Embed Size (px)

Citation preview

February 21, 2013

(Revised June 10, 2013)

Phase1:CommercialMarketSupplyandDemandAnalysis

CityofBurlingtonOfficialPlanReview– CommercialStrategyStudy

February21,2013

Ms.AndreaSmith,MCIP,RPPSeniorPlanner–Policy,PlanningandBuildingDepartmentCityofBurlington426BrantStreetBurlington,OntarioL7R3Z6

DearMs.Smith:

Re:CommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

urbanMetricsinc.ispleasedtosubmitourCommercialMarketSupplyandDemandAnalysisreporttotheCityofBurlington,whichprovidesasummaryofourfindingsastheyrelatetothesupplyofandfuturedemandforcommercialfacilitiesthroughouttheCityto2031.ThisbackgroundreporthasbeenpreparedaspartoftheCityofBurlington’sbroaderOfficialPlanReviewCommercialStrategyStudy,whichisbeingundertakenjointlybyurbanMetricsinc.andThePlanningPartnership,plusstafffromtheCityofBurlington’sPlanningandBuildingDepartment.

TheprimarypurposeofthisreportistoprovidecommercialmarketanalysistotheCityofBurlingtontoguidetheformationoffuturecommerciallandusepolicyrecommendations.Inparticular,thisreportquantifiesthefutureretailandservicecommercialspacerequirementsintheCityofBurlingtonto2031,andprovidesrecommendationsastohowfuturespacecanbeaccommodatedwithintheurbansystem.

Theanalysesandappendicesintheattachedreportprovideourdetailedstudyfindingsandconclusions.Thesefindingsandconclusionsrepresentourbestjudgement,basedontheinformationthatwasavailabletousatthetimeofourresearch.Accordingly,thefindings,conclusions,projections,andrecommendationspresentedhereinshouldbereviewedandinterpretedwithreferencetoevolvingcircumstancesandeconomicconditions.

IthasbeenapleasureconductingthispartoftheassignmentonbehalfoftheCityofBurlington,andwelookforwardtodiscussingourresults.

Yourstruly,urbanMetrics inc. RowanF.J.Faludi,CMC,MCIP,RPP,PLEPartner416‐351‐[email protected]

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

TABLE OF CONTENTS

EXECUTIVESUMMARY................................................................................................................................................................................................I

1 INTRODUCTION....................................................................................................................................................................................................1 1.1 BACKGROUND...................................................................................................................................................................................................................................................1 1.2 STUDYOBJECTIVES.........................................................................................................................................................................................................................................2 1.3 2003OFFICIALPLANREVIEWRETAILCOMMERCIALSTUDY................................................................................................................................................................3 1.4 APPROACH........................................................................................................................................................................................................................................................4 1.5 ASSUMPTIONS..................................................................................................................................................................................................................................................7

2 CITYOFBURLINGTON–GEOGRAPHYANDDEMOGRAPHICCHARACTERISTICS...........................................................................9 2.1 LOCATIONALCHARACTERISTICS...................................................................................................................................................................................................................9 2.1.1 Regionalcontext...............................................................................................................................................................................................................................................9 2.1.2 InternalTransportation............................................................................................................................................................................................................................10

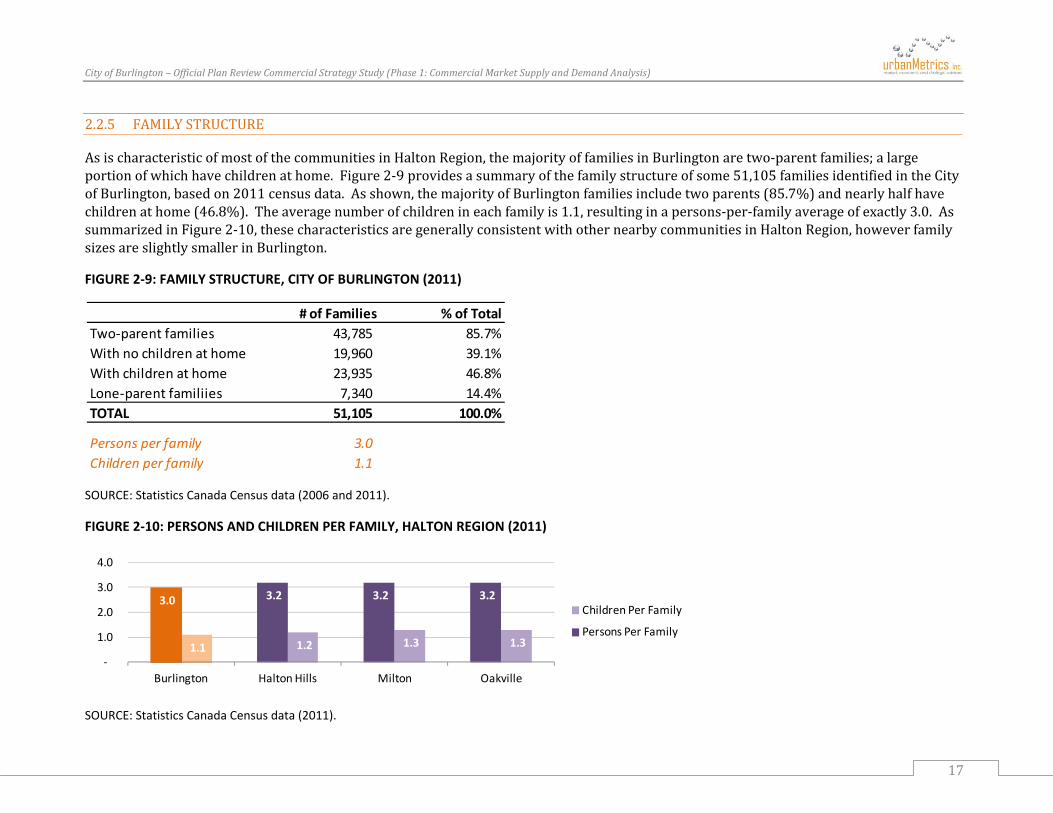

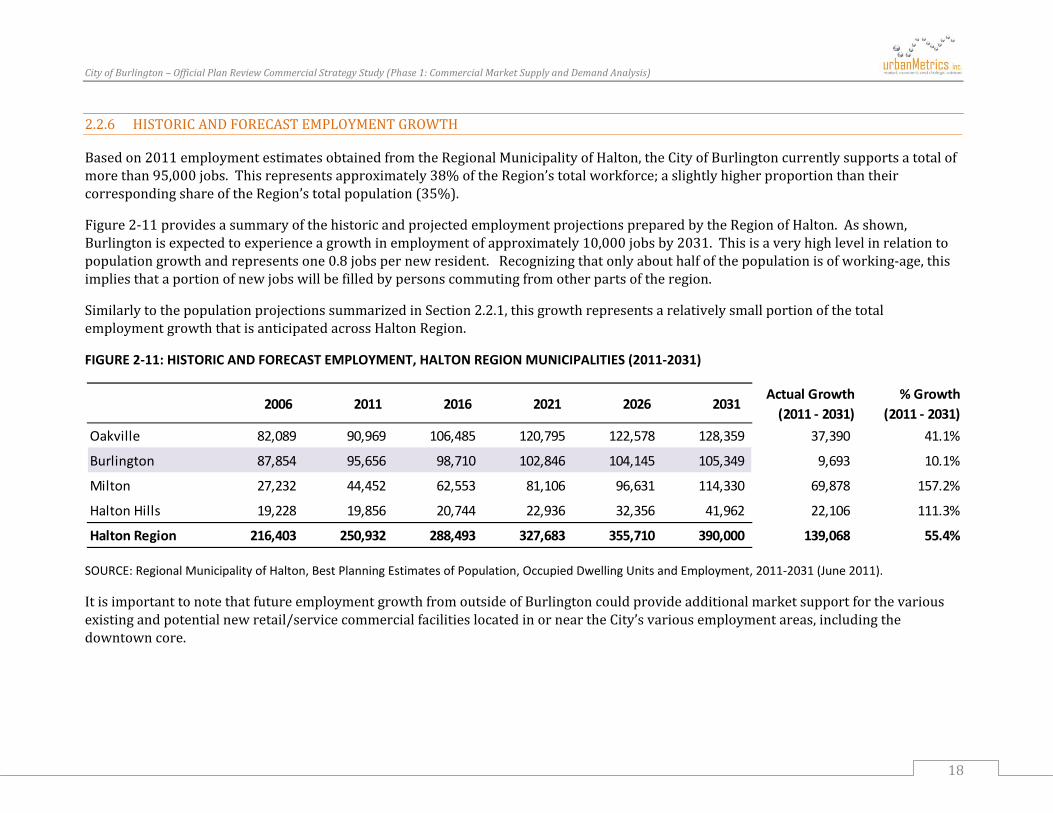

2.2 DEMOGRAPHICCHARACTERISTICS............................................................................................................................................................................................................11 2.2.1 HistoricandForecastPopulationGrowth.........................................................................................................................................................................................11 2.2.2 AgeStructure..................................................................................................................................................................................................................................................13 2.2.3 IncomeStructure..........................................................................................................................................................................................................................................14 2.2.4 Ethnicity............................................................................................................................................................................................................................................................16 2.2.5 FamilyStructure...........................................................................................................................................................................................................................................17 2.2.6 HistoricandForecastEmploymentGrowth.....................................................................................................................................................................................18

