Embed Size (px)

Citation preview

Clústers Globales de

Innovación

Xavier Ferràs, MBA, PhD.

Octubre 2016

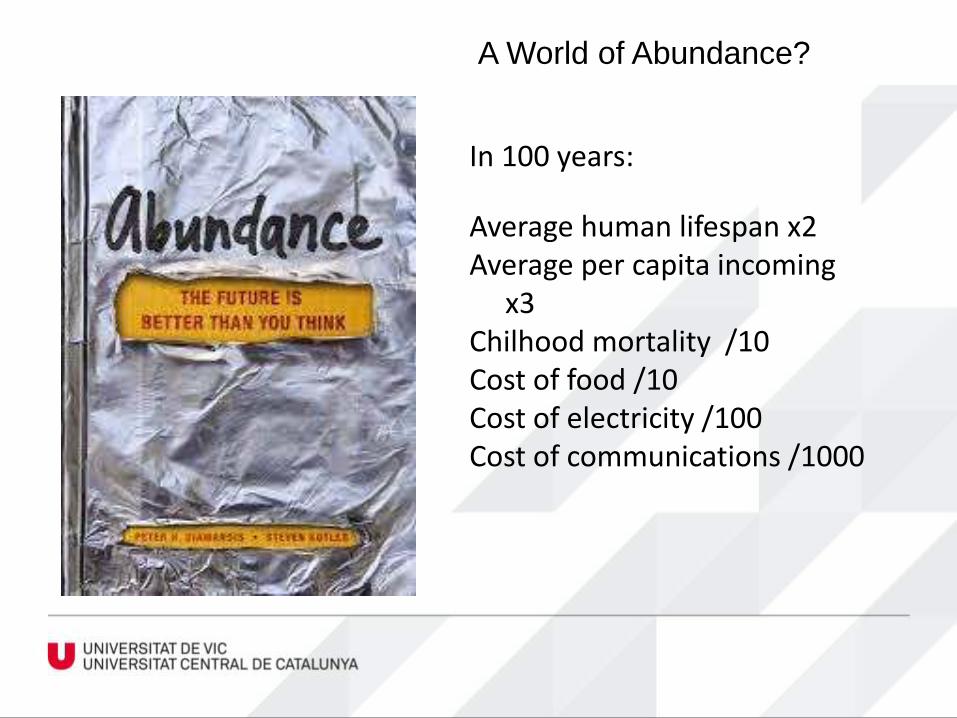

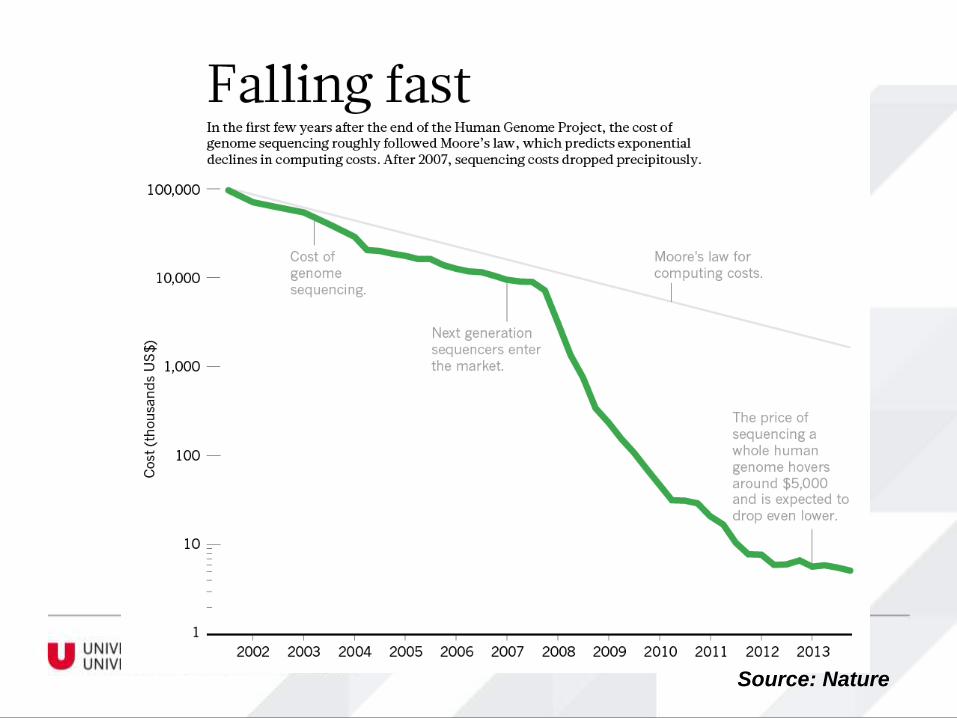

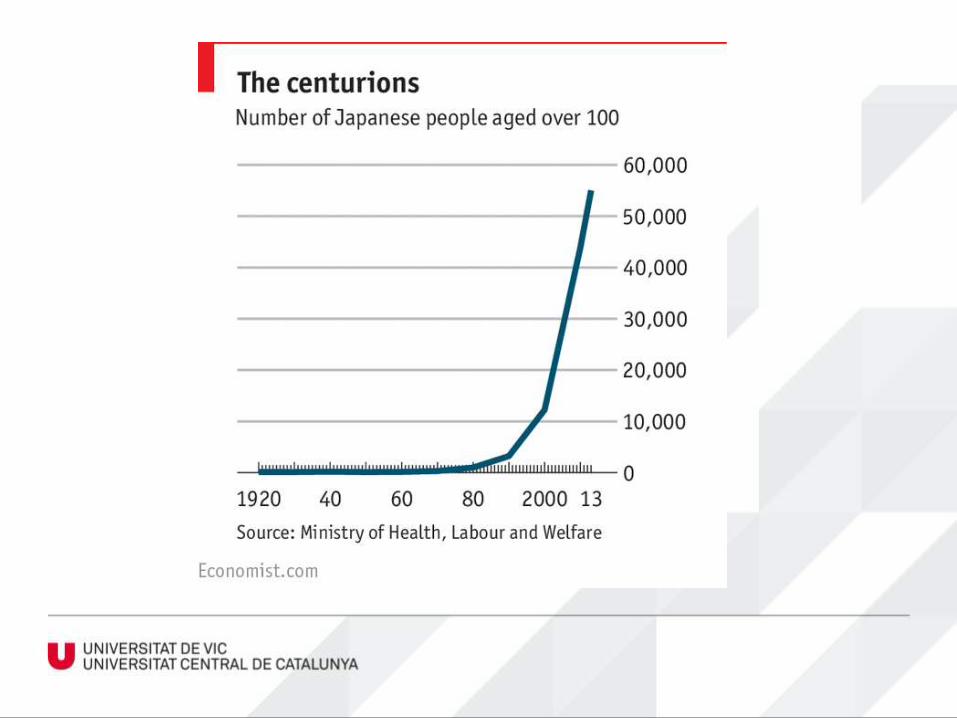

In 100 years:

Average human lifespan x2Average per capita incoming

x3Chilhood mortality /10Cost of food /10Cost of electricity /100Cost of communications /1000

A World of Abundance?

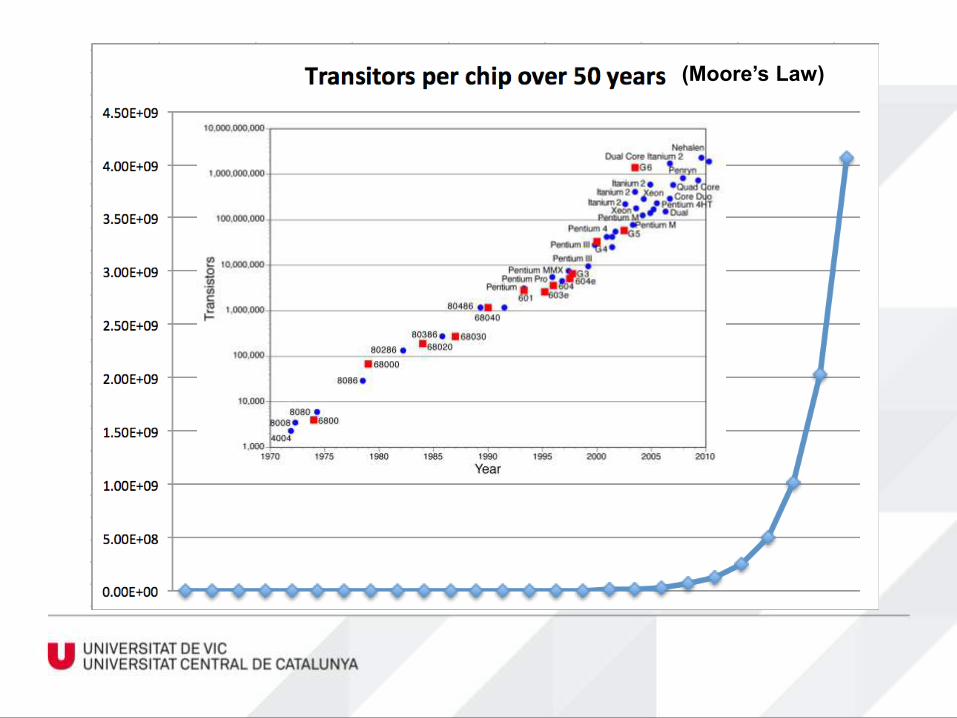

(Moore’s Law)

5

Source: Nature

www.acc10.cat

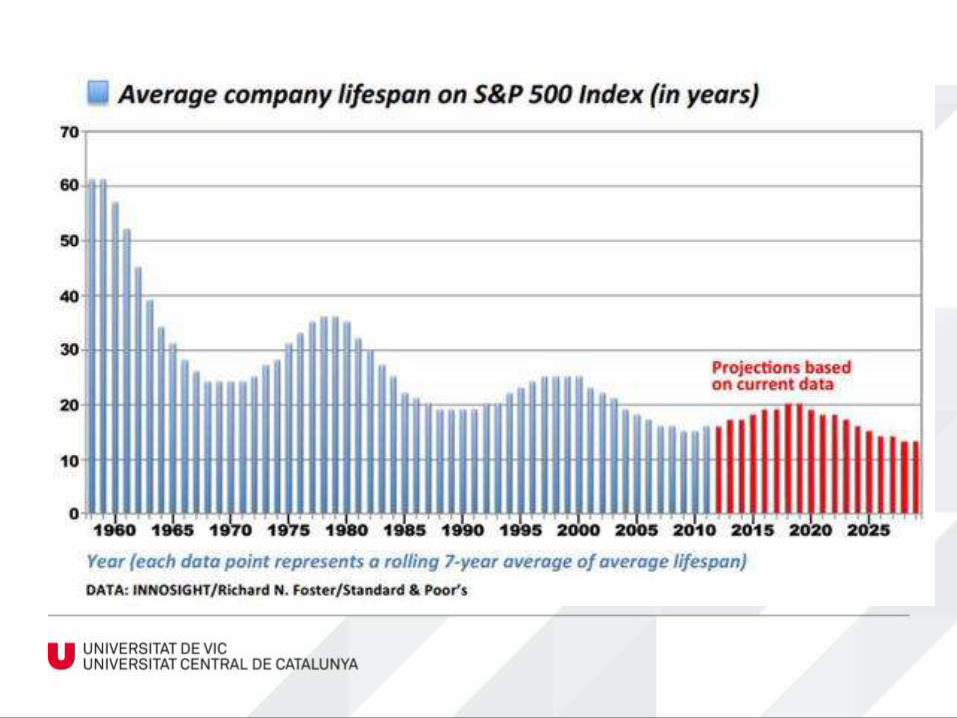

Technology kills business models

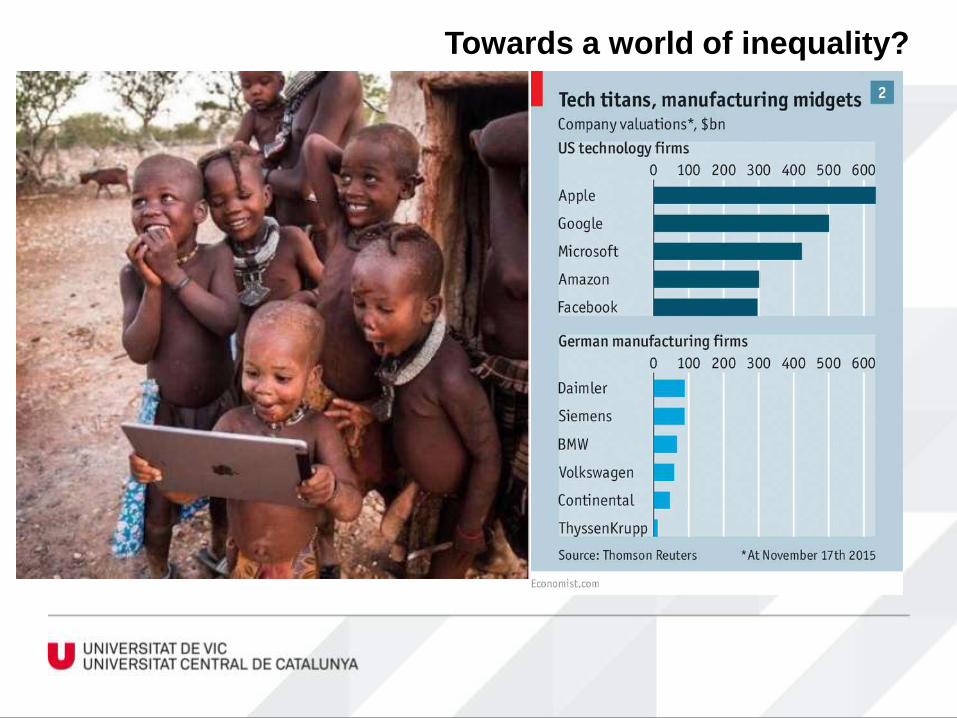

Towards a world of inequality?

