Embed Size (px)

Citation preview

Coal as a Market Driver for Port and Rail Infrastructure

DevelopmentAlok Shrivastava, MD&CEO, ICVL

Overview of ICVL in Mozambique

• International Coal Ventures Pvt. Limited (ICVL), an initiative of the Government of India, has

been carved out as a Joint Venture Company of the best Public Sector companies in the Steel,

Mining and Power sectors of India.

• It is headquartered in New Delhi, India.

• ICVL acquired the operating Benga coal mine and greenfield coal assets from Rio Tinto in

Mozambique, on 7th October, 2014 located at Moatize basin in Tete province.

• ICVL has acquired all the equity held by Rio Tinto in Riversdale Mining Limited (RML), Australia.

• A very large and strategic acquisition by ICVL for providing a long-term raw material and fuel

security to the promoter companies of ICVL.

• ICVL currently holds 6 Mining Concessions, in Tete province, to explore coal and other minerals

Current Projects – Benga Mine• Mine area is 7km by 1.5km, with a maximum planned depth of 500m

• An open-pit operation with a designed capacity of 5,3Mtpa RoM coalProduction

• Mining is by conventional methods with diesel hydraulic shovels andexcavators.

• Hard Coking Coal (HCC) and Thermal Coal (TC) products are being produced.

• ROM coal from the mine is transported to the Coal Handling & Preparation

• Both HCC and TC are being shipped to India for use by its promotercompanies

• Coal transportation and shipping network for 1.6 MTPA, that includes a CHPP(Throughput 5.3 MTPA) and a fleet of 15 Locos and 310 Wagons.

Current Projects – Benga Mine

• Logistics

• Moatize region is in the north western part of Mozambique; It is 450 Kmnorthwest of Port of Beira, 800 Km west of the port of Nacala and has theZambeze River flowing through it.

• HCC and TC from Benga mine are transported 580 Km to the Port of Beira viathe Sena railway line.

• Average nr of Trains per month - 40

Current Projects – Zambeze Project

• Development of an open-cut mine using conventional truck/shovelequipment to a maximum depth of 200m for the initial 20 year LoM,to feed the CHPP 22 Mtpa of RoM coal.

• Transportation of the coal through conveyor or railway from ZambezeCHPP to Benga CHPP, where load out of product will be at the Bengarail siding and from there to Port of Beira.

• ESIA studies concluded, under MITADER review

• RAP studies ongoing

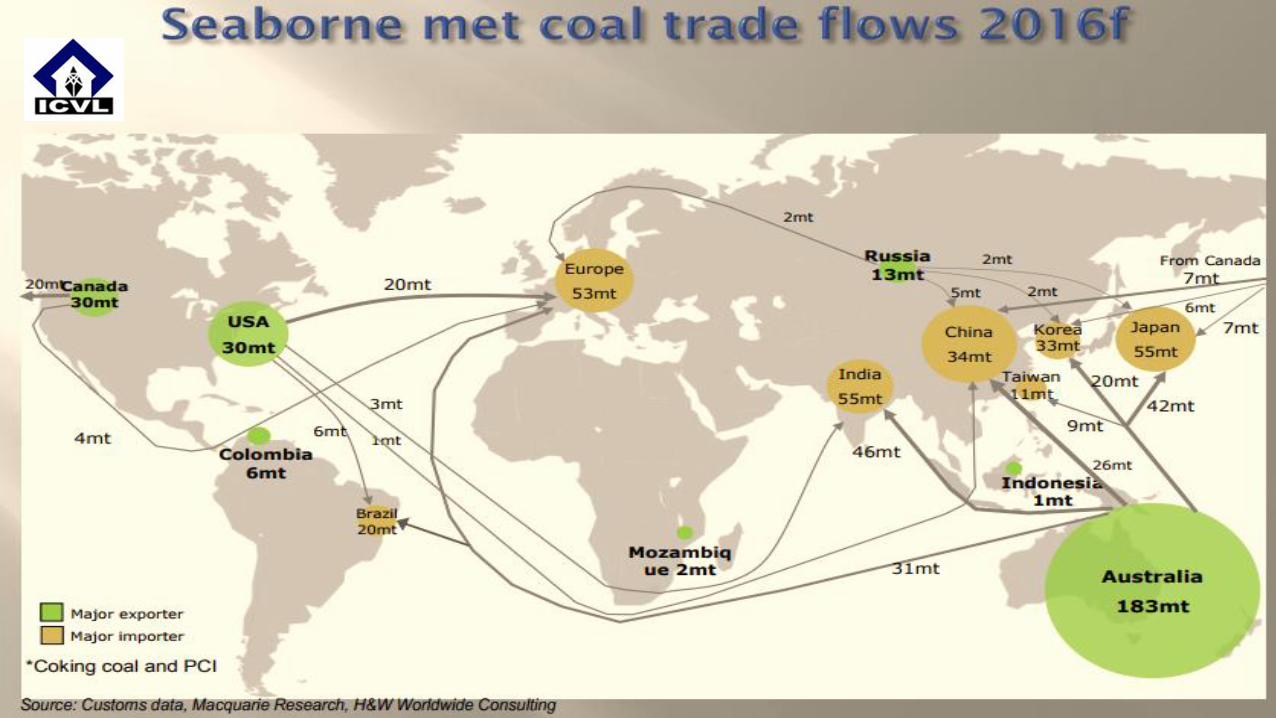

Coal - Future Demand Scenario

• Although over the period of time the percentage share of Coal use in total energyrequirement/power generation will decline. Quantity wise there will be marginal increase.

