control program is steadily delivering expected results

c/lb

164 163

150

139

126

110

120

130

140

150

160

170

2012 2013 2014 2015 (P) 2016 (E )

CODELCO CASH COST C1

Increasing productivity Lower input prices (exchange rates, energy, fuels, other supplies and services)

Despite 36% lower average molybdenum price in 2015, Codelco

has reduced its cost significantly

2015 Cost Reduction Main Drivers

(P): All 2015 figures contained in this presentation are preliminary (E): All 2016 figures contained in this presentation are estimated.

14 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

CODELCO’S CURRENT OPERATIONS AND THEIR FUTURE TRANSFORMATION

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 15

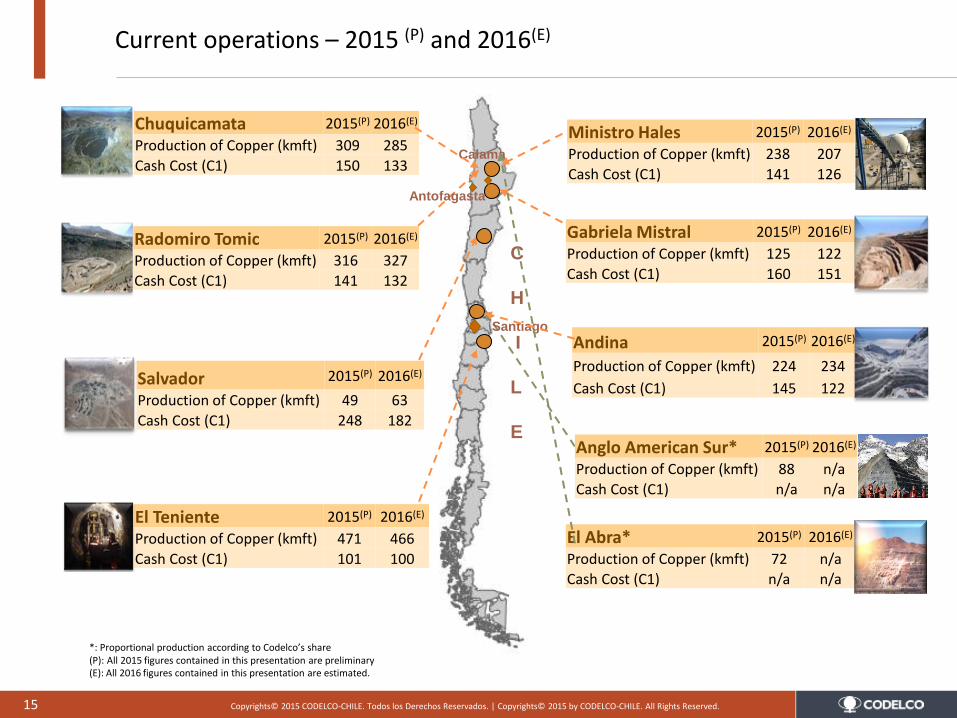

Current operations – 2015 (P) and 2016(E)

Santiago

Calama

C

H

I

L

E

Antofagasta

Radomiro Tomic 2015(P) 2016(E)

Production of Copper (kmft) 316 327

Cash Cost (C1) 141 132

Gabriela Mistral 2015(P) 2016(E)

Production of Copper (kmft) 125 122

Cash Cost (C1) 160 151

Salvador 2015(P) 2016(E)

Production of Copper (kmft) 49 63

Cash Cost (C1) 248 182

Andina 2015(P) 2016(E)

Production of Copper (kmft) 224 234

Cash Cost (C1) 145 122

El Teniente 2015(P) 2016(E)

Production of Copper (kmft) 471 466

Cash Cost (C1) 101 100

Chuquicamata 2015(P) 2016(E)

Production of Copper (kmft) 309 285

Cash Cost (C1) 150 133

El Abra* 2015(P) 2016(E)

Production of Copper (kmft) 72 n/a

Cash Cost (C1) n/a n/a

Anglo American Sur* 2015(P) 2016(E)

Production of Copper (kmft) 88 n/a

Cash Cost (C1) n/a n/a

Ministro Hales 2015(P) 2016(E)

Production of Copper (kmft) 238 207

Cash Cost (C1) 141 126

*: Proportional production according to Codelco’s share (P): All 2015 figures contained in this presentation are preliminary (E): All 2016 figures contained in this presentation are estimated.