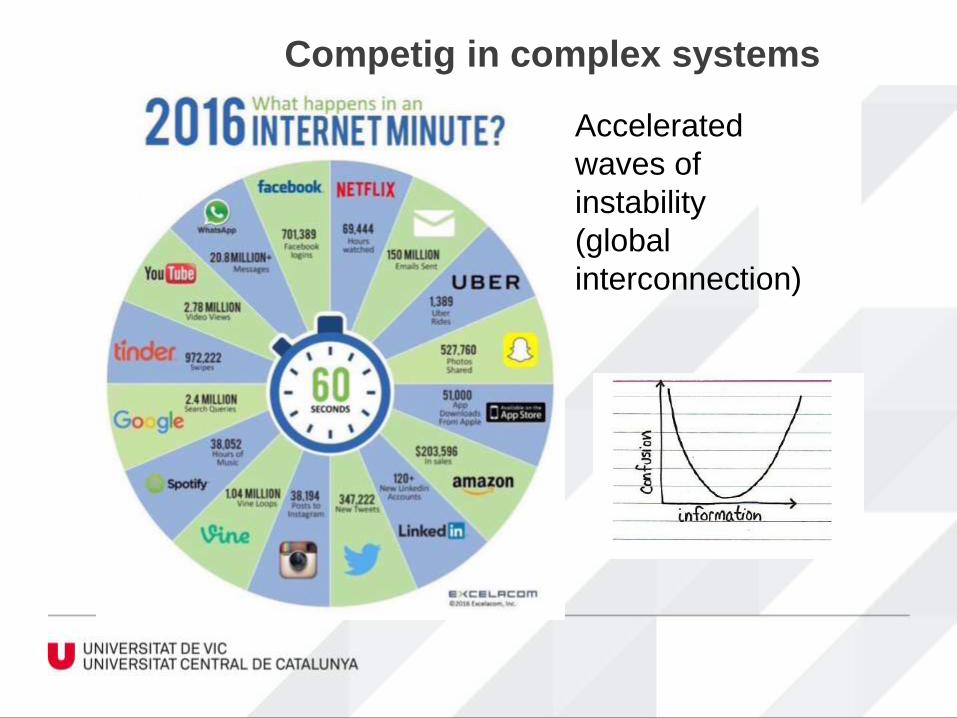

Accelerated

waves of

instability

(global

interconnection)

Competig in complex systems

Competing in a VUCAenvironment.

(Volatility, Uncertainty, Complexity,

Ambiguity)

DYNAMIC ENVIRONMENTS

“Si el ritmo de cambio de una empresa

es inferior al de su entorno, el final de

la empresa está a la vista… La única

pregunta es cuándo será el final”

Jack Welch

CEO, General Electric

¿Qué cambia más rápidamente, vuestra

empresa o vuestro entorno?

Doing nothing is doing something…

But… WHAT IS INNOVATION?

Or, to go to the point… Which is the

difference between INNOVATION and

IMPROVEMENT?

“An innovator is who

goes where no other

is”

Reinhold Messner

“Every significant

innovation incorporates

significant risk”

Henry Chesbrough

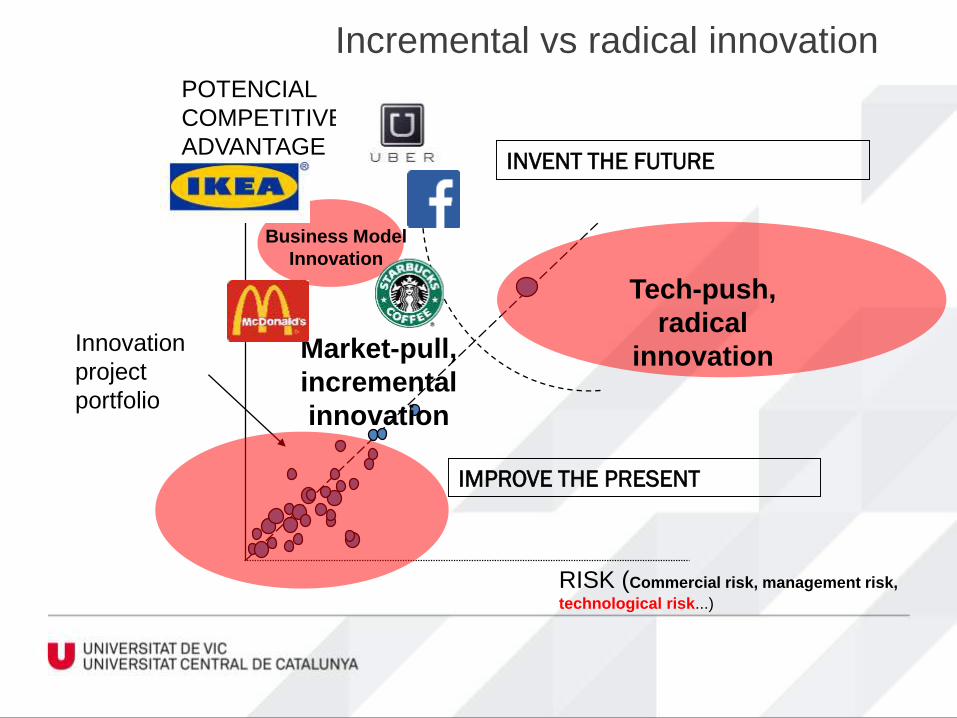

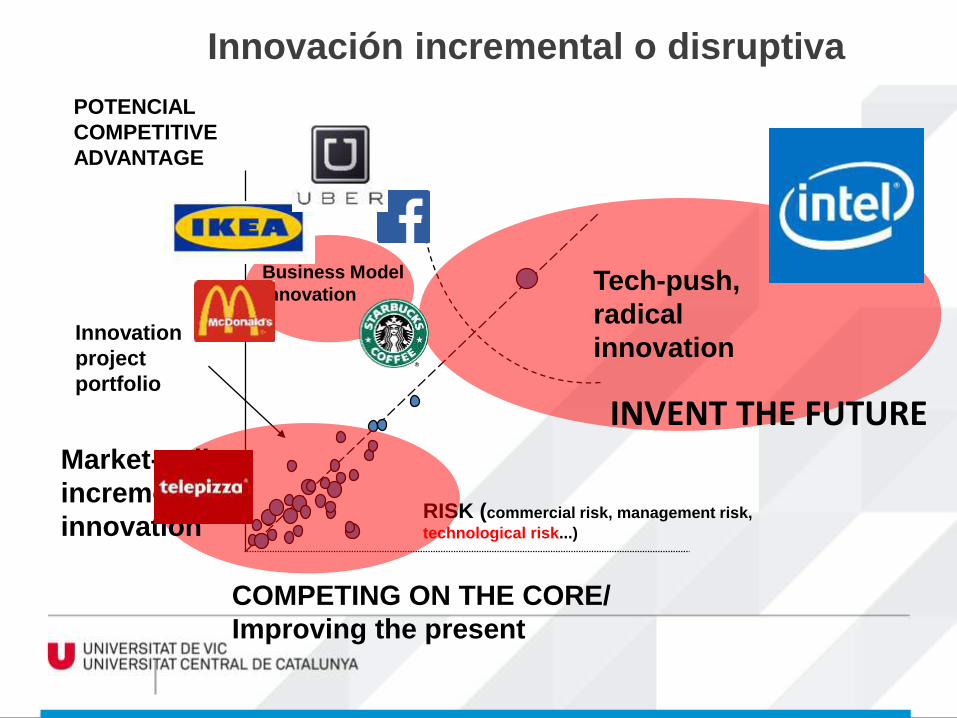

POTENCIAL

COMPETITIVE

ADVANTAGE

RISK (Commercial risk, management risk,

technological risk...)

Innovation

project

portfolio

Market-pull,

incremental

innovation

Tech-push,

radical

innovation

Business Model

Innovation

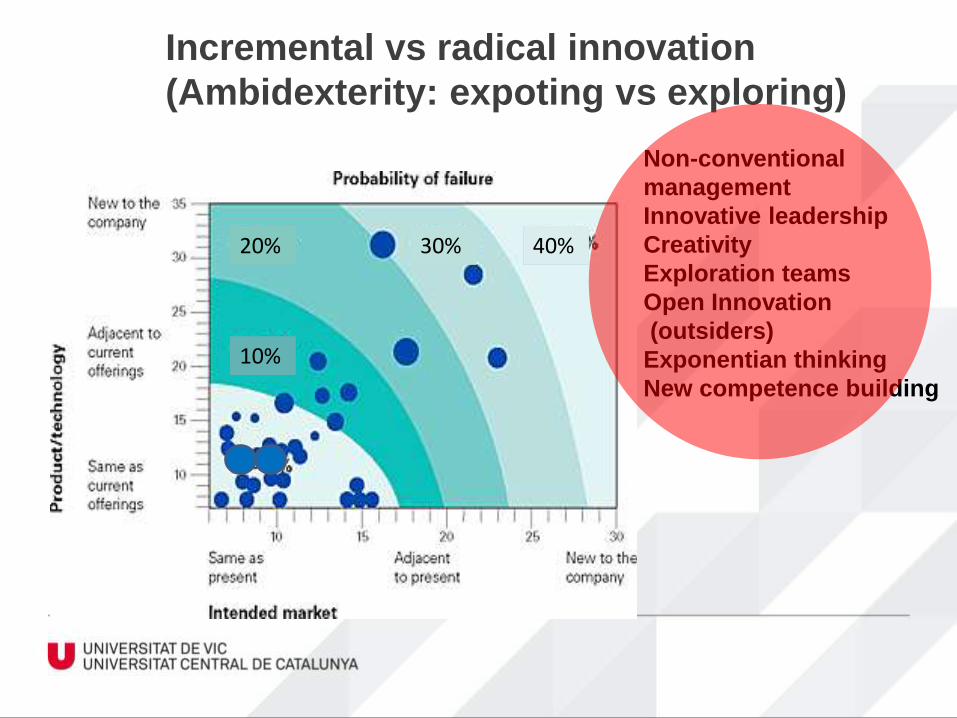

Incremental vs radical innovation

IMPROVE THE PRESENT

INVENT THE FUTURE

“El problema del emprendedor”

Definir las bases de un business plan:

Características del producto

Mercado potencial

Precio

Previsiones de venta

Necesidades operativas (proveedores,

manufactura, logística…)

Necesidades financieras

POTENCIAL

COMPETITIVE

ADVANTAGE

RISK (commercial risk, management risk,

technological risk...)

Innovation

project

portfolio

COMPETING ON THE CORE/

Improving the present

Tech-push,

radical

innovation

Innovación incremental o disruptiva

Market-pull,

incremental

innovation

INVENT THE FUTURE

Business Model

Innovation

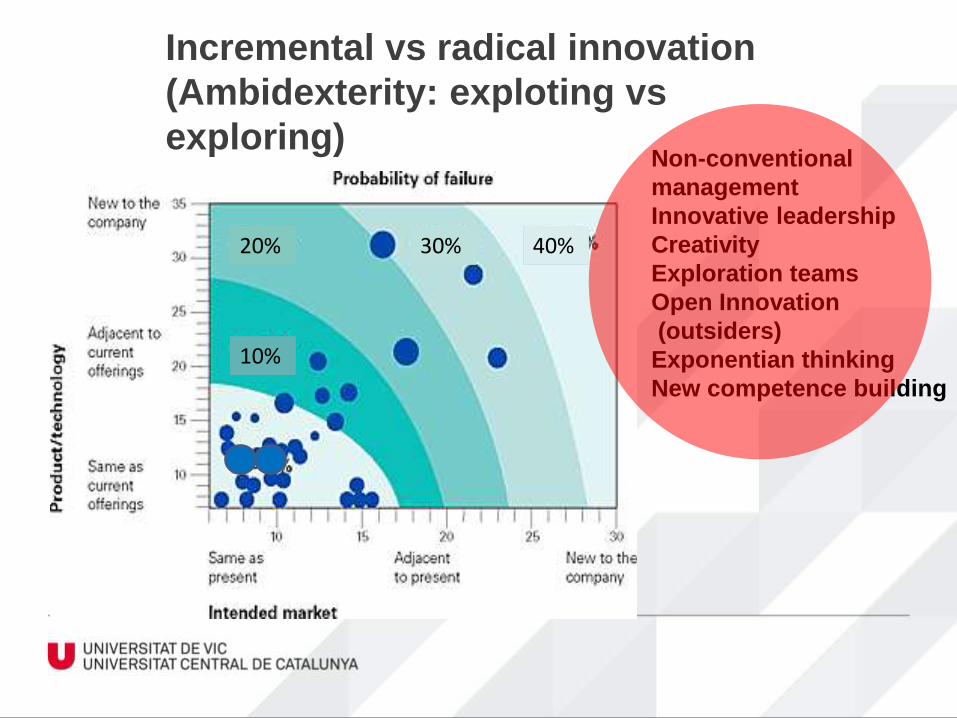

Non-conventional

management

Innovative leadership

Creativity

Exploration teams

Open Innovation

(outsiders)

