Embed Size (px)

Citation preview

Division of LocaL Government & schooL accountabiLity

o f f i c e o f t h e n e w y o r k s t a t e c o m p t r o L L e r

report of ExaminationPeriod Covered:

January 1, 2012 — August 19, 2016

2016M-298

City of JamestownFinancial Condition

thomas p. Dinapoli

Page

AUTHORITY LETTER 1

EXECUTIVE SUMMARY 2

INTRODUCTION 4 Background 4 Objective 7 Scope and Methodology 7 CommentsofCityOfficialsandCorrectiveAction 7

FINANCIAL CONDITION 8 Budgeting and Fund Balance 9 2016 Outlook 12 2017 Preliminary Budget Estimates 12 Public Utilities 13 Financial Reports 15 Multiyear Planning 15 Recommendations 16

APPENDIX A ResponseFromCityOfficials 18APPENDIX B OSC Comments on the City’s Response 30APPENDIX C AuditMethodologyandStandards 31APPENDIX D HowtoObtainAdditionalCopiesoftheReport 33APPENDIX E LocalRegionalOfficeListing 34

Table of Contents

11Division of LocaL Government anD schooL accountabiLity

State of New YorkOffice of the State Comptroller

Division of Local Governmentand School Accountability September 2016

DearCityOfficials:

A toppriorityof theOfficeof theStateComptroller is tohelp localgovernmentofficialsmanagegovernment resources efficiently and effectively and, by so doing, provide accountability for taxdollarsspenttosupportgovernmentoperations.TheComptrolleroverseesthefiscalaffairsoflocalgovernmentsstatewide,aswellascompliancewithrelevantstatutesandobservanceofgoodbusinesspractices.Thisfiscaloversightisaccomplished,inpart,throughouraudits,whichidentifyopportunitiesforimprovingoperationsandCityCouncilgovernance.Auditsalsocanidentifystrategiestoreducecosts and to strengthen controls intended to safeguard local government assets.

FollowingisareportofourauditoftheCityofJamestown,entitledFinancialCondition.ThisauditwasconductedpursuanttoArticleV,Section1oftheStateConstitutionandtheStateComptroller’sauthorityassetforthinArticle3oftheNewYorkStateGeneralMunicipalLaw.

This audit’s results and recommendations are resources for local government officials to use ineffectivelymanagingoperationsand inmeeting theexpectationsof their constituents. Ifyouhavequestionsaboutthisreport,pleasefeelfreetocontactthelocalregionalofficeforyourcounty,aslistedat the end of this report.

Respectfullysubmitted,

Office of the State ComptrollerDivision of Local Governmentand School Accountability

State of New YorkOffice of the State Comptroller

2 Office Of the New YOrk State cOmptrOller2

Office of the State ComptrollerState of New York

EXECUTIVE SUMMARY

TheCityofJamestown(City)islocatedinChautauquaCountyandhasapopulationofapproximately31,000.TheCityisgovernedbytheCityCharter(Charter),Statestatutes,andlocallawsandordinances.Thenine-memberCityCouncil(Council)istheCity’slegislativebranch,whichiscomposedofthePresident and eight other elected members.

TheMayoristheCity’schiefexecutiveofficerandadministrativeofficerandisgenerallyresponsiblefortheadministrationandsupervisionofCityaffairs.TheCityComptroller(Comptroller),inconjunctionwiththeCity’sDirectorofFinancialServices(Director),isresponsibleforsupervisingtheCity’sfiscalaffairs.TheCharteroutlinesthepowersanddutiesoftheCouncil,Mayor,ComptrollerandDirector.TheCity’s general fundbudgeted appropriations for the2016fiscal year are approximately$35.1million,whicharefundedprimarilywithrevenuesfromrealpropertytaxes,salestaxandStateaid.

InJune2016,theMayorcontactedourofficetorequestanauditbecausehebelievedtheCitywasexperiencingfiscalproblems.WeconductedthisauditasaresultoftheMayor’srequestforassistanceinreviewingtheCity’sfinancialcondition.

Scope and Objective

TheobjectiveofourauditwastoreviewtheCity’sfinancialconditionfortheperiodJanuary1,2012throughAugust19,2016.Ourauditaddressedthefollowingrelatedquestion:

• Do City officials adopt realistic budgets that are structurally balanced, routinely monitorfinancialoperationsandtakeappropriateactionstomaintaintheCity’sfiscalstability?

Audit Results

Fromfiscalyears2012through2015,theCity’sfinancialconditionhasdeteriorated.TheCityincurredoperating deficits in 2012 through 2015 totaling $2.8 million.As a result, general fund balancedecreasedbyapproximately58percent,from$4.8millionto$2million.

TheCity’sfinancialconditionhasdeterioratedoverthepastfouryearsbecauseCityofficialshavenotdevelopedamultiyearfinancialplanandhaveadoptedbudgetsthatwerenotstructurallybalanced.Inaddition,theMayor,CouncilandDirectordidnotproperlybudgetfor,andtheMayordidnotensurethattheComptrollerproperlyaccountedfor,healthcareexpenditures.

33Division of LocaL Government anD schooL accountabiLity

TheCity’sfinancialconditionwillcontinue toworsenduring2016;weestimate that theCitywilllikelyincuranoperatingdeficitofatleast$400,000.Asaresult,theCity’sgeneralfundbalancewillcontinuetodecline.Wealsoestimatethat theCitywillhaveless than$800,000inspendablefundbalanceandminimalcashattheendof2016.Asaresult,itwilllikelyexperiencecashflowproblems.Further,theMayor,CouncilandCityofficialswillneedtocloseabudgetgapofmorethan$2millionin 2017.

Wereviewedthe2017preliminarybudgetestimatesforthegeneralfundandfoundthatappropriationestimates appear reasonable except for employee benefit costs, which appear overestimated byapproximately$300,000(2percent).However,certainrevenueestimatesareofconcern.TheMayor’spreliminary budget estimates indicate that the projected budget gap would be addressed with a property taxincreaseof$2.6million;however,theMayorreportsthattheCityisnearingitsconstitutionaltaxlimitandisawarethattheCitycannotraisetaxesenoughtocovertheentirebudgetgap.

AlthoughtheCity’sabilitytoraisepropertytaxesislimited,ithastheabilitytoshareprofitsfromits municipally-owned public utilities.1 The Jamestown Board of Public Utilities (BPU) manages the City’spublicutilities.For thepast fewyears, theBPUhasprovided theCitywithaprofit-sharingpaymentofapproximately$465,000eachyearonaverage.However,theserevenueswerenotincludedinthepreliminarybudgetestimatefor2017.InaccordancewiththeGeneralMunicipalLaw,2 the City isallowedtoearnafairreturnonitsinvestmentintheutilitiesandtakeaportionoftheprofitsfromitsmunicipalutilities.Therefore,Cityofficialsshouldworkwith theBPUtoensure theapplicableutilitiesshareprofitswiththeCityandprovidetheCitywithareasonablereturnonitsinvestment.

