Embed Size (px)

Citation preview

Click to edit Master title style

28/01/2014 1

CLEAR PRACTICAL EFFECTIVE

Investment Lunch

January 2014

2

CLEAR PRACTICAL EFFECTIVE

AGENDA

Nick Frank

Eric Clapton

Richard Miller

Ellie Clapton

• Introduction

• Proposition Update

• Macro Economic View

• Fund Selection and Analysis

January 2014

• Fund Selection and

Analysis

3

CLEAR PRACTICAL EFFECTIVE

Nick Frank Business

Development

January 2014

4

CLEAR PRACTICAL EFFECTIVE

Conservative Model 3 Year

Risk Return Graph Total Return Bid-Bid performance vs volatility scatter chart over 36 months (from 31 Dec 2010 to 31 Dec 2013) from UK IMA universe. Rebased in Pounds Sterling

5

CLEAR PRACTICAL EFFECTIVE

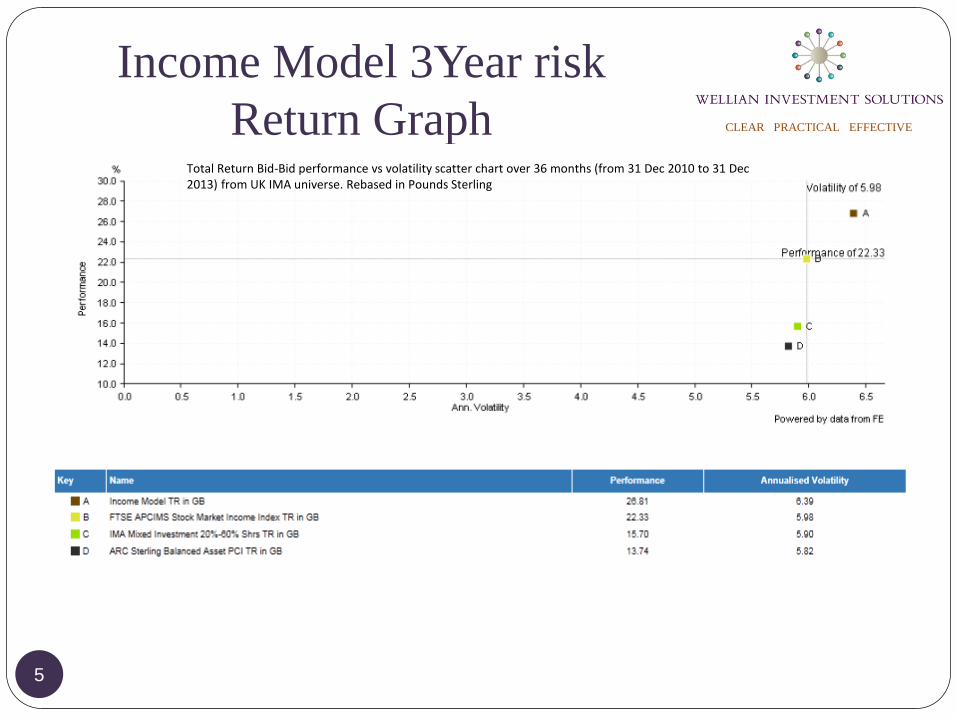

Income Model 3Year risk

Return Graph Total Return Bid-Bid performance vs volatility scatter chart over 36 months (from 31 Dec 2010 to 31 Dec 2013) from UK IMA universe. Rebased in Pounds Sterling

