Embed Size (px)

Citation preview

Closing Retail Sales In-Store: Two Ways to Fight Back With Mobile

A Frost & Sullivan White Paper

frost.com

contents

Introduction ................................................................................................................................... 3

Harness Mobile to Keep Sales In-Store ...................................................................................... 3

Tablet POS Solutions: Engaging Seamlessly ............................................................................... 4

Mobile Payment: Good, but Not Great ...................................................................................... 5

Samsung Pay: Innovative, Ubiquitous, Disruptive ..................................................................... 6

Mobile Technology Wins in Retail ................................................................................................ 7

3

Closing Retail Sales In-Store: Two Ways to Fight Back With Mobile

All rights reserved © 2016 Frost & Sullivan

IntroductIon

Brick-and-mortar retailers are in a fight for their lives — competing against new channels, trying to satisfy demanding consumers, and dealing with worrisome profit margins.

Mobile technology is often portrayed negatively in this scenario, painted as one of many competitive bandits stealing sales away from today’s store owners. However, innovative retailers realize that there’s another side to the mobility coin— a side that uses mobile and wireless technology to actually enhance the in-store shopping experience and entice the customer to stay and buy.

This paper suggests two mobile solutions for the retailer’s consideration. The first leverages tablet devices and the second introduces Samsung Pay, a service that dispenses with the NFC requirement and finally allows almost any retailer to offer a quick and convenient mobile payment option to its customers.

Harness MobIle to Keep sales In-store

Customers want to be knowledgeable; they want to make good purchase decisions. To do that, they’ll take the time to search for information and explore multiple sources. Many shoppers begin their purchase journey online, browse through the data and the various pitches, and then either choose to buy on a website or decide to do further reconnaissance in a brick-and-mortar store.

Other buyers’ omni-channel shopping excursion takes a reverse path, with the consumer first visiting a retailer’s physical location to gather product information and insights and then going— and staying — online to make the actual purchase.

Whatever the individual approach, retailers now have the opportunity to leverage mobile technology to enhance each customer’s in-store shopping experience and to close the sale onsite. Savvy store owners have begun using mobile products to actively engage shoppers and encourage purchase decision-making while still in the store. Two of these retail-friendly mobile solutions offer special promise:

• Tablets at the point of sale

• Mobile payments made easy and ubiquitous

Properly implemented, both of these solutions offer a win-win opportunity. With more information and convenience at their fingertips, customers enjoy an improved in-store shopping experience. And, as a result, the retailer sees both in-store sales and conversion rates increase.

4

frost.com

All rights reserved © 2016 Frost & Sullivan

tablet pos solutIons: engagIng seaMlessly

It has become instinct. Thinking of buying a product or service? Consumers don’t consider their research complete until they search in a retail store or two and also check online for the best prices, the best product match, and the best messaging. Once online, many stay at the website to make the actual purchase. The challenge for retailers is to differentiate their in-store experience in ways that draw customers in and then seamlessly engage with them to close the sale on a face-to-face basis. Tablets, strategically located in a display or in the sales rep’s hand, can do just that, keeping both the customer and the purchase in the store.

If there was ever a device made for the retail environment, the tablet form factor takes first honors. Less than a pound in weight, easy to hold in one hand, and offering a crisp, clear display, these devices directly engage the customer.

Tablets can be used in both stationary and mobile modes:

• Tablets that are available for customer access are typically anchored to a display or kiosk. They can be programmed to provide a range of capabilities, all designed to entice the customer and score a sale. Some function as a one-way digital merchandising display that offers pre-programmed content on preselected topics. But the most highly valued tablet solutions provide a two-way experience, allowing the shopper to research a product themselves or access an online expert for the kind of detailed assistance that not every onsite sales associate is trained to provide.

• Tablets can also act as a mobile sales assistant for store personnel, allowing the store manager or sales rep to look up inventory while on the sales floor, enter customer orders for products that may be out of stock or not carried in their store, and even provide product comparisons and demos for more complex items. If the retailer normally provides a personal shopping or clientelling experience, then the tablet can even function as a convenient repository for specific customer information regarding past purchases, color and style preferences, etc.

The tablet form factor is appearing in a wide range of industries, but is especially relevant in retail. Prices are affordable, even in the retail world of tight margins and challenging budgets. And, very importantly, these devices are familiar and easy to use by both shoppers and employees. From an administrative perspective, tablets are simple to deploy and maintain, especially with cloud-based software that is managed and updated off-site. Looking forward, innovative new technology such as augmented reality (AR) promises to make tablets—and the in-store shopping experience — even more compelling and enjoyable for customers.