Comments of City Officials

The results of our audit and recommendations have been discussedwith City officials, and theircomments,whichappear inAppendixA,havebeenconsidered inpreparing this report.ExceptasindicatedinAppendixA,Cityofficialsgenerallyagreedwithourfindingsandindicatedtheyplantoinitiatecorrectiveaction.AppendixBincludesourcommentsonissuesCityofficialsraisedintheirresponse.

1 Applicabletoelectricandwaterpublicutilities.2 GMLSection94

4 Office Of the New YOrk State cOmptrOller4

Background

Introduction

Objective

Scope andMethodology

The City of Jamestown (City) is located in Chautauqua County (County) and has a population of approximately 31,000.TheCityisgovernedby theCityCharter (Charter),State statutes, and locallaws and ordinances. The nine-member City Council (Council) is theCity’slegislativebranch,whichiscomposedofthePresidentandeightotherelectedmembers.TheMayoristheCity’schiefexecutiveofficerandadministrativeofficerandisgenerallyresponsiblefortheadministration and supervision of City affairs. The City Comptroller (Comptroller), in conjunctionwith theCity’sDirectorofFinancialServices (Director), is responsible for supervising theCity’s fiscalaffairs.TheCharteroutlines thepowersanddutiesof theCouncil,Mayor,ComptrollerandDirector.

TheCityemploysapproximately400full-andpart-timeemployeeswho are assigned to various departments. These departments provide services includinggeneralgovernmentsupport,streetmaintenance,parks and recreationprograms, andpolice andfireprotection.TheCity’sgeneralfundbudgetedappropriationsforthe2016fiscalyearare approximately $35.1million,which are funded primarilywithrevenuesfromrealpropertytaxes,salestaxandStateaid.

TheCityalsohasfivemunicipally-ownedpublicutilitiesthatprovideelectricity, water, wastewater, sanitation, and heating and coolingservices to residents and businesses located both within and outside the City’s boundaries.3 The Jamestown Board of Public Utilities (BPU) was established in 1923 to guide the development of the City’s electric and water services. The BPU is responsible for managing and controlling the utility operations. The BPU is composed of the Mayor (who is the President of the BPU), the City’s Director of PublicWorks, twoCouncil representatives and five communitymembersappointedbytheMayorandapprovedbytheCouncil.AlthoughpartoftheCity,theutilitiesareoperatedasseparateanddistinctunitsbythe BPU and are not under the Council’s direct control.4 The BPU adopts separate annual budgets, supervises andmanages the fiscalaffairs of each utility and hires its own employees.

The BPU has an appointed General Manager responsible for theutilities’ day-to-day operations and a Business Manager responsible forthefinancialoperationsandmaintainingaccountingrecords.The

3 Heating and cooling services are only provided to residents and businesses located within City boundaries.

4 The Charter provides that the City’s utilities are under the full control and supervision of the BPU.

55Division of LocaL Government anD schooL accountabiLity

BPU’s2016budgettotaled$58.8millionandincludesthefollowingdivisions: electric ($45 million), water ($5.5 million), wastewater($5.3million),solidwaste/sanitation($2million)andheating/cooling($1million).Allofthesedivisionsarefundedprimarilythroughusercharges.

In June 2016, theMayor contacted our office to request an auditbecausehebelievedtheCitywasexperiencingfiscalproblems.Weconducted this audit as a result of the Mayor’s request for assistance inreviewingtheCity’sfinancialcondition.

The City’s economic drivers have posed many challenges in recent years. By most measures, the City continues to face a difficultenvironment within which to operate. The Jamestown area is an economichub inWesternNewYork for servicesandemployment.Healthcare,governmentandmanufacturingareimportantindustrialsectors.

TheCity’slaborforceisshrinking.AccordingtotheNewYorkStateDepartment ofLabor, the average size of the labor force for 2015was12,300,down10.9percentfrom2010.Thenumberofemployedpeoplealsodeclined,butmoreslowly;11,500workerswerereportedin2015,down7.3percent.5

Since2010,theCity’spopulationhascontracted3.4percent,comparedwith 2.2 percent growth statewide. The City’s population has been declining since the 1950s, down 1.8 percent between 2000 and2010.6 During thesameperiod, theCounty’spopulationcontracted3.6 percent. This population loss likely negatively affects the City’s propertyvaluesand itsassociated taxbase.These losses,however,aresimilartothoseexperiencedbynumerouscitiesinUpstateNewYork,particularlythosewithhistoricallylargemanufacturingsectors.

AsignificantrevenuesourcefortheCitycomesfrompropertytaxes.TheCity’staxlevyhasincreasedbyapproximately$2.2million(17percent)between2009and2015.However,slow-growingpropertyvalueshaveconstrainedtheCity’sabilitytousethisrevenuesource,astheCityhasreportedthatithasapproacheditsConstitutionalTaxLimit (CTL) ineachof the last fouryears.TheCTL,which is themaximum amount of real property tax that may be levied in anyfiscalyear,hasbeenalongstandingconcernfortheCity.TheCTLiscalculatedat2percentoftheCity’sfive-yearaverageoffullvaluation(withcertainexclusions).Since2009,theCity’staxlevyhasgenerally