6

CLEAR PRACTICAL EFFECTIVE

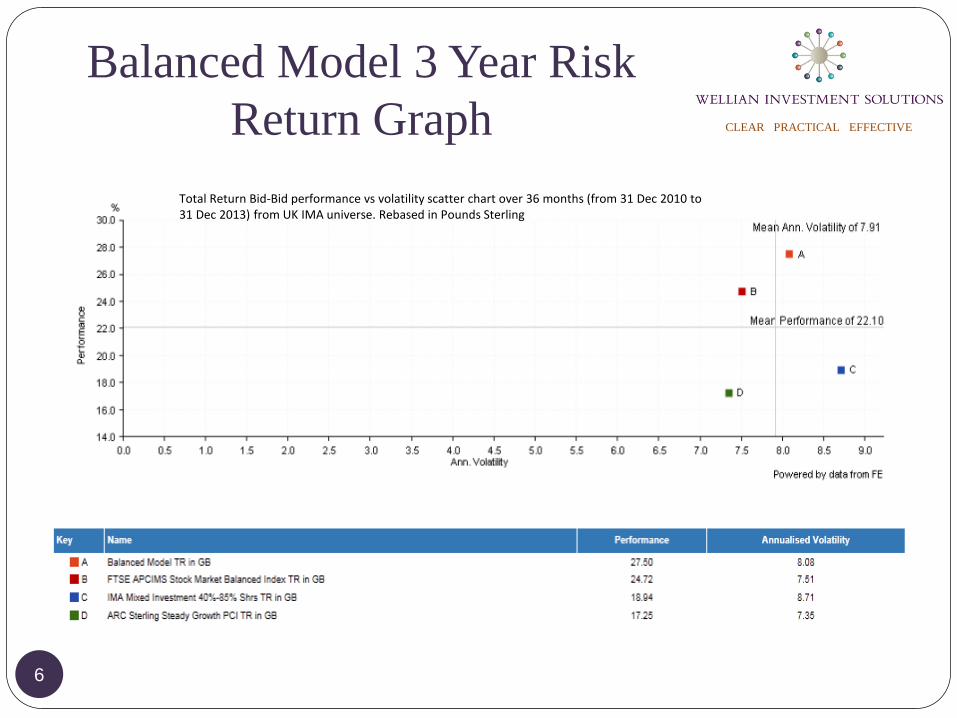

Balanced Model 3 Year Risk

Return Graph

Total Return Bid-Bid performance vs volatility scatter chart over 36 months (from 31 Dec 2010 to 31 Dec 2013) from UK IMA universe. Rebased in Pounds Sterling

7

CLEAR PRACTICAL EFFECTIVE

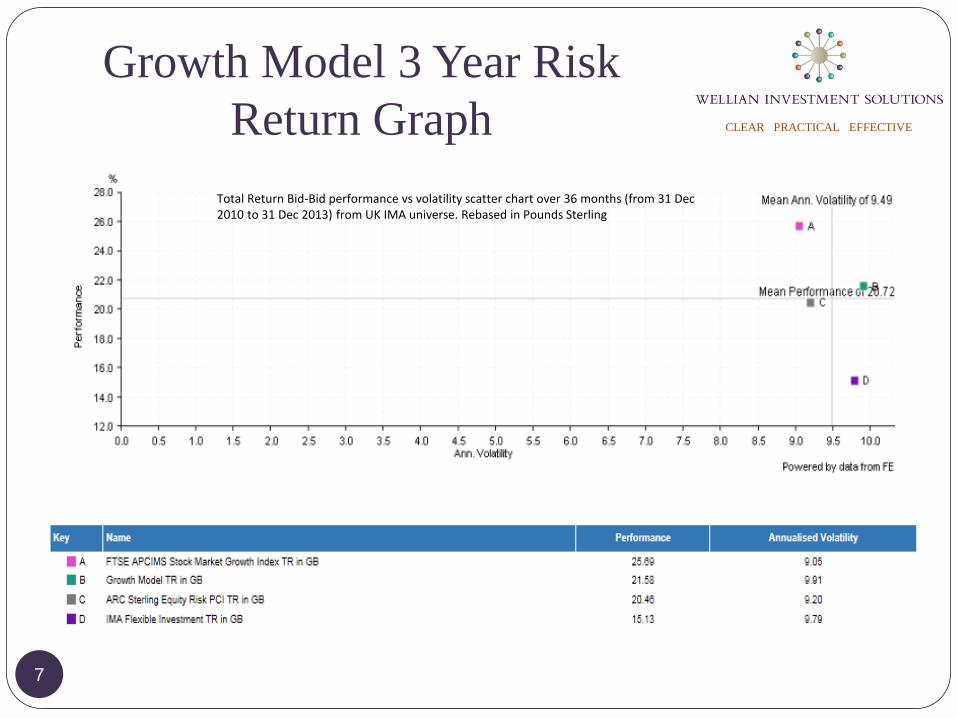

Growth Model 3 Year Risk

Return Graph

Total Return Bid-Bid performance vs volatility scatter chart over 36 months (from 31 Dec 2010 to 31 Dec 2013) from UK IMA universe. Rebased in Pounds Sterling