Exponentian thinking

New competence building

Incremental vs radical innovation

(Ambidexterity: expoting vs exploring)

30% 40%40%20%

10%

# Ecosistemas

de innovación

Croatia

Euskadi

Source: Guillermo Dorronsoro. Deusto Business School

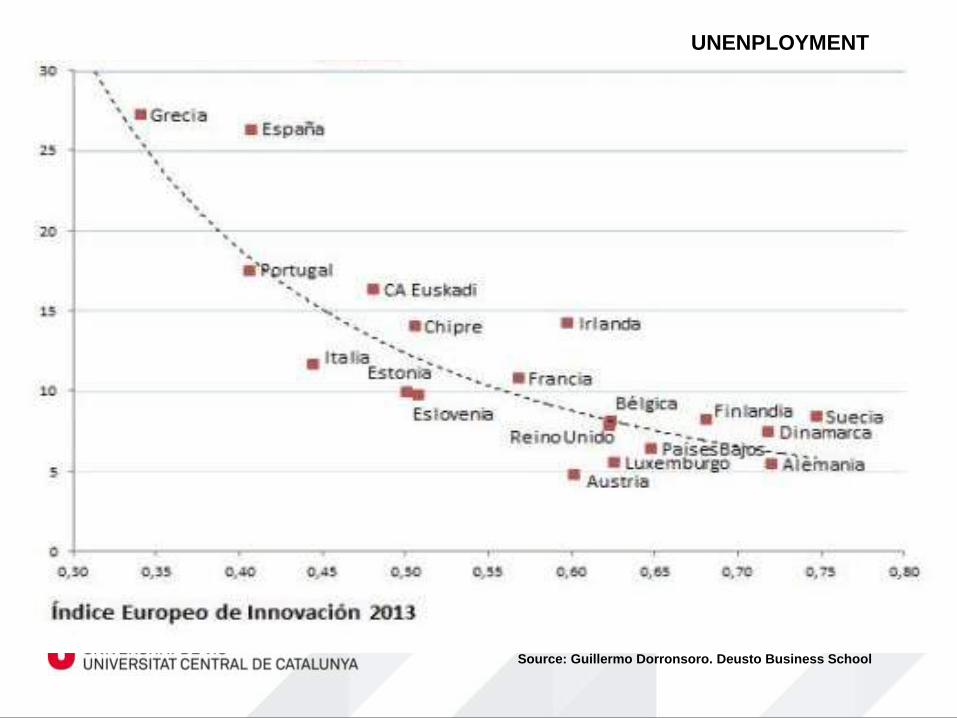

UNENPLOYMENT

| |

OmahaTelemarketingHotel ReservationsCredit Card Processing

Wisconsin / Iowa / IllinoisAgricultural Equipment

DetroitAuto Equipmentand Parts

RochesterImaging Equipment

Western MassachusettsPolymers

BostonMutual FundsBiotechnologySoftware and Networking

Venture Capital

HartfordInsurance

ProvidenceJewelryMarine Equipment

New York CityFinancial ServicesAdvertisingPublishingMultimedia

Pennsylvania / New JerseyPharmaceuticals

North CarolinaHousehold FurnitureSynthetic FibersHosiery

Dalton, GeorgiaCarpets

South FloridaHealth Technology Computers

Nashville / LouisvilleHospital Management

Baton Rouge / New OrleansSpecialty Foods

Southeast Texas / LouisianaChemicals

DallasReal Estate Development

WichitaLight AircraftFarm Equipment

Los Angeles AreaDefense AerospaceEntertainment

Silicon ValleyMicroelectronicsBiotechnologyVenture Capital

Cleveland / LouisvillePaints & Coatings

PittsburghAdvanced MaterialsEnergy

West MichiganOffice and Institutional Furniture

MichiganClocks

CarlsbadGolf Equipment

MinneapolisCardio-vascularEquipmentand Services

Warsaw, IndianaOrthopedic Devices

ColoradoComputer Integrated Systems / ProgrammingEngineering ServicesMining / Oil and Gas Exploration

