Embed Size (px)

Citation preview

COAL MARKET IN INDIA 2012

“ Demand - Supply Gap

&

Technical Challenges in

Augmenting Coal Production”

10th July, 2012T K Mukherjee

General Manager (Corporate Planning)

Coal India Limited

STRATEGIC IMPORTANCE OF COAL IN INDIA

Around 85 % of coal consumed is met through indigenous source

CIL produces 81 % of India’s current coal production and meets 70 % of coal demand equivalent to 37 % of India’s commercial energy needs

* Others - 9 %

SCCL - 10 %

CIL - 81 %

Steel - 2 %

** Others - 26 %

Power (U)-72%

Coal Production : Company -wise Share Sector-wise Supply Share from CIL Sources

2

* Others include captive producer ,TATA STEEL, Meghalaya & Other PSUs

** Others include cement, sponge iron, fertilizer. Bricks etc

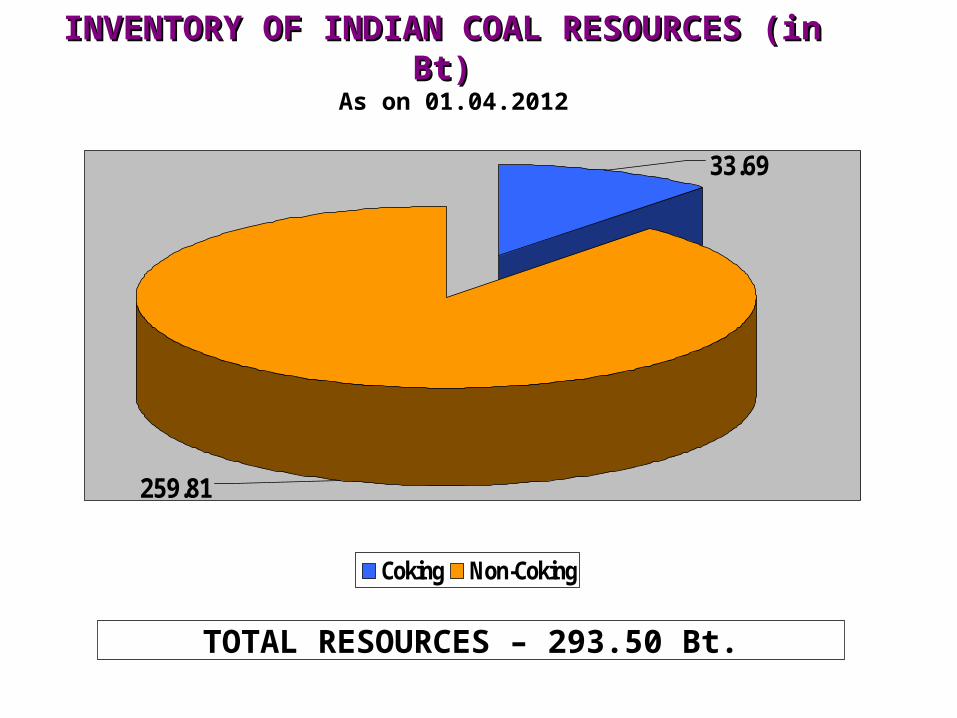

INVENTORY OF INDIAN COAL RESOURCES (in Bt)INVENTORY OF INDIAN COAL RESOURCES (in Bt)

259.81

33.69

Coking Non-Coking

TOTAL RESOURCES – 293.50 Bt.

As on 01.04.2012

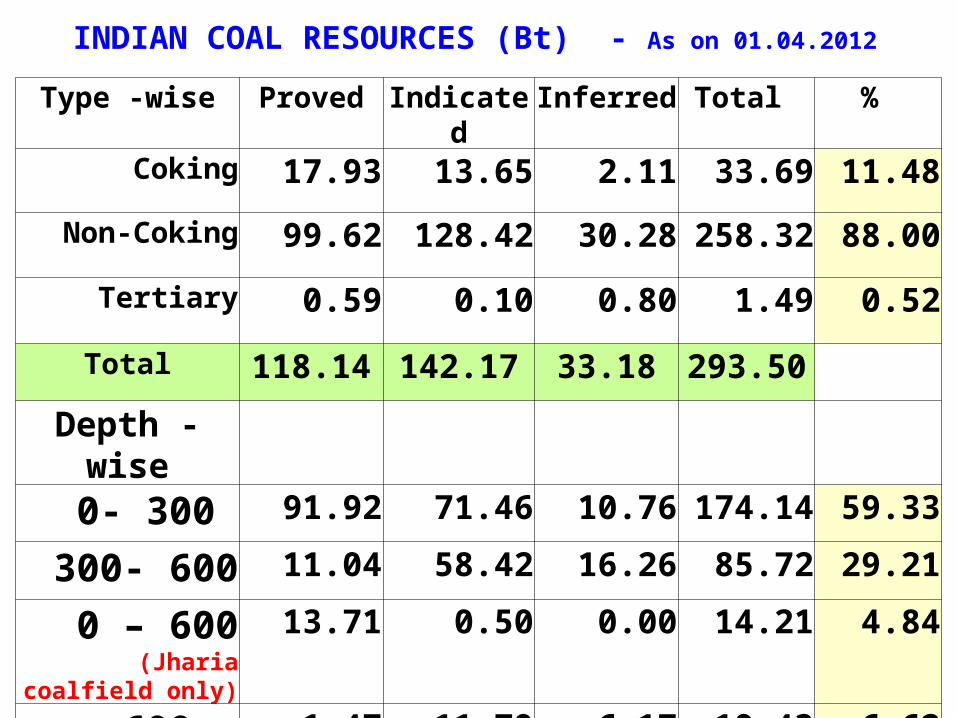

INDIAN COAL RESOURCES (Bt) - As on 01.04.2012

Type -wise Proved Indicated Inferred Total %

Coking 17.93 13.65 2.11 33.69 11.48

Non-Coking 99.62 128.42 30.28 258.32 88.00

Tertiary 0.59 0.10 0.80 1.49 0.52

Total 118.14 142.17 33.18 293.50

Depth -wise0- 300 91.92 71.46 10.76 174.14 59.33

300- 600 11.04 58.42 16.26 85.72 29.21

0 – 600(Jharia coalfield only)

13.71 0.50 0.00 14.21 4.84

600 – 1200 1.47 11.79 6.17 19.43 6.62

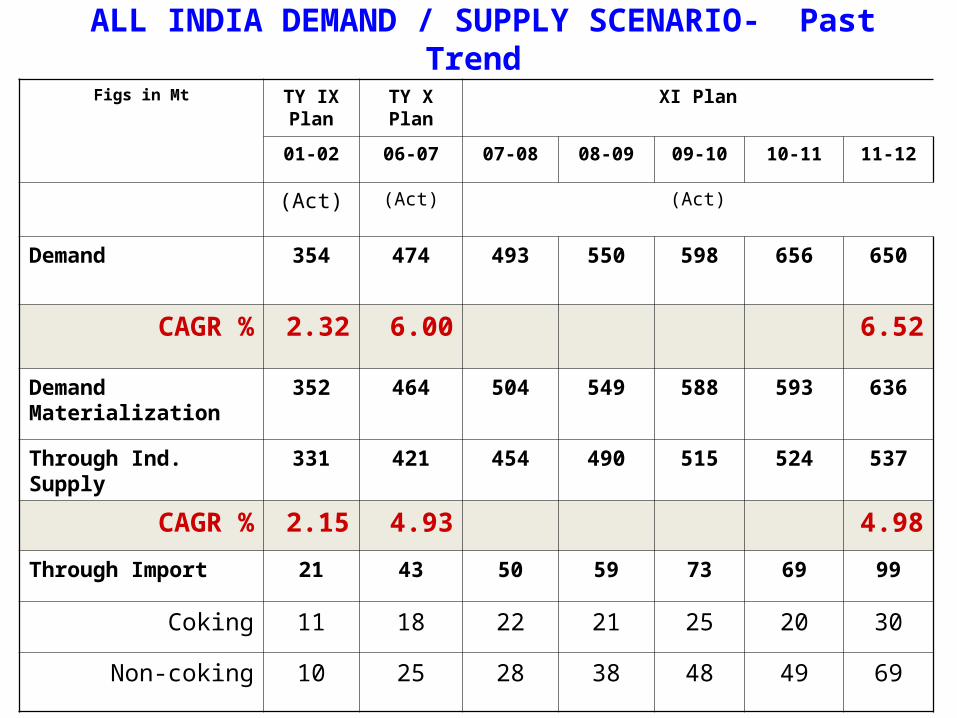

ALL INDIA DEMAND / SUPPLY SCENARIO- Past Trend

Figs in Mt TY IX Plan

TY X Plan

XI Plan

01-02 06-07 07-08 08-09 09-10 10-11 11-12

(Act) (Act) (Act)

