Embed Size (px)

Citation preview

Clements Worldwide Fleet Data Analysis for Improving Insurance

Expense Management

May 2016

2.1 Company Background

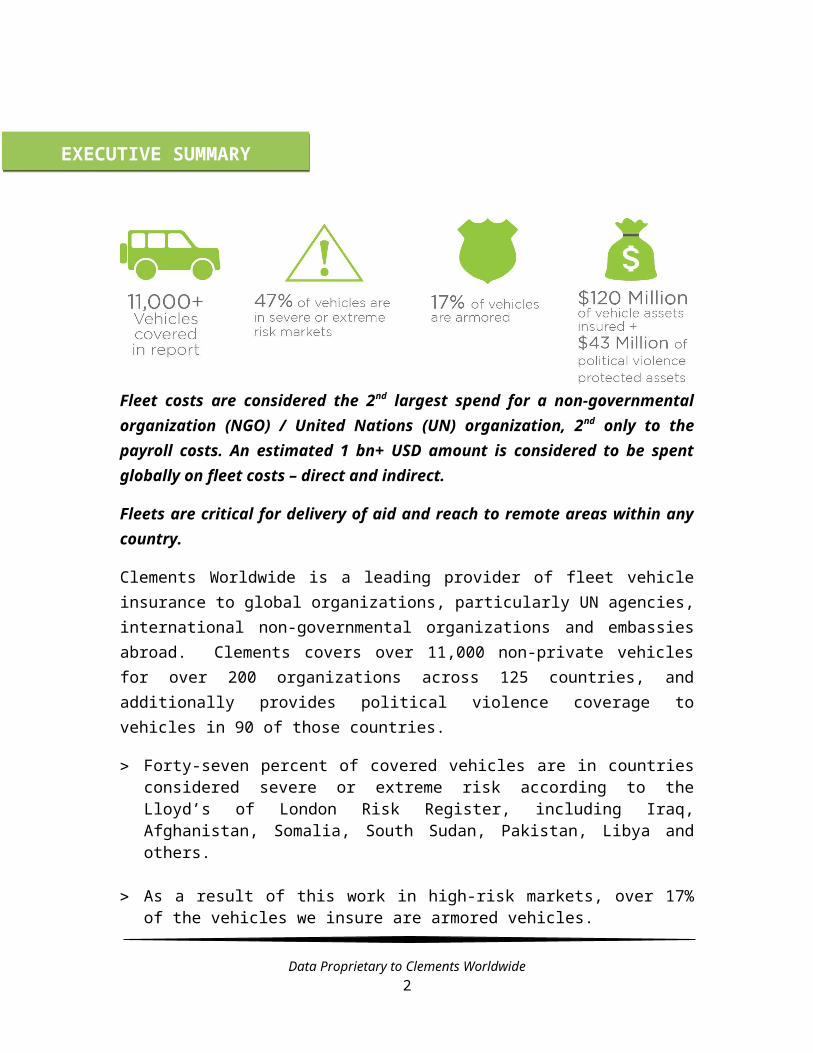

Fleet costs are considered the 2nd largest spend for a non-governmental organization (NGO) / United Nations (UN) organization, 2nd only to the payroll costs. An estimated 1 bn+ USD amount is considered to be spent globally on fleet costs – direct and indirect.

Fleets are critical for delivery of aid and reach to remote areas within any country.

Clements Worldwide is a leading provider of fleet vehicle insurance to global organizations, particularly UN agencies, international non-governmental organizations and embassies abroad. Clements covers over 11,000 non-private vehicles for over 200 organizations across 125 countries, and additionally provides political violence coverage to vehicles in 90 of those countries.

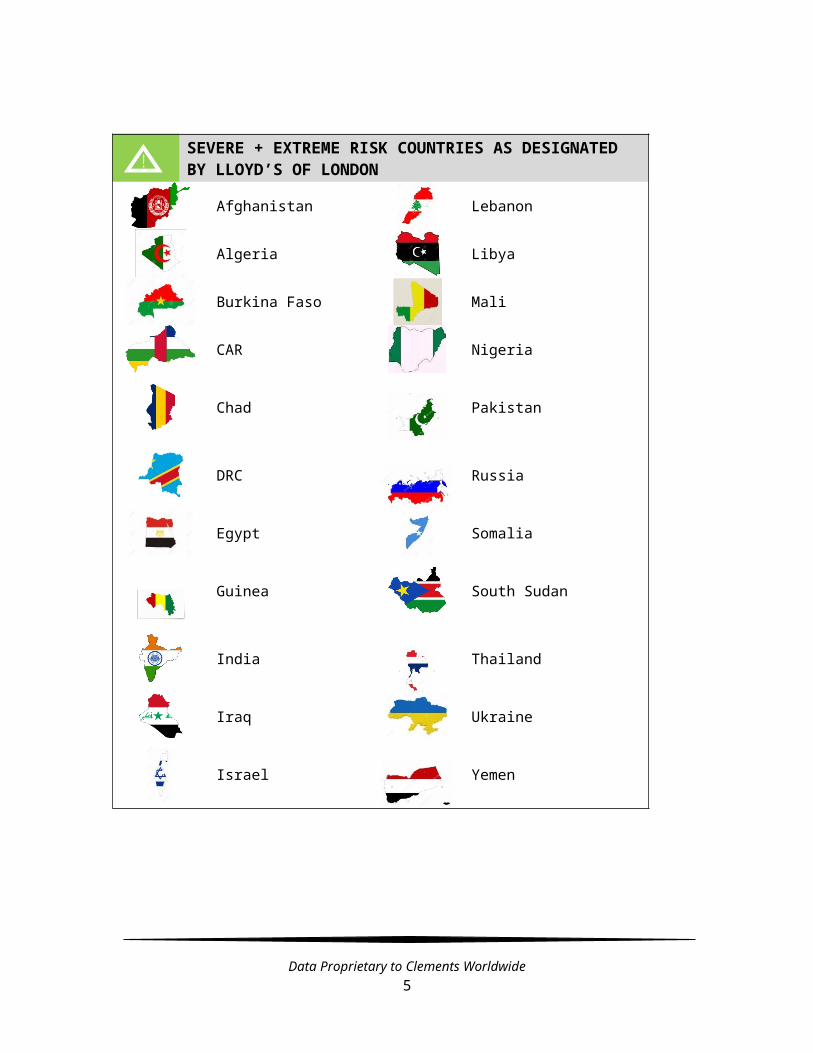

Forty-seven percent of covered vehicles are in countries considered severe or extreme risk according to the Lloyd’s of London Risk Register, including Iraq, Afghanistan, Somalia, South Sudan, Pakistan, Libya and others.

As a result of this work in high-risk markets, over 17% of the vehicles we insure are armored vehicles.

