Embed Size (px)

DESCRIPTION

Cmta Provision

Citation preview

1

CTMA-TCCP-RKC CORRELATION MATRIX AND RATIONALE OF AMENDMENTS

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

TITLE 1. PRELIMINARY PROVISIONS

CHAPTER 1. SHORT TITLE

SECTION 100. Short Title. This Act shall be known as the

“Customs and Tariff Modernization Act of 2008”.

New title

CHAPTER 2. GENERAL AND COMMON PROVISIONS New Chapter. The idea of a “general

and common provisions” is to be able

to reflect as basic customs policy the

standards mandated in the General

Annex of the RKC with which national

legislation is yet to be compliant.

Some standards with which current

national legislation/regulation is

compliant were no longer introduced

here.

SEC. 101. Declaration of Policy.

It is the declared policy of the State to promote and secure

international trade, protect government revenue, and

modernize customs and tariff administration by:

Developing and implementing programs aimed at

continuously improving customs systems and processes;

Adopting customs policies, rules, and procedures that are

clear, transparent, and consistent with international

agreements and customs best practices;

Establishing a regime of informed compliance for customs

stakeholders by providing easy access to all public

information, not otherwise confidential and for customs use

only, regarding Customs laws, rules and regulations,

administrative policies and guidelines, procedures and

practices that would enable them to fulfill their obligation to

exercise due diligence in dealing with customs;

RKC Preamble and proposed provisions to

reflect other mandate / function of BOC

New provision

2

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

Consulting and cooperating, wherever appropriate, with other

government agencies, and the private sector in customs

policy development and implementation;

Providing parties aggrieved by customs action and/or decision

with administrative and judicial appellate remedy;

Utilizing modern techniques in customs administration such as

risk management and post clearance-based controls, and

maximizing the use of information and communication

technology in carrying out the mandate of customs.

SEC. 102. Definition of Terms.

As used in this Code:

“ADMISSION” refers to the act of bringing imported articles

into free zone or non-customs territory directly or through

transit.

“Airway Bill (AWB)” is a transport document for airfreight used

by airlines and international freight forwarders. The holder or

consignee of the bill has the right to claim delivery of the

goods when they arrive at the port of destination. It is a

contract of carriage that includes carrier conditions, such as

limits of liability and claims procedures. In addition, it contains

transport instructions to airlines and carriers, a description of

the article, and applicable transportation charges.

“Appeal” means the act by which a person who is aggrieved

by ANY ACT, decision, ORDER or omission of Customs,

seeks redress before the Bureau of Customs, the Secretary

of Finance, or competent court, as the case may be.

"Articles" when used with reference to importation or

exportation, includes goods, wares and merchandise and in

general anything that may be made the subject of importation

or exportation.

“Assessment” means the process of determining the amount

of duties and taxes and other charges due on imported

SEC 3519 Words and Phrases Defined. - As used in this Code:

"Foreign Port" means a port or place outside the jurisdiction of

the Philippines.

"Port of Entry" is a domestic port open to both foreign and

coastwise trade. The term includes principal ports of entry and

subports of entry. A "principal port of entry” is the chief port of

entry of the collection district wherein it is situated and is the

permanent station of the Collector of such port. Subports of

entry are under the administrative jurisdiction of the Collector of

the principal port of entry of the district. Whenever the term

"Port of Entry" is used herein, it shall include “airport of entry”.

"Coastwise ports" are such domestic ports as are open to

coastwise trade only. These include all ports, harbors and

places not ports of entry.

"Vessels" includes every sort of boat, craft or other artificial

contrivance used, or capable of being used, as a means of

transportation on water.

"Aircraft" includes any weight -carrying devise or structure for

the navigation of the air.

"Bill of Lading" includes airway bill of lading.

"Articles", when used with reference to importation or

exportation, includes goods merchandise and in general

Lifted from TCCP Section 3519, as revised

and the RKC definition of terms

The terms included in this section are

based on those in the TCCP and on

the RKC.

3

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

articles.

“Bill of Lading (B/L)" is a transport document for ocean freight

issued by shipping lines, carriers AND INTERNATIONAL

FREIGHT FORWARDERS OR NON VESSEL OPERATING

COMMON CARRIER. The holder or consignee of the bill has

the right to claim delivery of the goods when they arrive at the

port of destination. It is a contract of carriage that includes

carrier conditions, such as limits of liability and claims

procedures. In addition, it contains transport instructions to

shipping lines and carriers, a description of the article, and

applicable transportation charges.

“Breakbulk” is non-containerized cargo which is grouped or

consolidated for shipment and broken down or sub-divided

INTO UNITIZED CARGO, SUCH AS IN PALLETS, OR

PACKED IN BAGS OR BOXES.

“Carrier” means the person actually transporting goods or in

charge of or responsible for the operation of the means of

transport.

“Checking the GOODS declaration” means the action taken

by customs to satisfy themselves that the GOODS declaration

is correctly made out and that the supporting documents

required fulfill the prescribed conditions for lodgment.

“Clearance” means the accomplishment of the customs

formalities necessary to allow goods to enter for home use,

warehousing, transit or transshipment, or to be exported or

placed under another customs procedure.

"Coastwise ports" are such domestic ports as are open to

coastwise trade only. These include all ports, harbors, and

places not ports of entry.

“Constructive import/export” shall refer to the movement of

imported goods to and from free zone and customs territory.

“CUSTOMS” SHALL MEAN THE BUREAU OF CUSTOMS.

anything that may be made the subject of importation or

exportation.

"Transit cargo" is article arriving at any port from another port

or place noted in the carrier's manifest and destined for

transshipment to another local port or to a foreign port.

"Seized property" means any property seized or held for the

satisfaction of any administrative fine or for the enforcement of

any forfeiture under the Tariff and Customs Code.

"Tariff and customs laws" includes not only the provisions of

this Code and regulations pursuant thereto but all other laws

and regulations which are subject to enforcement by the

Bureau of Customs or otherwise within its jurisdiction.

"Taxes" includes all taxes, fees and charges imposed by the

Bureau of Customs and the Bureau of Internal Revenue.

"Secretary" or "Department head" refers, unless otherwise

specified, to the Secretary of Finance.

"Commission” refers to the Tariff Commission.

"Person" whether singular or plural refers to an individual,

corporation, partnership, association company or any other

kind of organization.

"Dutiable value" refers to the value defined in section two

hundred one.

"Bulk cargo" refers to products in a mass of one commodity not

packaged, bundled, bottled or otherwise packed.

"Smuggling" is an act of any person who shall fraudulently

import or bring into the Philippines, or assist in so doing, any

article, contrary to law or shall receive, conceal, buy, sell or in

any manner facilitate the transportation, concealment, or sale

of such article after importation, knowing the same to have

been imported contrary to law. It includes the exportation of

articles in a manner contrary to law. Articles subject to this

4

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

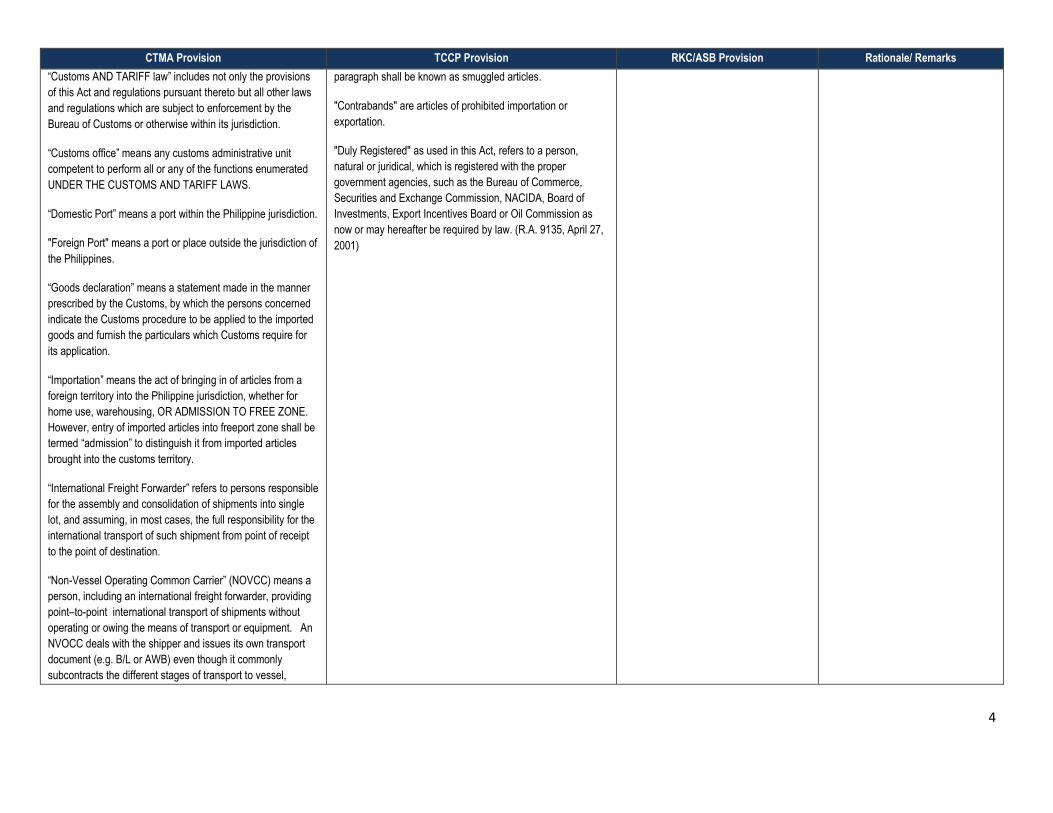

“Customs AND TARIFF law” includes not only the provisions

of this Act and regulations pursuant thereto but all other laws

and regulations which are subject to enforcement by the

Bureau of Customs or otherwise within its jurisdiction.

“Customs office” means any customs administrative unit

competent to perform all or any of the functions enumerated

UNDER THE CUSTOMS AND TARIFF LAWS.

“Domestic Port” means a port within the Philippine jurisdiction.

"Foreign Port" means a port or place outside the jurisdiction of

the Philippines.