Demand 354 474 493 550 598 656 650

CAGR % 2.32 6.00 6.52

Demand Materialization

352 464 504 549 588 593 636

Through Ind. Supply

331 421 454 490 515 524 537

CAGR % 2.15 4.93 4.98

Through Import 21 43 50 59 73 69 99

Coking 11 18 22 21 25 20 30

Non-coking 10 25 28 38 48 49 69

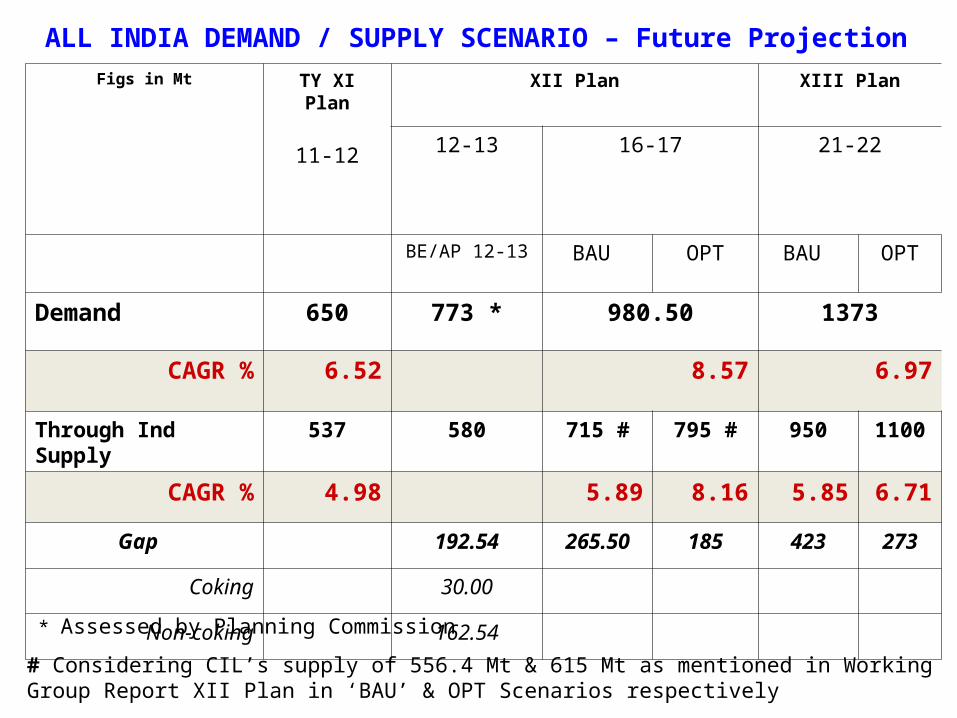

ALL INDIA DEMAND / SUPPLY SCENARIO – Future Projection Figs in Mt TY XI Plan

11-12

XII Plan XIII Plan

12-13 16-17 21-22

BE/AP 12-13 BAU OPT BAU OPT

Demand 650 773 * 980.50 1373

CAGR % 6.52 8.57 6.97

Through Ind Supply

537 580 715 # 795 # 950 1100

CAGR % 4.98 5.89 8.16 5.85 6.71

Gap 192.54 265.50 185 423 273

Coking 30.00

Non-coking 162.54

* Assessed by Planning Commission

# Considering CIL’s supply of 556.4 Mt & 615 Mt as mentioned in Working Group Report XII Plan in ‘BAU’ & OPT Scenarios respectively

Year-wise/Sector-wise Coal Consumption/Demand - Mt

Sector TY X Plan

XI Plan XII Plan

06-07 07-08 08-09 09-10 10-11 11-12 (Prov)

12-13 16-17

(Actual) TGT/AP12-13

PROJ

Steel 35.17 39.00 37.66 41.14 36.81 42.08 52.30 67.20

Power (U)

307.92 332.40 362.08 378.30 390.09

399.09 512.00 682.08

CAGR % 4.32 5.32 11.31

Others 120.78 132.89 149.28 167.77 166.10 194.45 208.54 231.22

Total 463.87 504.29 549.02 587.81 593.00

635.62 772.84 980.50

CAGR % 5.70 6.50 9.06

Drivers of future coal demand

Sufficient upside in demand available,

Per capita annual electricity consumption in FY08 was approx 704 kwh compared to USA (13066 kWh), UK (6231 kWh), China (1379 kWh), Brazil (1934 kWh)

High Unmet Demand

During summer, the power supply deficit is about 11-12 %

Electricity for All - As per the National Minimum Common Program, the government intends to provide access to electricity to all households. Rajiv Gandhi Grameen Vidyutikaran Yojana (RGGVY), is designed to provide access to all households and actually electrify only BPL households

Coal being the most abundant fuel source in India, the coal based power generation will remain strong in India

~ Coal based capacity addition is growing at a faster pace than the general power industry and as such the demand for coal is expected to remain strong

Coal based Generation Capacity Addition Scenario IX Plan (1997- 02) ~ 8000 MW X Plan (2002- 07) ~ 8500 MW XI Plan (2007-12) ~ 41660 MW XII Plan (2012-17) Projection: Proposed Capacity Addition Programme around 70, 000 MW