Retailers that haven’t yet implemented tablets onsite should step back, evaluate their current selling process and flow, and consider piloting a tablet solution with their customers and associates.

5

Closing Retail Sales In-Store: Two Ways to Fight Back With Mobile

All rights reserved © 2016 Frost & Sullivan

MobIle payMent: good, but not great

Today’s shoppers have little patience for delay or complication. They want to find their items quickly, receive their services immediately, and then enjoy fast and convenient check out. Often, the anticipated retail check-out experience alone is enough to convince consumers to stay home, fire up their laptops, and shop online.

Now, due to innovations in information and communications technologies, retailers are able to introduce the mobile payment option to their customers, leveraging the shopper’s smartphone to expedite and simplify the actual in-store purchase process.

How does the mobile payment process work? It starts with the shopper’s smartphone and the specific mobile payment app that has been downloaded to that phone. The service then allows users to purchase products and services at participating retailers by pulling up the app and simply waving or tapping their phones against the store’s payment terminal. The charge is then applied against the debit or credit card the shopper has on file.

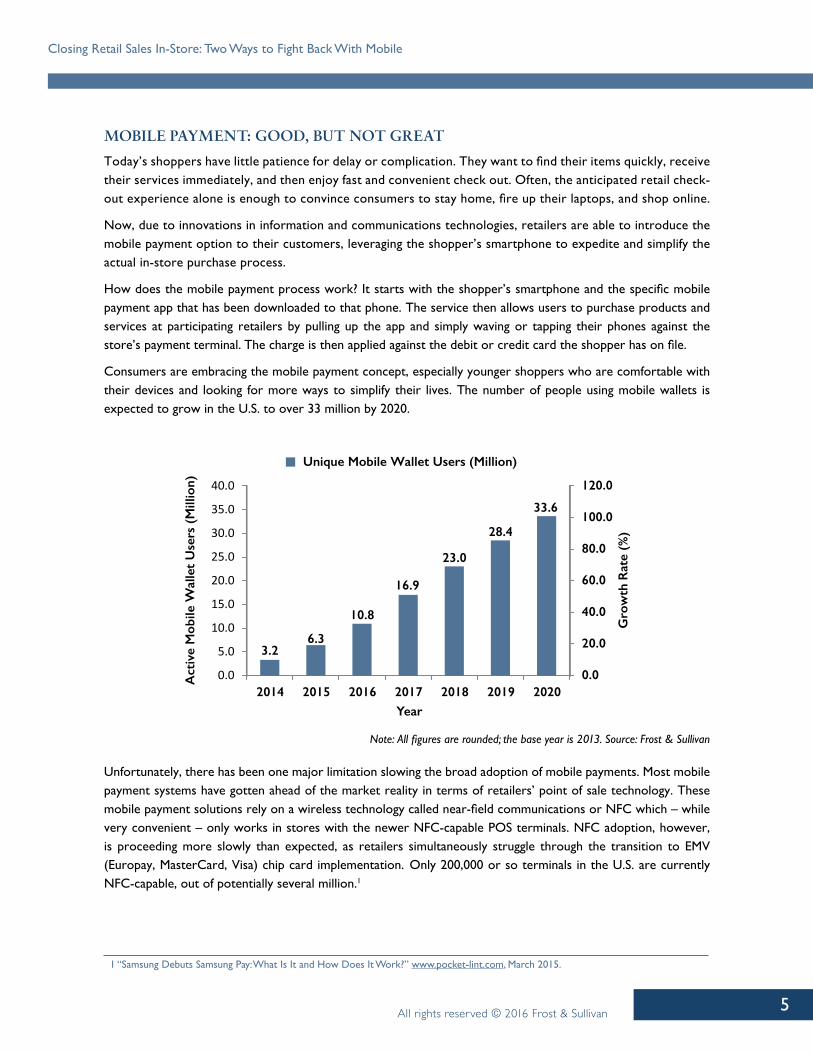

Consumers are embracing the mobile payment concept, especially younger shoppers who are comfortable with their devices and looking for more ways to simplify their lives. The number of people using mobile wallets is expected to grow in the U.S. to over 33 million by 2020.