PhoenixHelicoptersSemiconductorsElectronic Testing LabsOptics

Las VegasAmusement / CasinosSmall Airlines

OregonElectrical Measuring Equipment

Woodworking EquipmentLogging / Lumber Supplies

SeattleAircraft Equipment and DesignBoat and Ship BuildingMetal Fabrication

BoiseSawmillsFarm Machinery

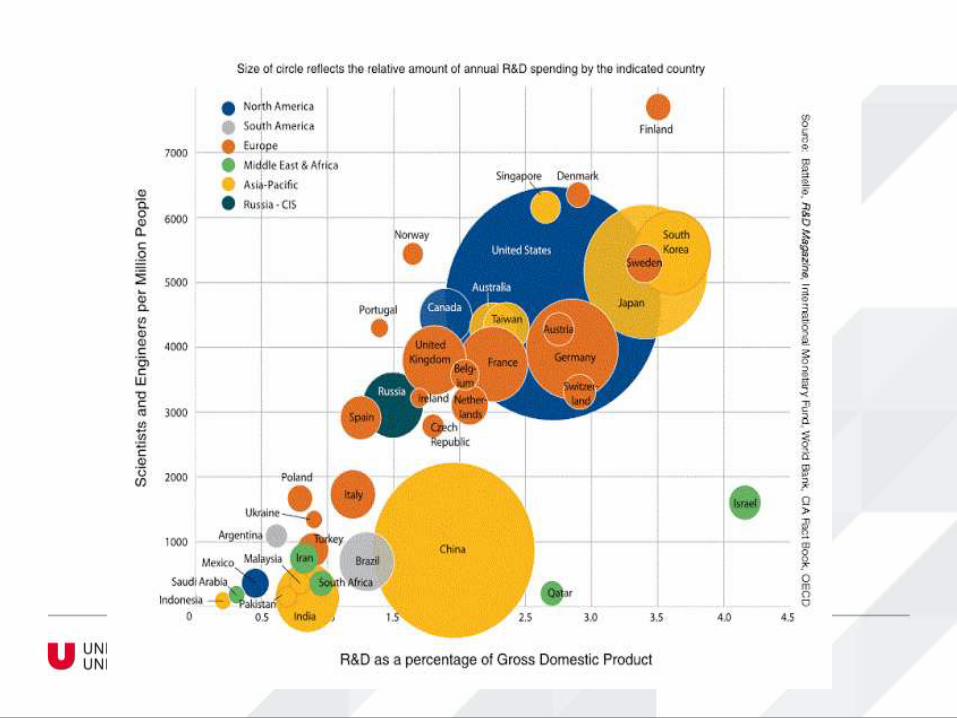

Los clusters son una realidad

Fuente: Cluster Development

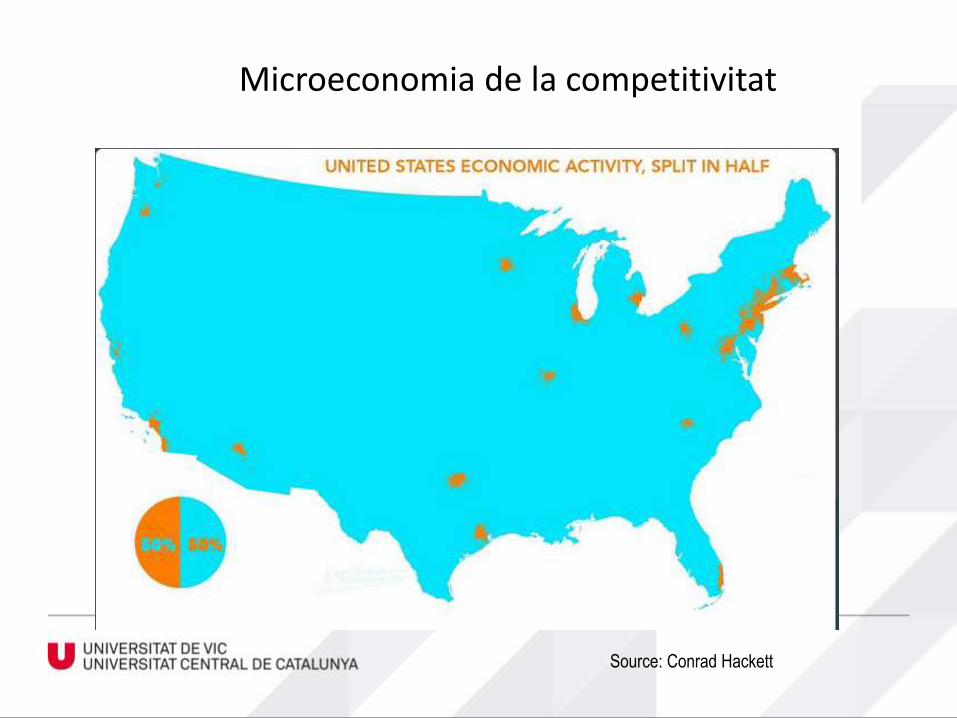

Microeconomia de la competitivitat

Source: Conrad Hackett

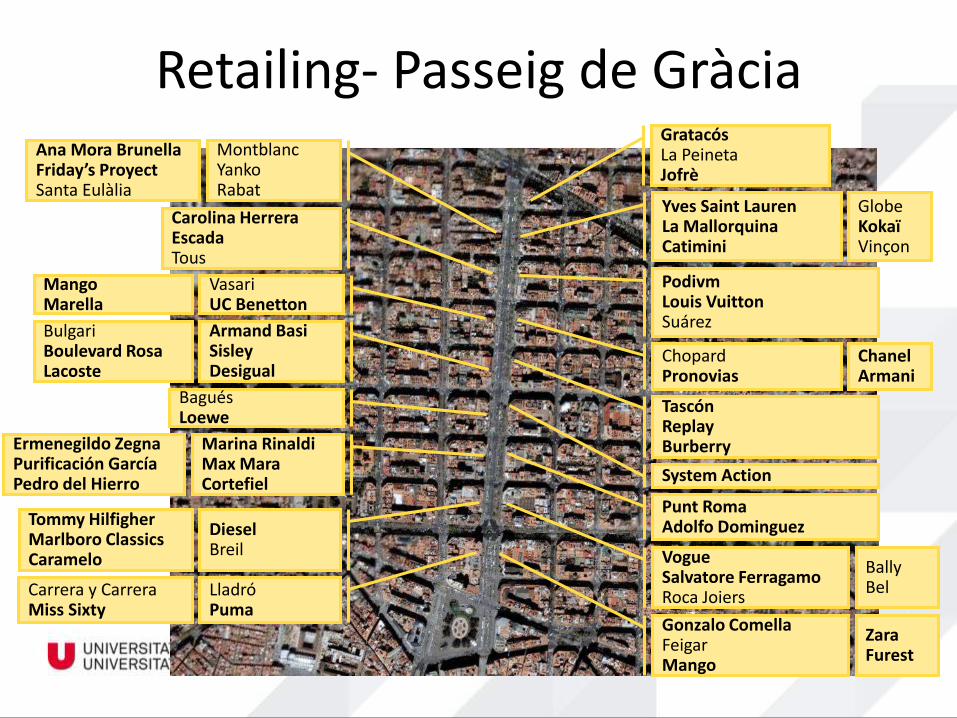

Retailing- Passeig de Gràcia

Yves Saint LaurenLa MallorquinaCatimini

PodivmLouis VuittonSuárez

ChopardPronovias

TascónReplayBurberry

System Action

Punt RomaAdolfo Dominguez

VogueSalvatore FerragamoRoca Joiers

Gonzalo ComellaFeigarMango

BallyBel

GlobeKokaïVinçon

ChanelArmani

GratacósLa PeinetaJofrè

MontblancYankoRabat

Ana Mora BrunellaFriday’s ProyectSanta Eulàlia

Carolina HerreraEscadaTous

VasariUC Benetton

MangoMarella

Armand BasiSisleyDesigual

BulgariBoulevard RosaLacoste

BaguésLoewe

ZaraFurest

Marina RinaldiMax MaraCortefiel

Ermenegildo ZegnaPurificación GarcíaPedro del Hierro

DieselBreil

Tommy HilfigherMarlboro ClassicsCaramelo

LladróPuma

Carrera y CarreraMiss Sixty

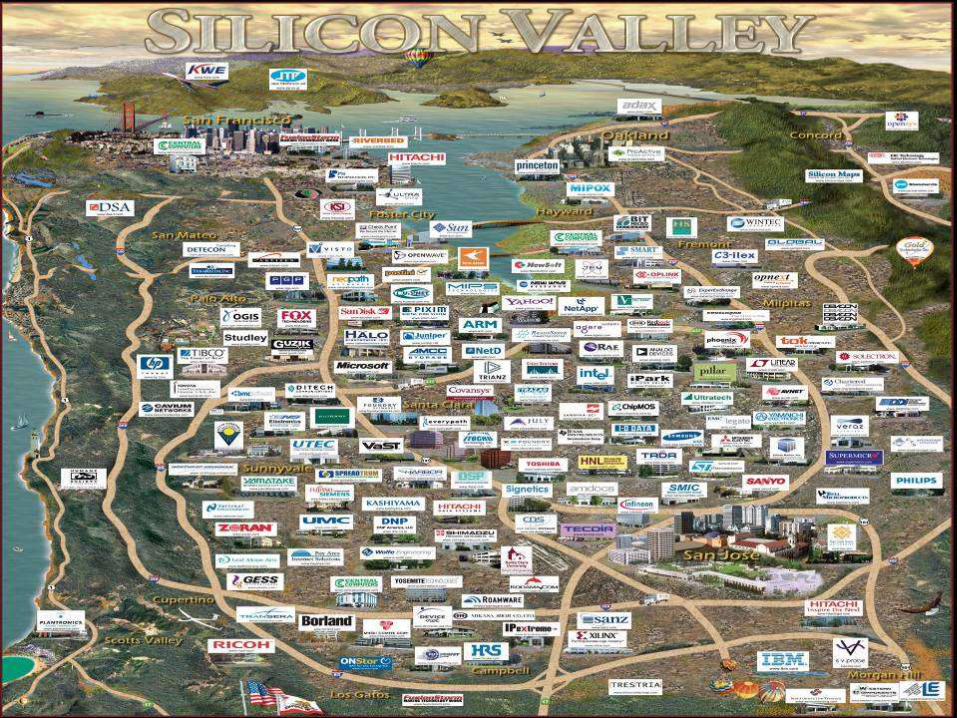

SILICON VALLEY

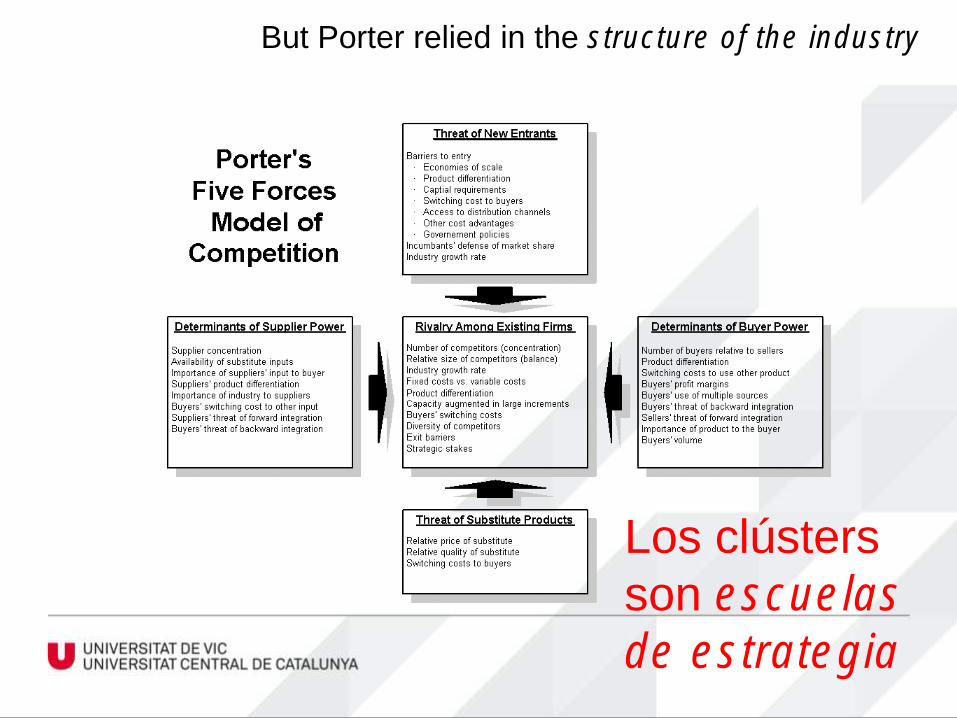

But Porter relied in the structure of the industry

Los clústers

son escuelas

de estrategia

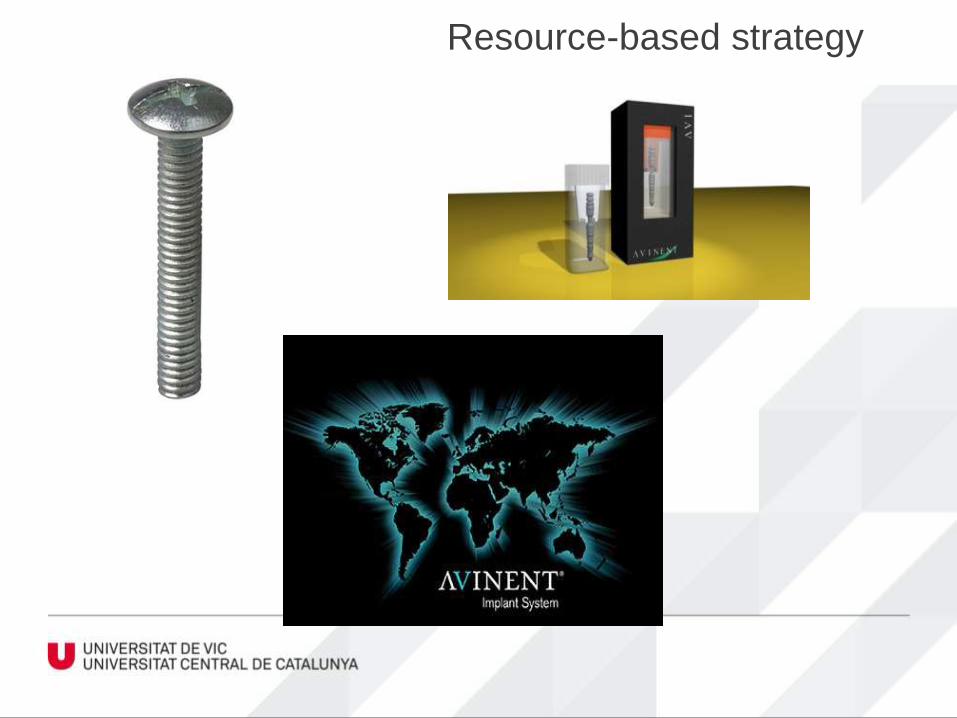

Resource-based strategy

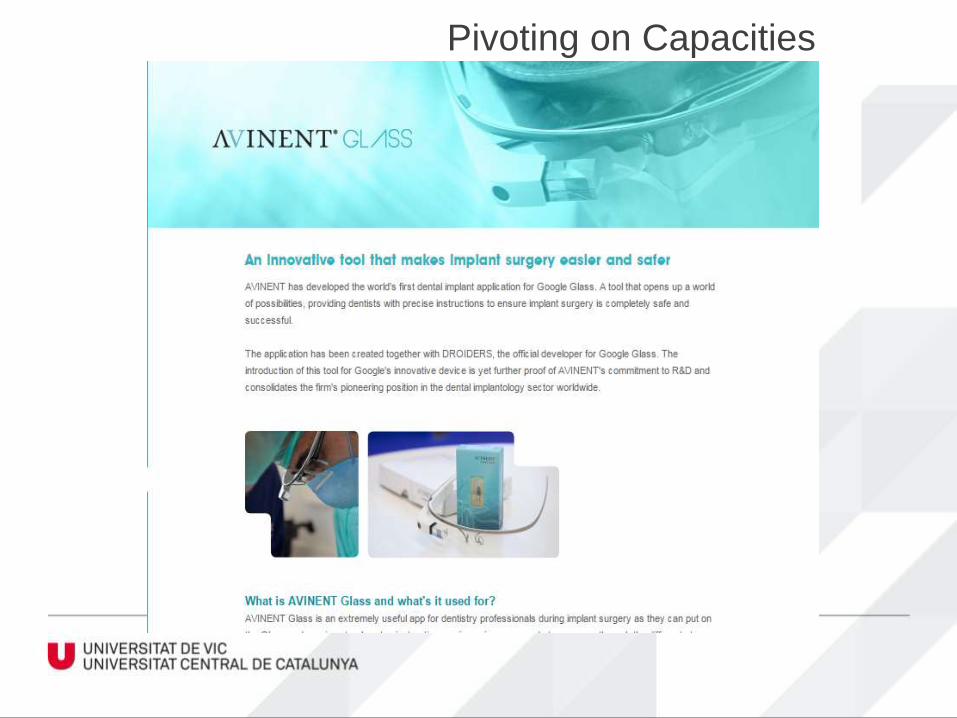

Pivoting on Capacities

Non-conventional

management

Innovative leadership

Creativity

Exploration teams

Open Innovation

(outsiders)

Exponentian thinking

New competence building

Incremental vs radical innovation

(Ambidexterity: exploting vs

exploring)

30% 40%40%20%

10%

# 1 EEUU

“Para competir con los líderes hay que

hacer lo que hacen ellos, no lo que

dicen que hacen”

Mariana Mazzucato, SPRU (Science Policy Research Unit, Sussex

University).

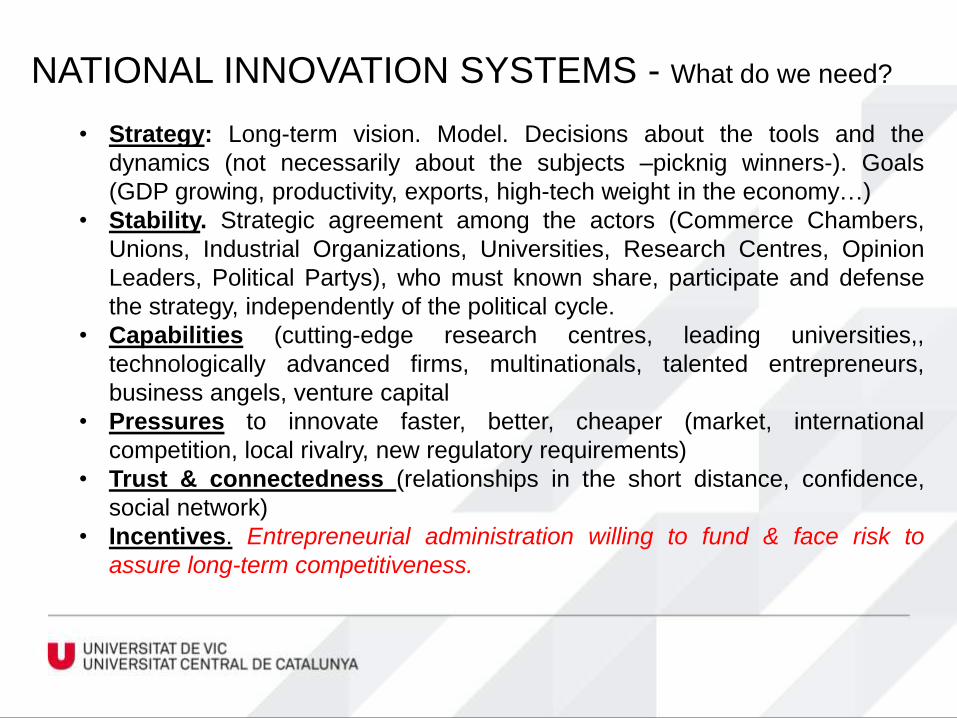

• Strategy: Long-term vision. Model. Decisions about the tools and the

dynamics (not necessarily about the subjects –picknig winners-). Goals

(GDP growing, productivity, exports, high-tech weight in the economy…)

• Stability. Strategic agreement among the actors (Commerce Chambers,

Unions, Industrial Organizations, Universities, Research Centres, Opinion

Leaders, Political Partys), who must known share, participate and defense

the strategy, independently of the political cycle.

• Capabilities (cutting-edge research centres, leading universities,,

technologically advanced firms, multinationals, talented entrepreneurs,

business angels, venture capital

• Pressures to innovate faster, better, cheaper (market, international

competition, local rivalry, new regulatory requirements)

• Trust & connectedness (relationships in the short distance, confidence,

social network)

• Incentives. Entrepreneurial administration willing to fund & face risk to

assure long-term competitiveness.

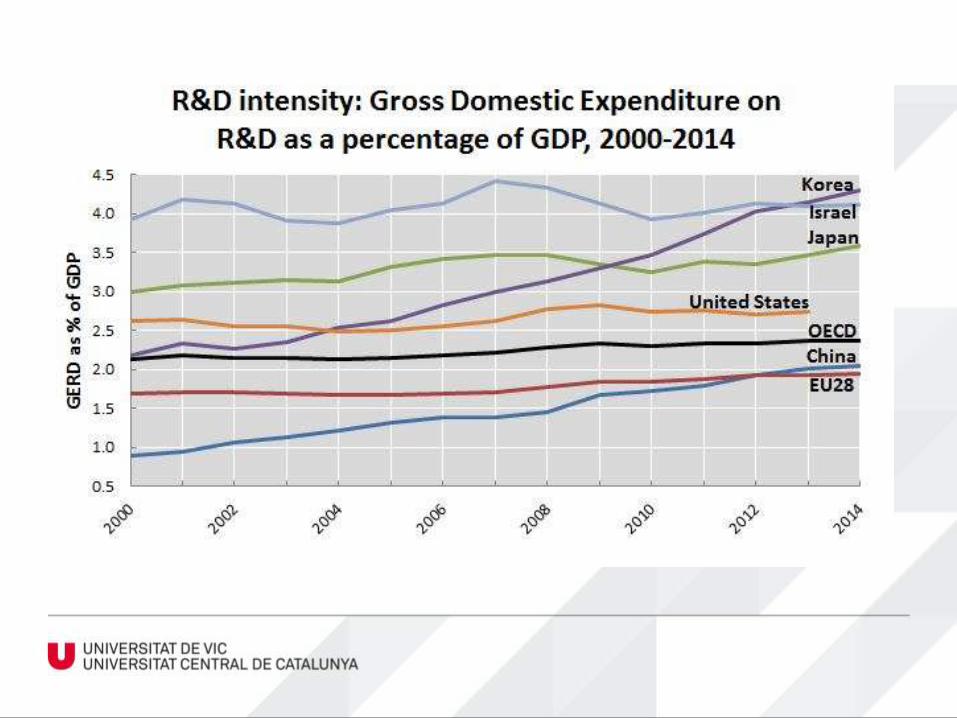

NATIONAL INNOVATION SYSTEMS - What do we need?

