Embed Size (px)

Citation preview

Code of Practice on LocalAuthority Accounting in the United Kingdom

2014/15 Accounts

disclosurechecklist

CIPFA, the Chartered Institute of Public Finance and Accountancy, is the professional body for people in public finance. Our 14,000 members work throughout the public services, in national audit agencies, in major accountancy firms, and in other bodies where public money needs to be effectively and efficiently managed. As the world’s only professional accountancy body to specialise in public services, CIPFA’s qualifications are the foundation for a career in public finance. We also champion high performance in public services, translating our experience and insight into clear advice and practical services. Globally, CIPFA shows the way in public finance by standing up for sound public financial management and good governance.

CIPFA values all feedback it receives on any aspects of its publications and publishing programme. Please send your comments to [email protected]

Our range of high quality advisory, information and consultancy services help public bodies – from small councils to large central government departments – to deal with the issues that matter today. And our monthly magazine, Public Finance, is the most influential and widely read periodical in the field.

Here is just a taste of what we provide:

� TISonline – online financial management guidance � Recruitment services

� Benchmarking � Research and statistical information

� Advisory services � Seminars and conferences

� Professional networks � Education and training

� Property and asset management services � CIPFA Regions – UK-wide events run by CIPFA members

Call or visit our website to find out more about CIPFA, our products and services – and how we can support you and your organisation in these unparalleled times.

020 7543 5600 [email protected] www.cipfa.org

Environmental Information

This CIPFA publication is printed on certified FSC mixed sources coated grade stock containing 50% recovered waste and 50% virgin fibre.

Printed on stock sourced from well-managed forests, ISO 14001.

Code of Practice on LocalAuthority Accounting in the United Kingdom

2014/15 Accounts

disclosurechecklist

Published by:

CIPFA \ THE CHARTERED INSTITUTE OF PUBLIC FINANCE AND ACCOUNTANCY

3 Robert Street, London WC2N 6RL

020 7543 5600 \ [email protected] \ www.cipfa.org

© August 2013 CIPFA

ISBN 978 1 84508 410 3

Edited by Sarah Williams ([email protected])

Designed and typeset by Ministry of Design, Bath (www.ministryofdesign.co.uk)

Printed by Trident Printing, London

No responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication can be accepted by the authors or publisher.

While every care has been taken in the preparation of this publication, it may contain errors for which the publisher and authors cannot be held responsible.

Apart from any fair dealing for the purposes of research or private study, or criticism or review, as permitted under the Copyright, Designs and Patents Act, 1988, this publication may be reproduced, stored or transmitted, in any form or by any means, only with the prior permission in writing of the publishers, or in the case of reprographic reproduction in accordance with the terms of licences issued by the Copyright Licensing Agency Ltd. Enquiries concerning reproduction outside those terms should be sent to the publishers at the above mentioned address.

Code of Practice on Local Authority Accounting in the United Kingdom Page 1

Introduction

The Code of Practice on Local Authority Accounting in the United Kingdom 2014/15 is based on International Financial Reporting Standards (IFRSs) and has been developed by the CIPFA/LASAAC Code Board under the oversight of the Financial Reporting Advisory Board.

The 2014/15 Code has been prepared on the basis of accounting standards and interpretations in effect for accounting periods commencing on or before 1 January 2014. It applies to accounting periods commencing on or after 1 April 2014.

This Disclosure Checklist reflects the requirements and format of the Code.

Disclosure Checklist for 2014/15 Accounts

Page 2 Code of Practice on Local Authority Accounting in the United Kingdom

Code of Practice on Local Authority Accounting in the United Kingdom Page 3

Disclosure Checklist 2014/15 Accounts England

This checklist identifies the requirements of the Code of Practice on Local Authority Accounting in the United Kingdom 2014/15. It applies to accounting periods commencing on or after 1 April 2014.

This checklist is intended for use as an aide-memoire by those who prepare and audit local authority accounts to ensure that the requirements of the Code are met. The checklist is in the form of a series of questions. If the answer to a question is ‘yes’, the Code is being complied with. If the answer is ‘no’, then a justification for departing from the Code should be given and potentially disclosed in the accounts, where the impact of departure is material.

Disclosure Checklist for 2014/15 Accounts – England

Page 4 Code of Practice on Local Authority Accounting in the United Kingdom

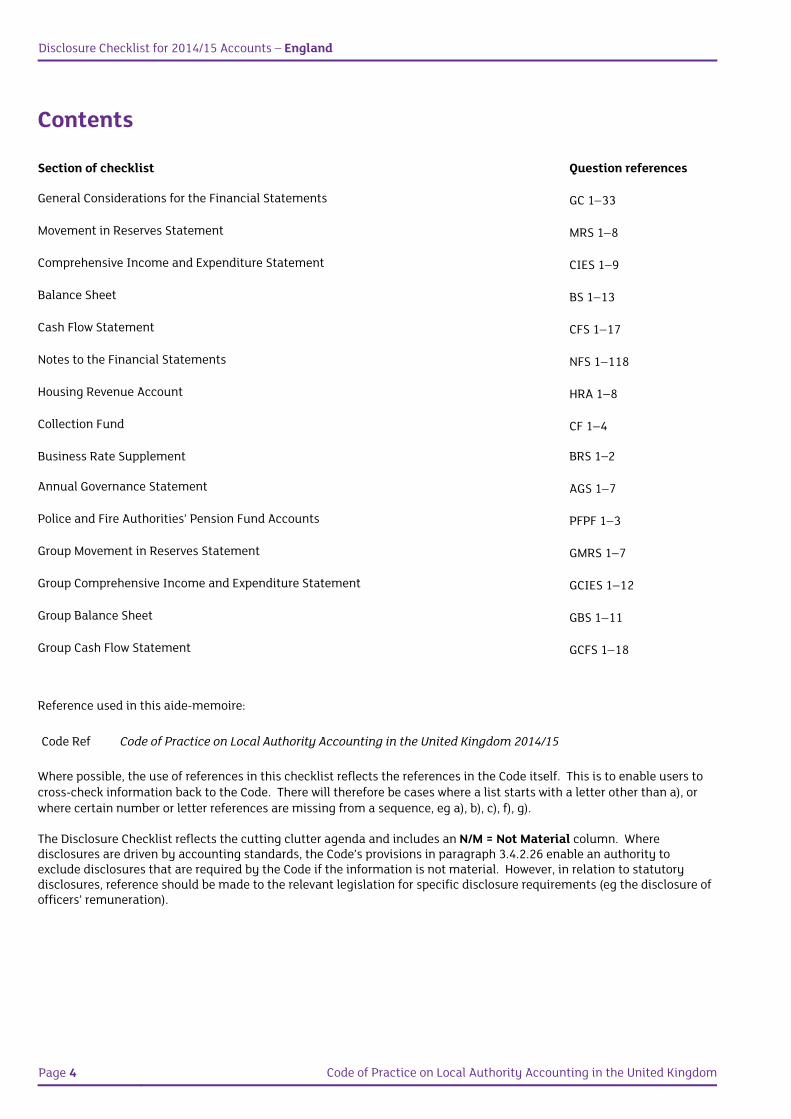

Contents

Section of checklist Question references

General Considerations for the Financial Statements GC 133

Movement in Reserves Statement MRS 18

Comprehensive Income and Expenditure Statement CIES 19

Balance Sheet BS 113

Cash Flow Statement CFS 117

Notes to the Financial Statements NFS 1118

Housing Revenue Account HRA 18

Collection Fund CF 14

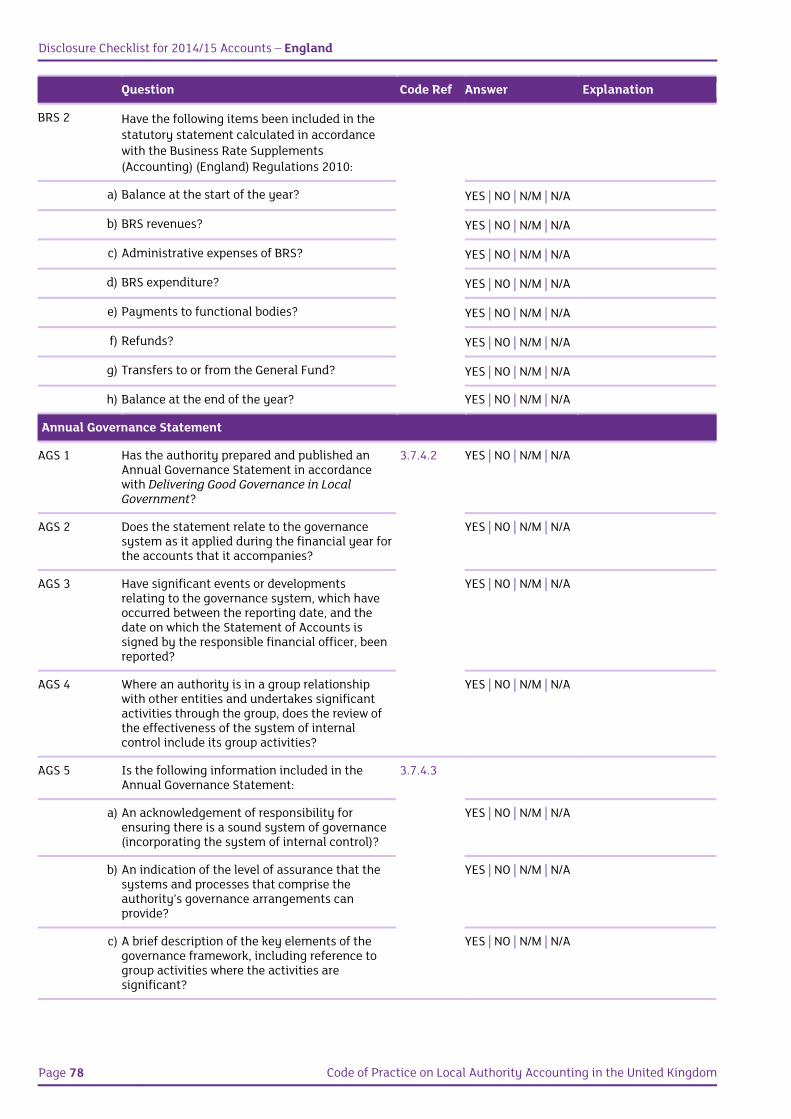

Business Rate Supplement BRS 1–2

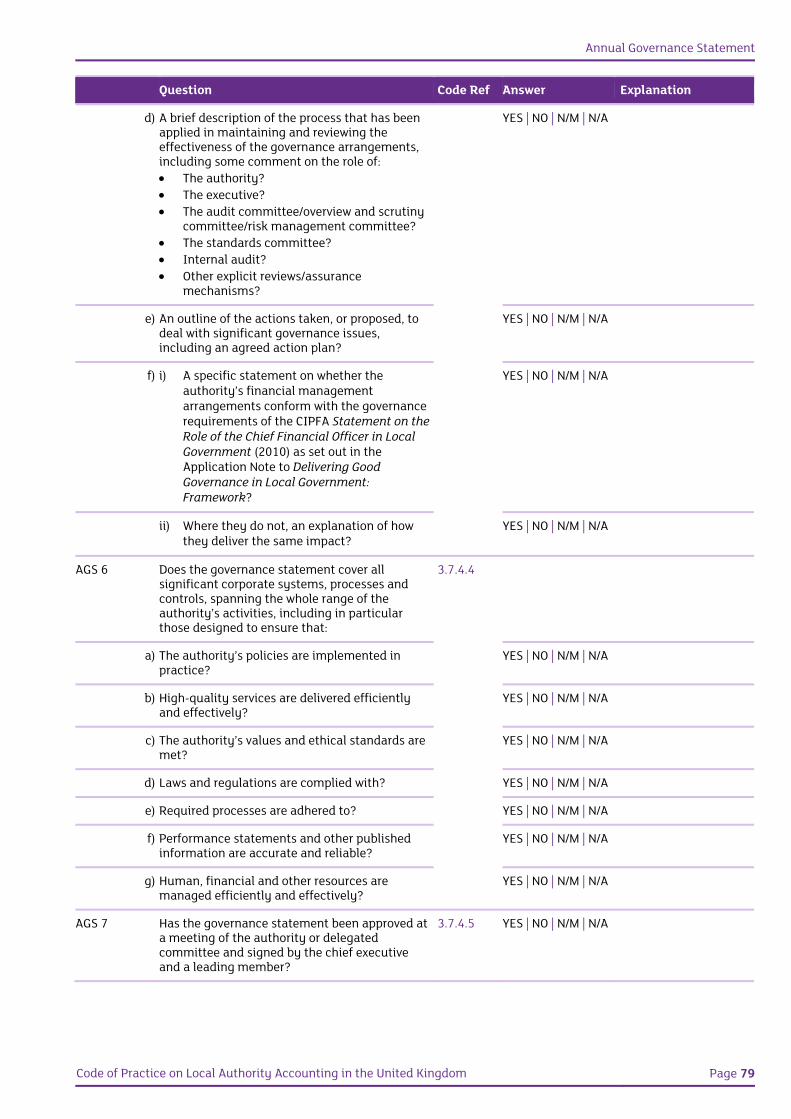

Annual Governance Statement AGS 17

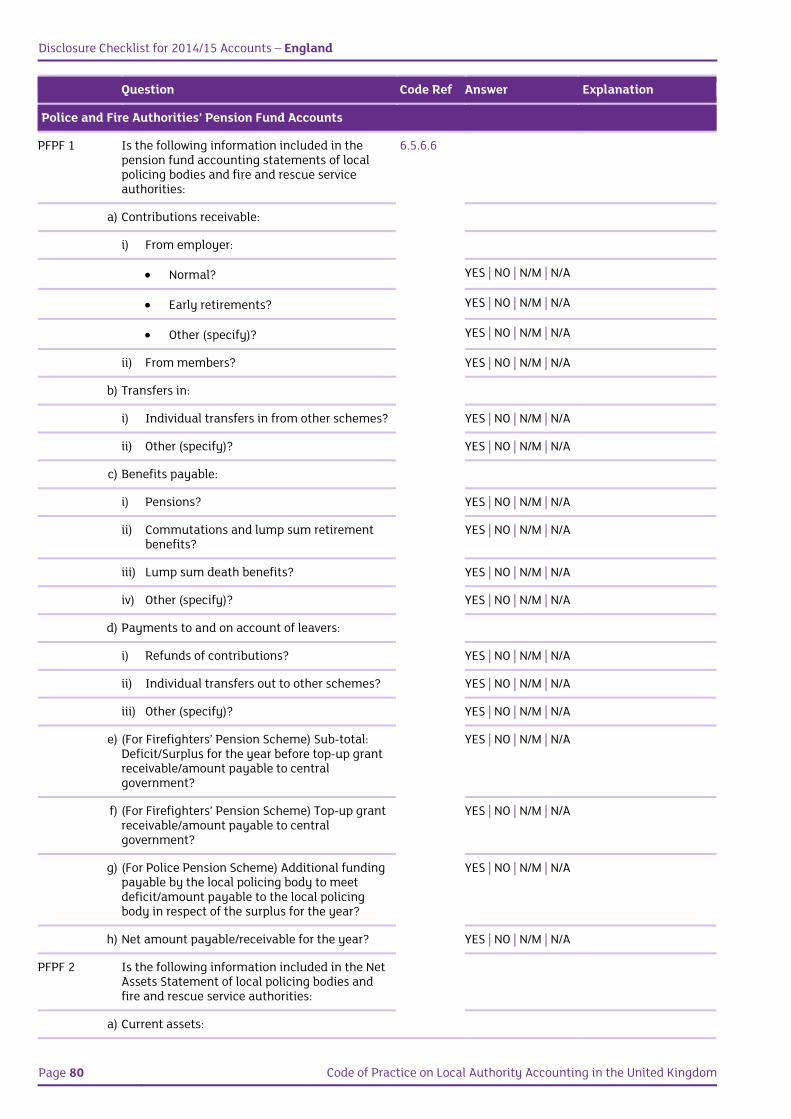

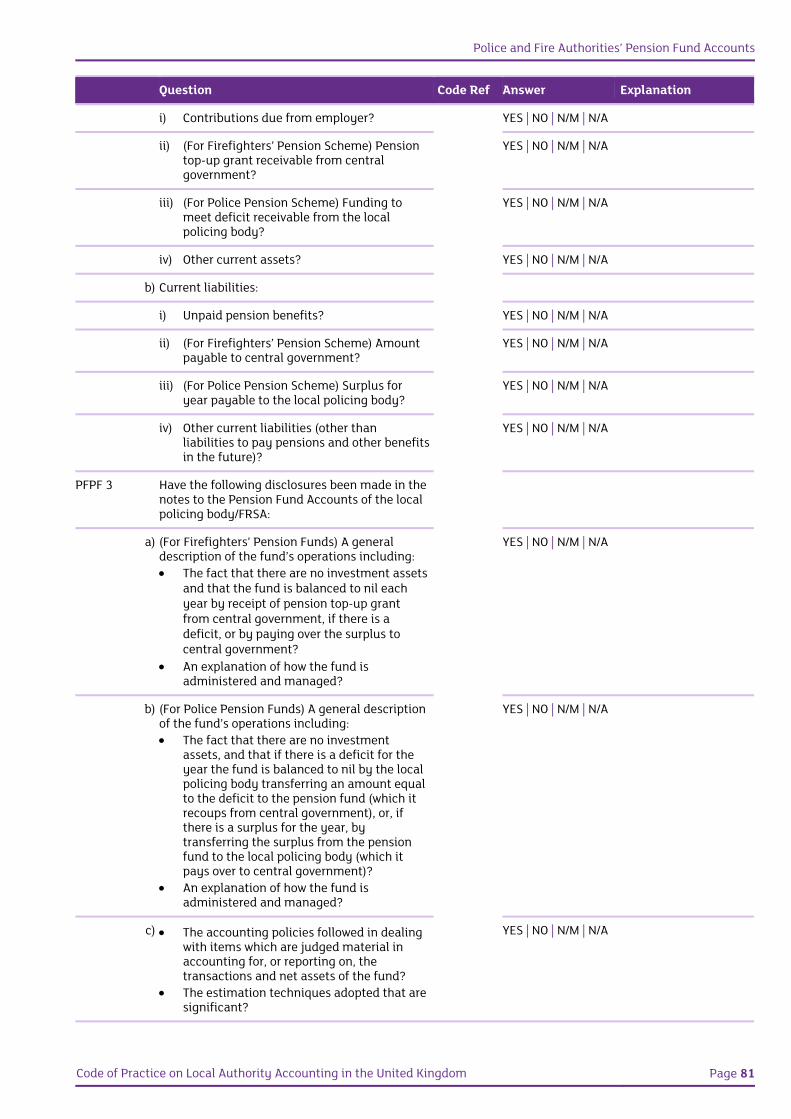

Police and Fire Authorities’ Pension Fund Accounts PFPF 13

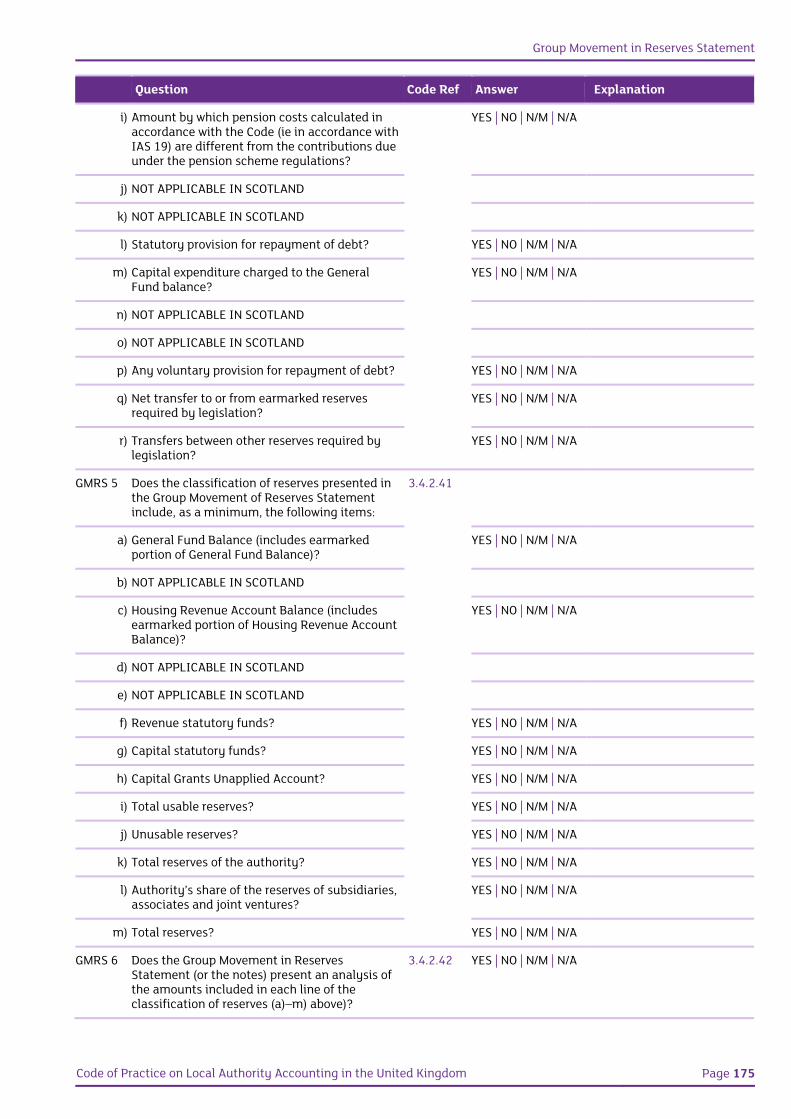

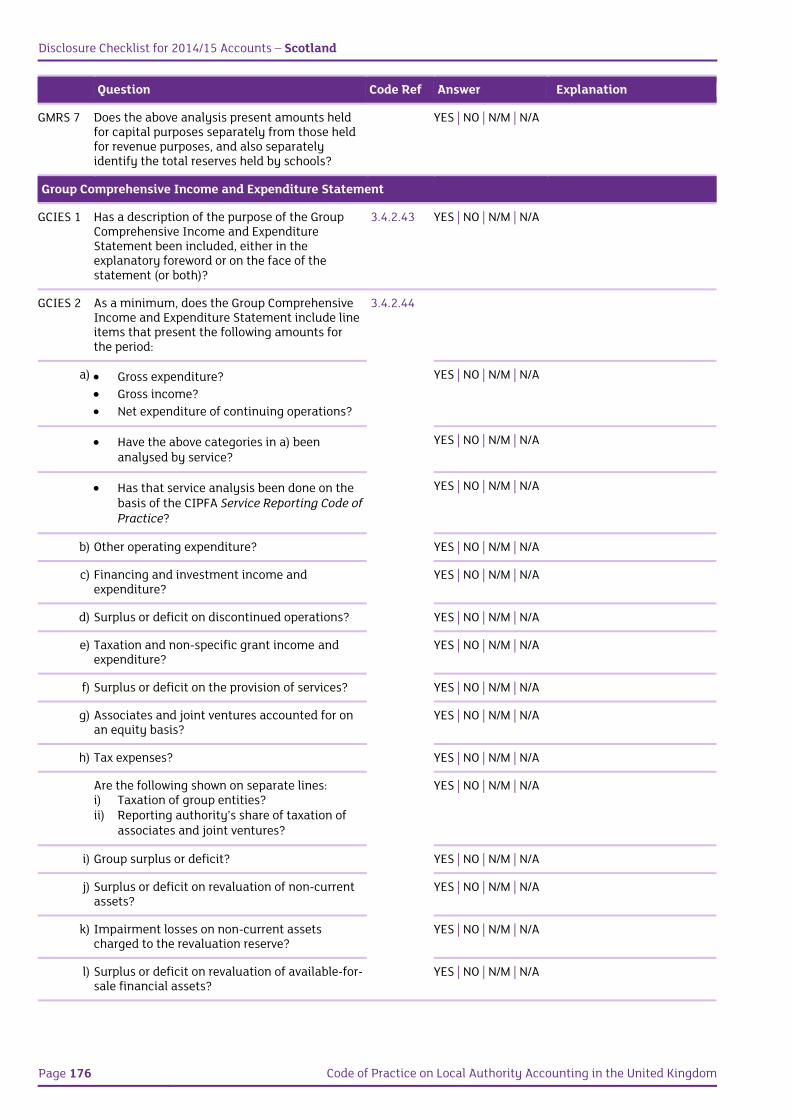

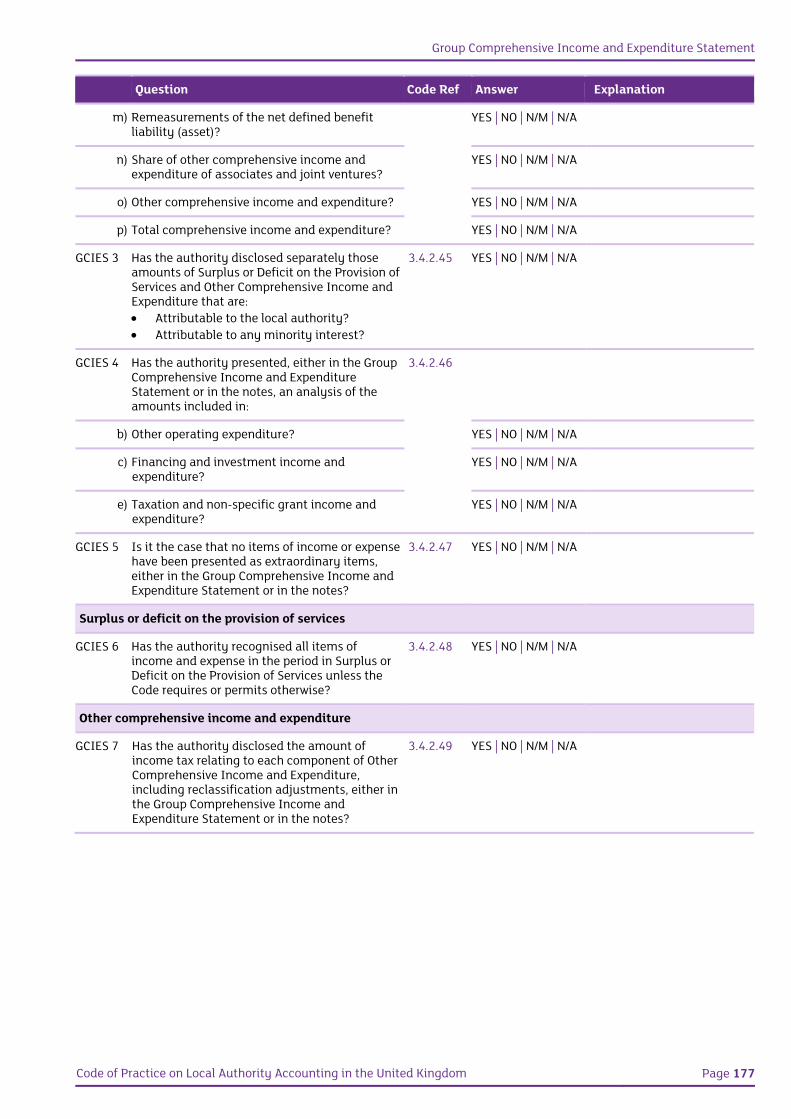

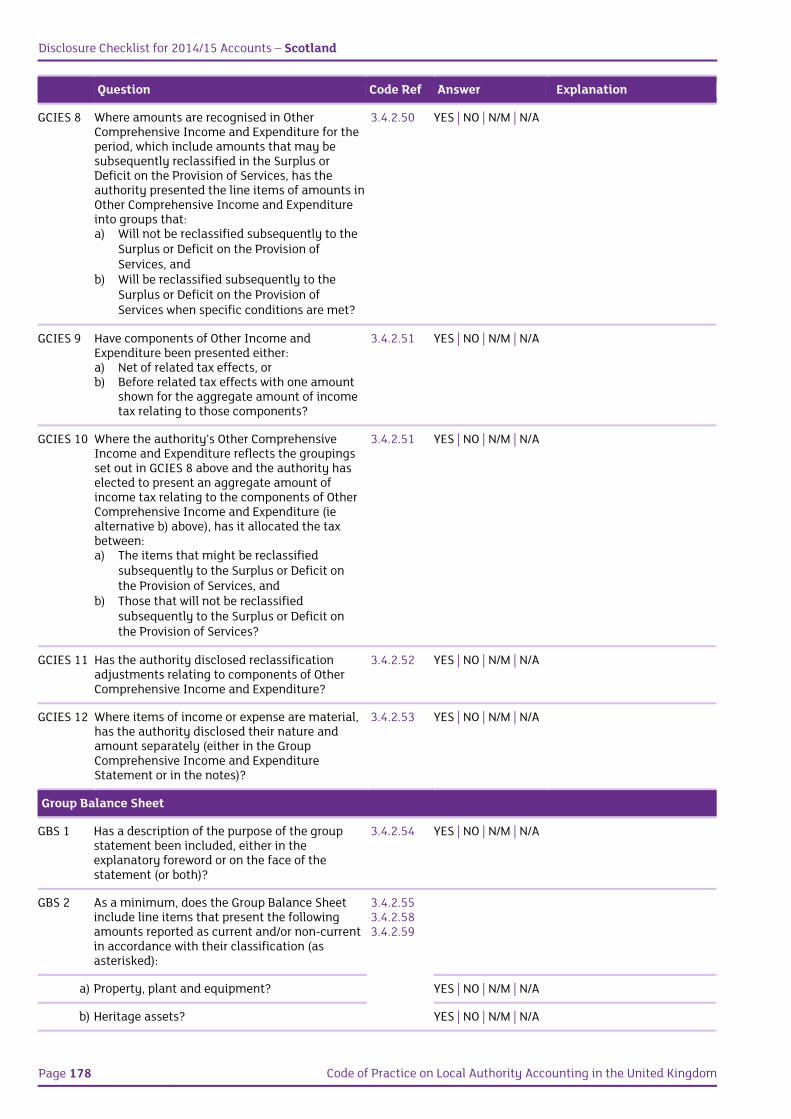

Group Movement in Reserves Statement GMRS 17

Group Comprehensive Income and Expenditure Statement GCIES 112

Group Balance Sheet GBS 111

Group Cash Flow Statement GCFS 118

Reference used in this aide-memoire: Code Ref Code of Practice on Local Authority Accounting in the United Kingdom 2014/15

Where possible, the use of references in this checklist reflects the references in the Code itself. This is to enable users to cross-check information back to the Code. There will therefore be cases where a list starts with a letter other than a), or where certain number or letter references are missing from a sequence, eg a), b), c), f), g). The Disclosure Checklist reflects the cutting clutter agenda and includes an N/M = Not Material column. Where disclosures are driven by accounting standards, the Code’s provisions in paragraph 3.4.2.26 enable an authority to exclude disclosures that are required by the Code if the information is not material. However, in relation to statutory disclosures, reference should be made to the relevant legislation for specific disclosure requirements (eg the disclosure of officers’ remuneration).

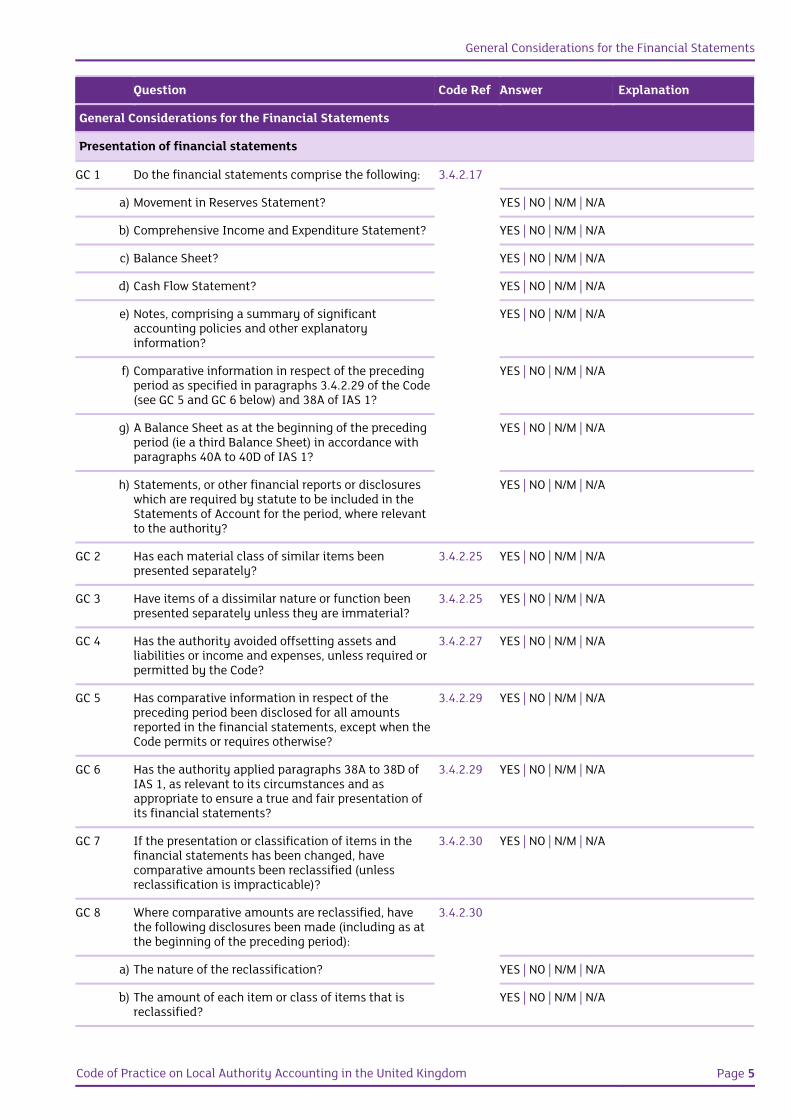

General Considerations for the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 5

Question Code Ref Answer Explanation

General Considerations for the Financial Statements

Presentation of financial statements

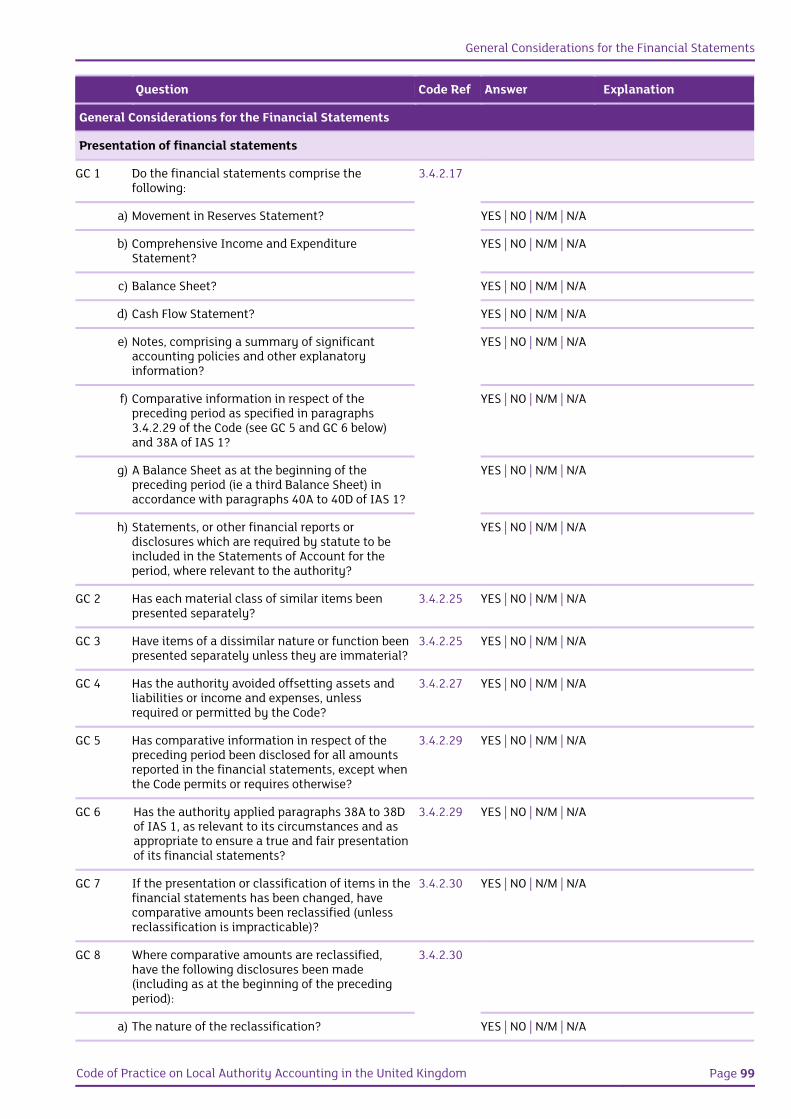

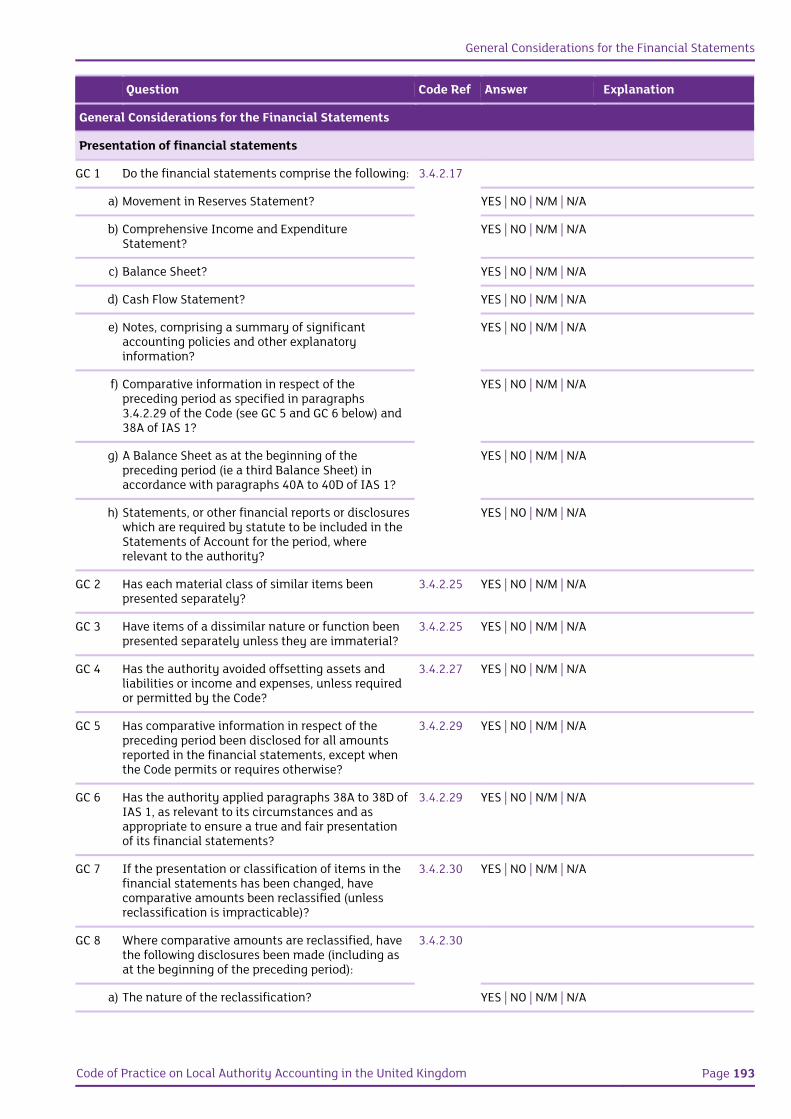

GC 1 Do the financial statements comprise the following: 3.4.2.17

a) Movement in Reserves Statement? YES | NO | N/M | N/A

b) Comprehensive Income and Expenditure Statement? YES | NO | N/M | N/A

c) Balance Sheet? YES | NO | N/M | N/A

d) Cash Flow Statement? YES | NO | N/M | N/A

e) Notes, comprising a summary of significant accounting policies and other explanatory information?

YES | NO | N/M | N/A

f) Comparative information in respect of the preceding period as specified in paragraphs 3.4.2.29 of the Code (see GC 5 and GC 6 below) and 38A of IAS 1?

YES | NO | N/M | N/A

g) A Balance Sheet as at the beginning of the preceding period (ie a third Balance Sheet) in accordance with paragraphs 40A to 40D of IAS 1?

YES | NO | N/M | N/A

h) Statements, or other financial reports or disclosures which are required by statute to be included in the Statements of Account for the period, where relevant to the authority?

YES | NO | N/M | N/A

GC 2 Has each material class of similar items been presented separately?

3.4.2.25 YES | NO | N/M | N/A

GC 3 Have items of a dissimilar nature or function been presented separately unless they are immaterial?

3.4.2.25 YES | NO | N/M | N/A

GC 4 Has the authority avoided offsetting assets and liabilities or income and expenses, unless required or permitted by the Code?

3.4.2.27 YES | NO | N/M | N/A

GC 5 Has comparative information in respect of the preceding period been disclosed for all amounts reported in the financial statements, except when the Code permits or requires otherwise?

3.4.2.29 YES | NO | N/M | N/A

GC 6 Has the authority applied paragraphs 38A to 38D of IAS 1, as relevant to its circumstances and as appropriate to ensure a true and fair presentation of its financial statements?

3.4.2.29 YES | NO | N/M | N/A

GC 7 If the presentation or classification of items in the financial statements has been changed, have comparative amounts been reclassified (unless reclassification is impracticable)?

3.4.2.30 YES | NO | N/M | N/A

GC 8 Where comparative amounts are reclassified, have the following disclosures been made (including as at the beginning of the preceding period):

3.4.2.30

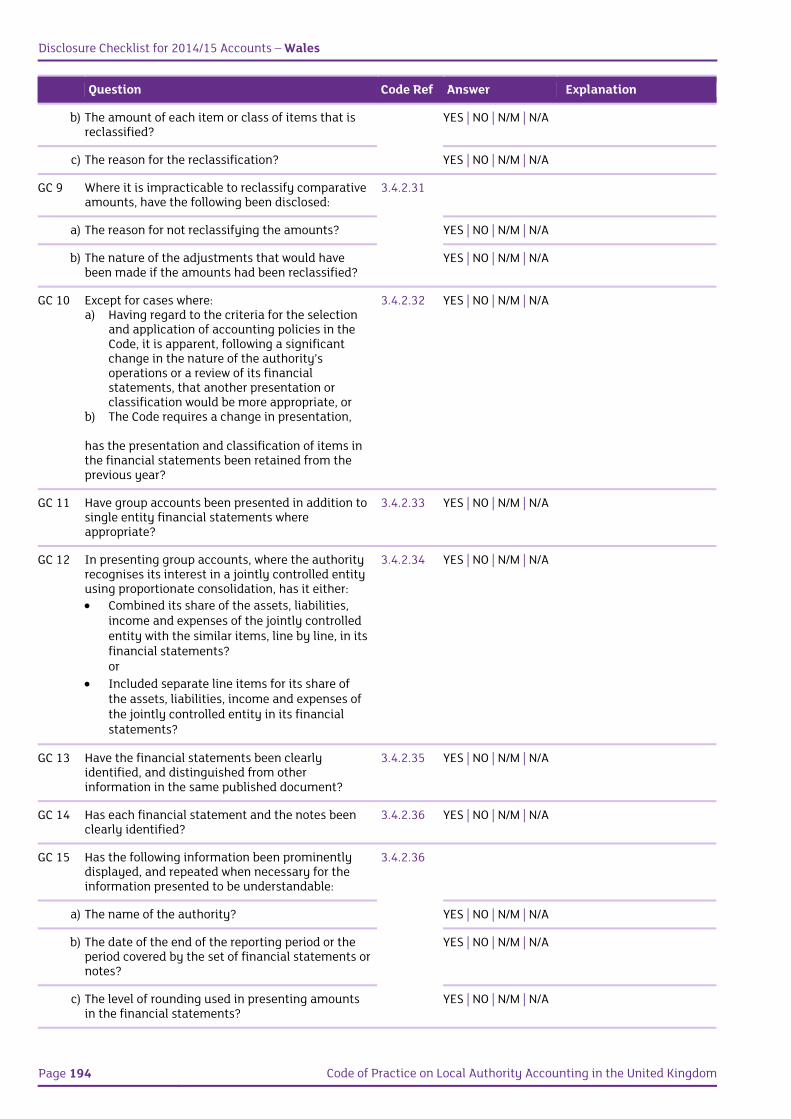

a) The nature of the reclassification? YES | NO | N/M | N/A

b) The amount of each item or class of items that is reclassified?

YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 6 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

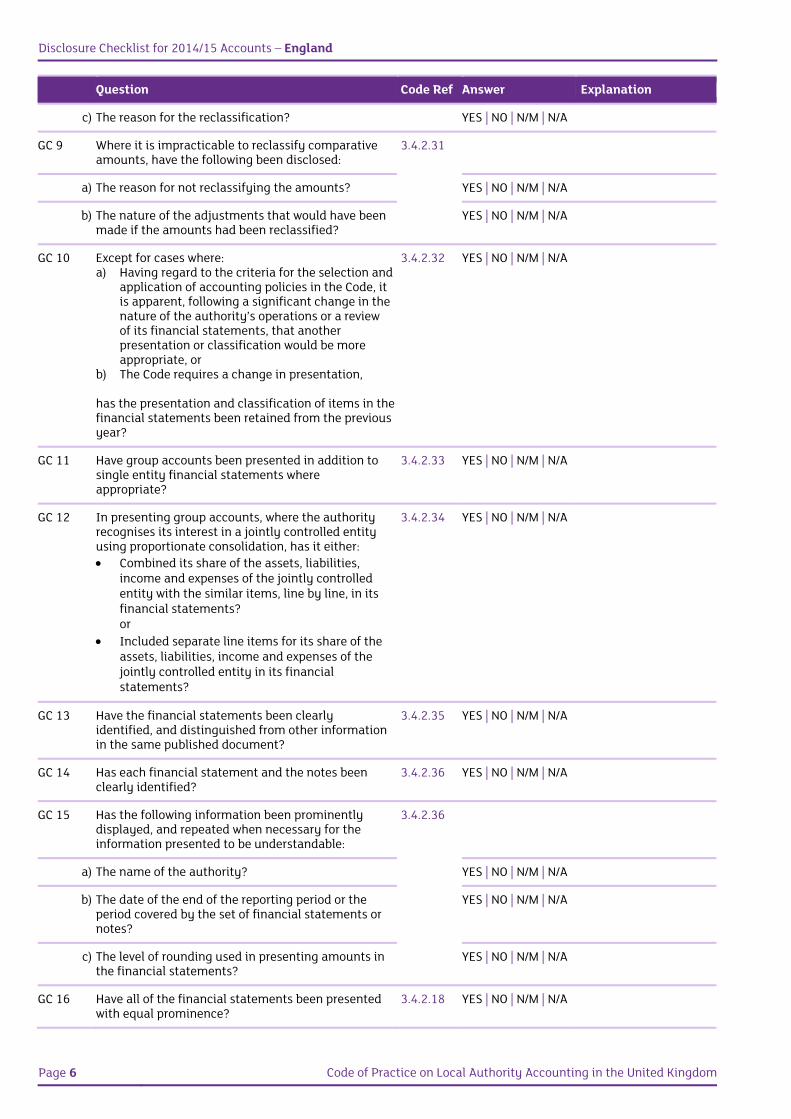

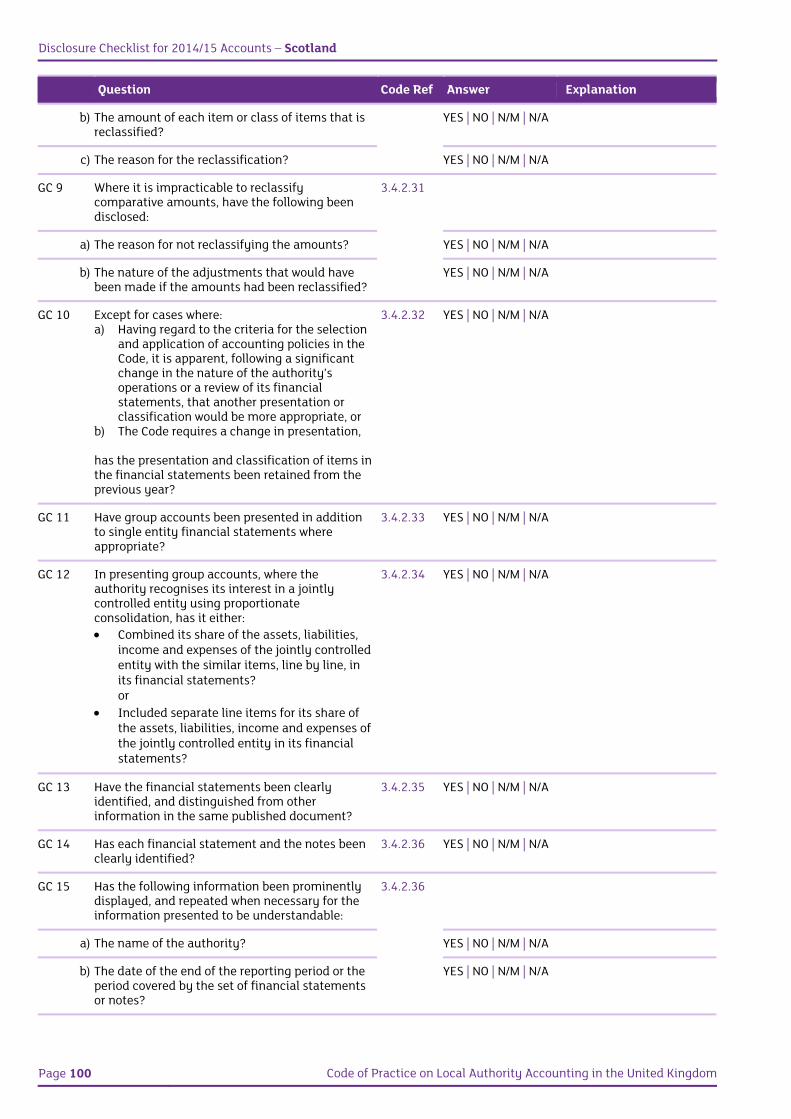

c) The reason for the reclassification? YES | NO | N/M | N/A

GC 9 Where it is impracticable to reclassify comparative amounts, have the following been disclosed:

3.4.2.31

a) The reason for not reclassifying the amounts? YES | NO | N/M | N/A

b) The nature of the adjustments that would have been made if the amounts had been reclassified?