8

CLEAR PRACTICAL EFFECTIVE

Eric Clapton MD

January 2014

9

CLEAR PRACTICAL EFFECTIVE

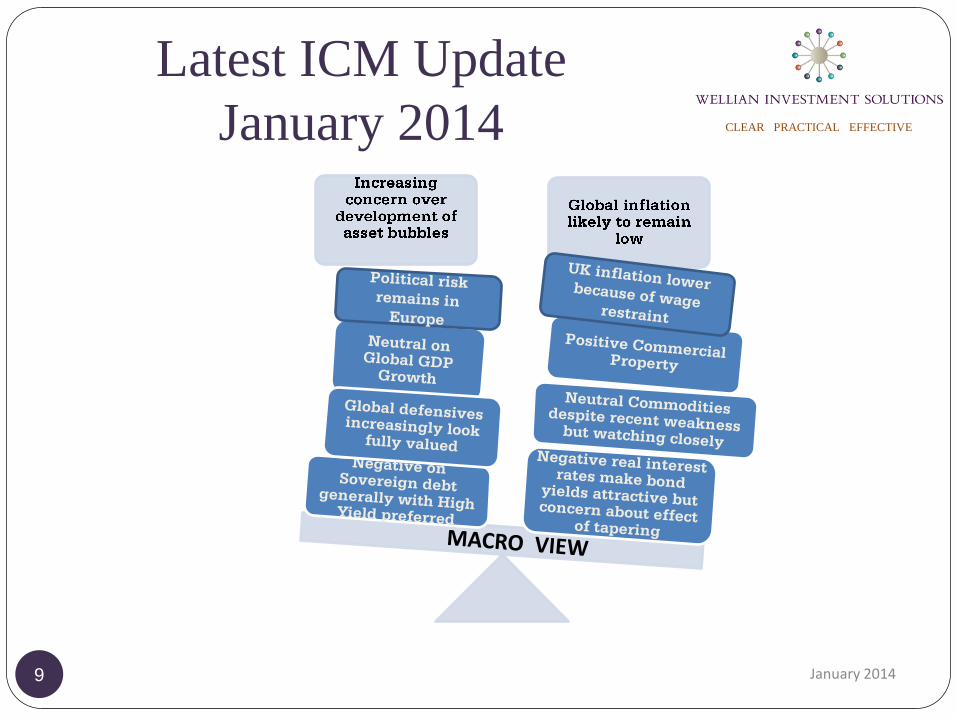

Latest ICM Update

January 2014

January 2014

10

CLEAR PRACTICAL EFFECTIVE

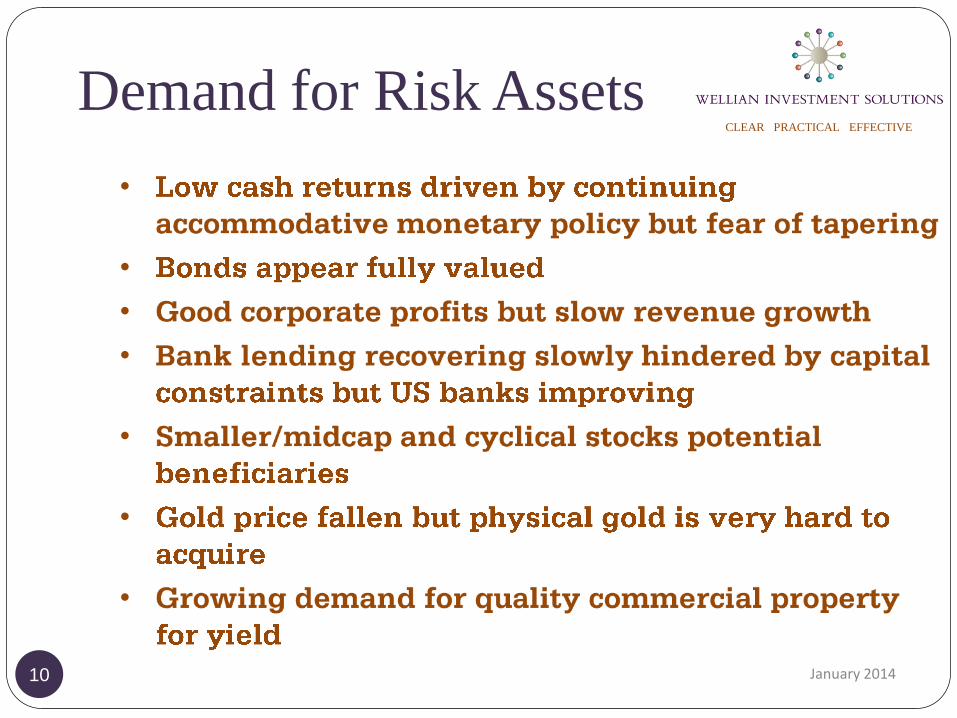

Demand for Risk Assets

•

•

•

•

•

•

•

January 2014

11

CLEAR PRACTICAL EFFECTIVE

By Region (UK)