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 16

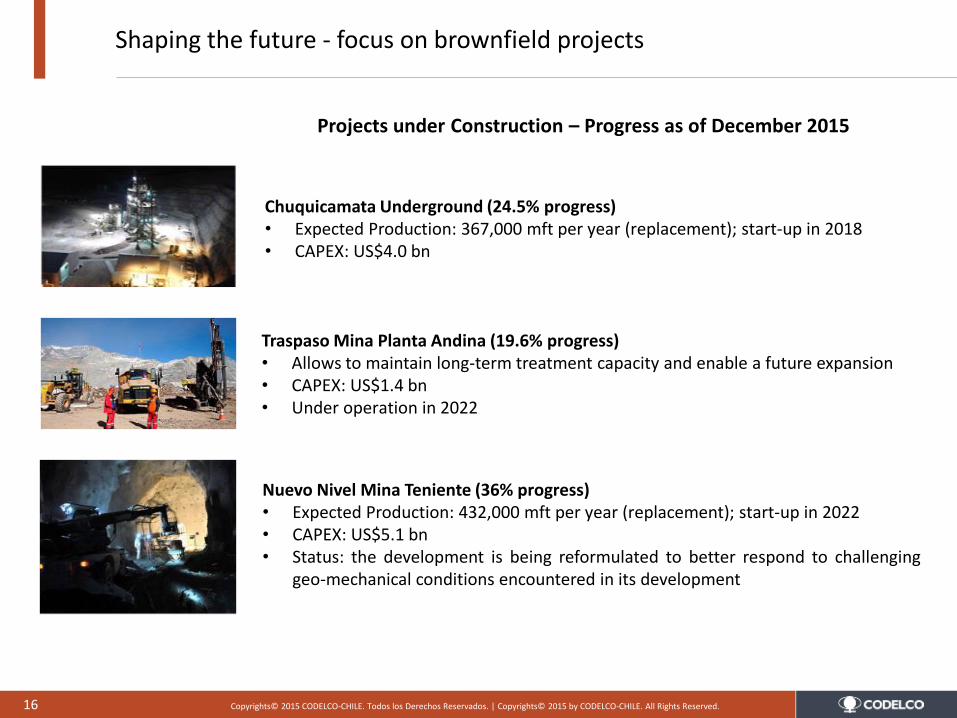

Shaping the future - focus on brownfield projects

Chuquicamata Underground (24.5% progress) • Expected Production: 367,000 mft per year (replacement); start-up in 2018 • CAPEX: US$4.0 bn

Traspaso Mina Planta Andina (19.6% progress) • Allows to maintain long-term treatment capacity and enable a future expansion • CAPEX: US$1.4 bn • Under operation in 2022

Projects under Construction – Progress as of December 2015

Nuevo Nivel Mina Teniente (36% progress) • Expected Production: 432,000 mft per year (replacement); start-up in 2022 • CAPEX: US$5.1 bn • Status: the development is being reformulated to better respond to challenging