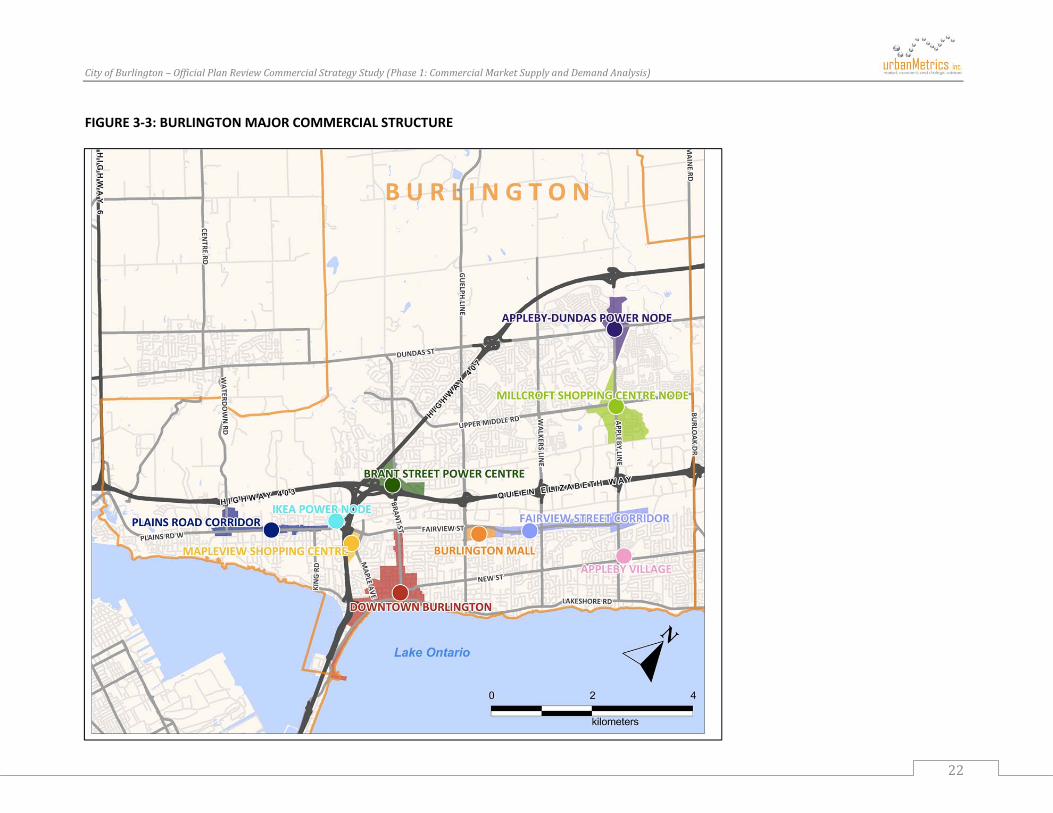

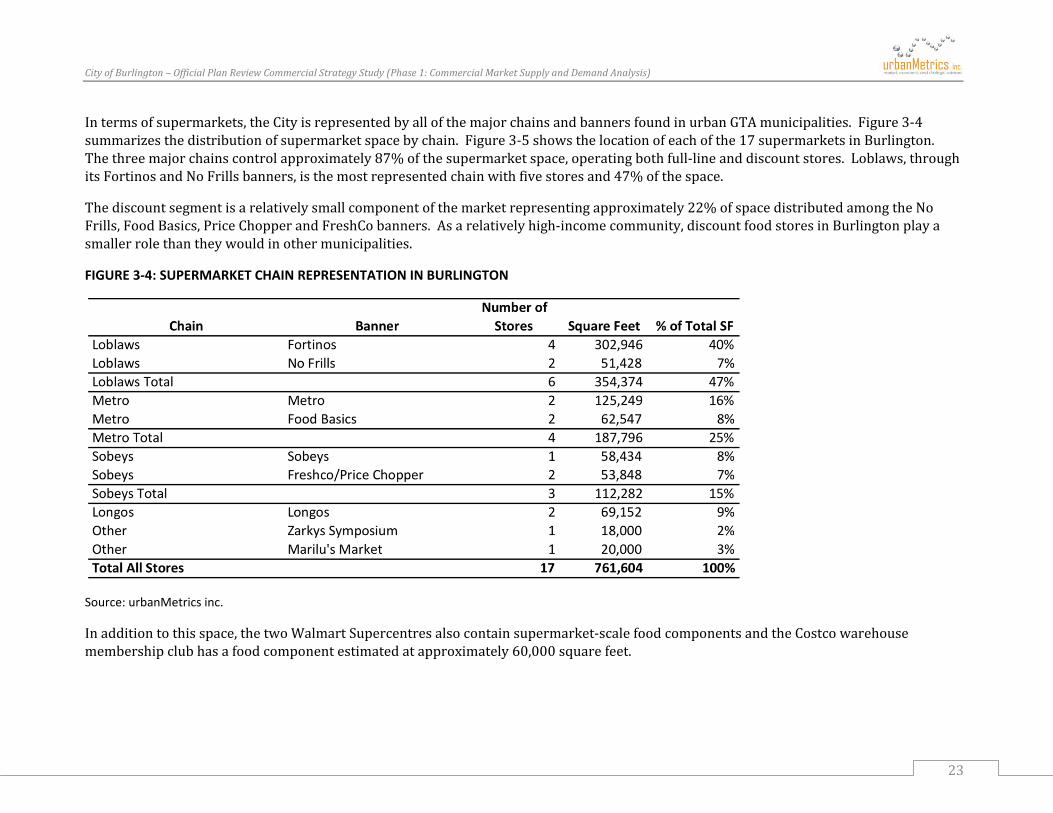

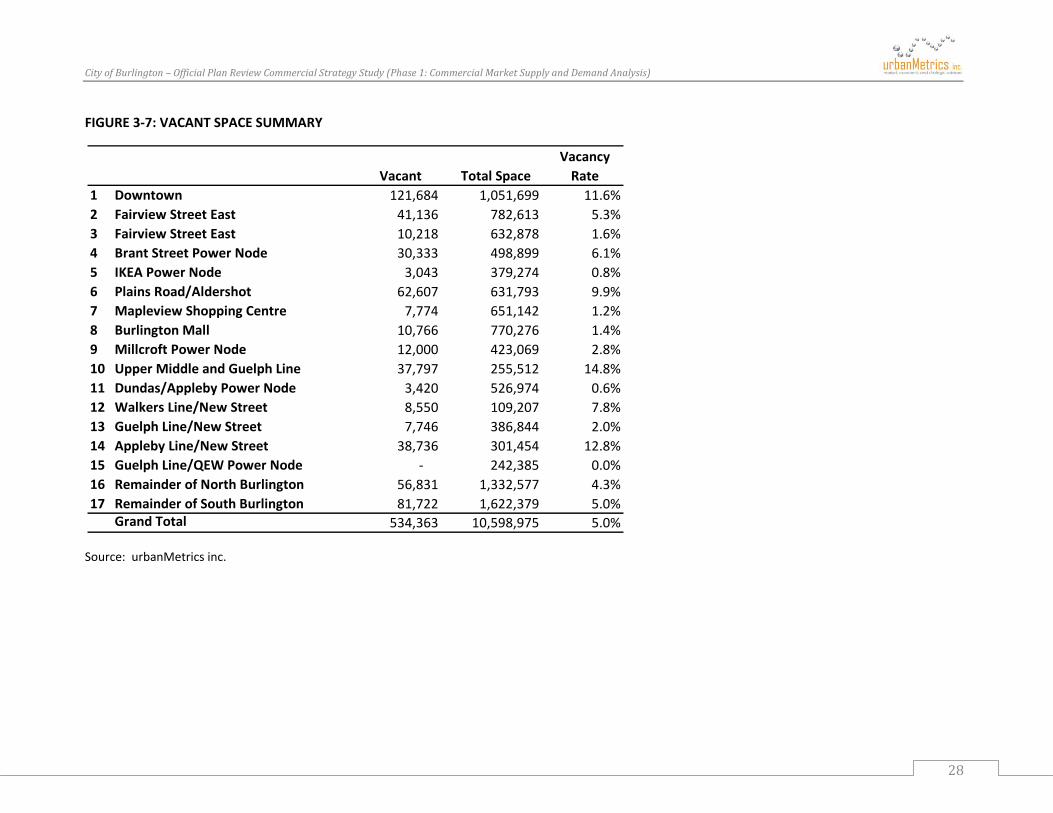

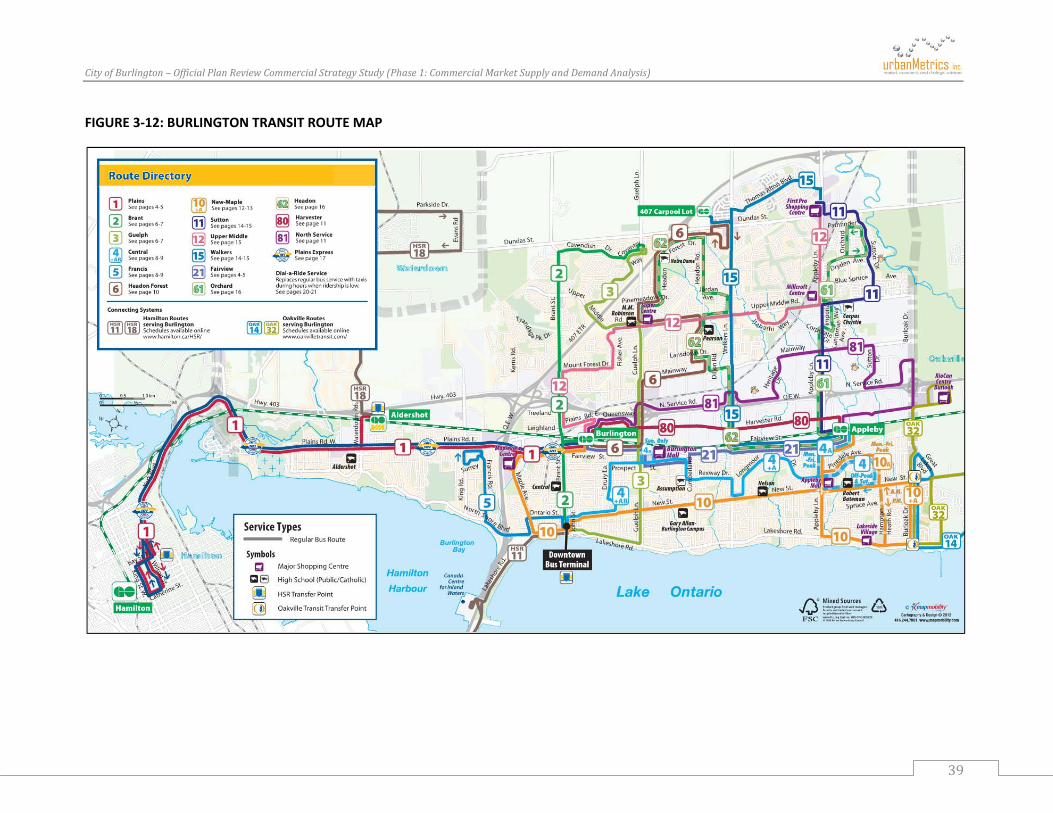

3 RETAILSTRUCTURE.........................................................................................................................................................................................19 3.1 INVENTORY....................................................................................................................................................................................................................................................19 3.2 INVENTORYOFVACANTSPACE..................................................................................................................................................................................................................27 3.3 CHANGEINCOMMERCIALSPACESINCE2002........................................................................................................................................................................................29 3.4 COMMERCIALSPACEPERCAPITA.............................................................................................................................................................................................................32 3.5 INVENTORYINRELATIONTOTHEACTIVETRANSPORTATIONNETWORK.........................................................................................................................................37 3.5.1 TransitAccessibility.....................................................................................................................................................................................................................................37 3.5.2 Walkability.......................................................................................................................................................................................................................................................37 3.5.3 CyclingandRecreationTrailNetwork...............................................................................................................................................................................................37

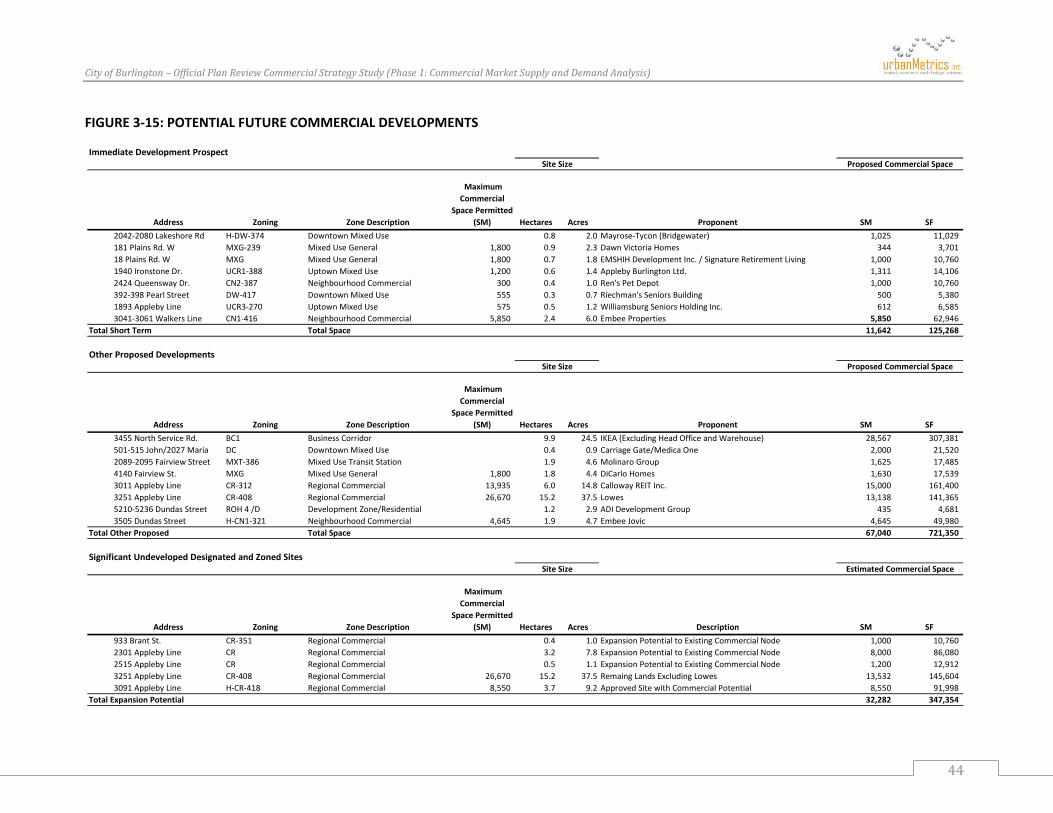

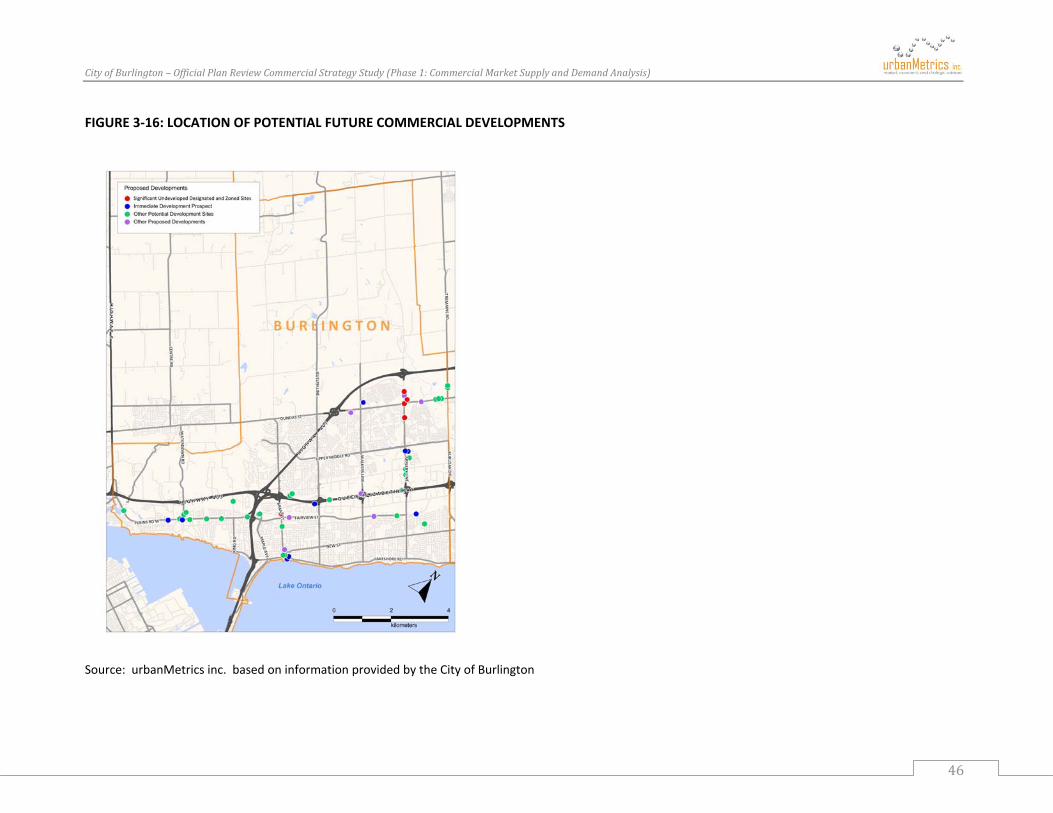

3.6 POTENTIALFUTURECOMMERCIALDEVELOPMENTS.............................................................................................................................................................................42

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

3.7 COMPETITIVERETAILFACILITIESOUTSIDEBURLINGTON....................................................................................................................................................................47

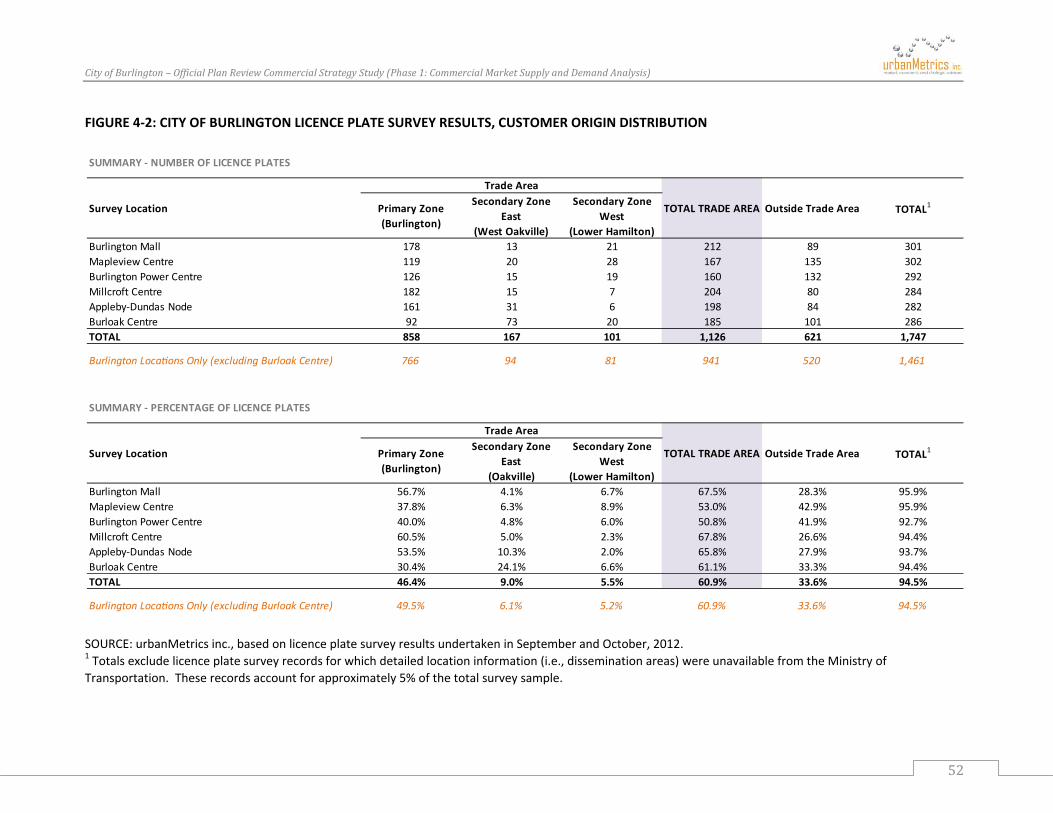

4 THECITYOFBURLINGTON’STRADEAREA..............................................................................................................................................49 4.1 TRADEAREADEFINED................................................................................................................................................................................................................................49 4.1.1 LicencePlateSurveys..................................................................................................................................................................................................................................49 4.1.2 DowntownSurveyOrigins........................................................................................................................................................................................................................53

