Embed Size (px)

Citation preview

Karen Friedman

EVP & Policy Director

Pension Rights Center (PRC)

CLOSING DISCUSSION:

Future of Retirement Solutions

Gordon Clark

Professor & Director-Smith School of Enterprise & the Environment

University of Oxford

CLOSING DISCUSSION:

Future of Retirement Solutions

Ash Williams

Executive Director & CIO

State Board of Administration of Florida

CLOSING DISCUSSION:

Future of Retirement Solutions

Florida Retirement System

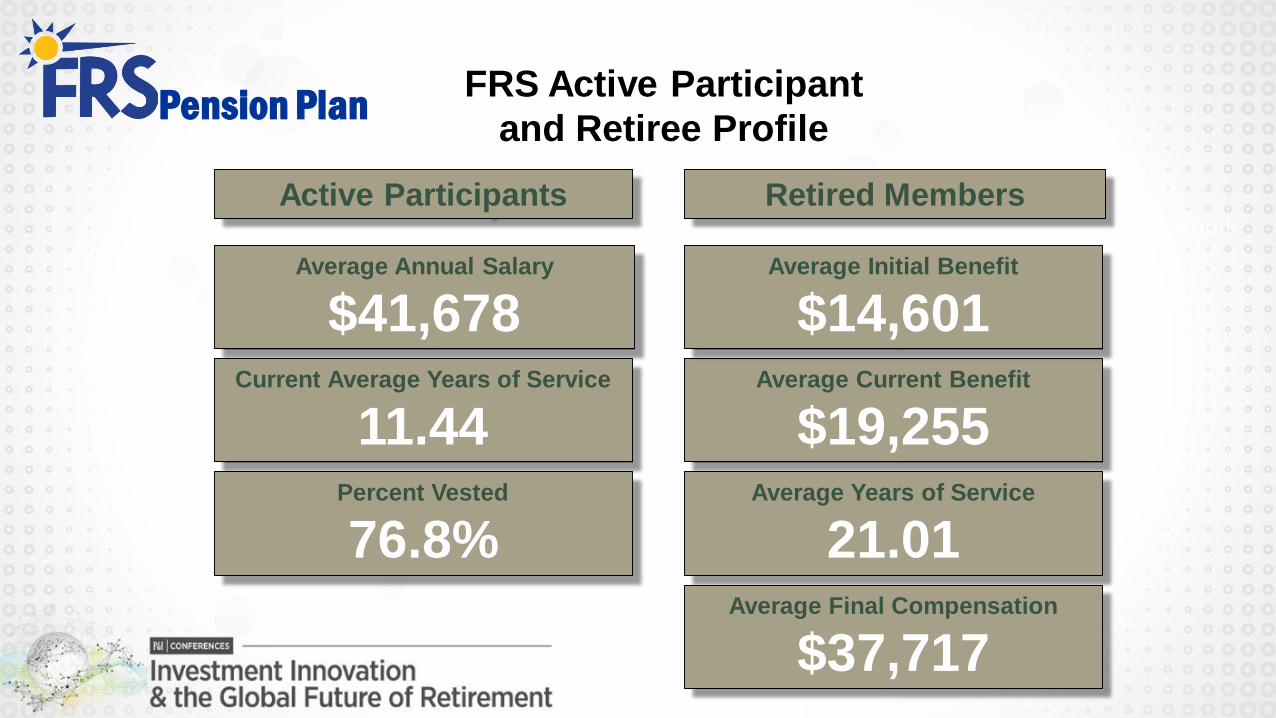

The Florida Retirement System serves an active

membership of approximately 620,000 employees

As of 6/30/2013 per DMS

FRS Active Participant

and Retiree Profile