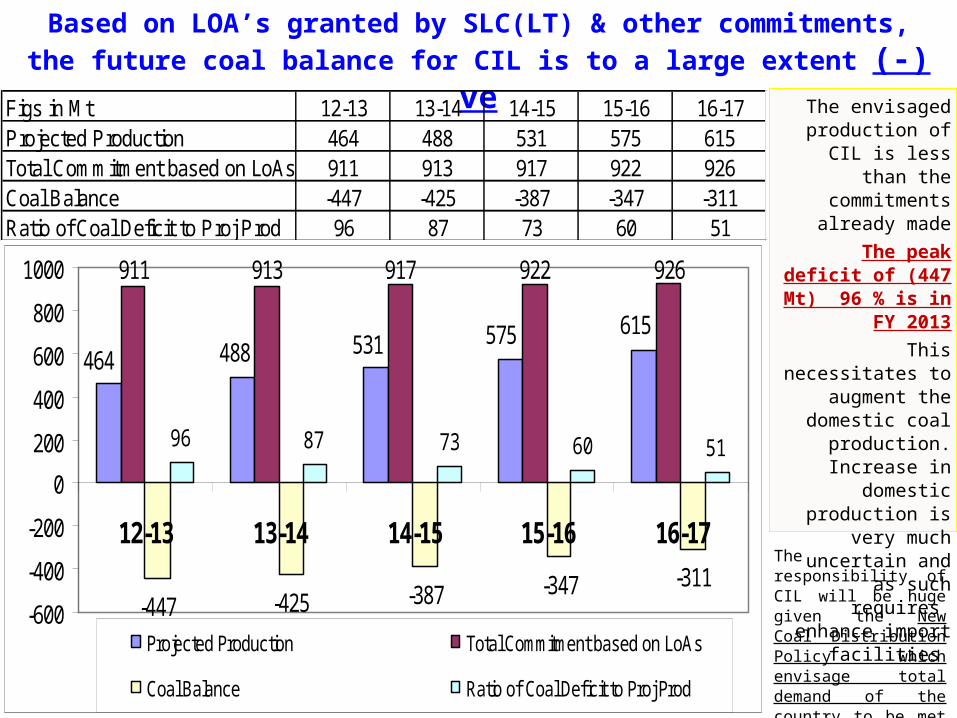

Based on LOA’s granted by SLC(LT) & other commitments, the future

coal balance for CIL is to a large extent (-) veThe envisaged

production of CIL is less than the commitments already made

The peak deficit of (447 Mt) 96 % is in

FY 2013

This necessitates to augment the

domestic coal production. Increase

in domestic production is very

much uncertain and as such requires

enhance import facilities

911 913 917 922 926

-447 -425 -387 -347 -311

96 87 73 60 51

615575531488464

-600

-400

-200

0

200

400

600

800

1000

12-13 13-14 14-15 15-16 16-17

Projected Production Total Commitment based on LoAs

Coal Balance Ratio of Coal Deficit to Proj Prod

Figs in Mt 12-13 13-14 14-15 15-16 16-17Projected Production 464 488 531 575 615Total Commitment based on LoAs 911 913 917 922 926Coal Balance -447 -425 -387 -347 -311Ratio of Coal Deficit to Proj Prod 96 87 73 60 51

The responsibility of CIL will be huge given the New Coal Distribution Policy which envisage total demand of the country to be met by CIL including coal imports, if required.

Source-wise Production (Mt) – Past Trend & Programme for 12-13 & XII Plan (Mt)

TY of VIII Plan

(96-97

TY of IX Plan

(01-02)

TY of X Plan

(06-07)

TY XI Plan

(11-12)

XII Plan

(12-13)

XII Plan

(16-17)

(BAU)

XII Plan

(16-17)

(OPT)

Production Actual TGT PROJ

CIL 250.62 279.65 360.91 435.84 464.10 556.40 615.00 #

CAGR % 4.19 2.22 5.23 3.84 ( 6.48)* 5.00 7.13

Non-CIL 38.70 48.14 69.92 103.95 110.30 180.00

All India 289.32 327.79 430.83 539.79 574.40 715.00 795.00

CAGR % 4.44 2.53 5.62 4.61 (6.42)* 5.78 8.05

10

* Growth% over previous year# The production in Optimistic Scenario is available only if the requisite clearances are processed in fast-tracked route and delivered within the specified time schedule. The issues affecting land acquisition, R & R, law & order and evacuation infrastructure in particular will also have to be addressed in a time bound manner

Production vs Off-take vs Stock Scenario in CIL

0

10

20

30

40

50

60

70

80

200

250

300

350

400

450

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY 10 FY11

ProductionOff-take

Stock position

Coal inventory levels have

grown as coal production has

increased.

It has not been possible to push

coal to customers & off take has lagged

behind coal production due

to non-availability of

scheduled no of rakes.

Evacuation not kept pace with

production leading to build-up of abnormal

coal stock(74 Mt)

(About 53 Mt increase in 8

years

Mt M

t

02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

290.69 306.36 323.58 343.39 360.91 379.46 403.73 431.26 431.32 435.84

289.23 304.44 321.55 333.67 351.14 375.33 401.44 415.88 424.50 433.08

19.26 21.18 23.21 32.93 42.70 46.83 49.12 64.50 71.32 74.08

X Plan XI Plan

Act

** As on 31st May 2012, Coal stock position is 63.618 Mt

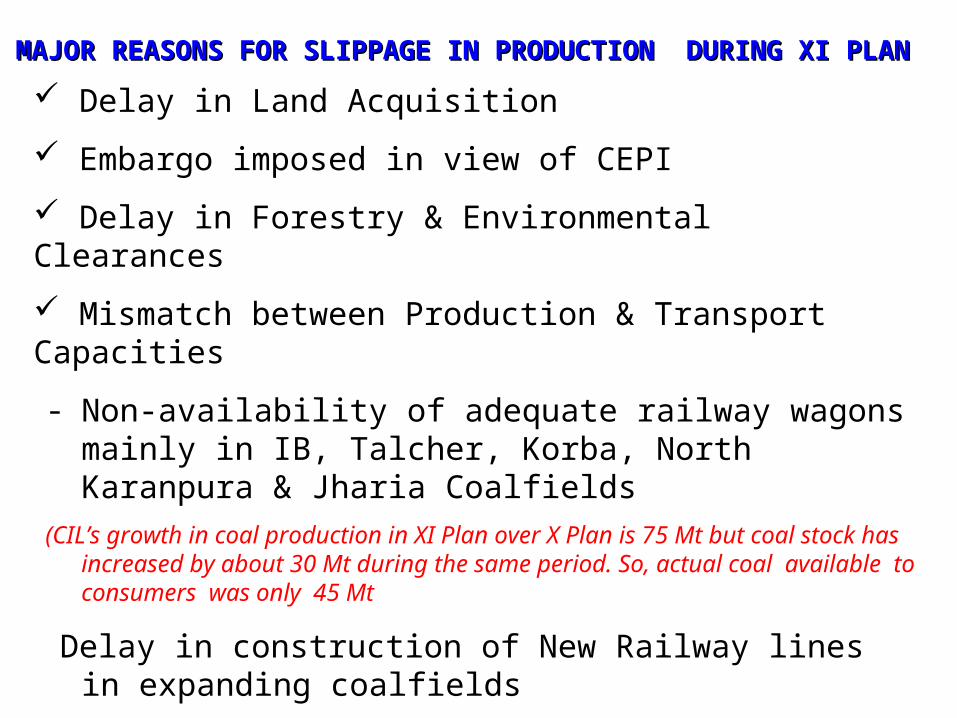

MAJOR REASONS FOR SLIPPAGE IN PRODUCTION DURING XI MAJOR REASONS FOR SLIPPAGE IN PRODUCTION DURING XI PLANPLAN Delay in Land Acquisition

Embargo imposed in view of CEPI

Delay in Forestry & Environmental Clearances

Mismatch between Production & Transport Capacities

- Non-availability of adequate railway wagons mainly in IB, Talcher, Korba, North Karanpura & Jharia Coalfields

(CIL’s growth in coal production in XI Plan over X Plan is 75 Mt but coal stock has increased by about 30 Mt during the same period. So, actual coal available to consumers was only 45 Mt

Delay in construction of New Railway lines in expanding coalfields

Delay in implementation of projects

Law & Order problems in Jharkhand & Orissa

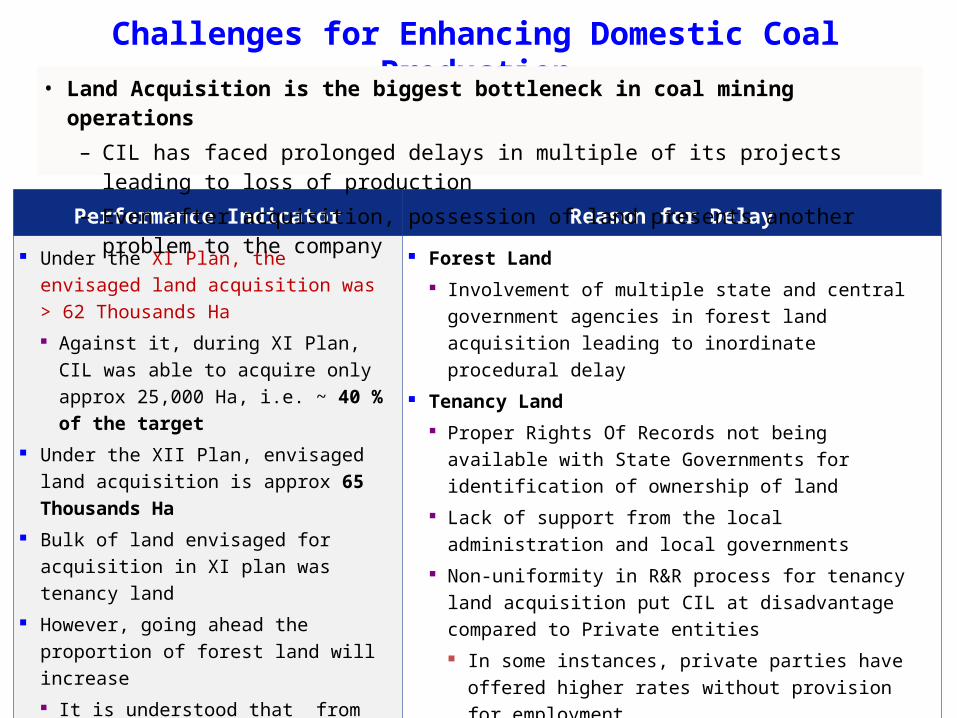

Challenges for Enhancing Domestic Coal Production

Performance Indicator Reason for Delay

Under the XI Plan, the envisaged land acquisition was > 62 Thousands Ha Against it, during XI Plan, CIL was

