Embed Size (px)

Citation preview

G<; u'.

CITY OF KAPLAN, LOUISIANA

Financial Report

Year Ended June 30, 2005

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Release Date 11 -2 3.

TABLE OF CONTENTS

Page

Independent Auditors' Report 1-2

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FINANCIAL STATEMENTS (GWFS)Statement of net assets 5Statement of activities 6

FUND FINANCIAL STATEMENTS (FFS)Balance sheet - governmental funds 9Reconciliation of the governmental funds balance sheet

to the statement of net assets 10Statement of revenues, expenditures, and changes in fund balances-

governmental funds 11Reconciliation of the statement of revenues, expenditures, and

changes in fund balances of governmental funds to the statement of activities 12Comparative statement of net assets - proprietary funds 13Comparative statement of revenues, expenses, and changes in fund net

assets - proprietary funds 14Comparative statement of cash flows - proprietary funds 15-16

Notes to basic financial statements 17-43

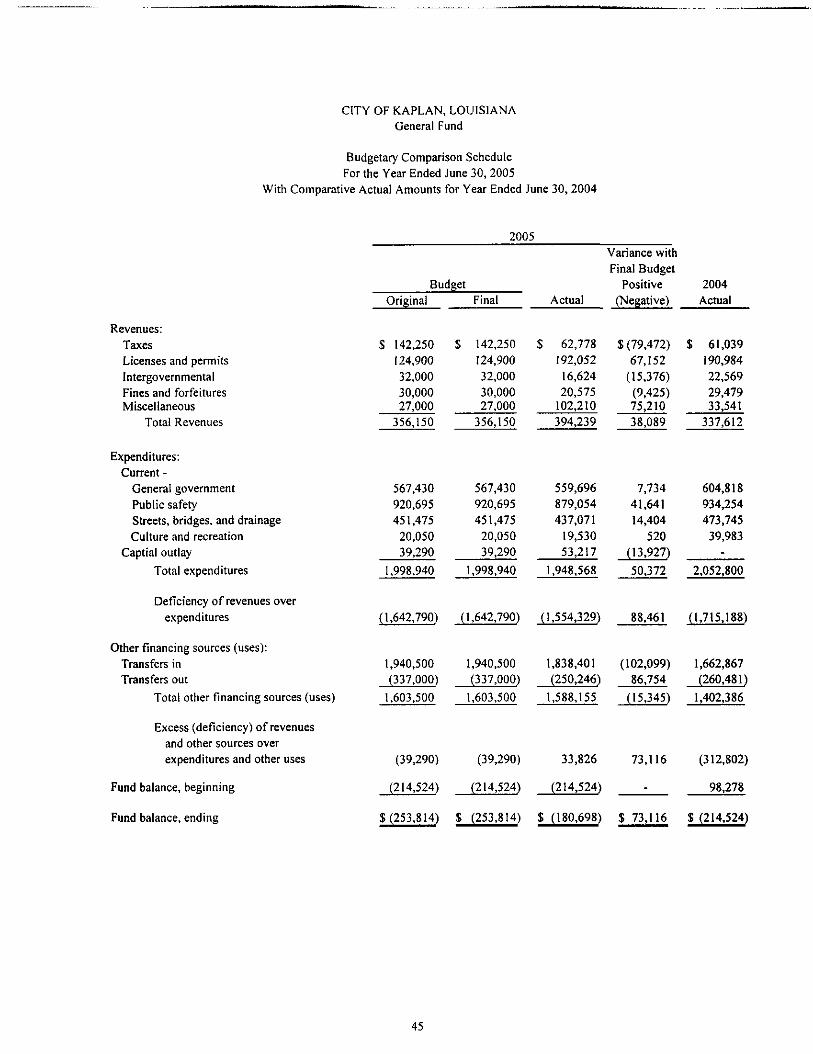

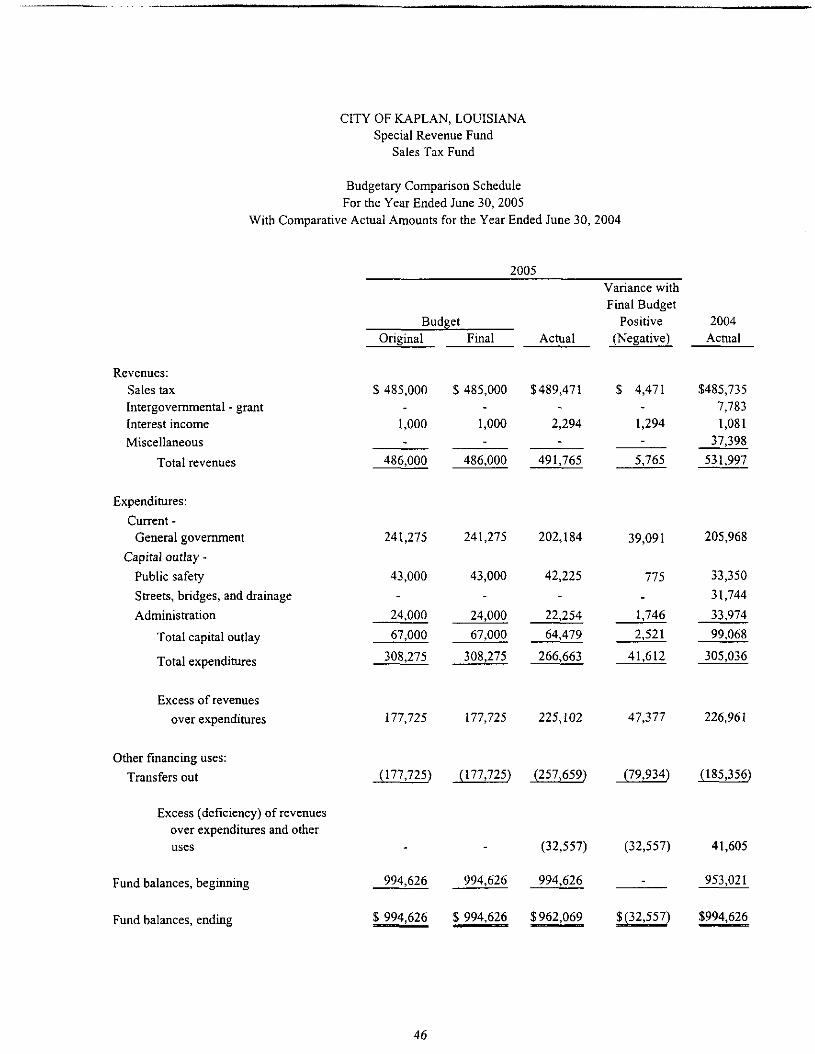

REQUIRED SUPPLEMENTARY INFORMATIONBudgetary comparison schedules:

General Fund 45Sales Tax Fund 46

OTHER SUPPLEMENTARY INFORMATION

OTHER FINANCIAL INFORMATIONMajor Governmental Funds -

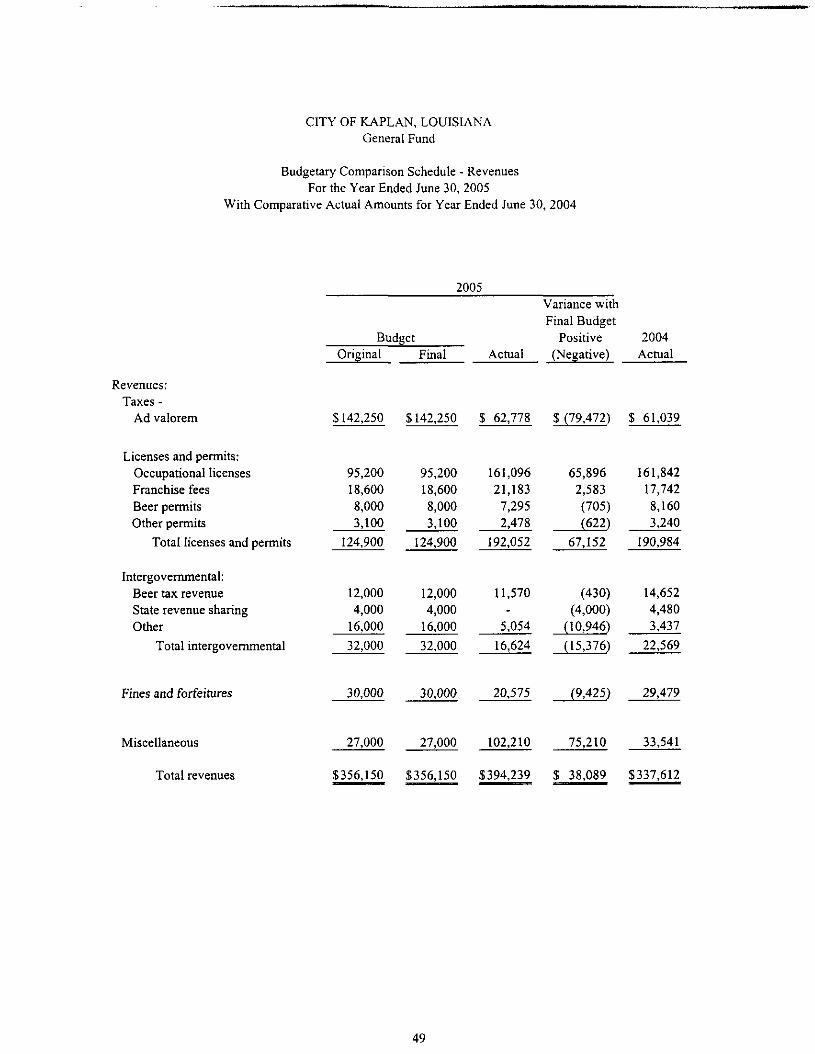

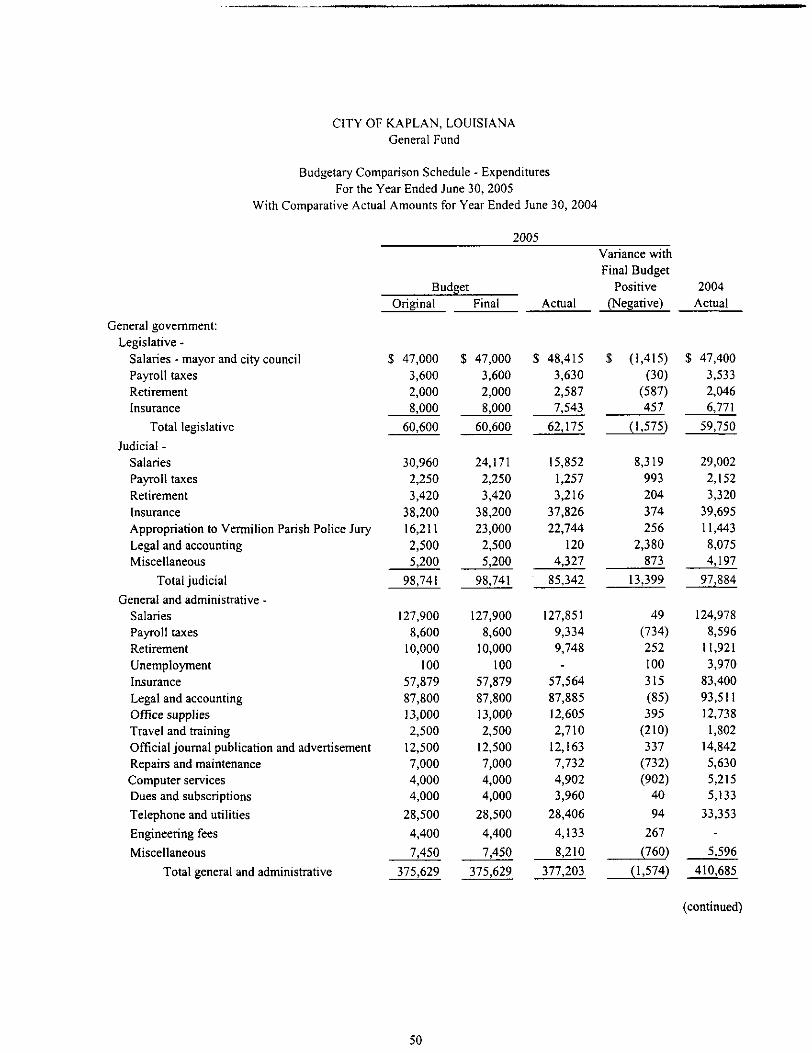

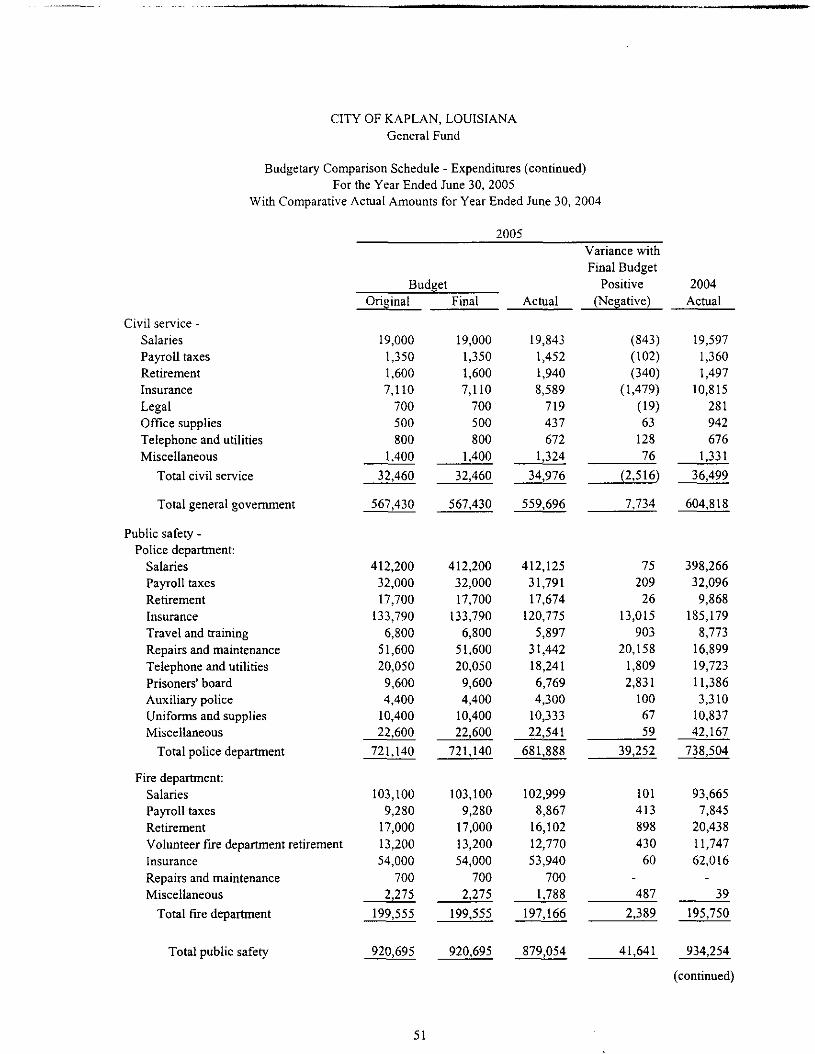

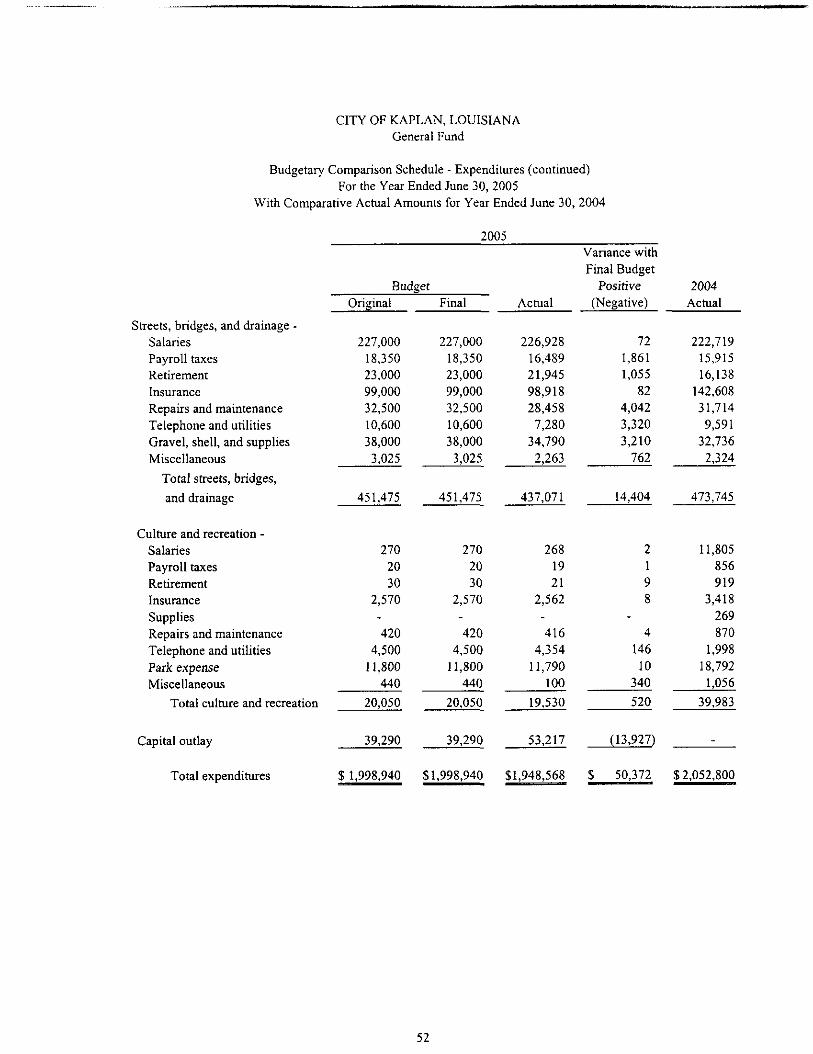

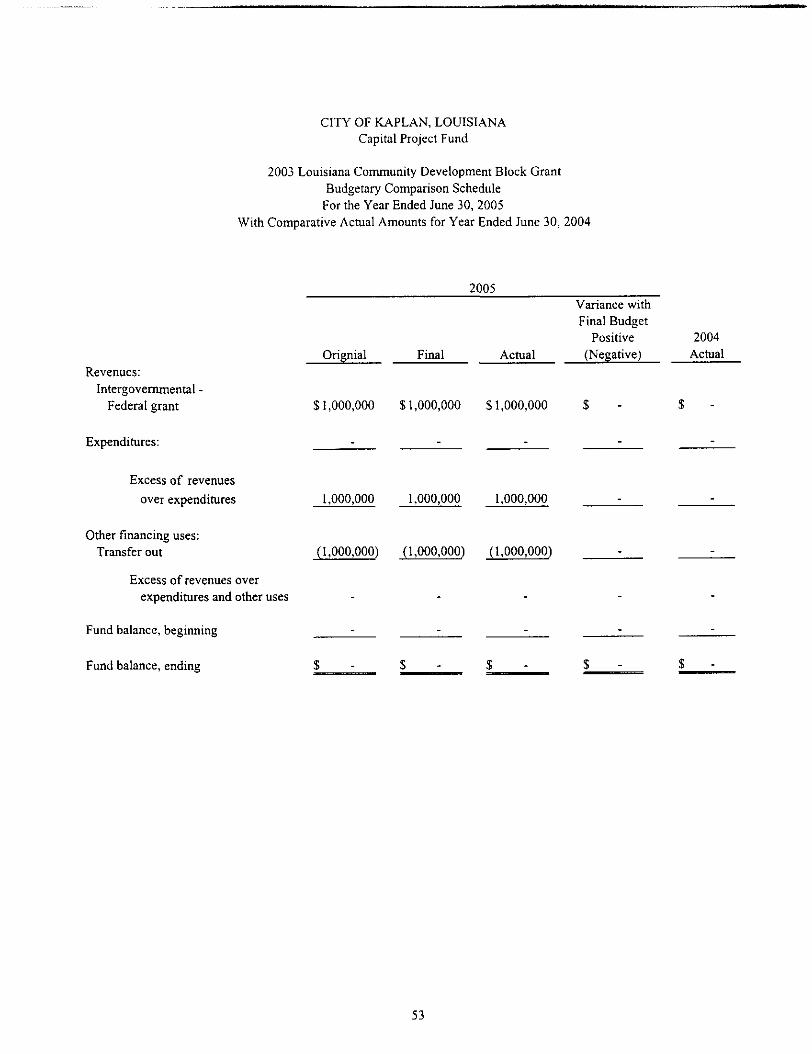

General Fund - budgetary comparison schedule - revenues 49General Fund - budgetary comparison schedule- expenditures 50-52Capital Projects Fund - bugetary comparison schedule 53

(continued)

TABLE OF CONTENTS (continued)