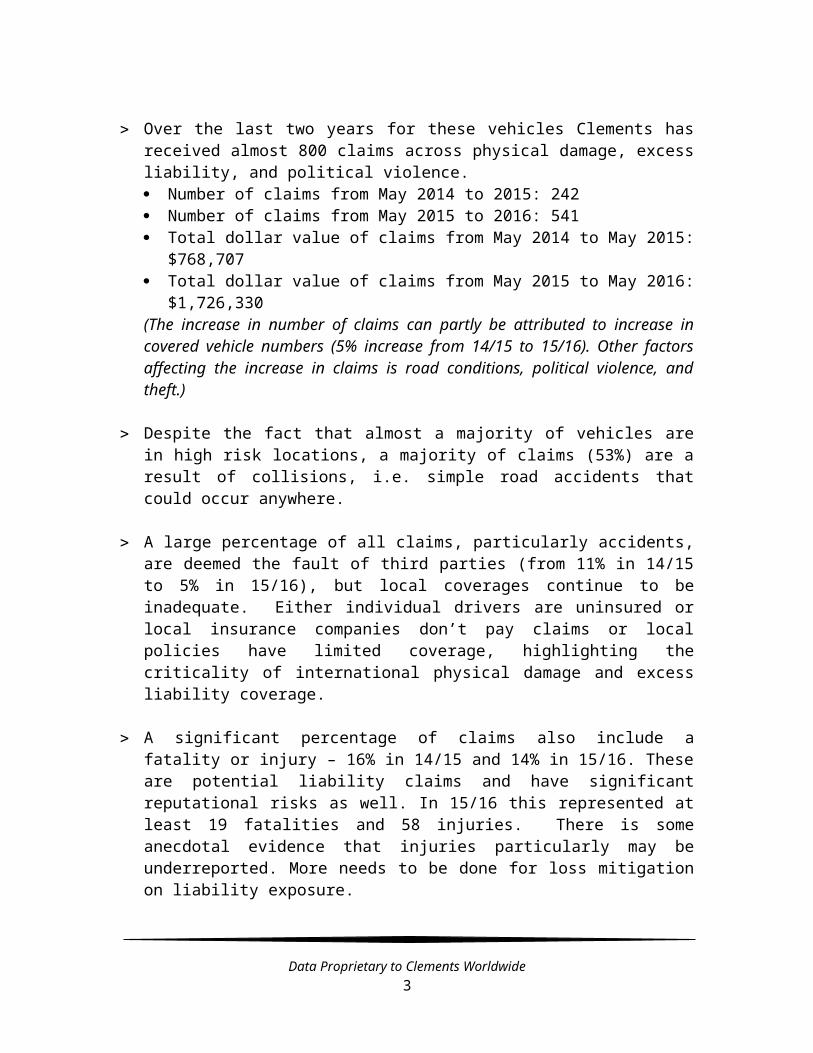

Over the last two years for these vehicles Clements has received almost 800 claims across physical damage, excess liability, and political violence. Number of claims from May 2014 to 2015: 242 Number of claims from May 2015 to 2016: 541 Total dollar value of claims from May 2014 to May 2015: $768,707 Total dollar value of claims from May 2015 to May 2016: $1,726,330(The increase in number of claims can partly be attributed to increase in covered vehicle numbers (5% increase from 14/15 to 15/16). Other factors affecting the increase in claims is road conditions, political violence, and theft.)

Data Proprietary to Clements Worldwide2

EXECUTIVE SUMMARY

Despite the fact that almost a majority of vehicles are in high risk locations, a majority of claims (53%) are a result of collisions, i.e. simple road accidents that could occur anywhere.

A large percentage of all claims, particularly accidents, are deemed the fault of third parties (from 11% in 14/15 to 5% in 15/16), but local coverages continue to be inadequate. Either individual drivers are uninsured or local insurance companies don’t pay claims or local policies have limited coverage, highlighting the criticality of international physical damage and excess liability coverage.

A significant percentage of claims also include a fatality or injury – 16% in 14/15 and 14% in 15/16. These are potential liability claims and have significant reputational risks as well. In 15/16 this represented at least 19 fatalities and 58 injuries. There is some anecdotal evidence that injuries particularly may be underreported. More needs to be done for loss mitigation on liability exposure.

Incident notifications are received, on average, 58 days after an incident with a huge amount of variation. Better training on claims submissions is critical as it is hard to collect any additional required data with such significant lag times. This time frame was consistent across both years.