able to acquire only approx 25,000 Ha, i.e. ~ 40 % of the target

Under the XII Plan, envisaged land acquisition is approx 65 Thousands Ha

Bulk of land envisaged for acquisition in XI plan was tenancy land

However, going ahead the proportion of forest land will increase It is understood that from the

present proportion of 30 %, the forest land will increase to 50 % in the future years

Forest Land Involvement of multiple state and central

government agencies in forest land acquisition leading to inordinate procedural delay

Tenancy Land Proper Rights Of Records not being available with

State Governments for identification of ownership of land

Lack of support from the local administration and local governments

Non-uniformity in R&R process for tenancy land acquisition put CIL at disadvantage compared to Private entities In some instances, private parties have offered

higher rates without provision for employment

• Land Acquisition is the biggest bottleneck in coal mining operations

– CIL has faced prolonged delays in multiple of its projects leading to loss of production

– Even after acquisition, possession of land presents another problem to the company

Evacuation Infrastructure

Performance Indicator Reason for Delay

Average time for Stage I Forestry clearance is about 4 years

Average time for Stage II clearance is about 3 years

Thus the total time for Forestry Clearance is 7 years against the normative time of 2-3 years.

SPCB takes considerable time to issue Consent to Establish and Consent to Operate

Environment Clearance is only given up to a certain capacity (projected peak production) for specific project. Further capacity expansion requires new clearance which again is a prolonged process

In last 8 years coal stock has been increased by approx 53 Mt due to non-availability of, Sufficient railway rakes Matching feeder lines as well

as loading facilities in IB Valley, Korba & N.Karanpura fields

Bulk of future production will come from 5 coal fields of CIL and it is imperative that continuous investment is made in logistics infrastructure

The progress of new railway line projects related to coal evacuation have not achieved the desired progress in the last few years (Tori-Shivpur-Hazaribagh, Angul-Kalinga, Gopalpur-Manoharpur,

Non-availability of sufficient number of railway rakes CCL , MCL & BCCL are particularly

facing the problems in dispatch of coal and increasing coal inventory levels

Forestry/ Environment

Clearance

Identification of Projects

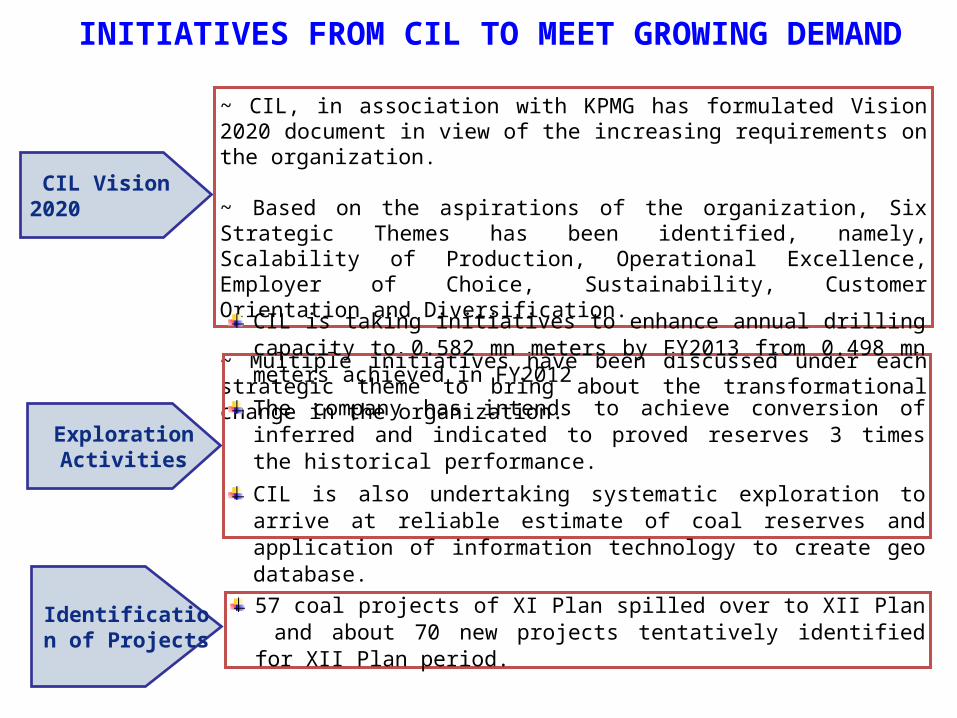

57 coal projects of XI Plan spilled over to XII Plan and about 70 new projects tentatively identified for XII Plan period.

CIL Vision 2020

~ CIL, in association with KPMG has formulated Vision 2020 document in view of the increasing requirements on the organization.

~ Based on the aspirations of the organization, Six Strategic Themes has been identified, namely, Scalability of Production, Operational Excellence, Employer of Choice, Sustainability, Customer Orientation and Diversification.

~ Multiple initiatives have been discussed under each strategic theme to bring about the transformational change in the organization.

Exploration Activities

CIL is taking initiatives to enhance annual drilling capacity to 0.582 mn meters by FY2013 from 0.498 mn meters achieved in FY2012

The company has intends to achieve conversion of inferred and indicated to proved reserves 3 times the historical performance.

CIL is also undertaking systematic exploration to arrive at reliable estimate of coal reserves and application of information technology to create geo database.

