Embed Size (px)

Citation preview

Climate and Transport: An Introduction

Eric ZusmanMRV Training ClassNovember 26, 2013

Outline

1. Sustainable Low Carbon Transport

2. Climate Finance and Transport

3. MRVing Transport NAMAs

1. Sustainable Low Carbon Transport

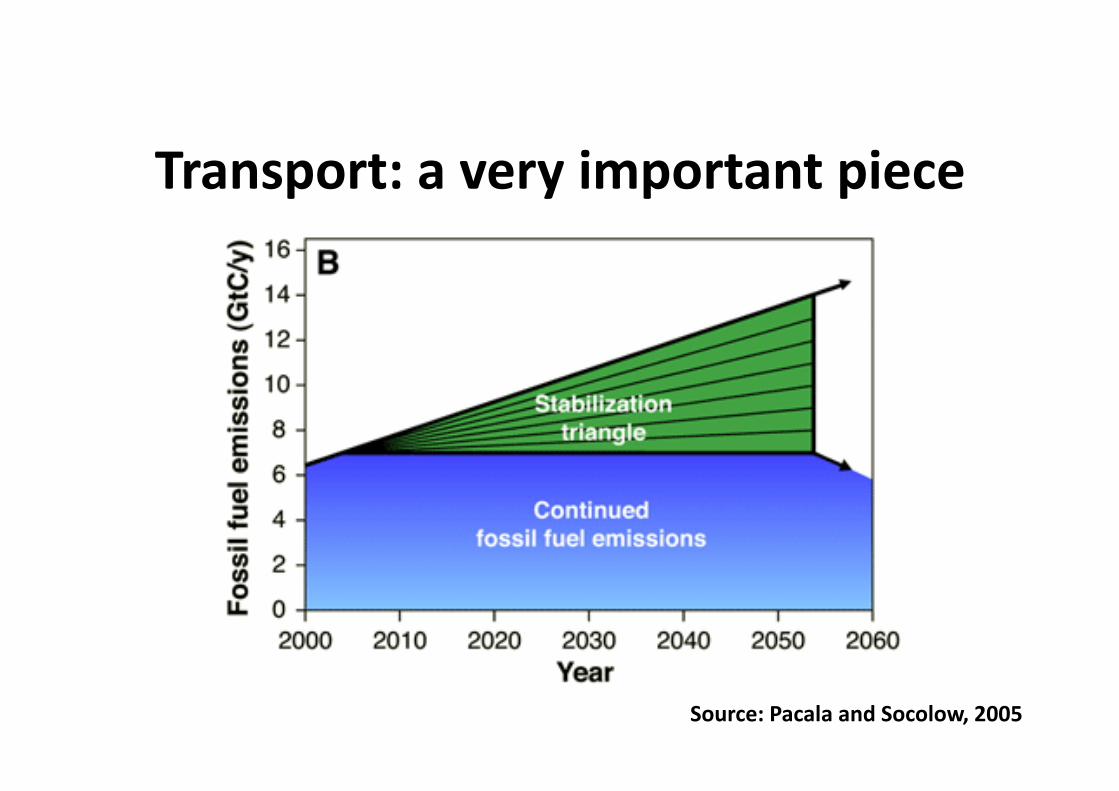

Transport: a very important piece

Source: Pacala and Socolow, 2005

A puzzle that has been difficult to solveChanges (%) in greenhouse gas emissions by source category in the EU, 1990‐2007