3.26.3

10.8

16.9

23.0

28.4

33.6

0.0

20.0

40.0

60.0

80.0

100.0

120.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2014 2015 2016 2017 2018 2019 2020

Gro

wth

Rat

e (%

)

Act

ive

Mob

ile W

alle

t U

sers

(M

illio

n)

Year

Unique Mobile Wallet Users (Million)

Note: All figures are rounded; the base year is 2013. Source: Frost & Sullivan

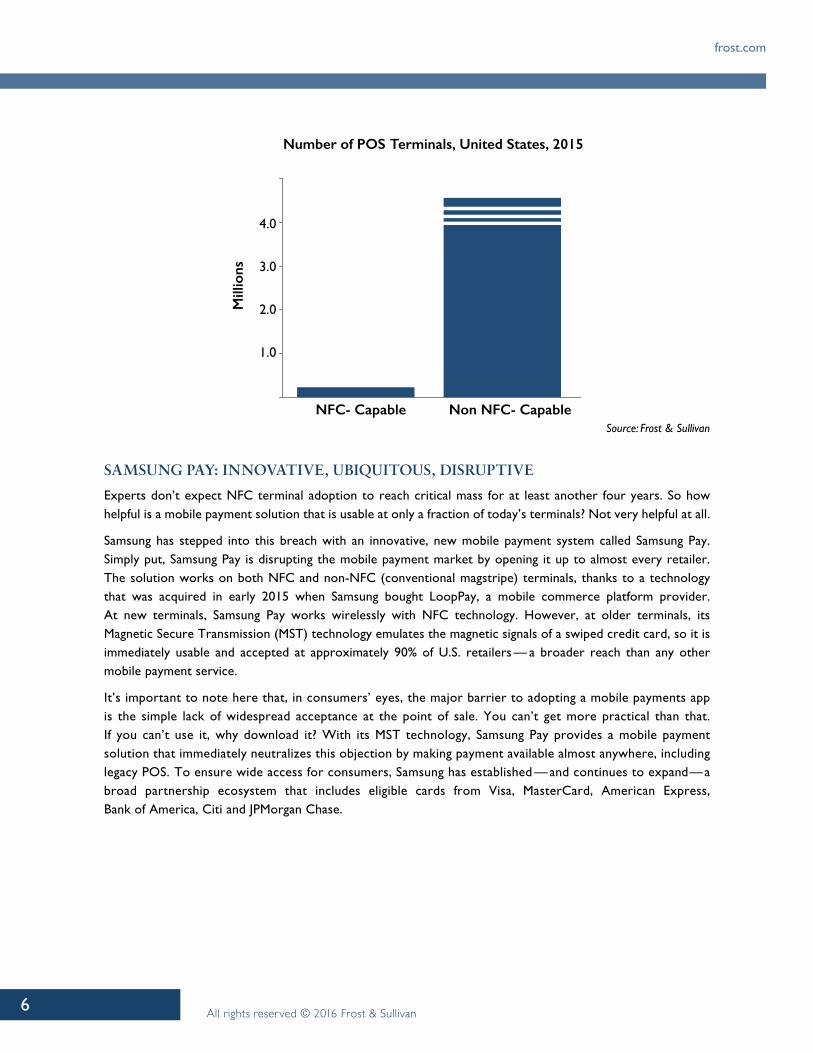

Unfortunately, there has been one major limitation slowing the broad adoption of mobile payments. Most mobile payment systems have gotten ahead of the market reality in terms of retailers’ point of sale technology. These mobile payment solutions rely on a wireless technology called near-field communications or NFC which – while very convenient – only works in stores with the newer NFC-capable POS terminals. NFC adoption, however, is proceeding more slowly than expected, as retailers simultaneously struggle through the transition to EMV (Europay, MasterCard, Visa) chip card implementation. Only 200,000 or so terminals in the U.S. are currently NFC-capable, out of potentially several million.1

1 “Samsung Debuts Samsung Pay: What Is It and How Does It Work?” www.pocket-lint.com, March 2015.

6

frost.com

All rights reserved © 2016 Frost & Sullivan

Number of POS Terminals, United States, 2015

Mill

ions

NFC- Capable Non NFC- Capable

4.0

3.0

2.0

1.0

Source: Frost & Sullivan

saMsung pay: InnovatIve, ubIquItous, dIsruptIve

Experts don’t expect NFC terminal adoption to reach critical mass for at least another four years. So how helpful is a mobile payment solution that is usable at only a fraction of today’s terminals? Not very helpful at all.

Samsung has stepped into this breach with an innovative, new mobile payment system called Samsung Pay. Simply put, Samsung Pay is disrupting the mobile payment market by opening it up to almost every retailer. The solution works on both NFC and non-NFC (conventional magstripe) terminals, thanks to a technology that was acquired in early 2015 when Samsung bought LoopPay, a mobile commerce platform provider. At new terminals, Samsung Pay works wirelessly with NFC technology. However, at older terminals, its Magnetic Secure Transmission (MST) technology emulates the magnetic signals of a swiped credit card, so it is immediately usable and accepted at approximately 90% of U.S. retailers — a broader reach than any other mobile payment service.

