Embed Size (px)

Citation preview

Larry Apfelbaum

Larry A. Apfelbaum a practicing attorney in Personal Injury Negotiation, Dispute Resolution, and Workers' Compensation departments.

Larry was born in Freeport, Illinois and raised in the suburbs of Chicago with three brothers. After graduating from Illinois State University in Bloomington, Ill,. in 1984 with a degree in Business Administration / Accounting, he attended the University of Illinois College of Law in Champaign-Urbana earning his Juris Doctor in 1987. Following graduation, Larry worked for a general practice law firm in Bloomington before joining Kanoski Bresney in 1989 to concentrate on personal injury and workers’ compensation cases. During his initial career, Larry quickly realized that the laws are often too complicated for everyday people to understand, and insurance companies like to take advantage of this fact. By focusing his legal career on helping injured people and workers, he knows he’s doing good work leveling the playing field with big insurance companies. In 1995, Larry opened the Bloomington office of Kanoski Bresney and, along with his staff of dedicated legal assistants, Larry has proudly represented thousands of clients in central Illinois over the past 26 years. Larry has been married to Karen since 1988 and together they currently have seven animal children: Clark, Sissy, Ebony, Nibbles, Fuzz, Banjo and Oscar.

Noah Hamann Noah Hamann is a partner with Brady, Connolly & Masuda, P.C. His practice is focused on defending employers, insurance companies and third party administrators in workers’ compensation litigation. He practices before the Illinois Workers’ Compensation Commission and he handles all aspects of the appellate process as well. He is a graduate of Northern Illinois University’s College of Law and Illinois State University. He resides in Normal with his wife and son.

Tuesday, October 18, 2016

10 S. LaSalle St. Suite 900

Chicago, IL 60603 (312) 425-3131

Fax: (312) 425-0110

www.bcm-law.com

211 Landmark Dr. Suite C-2

Normal, IL 61761 (309) 862-4914

Fax: (309) 862-4205

Noah P. Hamann, Esq.