5 NewYork State Department of Labor, LaborArea Unemployment StatisticsProgram,www.labor.ny.gov/stats/LSLAUS.shtm

6 United StatesCensusBureau, 2010DecennialCensus,AmericanCommunitySurvey and Current Population Survey

6 Office Of the New YOrk State cOmptrOller6

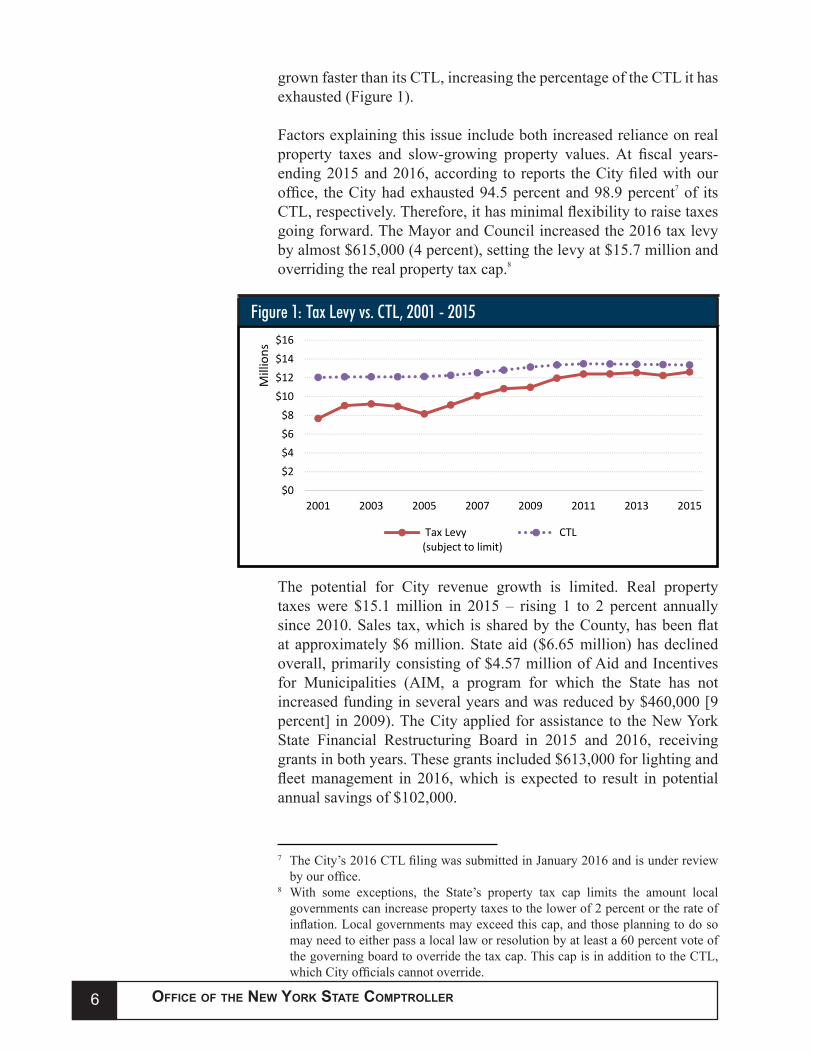

grownfasterthanitsCTL,increasingthepercentageoftheCTLithasexhausted(Figure1).

Factorsexplainingthisissueincludebothincreasedrelianceonrealproperty taxes and slow-growing property values.At fiscal years-ending2015and2016,according to reports theCityfiledwithouroffice, theCityhadexhausted94.5percentand98.9percent7 of its CTL,respectively.Therefore,ithasminimalflexibilitytoraisetaxesgoingforward.TheMayorandCouncilincreasedthe2016taxlevybyalmost$615,000(4percent),settingthelevyat$15.7millionandoverridingtherealpropertytaxcap.8

7 TheCity’s2016CTLfilingwassubmittedinJanuary2016andisunderreviewbyouroffice.

8 With some exceptions, the State’s property tax cap limits the amount localgovernmentscanincreasepropertytaxestothelowerof2percentortherateofinflation.Localgovernmentsmayexceedthiscap,andthoseplanningtodosomay need to either pass a local law or resolution by at least a 60 percent vote of thegoverningboardtooverridethetaxcap.ThiscapisinadditiontotheCTL,whichCityofficialscannotoverride.

$0$2$4$6$8

$10$12$14$16

2001 2003 2005 2007 2009 2011 2013 2015

Millions

Figure 1: Tax Levy vs. CTL, 2001 ‐ 2015

Tax Levy(subject to limit)

CTL

Figure 1: Tax Levy vs. CTL, 2001 - 2015

The potential for City revenue growth is limited. Real property taxeswere $15.1million in 2015 – rising 1 to 2 percent annuallysince2010.Sales tax,which issharedbytheCounty,hasbeenflatatapproximately$6million.Stateaid ($6.65million)hasdeclinedoverall,primarilyconsistingof$4.57millionofAidandIncentivesfor Municipalities (AIM, a program for which the State has notincreasedfundinginseveralyearsandwasreducedby$460,000[9percent] in2009).TheCityappliedforassistance to theNewYorkState Financial Restructuring Board in 2015 and 2016, receivinggrantsinbothyears.Thesegrantsincluded$613,000forlightingandfleetmanagement in 2016,which is expected to result in potentialannualsavingsof$102,000.

77Division of LocaL Government anD schooL accountabiLity

TheCityhasarelativelystrongandimproveddebtposition,havingreduceddebtoutstandingby$6.5million(14percent)since2010,to$38.8million.TheCityhasexhausted35.4percentofitsdebtlimit.However, any issuance of debt would require annual debt serviceexpenditures,puttingfurtherstrainontheCity’sbudget.

Furthermore,aspointedoutintheMayor’sbudgetmessages,theCityalso faces deferred maintenance of its infrastructure. This is a growing liabilitythatisnotrecordedinthefinancialbooksandrecords.Whilean assessment of the impact of deferred maintenance was not within thescopeofthisaudit,itisarealandgrowingconcern.

TheobjectiveofourauditwastoreviewtheCity’sfinancialcondition.Ourauditaddressedthefollowingrelatedquestion:

• DoCityofficialsadoptrealisticbudgetsthatarestructurallybalanced, routinely monitor financial operations and takeappropriateactionstomaintaintheCity’sfiscalstability?

WereviewedtheCity’sfinancialconditionfortheperiodJanuary1,2012throughAugust19,2016.Weextendedourreviewbackto2009toevaluatecertainrevenueandexpendituretrendsinmoredetail.

We conducted our audit in accordance with generally acceptedgovernmentauditingstandards(GAGAS).Moreinformationonsuchstandards and the methodology used in performing this audit are includedinAppendixCofthisreport.

The results of our audit and recommendations have been discussed withCityofficials,and theircomments,whichappear inAppendixA,havebeenconsideredinpreparingthisreport.ExceptasindicatedinAppendixA,Cityofficialsgenerallyagreedwithourfindingsandindicatedtheyplantoinitiatecorrectiveaction.AppendixBincludesourcommentsonissuesCityofficialsraisedintheirresponse.

The Council has the responsibility to initiate corrective action.Awrittencorrectiveactionplan(CAP)thataddressesthefindingsandrecommendations in this report should be prepared and forwarded to ourofficewithin90days,pursuanttoSection35ofGeneralMunicipalLaw.FormoreinformationonpreparingandfilingyourCAP,pleaserefer to our brochure,Responding to an OSC Audit Report,whichyoureceivedwiththedraftauditreport.WeencouragetheCounciltomakethisplanavailableforpublicreviewintheCityClerk’soffice.

Objective

Scope and Methodology

Comments of City Officials and Corrective Action

8 Office Of the New YOrk State cOmptrOller8

Financial Condition

The Mayor, Council, Comptroller and Director have a sharedresponsibility for managing and maintaining the City’s fiscalhealth. To do so, City officials must develop and adopt realisticand structurally balanced budgets that provide sufficient recurringrevenues to finance recurring expenditures. Additionally, officialsshould actively monitor available fund balance and cash balances to ensure neither is depleted to dangerously low levels. This can be accomplished,inpart,bycreatingamultiyearfinancialplanwhich,when updated and properly used, allows City officials to identifydevelopingrevenueandexpendituretrends,set long-termprioritiesandgoals,avoidpotentiallargefluctuationsinrealpropertytaxratesand assess the effect their decisions will have on fund balance levels.

