Embed Size (px)

Citation preview

CliftonLarsonAllen LLPCLAconnect.com

Council of Trustees Lock Haven University of Pennsylvania of the State System of Higher Education Lock Haven, Pennsylvania We have audited the financial statements of the business-type activities and the aggregate discretely presented component units of Lock Haven University of Pennsylvania of the State System of Higher Education (University), for the year ended June 30, 2018, and have issued our report thereon dated October 31, 2018. We did not audit the financial statements of the discretely presented component units, which statements reflect 100% of the total assets and net assets as of June 30, 2018 and 100% of the revenues of the discretely presented component units for the year then ended. Those financial statements were audited by other auditors whose reports have been furnished to us, and our opinion, insofar as it relates to the amounts included for the aggregate discretely presented component units, is based on the reports of the other auditors. We have previously communicated to you information about our responsibilities under auditing standards generally accepted in the United States of America, as well as certain information related to the planned scope and timing of our audit. Professional standards also require that we communicate to you the following information related to our audit.

Significant audit findings

Qualitative aspects of accounting practices

Accounting policies

Management is responsible for the selection and use of appropriate accounting policies. The significant accounting policies used by Lock Haven University are described in Note 1 to the financial statements.

As described in Note 1, the University implemented GASB Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions which changed accounting policies related to the accounting and financial reporting of its share of the other post-retirement benefits and expense, as well as the related deferred outflows of resources and deferred inflows of resources, allocated to it by the System Plan, the Retired Employees Health Program (REHP) and the Health Insurance Premium Assistance Program (Premium Assistance). The July 1, 2017 balance of the net OPEB liability and related deferred outflows of resources and deferred inflows of resources is reported in the Statement of Revenues, Expenses, and Changes in Net Position as a restatement to the 2017 net position-beginning of year in the amount of ($61,919) million. The System Plan, REHP and Premium Assistance were not able to provide sufficient information to restate the June 30, 2017 financial statements.

Also described in Note 1 are several other GASB Statements that the University will be required to adopt in future years. The most significant pending GASB Statements is Statement No. 87 Leases. Statement No. 87 establishes a single model for lease accounting based on the foundational principle that leases are financings of the right to use an underlying asset. In other words, most leases currently classified as operating leases will be accounted for and reported in a similar manner as capital leases, with assets and liabilities recorded at lease inception. The University has determined that, although Statement No. 87 will change the way it accounts for its operating leases, the effect on its net position and results of operations will be immaterial. The provisions in Statement No. 87 are effective for reporting periods beginning after December 15, 2019.

Council of Trustees Lock Haven University of Pennsylvania of the State System of Higher Education Page 2

We noted no transactions entered into by the entity during the year for which there is a lack of authoritative guidance or consensus. All significant transactions have been recognized in the financial statements in the proper period.

Accounting estimates

Accounting estimates are an integral part of the financial statements prepared by management and are based on management’s knowledge and experience about past and current events and assumptions about future events. Certain accounting estimates are particularly sensitive because of their significance to the financial statements and because of the possibility that future events affecting them may differ significantly from those expected. The most sensitive estimates affecting the financial statements were:

Management’s estimate of the allowance for doubtful student accounts and loans receivable is based on the University’s historical tuition and fees revenue, historical losses and periodic review of individual accounts. We evaluated the key factors and assumptions used to develop the allowance in determining that it is reasonable in relation to the financial statements taken as a whole.

Management’s estimate of the accumulated depreciation and related depreciation expense is based on the estimated useful lives of the various categories of capital assets. We evaluated the key factors and assumptions used to develop the estimated useful lives of capital assets and depreciation expense in determining that it is reasonable in relation to the financial statements taken as a whole.

Management’s estimate of the compensated absences liability is based on current and historical information on employee vacation and leave balances, salary and wage rates and other pertinent information available to management. We evaluated the key factors and assumptions used to develop the compensated absences liability estimate in determining that it is reasonable in relation to the financial statements taken as a whole.

Management’s estimate of the postretirement benefits liability and expense, the net pension liability, pension expense and the related deferred inflows and deferred outflows are based on actuarial calculations and allocations performed by third parties. We evaluated the key factors and assumptions used to develop the postretirement benefits liability, the net pension liability, pension expense and the related deferred inflows and deferred outflows in determining that these amounts are reasonable in relation to the financial statements taken as a whole.

Financial statement disclosures

Certain financial statement disclosures are particularly sensitive because of their significance to financial statement users. There were no particularly sensitive financial statement disclosures.

The financial statement disclosures are neutral, consistent, and clear.

Difficulties encountered in performing the audit

We encountered no significant difficulties in dealing with management in performing and completing our audit.

Council of Trustees Lock Haven University of Pennsylvania of the State System of Higher Education Page 3

Uncorrected misstatements

Professional standards require us to accumulate all misstatements identified during the audit, other than those that are clearly trivial, and communicate them to the appropriate level of management. Management did not identify and we did not notify them of any uncorrected financial statement misstatements.

Corrected misstatements

Management did not identify and we did not notify them of any financial statement misstatements detected as a result of audit procedures.

Disagreements with management

For purposes of this letter, a disagreement with management is a financial accounting, reporting, or auditing matter, whether or not resolved to our satisfaction, that could be significant to the financial statements or the auditors’ report. No such disagreements arose during our audit.

Management representations

We have requested certain representations from management that are included in the attached management representation letter dated October 31, 2018.

Management consultations with other independent accountants

In some cases, management may decide to consult with other accountants about auditing and accounting matters, similar to obtaining a “second opinion” on certain situations. If a consultation involves application of an accounting principle to the entity’s financial statements or a determination of the type of auditors’ opinion that may be expressed on those statements, our professional standards require the consulting accountant to check with us to determine that the consultant has all the relevant facts. To our knowledge, there were no such consultations with other accountants.

Significant issues discussed with management prior to engagement

We generally discuss a variety of matters, including the application of accounting principles and auditing standards, with management each year prior to engagement as the entity’s auditors. However, these discussions occurred in the normal course of our professional relationship and our responses were not a condition to our engagement.

Audits of group financial statements

We noted no matters related to the group audit that we consider to be significant to the responsibilities of those charged with governance of the group.

Quality of component auditor’s work

There were no instances in which our evaluation of the work of a component auditor gave rise to a concern about the quality of that auditor’s work.

Limitations on the group audit

There were no restrictions on our access to information of components or other limitations on the group audit.

Council of Trustees Lock Haven University of Pennsylvania of the State System of Higher Education Page 4

Other information in documents containing audited financial statements

With respect to the required supplementary information (RSI) accompanying the financial statements, we made certain inquiries of management about the methods of preparing the RSI, including whether the RSI has been measured and presented in accordance with prescribed guidelines, whether the methods of measurement and preparation have been changed from the prior period and the reasons for any such changes, and whether there were any significant assumptions or interpretations underlying the measurement or presentation of the RSI. We compared the RSI for consistency with management’s responses to the foregoing inquiries, the basic financial statements, and other knowledge obtained during the audit of the basic financial statements. Because these limited procedures do not provide sufficient evidence, we did not express an opinion or provide any assurance on the RSI.

Management has omitted the Management’s Discussion and Analysis that accounting principles generally accepted in the United States of America requires to be presented to supplement the basic financial statements. Such missing information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. Our opinion on the basic financial statements is not affected by this missing information. Our auditors’ opinion, the audited financial statements, and the notes to financial statements should only be used in their entirety. Inclusion of the audited financial statements in a document you prepare, such as an annual report, should be done only with our prior approval and review of the document.

* * *

This communication is intended solely for the information and use of the Council of Trustees and management of Lock Haven University and is not intended to be, and should not be, used by anyone other than these specified parties.

CliftonLarsonAllen LLP

Plymouth Meeting, Pennsylvania October 31, 2018

CliftonLarsonAllen LLP

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION

YEARS ENDED JUNE 30, 2018 AND 2017

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

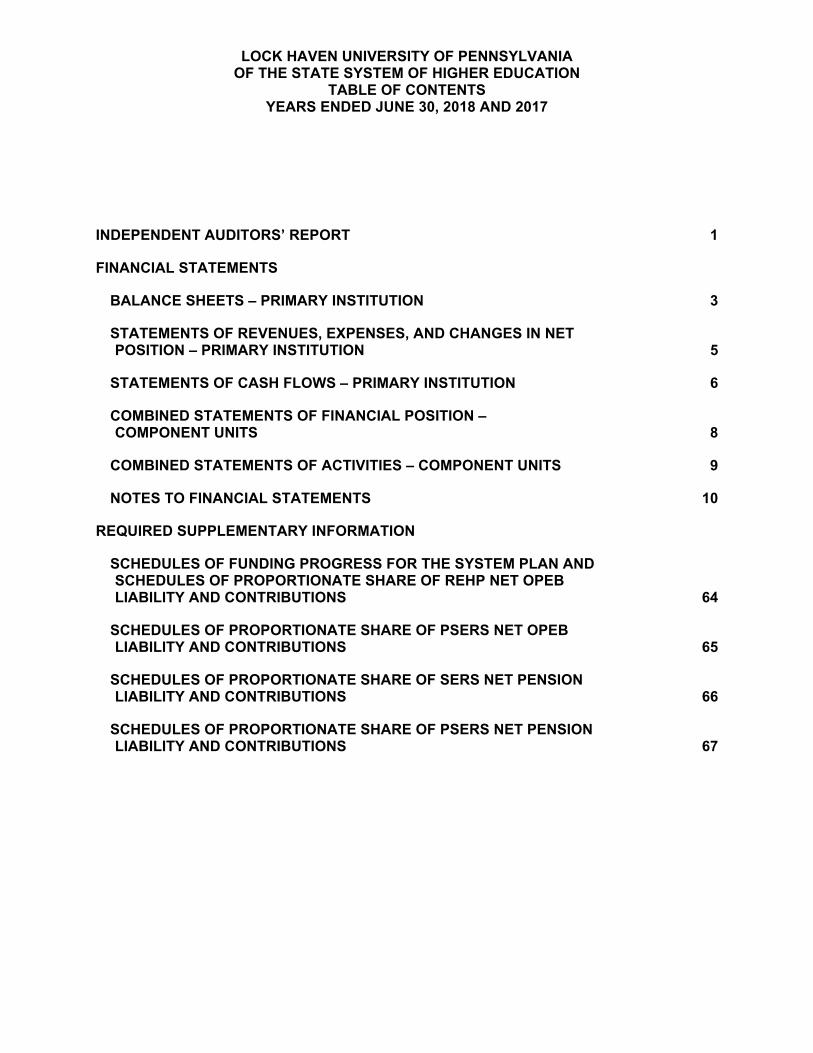

TABLE OF CONTENTS YEARS ENDED JUNE 30, 2018 AND 2017

INDEPENDENT AUDITORS’ REPORT 1

FINANCIAL STATEMENTS

BALANCE SHEETS – PRIMARY INSTITUTION 3

STATEMENTS OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION – PRIMARY INSTITUTION 5

STATEMENTS OF CASH FLOWS – PRIMARY INSTITUTION 6

COMBINED STATEMENTS OF FINANCIAL POSITION – COMPONENT UNITS 8

COMBINED STATEMENTS OF ACTIVITIES – COMPONENT UNITS 9

NOTES TO FINANCIAL STATEMENTS 10

REQUIRED SUPPLEMENTARY INFORMATION

SCHEDULES OF FUNDING PROGRESS FOR THE SYSTEM PLAN AND SCHEDULES OF PROPORTIONATE SHARE OF REHP NET OPEB LIABILITY AND CONTRIBUTIONS 64