INITIATIVES FROM CIL TO MEET GROWING DEMAND

Initiatives continued…

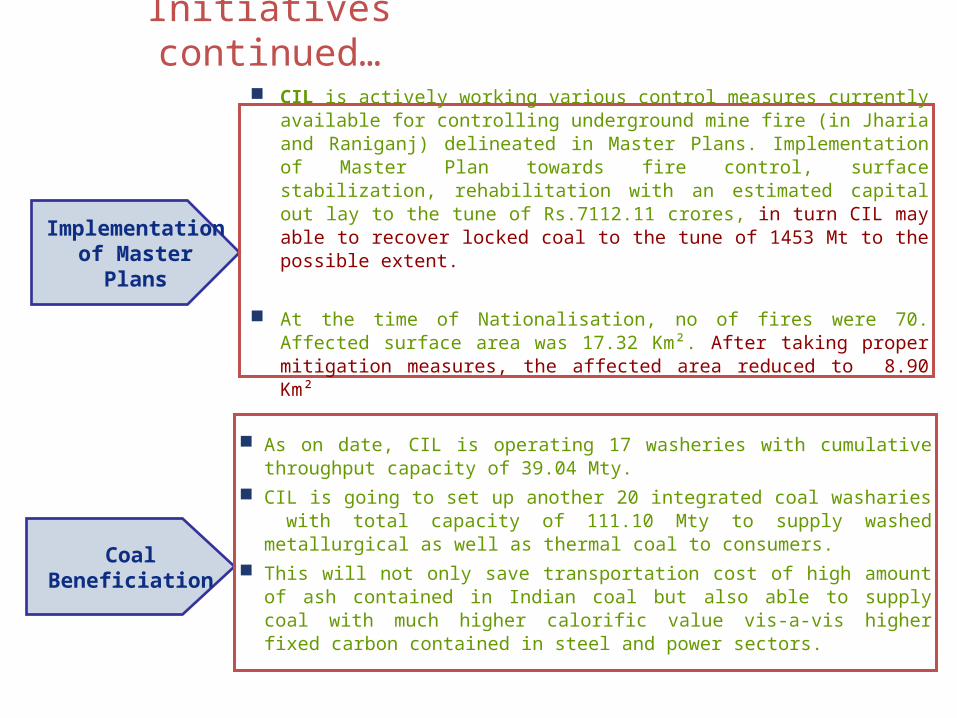

Implementation of Master Plans

CIL is actively working various control measures currently available for controlling underground mine fire (in Jharia and Raniganj) delineated in Master Plans. Implementation of Master Plan towards fire control, surface stabilization, rehabilitation with an estimated capital out lay to the tune of Rs.7112.11 crores, in turn CIL may able to recover locked coal to the tune of 1453 Mt to the possible extent.

At the time of Nationalisation, no of fires were 70. Affected surface area was 17.32 Km². After taking proper mitigation measures, the affected area reduced to 8.90 Km²

Coal Beneficiation

As on date, CIL is operating 17 washeries with cumulative throughput capacity of 39.04 Mty.

CIL is going to set up another 20 integrated coal washaries with total capacity of 111.10 Mty to supply washed metallurgical as well as thermal coal to consumers.

This will not only save transportation cost of high amount of ash contained in Indian coal but also able to supply coal with much higher calorific value vis-a-vis higher fixed carbon contained in steel and power sectors.

TECHNICAL CHALLENGES

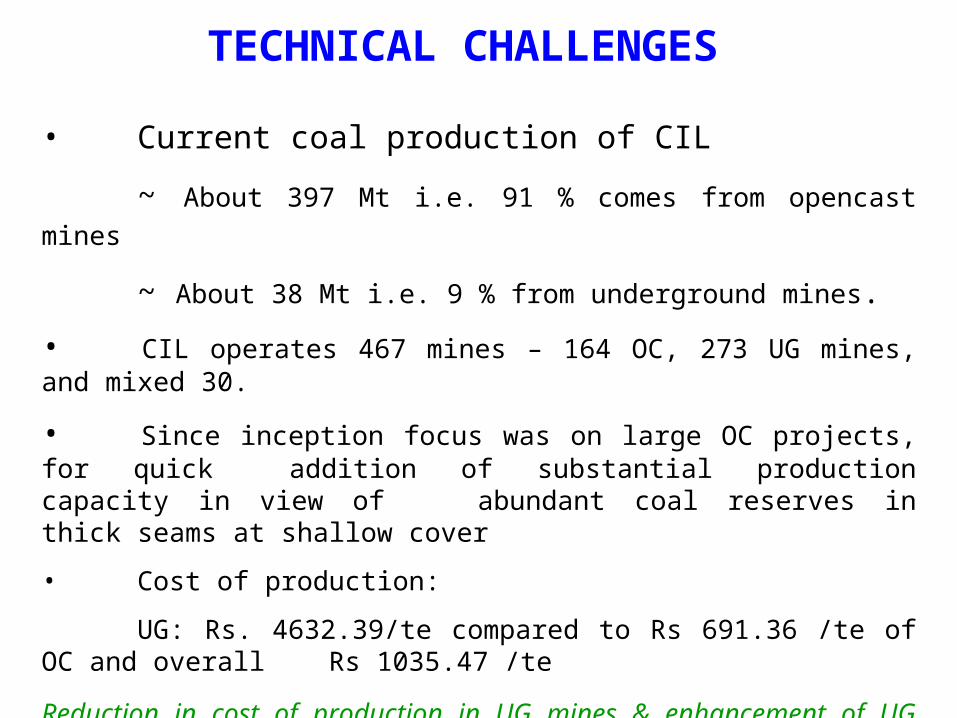

• Current coal production of CIL

~ About 397 Mt i.e. 91 % comes from opencast mines

~ About 38 Mt i.e. 9 % from underground mines.

• CIL operates 467 mines – 164 OC, 273 UG mines, and mixed 30.

• Since inception focus was on large OC projects, for quick addition of substantial production capacity in view of

abundant coal reserves in thick seams at shallow cover

• Cost of production:

UG: Rs. 4632.39/te compared to Rs 691.36 /te of OC and overall Rs 1035.47 /te

Reduction in cost of production in UG mines & enhancement of UG production is a challenge for CIL