Page

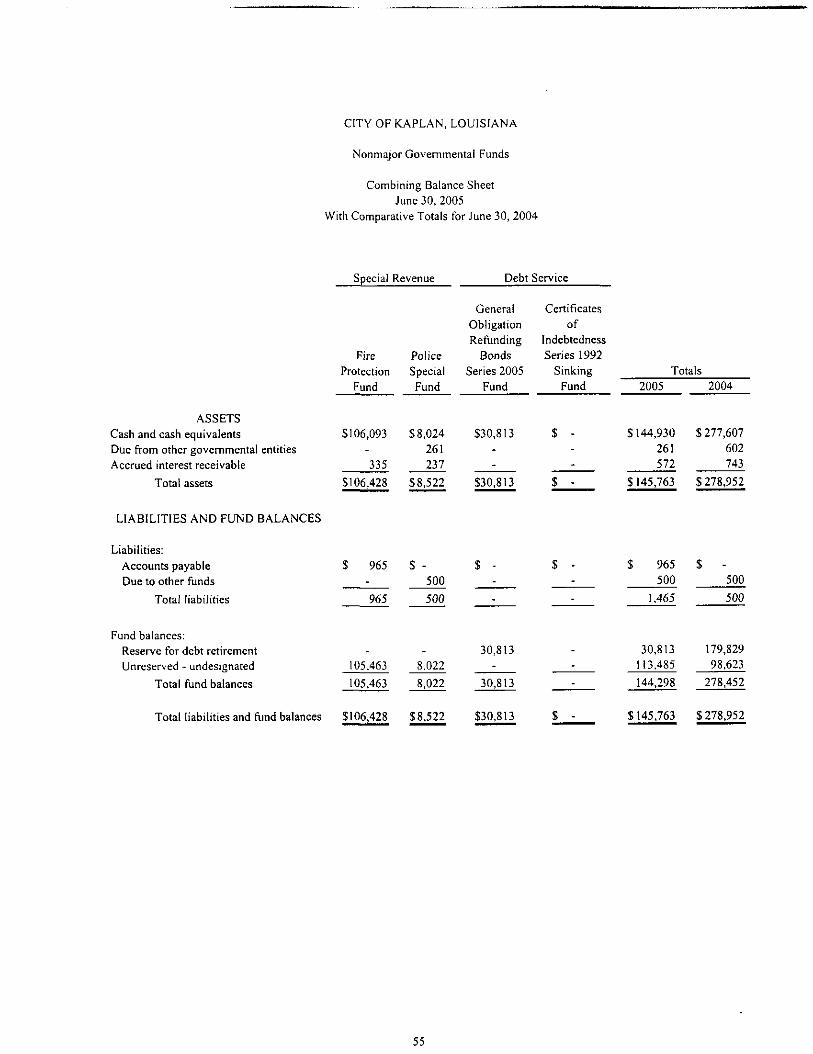

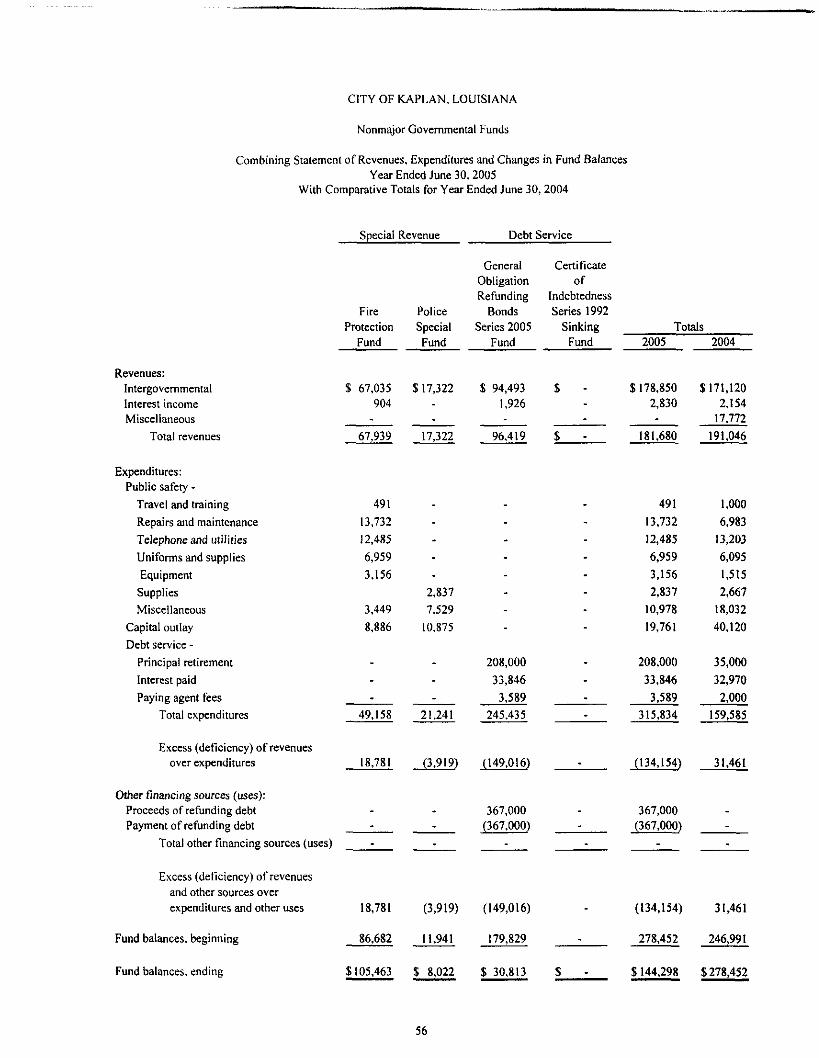

Nonmajor Governmental Funds -Combining balance sheet 55Combining statement of revenues, expenditures, and changes in fund balances 56

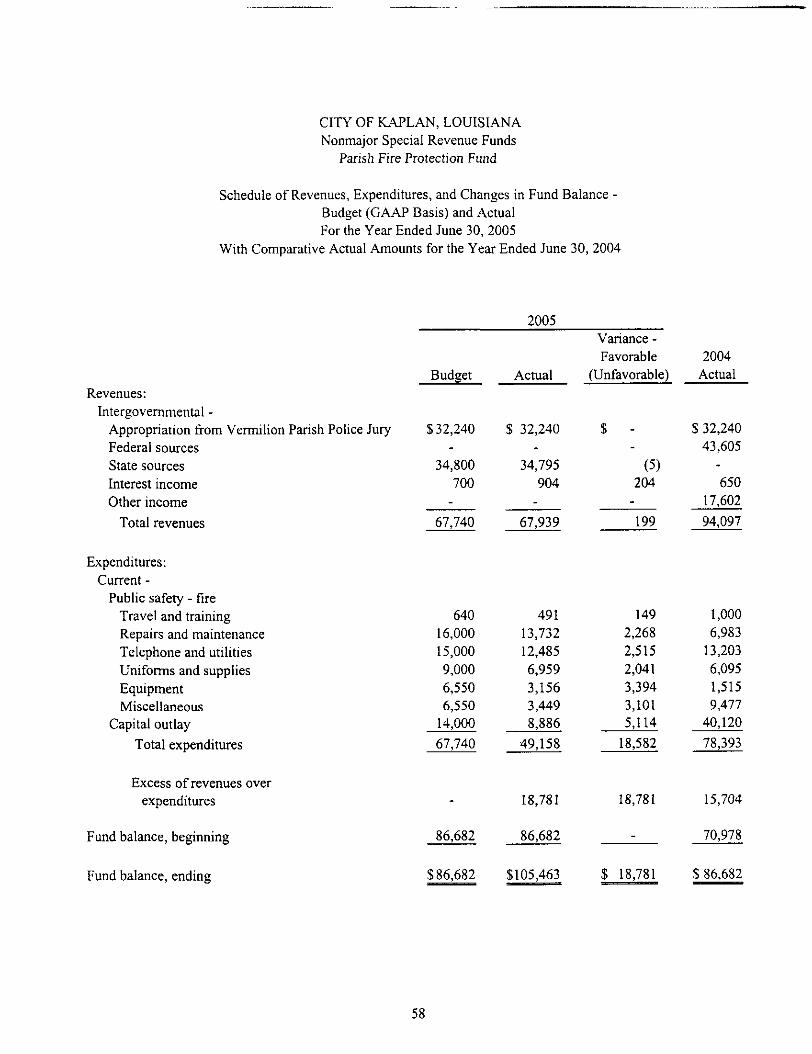

Nonmajor special revenue funds -Parish Fire Protection Fund -

Schedule of revenues, expenditures, and changes in fund balance - budget(GAAP basis) and actual 58

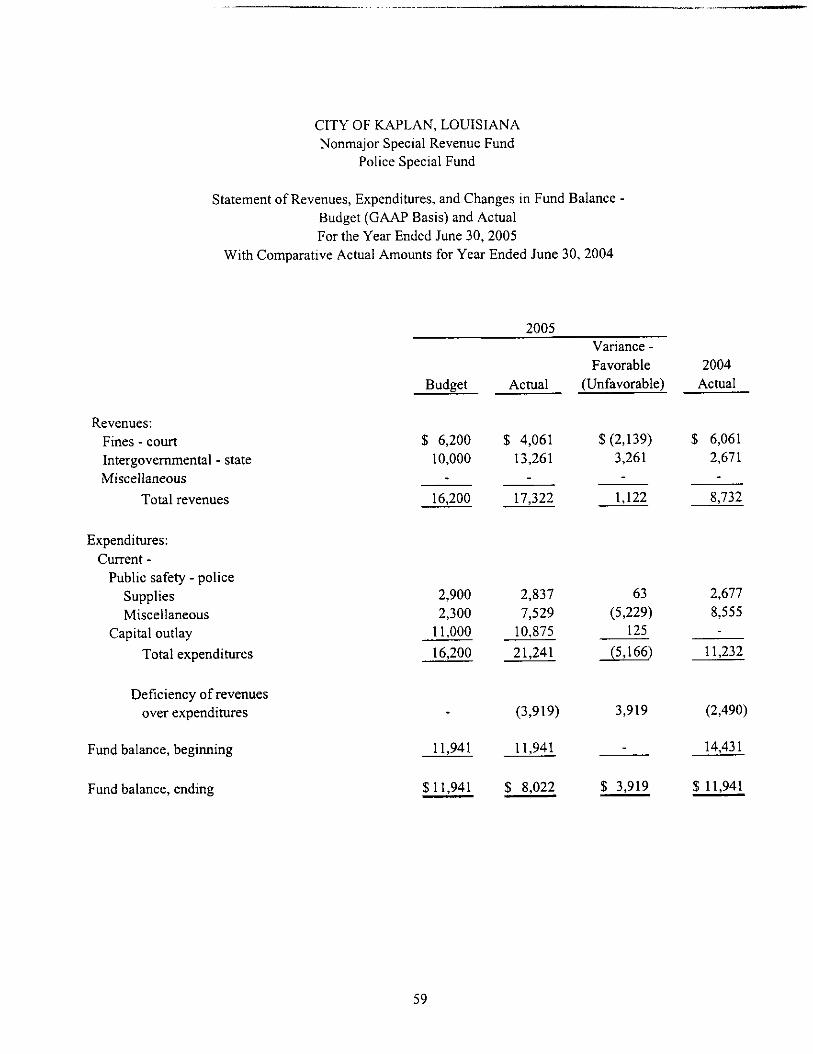

Police Special Fund -Schedule of revenues, expenditures, and changes in fund balance - budget(GAAP basis) and actual 59

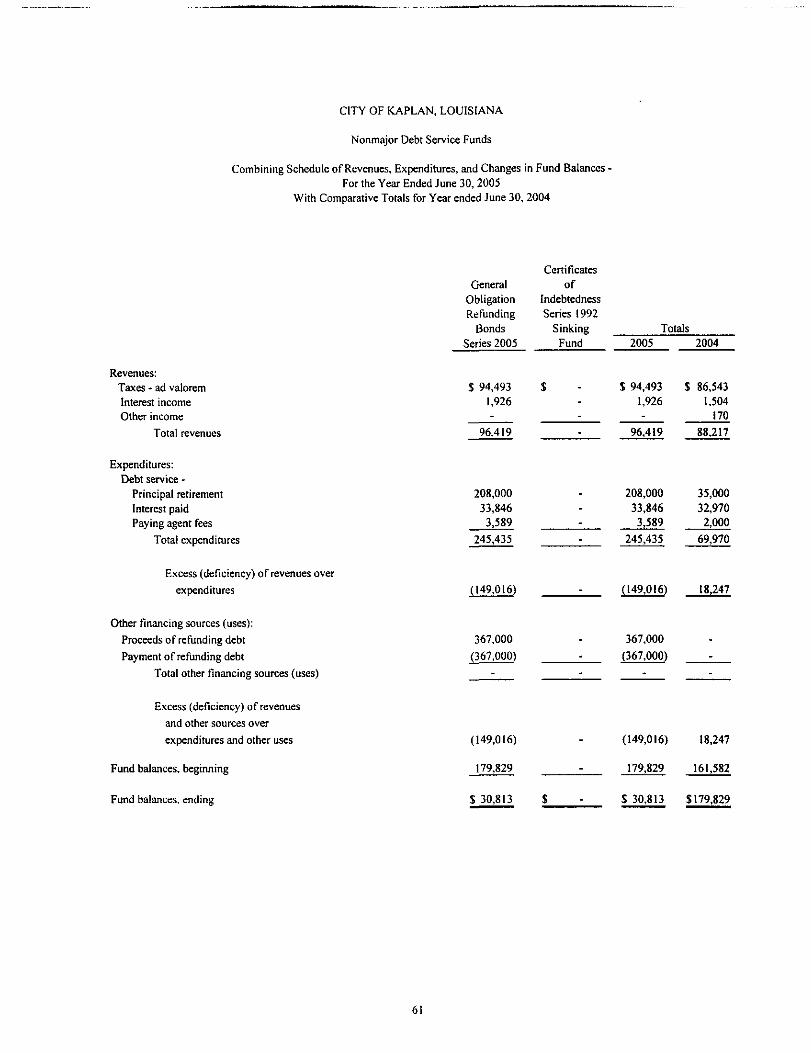

Nonmajor debt service funds -Combining schedule of revenues, expenditures and changes in fund balances 61