Average Annual Salary

$41,678Average Current Benefit

$19,255

Active Participants

Current Average Years of Service

11.44Percent Vested

76.8%

Retired Members

Average Years of Service

21.01Average Final Compensation

$37,717

Average Initial Benefit

$14,601

Pension Plan

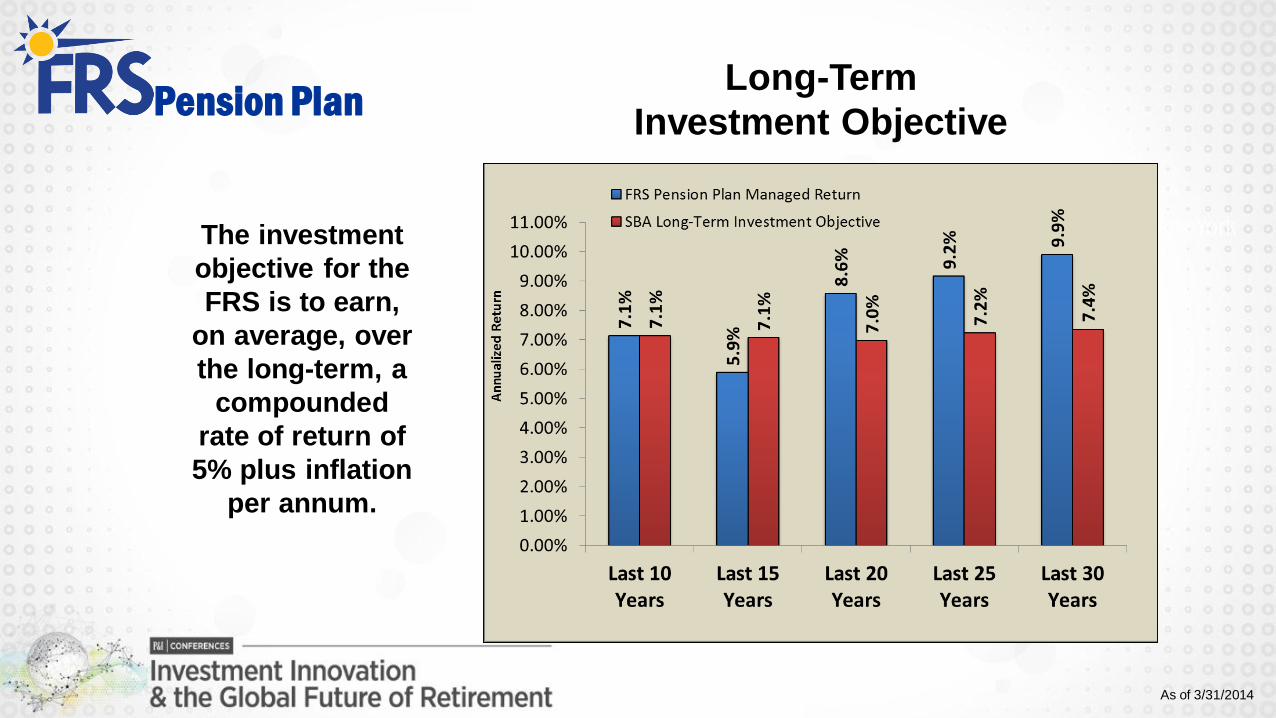

Long-Term

Investment Objective

The investment

objective for the

FRS is to earn,

on average, over

the long-term, a

compounded

rate of return of

5% plus inflation

per annum.

Pension Plan

As of 3/31/2014

Funded Ratio

The FRS

Pension Plan

funding

valuation takes

place in the fall

and was 85.9

percent

funded, as of

July 1, 2013.

