Embed Size (px)

Citation preview

Journey to Integra-on

Changing Market Place

• Affordable Care Act – Medicare Fee-‐for Service Cuts – $415 Billion by 2022 – Accountable Care OrganizaDon – Healthcare Exchanges, Public and Private

• Narrow Networks • Medicare Advantage Growth • Medicaid Expansion • High DeducDble Health Plans

– Retail RevoluDon • Healthcare Industry from B2B to B2C (Business to Business -‐ Business to Consumer)

Changing Market Place –Cont. • Meaningful Use -‐ IT Costs • Value Based Payment -‐ HHS Targets

– AlternaDve Payment Model • 30% by 2016 • 50% by 2018

– Fee-‐For-‐Service Payment Tied to Value • 85% by 2016 • 90% by 2018

• MACRA -‐ Medicare Access and CHIP ReauthorizaDon Act

• Industry ConsolidaDon “Our Mission is YOUR Health.”

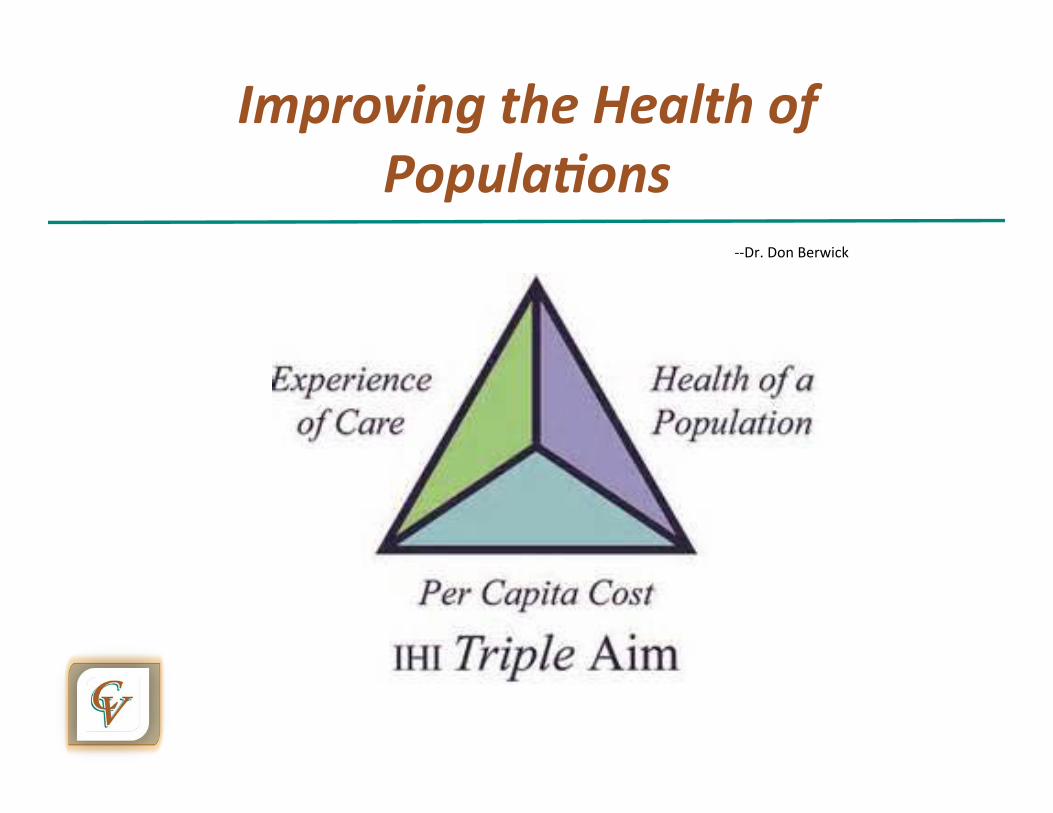

Improving the Health of Popula-ons

-‐-‐Dr. Don Berwick

CVRMC’s Strategies • Internal/External Environmental Assessment • Strategic Planning: Plan your work – Work your plan.

