Embed Size (px)

Citation preview

Client briefing Key aspects for insurers of the new UK regulatory regime

The pendulum continues to swing yet further in the direction of creating all-powerful regulators. Supervisors have been given larger and sharper sticks with which to threaten firms and their senior management who may take a different view on the appropriate way to conduct their businesses.

IntroductionIt was almost three years ago that the Chancellor, George Osborne, announced in his Mansion House speech that the Financial Services Authority would be abolished to pave the way for “fundamental reform” of the regulatory system - with supervision duties split between the Prudential Regulation Authority and the Financial Conduct Authority, and a new Financial Policy Committee of the Bank of England taking responsibility for macro-prudential issues.

Yet the implementation of the new structure and framework of powers of the two regulators has been undertaken within a precariously tight timeframe – a mere 66 working days passed from the legislation receiving Royal Assent, to full introduction of the new regime on 1 April 2013.

That period witnessed an avalanche of policy papers and draft rules. Some of the new powers are unprecedented in nature and striking in the breadth of discretion conferred on the PRA and FCA. Yet due to the volume of material published, they have in many cases received little public scrutiny. Keeping track of the raft of proposals, and ensuring the insurance industry’s voice is heard throughout the consultation process, has been a demanding exercise.

Our aim in preparing this document is to ensure the industry is aware of the most important changes and to share perspectives from members of the team on their real impact. If you would find it helpful to discuss the implications in more detail then please do get in touch.

Nathan Willmott Partner [email protected]

Some of the new powers are unprecedented in nature and striking in the breadth of discretion conferred.Nathan Willmott

Berwin Leighton Paisner LLP

Client briefing /01

The new UK regulatory architecture

What is happening?

02/ Client briefing

What is happening?