• Real wage falls helping job creation and unemployment

falls to 7.4%

• Increasing possibility of fine tune tightening of

monetary policy

• Government maintaining austerity strategy to reduce

public sector to 17% of economy by 2018

• UK economy median forecast growth at 2.4% for 2013

and 2.2% 2014

• UK inflation falls to target level 2.0% from 2.2%

January 2014

12

CLEAR PRACTICAL EFFECTIVE

By Region (UK) continued

• Increasing political uncertainties as the coalition parties

position for the next election

• Increasing concern regarding outcome of Scottish

devolution vote

• Debt/GDP percentage rising to 79.2% end 2013/2014 from

76.6% end 2012/2013, peaking at 85.6% in 2016/17

• Balanced budget forecast by 2018

January 2014

13

CLEAR PRACTICAL EFFECTIVE

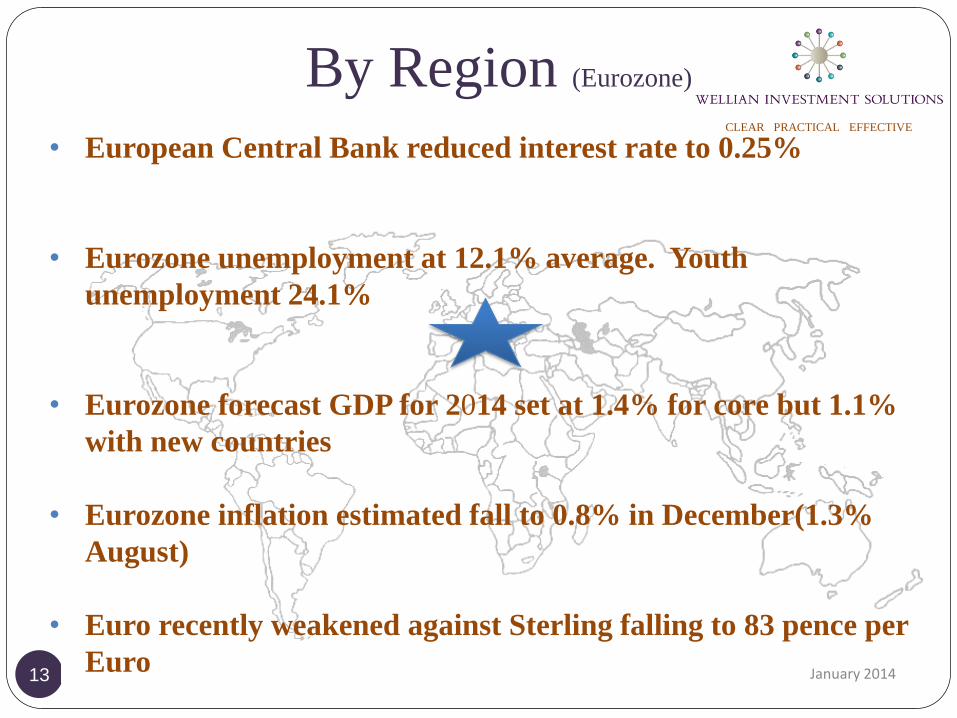

By Region (Eurozone)

• European Central Bank reduced interest rate to 0.25%

• Eurozone unemployment at 12.1% average. Youth

unemployment 24.1%

• Eurozone forecast GDP for 2014 set at 1.4% for core but 1.1%

with new countries

• Eurozone inflation estimated fall to 0.8% in December(1.3%

August)

• Euro recently weakened against Sterling falling to 83 pence per

Euro January 2014

14

CLEAR PRACTICAL EFFECTIVE

By Region (US)

• US growth revised up to 4.1% in Q3 from 2.5% in Q2

• Accommodative monetary policy still in place for now but

more tapering increasingly likely

• Unemployment rate 6.7% from 7.0% in November but

participation rate fallen to below 63%

• Cheap energy drives industrial repatriation. Increasing

reserves of shale oil and gas January 2014

15

CLEAR PRACTICAL EFFECTIVE

By Region (US) continued

• Savings rate reduced from 5.3% Q4 2012 to 2.3%

Q1 2013 but revised up to 5.0% in Q3

• Budget surplus of $53 billion in December

• Fall in deficit from $1.6 trillion to $1.2 trillion

since Q1 2011 – now fallen to $1.0 trillion Q2

2013 and $0.7 trillion initial for 2013

January 2014