Data Proprietary to Clements Worldwide3

SEVERE + EXTREME RISK COUNTRIES AS DESIGNATED BY LLOYD’S OF LONDON

Afghanistan Lebanon

Algeria Libya

Burkina Faso Mali

CAR Nigeria

Chad Pakistan

DRC Russia

Egypt Somalia

Guinea South Sudan

India Thailand

Iraq Ukraine

Israel Yemen

Data Proprietary to Clements Worldwide4

Conte

2014 2015

TOP VEHICLES BY

COUNTRY

# OF CLAIMS

BY COUNTRY

GROSS DOLLAR

VALUE OF CLAIMS BY COUNTRY

VEHICLES AS % OF

CLEMENTS

COVERED VEHICLES

# CLAIMS AS % OF TOTAL VEHICLES IN

COUNTRY

# CLAIMS AS % OF

OVERALL CLAIMS

$ CLAIMS BY COUNTRY AS

% OF OVERALL $

CLAIMS

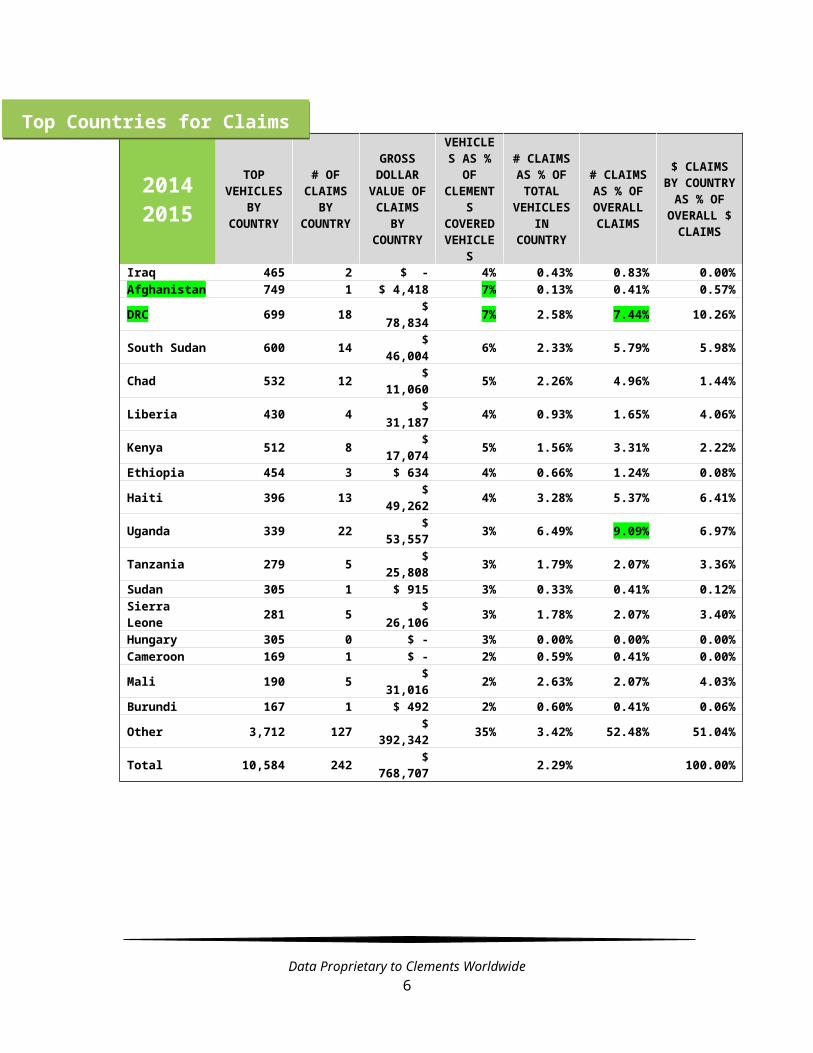

Iraq 465 2 $ - 4% 0.43% 0.83% 0.00%Afghanistan 749 1 $ 4,418 7% 0.13% 0.41% 0.57%DRC 699 18 $ 78,834 7% 2.58% 7.44% 10.26%South Sudan 600 14 $ 46,004 6% 2.33% 5.79% 5.98%Chad 532 12 $ 11,060 5% 2.26% 4.96% 1.44%Liberia 430 4 $ 31,187 4% 0.93% 1.65% 4.06%Kenya 512 8 $ 17,074 5% 1.56% 3.31% 2.22%Ethiopia 454 3 $ 634 4% 0.66% 1.24% 0.08%Haiti 396 13 $ 49,262 4% 3.28% 5.37% 6.41%Uganda 339 22 $ 53,557 3% 6.49% 9.09% 6.97%Tanzania 279 5 $ 25,808 3% 1.79% 2.07% 3.36%Sudan 305 1 $ 915 3% 0.33% 0.41% 0.12%Sierra Leone 281 5 $ 26,106 3% 1.78% 2.07% 3.40%Hungary 305 0 $ - 3% 0.00% 0.00% 0.00%Cameroon 169 1 $ - 2% 0.59% 0.41% 0.00%Mali 190 5 $ 31,016 2% 2.63% 2.07% 4.03%Burundi 167 1 $ 492 2% 0.60% 0.41% 0.06%Other 3,712 127 $ 392,342 35% 3.42% 52.48% 51.04%Total 10,584 242 $ 768,707 2.29% 100.00%