YES | NO | N/M | N/A

GC 10 Except for cases where: a) Having regard to the criteria for the selection and

application of accounting policies in the Code, it is apparent, following a significant change in the nature of the authority’s operations or a review of its financial statements, that another presentation or classification would be more appropriate, or

b) The Code requires a change in presentation, has the presentation and classification of items in the financial statements been retained from the previous year?

3.4.2.32 YES | NO | N/M | N/A

GC 11 Have group accounts been presented in addition to single entity financial statements where appropriate?

3.4.2.33 YES | NO | N/M | N/A

GC 12 In presenting group accounts, where the authority recognises its interest in a jointly controlled entity using proportionate consolidation, has it either: Combined its share of the assets, liabilities,

income and expenses of the jointly controlled entity with the similar items, line by line, in its financial statements? or

Included separate line items for its share of the assets, liabilities, income and expenses of the jointly controlled entity in its financial statements?

3.4.2.34 YES | NO | N/M | N/A

GC 13 Have the financial statements been clearly identified, and distinguished from other information in the same published document?

3.4.2.35 YES | NO | N/M | N/A

GC 14 Has each financial statement and the notes been clearly identified?

3.4.2.36 YES | NO | N/M | N/A

GC 15 Has the following information been prominently displayed, and repeated when necessary for the information presented to be understandable:

3.4.2.36

a) The name of the authority? YES | NO | N/M | N/A

b) The date of the end of the reporting period or the period covered by the set of financial statements or notes?

YES | NO | N/M | N/A

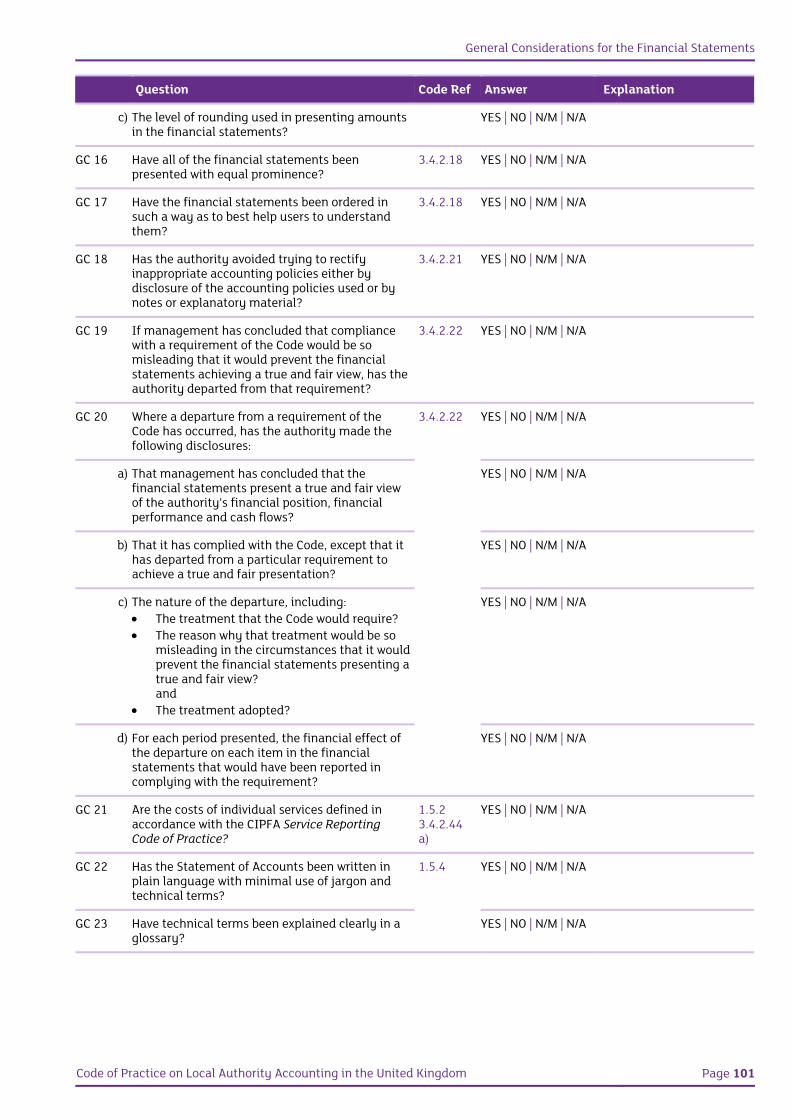

c) The level of rounding used in presenting amounts in the financial statements?

YES | NO | N/M | N/A

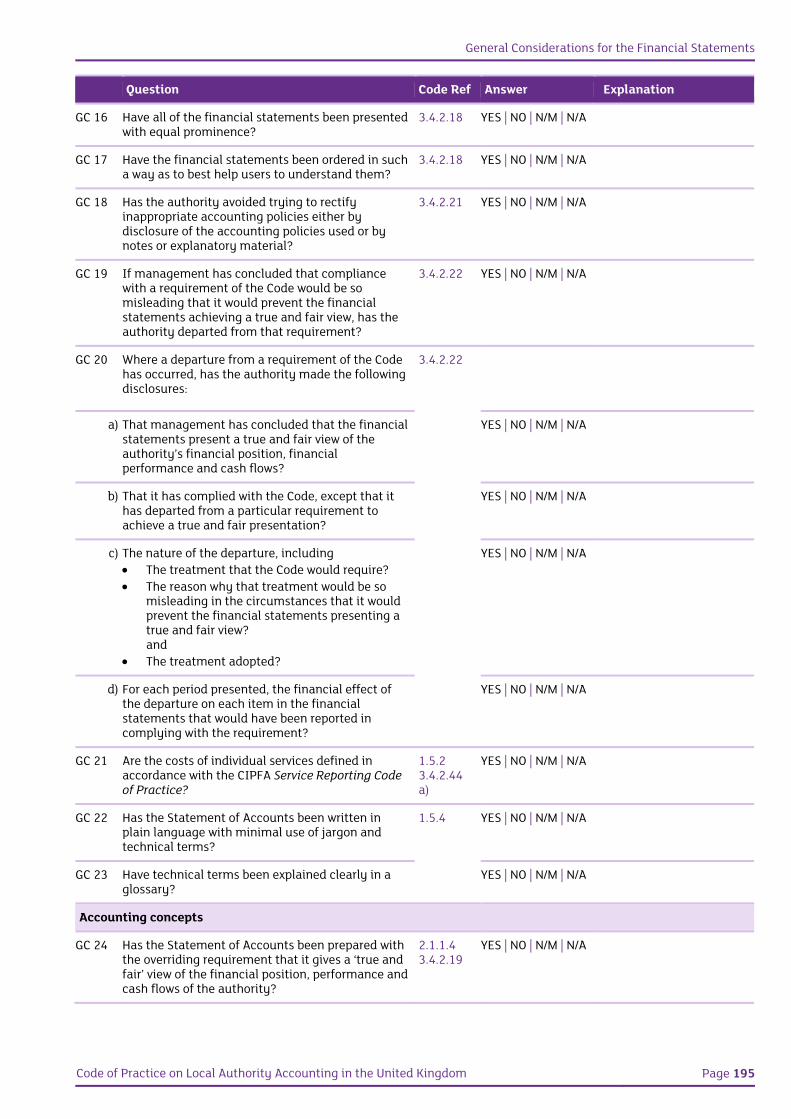

GC 16 Have all of the financial statements been presented with equal prominence?

3.4.2.18 YES | NO | N/M | N/A

General Considerations for the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 7

Question Code Ref Answer Explanation

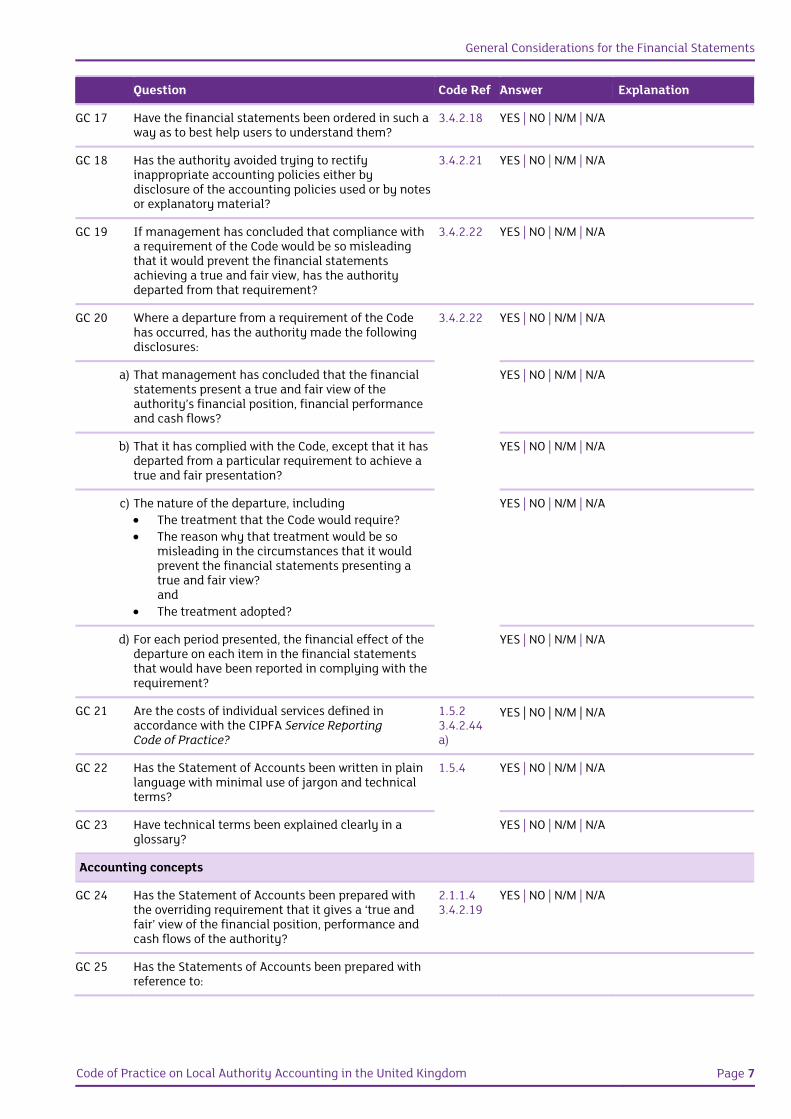

GC 17 Have the financial statements been ordered in such a way as to best help users to understand them?

3.4.2.18 YES | NO | N/M | N/A

GC 18 Has the authority avoided trying to rectify inappropriate accounting policies either by disclosure of the accounting policies used or by notes or explanatory material?

3.4.2.21 YES | NO | N/M | N/A

GC 19 If management has concluded that compliance with a requirement of the Code would be so misleading that it would prevent the financial statements achieving a true and fair view, has the authority departed from that requirement?

3.4.2.22 YES | NO | N/M | N/A

GC 20 Where a departure from a requirement of the Code has occurred, has the authority made the following disclosures:

3.4.2.22 YES | NO | N/M | N/A

a) That management has concluded that the financial statements present a true and fair view of the authority’s financial position, financial performance and cash flows?

YES | NO | N/M | N/A

b) That it has complied with the Code, except that it has departed from a particular requirement to achieve a true and fair presentation?

YES | NO | N/M | N/A

c) The nature of the departure, including The treatment that the Code would require? The reason why that treatment would be so

misleading in the circumstances that it would prevent the financial statements presenting a true and fair view? and

The treatment adopted?

YES | NO | N/M | N/A

d) For each period presented, the financial effect of the departure on each item in the financial statements that would have been reported in complying with the requirement?

YES | NO | N/M | N/A

GC 21 Are the costs of individual services defined in accordance with the CIPFA Service Reporting Code of Practice?

1.5.23.4.2.44 a)

YES | NO | N/M | N/A

GC 22 Has the Statement of Accounts been written in plain language with minimal use of jargon and technical terms?

1.5.4 YES | NO | N/M | N/A

GC 23 Have technical terms been explained clearly in a glossary?

YES | NO | N/M | N/A

Accounting concepts

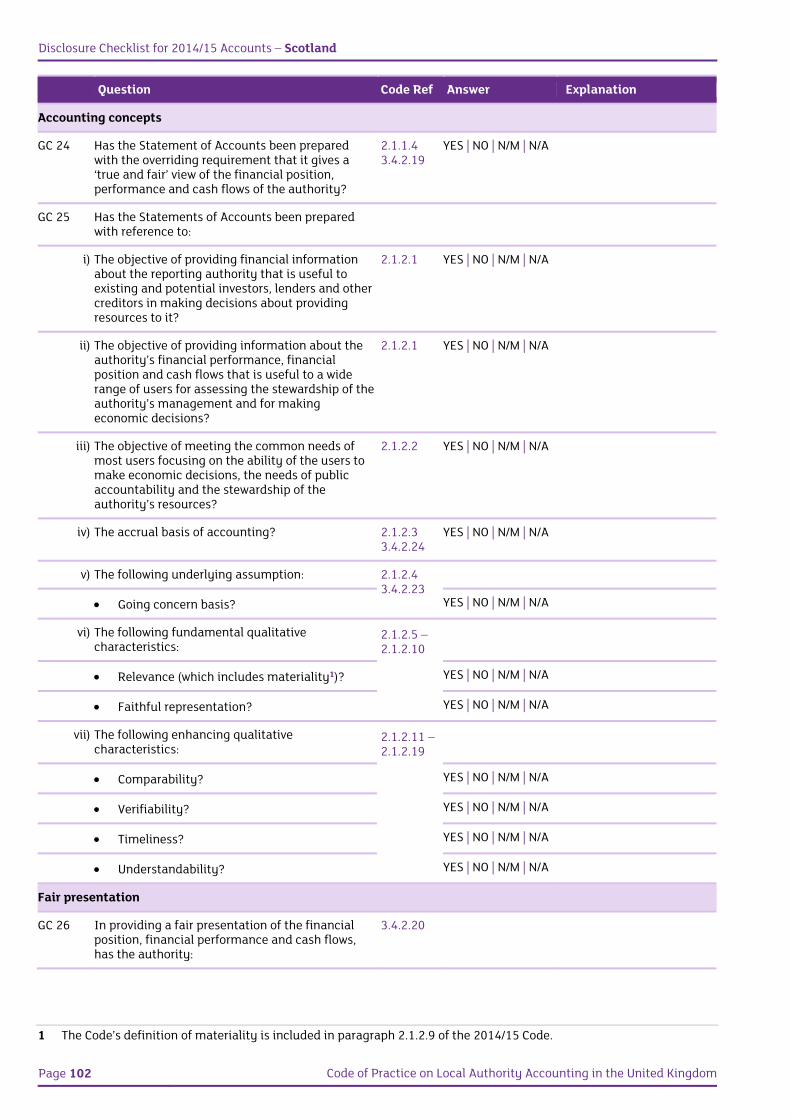

GC 24 Has the Statement of Accounts been prepared with the overriding requirement that it gives a ‘true and fair’ view of the financial position, performance and cash flows of the authority?

2.1.1.43.4.2.19

YES | NO | N/M | N/A

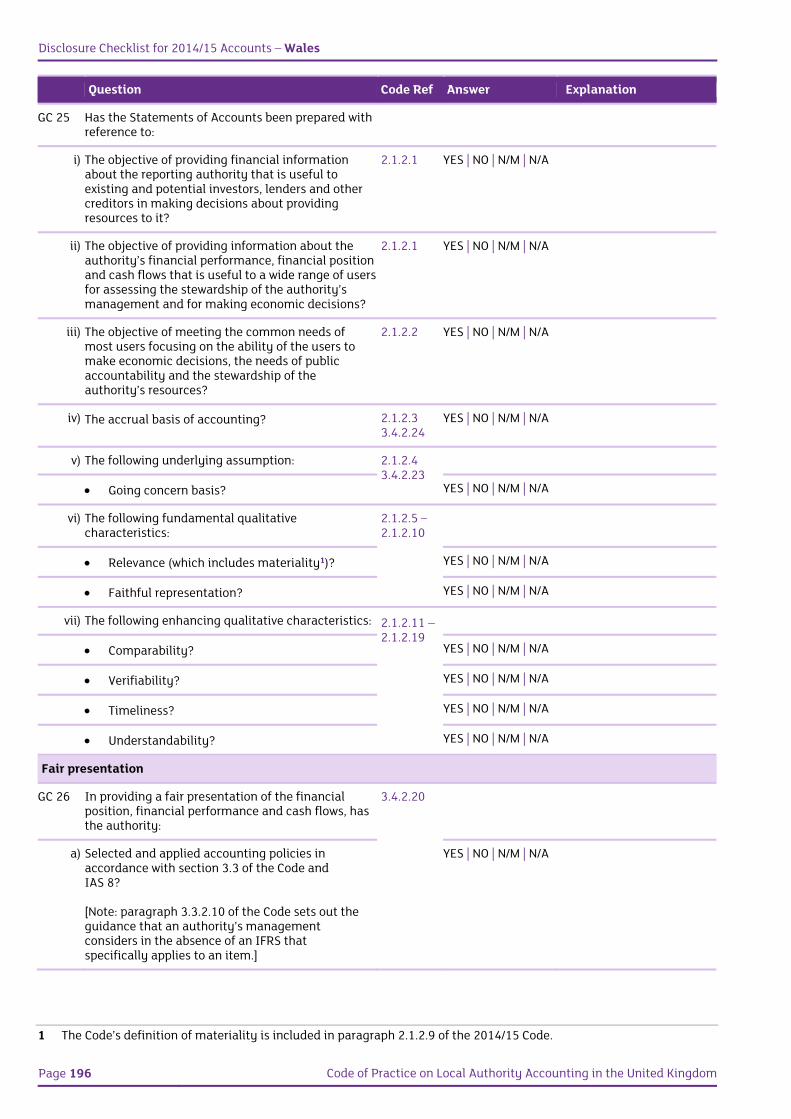

GC 25 Has the Statements of Accounts been prepared with reference to:

Disclosure Checklist for 2014/15 Accounts – England

Page 8 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

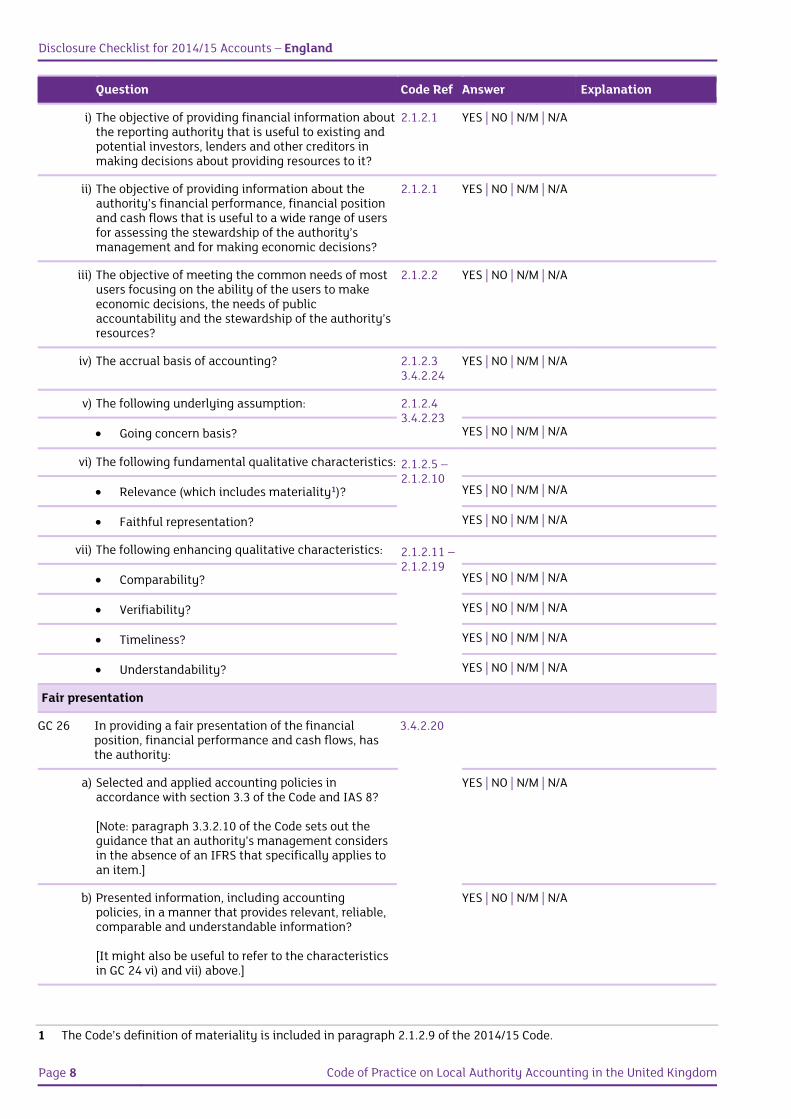

i) The objective of providing financial information about the reporting authority that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to it?

2.1.2.1 YES | NO | N/M | N/A

ii) The objective of providing information about the authority’s financial performance, financial position and cash flows that is useful to a wide range of users for assessing the stewardship of the authority’s management and for making economic decisions?

2.1.2.1 YES | NO | N/M | N/A

iii) The objective of meeting the common needs of most users focusing on the ability of the users to make economic decisions, the needs of public accountability and the stewardship of the authority’s resources?

2.1.2.2 YES | NO | N/M | N/A

iv) The accrual basis of accounting? 2.1.2.33.4.2.24

YES | NO | N/M | N/A

v) The following underlying assumption: 2.1.2.43.4.2.23

Going concern basis? YES | NO | N/M | N/A

vi) The following fundamental qualitative characteristics: 2.1.2.5 2.1.2.10

Relevance (which includes materiality1)? YES | NO | N/M | N/A

Faithful representation? YES | NO | N/M | N/A

vii) The following enhancing qualitative characteristics: 2.1.2.11 2.1.2.19

Comparability? YES | NO | N/M | N/A

Verifiability? YES | NO | N/M | N/A

Timeliness? YES | NO | N/M | N/A

Understandability? YES | NO | N/M | N/A

Fair presentation

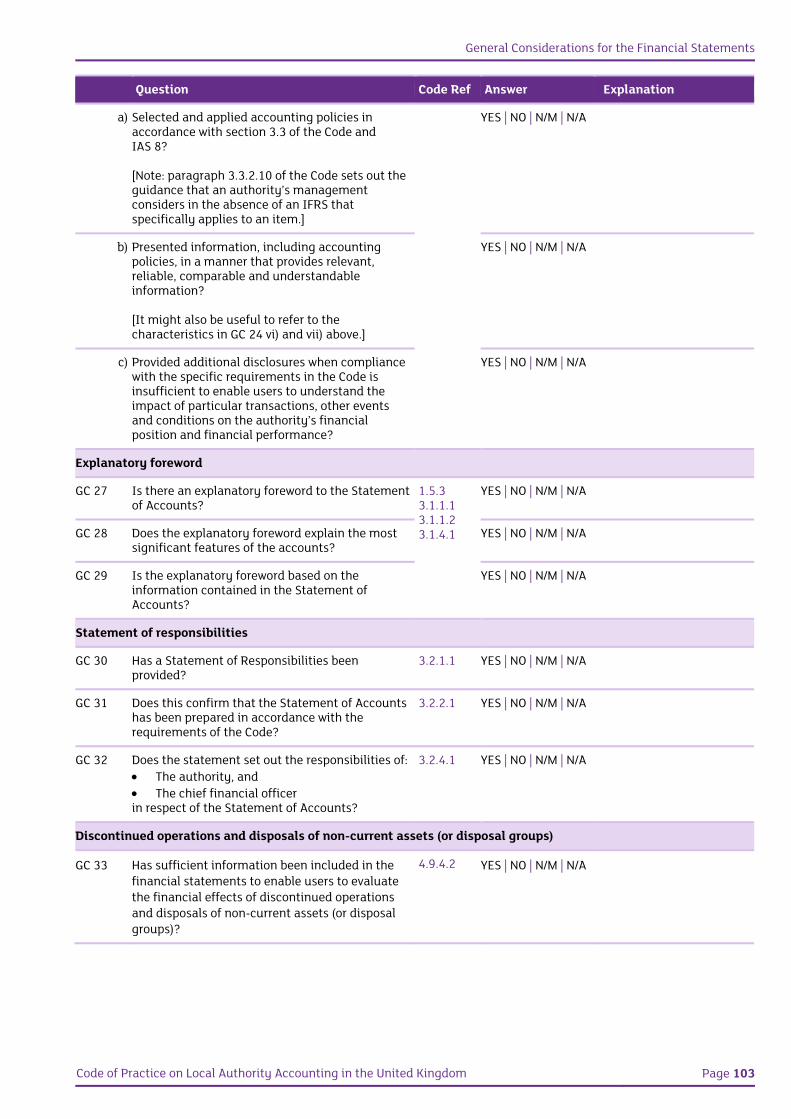

GC 26 In providing a fair presentation of the financial position, financial performance and cash flows, has the authority:

3.4.2.20

a) Selected and applied accounting policies in accordance with section 3.3 of the Code and IAS 8? [Note: paragraph 3.3.2.10 of the Code sets out the guidance that an authority’s management considers in the absence of an IFRS that specifically applies to an item.]

YES | NO | N/M | N/A

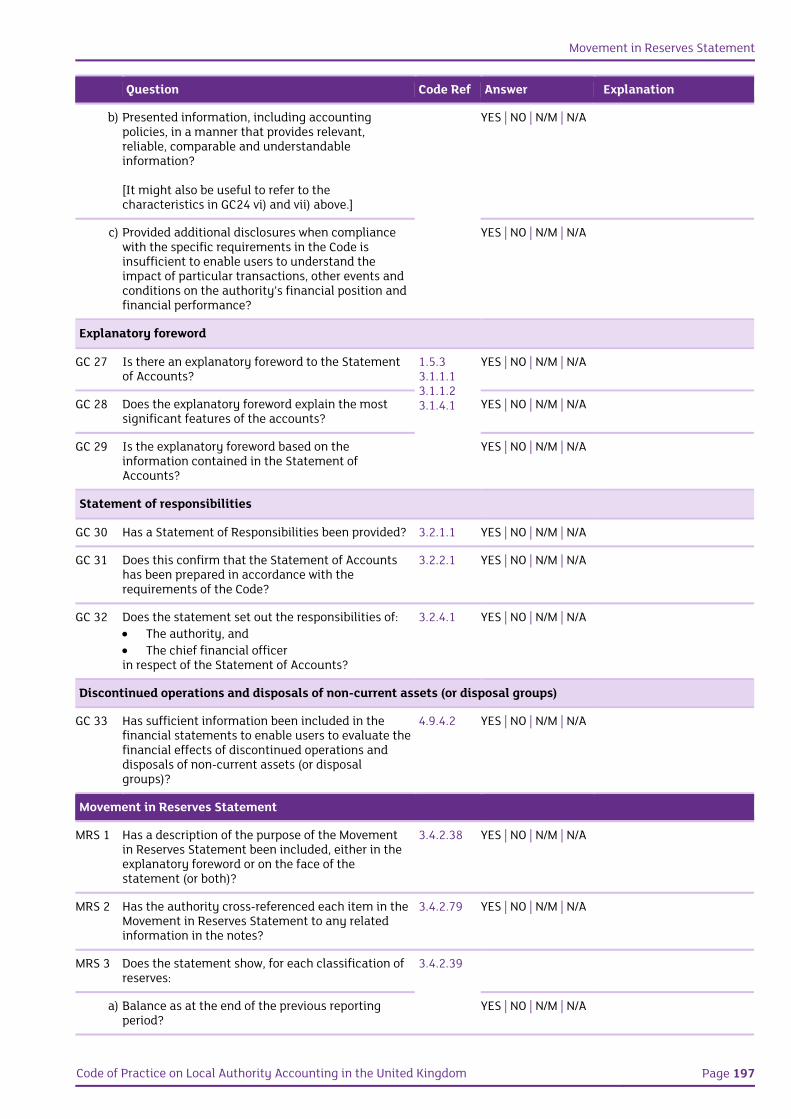

b) Presented information, including accounting policies, in a manner that provides relevant, reliable, comparable and understandable information? [It might also be useful to refer to the characteristics in GC 24 vi) and vii) above.]

YES | NO | N/M | N/A

1 The Code’s definition of materiality is included in paragraph 2.1.2.9 of the 2014/15 Code.

Movement in Reserves Statement

Code of Practice on Local Authority Accounting in the United Kingdom Page 9

Question Code Ref Answer Explanation

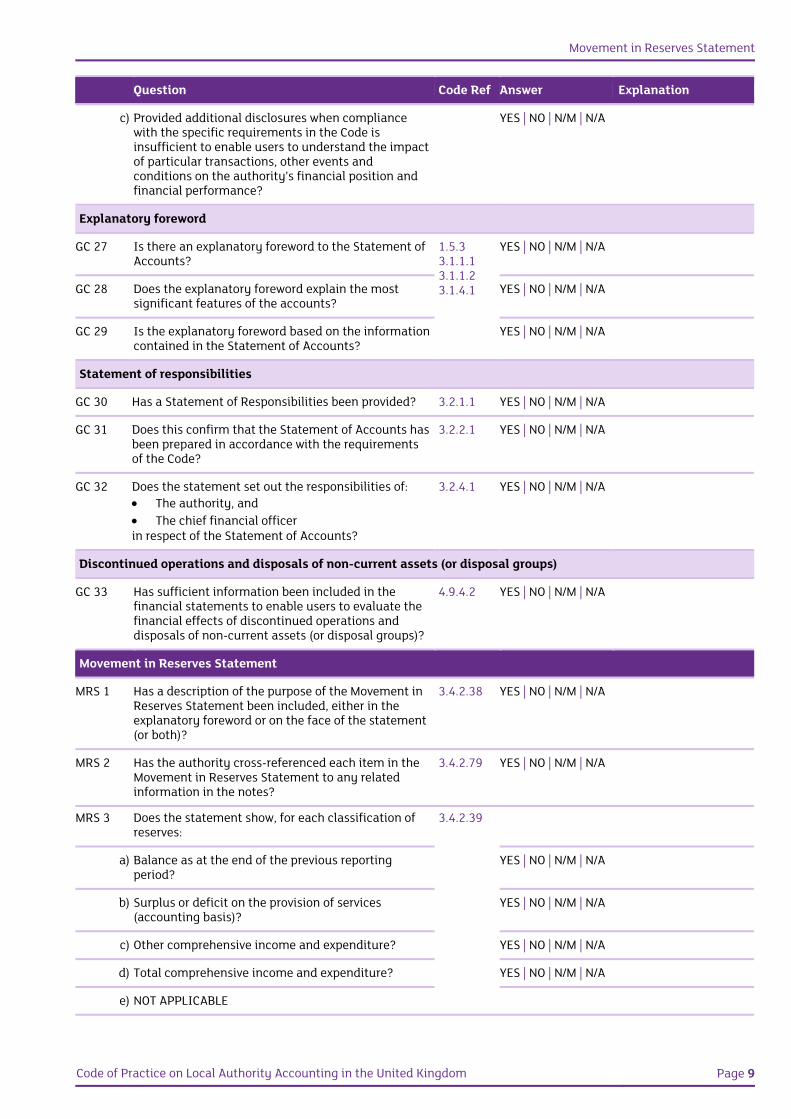

c) Provided additional disclosures when compliance with the specific requirements in the Code is insufficient to enable users to understand the impact of particular transactions, other events and conditions on the authority’s financial position and financial performance?

YES | NO | N/M | N/A

Explanatory foreword

GC 27 Is there an explanatory foreword to the Statement of Accounts?

1.5.33.1.1.1 3.1.1.2 3.1.4.1

YES | NO | N/M | N/A

GC 28 Does the explanatory foreword explain the most significant features of the accounts?

YES | NO | N/M | N/A

GC 29 Is the explanatory foreword based on the information contained in the Statement of Accounts?

YES | NO | N/M | N/A

Statement of responsibilities

GC 30 Has a Statement of Responsibilities been provided? 3.2.1.1 YES | NO | N/M | N/A

GC 31 Does this confirm that the Statement of Accounts has been prepared in accordance with the requirements of the Code?

3.2.2.1 YES | NO | N/M | N/A

GC 32 Does the statement set out the responsibilities of: The authority, and The chief financial officer in respect of the Statement of Accounts?

3.2.4.1 YES | NO | N/M | N/A

Discontinued operations and disposals of non-current assets (or disposal groups)

GC 33 Has sufficient information been included in the financial statements to enable users to evaluate the financial effects of discontinued operations and disposals of non-current assets (or disposal groups)?

4.9.4.2 YES | NO | N/M | N/A

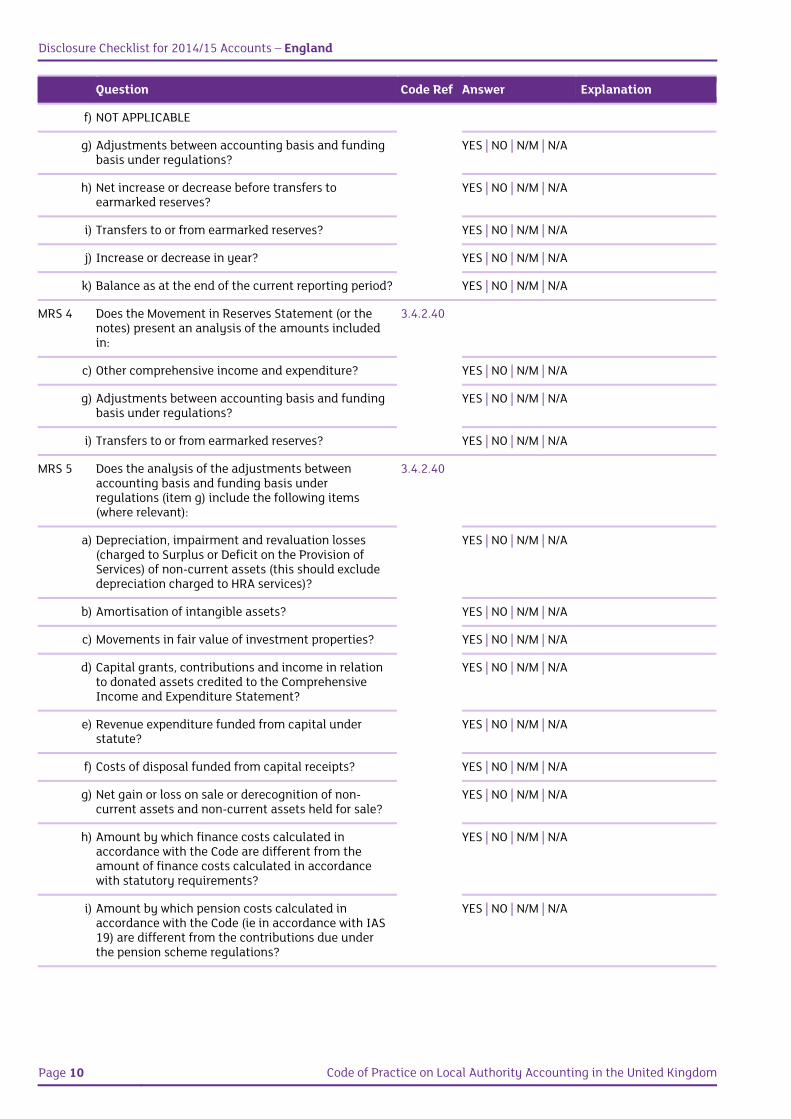

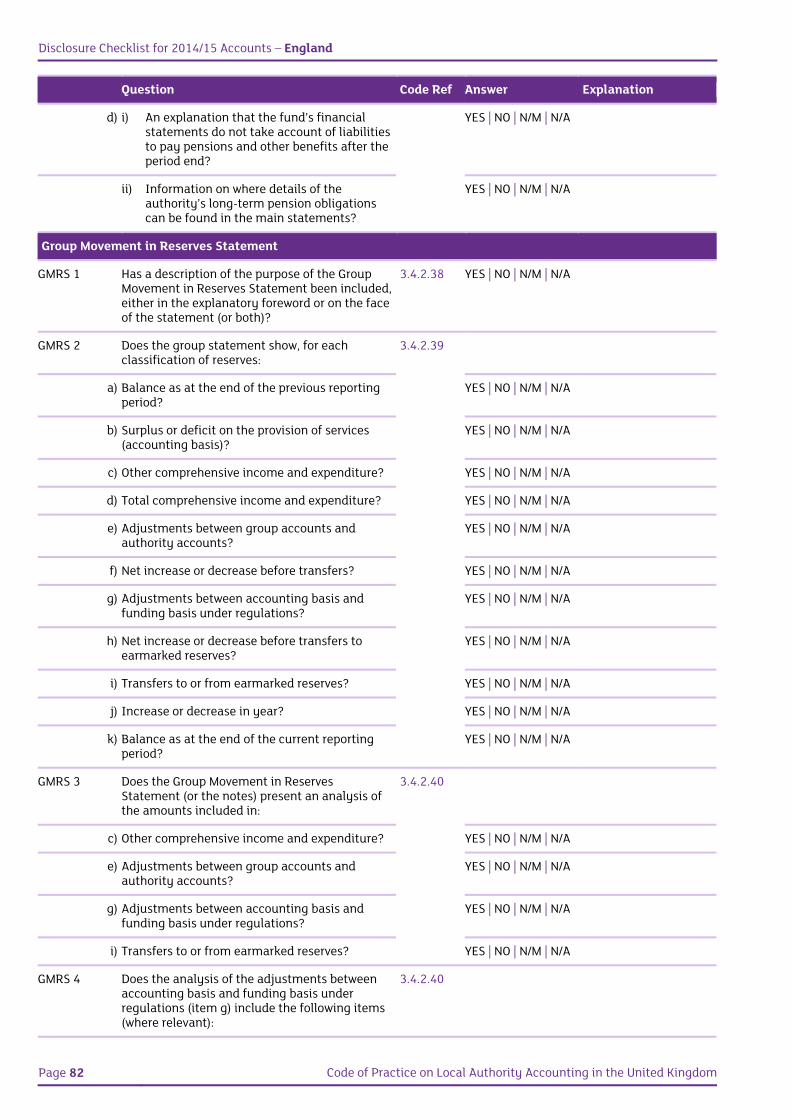

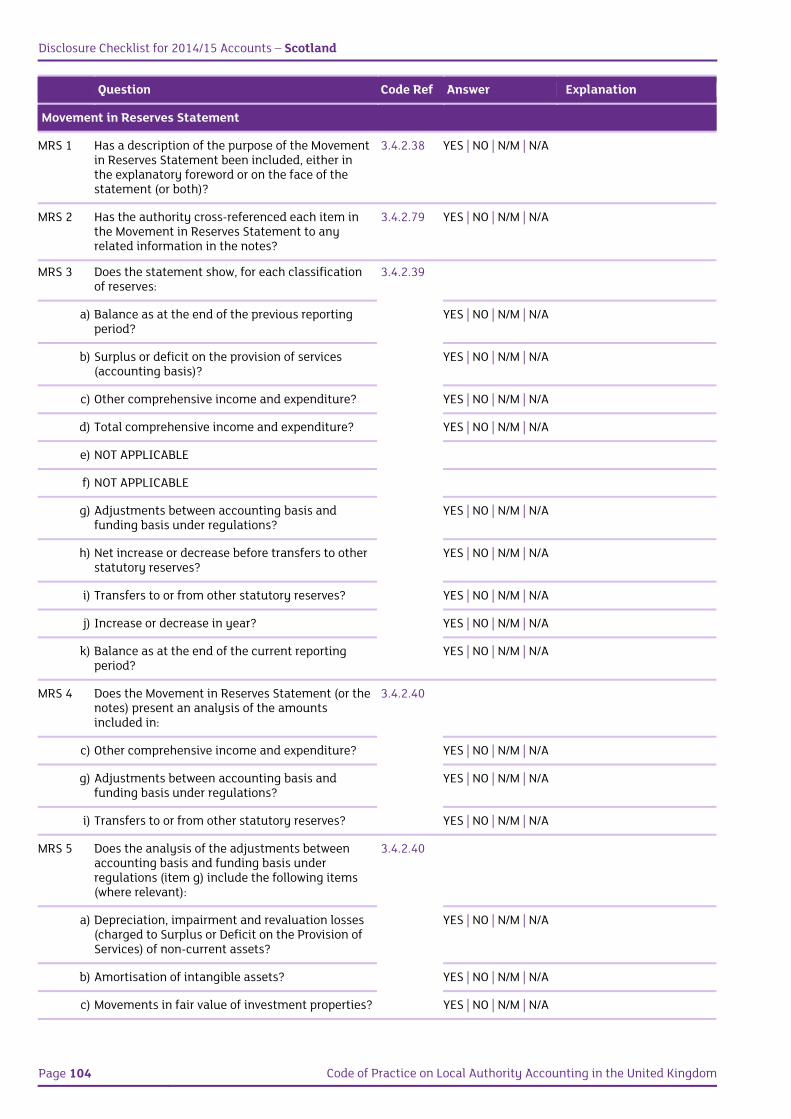

Movement in Reserves Statement

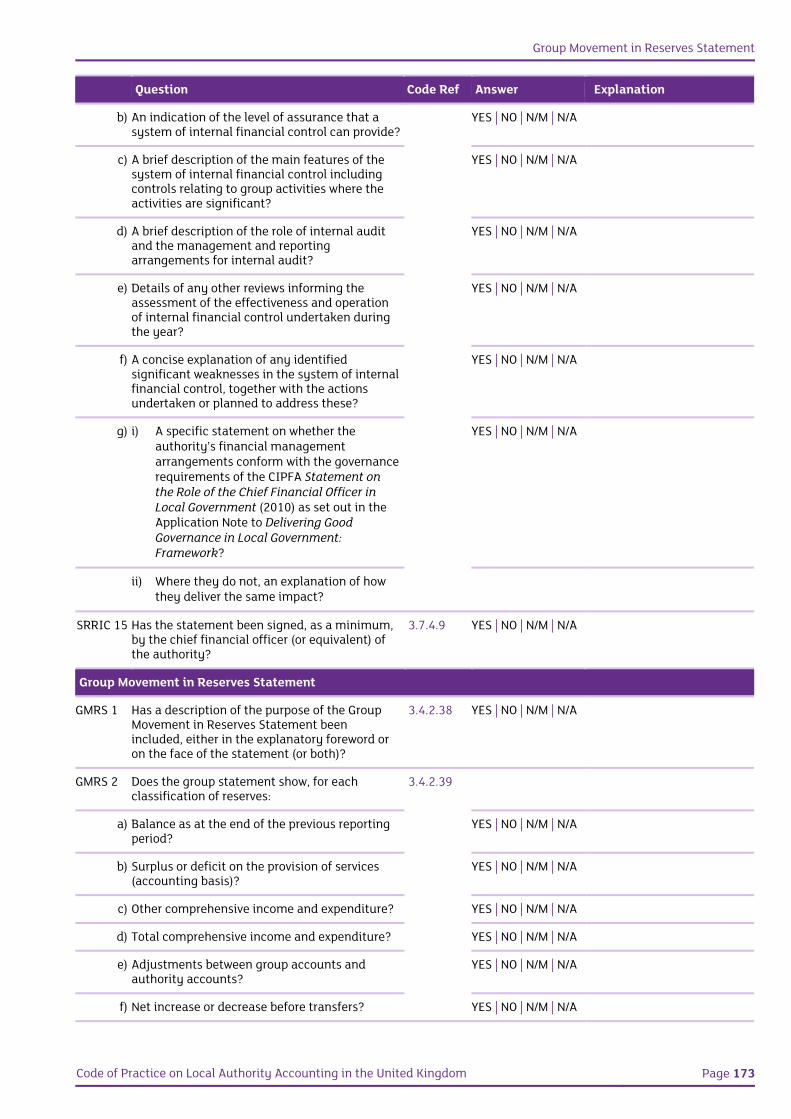

MRS 1 Has a description of the purpose of the Movement in Reserves Statement been included, either in the explanatory foreword or on the face of the statement (or both)?

3.4.2.38 YES | NO | N/M | N/A

MRS 2 Has the authority cross-referenced each item in the Movement in Reserves Statement to any related information in the notes?

3.4.2.79 YES | NO | N/M | N/A

MRS 3 Does the statement show, for each classification of reserves:

3.4.2.39

a) Balance as at the end of the previous reporting period?

YES | NO | N/M | N/A

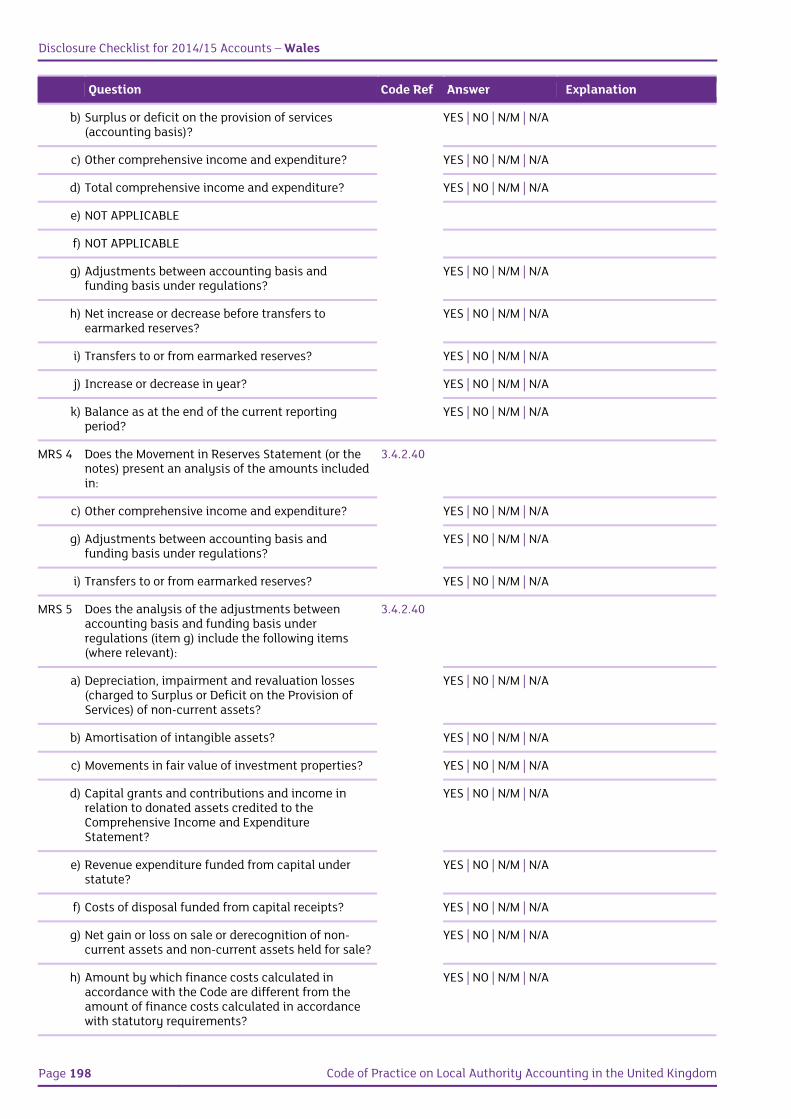

b) Surplus or deficit on the provision of services (accounting basis)?

YES | NO | N/M | N/A

c) Other comprehensive income and expenditure? YES | NO | N/M | N/A

d) Total comprehensive income and expenditure? YES | NO | N/M | N/A

e) NOT APPLICABLE

Disclosure Checklist for 2014/15 Accounts – England

Page 10 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

f) NOT APPLICABLE

g) Adjustments between accounting basis and funding basis under regulations?

YES | NO | N/M | N/A

h) Net increase or decrease before transfers to earmarked reserves?

YES | NO | N/M | N/A

i) Transfers to or from earmarked reserves? YES | NO | N/M | N/A

j) Increase or decrease in year? YES | NO | N/M | N/A

k) Balance as at the end of the current reporting period? YES | NO | N/M | N/A

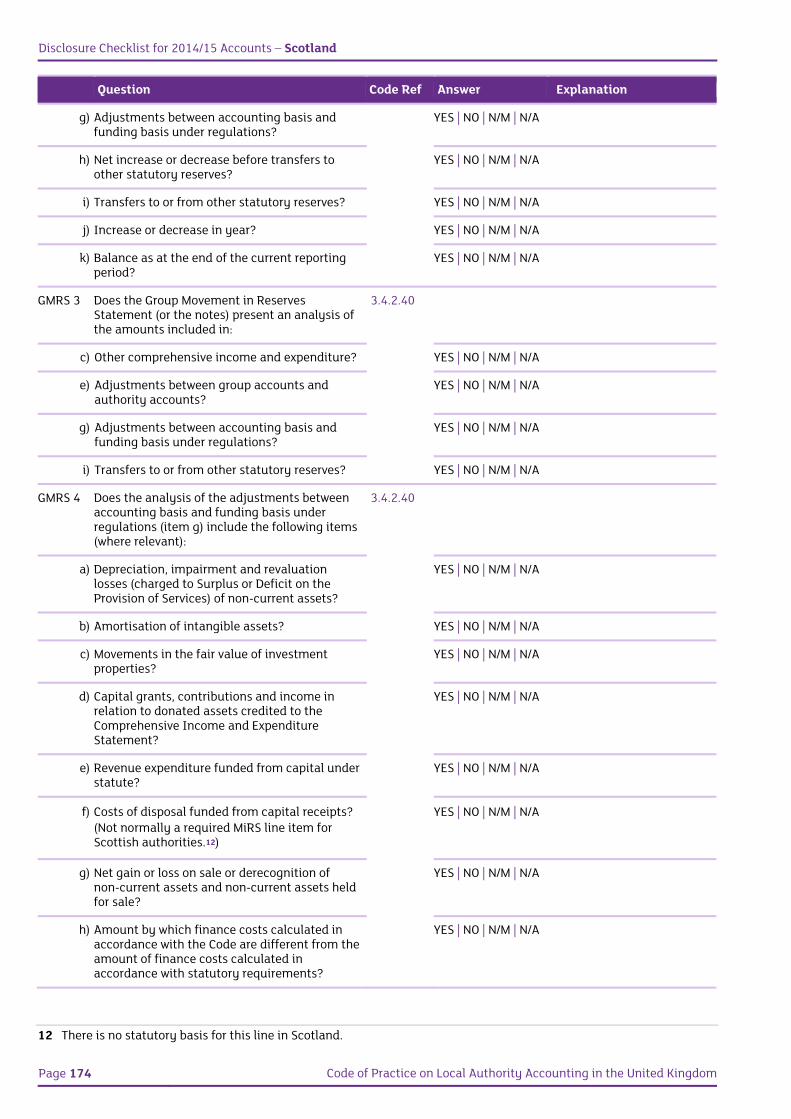

MRS 4 Does the Movement in Reserves Statement (or the notes) present an analysis of the amounts included in:

3.4.2.40

c) Other comprehensive income and expenditure? YES | NO | N/M | N/A

g) Adjustments between accounting basis and funding basis under regulations?