Source: European Environment Agency, 2011

Government solutions often promote motorization

Many drivers are behind this trend

Much of Asia is growing out—not up

Source: Perera and Permani, 2012

Energy subsidies help lock in these trends

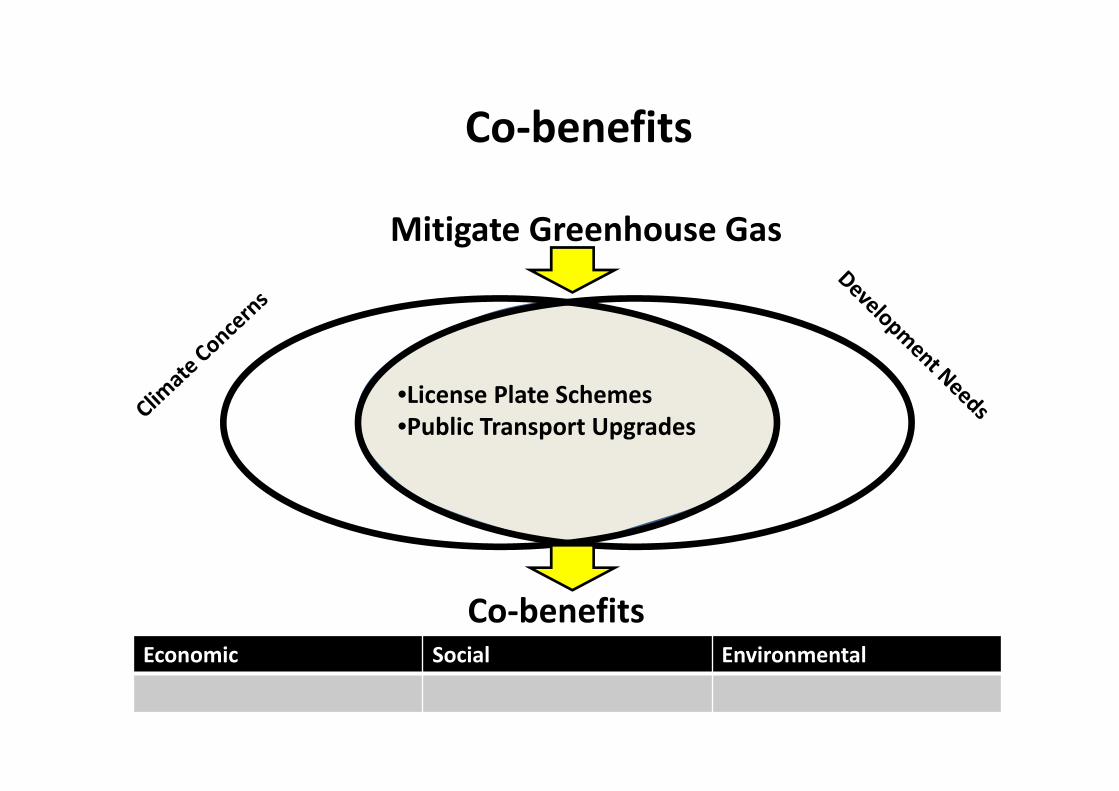

•License Plate Schemes•Public Transport Upgrades

Mitigate Greenhouse Gas

Co‐benefitsEconomic Social Environmental

Co‐benefits

•License Plate Schemes•Public Transport Upgrades

Mitigate Greenhouse GasEconomic Social Environmental

Co‐benefits

Four Options

• Do nothing: business as usual

• Invest in roads and infrastructure

• Control transport demand (road pricing, license plate schemes)

• Improve public transport (buses, metros, and subways)

1.A 2.S. 3.I

Improve

Improve

20

25

30

35

40

45

50

55

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

MIL

ES P

ER G

ALL

ON

(All

coun

tries

con

verte

d to

CA

FE te

st UNITED STATES EUROPE

JAPAN AUSTRALIACANADA CHINACALIFORNIA S. KOREA

JAPAN

UNITED STATES

EUROPEAN UNION

CHINA AUSTRALIA

CANADA

S. KOREA

CALIFORNIA+ 16 STATES

Dotted line: Proposed or contestedSolid lines: Enacted

Source: Passenger Vehicle Greenhouse Gas and Fuel Economy Standards: A Global Update, International Council on Clean Transportation, 2007

Standardized Comparison of International Fuel Economy and GHG Standar

Toyama: the first compact city in Japan

Source: Visit Toyama (Toyama City)

Avoid

Sticky Rice Ball Planning

Source: Visit Toyama (Toyama City)

Hospital

Work

Leisure

Station

Home

ShoppingStation

Home

School

Stick:Public transport system Rice dumplings:Pedestrian areas around transport system

