Embed Size (px)

Citation preview

© OECD/IEA 2015 © OECD/IEA 2015

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan

Aligning Policies for the Transition to a Low-carbon Economy:

OECD Recommendations and Implications for Asia-Pacific Including Japan

ISAP 2015 Yokohama, 29 July 2015

Takashi Hattori

Head of Environment & Climate Change

© OECD/IEA 2015

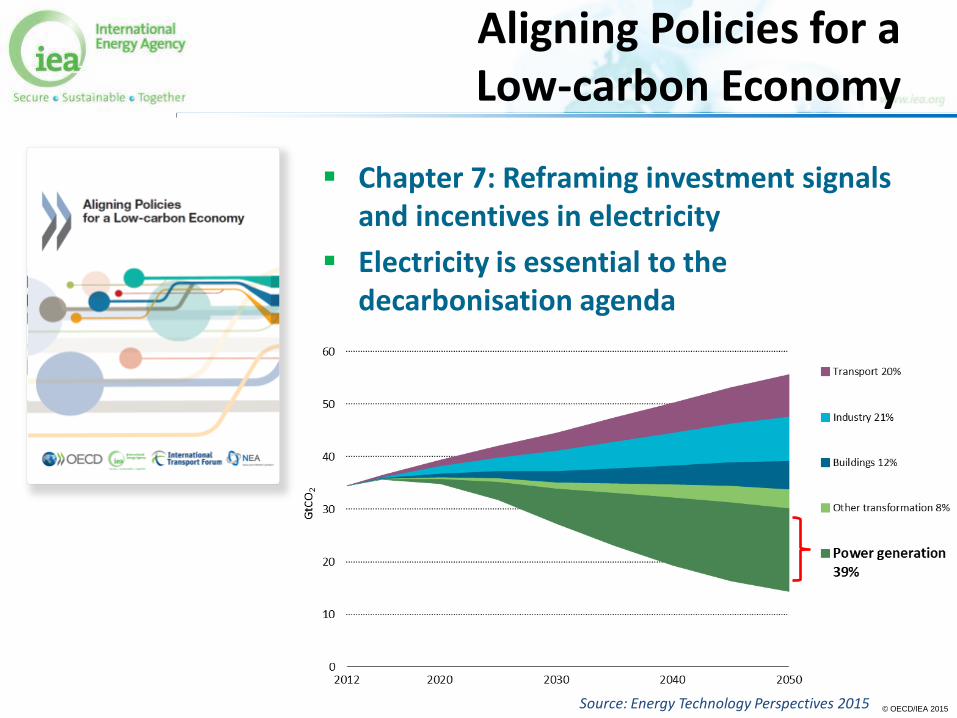

Aligning Policies for a Low-carbon Economy

Chapter 7: Reframing investment signals and incentives in electricity

Electricity is essential to the decarbonisation agenda

Source: Energy Technology Perspectives 2015

© OECD/IEA 2015

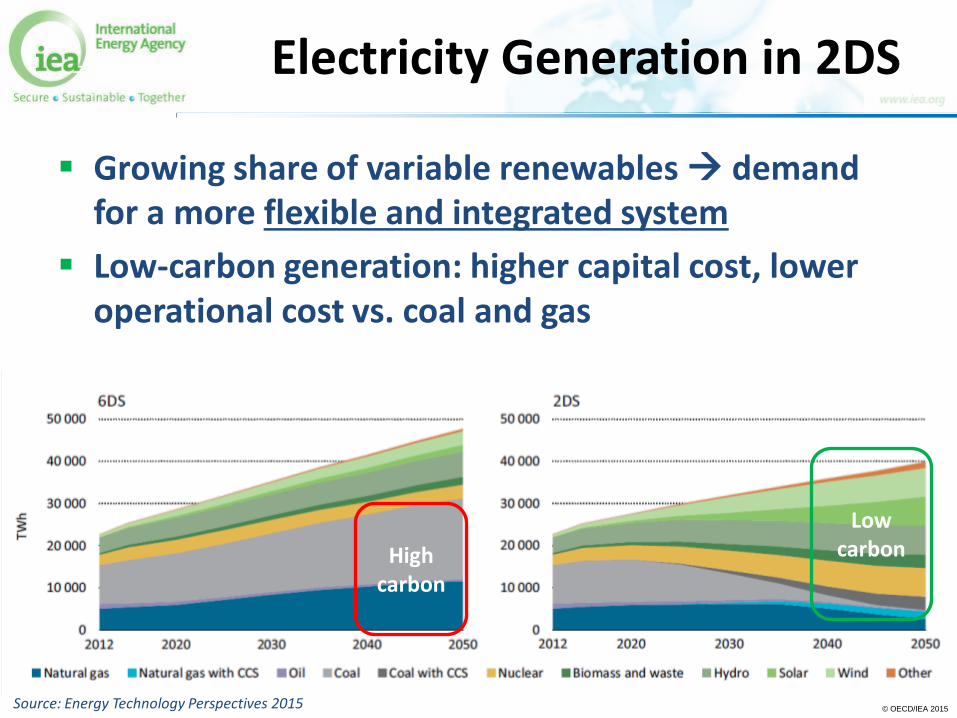

Electricity Generation in 2DS

Growing share of variable renewables demand for a more flexible and integrated system

Low-carbon generation: higher capital cost, lower operational cost vs. coal and gas

Source: Energy Technology Perspectives 2015

Low carbon High

carbon

© OECD/IEA 2015

Electricity markets