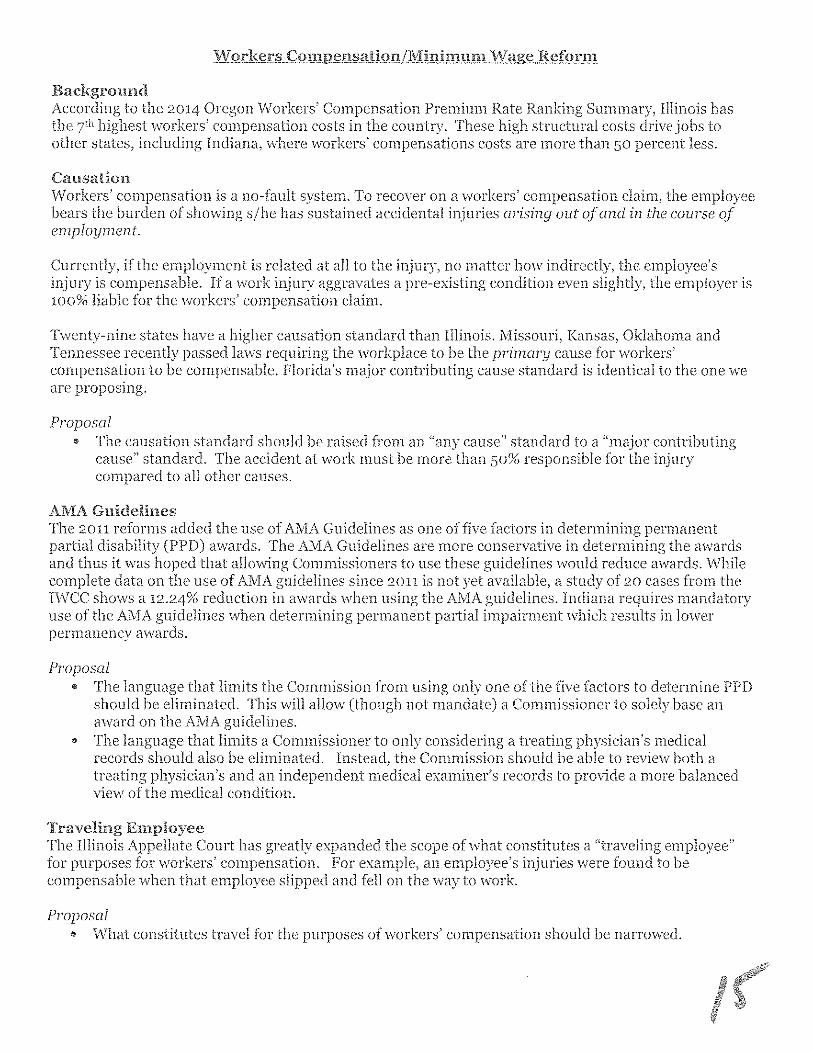

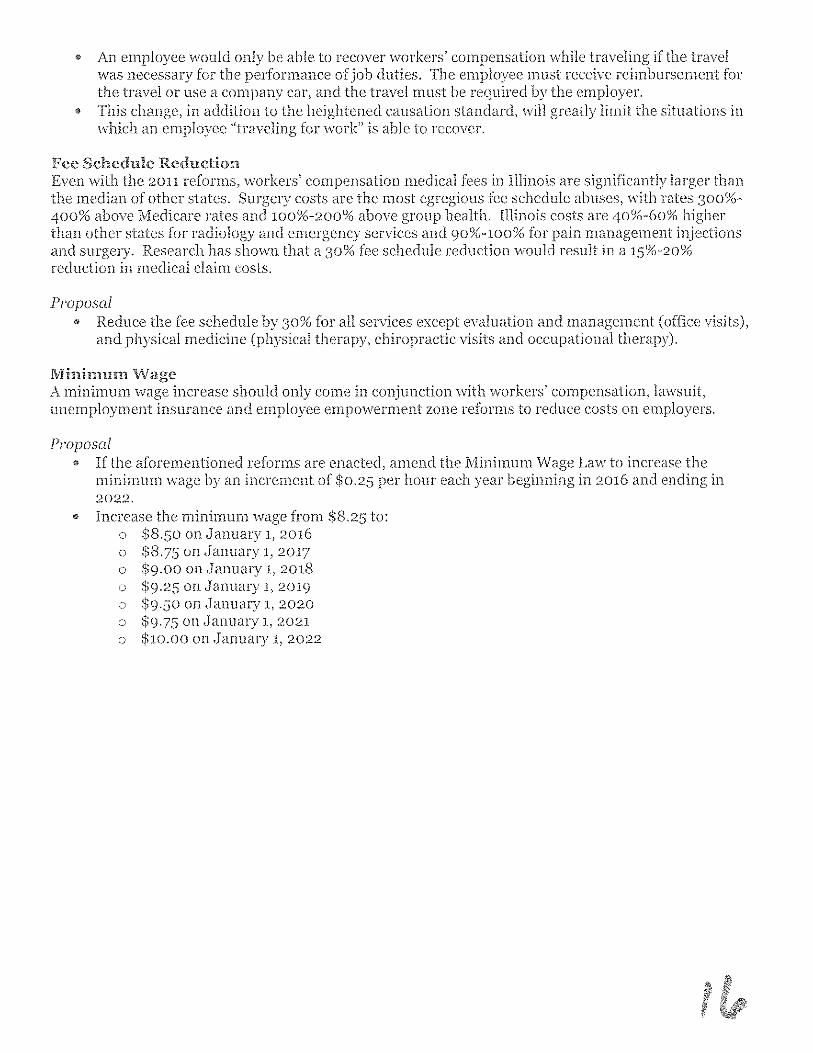

Major defenses to workers’ compensation cases

2

Accident Causation The Nature and Extent of the Injury

Accident

Did it even happen? Was it reported? (Late notice negatively impacts

workers’ credibility) What do coworkers have to say? Security camera footage? Are the medical records consistent with the worker’s

allegations?

3

Accident Must arise out of and in the course of employment 1. In the course of = The time, place and

circumstances under which the accident occurred. Orsini v. Industrial Comm'n (1987)

Examples of when an accident is not in the course of : A. Commuting to and from work? B. Performing a personal matter? C. Parking lot?