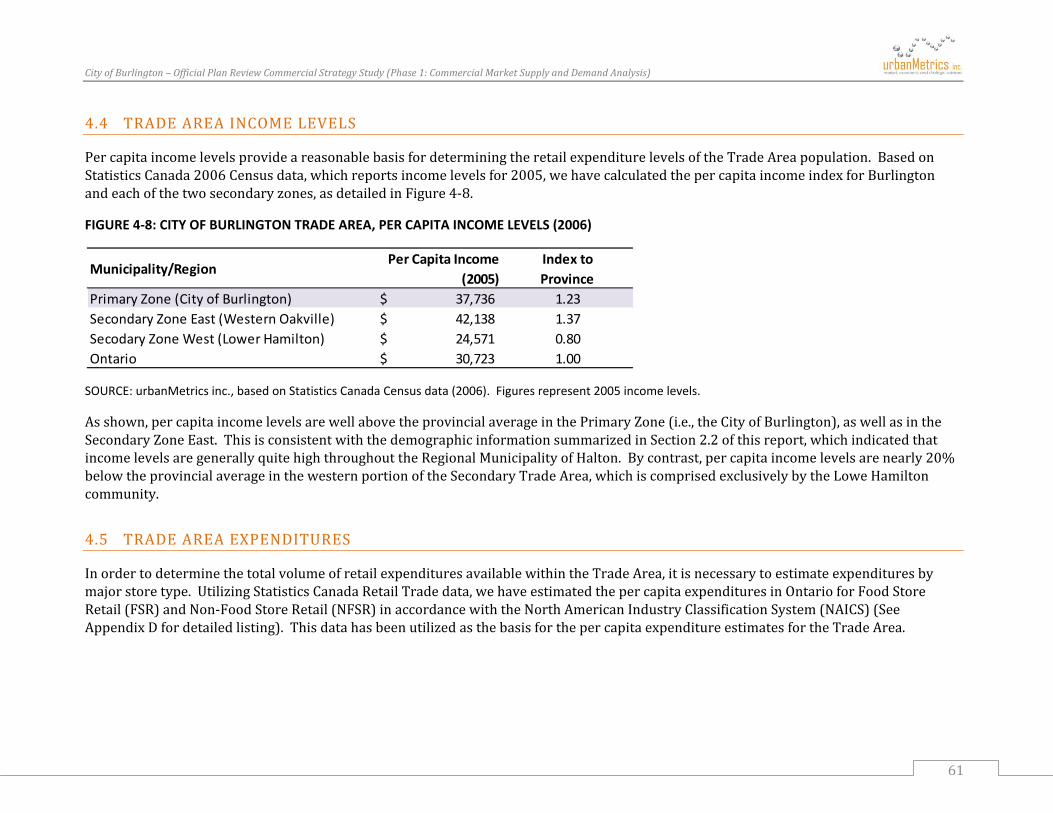

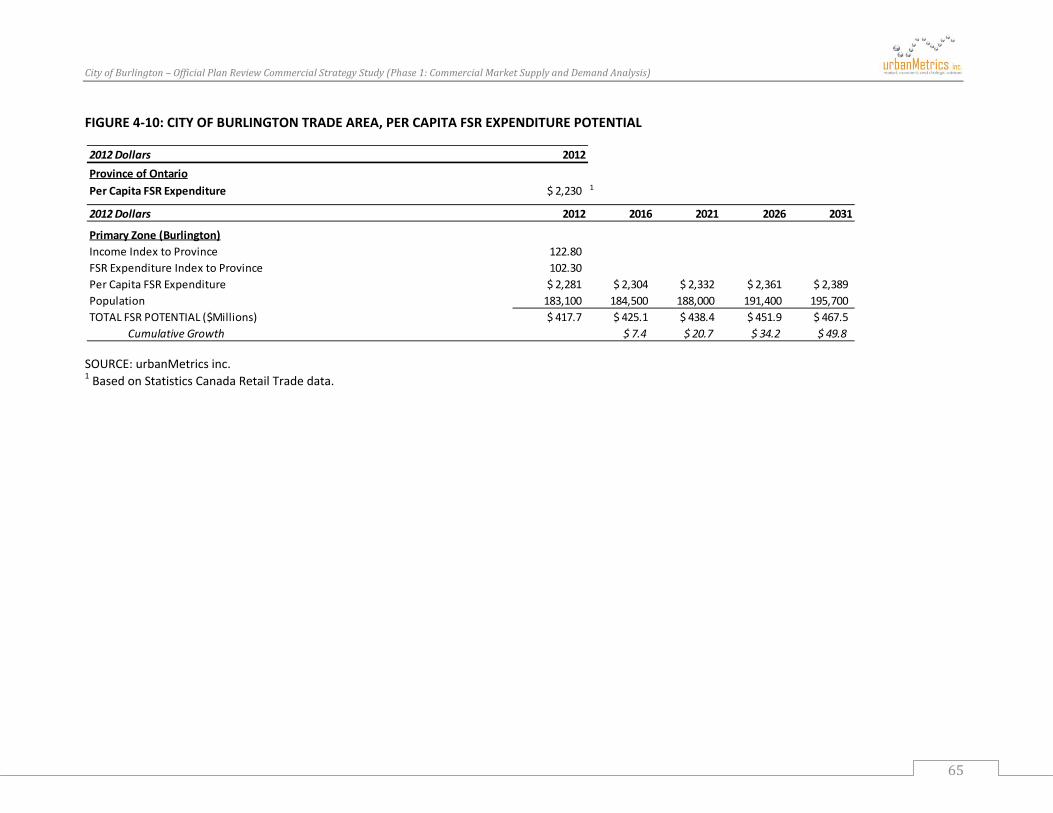

4.2 BURLINGTONTRADEAREA........................................................................................................................................................................................................................55 4.3 TRADEAREAPOPULATIONPROJECTIONS................................................................................................................................................................................................59 4.4 TRADEAREAINCOMELEVELS...................................................................................................................................................................................................................61 4.5 TRADEAREAEXPENDITURES.....................................................................................................................................................................................................................61 4.5.1 PerCapitaNon‐FoodStoreRetail(NFSR)Expenditures............................................................................................................................................................62 4.5.2 PerCapitaFoodStoreRetail(FSR)Expenditures.........................................................................................................................................................................64

5 BURLINGTONRESIDENTSSHOPPINGPATTERNS..................................................................................................................................66 5.1 DISTRIBUTIONOFBURLINGTONRESIDENTS’EXPENDITURES(2012)..............................................................................................................................................66 5.2 ONLINESHOPPING.......................................................................................................................................................................................................................................70

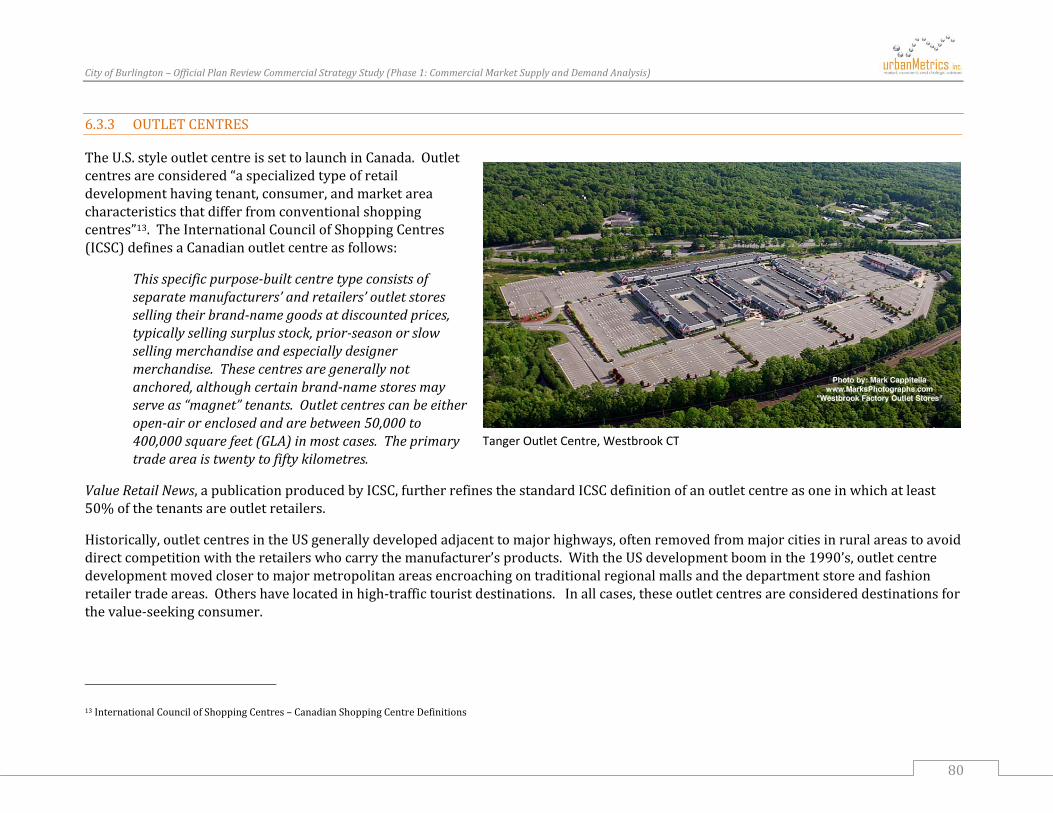

6 COMMERCIALTRENDS....................................................................................................................................................................................72 6.1 POWERCENTRESANDLARGEFORMATRETAILERS...............................................................................................................................................................................73 6.2 THEBROADENINGOFSHOPPINGCENTREMERCHANDISING...............................................................................................................................................................75 6.3 NEWDEVELOPMENTCONCEPTS...............................................................................................................................................................................................................75 6.3.1 LifestyleandHybridCentres....................................................................................................................................................................................................................75 6.3.2 NewUrbanism................................................................................................................................................................................................................................................78 6.3.3 OutletCentres.................................................................................................................................................................................................................................................80

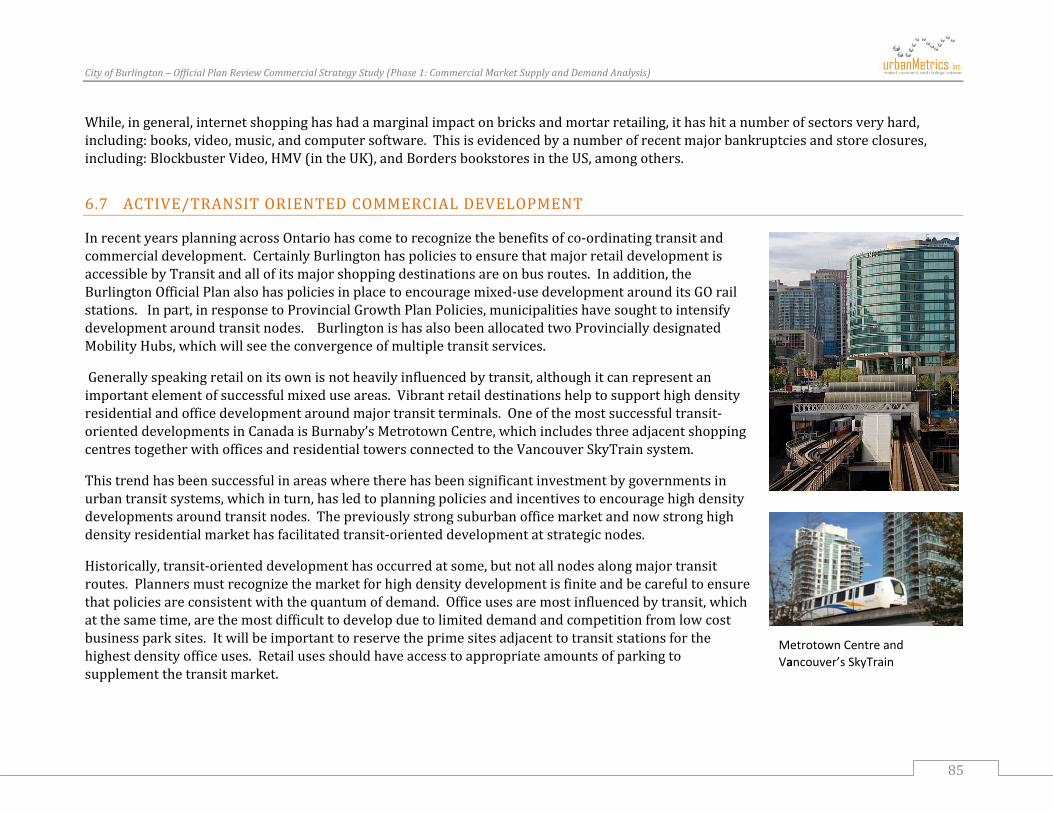

6.4 FOREIGNRETAILERS–THEUSINVASION................................................................................................................................................................................................82 6.5 BLURRINGOFTHERETAILHIERARCHY....................................................................................................................................................................................................83 6.6 NON‐STORERETAILING..............................................................................................................................................................................................................................84 6.7 ACTIVE/TRANSITORIENTEDCOMMERCIALDEVELOPMENT...............................................................................................................................................................85 6.8 SUMMARY......................................................................................................................................................................................................................................................86