By Region (China)

• Record trade surplus of $260 billion in 2013 ($230 billion 2012)

• But export growth slowed to 4.3% from 12.7% in November

• Chinese growth slowed to 7.8% for 2013 as budgeted

• Fear of bubbles in some markets after experience of 2008

• China to promote equality and reduce conspicuous

consumption(corruption); however, retail sales are still growing at

13.7% per annum which is above average run rate of 13.3%

January 2014 16

By Region (China) Continued

• Government allowing free market to increasingly allocate

resources

• Continue to purchase foreign strategic assets as evidenced in

Docklands and inclusion in UK NuGen Joint Venture

• London & Singapore approved as issuer of Qualifying Foreign

Investment

• Rules issued for market trading of certificates of deposit

January 2014 17

By Region (Japan)

• Government policy to weaken yen supported globally. Yen

weakened 34% cumulatively against US dollar since Oct

2012 (32% November 2013)

• Japanese GDP forecast at 3.8% for 2013 from initial estimate

of 2.6% but falling to 1.4% in 2014

• Japanese macro data still poor with aging workforce and

significant government borrowing

• Evidence that Japanese banks adequately

capitalised and able to lend to recovery

• Topix still ahead by 80% since October 2012 in local

currency terms (78% in November 2013) January 2014 18

Emerging Markets

• Better corporate governance

• PMI data flat but improving in Russia and Brazil

• Growth of middle class

• Countries are discovering increasing natural resources but

falling commodity prices have slowed economies

January 2014 19

Emerging Markets continued

• Brazil’s forecast growth decreased by 0.5% in Q3 with

forecast @ 1%

• Russian GDP equals 1.2% in Q3 and likely to miss 2014

forecast of 1.8%

• Indian growth forecast for 2013 reduced to 4.8% from

4.9% previously

January 2014 20

21

CLEAR PRACTICAL EFFECTIVE

Emerging Emerging

Markets!