Data Proprietary to Clements Worldwide5

Top Countries for Claims

Severe or Extreme Risk =

20152016

TOP VEHICLES

BY COUNTRY

# OF CLAIMS

BY COUNTRY

GROSS DOLLAR VALUE OF CLAIMS BY

COUNTRY

VEHICLES AS % OF

CLEMENTS COVERED VEHICLES

CLAIMS AS % OF TOTAL VEHICLES IN

COUNTRY

CLAIMS AS % OF OVERALL CLAIMS

$ CLAIMS BY COUNTRY AS

% OF OVERALL $

CLAIMS

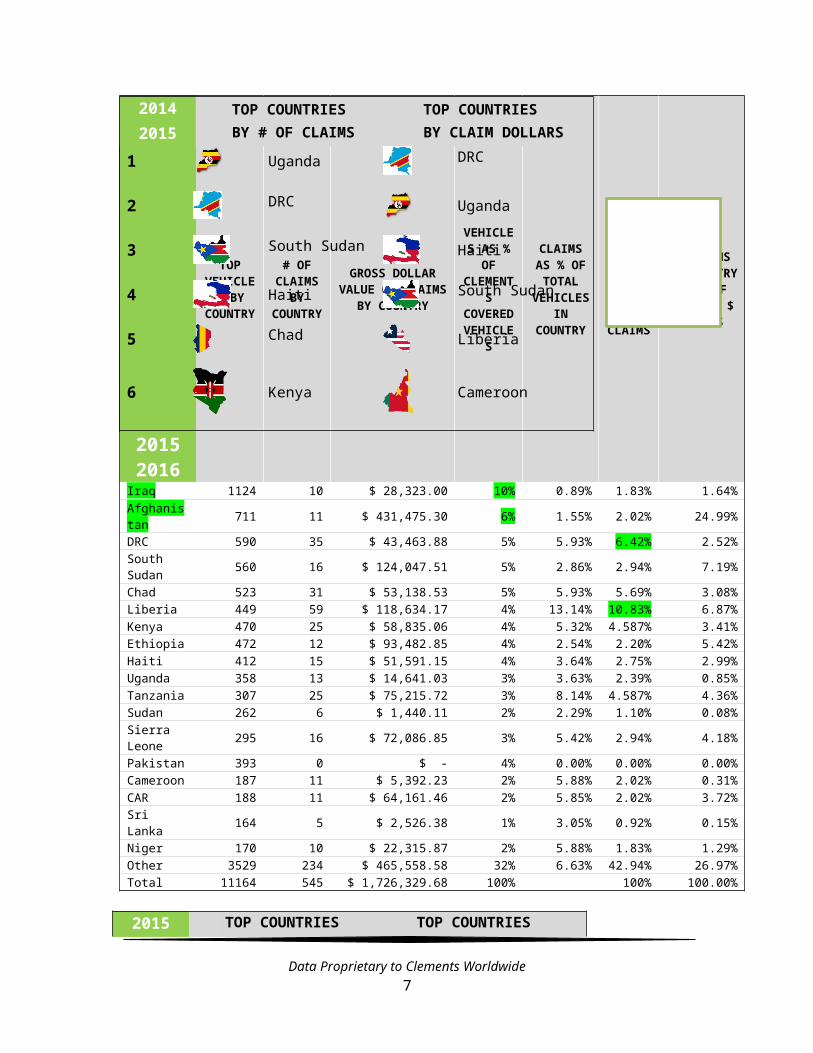

Iraq 1124 10 $ 28,323.00 10% 0.89% 1.83% 1.64%Afghanistan 711 11 $ 431,475.30 6% 1.55% 2.02% 24.99%DRC 590 35 $ 43,463.88 5% 5.93% 6.42% 2.52%South Sudan 560 16 $ 124,047.51 5% 2.86% 2.94% 7.19%Chad 523 31 $ 53,138.53 5% 5.93% 5.69% 3.08%Liberia 449 59 $ 118,634.17 4% 13.14% 10.83% 6.87%Kenya 470 25 $ 58,835.06 4% 5.32% 4.587% 3.41%Ethiopia 472 12 $ 93,482.85 4% 2.54% 2.20% 5.42%Haiti 412 15 $ 51,591.15 4% 3.64% 2.75% 2.99%Uganda 358 13 $ 14,641.03 3% 3.63% 2.39% 0.85%Tanzania 307 25 $ 75,215.72 3% 8.14% 4.587% 4.36%Sudan 262 6 $ 1,440.11 2% 2.29% 1.10% 0.08%Sierra Leone 295 16 $ 72,086.85 3% 5.42% 2.94% 4.18%Pakistan 393 0 $ - 4% 0.00% 0.00% 0.00%Cameroon 187 11 $ 5,392.23 2% 5.88% 2.02% 0.31%CAR 188 11 $ 64,161.46 2% 5.85% 2.02% 3.72%Sri Lanka 164 5 $ 2,526.38 1% 3.05% 0.92% 0.15%Niger 170 10 $ 22,315.87 2% 5.88% 1.83% 1.29%Other 3529 234 $ 465,558.58 32% 6.63% 42.94% 26.97%Total 11164 545 $ 1,726,329.68 100% 100% 100.00%