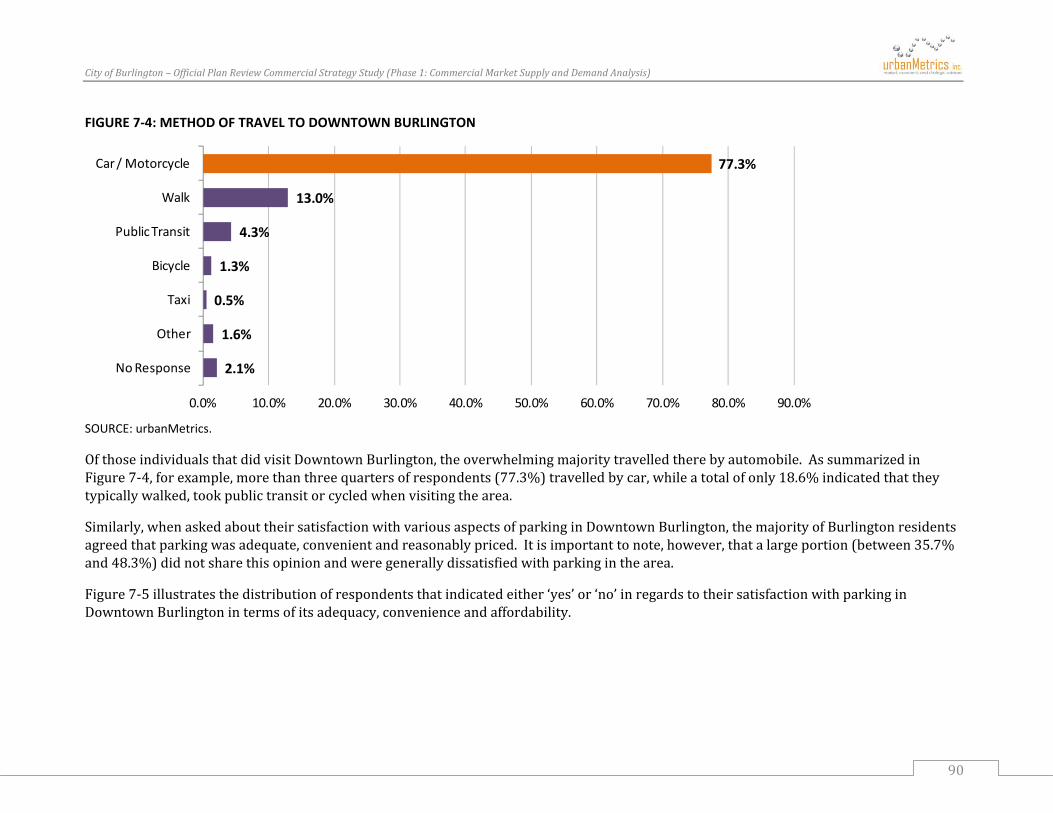

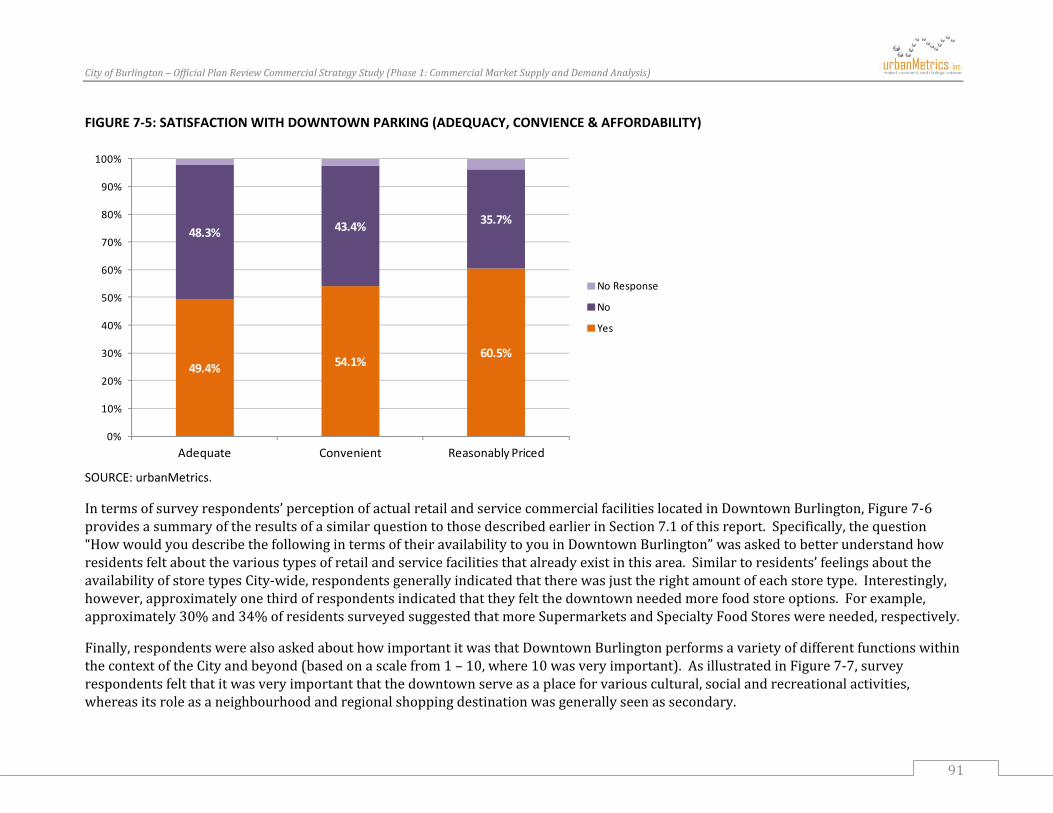

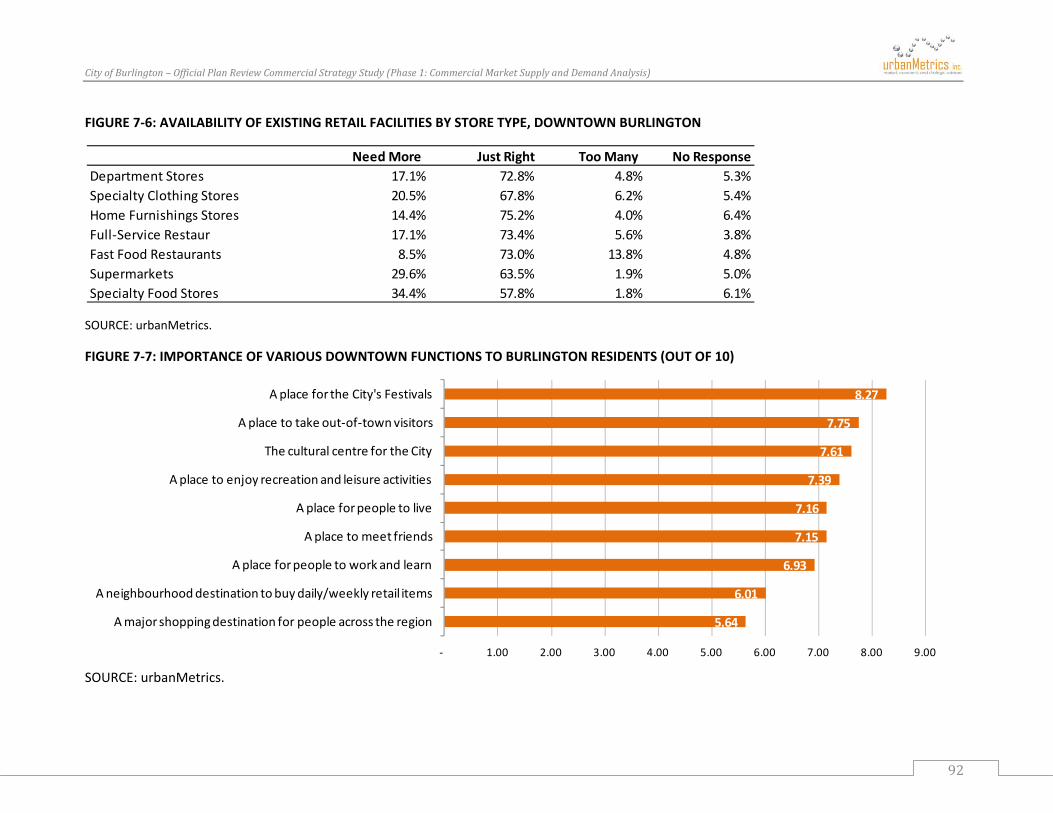

7 BURLINGTONRESIDENTSRETAILDESIRESANDPREFERENCES.....................................................................................................88 7.1 BURLINGTONRESIDENTS’PERCEPTIONSOFBURLINGTONSHOPPINGFACILITIES..........................................................................................................................88 7.2 BURLINGTONRESIDENTS’PERCEPTIONSOFDOWNTOWNBURLINGTON..........................................................................................................................................89

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

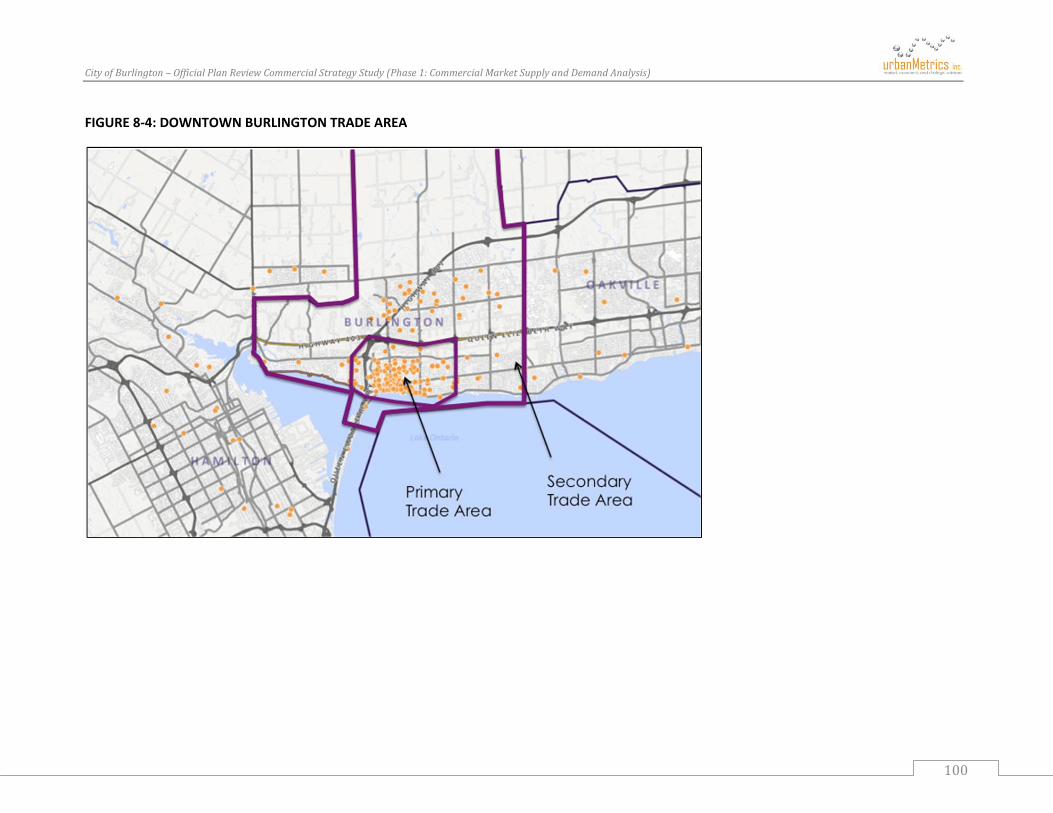

8 ROLEOFDOWNTOWNBURLINGTON.........................................................................................................................................................94 8.1 DOWNTOWNTRADEAREA..........................................................................................................................................................................................................................98

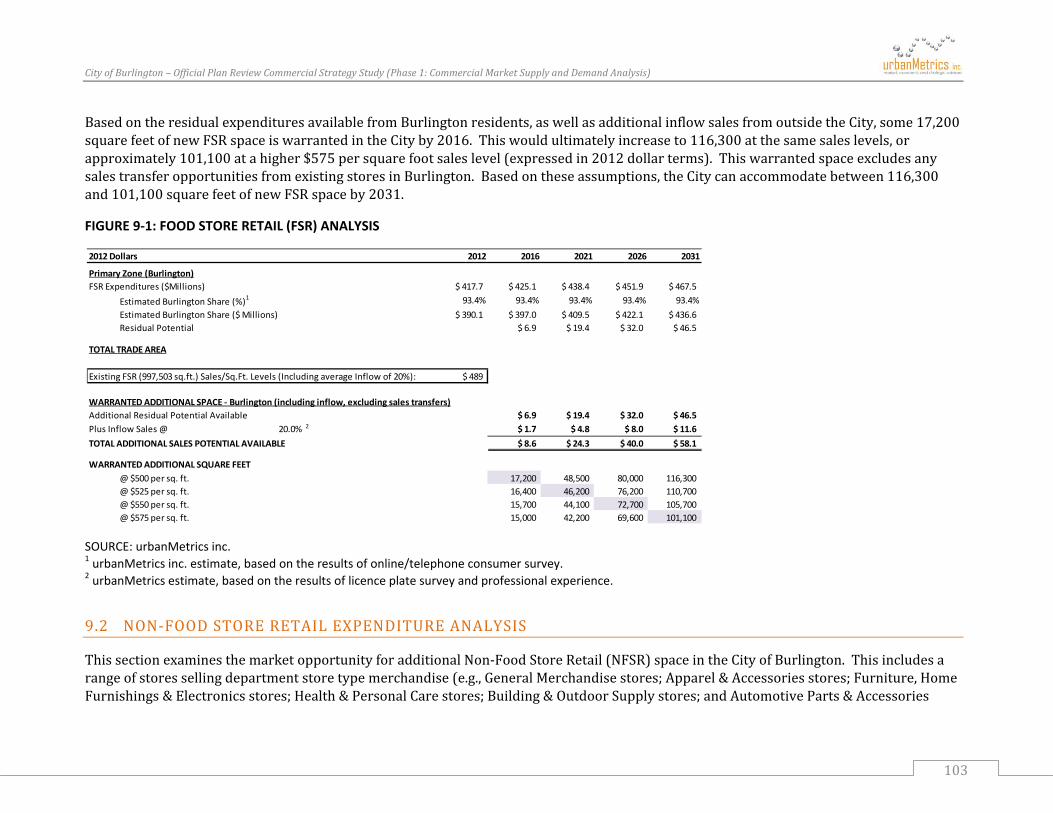

9 FUTUREWARRANTEDSPACEANALYSIS.................................................................................................................................................101 9.1 FOODSTORERETAILEXPENDITUREANALYSIS....................................................................................................................................................................................102 9.1.1 CItyofBurlingtonShare.........................................................................................................................................................................................................................102 9.1.2 ResidualExpenditurePotentialfromBurlingtonResidents..................................................................................................................................................102 9.1.3 MarketOpportunityforFSRSpace....................................................................................................................................................................................................102

9.2 NON‐FOODSTORERETAILEXPENDITUREANALYSIS..........................................................................................................................................................................103 9.2.1 CItyofBurlingtonandSecondaryTradeAreaShares..............................................................................................................................................................104 9.2.2 ResidualExpenditurePotentialfromTradeAreaResidents.................................................................................................................................................104 9.2.3 MarketOpportunityforNFSRSpace................................................................................................................................................................................................106

9.3 OTHERSELECTEDRETAILANDSERVICESPACEPOTENTIAL.............................................................................................................................................................106 9.4 SUMMARYOFADDITIONALWARRANTEDCOMMERCIALSPACE........................................................................................................................................................108

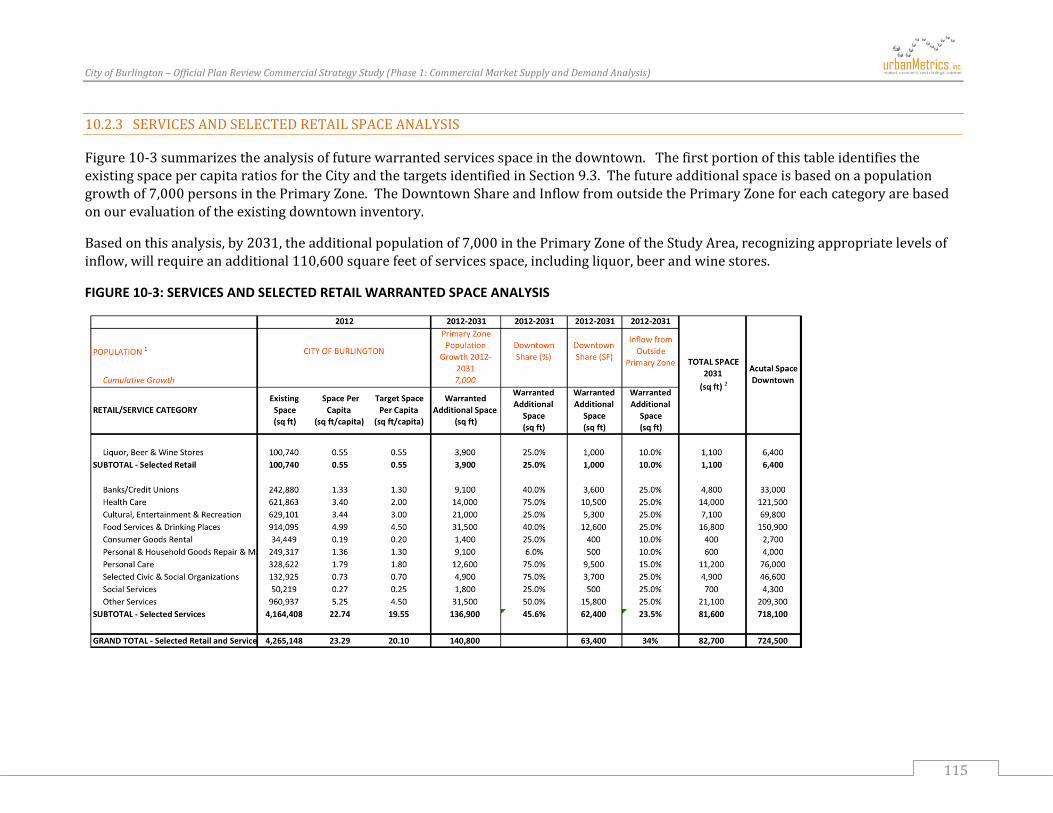

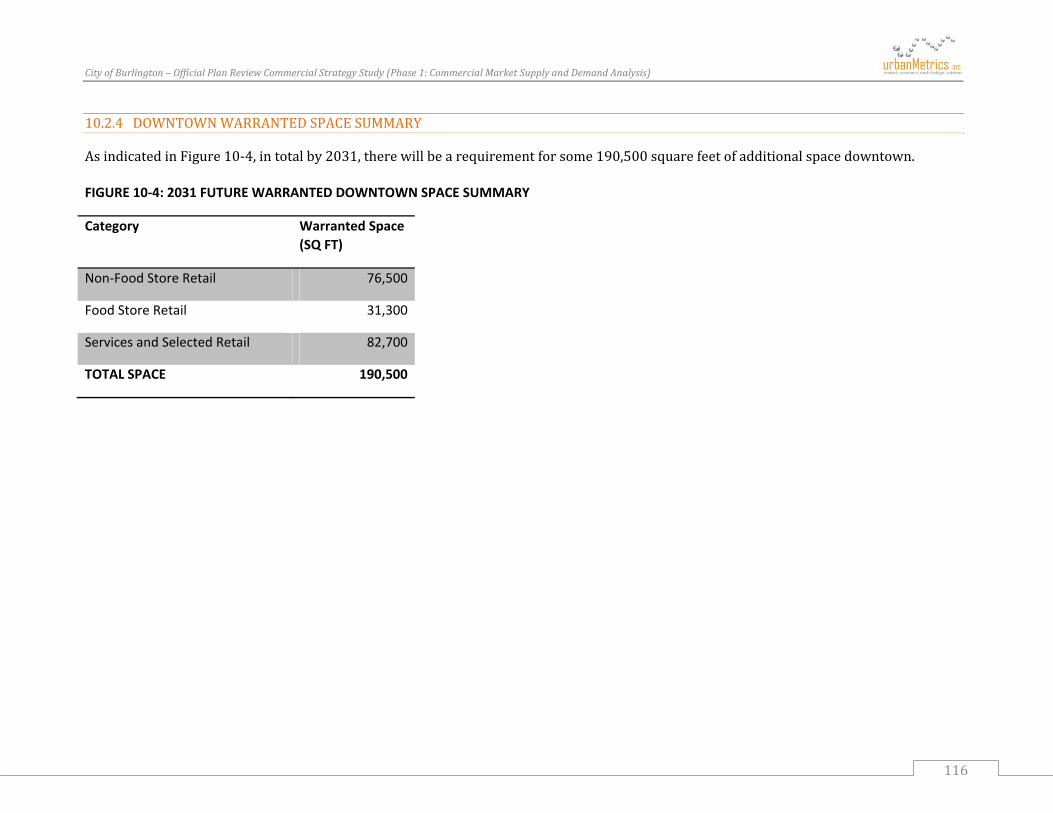

10 DOWNTOWNMARKETANALYSIS..............................................................................................................................................................110 10.1 DOWNTOWNPRIMARYTRADEAREAPOPULATIONGROWTH...............................................................................................................................................................110 10.2 PROJECTEDFUTUREWARRANTEDSPACEINTHEDOWNTOWN........................................................................................................................................................111 10.2.1 Non‐FoodStoreRetailAnalysis...........................................................................................................................................................................................................111 10.2.2 FoodStoreRetailAnalysis.....................................................................................................................................................................................................................113 10.2.3 ServicesandSelectedretailSpaceAnalysis...................................................................................................................................................................................115 10.2.4 DowntownWarrantedSpaceSummary.........................................................................................................................................................................................116

11 SUPPLYANDDEMANDRECONCILIATION...............................................................................................................................................117

12 CONCLUSIONS...................................................................................................................................................................................................119

APPENDIXA–LICENCEPLATESURVEYRESULTS.......................................................................................................................................123

APPENDIXB–ONLINE/TELEPHONECONSUMERSURVEYRESULTS....................................................................................................132

APPENDIXC–INVENTORYOFCOMMERCIALSPACE.................................................................................................................................159

APPENDIXD–BACKGROUNDDATAANDDEFINITIONOFTERMS........................................................................................................161