SCHEDULES OF PROPORTIONATE SHARE OF PSERS NET OPEB LIABILITY AND CONTRIBUTIONS 65

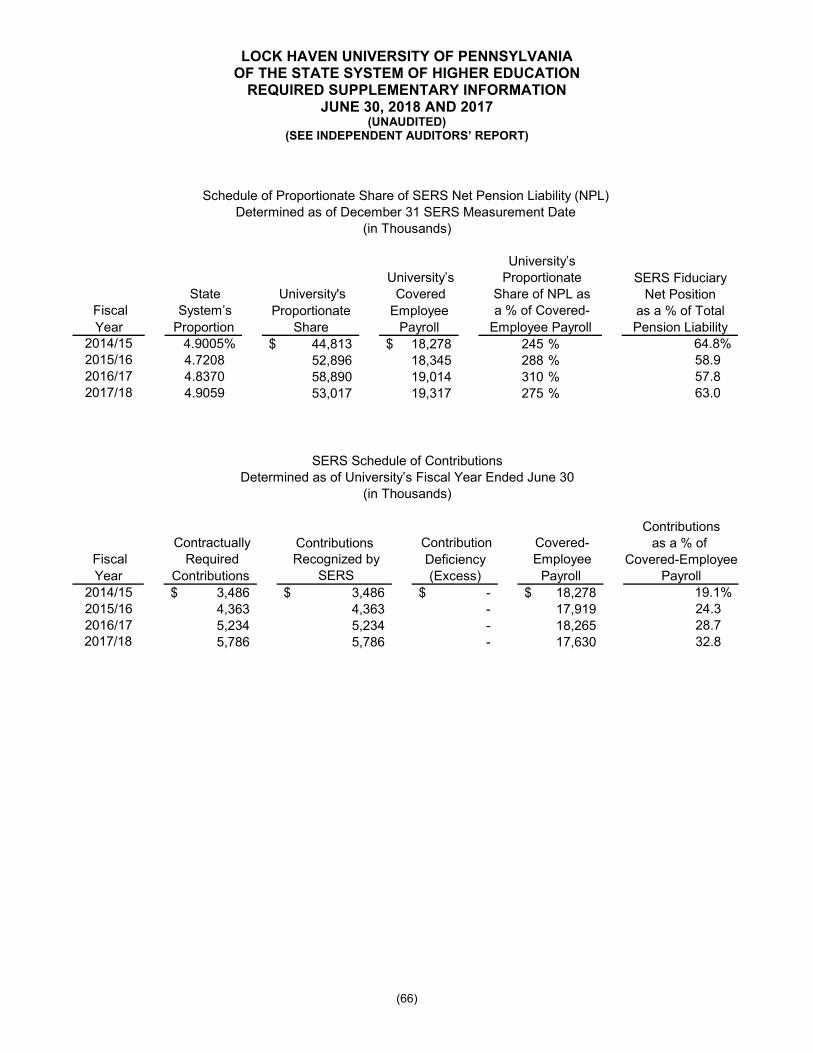

SCHEDULES OF PROPORTIONATE SHARE OF SERS NET PENSION LIABILITY AND CONTRIBUTIONS 66

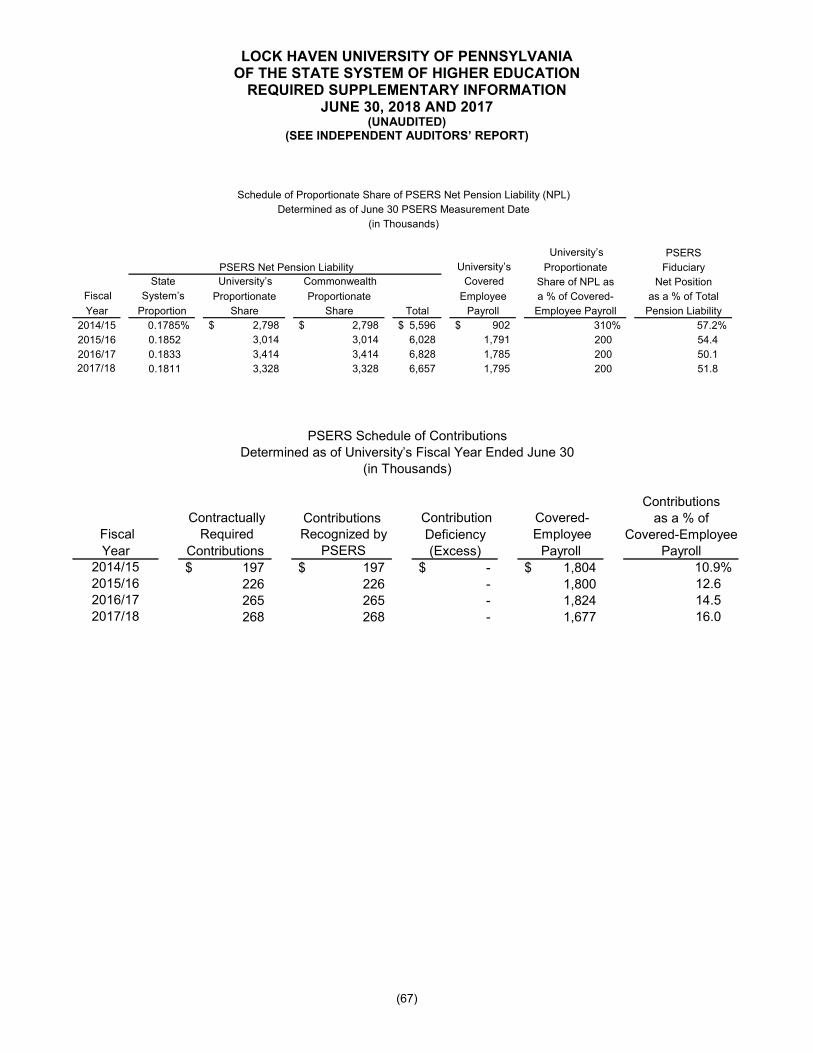

SCHEDULES OF PROPORTIONATE SHARE OF PSERS NET PENSION LIABILITY AND CONTRIBUTIONS 67

CliftonLarsonAllen LLPCLAconnect.com

(1)

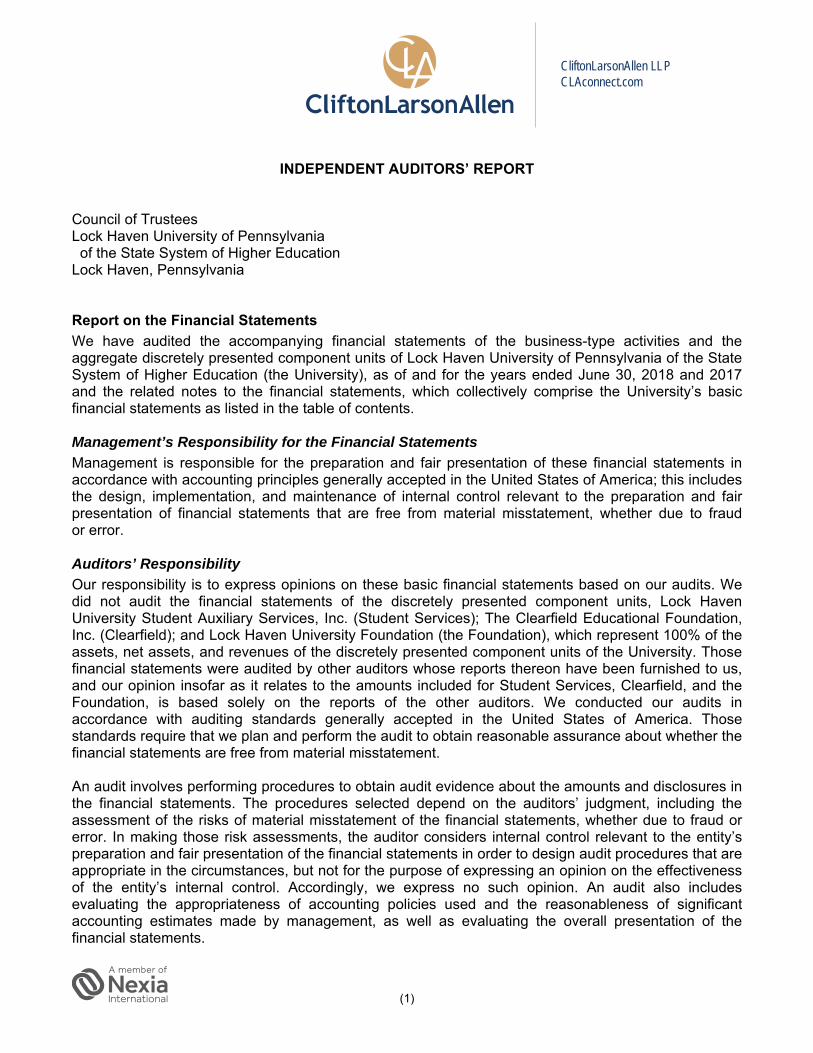

INDEPENDENT AUDITORS’ REPORT

Council of Trustees Lock Haven University of Pennsylvania of the State System of Higher Education Lock Haven, Pennsylvania Report on the Financial Statements

We have audited the accompanying financial statements of the business-type activities and the aggregate discretely presented component units of Lock Haven University of Pennsylvania of the State System of Higher Education (the University), as of and for the years ended June 30, 2018 and 2017 and the related notes to the financial statements, which collectively comprise the University’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility

Our responsibility is to express opinions on these basic financial statements based on our audits. We did not audit the financial statements of the discretely presented component units, Lock Haven University Student Auxiliary Services, Inc. (Student Services); The Clearfield Educational Foundation, Inc. (Clearfield); and Lock Haven University Foundation (the Foundation), which represent 100% of the assets, net assets, and revenues of the discretely presented component units of the University. Those financial statements were audited by other auditors whose reports thereon have been furnished to us, and our opinion insofar as it relates to the amounts included for Student Services, Clearfield, and the Foundation, is based solely on the reports of the other auditors. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

Council of Trustees Lock Haven University of Pennsylvania of the State System of Higher Education

(2)

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions

In our opinion, based on our audits and the reports of the other auditors, the financial statements referred to above present fairly, in all material respects, the respective financial position of the business-type activities and the aggregate discretely presented components units of Lock Haven University as of June 30, 2018 and 2017, and the respective changes in financial position and, where applicable, cash flows thereof for the years then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter

As discussed in Note 1 to the financial statements, the University implemented the provisions of Governmental Accounting Standards Board (GASB) Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions, for the year ended June 30, 2018, which represents a change in accounting principle. As of July 1, 2017, the University’s net position was restated to reflect the impact of adoption. A summary of the restatement is presented in Note 1. Our opinion is not modified with respect to this matter. Other Matters

Required Supplementary Information

Management has omitted the Management’s Discussion and Analysis that accounting principles generally accepted in the United States of America require to be presented to supplement the basic financial statements. Such missing information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of the financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. Our opinion on the basic financial statements is not affected by this missing information. Accounting principles generally accepted in the United States of America require that the various schedules of OPEB Liability, Proportionate Share of Net OPEB Liability and Contributions, and Proportionate Share of Net Pension Liability, on pages 64-67, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

CliftonLarsonAllen LLP

Harrisburg, Pennsylvania October 31, 2018

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

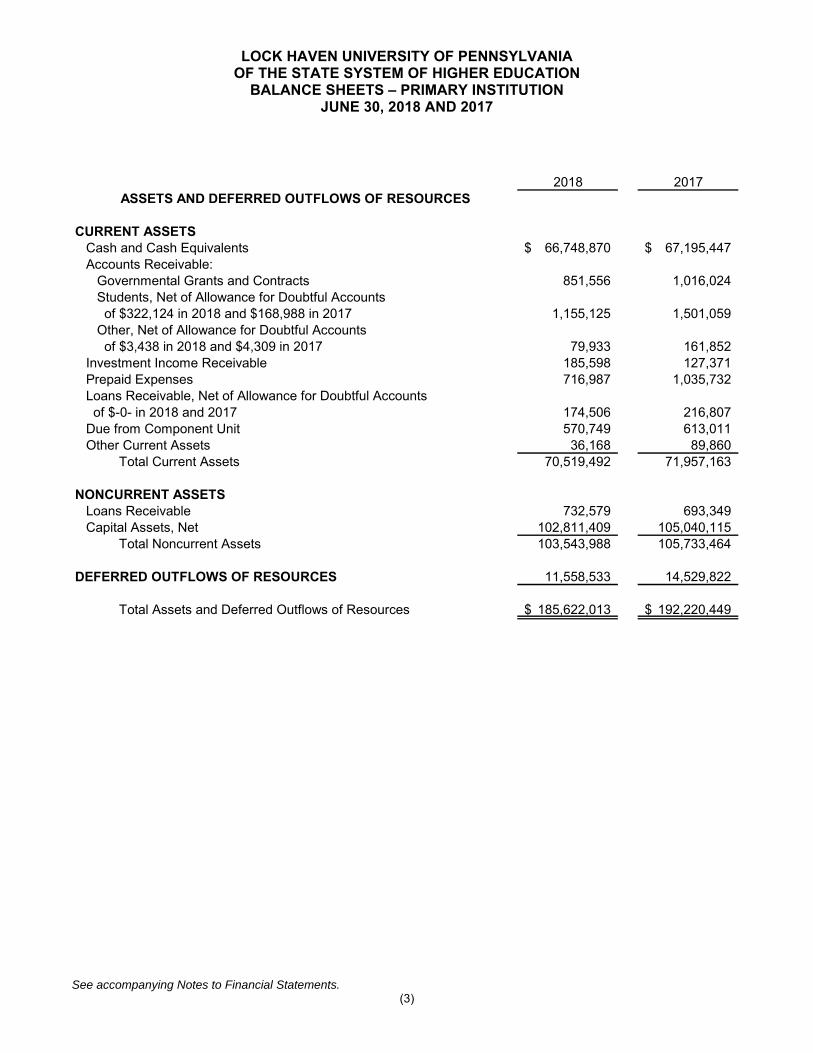

BALANCE SHEETS – PRIMARY INSTITUTION JUNE 30, 2018 AND 2017

See accompanying Notes to Financial Statements. (3)

2018 2017

ASSETS AND DEFERRED OUTFLOWS OF RESOURCES

CURRENT ASSETSCash and Cash Equivalents 66,748,870$ 67,195,447$ Accounts Receivable:

Governmental Grants and Contracts 851,556 1,016,024 Students, Net of Allowance for Doubtful Accounts of $322,124 in 2018 and $168,988 in 2017 1,155,125 1,501,059 Other, Net of Allowance for Doubtful Accounts of $3,438 in 2018 and $4,309 in 2017 79,933 161,852

Investment Income Receivable 185,598 127,371 Prepaid Expenses 716,987 1,035,732 Loans Receivable, Net of Allowance for Doubtful Accounts of $-0- in 2018 and 2017 174,506 216,807 Due from Component Unit 570,749 613,011 Other Current Assets 36,168 89,860

Total Current Assets 70,519,492 71,957,163

NONCURRENT ASSETSLoans Receivable 732,579 693,349 Capital Assets, Net 102,811,409 105,040,115

Total Noncurrent Assets 103,543,988 105,733,464

DEFERRED OUTFLOWS OF RESOURCES 11,558,533 14,529,822

Total Assets and Deferred Outflows of Resources 185,622,013$ 192,220,449$

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

BALANCE SHEETS – PRIMARY INSTITUTION (CONTINUED) JUNE 30, 2018 AND 2017

See accompanying Notes to Financial Statements. (4)

2018 2017

LIABILITIES, DEFERRED INFLOWS OF RESOURCES,AND NET POSITION

CURRENT LIABILITIESAccounts Payable and Accrued Expenses 7,889,982$ 8,644,256$ Unearned Revenue 869,701 1,281,015Students’ Deposits 367,431 358,637 Current Portion of Workers’ Compensation 165,078 159,832 Current Portion of Compensated Absences 390,700 325,000