Client briefing /03

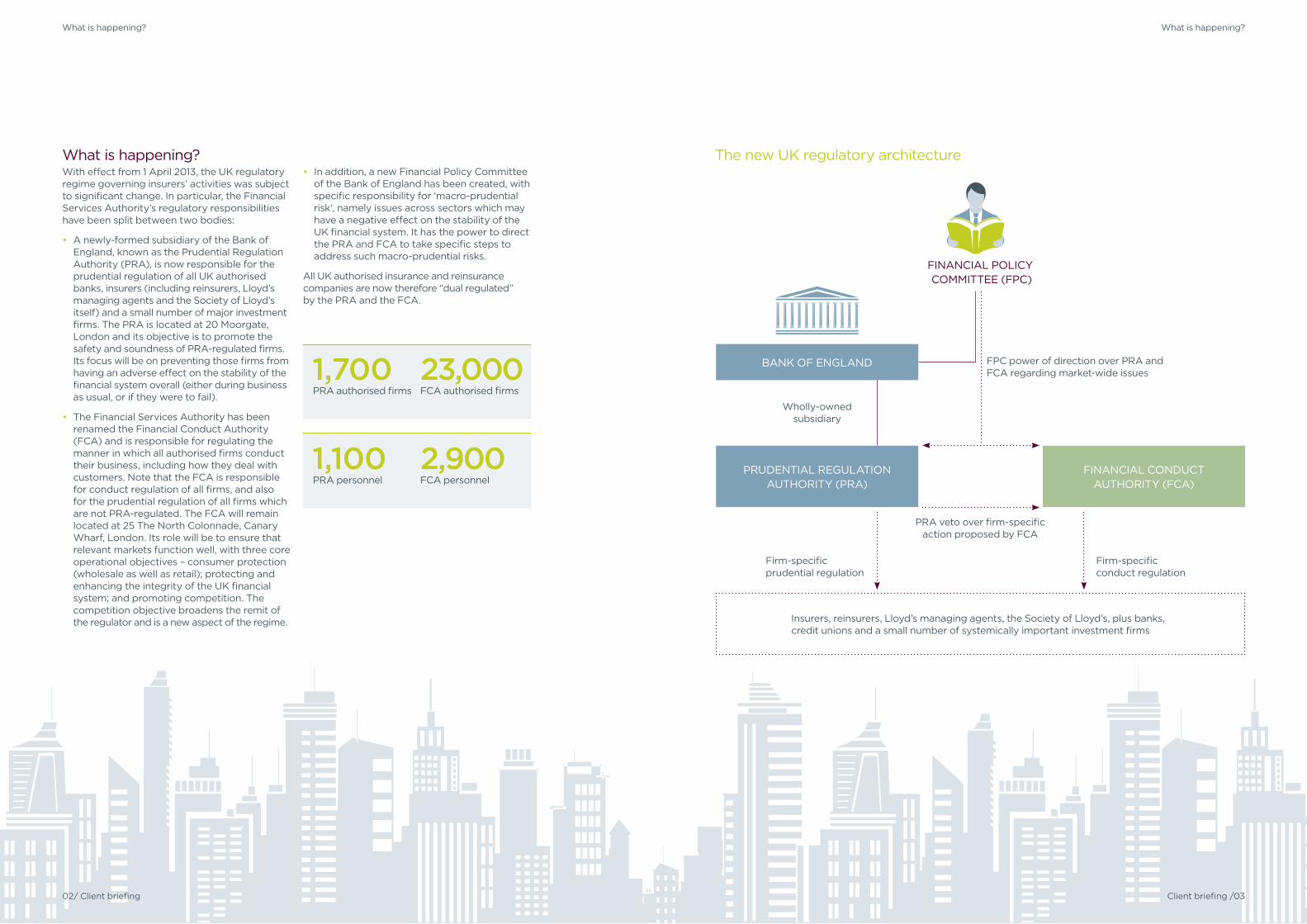

What is happening?With effect from 1 April 2013, the UK regulatory regime governing insurers’ activities was subject to significant change. In particular, the Financial Services Authority’s regulatory responsibilities have been split between two bodies:

• A newly-formed subsidiary of the Bank of England, known as the Prudential Regulation Authority (PRA), is now responsible for the prudential regulation of all UK authorised banks, insurers (including reinsurers, Lloyd’s managing agents and the Society of Lloyd’s itself) and a small number of major investment firms. The PRA is located at 20 Moorgate, London and its objective is to promote the safety and soundness of PRA-regulated firms. Its focus will be on preventing those firms from having an adverse effect on the stability of the financial system overall (either during business as usual, or if they were to fail).

• The Financial Services Authority has been renamed the Financial Conduct Authority (FCA) and is responsible for regulating the manner in which all authorised firms conduct their business, including how they deal with customers. Note that the FCA is responsible for conduct regulation of all firms, and also for the prudential regulation of all firms which are not PRA-regulated. The FCA will remain located at 25 The North Colonnade, Canary Wharf, London. Its role will be to ensure that relevant markets function well, with three core operational objectives – consumer protection (wholesale as well as retail); protecting and enhancing the integrity of the UK financial system; and promoting competition. The competition objective broadens the remit of the regulator and is a new aspect of the regime.

• In addition, a new Financial Policy Committee of the Bank of England has been created, with specific responsibility for ‘macro-prudential risk’, namely issues across sectors which may have a negative effect on the stability of the UK financial system. It has the power to direct the PRA and FCA to take specific steps to address such macro-prudential risks.

All UK authorised insurance and reinsurance companies are now therefore “dual regulated” by the PRA and the FCA.

FINANCIAL POLICY COMMITTEE (FPC)

FPC power of direction over PRA and FCA regarding market-wide issues

Firm-specific conduct regulation

FINANCIAL CONDUCT AUTHORITY (FCA)

PRA veto over firm-specific action proposed by FCA

Firm-specific prudential regulation

Insurers, reinsurers, Lloyd’s managing agents, the Society of Lloyd’s, plus banks, credit unions and a small number of systemically important investment firms

1,700 PRA authorised firms

23,000 FCA authorised firms

1,100 PRA personnel

2,900 FCA personnel

Wholly-owned subsidiary

BANK OF ENGLAND

PRUDENTIAL REGULATION AUTHORITY (PRA)

Client briefing /0504/ Client briefing

Key changes to the regulators’ legal powers Key changes to the regulators’ legal powers