TheCityincurredoperatingdeficitsinfiscalyears2012through2015totaling $2.8million.As a result, general fund balance9 decreased byapproximately58percent,from$4.8millionto$2million.10 The City’sfinancial conditionhas deterioratedover the past four yearsbecauseCityofficialshaveadoptedbudgetsthatwerenotstructurallybalanced. In addition, the Mayor, Council and Director did notproperlybudgetfor,andtheMayordidnotensurethattheComptrollerproperlyaccountedfor,healthcareexpenditures.

TheCity’sfinancialconditionwillcontinuetodeclineduring2016because the adopted budget is again not structurally balanced.WeestimatethattheCitywilllikelyincuranoperatingdeficitofatleast$400,000 unless significant and immediate spending changes areimplemented.Asa result, theCitywillhave less than$800,000 inspendablefundbalanceremainingasofDecember31,2016.Wealsoestimate that the City will have minimal cash at the end of 2016 and willlikelybeexperiencingcashflowproblemsasaresult.

We also reviewed the 2017 preliminary budget estimates anddetermined that the City is likely to have a budget gap of more than $2million.Cityofficialswillhavetotakemeaningfulstepstoreduceexpendituresorobtainadditionalrevenues.

DespitetheCity’sdeterioratingfinancialcondition,CityofficialshavenotdevelopedamultiyearfinancialplanthatwouldaidinplanningandmanagingtheCity’sfinancesandoperations,norhaveofficials9 Fund balance totals for the general fund have been adjusted to include the portion

of fund balance improperly reported in the trust and agency fund.10Approximately$837,000attheendof2015wasconsiderednonspendablefundbalance. It consists of inventory and prepaid expenditures, which cannot beliquidatedforpurposessuchascashfloworbalancingthebudget.

99Division of LocaL Government anD schooL accountabiLity

developedamultiyearcapitalplan.Amultiyearfinancialplancouldhelpofficialsdevelopmorestructurallybalancedbudgetsandworktowards rebuilding fund balance levels and restoring the City’s long-termfiscalhealth.

Astructurallybalancedbudgetensuresthatappropriationsarefundedwithrecurringrevenuesandthatfundbalanceservesasafinancialcushionforunexpectedeventsandmaintainingcashflow.TomaintaintheCity’sfiscal stability, it is important forCity officials to adoptrealistic budgets that are structurally balanced. City officialsmustalso ensure that the level of fund balancemaintained is sufficientto provide adequate cash flow and hedge against unanticipatedexpendituresandrevenueshortfalls.

A continuous decline in fund balance indicates a deterioratingfinancial condition.While fundbalance canbe appropriated in thebudgettohelpfinanceoperations,consistentlydoingso–insteadofplanningtouserecurringrevenuesources–candepletefundbalancetolevelsthatarenotsufficientforcontingenciesandcashflow,asisthe City’s current situation.

The City derives the majority of its general fund revenues from real propertytaxes,salestaxandStateaid.AIMwasreducedin2009.11 TheCity’sAIMwasreducedbyapproximately$460,000(9percent)andhasremainedat thisamounteversince.Overthesameperiod,generalfundexpenditureshaveincreasedbymorethan$5million(17percent).Althoughsalestaxrevenueshaveremainedfairlyconsistent,evenincreasingby$700,000(13percent),asrevenuefromStateaiddecreased and expenditures increased, theCity relied on increasesin real property taxes to finance operations. Specifically, between2009 and 2015, the tax levy has increased by approximately $2.2million (17 percent).However, the annual tax levy increaseswerenotsufficienttobalancetheincreasedexpendituresandastructuralbudgetdeficitremained.

The City’s general fund annual budget gap averaged more than $615,000eachyearfrom2012through2015.TheCityfundedthesestructural deficits by relying on fund balance. This approach hasnegativelyaffectedthegeneralfund’sfinancialconditionand,giventhecurrentbalance,cannotcontinue.

TheCitybegan2012withmore than$4.8million ingeneral fundbalance12 but ended 2015 with approximately $2 million in fund

Budgeting and Fund Balance

11Aidtosomemunicipalitieswasreducedby2percent,butmunicipalitiesliketheCity that were less reliant on State aid received larger reductions of 5 percent.

12 Fund balance totals for the general fund have been adjusted to include the portion of fund balance improperly reported in the trust and agency fund.

10 Office Of the New YOrk State cOmptrOller10

balance (Figure 2). Therefore, over this four-year period, generalfundbalancedecreasedbyabout$2.8million(58percent).However,approximately$800,000ofthe$2millioninfundbalanceattheendof 2015 was considered nonspendable13 and could not be used to providecashflowortohelpbalancetheCity’sbudget.Consequently,theCity had only approximately $1.2million in available generalfund balance.

13Thenonspendablefundbalanceconsistsofinventoryandprepaidexpenditures,which cannot be liquidated for purposes such as cash flow or balancing thebudget.

14 The Comptroller stated that he would transfer funds to the trust and agency fund when actual health care claims were less than appropriations.

15 The City has no authority to establish a reserve fund for health care costs. However,theproprietyofthisarrangementisoutsidethescopeofthisaudit.

$4,870,000 $4,600,000

$4,160,000

$3,180,000

$2,040,000 $1,620,000

$‐

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

2011 2012 2013 2014 2015 Projected 2016

Figure 2: Ending Fund BalanceFigure 2: Ending Fund Balance

In part, City officials have used fund balance to help financeexpendituresincreasingfasterthanrevenues.Almosthalfoftherisingexpenditureswereforthecostofhealthcarebenefits.TheComptrollertoldusthat,formanyyears,hehadtransferredaportionofthegeneralfund’s operating surpluses14 to the trust and agency fund to set aside funds for future health care costs.15Atthebeginningof2012,theCityhadapproximately$1.8millionsetasideforhealthcarecostsinthetrustandagencyfund.TheCityusedmore than$830,000of thesefundstopayforhealthcareexpendituresfrom2013through2015.

However,theMayor,CouncilandDirectordidnotproperlybudgetfor these health care costs. Further, theMayor did not ensure thattheComptrollerproperly recordedhealth care expenditures,whichwereaccountedforinaccuratelyandinconsistently.Fromfiscalyears2012through2015,generalfundappropriationsforhealthcarecostswereunderestimatedbynearly$1.1million(5percent)andrelated

1111Division of LocaL Government anD schooL accountabiLity

expenditures were understated in the general fund by more than$830,000.Asaresult,generalfundoperatingresultsweremisstatedandtheCity’struefinancialconditionwasnotreadilyapparent.