Current Portion of OPEB Liability 2,697,622 - Current Portion of Bonds Payable 2,909,785 2,787,374 Current Portion of Capitalized Lease Obligations 14,820 18,028 Current Portion of Due to System, Academic Facilities Renovation Bond Program (AFRP) 194,718 199,704 Due to Component Unit - 16,611 Other Current Liabilities 254,766 98,586

Total Current Liabilities 15,754,603 13,889,043

NONCURRENT LIABILITIESUnearned Revenue 63,359 72,148 Workers’ Compensation, Net of Current Portion 130,839 134,851 Compensated Absences, Net of Current Portion 5,704,832 5,547,707 Other Postemployment Benefits Liability, Net of Current Portion 105,405,648 52,285,641 Net Pension Liability 56,345,173 62,303,721 Capitalized Lease Obligations, Net of Current Portion 43,810 23,112 Bonds Payable, Net of Current Portion 48,552,231 51,462,016 Due to System, AFRP, Net of Current Portion 441,438 639,329 Other Noncurrent Liabilities 1,118,558 1,511,614

Total Noncurrent Liabilities 217,805,888 173,980,139

Total Liabilities 233,560,491 187,869,182

DEFERRED INFLOWS OF RESOURCES 13,593,570 2,892,860

NET POSITIONNet Investment in Capital Assets 50,828,523 50,118,564 Restricted for:

Nonexpendable:Student Loans 118,499 142,721

Expendable:Scholarships and Fellowships 53,991 53,094Other 30,479 28,495

Unrestricted (112,563,540) (48,884,467) Total Net Position (61,532,048) 1,458,407 Total Liabilities, Deferred Inflows of Resources, and Net Position 185,622,013$ 192,220,449$

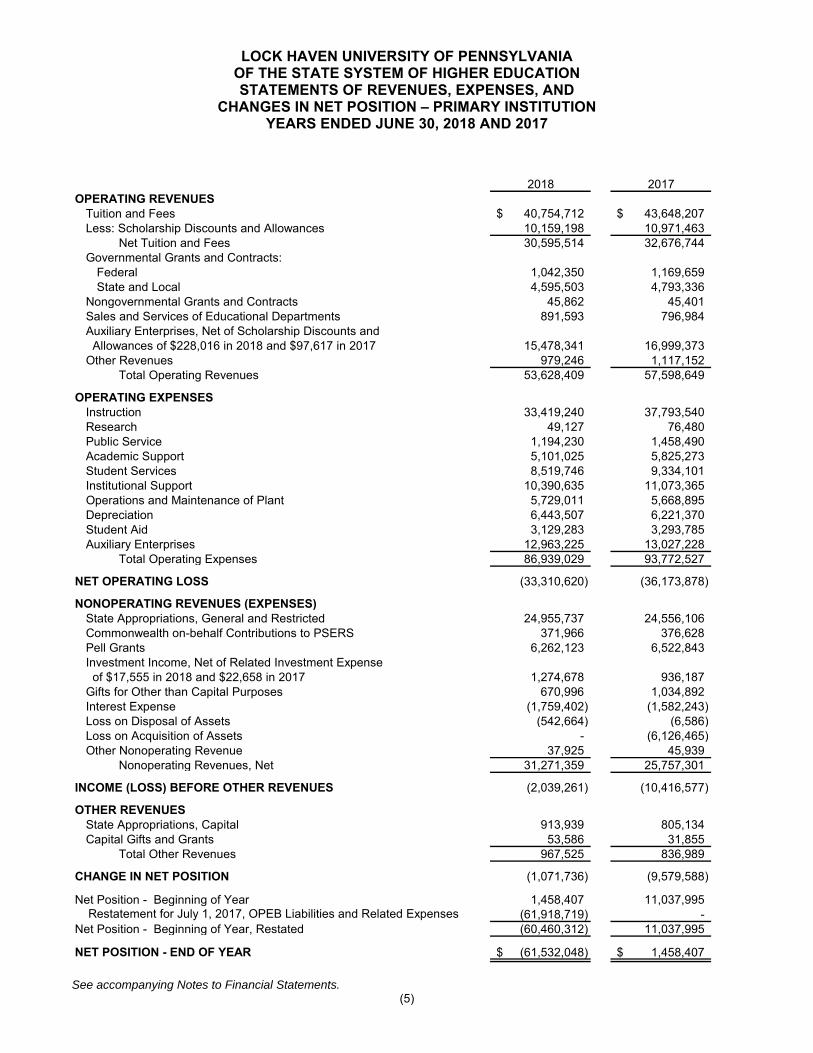

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION STATEMENTS OF REVENUES, EXPENSES, AND

CHANGES IN NET POSITION – PRIMARY INSTITUTION YEARS ENDED JUNE 30, 2018 AND 2017

See accompanying Notes to Financial Statements. (5)

2018 2017

OPERATING REVENUESTuition and Fees 40,754,712$ 43,648,207$ Less: Scholarship Discounts and Allowances 10,159,198 10,971,463

Net Tuition and Fees 30,595,514 32,676,744 Governmental Grants and Contracts:

Federal 1,042,350 1,169,659 State and Local 4,595,503 4,793,336

Nongovernmental Grants and Contracts 45,862 45,401 Sales and Services of Educational Departments 891,593 796,984 Auxiliary Enterprises, Net of Scholarship Discounts and Allowances of $228,016 in 2018 and $97,617 in 2017 15,478,341 16,999,373 Other Revenues 979,246 1,117,152

Total Operating Revenues 53,628,409 57,598,649

OPERATING EXPENSESInstruction 33,419,240 37,793,540 Research 49,127 76,480 Public Service 1,194,230 1,458,490 Academic Support 5,101,025 5,825,273 Student Services 8,519,746 9,334,101 Institutional Support 10,390,635 11,073,365 Operations and Maintenance of Plant 5,729,011 5,668,895 Depreciation 6,443,507 6,221,370 Student Aid 3,129,283 3,293,785 Auxiliary Enterprises 12,963,225 13,027,228

Total Operating Expenses 86,939,029 93,772,527

NET OPERATING LOSS (33,310,620) (36,173,878)

NONOPERATING REVENUES (EXPENSES)State Appropriations, General and Restricted 24,955,737 24,556,106 Commonwealth on-behalf Contributions to PSERS 371,966 376,628 Pell Grants 6,262,123 6,522,843 Investment Income, Net of Related Investment Expense of $17,555 in 2018 and $22,658 in 2017 1,274,678 936,187 Gifts for Other than Capital Purposes 670,996 1,034,892 Interest Expense (1,759,402) (1,582,243) Loss on Disposal of Assets (542,664) (6,586) Loss on Acquisition of Assets - (6,126,465) Other Nonoperating Revenue 37,925 45,939

Nonoperating Revenues, Net 31,271,359 25,757,301

INCOME (LOSS) BEFORE OTHER REVENUES (2,039,261) (10,416,577)

OTHER REVENUESState Appropriations, Capital 913,939 805,134 Capital Gifts and Grants 53,586 31,855

Total Other Revenues 967,525 836,989

CHANGE IN NET POSITION (1,071,736) (9,579,588)

Net Position - Beginning of Year 1,458,407 11,037,995 Restatement for July 1, 2017, OPEB Liabilities and Related Expenses (61,918,719) - Net Position - Beginning of Year, Restated (60,460,312) 11,037,995

NET POSITION - END OF YEAR (61,532,048)$ 1,458,407$

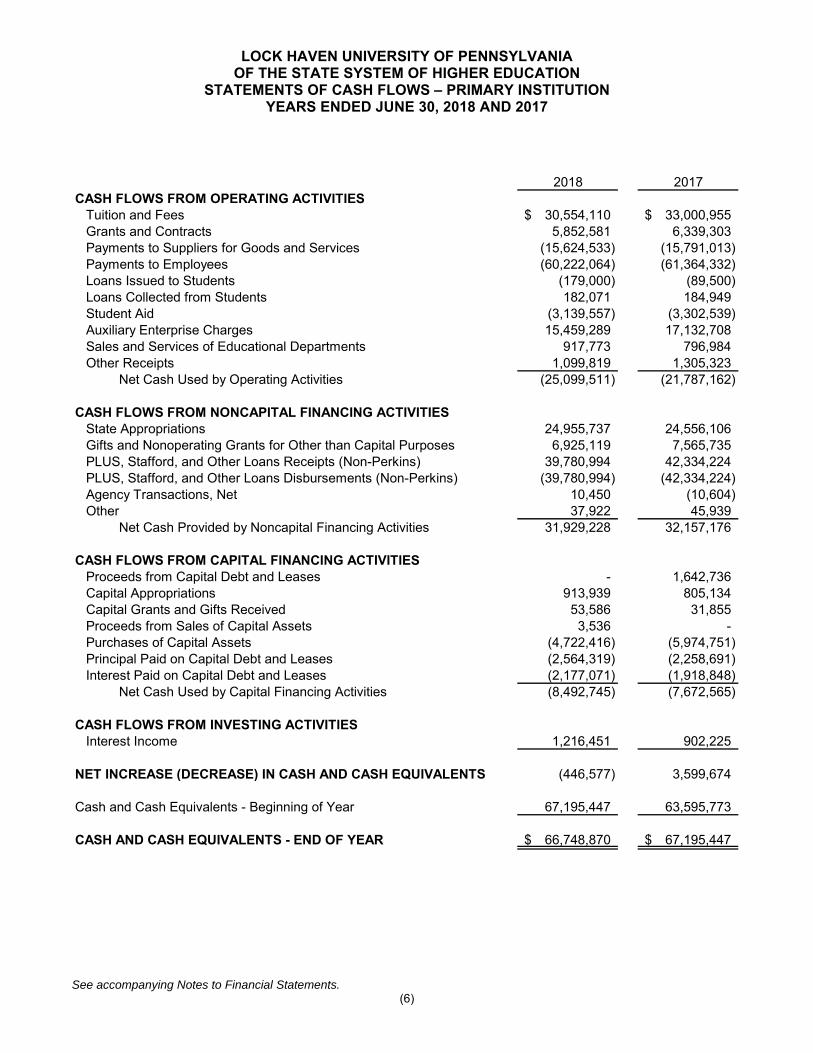

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

STATEMENTS OF CASH FLOWS – PRIMARY INSTITUTION YEARS ENDED JUNE 30, 2018 AND 2017

See accompanying Notes to Financial Statements. (6)

2018 2017

CASH FLOWS FROM OPERATING ACTIVITIESTuition and Fees 30,554,110$ 33,000,955$ Grants and Contracts 5,852,581 6,339,303 Payments to Suppliers for Goods and Services (15,624,533) (15,791,013) Payments to Employees (60,222,064) (61,364,332) Loans Issued to Students (179,000) (89,500) Loans Collected from Students 182,071 184,949 Student Aid (3,139,557) (3,302,539) Auxiliary Enterprise Charges 15,459,289 17,132,708 Sales and Services of Educational Departments 917,773 796,984 Other Receipts 1,099,819 1,305,323

Net Cash Used by Operating Activities (25,099,511) (21,787,162)

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIESState Appropriations 24,955,737 24,556,106 Gifts and Nonoperating Grants for Other than Capital Purposes 6,925,119 7,565,735 PLUS, Stafford, and Other Loans Receipts (Non-Perkins) 39,780,994 42,334,224 PLUS, Stafford, and Other Loans Disbursements (Non-Perkins) (39,780,994) (42,334,224) Agency Transactions, Net 10,450 (10,604) Other 37,922 45,939

Net Cash Provided by Noncapital Financing Activities 31,929,228 32,157,176

CASH FLOWS FROM CAPITAL FINANCING ACTIVITIESProceeds from Capital Debt and Leases - 1,642,736 Capital Appropriations 913,939 805,134 Capital Grants and Gifts Received 53,586 31,855 Proceeds from Sales of Capital Assets 3,536 - Purchases of Capital Assets (4,722,416) (5,974,751) Principal Paid on Capital Debt and Leases (2,564,319) (2,258,691) Interest Paid on Capital Debt and Leases (2,177,071) (1,918,848)

Net Cash Used by Capital Financing Activities (8,492,745) (7,672,565)