January 2014

Mexico

Indonesia

Nigeria

Turkey

22

CLEAR PRACTICAL EFFECTIVE

Mexico

Annual growth forecast 1.8% in 2013

International Reserves $170 billion

Population 125 million

Labour Force 52 million

23

CLEAR PRACTICAL EFFECTIVE

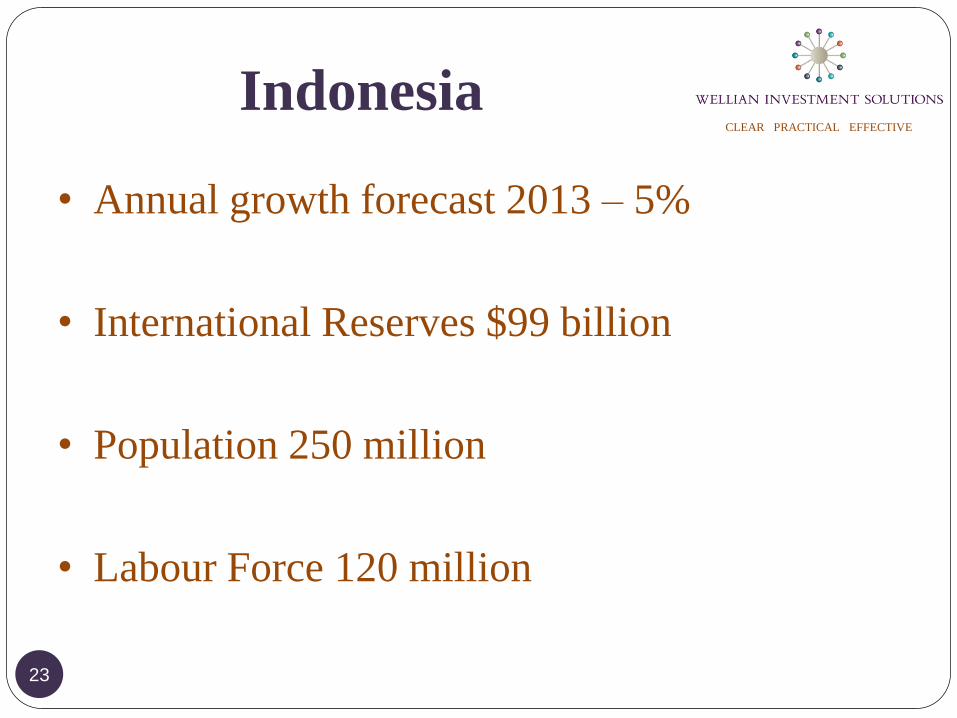

Indonesia

• Annual growth forecast 2013 – 5%

• International Reserves $99 billion

• Population 250 million

• Labour Force 120 million

24

CLEAR PRACTICAL EFFECTIVE

Nigeria

• Annual growth forecast 2013 – 6.5%

• International Reserves $48 billion

• Population 170 million

• Labour Force 54 million

25

CLEAR PRACTICAL EFFECTIVE

Turkey

• Annual growth forecast – 1%

• International reserves 120 billion

• Population 76 million

• Labour force 27 million

26

CLEAR PRACTICAL EFFECTIVE

Asset Allocation