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

L I ST OF F IGURES FigureES‐1:SummaryofFutureWarrantedSpaceinBurlington(2012‐2031)..............................................................................................................................vi FigureES‐2:SummaryofSupplyandDemandReconciliation...............................................................................................................................................................vii Figure2‐1:CityofBurlingtonRegionalContext.............................................................................................................................................................................................9 Figure2‐2BurlingtonStreetNetwork.............................................................................................................................................................................................................10 Figure2‐3:HistoricPopulation,CityofBurlington(2006‐2011).........................................................................................................................................................12 Figure2‐4:ForecastPopulation,HaltonRegionMunicipalities(2011‐2031)................................................................................................................................12 Figure2‐5:CityofBurlingtonAgeDistribution(2006–2011).............................................................................................................................................................13 Figure2‐6:PerCapitaIncome,HaltonRegionMunicipalities(2006)................................................................................................................................................14 Figure2‐7:PerCapitaIncomeIndextoProvincebyDisseminationArea,CItyofBurlington(2006)..................................................................................15 Figure2‐8:Top5EthnicOrigins,CityofBurlington(2006)...................................................................................................................................................................16 Figure2‐9:FamilyStructure,CItyofBurlington(2011)..........................................................................................................................................................................17 Figure2‐10:PersonsandChildrenperFamily,HaltonRegion(2011)..............................................................................................................................................17 Figure2‐11:HistoricandForecastEmployment,HaltonRegionMunicipalities(2011‐2031)...............................................................................................18 Figure3‐1:BurlingtonCommercialSpaceInventory(squarefeet).....................................................................................................................................................20 Figure3‐2:BurlingtonCommercialSpaceInventoryLocations...........................................................................................................................................................21 Figure3‐3:BurlingtonMajorCommercialStructure.................................................................................................................................................................................22 Figure3‐4:SupermarketChainRepresentationinBurlington..............................................................................................................................................................23 Figure3‐5:SupermarketsinBurlington.........................................................................................................................................................................................................25 Figure3‐6:TwoKilometreDistanceAroundSupermarkets..................................................................................................................................................................26 Figure3‐7:VacantSpaceSummary...................................................................................................................................................................................................................28 Figure3‐8:CityofBurlingtonChangeinCommercialSpace2002‐2012(squarefeet)...............................................................................................................31 Figure3‐9:CityofBurlingtonPerCapitaCommercialSpace.................................................................................................................................................................34 Figure3‐10:PerCapitaRetailSpaceinSelectedGTAMunicipalities.................................................................................................................................................35 Figure3‐11:PerCapitaFoodServicesandDrinkingSpaceinSelectedGTAMunicipalities.....................................................................................................36 Figure3‐12:BurlingtonTransitRouteMap...................................................................................................................................................................................................39 Figure3‐13:400MetreRadiusAroundSupermarkets.............................................................................................................................................................................40 Figure3‐14:MajorretailnodesandBurlington’sCycle/Trailnetwork............................................................................................................................................41 Figure3‐15:PotentialFutureCommercialDevelopments......................................................................................................................................................................44 Figure3‐16:LocationofPotentialFutureCommercialDevelopments..............................................................................................................................................46 Figure4‐1:CityofBurlingtonLicencePlateSurveyResults,MapofCustomerOrigins..............................................................................................................51 Figure4‐2:CityofBurlingtonLicencePlateSurveyResults,CustomerOriginDistribution.....................................................................................................52 Figure4‐3:DowntownBurlingtonOn‐StreetInterceptSurveyResults,RespondentOriginDistribution.........................................................................53

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

Figure4‐4:DowntownBurlingtonOn‐StreetInterceptSurveyResults,MapofRespondentOrigins..................................................................................54 Figure4‐5:CityofBurlingtonTradeArea......................................................................................................................................................................................................56 Figure4‐6:2003and2012BurlingtonTradeareas...................................................................................................................................................................................58 Figure4‐7:CityofBurlingtonTradeArea,HistoricandForecastPopulation(2006‐2031).....................................................................................................60 Figure4‐8:CityofBurlingtonTradeArea,PerCapitaIncomeLevels(2006).................................................................................................................................61 Figure4‐9:CityofBurlingtonTradeArea,PerCapitaNFSRExpenditurePotential....................................................................................................................63 Figure4‐10:CityofBurlingtonTradeArea,PerCapitaFSRExpenditurePotential.....................................................................................................................65 Figure5‐1:Online/TelephoneConsumerSurvey,MajorRetailNodes..............................................................................................................................................68 Figure5‐2:DistributionofBurlingtonResidents’ExpendituresbyREtailArea&StoreCategory(NFSR)........................................................................69 Figure5‐3:DistributionofBurlingtonResidents’ExpendituresbyREtailArea&StoreCategory(FSR+Restaurants)..............................................70 Figure5‐5:DistributionofOnlineExpendituresbyCategory(ValueofExpenditures)..............................................................................................................71 Figure5‐4:PrevalanceofOnlineShoppingAmongSurveyRespondents(MadeOn‐LinePurchaseinpastmonth)......................................................71 Figure7‐1:AvailabilityofExistingRetailFacilitiesbyStoreFormat,CityofBurlington...........................................................................................................88 Figure7‐2:AvailabilityofExistingRetailFacilitiesbyStoreType,CityofBurlington................................................................................................................89 Figure7‐3:FrequencyofVisitstoDowntownBurlington,Day&Evening.......................................................................................................................................89 Figure7‐4:MethodofTraveltoDowntownBurlington...........................................................................................................................................................................90 Figure7‐5:SatisfactionwithDowntownParking(Adequacy,Convience&Affordability)........................................................................................................91 Figure7‐6:AvailabilityofExistingRetailFacilitiesbyStoreType,DowntownBurlington......................................................................................................92 Figure7‐7:ImportanceofVariousDowntownFunctionstoBurlingtonResidents(Outof10)..............................................................................................92 Figure8‐1:ReasonsforVisitingDowntownBurlington,On‐StreetInterceptSurveys...............................................................................................................95 Figure8‐2:MapofDowntownBurlington......................................................................................................................................................................................................97 Figure8‐3:distributionofdowntownburlingtonvisitors.....................................................................................................................................................................98 Figure8‐4:downtownburlingtontradearea............................................................................................................................................................................................100 Figure9‐1:FoodStoreRetail(FSR)Analysis.............................................................................................................................................................................................103 Figure9‐2:Non‐FoodStoreRetail(FSR)Analysis...................................................................................................................................................................................105 Figure9‐3:WarrantedAdditionalRetailandServiceSpaceinBurlington(2012‐2031)......................................................................................................108 Figure9‐4:SummaryofFutureWarrantedSpaceinBurlington(2012–2031)........................................................................................................................109 Figure10‐1:DowntownWarrantedNFSRSpaceProjection...............................................................................................................................................................112 Figure10‐2:DowntownWarrantedFSRSpaceProjection..................................................................................................................................................................114 Figure10‐3:ServicesandSelectedRetailWarrantedSpaceAnalysis.............................................................................................................................................115 Figure10‐4:2031FutureWarrantedDowntownSpaceSummary..................................................................................................................................................116 Figure11‐1:SupplyandDemandReconciliation.....................................................................................................................................................................................118 FigureA‐1:CustomerOriginSurveyResults,2012(NumberofLicencePlates)........................................................................................................................124 FigureA‐2:CustomerOriginSurveyResults,2012(PercentageofLicencePlates)..................................................................................................................125

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

FigureA‐3:MapofCustomerOriginLicencePlateSurveyResults(MapleviewCentre).........................................................................................................126 FigureA‐4:MapofCustomerOriginLicencePlateSurveyResults(MapleviewCentre).........................................................................................................127 FigureA‐5:MapofCustomerOriginLicencePlateSurveyResults(BurlingtonPowerCentre)...........................................................................................128 FigureA‐6:MapofCustomerOriginLicencePlateSurveyResults(MillcroftCentre)..............................................................................................................129 FigureA‐7:MapofCustomerOriginLicencePlateSurveyResults(Appleby‐DundasPowerNode).................................................................................130 FigureA‐8:MapofCustomerOriginLicencePlateSurveyResults(BurloakCentre)...............................................................................................................131 FigureB‐1:Online/TelephoneConsumerSurveys,DemographicCharacteristics.....................................................................................................................133 FigureB‐2:Online/TelephoneConsumerSurveys,NFSRExpenditursbyBurlingtonResidents(WEIGHTED)...........................................................134 FigureB‐3:Online/TelephoneConsumerSurveys,FSR&RestaurantExpenditursbyBurlingtonResidents(WEIGHTED)...................................135 FigureB‐4:Online/TelephoneConsumerSurveys,SurveyQuestionnaire....................................................................................................................................136 FigureC‐1:InventoryofBurlingtonCommercialSpacebyRetailCategoryandMajorRetailNode...................................................................................159 FigureD‐1:OntarioRetailTrade–AveragePerCapitaExpendituresbyRetailCategory(2012).......................................................................................163 FigureD‐2:ProvinceofOntarioIncome/ExpenditureRegressionEquations,2010.................................................................................................................164 FigureD‐3:ProvinceofOntario,HistoricRealGrowthinFoodStoreRetail(FSR)Expenditures.......................................................................................165 FigureD‐4:ProvinceofOntario,HistoricRealGrowthinNon‐FoodStoreRetail(NFSR)Expenditures..........................................................................166 FigureD‐5:Retail/ServiceStoreClassification,BasedonNorthAmericanIndustryClassificationSystem(NAICS)..................................................167

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

i

EXECUTIVESUMMARY

urbanMetricsinc.andThePlanningPartnershiphavebeenretainedbytheCityofBurlingtontoundertakeaCommercialStrategyStudy,whichisbeingpreparedaspartoftheCity’songoingOfficialPlanReviewprocess.TheCommercialStrategyStudyisintendedtore‐evaluatethecommercialpoliciesoftheCityofBurlingtonOfficialPlaninordertoaddressStrategicPlandirections,andtoensurethat:

TheCity’spoliciesaddresscurrentandfuturecommerciallanduseneeds;

Commercialareascanbeeffectivelyandefficientlyplanned;

Policiesarereflectiveofrecentchangestocommerciallanduseplanningandothertrends;and,

Policiescanbeeffectivelyimplemented.

AspartofPhase1ofthisbroaderCommercialStrategyStudy,urbanMetricshaspreparedthefollowingCommercialMarketSupplyandDemandAnalysisbackgroundreport,whichisintendedtoprovidetherequiredcommercialmarketanalysistoguidetheformationoffuturecommerciallandusepolicyrecommendations.Inparticular,thisreportquantifiesthefutureretailandservicecommercialspacerequirementsintheCityofBurlingtonto2031,andprovidesrecommendationsastohowfuturespacecanbeaccommodatedwithintheurbansystemduringthistimeperiod.

Thefollowingprovidesabriefoverviewofourkeyresearchfindingsandconclusions.

REPORTFINDINGS

BURLINGTON’SCOMMERCIALMARKETCHARACTERISTICS

Basedon2011CensusdataandpopulationestimatespreparedbytheRegionalMunicipalityofHalton,thecurrentpopulationofBurlingtonisapproximately183,1001.Thislevelofpopulationprovidesthecriticalmasstomaintainthefullrangeofretailandservicefacilitiesinthecommercialhierarchy.

1Includesadjustmentsforcensusundercount,asdetailedinSection4.3ofthisreport.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

ii

Inrecentyears,theCityofBurlingtonhasexperiencedmoderatepopulationgrowth;increasingbyanestimated2,520individualsduringthepreviousinter‐censusperiod(i.e.,2006to2011).Thisrepresentsanaverageannualgrowthrateof1.3%.

By2031,Burlington’spopulationisforecasttoreachatotalofapproximately195,700persons,representingtotalmarketgrowthof12,600residentsbetween2012and2031.ThisadditionalmarketgrowthwillultimatelyincreasethedemandfornewretailandservicecommercialfacilitiesintheCity.

AstheCityisquicklyapproachingitsGreenfieldcapacity,thelargestshareofresidentialgrowthwillbeattractedtointensificationsites:includingthedowntownUrbanGrowthCentre;UrbanGrowthCorridorsalongPlainsRoadandFairviewStreet;andmixeduseareasaroundtheexistingmallsandGOrailstations.

IncomelevelsinBurlington,andinthebalanceofHaltonRegion,arewellabovetheaveragefortheProvinceofOntarioasawhole.Basedon2006Censusdata,forexample,percapitaincomelevelsintheCityofBurlingtonwereapproximately23%higherthantheProvincialaveragein2005.ThisindicatesthatthereissignificantindividualspendingpoweramongBurlingtonresidents.

BURLINGTON’SEXISTINGCOMMERCIALSTRUCTURE

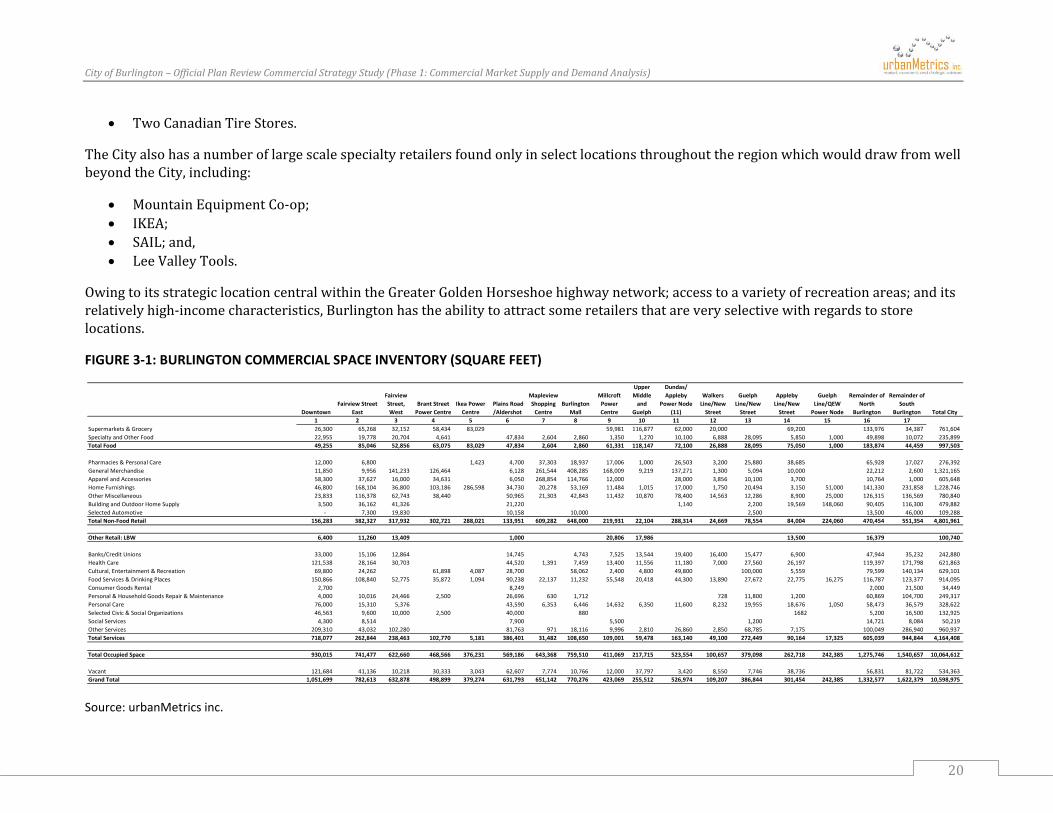

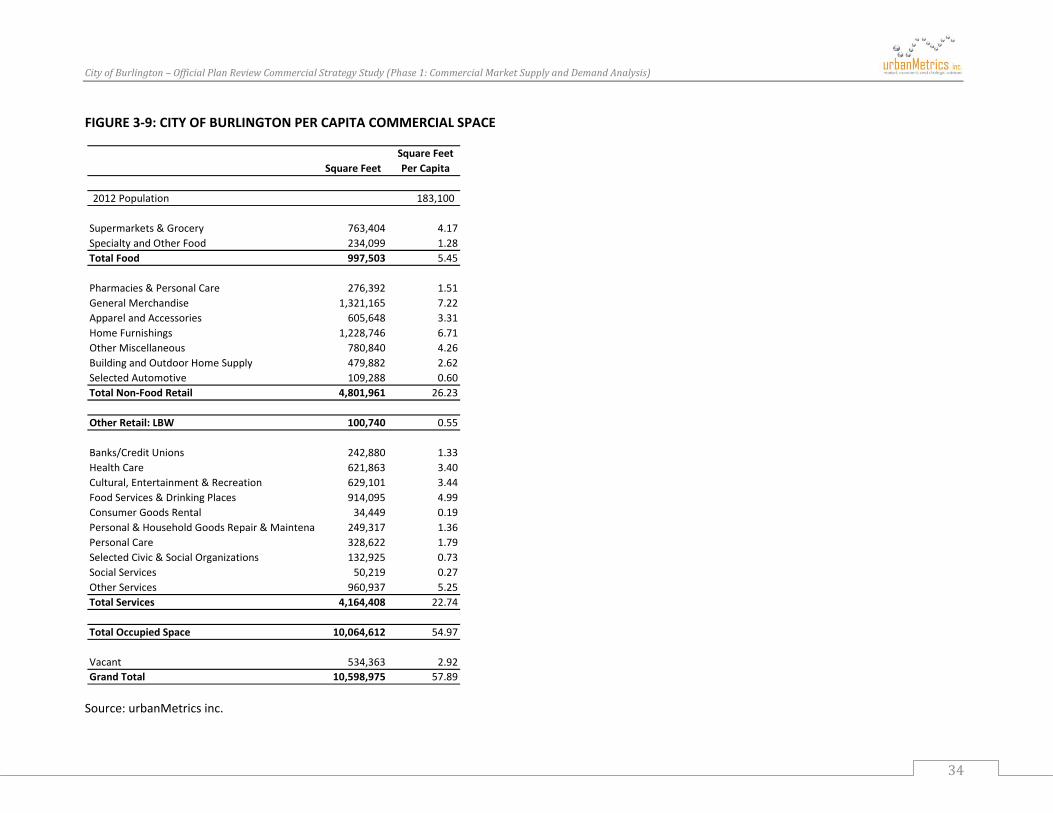

BasedonarecentinventoryofretailandservicecommercialusesintheCity,thereiscurrentlysome10.6millionsquarefeetofcommercialspacelocatedinBurlington.Ofthistotal,approximately45%iscomprisedofNon‐FoodStoreRetail(NFSR)facilities,39%iscomprisedofservices,9%ismadeupoffoodandbeveragefacilities,and5%isvacant.