CASH FLOWS FROM INVESTING ACTIVITIESInterest Income 1,216,451 902,225

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS (446,577) 3,599,674

Cash and Cash Equivalents - Beginning of Year 67,195,447 63,595,773

CASH AND CASH EQUIVALENTS - END OF YEAR 66,748,870$ 67,195,447$

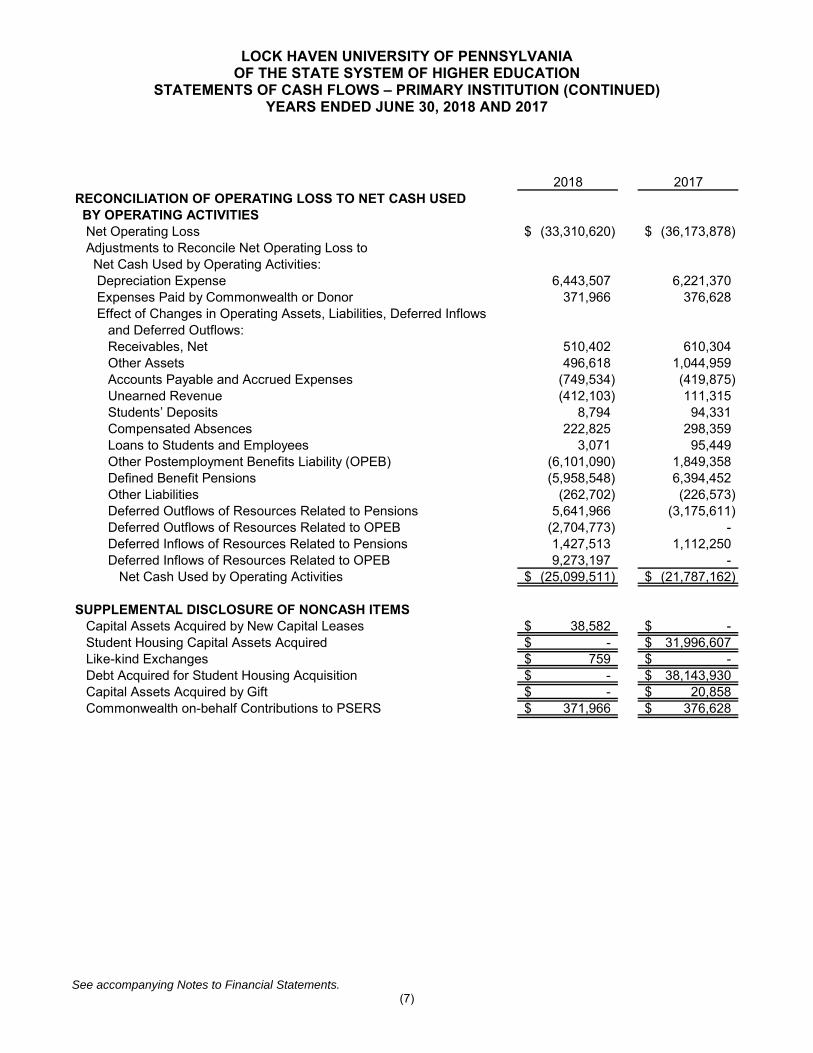

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

STATEMENTS OF CASH FLOWS – PRIMARY INSTITUTION (CONTINUED) YEARS ENDED JUNE 30, 2018 AND 2017

See accompanying Notes to Financial Statements. (7)

2018 2017

RECONCILIATION OF OPERATING LOSS TO NET CASH USED BY OPERATING ACTIVITIES

Net Operating Loss (33,310,620)$ (36,173,878)$ Adjustments to Reconcile Net Operating Loss to Net Cash Used by Operating Activities:

Depreciation Expense 6,443,507 6,221,370 Expenses Paid by Commonwealth or Donor 371,966 376,628 Effect of Changes in Operating Assets, Liabilities, Deferred Inflows and Deferred Outflows:

Receivables, Net 510,402 610,304 Other Assets 496,618 1,044,959 Accounts Payable and Accrued Expenses (749,534) (419,875) Unearned Revenue (412,103) 111,315 Students’ Deposits 8,794 94,331 Compensated Absences 222,825 298,359 Loans to Students and Employees 3,071 95,449 Other Postemployment Benefits Liability (OPEB) (6,101,090) 1,849,358 Defined Benefit Pensions (5,958,548) 6,394,452 Other Liabilities (262,702) (226,573) Deferred Outflows of Resources Related to Pensions 5,641,966 (3,175,611) Deferred Outflows of Resources Related to OPEB (2,704,773) - Deferred Inflows of Resources Related to Pensions 1,427,513 1,112,250 Deferred Inflows of Resources Related to OPEB 9,273,197 -

Net Cash Used by Operating Activities (25,099,511)$ (21,787,162)$

SUPPLEMENTAL DISCLOSURE OF NONCASH ITEMSCapital Assets Acquired by New Capital Leases 38,582$ -$ Student Housing Capital Assets Acquired -$ 31,996,607$ Like-kind Exchanges 759$ -$ Debt Acquired for Student Housing Acquisition -$ 38,143,930$ Capital Assets Acquired by Gift -$ 20,858$ Commonwealth on-behalf Contributions to PSERS 371,966$ 376,628$

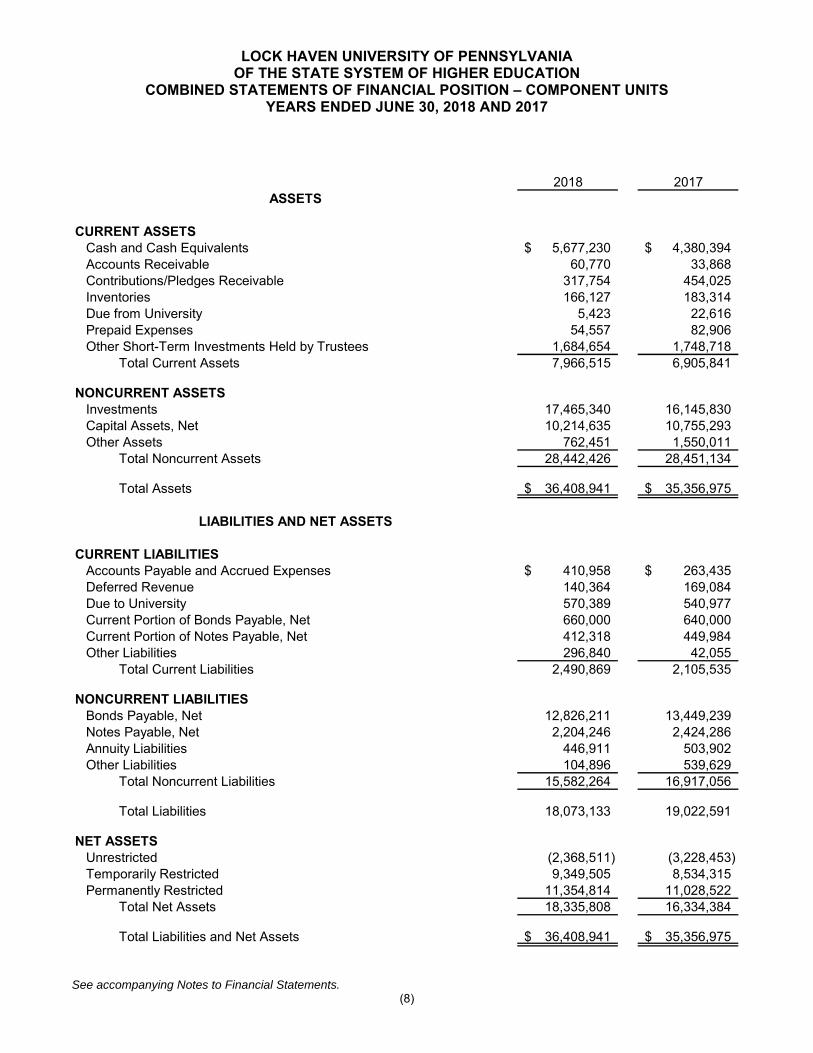

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

COMBINED STATEMENTS OF FINANCIAL POSITION – COMPONENT UNITS YEARS ENDED JUNE 30, 2018 AND 2017

See accompanying Notes to Financial Statements. (8)

2018 2017

ASSETS

CURRENT ASSETSCash and Cash Equivalents 5,677,230$ 4,380,394$ Accounts Receivable 60,770 33,868 Contributions/Pledges Receivable 317,754 454,025 Inventories 166,127 183,314 Due from University 5,423 22,616 Prepaid Expenses 54,557 82,906 Other Short-Term Investments Held by Trustees 1,684,654 1,748,718

Total Current Assets 7,966,515 6,905,841

NONCURRENT ASSETSInvestments 17,465,340 16,145,830 Capital Assets, Net 10,214,635 10,755,293 Other Assets 762,451 1,550,011

Total Noncurrent Assets 28,442,426 28,451,134

Total Assets 36,408,941$ 35,356,975$

LIABILITIES AND NET ASSETS

CURRENT LIABILITIESAccounts Payable and Accrued Expenses 410,958$ 263,435$ Deferred Revenue 140,364 169,084 Due to University 570,389 540,977 Current Portion of Bonds Payable, Net 660,000 640,000 Current Portion of Notes Payable, Net 412,318 449,984 Other Liabilities 296,840 42,055

Total Current Liabilities 2,490,869 2,105,535

NONCURRENT LIABILITIESBonds Payable, Net 12,826,211 13,449,239 Notes Payable, Net 2,204,246 2,424,286 Annuity Liabilities 446,911 503,902 Other Liabilities 104,896 539,629

Total Noncurrent Liabilities 15,582,264 16,917,056

Total Liabilities 18,073,133 19,022,591

NET ASSETSUnrestricted (2,368,511) (3,228,453) Temporarily Restricted 9,349,505 8,534,315 Permanently Restricted 11,354,814 11,028,522

Total Net Assets 18,335,808 16,334,384

Total Liabilities and Net Assets 36,408,941$ 35,356,975$

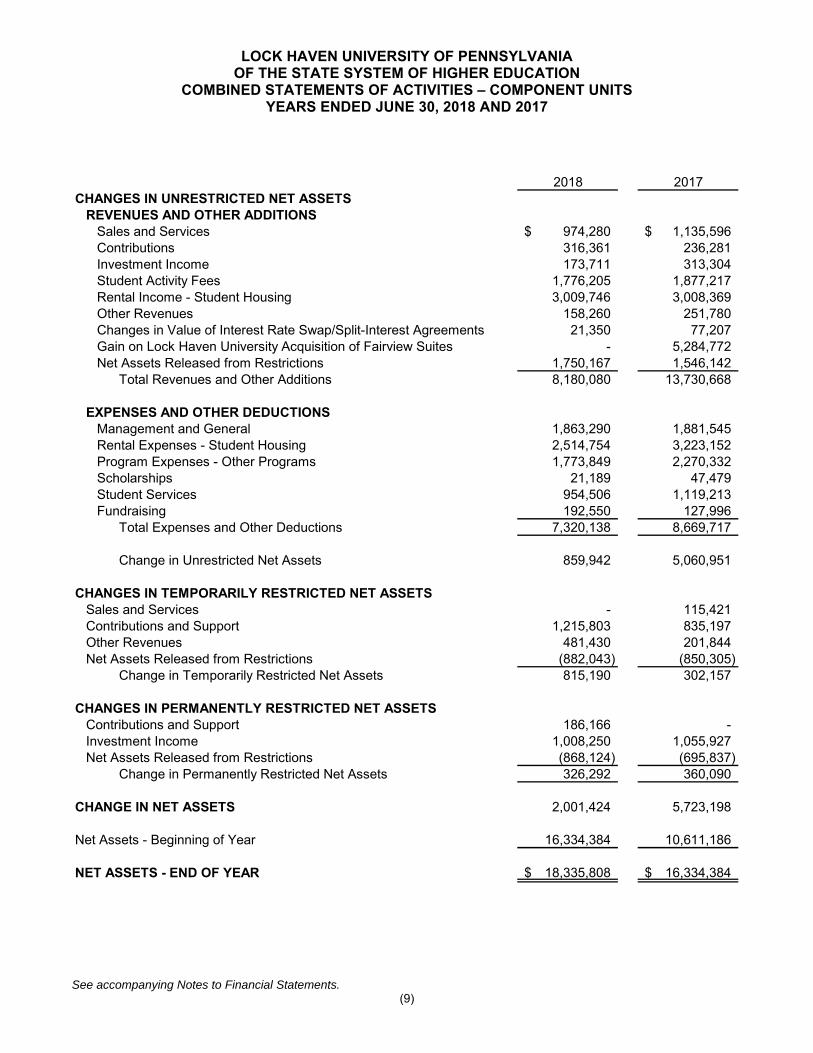

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

COMBINED STATEMENTS OF ACTIVITIES – COMPONENT UNITS YEARS ENDED JUNE 30, 2018 AND 2017

See accompanying Notes to Financial Statements. (9)

2018 2017

CHANGES IN UNRESTRICTED NET ASSETSREVENUES AND OTHER ADDITIONS

Sales and Services 974,280$ 1,135,596$ Contributions 316,361 236,281 Investment Income 173,711 313,304 Student Activity Fees 1,776,205 1,877,217 Rental Income - Student Housing 3,009,746 3,008,369 Other Revenues 158,260 251,780 Changes in Value of Interest Rate Swap/Split-Interest Agreements 21,350 77,207 Gain on Lock Haven University Acquisition of Fairview Suites - 5,284,772

Net Assets Released from Restrictions 1,750,167 1,546,142 Total Revenues and Other Additions 8,180,080 13,730,668

EXPENSES AND OTHER DEDUCTIONSManagement and General 1,863,290 1,881,545 Rental Expenses - Student Housing 2,514,754 3,223,152 Program Expenses - Other Programs 1,773,849 2,270,332 Scholarships 21,189 47,479 Student Services 954,506 1,119,213 Fundraising 192,550 127,996

Total Expenses and Other Deductions 7,320,138 8,669,717

Change in Unrestricted Net Assets 859,942 5,060,951

CHANGES IN TEMPORARILY RESTRICTED NET ASSETSSales and Services - 115,421 Contributions and Support 1,215,803 835,197 Other Revenues 481,430 201,844 Net Assets Released from Restrictions (882,043) (850,305)

Change in Temporarily Restricted Net Assets 815,190 302,157

CHANGES IN PERMANENTLY RESTRICTED NET ASSETSContributions and Support 186,166 - Investment Income 1,008,250 1,055,927 Net Assets Released from Restrictions (868,124) (695,837)

Change in Permanently Restricted Net Assets 326,292 360,090

CHANGE IN NET ASSETS 2,001,424 5,723,198

Net Assets - Beginning of Year 16,334,384 10,611,186

NET ASSETS - END OF YEAR 18,335,808$ 16,334,384$

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(10)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Lock Haven University of Pennsylvania of the State System of Higher Education (the University), a public four year institution located in Lock Haven, Pennsylvania, was founded in 1870. The University is one of fourteen universities of the Pennsylvania State System of Higher Education (the State System). The State System was created by the State System of Higher Education Act of November 12, 1982, P.L. 660, No. 188, as amended (Act 188). The State System is a component unit of the Commonwealth of Pennsylvania (the Commonwealth). The Commonwealth determines the State appropriation allocated to the State System. The State System determines the allocation to each University from the state appropriated amount. Tuition rates are set by the Board of Governors of the State System, for all fourteen member universities. Labor agreements are negotiated at either the State System level or Commonwealth level. Reporting Entity