“Goods declaration” means a statement made in the manner

prescribed by the Customs, by which the persons concerned

indicate the Customs procedure to be applied to the imported

goods and furnish the particulars which Customs require for

its application.

“Importation” means the act of bringing in of articles from a

foreign territory into the Philippine jurisdiction, whether for

home use, warehousing, OR ADMISSION TO FREE ZONE.

However, entry of imported articles into freeport zone shall be

termed “admission” to distinguish it from imported articles

brought into the customs territory.

“International Freight Forwarder” refers to persons responsible

for the assembly and consolidation of shipments into single

lot, and assuming, in most cases, the full responsibility for the

international transport of such shipment from point of receipt

to the point of destination.

“Non-Vessel Operating Common Carrier” (NOVCC) means a

person, including an international freight forwarder, providing

point–to-point international transport of shipments without

operating or owing the means of transport or equipment. An

NVOCC deals with the shipper and issues its own transport

document (e.g. B/L or AWB) even though it commonly

subcontracts the different stages of transport to vessel,

paragraph shall be known as smuggled articles.

"Contrabands" are articles of prohibited importation or

exportation.

"Duly Registered" as used in this Act, refers to a person,

natural or juridical, which is registered with the proper

government agencies, such as the Bureau of Commerce,

Securities and Exchange Commission, NACIDA, Board of

Investments, Export Incentives Board or Oil Commission as

now or may hereafter be required by law. (R.A. 9135, April 27,

2001)

5

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

aircraft, and truck operators.

"Port of Entry" is a domestic port open to both foreign and

coastwise trade. The term includes principal ports of entry

and subports of entry. A "principal port of entry” is the chief

port of entry of the collection district wherein it is situated and

is the permanent station of the Collector of such port.

Subports of entry are under the administrative jurisdiction of

the Collector of the principal port of entry of the district.

Whenever the term "Port of Entry" is used herein, it shall

include “airport of entry”.

“Release of goods” means the action by Customs to permit

goods undergoing clearance to be placed at the disposal of

the PERSON CONCERNED.

“Refund” means the return, in whole or in part, of duties and

taxes paid on goods.

“Remission” means the reduction or dimunition, in whole or in

part, of duties and taxes where payment has not been made;

the term remission is synonymous with abatement.

“Security” REFERS TO ANY FORM OF GUARANTY, E.G.,

SURETY BOND, CASH BOND, STANDBY LETTER OF

CREDIT, IRREVOCABLE LETTER OF CREDIT, which

ensures the satisfaction of an obligation to Customs.

"Smuggling" is an act of any person who shall fraudulently

import or bring into the Philippines, or assist in so doing, any

article, contrary to law or KNOWING THE ARTICLE TO HAVE

BEEN IMPORTED CONTRARY TO LAW shall receive,

conceal, buy, sell, DISPOSE or in any manner, facilitate the

transportation, concealment, PURCHASE, sale OR

DISPOSITION of such article after importation.[ It includes

the exportation of articles in a manner contrary to law.

Articles subject to this paragraph shall be known as smuggled

article.

"Taxes" includes all taxes, fees and charges imposed by THE

NATIONAL INTERNAL REVENUE CODE and collected by

6

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

the Bureau of Customs.

“Transit” means the customs procedure under which goods

are transported under customs control from one customs

office to another or to a free zone.

“Transshipment” means the customs procedure under which

goods are transferred under customs control from the

importing means of transport to the exporting means of

transport within the area of one customs office which is the

office of both importation and exportation.

SEC. 103. When Importation Begins and Deemed

Terminated.

Importation begins when the carrying vessel or aircraft enters

the jurisdiction of the Philippines with intention to unlade

therein. Importation is deemed terminated upon payment of

duties, taxes and other charges due upon the articles, or

secured to be paid, at a port of entry and the legal permit for

withdrawal shall have been granted, or in case said articles

are free of duties, taxes and other charges, until they have

legally left the jurisdiction of the customs.

SEC 1202 When Importation Begins and Deemed Terminated.

- Importation begins when the carrying vessel or aircraft enters

the jurisdiction of the Philippines with intention to unlade

therein. Importation is deemed terminated upon payment of

duties, taxes and other charges due upon the articles, or

secured to be paid, at a port of entry and the legal permit for

withdrawal shall have been granted, or in case said are free of

duties, taxes and other charges, until they have legally left the

jurisdiction of the customs.

En toto

SEC. 104. COMPETENT CUSTOMS OFFICES.

FOR ADMINISTRATIVE PURPOSES, THE PHILIPPINES

SHALL BE DIVIDED INTO AS MANY COLLECTION

DISTRICTS AS NECESSARY, THE RESPECTIVE LIMITS

OF WHICH MAY BE CHANGED FROM TIME TO TIME BY

THE COMMISSIONER OF CUSTOMS UPON THE

APPROVAL OF THE SECRETARY OF FINANCE. THE

LOCATION, STAFF COMPETENCIES AND BUSINESS

HOURS OF THESE OFFICES SHALL TAKE INTO

ACCOUNT THE PARTICULAR REQUIREMENTS OF

TRADE.

SEC 701 Collection Districts and Ports of Entry Thereof. - For

administrative purposes, the Philippines shall be divided into as

many collection districts as necessary, the respective limits of

which may be changed from time to time by the Commissioner

of Customs upon approval of the Secretary of Finance. The

principal ports of entry for the respective collection districts

shall be Manila, Manila International Container Port, Ninoy

Aquino International Airport, Cebu, Iloilo, Davao, Tacloban,

Zamboanga, Cagayan de Oro, Surigao, Legaspi, Batangas,

San Fernando, and Subic.

RKC GA Standard 3.1, 3.2, 3.3, 3.4, 3.5

3.1. Standard

The Customs shall designate the Customs

offices at which goods may be produced

or cleared. In determining the competence

and location of these offices and their

hours of business, the factors to be taken

into account shall include in particular the

requirements of the trade.

3.2. Standard

At the request of the person concerned

and for reasons deemed valid by the

Customs, the latter shall, subject to the

First part of sentence taken from Sec

701 the rest is based on RKC.

7

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

availability of resources, perform the

functions laid down for the purposes of a

Customs procedure and practice outside

the designated hours of business or away

from Customs offices. Any expenses

chargeable by the Customs shall be

limited to the approximate cost of the

services rendered.

3.3. Standard

Where Customs offices are located at a

common border crossing, the Customs

administrations concerned shall correlate

the business hours and the competence of

those offices.

3.4. Transitional Standard

At common border crossings, the Customs

administrations concerned shall, whenever

possible, operate joint controls.

3.5. Transitional Standard

Where the Customs intend to establish a

new Customs office or to convert an

existing one at a common border crossing,

they shall, wherever possible, co-operate

with the neighbouring Customs to

establish a juxtaposed Customs office to

facilitate joint controls.

SEC. 105. Owner of Imported Articles.

All articles Imported into the Philippines shall be held to be the

property of the person to whom the same are consigned and

the holder of a bill of lading OR AIRWAY BILL duly endorsed

by the consignee therein named, or, if consigned to order, by

the consignor, shall be deemed the consignee thereof.

SEC 1203 Owner of Imported Articles. - All articles Imported

into the Philippines shall be held to be the property of the

person to whom the same are consigned: and the holder of a

bill of lading duly endorsed by the consignee therein named,

or, if consigned to order, by the consignor, shall be deemed the

consignee thereof. The underwriters of abandoned articles and

the salvors of articles saved from wreck at sea, a coast or in

any area of the Philippines may be regarded as the

RKC GA Standard 8.1

8.1. Standard

Persons concerned shall have the choice

of transacting business with the Customs

either directly or by designating a third

The words “or airway bill” inserted to

complete reference document type.

8

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

The underwriters of abandoned articles and the salvors of

articles saved from wreck at sea, a coast or in any area of the

Philippines may be regarded as the consignees.

consignees. party to act on their behalf.

SEC. 106. Liability of Importer for Duties AND TAXES

Unless relieved by laws or regulations, the liability for duties,

taxes, fees and other charges attaching on importation

constitutes a personal debt due from the importer to the

government which can be discharged only by payment in full

of all duties, taxes, fees and other charges legally accruing. It

also constitutes a lien upon the articles imported which may

be enforced while such articles are in custody or subject to the

control of the government.

SEC 1204 Liability of Importer for Duties. - Unless relieved by

laws or regulations, the liability for duties, taxes, fees and other

charges attaching on importation constitutes a personal debt

due fro¬m the importer to the government which can be

discharged only by payment in full of all duties, taxes, fees and

other charges legally accruing. It also constitutes a lien upon

the articles imported which may be enforced while such articles

are in custody or subject to the control of the government.

RKC GA Standard 4.7

4.7. Standard

National legislation shall specify the

person(s) responsible for the payment of

duties and taxes.

Minor amendment on the title. “AND

TAXES” is added to make the

definition of liability more complete.

SEC. 107. Importations by the Government.

Except those provided for in Section 800 of this ACT, all

importations by the Government for its own use or that of its

subordinate branches or instrumentalities, or corporations,

agencies or instrumentalities owned or controlled by the

government shall be subject to the duties, taxes, fees and

other charges provided for in this ACT.

SEC 1205 Importations by the Government. - Except those

provided for in Section One Hundred and Five of this Code, all

importations by the Government for its own use or that of its

subordinate branches or instrumentalities, or corporations,

agencies or instrumentalities owned or controlled by the

government shall be subject to the duties, taxes, fees and

other charges provided for in this code.

En toto

SEC. 108. DECLARANT.

A DECLARANT IS A PERSON WHO MAKES AND SUBMITS

TO CUSTOMS GOODS DECLARATION OR IN WHOSE

NAME SUCH DECLARATION IS MADE. ANY PERSON

HAVING THE RIGHT TO DISPOSE OF THE GOODS SHALL

BE ENTITLED TO DIRECTLY ACT AS DECLARANT.