• While world coal consumption will start declining in China, US & EU but its consumption willsharply increase in India & other Asian countries. Coal consumption is also expected toincrease in Africa and in the Middle East.

Destination India

• Power Sector -India’s total coal based power generation will be around 1331.5 GW by 2026-27requiring 901 MT of coal. Power plants designed to use imported thermal coal will beimporting around 50 MT of coal. In addition to maintain the ash percentage power utilitieswill be importing coal for blending purpose.

• Steel Sector -India has projected its steel capacity as 300 MT by 2030-31. 60-65% of thisproduction will come through BF route. The projected coal demand for the steel sector at300 MT capacity will be 161 MT for coking coal and 136 MT for non coking coal.

Coal - Future Demand Scenario – Potential Within Africa• Limited access to power - Less than 30% of Africans have access to electricity and even those

connected to a power grid experience an average of 54 days of power outage a year – that’s darknessfor 15% of the year .

• Low per capita consumption of electricity & steel - Average electricity consumption in Africa (sub-Saharan), excluding South Africa, is only about 150 KWh/capita per year compared to a globalaverage of 7,000 KWh. The per capita steel consumption for Africa (excluding Egypt & South Africa) isonly 20 kg against the world consumption of 207.9 kg.

• Population growth & Increased urbanization – Africa by 2100 will become world’s most populousregion accounting for 39.94% (4468 million) of the world’s population compared to 16.16%(1256million) as on 2017.

• As on 2017 41% of Africa population is under the age of 15 another 19% is between the age of 15 to24. In future, Africa will have a young population thus a growing labour force a highly valuable asset inan gradually ageing world.

• Africa is still urbanizing and in future this increasing population will translate into world’s fastesturbanization rate. Over the next decade, it is expected that an additional 187 million Africanswill live in cities.

Opportunities for Mozambique Coal• To overcome and hedge themselves from this vulnerability, buyer’s of coking coal are interested in

developing alternate source of supply .

• Thus Mozambique coking coal has a ready overseas market (Like India/Japan). Thermal can also be

exported

• But to reap the export opportunities particularly in Coking Coal, Mozambique has to be price

competitive.

• Further infrastructure needed to be developed for mine to port connectivity & Capacity enhancement

at the port.

• Beside export option, huge opportunity exist internally both in African continent and Mozambique

itself.

• Mining company can use the thermal coal for power generation and this generated power can be used for

domestic consumption within Mozambique itself or it can be exported to Neighbouring countries or

countries across African continent.

Opportunities for Mozambique Coal

• Thermal coal can also be converted into Gas/Methanol. This will be of much interest toMozambique as well as to the coal miners as it will on one hand provide importsubstitute (alternative to petroleum based fuel) for Mozambique and on the other handwill give coal miner an alternate option for using their thermal coal.

• The Government of India has recently constituted a task force to explore the feasibility ofproducing methanol from coal at Mozambique and India, replacement of natural gas bycoal gas through gasification process in steel plants, and carbon dioxide capturing fromsteel plants into methanol liquid fuel.

• There can be a win-win situation when the coking coal from Mozambique isexported and the thermal coal is used for power generation or converted into methanolfor export or used as a alternative to petroleum based fuel within Mozambique.

Collectively we have to strive to make such a situation a reality

Some basic facts about Coal, its reserves, logistics and use in Steelmaking• About 1 billion ton of Metallurgical coal is used in global steel production which is

15% of total coal consumption worldwide.

• Coal and Iron Ore are the second and Third largest global traded commodity interms of volume of production, consumption and transportation globally justafter Crude oil which tops the list. Coal and Iron Ore are the basic inputs ofsteelmaking.

• Steel has the unique advantage that it is 100 % recyclable and reused infinitely.So the raw material invested in steel lasts far beyond the end of the life of thesteel product.

• Coal is actively mined in almost 70 countries globally. The biggestreserves are in US, China, Russia, Australia and India.

Some basic facts about Coal, its reserves,logistics and use in Steelmaking...continued

• Australia dominates Coking Coal exports accounting for 200 million tons out of 300 million tons of Coking Coal exported globally.

• About 30% of coal can be saved by injecting fine coal particles into the blast furnace. (Pulverised Coal Injection route technology).

Logistics asociated with Steelmaking

• To make 1 ton of crude steel, requirement is 1.4 ton of Iron Ore, 0.8ton of Coal, 0.3 ton of limestone and 0.1 ton of recycled steel.

• So the input logistic requirement is 2.5 times the output. Input andOutput logistics combined comes to 3.5 tons.

• This logistics get multiplied due to rail, road and shipping involved inmost logistic chains.

• The cascading effect of logistics come from the involvement ofvendors, suppliers, ancillary facilities, employees, customers, socialinfrastructure and the vast universe of steel end users like vehicles,roads, bridges, pipelines, housing and other social infrastructure etc.

Primary supply chain bottlenecks of coal• Adverse weather conditions.

• Far-off geographical location of mining areas.

• Capacity and location of ports and railway infrastructure.

• Price volatility due to temporary shortage/ surplus beyond market fundamentals.

Local Content Projects• The development of any project requires all types of suppliers (locals

and foreigns) of materials, equipments, labour, services, etc.

• It´s ICVL strategy to use as most as it is available, local suppliers andservice providers and currently we´ve awarded the followingcontracts for local companies:• HR

• Audit

• Logistics

• Mining Extraction

• ESIA/RAP Studies

• Environmental Monitoring

Thank You