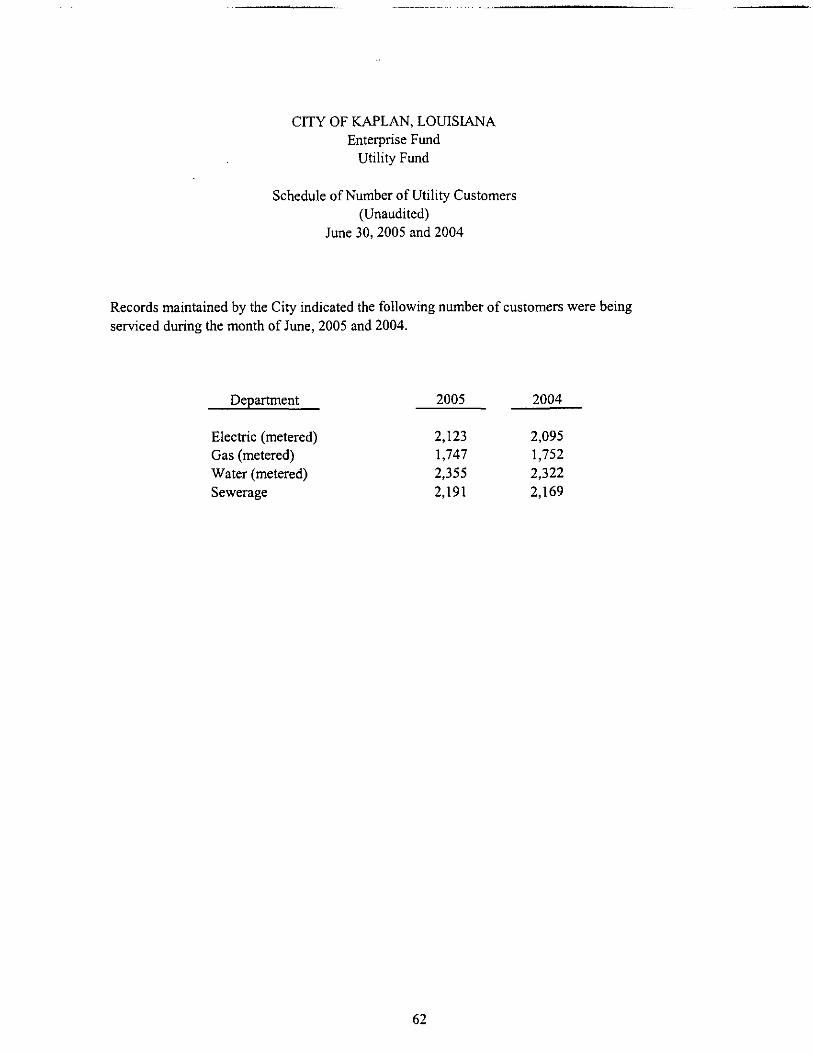

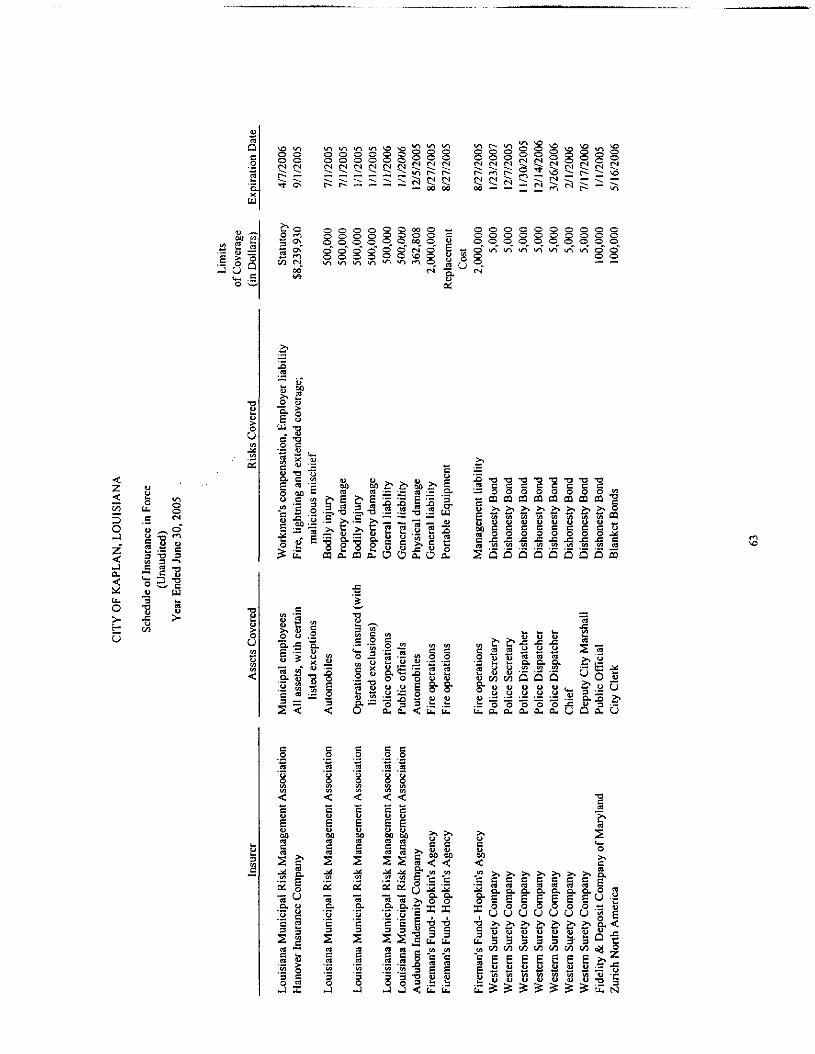

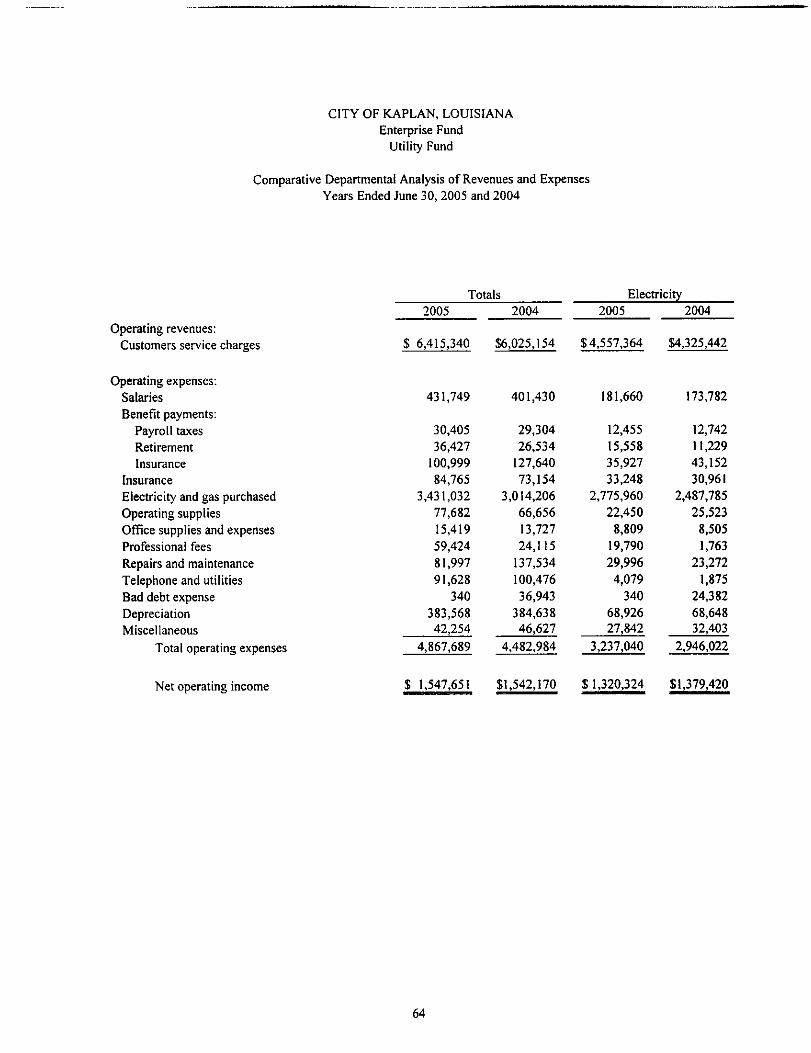

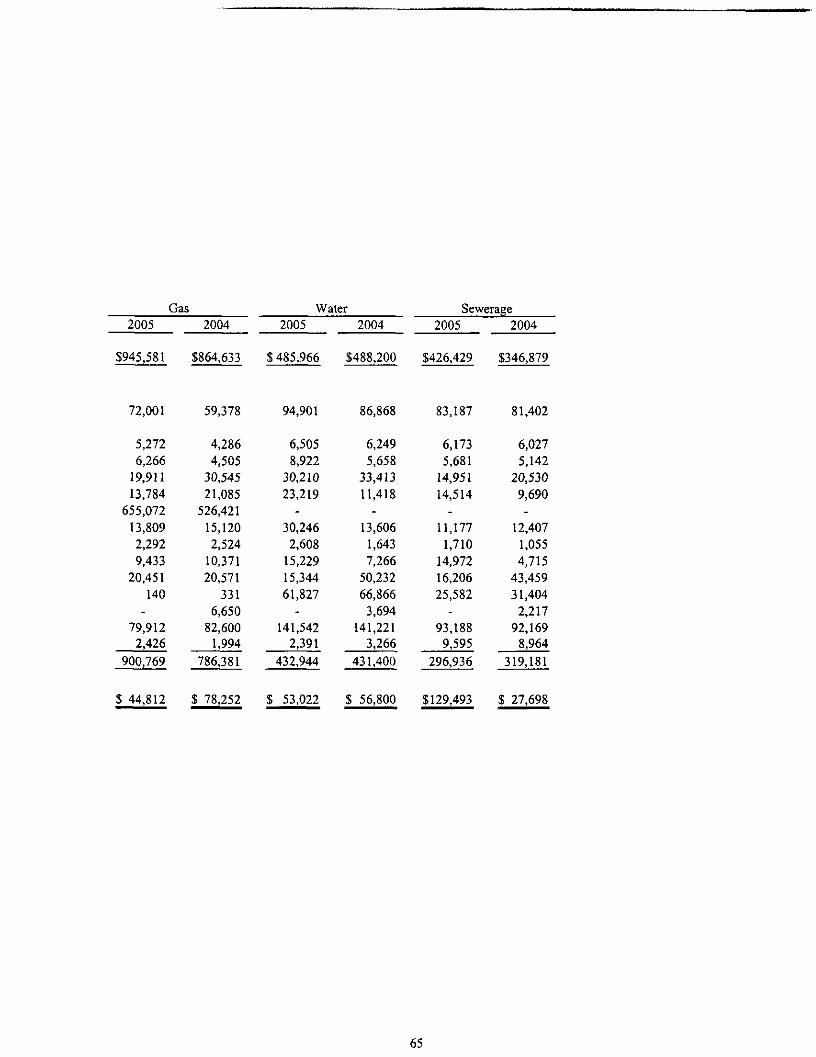

Schedule of number of utility customers (unaudited) 62Schedule of insurance in force (unaudited) 63Comparative departmental analysis of revenues and expenses - utility fund 64-65

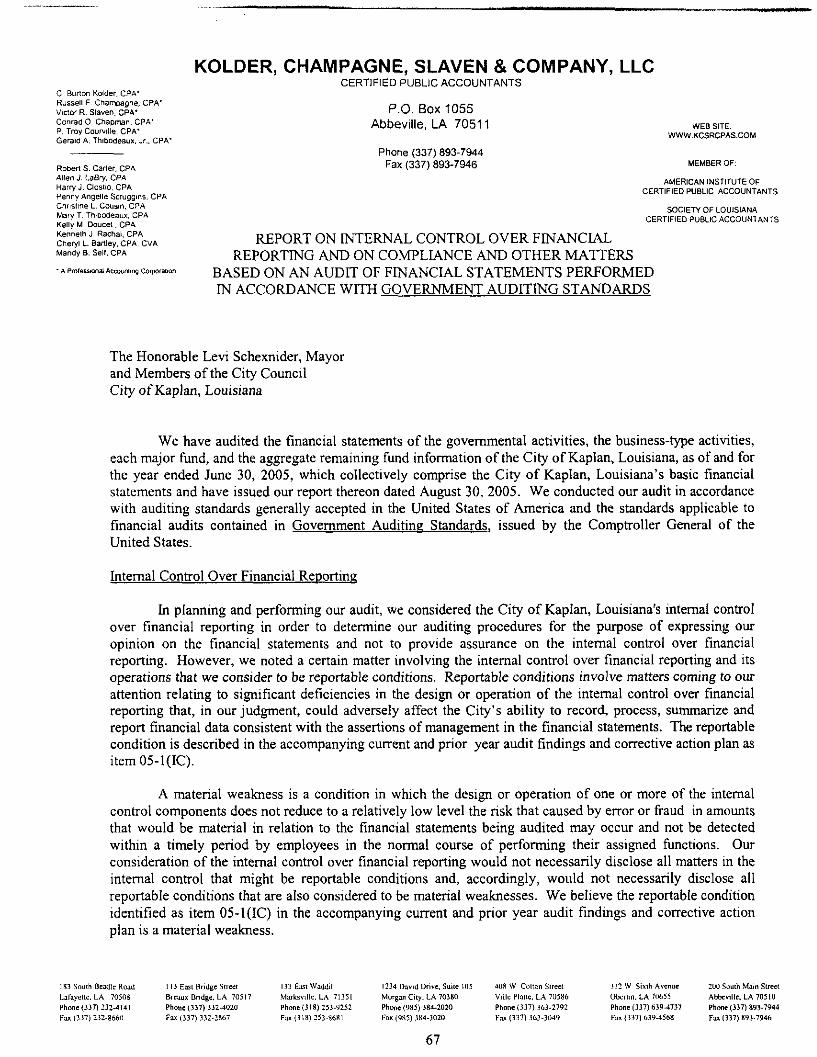

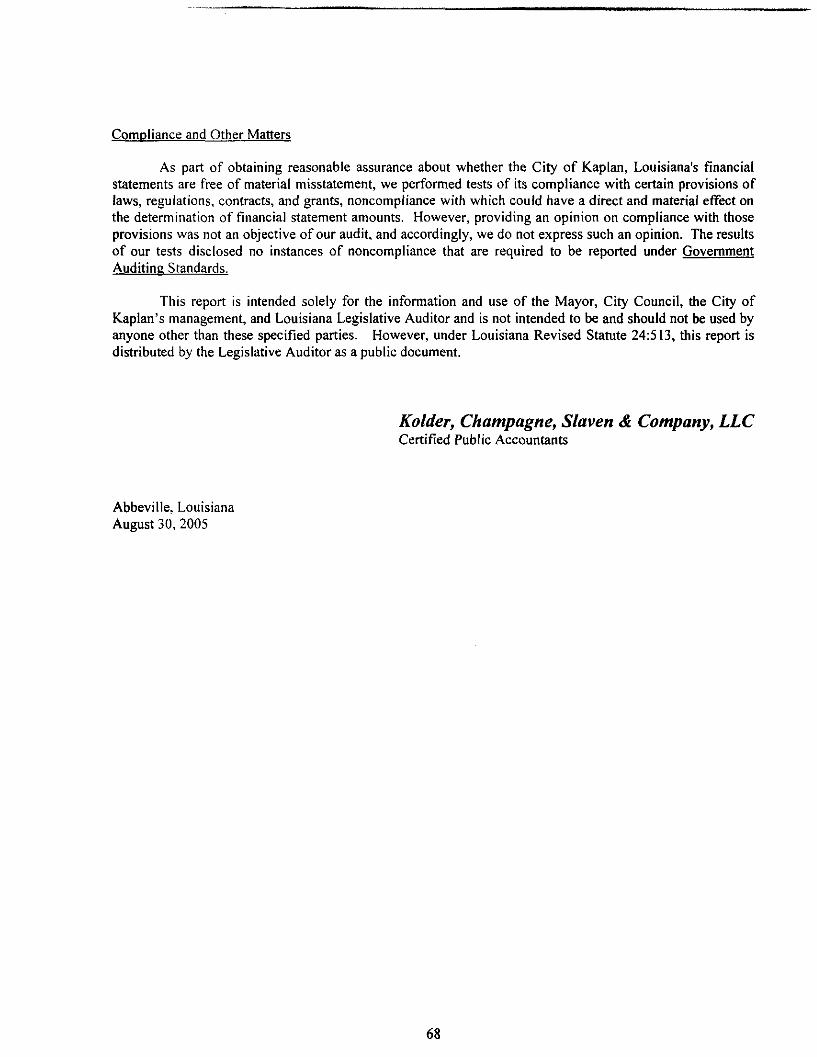

COMPLIANCE, INTERNAL CONTROL AND OTHER GRANT INFORMATIONReport on Internal Control over Financial Reporting

and on Compliance and Other Matters Based onan Audit of Financial Statements Performed inAccordance with Government Auditing Standards 67-68

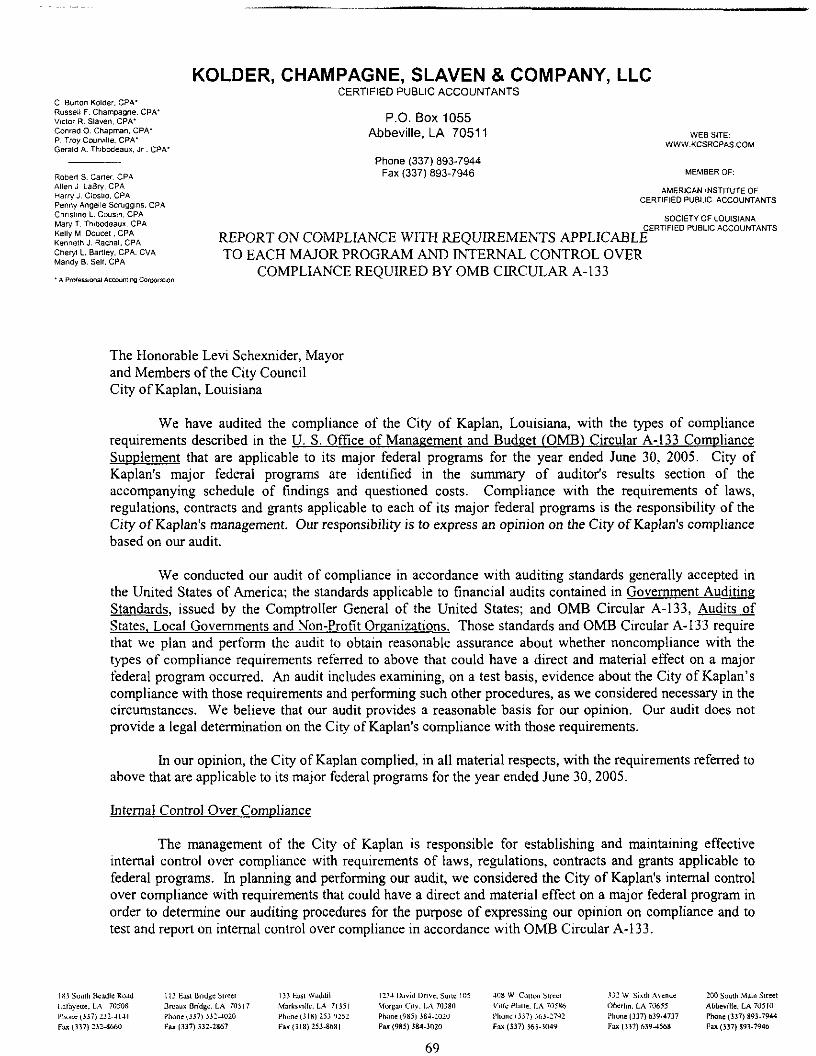

Report on Compliance with Requirements Applicableto Each Major Progam and Internal Control overCompliance Required by OMB Circular A-133 69-70

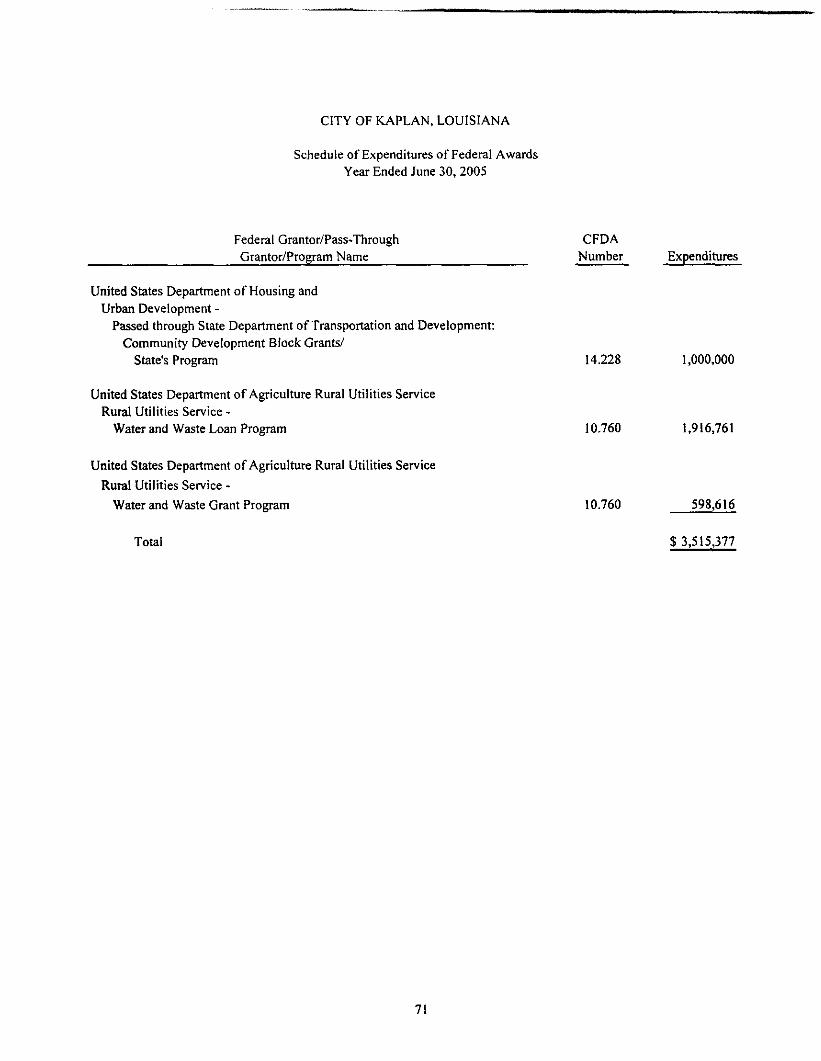

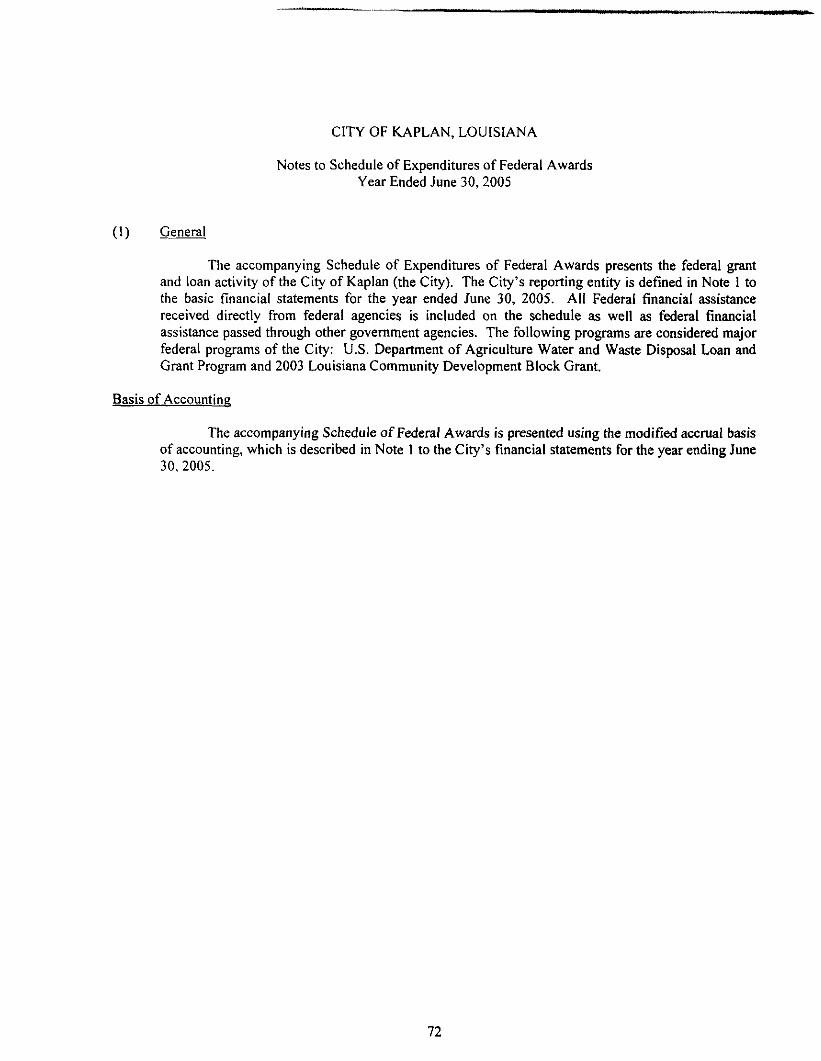

Schedule of Expenditures of Federal Awards 71

Notes to Schedule of Expenditures of Federal Awards 72

Schedule of Findings and Questioned Costs 73-74

Summary schedule of current and prior year audit findingsand corrective action plan 75

KOLDER, CHAMPAGNE, SLAVEN & COMPANY, LLCCERTIFIED PUBLIC ACCOUNTANTS

C. Burton KoWer. CPA'Russell F. Champagne, CPA* D — -j . nccVictorR. Slaven, CPA- r.U. OOX TUOO

Conrad 0. Chapman CPA- Abbeville, LA 70511 WEBSITE:

£' MfcTim. ^ , f-cn. WWW KCSRCPAS.COMGerald A. Trnbodeaux. Jr., CPA'

Phone (337) 893-7944Robert S. Carter. CPA Fax (337) 893-7946 MEMBER OF:

Allen J LaBry. CPA AMERICAN INSTITUTE OF

AOeoer CPA ' CERTIFIED PUBLIC ACCOUNTANTS

Penny Angelle Scruggins. CPA SOQETY OF LOUlslANft

Christine LCoUS1n. CPA CERTIFIED PUBLIC ACCOUNTANTSMary T. Thibodeaux. CPA

L INDEPENDENT AUDITORS' REPORTCheryl L. Sartey. CPA. CVAMandy 8. Self, CPA

• A P'OfBssenaJ Accounling Corporalkxi

The Honorable Levi Schexnider, Mayor,and Members of the City CouncilCity of Kaplan, Louisiana

We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Kaplan,Louisiana, as of and for the year ended June 30, 2005, which collectively comprise the City's basic financialstatements as listed in the table of contents. These financial statements are the responsibility of the City'smanagement. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United Statesof America and the standards applicable to financial audits contained in Government Auditing Standards.issued by the Comptroller General of the United States. Those standards require that we plan and perform theaudit to obtain reasonable assurance about whether the basic financial statements are free of materialmisstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosuresin the basic financial statements. An audit also includes assessing the accounting principles used andsignificant estimates made by management, as well as evaluating the overall financial statement presentation.We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities, the business-type activities, each major fund, andthe aggregate remaining fund information of the City of Kaplan, Louisiana, as of June 30, 2005, and therespective changes in financial position and cash flows, where applicable, thereof for the year then ended inconformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued a report dated August 30,2005, on our consideration of the City of Kaplan, Louisiana's internal control over financial reporting and onour tests of its compliance with certain provisions of laws, regulations, contracts and grants. That report is anintegral part of an audit performed in accordance with Government Auditing Standards and should be read inconjunction with this report in considering the results of our audit.