4

…Accident continued. Arising out of = the risk of injury must be connected or incidental to the employment. Caterpillar Tractor Co. v. Industrial Comm’n, 129 Ill. 2d 52, 58541 N.E.2d 665, 667 (1989) 1. Categories of risk (A) risks distinctly associated with

the employment, (B) risks that are personal to the employee, (C) neutral risks faced by members of the general public.

5

…Accident continued. (A) Risks distinctly associated with the employment are

compensable. (B) Risks that are personal can be defended, i.e. worker

has a history of fainting. He fainted at work and injured his head. The risk is unique to the worker and has no relationship to an employment related task.

(C) Neutral risks can be defended, i.e., She tripped while walking across the street to enter work. No greater risk of injury than a member of the general public.

6

Causation

7

The injury must be causally connected to the work accident. This defense generally arises when the worker has a

pre-existing condition, i.e. he has a history of low back problems, an accident happens at work and now he needs back surgery. Is the employer responsible?

…Causation continued. The chief causation defense is an independent medical examination (IME). Cases involving an IME will boil down to which physician the arbitrator finds to be more credible, the IME doctor or the treating doctor. Deference is usually given to the treating physician. So to prevail, the employer should aim to show: 1. The IME doctor has more knowledge about the medical history, i.e.

has the doctor reviewed all relevant medical records? 2. The IME doctor has a better understanding of the worker’s job

duties. Send a detailed job description, an ergonomics report or a job analysis video.

3. Does the IME doctor have surveillance that the treater does not? 4. Is the IME doctor better credentialed than the treating doctor?

8

Nature and Extent A “win” can involve minimizing the ultimate payout. High exposure cases: 1. A wage differential award allows a worker to recover 2/3rds

the difference between what would have been earned in the full performance of the job and the new lower wage resulting from an injury, until the age of 67 or 5 years from the award, whichever is later. Section 8(d)1.

2. A permanent total disability award grants weekly benefits for life if the worker can prove that the injury prevents him/her from working again. Section 8(f).

To defend these cases efforts focus on improving the medical condition and/or labor market to increase employment prospects.

9

…Nature and Extent continued. Example: 55 year old. Injured 1/15/14. Low back surgery. Has permanent restrictions. Was earning $700 per week. 25 year life expectancy. If he is permanently and totally disabled, the case is worth up to $367,423.46 If the employer can help find a job for the worker that pays $10.00 per hour, exposure drops to a wage differential. The wage differential value in this example is $92,178.32. (*Examples use 5% rate and reflect present cash value)