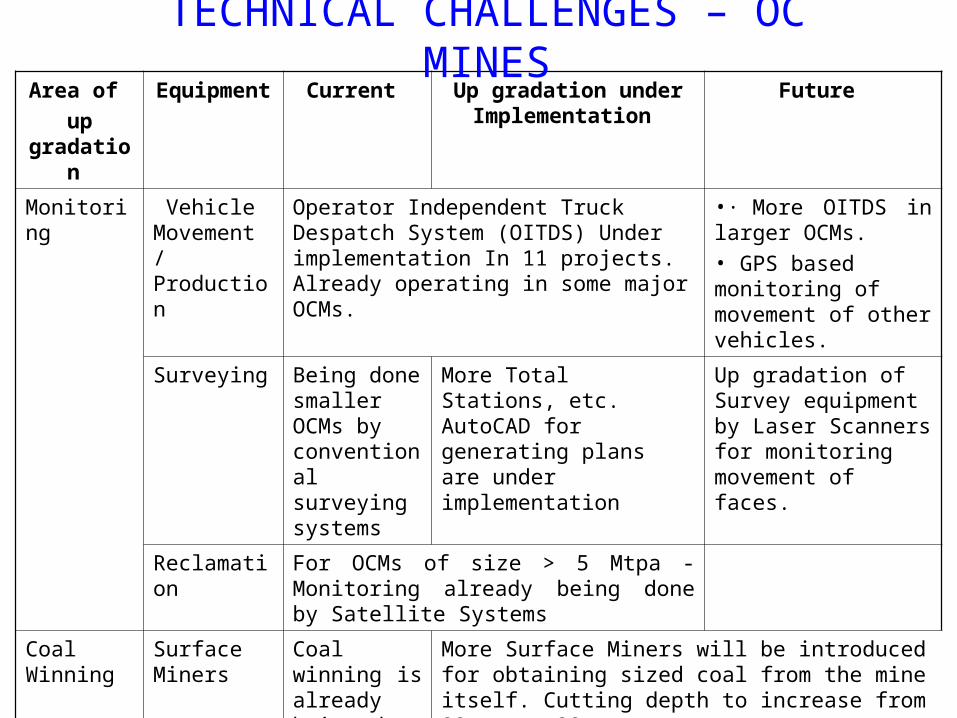

TECHNICAL CHALLENGES – OC MINES

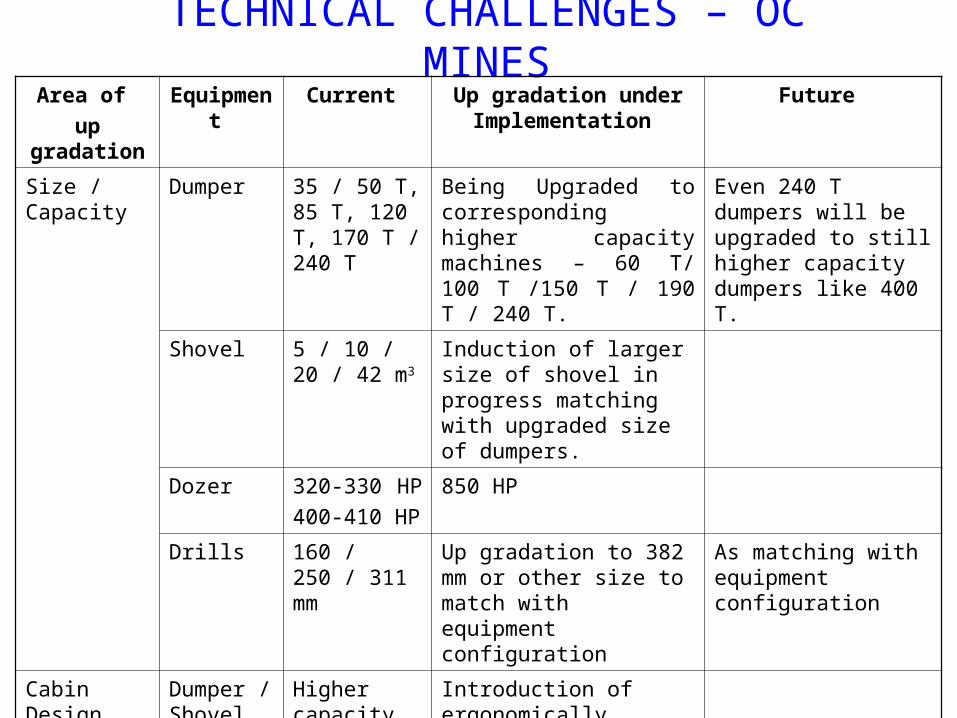

Area of up gradation

Equipment Current Up gradation under Implementation

Future

Size / Capacity

Dumper 35 / 50 T, 85 T, 120 T, 170 T / 240 T

Being Upgraded to corresponding higher capacity machines – 60 T/ 100 T /150 T / 190 T / 240 T.

Even 240 T dumpers will be upgraded to still higher capacity dumpers like 400 T.

Shovel 5 / 10 / 20 / 42 m3

Induction of larger size of shovel in progress matching with upgraded size of dumpers.

Dozer 320-330 HP 400-410 HP

850 HP

Drills 160 / 250 / 311 mm

Up gradation to 382 mm or other size to match with equipment configuration

As matching with equipment configuration

Cabin Design Dumper / Shovel

Higher capacity machines/ equipment are fitted with AC & ergonomic seats.

Introduction of ergonomically designed AC cabins with on screen gadget monitoring systems

Area of up

gradation

Equipment Current Up gradation under Implementation

Future

Monitoring Vehicle Movement / Production

Operator Independent Truck Despatch System (OITDS) Under implementation In 11 projects. Already operating in some major OCMs.

•· More OITDS in larger OCMs. • GPS based monitoring of movement of other vehicles.

Surveying Being done smaller OCMs by conventional surveying systems

More Total Stations, etc. AutoCAD for generating plans are under implementation

Up gradation of Survey equipment by Laser Scanners for monitoring movement of faces.

Reclamation For OCMs of size > 5 Mtpa - Monitoring already being done by Satellite Systems

Coal Winning

Surface Miners

Coal winning is already being done by SMs in a no. of mines

More Surface Miners will be introduced for obtaining sized coal from the mine itself. Cutting depth to increase from 22 mm to 38 mm

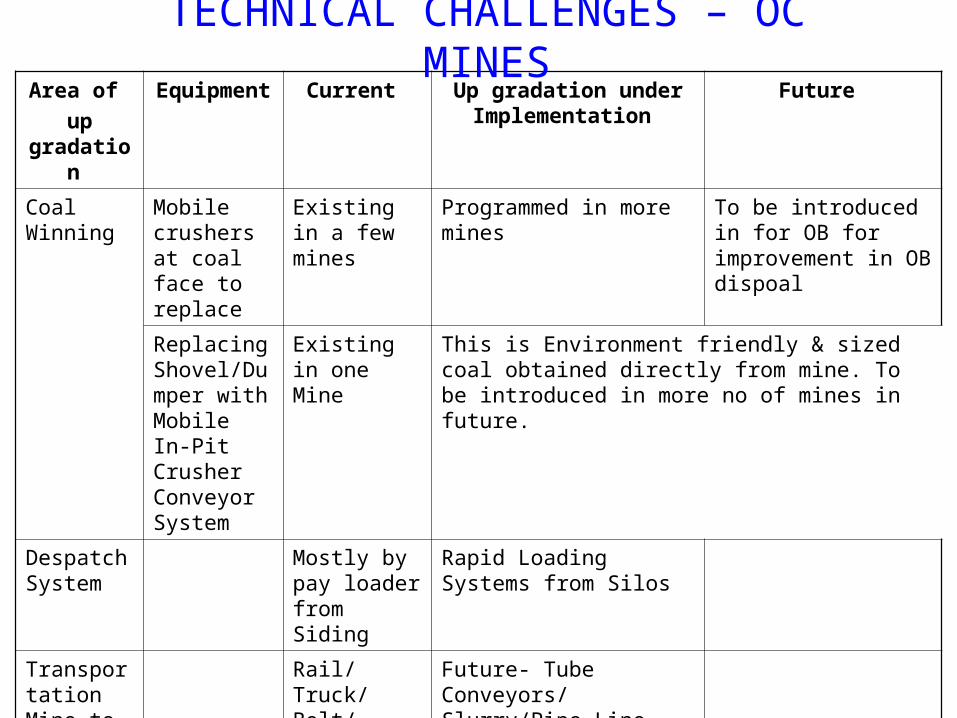

TECHNICAL CHALLENGES – OC MINES

Area of up

gradation

Equipment Current Up gradation under Implementation

Future

Coal Winning

Mobile crushers at coal face to replace

Existing in a few mines

Programmed in more mines To be introduced in for OB for improvement in OB dispoal

Replacing Shovel/Dumper with Mobile In-Pit Crusher Conveyor System

Existing in one Mine

This is Environment friendly & sized coal obtained directly from mine. To be introduced in more no of mines in future.

Despatch System

Mostly by pay loader from Siding

Rapid Loading Systems from Silos

Transportation Mine to End User

Rail/Truck/Belt/Conveyors

Future- Tube Conveyors/ Slurry/Pipe Line Transportation

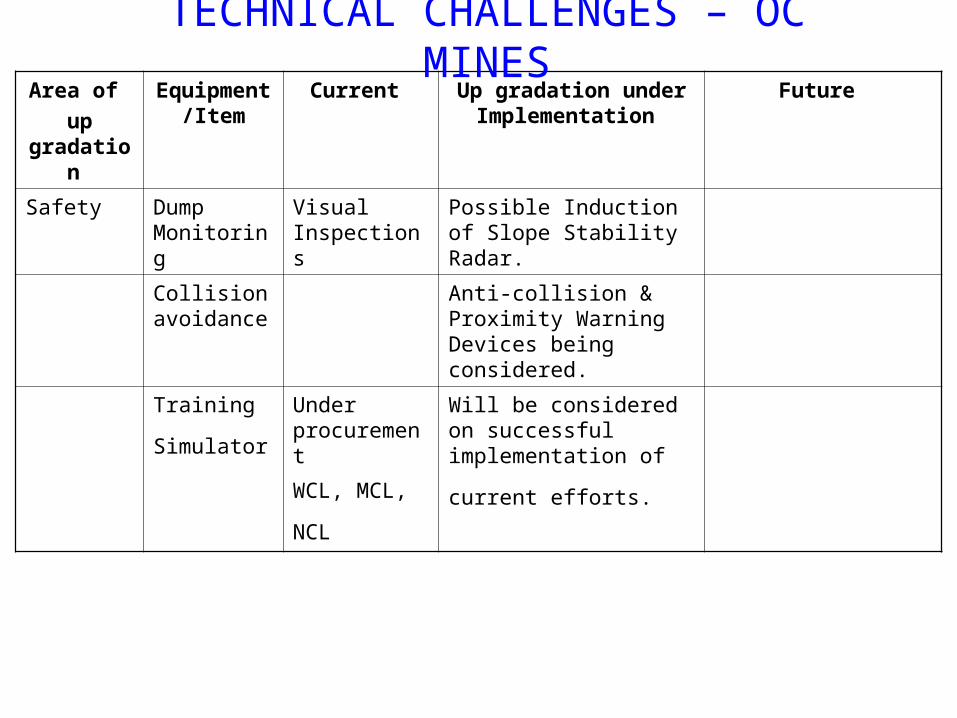

TECHNICAL CHALLENGES – OC MINES

Area of up

gradation

Equipment /Item

Current Up gradation under Implementation

Future

Safety Dump Monitoring

Visual Inspections

Possible Induction of Slope Stability Radar.