Pension Plan

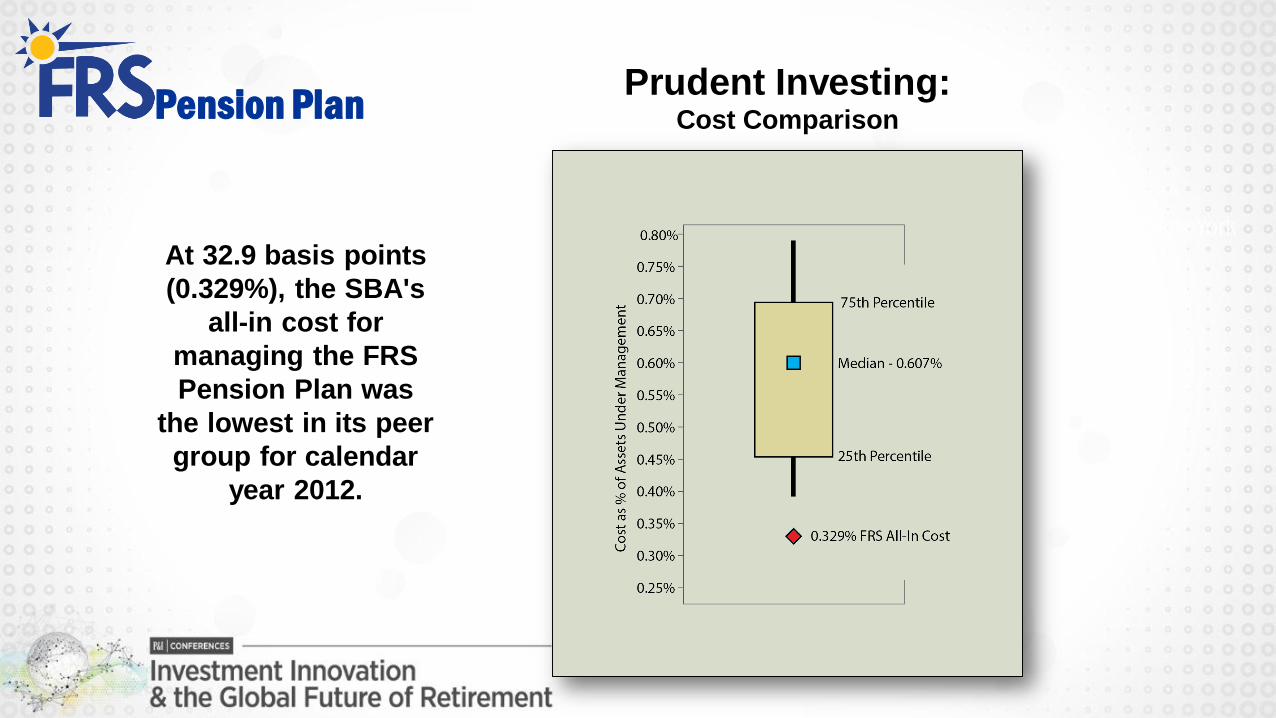

Prudent Investing:Cost Comparison

At 32.9 basis points

(0.329%), the SBA's

all-in cost for

managing the FRS

Pension Plan was

the lowest in its peer

group for calendar

year 2012.

Pension Plan

Growth

Billi

on

s

Me

mb

ers

As of 6/30/2013

Investment Plan

Total Plan Returns Investment Plan

Andreas Hilka

MD, Head of Pensions

Allianz Global Investors Europe GmbH

CLOSING DISCUSSION:

Future of Retirement Solutions

Demographic development in Germany

Constant increase of life

expectancy of 2-3 month per year

Increasing life expectancy*

79.2

84

86.6

83.5

87.7

90.1

72

74

76

78

80

82

84

86

88

90

92

2000 2035 2060

M änner Frauen

* Quelle: Statistisches Bundesamt, 12. koordinierte Bevölkerungsvorausberechnung, 11/2009

** Quelle: Statistische Ämter: Demografischer Wandel in Deutschland, Lebendgeborene in 1000

*** Quelle: Statistisches Bundesamt 2011

Shrinking fertility **

Current fertility rate is 1,4 per

woman

2010

82 Mio. persons

men women

-27%

16 Mio. 12 Mio.

21 Mio.

45 Mio.

29 Mio.

33 Mio.

2050

74 Mio. persons

Expected Development of population***

12

The German pension system at a glance:

13

Total retirement income

Statutory pension

insurance

(PAYG)

Occupational pensions

(deferred compensation

or employer-financed)

Private

pensions

(funded)

1st pillar 3rd pillar2nd pillar

TEE -> EET EET & TEEEET

Mandatory VoluntaryVoluntary

about

85%

about

5%

about

10%

EET:

Exempt contributions,

Exempt fund income,

Taxed pension payment

ETT:

Exempt contributions,

Taxed fund income,

Taxed pension payment

TEE:

Taxed contributions,

Exempt fund income,

Exempt pension payment

14

PKDI PK PF PK PF DI PK 1 2PC

Deferred Compensation Plans Personal Pensions

PF

1 - 4 % (§ 10 a EStG)

Personal Contracts

Company Sponsored Plans

Tax Free Riester-Subsidy

§ 40 b EStG

Flat Tax Rate

€ 1,752 p.a. 4% of Social Security Ceiling

Defined Benefit Plan

Defined Contribution Plan

Contributory DB Plan

Cash Balance Plan

Deferred Comp.