Regulatory framework for electricity systems determines investment context, cost, and reliability of system

Current wholesale electricity markets in many OECD countries are not strategically aligned with the low-carbon transition

Require new market arrangements as well as a robust CO2 price

Regulated electricity systems also face challenges, e.g. fair grid and market access for new low-carbon sources

© OECD/IEA 2015

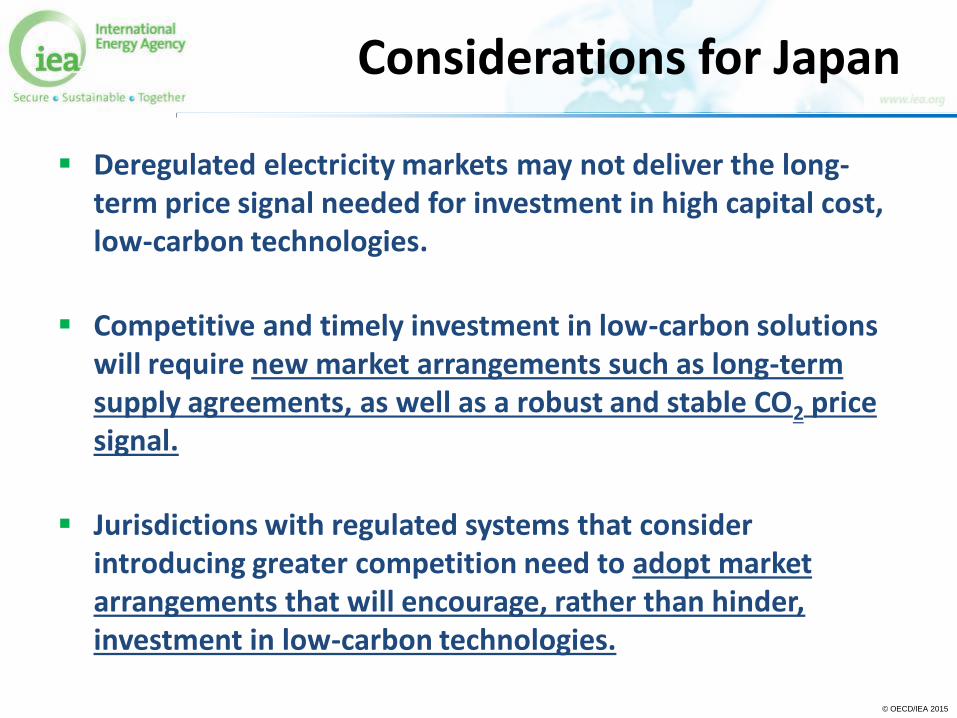

Considerations for Japan

Deregulated electricity markets may not deliver the long-term price signal needed for investment in high capital cost, low-carbon technologies.

Competitive and timely investment in low-carbon solutions will require new market arrangements such as long-term supply agreements, as well as a robust and stable CO2 price signal.

Jurisdictions with regulated systems that consider introducing greater competition need to adopt market arrangements that will encourage, rather than hinder, investment in low-carbon technologies.