YES | NO | N/M | N/A

i) Transfers to or from earmarked reserves? YES | NO | N/M | N/A

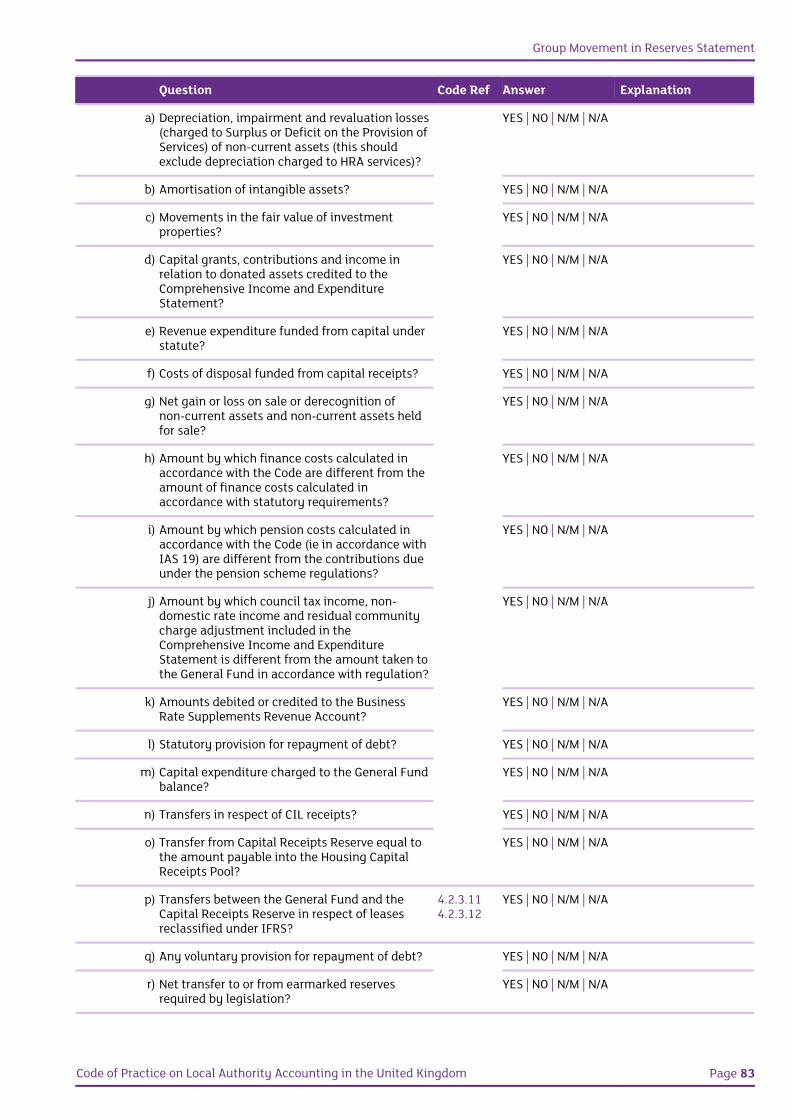

MRS 5 Does the analysis of the adjustments between accounting basis and funding basis under regulations (item g) include the following items (where relevant):

3.4.2.40

a) Depreciation, impairment and revaluation losses (charged to Surplus or Deficit on the Provision of Services) of non-current assets (this should exclude depreciation charged to HRA services)?

YES | NO | N/M | N/A

b) Amortisation of intangible assets? YES | NO | N/M | N/A

c) Movements in fair value of investment properties? YES | NO | N/M | N/A

d) Capital grants, contributions and income in relation to donated assets credited to the Comprehensive Income and Expenditure Statement?

YES | NO | N/M | N/A

e) Revenue expenditure funded from capital under statute?

YES | NO | N/M | N/A

f) Costs of disposal funded from capital receipts? YES | NO | N/M | N/A

g) Net gain or loss on sale or derecognition of non-current assets and non-current assets held for sale?

YES | NO | N/M | N/A

h) Amount by which finance costs calculated in accordance with the Code are different from the amount of finance costs calculated in accordance with statutory requirements?

YES | NO | N/M | N/A

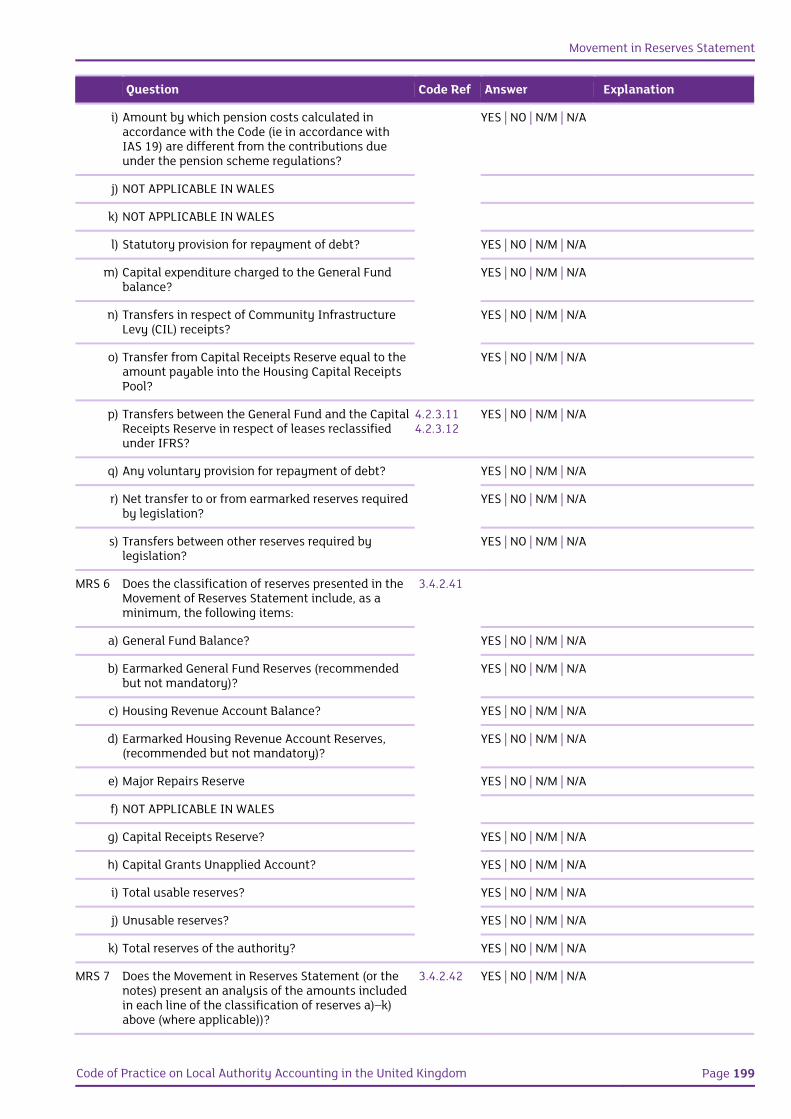

i) Amount by which pension costs calculated in accordance with the Code (ie in accordance with IAS 19) are different from the contributions due under the pension scheme regulations?

YES | NO | N/M | N/A

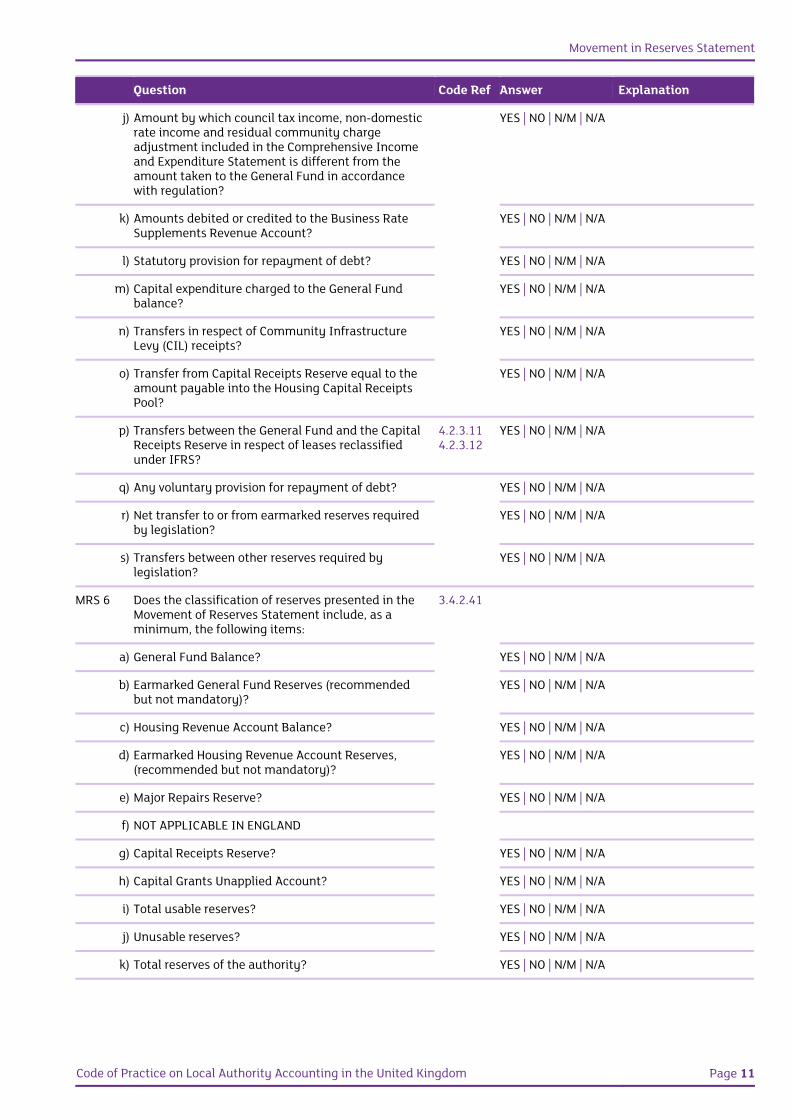

Movement in Reserves Statement

Code of Practice on Local Authority Accounting in the United Kingdom Page 11

Question Code Ref Answer Explanation

j) Amount by which council tax income, non-domestic rate income and residual community charge adjustment included in the Comprehensive Income and Expenditure Statement is different from the amount taken to the General Fund in accordance with regulation?

YES | NO | N/M | N/A

k) Amounts debited or credited to the Business Rate Supplements Revenue Account?

YES | NO | N/M | N/A

l) Statutory provision for repayment of debt? YES | NO | N/M | N/A

m) Capital expenditure charged to the General Fund balance?

YES | NO | N/M | N/A

n) Transfers in respect of Community Infrastructure Levy (CIL) receipts?

YES | NO | N/M | N/A

o) Transfer from Capital Receipts Reserve equal to the amount payable into the Housing Capital Receipts Pool?

YES | NO | N/M | N/A

p) Transfers between the General Fund and the Capital Receipts Reserve in respect of leases reclassified under IFRS?

4.2.3.114.2.3.12

YES | NO | N/M | N/A

q) Any voluntary provision for repayment of debt? YES | NO | N/M | N/A

r) Net transfer to or from earmarked reserves required by legislation?

YES | NO | N/M | N/A

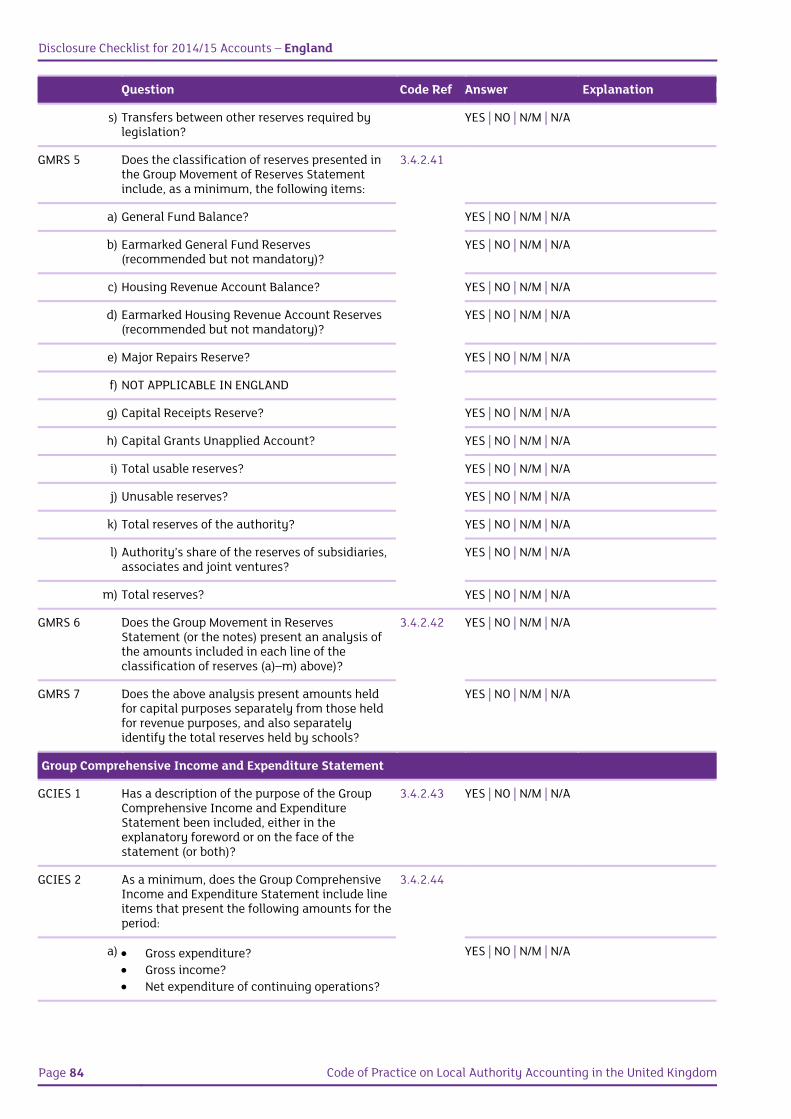

s) Transfers between other reserves required by legislation?

YES | NO | N/M | N/A

MRS 6 Does the classification of reserves presented in the Movement of Reserves Statement include, as a minimum, the following items:

3.4.2.41

a) General Fund Balance? YES | NO | N/M | N/A

b) Earmarked General Fund Reserves (recommended but not mandatory)?

YES | NO | N/M | N/A

c) Housing Revenue Account Balance? YES | NO | N/M | N/A

d) Earmarked Housing Revenue Account Reserves, (recommended but not mandatory)?

YES | NO | N/M | N/A

e) Major Repairs Reserve? YES | NO | N/M | N/A

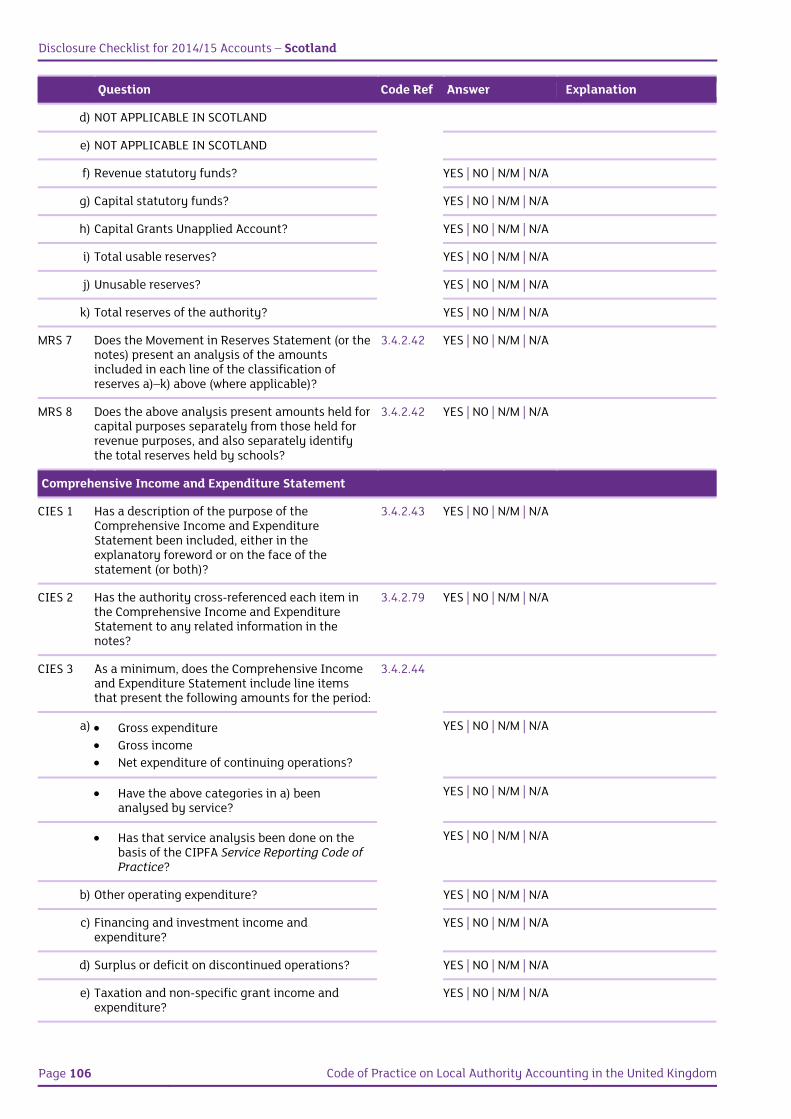

f) NOT APPLICABLE IN ENGLAND

g) Capital Receipts Reserve? YES | NO | N/M | N/A

h) Capital Grants Unapplied Account? YES | NO | N/M | N/A

i) Total usable reserves? YES | NO | N/M | N/A

j) Unusable reserves? YES | NO | N/M | N/A

k) Total reserves of the authority? YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 12 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

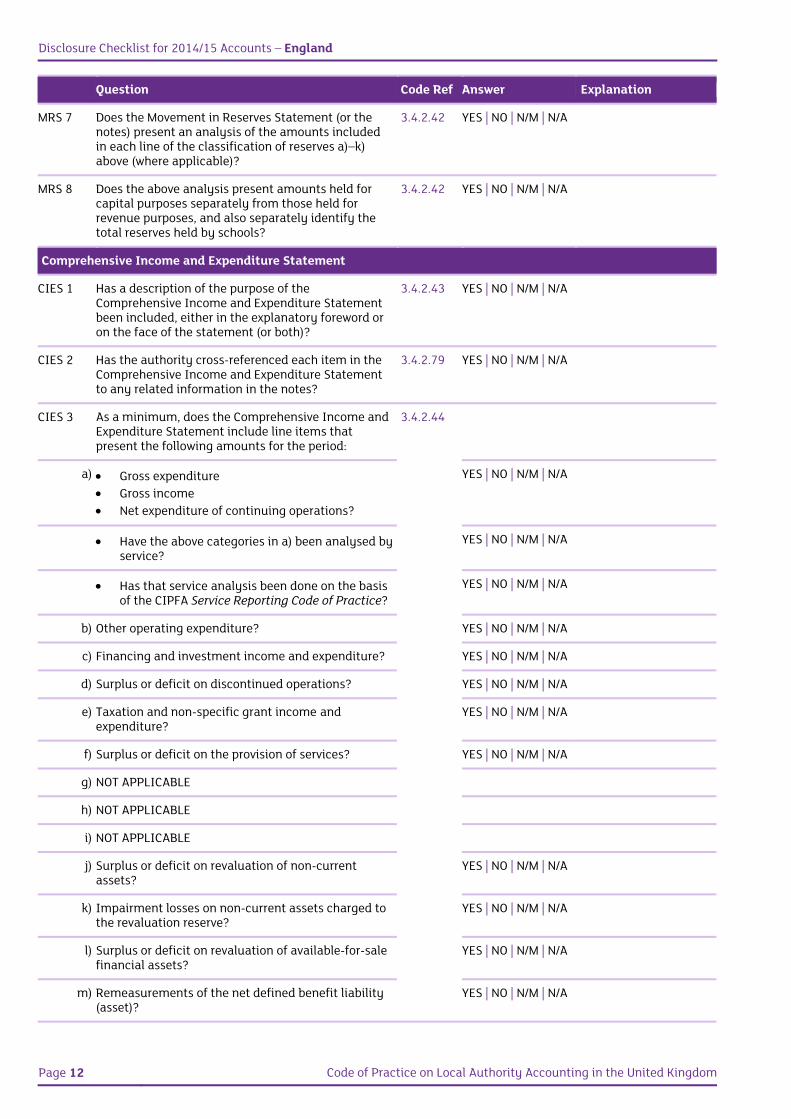

MRS 7 Does the Movement in Reserves Statement (or the notes) present an analysis of the amounts included in each line of the classification of reserves a)–k) above (where applicable)?

3.4.2.42 YES | NO | N/M | N/A

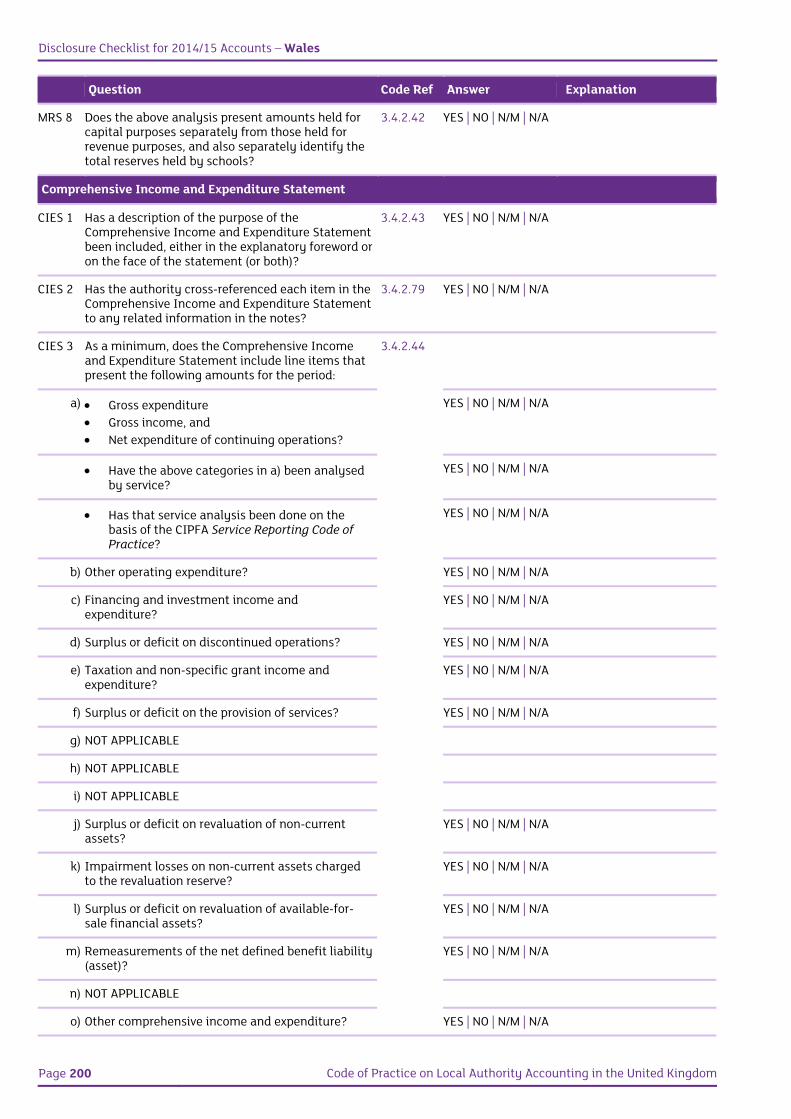

MRS 8 Does the above analysis present amounts held for capital purposes separately from those held for revenue purposes, and also separately identify the total reserves held by schools?

3.4.2.42 YES | NO | N/M | N/A

Comprehensive Income and Expenditure Statement

CIES 1 Has a description of the purpose of the Comprehensive Income and Expenditure Statement been included, either in the explanatory foreword or on the face of the statement (or both)?

3.4.2.43 YES | NO | N/M | N/A

CIES 2 Has the authority cross-referenced each item in the Comprehensive Income and Expenditure Statement to any related information in the notes?

3.4.2.79 YES | NO | N/M | N/A

CIES 3 As a minimum, does the Comprehensive Income and Expenditure Statement include line items that present the following amounts for the period:

3.4.2.44

a) Gross expenditure Gross income Net expenditure of continuing operations?

YES | NO | N/M | N/A

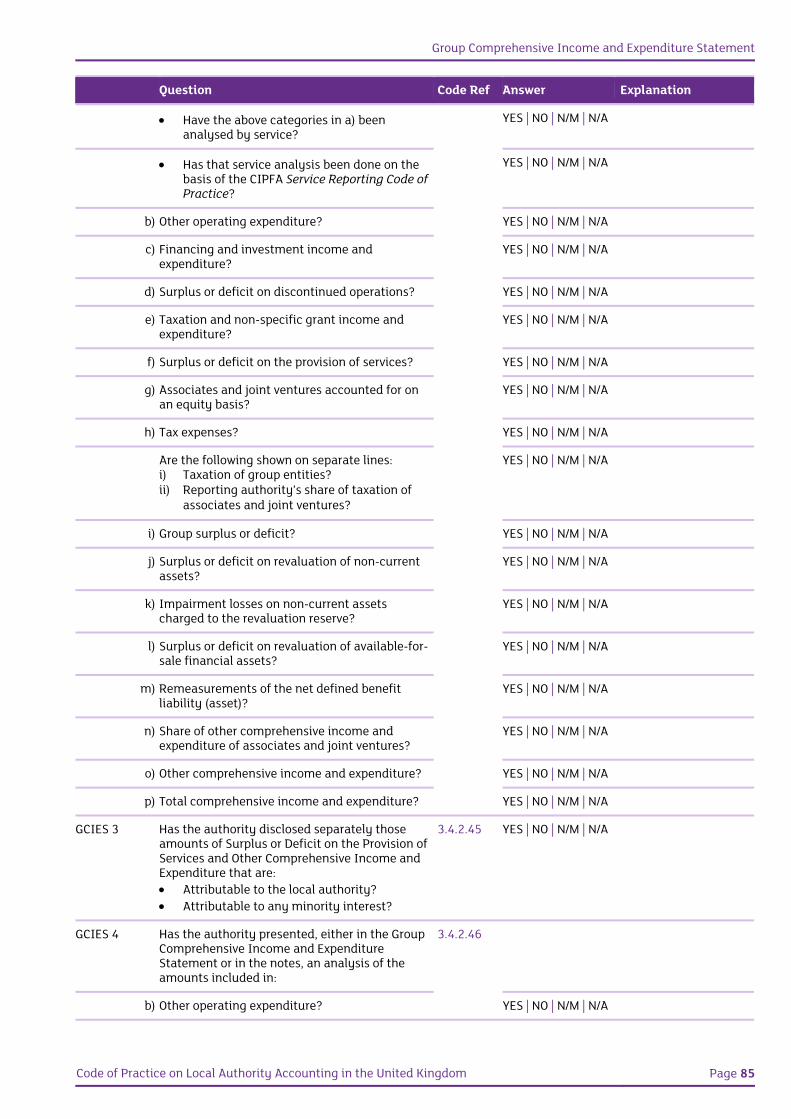

Have the above categories in a) been analysed by service?

YES | NO | N/M | N/A

Has that service analysis been done on the basis of the CIPFA Service Reporting Code of Practice?

YES | NO | N/M | N/A

b) Other operating expenditure? YES | NO | N/M | N/A

c) Financing and investment income and expenditure? YES | NO | N/M | N/A

d) Surplus or deficit on discontinued operations? YES | NO | N/M | N/A

e) Taxation and non-specific grant income and expenditure?

YES | NO | N/M | N/A

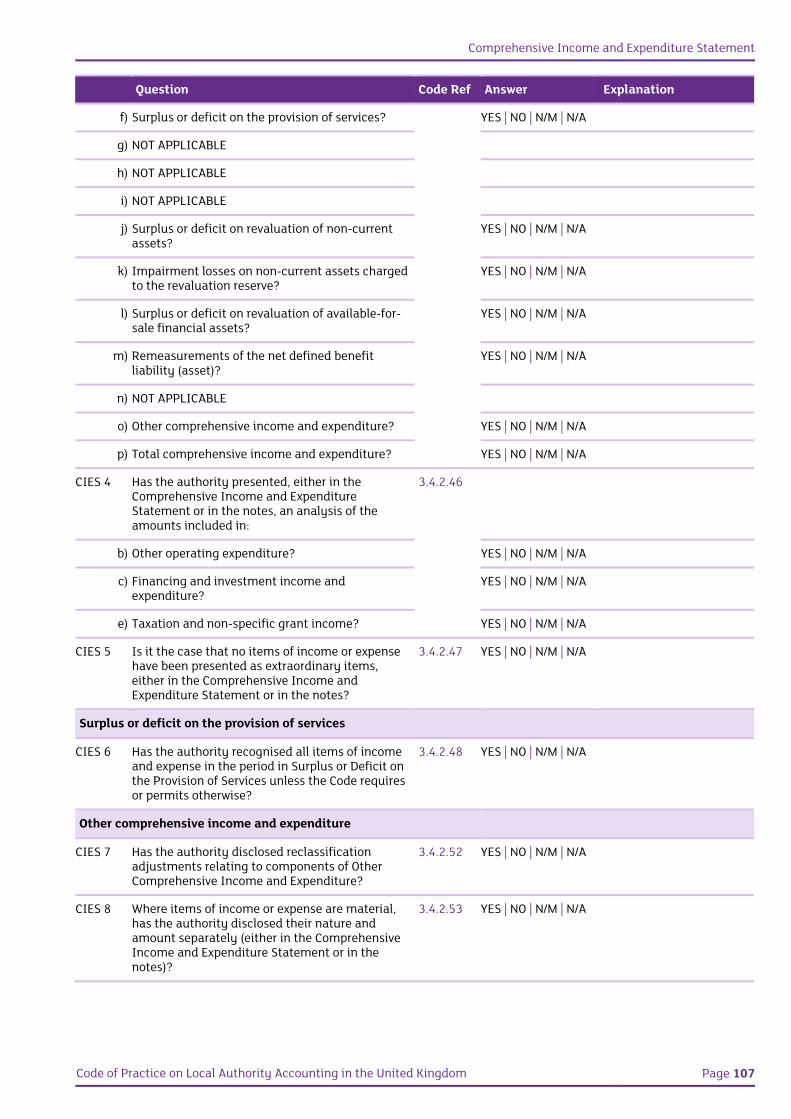

f) Surplus or deficit on the provision of services? YES | NO | N/M | N/A

g) NOT APPLICABLE

h) NOT APPLICABLE

i) NOT APPLICABLE

j) Surplus or deficit on revaluation of non-current assets?

YES | NO | N/M | N/A

k) Impairment losses on non-current assets charged to the revaluation reserve?

YES | NO | N/M | N/A

l) Surplus or deficit on revaluation of available-for-sale financial assets?

YES | NO | N/M | N/A

m) Remeasurements of the net defined benefit liability (asset)?

YES | NO | N/M | N/A

Balance Sheet

Code of Practice on Local Authority Accounting in the United Kingdom Page 13

Question Code Ref Answer Explanation

n) NOT APPLICABLE

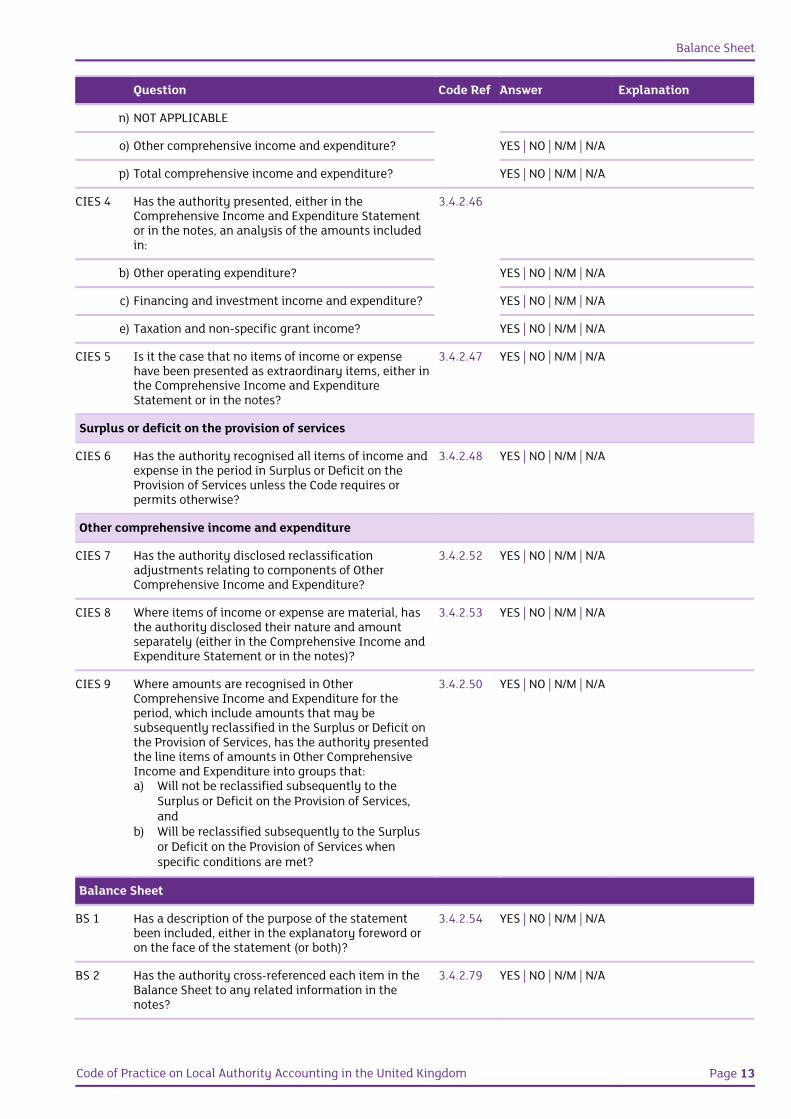

o) Other comprehensive income and expenditure? YES | NO | N/M | N/A

p) Total comprehensive income and expenditure? YES | NO | N/M | N/A

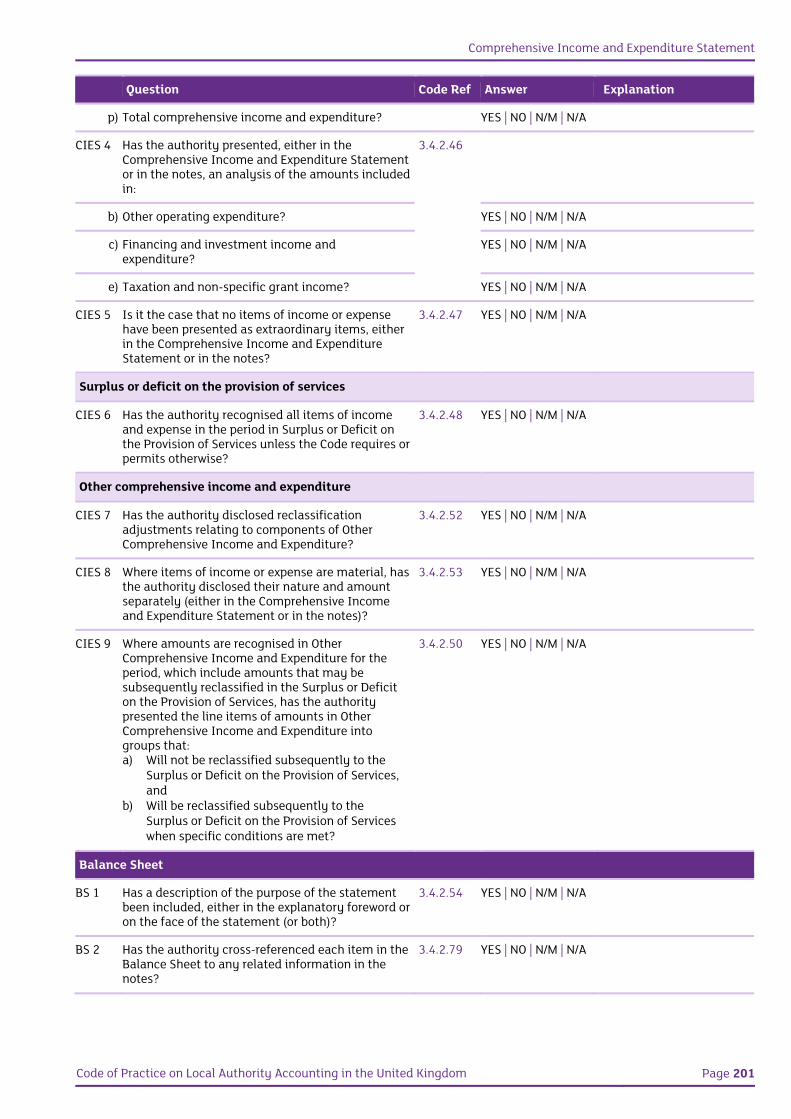

CIES 4 Has the authority presented, either in the Comprehensive Income and Expenditure Statement or in the notes, an analysis of the amounts included in:

3.4.2.46

b) Other operating expenditure? YES | NO | N/M | N/A

c) Financing and investment income and expenditure? YES | NO | N/M | N/A

e) Taxation and non-specific grant income? YES | NO | N/M | N/A

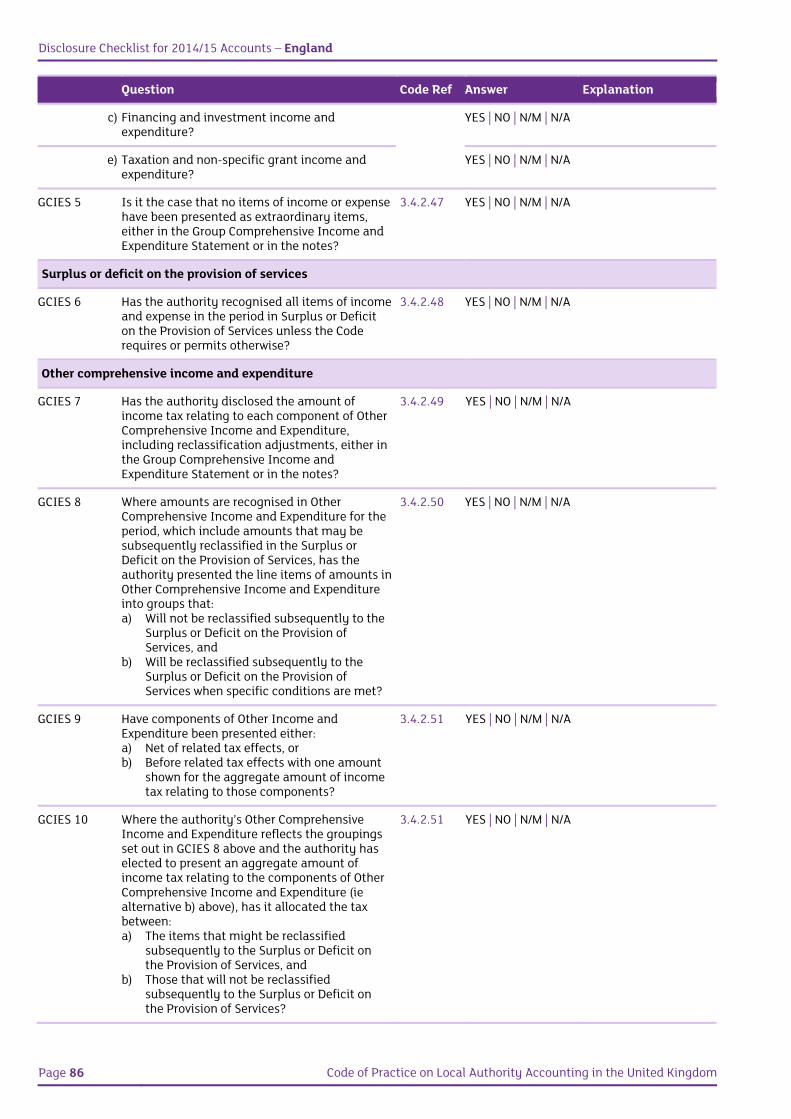

CIES 5 Is it the case that no items of income or expense have been presented as extraordinary items, either in the Comprehensive Income and Expenditure Statement or in the notes?

3.4.2.47 YES | NO | N/M | N/A

Surplus or deficit on the provision of services

CIES 6 Has the authority recognised all items of income and expense in the period in Surplus or Deficit on the Provision of Services unless the Code requires or permits otherwise?

3.4.2.48 YES | NO | N/M | N/A

Other comprehensive income and expenditure

CIES 7 Has the authority disclosed reclassification adjustments relating to components of Other Comprehensive Income and Expenditure?

3.4.2.52 YES | NO | N/M | N/A

CIES 8 Where items of income or expense are material, has the authority disclosed their nature and amount separately (either in the Comprehensive Income and Expenditure Statement or in the notes)?

3.4.2.53 YES | NO | N/M | N/A

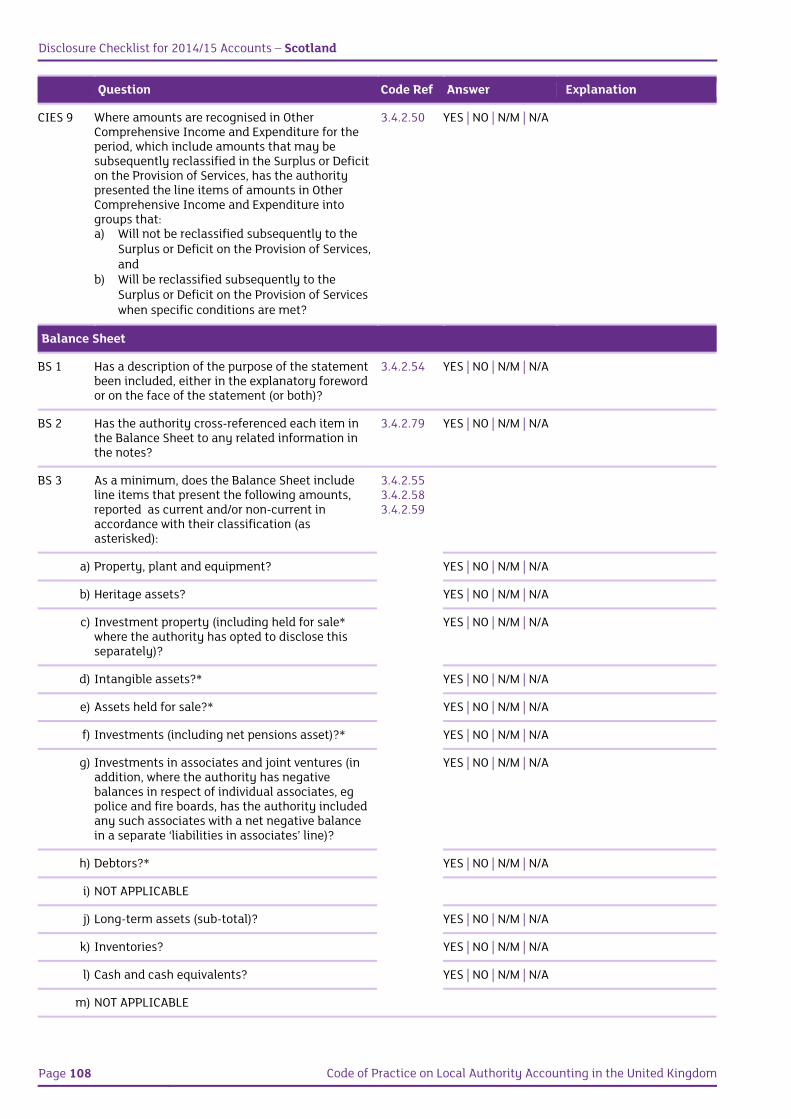

CIES 9 Where amounts are recognised in Other Comprehensive Income and Expenditure for the period, which include amounts that may be subsequently reclassified in the Surplus or Deficit on the Provision of Services, has the authority presented the line items of amounts in Other Comprehensive Income and Expenditure into groups that: a) Will not be reclassified subsequently to the

Surplus or Deficit on the Provision of Services, and

b) Will be reclassified subsequently to the Surplus or Deficit on the Provision of Services when specific conditions are met?

3.4.2.50 YES | NO | N/M | N/A

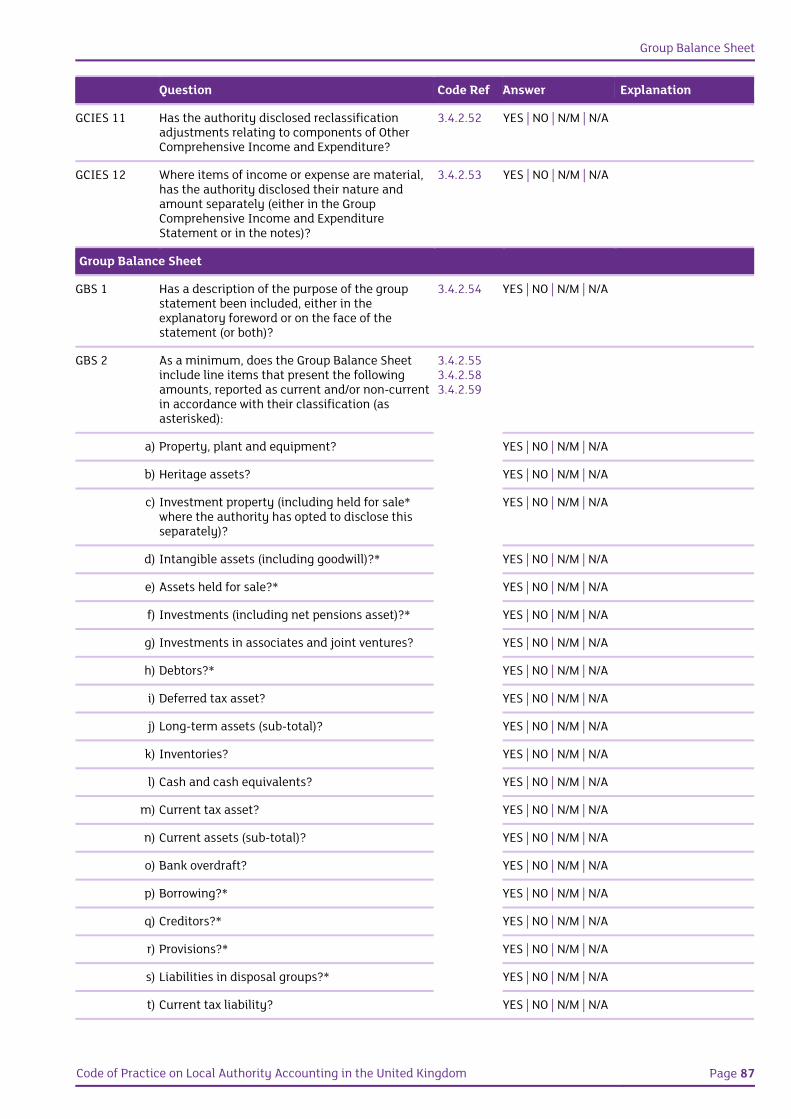

Balance Sheet

BS 1 Has a description of the purpose of the statement been included, either in the explanatory foreword or on the face of the statement (or both)?

3.4.2.54 YES | NO | N/M | N/A

BS 2 Has the authority cross-referenced each item in the Balance Sheet to any related information in the notes?