HOWEVER, WHEN HE AUTHORIZES AN AGENT TO MAKE

THE DECLARATION IN HIS BEHALF, HE CAN ONLY DO

SO THROUGH AN ACCREDITED CUSTOMS BROKER

EXCEPT IN CASE WHEN THE DECLARANT IS A

JURIDICAL PERSON IN WHICH CASE IT MAY AUTHORIZE

ITS EMPLOYEE OR OFFICER TO MAKE THE

DECLARATION IN BEHALF OF THE JURIDICAL PERSON.

See RA9280 (Customs Brokers’ Act) RKC Definition; RKC GA Standard 3.6 and

3.7

The declarant

(a) Persons entitled to act as declarant

3.6. Standard

National legislation shall specify the

conditions under which a person is entitled

to act as declarant.

3.7. Standard

Any person having the right to dispose of

the goods shall be entitled to act as

New provision. Recommended

provision seeks to find a middle

ground between the clamor to limit

authority to make import/export

declaration to licensed customs

brokers (even to the exclusion of

consignee/owner) and the old law

allowing even third parties (atty-in-fact)

to make a declaration in behalf of

consignee/owner. The suggested

provision allows owner (person with

right to dispose of the goods) to

declare (including employee or officer

if person is a juridical entity) or he may

appoint a licensed customs broker to

make the declaration. Any other third

party will no longer be authorized to

9

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

declarant. make such declaration. This is

calculated to be compliant with the

RKC standard and at the same time to

give protection to the customs brokers’

profession by barring non-customs

broker to act as a declarant.

SEC. 109. RIGHTS AND RESPONSIBILITIES OF THE

DECLARANT.

THE PERSON HAVING THE RIGHT TO DISPOSE SHALL

BE RESPONSIBLE FOR THE ACCURACY OF THE

INFORMATION IN THE GOODS DECLARATION MADE

DIRECTLY OR THROUGH AN AGENT AND SHALL BE

LIABLE FOR THE DUTIES, TAXES AND OTHER CHARGES

DUE ON THE IMPORTED ARTICLE.

THE DECLARANT SHALL SIGN THE GOODS

DECLARATION PERSONALLY OR THROUGH AN

EMPLOYEE OR OFFICER IN CASE OF JURIDICAL

PERSON OR EVEN WHEN ASSISTED BY A LICENSED

CUSTOMS BROKER WHO SHALL LIKEWISE SIGN SAID

GOODS DECLARATION. THE DECLARATION SHALL BE

UNDER OATH UNDER THE PENALTIES OF

FALSIFICATION OR PERJURY THAT THE STATEMENTS

CONTAINED IN THE GOODS DECLARATION ARE TRUE

AND CORRECT. SUCH STATEMENTS UNDER OATH

SHALL CONSTITUTE A PRIMA FACIE EVIDENCE OF

KNOWLEDGE OR CONSENT OF THE VIOLATION OF ANY

APPLICABLE PROVISIONS OF THIS ACT WHEN THE

IMPORTATION IS FOUND TO BE UNLAWFUL.

BEFORE FILING OF THE GOODS DECLARATION, THE

DECLARANT MAY, UPON REQUEST IN WRITING, AND

FOR SUCH JUSTIFIABLE REASONS AND UNDER SUCH

CONDITIONS AS THE COMMISSIONER OF CUSTOMS

SHALL DETERMINE, BE ALLOWED TO INSPECT THE

GOODS AND TO DRAW SAMPLES FROM THE

IMPORTATION. THERE SHALL BE NO NEED FOR A

SEPARATE DECLARATION FOR THE SAMPLES

RKC Definition; RKC GA Standard 3.6,

3.7, 3.8, 3.9, 3.24

3.6. Standard

National legislation shall specify the

conditions under which a person is entitled

to act as declarant.

3.7. Standard

Any person having the right to dispose of

the goods shall be entitled to act as

declarant.

(b) Responsibilities of the declarant

3.8. Standard

The declarant shall be held responsible to

the Customs for the accuracy of the

particulars given in the Goods declaration

and the payment of the duties and taxes.

(c) Rights of the declarant

3.9. Standard

Before lodging the Goods declaration the

declarant shall be allowed, under such

conditions as may be laid down by the

Customs:

a. to inspect the goods; and

The provision defines clearly that the

importer as the declarant is the one

primarily responsible for the

truthfulness and accuracy of the

declaration made. The customs broker

is likewise liable for his declaration to

the extent of what he attests to as true

and accurate. A new provision

pursuant to RKC standard-- Declarant

under certain conditions has the right

to request for inspection and draw

sample before making a declaration.

Customs must provide rules and

regulations as to when and how to

avail to ensure against possible abuse.

10

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

WITHDRAWN UNDER CUSTOMS SUPERVISION

PROVIDED, THAT SUCH SAMPLES ARE INCLUDED IN

THE GOODS DECLARATION FOR THE PARTICULAR

CONSIGNMENT CONCERNED.

b. to draw samples.

SEC. 110. GOODS DECLARATION.

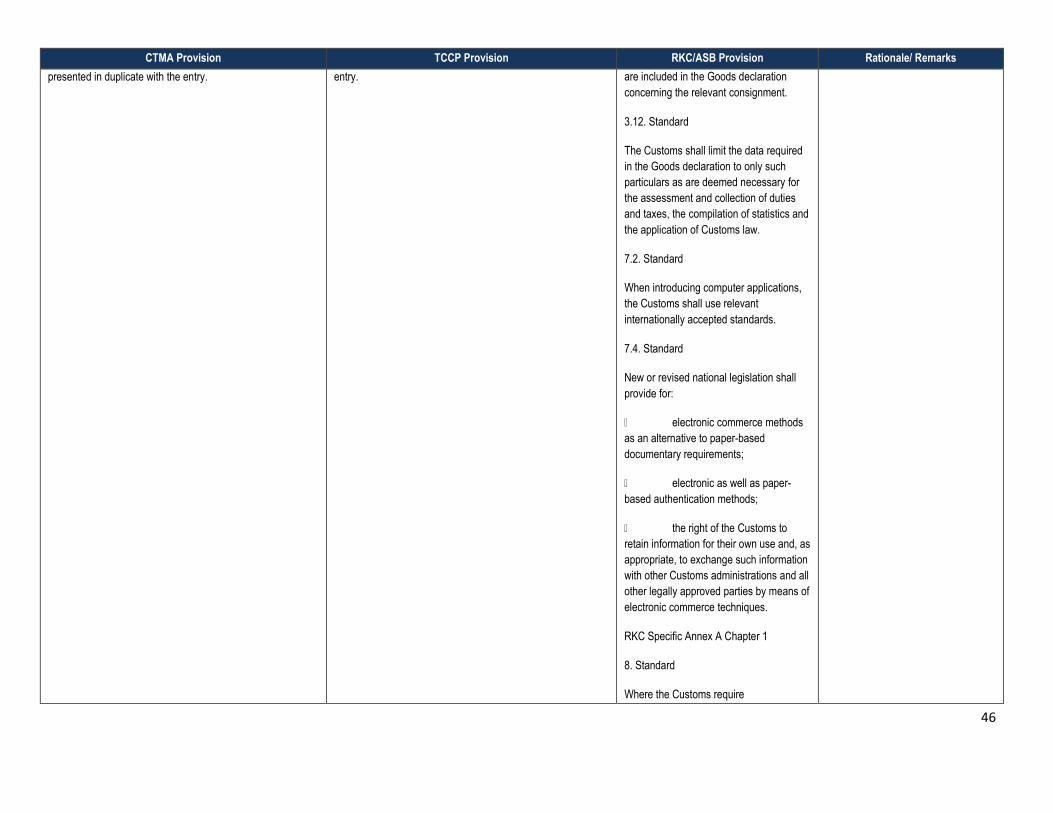

GOODS DECLARATION FORMAT AND CONTENTS

THE FORMAT OF THE GOODS DECLARATION SHALL

CONFORM TO INTERNATIONAL STANDARDS.

THE DATA REQUIRED IN THE GOODS DECLARATION

SHALL BE LIMITED TO ONLY SUCH PARTICULARS AS

ARE DEEMED NECESSARY FOR THE ASSESSMENT AND

COLLECTION OF DUTIES AND TAXES, THE

COMPILATION OF STATISTICS AND COMPLIANCE WITH

CUSTOMS AND TARIFF LAWS.

WHERE THE DECLARANT DOES NOT HAVE ALL THE

INFORMATION REQUIRED TO MAKE THE GOODS

DECLARATION, A PROVISIONAL OR INCOMPLETE

GOODS DECLARATION SHALL, FOR CERTAIN CASES

AND FOR REASONS DEEMED VALID BY CUSTOMS, BE

ALLOWED TO BE LODGED , PROVIDED THAT IT

CONTAINS THE PARTICULARS DEEMED NECESSARY BY

THE CUSTOMS FOR THE ACCEPTANCE OF THE ENTRY

FILED AND THAT THE DECLARANT UNDERTAKES TO

COMPLETE IT WITHIN A REASONABLE PERIOD OF TIME

AS SPECIFIED BY REGULATIONS.

IF CUSTOMS ACCEPTS A PROVISIONAL OR

INCOMPLETE GOODS DECLARATION, THE TARIFF

TREATMENT TO BE ACCORDED TO THE GOODS SHALL

NOT BE DIFFERENT FROM THAT WHICH WOULD HAVE

BEEN ACCORDED HAD A COMPLETE AND CORRECT

GOODS DECLARATION BEEN LODGED IN THE FIRST

INSTANCE.

THE RELEASE OF THE GOODS SHALL NOT BE DELAYED

PROVIDED THAT ANY SECURITY REQUIRED HAS BEEN

RKC GA Standards 3.11 to 3.19

The Goods declaration

(a) Goods declaration format and contents

3.11. Standard

The contents of the Goods declaration

shall be prescribed by the Customs. The

paper format of the Goods declaration

shall conform to the UN-layout key.

For automated Customs clearance

processes, the format of the electronically

lodged Goods declaration shall be based

on international standards for electronic

information exchange as prescribed in the

Customs Co-operation Council

Recommendations on information

technology.

3.12. Standard

The Customs shall limit the data required

in the Goods declaration to only such

particulars as are deemed necessary for

the assessment and collection of duties

and taxes, the compilation of statistics and

the application of Customs law.