© OECD/IEA 2015

Towards COP21

A major milestone in efforts to combat climate change is fast approaching – COP21 in Paris in December 2015

Momentum is building:

• Historic US-China joint announcement; EU 2030 targets agreed

• Developed & developing countries are putting forward new pledges to reduce emissions

• Many energy companies & investors are starting to engage

• Pope Francis’ encyclical LAUDATO SI’

Source: Brookings Institute Source: Business & Climate Summit Source: US Embassy

© OECD/IEA 2015

WEO Special Report 2015

Pledges are not yet enough to achieve our climate goal, but are a basis from which to build ambition

Companies that do not anticipate stronger energy & climate policies risk being at a competitive disadvantage

Proposes four key energy sector outcomes for COP21

© OECD/IEA 2015

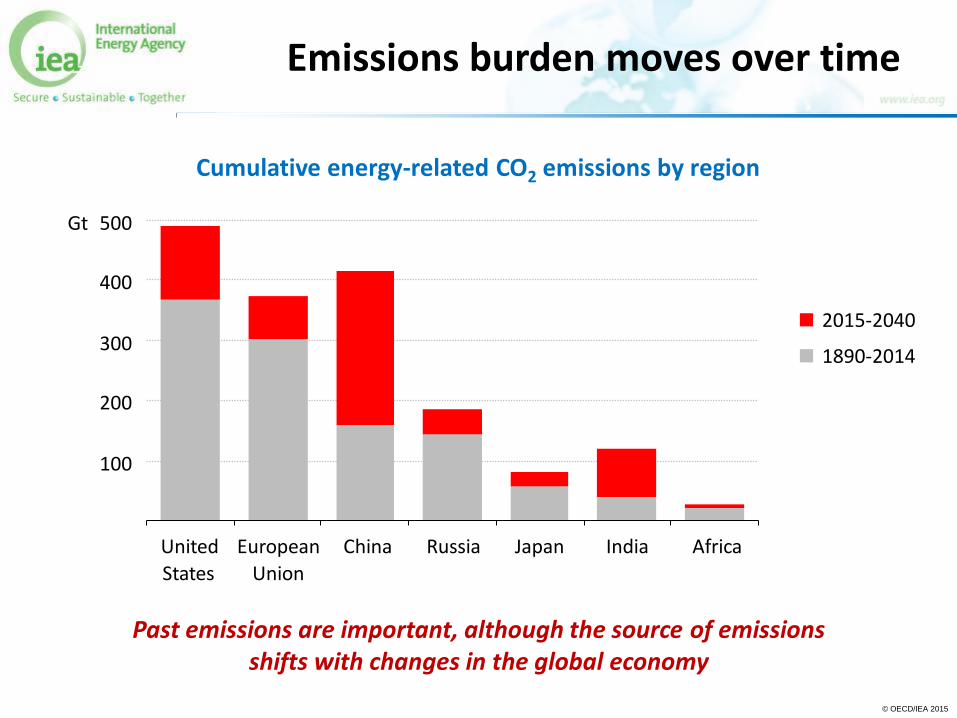

Emissions burden moves over time

Cumulative energy-related CO2 emissions by region

Past emissions are important, although the source of emissions shifts with changes in the global economy