The University functions as a business-type activity, as defined by the Governmental Accounting Standards Board (GASB). The University has determined the Lock Haven University Student Auxiliary Services, Inc. (SAS), the Lock Haven University Foundation and the Clearfield Educational Foundation, Inc. (collectively the Foundations), should be included in the University’s financial statements as discretely presented component units. A component unit is a legally separate organization for which the primary institution is financially accountable or closely related. The Foundations and SAS are private nonprofit organizations reported in accordance with Financial Accounting Standards Board (FASB) requirements, including FASB Codification Section 958-205, Presentation of Financial Statements. As such, certain revenue recognition criteria and presentation features are different from GASB revenue recognition criteria and presentation features. No modifications have been made to the component units’ financial information in the University’s financial reporting entity for these differences. SAS is the successor corporation to Lock Haven University Student Cooperative Council, Inc. (the Council). SAS collects student activity fees and other miscellaneous revenues, which are allocated to clubs, organizations, athletic programs, and general administration. SAS also operates the Campus Bookstore and the Student Recreation Center. SAS is a legally separate tax-exempt entity that is considered a component unit of the University and is included within the University’s financial reporting entity because the economic resources received and held by SAS are for the direct benefit of the University and because of the influence the University has over SAS. The financial activity of SAS is presented as of and for the fiscal years ended June 30, 2018 and 2017.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(11)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

Reporting Entity (Continued)

The Foundations are legally separate, tax-exempt entities that act as fundraising organizations to supplement the resources that are available to the University in support of its programs. In addition, the Lock Haven University Foundation develops and manages student housing facilities and the Durrwachter Alumni Conference Center. Although the University does not control the timing or amount of receipts from the Foundations, the majority of resources or income thereon that the Foundations hold and invest related to their fundraising efforts are restricted by the donors to the activities of the University. Because these restricted resources held by the Foundations can only be used by, or for the benefit of, the University, the Foundations are considered component units of the University and are discretely presented in the University’s financial statements. The financial activity of the Foundations is presented as of and for the fiscal years ended June 30, 2018 and 2017. During the years ended June 30, 2018 and 2017, the Lock Haven University Foundation (LHUF) awarded grants-in-aid and scholarships of $532,351 and $47,479, respectively. During the years ended June 30, 2018 and 2017, the Clearfield Educational Foundation, Inc. distributed $21,189 and $16,980, respectively, to the University for restricted purposes. The differences between the Due to/ Due from Component Units in the University’s financial statements and the Due to/ Due from University in the Component Units financial statements are due to timing of receipts and disbursements as of June 30, 2018 and 2017. Management does not consider these differences to be material. Complete financial statements for SAS and the Foundations may be obtained at the University’s Administrative Office. Measurement Focus, Basis of Accounting, and Basis of Presentation

The accompanying financial statements have been prepared using the economic resources measurement focus and the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America, as prescribed by GASB. The economic resources measurement focus reports all inflows, outflows, and balances that affect an entity’s net position. Under the accrual basis of accounting, revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Grants and similar items are recognized as revenue as soon as all eligibility requirements have been met.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(12)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

Measurement Focus, Basis of Accounting, and Basis of Presentation (Continued)

The accompanying financial statements of the component units, which are all private nonprofit organizations, are reported in accordance with Financial Standards Accounting Board (FASB) requirements, including FASB Codification Section 958-205, Presentation of Financial Statements. As such, revenue recognition criteria and presentation features are different from GASB revenue recognition criteria and presentation features. No modifications for these differences have been made to the component units’ financial information presented herein. Operating Revenues and Expenses

The University records tuition; all academic, instructional, and other student fees; grants and contracts; sales and services of educational activities; and auxiliary enterprise revenues as operating revenues. In addition, governmental and private grants and contracts in which the grantor receives equal value for the funds given to the University are recorded as operating revenue. All expenses, with the exception of interest expense, loss on investments, loss on the disposal of assets, and extraordinary expenses are recorded as operating expenses. Appropriations, gifts, investment income (except for interest earned by auxiliaries totaling $245,932 and $175,188 for the years ended June 30, 2018 and 2017, respectively, which are included in auxiliary revenues), capital grants, gains on investments, gains on the disposal of assets, parking and library fines, and governmental and private research and other grants and contracts (including Pell grants), in which the grantor does not receive equal value for the funds given to the University are reported as nonoperating revenue. Scholarship Discounts and Allowances and Waivers

Student tuition and fee revenues, and certain other revenues from students, are reported net of scholarship discounts and allowances in the statement of revenues, expenses, and changes in net position. Scholarship discounts and allowances are the difference between the stated charge for goods and services provided by the University and the amount that is paid by students and/or third-parties making payments on students’ behalf. To the extent that revenues from such programs are used to satisfy tuition and fees and other student services, the University has recorded a scholarship discount and allowance. In accordance with a formula prescribed by the National Association of College and University Business Officers (NACUBO), the University allocates the cost of scholarships, waivers, and other student financial aid between Scholarship discounts and allowances (netted against tuition and fees) and Student aid expense. Scholarships and waivers of room and board fees are reported in auxiliary enterprises. The cost of tuition waivers granted to employees is reported as employees’ benefits expense.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(13)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

Net Position

Net position is the residual of Assets plus Deferred Outflows of Resources less Liabilities less Deferred Inflows of Resources. The University maintains the following classifications of net position:

Net Investment in Capital Assets – Capital assets, net of accumulated depreciation, reduced by the outstanding principal balances of any borrowings used for the acquisition, construction or improvement of those assets and increased by any unspent proceeds related to that debt. Restricted – Nonexpendable – Net position subject to externally imposed conditions requiring that they be maintained by the University in perpetuity. Restricted – Expendable – Net position whose use is subject to externally imposed conditions that can be fulfilled by the actions of the University or by the passage of time. Unrestricted – All other categories of net position. Unrestricted net position may be designated for specific purposes by the University’s Council of Trustees.

When both restricted and unrestricted funds are available for expenditure, the decision as to which funds are used first is left to the discretion of the University. Cash Equivalents and Investments

The University considers all demand and time deposits and money market funds, and overnight repurchase agreements to be cash equivalents. Investments purchased are stated at fair value. Investments received as gifts are recorded at their fair value or appraised values as of the date of the gift. The University classifies investments as short-term when they are readily marketable and intended to be converted to cash within one year. Accounts and Loans Receivable

Accounts and loans receivable consist of tuition and fees charged to current and former students, amounts due from federal and state governments in connection with reimbursements of allowable expenditures made pursuant to grants and contracts and other miscellaneous sources. Accounts and loans receivable are reported at net realizable value. Accounts are written off when they are determined to be uncollectible based upon management’s assessment of individual accounts. The allowance for doubtful accounts is estimated based upon the University’s historical losses and periodic review of individual accounts.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(14)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

Capital Assets

Land and buildings at the University’s campus acquired or constructed prior to the creation of the State System on July 1, 1983, are owned by the Commonwealth and made available to the University. Since the University neither owns such assets nor is responsible to service associated bond indebtedness, no value is ascribed thereto in the accompanying financial statements. Likewise, no value is ascribed to the portion of any land or buildings acquired or constructed utilizing capital funds appropriated by the Commonwealth after June 30, 1983, and made available to the University. Buildings, equipment, and furnishings acquired or constructed by the University after June 30, 1983, through the expenditure of University funds or the incurring of debt, are stated at cost less accumulated depreciation, calculated using the straight-line method. All assets with a purchase cost, or acquisition value if acquired by gift, in excess of $5,000 with an estimated useful life of two years or greater are capitalized. Assets under capital leases are recorded at the lower of the present value of the minimum lease payments or the fair value of the asset. Amortization of assets under capital lease is included in depreciation. All library books are capitalized. Normal repair and maintenance expenditures are not capitalized because they neither add to the value of the property nor materially prolong its useful life. The University does not capitalize collections of art, rare books, historical items, etc., as they are held for public exhibition, education, or research rather than financial gain. Impairment of Capital Assets

Management reviews capital assets for impairment whenever events or changes in circumstances indicate that the service utility of an asset has declined significantly and unexpectedly. Any write-downs due to impairment are charged to operations at the time impairment is identified. No write-down of capital assets was required for the years ended June 30, 2018 and 2017. Deferred Outflows and Deferred Inflows of Resources

The balance sheet reports separate sections for Deferred Outflows of Resources and Deferred Inflows of Resources. Deferred Outflows of Resources, reported after Total Assets, is defined by GASB as a consumption of net position that applies to future periods. The expense is recognized in the applicable future period(s). Deferred Inflows of Resources, reported after Total Liabilities, is defined by GASB as an acquisition of net position that applies to future periods. The revenue is recognized in the applicable future period(s). Transactions are classified as deferred outflows of resources or deferred inflows of resources only when specifically prescribed by GASB standards.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(15)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

Deferred Outflows and Deferred Inflows of Resources (Continued)

The University is required to report the following as Deferred Outflows of Resources or Deferred Inflows of Resources. Deferred gain or loss on bond refunding, which results when the carrying value of a

refunded bond is greater or less than its reacquisition price. The difference is deferred and amortized over the remaining life of the old bond or the life of the new bond, whichever is shorter.

For defined benefit pension and other postemployment benefit (OPEB) plans: the

difference between expected (actuarial) and actual experience, changes in actuarial assumptions, net difference between projected (actuarial) and actual earnings on pension and OPEB plan investments, changes in the University’s proportion of expenses and liabilities to the pension or OPEB plans as a whole, differences between the University’s pension and OPEB plan contributions and its proportionate share of contributions, and University pension and OPEB plans contributions subsequent to the respective pension or OPEB valuation measurement date.

Unearned Revenue

Unearned revenue includes amounts for tuition and fees, grants, corporate sponsorship payments, and certain auxiliary activities received prior to the end of the fiscal year but earned in a subsequent accounting period. Compensated Absences

The estimated cost of future payouts of annual leave and sick leave that employees have earned for services rendered, and which the employees may be entitled to receive upon termination or retirement, is recorded as a liability. Pension Plans and OPEB Plans

Employees of the University enroll in one of three available retirement plans immediately upon employment. The Commonwealth of Pennsylvania State Employees’ Retirement System (SERS) and Public School Employees’ Retirement System (PSERS) are governmental cost-sharing multiple-employer defined benefit plans. The Alternative Retirement Plan (ARP) is a defined contribution plan administered by the State System. The State System also offers healthcare and tuition benefits to eligible University employees upon employment, which vary depending upon the employee’s labor group. Income Taxes

The University, as a member of the State System, is tax-exempt; accordingly, no provision for income taxes has been made in the accompanying financial statements.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(16)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosures of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Reclassifications

Certain amounts in the prior period presented have been reclassified to conform to the current period financial statement presentation. These reclassifications have no effect on the previously reported net position or changes therein. New Accounting Standards

The University has implemented GASB Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions. Statement No. 75 requires the University to report its share of the liabilities, expense, deferred outflows of resources, and deferred inflows of resources allocated to it by the Retired Employees Health Program and the Public School Employees’ Retirement System Health Insurance Premium Assistance Program, both of which are defined benefit retiree healthcare plans administered by the Commonwealth of Pennsylvania. Statement No. 75 also has significantly increased the liability that the University records for the defined benefit retiree healthcare and tuition benefits plan that the State System administers, and requires the recording of deferred outflows of resources and deferred inflows of resources associated with the plan. The July 1, 2017 balances of these other postemployment benefit liabilities (with “other” meaning “other than pensions”), known as OPEB liabilities, and related deferred outflows of resources and deferred inflows of resources, are reported in the Statement of Revenues, Expenses, and Changes in Net Position as a restatement to the 2017 Net position—beginning of year. The plans did not provide sufficient information to restate the June 30, 2017 financial statements. Net Position - Beginning of Year, as Previously Stated 1,458,407$

Restatement for July 1, 2017 OPEB Liabilities and Related Expenses (61,918,719)

Net Position - Beginning of Year, Restated (60,460,312)$

GASB has issued several accounting standards that are required to be adopted by the University in future years. The University is evaluating the impact of adoption of these standards on its financial statements as discussed below.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(17)

NOTE 1 NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

New Accounting Standards (Continued)

In June 2017, GASB issued Statement No. 87, Leases. Statement No. 87 establishes a single model for lease accounting based on the foundational principle that leases are financings of the right to use an underlying asset. In other words, most leases currently classified as operating leases will be accounted for and reported in a similar manner as capital leases, with assets and liabilities recorded at lease inception. The University has determined that, although Statement No. 87 will change the way it accounts for its operating leases, it will have little, if any, effect on its net position or results of operations. The provisions in Statement No. 87 are effective for reporting periods beginning after December 15, 2019. In March 2018, GASB issued Statement No. 88, Certain Disclosures Related to Debt, including Direct Borrowings and Direct Placements. Statement No. 88 is intended to improve the information that is disclosed in notes to government financial statements related to debt. The University has determined that Statement No. 88 will have no effect on its financial statements. In June 2018, GASB issued Statement No. 89, Accounting for Interest Cost Incurred before the End of a Construction Period. Statement No. 89 requires that interest cost incurred before the end of a construction period be recognized as an expense in the period in which the cost is incurred, and should no longer be capitalized as part of the cost of an asset. The University has determined that the effect of Statement No. 89 on its financial statements will vary from year to year, depending upon the amount of new debt incurred for capital assets. The provisions of Statement No. 89 are effective for reporting periods beginning after December 15, 2019. In August 2018, GASB issued Statement No. 90, Majority Equity Interests. Statement No. 90 is intended to improve the consistency and comparability of reporting a government’s majority equity interest in a legally separate organization and to improve the relevance of financial statement information for certain component units. The University has determined that Statement No. 90 will have no effect on its financial statements.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(18)