The required supplementary information on pages 45 and 46 is not a required part of the basicfinancial statements but are supplementary information required by Governmental Accounting StandardsBoard. We have applied certain limited procedures, which consisted principally of inquiries of managementregarding the methods of measurement and presentation of the required supplementary information.However, we did not audit the information and express no opinion on it.

I S3 South Beadle Road H3 East Biidise Street 113 Ea« WwUJil 1134 David Drive. Suitt (OS 4G&W. Cotton Street 332 W.Sklh Avenue 200 South Mun StreetLa&yellc.LA 70508 Breaux Bridge. LA 70517 Mirkwille, LA 71351 Morgan Cily. LA 70380 VilLe Plalte. LA 70586 Oberiin. LA 70655 Abbeville, LA 70510Phone (337) 232-4141 Phone (337) 332-4020 Phnne<318) 253-9252 Phone (985) 384-2020 Phone (337) 363-2792 Phone (337) 639-4737 Phone(>37) 813-7944Fax (337) 232-8660 Fax (337) 332-2867 Fax (318) 253-8681 Fax (985) 384-3020 Fax (337) 363-3049 Fax (337) 639-4568 Fax (337) 893-7946

The City of Kaplan has not presented management's discussion and analysis that the GovernmentalAccounting Standards Board has determined is necessary to supplement, although not required to be part of,the basic financial statements.

Our audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise the City of Kaplan's basic financial statements. The supplementary information onpages 49 through 70 is presented for purposes of additional analysis and is not a required part of the basicfinancial statements. The accompanying schedule of expenditures of federal awards (page 71) is presentedfor purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133,Audits of States. Local Governments, and Non-profit Organizations, and is not a required part of the financialstatements of the City of Kaplan. Such information, except for that portion marked "unaudited" on which weexpress no opinion, has been subjected to the auditing procedures applied in the audit of the basic financialstatements and, in our opinion, is fairly stated in all material respects in relation to the basic financialstatements taken as a whole.

The financial information for the preceding year, which is included for comparative purposes, wastaken from the financial report for that year in which we expressed an unqualified opinion on the basicfinancial statements of the City of Kaplan, Louisiana.

Kolder, Champagne, Slaven & Company, LLCCertified Public Accountants

Abbeville, LouisianaAugust 30, 2005

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDEFINANCIAL STATEMENTS (GWFS)

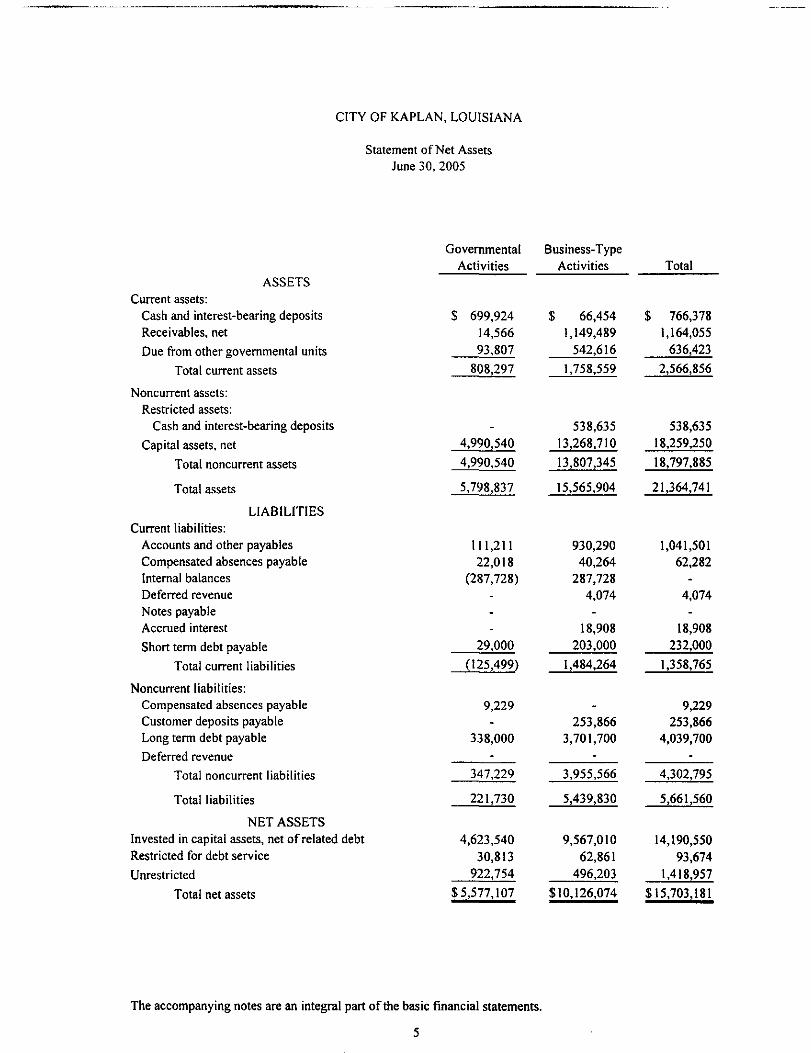

CITY OF KAPLAN, LOUISIANA

Statement of Net AssetsJune 30, 2005

ASSETSCurrent assets:

Cash and interest-bearing depositsReceivables, net

Due from other governmental units

Total current assets

Noncurrent assets:Restricted assets:

Cash and interest-bearing deposits

Capital assets, net

Total noncurrent assets

Total assets

LIABILITIESCurrent liabilities:

Accounts and other payablesCompensated absences payableInternal balancesDeferred revenueNotes payableAccrued interest

Short term debt payable

Total current liabilities

Noncurrent liabilities:Compensated absences payableCustomer deposits payableLong term debt payable

Deferred revenue

Total noncurrent liabilities

Total liabilities

NET ASSETSInvested in capital assets, net of related debtRestricted for debt service

Unrestricted

Total net assets

GovernmentalActivities

$ 699,92414,56693,807

808,297

4,990,540

4,990,540

5,798,837

111,21122,018

(287,728)

29,000

(125,499)

9,229

338,000

347,229

221,730

4,623,54030,813

922,754

$5,577,107

Business-TypeActivities

$ 66,4541,149,489

542,616

1,758,559

538,63513,268,710

13,807,345

15,565,904

930,29040,264

287,7284,074

18,908203,000

1,484,264

253,8663,701,700

3,955,566

5,439,830

9,567,01062,861

496,203

$10,126,074

Total

$ 766,3781,164,055

636,423

2,566,856

538,63518,259,250

18,797,885

21,364,741

1,041,50162,282

4,074

18,908232,000

1,358,765

9,229253,866

4,039,700

4,302,795

5,661,560

14,190,55093,674

1,418,957

$15,703,181

The accompanying notes are an integral part of the basic financial statements.

5

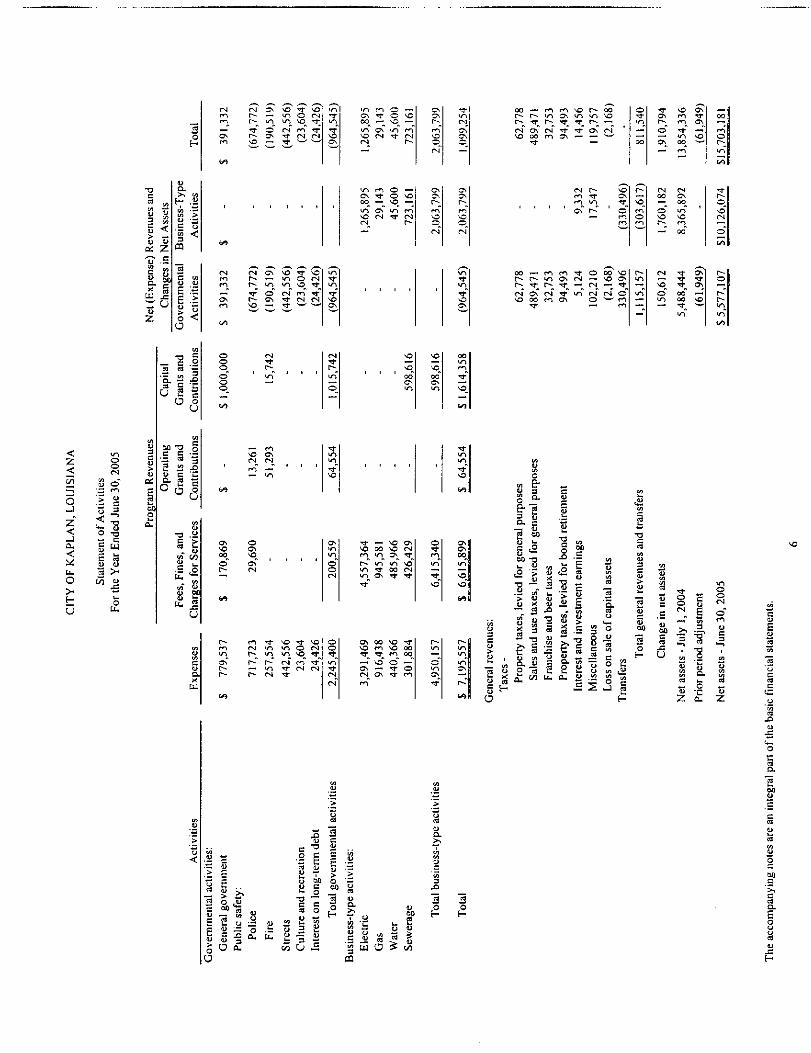

^COt/5

-T

cuuo;

"u"cuO.Xs2

inu

1 1 ^_;; <s u

1 IS gO | 1

O ^ 2)

zf ~a «"|J U— A ^""

CIT

Y O

F K

AP

L/

Sta

tem

ent

oF

or t

he Y

ear

End

in7JUl™

^OZ.5o60

U

—.t=a.U

00

"3QJa.O

d

2oH

Q.>> U)

E— .HVI • —in >= Oin -^3

CQ

3C mu u

o '50 <O

T3 =

1 •=„ 3£• - —

1 1d

V 1s -Brt 3« J=c *c2 |

u

inU

Fee

s, F

ines

, and

Exp

ense

s C

harg

es f

or S

ervi

c

CN fN Cs NO -3" NOro p~- — • in o r*jr*-i r^ in in NO *3*— * *T" o" (N" in" *a^OS P-- OS Tf oJ C^J""" S C. 3^ ~" ^

w

1 1 1 1 1 1

w

(N <N CS NO T M3r-"i P-- — in O (N

Os ("•• OS rf (N (N

O rso •*o" inO —o.

w

NO OS

~~ in

W

Ov O

OO NOo" cs" ' ' ' '

r*- r*"i ^f NO ^f N^m <*J in in O (N

ON r^ r^ fN rn ^f("» — • in rf (N rs

m-Tinrr"^DS-

1

inin

OS

r-i

m"» — »

S-

In

NO

mo"ocs

oo

T**!

i^ ?*) ~ _-O> ^ ^O soOO "-1 SO ^™

in" cs" in" fT\O (N 'T (Nf-j r-— .

in rn O —Os ^ ^^ 1OOO_ — NO^ —in cs in mNO (N ^r OJCN_ r-

—

NO

3

oo"^U-,

. 1 1 .

Tf- — NO OSNO OO NO CNr*^ in os ^p~" in u-T -o"m t oo 01

OS 00 NO -^\O *n NO oo•^- ^- m oo— \o o ^Cs — rf- O

Os^\r*^m"*oo(~-l

CsJ\

r^r*^'Oo.oi

\0

NO

oo"Osm

,

O

in"

r-in

in

•3-in(NoCONo_—

CS

r^m"Oo.(N

in?;o

oom

T"3

V*

inm

^O

^J

in

NO"

r-

m"

p-T

oo — « en m \o r^ oor^ r^ in cs in *n NOr^ ^r r^ "^ ^P P^ ^^01 o\ CN T ^ Os r^i\O oo r*"i os ^™ ~~ ^"^ '

f —

r-) r- NOr*l in T

' ' ' ' os" r-" ' o"— mro

oo — < n f ~ i T t O o o N Or - r ^ i n o s o j — N O O Sr - T r r - T f — (N — f< N O S O t ^ T i n ( N ( N ONO OO ro Oi O ^^ *n

I/>uMo- & -

y = =° - Ii" e s;D. c '«

— 0 ?>

Gen

eral

rev

enue

s:T

axes

-P

rope

rty

taxe

s, l

evie

d fo

r ge

nera

Sal

es a

nd u

se t

axes

, le

vied

for

gF

ranc

hise

and

bee

r ta

xes

Pro

pert

y ta

xes,

lev

ied

for

bond

iIn

tere

st a

nd i

nves

tmen

t ear

ning

sM

isce

llan

eous

Los

s on

sal

e of

cap

ital

ass

ets

Pran

sfer

s

oTfin— r• — •oo

p*~*NO

(--1o

r-m

m

—

in,ui*4C2

Tot

al g

ener

al r

even

ues

and

•*r NO Oscs m ^rc~~ rn cso" T" —— in NOOS_ OO^ --"

— m

fN (Noo cs— _ oo_o" m" 'NO NO

— " oo

CN ^f OS

SO ^ OsO 00 —in oo -o

m"

Cha

nge

in n

et a

sset

s

^et

asse

ts -

Jul

y 1

,20

04

Jrior

per

iod

adju

stm

ent

__

oo•— «m"Or-_in

^

P--o_so"(M

o"(A

r-o

inin

'Jet a

sset

s -

June

30,

200

5

a^2 Z<u L—

g -§U o.

ou po .=a. u.

-gc "a•- £M u% i,u c

Zaus tiE • £u •-> £o —

_ * 5T3 *~ « *>= = o "fl O r°

£ tt

3 S2Z U

5 «

ucOoQ.>,

Bus

ines

s-ty

fE

lect

ric

Gas

Wat

erS

ewer

age

FUND FINANCIAL STATEMENTS (FFS)

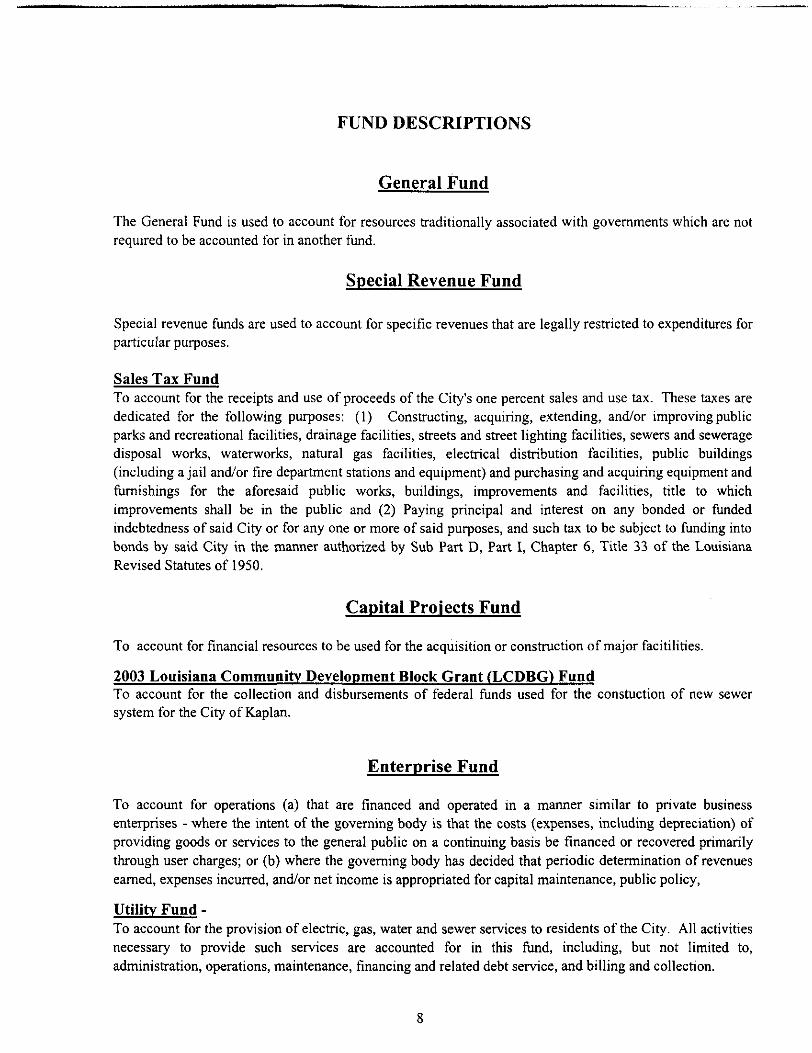

FUND DESCRIPTIONS

General Fund

The General Fund is used to account for resources traditionally associated with governments which are notrequired to be accounted for in another fund.

Special Revenue Fund

Special revenue funds are used to account for specific revenues that are legally restricted to expenditures forparticular purposes.

Sales Tax FundTo account for the receipts and use of proceeds of the City's one percent sales and use tax. These taxes arededicated for the following purposes: (1) Constructing, acquiring, extending, and/or improving publicparks and recreational facilities, drainage facilities, streets and street lighting facilities, sewers and seweragedisposal works, waterworks, natural gas facilities, electrical distribution facilities, public buildings(including a jail and/or fire department stations and equipment) and purchasing and acquiring equipment andfurnishings for the aforesaid public works, buildings, improvements and facilities, title to whichimprovements shall be in the public and (2) Paying principal and interest on any bonded or fundedindebtedness of said City or for any one or more of said purposes, and such tax to be subject to funding intobonds by said City in the manner authorized by Sub Part D, Part I, Chapter 6, Title 33 of the LouisianaRevised Statutes of 1950.

Capital Projects Fund

To account for financial resources to be used for the acquisition or construction of major facitilities.

2003 Louisiana Community Development Block Grant (LCDBG) FundTo account for the collection and disbursements of federal funds used for the constuction of new sewersystem for the City of Kaplan.