DI: direct insurance (Direktversicherung)

PK: „Pensionskasse“

PF: pension funds (Pensionsfonds)

PR: pension reserves (Direktzusage)

SF: support funds (Unterstützungskasse)

4%

(§ 3 No. 63 EStG)

4 %

(§ 3 No. 63 EStG)

1 - 4 %

(§ 10 a EStG)

The current German pension system: Many options imply complexity…

Bargaining agreements between Management and Unions

Riester-Subsidy

1

2

Annuity Insurance

Combination of Mutual Funds

and Annuity Insurance

PR SF DI PK PF SF

14

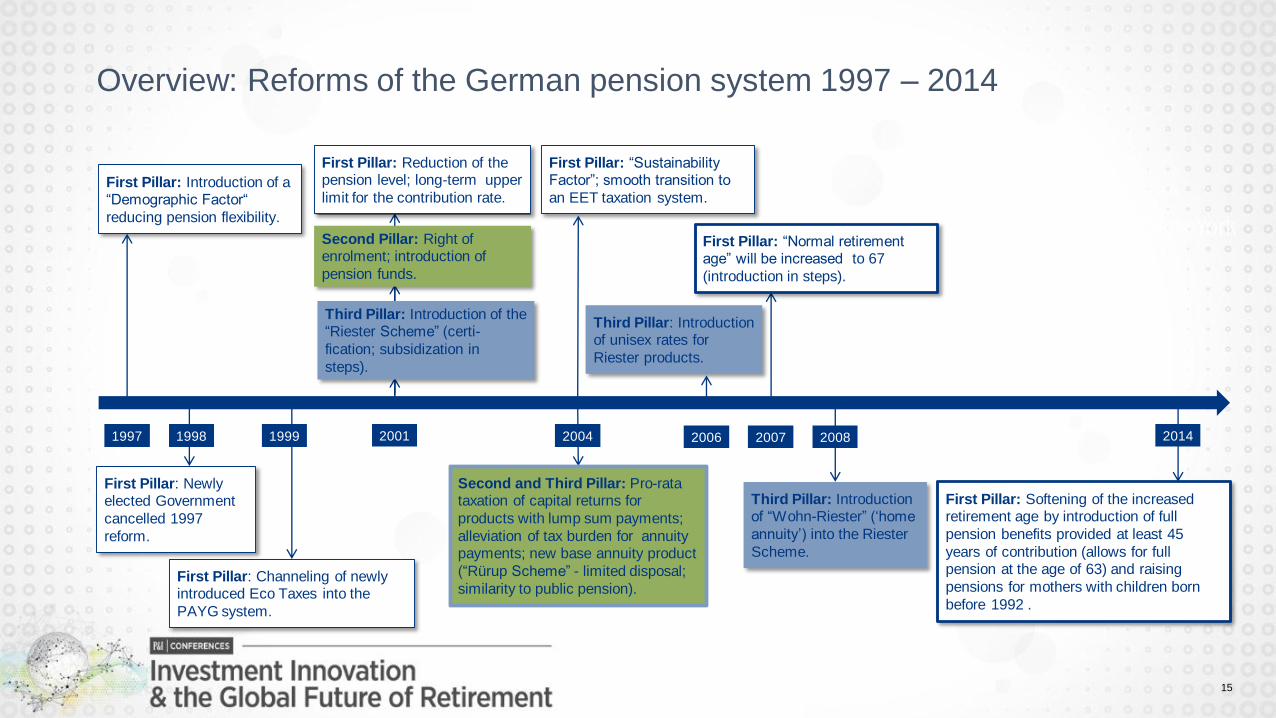

Overview: Reforms of the German pension system 1997 – 2014

15

1997 1998 1999 2004 2006 2007 2008 2014

First Pillar: Introduction of a “Demographic Factor“

reducing pension flexibility.

First Pillar: Newly elected Government

cancelled 1997

reform.

First Pillar: Channeling of newly introduced Eco Taxes into the

PAYG system.

2001

Second Pillar: Right of enrolment; introduction of

pension funds.

Third Pillar: Introduction of the “Riester Scheme” (certi-

fication; subsidization in

steps).

First Pillar: “Sustainability Factor”; smooth transition to

an EET taxation system.

Second and Third Pillar: Pro-rata taxation of capital returns for

products with lump sum payments;

alleviation of tax burden for annuity payments; new base annuity product

(“Rürup Scheme” - limited disposal;

similarity to public pension).

Third Pillar: Introduction of unisex rates for

Riester products.

First Pillar: “Normal retirement age” will be increased to 67

(introduction in steps).

Third Pillar: Introduction of “Wohn-Riester” (‘home

annuity’) into the Riester

Scheme.

First Pillar: Softening of the increased retirement age by introduction of full

pension benefits provided at least 45

years of contribution (allows for full pension at the age of 63) and raising

pensions for mothers with children born

before 1992 .

First Pillar: Reduction of the pension level; long-term upper

limit for the contribution rate.