3.13. Standard

Where, for reasons deemed valid by the

Customs, the declarant does not have all

the information required to make the

New provision. RKC standard

11

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

FURNISHED TO ENSURE COLLECTION OF ANY

APPLICABLE DUTIES AND TAXES.

CUSTOMS SHALL REQUIRE THE LODGEMENT OF THE

ORIGINAL GOODS DECLARATION AND ONLY THE

MINIMUM NUMBER OF COPIES AS ARE NECESSARY.

DOCUMENTS SUPPORTING THE GOODS DECLARATION

IN SUPPORT OF THE GOODS DECLARATION, CUSTOMS

SHALL ONLY REQUIRE DOCUMENTS NECESSARY FOR

CUSTOMS CONTROL AND TO ENSURE THAT ALL

REQUIREMENTS OF THE LAW HAVE BEEN COMPLIED

WITH.

WHERE CERTAIN SUPPORTING DOCUMENTS CANNOT

BE LODGED WITH THE GOODS DECLARATION FOR

REASONS DEEMED VALID BY THE CUSTOMS, THEY

SHALL ALLOW PRODUCTION OF THOSE DOCUMENTS

WITHIN A REASONABLE PERIOD AS SPECIFIED BY

REGULATION.

CUSTOMS SHALL PERMIT THE LODGEMENT OF

SUPPORTING DOCUMENTS BY ELECTRONIC MEANS.

CUSTOMS SHALL NOT REQUIRE A TRANSLATION OF

THE PARTICULARS OF SUPPORTING DOCUMENTS

EXCEPT WHEN NECESSARY TO PERMIT PROCESSING

OF THE GOODS DECLARATION.

Goods declaration, a provisional or

incomplete Goods declaration shall be

allowed to be lodged, provided that it

contains the particulars deemed

necessary by the Customs and that the

declarant undertakes to complete it within

a specified period.

3.14. Standard

If the Customs register a provisional or

incomplete Goods declaration, the tariff

treatment to be accorded to the goods

shall not be different from that which would

have been accorded had a complete and

correct Goods declaration been lodged in

the first instance.

The release of the goods shall not be

delayed provided that any security

required has been furnished to ensure

collection of any applicable duties and

taxes.

3.15. Standard

The Customs shall require the lodgement

of the original Goods declaration and only

the minimum number of copies necessary.

(b) Documents supporting the Goods

declaration

3.16. Standard

In support of the Goods declaration the

Customs shall require only those

documents necessary to permit control of

the operation and to ensure that all

requirements relating to the application of

12

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

Customs law have been complied with.

3.17. Standard

Where certain supporting documents

cannot be lodged with the Goods

declaration for reasons deemed valid by

the Customs, they shall allow production

of those documents within a specified

period.

3.18. Transitional Standard

The Customs shall permit the lodgement

of supporting documents by electronic

means.

3.19. Standard

The Customs shall not require a

translation of the particulars of supporting

documents except when necessary to

permit processing of the Goods

declaration.

SEC. 111. LODGEMENT AND REGISTRATION

CUSTOMS SHALL PERMIT THE LODGING OF THE

GOODS DECLARATION AT ANY DESIGNATED CUSTOMS

OFFICE.

GOODS DECLARATION SHALL BE LODGED DURING THE

HOURS DESIGNATED BY THE CUSTOMS.

CUSTOMS SHALL MAKE PROVISION UNDER SUCH

TERMS AND CONDITIONS AS THE COMMISSIONER OF

CUSTOMS MAY ESTABLISH FOR THE FILING OF GOODS

DECLARATION AND SUPPORTING DOCUMENTS PRIOR

TO THE ARRIVAL OF THE GOODS.

CUSTOMS SHALL FOR VALID REASON, PERMIT THE

DECLARANT TO AMEND THE GOODS DECLARATION

Standard 3.20, 3.22, 3.25 and 3.27

Lodgement, registration and checking of

the Goods declaration

3.20. Standard

The Customs shall permit the lodging of

the Goods declaration at any designated

Customs office.

3.22. Standard

The Goods declaration shall be lodged

during the hours designated by the

Customs.

New provision. Declarant may amend

declaration under certain conditions.

Customs must issue rules and

regulations to check possible abuse.

13

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

THAT HAS ALREADY BEEN LODGED, PROVIDED THAT

WHEN THE REQUEST IS RECEIVED THEY HAVE NOT

BEGUN TO CHECK THE GOODS DECLARATION OR TO

EXAMINE THE GOODS.

3.25. Standard

National legislation shall make provision

for the lodging and registering or checking

of the Goods declaration and supporting

documents prior to the arrival of the

goods.

3.27. Standard

The Customs shall permit the declarant to

amend the Goods declaration that has

already been lodged, provided that when

the request is received they have not

begun to check the Goods declaration or

to examine the goods.

SEC. 112. SPECIAL PROCEDURES FOR AUTHORIZED

PERSONS

FOR AUTHORIZED PERSONS WHO MEET THE CRITERIA

SET DOWN BY CUSTOMS, INCLUDING HAVING AN

APPROPRIATE RECORD OF COMPLIANCE WITH

CUSTOMS REQUIREMENTS AND A SATISFACTORY

SYSTEM FOR MANAGING THEIR COMMERCIAL

RECORDS, CUSTOMS SHALL PROVIDE FOR:

RELEASE OF THE GOODS ON THE PROVISION OF THE

MINIMUM INFORMATION NECESSARY TO IDENTIFY THE

GOODS AND PERMIT THE SUBSEQUENT COMPLETION

OF THE FINAL GOODS DECLARATION;

CLEARANCE OF THE GOODS AT THE DECLARANT'S

PREMISES OR ANOTHER PLACE AUTHORIZED BY THE

CUSTOMS; AND, IN ADDITION, TO THE EXTENT

POSSIBLE, OTHER SPECIAL PROCEDURES SUCH AS:

ALLOWING A SINGLE GOODS DECLARATION FOR ALL

IMPORTS OR EXPORTS IN A GIVEN PERIOD WHERE

GOODS ARE IMPORTED OR EXPORTED FREQUENTLY

SAFE Framework New provision. This will lay down the

legal basis for an “Authorized

Economic Operator” program for BoC

under the SAFE Framework.

14

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

BY THE SAME PERSON;

USE OF THE AUTHORIZED PERSONS’ COMMERCIAL

RECORDS TO SELF-ASSESS THEIR DUTY AND TAX

LIABILITY AND, WHERE APPROPRIATE, TO ENSURE

COMPLIANCE WITH OTHER CUSTOMS REQUIREMENTS;

ALLOWING THE LODGEMENT OF GOODS DECLARATION

BY MEANS OF AN ENTRY IN THE RECORDS OF THE

AUTHORIZED PERSON TO BE SUPPORTED

SUBSEQUENTLY BY A SUPPLEMENTARY GOODS

DECLARATION.

THIS SECTION SHALL BE IMPLEMENTED WITHIN FIVE (5)

YEARS FROM THE ENACTMENT OF THIS ACT.

SEC. 113 EXAMINATION OF THE GOODS

TIME REQUIRED FOR EXAMINATION OF GOODS

WHEN THE EXAMINATION OF GOODS IS REQUIRED BY

CUSTOMS, SUCH EXAMINATION SHALL TAKE PLACE AS

SOON AS POSSIBLE AFTER THE GOODS DECLARATION

HAS BEEN LODGED.

WHEN SCHEDULING EXAMINATIONS, PRIORITY SHALL

BE GIVEN TO THE EXAMINATION OF LIVE ANIMALS AND

PERISHABLE GOODS AND TO OTHER GOODS WHICH

CUSTOMS CONSIDER AS URGENTLY NEEDING

EXAMINATION.

CUSTOMS AND OTHER AGENCIES CONCERNED SHALL

COME OUT WITH A SYSTEM OF COORDINATION AND

JOINT EXAMINATION OF GOODS WHICH MUST BE

INSPECTED BY THE LATTER UNDER EXISTING

LEGISLATION.

PRESENCE OF THE DECLARANT AT EXAMINATION OF

GOODS

AS A GENERAL RULE, CUSTOMS MAY EXAMINE GOODS

RKC GA Standard 3.33 to 3.38

Examination of the goods

(a) Time required for examination of goods

3.33. Standard

When the Customs decide that goods

declared shall be examined, this

examination shall take place as soon as

possible after the Goods declaration has

been registered.

3.34. Standard

When scheduling examinations, priority

shall be given to the examination of live

animals and perishable goods and to other

goods which the Customs accept are

urgently required.

3.35. Transitional Standard

If the goods must be inspected by other

competent authorities and the Customs

New provision. Section 112 (2) states

the general rule that presence of

importer/broker not necessary during

examination except when requested

by the latter subject to approval, or

when customs so requires. This

principle is based on international best

customs practice .

15

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

WITHOUT THE PRESENCE OF THE DECLARANT OR AN

AUTHORIZED REPRESENTATIVE. HOWEVER, IF THE

DECLARANT SO REQUESTS, HE OR AN AUTHORIZED

REPRESENTATIVE SHALL BE ALLOWED TO BE PRESENT

UNLESS SERIOUS, EXCEPTIONAL CIRCUMSTANCES

EXIST TO BAR THEIR PRESENCE.

IF CUSTOMS DEEM IT USEFUL, THEY SHALL REQUIRE

THE DECLARANT TO BE PRESENT OR TO BE

REPRESENTED AT THE EXAMINATION OF THE GOODS

TO GIVE THEM ANY ASSISTANCE NECESSARY TO

FACILITATE THE EXAMINATION.

SAMPLING BY THE CUSTOMS

SAMPLES SHALL BE TAKEN ONLY WHERE DEEMED

NECESSARY BY CUSTOMS TO ESTABLISH THE TARIFF

DESCRIPTION AND/OR VALUE OF GOODS DECLARED

OR TO ENSURE COMPLIANCE WITH CUSTOMS AND

RELATED LAWS. SAMPLES DRAWN SHALL BE AS SMALL

AS POSSIBLE.

also schedules an examination, the

Customs shall ensure that the inspections

are co-ordinated and, if possible, carried

out at the same time.