2015-2040

1890-2014

100

200

300

400

500

United

States

European China

Union

Russia Japan India Africa

Gt

© OECD/IEA 2015

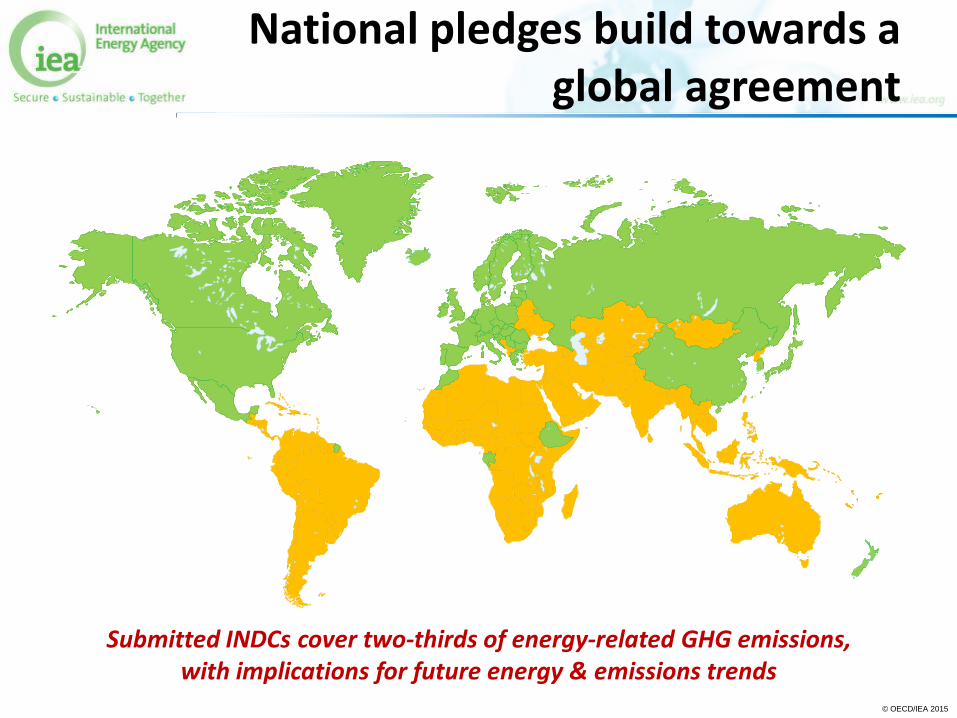

National pledges build towards a global agreement

Submitted INDCs cover two-thirds of energy-related GHG emissions, with implications for future energy & emissions trends