10

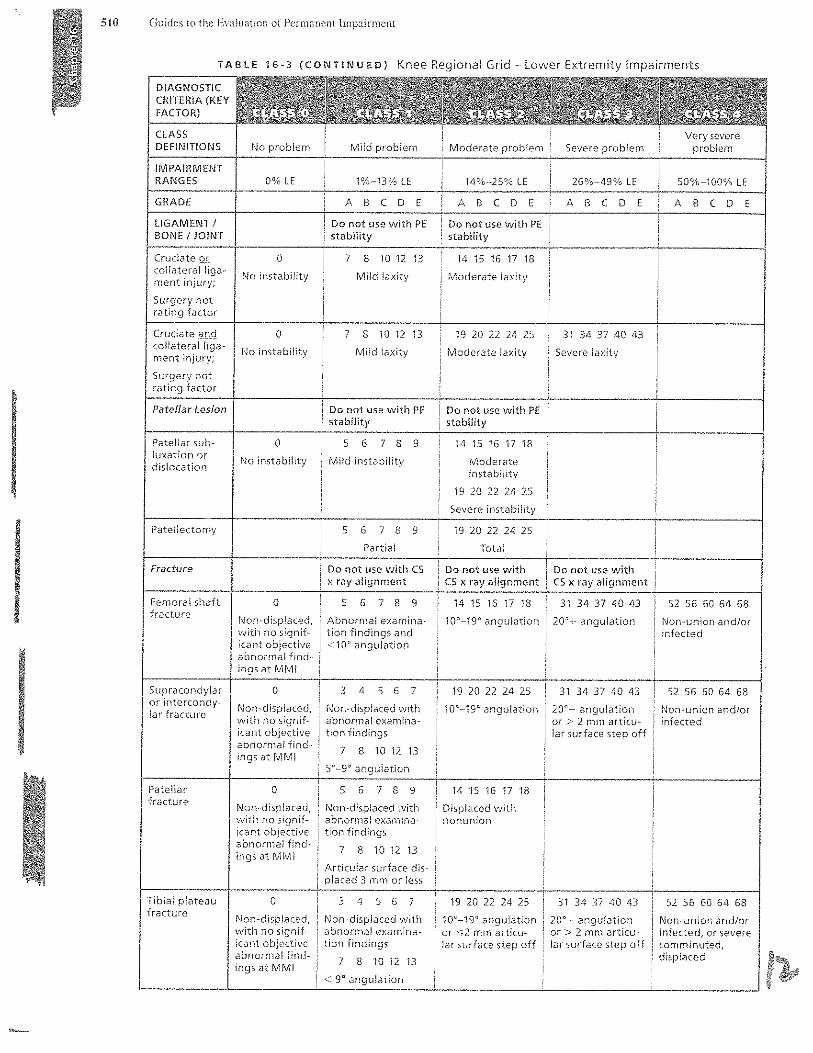

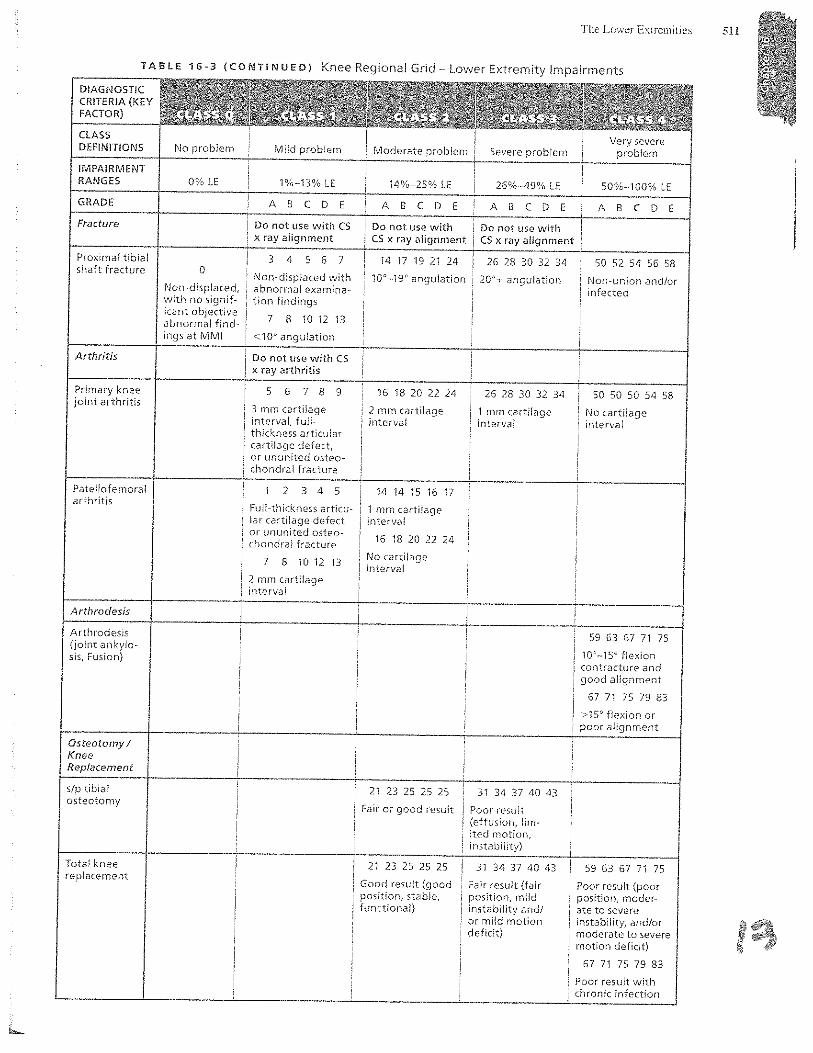

…Nature and Extent Continued. Factors used by Arbitrators to determine case value: 1. AMA Impairment Rating (impairment does not equal

disability in Illinois). 2. Occupation of the injured worker. The more labor

intense, the higher the value. 3. Age. The younger the worker is, the higher the value

because they have to live and work with the disability longer.