Enterprise Fund

To account for operations (a) that are financed and operated in a manner similar to private businessenterprises - where the intent of the governing body is that the costs (expenses, including depreciation) ofproviding goods or services to the general public on a continuing basis be financed or recovered primarilythrough user charges; or (b) where the governing body has decided that periodic determination of revenuesearned, expenses incurred, and/or net income is appropriated for capital maintenance, public policy,

Utility Fund -To account for the provision of electric, gas, water and sewer services to residents of the City. All activitiesnecessary to provide such services are accounted for in this fund, including, but not limited to,administration, operations, maintenance, financing and related debt service, and billing and collection.

o

2 1?r" G

oO

O

oo"CN

Omo\_

•ft/s

oO

o(N

— rs°°- "*.o" c\"

— OO

O\^O>O

O(N

OS ra

g Q(N (J

TOO

o_J

U)•o

*• 3 1/-S8 £ oj= -= °

O>HU

— P5 I

oO

2o

a.EoU

O

r-i r- —

O O\o —

ON•oo

O oom —— . o

o\o"o\6O

^~r-•*,\o"r-

UZ

enH(/I(/I

fflQ

QZ

Q.XV

E a

| IIC £ 01

3O1

-a

COupHj3

i- ^ -— «

o oS E ES S 2f5 ' M fri

"S 3 aH Q Q

u or-! H

o

5 o-o. 1=

S3 S E'I o E— ° '-S

" 0CJ ^^—E -au w c «^" <*• Kfl *^

00

w -a

a. H J2 s; w u To

o u b 3oi u a c3

IX

cD

J3T3C,3

O

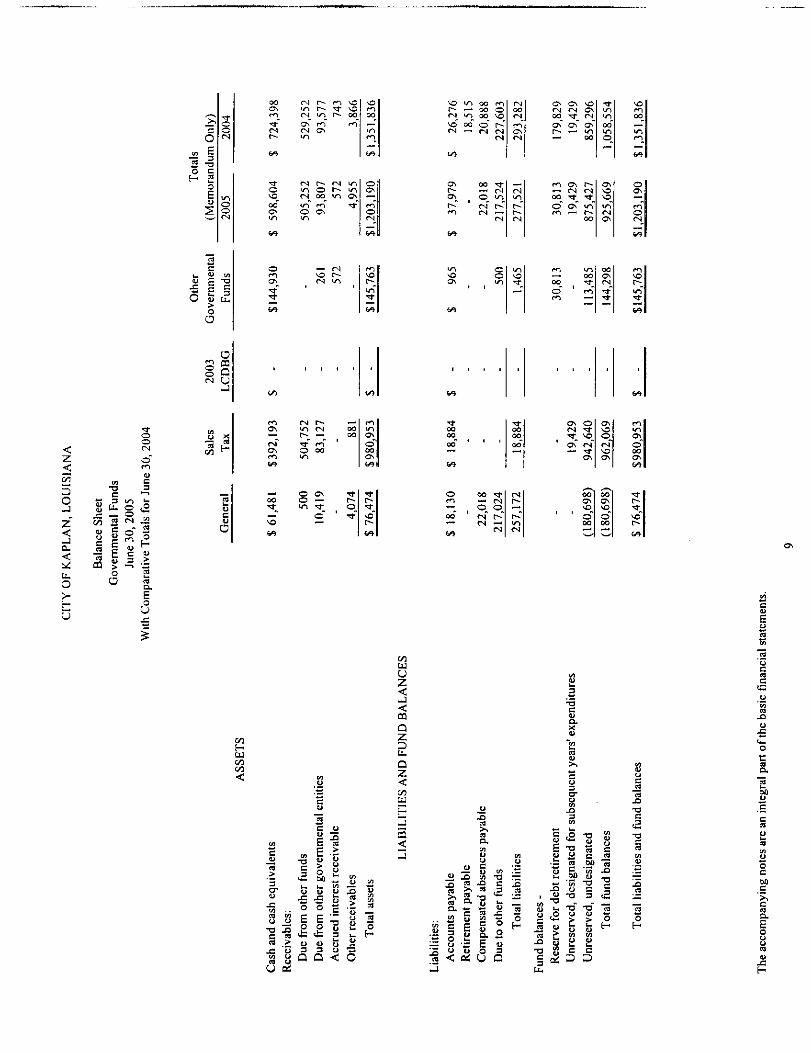

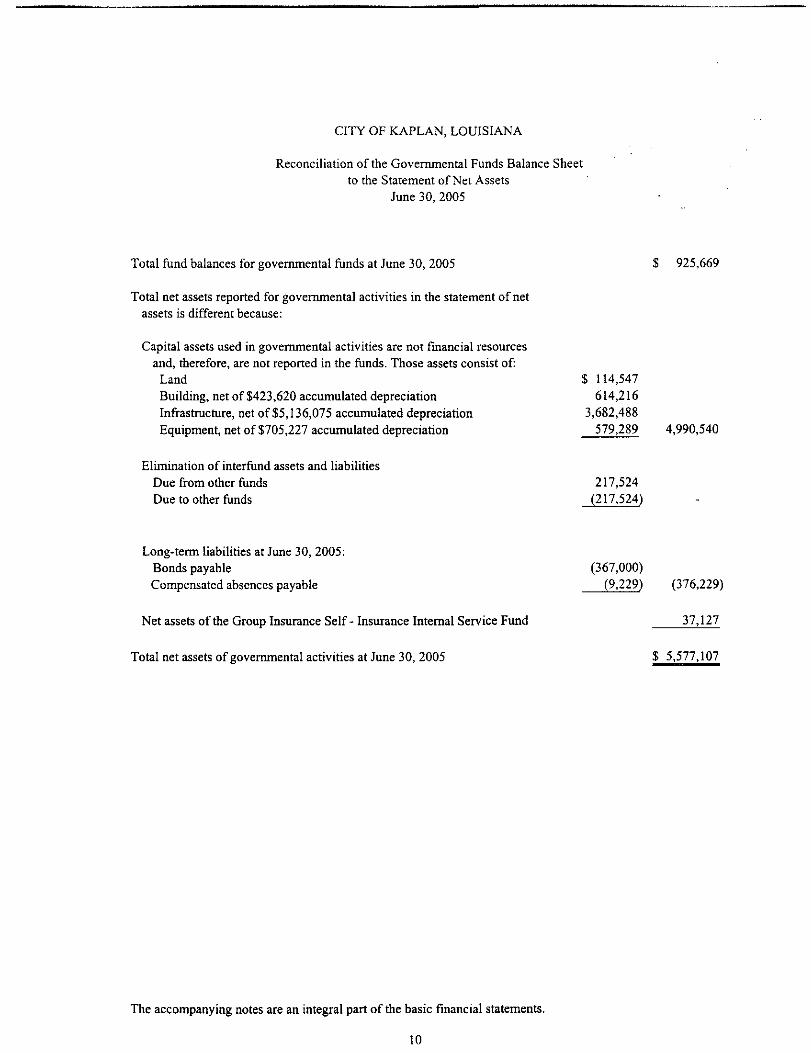

CITY OF KAPLAN, LOUISIANA

Reconciliation of the Governmental Funds Balance Sheetto the Statement of Net Assets

June 30, 2005

Total fund balances for governmental funds at June 30, 2005 $ 925,669

Total net assets reported for governmental activities in the statement of netassets is different because:

Capital assets used in governmental activities are not financial resourcesand, therefore, are not reported in the funds. Those assets consist of:

Land $ 114,547Building, net of $423,620 accumulated depreciation 614,216Infrastructure, net of $5,136,075 accumulated depreciation 3,682,488Equipment, net of $705,227 accumulated depreciation 579,289 4,990,540

Elimination of interfund assets and liabilitiesDue from other funds 217,524Due to other funds (217.524)

Long-term liabilities at June 30, 2005:Bonds payable (367,000)Compensated absences payable (9,229) (376,229)

Net assets of the Group Insurance Self- Insurance Internal Service Fund 37,127

Total net assets of governmental activities at June 30, 2005 $ 5.577,107

The accompanying notes are an integral part of the basic financial statements.

10

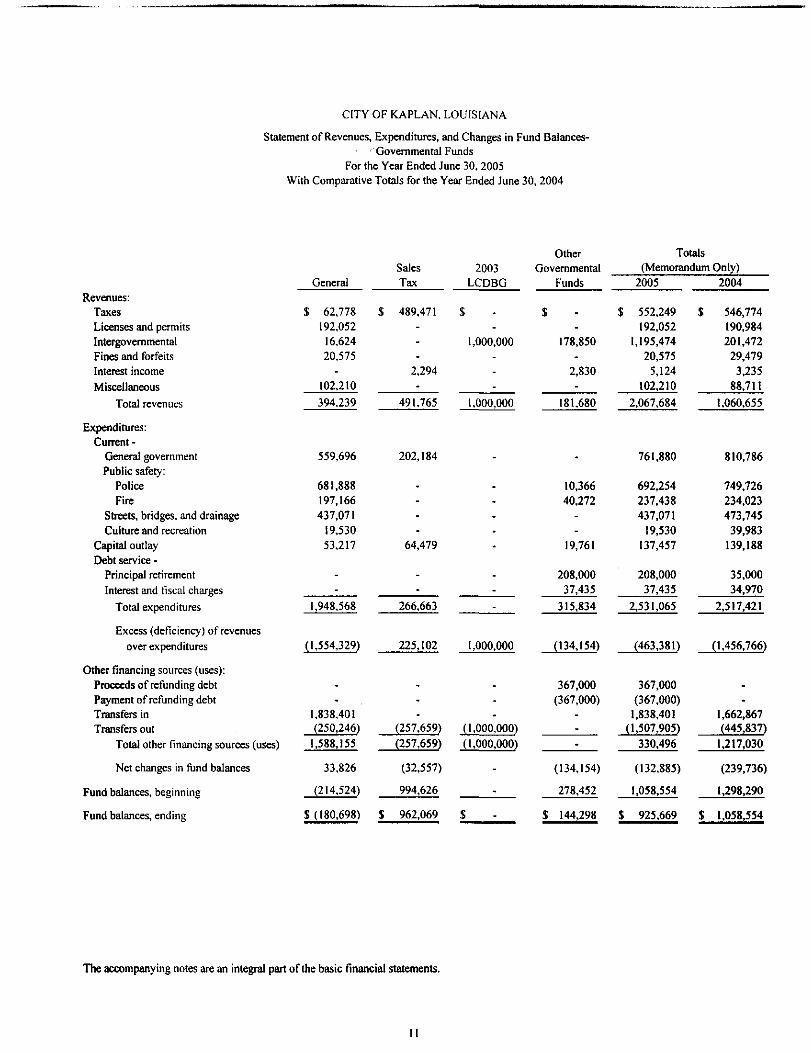

CITY OF KAPLAN, LOUISIANA

Statement of Revenues, Expenditures, and Changes in Fund Balances-Governmental Funds

For the Year Ended June 30, 2005With Comparative Totals for the Year Ended June 30, 2004

Revenues:TaxesLicenses and permitsIntergovernmentalFines and forfeitsInterest incomeMiscellaneous

Total revenues

Expenditures:Current -

General governmentPublic safety:

PoliceFire

Streets, bridges, and drainageCulture and recreation

Capital outlayDebt service -

Principal retirementInterest and fiscal charges

Total expenditures

Excess (deficiency) of revenuesover expenditures

Other financing sources (uses):Proceeds of refunding debtPayment of refunding debtTransfers inTransfers out

Total other financing sources (uses)

Net changes in fund balances

Fund balances, beginning

Fund balances, ending

General

$ 62,778192,052

16,62420.575

-102,210

394.239

559,696

681,888197,166437,071

19,53053,217

.-

1,948,568

(1,554,329)

-1,838,401(250,246)

1,588,155

33,826

(214.524)

$ (180,698)

Sales 2003Tax LCDBG

$ 489,471 $-

1,000,000-

2,294-

491,765 1,000,000

202,184

.---

64,479

--

266,663

225,102 1,000,000

--

(257,659) (1,000,000)(257,659) (1,000,000)

(32,557)

994,626

J 962,069 $

OtherGovernmental

Funds

$-

178,850-

2,830-

181,680

10,36640,272

--

19,761

208,00037,435

315,834

(134,154)

367,000(367,000)

--.

(134,154)

278,452

5 144,298

Totals(Memorandum Only)

2005

$ 552,249192,052

1,195,47420,575

5,124102,210

2,067,684

761,880

692,254237,438437,071

19,530137,457

208,00037,435

2,531,065

(463,381)

367,000(367,000)

1,838,401(1,507,905)

330,496

(132.885)

1,058,554

$ 925,669

2004

$ 546,774190,984201,472

29,4793,235

88,711

1,060,655

810,786

749,726234,023473,74539,983

139,188

35,00034,970

2,517,421

(1,456,766)

-1,662,867(445,837)

1,217,030

(239,736)

1,298,290

$ 1,058,554

The accompanying notes are an integral part of the basic financial statements.

11

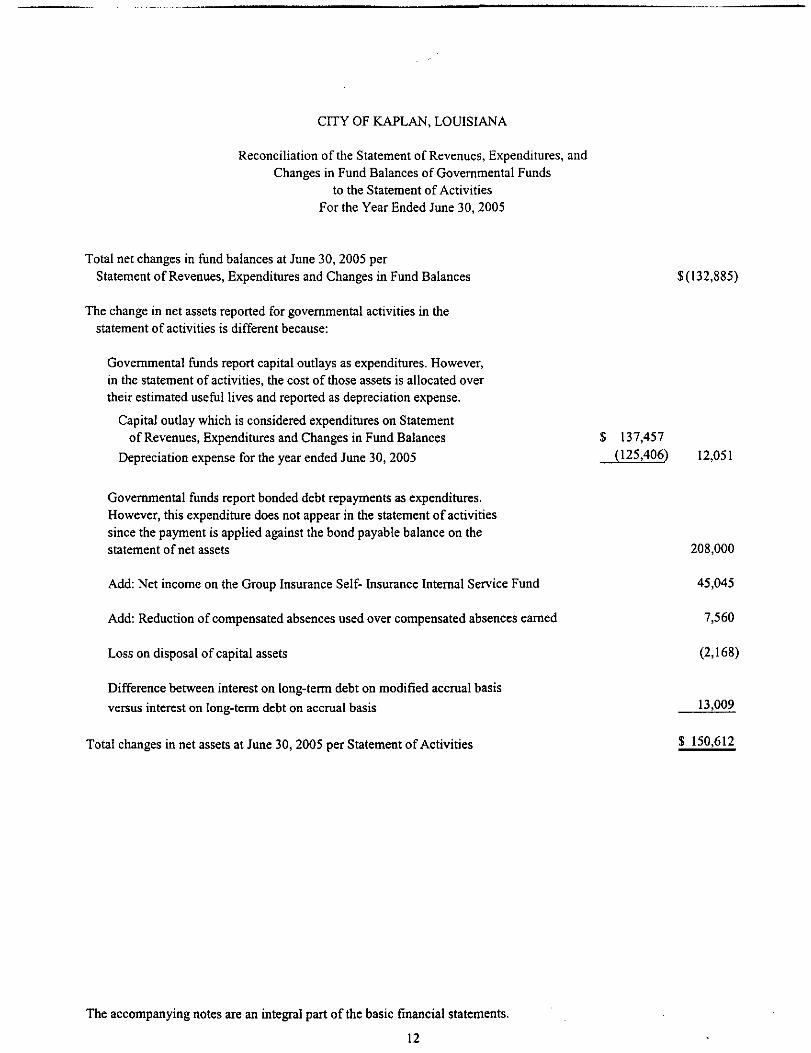

CITY OF KAPLAN, LOUISIANA

Reconciliation of the Statement of Revenues, Expenditures, andChanges in Fund Balances of Governmental Funds

to the Statement of ActivitiesFor the Year Ended June 30, 2005

Total net changes in fund balances at June 30, 2005 perStatement of Revenues, Expenditures and Changes in Fund Balances $(132,885)

The change in net assets reported for governmental activities in thestatement of activities is different because:

Governmental funds report capital outlays as expenditures. However,in the statement of activities, the cost of those assets is allocated overtheir estimated useful lives and reported as depreciation expense.

Capital outlay which is considered expenditures on Statementof Revenues, Expenditures and Changes in Fund Balances $ 137,457

Depreciation expense for the year ended June 30, 2005 (125,406) 12,051

Governmental funds report bonded debt repayments as expenditures.However, this expenditure does not appear in the statement of activitiessince the payment is applied against the bond payable balance on thestatement of net assets 208,000

Add: Net income on the Group Insurance Self- Insurance Internal Service Fund 45,045

Add: Reduction of compensated absences used over compensated absences earned 7,560

Loss on disposal of capital assets (2,168)

Difference between interest on long-term debt on modified accrual basis

versus interest on long-term debt on accrual basis 13,009

Total changes in net assets at June 30, 2005 per Statement of Activities S 150,612

The accompanying notes are an integral part of the basic financial statements.

12

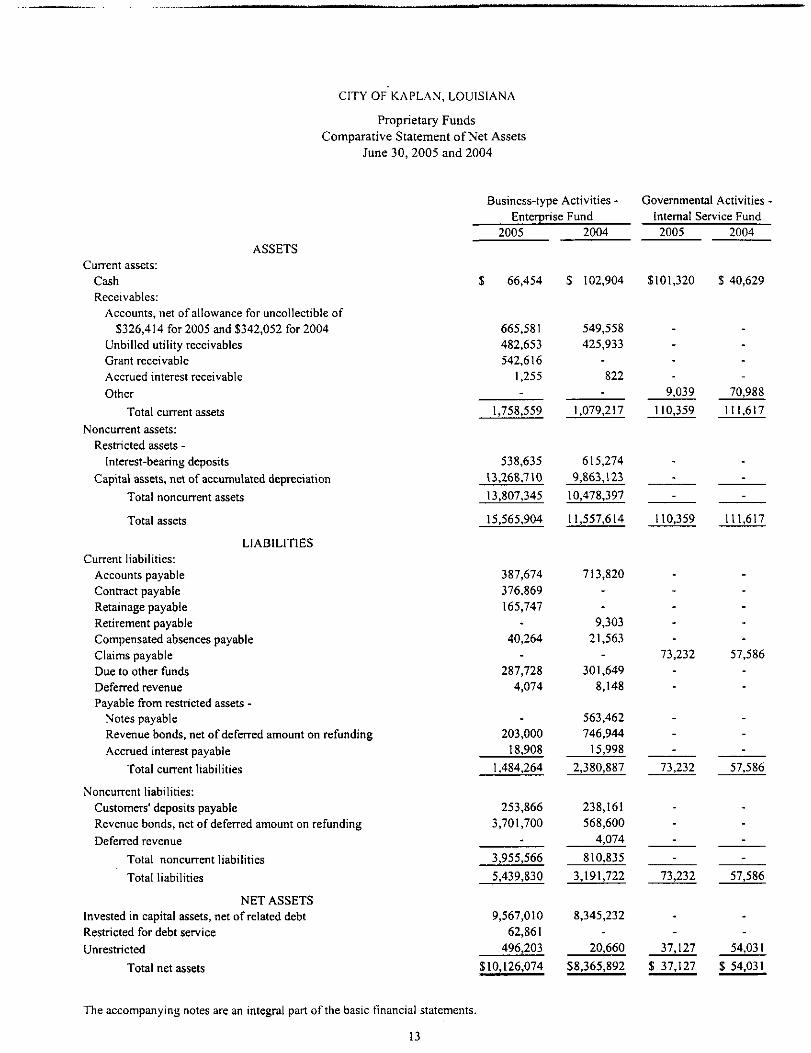

CITY OF KAPLAN, LOUISIANA

Proprietary FundsComparative Statement of Net Assets

June 30, 2005 and 2004

ASSETSCurrent assets:

CashReceivables:

Accounts, net of allowance for uncollectible of5326,414 for 2005 and $342,052 for 2004

Unbilled utility receivablesGrant receivableAccrued interest receivableOther

Total current assetsNoncurrent assets:

Restricted assets -Interest-bearing deposits

Capital assets, net of accumulated depreciation

Total noncurrent assets

Total assets

LIABILITIESCurrent liabilities:

Accounts payableContract payableRetainage payableRetirement payableCompensated absences payableClaims payableDue to other fundsDeferred revenuePayable from restricted assets -

Notes payableRevenue bonds, net of deferred amount on refundingAccrued interest payable

Total current liabilities

Noncurrent liabilities:Customers' deposits payableRevenue bonds, net of deferred amount on refundingDeferred revenue

Total noncurrent liabilities

Total liabilities

NET ASSETSInvested in capital assets, net of related debtRestricted for debt serviceUnrestricted

Total net assets

Business-type Activities -Enterprise Fund

Governmental ActivitiesInternal Service Fund

2005 2004 2005 2004

665,581482,653542,616

1,255

1,758,559

538,63513,268.710

13,807,345

15,565,904

387,674376,869165,747

40,264

287,7284,074

203,00018,908

1,484,264

9,567,01062,861

496,203

66,454 $ 102,904 $101,320 $ 40,629

549,558425,933

822

1,079,217

615,2749,863,123

10,478,397

11,557,614

713,820

9,30321,563

301,6498,148

563,462746,944

15,998

2,380,887

253,866 238,1613,701,700 568,600

- 4,074

3,955,566 810.835

5,439,830 3,191,722

8,345,232

20,660

9,039

110,359

70,988

111,617

110,359 111,617

73,232 57,586

73,232 57,586

73,232

37,127

57,586

54,031

$10,126,074 $8,365,892 $ 37,127 $ 54,031

The accompanying notes are an integral part of the basic financial statements.