16

Increasing demand for

hybrid pension solutions

Traditional insurance-based

occupational pension solutions are

more and more complemented by

asset-based products

Trend from defined benefit plans

to defined contribution plans

Trend towards flexible working

hours and design of working

lifetime models

Current development and trends in the German occupational pension market

Dealing with a possible funding

solution for the existing liabilitiesTrends against one-off fees and in favor

of more cost-transparency for pension

products

16

Direct pension promises

are still the most

important pension

vehicle in Germany

(as measured by size of

obligations)

One of our major topics: Unfunded pension obligations

17

53,1%

23.4%

11.0%

7.2%

5,3%

Direct pension promise

"Pensionskasse" (superannuation fund)

Direct insurance

Support fund

German-style pension fund

Pension obligations in German companies are only

partially funded:

- DAX 30 companies as “first movers”:

funding ratio approximately 62 %

(compared to worldwide

funding ratio of approximately 78 %)

- companies < DAX 30:

considerable shortfall

Trend towards funding of pension obligations will

continue

(Multi-employer) trust agreements will be the funding

vehicle of choice in many cases

Importance of pension vehicles (2010) in % Unfunded pension obligations

Sources: aba 2012, Towers Watson 2012

17

Considerable need for funding solutions in companies < DAX 30

AllianzGI – Pension Sustainability Index for Germany

The Pension Sustainability Index (PSI)

systematically examines relevant elements of

pension systems in order to measure and

evaluate the pressure on governments to reform

their national pension systems

A country with an overall score of 1 would

indicate there is no need for reform

10 would indicate there is great need for reform

The PSI is splitted into three sub-indicators

Demography

Pension system

Public finance

18

European Union: current regulatory issues

19

effective as of January 1, 2016,

three pillars: quantitative rules, governance rules and reporting and disclosure

requirements

will introduce a common European approach to prudential regulation based on economic

principles for the measurement of assets and liabilities (marked-to-market)

will be binding for EU (re)insurance undertakings

Solvency II

(Directive 2009/138/EC)

IORP II proposal

(Dir 2014/0091 COD,

published March 27, 2014)

effective as of January 1, 2017

shall remove remaining prudential barriers for cross-border IORPs and ensure good

governance and risk management, still in force: cross bordering pension schemes

have to be fully-funded at all times

does not (yet) contain the so-called ‘Solvency II for pensions’ requirements which

would have introduced a pensions solvency regime across Europe

but solvency measurement proposals (so called ‘Holistic Balance Sheet’ approach)

have not been dropped as such and are likely to be revisited over the next four years.

20

shall enhance worker mobility between Member States

total combined vesting period shall not exceed three years, the minimum age for vesting

shall not exceed 21 years

employees who leave employment prior to retirement age must be treated fairly and

have their pension rights preserved in line with active members

improves the information rights of active scheme members as well as deferred

beneficiaries and survivors

Member States have to implement the Directive into domestic legislation until May 21,

2018

Supplementary

Pension Rights

Directive

(Directive 2014/50/EU,

in force effective May 20,

2014)

considers such issues as tax, social law and harmonization of contract law to be most

significant hurdles to developing a single market for personal pensions

EIOPA supports both a Directive to introduce common EU consumer protection rules for

all existing and future personal pensions and a Regulation addressing tax and possibly

other differences between Member States to enable transferability of accumulated

capital and highly standardized product rules

European Insurance

and Occupational

Pensions Authority

(EIOPA): preliminary

report on Personal

Pension Plans

(published Februar 19,

2014)

European Union: current regulatory issues

Easy access to working population through

HR departments of companies

Lower distribution and administration costs

(„economies of scale“)

Tailor-made solutions for larger companies

possible

Layer of security due to employer‘s

commitment

Collective investment decisions possible

Occupational provisions

Product choice according to individual

investment preferences (life-cycle

investment, annuity vs. high-yielding

products)

Highly standardized products are common

practice

Broad distribution network (agents, banks)

Clear link to individual savings decisions

Private provisions

vs

Contrast: Private vs. occupational provisions

Easy access to working population through

HR departments of companies

Lower distribution and administration costs

(„economies of scale“)

Tailor-made solutions for larger companies

possible

Layer of security due to employer‘s

commitment

Collective investment decisions possible

Occupational provisions

Product choice according to individual

investment preferences (life-cycle

investment, annuity vs. high-yielding

products)

Highly standardized products are common

practice

Broad distribution network (agents, banks)

Clear link to individual savings decisions

Private provisions

vs

Contrast: Private vs. occupational provisions