Collision avoidance

Anti-collision & Proximity Warning Devices being considered.

Training

Simulator Under procurement

WCL, MCL, NCL

Will be considered on successful implementation

of current efforts.

TECHNICAL CHALLENGES – OC MINES

Area of up

gradation

Equipment /Item

Current Up gradation under Implementation

Future

Mechanised Mining

Powered Support Long wall systems

In a few mines Being planned in more mines on turn-key on basis with OEMs

Shall be introduced in more mines wherever geo-mining conditions permit

Short wall systems for extraction of developed pillars

Introduced in one mine

To be introduced in more mines if found techno-economically viable

Continuous

Miners (CM) Existing in a number of

mines

To be introduced in more no. of mines where geo-mining conditions permit

Shuttle cars to be replaced with flexible conveyors. Small size cutting /bolting equipment for thin seams

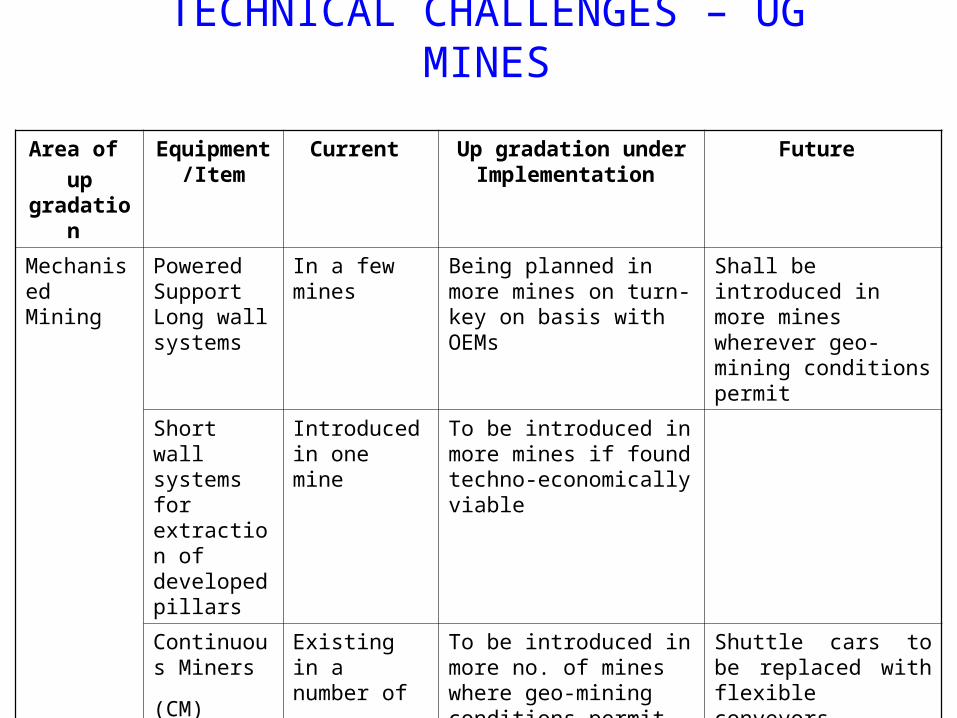

TECHNICAL CHALLENGES – UG MINES

Area of up

gradation

Equipment /Item

Current Up gradation under Implementation

Future

Mechanised Mining

Shaft Sinking / Drift Drivage

Conventional · Rapid Shaft Sinking Systems.Tunnel Borers for faster drift drivage

Man-Riding Systems

In operation in a number of mines

Under implementation in more mines

To be introduced in more extensive UG mines.

Man & Material Transportation

Multi-Utility Vehicles & Diesel Carts – Will be considered after DGMS approval.

Safety Strata

Monitoring Manually by

experience. Load Cells, Extensometers,

etc. On line Roof Behavior

Monitoring Systems Environmental

Systems Installed in a no. of highly gassy fiery mines

Gas chromatography for enhanced accuracy.

Tube Bundle technology

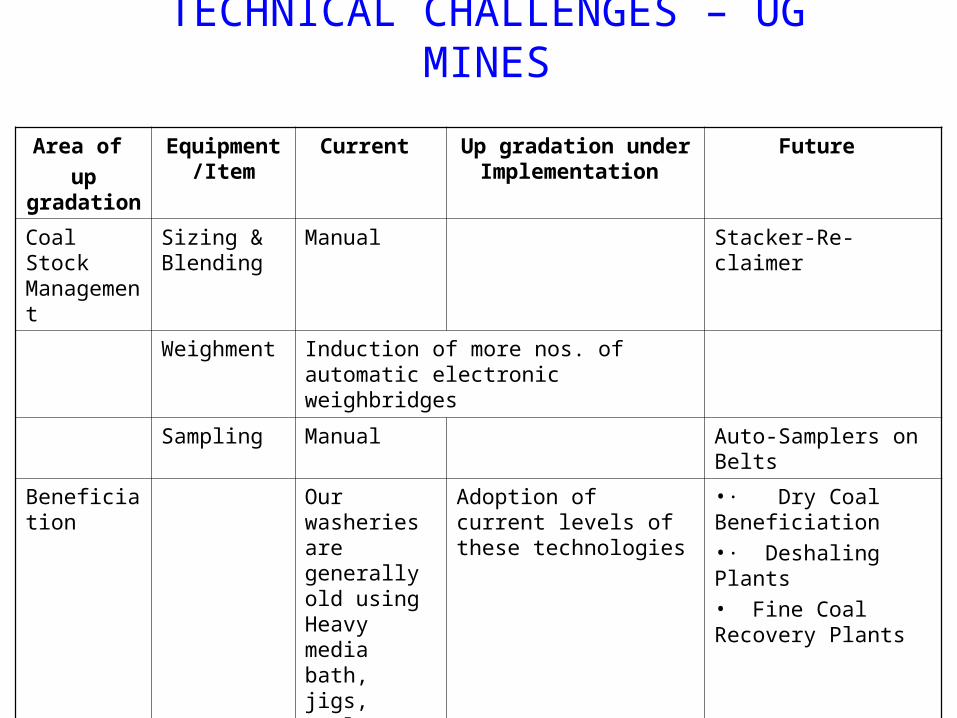

TECHNICAL CHALLENGES – UG MINES

Area of up gradation

Equipment /Item

Current Up gradation under Implementation

Future

Coal Stock Management

Sizing & Blending

Manual Stacker-Re-claimer

Weighment Induction of more nos. of automatic electronic weighbridges

Sampling Manual Auto-Samplers on Belts

Beneficiation Our washeries are generally old using Heavy media bath, jigs, cyclone, flotation

Adoption of current levels of these technologies

•· Dry Coal Beneficiation•· Deshaling Plants• Fine Coal Recovery Plants

TECHNICAL CHALLENGES – UG MINES

BUSINESS MODEL:• Equity Model

– Stake with off take contract in brown field assets

– 100% or majority stake in green field assets

• Off-take Model :

– Long term contract essentially with coal miners

– Short term contract

TARGET PRODUCTS & DESTINATIONS:

• Mozambique – Coking & thermal from own assets

• Indonesia - Thermal coal [ > 4000 kcal/kg (ARB)]

• South Africa - Thermal Coal [ > 5500 kcal/kg(ARB)]

• USA - Thermal Coal [ > 6000 kcal/kg(ARB)]