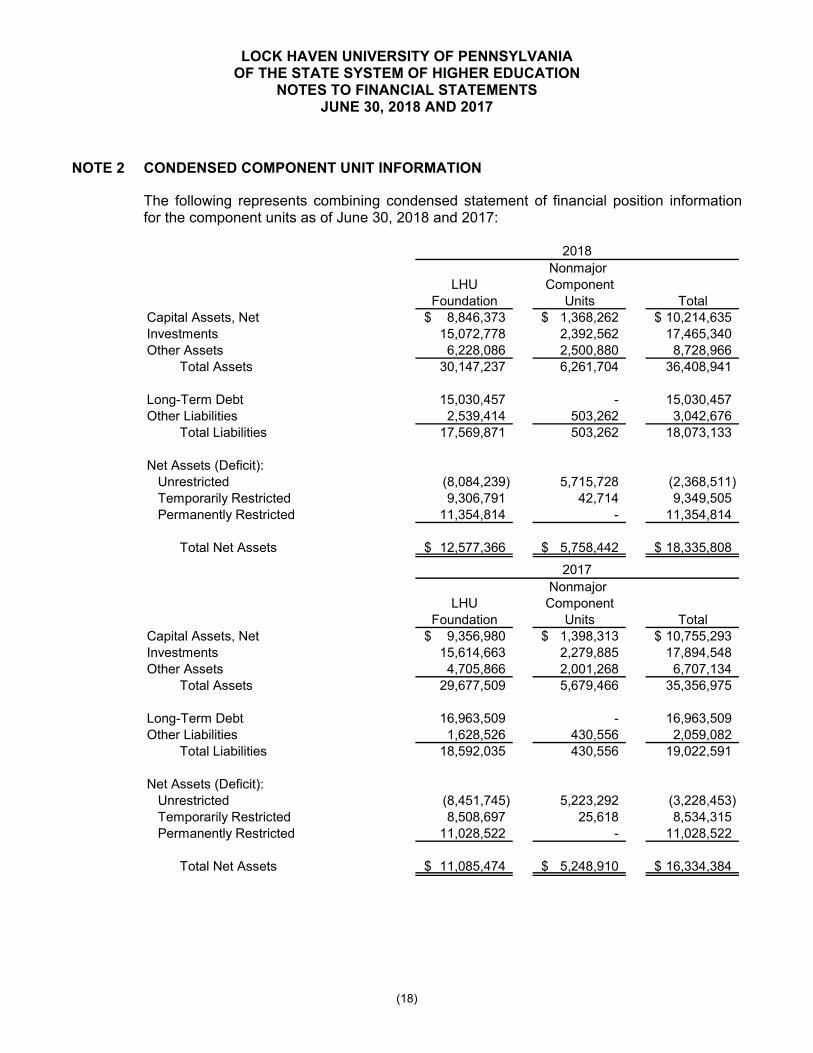

NOTE 2 CONDENSED COMPONENT UNIT INFORMATION

The following represents combining condensed statement of financial position information for the component units as of June 30, 2018 and 2017:

Nonmajor LHU Component

Foundation Units TotalCapital Assets, Net 8,846,373$ 1,368,262$ 10,214,635$ Investments 15,072,778 2,392,562 17,465,340 Other Assets 6,228,086 2,500,880 8,728,966

Total Assets 30,147,237 6,261,704 36,408,941

Long-Term Debt 15,030,457 - 15,030,457 Other Liabilities 2,539,414 503,262 3,042,676

Total Liabilities 17,569,871 503,262 18,073,133

Net Assets (Deficit):Unrestricted (8,084,239) 5,715,728 (2,368,511) Temporarily Restricted 9,306,791 42,714 9,349,505 Permanently Restricted 11,354,814 - 11,354,814

Total Net Assets 12,577,366$ 5,758,442$ 18,335,808$

2018

Nonmajor LHU Component

Foundation Units TotalCapital Assets, Net 9,356,980$ 1,398,313$ 10,755,293$ Investments 15,614,663 2,279,885 17,894,548 Other Assets 4,705,866 2,001,268 6,707,134

Total Assets 29,677,509 5,679,466 35,356,975

Long-Term Debt 16,963,509 - 16,963,509 Other Liabilities 1,628,526 430,556 2,059,082

Total Liabilities 18,592,035 430,556 19,022,591

Net Assets (Deficit):Unrestricted (8,451,745) 5,223,292 (3,228,453) Temporarily Restricted 8,508,697 25,618 8,534,315 Permanently Restricted 11,028,522 - 11,028,522

Total Net Assets 11,085,474$ 5,248,910$ 16,334,384$

2017

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(19)

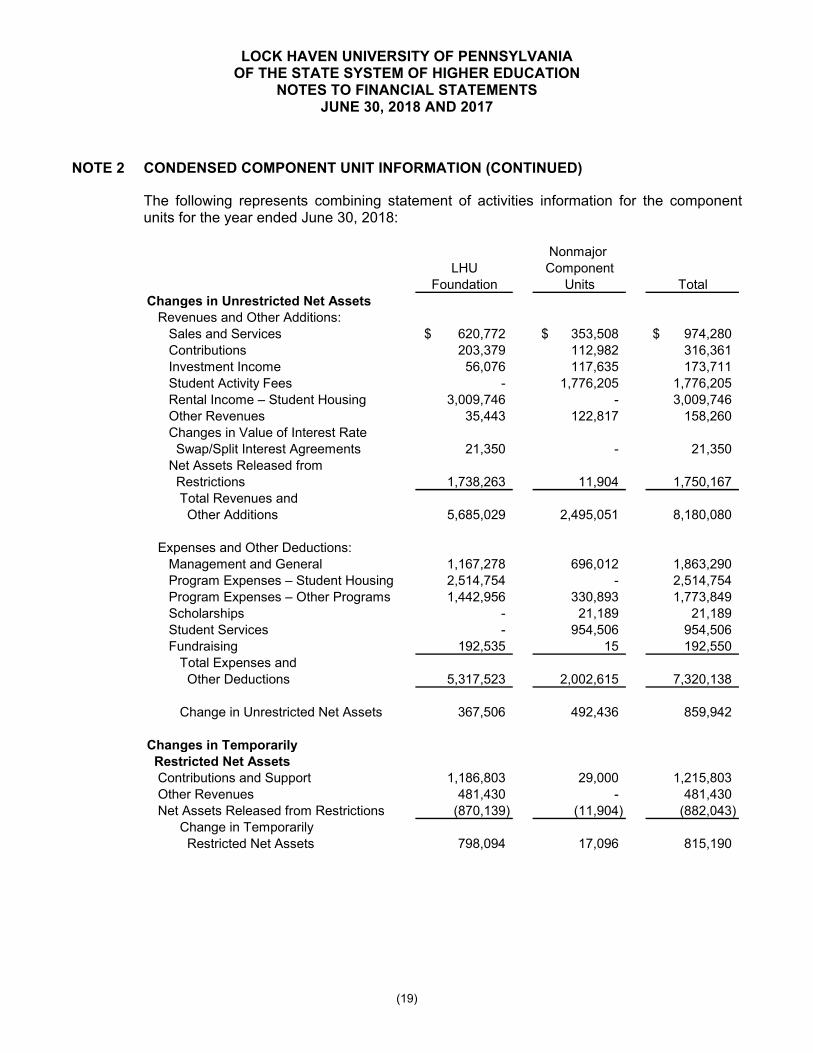

NOTE 2 CONDENSED COMPONENT UNIT INFORMATION (CONTINUED)

The following represents combining statement of activities information for the component units for the year ended June 30, 2018:

Nonmajor LHU Component

Foundation Units TotalChanges in Unrestricted Net Assets

Revenues and Other Additions:Sales and Services 620,772$ 353,508$ 974,280$ Contributions 203,379 112,982 316,361 Investment Income 56,076 117,635 173,711 Student Activity Fees - 1,776,205 1,776,205 Rental Income – Student Housing 3,009,746 - 3,009,746 Other Revenues 35,443 122,817 158,260 Changes in Value of Interest Rate Swap/Split Interest Agreements 21,350 - 21,350 Net Assets Released from Restrictions 1,738,263 11,904 1,750,167

Total Revenues and Other Additions 5,685,029 2,495,051 8,180,080

Expenses and Other Deductions:Management and General 1,167,278 696,012 1,863,290 Program Expenses – Student Housing 2,514,754 - 2,514,754 Program Expenses – Other Programs 1,442,956 330,893 1,773,849 Scholarships - 21,189 21,189 Student Services - 954,506 954,506 Fundraising 192,535 15 192,550

Total Expenses and Other Deductions 5,317,523 2,002,615 7,320,138

Change in Unrestricted Net Assets 367,506 492,436 859,942

Changes in Temporarily Restricted Net Assets

Contributions and Support 1,186,803 29,000 1,215,803 Other Revenues 481,430 - 481,430 Net Assets Released from Restrictions (870,139) (11,904) (882,043)

Change in Temporarily Restricted Net Assets 798,094 17,096 815,190

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(20)

NOTE 2 CONDENSED COMPONENT UNIT INFORMATION (CONTINUED)

Nonmajor LHU Component

Foundation Units TotalChanges in Permanently Restricted Net Assets

Contributions and Support 186,166$ -$ 186,166$ Investment Income 1,008,250 - 1,008,250 Net Assets Released from Restrictions (868,124) - (868,124)

Change in Permanently Restricted Net Assets 326,292 - 326,292

CHANGE IN NET ASSETS 1,491,892 509,532 2,001,424

Net Assets - Beginning of Year 11,085,474 5,248,910 16,334,384

NET ASSETS - END OF YEAR 12,577,366$ 5,758,442$ 18,335,808$

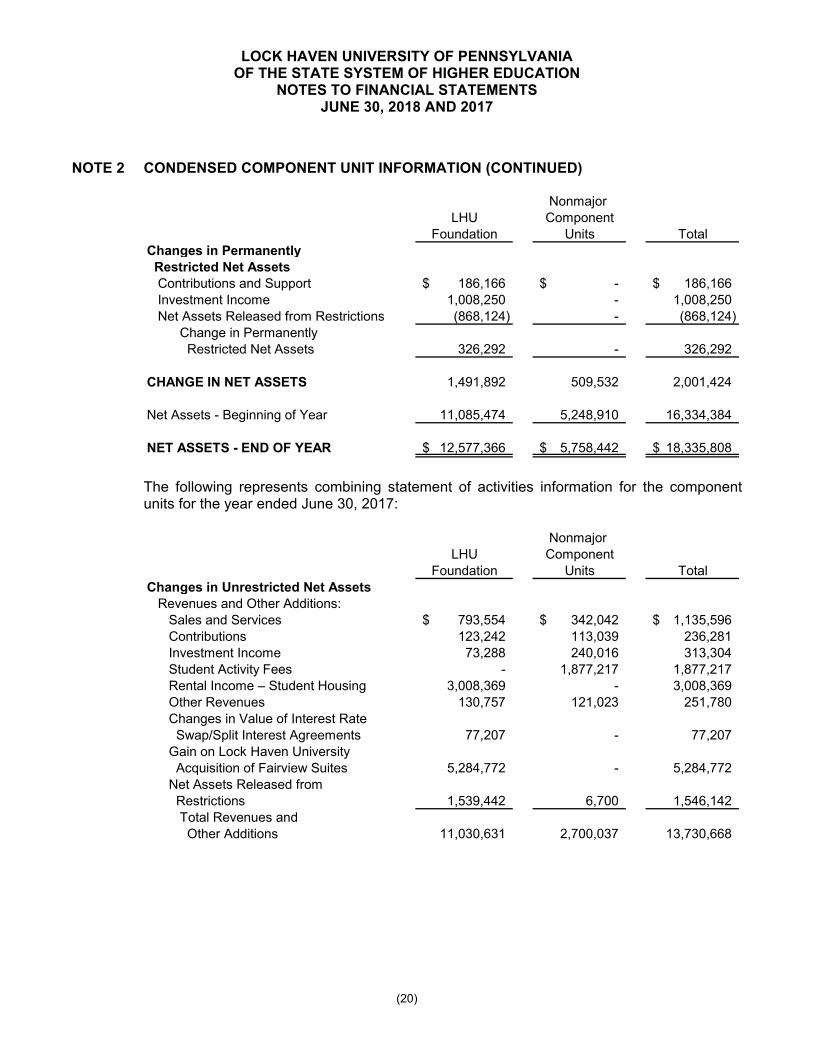

The following represents combining statement of activities information for the component units for the year ended June 30, 2017:

Nonmajor LHU Component

Foundation Units TotalChanges in Unrestricted Net Assets

Revenues and Other Additions:Sales and Services 793,554$ 342,042$ 1,135,596$ Contributions 123,242 113,039 236,281 Investment Income 73,288 240,016 313,304 Student Activity Fees - 1,877,217 1,877,217 Rental Income – Student Housing 3,008,369 - 3,008,369 Other Revenues 130,757 121,023 251,780 Changes in Value of Interest Rate Swap/Split Interest Agreements 77,207 - 77,207 Gain on Lock Haven University Acquisition of Fairview Suites 5,284,772 - 5,284,772 Net Assets Released from Restrictions 1,539,442 6,700 1,546,142