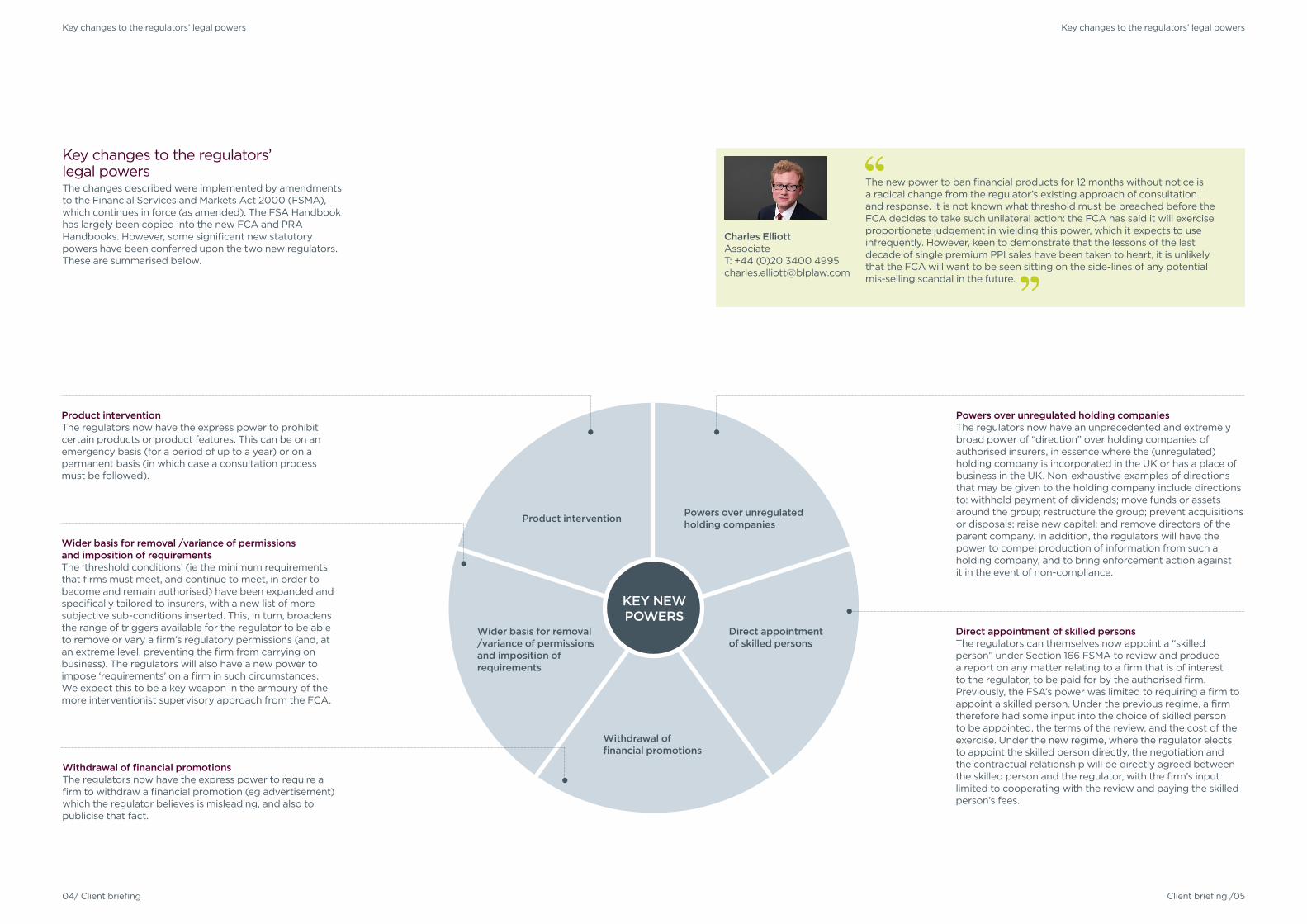

Key changes to the regulators’ legal powersThe changes described were implemented by amendments to the Financial Services and Markets Act 2000 (FSMA), which continues in force (as amended). The FSA Handbook has largely been copied into the new FCA and PRA Handbooks. However, some significant new statutory powers have been conferred upon the two new regulators. These are summarised below.