geo-mechanical conditions encountered in its development

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 17

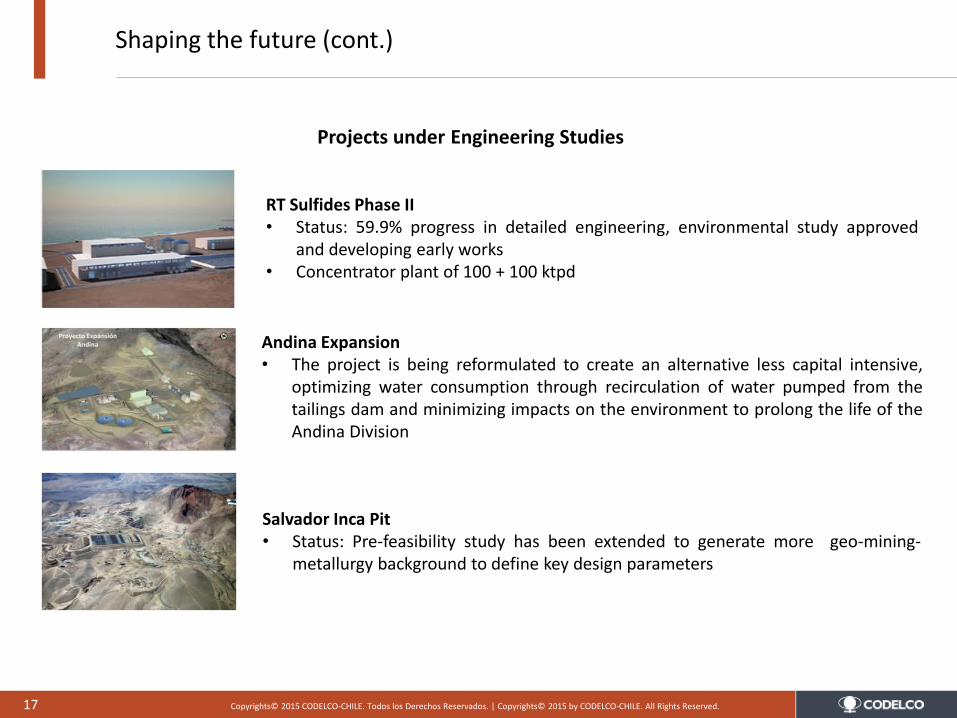

Shaping the future (cont.)

RT Sulfides Phase II • Status: 59.9% progress in detailed engineering, environmental study approved

and developing early works • Concentrator plant of 100 + 100 ktpd

Andina Expansion • The project is being reformulated to create an alternative less capital intensive,

optimizing water consumption through recirculation of water pumped from the tailings dam and minimizing impacts on the environment to prolong the life of the Andina Division

Projects under Engineering Studies

Salvador Inca Pit • Status: Pre-feasibility study has been extended to generate more geo-mining-

metallurgy background to define key design parameters

18 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

CODELCO STRATEGY

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 19

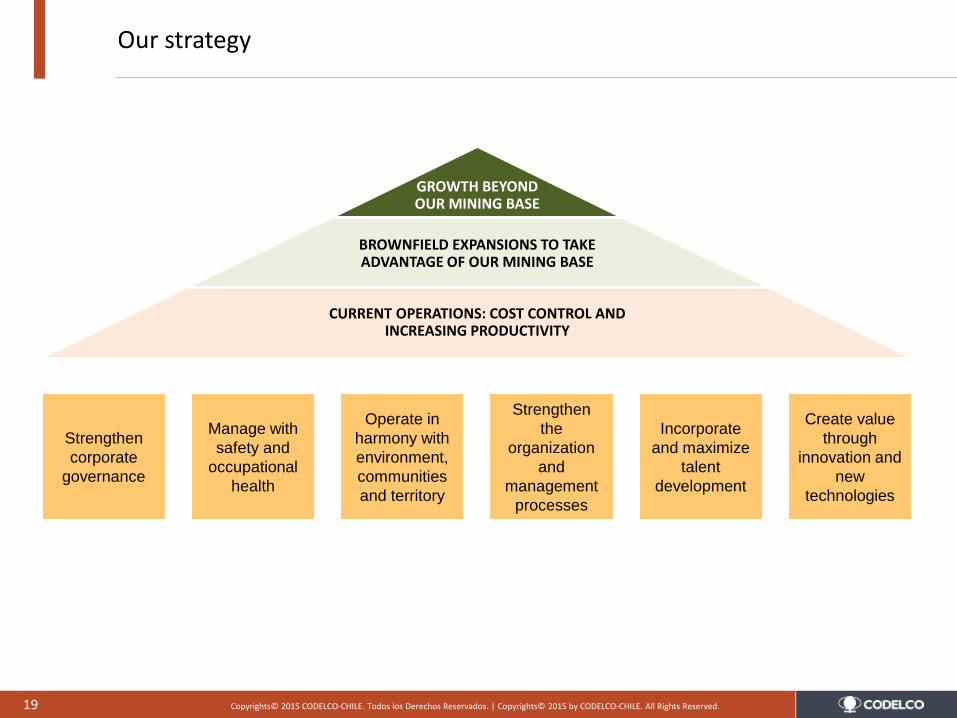

Our strategy

Strengthen

corporate

governance

Manage with

safety and

occupational

health

Operate in

harmony with

environment,

communities

and territory

Strengthen

the

organization

and

management

processes

Create value

through

innovation and

new

technologies

Incorporate

and maximize

talent

development

GROWTH BEYOND OUR MINING BASE

BROWNFIELD EXPANSIONS TO TAKE ADVANTAGE OF OUR MINING BASE

CURRENT OPERATIONS: COST CONTROL AND INCREASING PRODUCTIVITY

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 20

Innovations oriented to three key objectives

• Solving operational difficulties

– Open pit dangerous areas / Remote mining.