January 2014

27

CLEAR PRACTICAL EFFECTIVE Richard Miller &

Ellie Clapton

January 2014

28

CLEAR PRACTICAL EFFECTIVE

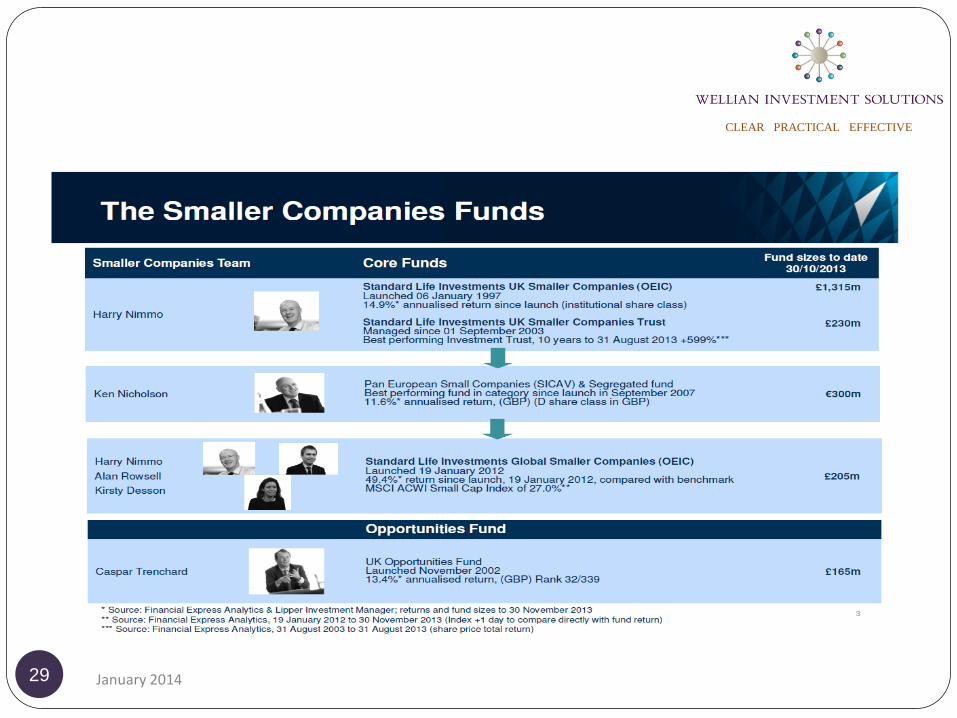

Standard Life Investments UK

Smaller Companies Fund

Investment

Philosophy

“Aiming to achieve capital growth over the longer term.’’

January 2014

29

CLEAR PRACTICAL EFFECTIVE

January 2014

30

CLEAR PRACTICAL EFFECTIVE

31

CLEAR PRACTICAL EFFECTIVE

32

CLEAR PRACTICAL EFFECTIVE

33

CLEAR PRACTICAL EFFECTIVE

34

CLEAR PRACTICAL EFFECTIVE

Total Return Bid-Bid line chart over 10 years (from 14 Jan 2004 to

14 Jan 2014) from UK IMA universe. Rebased in Pounds Sterling

35

CLEAR PRACTICAL EFFECTIVE

Total Return Bid-Bid performance vs volatility scatter chart over 60

months (from 31 Dec 2008 to 31 Dec 2013) from UK IMA universe.