• Service Excellence Strategy • Quality Improvement Strategy • Community Partnerships • Growth • OperaDng Performance • CollaboraDon • Regional Partnerships

“Quality, Efficiency, Compassion.”

Environmental Assessment • Hospital Market Data

– Service Area DefiniDon – Demographics – Market Share – Internal Trends – Snapshot of Area Hospitals & Medical Centers

• Future ProjecDons • Physician Demand

6 “It’s All About You.”

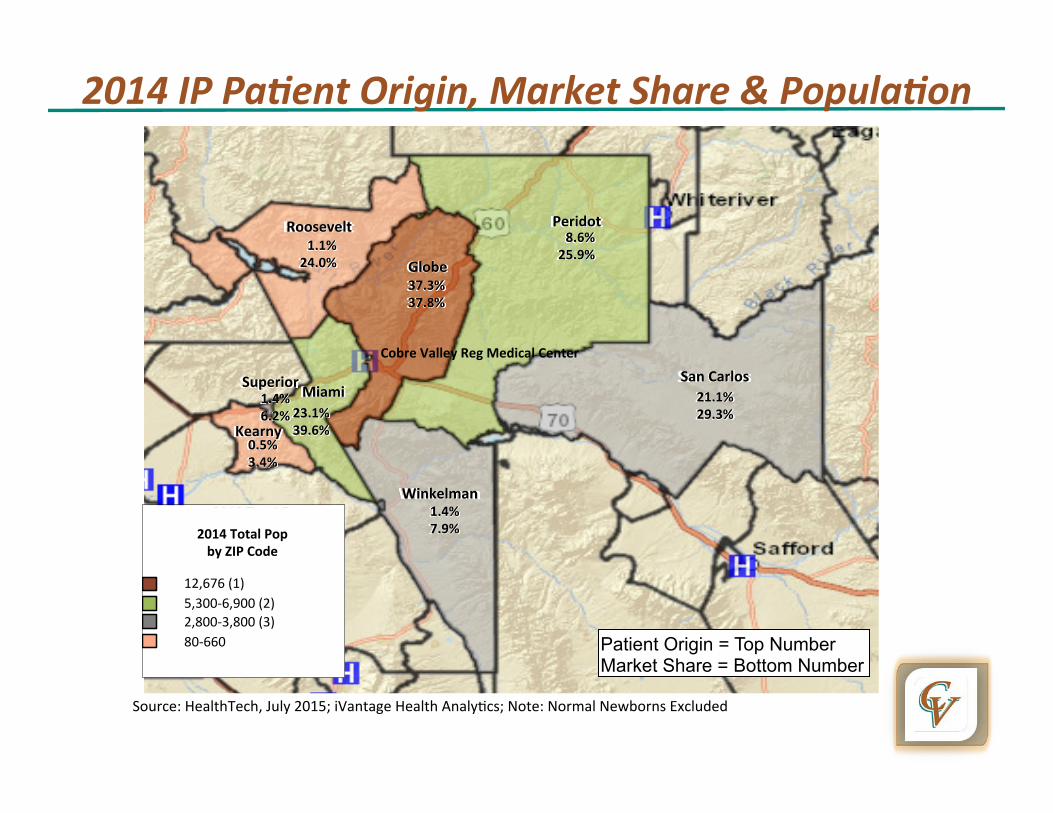

2014 IP Pa-ent Origin, Market Share & Popula-on

7

Roosevelt Peridot

Globe

San Carlos Superior

Kearny

Miami

Winkelman

37.3% 37.8%

21.1% 29.3%

1.1% 24.0%

8.6% 25.9%

1.4% 7.9%

23.1% 39.6%

0.5% 3.4%

1.4% 6.2%

Patient Origin = Top Number Market Share = Bottom Number

Source: HealthTech, July 2015; iVantage Health AnalyDcs; Note: Normal Newborns Excluded

Cobre Valley Reg Medical Center

2012 Total Pop

by ZIP Code

13,125 (1) (0)5,200 - 6,600 (2) (0)