In Asia: Potential to Shift

Source: UITP

Key Messages• Transport will have a big impact on climate change

• But transport is first and foremost about development

• There is a reason sustainability comes before low carbon

• This is the same reason we need to turn over the approach to co‐benefits

• ASI nicely summarizes key elements of a sustainable low carbon transport strategy

• Many parts of Asia are in a good position to introduce these elements

• There is a potential to get support from the international climate regime

2. Climate Finance and Transport

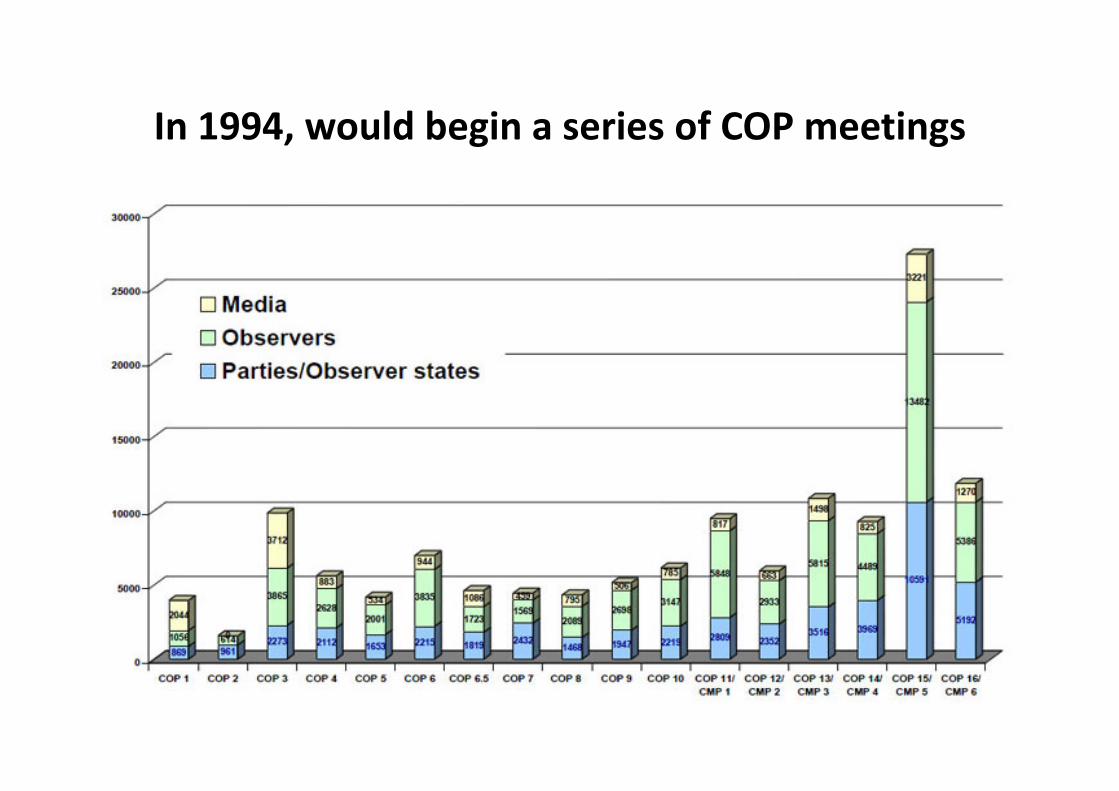

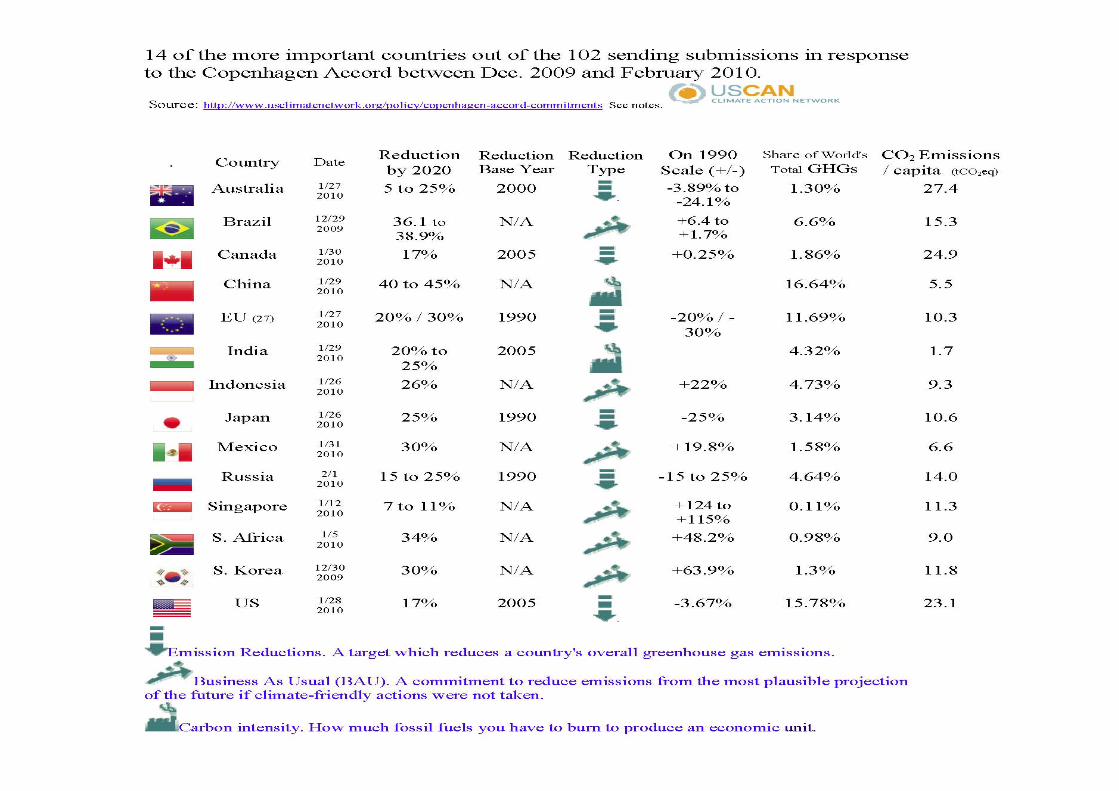

In 1994, would begin a series of COP meetings

What does a meeting in Warsaw have to do with

transportation in your city?

The Kyoto Protocol (1997)

• Commits Annex I parties to targets and timetables

• Average 5% off 1990 levels by 2008-2012

• Basket of six GHGs

The Kyoto Surprise (1997)

The CDM in Theory

CDM Barriers

• Low revenue relative to investment

• Investment often led by public sector

• Multiple small sources

• Transaction costs

Key messages

• The Kyoto protocol was developed out of the UNFCCC

• It employed a top down approach with targets and timetables for Annex 1 countries

• Though the CDM was more bottom‐up in orientation

• It did not fit well with the transport sector

3. MRVing Transport NAMAs

The Bali Action Plan

1(b)(ii): Nationally appropriate mitigation actions (NAMAs)

Finance

Technology

Capacity building

in a measurable, reportable and verifiable (MRV) manner

The Copenhagen Accord (2010‐)

Unilateral

Supported

Credited

Finance

Technology

Capacity building

NAMAs

MRV

2010‐2012

• Immediate financing

• 30 USD billion

2020

• Green Climate Fund

• 100 USD billion per year

How can transport get access to a greater share of climate finance.

• Voluntary pledge of 10 billion dollars between 2013‐2015

• Scaling up to $100 billion dollars by 2020.