Rebased in Pounds Sterling

36

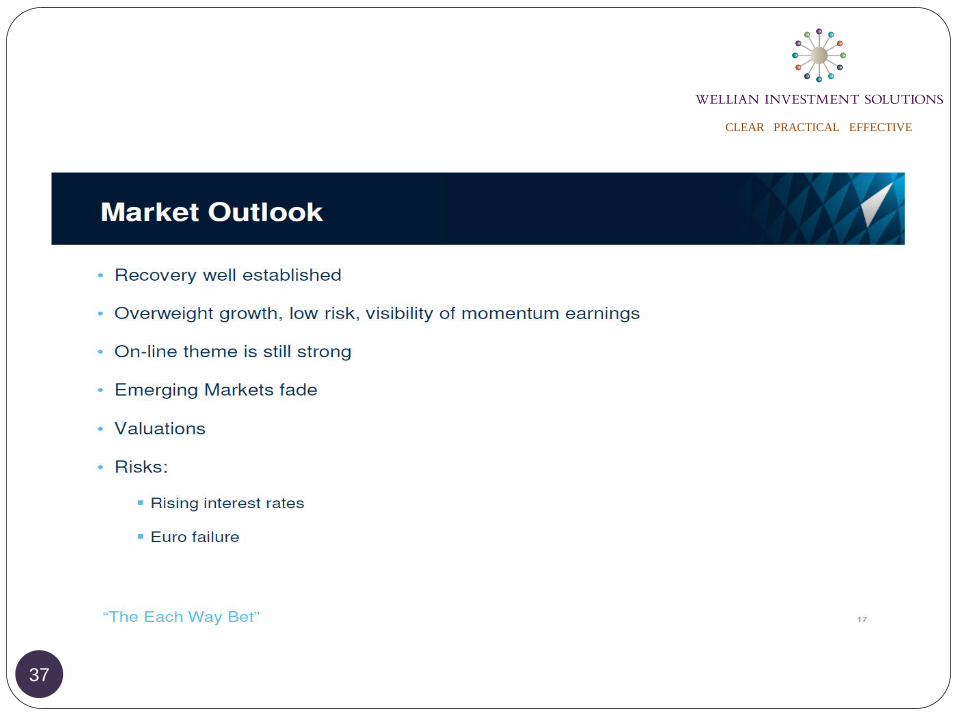

CLEAR PRACTICAL EFFECTIVE

37

CLEAR PRACTICAL EFFECTIVE

38

CLEAR PRACTICAL EFFECTIVE

Newton Asian Income

Investment

Philosophy

“The Fund aims to achieve income and capital growth over the long term by investing primarily in companies located in the Asia Pacific region.”

January 2014

39

CLEAR PRACTICAL EFFECTIVE

Investment Process

Screening

Valuation based

research

Quality ranking model

Portfolio construction

Risk management

40

CLEAR PRACTICAL EFFECTIVE

Yield Discipline

• Strategy portfolios as a whole aim is to yield 35% above the

Index.

• Buy discipline: All new holdings must have a prospective

yield greater than the Index – FTSE AW Asia Pacific ex Japan.

• Sell discipline: Any holding where prospective yield falls

below a 15% discount to the Index.

41

CLEAR PRACTICAL EFFECTIVE

Our Concerns

Asian Income fund has slumped to the bottom of performance

tables

What is this underperformance being attributed to?

42

CLEAR PRACTICAL EFFECTIVE

Peer Group Analysis over 1yr

43

CLEAR PRACTICAL EFFECTIVE

Peer Group Analysis over 3yrs

44

CLEAR PRACTICAL EFFECTIVE

Peer Group Analysis over 5yrs

45

CLEAR PRACTICAL EFFECTIVE

What effect has this had on the

portfolio? (risk/reward graph 6 months)

46

CLEAR PRACTICAL EFFECTIVE

What effect has this had on the

portfolio? (risk/reward graph 5yrs)

47

CLEAR PRACTICAL EFFECTIVE

Performance – since inception

(30/11/2005 – 14/01/2014)

48

CLEAR PRACTICAL EFFECTIVE

Top 10 Holdings as at December 2013

Stock Name % Country Sector

1 Sands China 4.41% Hong Kong Travel & Leisure

2 Wesfarmers 3.43% Australia General Retailers

3 Telstra Corp. 3.37% Australia Fixed Line Telecomms

4 HSBC Holdings 3.26% UK Banks

5 Taiwan Semiconductor Manufacturing 3.10% Taiwan Technology Hardware & Equipment

6 Australia & NZ Banking Group 2.97% Australia Banks

7 Philippine Long Distance Telephone Co. 2.71% Philippines Mobile Telecomms

8 Transurban Group 2.71% Australia Industrial Transportation

9 Sydney Airport NPV Dfd 031213 (Ex-Stapled) 2.60% Australia Non-Classifed

10 Woodside Petroleum 2.49% Australia Oil & Gas Producers

49

CLEAR PRACTICAL EFFECTIVE

Fund positioning

Australia

New Zealand

Thailand

Taiwan

Philippines China Malaysia South Korea Indonesia

Hong

Kong

Singapore

UK

Property

Country Allocation

50

CLEAR PRACTICAL EFFECTIVE

The Garden Suite

77 Mount Ephraim

Tunbridge Wells

Kent

TN4 8BS

www.wellian-is.com

Wellian Investment Solutions Limited is authorised and regulated by the Financial Conduct Authority.

Slides are not intended to give personalised advice and you should contact us before taking any action based upon them. You should be aware that where

past performance is quoted it is not a guide to future performance.