2,200 - 3,300 (4) (0)85 (1) (0)

Bound ary Styles

ZIP Code

L an dmarks

US Hospitals

Scale

13.45 mi/inch

2014 Total Pop by ZIP Code

12,676 (1) 5,300-‐6,900 (2) 2,800-‐3,800 (3) 80-‐660

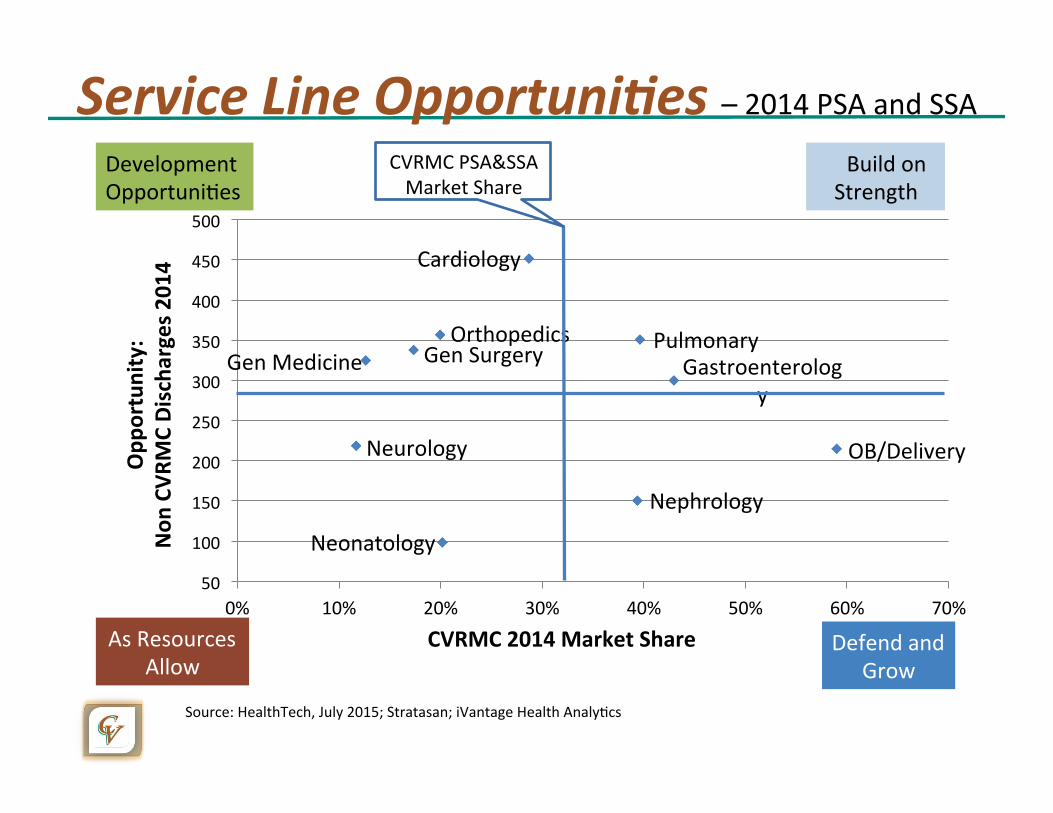

Service Line Opportuni-es – 2014 PSA and SSA

Cardiology

Orthopedics Pulmonary Gen Surgery Gen Medicine Gastroenterology

Neurology OB/Delivery

Nephrology

Neonatology

50

100

150

200

250

300

350

400

450

500

0% 10% 20% 30% 40% 50% 60% 70%

Opp

ortunity:

Non

CVR

MC Discha

rges 201

4

CVRMC 2014 Market Share

Development OpportuniDes

As Resources Allow

Build on Strength

Defend and Grow

CVRMC PSA&SSA Market Share

Source: HealthTech, July 2015; Stratasan; iVantage Health AnalyDcs

Strategic Planning • Comprehensive Planning Completed Every 3 Years • Annual Updates • OperaDonal Plan – Pushed to Employees • Quarterly Review with Board of Directors • Bi-‐Annual Environmental Assessment