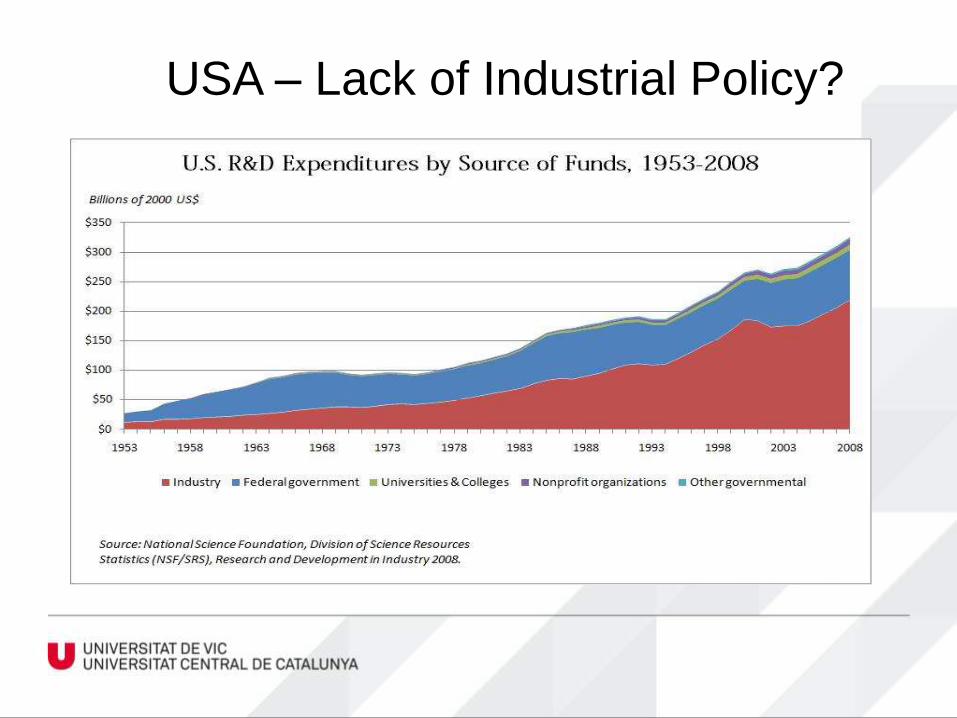

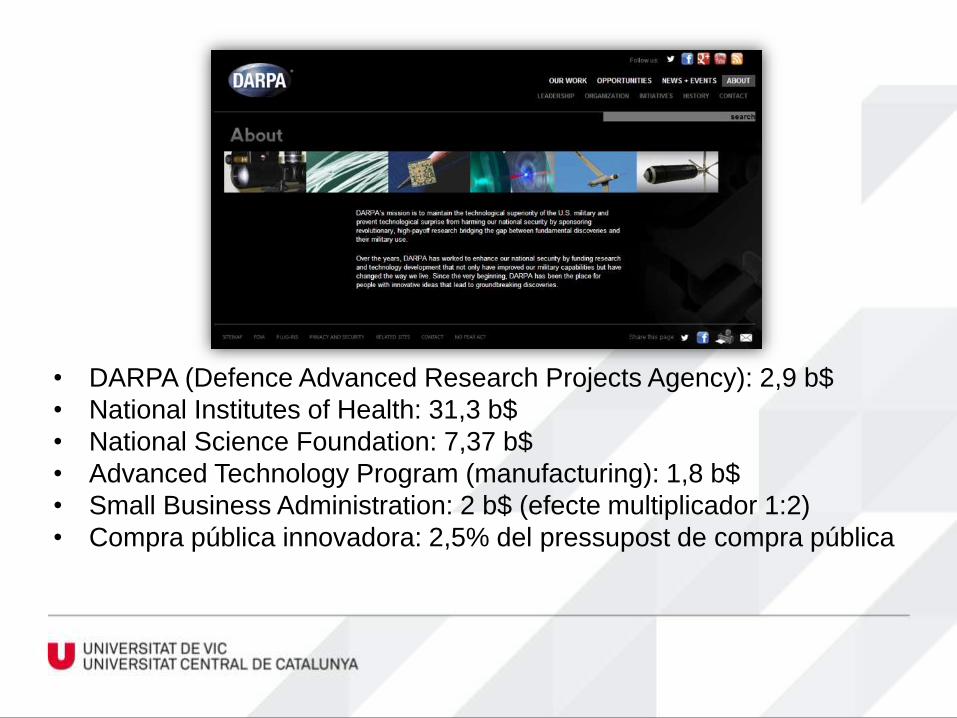

USA – Lack of Industrial Policy?

• DARPA (Defence Advanced Research Projects Agency): 2,9 b$

• National Institutes of Health: 31,3 b$

• National Science Foundation: 7,37 b$

• Advanced Technology Program (manufacturing): 1,8 b$

• Small Business Administration: 2 b$ (efecte multiplicador 1:2)

• Compra pública innovadora: 2,5% del pressupost de compra pública

Total budget:

18.000 M US $

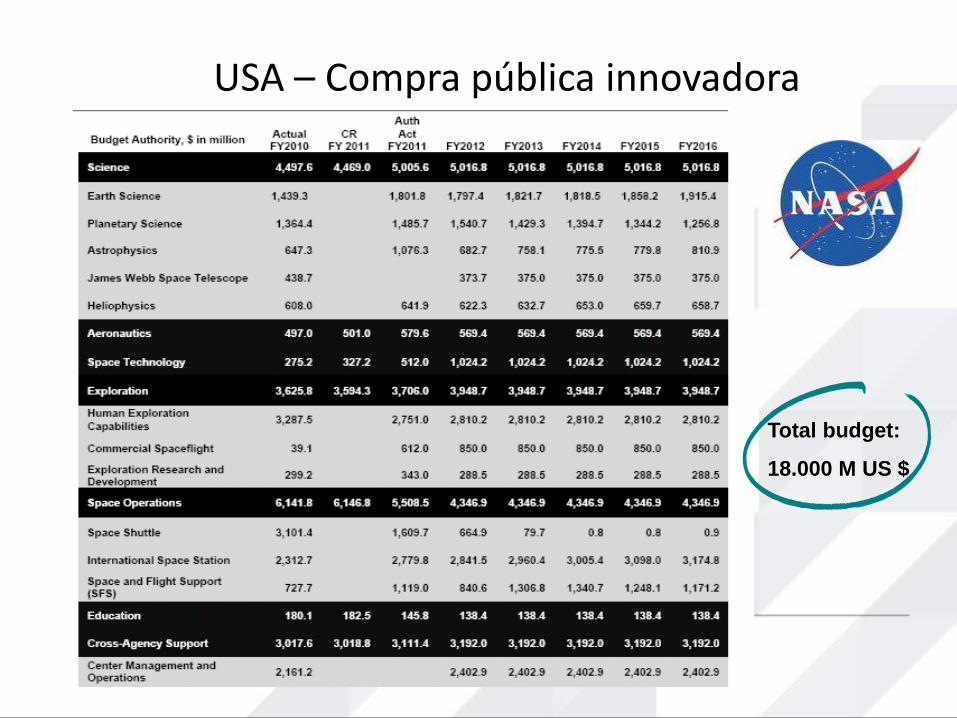

USA – Compra pública innovadora

Israel – Start-Up Nation

The World Economic Forum has designated Israel as one of the leading countries in the world in technological innovation. In the 2010-2011 WEF Global Competitive Index Report, Israel received an overall rank of the 24th most competitive country.

Israeli highlights from IMD World Competitiveness Yearbook include:

ranked 1st for total expenditure on R&D

ranked 1st for business expenditure on R&D

ranked 1st for availability of qualified scientists and engineers

ranked 2nd for venture capital availability

ranked 2nd for information technology skills

ranked 3rd for Quality of Scientific Research Organizations

ranked 3rd for Registered Patents Per Capita

ranked 3rd for flexibility and availability of the workforce

ranked 4th for higher education achievements

ranked 6th for overall innovation

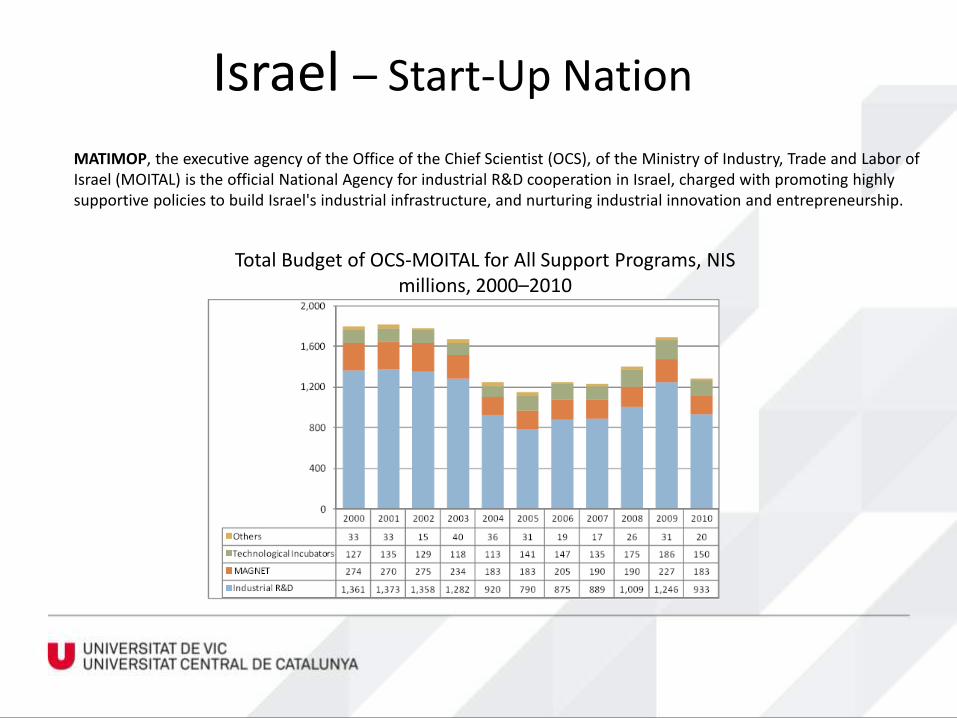

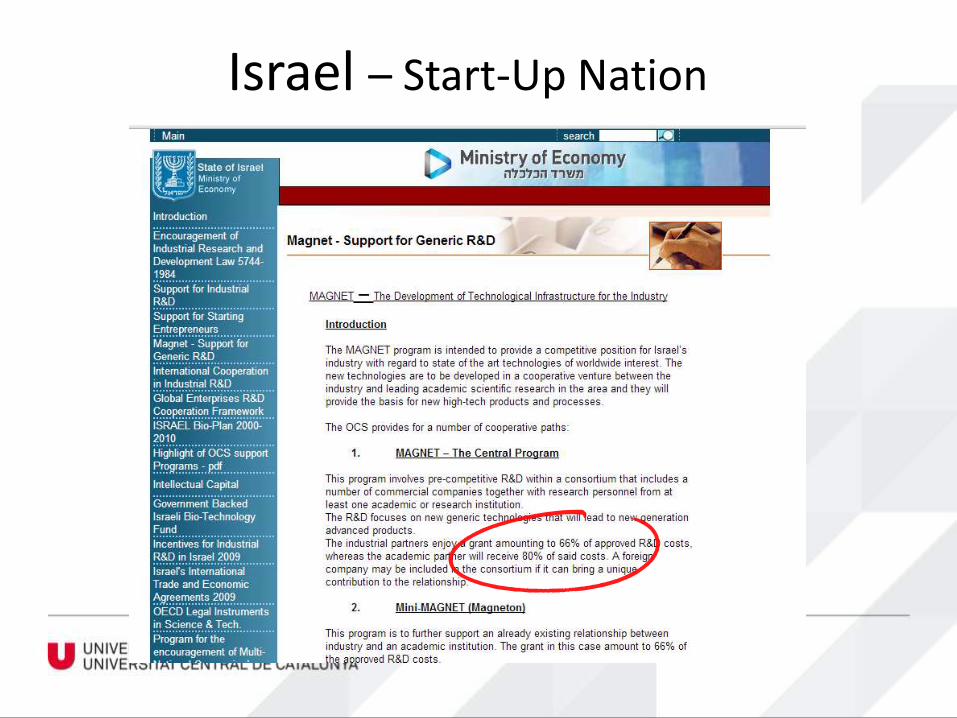

MATIMOP, the executive agency of the Office of the Chief Scientist (OCS), of the Ministry of Industry, Trade and Labor of Israel (MOITAL) is the official National Agency for industrial R&D cooperation in Israel, charged with promoting highly supportive policies to build Israel's industrial infrastructure, and nurturing industrial innovation and entrepreneurship.