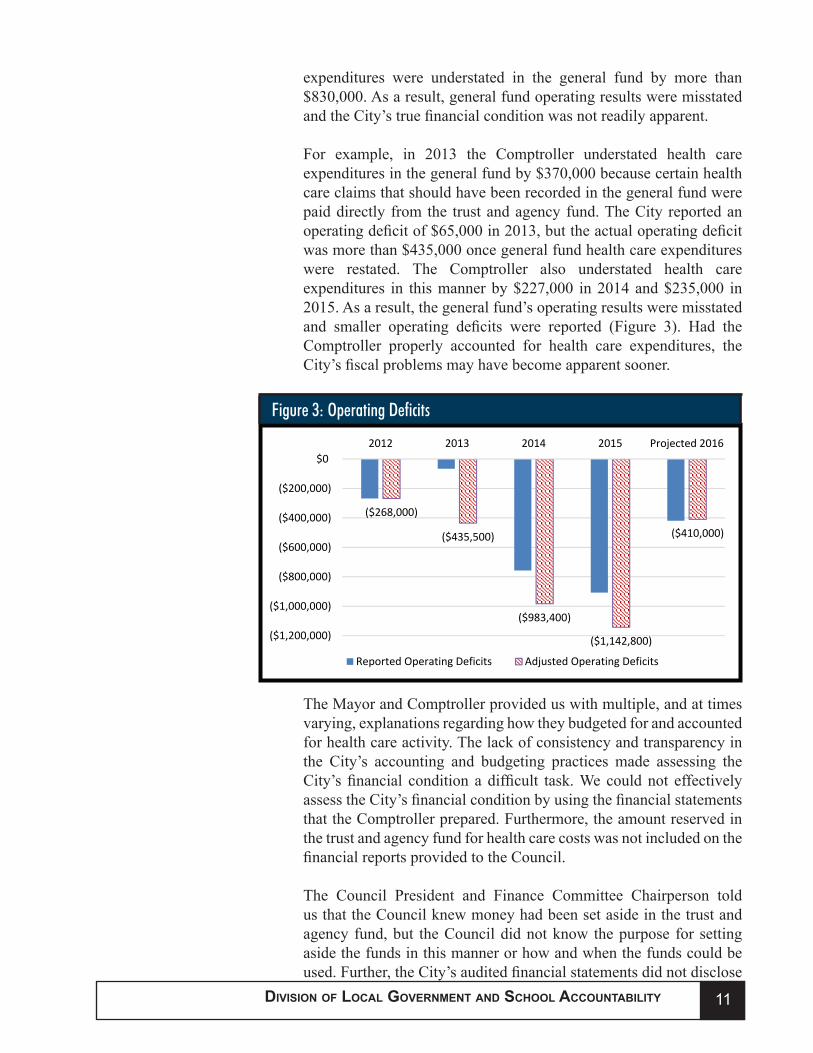

For example, in 2013 the Comptroller understated health careexpendituresinthegeneralfundby$370,000becausecertainhealthcare claims that should have been recorded in the general fund were paid directly from the trust and agency fund. The City reported an operatingdeficitof$65,000in2013,buttheactualoperatingdeficitwasmorethan$435,000oncegeneralfundhealthcareexpenditureswere restated. The Comptroller also understated health care expenditures in thismannerby$227,000 in2014and$235,000 in2015.Asaresult,thegeneralfund’soperatingresultsweremisstatedand smaller operating deficits were reported (Figure 3). Had theComptroller properly accounted for health care expenditures, theCity’sfiscalproblemsmayhavebecomeapparentsooner.

($268,000)

($435,500)

($983,400)

($1,142,800)

($410,000)

($1,200,000)

($1,000,000)

($800,000)

($600,000)

($400,000)

($200,000)

$02012 2013 2014 2015 Projected 2016

Figure 3: Operating Deficits

Reported Operating Deficits Adjusted Operating Deficits

Figure 3: Operating Deficits

TheMayorandComptrollerprovideduswithmultiple,andattimesvarying,explanationsregardinghowtheybudgetedforandaccountedfor health care activity. The lack of consistency and transparency in the City’s accounting and budgeting practices made assessing the City’sfinancial condition a difficult task.Wecouldnot effectivelyassesstheCity’sfinancialconditionbyusingthefinancialstatementsthattheComptrollerprepared.Furthermore,theamountreservedinthe trust and agency fund for health care costs was not included on the financialreportsprovidedtotheCouncil.

The Council President and Finance Committee Chairperson told us that the Council knew money had been set aside in the trust and agency fund,but theCouncildidnotknow thepurpose for settingaside the funds in this manner or how and when the funds could be used.Further,theCity’sauditedfinancialstatementsdidnotdisclose

12 Office Of the New YOrk State cOmptrOller12

the true nature of these funds as general fund surplus but instead incorrectly indicated that funds belonged to a third-party and were beingheldbytheCityinafiduciarycapacity.

This incorrect and inconsistent accounting treatment not only clouds theCity’sfinancialconditionbutalsomakesyear-to-yearcomparisonsandbudgetaryprojectionsdifficult.

As of July 2016, the Comptroller anticipated that the City wouldincur an operating deficit of about $410,000 for 2016. Totalappropriationsfor2016are$464,000(1percent)lessthantheprioryear’sexpenditures.AlthoughtheMayorandCouncilincreasedthe2016 tax levybyalmost$615,000 (4percent), theystillneeded toappropriate approximately $409,000 from fund balance to balancethebudget.TheCityhasexpended$15.9million(45percent)ofits$35.1milliongeneralfundbudgetasofJuly6,2016.Positively, itappearsthatexpenditureswillbelessthanestimatedmainlybecausehealth care costs have been about 20 percent less than anticipated so far in 2016.

Based on the adopted budget, current year-to-date revenues andexpenditures, and historical revenue and expenditure trends, weestimate that the City will likely incur an operating deficit of atleast$400,000.Asaresult,theCitywillhavelessthan$800,000inspendablefundbalanceremainingasofDecember31,2016.

Now,withfundbalancealmostdepleted,theCityhaslimitedoptionsavailabletofundanyincreasesinoperatingcosts.IftheMayorandCouncilchoosetofurtherincreasepropertytaxes,itcouldrequireanoverrideofthepropertytaxcap.Further,attheendof2015,theCityreportedthatithadexhausted94.5percentofitsconstitutionalCTL,leavingtheCitywithamarginoflessthan$740,000toraisetaxesgoingforward.TheCityincreasedits2016taxlevyby$615,000andreportedthatitwillexhaust98.9percentofitsCTL,leavingitwithamarginoflessthan$160,000toincreasetaxesin2017.

TheCharterrequiresthattheMayorpresenttheExecutiveOperatingBudget to the Council by October 8. We reviewed the 2017preliminary budget estimates for the general fund, which includetotal appropriations of $36.7 million.Appropriations are expectedtoincreasebyapproximately$1.6million(5percent).Thisincludesincreasesof$975,000inhealthcarecosts,$430,000insalariesand$130,000 invariouscontractualcosts. Italso includesasavingsofapproximately$130,000indebtservicecosts.Overall,appropriationestimatesappearreasonableexceptforemployeebenefitcosts,whichappearoverestimatedbyapproximately$300,000(2percent).