4. Impact of the injury on future earning capacity. 5. Evidence of disability corroborated by the treating

medical records.

11

Questions?

12

John M. Muir, Esq.

O B J E C T I V E S E T T L E M E N T A D V I S O R S

Settlement Advisor

Expertise

John M. Muir is a Settlement Advisor with Ringler offices in Bloomington,

Illinois and St. Louis, Missouri. He joined Ringler full-time in 2013. He

provides expertise to clients regarding financial security and investment.

He attends mediations and settlement conferences for his clients. He has

provided judicial training for the Illinois Workers’ Compensation

Commission Commissioners, Arbitrators and Staff Attorneys and

presented structured settlement CLE & CE programs for professionals in

the industry .

John M. Muir, Jr. is an attorney licensed in Illinois and a Structured

Settlement Consultant for Ringler Associates covering Eastern Missouri

including Greater St. Louis and Southern Illinois. He specializes in

Personal Injury and Workers’ Compensation cases and has expertise

regarding both Liability and Workers’ Compensation Medicare Set-Asides.

John received his Juris Doctorate from John Marshall Law School in Chicago, Illinois, where he

achieved the CALI award for Workers’ Compensation. Additionally, he received high marks

during a semester he spent at the University Of Illinois College Of Law. John has worked for the

McLean County and Peoria County Public Defender, and currently works on a pro bono basis for

those in need.

Education

John Marshall Law School (JD)

University of Illinois College of Law (Visiting student)

B.A., Philosophy, Illinois State University

Professional Associations McLean County Bar Association

National Structured Settlements Trade Association - Member

Workers’ Compensation Lawyers Association – Gold Sponsor

Public Speaking Judicial Training for Illinois Workers’ Compensation Commission – On Workers’ Compensation

Structured Settlements and Present Value

John W. Muir, CCLA, CPCU

O B J E C T I V E S E T T L E M E N T A D V I S O R S

Settlement Advisor

Expertise

John Muir is a Settlement Advisor and Managing Partner of Ringler offices

in Bloomington, Illinois and St. Louis, Missouri. He works with and is a

trusted advisor to Insurance Companies, Third Party Administrators and

Attorneys throughout the United States to resolve workers’ compensation

and personal injury claims beneficial to all parties utilizing structured

settlements.

John has 37 years of experience in the industry. He provides support and

advice during all phases of settlement negotiations, court hearings,

mediations, arbitrations and settlement conferences. He specializes in

settling workers’ compensation and personal injury cases with specific

expertise in funding and Medicare Set-Aside Arrangements, Life

Life Care Plans and Special Needs Trusts. He creates structured annuities for physical injury cases

including workers’ compensation, medical malpractice, personal injury and products liability, as

well as non-physical injury structures for employment and discrimination, punitive damages and

attorney fees. He also provides educational seminars on the use of settlement annuities and

funding Medicare Set- Aside Arrangements in tort and workers’ compensation cases.

Education

Graduate of University of Michigan Executive Program

Chartered Property Casualty Underwriter (CPCU) designation

Casualty Claim Law Associate

B.A., Accounting, Illinois Wesleyan University

Professional Associations National Structured Settlements Trade Association - Member

Workers’ Compensation Lawyers Association – Gold Sponsor

Workers’ Compensation Claims Association of Illinois -Past President

Public Speaking Judicial Training for Illinois Workers’ Compensation Commission – On Workers’ Compensation

Structured Settlements and Present Value

Claims and Litigation Management Midwest Conference - Pros & Cons of an ACA Defense

Ringler Radio - Motor Vehicle Collisions, Structures and the Injured

National Alliance of Medicare Set-Aside Professionals - Optimizing Medicare Set-Aside