© OECD/IEA 2015

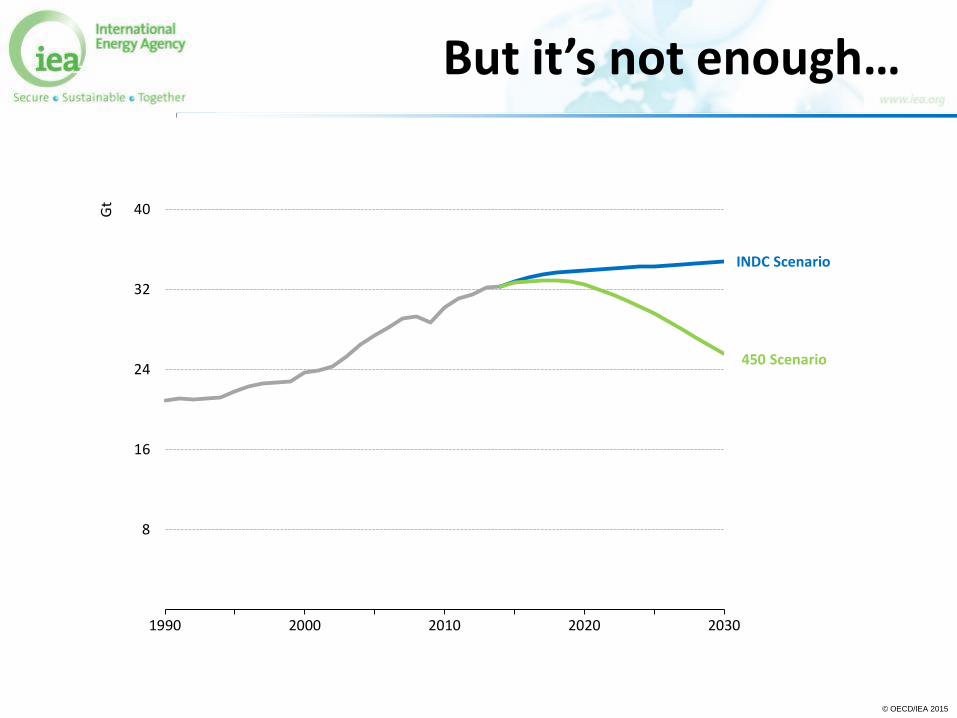

But it’s not enough…

8

16

24

32

40

1990 2000 2010 2020 2030

Gt

INDC Scenario

450 Scenario

© OECD/IEA 2015

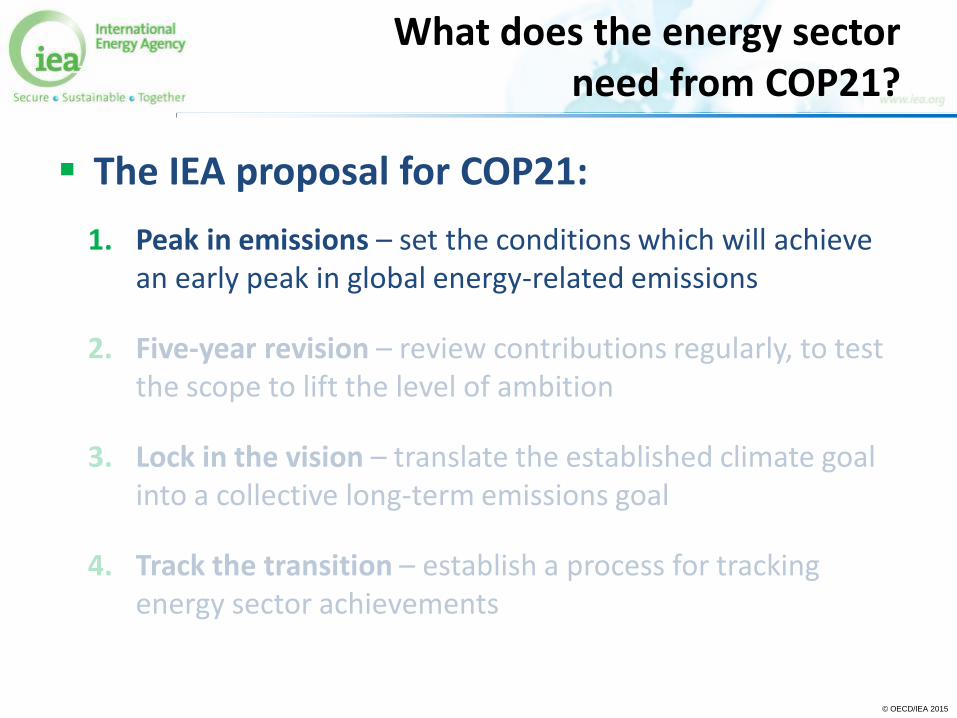

What does the energy sector need from COP21?

The IEA proposal for COP21:

1. Peak in emissions – set the conditions which will achieve an early peak in global energy-related emissions

2. Five-year revision – review contributions regularly, to test the scope to lift the level of ambition

3. Lock in the vision – translate the established climate goal into a collective long-term emissions goal

4. Track the transition – establish a process for tracking energy sector achievements

© OECD/IEA 2015

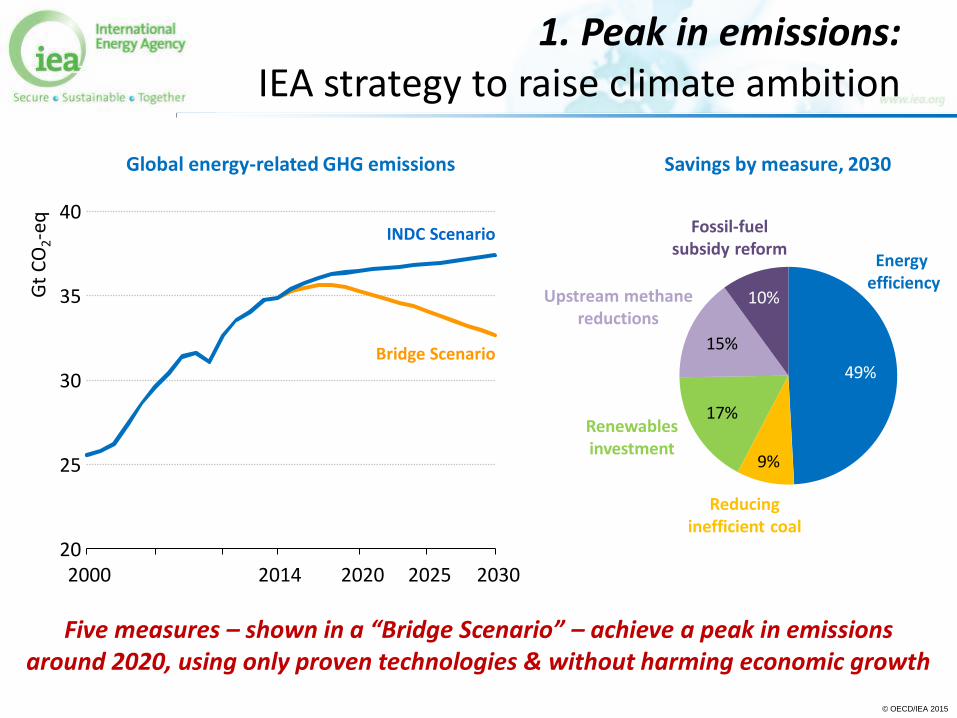

1. Peak in emissions: IEA strategy to raise climate ambition

Global energy-related GHG emissions

Five measures – shown in a “Bridge Scenario” – achieve a peak in emissions around 2020, using only proven technologies & without harming economic growth

20

25

30

35

40

2000 2014 2020 2025 2030

Gt

CO

2-eq

Bridge Scenario

INDC Scenario

Energy efficiency

49%

Reducing inefficient coal

Renewables investment

Upstream methane reductions

Fossil-fuel subsidy reform

17%

15%

10%

Savings by measure, 2030

9%

© OECD/IEA 2015

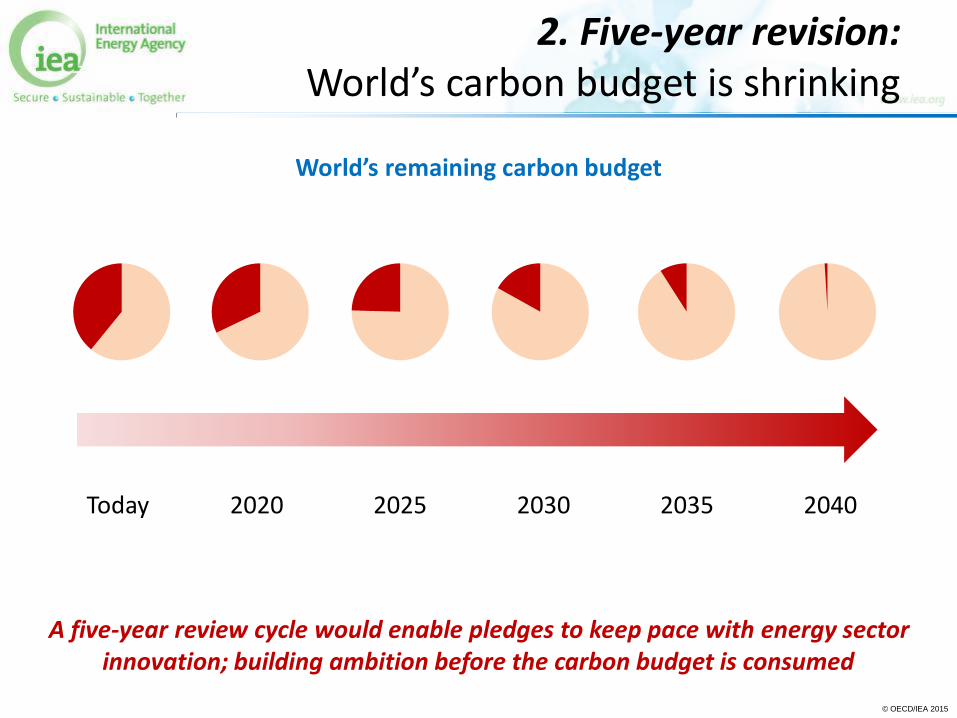

A five-year review cycle would enable pledges to keep pace with energy sector innovation; building ambition before the carbon budget is consumed