2016 Outlook

2017 Preliminary Budget Estimates

1313Division of LocaL Government anD schooL accountabiLity

Sales tax revenues are anticipated tobe$6million, approximatelythe same as 2016 revenues, which is reasonable.A real propertytaxincreaseofapproximately$2.6million(16.8percent)wouldbeneeded tobalance thebudget.However, theCityhas reported thatitexhausted98.9percentofits2016CTL;therefore,ithasminimalflexibilitytoraisetaxesgoingforwardandwillneedtoidentifynewrecurring revenue sources or use a combination of increased recurring revenues anddecreased recurring expenditures to close the budgetgap.

AlthoughtheCity’sabilitytoraisepropertytaxesislimited,ithastheabilitytoshareprofitsfromitsmunicipally-ownedpublicutilities.16

The utilities provide electricity, water, wastewater, sanitation, andheating and cooling services to residents and businesses located both within and outside the City’s boundaries.17 The BPU is responsible for managing and controlling the utility operations.

Profit-sharingPayments−Fromfiscalyears2012through2014,theBPUhasprovidedtheCitywithaprofit-sharingpaymentfromtheelectricandwaterutilitiesofapproximately$465,000eachyearonaverage.ThepaymentsaremadepursuanttotheGeneralMunicipalLaw(GML)andprovidetheCitywithareturnonitsinvestmentintheutilities.However,thesepaymentswerenotincludedinthe2017preliminary budget estimates. TheMayor, who also serves as theBPUPresident,toldusthatotherBPUmembersandsomecustomershavechallengedtheequityofthesepayments; therefore, theywerenot included in the preliminary budget estimates.

In accordance with GML, the City is allowed to earn from theoperation of its electric and water utilities a “fair return” on the value ofthepropertyusedandusefulintheelectricservice,overandabovethe costs of operation and necessary and proper reserves. The statute goesontoprovidethat“profits”resultingfromtheoperationoftheelectric utility may be used for municipal purposes or consumer refunds.18AlthoughtheBPU’sfinancialoperationswereoutsidethescopeofthisaudit,weattemptedtoassesstheutilities’overallfiscalhealth to evaluate their ability to continue providing the City with profit-sharingpayments.However,theBPU’sformerfiscalofficerhaddestroyedcertainfinancialrecordsthatshouldhavebeenmaintained.The current records contained numerous discrepancies and could not be proven reliable.

Public Utilities

16Applicabletoelectricandwaterpublicutilities.17 Heating and cooling services are only provided to residents and businesses

located within City boundaries.18GMLSection94

14 Office Of the New YOrk State cOmptrOller14

Theelectricutility’sratesareregulatedbytheNewYorkStatePublicServiceCommission(PSC).In2015,theBPUrequestedthePSC’sapproval to increase electric rates. The PSC granted approval for a rate increase in February 2016.As part of its order approving therate increase, the PSCnoted the electric utility’s “currently strongfinancialcondition,”andstated that“wedonothaveanyconcernsovertherecentlevelof[theutility’s]contributions[totheCity].19 The PSCalsostatedthat,astheelectricutility’ssoleinvestor,“theCityofJamestown is entitled to the return earned on that investment.”20 Inourview,thesestatementssuggestthattherecentamountsoftheelectricutility’sprofit-sharingpaymentstotheCityaresustainable(assumingnomaterialnegativechangeintheutility’sfinancialcondition)andthat the City is entitled to those payments. The City should work with theBPUtocontinuetheprofit-sharingpayments.

City officials should continue to work with the BPU to establishadequatecontrolsoverfinancialrecordsandtoassesseachutility’sfinancialposition.Cityofficials shouldalsocontinue toworkwiththe BPU to ensure the applicable utilities provide the City with a reasonable return on the City’s investment.

Administrative Cost Allocation − The City provides variousadministrative services to the BPU and is reimbursed $12,000annually.Although a lesser amount ($6,400)21 is stipulated in the Charter,theCitydidnotuseacostallocationmethodtodetermineareasonable and equitable basis for charging the BPU for the services it provides. The City Treasurer’s Office collects utility payments,reconciles daily collections, reviews suspended utility accounts,performs taxcertificate searches forunpaid taxesandassessments,and prepares annual financial reports. The Comptroller preparesandfiles quarterly payroll reportswith federal andState agencies,prepares debt schedules for constitutional debt limit reporting,prepares monthly bank reconciliations and processes wire transfers between BPU bank accounts.

WecalculatedtheapproximatedollarvalueoftheservicesprovidedusingsalaryandbenefitinformationandtheapproximatetimespentbyCityemployeesperformingservicesfortheBPU.IftheCitychoseasimilarapproach,theannualcostcouldbeapproximately$36,000,or about triple the amount currently being charged. City officials

19PSCRateCase15-E-0184,p15-1620 Id. at p 1621TheCharterstatesthattheBPUshallpay$6,400annuallyintotheCity’sgeneral

fund to reimburse the City for collecting the revenues accruing to the City’s publicutilitysystems.CurrentCityofficialscouldnotexplainwhenorwhytheamount changed to $12,000 annually. However, the services being providedseem to be additional services outside the revenue collection function and might serveasjustificationfortheBPU’s$12,000payment.

1515Division of LocaL Government anD schooL accountabiLity

should periodically evaluate the cost of services the City provides to the BPU to ensure the annual fee reasonably relates to the cost of providing those services.

TheMayorandCouncilneedcomplete,accurateandtimelyfinancialinformationtoeffectivelymonitortheCity’soperationsandfinancialcondition. The Charter requires the Comptroller to submit annual financialreports totheMayorandquarterlyfinancialreports totheCouncil. The quarterly reports should include comparisons of actual revenuesandexpenditureswiththeamountsestimatedintheannualbudget for each operating fund.

AlthoughtheComptrollerprovidedtheMayorandCouncilwiththerequiredfinancialreports,thereportswerenotaccuratebecausehealthcare expenditures were understated. Further, the Council was notprovidedwithfinancialreportsindicatingthattherewasgeneralfundmoney being retained in the trust and agency fund. The Comptroller stated that his reports will typically contain information about health care expenditures starting in themiddle of the fiscal year throughyear-end. However, the information provided mainly consists ofwhetherhealthcareexpenditureswillbewithinbudgetfortheyearand does not include any discussion of the health care funds retained in or paid directly out of the trust and agency fund.

The Comptroller also indicated that these funds were kept separate from the general fund so that the Council would not opt to use them as awaytolowertaxesandfurtherdecreasefundbalanceandtopreventthe unions from being aware of the cash on hand. By not providing the Council with complete financial information relating to healthcarecostresourcesandexpenditures,theCouncilwasnotfullyawareoftheCity’struefinancialposition.