Arrangements Via Structured Settlements

1

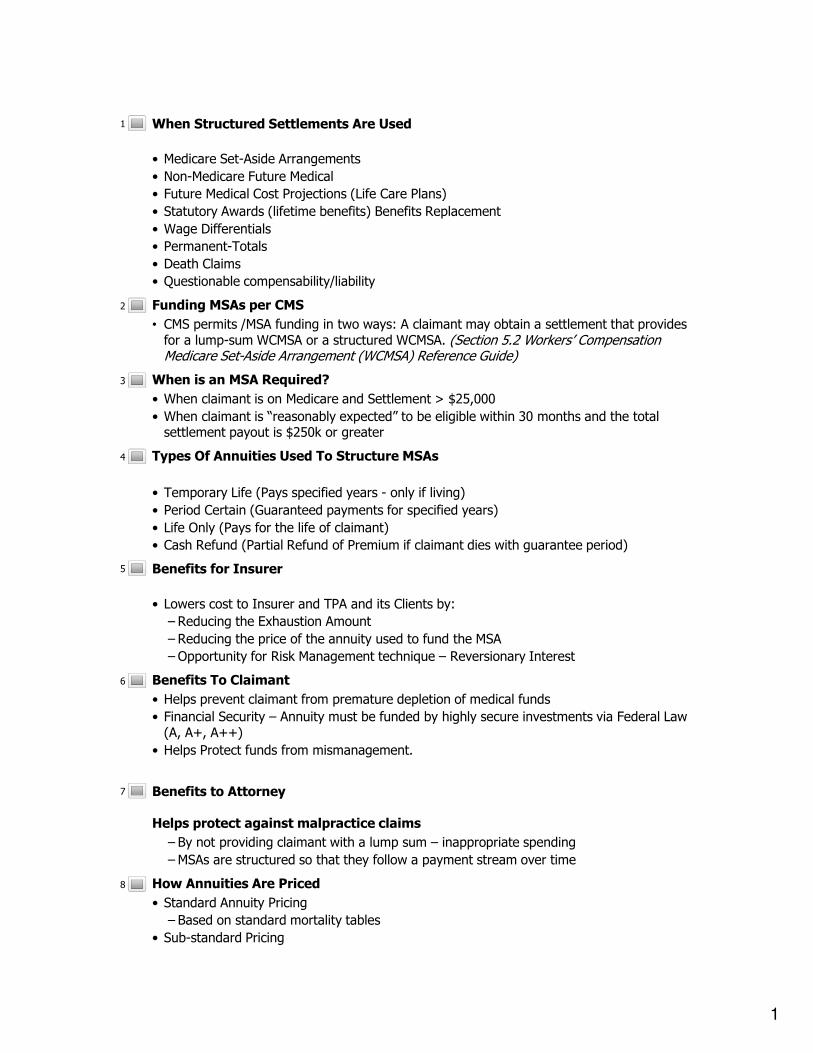

When Structured Settlements Are Used

• Medicare Set-Aside Arrangements

• Non-Medicare Future Medical

• Future Medical Cost Projections (Life Care Plans)

• Statutory Awards (lifetime benefits) Benefits Replacement

• Wage Differentials

• Permanent-Totals

• Death Claims

• Questionable compensability/liability

Funding MSAs per CMS

• CMS permits /MSA funding in two ways: A claimant may obtain a settlement that provides for a lump-sum WCMSA or a structured WCMSA. (Section 5.2 Workers’ Compensation Medicare Set-Aside Arrangement (WCMSA) Reference Guide)

When is an MSA Required?

• When claimant is on Medicare and Settlement > $25,000

• When claimant is “reasonably expected” to be eligible within 30 months and the total settlement payout is $250k or greater

Types Of Annuities Used To Structure MSAs

• Temporary Life (Pays specified years - only if living)

• Period Certain (Guaranteed payments for specified years)

• Life Only (Pays for the life of claimant)

• Cash Refund (Partial Refund of Premium if claimant dies with guarantee period)

Benefits for Insurer

• Lowers cost to Insurer and TPA and its Clients by:

– Reducing the Exhaustion Amount

– Reducing the price of the annuity used to fund the MSA

– Opportunity for Risk Management technique – Reversionary Interest

Benefits To Claimant

• Helps prevent claimant from premature depletion of medical funds

• Financial Security – Annuity must be funded by highly secure investments via Federal Law (A, A+, A++)

• Helps Protect funds from mismanagement.