Total Budget of OCS-MOITAL for All Support Programs, NIS millions, 2000–2010

Israel – Start-Up Nation

Israel – Start-Up Nation

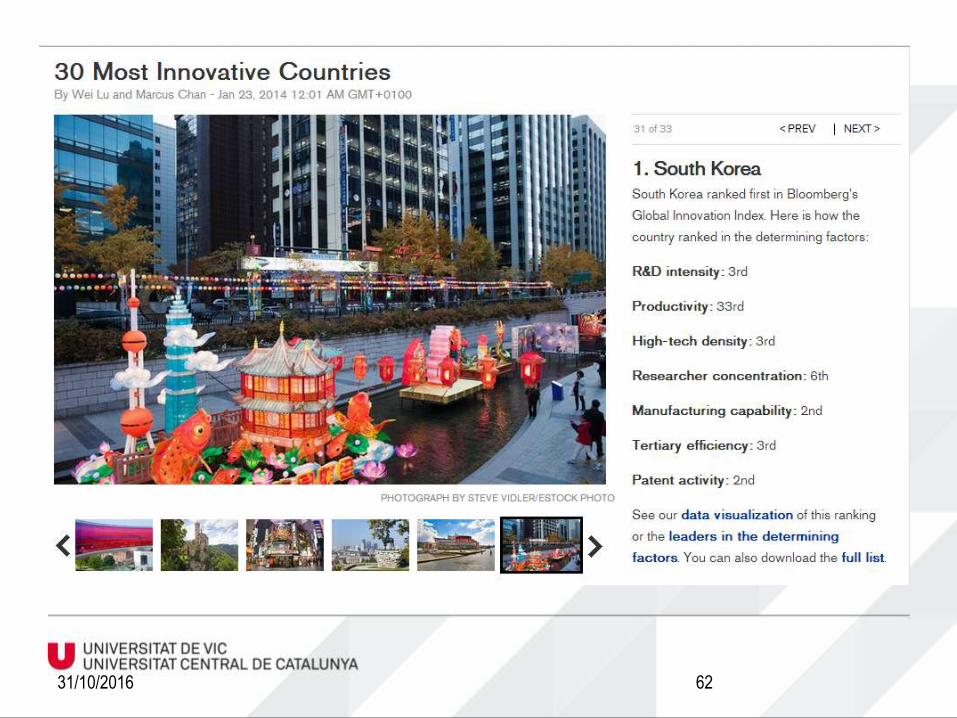

# 2 ASIA

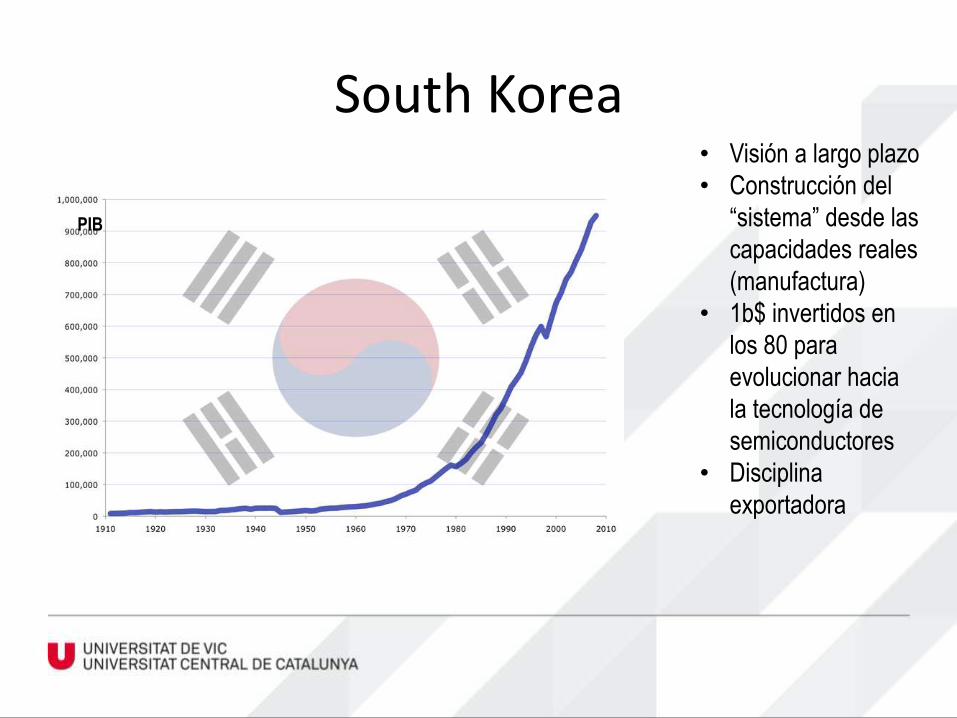

South Korea• Visión a largo plazo

• Construcción del

“sistema” desde las

capacidades reales

(manufactura)

• 1b$ invertidos en

los 80 para

evolucionar hacia

la tecnología de

semiconductores

• Disciplina

exportadora

PIB

31/10/2016 62

63

Singapur

# 3 Norte de

Europa

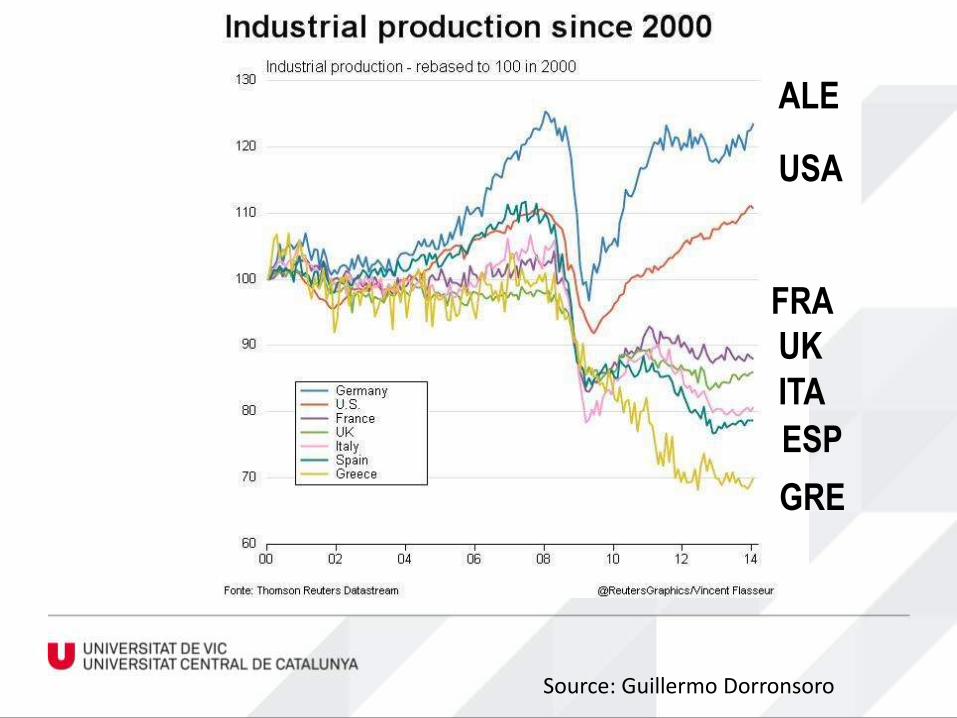

USA

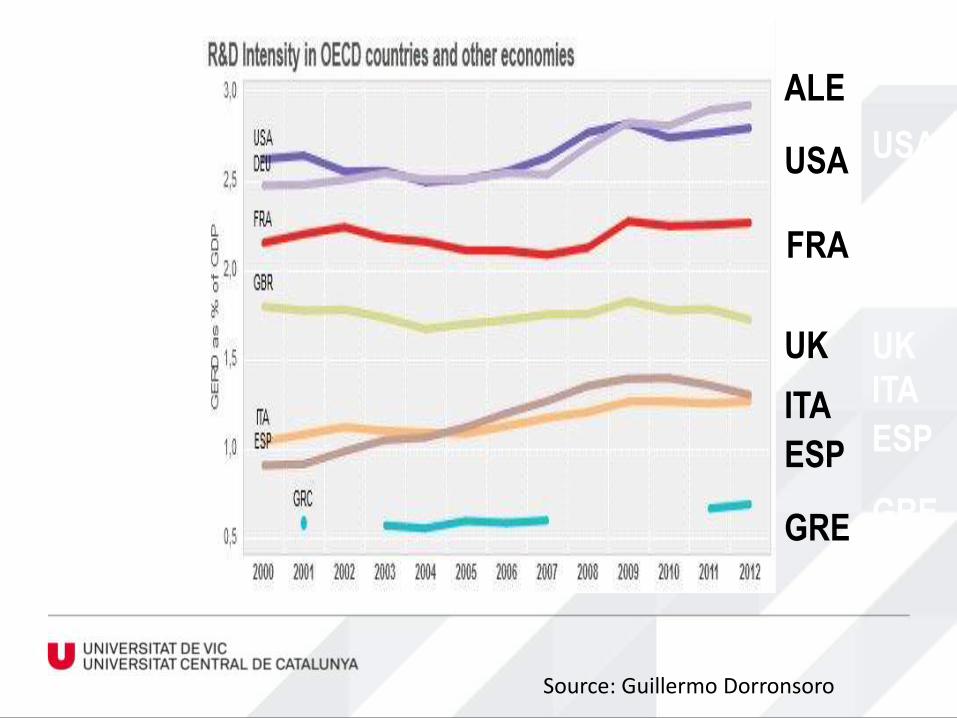

ALE

FRA

UK

ITA

ESP

GRE

USA

ALE

FRA

UK

ITA

ESP

GRE

Source: Guillermo Dorronsoro

ALE

USA

ALE

FRA

UK

ITA

ESP

GRE

Source: Guillermo Dorronsoro

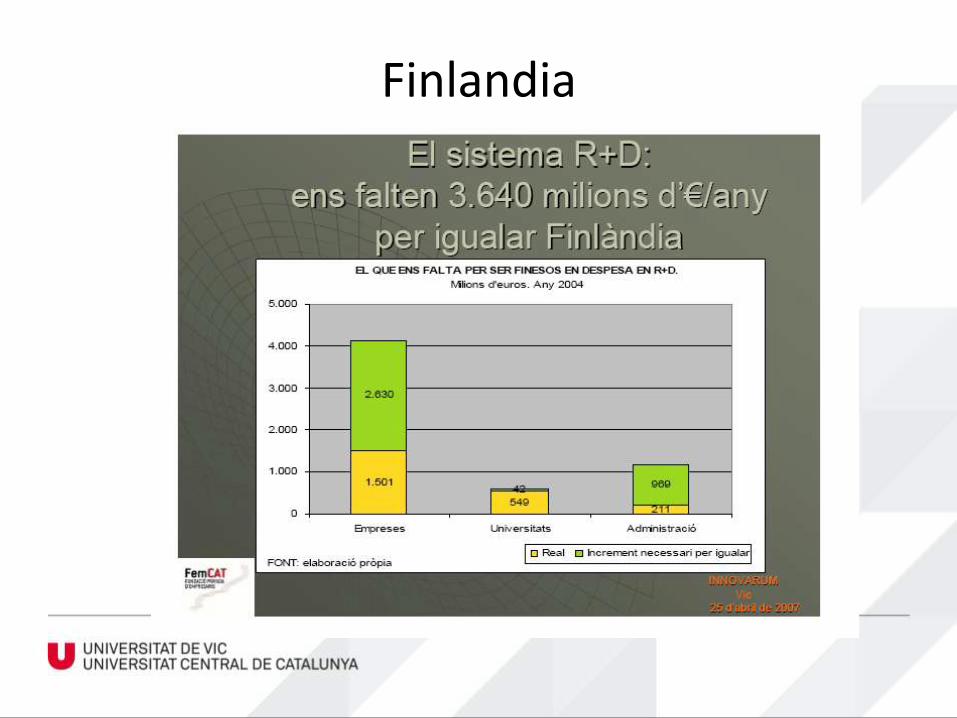

Finlandia

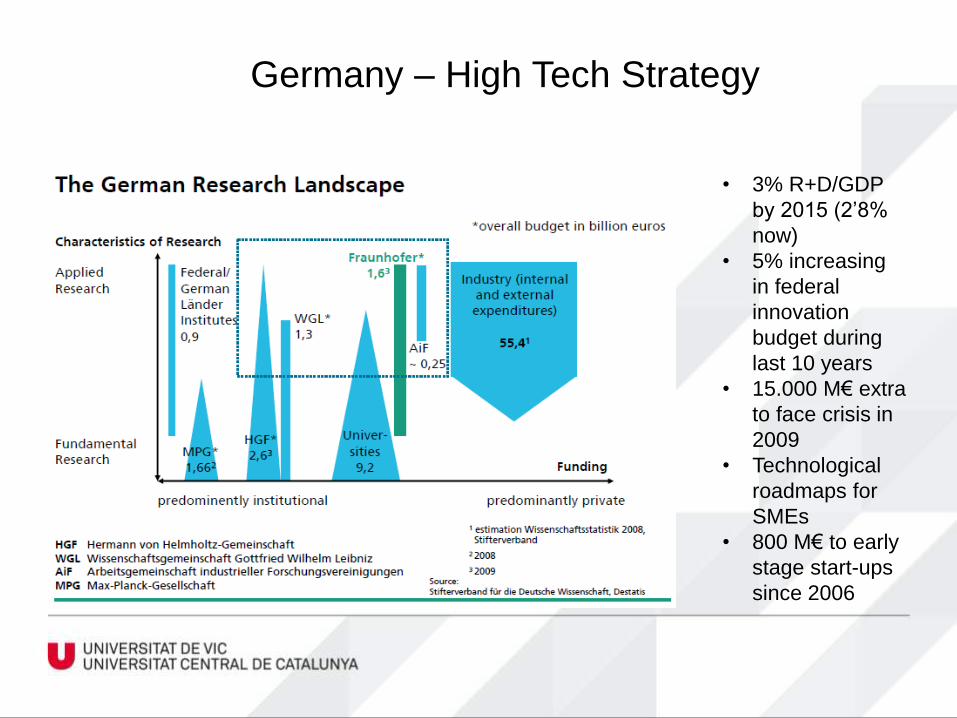

Germany – High Tech Strategy

• 3% R+D/GDP

by 2015 (2’8%

now)