Wider basis for removal /variance of permissions and imposition of requirementsThe ‘threshold conditions’ (ie the minimum requirements that firms must meet, and continue to meet, in order to become and remain authorised) have been expanded and specifically tailored to insurers, with a new list of more subjective sub-conditions inserted. This, in turn, broadens the range of triggers available for the regulator to be able to remove or vary a firm’s regulatory permissions (and, at an extreme level, preventing the firm from carrying on business). The regulators will also have a new power to impose ‘requirements’ on a firm in such circumstances. We expect this to be a key weapon in the armoury of the more interventionist supervisory approach from the FCA.

Withdrawal of financial promotionsThe regulators now have the express power to require a firm to withdraw a financial promotion (eg advertisement) which the regulator believes is misleading, and also to publicise that fact.

Product interventionThe regulators now have the express power to prohibit certain products or product features. This can be on an emergency basis (for a period of up to a year) or on a permanent basis (in which case a consultation process must be followed).

Direct appointment of skilled personsThe regulators can themselves now appoint a “skilled person” under Section 166 FSMA to review and produce a report on any matter relating to a firm that is of interest to the regulator, to be paid for by the authorised firm. Previously, the FSA’s power was limited to requiring a firm to appoint a skilled person. Under the previous regime, a firm therefore had some input into the choice of skilled person to be appointed, the terms of the review, and the cost of the exercise. Under the new regime, where the regulator elects to appoint the skilled person directly, the negotiation and the contractual relationship will be directly agreed between the skilled person and the regulator, with the firm’s input limited to cooperating with the review and paying the skilled person’s fees.

Powers over unregulated holding companiesThe regulators now have an unprecedented and extremely broad power of “direction” over holding companies of authorised insurers, in essence where the (unregulated) holding company is incorporated in the UK or has a place of business in the UK. Non-exhaustive examples of directions that may be given to the holding company include directions to: withhold payment of dividends; move funds or assets around the group; restructure the group; prevent acquisitions or disposals; raise new capital; and remove directors of the parent company. In addition, the regulators will have the power to compel production of information from such a holding company, and to bring enforcement action against it in the event of non-compliance.

Product intervention

Withdrawal of financial promotions

Wider basis for removal /variance of permissions and imposition of requirements

Direct appointment of skilled persons

Powers over unregulated holding companies

KEY NEW POWERS

The new power to ban financial products for 12 months without notice is a radical change from the regulator’s existing approach of consultation and response. It is not known what threshold must be breached before the FCA decides to take such unilateral action: the FCA has said it will exercise proportionate judgement in wielding this power, which it expects to use infrequently. However, keen to demonstrate that the lessons of the last decade of single premium PPI sales have been taken to heart, it is unlikely that the FCA will want to be seen sitting on the side-lines of any potential mis-selling scandal in the future.

Charles Elliott Associate T: +44 (0)20 3400 4995 [email protected]

Key changes in the approach of the regulatorsBoth new regulators have promised to adopt a risk-based and judgement-based approach to regulation, focussing their attention where the real risks lie. They will seek to develop a close understanding of the business models of the most significant firms, with a view to being able to take a more interventionist approach than that of the FSA. What this will mean for individual firms in practice will depend greatly upon how far up the risk ‘scale’ the firm is assessed to be.

During the first three months of the new regime, the PRA and FCA intend to assess and categorise all UK insurers, based on the level of risk posed to their statutory objectives - from level 1 (highest risk) to level 5 (lowest risk) for the PRA and from level 1 (highest risk) and level 4 (lowest risk) for the FCA. The level of attention and resource that the PRA and FCA devote to each firm will then be decided by reference to the risk category that it has been allocated.

The PRA has stated that it intends for its relationship with the firms it supervises to be conducted at a more senior level of staff, with a more trusting approach on both sides, and focused on understanding how the firm makes its profits and where its risks lie.

In the PRA’s April 2013 paper describing its approach to insurance supervision, the PRA said:

“Insurers should be open and straightforward in their dealings with the PRA, taking the initiative to raise issues of possible prudential concern… at an early stage. The PRA, for its part, will respond proportionately. Trust can thus be fostered on both sides.”

Client briefing /0706/ Client briefing

Key changes to regulatory processes Key changes in the approach of the regulators

Key changes to regulatory processesBoth the PRA and FCA have their own Enforcement divisions to investigate and take disciplinary action in the case of breaches by authorised firms or their approved persons. However, in practice, the vast majority of Enforcement action is likely to be taken by the FCA rather than the PRA.