3.4.2.79 YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 14 Code of Practice on Local Authority Accounting in the United Kingdom

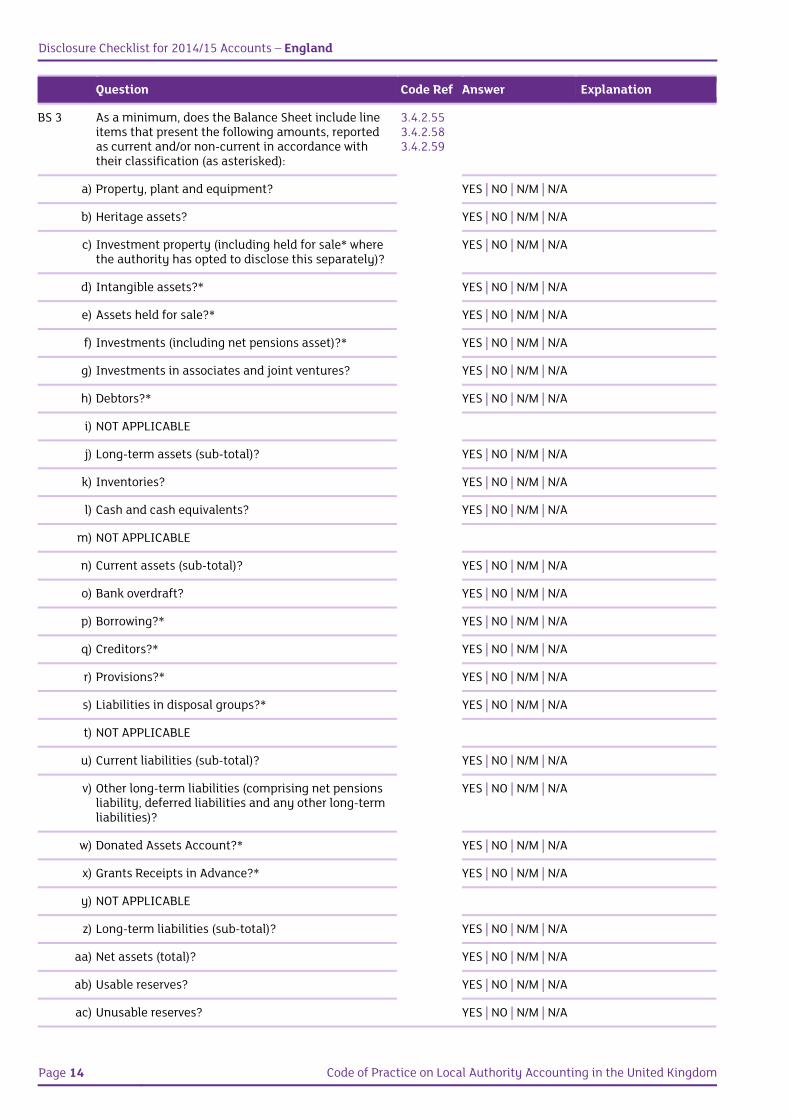

Question Code Ref Answer Explanation

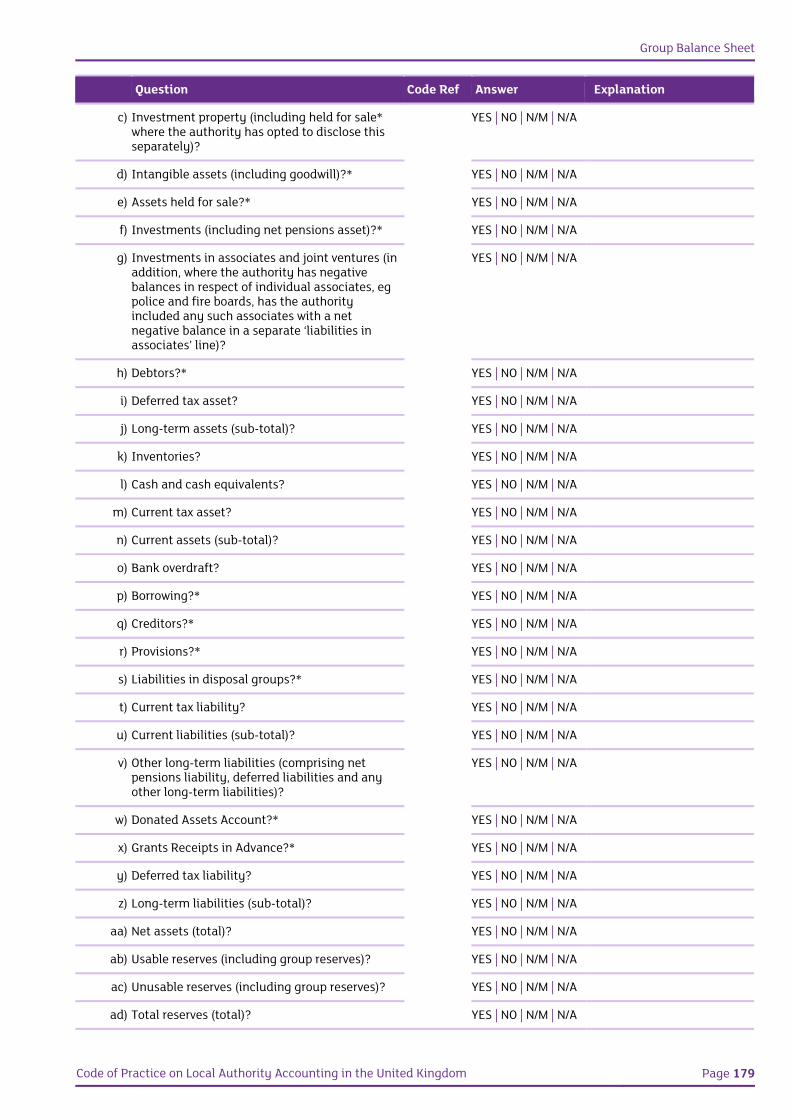

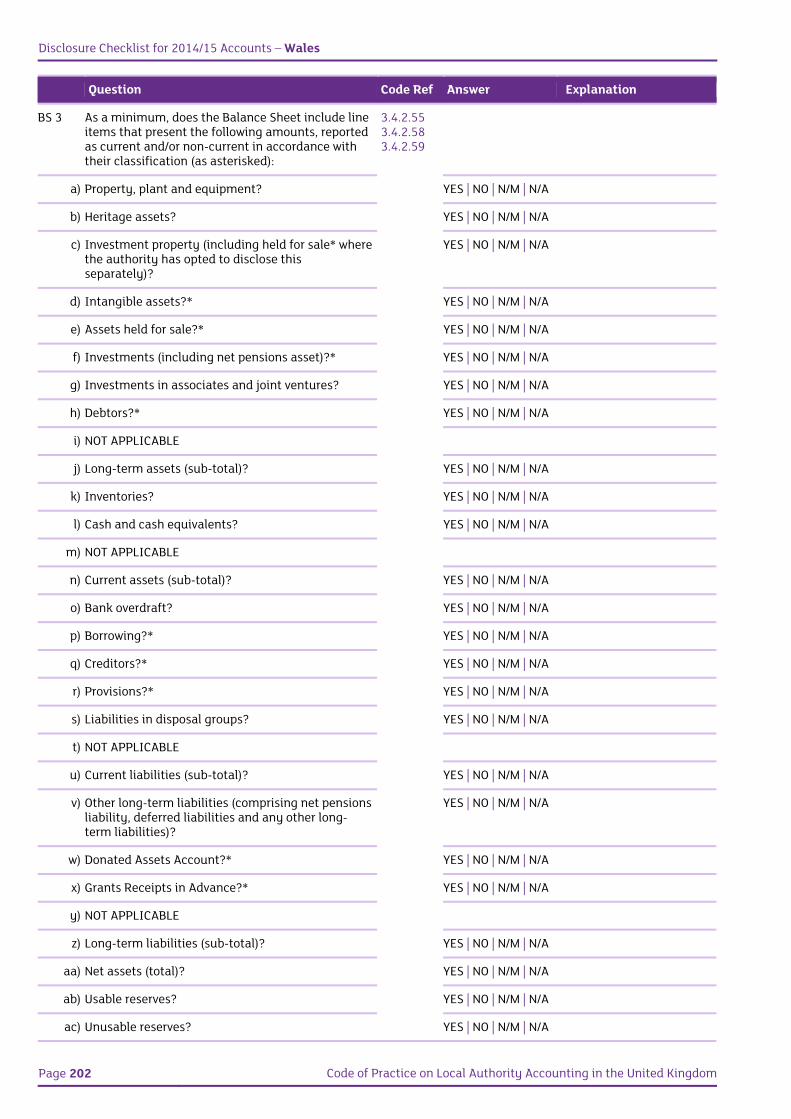

BS 3 As a minimum, does the Balance Sheet include line items that present the following amounts, reported as current and/or non-current in accordance with their classification (as asterisked):

3.4.2.553.4.2.58 3.4.2.59

a) Property, plant and equipment? YES | NO | N/M | N/A

b) Heritage assets? YES | NO | N/M | N/A

c) Investment property (including held for sale* where the authority has opted to disclose this separately)?

YES | NO | N/M | N/A

d) Intangible assets?* YES | NO | N/M | N/A

e) Assets held for sale?* YES | NO | N/M | N/A

f) Investments (including net pensions asset)?* YES | NO | N/M | N/A

g) Investments in associates and joint ventures? YES | NO | N/M | N/A

h) Debtors?* YES | NO | N/M | N/A

i) NOT APPLICABLE

j) Long-term assets (sub-total)? YES | NO | N/M | N/A

k) Inventories? YES | NO | N/M | N/A

l) Cash and cash equivalents? YES | NO | N/M | N/A

m) NOT APPLICABLE

n) Current assets (sub-total)? YES | NO | N/M | N/A

o) Bank overdraft? YES | NO | N/M | N/A

p) Borrowing?* YES | NO | N/M | N/A

q) Creditors?* YES | NO | N/M | N/A

r) Provisions?* YES | NO | N/M | N/A

s) Liabilities in disposal groups?* YES | NO | N/M | N/A

t) NOT APPLICABLE

u) Current liabilities (sub-total)? YES | NO | N/M | N/A

v) Other long-term liabilities (comprising net pensions liability, deferred liabilities and any other long-term liabilities)?

YES | NO | N/M | N/A

w) Donated Assets Account?* YES | NO | N/M | N/A

x) Grants Receipts in Advance?* YES | NO | N/M | N/A

y) NOT APPLICABLE

z) Long-term liabilities (sub-total)? YES | NO | N/M | N/A

aa) Net assets (total)? YES | NO | N/M | N/A

ab) Usable reserves? YES | NO | N/M | N/A

ac) Unusable reserves? YES | NO | N/M | N/A

Balance Sheet

Code of Practice on Local Authority Accounting in the United Kingdom Page 15

Question Code Ref Answer Explanation

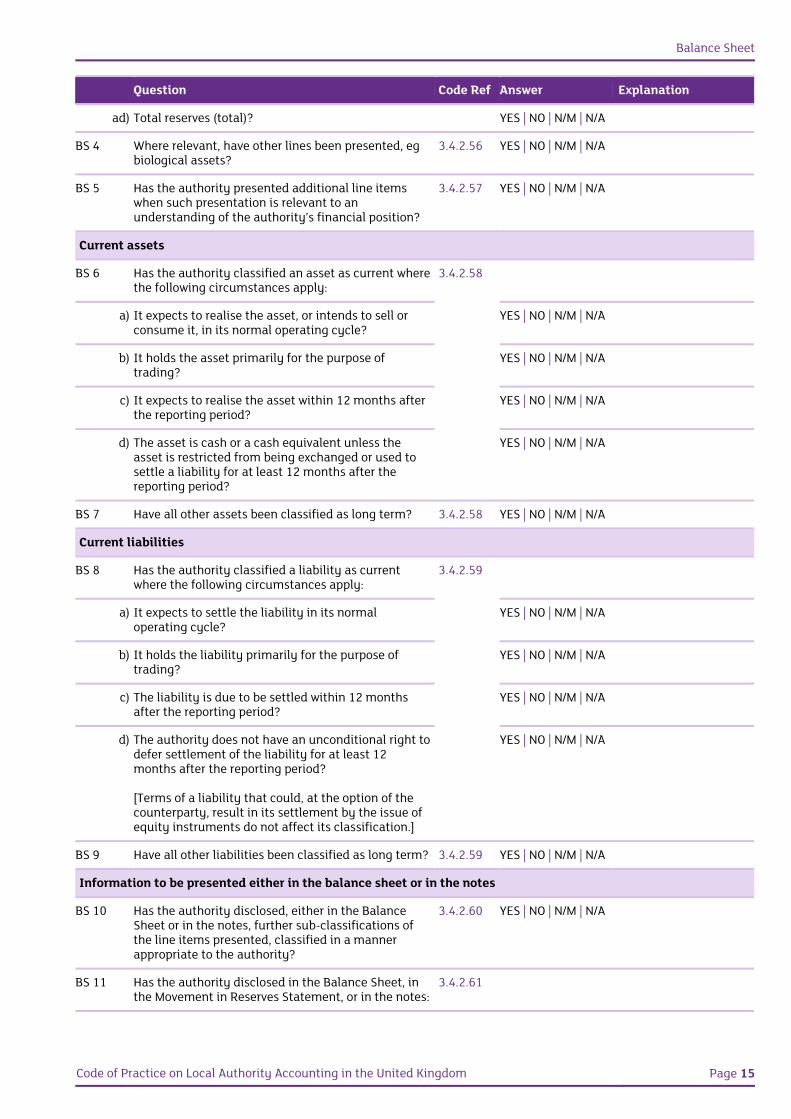

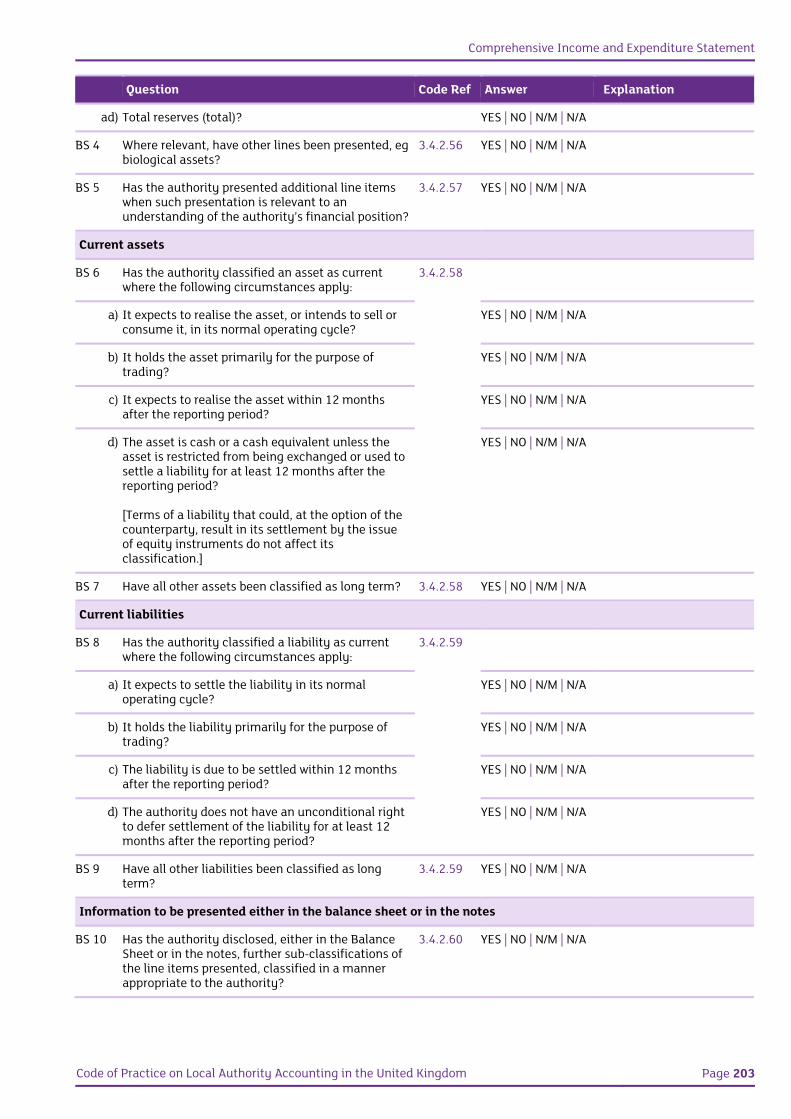

ad) Total reserves (total)? YES | NO | N/M | N/A

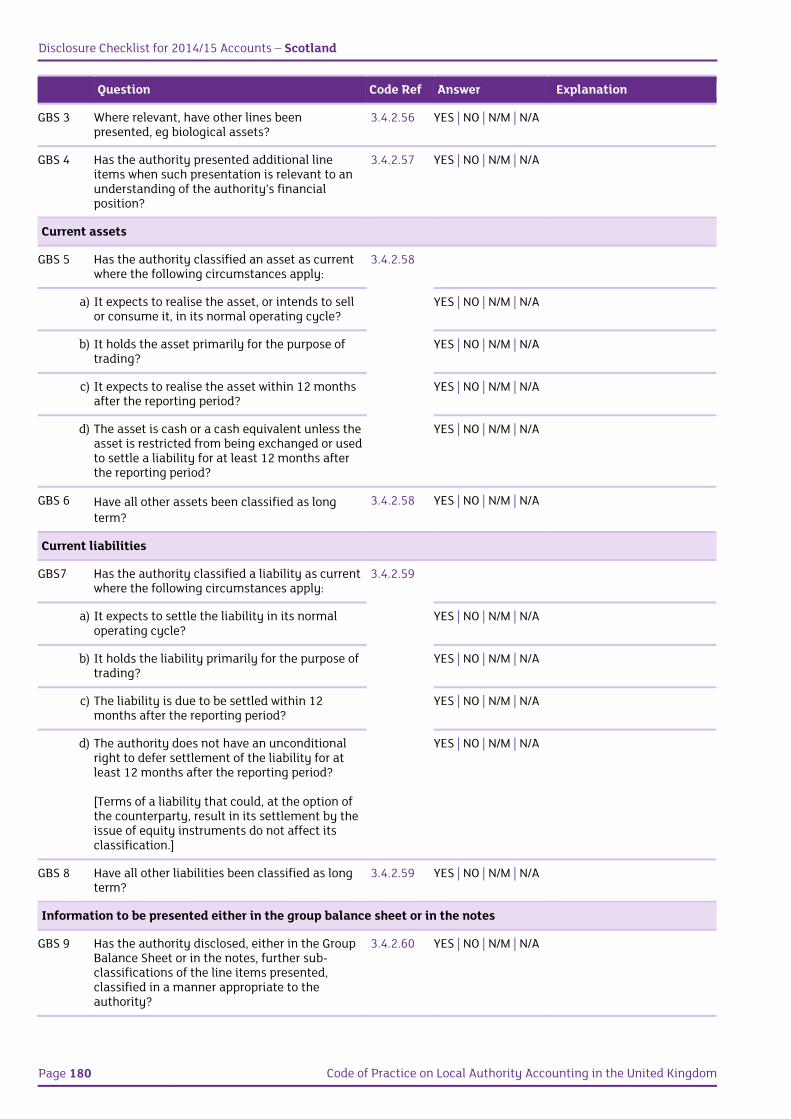

BS 4 Where relevant, have other lines been presented, eg biological assets?

3.4.2.56 YES | NO | N/M | N/A

BS 5 Has the authority presented additional line items when such presentation is relevant to an understanding of the authority’s financial position?

3.4.2.57 YES | NO | N/M | N/A

Current assets

BS 6 Has the authority classified an asset as current where the following circumstances apply:

3.4.2.58

a) It expects to realise the asset, or intends to sell or consume it, in its normal operating cycle?

YES | NO | N/M | N/A

b) It holds the asset primarily for the purpose of trading?

YES | NO | N/M | N/A

c) It expects to realise the asset within 12 months after the reporting period?

YES | NO | N/M | N/A

d) The asset is cash or a cash equivalent unless the asset is restricted from being exchanged or used to settle a liability for at least 12 months after the reporting period?

YES | NO | N/M | N/A

BS 7 Have all other assets been classified as long term? 3.4.2.58 YES | NO | N/M | N/A

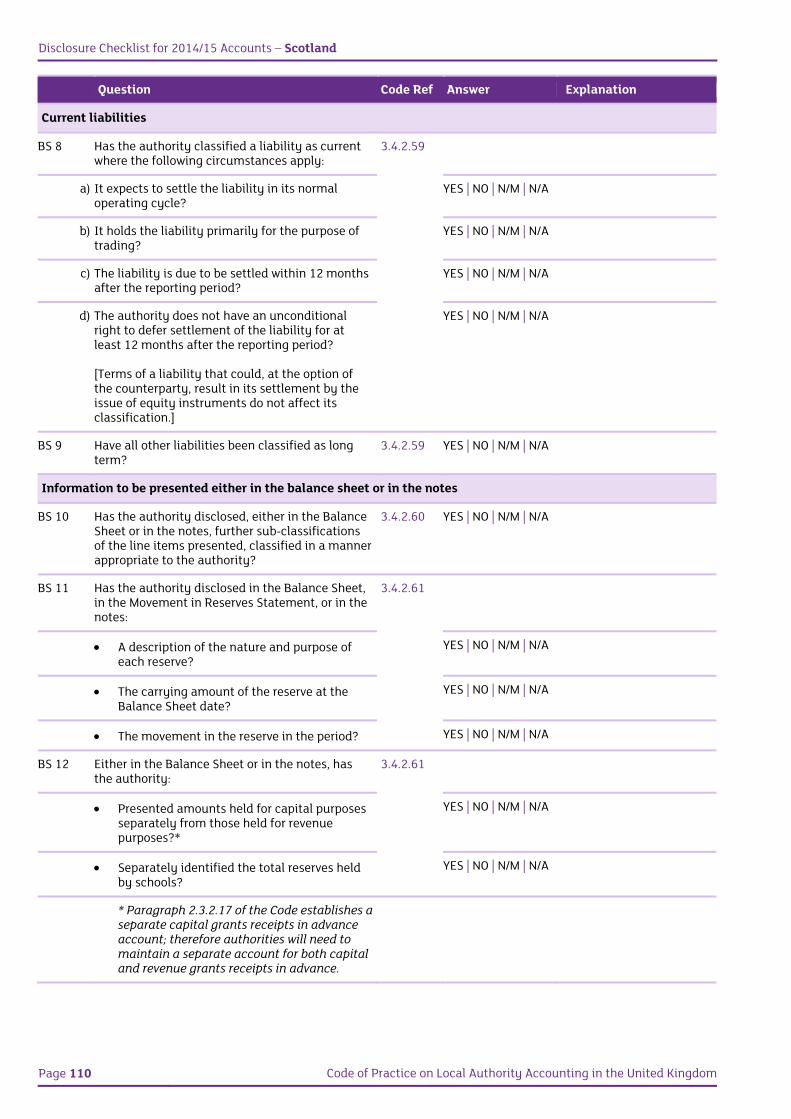

Current liabilities

BS 8 Has the authority classified a liability as current where the following circumstances apply:

3.4.2.59

a) It expects to settle the liability in its normal operating cycle?

YES | NO | N/M | N/A

b) It holds the liability primarily for the purpose of trading?

YES | NO | N/M | N/A

c) The liability is due to be settled within 12 months after the reporting period?

YES | NO | N/M | N/A

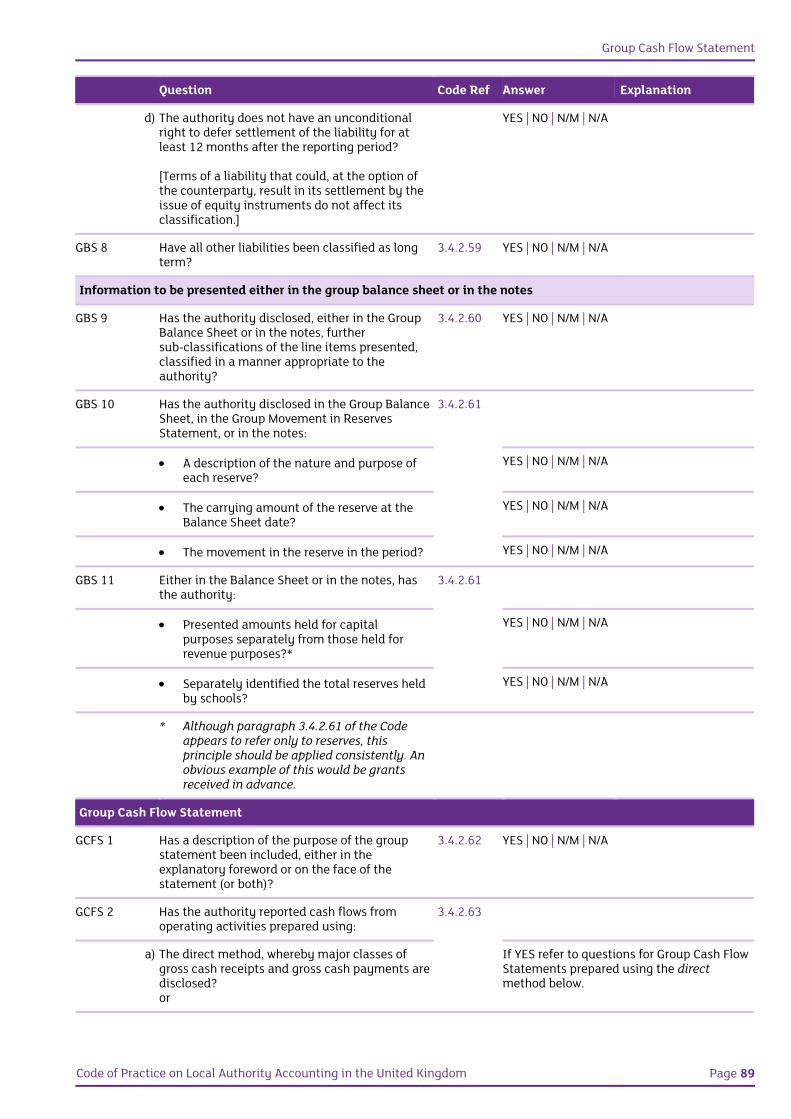

d) The authority does not have an unconditional right to defer settlement of the liability for at least 12 months after the reporting period? [Terms of a liability that could, at the option of the counterparty, result in its settlement by the issue of equity instruments do not affect its classification.]

YES | NO | N/M | N/A

BS 9 Have all other liabilities been classified as long term? 3.4.2.59 YES | NO | N/M | N/A

Information to be presented either in the balance sheet or in the notes

BS 10 Has the authority disclosed, either in the Balance Sheet or in the notes, further sub-classifications of the line items presented, classified in a manner appropriate to the authority?

3.4.2.60 YES | NO | N/M | N/A

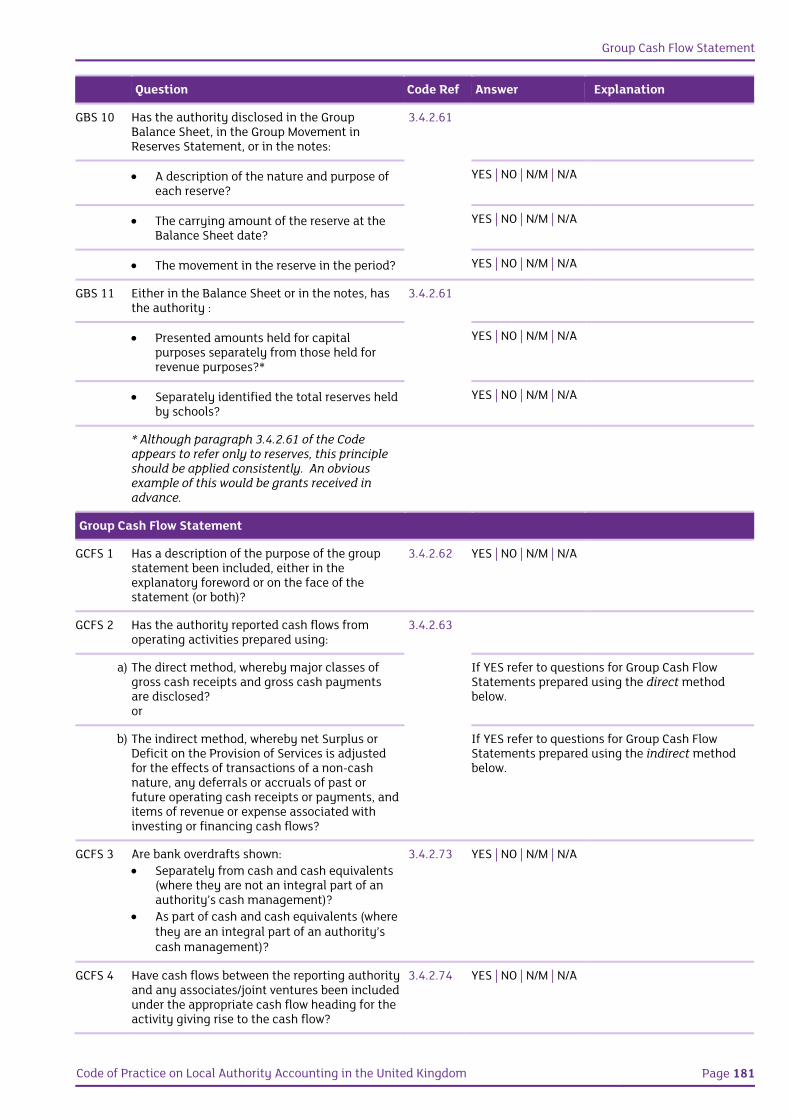

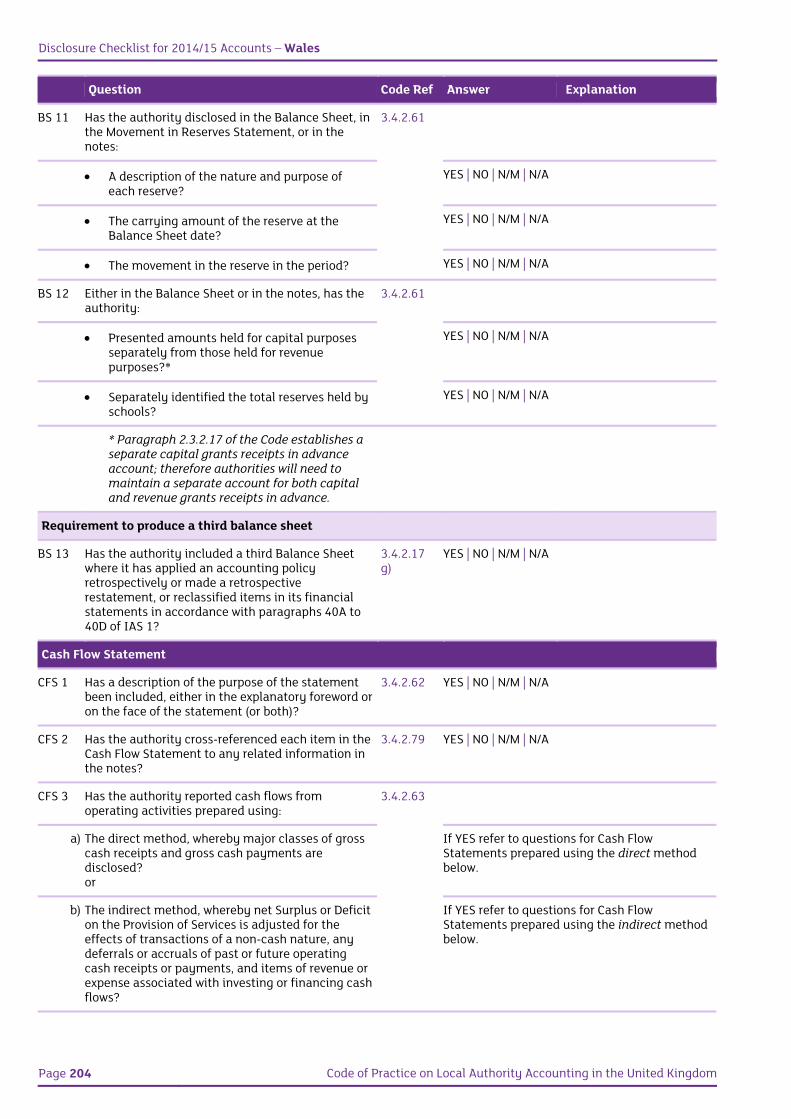

BS 11 Has the authority disclosed in the Balance Sheet, in the Movement in Reserves Statement, or in the notes:

3.4.2.61

Disclosure Checklist for 2014/15 Accounts – England

Page 16 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

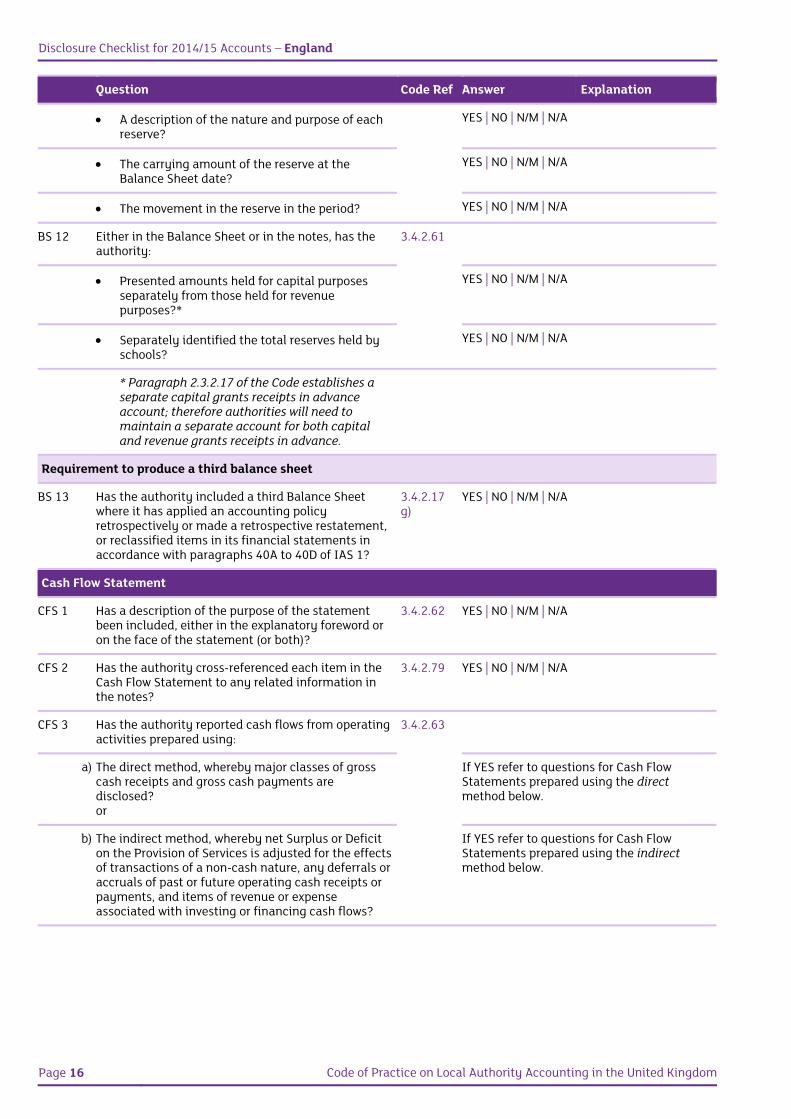

A description of the nature and purpose of each reserve?

YES | NO | N/M | N/A

The carrying amount of the reserve at the Balance Sheet date?

YES | NO | N/M | N/A

The movement in the reserve in the period? YES | NO | N/M | N/A

BS 12 Either in the Balance Sheet or in the notes, has the authority:

3.4.2.61

Presented amounts held for capital purposes separately from those held for revenue purposes?*

YES | NO | N/M | N/A

Separately identified the total reserves held by schools?

YES | NO | N/M | N/A

* Paragraph 2.3.2.17 of the Code establishes a separate capital grants receipts in advance account; therefore authorities will need to maintain a separate account for both capital and revenue grants receipts in advance.

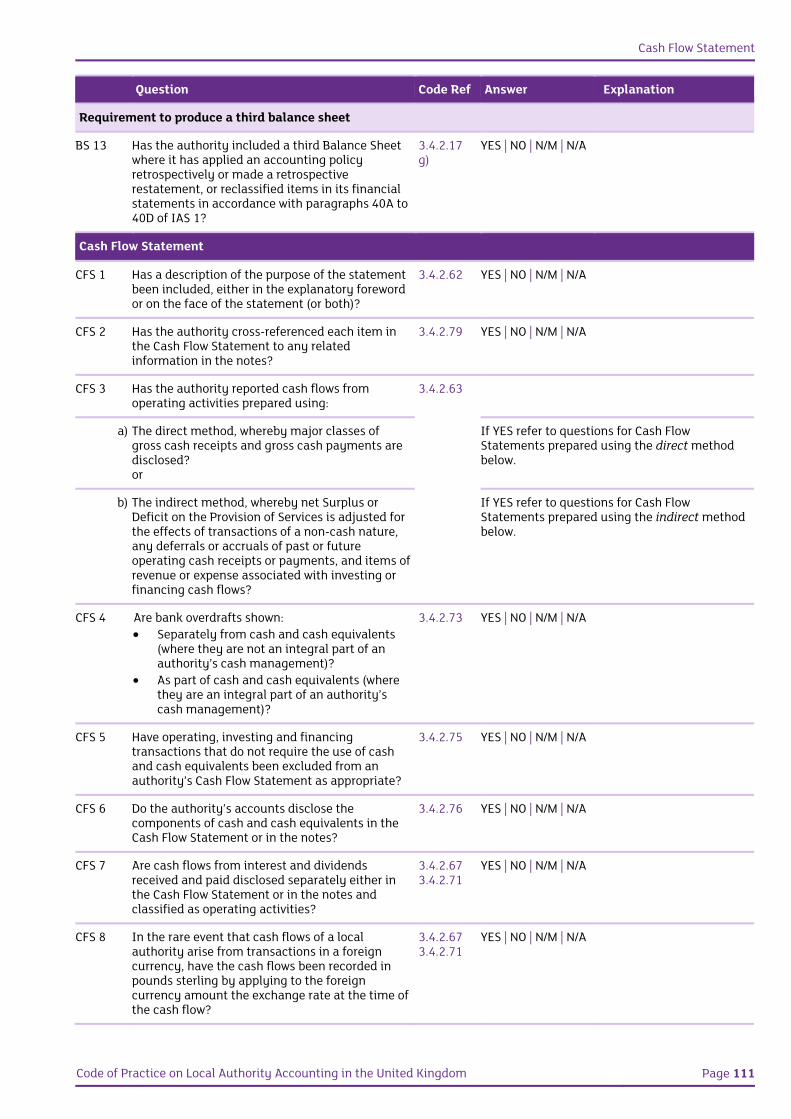

Requirement to produce a third balance sheet

BS 13 Has the authority included a third Balance Sheet where it has applied an accounting policy retrospectively or made a retrospective restatement, or reclassified items in its financial statements in accordance with paragraphs 40A to 40D of IAS 1?

3.4.2.17 g)

YES | NO | N/M | N/A

Cash Flow Statement

CFS 1 Has a description of the purpose of the statement been included, either in the explanatory foreword or on the face of the statement (or both)?

3.4.2.62 YES | NO | N/M | N/A

CFS 2 Has the authority cross-referenced each item in the Cash Flow Statement to any related information in the notes?

3.4.2.79 YES | NO | N/M | N/A

CFS 3 Has the authority reported cash flows from operating activities prepared using:

3.4.2.63

a) The direct method, whereby major classes of gross cash receipts and gross cash payments are disclosed? or

If YES refer to questions for Cash Flow Statements prepared using the direct method below.

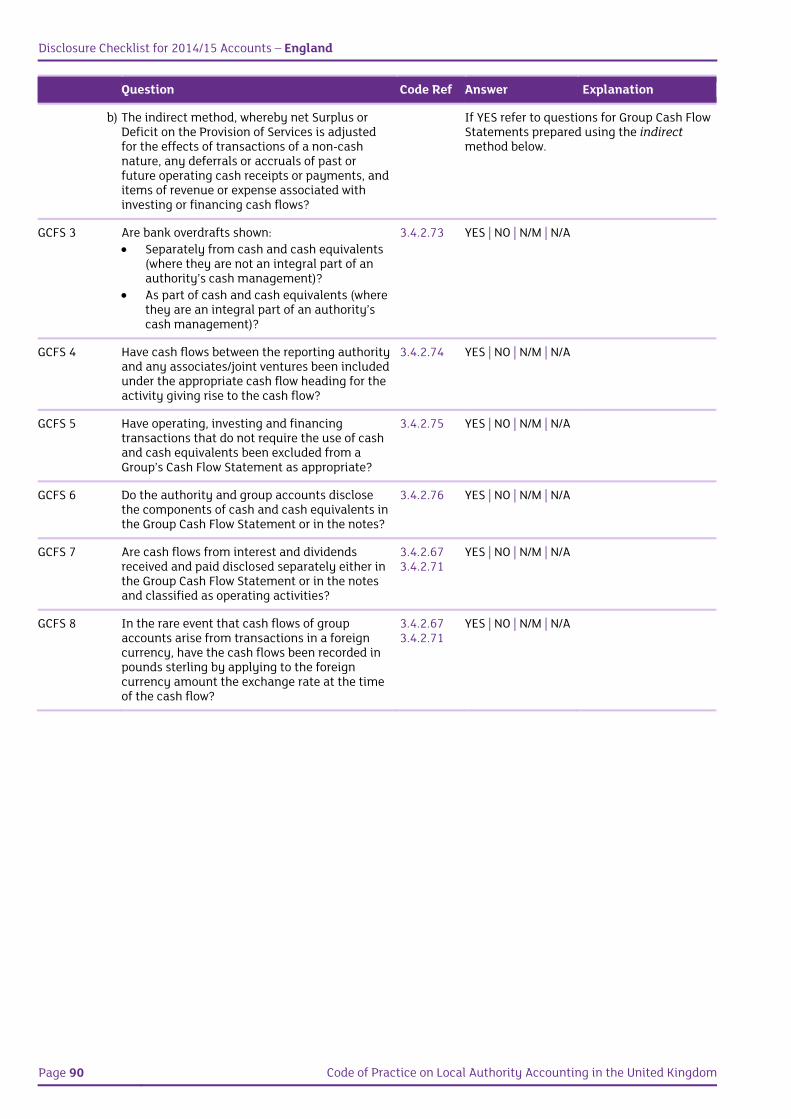

b) The indirect method, whereby net Surplus or Deficit on the Provision of Services is adjusted for the effects of transactions of a non-cash nature, any deferrals or accruals of past or future operating cash receipts or payments, and items of revenue or expense associated with investing or financing cash flows?

If YES refer to questions for Cash Flow Statements prepared using the indirect method below.

Cash Flow Statement

Code of Practice on Local Authority Accounting in the United Kingdom Page 17

Question Code Ref Answer Explanation

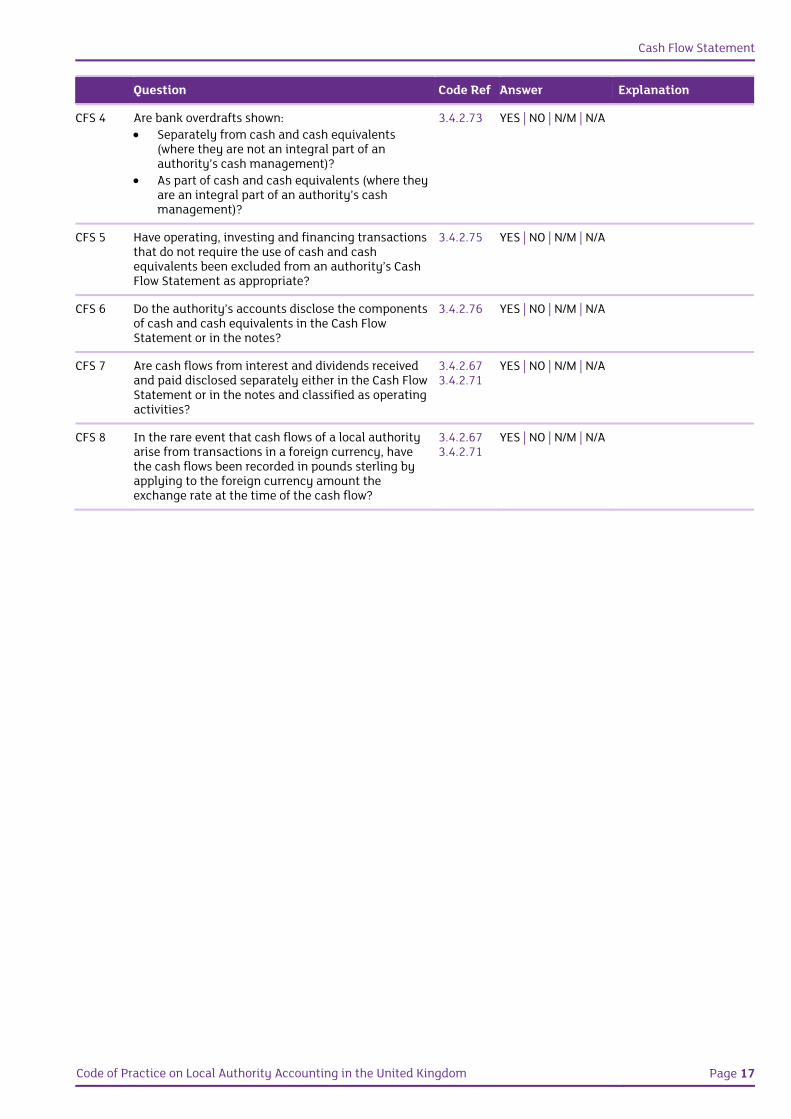

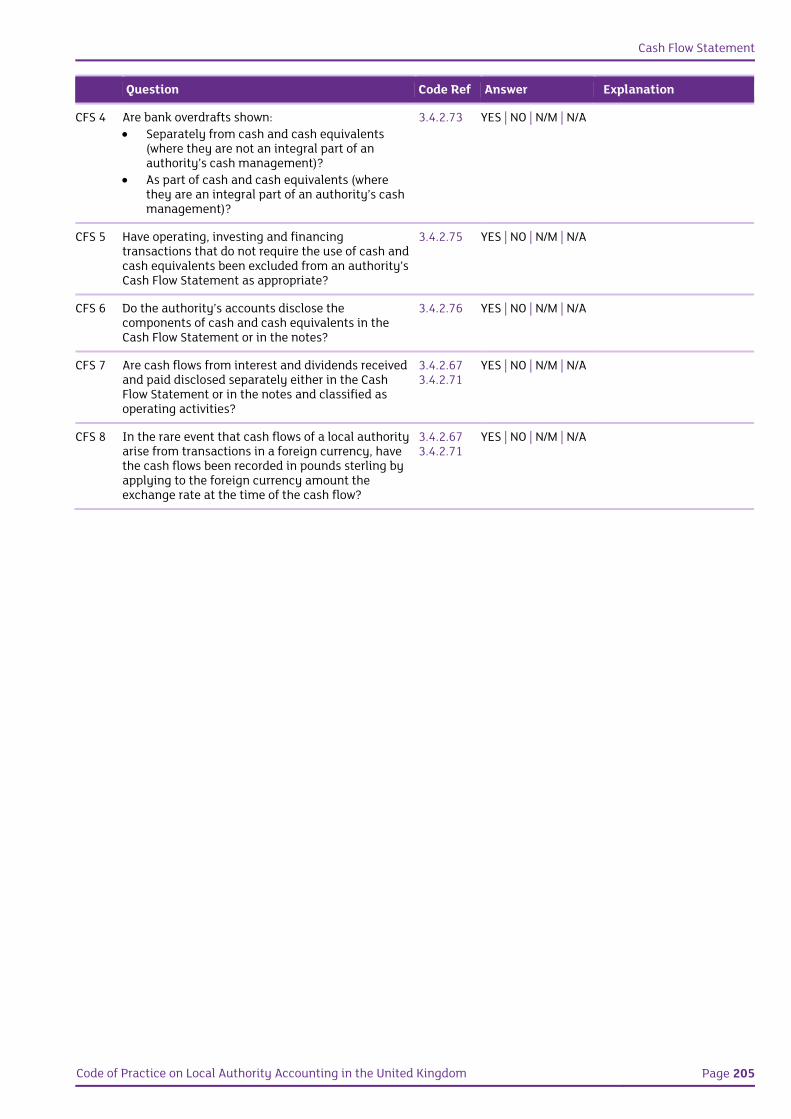

CFS 4 Are bank overdrafts shown: Separately from cash and cash equivalents

(where they are not an integral part of an authority’s cash management)?

As part of cash and cash equivalents (where they are an integral part of an authority’s cash management)?

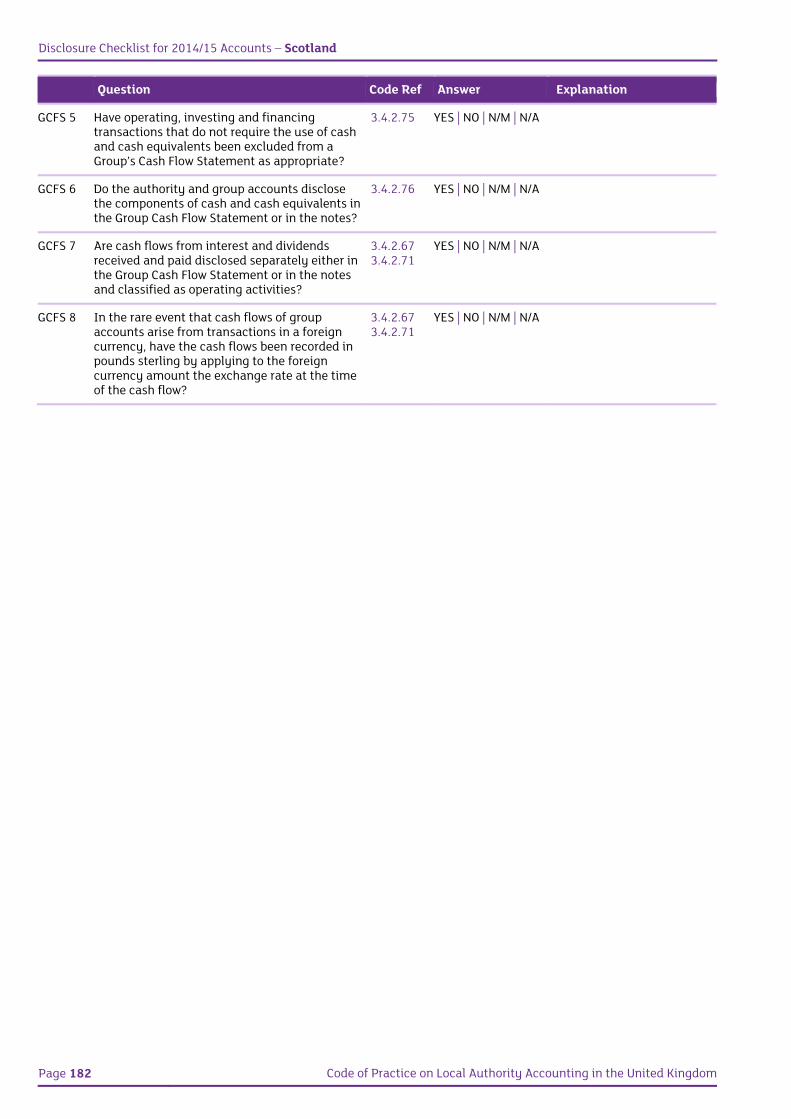

3.4.2.73 YES | NO | N/M | N/A

CFS 5 Have operating, investing and financing transactions that do not require the use of cash and cash equivalents been excluded from an authority’s Cash Flow Statement as appropriate?

3.4.2.75 YES | NO | N/M | N/A

CFS 6 Do the authority’s accounts disclose the components of cash and cash equivalents in the Cash Flow Statement or in the notes?

3.4.2.76 YES | NO | N/M | N/A

CFS 7 Are cash flows from interest and dividends received and paid disclosed separately either in the Cash Flow Statement or in the notes and classified as operating activities?

3.4.2.673.4.2.71

YES | NO | N/M | N/A

CFS 8 In the rare event that cash flows of a local authority arise from transactions in a foreign currency, have the cash flows been recorded in pounds sterling by applying to the foreign currency amount the exchange rate at the time of the cash flow?