Total Revenues and Other Additions 11,030,631 2,700,037 13,730,668

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(21)

NOTE 2 CONDENSED COMPONENT UNIT INFORMATION (CONTINUED)

Nonmajor LHU Component

Foundation Units TotalChanges in Unrestricted Net Assets (Continued)

Expenses and Other Deductions:Management and General 1,180,845$ 700,700$ 1,881,545$ Program Expenses – Student Housing 3,223,152 - 3,223,152 Program Expenses – Other Programs 1,851,530 418,802 2,270,332 Scholarships 30,391 17,088 47,479 Student Services - 1,119,213 1,119,213 Fundraising 127,981 15 127,996

Total Expenses and Other Deductions 6,413,899 2,255,818 8,669,717

Change in Unrestricted Net Assets 4,616,732 444,219 5,060,951

Changes in Temporarily Restricted Net Assets

Sales and Services 115,421 - 115,421 Contributions and Support 809,697 25,500 835,197 Other Revenues 201,844 - 201,844 Net Assets Released Restrictions (843,605) (6,700) (850,305)

Change in Temporarily Restricted Net Assets 283,357 18,800 302,157

Changes in Permanently Restricted Net Assets

Investment Income 1,055,927 - 1,055,927 Net Assets Released from Restrictions (695,837) - (695,837)

Change in Permanently Restricted Net Assets 360,090 - 360,090

CHANGE IN NET ASSETS 5,260,179 463,019 5,723,198

Net Assets - Beginning of Year 5,825,295 4,785,891 10,611,186

NET ASSETS - END OF YEAR 11,085,474$ 5,248,910$ 16,334,384$

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(22)

NOTE 3 DEPOSITS AND INVESTMENTS

The University predominantly maintains its cash balances on deposit with the State System. The State System maintains these and other System funds on a pooled basis. Although the State System pools its funds in a manner similar to an internal investment pool, individual State System entities do not hold title to any assets in the fund. The State System as a whole owns title to all assets. The University does not participate in the unrealized gains or losses on the investment pool; instead, the University holds shares equal to its cash balance. Each share has a constant value of $1, and income is allocated based on the number of shares owned. Revenue realized at the State System level is calculated on a daily basis and posted monthly to each entity’s account as interest income. The University’s portion of pooled funds was $66,678,760 and $66,800,132 at June 30, 2018 and 2017, respectively. The State System invests its funds in accordance with Board of Governors’ Policy 1986 02-A, Investment, which authorizes the State System to invest in obligations of the U.S. Treasury, repurchase agreements, commercial paper, certificates of deposit, banker’s acceptances, U.S. money market funds, municipal bonds, corporate bonds, collateralized mortgage obligations (CMOs), asset-backed securities, and internal loan funds. Restricted nonexpendable funds and amounts designated by the board or university trustees may be invested in the investments described above as well as in corporate equities and approved pooled common funds. For purposes of convenience and expedience, universities use local financial institutions for activities such as deposits of cash. In addition, universities may accept gifts of investments from donors as long as risk is limited to the investment itself. Restricted gifts of investments fall outside the scope of the investment policy. In keeping with its legal status as a system of public universities, the State System recognizes a fiduciary responsibility to invest all funds prudently and in accordance with ethical and prevailing legal standards. Investment decisions are intended to minimize risk while maximizing asset value. Adequate liquidity is maintained so that assets can be held to maturity. High quality investments are preferred. Reasonable portfolio diversification is pursued to ensure that no single security or investment or class of securities or investments will have a disproportionate or significant impact on the total portfolio. Investments may be made in U.S. dollar-denominated debt of high quality U.S. and non-U.S. corporations. Investment performance is monitored on a frequent and regular basis to ensure that objectives are attained and guidelines are followed. Safety of principal and liquidity are the top priorities for the investment of the State System’s operating funds. Within those guidelines, income optimization is pursued. Speculative investment activity is not allowed: this includes investing in asset classes such as commodities, futures, short-sales, equities, real or personal property, options, venture capital investments, private placements, letter stocks, and unlisted securities.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(23)

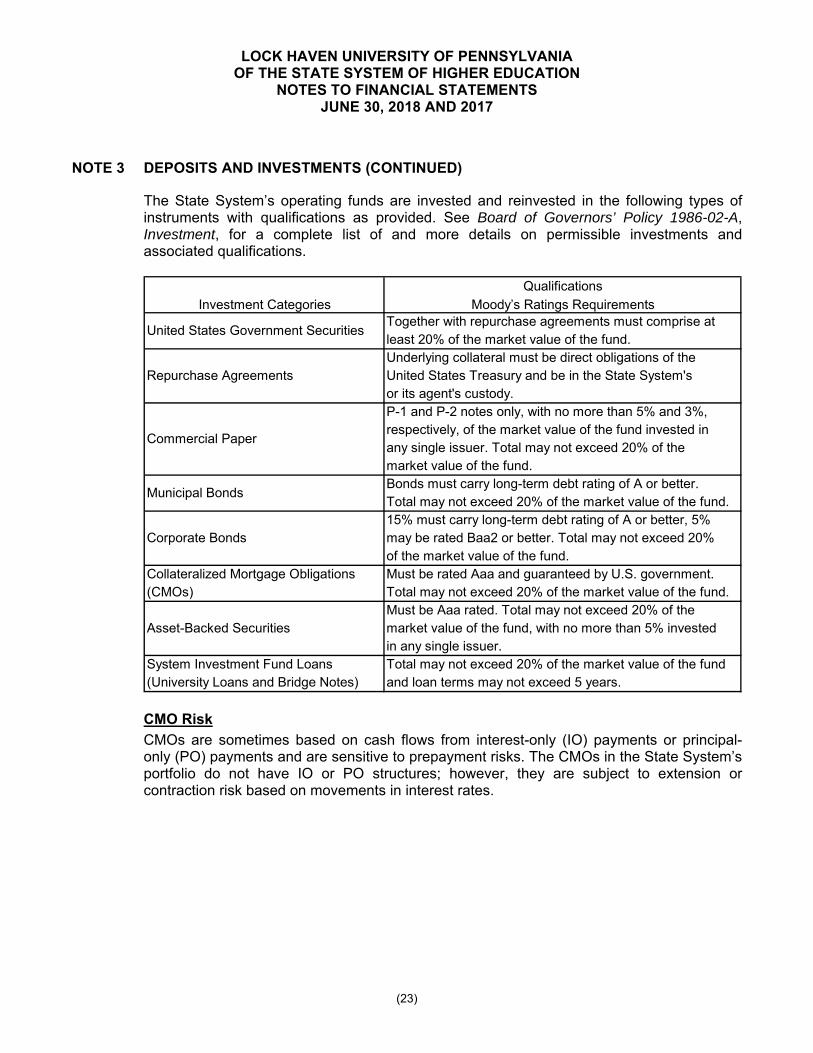

NOTE 3 DEPOSITS AND INVESTMENTS (CONTINUED)

The State System’s operating funds are invested and reinvested in the following types of instruments with qualifications as provided. See Board of Governors’ Policy 1986-02-A, Investment, for a complete list of and more details on permissible investments and associated qualifications.

Qualifications

Investment Categories Moody’s Ratings RequirementsTogether with repurchase agreements must comprise atleast 20% of the market value of the fund.Underlying collateral must be direct obligations of the

Repurchase Agreements United States Treasury and be in the State System'sor its agent's custody.P-1 and P-2 notes only, with no more than 5% and 3%,respectively, of the market value of the fund invested in any single issuer. Total may not exceed 20% of themarket value of the fund.Bonds must carry long-term debt rating of A or better.Total may not exceed 20% of the market value of the fund.15% must carry long-term debt rating of A or better, 5%

Corporate Bonds may be rated Baa2 or better. Total may not exceed 20%of the market value of the fund.

Collateralized Mortgage Obligations Must be rated Aaa and guaranteed by U.S. government.(CMOs) Total may not exceed 20% of the market value of the fund.

Must be Aaa rated. Total may not exceed 20% of theAsset-Backed Securities market value of the fund, with no more than 5% invested

in any single issuer.System Investment Fund Loans Total may not exceed 20% of the market value of the fund(University Loans and Bridge Notes) and loan terms may not exceed 5 years.

Commercial Paper

United States Government Securities

Municipal Bonds

CMO Risk

CMOs are sometimes based on cash flows from interest-only (IO) payments or principal-only (PO) payments and are sensitive to prepayment risks. The CMOs in the State System’s portfolio do not have IO or PO structures; however, they are subject to extension or contraction risk based on movements in interest rates.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(24)

NOTE 3 DEPOSITS AND INVESTMENTS (CONTINUED)

Moody’s Rating

The State System uses ratings from Moody’s Investors Service, Inc. to indicate the credit risk of investments, i.e., the risk that an issuer or other counterparty to an investment will not fulfill its obligations. An Aaa rating indicates the highest quality obligations with minimal credit risk. Ratings that begin with Aa indicate high quality obligations subject to very low credit risk; ratings that begin with A indicate upper-medium-grade obligations subject to low credit risk; and ratings that begin with Baa indicate medium-grade obligations, subject to moderate credit risk, that may possess certain speculative characteristics. Moody’s appends the ratings with numerical modifiers 1, 2, and 3, with 1 indicating a higher ranking and 3 indicating a lower ranking within the category. For short-term obligations, a rating of P-1 indicates that issuers have a superior ability to repay short-term debt obligations, and a rating of P-2 indicates that issuers have a strong ability to repay short-term debt obligations. Modified Duration

The State System denotes interest rate risk, or the risk that changes in interest rates will affect the fair value of an investment, using modified duration. Duration is a measurement in years of how long it takes for the price of a bond to be repaid by its internal cash flows. Modified duration takes into account changing interest rates. The State System maintains a portfolio duration target of 1.8 years with an upper limit of 2.5 years for the intermediate-term component of the operating portion of the investment portfolio. The State System’s duration targets are not applicable to its long-term investments. Fair Value Hierarchy

GASB Statement No. 72, Fair Value Measurement and Application, requires that investments be classified according to a “fair value hierarchy.” With respect to Statement No. 72’s fair value hierarchy, GASB defines “inputs” as “the assumptions that market participants would use when pricing an asset or liability, including assumptions about risk.” Statement No. 72 further categorizes inputs as observable or unobservable: Observable inputs are “inputs that are developed using market data, such as publicly available information about actual events or transactions, and which reflect the assumptions that market participants would use when pricing an asset or liability”; Unobservable inputs are “inputs for which market data are not available and that are developed using the best information available about the assumptions that market participants would use when pricing an asset or liability.”

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(25)

NOTE 3 DEPOSITS AND INVESTMENTS (CONTINUED)

Fair Value Hierarchy (Continued)

Statement No. 72’s fair value hierarchy categorizes the inputs to valuation techniques used to measure fair value into three “levels”:

Level 1 – Investments whose values are based on unadjusted quoted prices for identical assets or liabilities in an active market, such as stocks listed in the S&P 500 or NASDAQ. If an up-to-date price of the investment can be found on a major exchange, it is a Level 1 investment. Level 2 – Investments whose values are based on their quoted prices in inactive markets or whose values are based on models, and the inputs to those models are observable either directly or indirectly for substantially the full term of the asset or liability. Level 3 – Investments that trade infrequently, and as a result do not have many reliable market prices. Valuations of Level 3 investments typically are based on management assumptions or expectations. For example, a private equity investment or complex derivative would likely be a Level 3 investment.

In addition, the fair value of certain investments that do not have a readily determinable fair value is classified as NAV, meaning Net Asset Value per share, when the fair value is calculated in a manner consistent with the Financial Accounting Standards Board’s measurement principles for investment companies. Debt and equity securities classified in Level 1 of the fair value hierarchy are valued using prices quoted in active markets for those securities. Debt and equity securities classified in Level 2 of the fair value hierarchy are valued using a matrix pricing technique. Matrix pricing is used to value securities based on the securities’ relationship to benchmark quoted prices. Securities classified in Level 3 of the fair value hierarchy lack an independent pricing source and so are valued using an internal fair value as provided by the investment manager. Detailed information regarding the fair value of the State System pooled deposits and investment portfolio is available in the financial statements of the State System, which can be found at www.passhe.edu. The University had no local investments recorded at fair value as of June 30, 2018 and 2017.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(26)

NOTE 3 DEPOSITS AND INVESTMENTS (CONTINUED)

University Local Deposits

At June 30, 2018 and 2017, the carrying amount of the University’s local demand and time deposits were $70,110 and $395,315, respectively, as compared to bank balances of $86,708 and $382,518, respectively. The difference is caused primarily by items in transit. Of the bank balances, $28,732 and $163,338, respectively, were covered by federal government depository insurance, and $57,976 and $219,180, respectively, were uninsured and uncollateralized but covered under the collateralization provisions of the Commonwealth of Pennsylvania Act 72 of 1971, as amended. Act 72 allows banking institutions to satisfy the collateralization requirements by pooling eligible investments to cover total public funds on deposit in excess of federal insurance. Such pooled collateral is pledged with the financial institutions’ trust departments. At June 30, 2018 and 2017, none of the University’s demand and time deposits are exposed to foreign currency risk. Component Units

The fair value of investments for the component units at June 30 is as follows:

Fair ValueHierarchy Level 2018 2017

Investments:Cash and Cash Equivalents Not Applicable 3,478,447$ 3,012,457$ Equity-Based Mutual Funds Level 1 10,512,518 2,693,434 Fixed Income Mutual Funds Level 1 2,746,112 2,104,788 Common Stock Level 1 757,593 5,427,015 Alternative Investment Fund NAV 1,566,180 1,486,884 Dynamic Asset Allocation Mutual Funds Level 1 - 3,089,238 Cash Value of Life Insurance Policies Level 2 89,144 80,732