(b) Presence of the declarant at

examination of goods

3.36. Standard

The Customs shall consider requests by

the declarant to be present or to be

represented at the examination of the

goods. Such requests shall be granted

unless exceptional circumstances exist.

3.37. Standard

If the Customs deem it useful, they shall

require the declarant to be present or to be

represented at the examination of the

goods to give them any assistance

necessary to facilitate the examination.

(c) Sampling by the Customs

3.38. Standard

Samples shall be taken only where

deemed necessary by the Customs to

establish the tariff description and/or value

of goods declared or to ensure the

application of other provisions of national

legislation. Samples drawn shall be as

small as possible.

SEC. 114. ERRORS IN GOODS DECLARATION

CUSTOMS SHALL NOT IMPOSE SUBSTANTIAL

PENALTIES FOR ERRORS WHERE THEY ARE SATISFIED

THAT SUCH ERRORS ARE INADVERTENT AND THAT

RKC GA Standard 3.39

Errors

3.39. Standard

New provision laying down the

principle that customs should not

impose excessive sanctions for non-

compliance when error is inadvertent

16

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

THERE HAS BEEN NO FRAUDULENT INTENT OR GROSS

NEGLIGENCE IN THE COMMISSION THEREOF. WHERE

THEY CONSIDER IT NECESSARY TO DISCOURAGE A

REPETITION OF SUCH ERRORS, A PENALTY MAY BE

IMPOSED BUT SHALL BE NO GREATER THAN IS

NECESSARY FOR THIS PURPOSE.

The Customs shall not impose substantial

penalties for errors where they are

satisfied that such errors are inadvertent

and that there has been no fraudulent

intent or gross negligence. Where they

consider it necessary to discourage a

repetition of such errors, a penalty may be

imposed but shall be no greater than is

necessary for this purpose.

or in good faith.

SEC. 115. RELEASE OF GOODS

GOODS DECLARED SHALL BE RELEASED AS SOON AS

DUTIES AND TAXES AND OTHER LAWFUL CHARGES

HAVE BEEN PAID OR SECURED TO BE PAID AND/OR

OTHERWISE ALL THE PERTINENT LAWS, RULES AND

REGULATIONS HAVE BEEN COMPLIED WITH.

WHEN CUSTOMS DECIDE THAT THEY REQUIRE

LABORATORY ANALYSIS OF SAMPLES, DETAILED

TECHNICAL DOCUMENTS OR EXPERT ADVICE, THEY

SHALL RELEASE THE GOODS BEFORE THE RESULTS OF

SUCH EXAMINATION ARE KNOWN, PROVIDED THAT ANY

SECURITY REQUIRED HAS BEEN FURNISHED AND

PROVIDED THEY ARE SATISFIED THAT THE GOODS ARE

NOT SUBJECT TO PROHIBITIONS OR RESTRICTIONS.

RKC GA Standard 3.42

3.42. Standard

When the Customs decide that they

require laboratory analysis of samples,

detailed technical documents or expert

advice, they shall release the goods

before the results of such examination are

known, provided that any security required

has been furnished and provided they are

satisfied that the goods are not subject to

prohibitions or restrictions.

New provision mandating the

immediate release of goods from

customs custody upon payment of

duties and taxes. RKC standard.

SEC. 116. ABANDONMENT OR DESTRUCTION OF

GOODS

WHEN GOODS HAVE NOT YET BEEN RELEASED FOR

CONSUMPTION OR WHEN THEY HAVE BEEN PLACED

UNDER ANOTHER CUSTOMS PROCEDURE, AND

PROVIDED THAT NO OFFENCE HAS BEEN DETECTED,

THE PERSON CONCERNED SHALL NOT BE REQUIRED

TO PAY THE DUTIES AND TAXES OR SHALL BE

ENTITLED TO REFUND THEREOF:

WHEN, AT HIS REQUEST, SUCH GOODS ARE

ABANDONED OR DESTROYED OR RENDERED

COMMERCIALLY VALUELESS UNDER CUSTOMS

RKC GA Standard 3.44

Abandonment or destruction of goods

3.44. Standard

When goods have not yet been released

for home use or when they have been

placed under another Customs procedure,

and provided that no offence has been

detected, the person concerned shall not

be required to pay the duties and taxes or

shall be entitled to repayment thereof:

New provision. This is introduced as a

general standard to reflect the RKC

mandate. Note however that current

legislation provides for abatement or

refund relief in similar circumstances.

17

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

CONTROL, AS CUSTOMS MAY DECIDE. ANY COSTS

INVOLVED SHALL BE BORNE BY THE PERSON

CONCERNED;

WHEN SUCH GOODS ARE DESTROYED OR

IRRECOVERABLY LOST BY ACCIDENT OR FORCE

MAJEURE, PROVIDED THAT SUCH DESTRUCTION OR

LOSS IS DULY ESTABLISHED TO THE SATISFACTION OF

CUSTOMS;

ON SHORTAGES DUE TO THE NATURE OF THE GOODS

WHEN SUCH SHORTAGES ARE DULY ESTABLISHED TO

THE SATISFACTION OF CUSTOMS.

ANY WASTE OR SCRAP REMAINING AFTER

DESTRUCTION SHALL BE LIABLE, IF TAKEN INTO

CONSUMPTION, TO THE DUTIES AND TAXES THAT

WOULD BE APPLICABLE TO SUCH WASTE OR SCRAP

IMPORTED IN THAT STATE.

P when, at his request, such

goods are abandoned to the Revenue or

destroyed or rendered commercially

valueless under Customs control, as the

Customs may decide. Any costs involved

shall be borne by the person concerned;

P when such goods are

destroyed or irrecoverably lost by accident

or force majeure, provided that such

destruction or loss is duly established to

the satisfaction of the Customs;

P on shortages due to the nature

of the goods when such shortages are

duly established to the satisfaction of the

Customs.

Any waste or scrap remaining after

destruction shall be liable, if taken into

home use or

exported, to the duties and taxes that

would be applicable to such waste or

scrap imported

or exported in that state.

SEC. 117. DISPOSITION OF ABANDONED GOODS

WHEN CUSTOMS SELL GOODS WHICH HAVE NOT BEEN

DECLARED WITHIN THE TIME ALLOWED OR COULD NOT

BE RELEASED ALTHOUGH NO OFFENCE HAS BEEN

DISCOVERED, THE PROCEEDS OF THE SALE, AFTER

DEDUCTION OF ANY DUTIES AND TAXES AND ALL

OTHER CHARGES AND EXPENSES INCURRED, SHALL

BE MADE OVER TO THOSE PERSONS ENTITLED TO

RECEIVE THEM OR, WHEN THIS IS NOT POSSIBLE, HELD

AT THEIR DISPOSAL FOR A SPECIFIED PERIOD.

RKC GA 3.45 Transitional standard

3.45. Transitional Standard

When the Customs sell goods which have

not been declared within the time allowed

or could not be released although no

offence has been discovered, the

proceeds of the sale, after deduction of

any duties and taxes and all other charges

and expenses incurred, shall be made

over to those persons entitled to receive

them or, when this is not possible, held at

New provision. This seems to apply to

implied abandonment. That means

that if abandonment is express,

importer is not entitled to net proceeds.

Relate this to the proposed Forfeiture

Fund in Section 1049.

18

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

their disposal for a specified period.

SEC. 118. When Duty and Tax is Due on Imported

Article.

All articles, when imported from any foreign country into the

Philippines, shall be subject to duty upon each importation,

even though previously exported from the Philippines, except

as otherwise specifically provided for in this ACT or in other

laws.

DUTIES, TAXES AND OTHER CHARGES SHALL BE PAID

PRIOR TO RELEASE FROM CUSTOMS CUSTODY OR

PRIOR TO ENTRY INTO THE CUSTOMS TERRITORY IN

CASE OF WITHDRAWAL FROM FREE ZONES OR FROM

CBWs. HOWEVER, FOR CERTAIN HIGHLY COMPLIANT

AND LOW RISK IMPORTERS OR EXPORTERS AS

DETERMINED BY REGULATION, THE BUREAU SHALL

ALLOW THE DEFERRED PAYMENT OF DUTIES AND

TAXES FOR A PERIOD OF NOT LESS THAN 14 DAYS BUT

NOT EXCEEDING 30 DAYS.

UNPAID DUTIES, TAXES AND ANY OTHER CHARGES,

SHALL BE SUBJECT TO THE LEGAL INTEREST OF 20%

PER ANNUM COMPUTED FROM THE EXPIRATION OF

THE DUE DATE OR IN CASE OF GOODS ADMITTED INTO

FREE ZONES, FROM THE TIME THE ASSESSMENT IS

MADE AFTER GOODS ENTER THE CUSTOMS

TERRITORY. THE LEGAL INTEREST SHALL BE IMPOSED

IN ADDITION TO ANY APPLICABLE FINE OR PENALTY.

WHEN DUTIES, TAXES AND OTHER CHARGES ARE PAID,

THE BUREAU SHALL ISSUE THE NECESSARY RECEIPT

OR ACKNOWLEDGEMENT AS PROOF OF SUCH

PAYMENT.

IN CASE OF DEFERRED PAYMENT, CUSTOMS SHALL

HAVE 3 YEARS WITHIN WHICH IT MAY TAKE LEGAL

ACTION TO COLLECT DUTIES AND TAXES NOT PAID BY

THE DUE DATE.

SEC 100 Imported Articles Subject to Duty.

All articles, when imported from any foreign country into the

Philippines, shall be subject to duty upon each importation,

even though previously exported from the Philippines, except

as otherwise specifically provided for in this Code or in other

laws.

RKC General Annex Standards 4.1 and

4.2, 4.3, 4.4, 4.5, 4.6, 4.8, 4.9, 4.10, 4.11,

4.12, 4.15, 4.16

A. ASSESSMENT, COLLECTION AND

PAYMENT OF DUTIES AND TAXES

4.1. Standard

National legislation shall define the

circumstances when liability to duties and

taxes is incurred.

4.2. Standard

The time period within which the

applicable duties and taxes are assessed

shall be stipulated in national legislation.