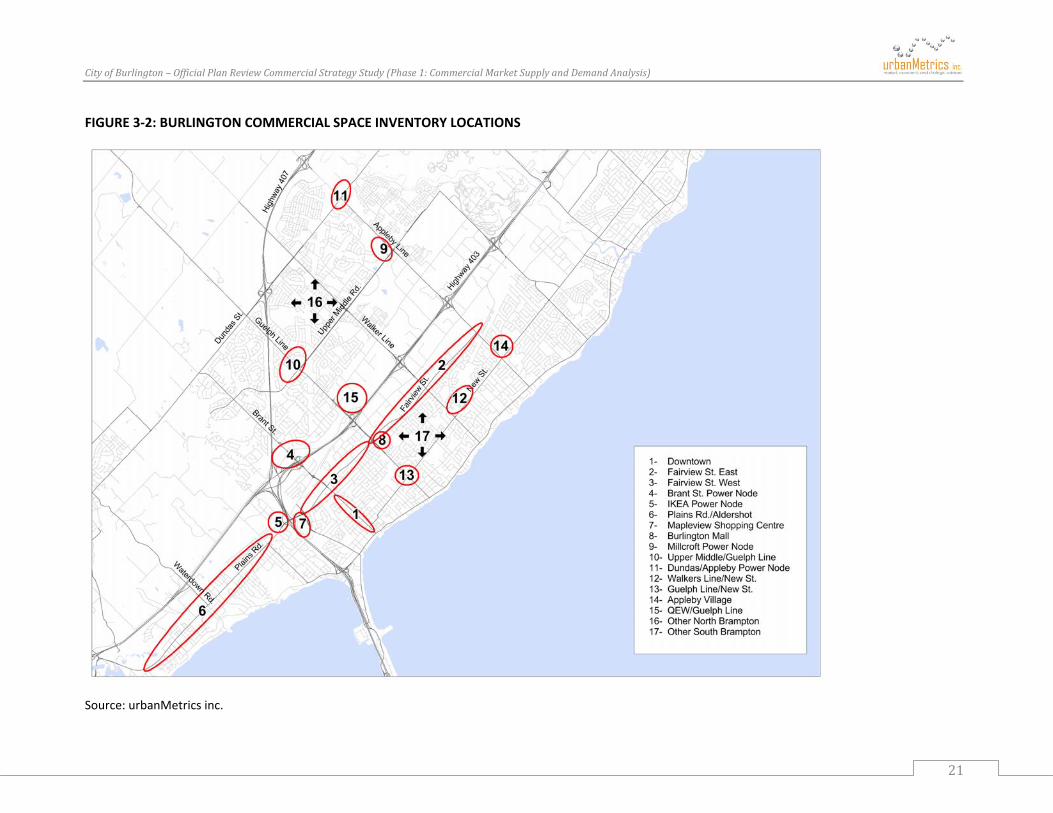

Burlingtonhasatraditionalcommercialstructure,withthesinglelargestconcentrationofoverallcommercialspacewithinthedowntowncore.Italsohastwoenclosedregionalshoppingcentres(BurlingtonMallandMapleviewShoppingCentre)andfourmajorpowercentrenodes,whicharesituatedatBrantStreetandtheQueenElizabethWay(QEW);PlainsRoadandtheQueenElizabethWay(QEW);ApplebyandUpperMiddleRoad;andDundasandAppleby.

Together,thesemajorretailnodescontainsome4.3millionsquarefeetofcommercialspaceandaccountforapproximately41%ofthetotalsupplyinBurlington.

ThecommercialvacancyrateinBurlingtoniscurrently5.0%,whichisindicativeofabalancedandhealthymarket.Althoughthereareseveralnodeswithrelativelyhighvacancyrates,theytendtobeduetospacetransitionsanduniquecircumstancesratherthansignifyingstructuralissueswiththeCity’s’commercialsupply.

SincetheCity’spreviouscommercialstudywaspreparedin2003,thegrowthincommercialspaceinBurlingtongenerallyoutpacedpopulationgrowth.Accordingly,Burlingtonhasexperiencedasignificantgrowthinspaceonapercapitabasisoverthepasttenyears.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

iii

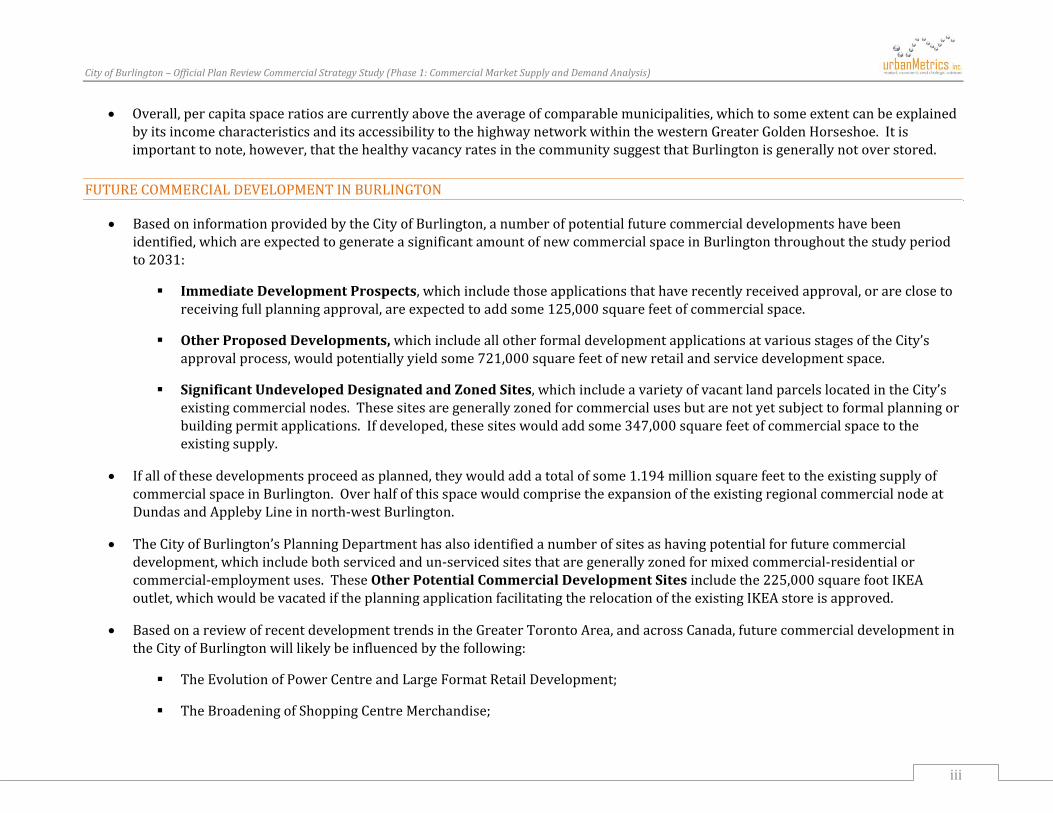

Overall,percapitaspaceratiosarecurrentlyabovetheaverageofcomparablemunicipalities,whichtosomeextentcanbeexplainedbyitsincomecharacteristicsanditsaccessibilitytothehighwaynetworkwithinthewesternGreaterGoldenHorseshoe.Itisimportanttonote,however,thatthehealthyvacancyratesinthecommunitysuggestthatBurlingtonisgenerallynotoverstored.

FUTURECOMMERCIALDEVELOPMENTINBURLINGTON

BasedoninformationprovidedbytheCityofBurlington,anumberofpotentialfuturecommercialdevelopmentshavebeenidentified,whichareexpectedtogenerateasignificantamountofnewcommercialspaceinBurlingtonthroughoutthestudyperiodto2031:

ImmediateDevelopmentProspects,whichincludethoseapplicationsthathaverecentlyreceivedapproval,orareclosetoreceivingfullplanningapproval,areexpectedtoaddsome125,000squarefeetofcommercialspace.

OtherProposedDevelopments,whichincludeallotherformaldevelopmentapplicationsatvariousstagesoftheCity’sapprovalprocess,wouldpotentiallyyieldsome721,000squarefeetofnewretailandservicedevelopmentspace.

SignificantUndevelopedDesignatedandZonedSites,whichincludeavarietyofvacantlandparcelslocatedintheCity’sexistingcommercialnodes.Thesesitesaregenerallyzonedforcommercialusesbutarenotyetsubjecttoformalplanningorbuildingpermitapplications.Ifdeveloped,thesesiteswouldaddsome347,000squarefeetofcommercialspacetotheexistingsupply.

Ifallofthesedevelopmentsproceedasplanned,theywouldaddatotalofsome1.194millionsquarefeettotheexistingsupplyofcommercialspaceinBurlington.OverhalfofthisspacewouldcomprisetheexpansionoftheexistingregionalcommercialnodeatDundasandApplebyLineinnorth‐westBurlington.

TheCityofBurlington’sPlanningDepartmenthasalsoidentifiedanumberofsitesashavingpotentialforfuturecommercialdevelopment,whichincludebothservicedandun‐servicedsitesthataregenerallyzonedformixedcommercial‐residentialorcommercial‐employmentuses.TheseOtherPotentialCommercialDevelopmentSitesincludethe225,000squarefootIKEAoutlet,whichwouldbevacatediftheplanningapplicationfacilitatingtherelocationoftheexistingIKEAstoreisapproved.

BasedonareviewofrecentdevelopmenttrendsintheGreaterTorontoArea,andacrossCanada,futurecommercialdevelopmentintheCityofBurlingtonwilllikelybeinfluencedbythefollowing:

TheEvolutionofPowerCentreandLargeFormatRetailDevelopment;

TheBroadeningofShoppingCentreMerchandise;

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

iv

TheIntroductionofLifestyleCentresandHybridMixed‐UseCentres;

ThePrinciplesofNewUrbanism;

OutletCentreDevelopment;

TheInfluxofU.S.RetailerstoCanada;

TheBlurringoftheRetailHierarchy;

Non‐StoreShopping;and,

Transit/ActiveTransportationSupportiveCommercialDevelopment.

CITYOFBURLINGTONANDDOWNTOWNTRADEAREAS

BasedontheresultsoflicenceplatessurveysconductedatfiveofBurlington’smajorshoppingdestinations,aswellason‐streetinterceptsurveysundertakeninthedowntown,BurlingtoncommercialfacilitiesderivethemajorityoftheirsalesvolumefromresidentsoftheCity.Inaddition,however,BurlingtonretailersalsoattractasignificantportionoftheircustomersfromnearbycommunitiesinneighbouringmunicipalitiessuchasOakvilleandHamilton.

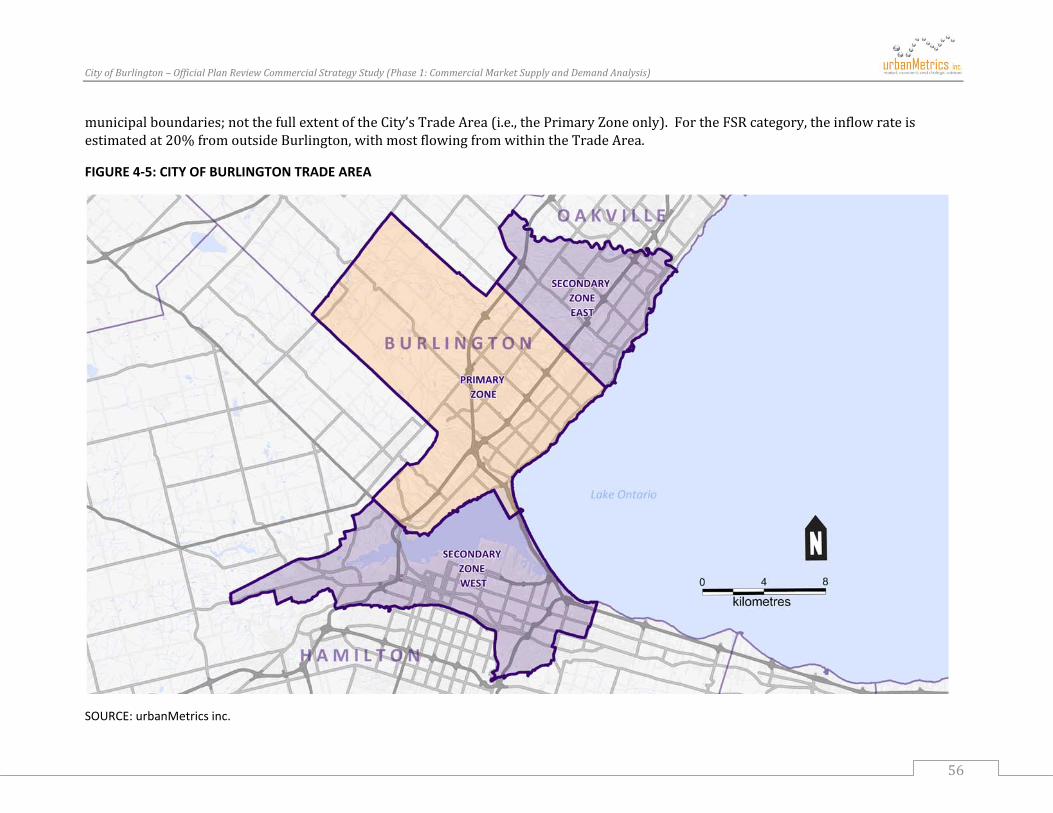

Accordingly,aTradeAreafortheCityofBurlingtonhasbeendelineatedthatincludesthreeseparatezones,asfollows:PrimaryZone(CityofBurlington);SecondaryZoneEast(WesternOakville);andSecondaryZoneWest(LowerHamiltonandDundas).

BasedonrecentCensusdataandpopulationestimatespreparedbytheRegionalMunicipalityofHaltonandCityofHamilton,atotalofsome497,700individualscurrentlyresideintheBurlingtonTradeArea.Thepopulationofthisareaisforecasttoincreasebysome45,900personsoverthestudyperiod;reachingatotalof543,600by2031.

DowntownBurlingtonservestheentireCityofBurlington,withacommercialPrimaryZonethatextendseastofKingRoad;southofHighway403andtheQueenElizabethWay(QEW);westofWalkersLine;andnorthofLakeOntario.Basedontheresultsofon‐streetinterceptsurveysundertakenintheCity’score,approximately63%ofvisitorstothedowntownoriginatefromthisPrimaryTradeArea.