– Operational control / Robotic concentrates sampler.

– Preventive maintenance / Big data.

• Transforming resources into reserves

– Higher productivity and safety / Semiautonomous trucks.

– Increasing impurities / Complex concentrates processing.

• Breakthrough to achieve competitive advantages

– Higher productivity and safety / Continuous mining.

– Higher productivity and lower environmental impact / Leaching sulfides.

ROBOTIC CONCENTRATES SAMPLER

LHD SEMIAUTONOMOUS

LEACHING SULFIDES

21 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

FINANCING PLAN

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 22

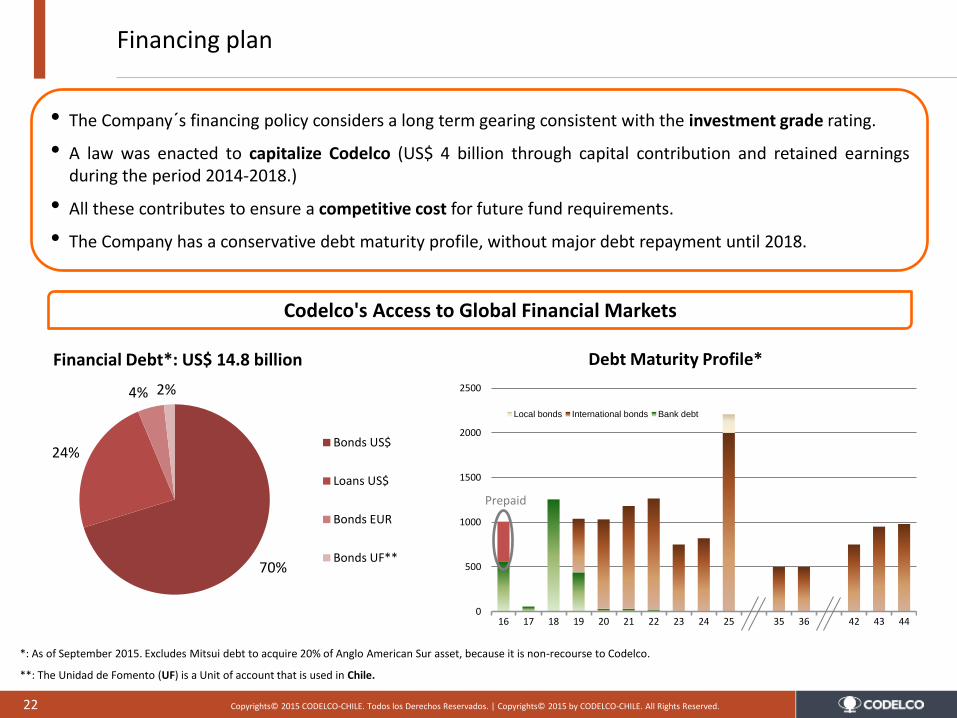

0

500

1000

1500

2000

2500

16 17 18 19 20 21 22 23 24 25 35 36 42 43 44

Local bonds International bonds Bank debt

Financing plan

Codelco's Access to Global Financial Markets

70%

24%

4% 2%

Financial Debt*: US$ 14.8 billion

Bonds US$

Loans US$

Bonds EUR

Bonds UF**

*: As of September 2015. Excludes Mitsui debt to acquire 20% of Anglo American Sur asset, because it is non-recourse to Codelco.

**: The Unidad de Fomento (UF) is a Unit of account that is used in Chile.

Debt Maturity Profile*

• The Company´s financing policy considers a long term gearing consistent with the investment grade rating.