Benefits to Attorney

Helps protect against malpractice claims

– By not providing claimant with a lump sum – inappropriate spending

– MSAs are structured so that they follow a payment stream over time

How Annuities Are Priced

• Standard Annuity Pricing

– Based on standard mortality tables

• Sub-standard Pricing

1

2

3

4

5

6

7

8

2

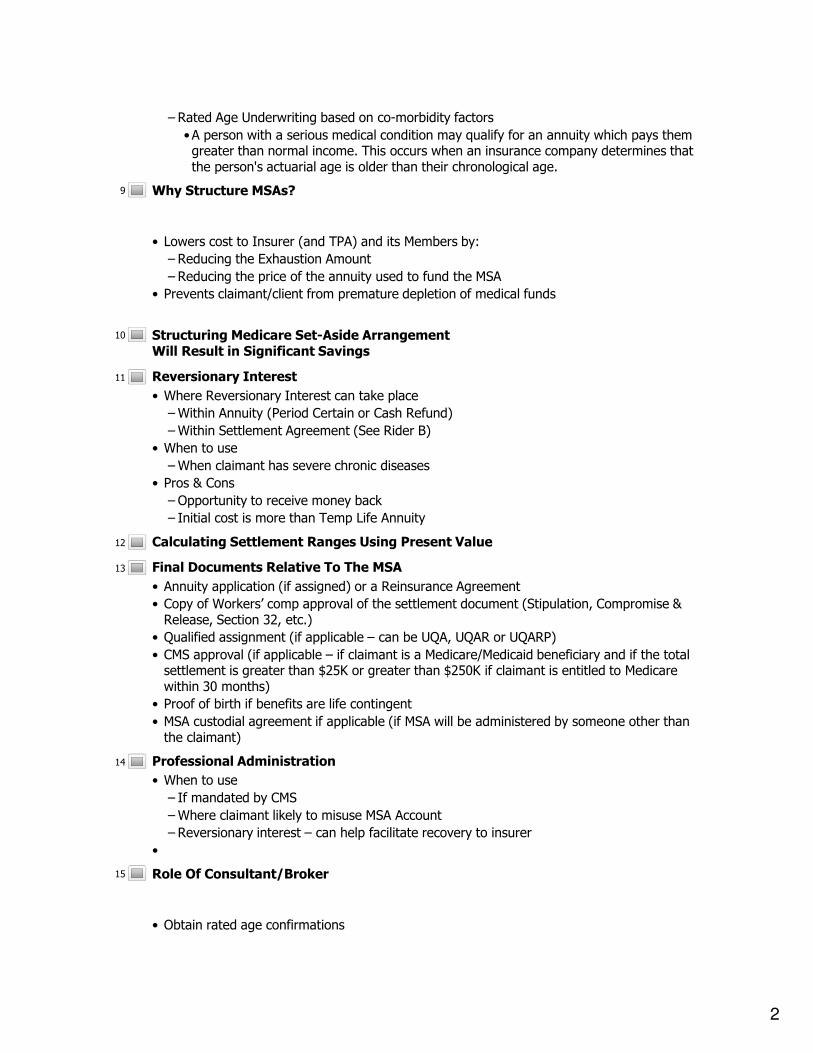

– Rated Age Underwriting based on co-morbidity factors

•A person with a serious medical condition may qualify for an annuity which pays them greater than normal income. This occurs when an insurance company determines that the person's actuarial age is older than their chronological age.

Why Structure MSAs?

• Lowers cost to Insurer (and TPA) and its Members by:

– Reducing the Exhaustion Amount

– Reducing the price of the annuity used to fund the MSA

• Prevents claimant/client from premature depletion of medical funds

Structuring Medicare Set-Aside Arrangement Will Result in Significant Savings

Reversionary Interest

• Where Reversionary Interest can take place

–Within Annuity (Period Certain or Cash Refund)

–Within Settlement Agreement (See Rider B)

• When to use

–When claimant has severe chronic diseases

• Pros & Cons

– Opportunity to receive money back

– Initial cost is more than Temp Life Annuity

Calculating Settlement Ranges Using Present Value

Final Documents Relative To The MSA

• Annuity application (if assigned) or a Reinsurance Agreement

• Copy of Workers’ comp approval of the settlement document (Stipulation, Compromise & Release, Section 32, etc.)