3.4.2.673.4.2.71

YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 18 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

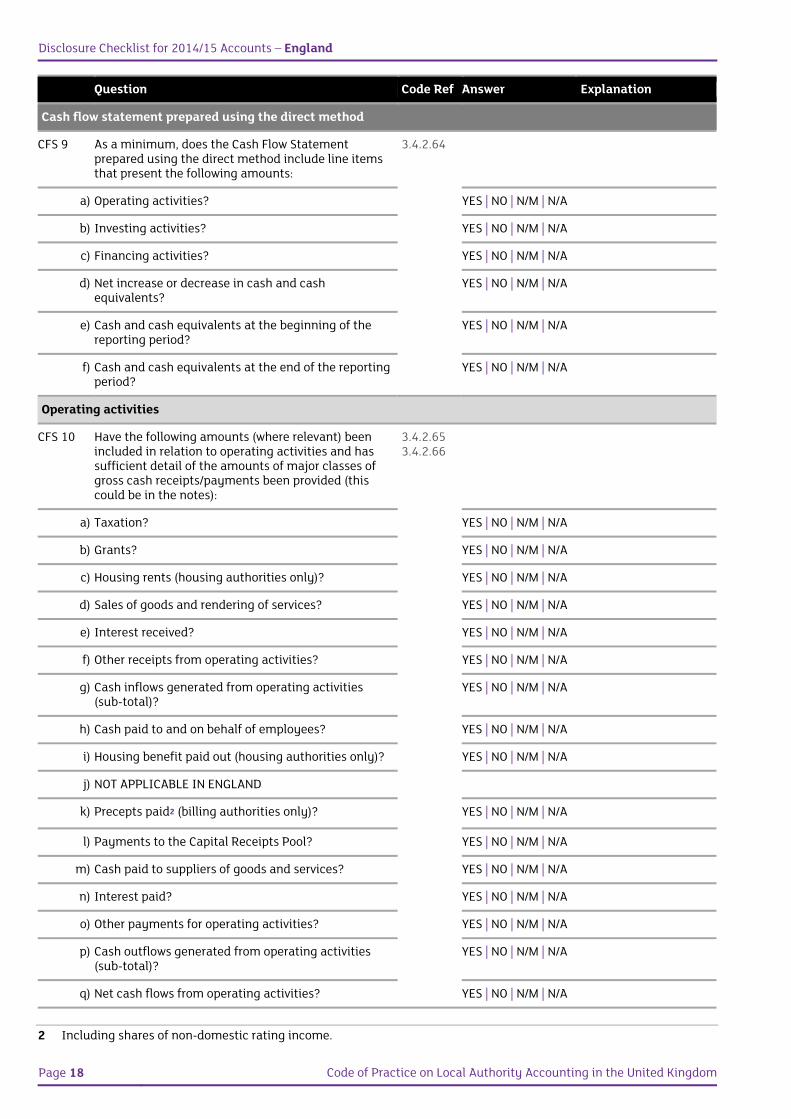

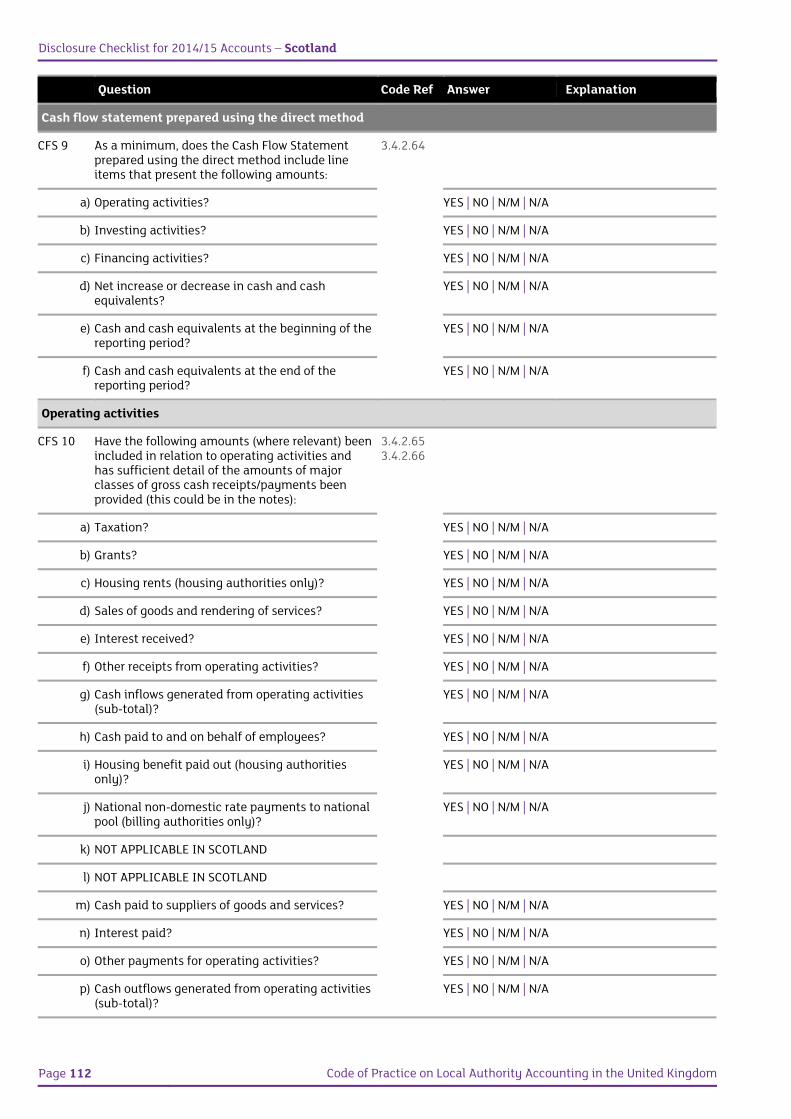

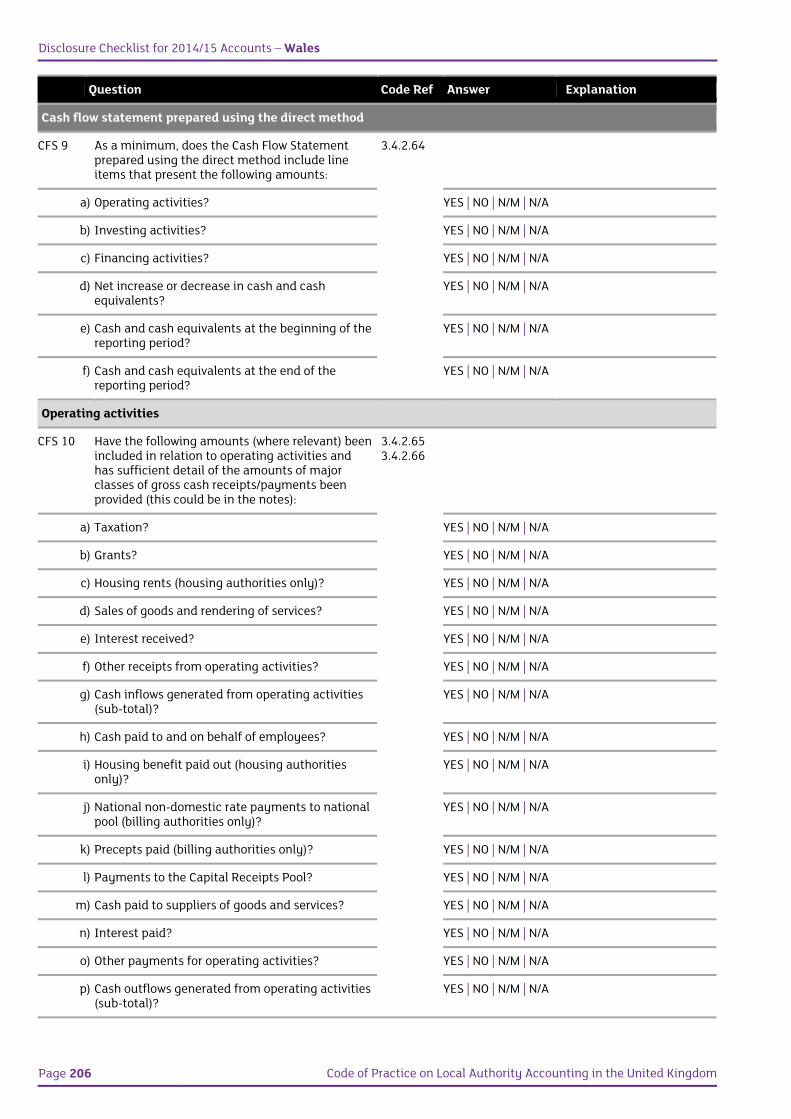

Cash flow statement prepared using the direct method

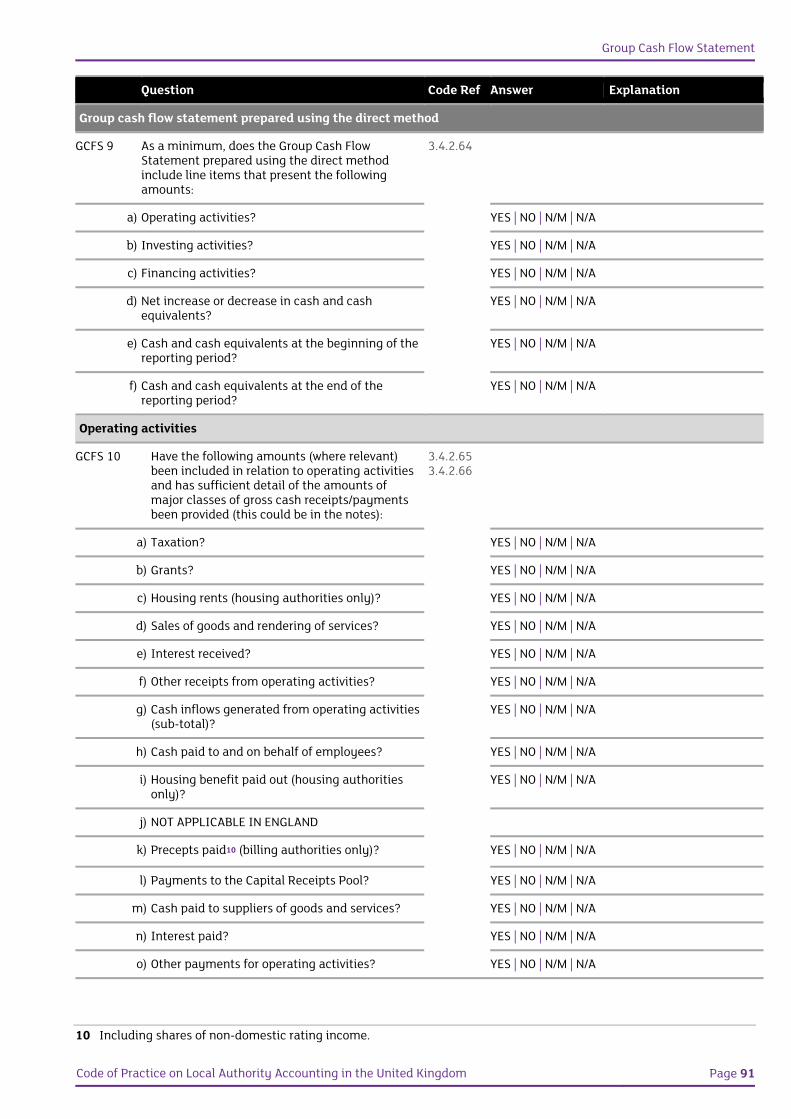

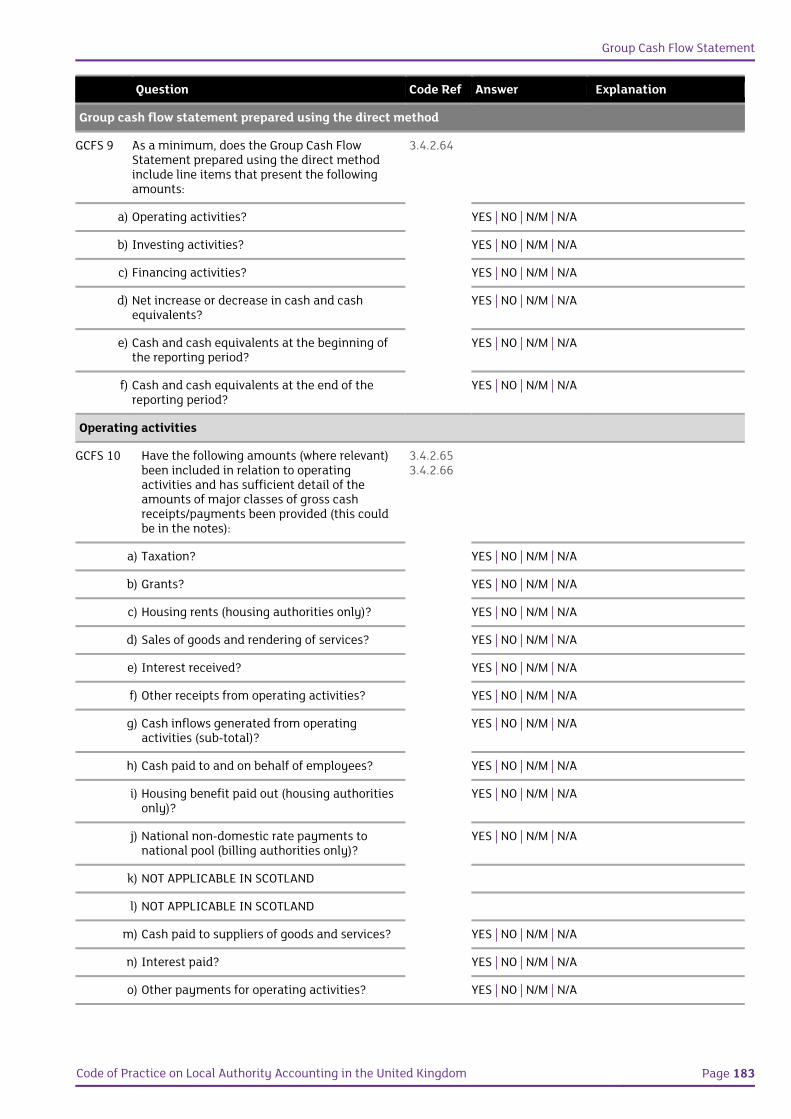

CFS 9 As a minimum, does the Cash Flow Statement prepared using the direct method include line items that present the following amounts:

3.4.2.64

a) Operating activities? YES | NO | N/M | N/A

b) Investing activities? YES | NO | N/M | N/A

c) Financing activities? YES | NO | N/M | N/A

d) Net increase or decrease in cash and cash equivalents?

YES | NO | N/M | N/A

e) Cash and cash equivalents at the beginning of the reporting period?

YES | NO | N/M | N/A

f) Cash and cash equivalents at the end of the reporting period?

YES | NO | N/M | N/A

Operating activities

CFS 10 Have the following amounts (where relevant) been included in relation to operating activities and has sufficient detail of the amounts of major classes of gross cash receipts/payments been provided (this could be in the notes):

3.4.2.653.4.2.66

a) Taxation? YES | NO | N/M | N/A

b) Grants? YES | NO | N/M | N/A

c) Housing rents (housing authorities only)? YES | NO | N/M | N/A

d) Sales of goods and rendering of services? YES | NO | N/M | N/A

e) Interest received? YES | NO | N/M | N/A

f) Other receipts from operating activities? YES | NO | N/M | N/A

g) Cash inflows generated from operating activities (sub-total)?

YES | NO | N/M | N/A

h) Cash paid to and on behalf of employees? YES | NO | N/M | N/A

i) Housing benefit paid out (housing authorities only)? YES | NO | N/M | N/A

j) NOT APPLICABLE IN ENGLAND

k) Precepts paid2 (billing authorities only)? YES | NO | N/M | N/A

l) Payments to the Capital Receipts Pool? YES | NO | N/M | N/A

m) Cash paid to suppliers of goods and services? YES | NO | N/M | N/A

n) Interest paid? YES | NO | N/M | N/A

o) Other payments for operating activities? YES | NO | N/M | N/A

p) Cash outflows generated from operating activities (sub-total)?

YES | NO | N/M | N/A

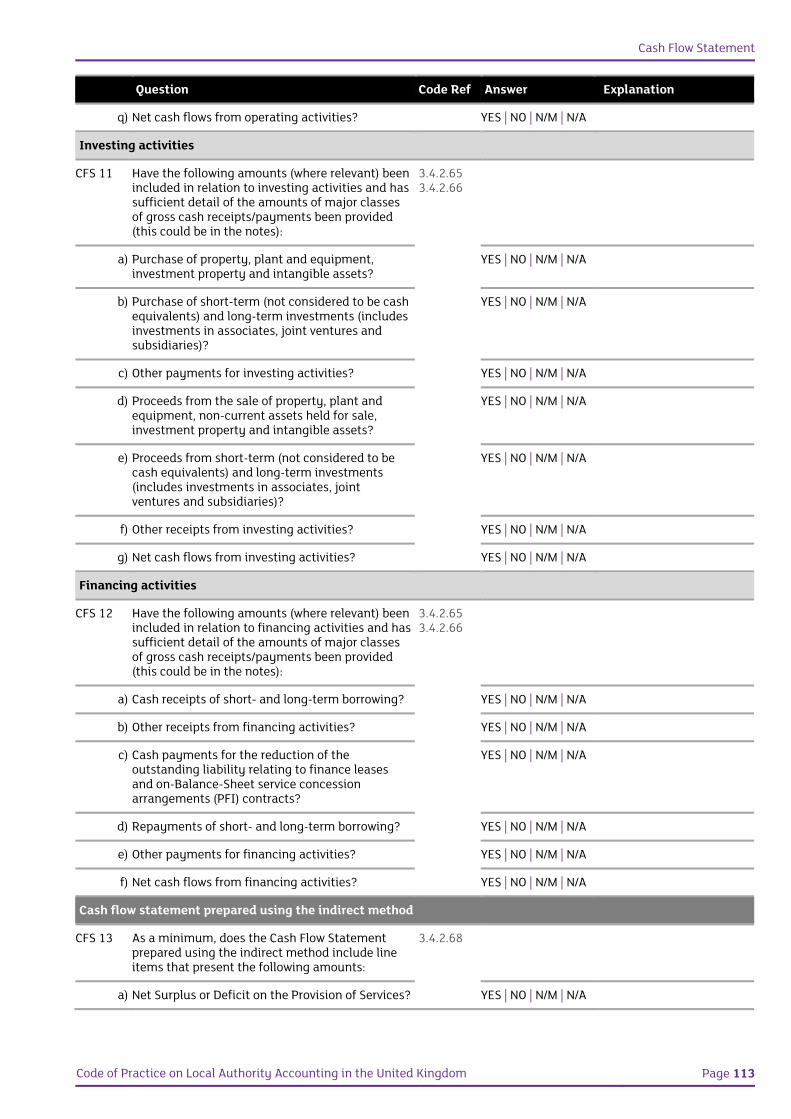

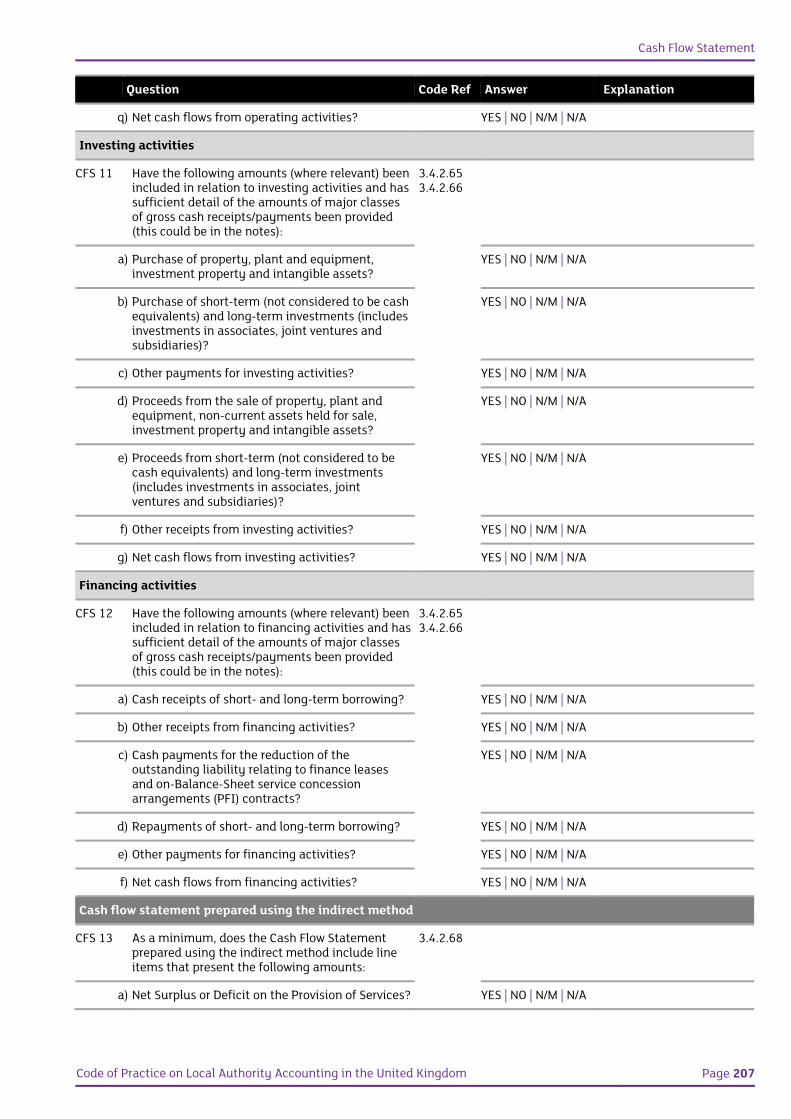

q) Net cash flows from operating activities? YES | NO | N/M | N/A

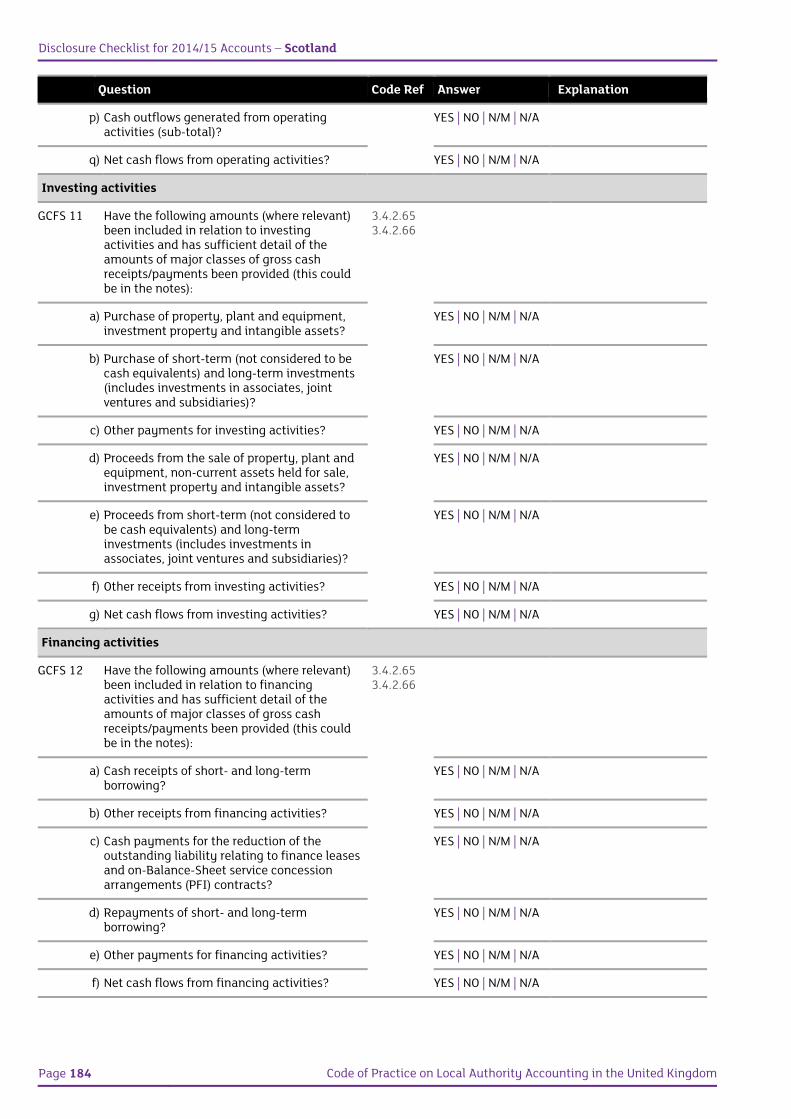

2 Including shares of non-domestic rating income.

Cash Flow Statement

Code of Practice on Local Authority Accounting in the United Kingdom Page 19

Question Code Ref Answer Explanation

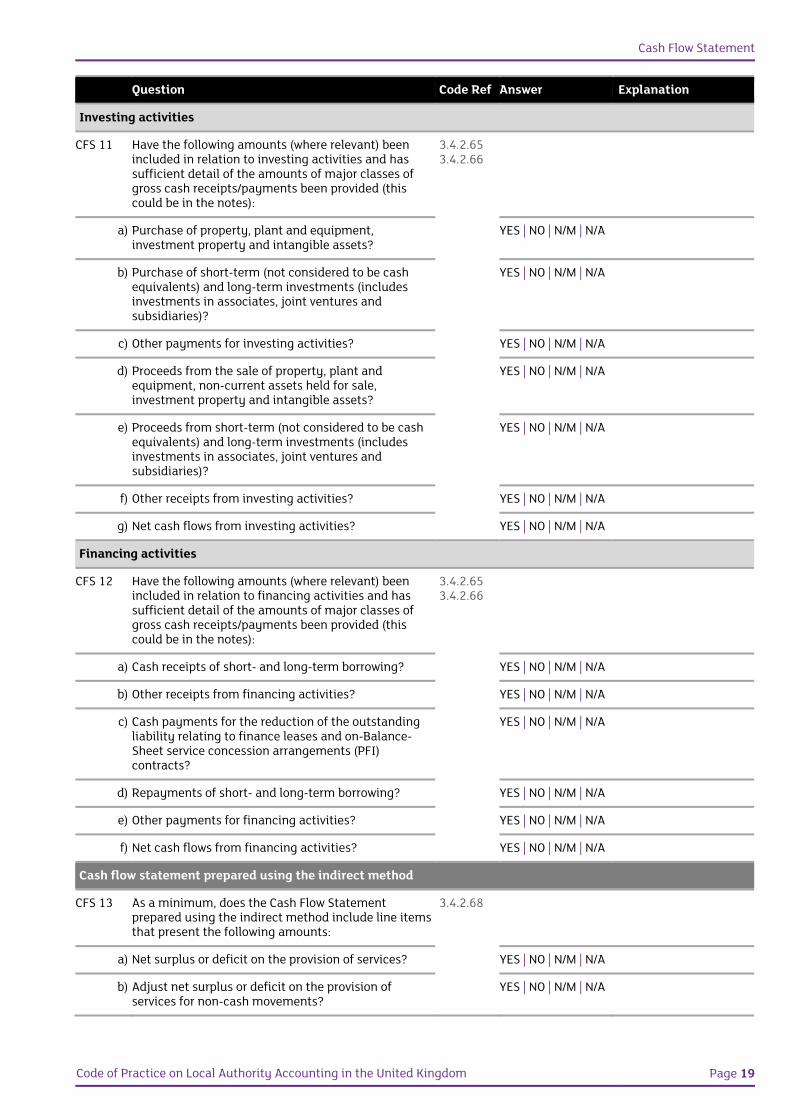

Investing activities

CFS 11 Have the following amounts (where relevant) been included in relation to investing activities and has sufficient detail of the amounts of major classes of gross cash receipts/payments been provided (this could be in the notes):

3.4.2.653.4.2.66

a) Purchase of property, plant and equipment, investment property and intangible assets?

YES | NO | N/M | N/A

b) Purchase of short-term (not considered to be cash equivalents) and long-term investments (includes investments in associates, joint ventures and subsidiaries)?

YES | NO | N/M | N/A

c) Other payments for investing activities? YES | NO | N/M | N/A

d) Proceeds from the sale of property, plant and equipment, non-current assets held for sale, investment property and intangible assets?

YES | NO | N/M | N/A

e) Proceeds from short-term (not considered to be cash equivalents) and long-term investments (includes investments in associates, joint ventures and subsidiaries)?

YES | NO | N/M | N/A

f) Other receipts from investing activities? YES | NO | N/M | N/A

g) Net cash flows from investing activities? YES | NO | N/M | N/A

Financing activities

CFS 12 Have the following amounts (where relevant) been included in relation to financing activities and has sufficient detail of the amounts of major classes of gross cash receipts/payments been provided (this could be in the notes):

3.4.2.653.4.2.66

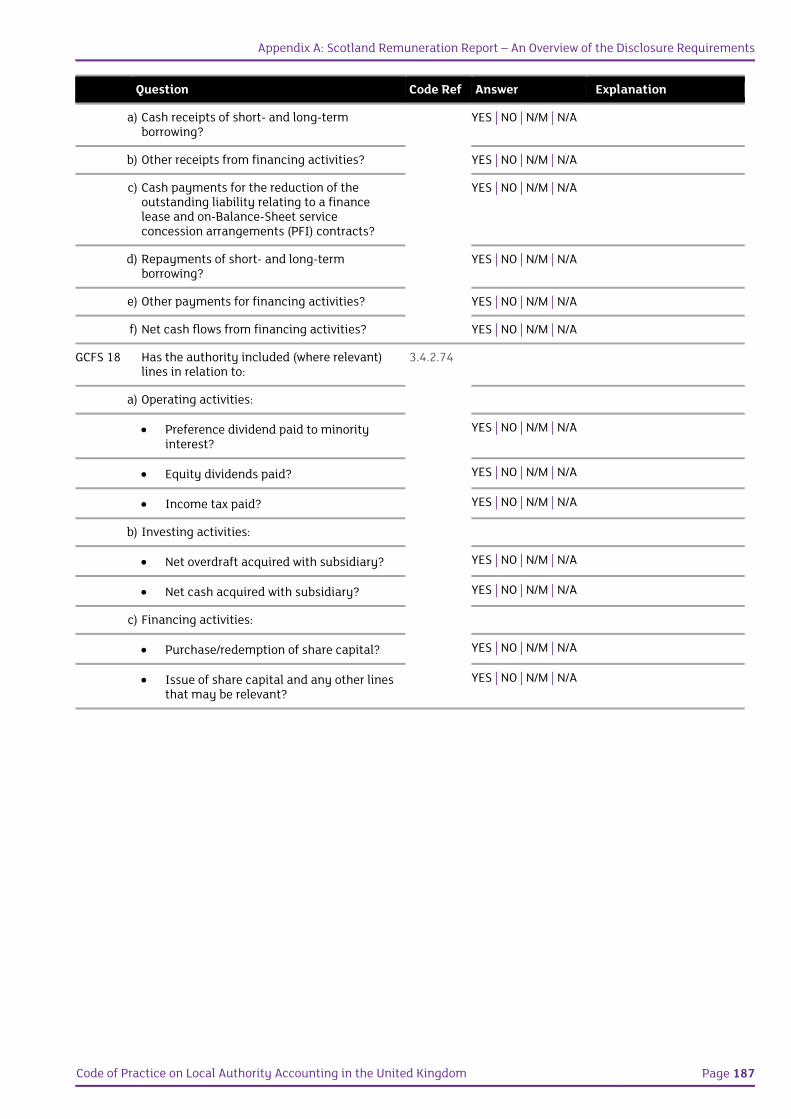

a) Cash receipts of short- and long-term borrowing? YES | NO | N/M | N/A

b) Other receipts from financing activities? YES | NO | N/M | N/A

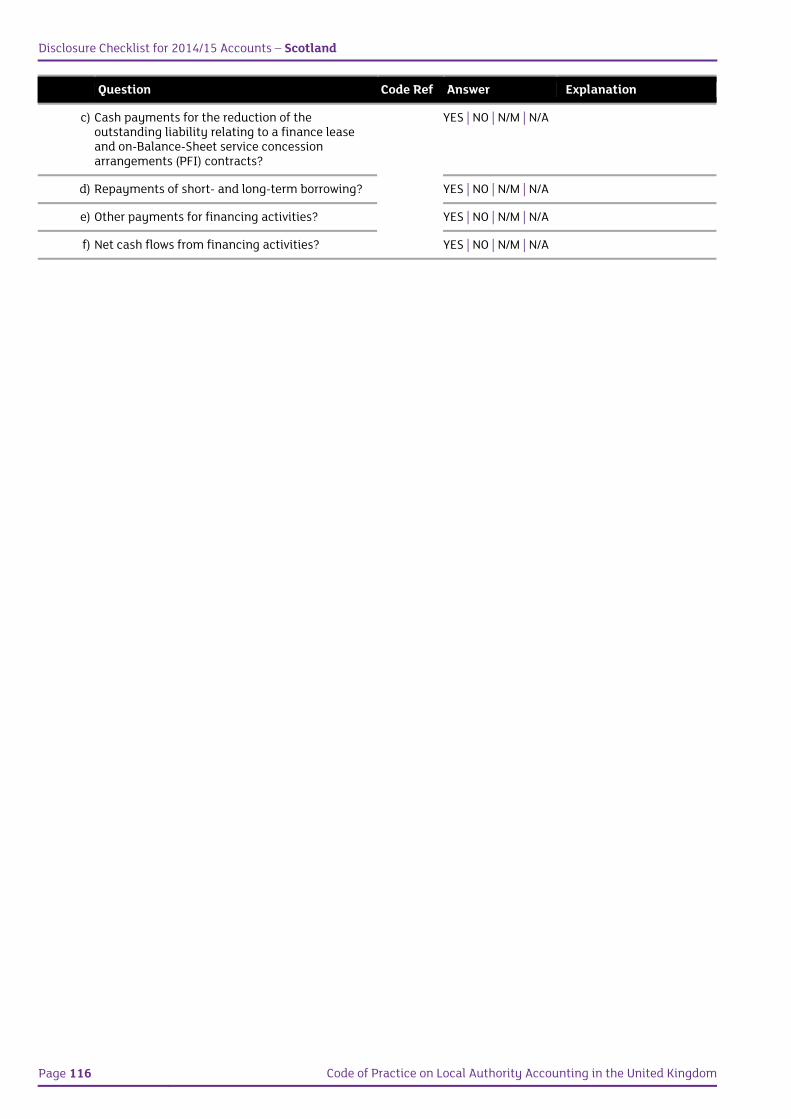

c) Cash payments for the reduction of the outstanding liability relating to finance leases and on-Balance-Sheet service concession arrangements (PFI) contracts?

YES | NO | N/M | N/A

d) Repayments of short- and long-term borrowing? YES | NO | N/M | N/A

e) Other payments for financing activities? YES | NO | N/M | N/A

f) Net cash flows from financing activities? YES | NO | N/M | N/A

Cash flow statement prepared using the indirect method

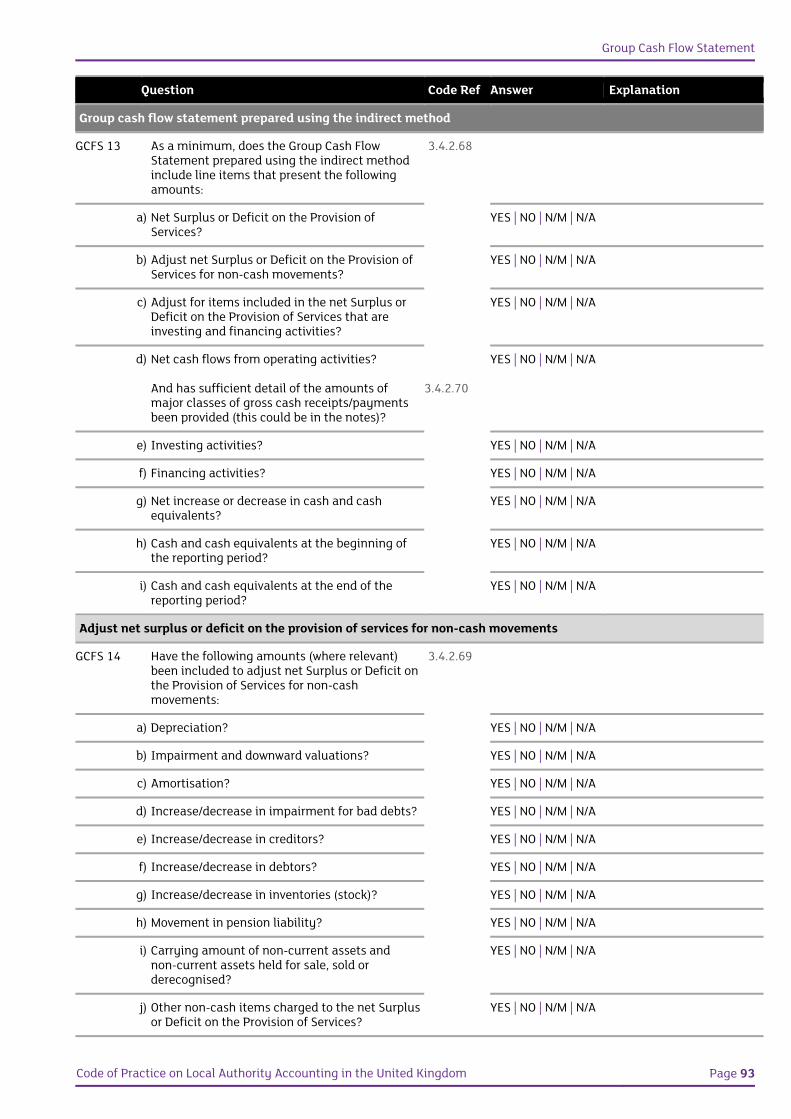

CFS 13 As a minimum, does the Cash Flow Statement prepared using the indirect method include line items that present the following amounts:

3.4.2.68

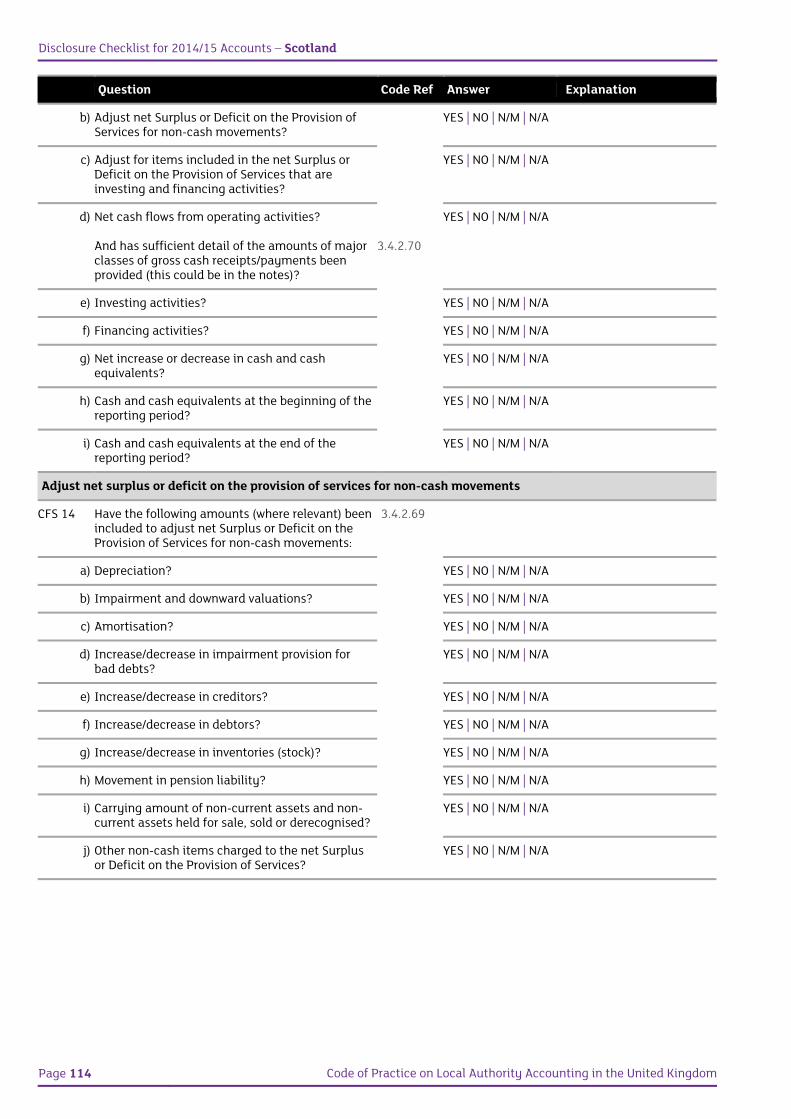

a) Net surplus or deficit on the provision of services? YES | NO | N/M | N/A

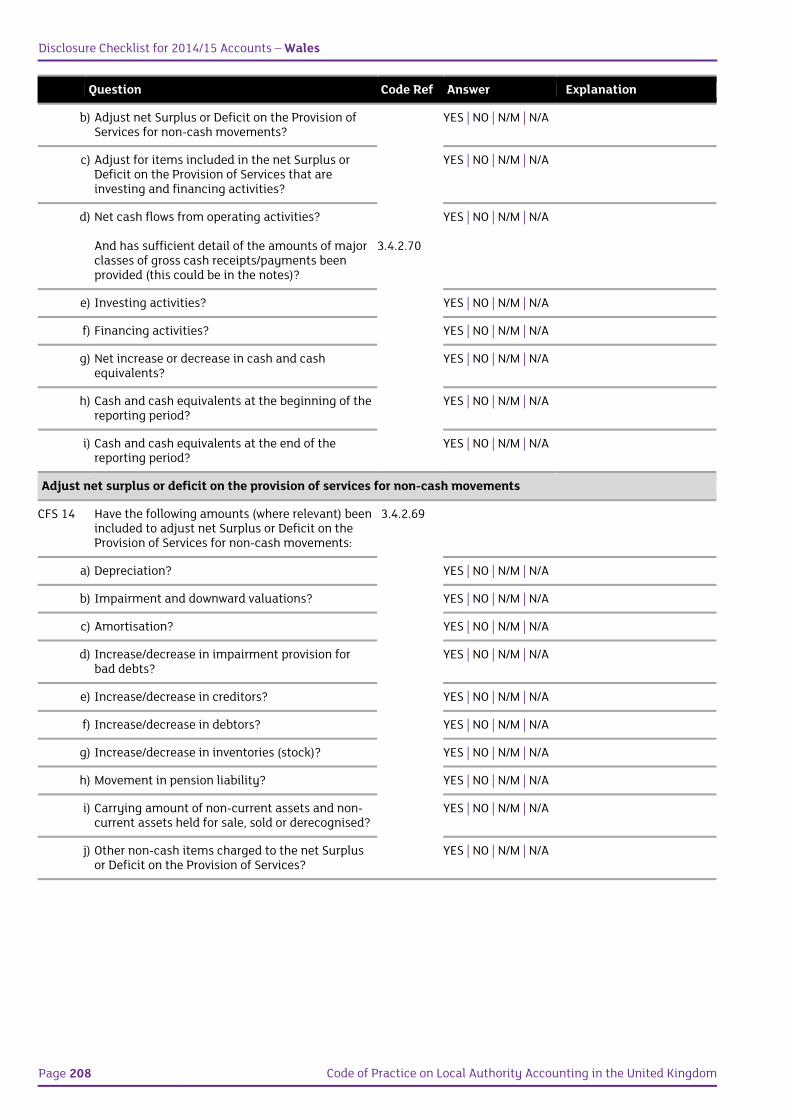

b) Adjust net surplus or deficit on the provision of services for non-cash movements?

YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 20 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

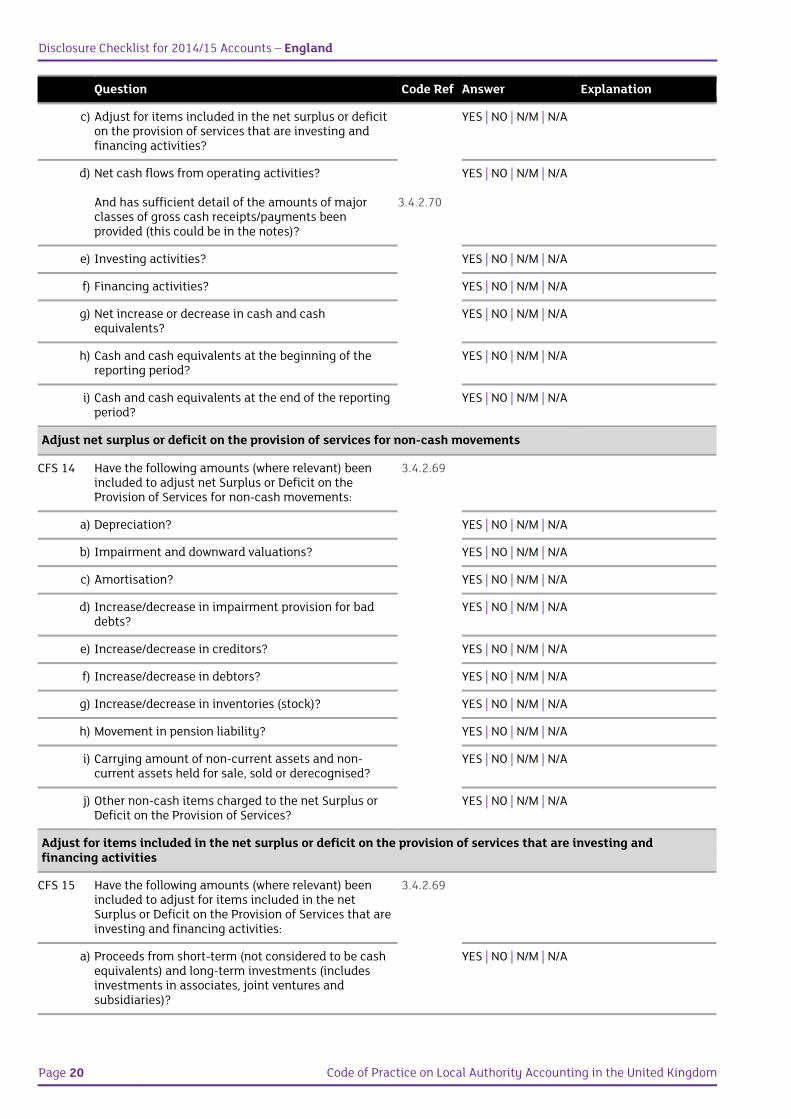

c) Adjust for items included in the net surplus or deficit on the provision of services that are investing and financing activities?

YES | NO | N/M | N/A

d) Net cash flows from operating activities? And has sufficient detail of the amounts of major classes of gross cash receipts/payments been provided (this could be in the notes)?

3.4.2.70

YES | NO | N/M | N/A

e) Investing activities? YES | NO | N/M | N/A

f) Financing activities? YES | NO | N/M | N/A

g) Net increase or decrease in cash and cash equivalents?

YES | NO | N/M | N/A

h) Cash and cash equivalents at the beginning of the reporting period?

YES | NO | N/M | N/A

i) Cash and cash equivalents at the end of the reporting period?

YES | NO | N/M | N/A

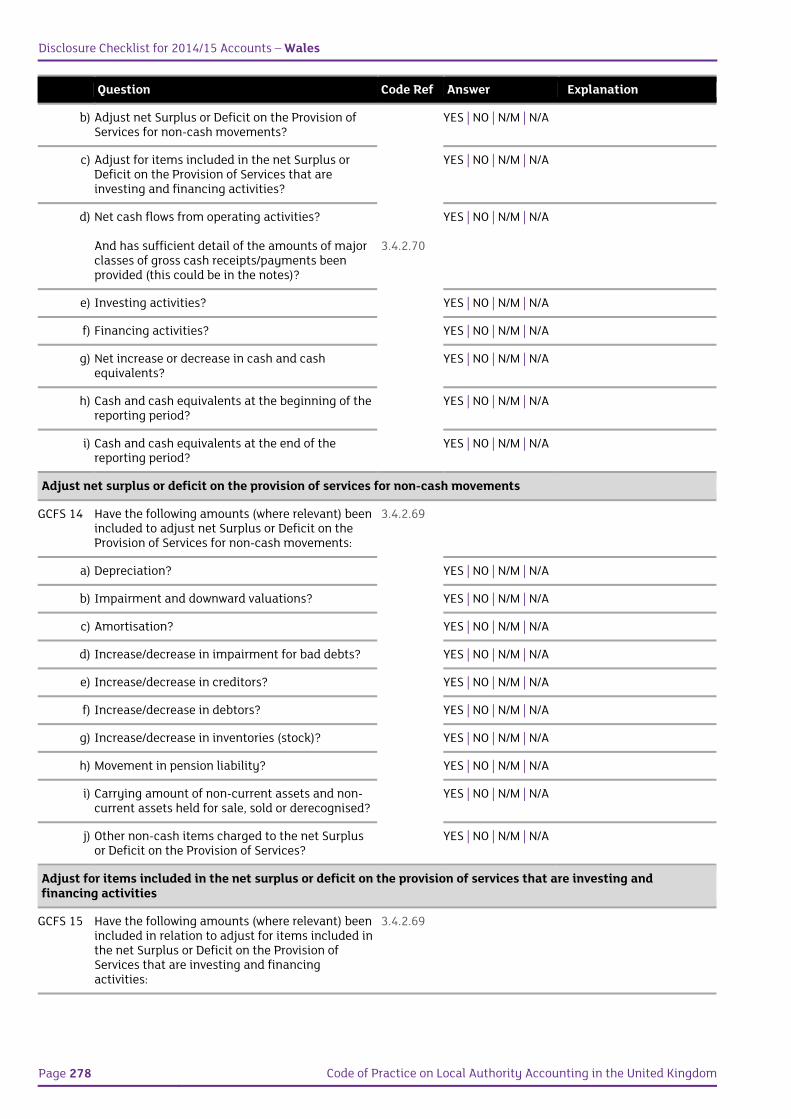

Adjust net surplus or deficit on the provision of services for non-cash movements

CFS 14 Have the following amounts (where relevant) been included to adjust net Surplus or Deficit on the Provision of Services for non-cash movements:

3.4.2.69

a) Depreciation? YES | NO | N/M | N/A

b) Impairment and downward valuations? YES | NO | N/M | N/A

c) Amortisation? YES | NO | N/M | N/A

d) Increase/decrease in impairment provision for bad debts?

YES | NO | N/M | N/A

e) Increase/decrease in creditors? YES | NO | N/M | N/A

f) Increase/decrease in debtors? YES | NO | N/M | N/A

g) Increase/decrease in inventories (stock)? YES | NO | N/M | N/A

h) Movement in pension liability? YES | NO | N/M | N/A

i) Carrying amount of non-current assets and non-current assets held for sale, sold or derecognised?