The assessment shall follow as soon as

possible after the Goods declaration is

lodged or the liability is otherwise incurred.

4.3. Standard

The factors on which the assessment of

duties and taxes is based and the

conditions under which they are

determined shall be specified in national

legislation.

4.4. Standard

The rates of duties and taxes shall be set

out in official publications.

4.5. Standard

National legislation shall specify the point

in time to be taken into consideration for

the purpose of determining the rates of

Section 100 is expanded to

incorporate RKC standards 4.1 up to

4.16. A new provision allows deferred

payment for a period of not less than

14 to not more than 30 days. Customs

must issue guidelines when to avail to

check possible abuse.

19

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

duties and taxes.

4.6. Standard

National legislation shall specify the

methods that may be used to pay the

duties and taxes.

4.8. Standard

National legislation shall determine the

due date and the place where payment is

to be made.

4.9. Standard

When national legislation specifies that the

due date may be after the release of the

goods, that date shall be at least ten days

after the release. No interest shall be

charged for the period between the date of

release and the due date.

4.10. Standard

National legislation shall specify the period

within which the Customs may take legal

action to collect duties and taxes not paid

by the due date.

4.11. Standard

National legislation shall determine the

rate of interest chargeable on amounts of

duties and taxes that have not been paid

by the due date and the conditions of

application of such interest.

4.12. Standard

When the duties and taxes have been

paid, a receipt constituting proof of

20

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

payment shall be issued to the payer,

unless there is other evidence constituting

proof of payment.

B. DEFERRED PAYMENT OF DUTIES

AND TAXES

4.15. Standard

Where national legislation provides for the

deferred payment of duties and taxes, it

shall specify the conditions under which

such facility is allowed.

4.16. Standard

Deferred payment shall be allowed without

interest charges to the extent possible.

SEC. 119. Effective Date of Rate of Import Duty.

Imported articles shall be subject to the rate or rates of import

duty OF THE APPLICABLE TARIFF HEADING at the time of

entry or UPON withdrawal from the warehouse for

consumption.

On article abandoned or forfeited to, or seized by, the

government, and then sold at public auction, the rates of duty

and the tariff in force on the date of the auction shall apply:

Provided, That duty based on the weight, volume and quantity

of articles shall be levied and collected on the weight, volume

and quantity at the time of their entry into the warehouse or

the date of abandonment, forfeiture and/or seizure.

RKC GA 4.1 and 4.2, 4.3, 4.4, 4.5, 4.6

4.1. Standard

National legislation shall define the

circumstances when liability to duties and

taxes is incurred.

4.2. Standard

The time period within which the

applicable duties and taxes are assessed

shall be stipulated in national legislation.

The assessment shall follow as soon as

possible after the Goods declaration is

lodged or the liability is otherwise incurred.

4.3. Standard

The factors on which the assessment of

duties and taxes is based and the

conditions under which they are

determined shall be specified in national

Provision amended deleting second

paragraph for not being relevant

anymore and simplifying the first

paragraph to make it clearer.

21

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

legislation.

4.4. Standard

The rates of duties and taxes shall be set

out in official publications.

4.5. Standard

National legislation shall specify the point

in time to be taken into consideration for

the purpose of determining the rates of

duties and taxes.

4.6. Standard

National legislation shall specify the

methods that may be used to pay the

duties and taxes.

SEC. 120. Treatment of Importation.

Imported articles shall be deemed "entered" in the Philippines

for consumption when the specified entry form is properly filed

and accepted, together with any related documents required

by the provisions of this ACT and/or regulations to be filed

with such form at the time of entry, at the port or station by the

customs official designated to receive such entry papers and

any duties, taxes, fees and/or other lawful charges required to

be paid at the time of making such entry have been paid or

secured to be paid with the customs official designated to

receive such monies, provided that the article has previously

arrived within the limits of the port of entry.

Imported articles shall be deemed “withdrawn" from

warehouse in the Philippines for consumption when the

specified form is properly filed and accepted, together with

any related documents required by any provisions of this ACT

and/or regulations to be filed with such form at the time of

withdrawal, by the customs official designated to receive the

withdrawal entry and any duties, taxes, fees and/or other

SEC 205 Entry, or Withdrawal from Warehouse, for

Consumption.

Imported articles shall be deemed "entered" in the Philippines

for consumption when the specified entry form is properly filed

and accepted, together with any related documents required by

the provisions of this Code and/or regulations to be filed with

such form at the time of entry, at the port or station by the

customs official designated to receive such entry papers and

any duties, taxes, fees and/or other lawful charges required to

be paid at the time of making such entry have been paid or

secured to be paid with the customs official designated to

receive such monies, provided that the article has previously

arrived within the limits of the port of entry.

Imported articles shall be deemed “wthdrawn" from warehouse

in the Philippines for consumption when the specified form is

properly filed and accepted, together with any related

documents required by any provisions of this Code and/or

regulations to be filed with such form at the time of withdrawal,

by the customs official designated to receive the withdrawal

RKC GA Standards 4.1 and 4.2, 4.3, 4.4,

4.5, 4.6, Specific Annex D2

4.1. Standard

National legislation shall define the

circumstances when liability to duties and

taxes is incurred.

4.2. Standard

The time period within which the

applicable duties and taxes are assessed

shall be stipulated in national legislation.

The assessment shall follow as soon as

possible after the Goods declaration is

lodged or the liability is otherwise incurred.

4.3. Standard

The factors on which the assessment of

duties and taxes is based and the

Minor amendment. “Have been Paid”

is inserted to make clearer the

obligation to pay duties and taxes

upon withdrawal for local consumption

of goods from bonded warehouse.

22

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

lawful charges HAVE BEEN PAID with the customs official

designated to receive such payment.

entry and any duties, taxes, fees and/or other lawful charges

required to be paid at the time of withdrawal have been

deposited with the customs official designated to receive such

payment.

conditions under which they are

determined shall be specified in national

legislation.

4.4. Standard

The rates of duties and taxes shall be set

out in official publications.

4.5. Standard

National legislation shall specify the point

in time to be taken into consideration for

the purpose of determining the rates of

duties and taxes.

4.6. Standard

National legislation shall specify the

methods that may be used to pay the

duties and taxes.

Specific Annex D Chapter 1

2. Standard

National legislation shall provide for

Customs warehouses open to any person

having the right to dispose of the goods

(public Customs warehouses).

SEC. 121. DEFERRED PAYMENT FOR GOVERNMENT

IMPORTATION

THE GOVERNMENT OR ANY OF ITS

INSTRUMENTALITIES OR AGENCIES MAY AVAIL OF

DEFERRED PAYMENT FOR ITS IMPORTATIONS UNDER

SUCH TERMS AND CONDITIONS THAT SHALL BE

DETERMINED BY REGULATION TO BE JOINTLY ISSUED

BY THE DEPARTMENT OF FINANCE AND THE

DEPARTMENT OF BUDGET MANAGEMENT .

RKC Standard allowing deferred payment.

RKC GA 4.15. Standard

Where national legislation provides for the

deferred payment of duties and taxes, it

shall specify the conditions under which

such facility is allowed.

New provision. Current policy allows

deferred payment for govt

importations. This provision will

provide for a clear statutory basis for

such privilege.

23

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

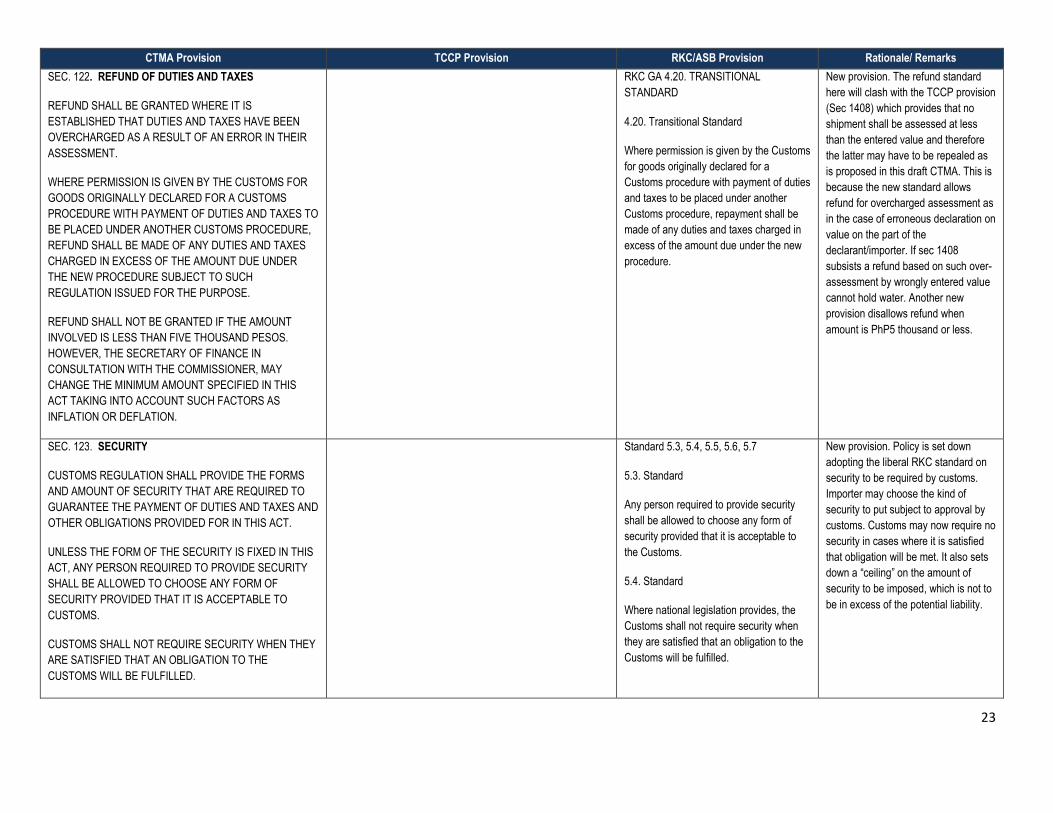

SEC. 122. REFUND OF DUTIES AND TAXES

REFUND SHALL BE GRANTED WHERE IT IS

ESTABLISHED THAT DUTIES AND TAXES HAVE BEEN

OVERCHARGED AS A RESULT OF AN ERROR IN THEIR

ASSESSMENT.