The2011populationofthePrimaryTradeAreaforDowntownBurlingtonhasbeenestimatedat46,000persons,includingadjustmentsforcensusundercount.BasedonHaltonRegion’sBestPlanningestimates,thepopulationofthisareaisexpectedtoreach53,000by2031;largelythroughinfillandintensificationintheCity’sUrbanGrowthCentre.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

v

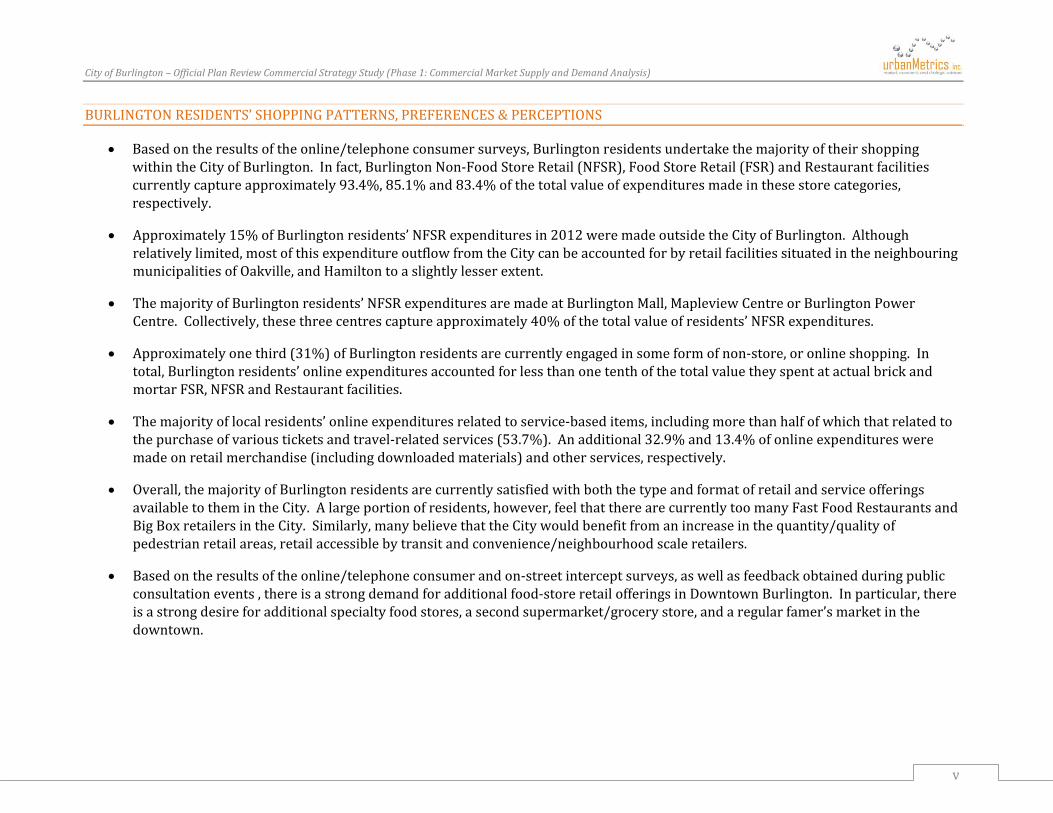

BURLINGTONRESIDENTS’SHOPPINGPATTERNS,PREFERENCES&PERCEPTIONS

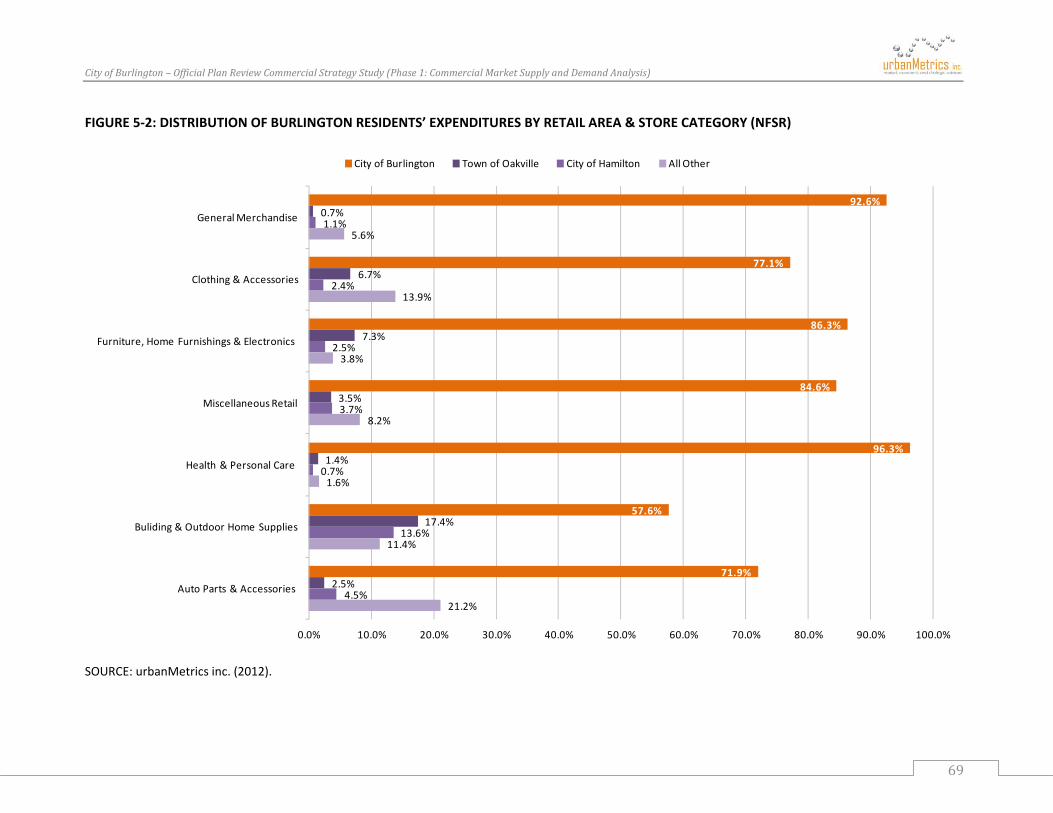

Basedontheresultsoftheonline/telephoneconsumersurveys,BurlingtonresidentsundertakethemajorityoftheirshoppingwithintheCityofBurlington.Infact,BurlingtonNon‐FoodStoreRetail(NFSR),FoodStoreRetail(FSR)andRestaurantfacilitiescurrentlycaptureapproximately93.4%,85.1%and83.4%ofthetotalvalueofexpendituresmadeinthesestorecategories,respectively.

Approximately15%ofBurlingtonresidents’NFSRexpendituresin2012weremadeoutsidetheCityofBurlington.Althoughrelativelylimited,mostofthisexpenditureoutflowfromtheCitycanbeaccountedforbyretailfacilitiessituatedintheneighbouringmunicipalitiesofOakville,andHamiltontoaslightlylesserextent.

ThemajorityofBurlingtonresidents’NFSRexpendituresaremadeatBurlingtonMall,MapleviewCentreorBurlingtonPowerCentre.Collectively,thesethreecentrescaptureapproximately40%ofthetotalvalueofresidents’NFSRexpenditures.

Approximatelyonethird(31%)ofBurlingtonresidentsarecurrentlyengagedinsomeformofnon‐store,oronlineshopping.Intotal,Burlingtonresidents’onlineexpendituresaccountedforlessthanonetenthofthetotalvaluetheyspentatactualbrickandmortarFSR,NFSRandRestaurantfacilities.

Themajorityoflocalresidents’onlineexpendituresrelatedtoservice‐baseditems,includingmorethanhalfofwhichthatrelatedtothepurchaseofvariousticketsandtravel‐relatedservices(53.7%).Anadditional32.9%and13.4%ofonlineexpendituresweremadeonretailmerchandise(includingdownloadedmaterials)andotherservices,respectively.

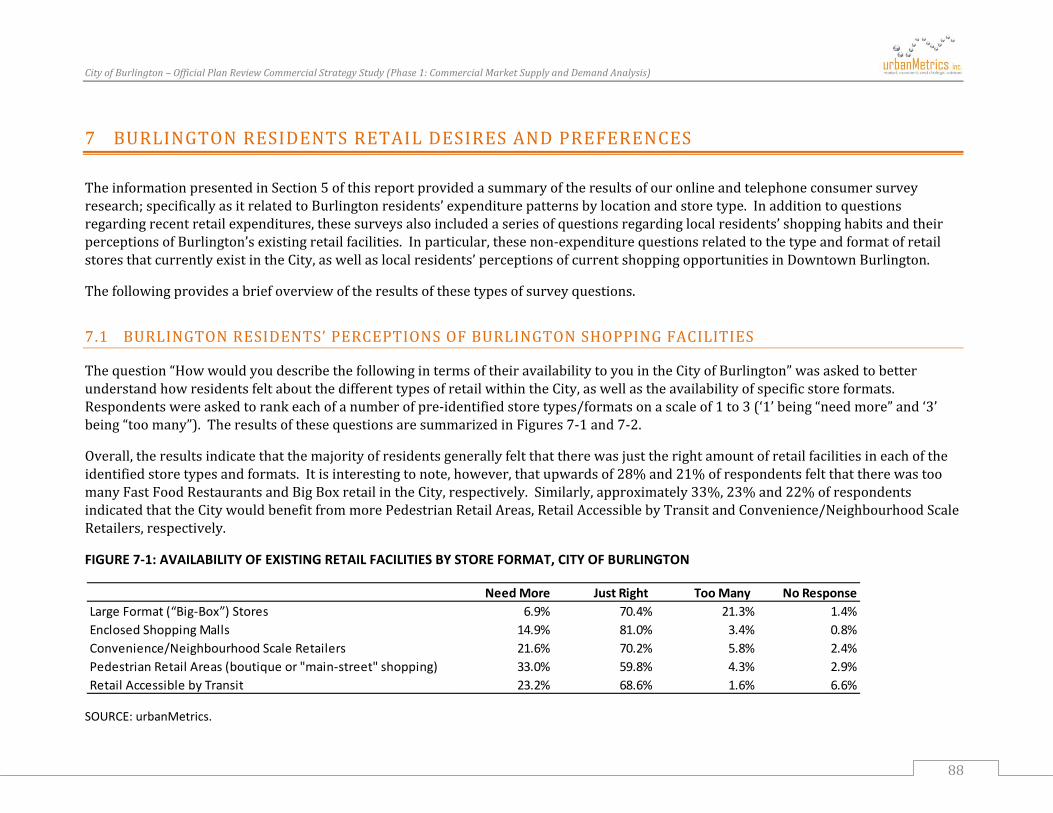

Overall,themajorityofBurlingtonresidentsarecurrentlysatisfiedwithboththetypeandformatofretailandserviceofferingsavailabletothemintheCity.Alargeportionofresidents,however,feelthattherearecurrentlytoomanyFastFoodRestaurantsandBigBoxretailersintheCity.Similarly,manybelievethattheCitywouldbenefitfromanincreaseinthequantity/qualityofpedestrianretailareas,retailaccessiblebytransitandconvenience/neighbourhoodscaleretailers.

Basedontheresultsoftheonline/telephoneconsumerandon‐streetinterceptsurveys,aswellasfeedbackobtainedduringpublicconsultationevents,thereisastrongdemandforadditionalfood‐storeretailofferingsinDowntownBurlington.Inparticular,thereisastrongdesireforadditionalspecialtyfoodstores,asecondsupermarket/grocerystore,andaregularfamer’smarketinthedowntown.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

vi

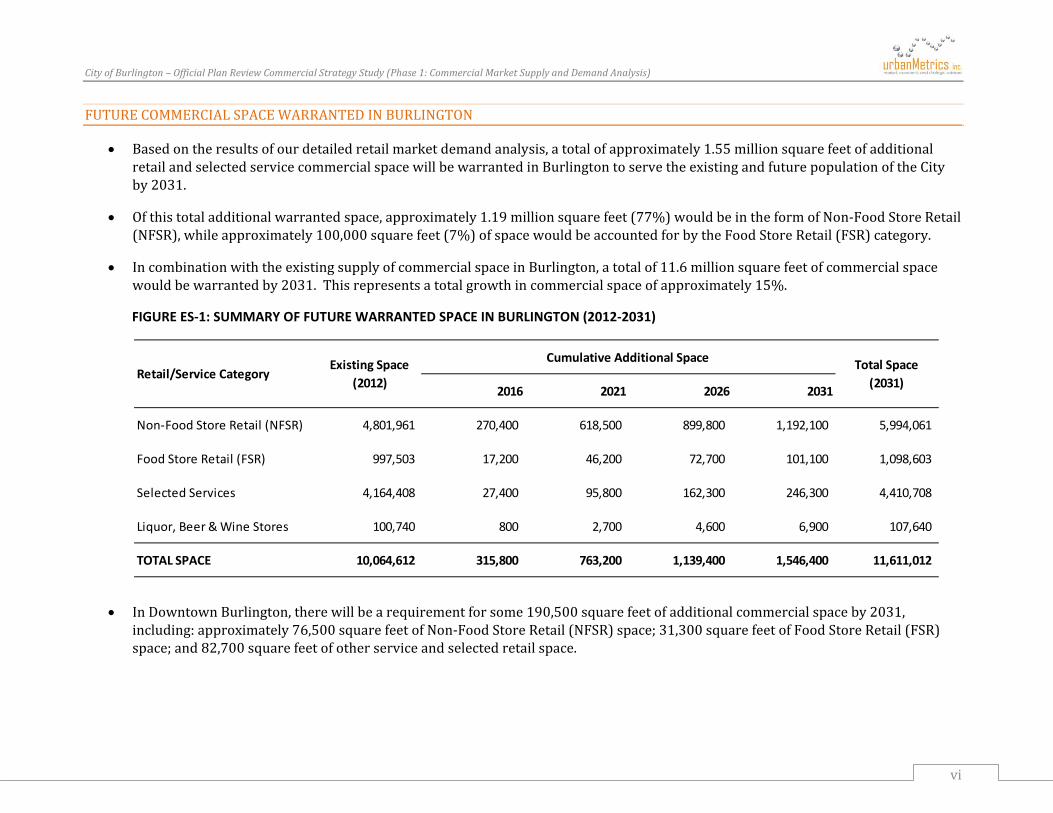

FUTURECOMMERCIALSPACEWARRANTEDINBURLINGTON

Basedontheresultsofourdetailedretailmarketdemandanalysis,atotalofapproximately1.55millionsquarefeetofadditionalretailandselectedservicecommercialspacewillbewarrantedinBurlingtontoservetheexistingandfuturepopulationoftheCityby2031.

Ofthistotaladditionalwarrantedspace,approximately1.19millionsquarefeet(77%)wouldbeintheformofNon‐FoodStoreRetail(NFSR),whileapproximately100,000squarefeet(7%)ofspacewouldbeaccountedforbytheFoodStoreRetail(FSR)category.

IncombinationwiththeexistingsupplyofcommercialspaceinBurlington,atotalof11.6millionsquarefeetofcommercialspacewouldbewarrantedby2031.Thisrepresentsatotalgrowthincommercialspaceofapproximately15%.

FIGURE ES‐1: SUMMARY OF FUTURE WARRANTED SPACE IN BURLINGTON (2012‐2031)

InDowntownBurlington,therewillbearequirementforsome190,500squarefeetofadditionalcommercialspaceby2031,including:approximately76,500squarefeetofNon‐FoodStoreRetail(NFSR)space;31,300squarefeetofFoodStoreRetail(FSR)space;and82,700squarefeetofotherserviceandselectedretailspace.