• A law was enacted to capitalize Codelco (US$ 4 billion through capital contribution and retained earnings during the period 2014-2018.)

• All these contributes to ensure a competitive cost for future fund requirements.

• The Company has a conservative debt maturity profile, without major debt repayment until 2018.

Prepaid

23 Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved.

SUMMARY

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 24

In summary

Codelco’s strength and future growth are based on:

• High Quality Assets and Resource Base

– 8% worldwide reserves.

– World largest copper producer, with 10% of industry share.

– Second largest molybdenum producer, with 10% of industry share.

– Long-life reserve base (63 years for reserves and mineral resources; 191 years for geological resources.)

• Focus on operating cost control and productivity

– Fully integrated competitive cost operations (C1: 126 c/lb (E), expected for 2016).

– Strong operating margins (2015 Adjusted Mining EBITDA margin reached 41% (P).)

• Investing through the cycle

– Excellent brownfield projects under execution.

– Robust pipeline of brownfield project throughout operations under engineering study status.

• Innovation and technology oriented to enhance productivity

• Experienced management with proven track record

• Owner strong support (US$4 billion approved capitalization program (2014-2018)) (P): All 2015 figures contained in this presentation are preliminary (E): All 2016 figures contained in this presentation are estimated.

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 25

This presentation has been prepared by Corporación Nacional del Cobre de Chile (“Codelco” or the “Company”) This presentation does

not constitute or form part of an offer or any solicitation to any other person or to the general public to subscribe for or otherwise acquire

securities issued by Codelco in any jurisdiction or an inducement to enter into investment activity, nor shall it (or any part of it) or the fact

of its distribution or availability, form the basis of, or be relied on in connection with, or act as any inducement to enter into, any contract or

commitment or investment decision.

The information contained in this independently presentation has not been verified and is subject to change without notice. No

representation or warranty express or implied is made as to and no reliance should be placed on, the fairness, accuracy, completeness or

correctness of the information or the opinions contained herein. None of the Company, any of its respective affiliates, advisers or

representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this

presentation or its contents or otherwise arising in connection with the presentation.

This presentation is only for persons having professional experience in matters relating to investments and must not be acted or relied on

by people who are not relevant persons.

This presentation includes ‘forward-looking statements’. These statements may include words such as “anticipated”, “believe”, “intend”,

“estimate”, “expect”, “preliminary” and words of similar meaning. All statements other than statements of historical facts included in this

presentation, including, without limitation, those regarding the Company’s financial position, business strategy, plans and objectives of

management for future operations (including development plans and objectives relating to the Company’s products and services) are

forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors

that could cause the actual results, performance or achievements of the Company to be materially different from future results,

performance or achievements expressed or implied by such forward looking statements. Such forward-looking statements are based on

numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will

operate in the future. These forward-looking statements speak only as at the date of this presentation. The Company expressly disclaims

any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect any

change in the Company’s expectations with regard thereto or any change in events, conditions or circumstances on which any such

statement is based.

As is standard in the industry, CODELCO divides its mineral holdings into two categories, reserves and resources. Resources are ore

bodies of economic value that have been identified and evaluated through exploration, reconnaissance and sampling. Reserves are the

portion of the resource that can be extracted based on an economic, environmental and technological analysis set forth in the mining

plan. Reserves and resources are both subdivided further, based on the degree of knowledge that CODELCO has of their extent and

composition. The system used by CODELCO for categorizing mineral ore is widely used within the mining industry (and codified in such

international regulations as the Joint One Reserves Committee (JORC) code of Australia, the South African Mineral Resources

Committee (SAMREC), and the Reporting Code of Great Britain). Other systems of categorization are also used; one such system is that

used by the U.S. Geological Survey. This presentation may not be taken away with you. The contents of this presentation may not be

reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose.

Disclaimer

February 28 - March 2, 2016

Oscar Landerretche M. Chairman of the Board

BMO CAPITAL MARKETS 25th GLOBAL METALS & MINING CONFERENCE

CODELCO: RECENT DEVELOPMENTS AND PERSPECTIVES

Copyrights© 2015 CODELCO-CHILE. Todos los Derechos Reservados. | Copyrights© 2015 by CODELCO-CHILE. All Rights Reserved. 27

Notes