2010‐2012 2013‐2015 2020

50

100

Billion dollars

Green Climate Fund

Example of a NAMA

Bila

tera

l

Climate Funds

$1.5b

$3.9b

UNFCCC

GCF $$$$$

GEF

GEF Trust FundGEF4(2006-2010) $$$GEF5(2011-2014) $$$$

LDCF $

SCCF $

AF $

UN REDD $UN-agencies

World Bank

CIFs

CTF(2009-2012) $$$$

SCF(2009-2012) $$$$

PPCR $$ FIP $$ SREP $

CarbonFinance Unit

FCPF $

PMR $

The EU

Kyoto Protocol

GCCA $

GEEREF $

CBFF $

Fund size<$500M $$500M-$1B $$$1B-$2B $$$$2B-$10B $$$$$10B- $100B $$$$$

AF: Adaptation FundCBFF: Congo Basin Forest FundCIFs: Climate Investment FundsCTF: Clean Technology FundFCPF: Forest Carbon Partnership FacilityFIP: Forest Investment ProgramGCCA: Global Climate Change AllianceGCF: Green Climate FundGEEREF: Global Energy Efficiency and Renewable Energy FundGEF: Global Environment FacilityLDCF: Least Developed Countries FundPMR: Partnership for Market ReadinessPPCR: Pilot Program on Climate ResilienceSCCF: Special Climate Change FundSCF: Strategic Climate FundSREP: Scaling Up Renewable Energy ProgramUN REDD: United Nations Collective Program on Reducing Emissions from Deforestration and Forest Degradation

General

Mitigation

Adaptation

REDD+

Fund type

European Investment BankAfrican Development Bank

Mul

tilat

eral

Australia IFCIAusAID 31.4

ICIBMU 89.7Germany

Brazil BNDES5.8MAI

FA 26.9

Guyana GRIFMultiple donors

0.4

Japan FSFJICA799.7

Norway ICFINORAD 517

UK 78.2

IFCI

ICFDFID DECC

General

REDD+

Fund type

BFI Fund

Amount in 2011/2012 (USD million)

BFIAusAID: Australian Agency for International DevelopmentBNDES: Brazilian Development BankBMU: Federal Ministry for Environment, Natural Conservation and Nuclear SafetyJICA: Japan International Cooperation AgencyNORAD: Norwegian Agency for Development CooperationDFID: Department for International DevelopmentDECC: Department of Energy and Climate Change USAID: US Agency for International Development

FundIFCI: International Forest Carbon InitiativeMAI: Mata Atlantica InitiativeFA: Amazon Fund (Fundo Amazonia)ICI: International Climate InitiativeGRIF: Guyana REDD+ Investment FundFSF: Fast-Start FinanceICFI: International Climate and Forest InitiativeICF: International Climate FundGCCI: Global Climate Change Initiative

US GCCIUSAID 858

$2.4b

Development Finance Institutions

Sub-regional and national• Largest National Development Banks• Sub-regional development banks;

(Development Bank of Latin America);• Smaller players, like the Mexican

Nacional Financiera (NAFIN)

$42.7b Bilateral• Agence Francaise de Development and

Proparco (AFD)• KfW Entwicklungsbank and DEG (KfW)• Japan International Cooperation Agency (JICA)• Overseas Private Investment Corporation (OPIC)

$11.3b Multilateral• The World Bank Group• Regionally oriented agencies, like

AfDB and ADB• Entities without a banking basis, like

the EU

$21.2b

$75.2b

Private sector

Commercial institutions• Profit-driven investment banks• Carbon brokers and funds• Banks and insurance companies

$36b Other intermediaries• Venture capital funds• Private equity funds• Infrastructure funds

$2.4b Private sector actors• Corporate actors • Institutional investors• Project developers• Households

$230b

$268b

$364b

Adaptation

Mitigation (including REDD+)

Government budgets

Carbon market revenues $2b Carbon taxes $7.3b General tax revenues NE

$16b

$14b

$350b

Note: Figures are expressed in USD billions for the latest year available (2011 or 2012).Sources: CPI, 2012; Caravani et al, 2012; Lattanzio, 2013c

Actually, many sources of climate finance; all will require some form of MRV

MRV is not new

1936 Flood Control Act

1980 Executive Order 122911804‐1866

Jules Dupuit

1999 ASIFTransport NAMAS

1950 Detroit Area Transportation Study

Applications: the next big challenge

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

Metro Traffic Police Tax Revenue Office

Number of Vehicles (Jakarta)

Motorcycle

Bus

Truck

Passenger car

Source: Suhadi, 2010

Key messages

• The Bali Action Plan began to change the nature of the climate change regime

• It allowed countries to pledge their own actions or NAMAs

• Some of these will qualify for support from international institutions

• MRV will be a requirement for what could be increasingly diverse sources of finance