YES | NO | N/M | N/A

j) Other non-cash items charged to the net Surplus or Deficit on the Provision of Services?

YES | NO | N/M | N/A

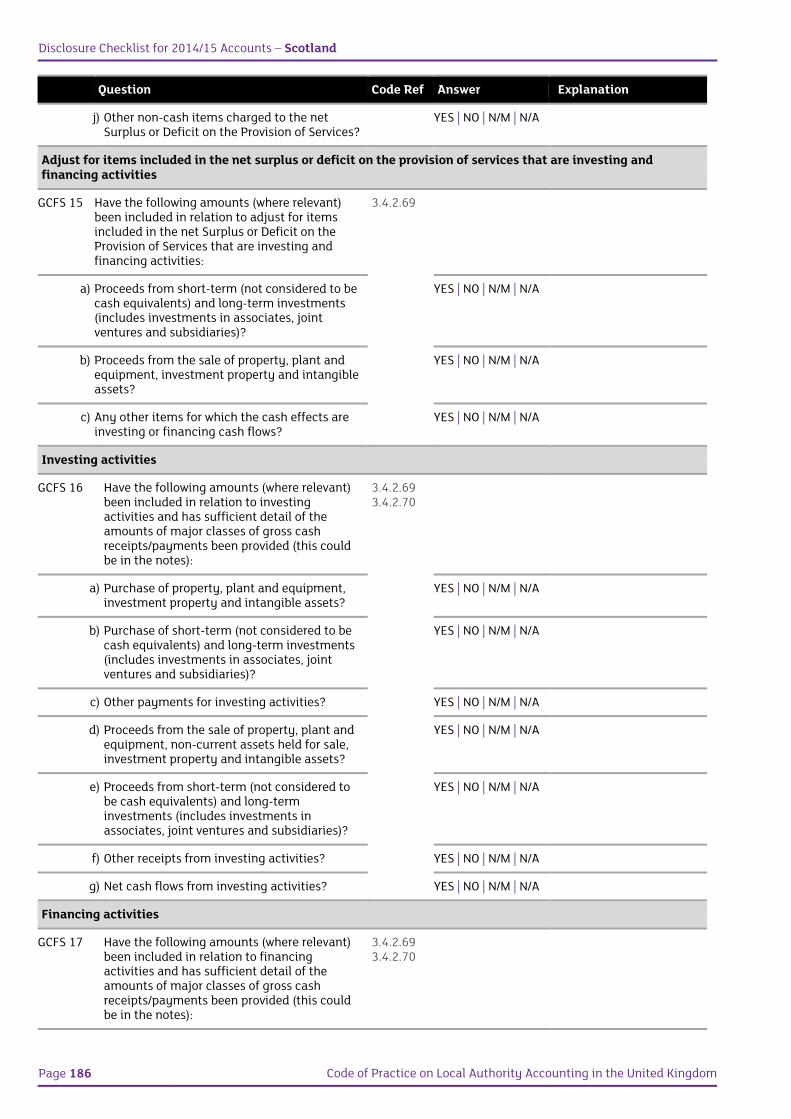

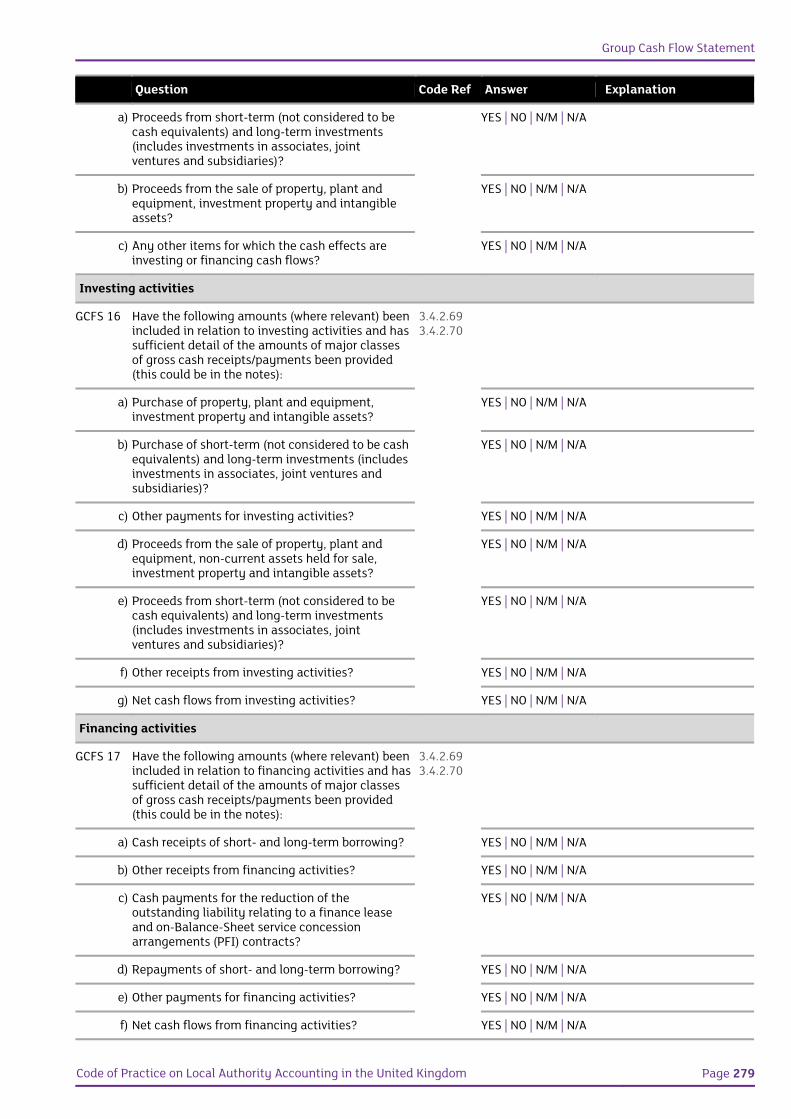

Adjust for items included in the net surplus or deficit on the provision of services that are investing and financing activities

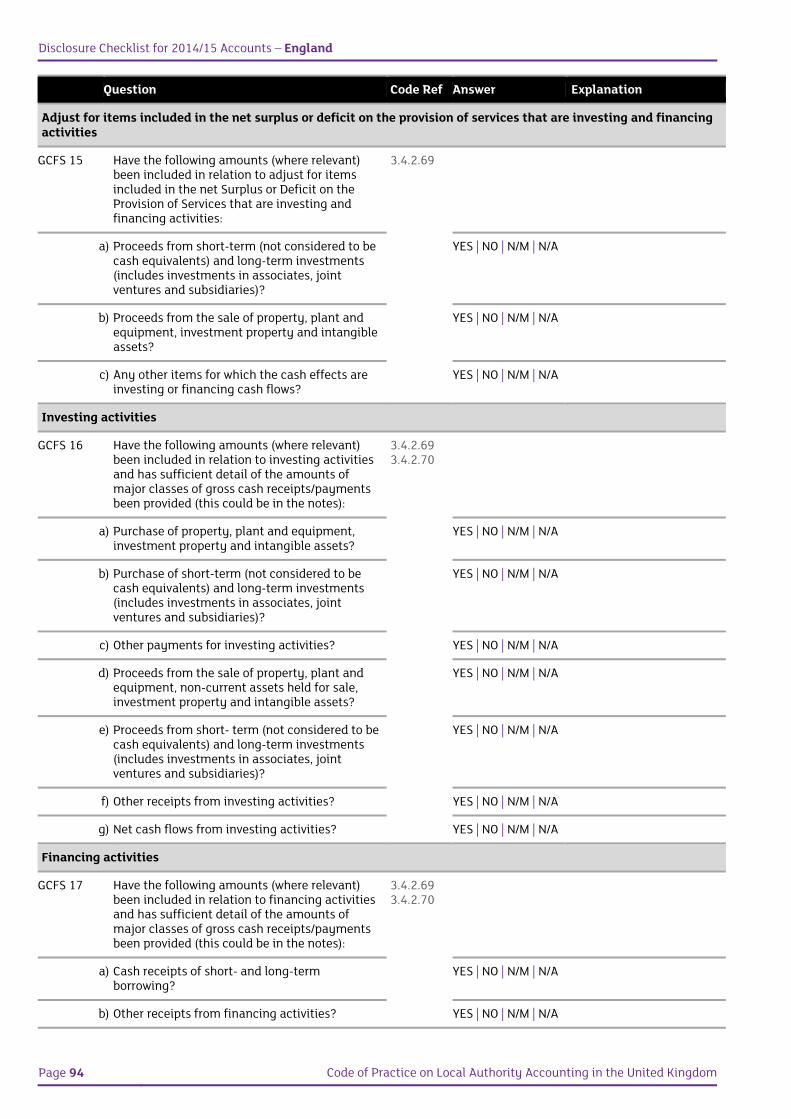

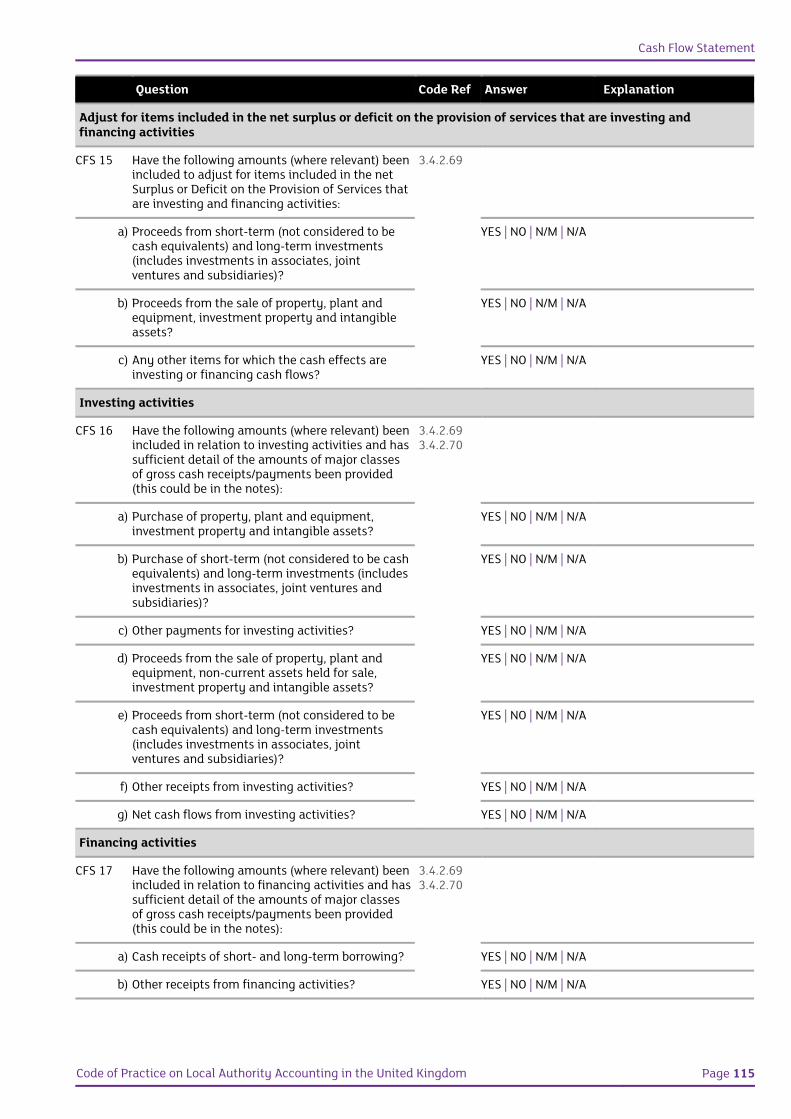

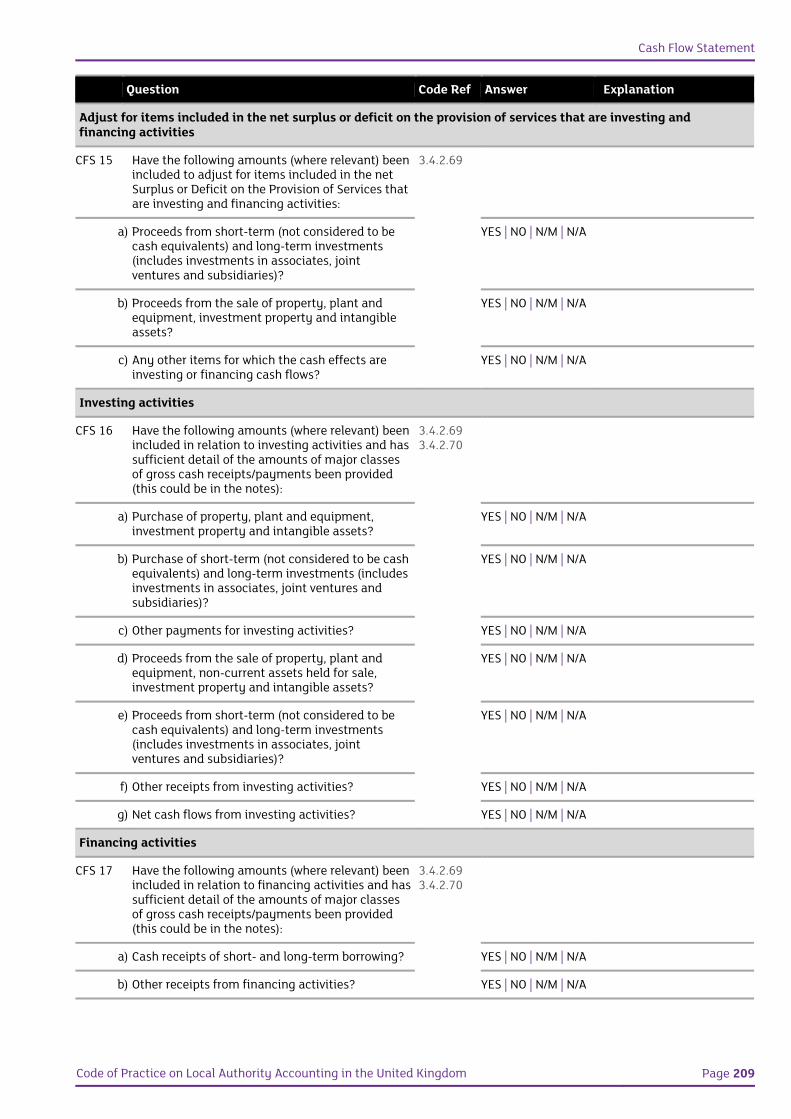

CFS 15 Have the following amounts (where relevant) been included to adjust for items included in the net Surplus or Deficit on the Provision of Services that are investing and financing activities:

3.4.2.69

a) Proceeds from short-term (not considered to be cash equivalents) and long-term investments (includes investments in associates, joint ventures and subsidiaries)?

YES | NO | N/M | N/A

Cash Flow Statement

Code of Practice on Local Authority Accounting in the United Kingdom Page 21

Question Code Ref Answer Explanation

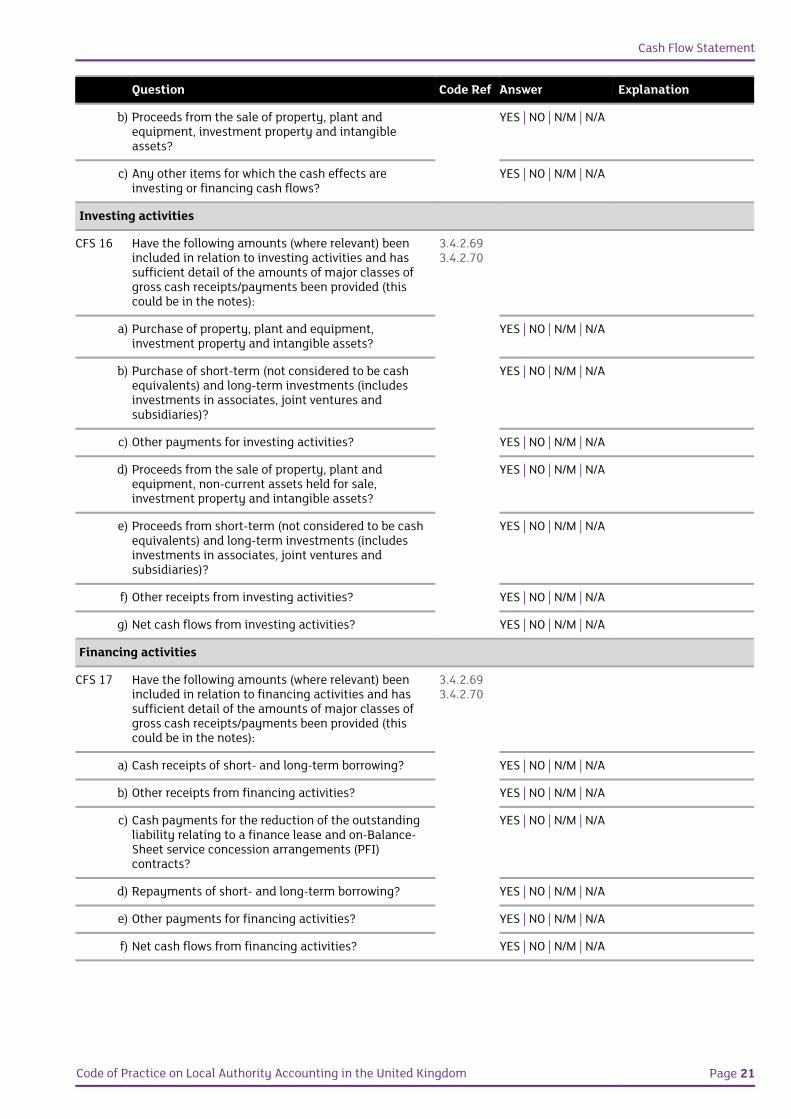

b) Proceeds from the sale of property, plant and equipment, investment property and intangible assets?

YES | NO | N/M | N/A

c) Any other items for which the cash effects are investing or financing cash flows?

YES | NO | N/M | N/A

Investing activities

CFS 16 Have the following amounts (where relevant) been included in relation to investing activities and has sufficient detail of the amounts of major classes of gross cash receipts/payments been provided (this could be in the notes):

3.4.2.693.4.2.70

a) Purchase of property, plant and equipment, investment property and intangible assets?

YES | NO | N/M | N/A

b) Purchase of short-term (not considered to be cash equivalents) and long-term investments (includes investments in associates, joint ventures and subsidiaries)?

YES | NO | N/M | N/A

c) Other payments for investing activities? YES | NO | N/M | N/A

d) Proceeds from the sale of property, plant and equipment, non-current assets held for sale, investment property and intangible assets?

YES | NO | N/M | N/A

e) Proceeds from short-term (not considered to be cash equivalents) and long-term investments (includes investments in associates, joint ventures and subsidiaries)?

YES | NO | N/M | N/A

f) Other receipts from investing activities? YES | NO | N/M | N/A

g) Net cash flows from investing activities? YES | NO | N/M | N/A

Financing activities

CFS 17 Have the following amounts (where relevant) been included in relation to financing activities and has sufficient detail of the amounts of major classes of gross cash receipts/payments been provided (this could be in the notes):

3.4.2.693.4.2.70

a) Cash receipts of short- and long-term borrowing? YES | NO | N/M | N/A

b) Other receipts from financing activities? YES | NO | N/M | N/A

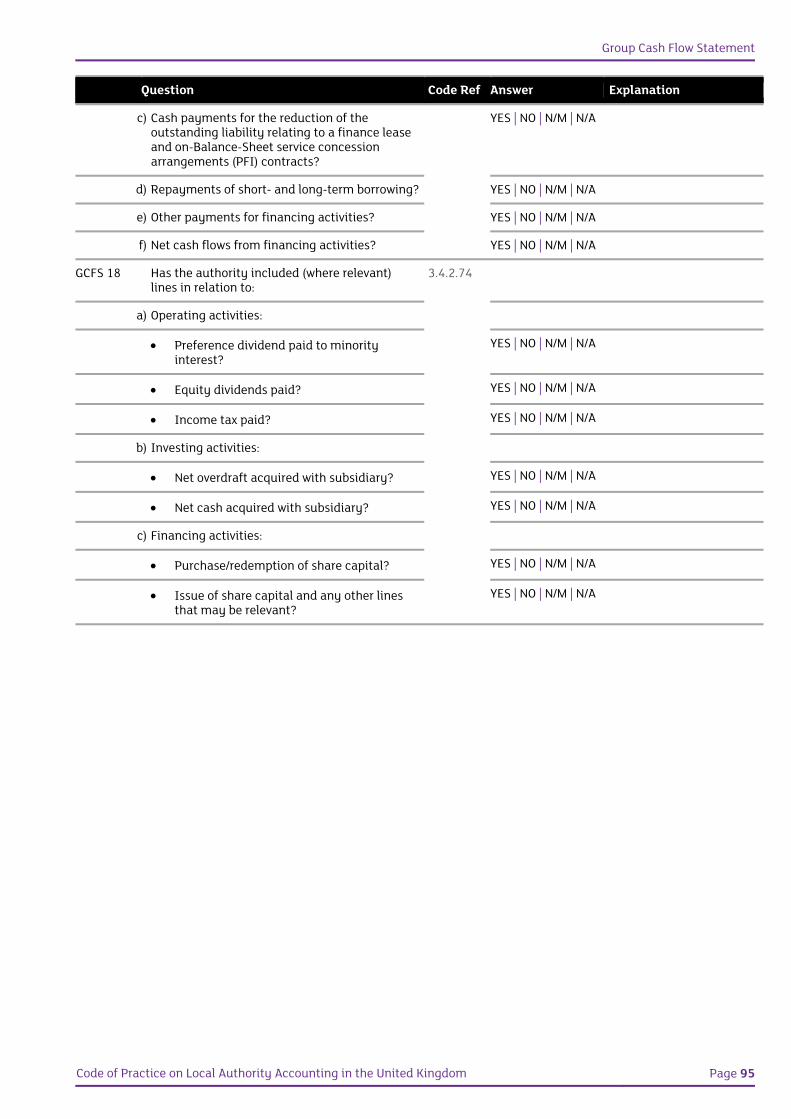

c) Cash payments for the reduction of the outstanding liability relating to a finance lease and on-Balance-Sheet service concession arrangements (PFI) contracts?

YES | NO | N/M | N/A

d) Repayments of short- and long-term borrowing? YES | NO | N/M | N/A

e) Other payments for financing activities? YES | NO | N/M | N/A

f) Net cash flows from financing activities? YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 22 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

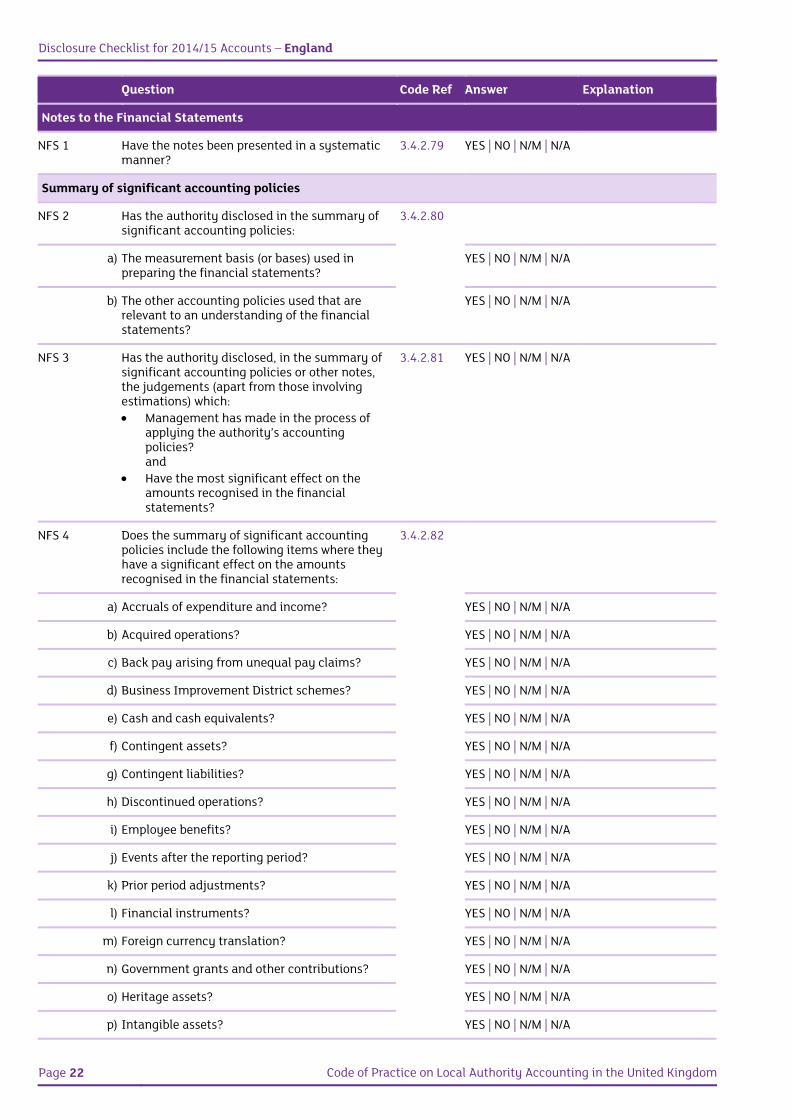

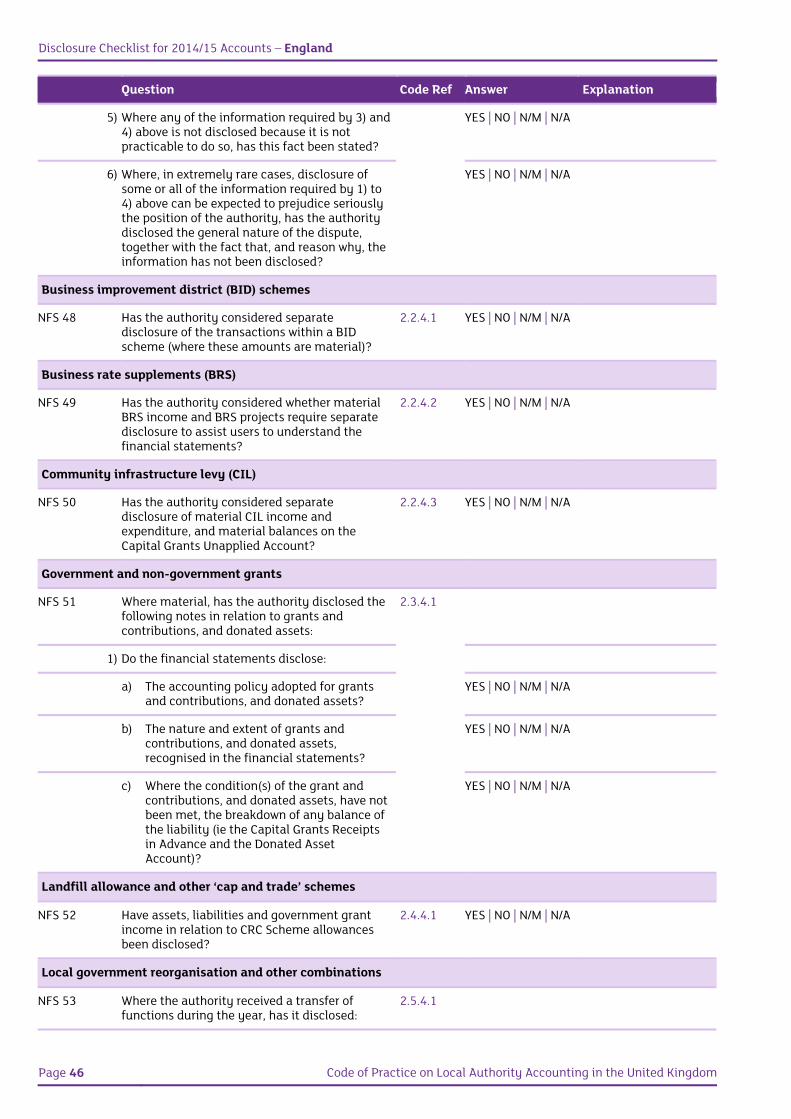

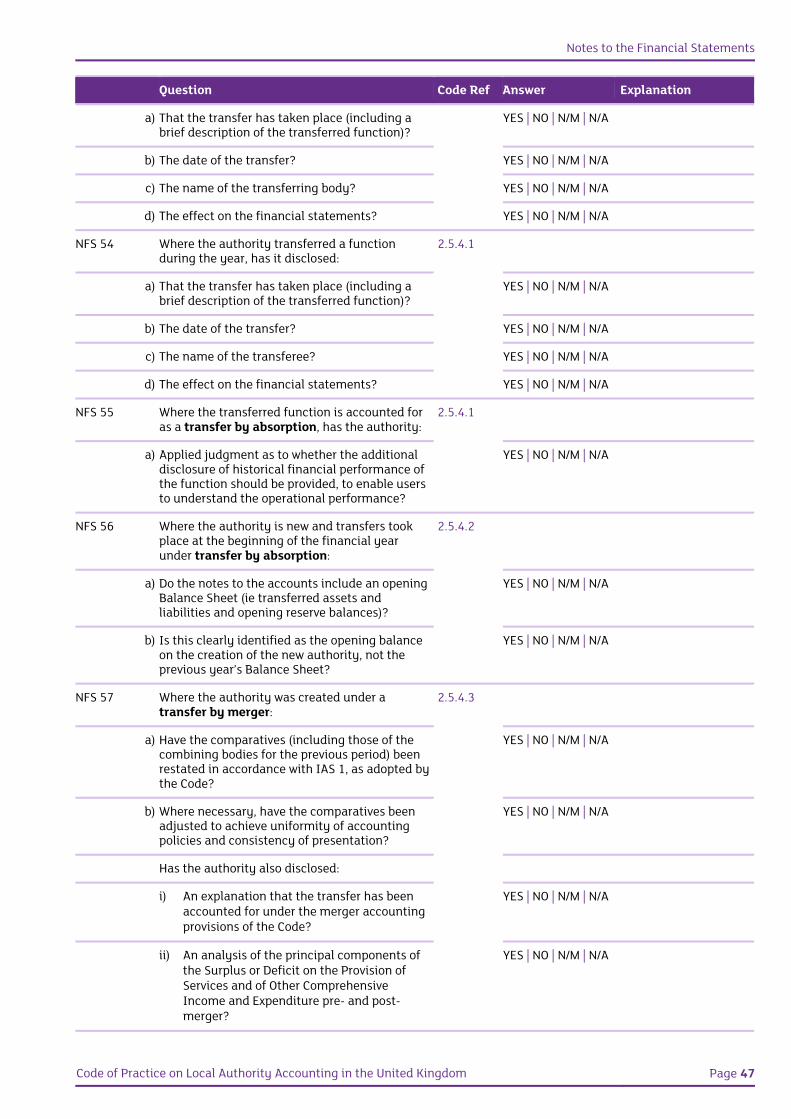

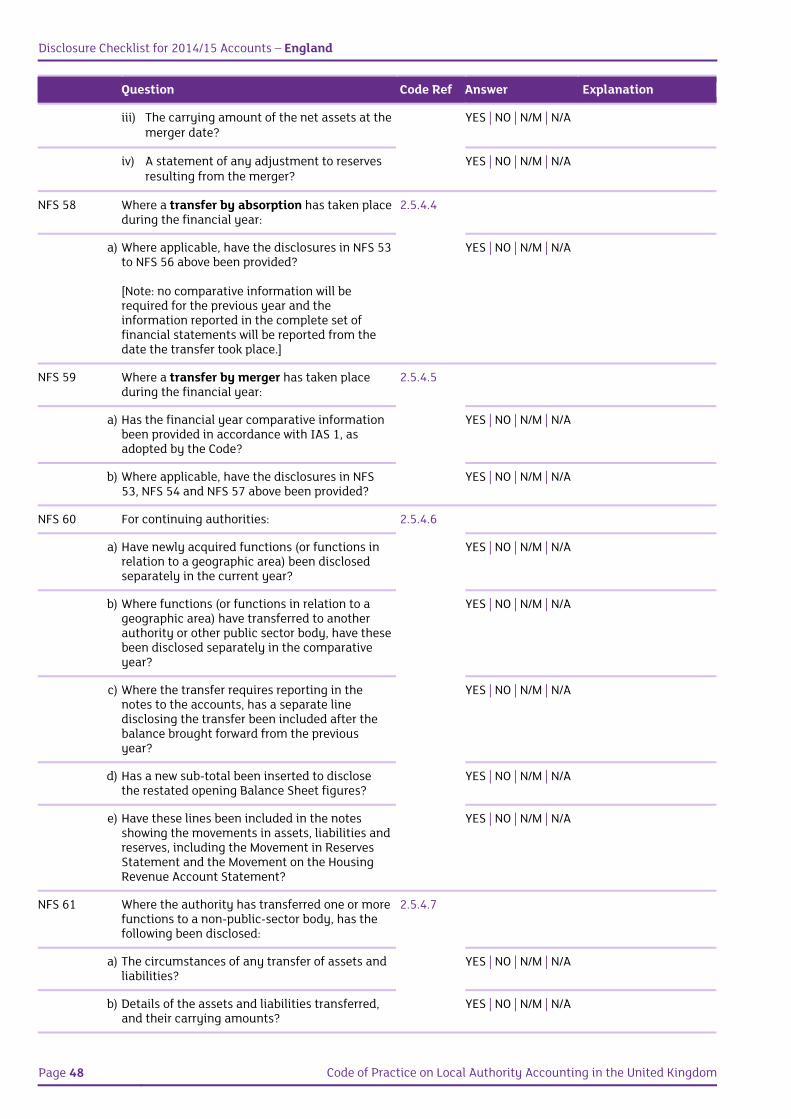

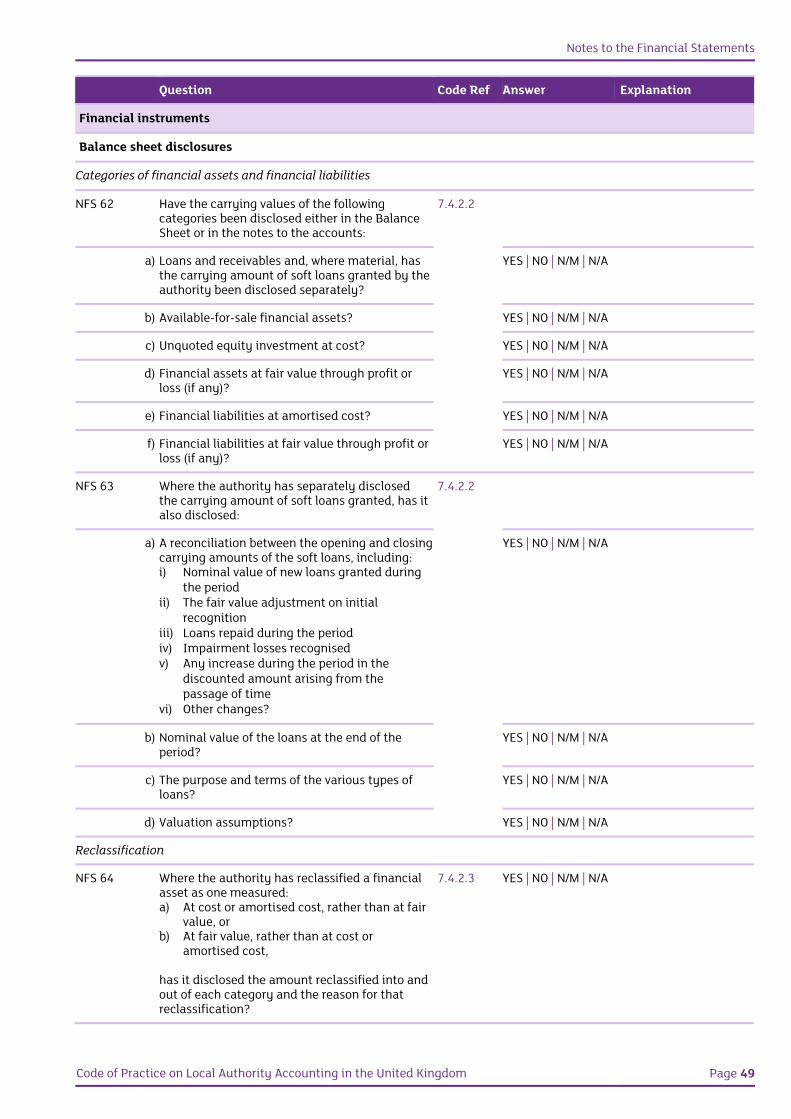

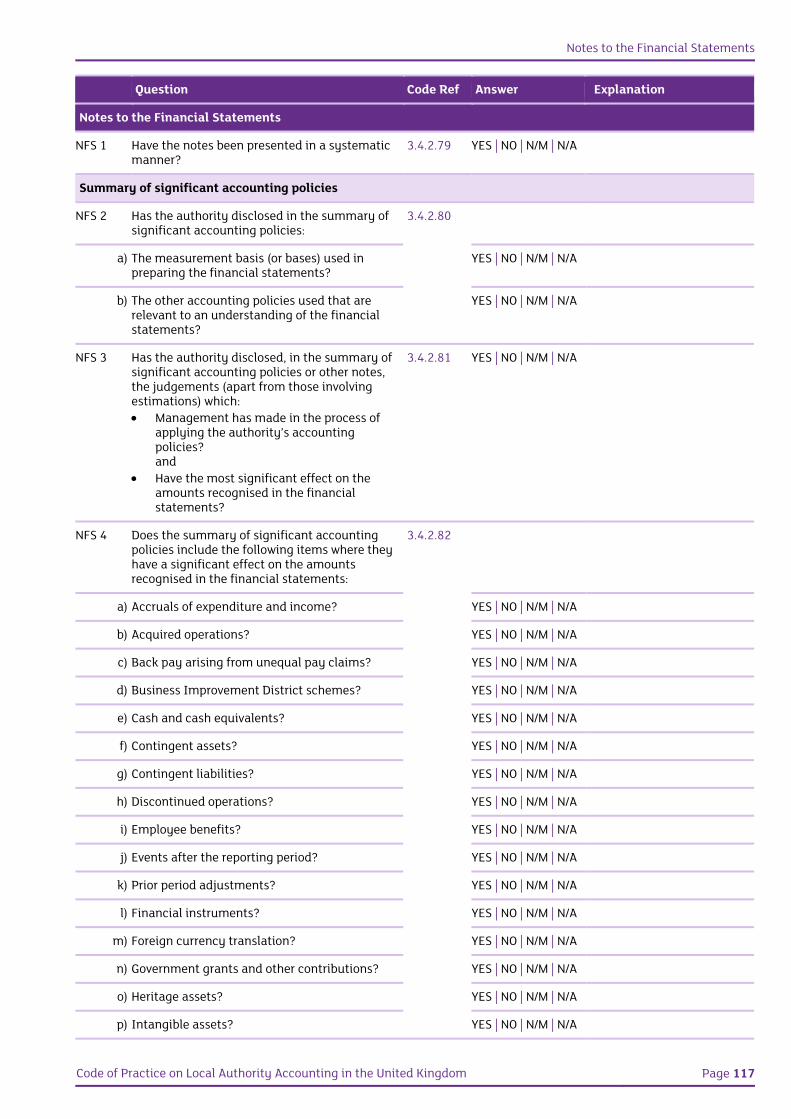

Notes to the Financial Statements

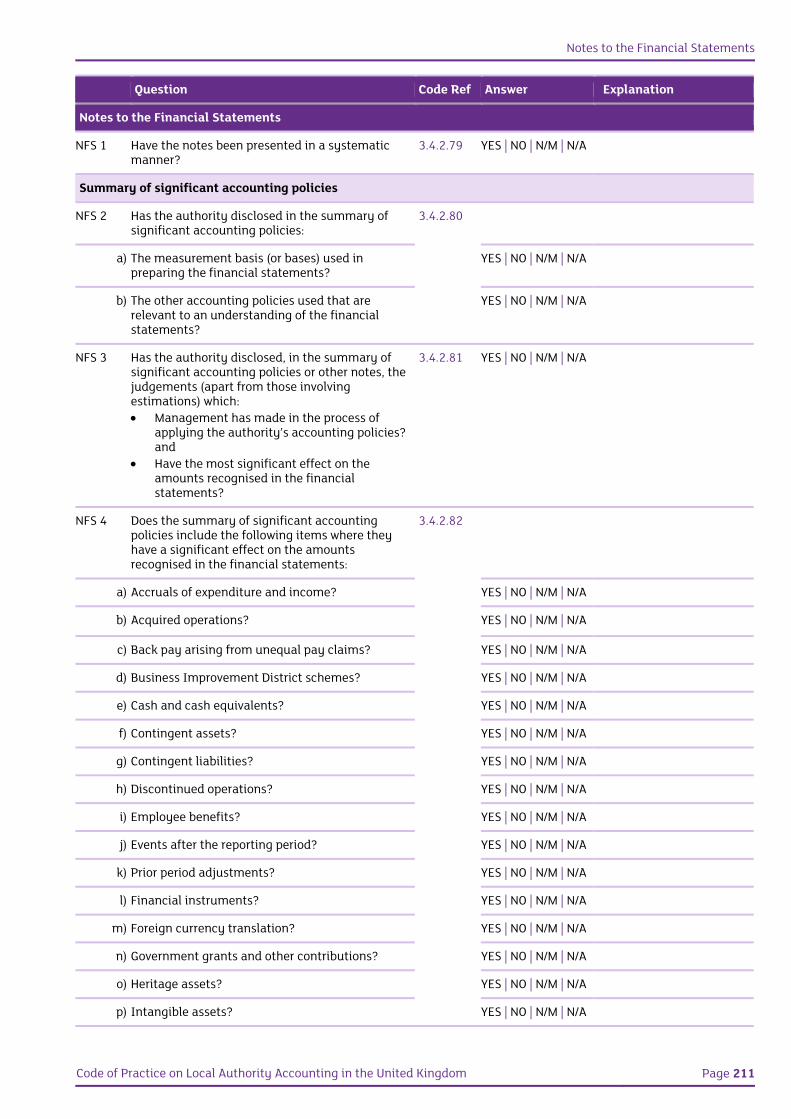

NFS 1 Have the notes been presented in a systematic manner?

3.4.2.79 YES | NO | N/M | N/A

Summary of significant accounting policies

NFS 2 Has the authority disclosed in the summary of significant accounting policies:

3.4.2.80

a) The measurement basis (or bases) used in preparing the financial statements?

YES | NO | N/M | N/A

b) The other accounting policies used that are relevant to an understanding of the financial statements?

YES | NO | N/M | N/A

NFS 3 Has the authority disclosed, in the summary of significant accounting policies or other notes, the judgements (apart from those involving estimations) which: Management has made in the process of

applying the authority’s accounting policies? and

Have the most significant effect on the amounts recognised in the financial statements?

3.4.2.81 YES | NO | N/M | N/A

NFS 4 Does the summary of significant accounting policies include the following items where they have a significant effect on the amounts recognised in the financial statements:

3.4.2.82

a) Accruals of expenditure and income? YES | NO | N/M | N/A

b) Acquired operations? YES | NO | N/M | N/A

c) Back pay arising from unequal pay claims? YES | NO | N/M | N/A

d) Business Improvement District schemes? YES | NO | N/M | N/A

e) Cash and cash equivalents? YES | NO | N/M | N/A

f) Contingent assets? YES | NO | N/M | N/A

g) Contingent liabilities? YES | NO | N/M | N/A

h) Discontinued operations? YES | NO | N/M | N/A

i) Employee benefits? YES | NO | N/M | N/A

j) Events after the reporting period? YES | NO | N/M | N/A

k) Prior period adjustments? YES | NO | N/M | N/A

l) Financial instruments? YES | NO | N/M | N/A

m) Foreign currency translation? YES | NO | N/M | N/A

n) Government grants and other contributions? YES | NO | N/M | N/A

o) Heritage assets? YES | NO | N/M | N/A

p) Intangible assets? YES | NO | N/M | N/A

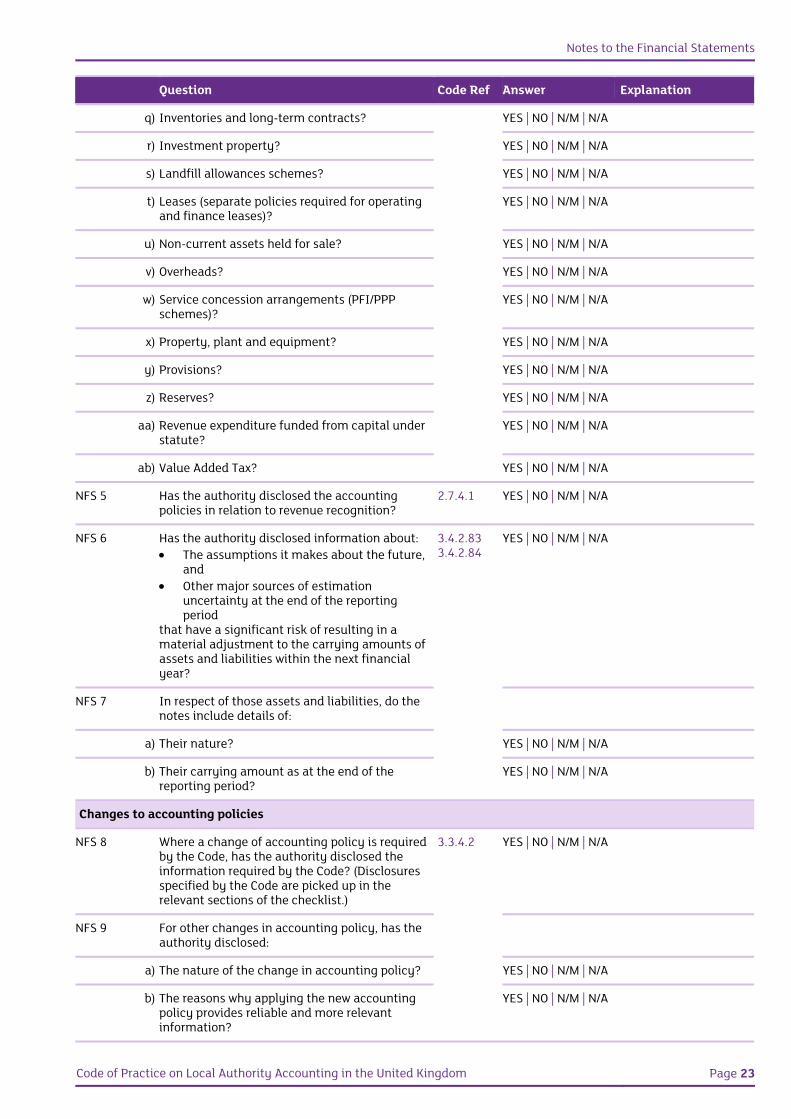

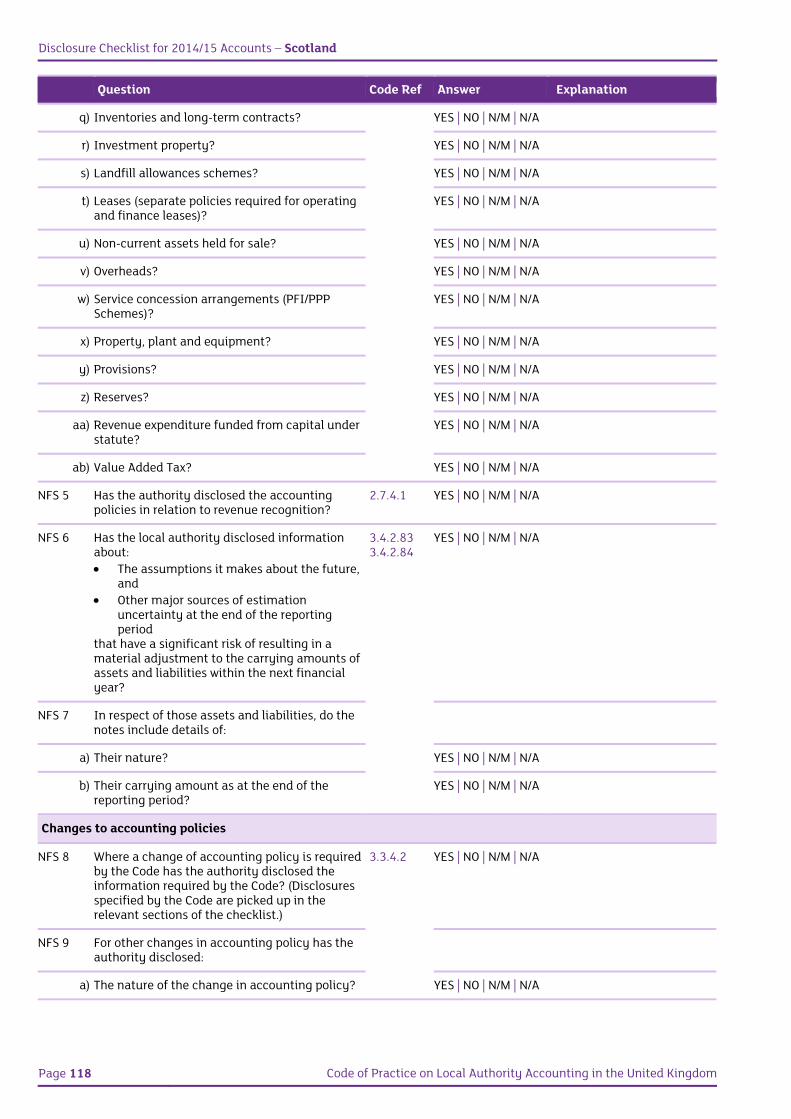

Notes to the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 23

Question Code Ref Answer Explanation

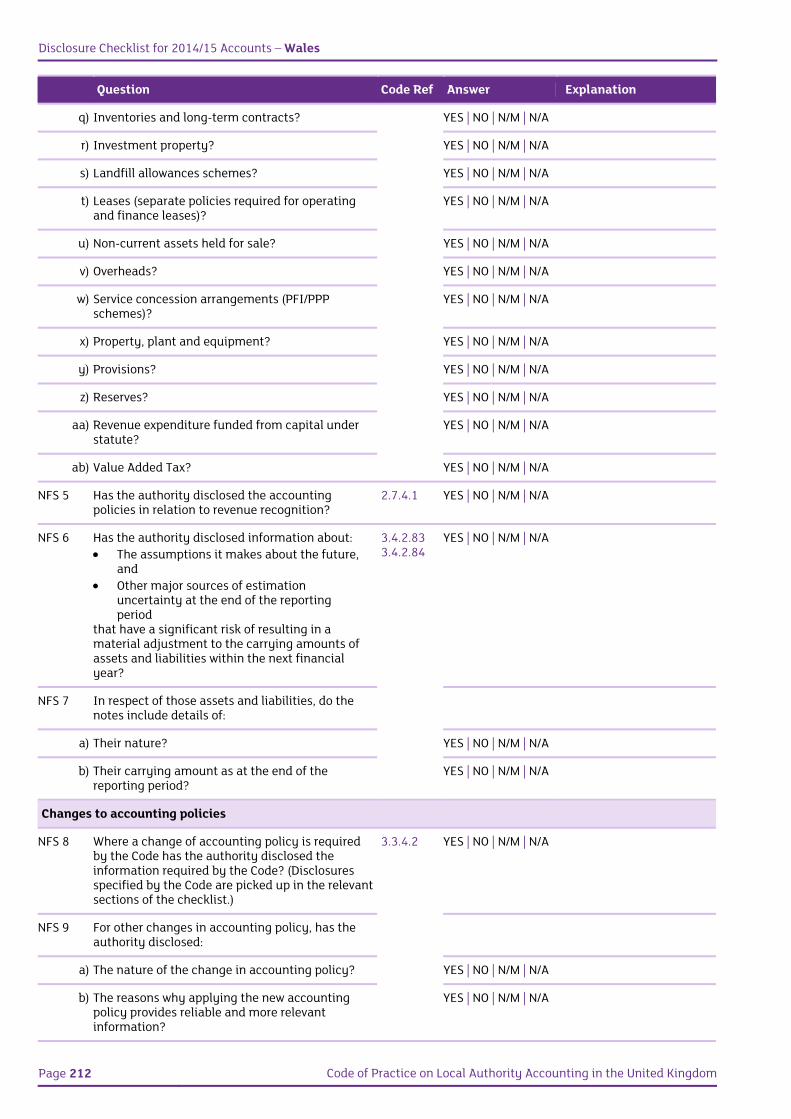

q) Inventories and long-term contracts? YES | NO | N/M | N/A

r) Investment property? YES | NO | N/M | N/A

s) Landfill allowances schemes? YES | NO | N/M | N/A

t) Leases (separate policies required for operating and finance leases)?