Today 2020 2025 2030 2035 2040

World’s remaining carbon budget

2. Five-year revision: World’s carbon budget is shrinking

© OECD/IEA 2015

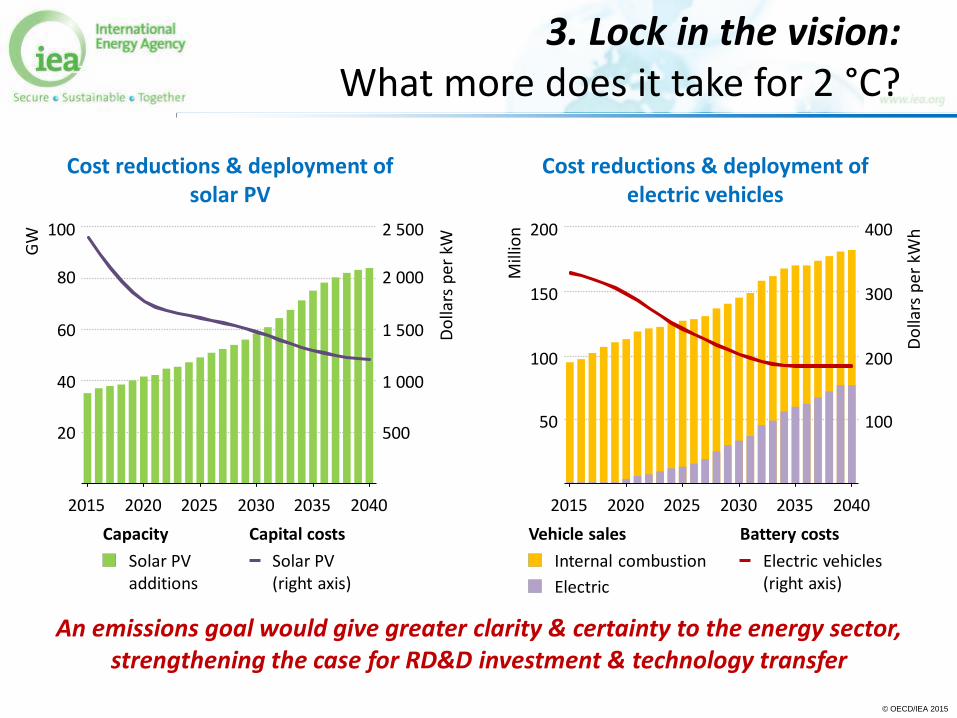

Total

50

100

150

200

2015 2020 2025 2030 2035 2040 M

illio

n

Vehicle sales

Cost reductions & deployment of electric vehicles

An emissions goal would give greater clarity & certainty to the energy sector, strengthening the case for RD&D investment & technology transfer

100

200

300

400

Do

llars

pe

r kW

h

Electric

Battery costs

Electric vehicles (right axis)

Solar PV additions

Capacity Capital costs

Solar PV (right axis)