MultiyearfinancialplanningisatoolCityofficialscanusetoimprovethebudgetdevelopmentprocess.Comprehensivemultiyearfinancialplanningshouldconsideroperatingandcapitalneedsandfinancingsources over an extended period. Planning on a multiyear basisenables officials to identify developing revenue and expendituretrends, establish long-term priorities and goals, and consider theimpactofone-timefinancingsourcesorothershort-termbudgetingdecisionson futurefiscalyears.Any long-termfinancialplanmustbe monitored and updated on a continuing basis to provide a reliable framework for preparing budgets and to ensure that information used to guide decisions is current and accurate.

Cityofficialsdidnotdevelopamultiyearfinancialor capitalplan.Hadsuchplansbeendeveloped,theMayorandCouncilwouldhavehad a valuable resource that would have allowed them to make

Financial Reports

Multiyear Planning

16 Office Of the New YOrk State cOmptrOller16

more informed financial decisions. This may have prevented theCity’sdecliningfiscalhealth.Goingforward,developingafinancialplan would be a useful tool for the Mayor and Council to ensure that recurring revenue sources are sufficient to finance anticipatedrecurringexpenditures.Thiswillhelptomaintainareasonablelevelof unrestricted fund balance at year end and to develop a plan for building fund balance up. In addition, a capital plan identifyingcapital needs with time schedules and the method of financingeach improvement or capital expenditure would aid City officialswith assessing the impact future capital expenditureswill have onsubsequent years’ operating budgets.

Because City officials did not develop a multiyear financial andcapitalplan,itmayleadtothefurtherdepletionoffundbalanceandundesirable constraints on the City’s financial flexibility in futureyears.

TheMayor,CouncilandCityofficialsshould:

1. Adopt structurally balanced budgets that include realisticestimates and fund recurring expenditures with recurringrevenues.

2. Closely monitor the City’s finances, including availablefundbalanceandcashbalances,topreventfurtherdeclineinfinancialcondition.

3. Modify revenue and expenditure estimates in the 2017preliminary budget prior to adoption.

4. Workwith the BPU to establish adequate internal controlsoverfinancialoperationsandrecords.

5. Reassess the amount of administrative support being provided to the BPU and develop a reasonable cost allocation method to ensure annual charges are adequate to reimburse the City for the cost of providing such services.

6. Develop and regularly update a comprehensive written multiyear financial and capital plan that includes realisticmeasures for rebuilding fund balance levels, addressingcapitalneedsandrestoringtheCity’slong-termfiscalhealth.

TheComptrollershould:

7. Correct the accounting records to ensure health care costs and fund balance are properly recorded and reported in the general fund.

Recommendations

1717Division of LocaL Government anD schooL accountabiLity

8. Ensure that reports provided to the Council are comprehensive and complete and provide an accurate presentation of the City’sfinancialcondition.

18 Office Of the New YOrk State cOmptrOller18

APPENDIX A

RESPONSE FROM CITY OFFICIALS

TheCityofficials’responsetothisauditcanbefoundonthefollowingpages.

PleasenotethattheCityofficials’responseletterreferstopagenumbersthatappearedinthedraftreport.Thepagenumbershavechangedduringtheformattingofthisfinalreport.

1919Division of LocaL Government anD schooL accountabiLity

20 Office Of the New YOrk State cOmptrOller20

2121Division of LocaL Government anD schooL accountabiLity

22 Office Of the New YOrk State cOmptrOller22

SeeNote1Page 30

2323Division of LocaL Government anD schooL accountabiLity

24 Office Of the New YOrk State cOmptrOller24

2525Division of LocaL Government anD schooL accountabiLity

SeeNote2Page 30

26 Office Of the New YOrk State cOmptrOller26

SeeNote3Page 30

SeeNote4Page 30

2727Division of LocaL Government anD schooL accountabiLity

28 Office Of the New YOrk State cOmptrOller28

SeeNote5Page 30

2929Division of LocaL Government anD schooL accountabiLity

30 Office Of the New YOrk State cOmptrOller30

APPENDIX B

OSC COMMENTS ON THE CITY’S RESPONSE

Note1

WerecognizethatCityofficialswerecontinuingtorevisethepreliminarybudgetestimateswhilewewereconductingtheaudit.However,the2017budgetdocumentprovidedtousindicatedthatthetaxlevyestimateis$2.6millionhigherthanthepreviousyear.

Note2

The objective and scope of each OSC audit is unique and does not entail a comprehensive review of a localgovernment’soperationsortherecordingofallfinancialactivity.Forexample,ourlastauditofthe City in 2013 was limited to procurement and cash receipts and would not have included a review ofthetrustandagencyfund.Assuch,OSCdidnotbecomeawareoftheCity’saccountingforhealthcareexpendituresanditsuseofthetrustandagencyfunduntilweconductedthisaudit.

Note3

Thefinancial reportspreparedfor theCouncilandavailable to thepublicdidnot includeaproperaccountingforhealthcareexpendituresand,assuch,didnotprovideatruedepictionoftheCity’soverall financial health. Further, the Comptroller provided us with the informationwe requested.However,healsoprovideduswithvaryingresponsespertainingtohowheaccountedandbudgetedfor health care costs using the trust and agency fund.

Note4

WescheduledmeetingswiththeCouncilPresidentandFinanceCommitteeChairinadvance.ThesemeetingswerenotintendedtoascertainifCityofficialsknewtheexactamountofmoneybeingheldinthetrustandagencyfund,butrathertoassessiftheywereawareofthemoneyinthetrustandagencyfund and how it was being used.

Note5

Onmultipleoccasions,includingduringtheexitdiscussion,CityofficialstoldusthatthesefundswereintentionallysegregatedsothattheCouncilwouldnotusethesefundstolowerpropertytaxes.

3131Division of LocaL Government anD schooL accountabiLity

APPENDIX C

AUDIT METHODOLOGY AND STANDARDS

TheobjectiveofourauditwastoreviewtheCity’sfinancialconditionfortheperiodJanuary1,2012throughAugust19,2016.Togainanunderstandingofcertain revenueandexpenditure trends,weextendedourreviewbackto2009.

To accomplish our audit objective and obtain valid audit evidence, our procedures included thefollowing:

• WereviewedtheCharter,AdministrativeCode,andanypoliciesandproceduresforinformationrelevanttofinancialandbudgetingactivities,fundbalancemanagementandmultiyearfinancialplanning,includingdeterminingthefiscalresponsibilitiesofCityofficialsandcommitteesorsubcommittees of the Council in this regard.

• We interviewed appropriate City officials to gain an understanding of the City’s financialconditionandtodeterminewhatprocessesareinplaceforfiscalmonitoring,budgeting,fundbalancemanagement,multiyearfinancialplanningandfinancialoversight.

• WereviewedminutesfromCouncil,financeandbudgetcommitteemeetingsandinterviewedCouncilmembers to determine and evaluate how theCouncil providesfinancial oversight,includingdeterminingwhatfinancialinformationispresentedtotheCouncil.