WHERE PERMISSION IS GIVEN BY THE CUSTOMS FOR

GOODS ORIGINALLY DECLARED FOR A CUSTOMS

PROCEDURE WITH PAYMENT OF DUTIES AND TAXES TO

BE PLACED UNDER ANOTHER CUSTOMS PROCEDURE,

REFUND SHALL BE MADE OF ANY DUTIES AND TAXES

CHARGED IN EXCESS OF THE AMOUNT DUE UNDER

THE NEW PROCEDURE SUBJECT TO SUCH

REGULATION ISSUED FOR THE PURPOSE.

REFUND SHALL NOT BE GRANTED IF THE AMOUNT

INVOLVED IS LESS THAN FIVE THOUSAND PESOS.

HOWEVER, THE SECRETARY OF FINANCE IN

CONSULTATION WITH THE COMMISSIONER, MAY

CHANGE THE MINIMUM AMOUNT SPECIFIED IN THIS

ACT TAKING INTO ACCOUNT SUCH FACTORS AS

INFLATION OR DEFLATION.

RKC GA 4.20. TRANSITIONAL

STANDARD

4.20. Transitional Standard

Where permission is given by the Customs

for goods originally declared for a

Customs procedure with payment of duties

and taxes to be placed under another

Customs procedure, repayment shall be

made of any duties and taxes charged in

excess of the amount due under the new

procedure.

New provision. The refund standard

here will clash with the TCCP provision

(Sec 1408) which provides that no

shipment shall be assessed at less

than the entered value and therefore

the latter may have to be repealed as

is proposed in this draft CTMA. This is

because the new standard allows

refund for overcharged assessment as

in the case of erroneous declaration on

value on the part of the

declarant/importer. If sec 1408

subsists a refund based on such over-

assessment by wrongly entered value

cannot hold water. Another new

provision disallows refund when

amount is PhP5 thousand or less.

SEC. 123. SECURITY

CUSTOMS REGULATION SHALL PROVIDE THE FORMS

AND AMOUNT OF SECURITY THAT ARE REQUIRED TO

GUARANTEE THE PAYMENT OF DUTIES AND TAXES AND

OTHER OBLIGATIONS PROVIDED FOR IN THIS ACT.

UNLESS THE FORM OF THE SECURITY IS FIXED IN THIS

ACT, ANY PERSON REQUIRED TO PROVIDE SECURITY

SHALL BE ALLOWED TO CHOOSE ANY FORM OF

SECURITY PROVIDED THAT IT IS ACCEPTABLE TO

CUSTOMS.

CUSTOMS SHALL NOT REQUIRE SECURITY WHEN THEY

ARE SATISFIED THAT AN OBLIGATION TO THE

CUSTOMS WILL BE FULFILLED.

Standard 5.3, 5.4, 5.5, 5.6, 5.7

5.3. Standard

Any person required to provide security

shall be allowed to choose any form of

security provided that it is acceptable to

the Customs.

5.4. Standard

Where national legislation provides, the

Customs shall not require security when

they are satisfied that an obligation to the

Customs will be fulfilled.

New provision. Policy is set down

adopting the liberal RKC standard on

security to be required by customs.

Importer may choose the kind of

security to put subject to approval by

customs. Customs may now require no

security in cases where it is satisfied

that obligation will be met. It also sets

down a “ceiling” on the amount of

security to be imposed, which is not to

be in excess of the potential liability.

24

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

WHEN SECURITY IS REQUIRED TO ENSURE THAT THE

OBLIGATIONS ARISING FROM A CUSTOMS PROCEDURE

WILL BE FULFILLED, THE CUSTOMS SHALL ACCEPT A

GENERAL SECURITY, IN PARTICULAR FROM

DECLARANTS WHO REGULARLY DECLARE GOODS AT

DIFFERENT OFFICES IN THE CUSTOMS TERRITORY

UNDER SUCH TERMS AND CONDITIONS AS THE

COMMISSIONER MAY DETERMINE.

WHERE SECURITY IS REQUIRED, THE AMOUNT OF

SECURITY TO BE PROVIDED SHALL BE AS LOW AS

POSSIBLE AND, IN RESPECT OF THE PAYMENT OF

DUTIES AND TAXES, SHALL NOT EXCEED THE AMOUNT

POTENTIALLY CHARGEABLE.

WHERE SECURITY HAS BEEN FURNISHED, IT SHALL BE

DISCHARGED AS SOON AS POSSIBLE AFTER THE

CUSTOMS ARE SATISFIED THAT THE OBLIGATIONS

UNDER WHICH THE SECURITY WAS REQUIRED HAVE

BEEN DULY FULFILLED.

5.5. Standard

When security is required to ensure that

the obligations arising from a Customs

procedure will be fulfilled, the Customs

shall accept a general security, in

particular from declarants who regularly

declare goods at different offices in the

Customs territory.

5.6. Standard

Where security is required, the amount of

security to be provided shall be as low as

possible and, in respect of the payment of

duties and taxes, shall not exceed the

amount potentially chargeable.

5.7. Standard

Where security has been furnished, it shall

be discharged as soon as possible after

the Customs are satisfied that the

obligations under which the security was

required have been duly fulfilled.

SEC. 124. CUSTOMS CONTROL

ALL GOODS, INCLUDING MEANS OF TRANSPORT,

WHICH ENTER OR LEAVE THE CUSTOMS TERRITORY,

REGARDLESS OF WHETHER THEY ARE LIABLE TO

DUTIES AND TAXES, SHALL BE SUBJECT TO CUSTOMS

CONTROL WHICH SHALL BE LIMITED TO THAT

NECESSARY TO ENSURE COMPLIANCE WITH CUSTOMS

AND RELATED LAWS.

IN THE APPLICATION OF CUSTOMS CONTROL, THE

CUSTOMS SHALL USE AUDIT-BASED CONTROLS AND

RISK MANAGEMENT SYSTEMS AND ADOPT A

COMPLIANCE MEASUREMENT STRATEGY TO SUPPORT

RKC GA Standard 6.1, 6.2, 6.3, 6.5, 6.7,

6.8, 6.10

6.1. Standard

All goods, including means of transport,

which enter or leave the Customs territory,

regardless of whether they are liable to

duties and taxes, shall be subject to

Customs control.

6.2. Standard

Customs control shall be limited to that

necessary to ensure compliance with the

New provision. Customs has now a

legal basis to create or ask for fund to

support international networking

efforts.

25

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

RISK MANAGEMENT.

CUSTOMS SHALL SEEK TO COOPERATE WITH OTHER

CUSTOMS ADMINISTRATIONS AND AIM AT CONCLUDING

MUTUAL ADMINISTRATIVE ASSISTANCE AGREEMENTS

TO ENHANCE CUSTOMS CONTROL.

CUSTOMS SHALL CONSULT AND COOPERATE WITH

OTHER GOVERNMENT REGULATORY AGENCIES,

INCLUDING FREE AND SPECIAL ECONOMIC ZONE

AUTHORITIES, AND THE CUSTOMS STAKEHOLDERS IN

GENERAL TO ENHANCE CUSTOMS CONTROL.

CUSTOMS SHALL EVALUATE TRADERS’ COMMERCIAL

SYSTEMS WHERE THOSE SYSTEMS HAVE AN IMPACT

ON CUSTOMS OPERATIONS TO ENSURE COMPLIANCE

WITH CUSTOMS REQUIREMENTS.

Customs law.

6.3. Standard

In the application of Customs control, the

Customs shall use risk management.

6.5. Standard

The Customs shall adopt a compliance

measurement strategy to support risk

management.

6.6. Standard

Customs control systems shall include

audit-based controls.

6.7. Standard

The Customs shall seek to co-operate with

other Customs administrations and seek to

conclude mutual administrative assistance

agreements to enhance Customs control.

6.8. Standard

The Customs shall seek to co-operate with

the trade and seek to conclude

Memoranda of Understanding to enhance

Customs control.

6.10. Standard

The Customs shall evaluate traders’

commercial systems where those systems

have an impact on Customs operations to

ensure compliance with Customs

requirements.

26

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

SEC. 125. APPLICATION OF INFORMATION AND

COMMUNICATION TECHNOLOGY

CUSTOMS SHALL APPLY INFORMATION AND

COMMUNICATION TECHNOLOGY TO ENHANCE

CUSTOMS CONTROL AND SUPPORT A COST-

EFFECTIVE AND EFFICIENT CUSTOMS OPERATIONS

GEARED TOWARDS A PAPERLESS CUSTOMS

ENVIRONMENT USING INTERNATIONALLY ACCEPTED

STANDARDS.

THE INTRODUCTION OF INFORMATION AND

COMMUNICATION TECHNOLOGY SHALL BE CARRIED

OUT IN CONSULTATION WITH ALL RELEVANT PARTIES

DIRECTLY AFFECTED, TO THE GREATEST EXTENT

POSSIBLE.

RKC GA Standard 7.1, 7.2 and 7.3

7.1. Standard

The Customs shall apply information

technology to support Customs

operations, where it is cost-effective and

efficient for the Customs and for the trade.

The Customs shall specify the conditions

for its application.

7.2. Standard

When introducing computer applications,

the Customs shall use relevant

internationally accepted standards.

7.3. Standard

The introduction of information technology

shall be carried out in consultation with all

relevant parties directly affected, to the

greatest extent possible.

New provision establishing policy on

the use of ICT technology in customs

administration.

SEC. 126. RELATIONSHIP BETWEEN CUSTOMS AND

THIRD PARTIES

PERSONS CONCERNED SHALL HAVE THE CHOICE OF

TRANSACTING BUSINESS WITH CUSTOMS EITHER

DIRECTLY OR BY DESIGNATING A THIRD PARTY TO ACT

ON THEIR BEHALF.