2015 2016

TOP COUNTRIESBY # OF CLAIMS

TOP COUNTRIESBY CLAIM DOLLARS

1 LiberiaAfghanistan

Data Proprietary to Clements Worldwide6

Severe or Extreme Risk =

2014 2015

TOP COUNTRIESBY # OF CLAIMS

TOP COUNTRIESBY CLAIM DOLLARS

1 Uganda DRC

2 DRC Uganda

3 South Sudan Haiti

4 Haiti South Sudan

5 Chad Liberia

6 Kenya Cameroon

2DRC DRC

3Chad

Liberia

4 Tanzania Ethiopia

5 Kenya Tanzania

6South Sudan

Sierra Leone

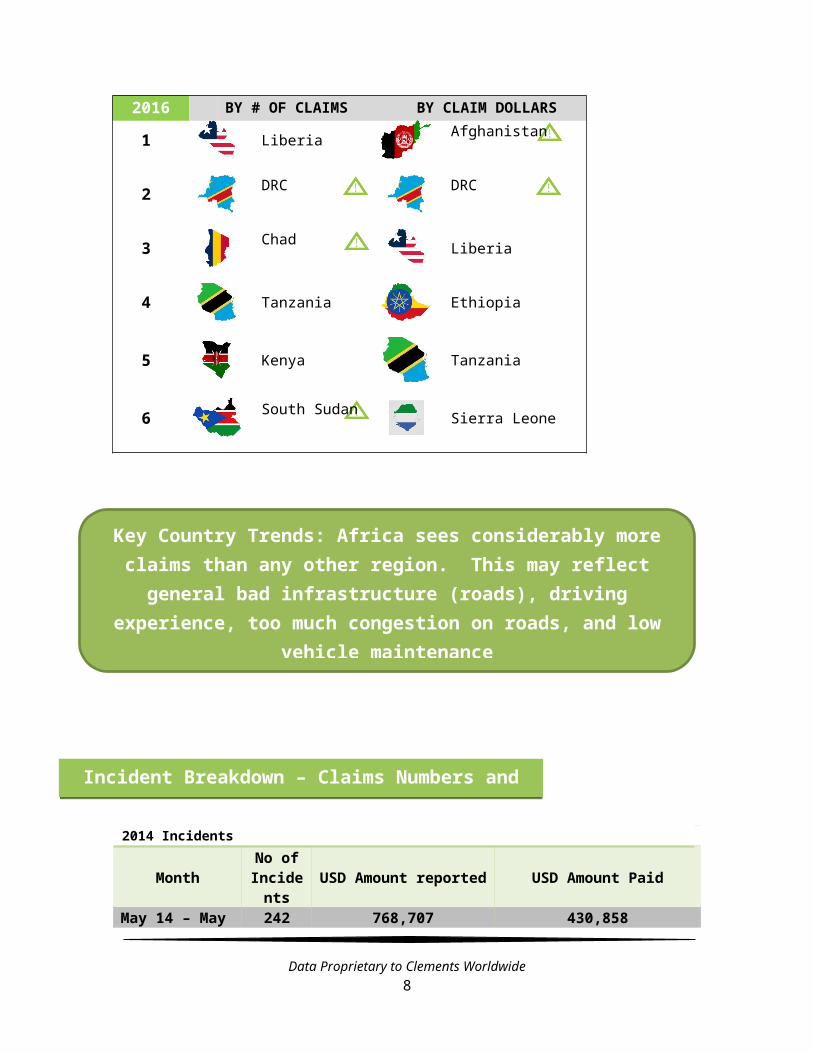

2014 Incidents

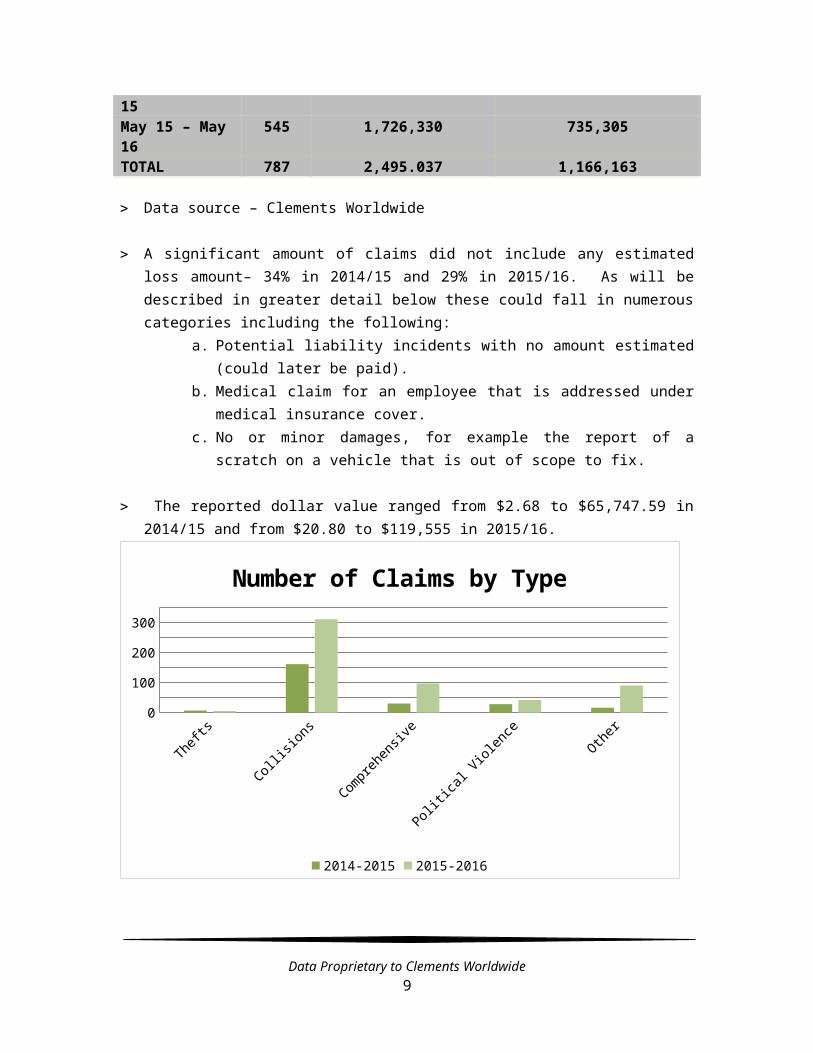

Month No of Incidents USD Amount reported USD Amount Paid

May 14 – May 15 242 768,707 430,858May 15 – May 16 545 1,726,330 735,305TOTAL 787 2,495.037 1,166,163

Data source – Clements Worldwide

Data Proprietary to Clements Worldwide7

Key Country Trends: Africa sees considerably more claims than any other region. This may reflect general bad infrastructure (roads), driving

experience, too much congestion on roads, and low vehicle maintenance

Incident Breakdown – Claims Numbers and Amounts

A significant amount of claims did not include any estimated loss amount– 34% in 2014/15 and 29% in 2015/16. As will be described in greater detail below these could fall in numerous categories including the following:

a. Potential liability incidents with no amount estimated (could later be paid).b. Medical claim for an employee that is addressed under medical insurance cover.c. No or minor damages, for example the report of a scratch on a vehicle that is

out of scope to fix.

The reported dollar value ranged from $2.68 to $65,747.59 in 2014/15 and from $20.80 to $119,555 in 2015/16.

Thefts Collisions Comprehensive Political Violence Other0

50

100

150

200

250

300

350

Number of Claims by Type

2014-2015 2015-2016

As stated in the executive summary a large percentage of claims, 67% in 2014/15 and 53% in 2015/16 were a result of collisions but claims as a result of political violence are significant and often represent high dollar value claims.

As relates to comprehensive claims, which includes items like vandalism and wear and tear, insurance policy design really needs to reflect the reality of these types of claims.

Poor road conditions and spurious fuel which damages engines may be excluded from local policies but Clements Worldwide consistently pays these claims.

Data Proprietary to Clements Worldwide8

% of Number of Claims % of Dollar Value of Claims0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

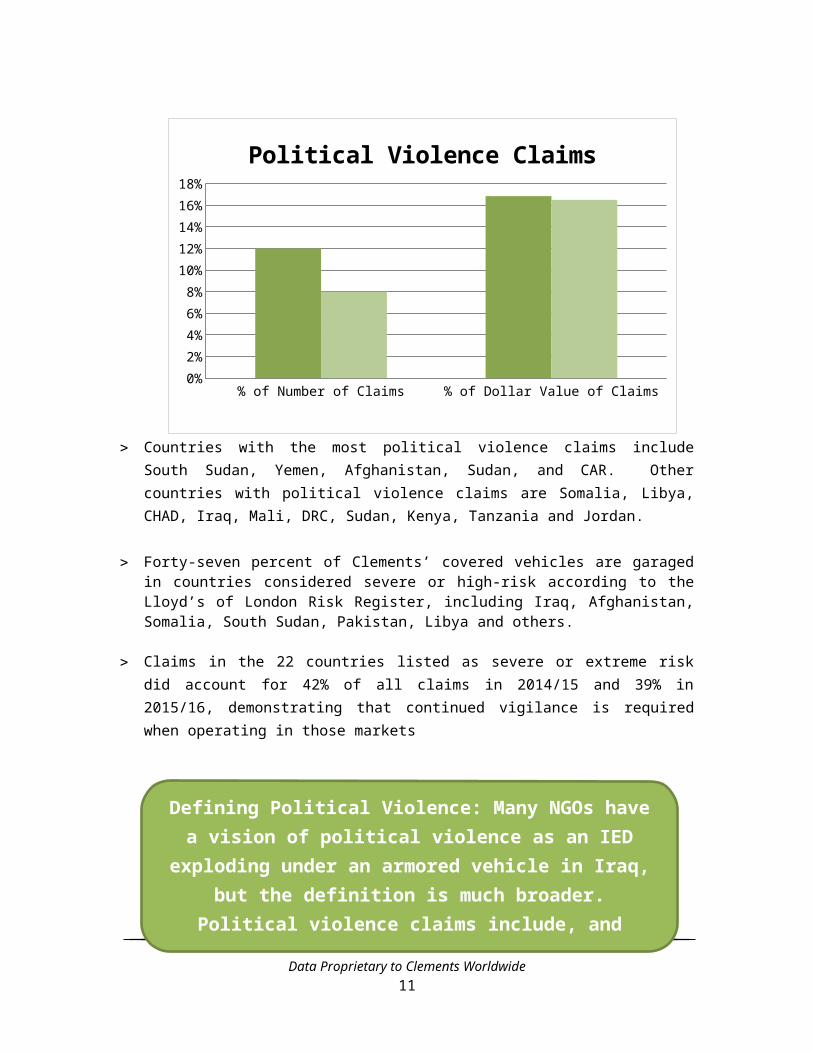

Political Violence Claims

Countries with the most political violence claims include South Sudan, Yemen, Afghanistan, Sudan, and CAR. Other countries with political violence claims are Somalia, Libya, CHAD, Iraq, Mali, DRC, Sudan, Kenya, Tanzania and Jordan.

Forty-seven percent of Clements’ covered vehicles are garaged in countries considered severe or high-risk according to the Lloyd’s of London Risk Register, including Iraq, Afghanistan, Somalia, South Sudan, Pakistan, Libya and others.

Claims in the 22 countries listed as severe or extreme risk did account for 42% of all claims in 2014/15 and 39% in 2015/16, demonstrating that continued vigilance is required when operating in those markets

Data Proprietary to Clements Worldwide9

Defining Political Violence: Many NGOs have a vision of political violence as an IED exploding under an armored vehicle in Iraq,

but the definition is much broader. Political violence claims include, and frequently are more attributed to, strike, terrorism riots, civil disobedience, refuges throwing stones at vehicles etc.