• WereviewedtheCity’saccountingrecordsforgovernmentaloperatingfundstoassessiftheywereaccuratebyverifyingthatbalancesheetaccounts(significantcurrentassetsandliabilities)wereproperlyrecordedandsupportedandthatrevenuesandexpendituresweresupportedandrecorded in the proper fund.

• Weanalyzedchangesinfundbalancewithinthegovernmentaloperatingfundsasaresultofoperations.Foranyfundsinfiscaldecline,weidentifiedfactorscontributingtothedecline.

• Weanalyzedcashflowanddocumentedfactorsimpactingcashflow.WeassessedtheCity’sability to liquidate current liabilities from available cash by comparing cash on hand at the end of the year in relation to current liabilities.

• Weanalyzedactualrevenueandexpendituretrendsandprojected2016and2017operatingresultsusinghistoricaltrendsandotherpertinentinformationprovidedbyCityofficials.

• We compared budget estimates to actual results to determine if revenue and appropriationestimates were reasonable.

• Weanalyzedsignificantbudget-to-actualvariancesandinterviewedCityofficialstodeterminethe methods and rationale used to develop estimates. We reviewed relevant supportingdocumentation for any estimates that appeared to be unreasonable or inaccurate.

32 Office Of the New YOrk State cOmptrOller32

• Wereviewedsignificantbudgetadjustments/modifications/transfersandinterviewedofficialstodeterminethecauseforanysignificantmodifications.

• Wecomparedbudgetestimatestohistoricaldata(actualrevenueandexpendituretrends)andsupporting documentation to determine if estimates were reasonable and the budgets were structurally balanced.

• Wereviewedrealproperty tax levydocumentationandanalyzedchanges in the tax levytoensuretheyappearedreasonableandsufficienttosupporttheadoptedbudgets.

• WereviewedtheCharterandAdministrativeCodeasitpertainstotheCity’spublicutilitiesand relevant laws and regulations. This helped us to gain an understanding of the relationship betweentheCityandtheBPU,theauthoritytooperateandmaintainpublicutilities,andthegoverning structure of the municipally-owned utilities.

• We interviewedappropriateCity andBPUofficials togain anunderstandingof theBPU’sfinancialoperationsandmanagement,relevantpoliciesandprocedures,andrelationshipwiththe City.

• Weattempted to review theBPU’s accounting records to analyze changes in fundbalanceasaresultofoperations,andanalyzecashflowandactualrevenueandexpendituretrendstodeterminethecurrentfinancialpositionofeachutility.Basedonthemissingrecordsandtheconditionoftherecordsremaining,wecouldnotbaseanyrelianceontheserecords.

WeconductedthisperformanceauditinaccordancewithGAGAS.Thosestandardsrequirethatweplanandperform theaudit toobtainsufficient,appropriateevidence toprovidea reasonablebasisforourfindingsandconclusionsbasedonourauditobjective.Webelievethattheevidenceobtainedprovidesareasonablebasisforourfindingsandconclusionsbasedonourauditobjective.

3333Division of LocaL Government anD schooL accountabiLity

APPENDIX D

HOW TO OBTAIN ADDITIONAL COPIES OF THE REPORT

OfficeoftheStateComptrollerPublicInformationOffice110StateStreet,15thFloorAlbany,NewYork12236(518) 474-4015http://www.osc.state.ny.us/localgov/

Toobtaincopiesofthisreport,writeorvisitourwebpage:

34 Office Of the New YOrk State cOmptrOller34

APPENDIX EOFFICE OF THE STATE COMPTROLLER

DIVISION OF LOCAL GOVERNMENTAND SCHOOL ACCOUNTABILITYAndrewA.SanFilippo,ExecutiveDeputyComptroller

GabrielF.Deyo,DeputyComptrollerTraceyHitchenBoyd,AssistantComptroller

LOCAL REGIONAL OFFICE LISTING

BINGHAMTON REGIONAL OFFICEH.ToddEames,ChiefExaminerOfficeoftheStateComptrollerStateOfficeBuilding,Suite170244 Hawley StreetBinghamton,NewYork13901-4417(607)721-8306Fax(607)721-8313Email:[email protected]

Serving:Broome,Chenango,Cortland,Delaware,Otsego,Schoharie,Sullivan,Tioga,TompkinsCounties

BUFFALO REGIONAL OFFICEJeffreyD.Mazula,ChiefExaminerOfficeoftheStateComptroller295MainStreet,Suite1032Buffalo,NewYork14203-2510(716)847-3647Fax(716)847-3643Email:[email protected]

Serving:Allegany,Cattaraugus,Chautauqua,Erie,Genesee,Niagara,Orleans,WyomingCounties

GLENS FALLS REGIONAL OFFICEJeffreyP.Leonard,ChiefExaminerOfficeoftheStateComptrollerOneBroadStreetPlazaGlensFalls,NewYork12801-4396(518)793-0057Fax(518)793-5797Email:[email protected]

Serving:Albany,Clinton,Essex,Franklin,Fulton,Hamilton,Montgomery,Rensselaer,Saratoga,Schenectady,Warren,WashingtonCounties

HAUPPAUGE REGIONAL OFFICEIraMcCracken,ChiefExaminerOfficeoftheStateComptrollerNYSOfficeBuilding,Room3A10250VeteransMemorialHighwayHauppauge,NewYork11788-5533(631)952-6534Fax(631)952-6530Email:[email protected]

Serving:NassauandSuffolkCounties

NEWBURGH REGIONAL OFFICETennehBlamah,ChiefExaminerOfficeoftheStateComptroller33AirportCenterDrive,Suite103NewWindsor,NewYork12553-4725(845)567-0858Fax(845)567-0080Email:[email protected]

Serving:Columbia,Dutchess,Greene,Orange,Putnam,Rockland,Ulster,WestchesterCounties

ROCHESTER REGIONAL OFFICEEdwardV.Grant,Jr.,ChiefExaminerOfficeoftheStateComptrollerThe Powers Building16WestMainStreet,Suite522Rochester,NewYork14614-1608(585)454-2460Fax(585)454-3545Email:[email protected]

Serving:Cayuga,Chemung,Livingston,Monroe,Ontario,Schuyler,Seneca,Steuben,Wayne,YatesCounties

SYRACUSE REGIONAL OFFICERebeccaWilcox,ChiefExaminerOfficeoftheStateComptrollerStateOfficeBuilding,Room409333E.WashingtonStreetSyracuse,NewYork13202-1428(315)428-4192Fax(315)426-2119Email:[email protected]

Serving:Herkimer,Jefferson,Lewis,Madison,Oneida,Onondaga,Oswego,St.LawrenceCounties

STATEWIDE AUDITSAnnC.Singer,ChiefExaminerStateOfficeBuilding,Suite170244 Hawley Street Binghamton,NewYork13901-4417(607)721-8306Fax(607)721-8313