It’s important to note here that, in consumers’ eyes, the major barrier to adopting a mobile payments app is the simple lack of widespread acceptance at the point of sale. You can’t get more practical than that. If you can’t use it, why download it? With its MST technology, Samsung Pay provides a mobile payment solution that immediately neutralizes this objection by making payment available almost anywhere, including legacy POS. To ensure wide access for consumers, Samsung has established — and continues to expand—a broad partnership ecosystem that includes eligible cards from Visa, MasterCard, American Express, Bank of America, Citi and JPMorgan Chase.

7

Closing Retail Sales In-Store: Two Ways to Fight Back With Mobile

All rights reserved © 2016 Frost & Sullivan

Another perpetual concern—on the part of both shoppers and retailers—is data security. Samsung Pay, like its major competitors, authenticates transactions with a fingerprint scan. The user has been assigned a number unique to his or her smartphone as a substitute for the actual credit card number. This number is then paired with a one-time transaction code to complete a purchase. If the store’s system is hacked or the user’s smartphone stolen, the credit card number remains safe and unattainable.

The payment process itself is kept simple for the customer. Samsung summarizes it in four quick steps:

1. Swipe up from the home screen to open the Samsung Pay app.

2. Choose credit card.

3. Scan fingerprint on the Home button.

4. Tap phone to the payment terminal.

Samsung also provides a number of value-added services to support its Samsung Pay users, including card life management, transaction history on the device, and remote, cloud-based management. Gift card support is another feature built in for customer convenience.

With the NFC barrier neutralized, retailers are not required to do anything in order to support Samsung Pay. However, they can enhance both their tech-savvy credentials and the customer’s shopping experience by advertising the availability of Samsung Pay at their location.

In summary, Samsung Pay offers merchants quite a few advantages. It’s the type of ubiquitous, works almost anywhere solution that appeals to all generations of customers. It’s easy to use and speeds transaction time at checkout, reducing total transaction costs. It directly addresses and neutralizes worries around data security. And it promises to support additional services, such as loyalty and couponing, in the future.

Mobile payment, especially the Samsung Pay version of mobile payment, is just one more way to make in-store shopping a pleasant and fruitful experience for consumers. And by enabling this type of customer-centric payment solution, merchants boost their own brand image.

MobIle tecHnology WIns In retaIl

For retailers who don’t want to see potential sales drift out their doors, mobile solutions hold tremendous promise. Tablets at the point of sale can engage shoppers and close the deal. An innovative mobile payment service such as Samsung Pay can provide them with quick and easy check out. Combine the two – sales associates accepting mobile payments on their POS tablets – and retailers can make true mobile-to-mobile transactions and convenience become very real very quickly.

The bottom line with mobile: Customers are happy with their purchase experience, and retailers see in-store conversion rates and average order size increase.

For information regarding permission, write:Frost & Sullivan331 E. Evelyn Ave., Suite 100Mountain View, CA 94041

Silicon Valley331 E. Evelyn Ave., Suite 100Mountain View, CA 94041Tel 650.475.4500Fax 650.475.1570

San Antonio7550 West Interstate 10, Suite 400San Antonio, TX 78229Tel 210.348.1000 Fax 210.348.1003

London4 Grosvenor GardensLondon SW1W 0DHTel +44 (0)20 7343 8383Fax +44 (0)20 7730 3343

AucklandBahrainBangkokBeijingBengaluruBuenos AiresCape TownChennaiDammamDelhiDetroitDubai

FrankfurtHerzliyaHoustonIrvineIskander Malaysia/Johor BahruIstanbulJakartaKolkataKotte ColomboKuala LumpurLondonManhattan

MiamiMilanMoscowMountain ViewMumbaiOxfordParisPuneRockville CentreSan AntonioSão PauloSeoul

ShanghaiShenzhenSingaporeSydneyTaipeiTokyoTorontoValbonneWarsaw

Frost & Sullivan, the Growth Partnership Company, works in collaboration with clients to leverage visionary innovation that

addresses the global challenges and related growth opportunities that will make or break today’s market participants. For more than

50 years, we have been developing growth strategies for the Global 1000, emerging businesses, the public sector and the investment

community. Is your organization prepared for the next profound wave of industry convergence, disruptive technologies, increasing

competitive intensity, Mega Trends, breakthrough best practices, changing customer dynamics and emerging economies?