Open Paid Closed Without Payment0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Status of Claims

2014-2015 2015-2016

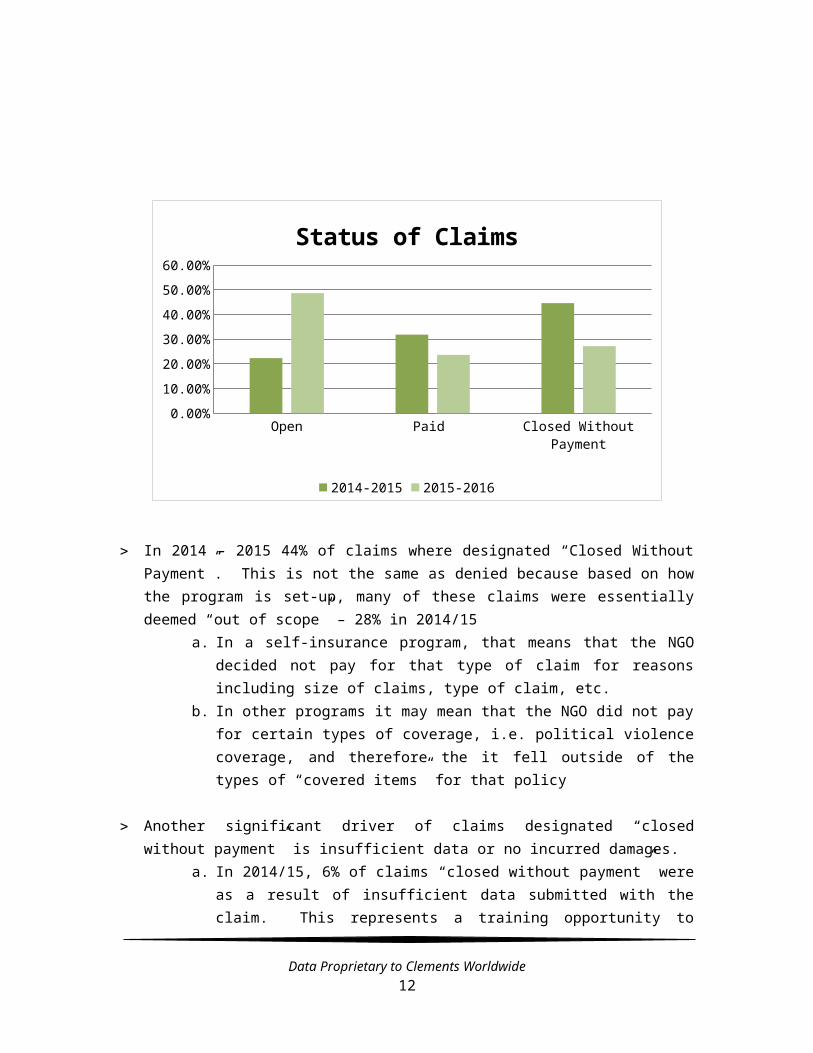

In 2014 – 2015 44% of claims where designated “Closed Without Payment”. This is not the same as denied because based on how the program is set-up, many of these claims were essentially deemed “out of scope” – 28% in 2014/15

a. In a self-insurance program, that means that the NGO decided not pay for that type of claim for reasons including size of claims, type of claim, etc.

b. In other programs it may mean that the NGO did not pay for certain types of coverage, i.e. political violence coverage, and therefore the it fell outside of the types of “covered items” for that policy

Another significant driver of claims designated “closed without payment” is insufficient data or no incurred damages.

a. In 2014/15, 6% of claims “closed without payment” were as a result of insufficient data submitted with the claim. This represents a training opportunity to ensure staff understand how to submit claims forms and respond to additional requests for information.

b. 13% of claims “closed without payment” were as a result of “no damages” meaning that an incident occurred, but the resulting damages were so minor, i.e. a scratch on the vehicle, or recovered vehicle, in the event of a theft. These are legitimate claims and should be encouraged to be filed to provide a full picture of the fleet.

Data Proprietary to Clements Worldwide10

2014-2015 2015-20160

10

20

30

40

50

60

70

FatalitiesInjuries

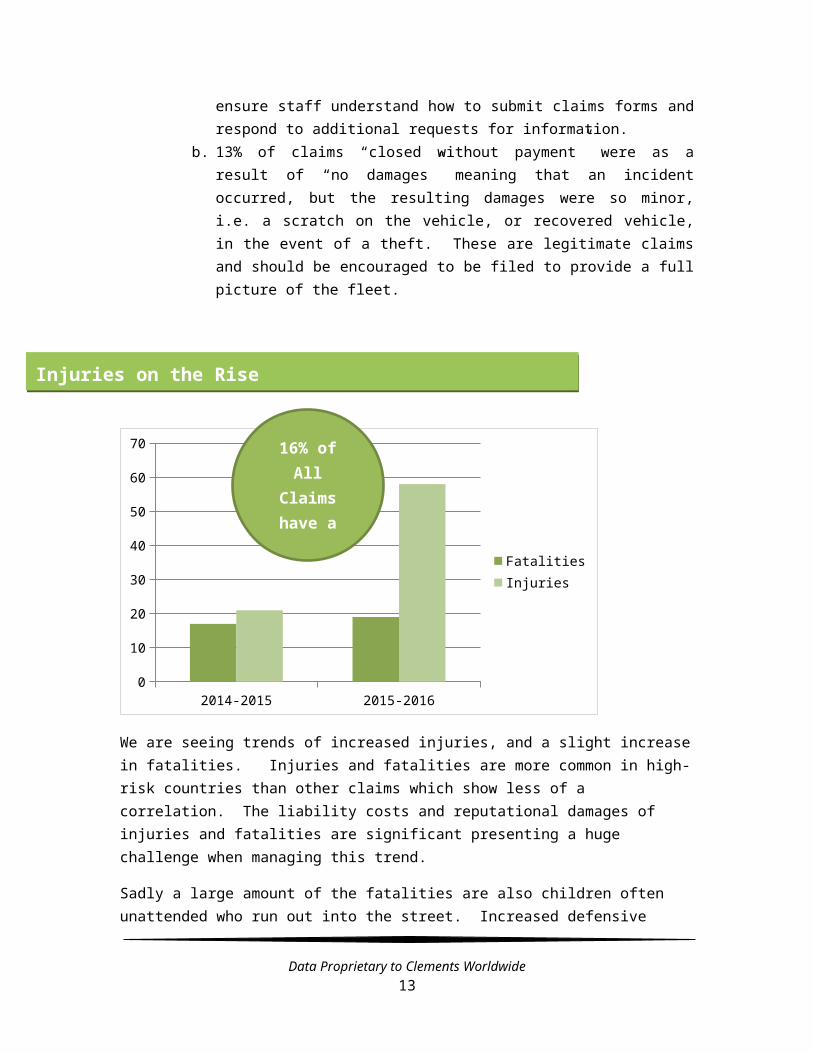

We are seeing trends of increased injuries, and a slight increase in fatalities. Injuries and fatalities are more common in high-risk countries than other claims which show less of a correlation. The liability costs and reputational damages of injuries and fatalities are significant presenting a huge challenge when managing this trend.