Total 19,149,994$ 17,894,548$

Reconciliation of Investments:Other Short-Term Investments Held by Trustees:

Cash and Cash Equivalents 1,684,654$ 1,748,718$ Investments - Noncurrent 17,465,340 16,145,830

Total 19,149,994$ 17,894,548$

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(27)

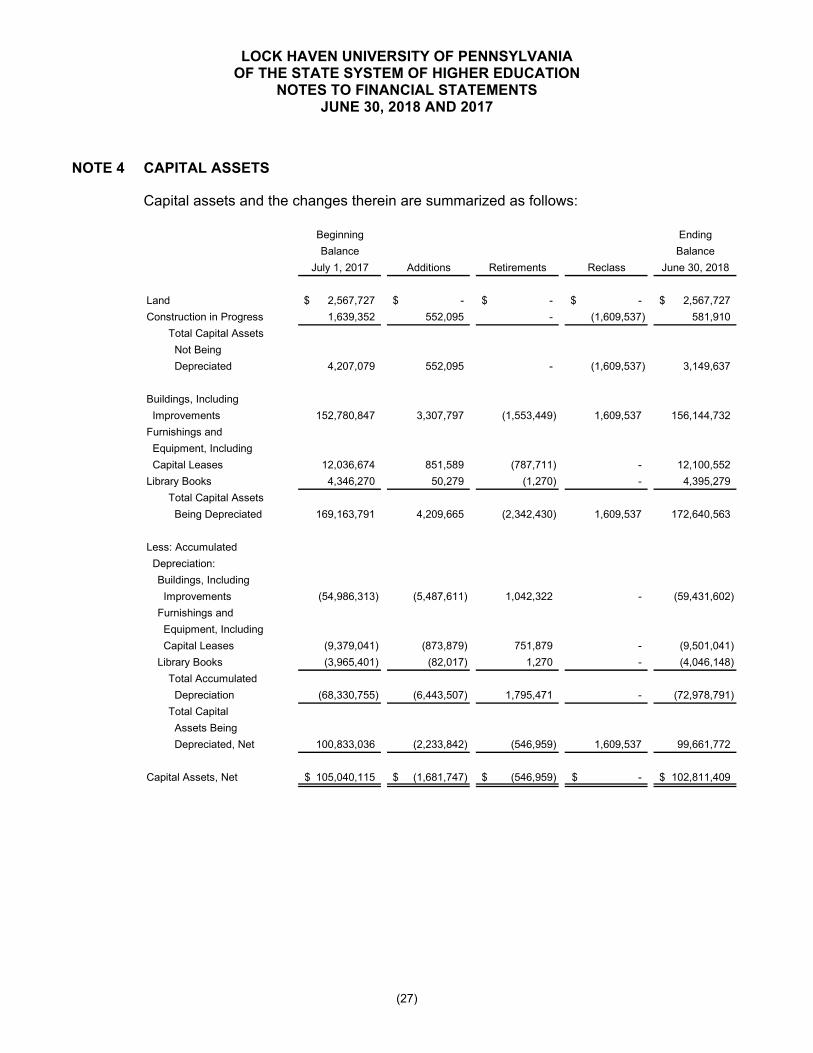

NOTE 4 CAPITAL ASSETS

Capital assets and the changes therein are summarized as follows:

Beginning Ending

Balance Balance

July 1, 2017 Additions Retirements Reclass June 30, 2018

Land 2,567,727$ -$ -$ -$ 2,567,727$

Construction in Progress 1,639,352 552,095 - (1,609,537) 581,910

Total Capital Assets

Not Being

Depreciated 4,207,079 552,095 - (1,609,537) 3,149,637

Buildings, Including

Improvements 152,780,847 3,307,797 (1,553,449) 1,609,537 156,144,732

Furnishings and

Equipment, Including

Capital Leases 12,036,674 851,589 (787,711) - 12,100,552

Library Books 4,346,270 50,279 (1,270) - 4,395,279

Total Capital Assets

Being Depreciated 169,163,791 4,209,665 (2,342,430) 1,609,537 172,640,563

Less: Accumulated

Depreciation:

Buildings, Including

Improvements (54,986,313) (5,487,611) 1,042,322 - (59,431,602)

Furnishings and

Equipment, Including

Capital Leases (9,379,041) (873,879) 751,879 - (9,501,041)

Library Books (3,965,401) (82,017) 1,270 - (4,046,148)

Total Accumulated

Depreciation (68,330,755) (6,443,507) 1,795,471 - (72,978,791)

Total Capital

Assets Being

Depreciated, Net 100,833,036 (2,233,842) (546,959) 1,609,537 99,661,772

Capital Assets, Net 105,040,115$ (1,681,747)$ (546,959)$ -$ 102,811,409$

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(28)

NOTE 4 CAPITAL ASSETS (CONTINUED)

Beginning Ending

Balance Balance

July 1, 2016 Additions Retirements Reclass June 30, 2017

Land 2,567,727$ -$ -$ -$ 2,567,727$

Construction in Progress 3,611,810 1,575,730 (1) (3,548,187) 1,639,352

Total Capital Assets

Not Being

Depreciated 6,179,537 1,575,730 (1) (3,548,187) 4,207,079

Buildings, Including

Improvements 113,753,688 35,478,972 - 3,548,187 152,780,847

Furnishings and

Equipment, Including

Capital Leases 11,190,751 893,958 (48,035) - 12,036,674

Library Books 4,304,994 43,556 (2,280) - 4,346,270

Total Capital Assets

Being Depreciated 129,249,433 36,416,486 (50,315) 3,548,187 169,163,791

Less: Accumulated

Depreciation:

Buildings, Including

Improvements (49,650,557) (5,335,756) - - (54,986,313)

Furnishings and

Equipment, Including

Capital Leases (8,623,417) (797,074) 41,450 - (9,379,041)

Library Books (3,879,141) (88,540) 2,280 - (3,965,401)

Total Accumulated

Depreciation (62,153,115) (6,221,370) 43,730 - (68,330,755)

Total Capital

Assets Being

Depreciated, Net 67,096,318 30,195,116 (6,585) 3,548,187 100,833,036

Capital Assets, Net 73,275,855$ 31,770,846$ (6,586)$ -$ 105,040,115$

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(29)

NOTE 4 CAPITAL ASSETS (CONTINUED)

Major Component Unit

Capital assets of the Lock Haven University Foundation consist of the following at June 30:

2018 2017 Construction in Progress 22,450$ 1,141$ Evergreen Commons 15,412,851 15,286,497 Foundation Village 1,316,849 1,316,849 Durrwachter Alumni Conference Center 563,675 563,675 Fredericks Guest House 430,496 430,496 McGhee School Property 404,406 404,406 Beth Yehuda Synagogue 276,059 276,059 Land 55,000 55,000 Steinway Pianos 58,665 58,665 Vehicle 19,900 40,983

Total Capital Assets 18,560,351 18,433,771 Less: Accumulated Depreciation (9,713,978) (9,076,791)

Total 8,846,373$ 9,356,980$

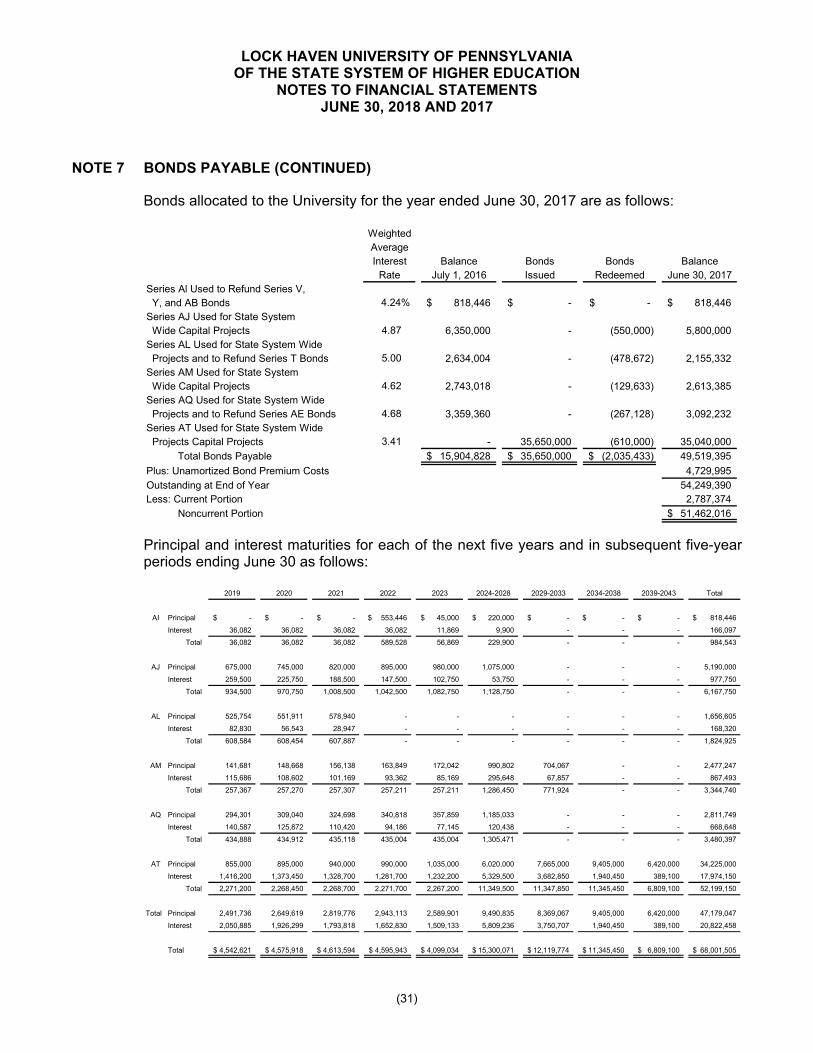

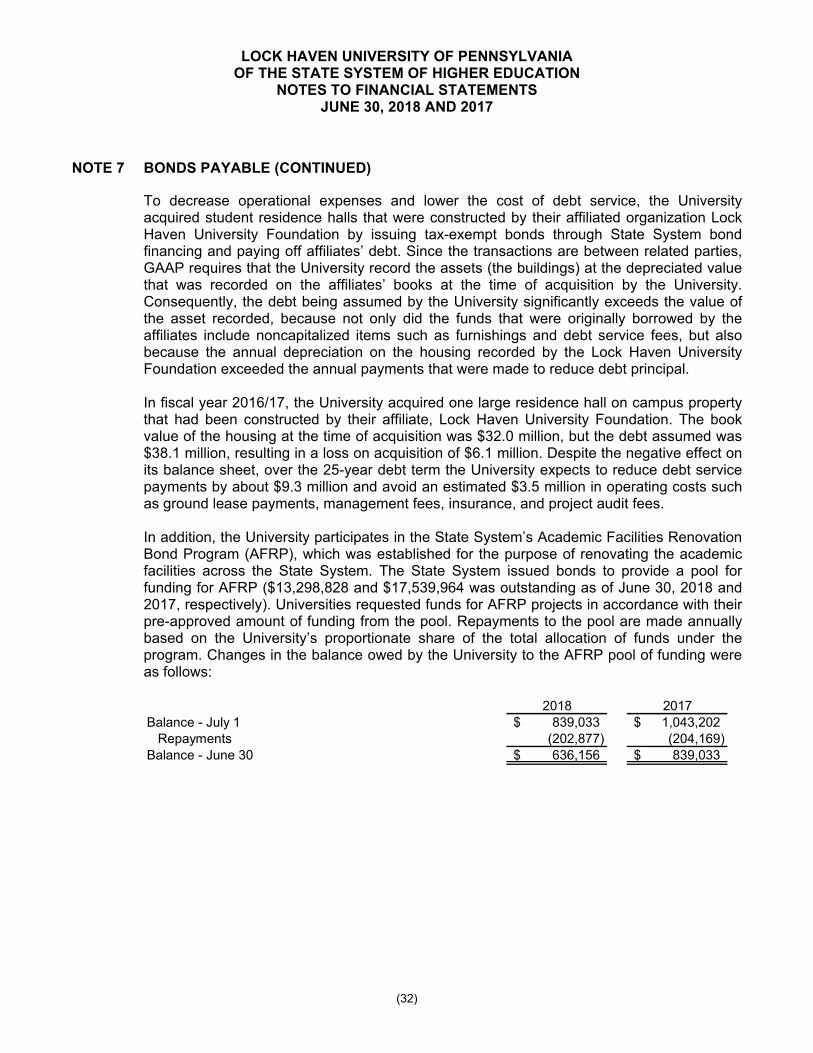

During FY2016/17 the University acquired the Fairview Suites student housing facility from the Foundation under an agreement that included the refunding of the Foundation’s debt related to the facility. Since the carrying value of the capital and other assets acquired by the University was less than the amount of the Foundation’s debt paid off, the Foundation recognized a gain on the transaction. See Note 7 for additional information.

NOTE 5 CAPITAL LEASES

The University has entered into capital lease agreements for the financing of a mail machine and several copiers. Future minimum payments by year and in the aggregate, with initial or remaining terms of one year or more are as follows:

Year Ending June 30, Amount2019 19,054$ 2020 17,897 2021 15,754 2022 9,098 2023 6,066

Total Minimum Lease Payments 67,869 Less: Amount Representing Interest on Capital Leases 9,239 Present Value of Net Minimum Capital Lease Payment 58,630$

Capital assets, net includes $53,456 and $35,335 of equipment acquired through leases that are capitalized at June 30, 2018 and 2017, respectively.

LOCK HAVEN UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2018 AND 2017

(30)

NOTE 6 ACCOUNTS PAYABLE AND ACCRUED EXPENSES