• Australia - Thermal Coal [ > 5500 kcal/kg(ARB)] 25

Foreign Acquisitions - Strategy Framework

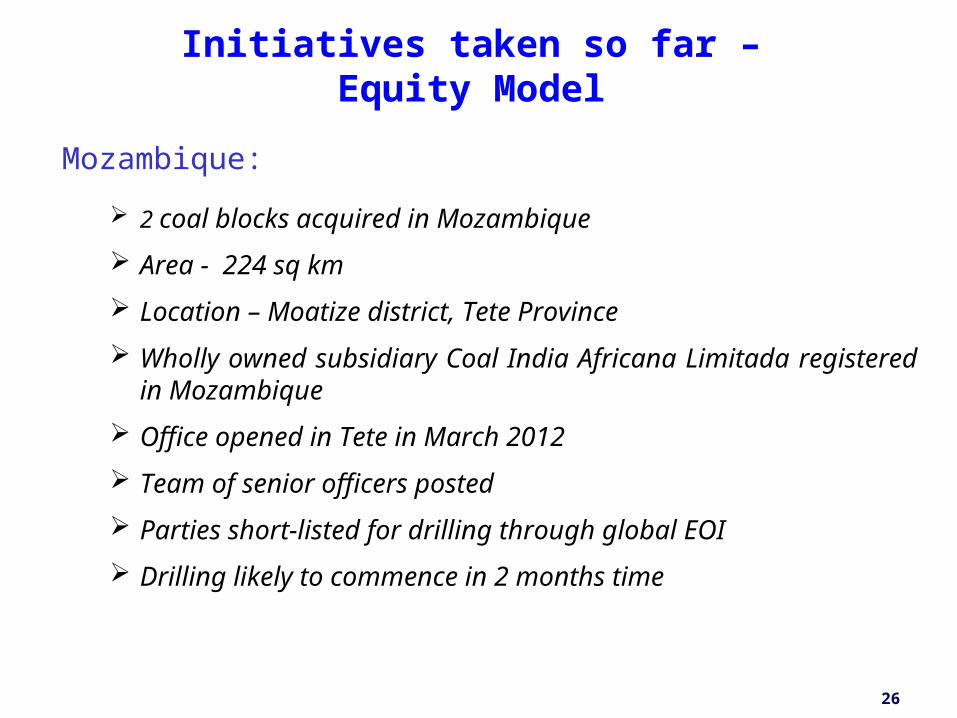

Mozambique:

2 coal blocks acquired in Mozambique

Area - 224 sq km

Location – Moatize district, Tete Province

Wholly owned subsidiary Coal India Africana Limitada registered in Mozambique

Office opened in Tete in March 2012

Team of senior officers posted

Parties short-listed for drilling through global EOI

Drilling likely to commence in 2 months time

26

Initiatives taken so far – Equity Model

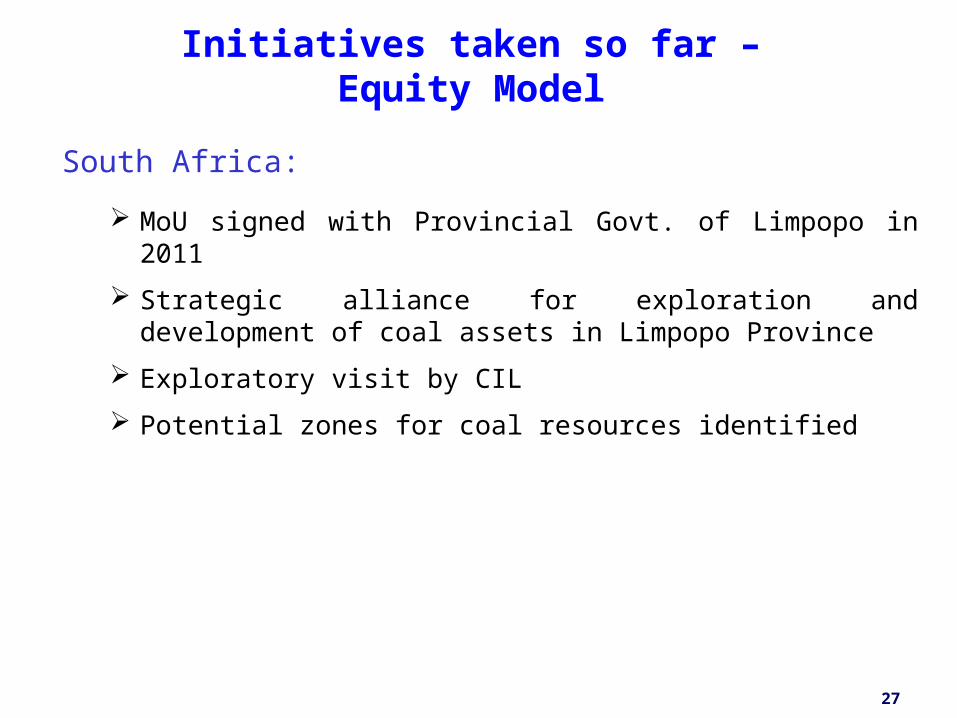

South Africa:

MoU signed with Provincial Govt. of Limpopo in 2011

Strategic alliance for exploration and development of coal assets in Limpopo Province

Exploratory visit by CIL

Potential zones for coal resources identified

27

Initiatives taken so far – Equity Model

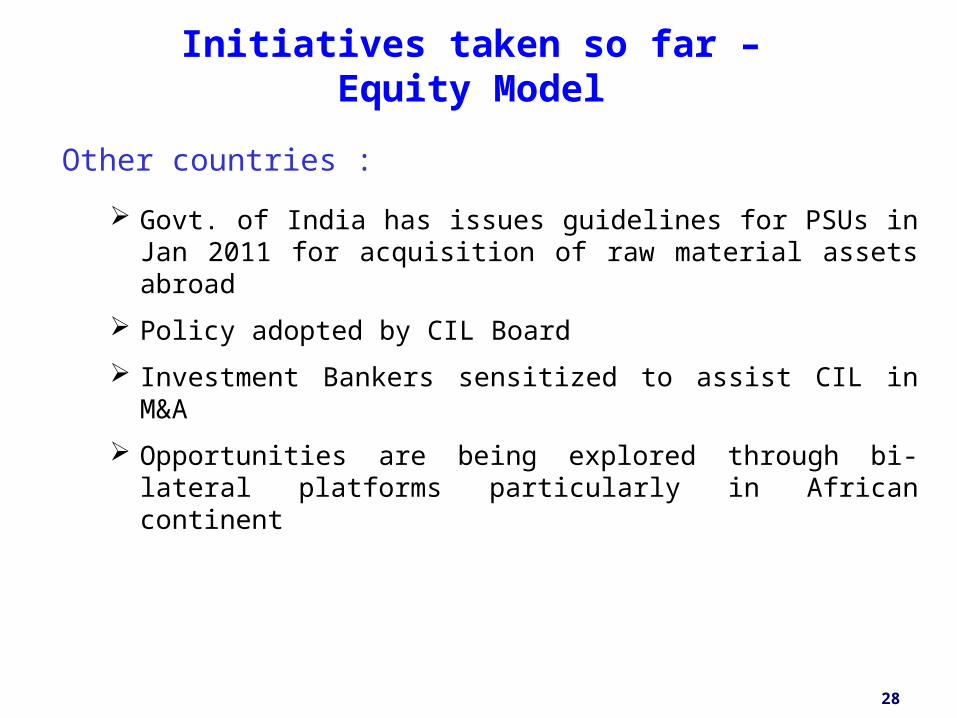

Other countries :

Govt. of India has issues guidelines for PSUs in Jan 2011 for acquisition of raw material assets abroad

Policy adopted by CIL Board

Investment Bankers sensitized to assist CIL in M&A

Opportunities are being explored through bi-lateral platforms particularly in African continent

28

Initiatives taken so far – Equity Model

THANK YOU