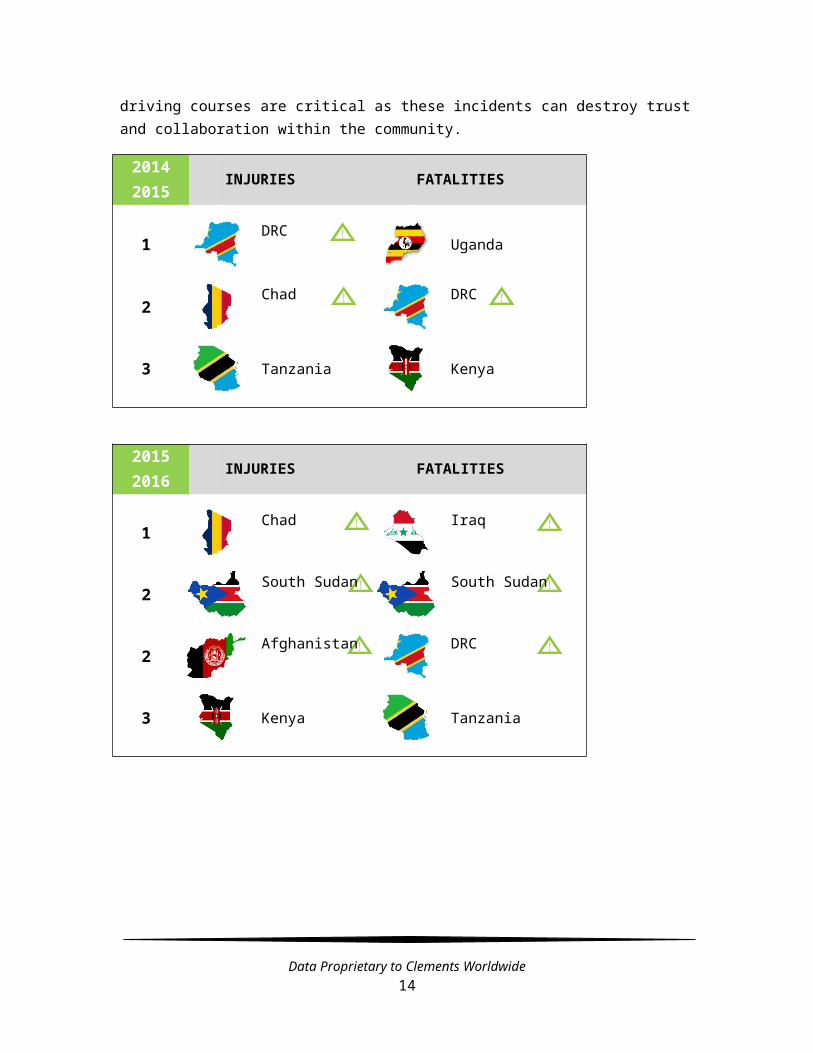

Sadly a large amount of the fatalities are also children often unattended who run out into the street. Increased defensive driving courses are critical as these incidents can destroy trust and collaboration within the community.

2014 2015

INJURIES FATALITIES

1DRC

Uganda

2Chad DRC

3 Tanzania Kenya

2015 INJURIES FATALITIES

Data Proprietary to Clements Worldwide11

16% of All Claims have a Fatality or

Injury

Injuries on the Rise

2016

1Chad Iraq

2South Sudan South Sudan

2Afghanistan DRC

3 Kenya Tanzania

Data Proprietary to Clements Worldwide12

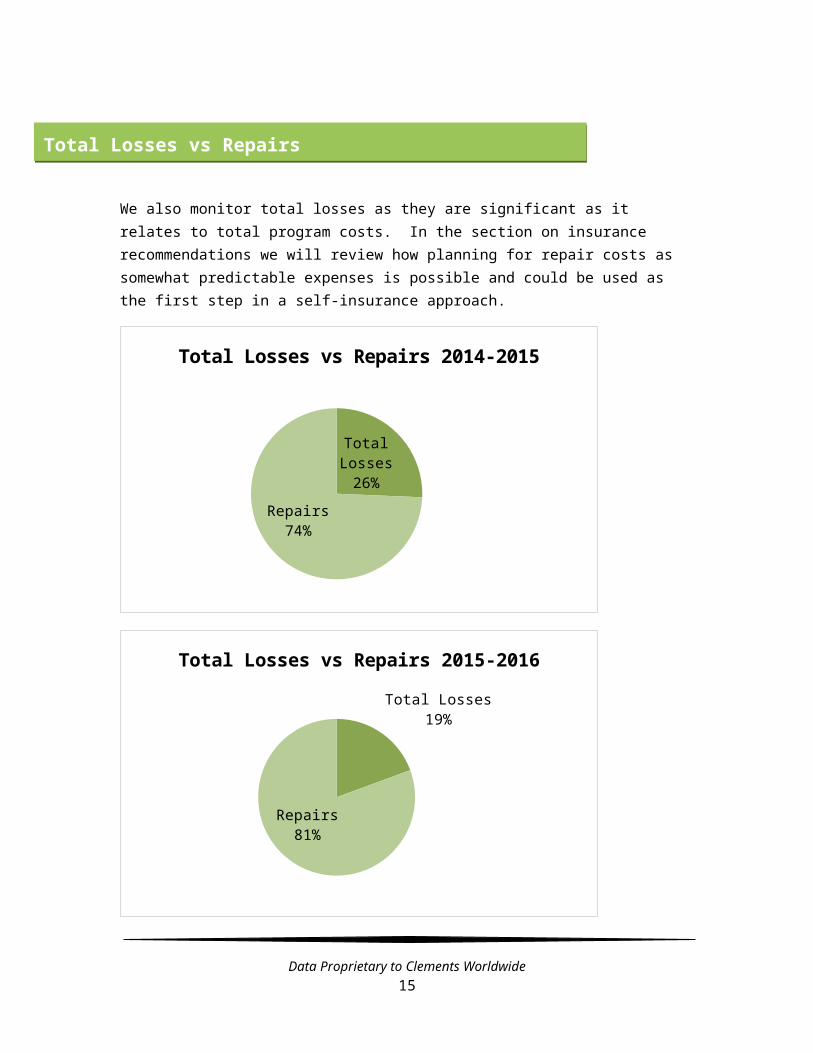

We also monitor total losses as they are significant as it relates to total program costs. In the section on insurance recommendations we will review how planning for repair costs as somewhat predictable expenses is possible and could be used as the first step in a self-insurance approach.