THE CUSTOMS TRANSACTIONS WHERE THE PERSON

CONCERNED ELECTS TO DO BUSINESS ON HIS OWN

ACCOUNT SHALL NOT BE TREATED LESS FAVOURABLY

OR BE SUBJECT TO MORE STRINGENT REQUIREMENTS

THAN THOSE CUSTOMS TRANSACTIONS WHICH ARE

HANDLED FOR THE PERSON CONCERNED BY A THIRD

PARTY.

A PERSON DESIGNATED AS A THIRD PARTY SHALL

RKC GA Standard 8.1, 8.3, 8.4

8.1. Standard

Persons concerned shall have the choice

of transacting business with the Customs

either directly or by designating a third

party to act on their behalf.

8.3. Standard

The Customs transactions where the

person concerned elects to do business

on his own account shall not be treated

less favourably or be subject to more

stringent requirements than those

Customs transactions which are handled

New provision adopting policy on how

to treat third parties transacting with

customs.

27

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

HAVE THE SAME RIGHTS AS THE PERSON WHO

DESIGNATED HIM IN THOSE MATTERS RELATED TO

TRANSACTING BUSINESS WITH CUSTOMS.

for the person concerned by a third party.

8.4. Standard

A person designated as a third party shall

have the same rights as the person who

designated him in those matters related to

transacting business with the Customs.

SEC. 127. INFORMATION OF GENERAL APPLICATION

TO FOSTER AN INFORMED COMPLIANCE REGIME,

CUSTOMS SHALL ENSURE THAT ALL RELEVANT AND

AVAILABLE INFORMATION OF GENERAL APPLICATION

PERTAINING TO CUSTOMS LAW, NOT OTHERWISE

CONFIDENTIAL OR FOR CUSTOMS USE ONLY IS

READILY ACCESSIBLE TO ANY INTERESTED PERSON

FOR LEGITIMATE USE.

WHEN INFORMATION THAT HAS BEEN MADE AVAILABLE

MUST BE AMENDED DUE TO CHANGES IN CUSTOMS

LAW, ADMINISTRATIVE ARRANGEMENTS OR

REQUIREMENTS, CUSTOMS SHALL, AS FAR AS MAY BE

FEASIBLE, MAKE THE REVISED INFORMATION READILY

AVAILABLE SUFFICIENTLY IN ADVANCE OF THE ENTRY

INTO FORCE OF THE CHANGES TO ENABLE

INTERESTED PERSONS TO TAKE ACCOUNT OF THEM,

UNLESS ADVANCE NOTICE IS PRECLUDED.

RKC GA Standard 9.1, 9.2

9.1. Standard

The Customs shall ensure that all relevant

information of general application

pertaining to Customs law is readily

available to any interested person.

9.2. Standard

When information that has been made

available must be amended due to

changes in Customs law, administrative

arrangements or requirements, the

Customs shall make the revised

information readily available sufficiently in

advance of the entry into force of the

changes to enable interested persons to

take account of them, unless advance

notice is precluded.

New provision. Transparency

standard.

SEC. 128. INFORMATION OF A SPECIFIC NATURE

SUBJECT TO REGULATION ISSUED FOR THE PURPOSE,

CUSTOMS SHALL PROVIDE INFORMATION AS MAY BE

AVAILABLE AND IS NOT OTHERWISE CONFIDENTIAL OR

FOR CUSTOMS USE ONLY, RELATING TO A SPECIFIC

MATTER AS REQUESTED BY AN INTERESTED PERSON

FOR LEGITIMATE USE.

CUSTOMS MAY REQUIRE THE PAYMENT OF A

RKC GA 9.4, 9.7

9.4. Standard

At the request of the interested person, the

Customs shall provide, as quickly and as

accurately as possible, information relating

to the specific matters raised by the

interested person and pertaining to

Customs law.

New provision. Transparency

standard.

28

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

REASONABLE FEE IN PROVIDING SUCH INFORMATION

OF A SPECIFIC NATURE TO INTERESTED PARTIES.

9.7. Standard

When the Customs cannot supply

information free of charge, any charge

shall be limited to the approximate cost of

the services rendered.

SEC. 129. DECISIONS AND RULINGS

AT THE WRITTEN REQUEST OF THE PERSON

CONCERNED, CUSTOMS SHALL NOTIFY THEIR

DECISION IN WRITING WITHIN A PERIOD SPECIFIED IN

THIS ACT. WHERE THE DECISION IS ADVERSE TO THE

PERSON CONCERNED, THE REASONS SHALL BE GIVEN

AND THE RIGHT OF APPEAL ADVISED.

CUSTOMS, SHALL, WITHIN THE BOUNDS OF ITS

MANDATE UNDER THIS ACT, ISSUE BINDING RULINGS

AT THE REQUEST OF THE INTERESTED PERSON ON

MATTERS PERTAINING TO IMPORTATION OR

EXPORTATION OF GOODS, PROVIDED THAT IT HAS ALL

THE INFORMATION THEY DEEM NECESSARY.

RKC GA Standard 9.8, 9.9

9.8. Standard

At the written request of the person

concerned, the Customs shall notify their

decision in writing within a period specified

in national legislation. Where the decision

is adverse to the person concerned, the

reasons shall be given and the right of

appeal advised.

9.9. Standard

The Customs shall issue binding rulings at

the request of the interested person,

provided that the Customs have all the

information they deem necessary.

New provision Transparency standard

SEC. 130. RIGHT OF APPEAL, FORMS AND GROUND

ANY PERSON WHO IS DIRECTLY AFFECTED BY A

DECISION OR OMISSION OF CUSTOMS PERTAINING TO

HIS IMPORTATION OR EXPORTATION OR LEGAL CLAIM

SHALL HAVE A RIGHT OF APPEAL.

AN APPEAL IN WRITING SHALL BE LODGED WITHIN THE

SUFFICIENT TIME PERIOD AS SPECIFIED IN THIS ACT

OR BY REGULATION STATING THE GROUNDS ON

WHICH IT IS BEING MADE.

CUSTOMS SHALL NOT, AS A MATTER OF COURSE,

REQUIRE THAT ANY SUPPORTING EVIDENCE BE

LODGED TOGETHER WITH THE APPEAL BUT SHALL, IN

RKC GA Standard 10.2, 10.7, 10.8, 10.9

10.2. Standard

Any person who is directly affected by a

decision or omission of the Customs shall

have a right of appeal.

10.7. Standard

An appeal shall be lodged in writing and

shall state the grounds on which it is being

made.

10.8. Standard

New provision. Standard policy on

appellate relief.

29

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

APPROPRIATE CIRCUMSTANCES, ALLOW A

REASONABLE TIME FOR THE LODGEMENT OF SUCH

EVIDENCE.

A time limit shall be fixed for the

lodgement of an appeal against a decision

of the Customs and it shall be such as to

allow the appellant sufficient time to study

the contested decision and to prepare an

appeal.

10.9. Standard

Where an appeal is to the Customs they

shall not, as a matter of course, require

that any supporting evidence be lodged

together with the appeal but shall, in

appropriate circumstances, allow a

reasonable time for the lodgement of such

evidence.

CHAPTER 3. TYPES OF IMPORTATION

SEC. 131. FREE AND REGULATED IMPORTATIONS AND

EXPORTATIONS

UNLESS OTHERWISE PROVIDED BY LAW OR

REGULATION, ALL ARTICLES MAY BE FREELY

IMPORTED INTO AND EXPORTED FROM THE

PHILIPPINES WITHOUT NEED FOR IMPORT AND

EXPORT PERMITS, CLEARANCES OR LICENSES.

ARTICLES SUBJECT TO GOVERNMENT REGULATION

MAY BE BROUGHT IN OR EXPORTED ONLY AFTER

SECURING THE REQUIRED IMPORT OR EXPORT

PERMITS, CLEARANCES, LICENSES, AND THE LIKE,

PRIOR TO IMPORTATION OR EXPORTATION; AND IF

ALLOWED BY GOVERNING LAWS OR REGULATIONS,

AFTER ARRIVAL OF THE ARTICLES BUT PRIOR TO

RELEASE FROM CUSTOMS CUSTODY IN CASE OF

IMPORTATION.

New provision. This is the first attempt

to statutorily define “freely” and

“regulated” importations. Only

“prohibited” importation is defined in

the TCCP. Also the word “exportation”

is included as the TCCP only mentions

“importation”. The provision also sets

down the policy on when the import

permit or license must be secured.

This allows certain leeway to clear

certain regulated goods instead of

subjecting them to undue sanctions

such as seizure which does not serve

primary goals of customs.

SEC. 132. Prohibited Importations AND EXPORTATIONS.

The importation into AND EXPORTATION FROM the

SEC 101 Prohibited Importations. Minor amendments. ”Infringing goods”

already included in the list of prohibited

imports and so with those defined in

30

CTMA Provision TCCP Provision RKC/ASB Provision Rationale/ Remarks

Philippines of the following articles ARE prohibited:

(a) Dynamite, gunpowder, ammunitions and other

explosives, firearms and weapons of war, and parts thereof,

except when authorized by law;

(b) Written or printed articles in any form containing

any matter advocating or inciting treason, or rebellion,

insurrection, sedition or subversion against the Government of

the Philippines, or forcible resistance to any law of the

Philippines, or containing any threat to take the life of, or inflict

bodily harm upon any person in the Philippines;

(c). Written or printed articles, negatives or

cinematographic film, photographs, engravings, lithographs,

objects, paintings, drawings or other representation of an

obscene or immoral character;

(d) Articles, instruments, drugs and substances

designed, intended or adapted for producing unlawful

abortion, or any printed matter which advertises or describes

or gives directly or indirectly information where, how or by

whom unlawful abortion is produced;

(e) Roulette wheels, gambling outfits, loaded dice,

marked cards, machines, apparatus or mechanical devices

used in gambling or the distribution of money, cigars,

cigarettes or other articles when such distribution is

dependent on chance, including jackpot and pinball machines

or similar contrivances, or parts thereof;

(f) Lottery and sweepstakes tickets except those

authorized by the Philippine Government, advertisements

thereof, and lists of drawings therein;

(g) Any article manufactured in whole or in part of

gold, silver or other precious metals or alloys thereof, the

stamps, brands or marks or which do not indicate the actual

fineness of quality of said metals or alloys;.-