YES | NO | N/M | N/A

u) Non-current assets held for sale? YES | NO | N/M | N/A

v) Overheads? YES | NO | N/M | N/A

w) Service concession arrangements (PFI/PPP schemes)?

YES | NO | N/M | N/A

x) Property, plant and equipment? YES | NO | N/M | N/A

y) Provisions? YES | NO | N/M | N/A

z) Reserves? YES | NO | N/M | N/A

aa) Revenue expenditure funded from capital under statute?

YES | NO | N/M | N/A

ab) Value Added Tax? YES | NO | N/M | N/A

NFS 5 Has the authority disclosed the accounting policies in relation to revenue recognition?

2.7.4.1 YES | NO | N/M | N/A

NFS 6 Has the authority disclosed information about: The assumptions it makes about the future,

and Other major sources of estimation

uncertainty at the end of the reporting period

that have a significant risk of resulting in a material adjustment to the carrying amounts of assets and liabilities within the next financial year?

3.4.2.833.4.2.84

YES | NO | N/M | N/A

NFS 7 In respect of those assets and liabilities, do the notes include details of:

a) Their nature? YES | NO | N/M | N/A

b) Their carrying amount as at the end of the reporting period?

YES | NO | N/M | N/A

Changes to accounting policies

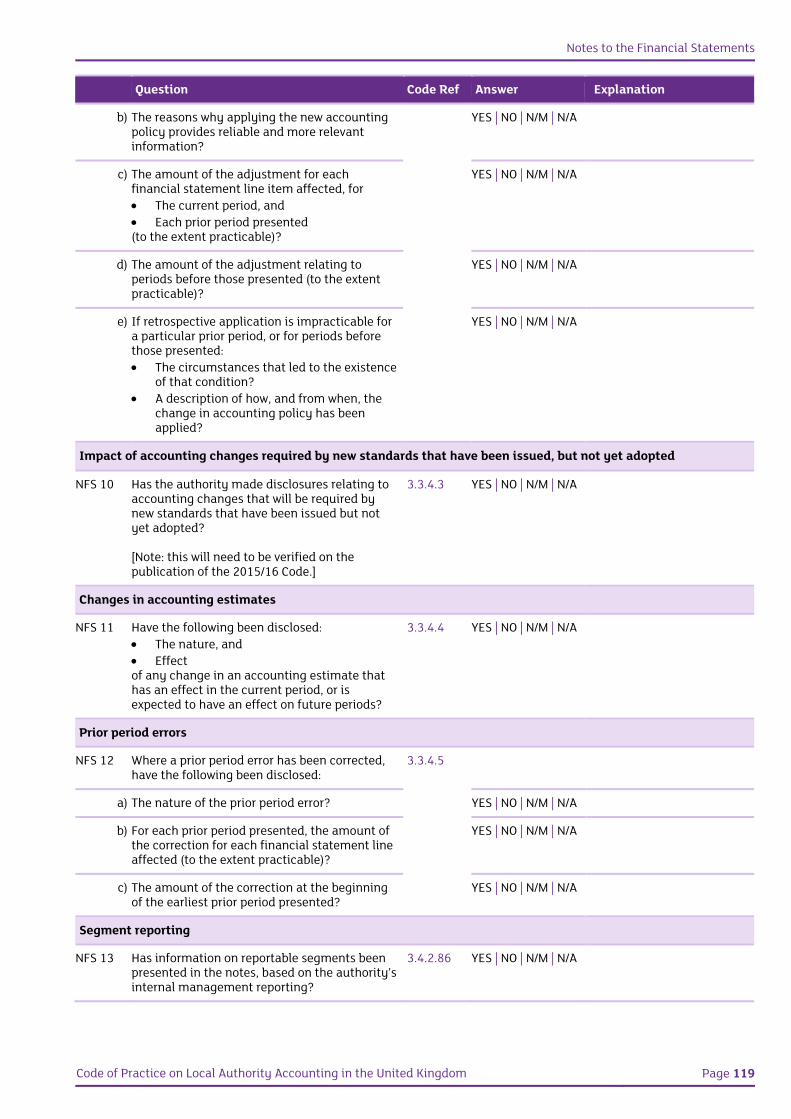

NFS 8 Where a change of accounting policy is required by the Code, has the authority disclosed the information required by the Code? (Disclosures specified by the Code are picked up in the relevant sections of the checklist.)

3.3.4.2 YES | NO | N/M | N/A

NFS 9 For other changes in accounting policy, has the authority disclosed:

a) The nature of the change in accounting policy? YES | NO | N/M | N/A

b) The reasons why applying the new accounting policy provides reliable and more relevant information?

YES | NO | N/M | N/A

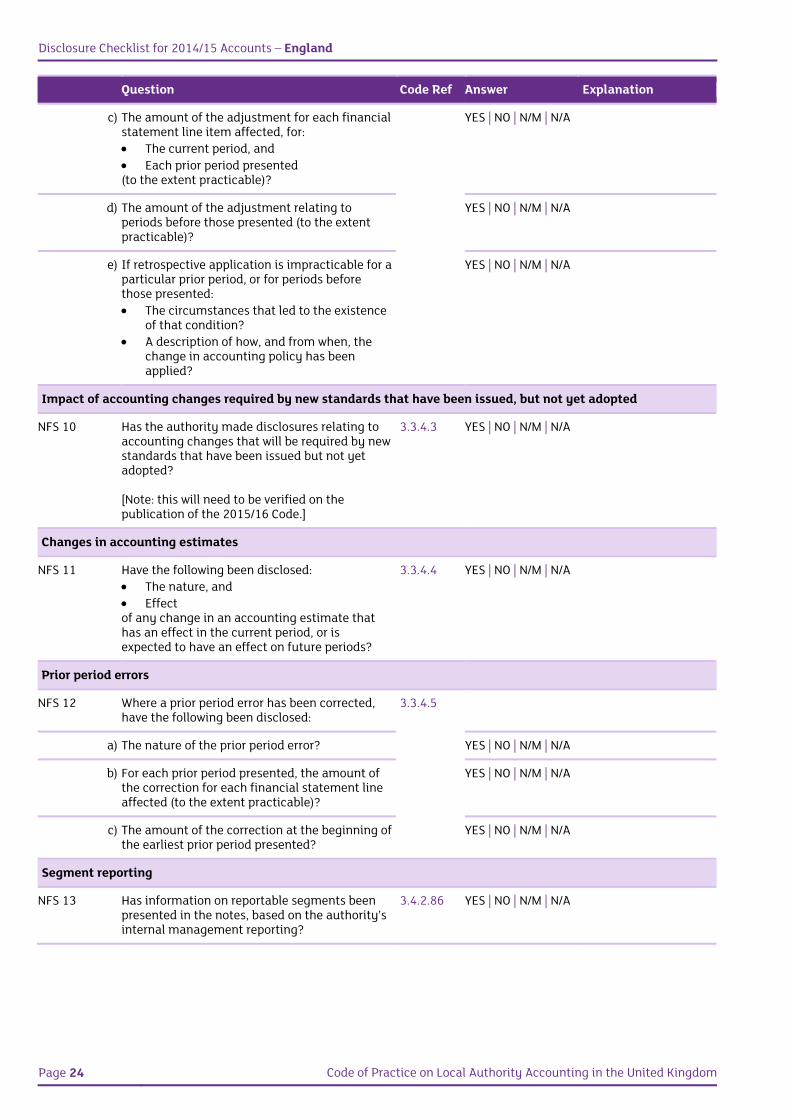

Disclosure Checklist for 2014/15 Accounts – England

Page 24 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

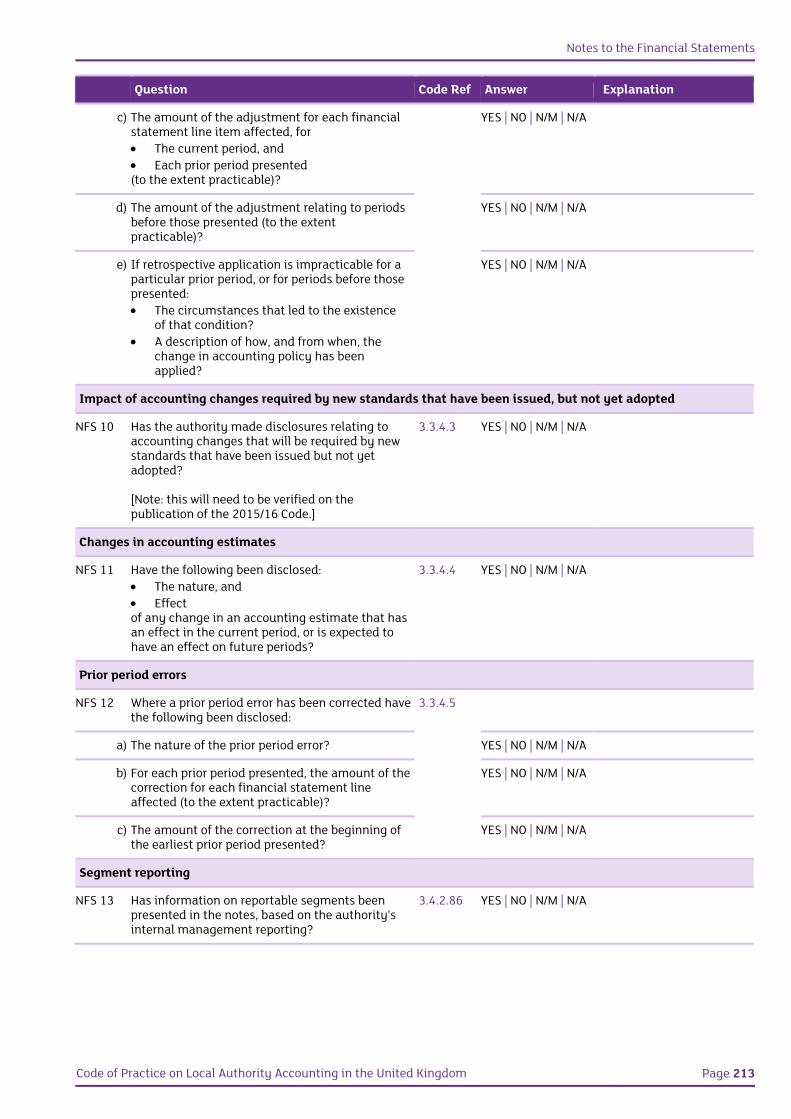

c) The amount of the adjustment for each financial statement line item affected, for: The current period, and Each prior period presented (to the extent practicable)?

YES | NO | N/M | N/A

d) The amount of the adjustment relating to periods before those presented (to the extent practicable)?

YES | NO | N/M | N/A

e) If retrospective application is impracticable for a particular prior period, or for periods before those presented: The circumstances that led to the existence

of that condition? A description of how, and from when, the

change in accounting policy has been applied?

YES | NO | N/M | N/A

Impact of accounting changes required by new standards that have been issued, but not yet adopted

NFS 10 Has the authority made disclosures relating to accounting changes that will be required by new standards that have been issued but not yet adopted? [Note: this will need to be verified on the publication of the 2015/16 Code.]

3.3.4.3 YES | NO | N/M | N/A

Changes in accounting estimates

NFS 11 Have the following been disclosed: The nature, and Effect of any change in an accounting estimate that has an effect in the current period, or is expected to have an effect on future periods?

3.3.4.4 YES | NO | N/M | N/A

Prior period errors

NFS 12 Where a prior period error has been corrected, have the following been disclosed:

3.3.4.5

a) The nature of the prior period error? YES | NO | N/M | N/A

b) For each prior period presented, the amount of the correction for each financial statement line affected (to the extent practicable)?

YES | NO | N/M | N/A

c) The amount of the correction at the beginning of the earliest prior period presented?

YES | NO | N/M | N/A

Segment reporting

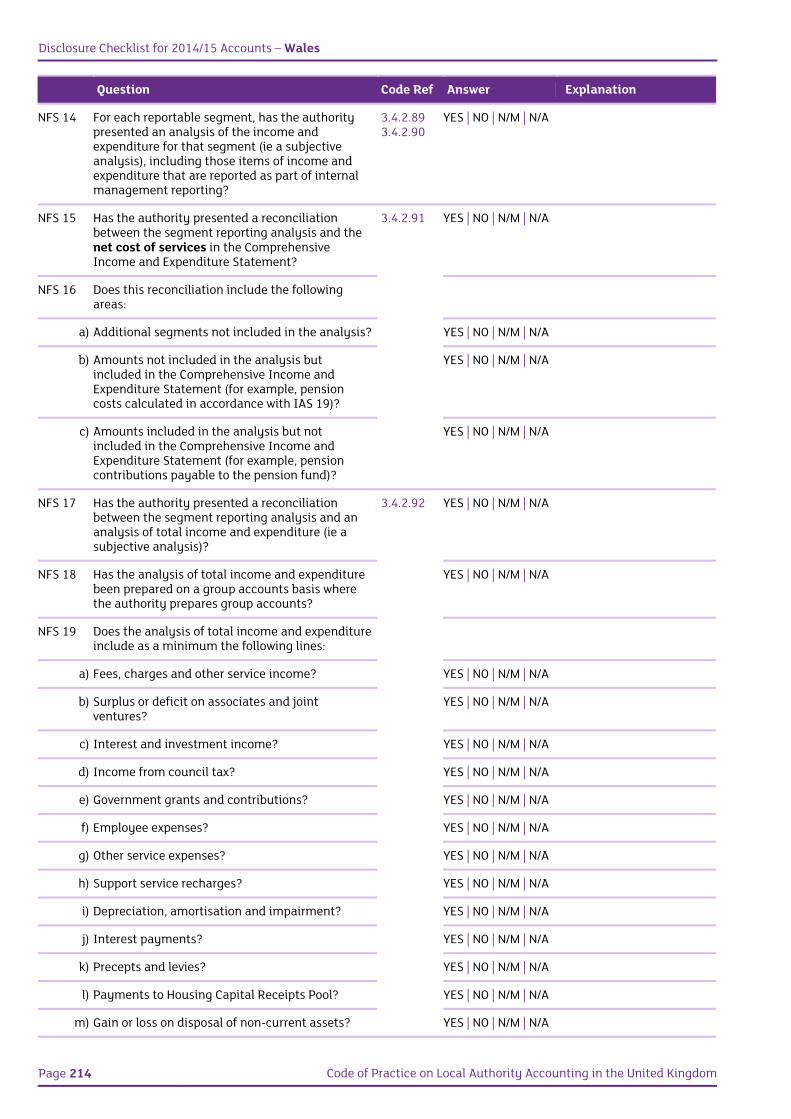

NFS 13 Has information on reportable segments been presented in the notes, based on the authority’s internal management reporting?

3.4.2.86 YES | NO | N/M | N/A

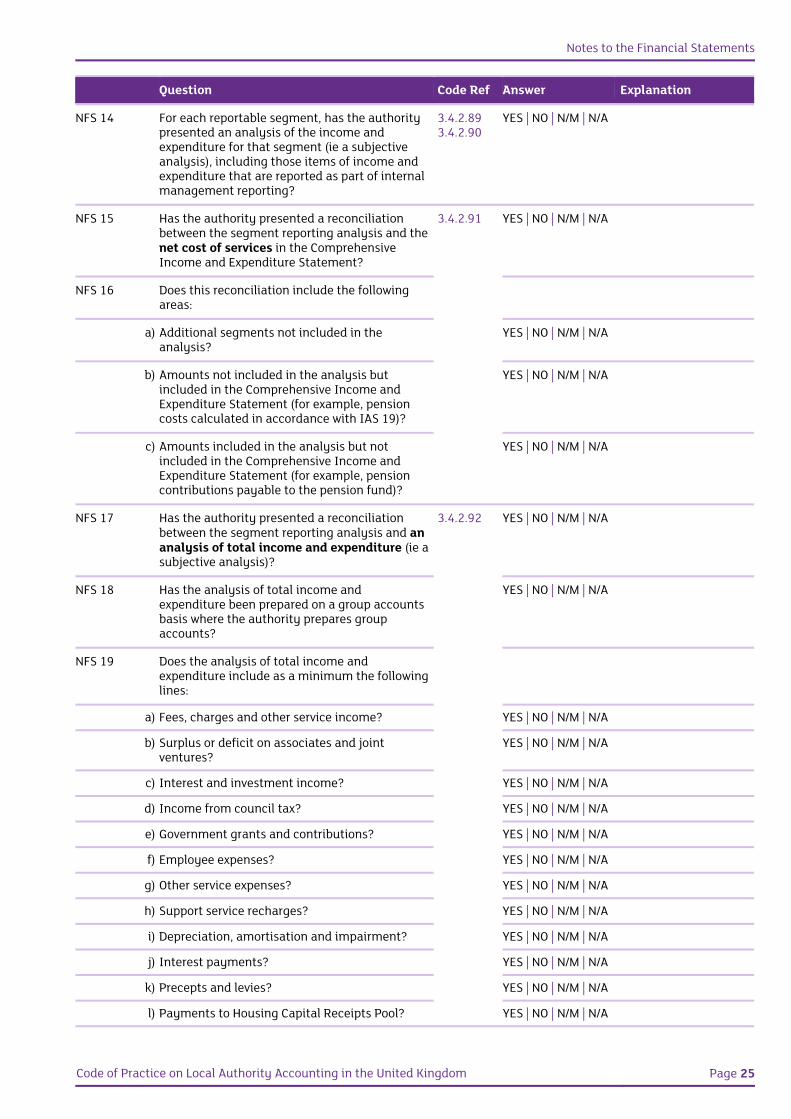

Notes to the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 25

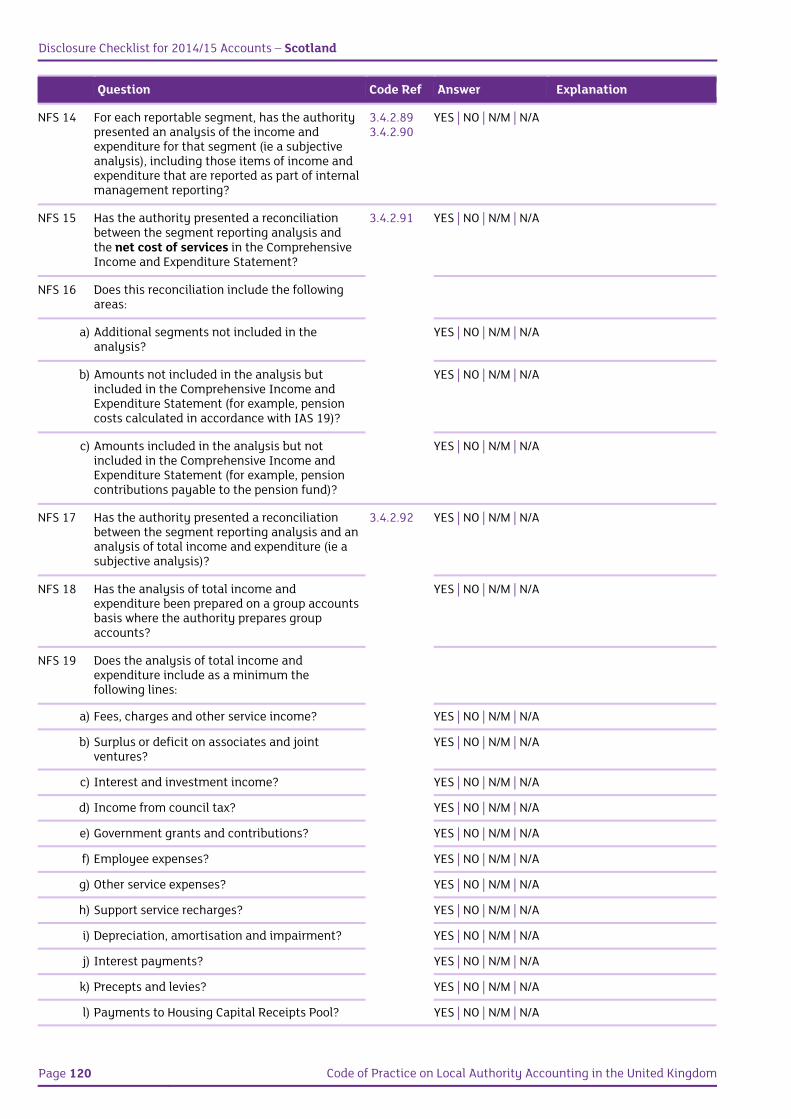

Question Code Ref Answer Explanation

NFS 14 For each reportable segment, has the authority presented an analysis of the income and expenditure for that segment (ie a subjective analysis), including those items of income and expenditure that are reported as part of internal management reporting?

3.4.2.893.4.2.90

YES | NO | N/M | N/A

NFS 15 Has the authority presented a reconciliation between the segment reporting analysis and the net cost of services in the Comprehensive Income and Expenditure Statement?

3.4.2.91 YES | NO | N/M | N/A

NFS 16 Does this reconciliation include the following areas:

a) Additional segments not included in the analysis?

YES | NO | N/M | N/A

b) Amounts not included in the analysis but included in the Comprehensive Income and Expenditure Statement (for example, pension costs calculated in accordance with IAS 19)?

YES | NO | N/M | N/A

c) Amounts included in the analysis but not included in the Comprehensive Income and Expenditure Statement (for example, pension contributions payable to the pension fund)?

YES | NO | N/M | N/A

NFS 17 Has the authority presented a reconciliation between the segment reporting analysis and an analysis of total income and expenditure (ie a subjective analysis)?

3.4.2.92 YES | NO | N/M | N/A

NFS 18 Has the analysis of total income and expenditure been prepared on a group accounts basis where the authority prepares group accounts?

YES | NO | N/M | N/A

NFS 19 Does the analysis of total income and expenditure include as a minimum the following lines:

a) Fees, charges and other service income? YES | NO | N/M | N/A

b) Surplus or deficit on associates and joint ventures?

YES | NO | N/M | N/A

c) Interest and investment income? YES | NO | N/M | N/A

d) Income from council tax? YES | NO | N/M | N/A

e) Government grants and contributions? YES | NO | N/M | N/A

f) Employee expenses? YES | NO | N/M | N/A

g) Other service expenses? YES | NO | N/M | N/A

h) Support service recharges? YES | NO | N/M | N/A

i) Depreciation, amortisation and impairment? YES | NO | N/M | N/A

j) Interest payments? YES | NO | N/M | N/A

k) Precepts and levies? YES | NO | N/M | N/A

l) Payments to Housing Capital Receipts Pool? YES | NO | N/M | N/A

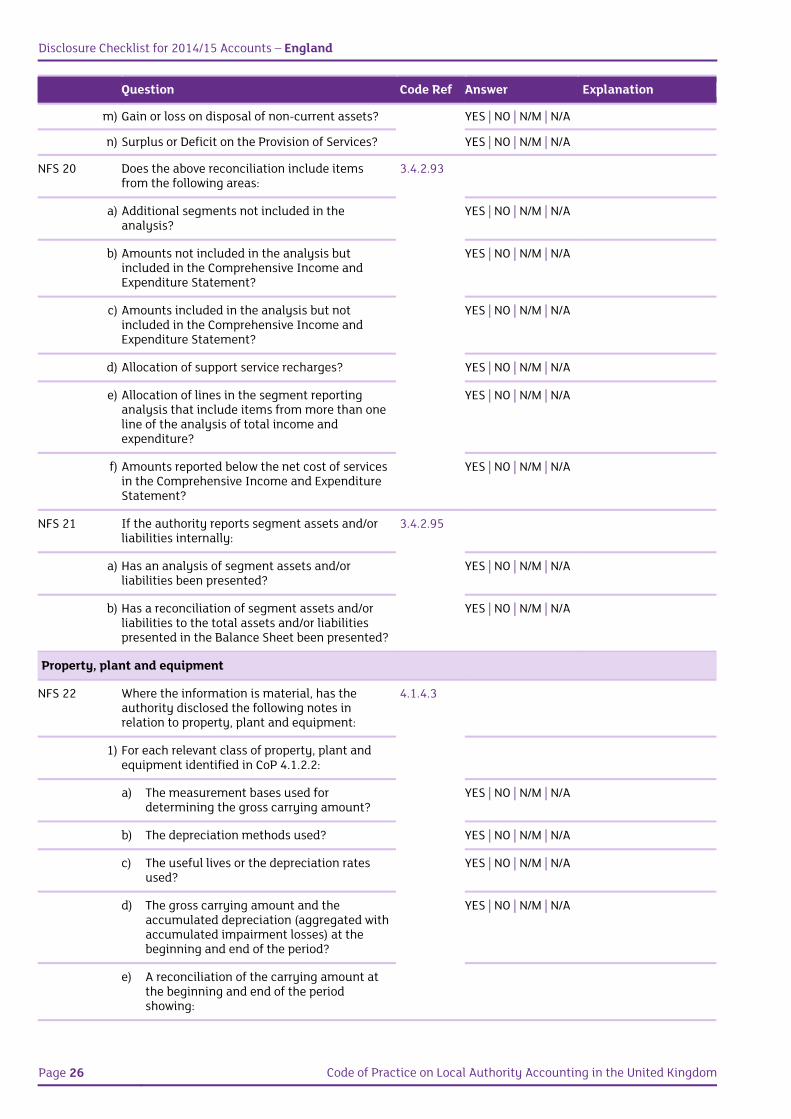

Disclosure Checklist for 2014/15 Accounts – England

Page 26 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

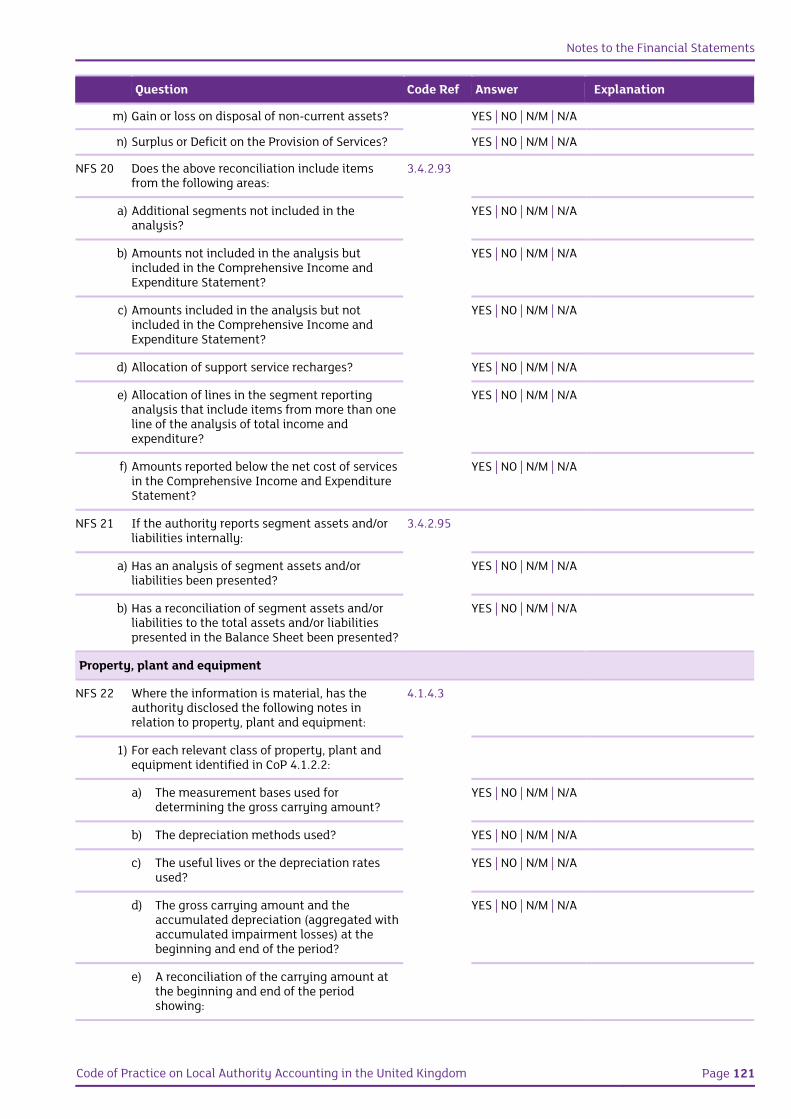

m) Gain or loss on disposal of non-current assets? YES | NO | N/M | N/A

n) Surplus or Deficit on the Provision of Services? YES | NO | N/M | N/A

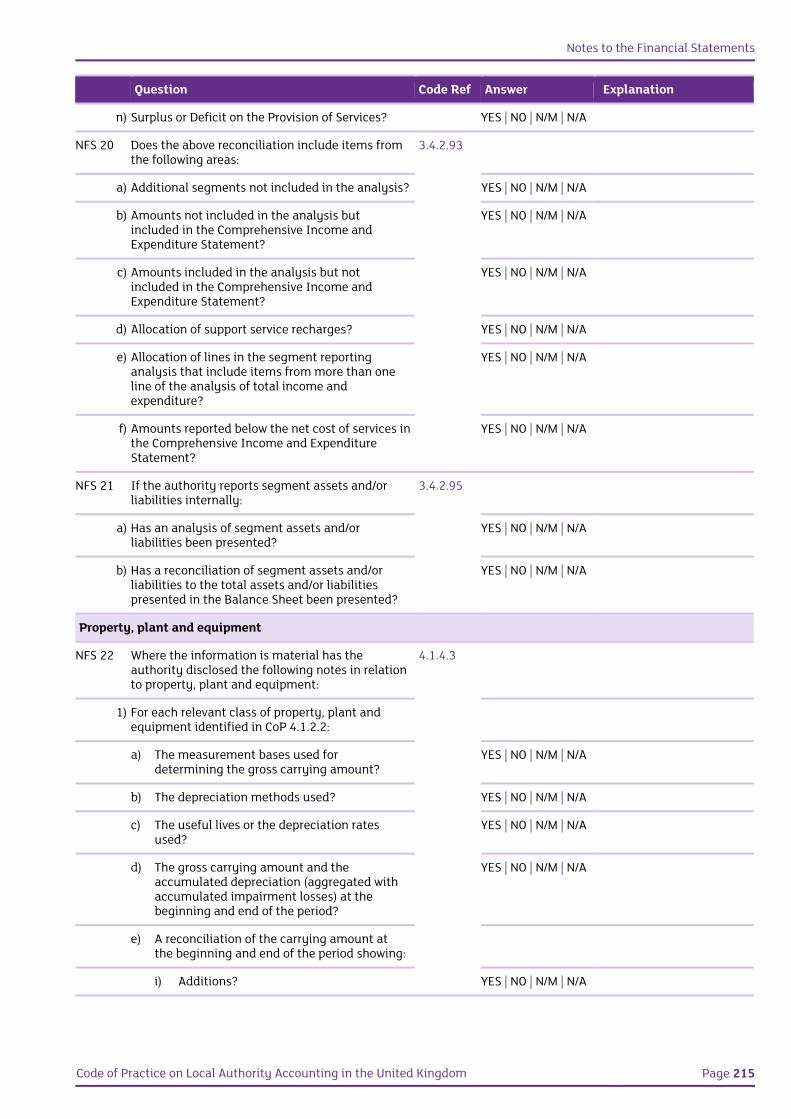

NFS 20 Does the above reconciliation include items from the following areas:

3.4.2.93

a) Additional segments not included in the analysis?

YES | NO | N/M | N/A

b) Amounts not included in the analysis but included in the Comprehensive Income and Expenditure Statement?

YES | NO | N/M | N/A

c) Amounts included in the analysis but not included in the Comprehensive Income and Expenditure Statement?

YES | NO | N/M | N/A

d) Allocation of support service recharges? YES | NO | N/M | N/A

e) Allocation of lines in the segment reporting analysis that include items from more than one line of the analysis of total income and expenditure?

YES | NO | N/M | N/A

f) Amounts reported below the net cost of services in the Comprehensive Income and Expenditure Statement?

YES | NO | N/M | N/A

NFS 21 If the authority reports segment assets and/or liabilities internally:

3.4.2.95

a) Has an analysis of segment assets and/or liabilities been presented?

YES | NO | N/M | N/A

b) Has a reconciliation of segment assets and/or liabilities to the total assets and/or liabilities presented in the Balance Sheet been presented?

YES | NO | N/M | N/A

Property, plant and equipment

NFS 22 Where the information is material, has the authority disclosed the following notes in relation to property, plant and equipment:

4.1.4.3

1) For each relevant class of property, plant and equipment identified in CoP 4.1.2.2:

a) The measurement bases used for determining the gross carrying amount?

YES | NO | N/M | N/A

b) The depreciation methods used? YES | NO | N/M | N/A

c) The useful lives or the depreciation rates used?

YES | NO | N/M | N/A

d) The gross carrying amount and the accumulated depreciation (aggregated with accumulated impairment losses) at the beginning and end of the period?

YES | NO | N/M | N/A

e) A reconciliation of the carrying amount at the beginning and end of the period showing:

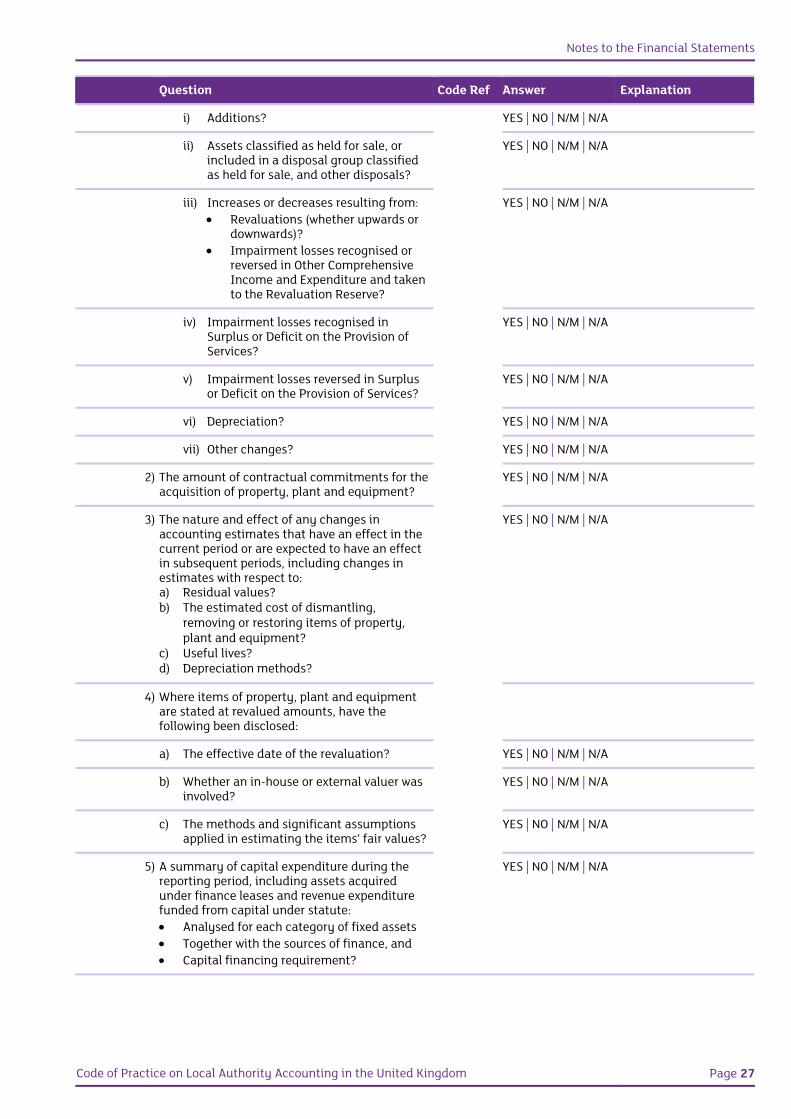

Notes to the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 27

Question Code Ref Answer Explanation

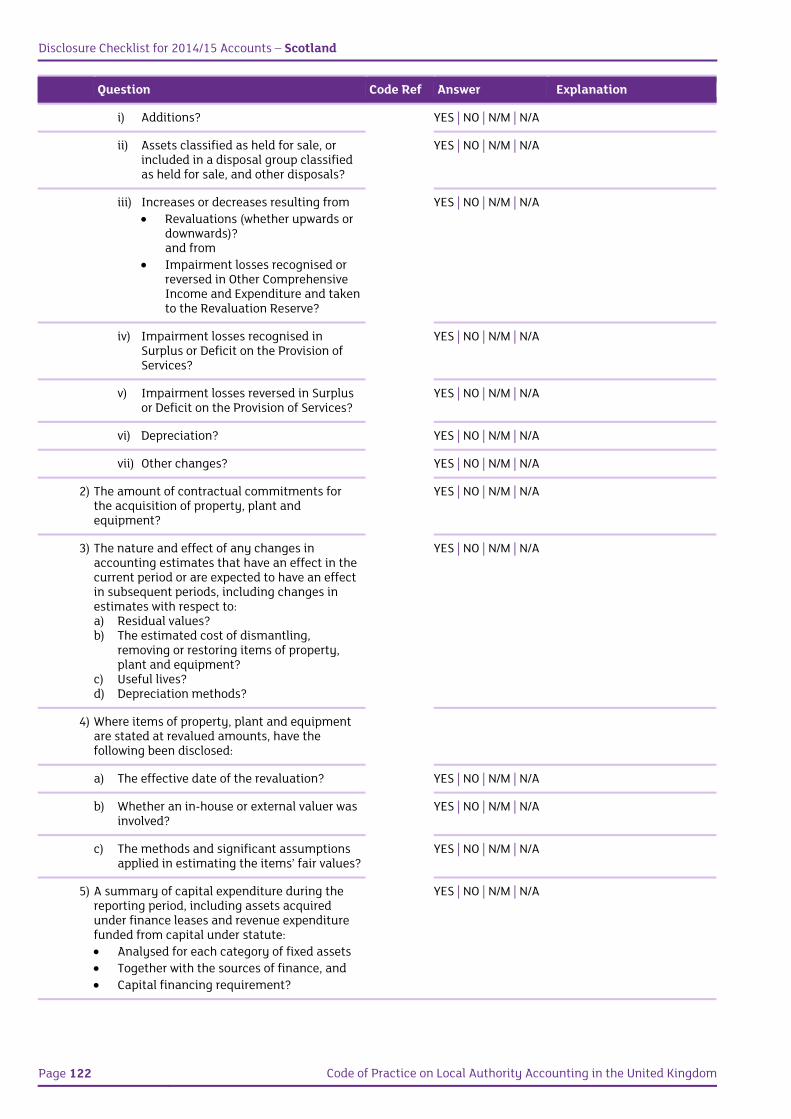

i) Additions? YES | NO | N/M | N/A

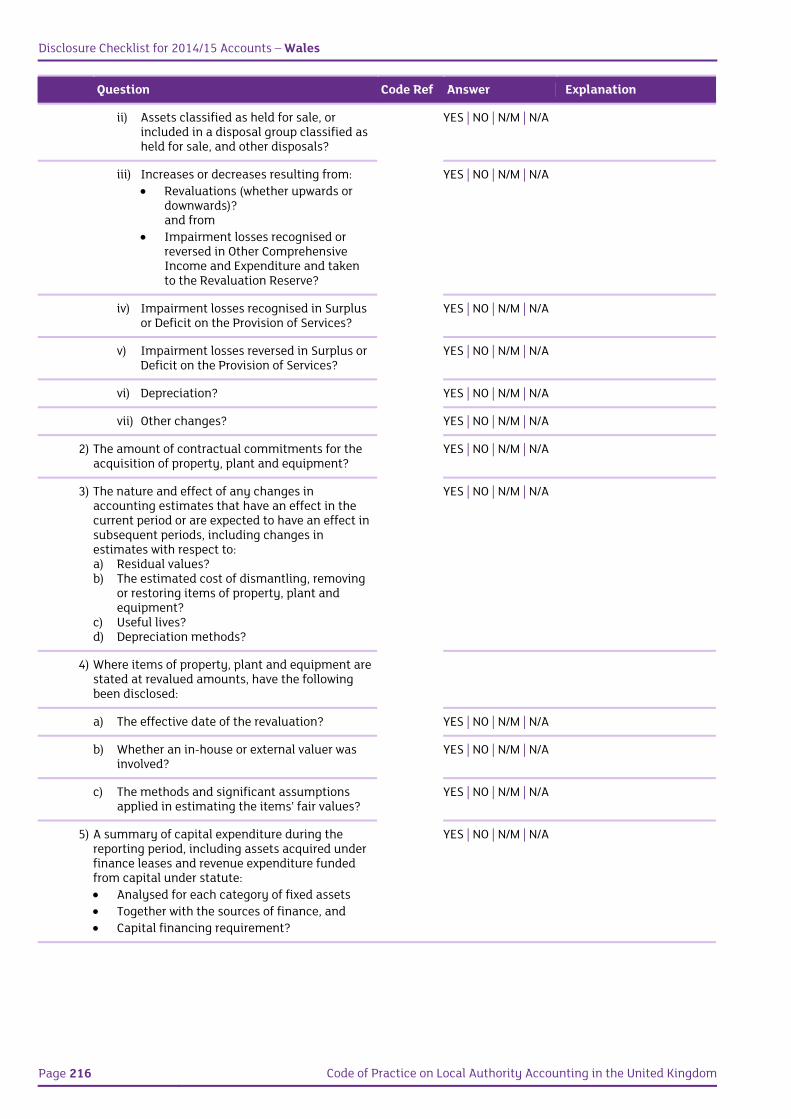

ii) Assets classified as held for sale, or included in a disposal group classified as held for sale, and other disposals?

YES | NO | N/M | N/A

iii) Increases or decreases resulting from: Revaluations (whether upwards or

downwards)? Impairment losses recognised or

reversed in Other Comprehensive Income and Expenditure and taken to the Revaluation Reserve?

YES | NO | N/M | N/A

iv) Impairment losses recognised in Surplus or Deficit on the Provision of Services?

YES | NO | N/M | N/A

v) Impairment losses reversed in Surplus or Deficit on the Provision of Services?

YES | NO | N/M | N/A

vi) Depreciation? YES | NO | N/M | N/A

vii) Other changes? YES | NO | N/M | N/A

2) The amount of contractual commitments for the acquisition of property, plant and equipment?

YES | NO | N/M | N/A

3) The nature and effect of any changes in accounting estimates that have an effect in the current period or are expected to have an effect in subsequent periods, including changes in estimates with respect to: a) Residual values? b) The estimated cost of dismantling,

removing or restoring items of property, plant and equipment?

c) Useful lives? d) Depreciation methods?

YES | NO | N/M | N/A

4) Where items of property, plant and equipment are stated at revalued amounts, have the following been disclosed:

a) The effective date of the revaluation? YES | NO | N/M | N/A

b) Whether an in-house or external valuer was involved?

YES | NO | N/M | N/A

c) The methods and significant assumptions applied in estimating the items’ fair values?

YES | NO | N/M | N/A

5) A summary of capital expenditure during the reporting period, including assets acquired under finance leases and revenue expenditure funded from capital under statute: Analysed for each category of fixed assets Together with the sources of finance, and Capital financing requirement?

YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 28 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

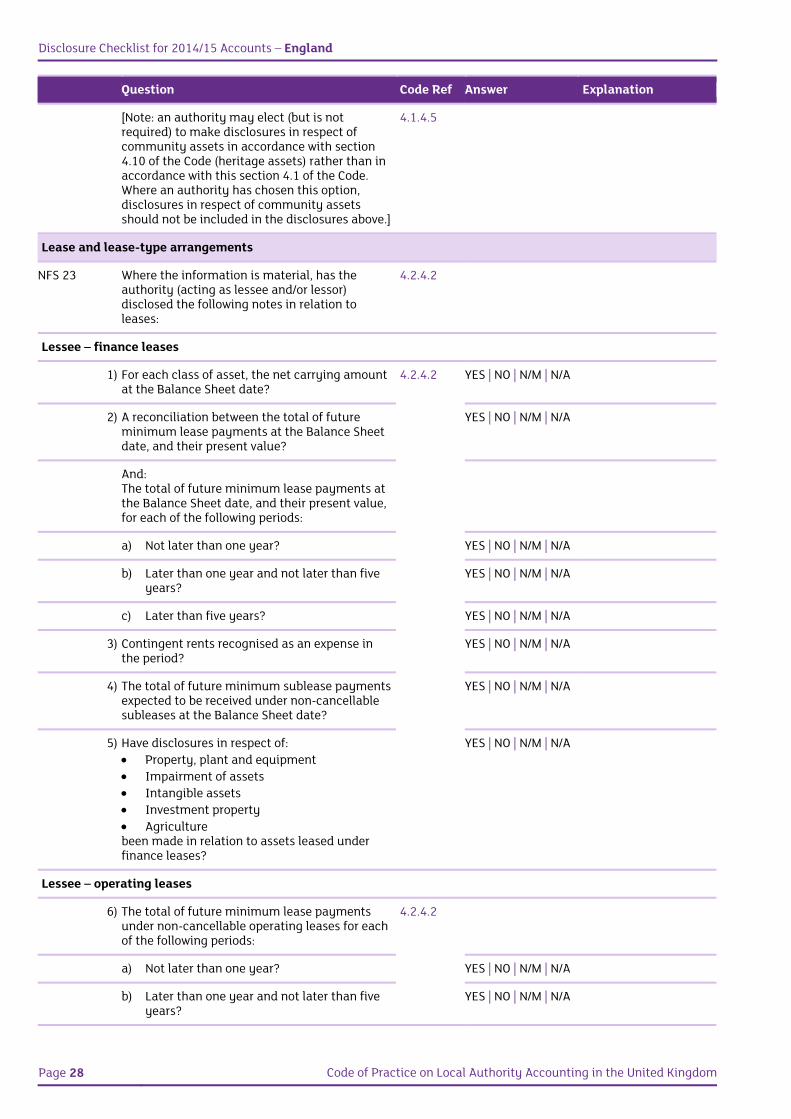

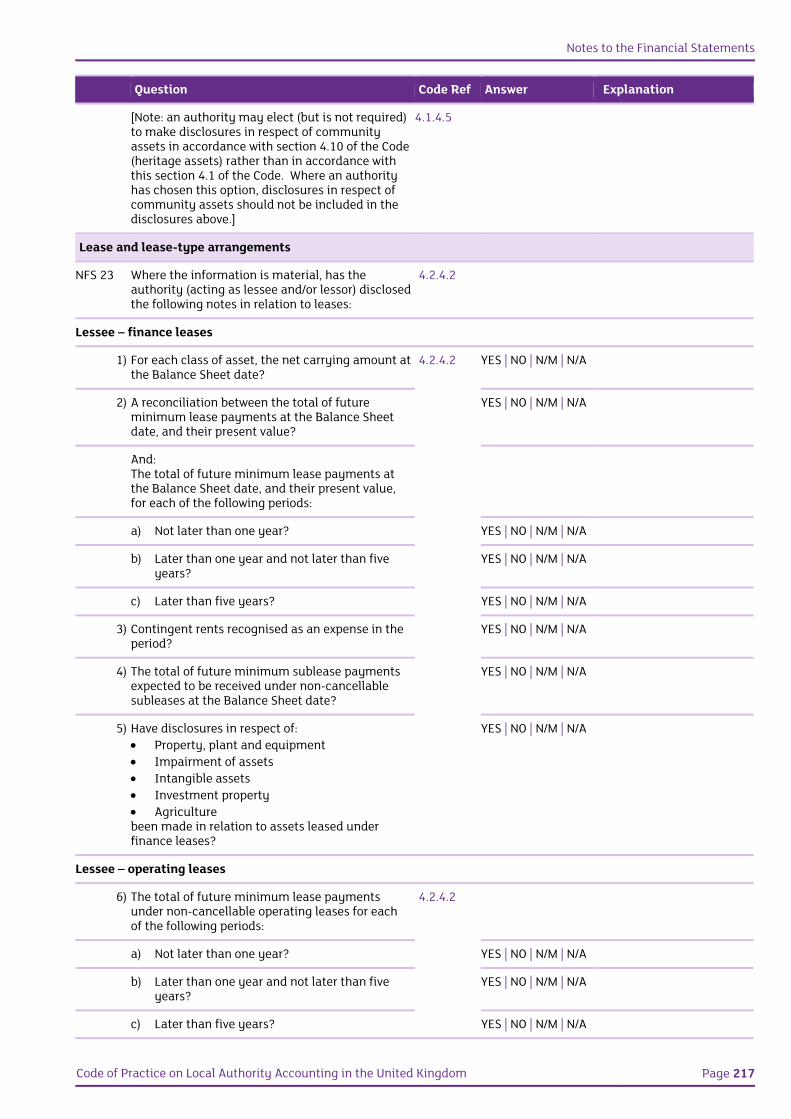

[Note: an authority may elect (but is not required) to make disclosures in respect of community assets in accordance with section 4.10 of the Code (heritage assets) rather than in accordance with this section 4.1 of the Code. Where an authority has chosen this option, disclosures in respect of community assets should not be included in the disclosures above.]