Cost reductions & deployment of solar PV

40

60

80

100

2015 2020 2025 2030 2035 2040

GW

20

1 000

1 500

2 000

2 500

Do

llars

per

kW

500

Internal combustion

3. Lock in the vision: What more does it take for 2 °C?

© OECD/IEA 2015

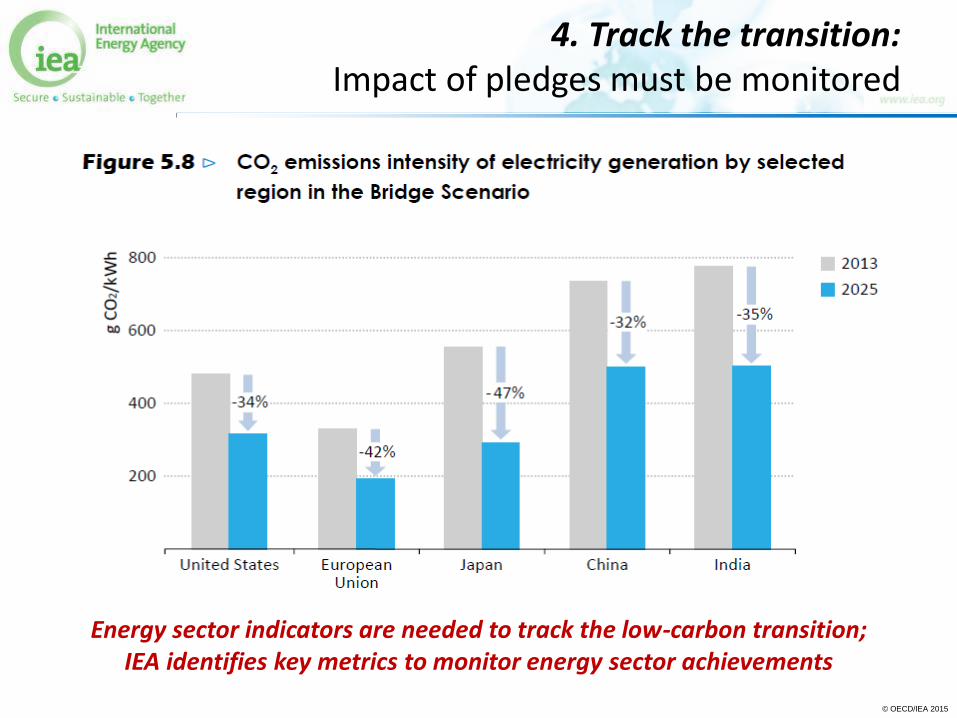

Energy sector indicators are needed to track the low-carbon transition; IEA identifies key metrics to monitor energy sector achievements

4. Track the transition: Impact of pledges must be monitored

© OECD/IEA 2015

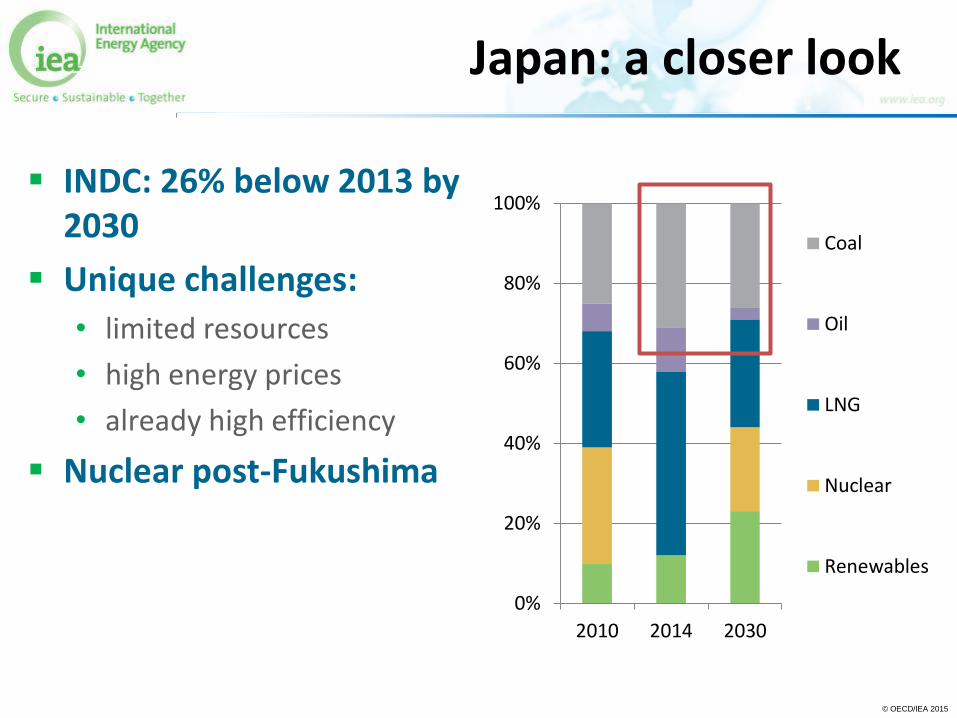

Japan: a closer look

INDC: 26% below 2013 by 2030

Unique challenges:

• limited resources

• high energy prices

• already high efficiency

Nuclear post-Fukushima

0%

20%

40%

60%

80%

100%

2010 2014 2030

Coal

Oil

LNG

Nuclear

Renewables

© OECD/IEA 2015

Energy, Climate Change & Environment 2014:

Unlocking high-emission assets

Chapter on policies and actions to “unlock” existing high-emissions assets • Retirement of coal plant

• Change dispatch of existing power plant fleet

• Efficiency retrofit of coal plant

• Retrofit of coal plant for CCS

Examples from Canada, China, UK, US, EU

© OECD/IEA 2015

Energy, Climate Change & Environment 2016

Preliminary topics:

Tracking the progress of the INDCs and the 2015 agreement

Coal and climate

Complementary approaches in industry/business

Energy sector resilience to climate change

Electricity markets and climate policy

Energy and emissions data

© OECD/IEA 2015

Thank you

Takashi Hattori [email protected]

Head, Environment & Climate Change Unit

Sustainable Technology and Policy Directorate

International Energy Agency