The internal decision-making body for PRA disciplinary cases will not be independent of the PRA executive. There are different levels of PRA committee that will determine such disciplinary cases, dependent on the (i) risk category of the relevant firm; and (ii) the nature of the breach. In contrast, the FCA will retain a semi-independent, dedicated “Regulatory Decisions Committee” to determine disciplinary cases on behalf of the FCA. In both cases, the defendant will retain the right to refer a disciplinary case to the Upper Tribunal for an independent hearing.

The PRA and FCA have been given a new power to publish details relating to disciplinary cases where a “Warning Notice” has been issued (ie at the stage before representations can be made by the defendant to the relevant decision-making committee). The regulators have indicated that they will ordinarily proceed to publish details in summary form, without details of the level of penalty that the regulator wishes to impose.

£31.2m total cost to firms of s166 reviews 2011/12

We can expect the FCA to maintain its focus on financial crime, using its powers to identify and prosecute wrongdoers, but also to hold firms to high standards in terms of their regulatory compliance programmes and controls. For insurers, I expect anti-bribery and corruption and financial sanctions to get the most attention. I also expect the FCA to give serious consideration to the introduction of whistleblower incentive programmes similar to those introduced in the US via the Dodd-Frank Act. In such circumstances, any firm that fails to treat employee whistleblowing reports appropriately will risk employees taking their concerns directly to the regulator.Aaron Stephens Partner T: +44 (0)20 3400 4163 [email protected]

The FCA’s increased focus on product governance is, for me, a positive development for both firms and customers. Firms need to ensure that they have robust systems and controls in place for the design, operation and sale of products, to show that customers’ interests are considered at each stage in the product life-cycle. I believe that this should reduce the risk of customer detriment and as a consequence, mis-selling claims against firms.Victoria Brocklehurst Knowledge Development Lawyer T: +44 (0)20 3400 4503 [email protected]

One of the most radical aspects of the new regime is the extension of regulatory powers to certain unregulated UK holding companies (such as PLCs and intermediate UK holding companies) of authorised firms. These powers are unprecedented and will bring a significant number of firms within the jurisdiction of the new regulators for the first time.Adam Bogdanor Partner T: +44 (0)20 3400 4808 [email protected]

I am keeping a close eye on the range of risk-ratings that the PRA is applying to insurers. The PRA has said that it is recruiting heavily from industry in order to build the right skill-set to carry out prudential regulation for insurers – but it may be that the PRA takes a cautious approach towards risk assessment in the early days, leaving some insurers with a heavier regulatory burden than they really need.Jacob Ghanty Partner T: +44 (0)20 3400 4088 [email protected]

Client briefing /0908/ Client briefing

Key changes in the approach of the regulators

For the FCA’s part, all the early indications are that it will be the more aggressive regulator, and that it intends to use its broad new powers (of both a supervisory and enforcement nature) to take strong action against firms who have either breached its rules, or who are not perceived as being sufficiently cooperative in their dealings with the FCA. We expect that a core focus of the FCA will be ‘product governance’, particularly (but not exclusively) in retail markets. The FCA is concerned to ensure that firms have proper governance processes in place to ensure that new products are designed with the interests of the end-user in mind, and that customers’ interests are considered at each stage in the product life-cycle.

Another key theme of the new regime is transparency, which the FCA regards as a key regulatory “tool”. The FSA felt that its 2010 decision to publish the numbers of customer complaints referred to the FOS on a firm by firm basis had a significant impact both upon firms’ behaviour towards their retail customers, and upon customers’ awareness of the choices available to them. Particularly in light of the FCA’s new statutory objective to promote effective competition in financial services markets in the interests of consumers, we expect to see the FCA requiring firms to release increasing amounts of data for publication and use by consumer organisations.

Consultations are already underway on mandating the publication by insurers of claims data, including numbers of claims per customer; successful claims percentage following an initial contact; premiums vs. payout ratios; and numbers of claims reduced or refused for non-disclosure. In addition, the thematic review of general insurance products sold as “add-ons” to other goods or services (begun by the FSA before legal cutover) has signalled the conduct regulator’s determination to compel disclosure by firms of much broader information about the design and performance of their products, in line with its wider competition objectives.