Partnership Types • Merger or AcquisiDon -‐

• Formal Purchase or Another OrganizaDon • Clinically-‐Integrated Network

• CollecDon of hospitals contracDng jointly to improve coordinaDon and outcomes

• Accountable Care OrganizaDons • Independent enDty, owned by one or several independent organizaDons to

accept and share risk and savings • CollaboraDon

• Flexible umbrella structure ojen encompassing many independent organizaDons of geography that may serve as foundaDon for further integraDon

• Clinical AffiliaDon • An agreement to cooperate around a parDcular iniDaDve or service line

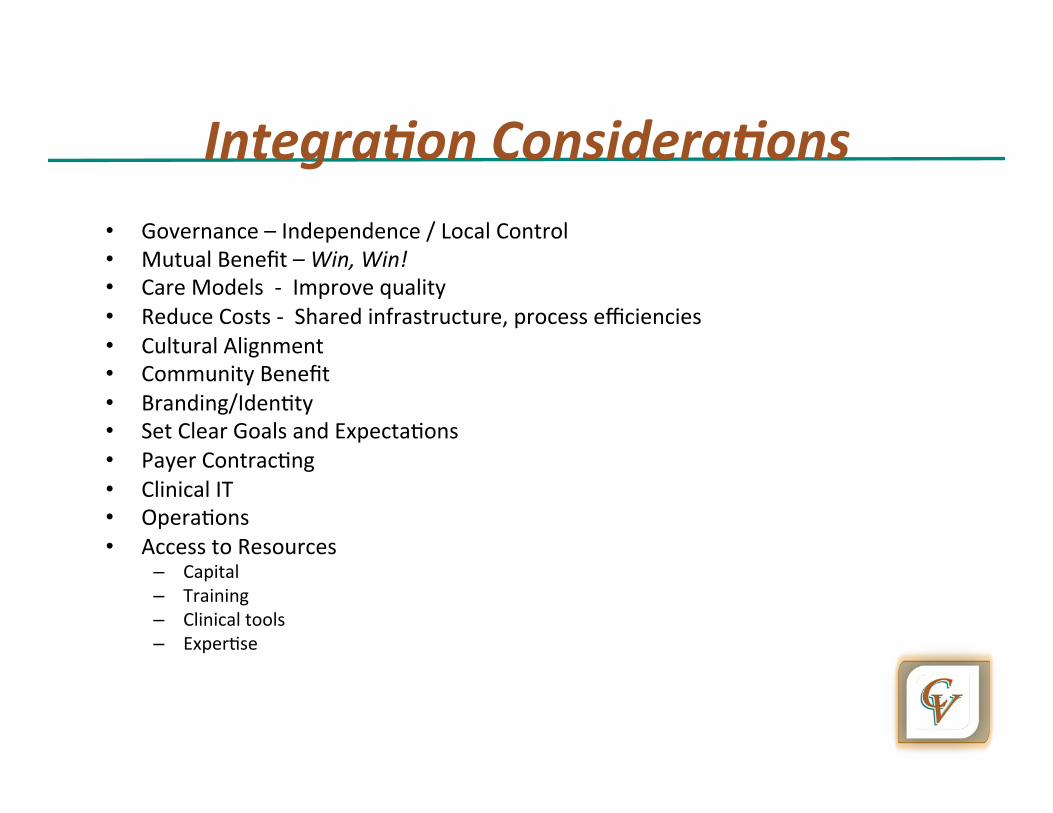

Integra-on Considera-ons • Governance – Independence / Local Control • Mutual Benefit – Win, Win! • Care Models -‐ Improve quality • Reduce Costs -‐ Shared infrastructure, process efficiencies • Cultural Alignment • Community Benefit • Branding/IdenDty • Set Clear Goals and ExpectaDons • Payer ContracDng • Clinical IT • OperaDons • Access to Resources

– Capital – Training – Clinical tools – ExperDse

Ques-ons?