• 5% increasing

in federal

innovation

budget during

last 10 years

• 15.000 M€ extra

to face crisis in

2009

• Technological

roadmaps for

SMEs

• 800 M€ to early

stage start-ups

since 2006

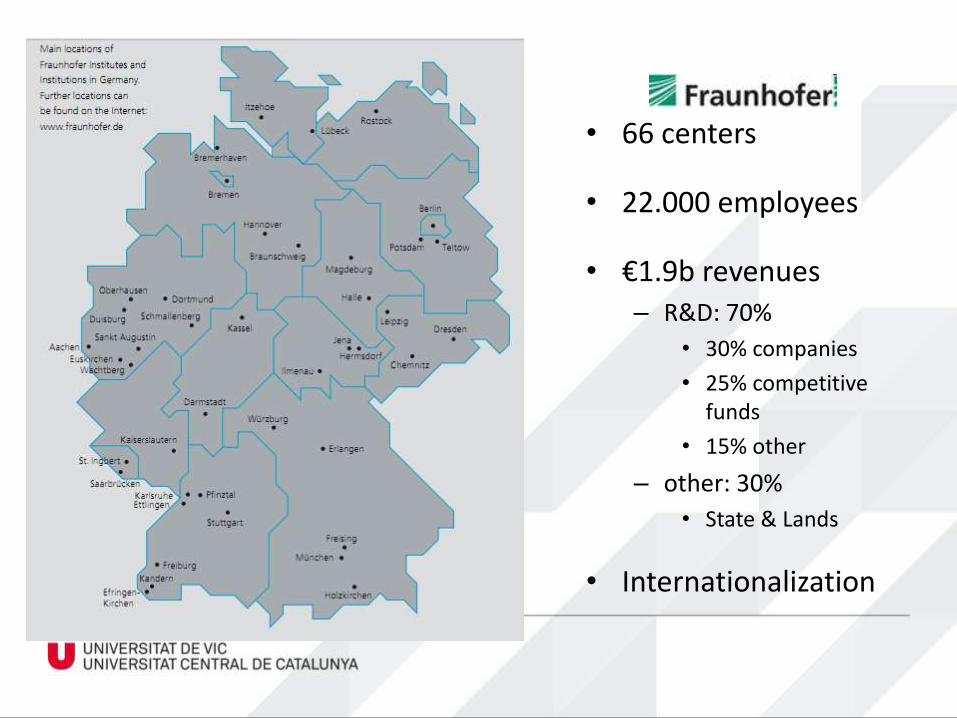

• 66 centers

• 22.000 employees

• €1.9b revenues– R&D: 70%

• 30% companies

• 25% competitive funds

• 15% other

– other: 30%

• State & Lands

• Internationalization

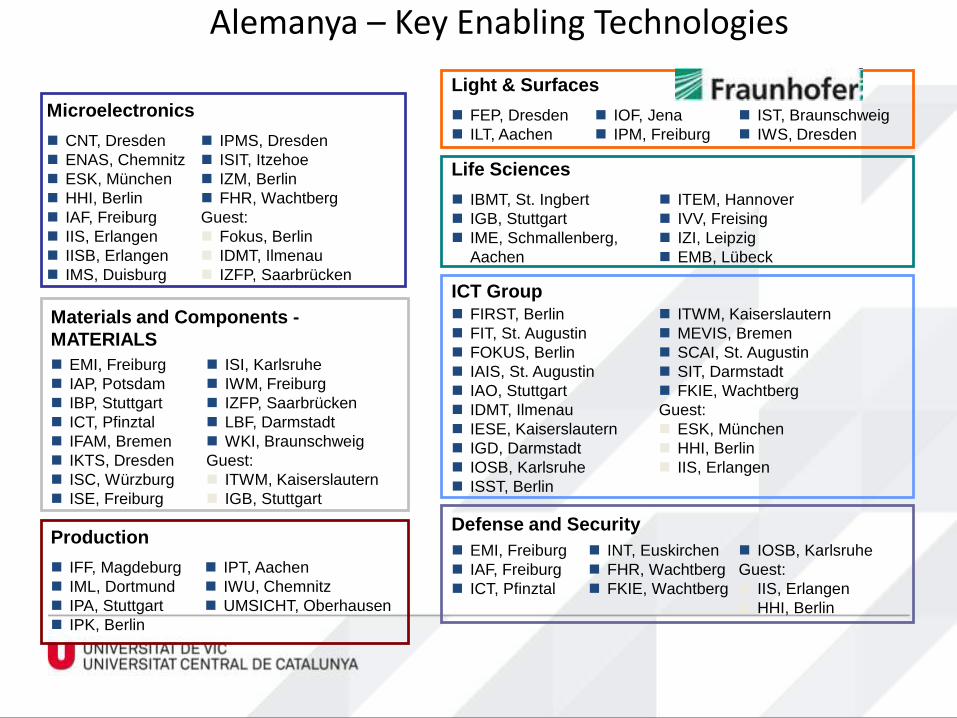

Materials and Components -

MATERIALS

EMI, Freiburg

IAP, Potsdam

IBP, Stuttgart

ICT, Pfinztal

IFAM, Bremen

IKTS, Dresden

ISC, Würzburg

ISE, Freiburg

ISI, Karlsruhe

IWM, Freiburg

IZFP, Saarbrücken

LBF, Darmstadt

WKI, Braunschweig

Guest:

ITWM, Kaiserslautern

IGB, Stuttgart

Production

IFF, Magdeburg

IML, Dortmund

IPA, Stuttgart

IPK, Berlin

IPT, Aachen

IWU, Chemnitz

UMSICHT, Oberhausen

Microelectronics

CNT, Dresden

ENAS, Chemnitz

ESK, München

HHI, Berlin

IAF, Freiburg

IIS, Erlangen

IISB, Erlangen

IMS, Duisburg

IPMS, Dresden

ISIT, Itzehoe

IZM, Berlin

FHR, Wachtberg

Guest:

Fokus, Berlin

IDMT, Ilmenau

IZFP, Saarbrücken

Light & Surfaces

FEP, Dresden

ILT, Aachen

IOF, Jena

IPM, Freiburg

IST, Braunschweig

IWS, Dresden

Life Sciences

IBMT, St. Ingbert

IGB, Stuttgart

IME, Schmallenberg,

Aachen

ITEM, Hannover

IVV, Freising

IZI, Leipzig

EMB, Lübeck

ICT Group FIRST, Berlin

FIT, St. Augustin

FOKUS, Berlin

IAIS, St. Augustin

IAO, Stuttgart

IDMT, Ilmenau

IESE, Kaiserslautern

IGD, Darmstadt

IOSB, Karlsruhe

ISST, Berlin

ITWM, Kaiserslautern

MEVIS, Bremen

SCAI, St. Augustin

SIT, Darmstadt

FKIE, Wachtberg

Guest:

ESK, München

HHI, Berlin

IIS, Erlangen

Defense and Security

EMI, Freiburg

IAF, Freiburg

ICT, Pfinztal

INT, Euskirchen

FHR, Wachtberg

FKIE, Wachtberg

IOSB, Karlsruhe

Guest:

IIS, Erlangen

HHI, Berlin

Alemanya – Key Enabling Technologies

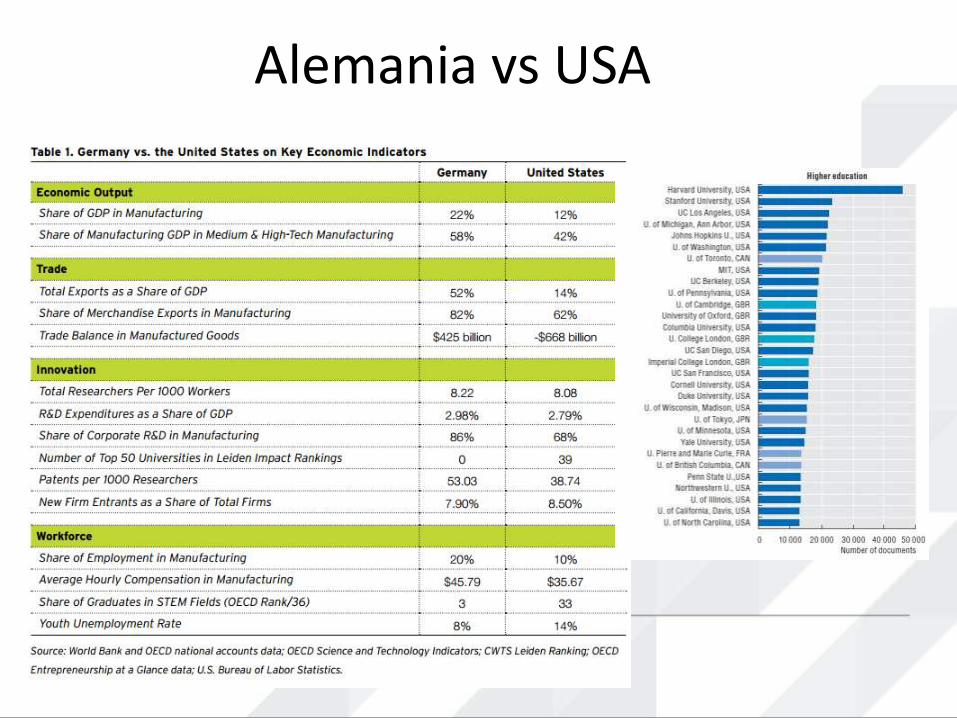

Alemania vs USA

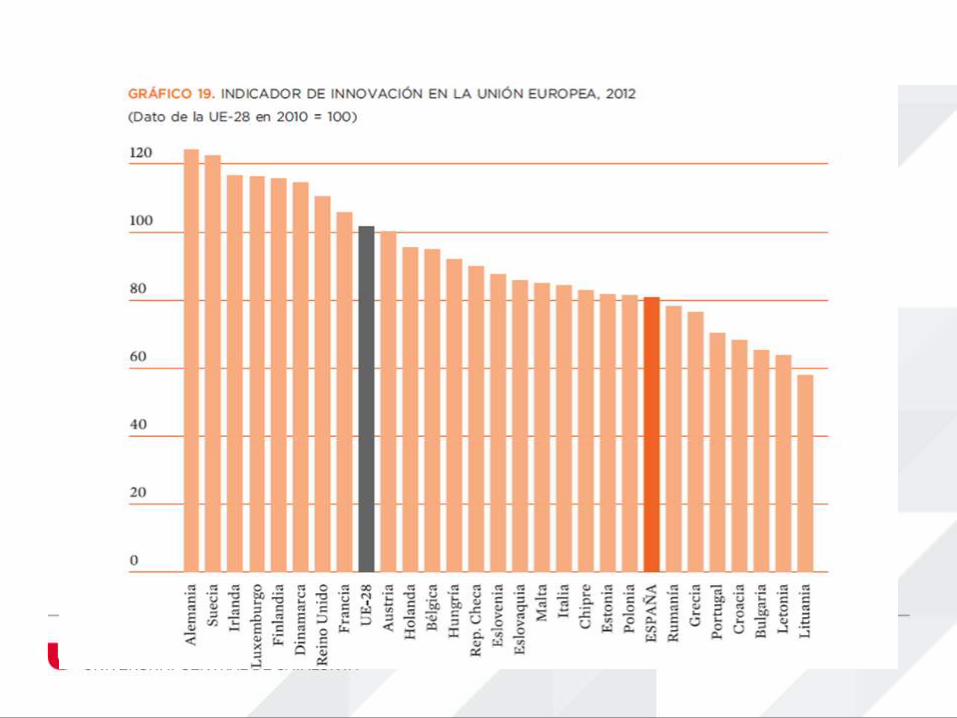

# 4 Sur de Europa

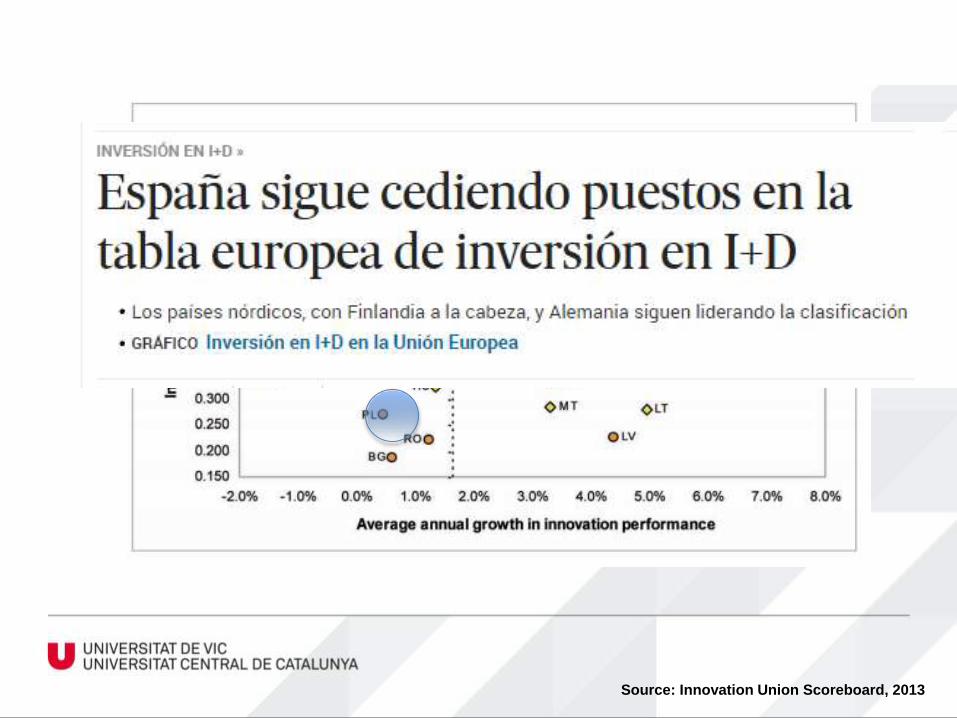

Source: Innovation Union Scoreboard, 2013

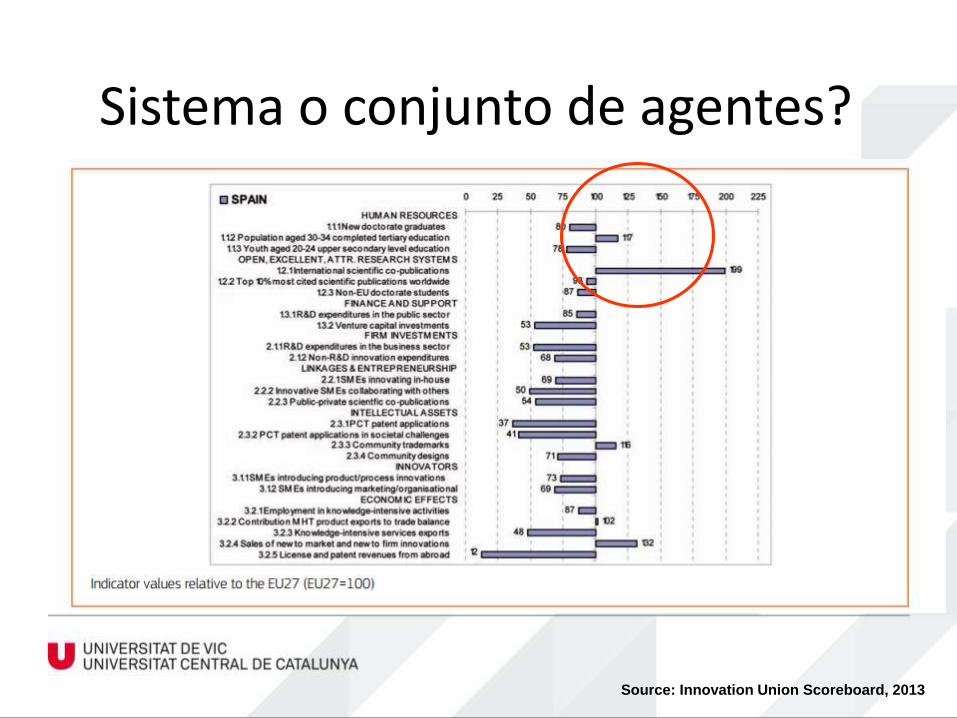

Sistema o conjunto de agentes?

Source: Innovation Union Scoreboard, 2013

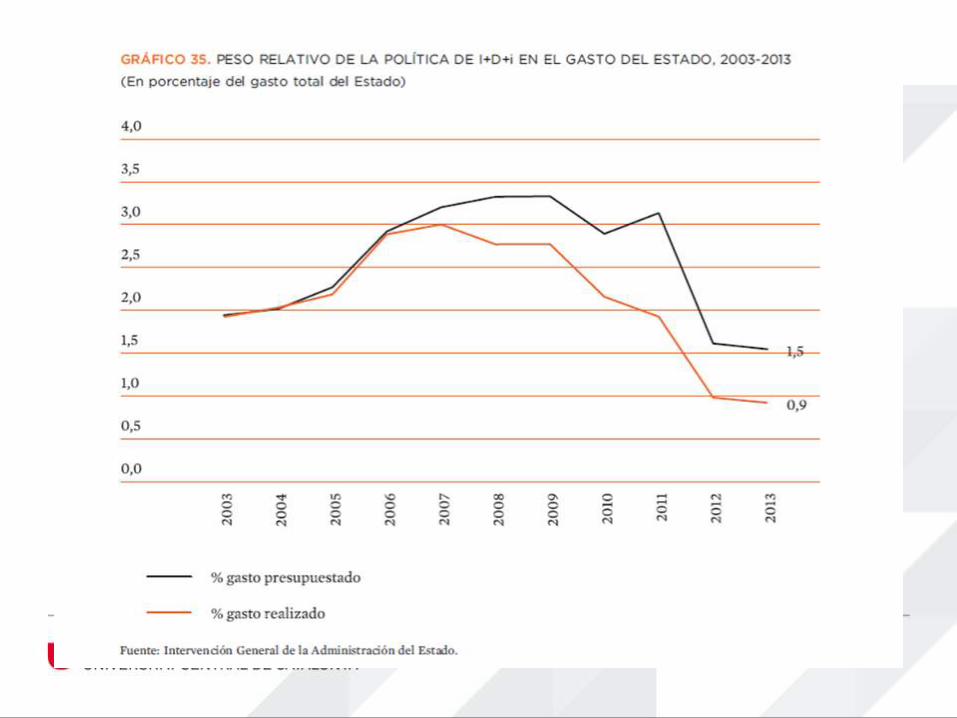

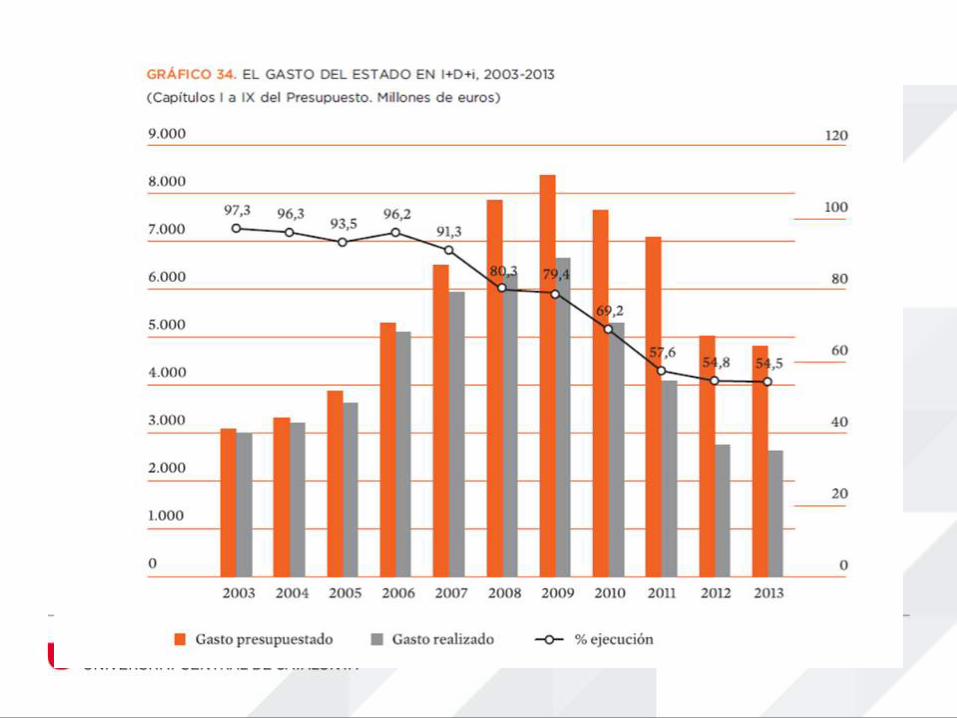

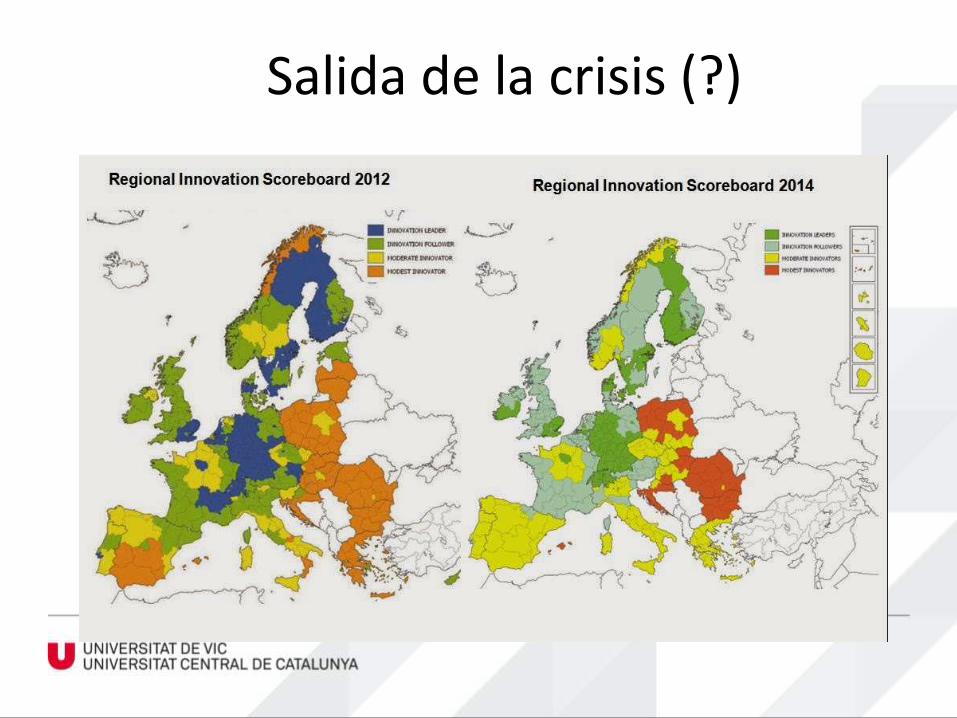

Salida de la crisis (?)

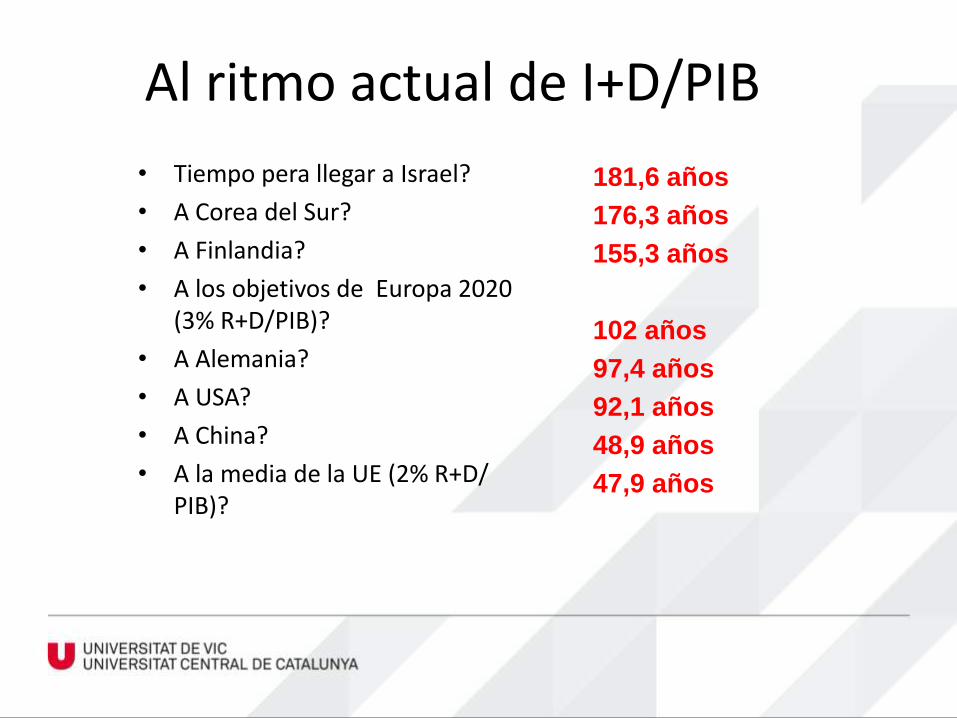

• Tiempo pera llegar a Israel?

• A Corea del Sur?

• A Finlandia?

• A los objetivos de Europa 2020 (3% R+D/PIB)?

• A Alemania?

• A USA?

• A China?

• A la media de la UE (2% R+D/ PIB)?

Al ritmo actual de I+D/PIB

181,6 años

176,3 años

155,3 años

102 años

97,4 años

92,1 años

48,9 años

47,9 años

En investigación e innovación solo

queda un camino:

Seguir adelante, con más excelencia,

más esfuerzo y más compromiso

Thanks for your attention!

Xavier Ferràs

@XavierFerras

LinkedIn Me!!!!