13

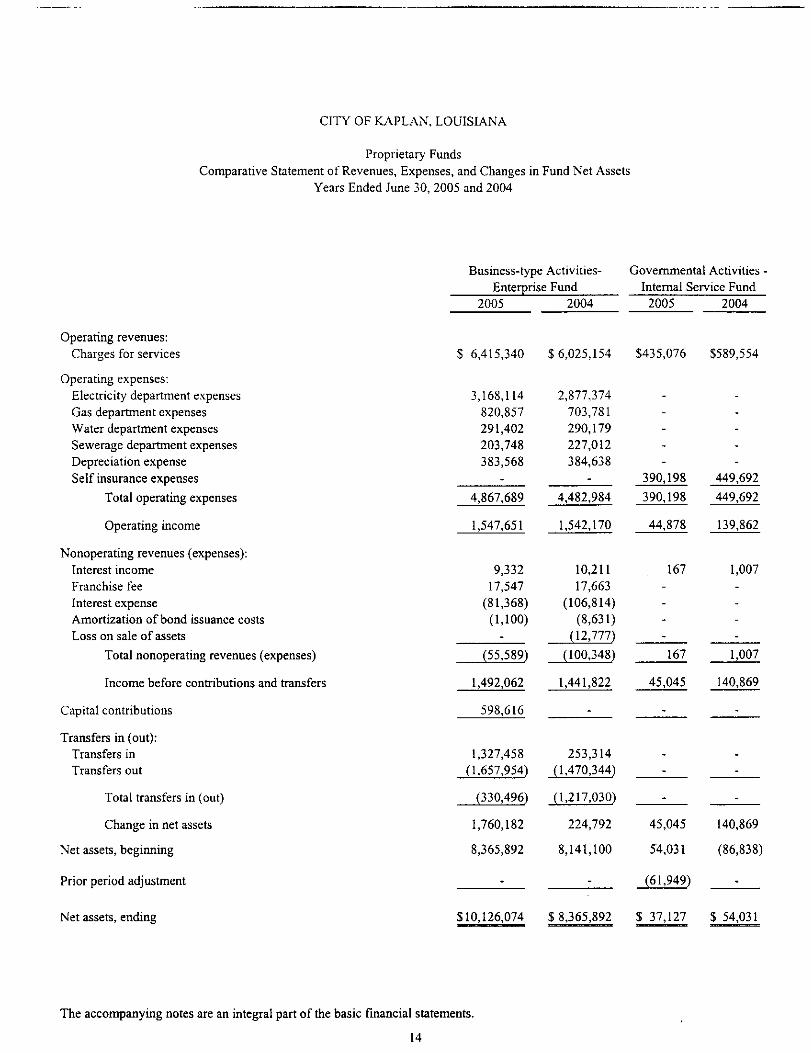

CITY OF KAPLAN, LOUISIANA

Proprietary FundsComparative Statement of Revenues, Expenses, and Changes in Fund Net Assets

Years Ended June 30, 2005 and 2004

Business-type Activities-Enterprise Fund

Governmental ActivitiesInternal Service Fund

Operating revenues:Charges for services

Operating expenses:Electricity department expensesGas department expensesWater department expensesSewerage department expensesDepreciation expenseSelf insurance expenses

Total operating expenses

Operating income

Nonoperating revenues (expenses):Interest incomeFranchise feeInterest expenseAmortization of bond issuance costsLoss on sale of assets

Total nonoperating revenues (expenses)

Income before contributions and transfers

Capital contributions

Transfers in (out):Transfers inTransfers out

Total transfers in (out)

Change in net assets

Net assets, beginning

Prior period adjustment

Net assets, ending

2005

$ 6,415,340

3,168,114820,857291,402203,748383,568

4,867,689

1,547,651

9,33217,547(81,368)(1,100)

(55,589)

1,492,062

2004

$6,025,154

2,877,374703,781290,179227,012384,638

4,482,984

1,542,170

10,21117,663

(106,814)(8,631)(12,777)

(100,348)

1,441,822

2005 2004

$435,076 $589,554

390,198 449,692

390,198 449,692

44,878 139,862

167 1,007

167 1,007

45,045 140,869

598,616

1,327,458(1,657,954)

(330,496)

1,760,182

8,365,892

$10,126,074

253,314(1,470,344)

(1,217,030)

224,792

8,141,100

$ 8,365,892

-

.

45,045 140,869

54,031 (86,838)

(61,949)

$ 37,127 $ 54,031

The accompanying notes are an integral part of the basic financial statements.

14

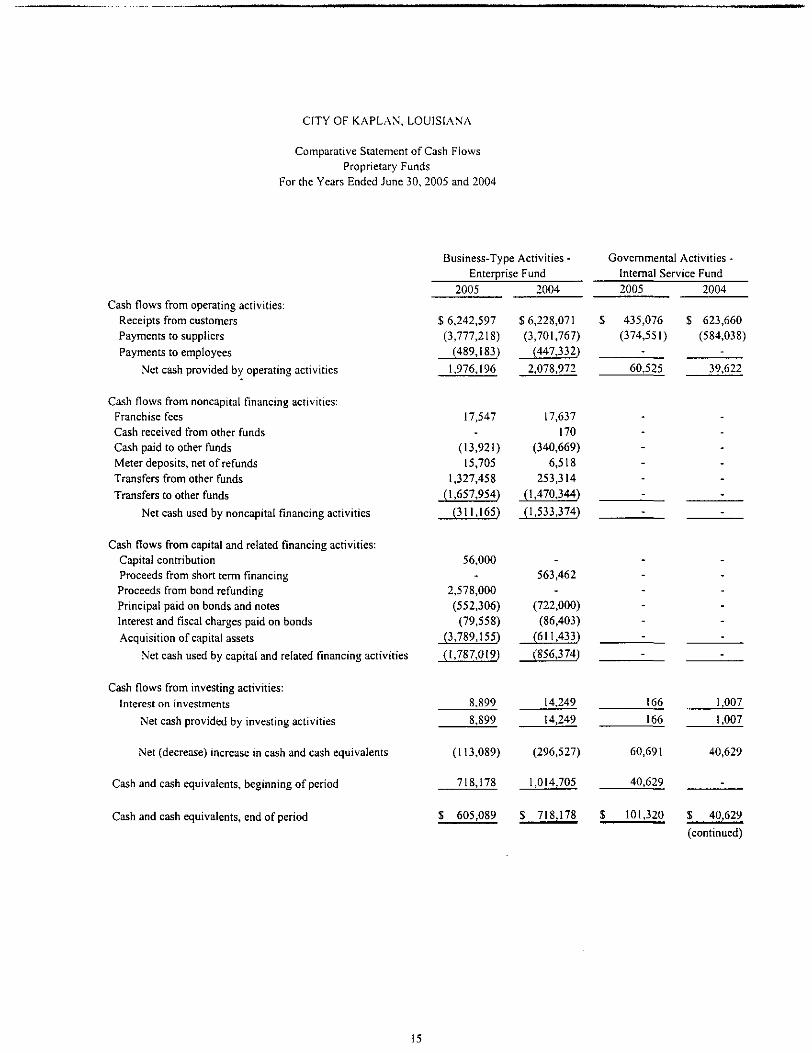

CITY OF KAPLAN, LOUISIANA

Comparative Statement of Cash FiowsProprietary Funds

For the Years Ended June 30, 2005 and 2004

Cash flows from operating activities:Receipts from customersPayments to suppliersPayments to employees

Net cash provided by operating activities

Cash flows from noncapital financing activities:Franchise feesCash received from other fundsCash paid to other fundsMeter deposits, net of refundsTransfers from other fundsTransfers to other funds

Net cash used by noncapital financing activities

Cash flows from capital and related financing activities:Capital contributionProceeds from short term financingProceeds from bond refundingPrincipal paid on bonds and notesInterest and fiscal charges paid on bonds

Acquisition of capital assets

Net cash used by capital and related financing activities

Cash flows from investing activities:Interest on investments

Net cash provided by investing activities

Net (decrease) increase in cash and cash equivalents

Cash and cash equivalents, beginning of period

Cash and cash equivalents, end of period

Business-Type Activities -Enterprise Fund

2005

1,976,196

17,547

(13,921)15,705

1,327,458(1,657,954)

(311,165)

56,000

2,578,000(552,306)

(79,558)(3.789.155)

(1,787,019)

8,899

8,899

(113,089)

718,178

2004

$6,242,597 $6,228,071(3,777,218) (3,701,767)

(489,183) (447,332)

2,078,972

17,637170

(340,669)6,518

253,314(1.470.344)

(1,533,374)

563,462

(722,000)(86,403)

(611.433)

(856,374)

14,249

14,249

(296,527)

1,014,705

Governmental Activities -Internal Service Fund2005

60,525

166

166

60,691

40,629

2004

435,076 $ 623,660(374,551) (584,038)

39,622

1,007

1,007

40,629

$ 605,089 S 718,178 S 101.320 S 40.629

(continued)

15

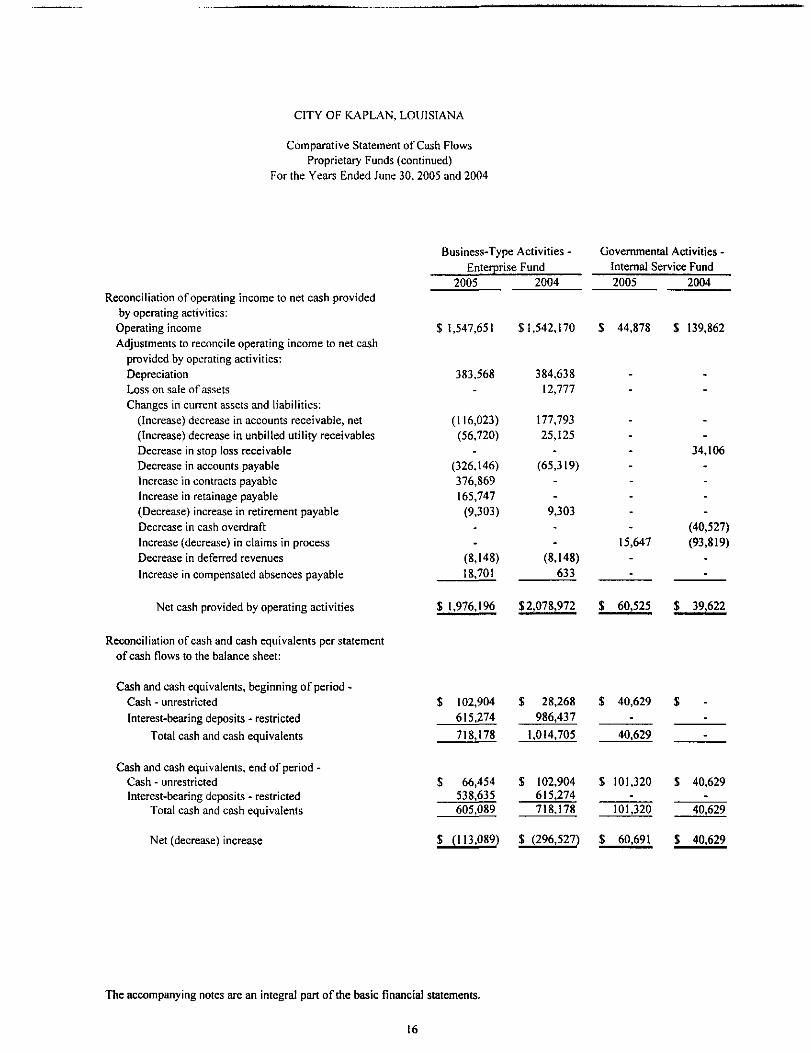

CITY OF KAPLAN, LOUISIANA

Comparative Statement of Cash FlowsProprietary Funds (continued)

For the Years Ended June 30, 2005 and 2004

Reconciliation of operating income to net cash providedby operating activities:

Operating incomeAdjustments to reconcile operating income to net cash

provided by operating activities:DepreciationLoss on sale of assetsChanges in current assets and liabilities:

(Increase) decrease in accounts receivable, net(Increase) decrease in unbilled utility receivablesDecrease in stop loss receivableDecrease in accounts payableIncrease in contracts payableIncrease in retainage payable(Decrease) increase in retirement payableDecrease in cash overdraftIncrease (decrease) in claims in processDecrease in deferred revenuesIncrease in compensated absences payable

Net cash provided by operating activities

Business-Type Activities -Enterprise Fund

Governmental Activities -internal Service Fund

2005

383,568

(116,023)(56,720)

(326,146)376,869165,747

(9,303)

(8,148)18,701

2004 2005

384,63812,777

177,79325,125

(65,319)

9,303

(8,148)633

2004

$1,547,651 $1,542,170 $ 44,878 $139,862

34,106

(40,527)15,647 (93,819)

$ 1,976,196 $2,078,972 $ 60,525 $ 39,622

Reconciliation of cash and cash equivalents per statementof cash flows to the balance sheet:

Cash and cash equivalents, beginning of period -Cash - unrestrictedInterest-bearing deposits - restricted

Total cash and cash equivalents

Cash and cash equivalents, end of period -Cash - unrestrictedInterest-bearing deposits - restricted

Total cash and cash equivalents

Net (decrease) increase

$ 102,904 $ 28,268 $ 40,629 $615,274 986,437 -

718,178

$ 66,454538,635605,089

1,014,705

$ 102,904615,274718,178

40,629

101,320

$ 101,320 $ 40,629

40,629

S (113,089) $ (296,527) $ 60,691 $ 40,629

The accompanying notes are an integral part of the basic financial statements.

16

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements

(1) Summary of Significant Accounting Policies

The accompanying financial statements of the City of Kaplan (the City) have been preparedin conformity with generally accepted accounting principles (GAAP) as applied to governmentalunits. GAAP includes all relevant Governmental Accounting Standards Board (GASB)pronouncements. In the government-wide financial statements and the fund financial statements forthe proprietary funds, Financial Accounting Standards Board (FASB) pronouncements andAccounting Principles Board (APB) opinions on or before November 30, 1989, have been appliedunless those pronouncements conflict with or contradict GASB pronouncements, in which case,GASB prevails. The accounting and reporting framework and the more significant accountingpolicies are discussed in subsequent subsections of this note.

A. Financial Reporting Entity

The City of Kaplan was incorporated in 1902 under the provisions of theLawrason Act. The City operates under a Mayor-City Council form of governmentand provides the following services as authorized by its charter: public safety, police,fire, civil defense, highways and streets, sanitation, culture - recreation, publicimprovements, planning and zoning, and general administrative services.

A financial reporting entity consists of (1) the primary government, (2)organizations for which the primary government is financially accountable, and (3)other organizations for which the primary government is not accountable, but forwhich the nature and significance of their relationship with the primary governmentare such that exclusion would cause the reporting entity's financial statements to bemisleading or incomplete. GASB Statement No. 14, The Financial Reporting Entity.establishes criteria for determining which entities should be considered a componentunit and, as such, part of the reporting entity for financial reporting purposes. Thebasic criteria are as follows:

1. A potential component unit must have separate corporate powers that distinguishit as being legally separate from the primary government. These include theright to incur its own debt, levy its own taxes and charges, expropriate propertyin its own name, sue and be sued in its own name without recourse to a State orlocal government, and the right to buy, sell, lease, and mortgage property in itsown name.

2. The primary government must be financially accountable for a potentialcomponent unit. Financial accountability may exist as a result of the primarygovernment appointing a voting majority of the potential component unit'sgoverning body; their ability to impose their will on the potential component unitby significantly influencing the programs, projects, activities, or level of servicesperformed or provided by the potential component unit; or the existence of afinancial benefit or burden. In addition, financial accountability may also exist asa result of a potential component unit being fiscally dependent on the primarygovernment.

17

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

In some instances, the potential component unit should be included in the reportingentity (even when the criteria in No. 2 above are met), if exclusion would render thereporting entity's financial statements incomplete or misleading.

Based on the foregoing criteria, the following governmental organizations are notconsidered part of the City and are thus excluded from the accompanying financialstatements for the reasons noted:

The Kaplan Housing Authority was chartered by the City, and its Board ofDirectors was appointed by the Mayor and City Council. However, the City'soversight responsibilities in the management of operations and financialaccountability are remote.

The City of Kaplan has no authority over nor is it involved with the recordkeeping of the Kaplan Volunteer Fire Department.

The Kaplan City Court is operated under the directorship of the Kaplan CityJudge who is an elected public official. Revenues are derived from court costsand appropriations from the City's General Fund. However, the City cannotsignificantly influence operations nor does it have responsibility for fiscalmanagement.

B. Basis of Presentation

Government-Wide Financial Statements (GWFS)

The statement of net assets and statement of activities displays informationabout the City of Kaplan, the reporting government, as a whole. They include allfunds of the reporting entity. The statements distinguish between governmental andbusiness-type activities. Governmental activities generally are financed throughtaxes, intergovernmental revenues, and other nonexchange revenues. Business-typeactivities are financed in whole or in part by fees charged to external parties forgoods or services. The City's internal service fund is a governmental activity.Internal service fund activity is eliminated to avoid "doubling up" revenues andexpenses.

The statement of activities presents a comparison between direct expensesand program revenues for the business-type activities of the City and for eachfunction of the City's governmental activities. Direct expenses are those that arespecifically associated with a program or function and therefore, are clearlyidentifiable to a particular function. Program revenues include (a) fees, fines, andcharges paid by the recipients of goods or services offered by the programs, and (b)grants and contributions that are restricted to meeting the operational or capitalrequirements of a particular program. Revenues that are not classified as programrevenues, including all taxes, are presented as general revenues.

18

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Fund Financial Statements

The accounts of the City are organized and operated on the basis of funds. Afund is an independent fiscal and accounting entity with a separate set of self-balancing accounts. Fund accounting segregates funds according to their intendedpurpose and is used to aid management in demonstrating compliance with finance-related legal and contractual provisions. The minimum number of funds ismaintained consistent with legal and managerial requirements. Fund financialstatements report detailed information about the City.

The various funds of the City are classified into two categories:governmental and proprietary. The emphasis on fund financial statements is onmajor governmental and enterprise funds, each displayed in a separate column. Afund is considered major if it is the primary operating fund of the City or meets thefollowing criteria:

a. Total assets, liabilities, revenues or expenditures/expenses of thatindividual governmental or enterprise fund are at least 10 percentof the corresponding total for all funds of that category or type;and

b. Total assets, liabilities, revenues, or expenditures/expenses of theindividual governmental or enterprise fund are at least 5 percentof the corresponding total of all governmental and enterprisefunds combined.

The major funds of the City are described below:

Governmental Funds -

General Fund

The General fund is the general operating fund of the City. It is used toaccount for all financial resources except those required to be accounted for inanother fund. All general tax revenues and other receipts that are not allocated bylaw or contractual agreement to some other fund are accounted for in this fund.General operating expenditures and the capital improvement costs that are not paidthrough other funds are paid from the general fund.

Special Revenue Fund -

Sales Tax Fund

The Sales Tax Fund is used to account for the proceeds of a one percent salesand use tax that is legally restricted to expenditures for a specific purpose.

19

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Capital Projects Fund -

The Capital Projects Fund is used to account for financial resources to beused for the construction of the new sewer plant.

Proprietary Funds -

The City reports the following major enterprise fund:

Utility Fund

The Utility fund is used to account for operations (a) that are financed andoperated in a manner similar to private business enterprises - where the intent of thegoverning body is that the costs (expenses, including depreciation) of providinggoods or services to the general public on a continuing basis be financed or recoveredprimarily through user charges; or (b) where the governing body has decided thatperiodic determination of revenues earned, expenses incurred, and/or net income isappropriate for capital maintenance, public policy, management control,accountability, or other purposes. The City applies all applicable FASBpronouncements issued after November 30, 1989 in accounting and reporting for itsenterprise fund.

Other Fund Types -

The City also reports the following fund types:

Internal Service Funds

Internal service funds are used to account for the financing of goods orservices provided by one department or agency to other departments or agencies ofthe governmental unit, or to other governmental units, on a cost-reimbursement basis.The City's internal service fund is the Self Insurance Fund. This proprietary fund isreported with governmental activities in the government-wide statements.

C. Measurement Focus/Basis of Accounting

Measurement focus is a term used to describe "which" transactions arerecorded within the various financial statements. Basis of accounting refers to"when" transactions are recorded regardless of the measurement focus applied.

Measurement Focus

On the government-wide statement of net assets and the statement ofactivities, both governmental and business-type activities are presented using theeconomic resources measurement focus as defined in item b. below.

tn the fund financial statements, the "current financial resources"measurement focus or the "economic resources" measurement focus is used asappropriate:

20

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

a. All governmental funds utilize a "current financial resources"measurement focus. Only current financial assets and liabilities aregenerally included on their balance sheets. Their operating statementspresent sources and uses of available spendable financial resourcesduring a given period. These funds use fund balance as their measureof available spendable financial resources at the end of the period.

b. The proprietary fund utilizes an "economic resources" measurementfocus. The accounting objectives of this measurement focus are thedetermination of operating income, changes in net assets (or costrecovery), financial position, and cash flows. All assets and liabilities(whether current or noncurrent) associated with their activities arereported. Proprietary fund equity is classified as net assets.

Basis of Accounting

In the government-wide statement of net assets and statement of activities,both governmental and business-type activities are presented using the accrual basisof accounting. Under the accrual basis of accounting, revenues are recognized whenearned and expenses are recorded when the liability is incurred or economic assetused. Revenues, expenses, gains, losses, assets, and liabilities resulting fromexchange and exchange-like transactions are recognized when the exchange takesplace.

Governmental fund financial statements are reported using the currentfinancial resources measurement focus and the modified accrual basis of accounting.Revenues are recognized as soon as they are both measurable and available.Revenues are considered to be available when they are collectible within the currentperiod or soon enough thereafter to pay liabilities of the current period. For thispurpose, the government considers revenues to be available if they are collectedwithin 60 days of the end of the current fiscal period. Expenditures (including capitaloutlay) generally are recorded when a liability is incurred, as under accrualaccounting. However, debt service expenditures are recorded only when payment isdue.

The proprietary fund utilizes the accrual basis of accounting. Under theaccrual basis of accounting, revenues are recognized when earned and expenses arerecorded when the liability is incurred or economic asset is used.