• Qualified assignment (if applicable – can be UQA, UQAR or UQARP)

• CMS approval (if applicable – if claimant is a Medicare/Medicaid beneficiary and if the total settlement is greater than $25K or greater than $250K if claimant is entitled to Medicare within 30 months)

• Proof of birth if benefits are life contingent

• MSA custodial agreement if applicable (if MSA will be administered by someone other than the claimant)

Professional Administration

• When to use

– If mandated by CMS

–Where claimant likely to misuse MSA Account

– Reversionary interest – can help facilitate recovery to insurer

•

Role Of Consultant/Broker

• Obtain rated age confirmations

9

10

11

12

13

14

15

3

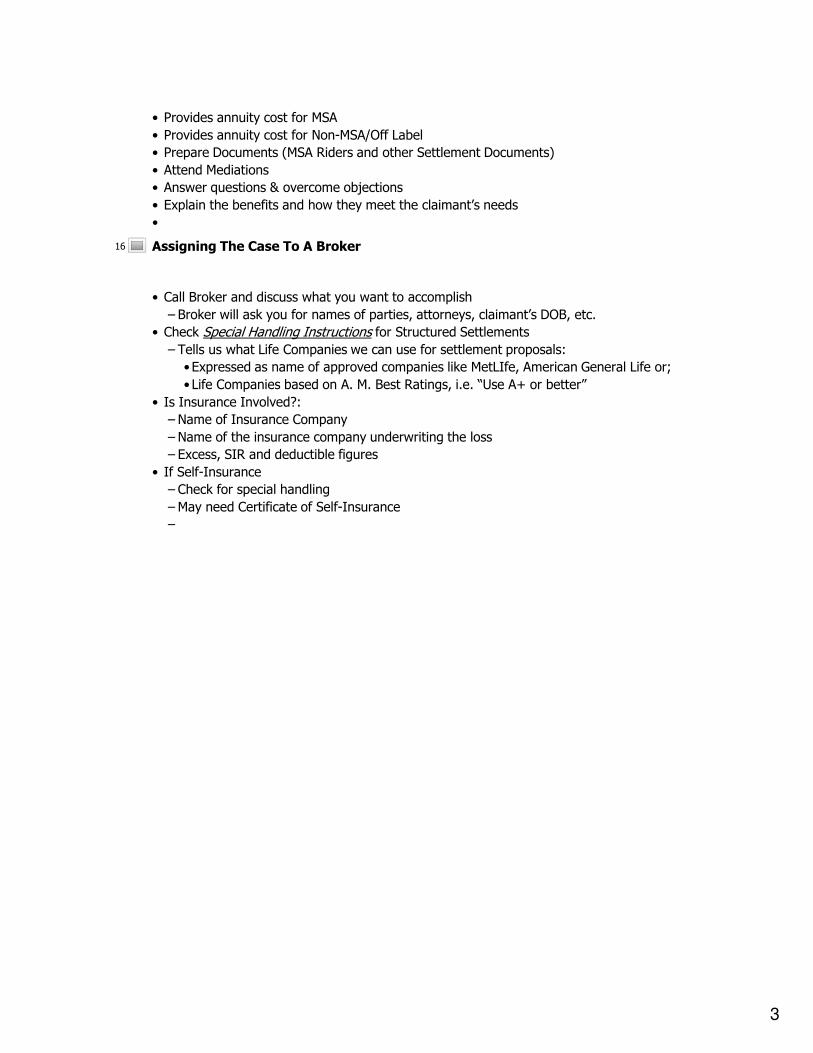

• Provides annuity cost for MSA

• Provides annuity cost for Non-MSA/Off Label

• Prepare Documents (MSA Riders and other Settlement Documents)

• Attend Mediations

• Answer questions & overcome objections

• Explain the benefits and how they meet the claimant’s needs

•

Assigning The Case To A Broker

• Call Broker and discuss what you want to accomplish

– Broker will ask you for names of parties, attorneys, claimant’s DOB, etc.

• Check Special Handling Instructions for Structured Settlements

– Tells us what Life Companies we can use for settlement proposals:

• Expressed as name of approved companies like MetLIfe, American General Life or;

• Life Companies based on A. M. Best Ratings, i.e. “Use A+ or better”

• Is Insurance Involved?:

– Name of Insurance Company

– Name of the insurance company underwriting the loss

– Excess, SIR and deductible figures

• If Self-Insurance

– Check for special handling

– May need Certificate of Self-Insurance

–

16