Total Losses26%

Repairs74%

Total Losses vs Repairs 2014-2015

Total Losses19%

Repairs81%

Total Losses vs Repairs 2015-2016

Data Proprietary to Clements Worldwide13

Total Losses vs Repairs

Confiscations

While Clements Worldwide does not have specific quantifiable data related to government or non-state action confiscations of vehicles, we are hearing anecdotally about increased concern from our NGO partners. The largest example of widespread vehicle confiscation was in Sudan in 2009 when many NGOs were ejected from the countries, but there have been other examples from Afghanistan to Belarus.

In addition Forced Abandonment also remains a growing concern especially in war ravaged countries where organizations need to evacuate the country on short notice, with no means or time to protect or expatriate the in-country assets

Any insurance policy design must consider this possibility in companies where they operate, particularly if those countries are on the severe or extreme risk registry.

Data Proprietary to Clements Worldwide14

Confiscations and Forced Abandonment

To Self – Insure or Not to Self-Insure

There continues to be a trend by large NGOs to move to a self-insurance model for fleet. This is driven by the fact that many of the type of claims are “predictable and expected”. Collisions and minor accidents requiring repairs only, such as cracked windshields, are normal and expected claims. These principally refer to physical damage claims as a result of collision or comprehensive claim type, including vandalism, normal wear and tear, theft, etc. Some NGOs may choose to put aside a reserve for such items rather than pay insurance premiums for this type of expense. It is important to note that self-insurance definitely does not mean no insurance – the NGO must still develop guidelines as to what types of claims will be covered by the reserve and the operational processes to manage these claims against the reserve. Typically field offices will pay into that reserve.

To limit reserve requirements on physical damage, organizations can set-up a stop loss for excessive losses typically as a result of physical violence or total losses, which were 24% of all claims in 2014/15 and 15% in 2015/16. The cost of a total loss claim or political violence claim is not surprisingly much larger and less likely to occur on an annual basis so an NGO might not wish to hold this much funds in reserve. The stop loss can be set as a limit threshold for an annual aggregate over which the stop loss policy responds to any physical damage or political violence claim. Alternatively, it can be set as a limit threshold per event. If a claim crosses the per event limit, then the stop loss is triggered.

Certain types of losses and covers are not advisable to self-insure due to the catastrophic nature and severity of such losses such as Third Party Liability and Political Violence

How to Address Implementing Partners

While this report does not highlight the amount of vehicles and claims associated with Implementing Partners (IPs), this is a critical issue for larger NGOs. First if the NGO is using a self-insurance model it must make the decision whether to cover IPs. If the NGO chooses to cover them then those organizations should pay into the reserve like any field office.

When an IP is involved in an incident involving a third party where there is a potential risk of liability exposure, any potential claims should be covered by the IP’s insurance. The IP should also still be considered responsible for any remaining amount not covered by their insurance. Clements Worldwide, however, has consistently seen cases where the principal NGO also faces liability by the third party so it needs to be prepared for this risk. To be clear, the NGO MAY BE ULTIMATELY responsible for any liability associated with vehicles operated by IPs.

Data Proprietary to Clements Worldwide15

Insurance Recommendations Based on Fleet Data Analysis

Therefore, it is critical that the NGO ensures that its local offices and IPs obtain a local third party liability policy that meets legal requirements of the host country. Because of the extent of third party liability claims and the lack of consistency in actually obtaining funds from local insurance companies in developing markets as a result of discrepancies in benefits, terms, limits, and professionalism, Clements Worldwide also recommends that NGOs obtain global third party subsidiary liability, which is an additional insurance to cover claims not met by the local third party liability policy.

Important Limitations Commonly Seen in Local Third Party Liability Policies

Below are some common limitations of third party liability policies:

o Some local policies may not cover property damage for 3rd party vehicles / property. Coverage may be limited to bodily injuries only.

o Local policies may not cover passenger legal liability and that leaves a big gap in cover.

o Many of the locations have only the compulsory Third party / auto liability policy in place locally.

o With local covers the limits are fairly low and in the event of a foreign national being injured, these limits may not be adequate.

o Local policies will also have limited Jurisdiction / Territory and may not cover suits brought outside the local jurisdiction. In contrast Group / Global covers will provide this flexible cover for lawsuits filed anywhere in the world.

As a result of all of these limitations local policies should be backed by Excess/ Contingent Auto Liability policies held at the organizational or group level. As stated above, because of local legal requirements the primary auto liability will need to be organized through local placements, however all NGOs should explore Worldwide Third Party Excess Liability.

More on Worldwide Third Party Excess Liability

Where local third party liability is not available or not in place, the policy pays claims on a first dollar basis. Where local third party liability is obtained, the policy will pay claims on the next dollar basis, above local limits, or if the local program fails to comply. Another benefit of global cover is that it is borderless. Therefore, if vehicles are driven across borders as part of continuing operations, no additional coverage is necessary.

To find out more about insurance coverage options for your fleet read the Clements 2015 White Paper – Prioritizing Fleet Risk Management to Improve your ROI and Mission Completion,

Data Proprietary to Clements Worldwide16

While collisions greatly outweigh the number of political violence claims, the cost of political violence claims is greater than the average claim and Clements Worldwide still sees many organizations not opting to upgrade to this type of coverage. Particularly for organizations with significant operations in the 22 Severe and Extreme Risk countries, political violence really is a must have in today’s environment.

The amount of claims attributed to third parties also continue to be significant – but many organizations still only purchase the required local third party liability policies that we consistently see through the claim recovery process is inadequate in terms of benefits, limits, terms, and professionalism. As a result, Clements Worldwide continues to recommend that customers purchase Worldwide Third Party Excess Liability.

In regards to Third Party Excess Liability, large NGOs must be diligent that Implementing Partners also purchase this policy as they could still be exposed.

Additional training is still needed regarding claims submission best practices. The average lag between incident date and reported date of almost 60 days can result in more claims being denied as attempts to get additional detail become more difficult over that extended time.

Furthermore, with 3 to 7% of claims including a fatality, often of a child, defensive driving courses should also be considered. While there will always be some number of accidents, the NGO has the critical responsibility of training its drivers to protect and support the communities in which they operate.

Finally some Important considerations for better fleet risk management include standardized, borderless coverage across all locations and vicarious liability coverage for the group entity/ HQ/ cross jurisdictional claims. A global approach to fleet insurance and management would not only result in costs savings but also result in better control of the program, administration, claims etc.

Data Proprietary to Clements Worldwide17

Conclusions