We expect to see this drive towards transparency gaining momentum over the months and years ahead. The challenge for the FCA will be in identifying the point at which information transparency escalates into information overload and, instead of helping consumers to make informed decisions, becomes overwhelming. In the meantime, firms will face ever increasing demands for the production of data and will need to ensure they have developed systems that can keep pace with those demands.

What happens next?Insurers and reinsurers will be receiving their risk categorisations from the PRA and FCA early in the life of the new regime. This information will allow firms to build a fairly realistic picture of the level of regulatory scrutiny to expect. In addition, the new regulators will be keen to emphasise their key areas of focus and concern – analysing the firm’s activities against the regulators’ core priorities can often serve as a further barometer of regulatory risk.

In the meantime, insurers and reinsurers will already be beginning the somewhat daunting task of working with their new PRA and FCA supervisory teams in order to educate them about their businesses and the risks they face, with a view to establishing a strong working relationship of trust and confidence.

What happens next?

total FSA fines in 2012

£646.3m combined PRA and FCA annual funding requirement for 2013/14

15% increase in annual funding requirement under the ‘twin peaks’ regime

This rather wild enthusiasm for transparency and information disclosure concerns me: there are so many ways in which information can be presented (and misrepresented) that there must be a danger of the financial markets becoming so saturated with misinformation that consumers lose interest altogether, which is the opposite of what the FCA is hoping to achieve. Also, wherever there are onerous data requests, you have resource being taken from elsewhere in the business – minds that could be usefully occupied in making judgements, rather than crunching numbers.

Polly James Consultant T: +44 (0)20 3400 3158 [email protected]

The regulators’ controversial new powers to publish warning notices clearly have the potential to cause significant reputational problems for firms and their senior management. The powers allow the PRA and FCA to publish details of disciplinary cases at a stage when the firm under investigation has not yet had a chance to say anything in its defence. In my view, there is a risk of ‘trial by press’ in high profile cases, and the public is unlikely to realise that there has not yet been any formal finding of wrongdoing by the firm. Adam Jamieson Associate T: +44 (0)20 3400 3251 [email protected]

I am expecting to see a far more interventionist approach by both of the new regulators. Some firms are likely to experience a very different style of supervision, with less negotiation where the regulator identifies what it regards as a serious issue which threatens one or more of its statutory objectives. Firms can expect to see the regulators acting earlier and more decisively, using their new power to impose ‘requirements’ on firms to get them to do what the regulators want. This, in turn, is likely to lead to more legal challenges.Sidney Myers Partner T: +44 (0)20 3400 4847 [email protected]

Getting in touchWhen you need a practical legal solution for your next business opportunity or challenge, please get in touch.

LondonAdelaide House, London BridgeLondon EC4R 9HA England

Nathan Willmott Tel: +44 (0)20 3400 [email protected]

Clients and work in 130 countries, delivered via offices in: Abu Dhabi, Beijing, Berlin, Brussels, Dubai, Frankfurt, Hong Kong, London, Moscow, Paris and Singaporewww.blplaw.com

About BLPToday’s world demands clear, pragmatic legal advice that is grounded in commercial objectives. Our clients benefit not just from our excellence in technical quality, but also from our close understanding of the business realities and imperatives that they face.

Our achievements for clients are made possible by brilliant people. Prized for their legal talent and commercial focus, BLP lawyers are renowned for being personally committed to clients’ success. Our approach has seen us win five Law Firm of the Year awards and three FT Innovative Lawyer awards.

With experience in over 70 legal disciplines and 130 countries, you will get the expertise, business insight and value-added thinking you need, wherever you need it.

Expertise•Commercial•Competition, EU and Trade•Construction•Corporate Finance•Dispute Resolution•Employment, Pensions and Incentives•Finance•Funds and Financial Services•Intellectual Property•Private Client•Projects•Real Estate•Regulatory and Compliance•Restructuring and Insolvency•Tax

This document provides a general summary only and does not constitute legal advice. Specific legal advice should always be sought in relation to the particular facts of a given situation.