Program revenues

Program revenues included in the statement of activities are derived directlyfrom the program itself or from parties outside the City's taxpayers or citizenry, as awhole; program revenues reduce the cost of the function to be financed from theCity's general revenues.

21

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Allocation of indirect expenses

The City reports all direct expenses by function in the statement of activities.Direct expenses are those that are clearly identifiable with a function. Indirectexpenses of other functions are not allocated to those functions but are reportedseparately in the statement of activities. Depreciation expense is specificallyidentified by function and is included in the direct expense of each function. Intereston general long-term debt is considered an indirect expense and is reported separatelyon the statement of activities.

D. Assets, Liabilities and Equity

Cash, interest-bearing deposits, and investments

For purposes of the statements of net assets, cash and interest-bearingdeposits include all demand accounts, saving accounts, and certificates of deposits ofthe City. For the purpose of the proprietary fund statement of cash flows, "cash andcash equivalents" include all demand and savings accounts, and certificates ofdeposit or short-term investments with an original maturity of three months or lesswhen purchased. See Note (4) for other GASB No. 3 disclosures.

Investments

Under state law, the City may deposit funds with a fiscal agent organizedunder the laws of the State of Louisiana, the laws of any other state in the union, orthe laws of the United States. The City may invest in United States bonds, treasurynotes and bills, government backed agency securities, or certificates and timedeposits of state banks organized under Louisiana Law and national banks havingprincipal offices in Louisiana. In addition, local governments in Louisiana areauthorized to invest in the Louisiana Asset Management Pool (LAMP), a nonprofitcorporation formed by the State Treasurer and organized under the laws of the Stateof Louisiana, which operates a local government investment pool.

Interfund receivables and payables

During the course of operations, numerous transactions occur betweenindividual funds that may result in amounts owed between funds. Those related togoods and services type transactions are classified as "due to and from other funds."Short-term interfund loans are reported as "interfund receivables and payables."Long-term interfund loans (noncurrent portion) are reported as "advances from and toother funds." Interfund receivables and payables between funds within governmentalactivities are eliminated in the statement of net assets.

22

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Receivables

In the government-wide statements, receivables consist of all revenuesearned at year-end and not yet received. Major receivable balances for thegovernmental activities include ad valorem and sales and use taxes. Business-typeactivities report customer's utility service receivables as their major receivables.Uncollectible utility service receivables are recognized as bad debts through theestablishment of an allowance account at the time information becomes availablewhich would indicated the uncollectiblity of the particular receivable. The allowancefor uncollectibles for customers' utility receivables was $482,653 and $425,933 atJune 30, 2005 and 2004; respectively. Unbilled utility service receivable resultingfrom utility services rendered between the date of meter reading and billing and theend of the month are recorded at year-end.

Capital Assets

Capital assets, which include property, plant, equipment, and infrastructureassets, are reported in the applicable governmental or business-type activitiescolumns in the government-wide financial statements. Capital assets are capitalizedat historical cost or estimated cost if historical is not available. Donated assets arerecorded as capital assets at their estimated fair market value at the date of donation.The City maintains a threshold level of $500 or more for capitalizing capital assets.

The costs of normal maintenance and repairs that do not add to the value ofthe asset or materially extend assets lives are not capitalized. Prior to July 1, 2001,governmental funds' infrastructure assets were not capitalized. These assets havebeen valued at estimated historical cost.

Depreciation of all exhaustible capital assets is recorded as an allocatedexpense in the statement of activities, with accumulated depreciation reflected in thestatement of net assets. Depreciation is provided over the assets' estimated usefullives using the straight-line method of depreciation. The range of estimated usefullives by type of asset is as follows:

Buildings 40 yearsEquipment 5-30 yearsUtility system and improvements 25 yearsInfrastructure 20-50 years

In the fund financial statements, capital assets used in governmental fundoperations are accounted for as capital outlay expenditures of the governmental fundupon acquisition. Capital assets used in proprietary fund operations are accounted forthe same as in the government-wide statements.

23

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Compensated Absences

It is the City's policy to permit employees to accumulate earned but unusedvacation and sick leave benefits. Sick leave vest only upon retirement, therefore anaccrual is made only when an employee is eligible for retirement. Amounts areaccrued when incurred in proprietary funds and reported as a fund liability. Amountsthat are expected to be liquidated with expendable available financial resources isreported as expenditure and a fund liability of the governmental fund that will pay it.

Restricted Assets

Restricted assets include cash and interest-bearing deposits of the proprietaryfund that are legally restricted as to their use. The restricted assets are related to therevenue bond accounts and utility meter deposits.

Long-term debt

The accounting treatment of long-term debt depends on whether the assetsare used in governmental fund operations or proprietary fund operations and whetherthey are reported in the government-wide or fund financial statements.

All long-term debt to be repaid from governmental and business-typeresources are reported as liabilities in the government-wide statements. The long-term debt consists primarily of the revenue bonds payable and utility meter depositspayable.

Long-term debt for governmental funds is not reported as liabilities in thefund financial statements. The debt proceeds are reported as other financing sourcesand payment of principal and interest reported as expenditures. The accounting forproprietary fund long-term debt is the same in the fund statements as it is in thegovernment-wide statements.

Equity Classification

In the government-wide statements, equity is classified as net assets anddisplayed in three components:

Invested in capital assets, net of related debt - Consists of capital assetsincluding restricted capital assets, net of accumulated depreciationand reduced by the outstanding balances of any bonds, mortgages,notes, or other borrowings that are attributable to the acquisition,construction, or improvement of those assets.

Restricted net assets - Consists of net assets with constraints placed onthe use either by (I) external groups such as creditors, grantors,contributors, or laws or regulations of other governments; or (2) lawthrough constitutional provisions or enabling legislation.

24

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Unrestricted net assets - All other net assets that do not meet thedefinition of "restricted" or "invested in capital assets, net of relateddebt."

In the fund statements, governmental fund equity is classified as fundbalance. Fund balance is further classified as reserved and unreserved, withunreserved further split between designated and undesignated. Proprietary fundequity is classified the same as in the government-wide statements.

E. Revenues, Expenditures, and Expenses

Operating Revenues and Expenses

Operating revenues and expenses for proprietary funds are those that resultfrom providing services and producing and delivering goods and/or services. It alsoincludes all revenue and expenses not related to capital and related financing,noncapital financing, or investing activities.

Expenditures/Expenses

In the government-wide financial statements, expenses are classified byfunction for both governmental and business-type activities.

In the fund financial statements, expenditures are classified as follows:

Governmental Funds - By CharacterProprietary Fund - By Operating and Nonoperating

In the fund financial statements, governmental funds report expenditures offinancial resources. Proprietary funds report expenses relating to use of economicresources.

Interfund Transfers

Permanent reallocations of resources between funds of the reporting entityare classified as interfund transfers. For the purposes of the statement of activities,all interfund transfers between individual governmental funds have been eliminated.

F. Revenue Restrictions

The City has various restrictions placed over certain revenue sources fromstate or local requirements. The primary restricted revenue sources include:

Revenue Source Legal Restrictions of Use

Sales tax See Note 3Electricity, gas, water and sewer revenue Debt service and utility operations

25

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

The City uses unrestricted resources only when restricted resources are fullydepleted.

G. Budgets and Budgetary Accounting

The City follows these procedures in establishing the budgetary datareflected in the financial statements:

1. The City Clerk prepares a proposed budget for the fiscal year andsubmits it to the Mayor and Council no later than fifteen days priorto the beginning of each fiscal year.

2. A summary of the proposed budget is published and the public isnotified that the proposed budget is available for public inspection.At the same time, a public hearing is called.

3. A public hearing is held on the proposed budget at least ten daysafter publication of the call for the hearing.

4. After the holding of the public hearing and completion of all actionnecessary to finalize and implement the budget, the budget isadopted through passage of a resolution prior to the commencementof the fiscal year for which the budget is being adopted.

5. Budgetary amendments involving the transfer of funds from onedepartment, program or function to another or involving increases inexpenditures resulting from revenues exceeding amounts estimatedrequire the approval of the Council.

6. All budgetary appropriations lapse at the end of each fiscal year.

7. Budgets for all funds are adopted on a basis consistent with generallyaccepted accounting principles (GAAP). Budgeted amounts are asoriginally adopted or as finally amended by the Council.

H. Use of Estimates

The preparation of financial statements in conformity with generallyaccepted accounting principles requires management to make estimates andassumptions that affect the reported amounts of assets and liabilities and disclosure ofcontingent assets and liabilities at the date of the financial statements and the reportedamounts of revenues and expenditures during the reported period. Actual resultscould differ from those estimates.

I. Report Classification

Certain previously reported amounts for the year ended June 30, 2004 havebeen reclassified to conform to the June 30, 2005 classifications.

26

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

(2) Ad^y_al_grem Taxes

Ad valorem taxes attach as an enforceable lien on property as of January 1 of each year.Taxes are levied by the City on September 1 and are actually billed to taxpayers in November. Thetaxes are generally collected in December of the current year and January and February of thesubsequent year. Property tax revenues are recognized when levied to the extent that they result incurrent receivables.

For the years ended June 30, 2005, and 2004, taxes of 10.31 mills were levied on propertywith assessed valuations totaling $15,289,730 and $14,517,550 and were dedicated as follows:

General corporate purposes 4.20 millsBond indebtedness 6.11 mills

Total 10.31 mills

Total taxes levied at June 30, 2005 and 2004 were $157,271 and $148,661, respectively.There were no ad valorem taxes receivable at June 30, 2005 and 2004.

(3) Dedication of Proceeds and Flow of Funds - Sales and Use Tax Levies

Proceeds of the one percent sales and use tax levied by the City (2005 collections$489,471; 2004 $485,735) are dedicated to the following purposes:

1. Constructing, acquiring, extending, and/or improving public parks andrecreational facilities, drainage facilities, streets and street lighting facilities,sewers and sewerage disposal works, waterworks, natural gas facilities,electrical distribution facilities, public buildings (including a jail and/or firedepartment stations and equipment) and purchasing and acquiring equipmentand furnishings for the aforesaid public works, buildings, improvements andfacilities, title to which improvements shall be in the public.

2. Paying principal and interest on any bonded or funded indebtedness of saidCity or for any one or more of said purposes, and such tax to be subject tofunding into bonds by said City in the manner authorized by Sub Part D, PartI, Chapter 6, Title 33 of the Louisiana Revised Statutes of 1950.

Proceeds of the sales and use tax have been pledged and dedicated to the retirement ofRefunding Certificates of Indebtedness, Series 2002, dated December 2, 2002.

27

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

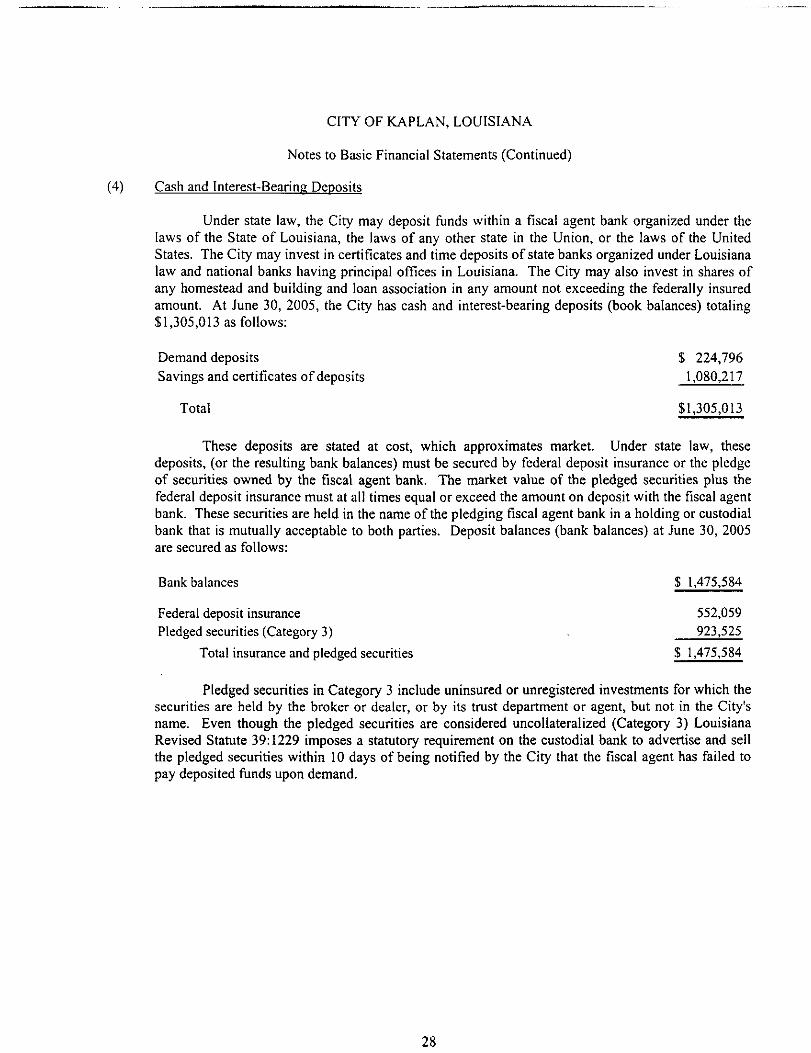

(4) Cash and Interest-Bearing Deposits

Under state law, the City may deposit funds within a fiscal agent bank organized under thelaws of the State of Louisiana, the laws of any other state in the Union, or the laws of the UnitedStates. The City may invest in certificates and time deposits of state banks organized under Louisianalaw and national banks having principal offices in Louisiana. The City may also invest in shares ofany homestead and building and loan association in any amount not exceeding the federally insuredamount. At June 30, 2005, the City has cash and interest-bearing deposits (book balances) totaling$1,305,013 as follows:

Demand deposits $ 224,796Savings and certificates of deposits 1,080,217

Total $1,305,013

These deposits are stated at cost, which approximates market. Under state law, thesedeposits, (or the resulting bank balances) must be secured by federal deposit insurance or the pledgeof securities owned by the fiscal agent bank. The market value of the pledged securities plus thefederal deposit insurance must at all times equal or exceed the amount on deposit with the fiscal agentbank. These securities are held in the name of the pledging fiscal agent bank in a holding or custodialbank that is mutually acceptable to both parties. Deposit balances (bank balances) at June 30, 2005are secured as follows:

Bank balances $ 1,475,584

Federal deposit insurance 552,059Pledged securities (Category 3) , 923,525

Total insurance and pledged securities $ 1,475,584

Pledged securities in Category 3 include uninsured or unregistered investments for which thesecurities are held by the broker or dealer, or by its trust department or agent, but not in the City'sname. Even though the pledged securities are considered unco 1 lateralized (Category 3) LouisianaRevised Statute 39:1229 imposes a statutory requirement on the custodial bank to advertise and sellthe pledged securities within 10 days of being notified by the City that the fiscal agent has failed topay deposited funds upon demand.

28

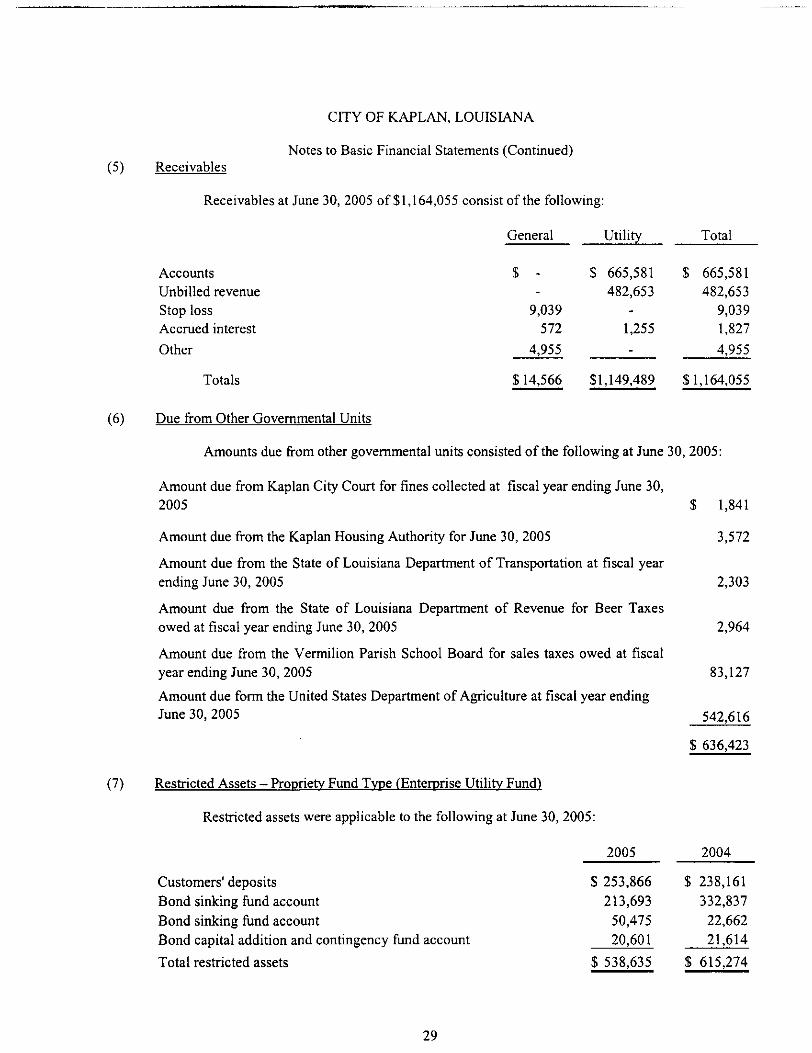

$ --9,039572

4,955

$ 14,566

$ 665,581482,653

-1,255-

$1,149,489

$ 665,581482,6539,0391,827

4,955

$1,164,055

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)(5) Receivables

Receivables at June 30, 2005 of $1,164,055 consist of the following:

General Utility Total

AccountsUnbilled revenueStop lossAccrued interest

Other

Totals

(6) Due from Other Governmental Units

Amounts due from other governmental units consisted of the following at June 30, 2005:

Amount due from Kaplan City Court for fines collected at fiscal year ending June 30,2005 $ 1,841

Amount due from the Kaplan Housing Authority for June 30, 2005 3,572

Amount due from the State of Louisiana Department of Transportation at fiscal yearending June 30, 2005 2,303

Amount due from the State of Louisiana Department of Revenue for Beer Taxesowed at fiscal year ending June 30, 2005 2,964

Amount due from the Vermilion Parish School Board for sales taxes owed at fiscalyear ending June 30, 2005 83,127

Amount due form the United States Department of Agriculture at fiscal year endingJune 30, 2005 542,616

$ 636,423

(7) Restricted Assets - Propriety Fund Type (Enterprise Utility Fund)

Restricted assets were applicable to the following at June 30, 2005:

2005 2004

Customers'deposits $ 253,866 $ 238,161Bond sinking fund account 213,693 332,837Bond sinking fund account 50,475 22,662Bond capital addition and contingency fund account 20,601 21,614

Total restricted assets $538,635 $ 615,274

29

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

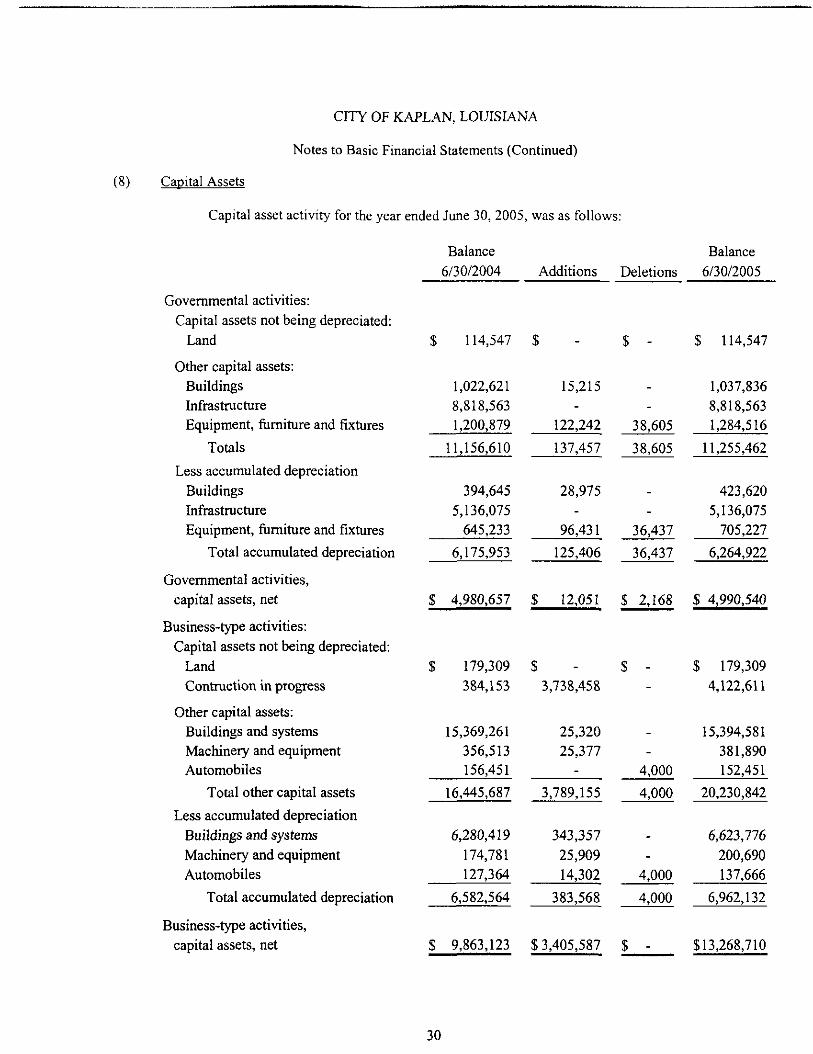

(8) Capital Assets

Capital asset activity for the year ended June 30, 2005, was as follows:

Balance Balance6/30/2004 Additions Deletions 6/30/2005

Governmental activities:Capital assets not being depreciated:

Land $ 114,547 $ - $ - $ 114,547

Other capital assets:Buildings 1,022,621 15,215 - 1,037,836Infrastructure 8,818,563 - - 8,818,563Equipment, ftirniture and fixtures 1,200,879 122,242 38,605 1,284,516

Totals 11,156,610 137,457 38,605 11,255,462

Less accumulated depreciationBuildings 394,645 28,975 - 423,620Infrastructure 5,136,075 - - 5,136,075Equipment, furniture and fixtures 645,233 96,431 36,437 705,227

Total accumulated depreciation 6,175,953 125,406 36,437 6,264,922

Governmental activities,capital assets, net $ 4,980,657 S 12,051 $ 2,168 S 4,990,540

Business-type activities:Capital assets not being depreciated:

Land $ 179,309 $ - $ - $ 179,309Contraction in progress 384,153 3,738,458 - 4,122,611

Other capital assets:Buildings and systems 15,369,261 25,320 - 15,394,581Machinery and equipment 356,513 25,377 - 381,890Automobiles 156,451 - 4,000 152,451

Total other capital assets 16,445,687 3,789,155 4,000 20,230,842

Less accumulated depreciationBuildings and systems 6,280,419 343,357 - 6,623,776Machinery and equipment 174,781 25,909 - 200,690Automobiles 127,364 14,302 4,000 137,666

Total accumulated depreciation 6,582,564 383,568 4,000 6,962,132

Business-type activities,capital assets, net $ 9,863,123 $ 3,405,587 S - $13,268,710

30

(9)

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Depreciation expense was charged to governmental activities as follows:

General governmentPoliceFireStreetsRecreation

Total depreciation expense

Depreciation expense was charged to business-type activities as follows:

ElectricGasWaterSewer

Total depreciation expense

Accounts and Other Payables

The accounts and other payables consisted of the following at June 30, 2005:

$ 33,36643,26827,17217,5244,076

$ 125,406

$ 68,92679,912

141,54293,188

$383,568

AccountsContract payableRetainage payableClaims in process

Totals

GovernmentalActivities

$ 37,979--

73,232

Business -typeActivities

$ 387,674376,869165,747

-

Total

$ 425,653376,869165,74773,232

$ 111,211 $ 930,290 $1,041,501

(10) Changes in Long-Term Debt

The following is a summary of long-term debt for the year ended June 30, 2005:

Long-term bonds payable, July 1,2005

Additions

Reductions

Long-term bonds payable, June 30, 2005

GovernmentalActivities

$ 575,000

-

(208,000)

$ 367,000

Business-typeActivities

$ 1,315,544

3,141,462

(552,306)

$ 3,904,700

Total

$ 1,890,544

3,141,462

(760,306)

$ 4,271,700

31

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

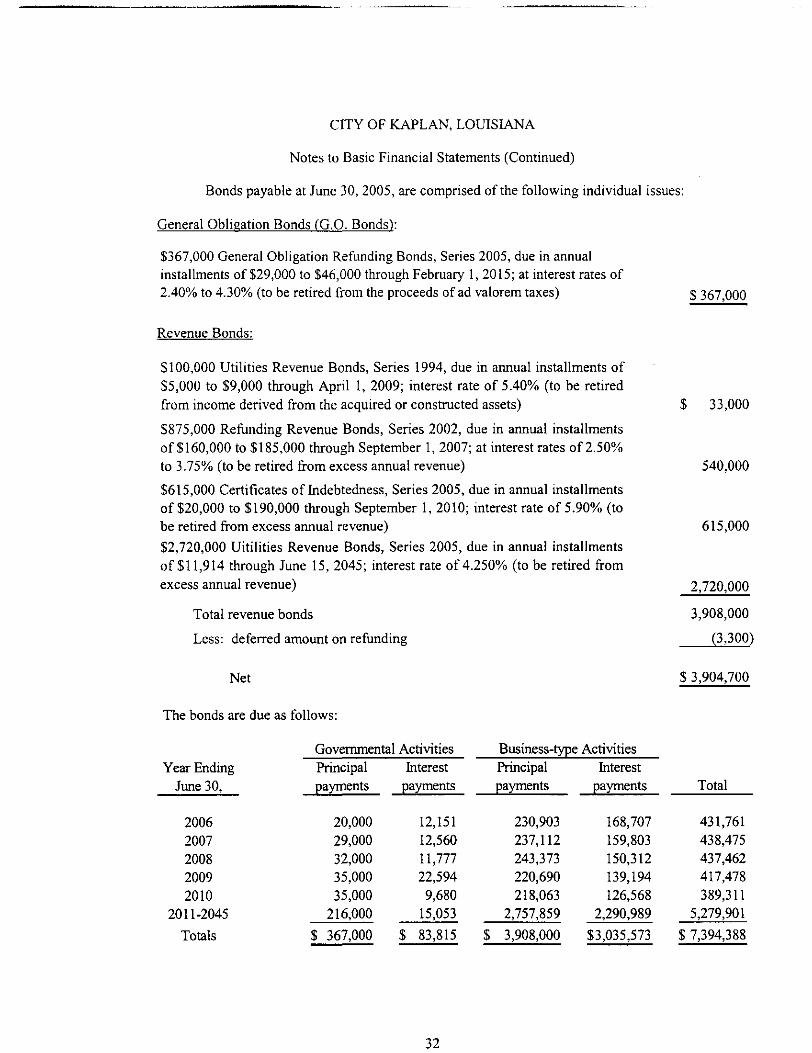

Bonds payable at June 30, 2005, are comprised of the following individual issues:

General Obligation Bonds fG.O. Bonds):

$367,000 General Obligation Refunding Bonds, Series 2005, due in annualinstallments of $29,000 to $46,000 through February 1, 2015; at interest rates of2.40% to 4.30% (to be retired from the proceeds of ad valorem taxes) $ 357 QOO

Revenue Bonds:

$100,000 Utilities Revenue Bonds, Series 1994, due in annual installments of$5,000 to $9,000 through April 1, 2009; interest rate of 5.40% (to be retiredfrom income derived from the acquired or constructed assets)

$875,000 Refunding Revenue Bonds, Series 2002, due in annual installmentsof $160,000 to $185,000 through September 1, 2007; at interest rates of 2.50%to 3.75% (to be retired from excess annual revenue)

$615,000 Certificates of Indebtedness, Series 2005, due in annual installmentsof $20,000 to $190,000 through September 1, 2010; interest rate of 5.90% (tobe retired from excess annual revenue)

$2,720,000 Uitilities Revenue Bonds, Series 2005, due in annual installmentsof $11,914 through June 15, 2045; interest rate of 4.250% (to be retired fromexcess annual revenue)

Total revenue bonds

Net

The bonds are due as follows:

Year EndingJune 30,

20062007200820092010

2011-2045

Totals

$ 33,000

540,000

615,000

is

ount on refunding

Hows:

Governmental ActivitiesPrincipalpayments

20,00029,00032,00035,00035,000

216,000

$ 367,000

Interestpayments

12,15112,56011,77722,594

9,68015,053

$ 83,815

2,720,000

3,908,000

(3,300)

$3,904,700

Business-type ActivitiesPrincipalpayments

230,903237,112243,373220,690218,063

2,757,859

$ 3,908,000

Interestpayments

168,707159,803150,312139,194126,568

2,290,989

$3,035,573

Total

431,761438,475437,462417,478389,311

5,279,901

$ 7,394,388

32

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

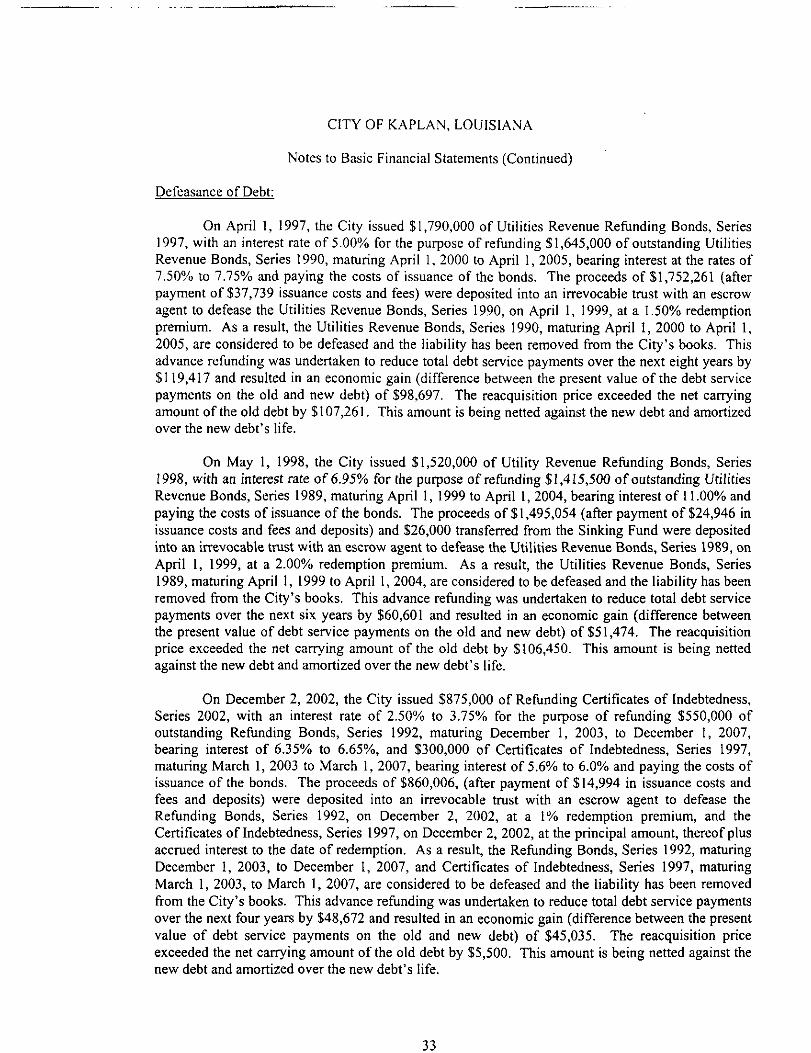

Defeasance of Debt:

On April 1, 1997, the City issued $1,790,000 of Utilities Revenue Refunding Bonds, Series1997, with an interest rate of 5.00% for the purpose of refunding $1,645,000 of outstanding UtilitiesRevenue Bonds, Series 1990, maturing April 1, 2000 to April 1, 2005, bearing interest at the rates of7.50% to 7.75% and paying the costs of issuance of the bonds. The proceeds of $1,752,261 (afterpayment of $37,739 issuance costs and fees) were deposited into an irrevocable trust with an escrowagent to defease the Utilities Revenue Bonds, Series 1990, on April 1, 1999, at a 1.50% redemptionpremium. As a result, the Utilities Revenue Bonds, Series 1990, maturing April 1, 2000 to April 1,2005, are considered to be defeased and the liability has been removed from the City's books. Thisadvance refunding was undertaken to reduce total debt service payments over the next eight years by$119,417 and resulted in an economic gain (difference between the present value of the debt servicepayments on the old and new debt) of $98,697. The reacquisition price exceeded the net carryingamount of the old debt by $107,261. This amount is being netted against the new debt and amortizedover the new debt's life.

On May 1, 1998, the City issued $1,520,000 of Utility Revenue Refunding Bonds, Series1998, with an interest rate of 6.95% for the purpose of refunding $1,415,500 of outstanding UtilitiesRevenue Bonds, Series 1989, maturing April 1, 1999 to April 1, 2004, bearing interest of 11.00% andpaying the costs of issuance of the bonds. The proceeds of $ 1,495,054 (after payment of $24,946 inissuance costs and fees and deposits) and $26,000 transferred from the Sinking Fund were depositedinto an irrevocable trust with an escrow agent to defease the Utilities Revenue Bonds, Series 1989, onApril 1, 1999, at a 2.00% redemption premium. As a result, the Utilities Revenue Bonds, Series1989, maturing April 1, 1999 to April 1, 2004, are considered to be defeased and the liability has beenremoved from the City's books. This advance refunding was undertaken to reduce total debt servicepayments over the next six years by $60,601 and resulted in an economic gain (difference betweenthe present value of debt service payments on the old and new debt) of $51,474. The reacquisitionprice exceeded the net carrying amount of the old debt by $106,450. This amount is being nettedagainst the new debt and amortized over the new debt's life.

On December 2, 2002, the City issued $875,000 of Refunding Certificates of Indebtedness,Series 2002, with an interest rate of 2.50% to 3.75% for the purpose of refunding $550,000 ofoutstanding Refunding Bonds, Series 1992, maturing December 1, 2003, to December I, 2007,bearing interest of 6.35% to 6.65%, and $300,000 of Certificates of Indebtedness, Series 1997,maturing March 1, 2003 to March 1, 2007, bearing interest of 5.6% to 6.0% and paying the costs ofissuance of the bonds. The proceeds of $860,006, (after payment of $14,994 in issuance costs andfees and deposits) were deposited into an irrevocable trust with an escrow agent to defease theRefunding Bonds, Series 1992, on December 2, 2002, at a 1% redemption premium, and theCertificates of Indebtedness, Series 1997, on December 2, 2002, at the principal amount, thereof plusaccrued interest to the date of redemption. As a result, the Refunding Bonds, Series 1992, maturingDecember 1, 2003, to December 1, 2007, and Certificates of Indebtedness, Series 1997, maturingMarch 1, 2003, to March 1, 2007, are considered to be defeased and the liability has been removedfrom the City's books. This advance refunding was undertaken to reduce total debt service paymentsover the next four years by $48,672 and resulted in an economic gain (difference between the presentvalue of debt service payments on the old and new debt) of $45,035. The reacquisition priceexceeded the net carrying amount of the old debt by $5,500. This amount is being netted against thenew debt and amortized over the new debt's life.

33

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

On March 23, 2005, the City issued $367,000 of General Obligation Refunding Bonds, Senes2005, with an interest rate of 2.40% to 4.30% for the purpose of refunding $335,000 of outstandingGeneral Obligation Bonds, Series 1995 A, maturing February 1, 2015, bearing interest of 5.20% to9.00%, and $200,000 of General Obligation Bonds, Senes 1995 B, maturing February 1, 2015,bearing interest of 5.20% to 9.00% and paying the costs of issuance of the bonds. As a result, theGeneral Obligation Bond, Series 1995 A & B, maturing on February 1, 20015, are considered to bedefeased and the liability has been removed from the City's books. This current refunding wasundertaken to reduce total debt service payments over the next six years by $83,197 and resulted in aneconomic gain (difference between the present value of debt service payments on the old and newdebt) of $36,936.

Bond Covenants:

The various bond indentures identified above contain significant limitations and restrictionson annual debt service requirements, maintenance of and flow of monies through various restrictedaccounts, minimum amounts to be maintained in various sinking funds, and minimum revenue bondcoverage. The City is substantially in compliance with all such significant limitations and restrictionsfor the year ended June 30, 2005.

(11) Compensated Absences

Employees of the City earn sick leave at the rate of one day per month, up to a maximum of120 days. No sick leave is paid upon resignation. Employees separated due to retirement are paid foraccumulated sick leave at the hourly rates being earned by that employee at separation. As of June30, 2005, an accrual of $20,727 for accumulated sick leave has been recorded. The amountsattributable to the governmental activities and business-type activities are $9,229 and $11,498,respectively.

Employees of the City earn vacation when they are hired and it is based upon the number ofyears of full-time service and varies from 5 to 15 days per year. Vacation leave cannot carryover tothe following year. As of June 30, 2005, unpaid accumulated vacation leave totaled $26,828. As ofJune 30, 2005, the amount attributable to the governmental activities and business-type activities are$17,195 and $9,633, respectively, since it is anticipated the liability will be liquidated with availablefinancial resources.

Employees of the City earn paid time off, instead of overtime pay at a rate of time and a halfwhich is based on the employee's hourly rate, up to a maximum of 240 days. Employees separateddue to resignation or termination are paid for the amount of accumulated paid time off they earned bythat employee at separation. As of June 30, 2005, an accrual of $23,956 for accumulated paid timeoff has been recorded. The amounts attributable to the governmental activities and business-typeactivities are $4,823 and $19,133, respectively.

(12) Flows of Funds; Restrictions on Use - Utilities Revenues

Under the terms of the $100,000 Utilities Revenue Bonds, Series 1994, $875,000 RefundingRevenue Bonds, Series 2002 bond indentures dated April 1, 1994 and December 2, 2002, all incomeand revenues of every nature derived from the operation of the system are pledged and dedicated tothe retirement of said bonds.

34

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Bonds and Interest Sinking Fund

The City is required to set aside into a Utilities Revenue Bond Sinking Fund each month asum equal to 1/6 of the interest falling due on the next payment dated plus 1/12 of the principal fallingdue on the next principal payment date. Funds deposited in this account are available only for theretirement of maturing bonds and interest.

Reserve Fund

The Utilities Revenue Bond Reserve Fund is maintained solely for the purpose of paying theprincipal of and interest on bonds payable from the sinking fund as which there would otherwisedefault. The fund is required to be funded in an amount equal to the reserve fund requirement(SI54,646 at June 30, 2005).

(13) Employee Retirement

The City has several pension plans covering substantially all of its employees, as follows:

-Municipal Employees' Retirement System of Louisiana-State of Louisiana - Municipal Police Employees' Retirement System-State of Louisiana - Firefighters' Retirement System-Louisiana State Employees' Retirement System

Substantially all City employees are covered under the Municipal Employees' RetirementSystem of Louisiana except firemen, policemen, and judges, who are covered under the Firefighters'Retirement System, Municipal Police Employees' Retirement System, and Louisiana StateEmployees' Retirement System, respectively. Details concerning these plans follow:

Municipal Employees' Retirement System of Louisiana

Plan description:

The Municipal Employees' Retirement System of Louisiana (the System) is a cost-sharing multiple-employer public employee retirement system (PERS) asestablished and provided for by R.S. 11:1731 of the Louisiana Revised Statutes(LRS). The System is composed of two distinct plans, Plan A and Plan B, withseparate assets and benefit provisions. Employees of the City are members of PlanB.

35

CITY OF KAPLAN, LOUISIANA

Notes to Basic Financial Statements (Continued)

Membership is mandatory as a condition of employment beginning on the dateemployed if the employee is on a permanent basis working at least thirty-five hoursper week, not participating in another public funded retirement system and underage sixty (60) at date of employment. Those individuals paid jointly by aparticipating employer and the City are not eligible for membership in the System.Under Plan B, employees who retire at or after age 60 with at least 10 years ofcreditable service or at or after age 55 with 30 years of creditable service are entitledto a retirement benefit, payable monthly for life, equal to 2% of their finalcompensation multiplied by the employee's years of creditable service. Finalcompensation is the employee's monthly earnings during the 36 consecutive orjoined months that produce the highest average. The System also provides deathand disability benefits. Benefits are established by State statute.

The Municipal Employees' Retirement System of Louisiana issues a publiclyavailable financial report that includes financial statements and requiredsupplemental information. That report may be obtained by writing to MunicipalEmployees' Retirement System of Louisiana, 7937 Office Park Boulevard, BatonRouge, Louisiana 70809.

Funding policy:

Plan members are required to contribute 5.0% of their annual covered salary and theCity is required to contribute at an actuarially determined rate. The current rate is9.50% of annual covered payroll. The contribution requirements of plan membersand the City are established and may be amended by the System's Board ofTrustees. The City's contributions to the System for the years ended June 30, 2005,2004, and 2003, were $72,647, $62,375, and $53,334, respectively, equal to therequired contributions for each year.

State of Louisiana - Municipal Police Employees' Retirement System

Plan description:

The Municipal Police Employees' Retirement System (the System) is a cost-sharing multiple -employer public employee retirement system (PERS).