4.1.4.5

Lease and lease-type arrangements

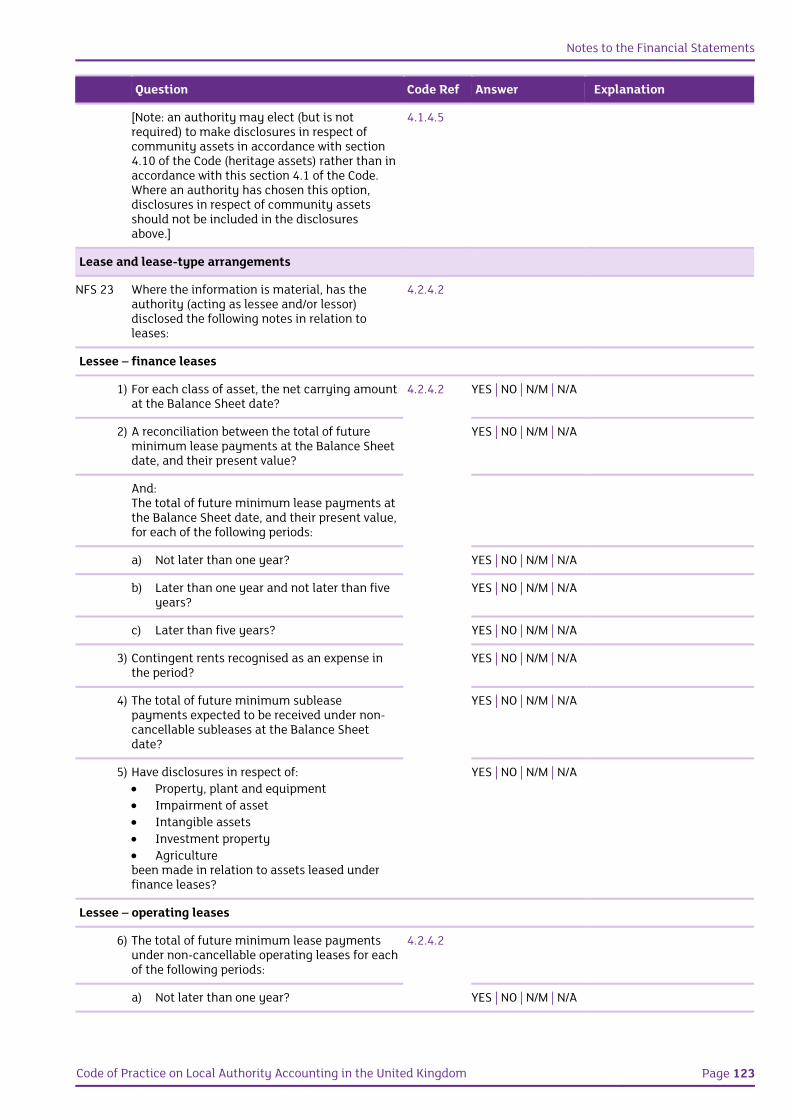

NFS 23 Where the information is material, has the authority (acting as lessee and/or lessor) disclosed the following notes in relation to leases:

4.2.4.2

Lessee – finance leases

1) For each class of asset, the net carrying amount at the Balance Sheet date?

4.2.4.2 YES | NO | N/M | N/A

2) A reconciliation between the total of future minimum lease payments at the Balance Sheet date, and their present value?

YES | NO | N/M | N/A

And: The total of future minimum lease payments at the Balance Sheet date, and their present value, for each of the following periods:

a) Not later than one year? YES | NO | N/M | N/A

b) Later than one year and not later than five years?

YES | NO | N/M | N/A

c) Later than five years? YES | NO | N/M | N/A

3) Contingent rents recognised as an expense in the period?

YES | NO | N/M | N/A

4) The total of future minimum sublease payments expected to be received under non-cancellable subleases at the Balance Sheet date?

YES | NO | N/M | N/A

5) Have disclosures in respect of: Property, plant and equipment Impairment of assets Intangible assets Investment property Agriculture been made in relation to assets leased under finance leases?

YES | NO | N/M | N/A

Lessee – operating leases

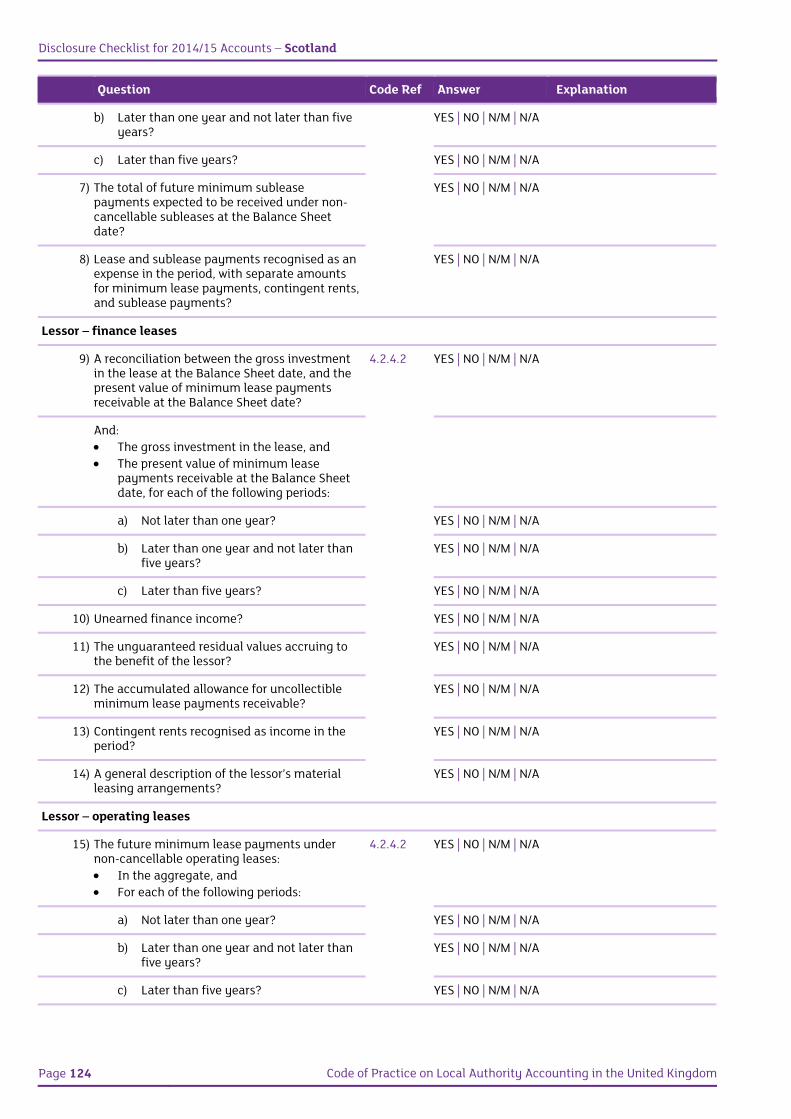

6) The total of future minimum lease payments under non-cancellable operating leases for each of the following periods:

4.2.4.2

a) Not later than one year? YES | NO | N/M | N/A

b) Later than one year and not later than five years?

YES | NO | N/M | N/A

Notes to the Financial Statements

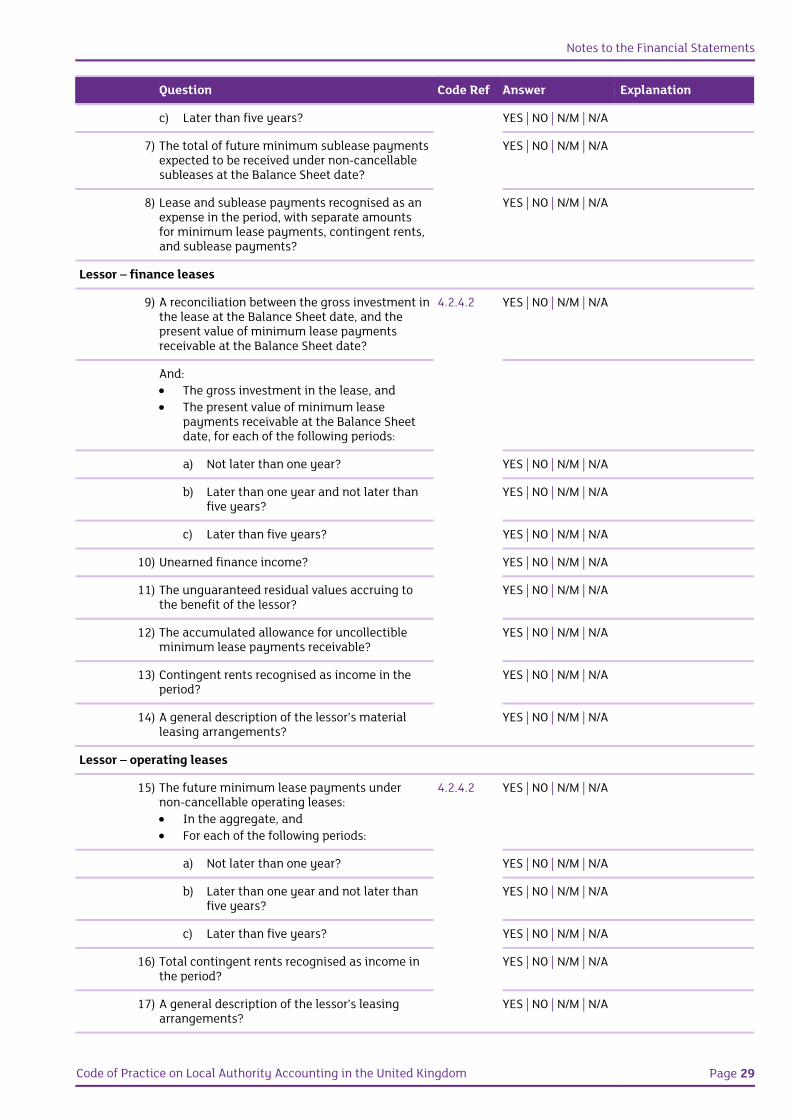

Code of Practice on Local Authority Accounting in the United Kingdom Page 29

Question Code Ref Answer Explanation

c) Later than five years? YES | NO | N/M | N/A

7) The total of future minimum sublease payments expected to be received under non-cancellable subleases at the Balance Sheet date?

YES | NO | N/M | N/A

8) Lease and sublease payments recognised as an expense in the period, with separate amounts for minimum lease payments, contingent rents, and sublease payments?

YES | NO | N/M | N/A

Lessor – finance leases

9) A reconciliation between the gross investment in the lease at the Balance Sheet date, and the present value of minimum lease payments receivable at the Balance Sheet date?

4.2.4.2 YES | NO | N/M | N/A

And: The gross investment in the lease, and The present value of minimum lease

payments receivable at the Balance Sheet date, for each of the following periods:

a) Not later than one year? YES | NO | N/M | N/A

b) Later than one year and not later than five years?

YES | NO | N/M | N/A

c) Later than five years? YES | NO | N/M | N/A

10) Unearned finance income? YES | NO | N/M | N/A

11) The unguaranteed residual values accruing to the benefit of the lessor?

YES | NO | N/M | N/A

12) The accumulated allowance for uncollectible minimum lease payments receivable?

YES | NO | N/M | N/A

13) Contingent rents recognised as income in the period?

YES | NO | N/M | N/A

14) A general description of the lessor’s material leasing arrangements?

YES | NO | N/M | N/A

Lessor – operating leases

15) The future minimum lease payments under non-cancellable operating leases: In the aggregate, and For each of the following periods:

4.2.4.2 YES | NO | N/M | N/A

a) Not later than one year? YES | NO | N/M | N/A

b) Later than one year and not later than five years?

YES | NO | N/M | N/A

c) Later than five years? YES | NO | N/M | N/A

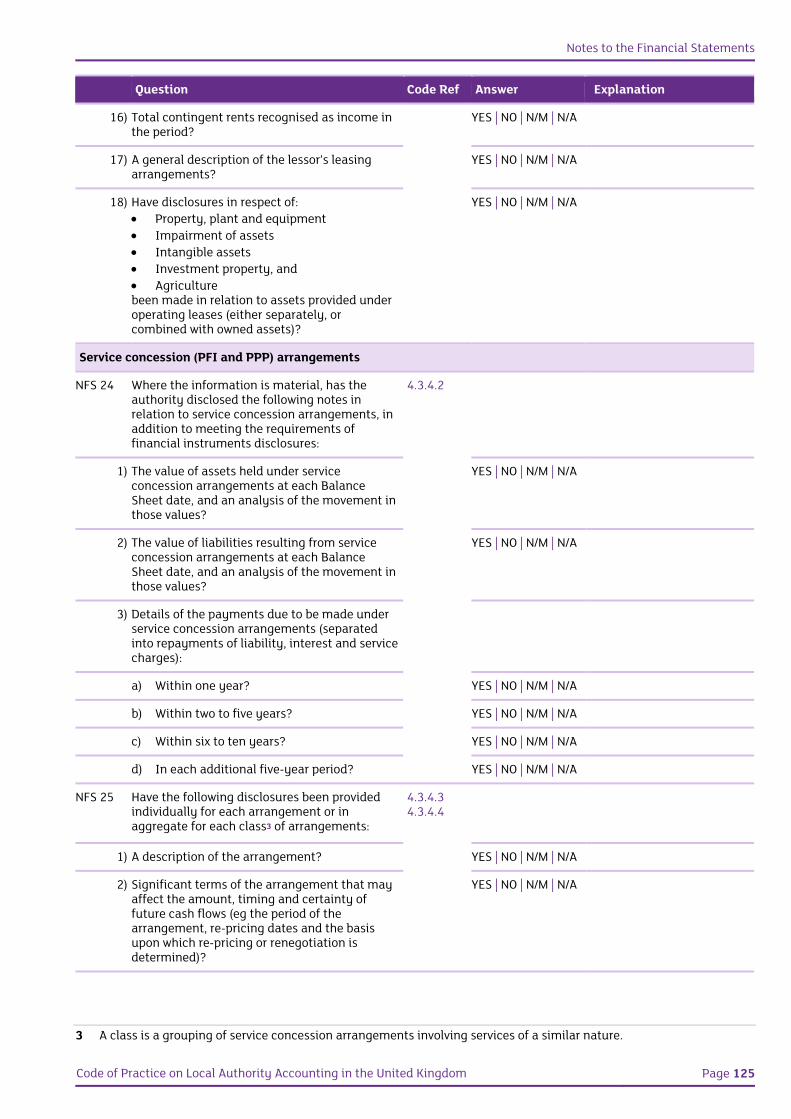

16) Total contingent rents recognised as income in the period?

YES | NO | N/M | N/A

17) A general description of the lessor’s leasing arrangements?

YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 30 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

18) Have disclosures in respect of: Property, plant and equipment Impairment of assets Intangible assets Investment property, and Agriculture been made in relation to assets provided under operating leases (either separately, or combined with owned assets)?

YES | NO | N/M | N/A

Service concession (PFI and PPP) arrangements

NFS 24 Where the information is material, has the authority disclosed the following notes in relation to service concession arrangements, in addition to meeting the requirements of financial instruments disclosures:

4.3.4.2

1) The value of assets held under service concession arrangements at each Balance Sheet date, and an analysis of the movement in those values?

YES | NO | N/M | N/A

2) The value of liabilities resulting from service concession arrangements at each Balance Sheet date, and an analysis of the movement in those values?

YES | NO | N/M | N/A

3) Details of the payments due to be made under service concession arrangements (separated into repayments of liability, interest and service charges):

a) Within one year? YES | NO | N/M | N/A

b) Within two to five years? YES | NO | N/M | N/A

c) Within six to ten years? YES | NO | N/M | N/A

d) In each additional five-year period? YES | NO | N/M | N/A

NFS 25 Have the following disclosures been provided individually for each arrangement or in aggregate for each class3 of arrangements:

4.3.4.34.3.4.4

1) A description of the arrangement? YES | NO | N/M | N/A

2) Significant terms of the arrangement that may affect the amount, timing and certainty of future cash flows (eg the period of the arrangement, re-pricing dates and the basis upon which re-pricing or renegotiation is determined)?

YES | NO | N/M | N/A

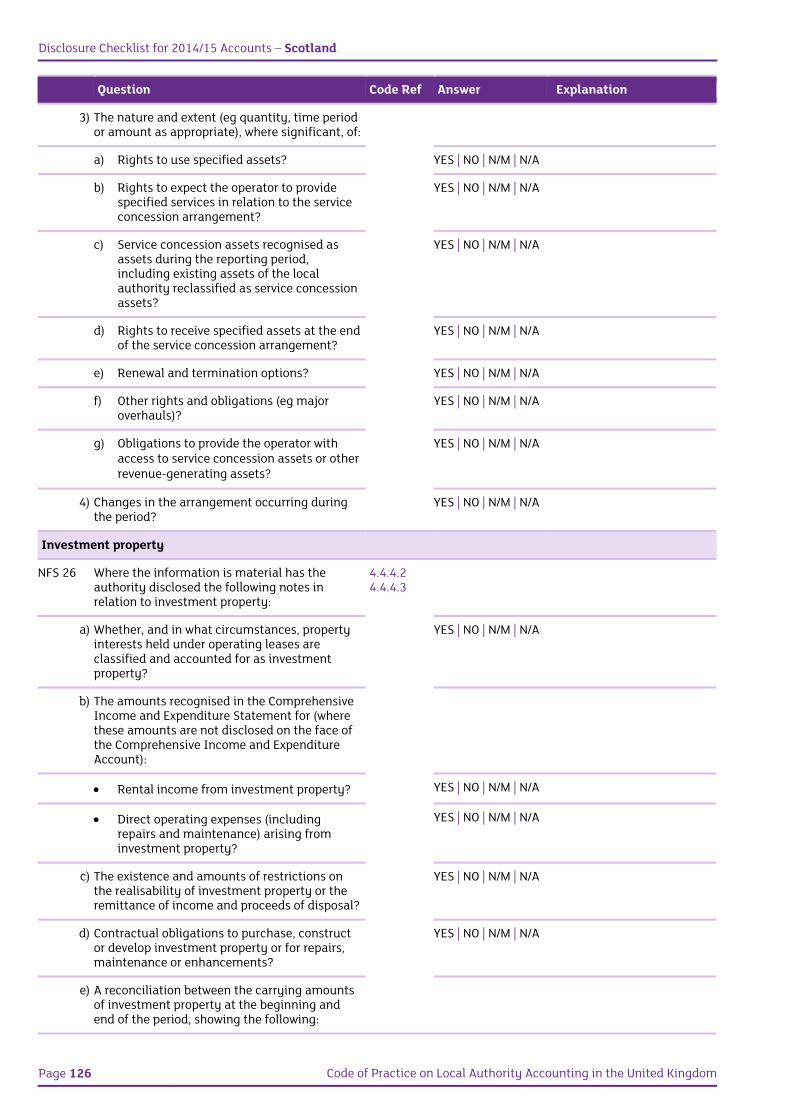

3) The nature and extent (eg quantity, time period or amount as appropriate), where significant, of:

a) Rights to use specified assets? YES | NO | N/M | N/A

3 A class is a grouping of service concession arrangements involving services of a similar nature.

Notes to the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 31

Question Code Ref Answer Explanation

b) Rights to expect the operator to provide specified services in relation to the service concession arrangement?

YES | NO | N/M | N/A

c) Service concession assets recognised as assets during the reporting period, including existing assets of the local authority reclassified as service concession assets?

YES | NO | N/M | N/A

d) Rights to receive specified assets at the end of the service concession arrangement?

YES | NO | N/M | N/A

e) Renewal and termination options? YES | NO | N/M | N/A

f) Other rights and obligations (eg major overhauls)?

YES | NO | N/M | N/A

g) Obligations to provide the operator with access to service concession assets or other revenue-generating assets?

YES | NO | N/M | N/A

4) Changes in the arrangement occurring during the period?

YES | NO | N/M | N/A

Investment property

NFS 26 Where the information is material, has the authority disclosed the following notes in relation to investment property:

4.4.4.24.4.4.3

a) Whether, and in what circumstances, property interests held under operating leases are classified and accounted for as investment property?

YES | NO | N/M | N/A

b) The amounts recognised in the Comprehensive Income and Expenditure Statement for (where these amounts are not disclosed on the face of the Comprehensive Income and Expenditure Account):

Rental income from investment property? YES | NO | N/M | N/A

Direct operating expenses (including repairs and maintenance) arising from investment property?

YES | NO | N/M | N/A

c) The existence and amounts of restrictions on the realisability of investment property or the remittance of income and proceeds of disposal?

YES | NO | N/M | N/A

d) Contractual obligations to purchase, construct or develop investment property or for repairs, maintenance or enhancements?

YES | NO | N/M | N/A

e) A reconciliation between the carrying amounts of investment property at the beginning and end of the period, showing the following:

Disclosure Checklist for 2014/15 Accounts – England

Page 32 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

Additions, disclosing separately those additions resulting from acquisitions and those resulting from subsequent expenditure recognised in the carrying amount of an asset?

YES | NO | N/M | N/A

Assets classified as held for sale or included in a disposal group classified as held for sale and other disposals?

YES | NO | N/M | N/A

Net gains or losses from fair value adjustments?

YES | NO | N/M | N/A

Transfers to and from inventories and owner-occupied property?

YES | NO | N/M | N/A

Other changes? YES | NO | N/M | N/A

f) Where the authority has elected to separately report investment property that meets the criteria to be classified as held for sale under IFRS 5, has it provided the disclosures required by section 4.9 of the Code in respect of that property?

YES | NO | N/M | N/A

g) Where the authority holds an investment property under a finance or operating lease, has it provided lessees’ disclosures for finance leases and lessors’ disclosures for any operating leases into which it has entered?

YES | NO | N/M | N/A

Intangible assets

NFS 27 Where the information is material, has the authority disclosed the following notes in relation to intangible assets:

4.5.4.2

1) For each class of intangible assets, distinguishing between internally generated intangible assets and other intangible assets:

a) Whether the useful lives are indefinite or finite and, if finite, the useful lives or the amortisation rates used?

YES | NO | N/M | N/A

b) The amortisation methods used for intangible assets with finite useful lives?

YES | NO | N/M | N/A

c) The gross carrying amount and any accumulated amortisation (aggregated with accumulated impairment losses) at the beginning and end of the period?

YES | NO | N/M | N/A

d) The line item(s) of the Comprehensive Income and Expenditure Statement in which any amortisation of intangible assets is included?

YES | NO | N/M | N/A

Notes to the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 33

Question Code Ref Answer Explanation

e) A reconciliation of the carrying amount at the beginning and end of the period showing:

i) Additions, indicating separately those from internal development, those acquired separately, and those acquired through business combinations?

YES | NO | N/M | N/A

ii) Assets classified as held for sale, or included in a disposal group classified as held for sale, and other disposals?

YES | NO | N/M | N/A

iii) Increases or decreases during the period resulting from revaluations, and from impairment losses recognised in, or reversed in, Other Comprehensive Income or Expenditure and taken to the Revaluation Reserve (if any)?

YES | NO | N/M | N/A

iv) Impairment losses recognised in Surplus or Deficit on the Provision of Services during the period (if any)?

YES | NO | N/M | N/A

v) Impairment losses reversed in Surplus or Deficit on the Provision of Services during the period (if any)?

YES | NO | N/M | N/A

vi) Any amortisation recognised during the period?

YES | NO | N/M | N/A

vii) Other changes? YES | NO | N/M | N/A

2) The nature and effect of any change in accounting estimates that: Has an effect in the current period, or Is expected to have an effect in subsequent

periods with respect to:

a) Residual values? YES | NO | N/M | N/A

b) An assessment of an intangible asset’s useful life?

YES | NO | N/M | N/A

c) Amortisation methods? YES | NO | N/M | N/A

3) For an intangible asset assessed as having an indefinite useful life: The carrying amount of that asset? The reasons supporting the assessment of

an indefinite useful life?

YES | NO | N/M | N/A

4) For each individual intangible asset that is material to the authority’s financial statements: A description? The carrying amount? The remaining amortisation period?

YES | NO | N/M | N/A

5) The amount of contractual commitments for the acquisition of intangible assets?

YES | NO | N/M | N/A

Disclosure Checklist for 2014/15 Accounts – England

Page 34 Code of Practice on Local Authority Accounting in the United Kingdom

Question Code Ref Answer Explanation

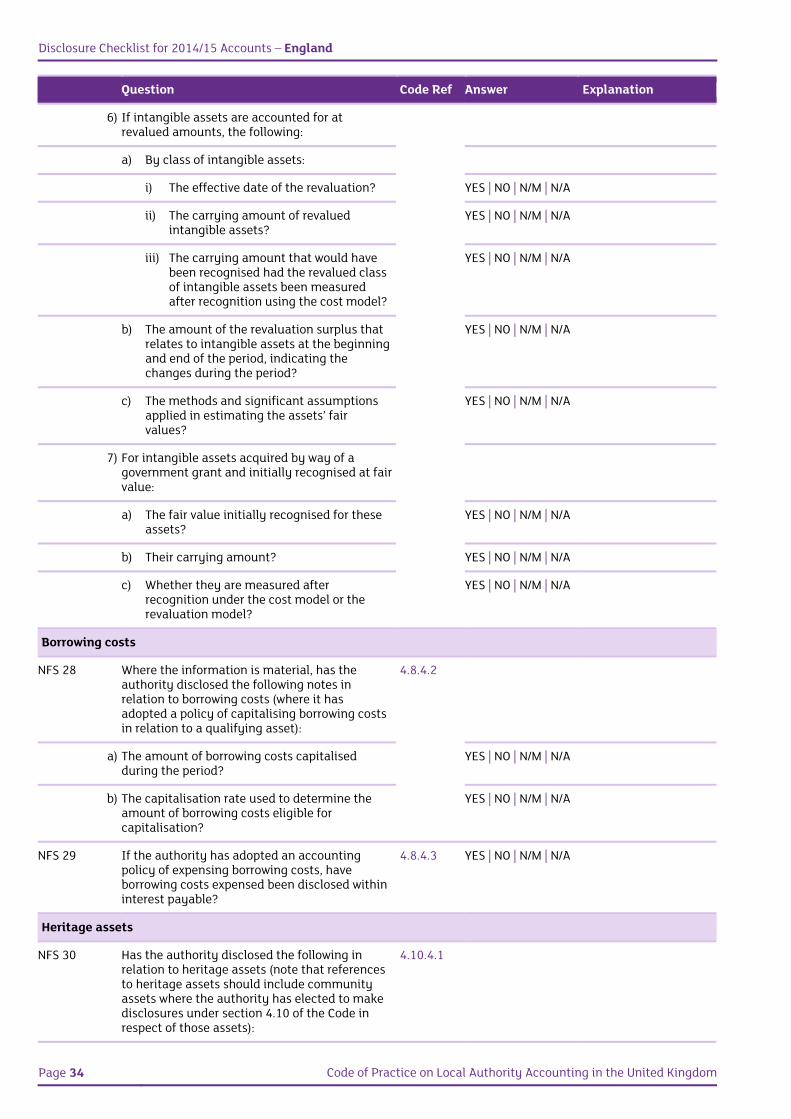

6) If intangible assets are accounted for at revalued amounts, the following:

a) By class of intangible assets:

i) The effective date of the revaluation? YES | NO | N/M | N/A

ii) The carrying amount of revalued intangible assets?

YES | NO | N/M | N/A

iii) The carrying amount that would have been recognised had the revalued class of intangible assets been measured after recognition using the cost model?

YES | NO | N/M | N/A

b) The amount of the revaluation surplus that relates to intangible assets at the beginning and end of the period, indicating the changes during the period?

YES | NO | N/M | N/A

c) The methods and significant assumptions applied in estimating the assets’ fair values?

YES | NO | N/M | N/A

7) For intangible assets acquired by way of a government grant and initially recognised at fair value:

a) The fair value initially recognised for these assets?

YES | NO | N/M | N/A

b) Their carrying amount? YES | NO | N/M | N/A

c) Whether they are measured after recognition under the cost model or the revaluation model?

YES | NO | N/M | N/A

Borrowing costs

NFS 28 Where the information is material, has the authority disclosed the following notes in relation to borrowing costs (where it has adopted a policy of capitalising borrowing costs in relation to a qualifying asset):

4.8.4.2

a) The amount of borrowing costs capitalised during the period?

YES | NO | N/M | N/A

b) The capitalisation rate used to determine the amount of borrowing costs eligible for capitalisation?

YES | NO | N/M | N/A

NFS 29 If the authority has adopted an accounting policy of expensing borrowing costs, have borrowing costs expensed been disclosed within interest payable?

4.8.4.3 YES | NO | N/M | N/A

Heritage assets

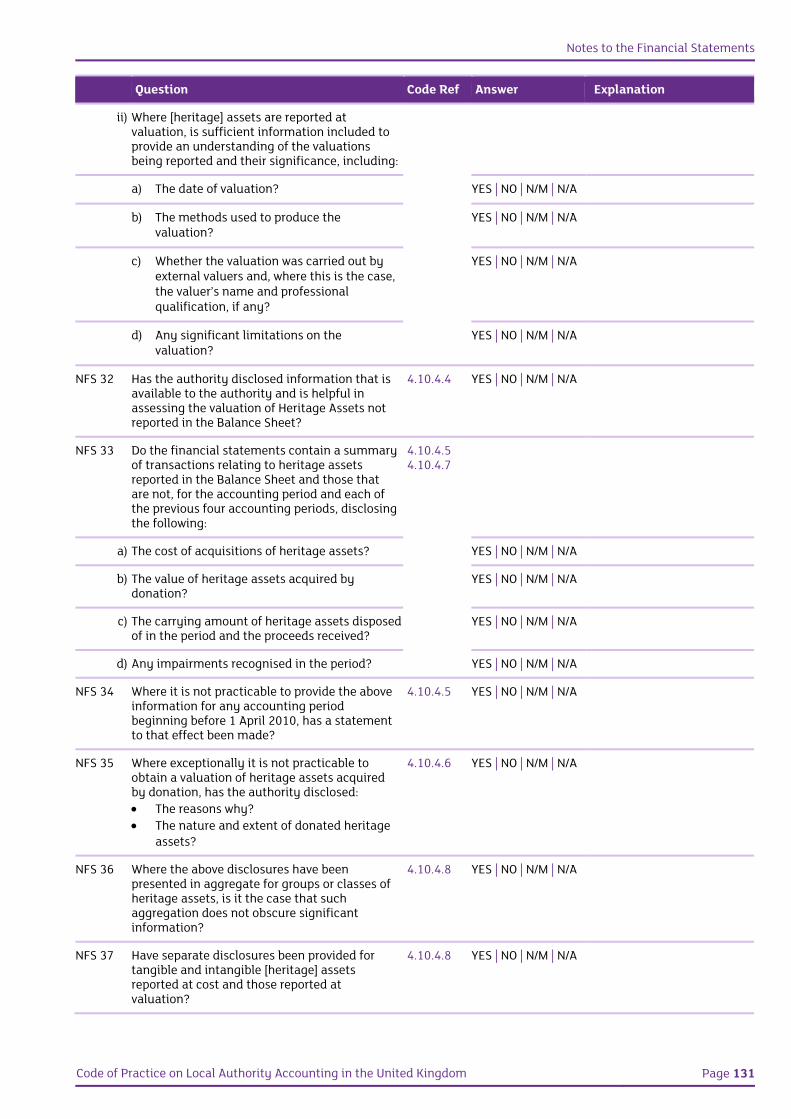

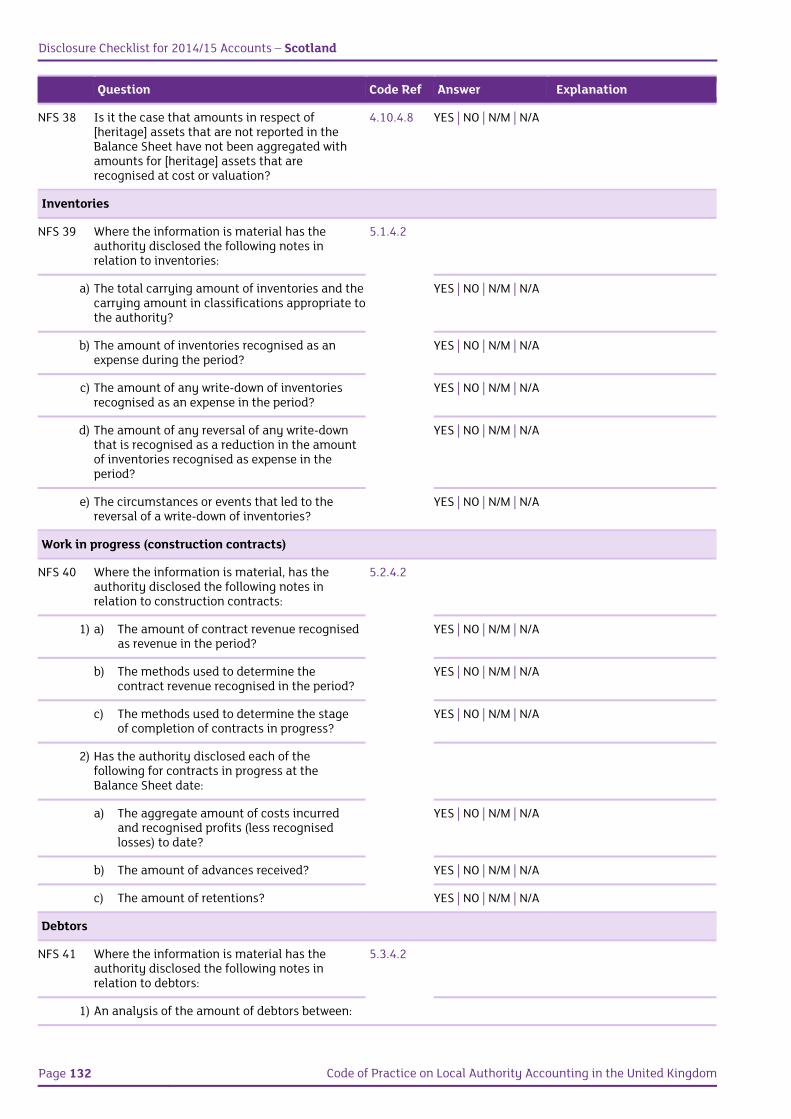

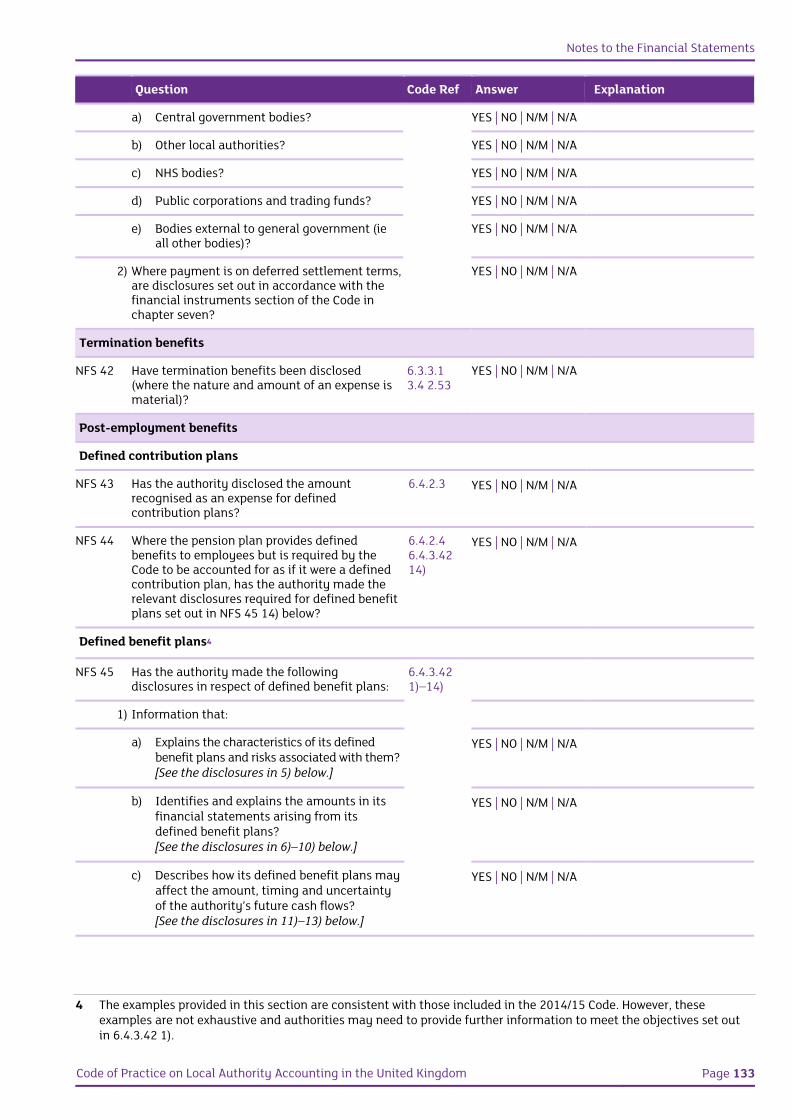

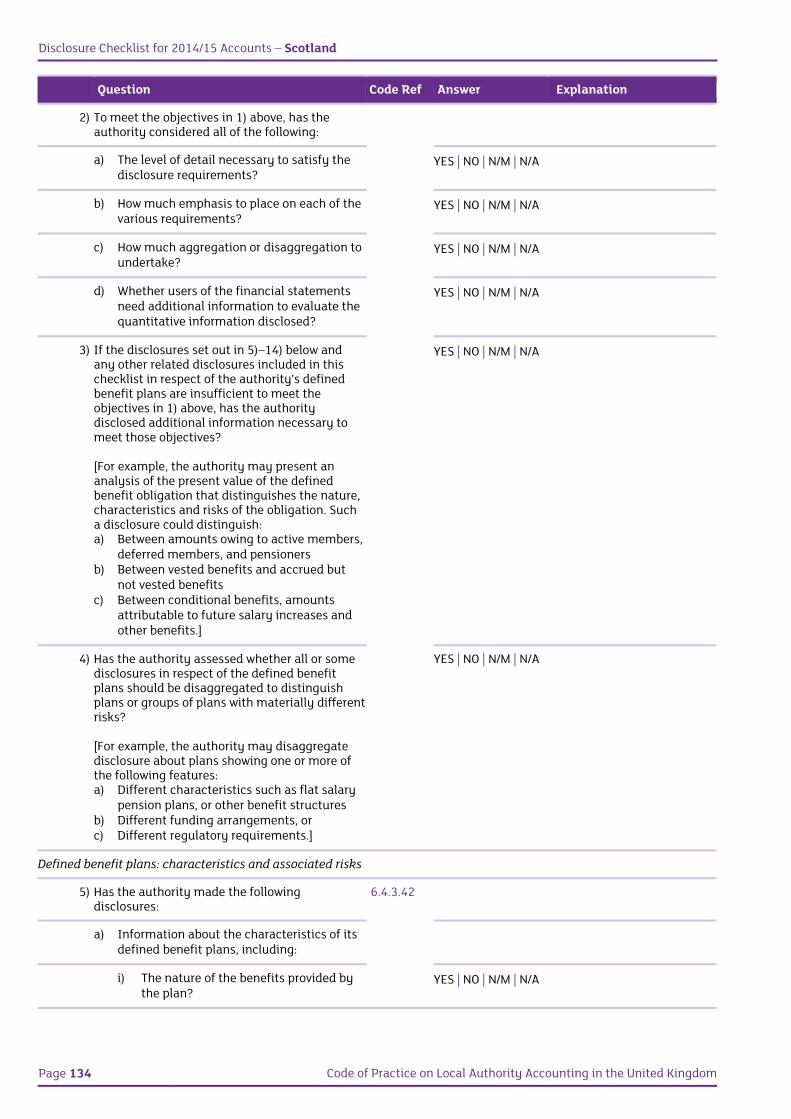

NFS 30 Has the authority disclosed the following in relation to heritage assets (note that references to heritage assets should include community assets where the authority has elected to make disclosures under section 4.10 of the Code in respect of those assets):

4.10.4.1

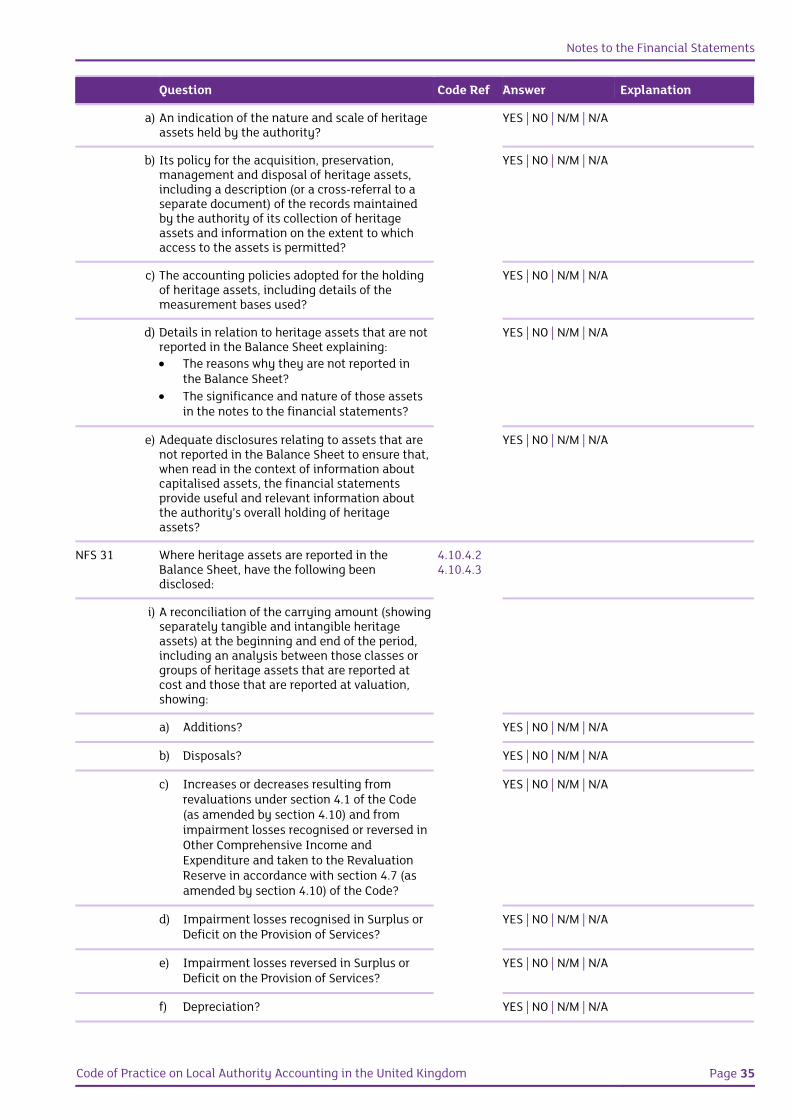

Notes to the Financial Statements

Code of Practice on Local Authority Accounting in the United Kingdom Page 35

Question Code Ref Answer Explanation

a) An indication of the nature and scale of heritage assets held by the authority?

YES | NO | N/M | N/A

b) Its policy for the acquisition, preservation, management and disposal of heritage assets, including a description (or a cross-referral to a separate document) of the records maintained by the authority of its collection of heritage assets and information on the extent to which access to the assets is permitted?

YES | NO | N/M | N/A

c) The accounting policies adopted for the holding of heritage assets, including details of the measurement bases used?

YES | NO | N/M | N/A

d) Details in relation to heritage assets that are not reported in the Balance Sheet explaining: The reasons why they are not reported in

the Balance Sheet? The significance and nature of those assets

in the notes to the financial statements?

YES | NO | N/M | N/A

e) Adequate disclosures relating to assets that are not reported in the Balance Sheet to ensure that, when read in the context of information about capitalised assets, the financial statements provide useful and relevant information about the authority’s overall holding of heritage assets?

YES | NO | N/M | N/A

NFS 31 Where heritage assets are reported in the Balance Sheet, have the following been disclosed:

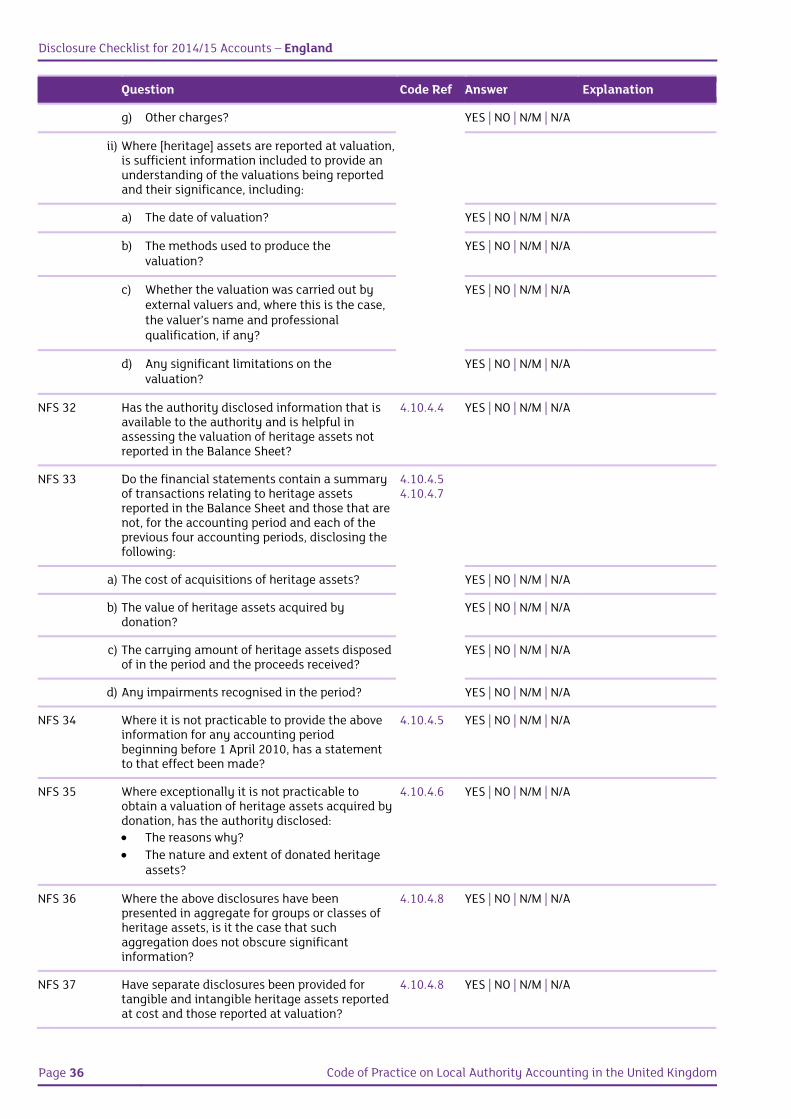

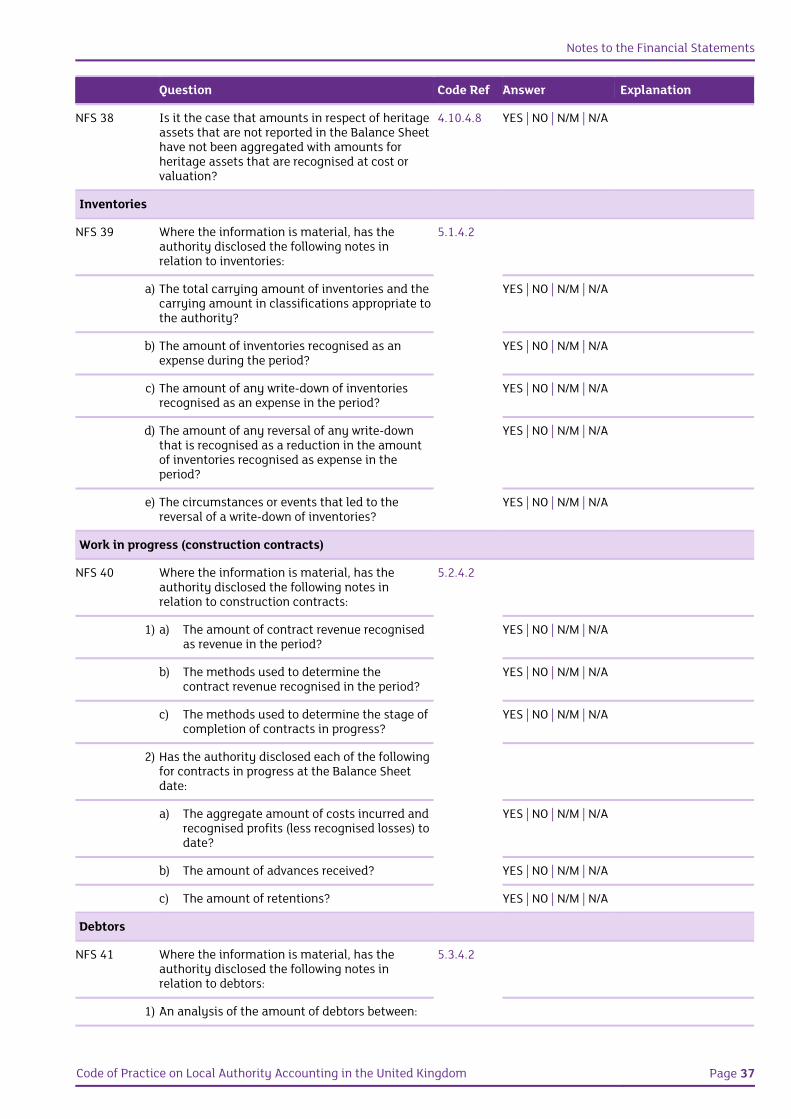

4.10.4.24.10.4.3