2016 2021 2026 2031

Non‐Food Store Retail (NFSR) 4,801,961 270,400 618,500 899,800 1,192,100 5,994,061

Food Store Retail (FSR) 997,503 17,200 46,200 72,700 101,100 1,098,603

Selected Services 4,164,408 27,400 95,800 162,300 246,300 4,410,708

Liquor, Beer & Wine Stores 100,740 800 2,700 4,600 6,900 107,640

TOTAL SPACE 10,064,612 315,800 763,200 1,139,400 1,546,400 11,611,012

Cumulative Additional SpaceExisting Space (2012)

Retail/Service CategoryTotal Space

(2031)

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

vii

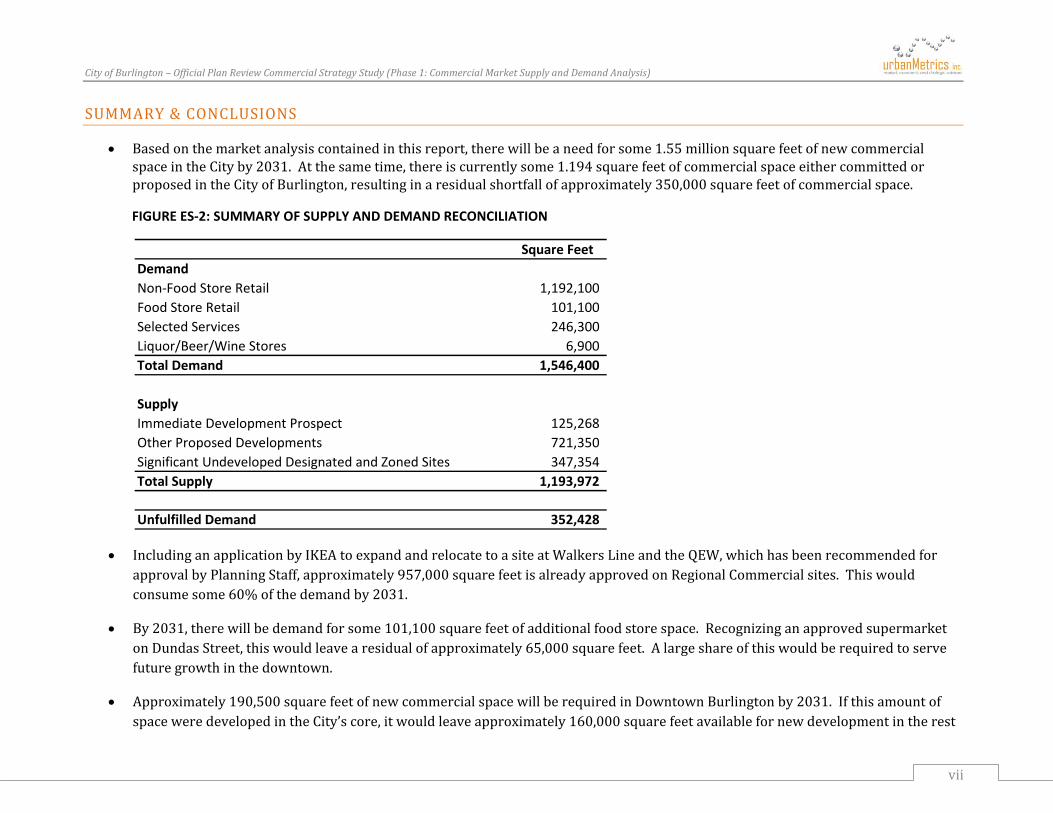

SUMMARY&CONCLUSIONS

Basedonthemarketanalysiscontainedinthisreport,therewillbeaneedforsome1.55millionsquarefeetofnewcommercialspaceintheCityby2031.Atthesametime,thereiscurrentlysome1.194squarefeetofcommercialspaceeithercommittedorproposedintheCityofBurlington,resultinginaresidualshortfallofapproximately350,000squarefeetofcommercialspace.

FIGURE ES‐2: SUMMARY OF SUPPLY AND DEMAND RECONCILIATION

IncludinganapplicationbyIKEAtoexpandandrelocatetoasiteatWalkersLineandtheQEW,whichhasbeenrecommendedforapprovalbyPlanningStaff,approximately957,000squarefeetisalreadyapprovedonRegionalCommercialsites.Thiswouldconsumesome60%ofthedemandby2031.

By2031,therewillbedemandforsome101,100squarefeetofadditionalfoodstorespace.RecognizinganapprovedsupermarketonDundasStreet,thiswouldleavearesidualofapproximately65,000squarefeet.Alargeshareofthiswouldberequiredtoservefuturegrowthinthedowntown.

Approximately190,500squarefeetofnewcommercialspacewillberequiredinDowntownBurlingtonby2031.IfthisamountofspaceweredevelopedintheCity’score,itwouldleaveapproximately160,000squarefeetavailablefornewdevelopmentintherest

Square FeetDemandNon‐Food Store Retail 1,192,100 Food Store Retail 101,100 Selected Services 246,300 Liquor/Beer/Wine Stores 6,900 Total Demand 1,546,400

SupplyImmediate Development Prospect 125,268 Other Proposed Developments 721,350 Significant Undeveloped Designated and Zoned Sites 347,354 Total Supply 1,193,972

Unfulfilled Demand 352,428

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

viii

oftheCity.ThisisarelativelysmallamountandshouldsupportnewpopulationalongtheUrbanGrowthCorridorandmixedusedevelopmentinproximitytotheGOTransitstationsandRegionalMallsites,aswellas,providinglocalservingcommercialspaceinareassuchaswestAldershotwhichmaylackcertainretailfacilities.

Therearealreadyanumberofvacantsitesintheseareaswithapprovalforcommercialspace,oftenaspartofamixed‐usezoningcategory.Whereapplicationsfornewcommercialspacearemade,approvalshouldgiveprioritytothosedevelopmentssupportingpopulationintensificationareasandinexistingareaslackinglocalservingretailfacilities.

Theresultsofthemarketanalysisclearlyindicatethattheavailablesupplyofcommerciallydesignatedlandswillbesufficienttomeetfuturedemandto2031.Assuch,therewillbenoneedtodesignateadditionalcommerciallandstosupportgrowthto2031.TheonlyexceptionstothiswouldbetomeetlocalservingneedsinexistingundersuppliedportionsoftheCity,suchaswestAldershot,ortoprovideforlocalservingretailtosupportfutureresidentialdevelopmentinintensificationareas.Similarly,theconversionofemploymentlandstocommercialisnotrequiredtosupportfuturegrowthinBurlingtonandshouldbeavoided.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

1

1 INTRODUCTION

1.1 BACKGROUND

ThisCommercialMarketreportrepresentsthefirstphaseofathreephaseprocesstocompleteacommercialstrategystudyaspartoftheCity’s2012OfficialPlanReview.ItcontainsanextensiveanalysisofthesupplyofanddemandforcommercialusesintheCityofBurlington.Areviewoflandusepoliciesregulatingthedevelopmentofcommerciallands,isalsopartofthisfirstphaseandcontainedinaseparatereport.

Theremainingtwophasesinclude:theformulationofpolicydirectionsanddesignrecommendations(Phase2),andthepreparationofurbandesignguidelines(Phase3).Inadditiontothesethreephases,thestudyprocesshasincludedadowntownstrategydiscussionpaper,whichhasbeenfinalizedandconsideredinaspartofthisreport.

AstheCityapproachesitsgreenfielddevelopmentcapacity,theemphasisofthecurrentOfficialPlanReviewistodeveloppolicythatguideslanduseplanningdecisionsinaplanningcontextwhereintensificationandinfillistheprimaryformofdevelopment.Ratherthanfocusonthecreationofnewneighbourhoods,theemphasiswillbeonrefiningexistingones.ItisthroughthislensthattheCommercialStrategyStudyhasbeenconducted.

Anadditionalareaoffocushasbeenthedowntownasthisareaisanintegralcomponentofthecurrentcommercialsysteminthecity.ItisalsoanareathathasbeenidentifiedasanUrbanGrowthCentretomeetintensificationtargets,andbecauseofthis,itscommercialrolewithinthecityhasthepotentialtoredefineitselfandevolve.

TheCommercialStrategyStudyalsoservestoaddresstheCity’sStrategicPlandirectionsregardingvibrantneighbourhoodsandprosperitydirections.Assuch,afocusofthestudyistocreateastrategytoredevelopagingretailareasintomixed‐use“peopleplaces”;encourageavibrantandhealthymixed‐usedowntown;andcreatemoremixedresidential/commercialplaceswithinexistingneighbourhoods.

Solutionsforintegratingretailareaswiththepublicandactivetransportationnetworksisalsoadirectiveforthisstudy.Tothisend,theimpactofthedesignatedProvinciallyidentifiedmobilityhubinthedowntownoncommercialopportunitieshasalsobeenconsidered.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

2

1.2 STUDYOBJECTIVES

ThepurposeoftheoverallCommercialStrategyStudyistoobtainpolicydirectionthatincorporatescommerciallanduseplanningwithneighbourhoodplanningandurbandesign.Thefocusisnotonlytoensureadequacyofcommercialspace,butalsoitsintegrationwithinneighbourhoodsandcommunityfacilities/infrastructure.Thereviewincludesbothretailandservicecommercialuses.

Specifically,thefundamentalinquiriesofthePhase1MarketandPolicyreportare:

1. Whatarethenational,provincial,regionalandlocalmarketconditionsandlifestyletrendsthatarelikelytoinfluencetheamount,location,design,formandfunctionofcommercialdevelopmentto2031,withinthecityandwithinthedowntown?

2. Howistheexistingsupplyofcommerciallandsandfloorareastoaccommodatecurrentandfutureretailandservicecommercialneedsto2031,withinthecityandthedowntown?

3. WhatisthegrowthpotentialofcommercialactivityinthedowntowngiventhataportionofthedowntownmixedusecentreisdesignatedasanUrbanGrowthCentre?

4. Howadequateistheexistingcommercialpolicyframeworkpositionedtoaddresscurrentandprojecteddemandinthecontextofexpectedtrends,inthecityandthedowntown?

Inadditiontothesebasicquestions,thefirstphaseofthestudyhasincludedextensiveinputfromBurlingtonresidents,businessesandotherstakeholders,intermsoftheirpreferencesforthefuturedevelopmentofthedowntownandtheurbanstructure.

Theprincipalareasofinquiryfortheremainingstudyphasesare:

5. Howshouldthecurrentpolicyframeworkbemodifiedtoservethecity’sanddowntown’slandneedsovertheplanningperiodto2031?

6. Givendowntown’ssize,locationandcompetitiveenvironment,whatroleshoulditplayinthecommercialhierarchy?Isitshighestpotentialasaregional,city‐wide,orneighbourhooddestination,orsomecombinationthereof?

7. WhatstepscanthecitytaketofacilitatethesuccessfulintegrationofcommercialareaswithinneighbourhoodstoimplementtheStrategicPlanwithrespecttoVibrantNeighbourhoodsandProsperitydirections?

8. Whatstepscanthecitytaketofacilitatethedevelopment,redevelopment,revitalizationandintensificationofcommerciallandswithinnodesandcorridors,andwithinmobilityhubareas,soasto:

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

3

a. incorporategoodprinciplesofurbandesignandsustainability;b. makeefficientuseofhardinfrastructure;c. accommodateco‐locationwithcommunityfacilities/infrastructure;andd. integratecommerciallandswithinaneighbourhood.

9. Howshouldthepolicyframeworkbemodifiedtoalignwithuppertierpolicy(e.g.ProvincialPolicyStatementandPlacestoGrow)?

10. Whatinformationdoesthecityneedtotrackinordertomonitorcommercialactivityinthecityandthedowntown?

11. Whatmechanismscanbeusedtoassistintheimplementationofthecommerciallanduseobjectives(e.g.programsandpartnerships)?

1.3 2003OFFICIALPLANREVIEWRETAILCOMMERCIALSTUDY

ThisMarketStudybuildsontheworkundertakeninthepreviousretailcommercialstudyforBurlingtonundertakenin2003byRobinDee&AssociatesandSorensonGravelyLowesPlanningAssociatesInc.

Inthe2003study,theconsultantsidentifiedademandforapproximatelytwomillionsquarefeetofadditionalcommercialspacebetween2003and2021inthePrimaryZonecomprisingtheCityofBurlingtonandtheHamiltoncommunityofWaterdown.Allofthiswarrantedspacehadbeenaccountedforbywayofexpansionpotentialatexistingcommercialprojects;vacantanddesignatedsites;andapprovedproposals.

BasedontheresultsofthiscurrentMarketStudy,theactualgrowthincommercialspaceinjusttheCityofBurlingtonto2012hasexceededthatamount.Atthesametime,however,theaveragevacancyratefortheCityhasdeclinedfrom6.4%to5.0%suggestingthateventhoughtheCityhasseenasizeableincreaseinitscommercialinventory,themarkethadthecapacitytoabsorbit.

The2003studyalsoconcludedthatthecurrentretailhierarchyintheOfficialPlan“provides,ingeneral,foranappropriatedistributionofretailspaceacrosstheCitywhileprovidingahighlevelofservice”.Withconsiderablegrowthinthecommercialstructuresince2003,thesameconclusioncanbereachedwithregardstothedistributionofcommercialspaceasitexiststoday.Sincethe2003study,theCityhasseentheadditionofanewregionalpowercentrenodeatApplebyLineandDundasandthestrengtheningofmostofitsothermajorcommercialnodes,includingthedowntown.Atthesametime,newcompetitionbywayofpowercentredevelopmentatBurloakandtheQEWinOakvilleandatDundasandHighway6inWaterdownhasmaintainedthecompetitivebalancebetweenBurlingtonanditsneighbouringmunicipalities.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

4

Itisalsoimportanttorecognizethatsincethe2003study,theGovernmentofOntariointroduceditsProvincialPolicyStatementandGrowthPlanfortheGreaterGoldenHorseshoe.Whileoverall,thepopulationgrowthratesassumedintheDee/SGLstudyareinlinewiththemorecurrentGrowthPlaninfluencedprojections,thereisnowagreateremphasisplacedonintensification.Asaresult,thiscurrentstudyisbasedonalargeshareoffuturepopulationgrowthwillinexistingareas,withthelargestshareinthedowntown.Thiswillultimatelyinfluencewherefuturecommercialdevelopmentshouldbefocused.

1.4 APPROACH

ThefollowingprovidesanoverviewofthevariousworkstepsthathavebeenundertakenurbanMetricsinpreparingthisCommercialMarketSupplyandDemandAnalysis:

Collection,ReviewandAnalysisofRelevantBackgroundMaterials

WehavecollectedandreviewedavarietyofrelevantbackgroundinformationthatwasobtaineddirectlyfromtheCityofBurlington,aswellasthroughourownindependentresearch.ThisincludesareviewoftheCity’sexistingOfficialPlancommercialpolicies;relevantpolicyandstrategicdocumentspreparedby–oronbehalfof–theCity;recentmarketdemandandimpactanalysesundertakeninandaroundtheCityofBurlington;Burlingtondevelopmentapplicationstatistics;aswellaspopulationandemploymentforecastspreparedbytheCityofBurlington,HaltonRegionandothernearbymunicipalities.

CommercialMarketandTrendsAnalysis

BasedonrecentworkundertakenbyurbanMetrics,wehaveprovidedasummaryofprevailingnational,regionalandlocaltrendsinretaildevelopmentandconsumershoppingbehavior,whichwilllikelyinfluencethefuturecommercialstructureandcompetitivenessofretail/servicefacilitieslocatedintheCityofBurlington.Inparticular,wehaveconsideredsuchfactorsandtrendsas:theentryofnewdepartmentstoresandothermajorretailersintoCanada;retailingandurbanintensification;theagingpopulation;transitsupportiveretaildevelopment;thefutureofpoweror“big‐box”retailing;andactivetransportationstrategiesaroundretailing.

DeterminationofBurlingtonMarketCharacteristics

WehaveundertakenadetaileddemographicandtrendanalysisfortheCityasawhole,includingareviewoftheCityandRegionalMunicipalityofHalton’spopulationprojections,economiccharacteristicsandagestructure.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

5

InventoryofCommercialSpaceinBurlington

AninventoryofallretailandservicecommercialspacelocatedintheCityofBurlingtonhasbeenundertakenandsubsequentlyclassifiedbystoretype,basedontheNorthAmericanIndustrialClassificationSystem(NAICS).Basedonthisinformation,wehavecalculatedkeyperformancemeasuresfortheCityasawholeandforspecificsub‐areas(e.g.,DowntownBurlington),including:vacancyratesandpercapitaspaceratios.

Wehavealsocomparedtheresultsofour2012inventorywiththatundertakenbyRobinDee&AssociatesaspartofthepreviousOfficialPlanReviewRetailCommercialStudypreparedfortheCityin2003.ThiscomparisonhasprovidedthecontexttodeterminehowthecurrentsupplyofcommercialspaceinBurlingtonshouldbetakenintoconsiderationwithregardstodeterminingfuturespacerequirements.

IdentificationofFutureRetailOpportunities

BasedprimarilyoninformationprovidedbytheCityofBurlington,areviewofOfficialPlanandZoninginformation,andourownfieldwork,wehaveidentifiedlocationsforpotentialfuturecommercialdevelopment,redevelopmentand/orintensification.

EmpiricalResearch(LicencePlate,On‐StreetInterceptandOnline/TelephoneConsumerSurveys)

WehaveundertakenavarietyofbackgroundconsumersurveyresearchtodeterminethecurrentshoppingpatternsandbehaviorofBurlingtonresidents.Thisbackgroundmarketresearchhasincludedlicenceplatesurveys,on‐streetinterceptsurveys,aswellasanonline/telephoneconsumersurveyofBurlingtonresidents,asdescribedbelow.

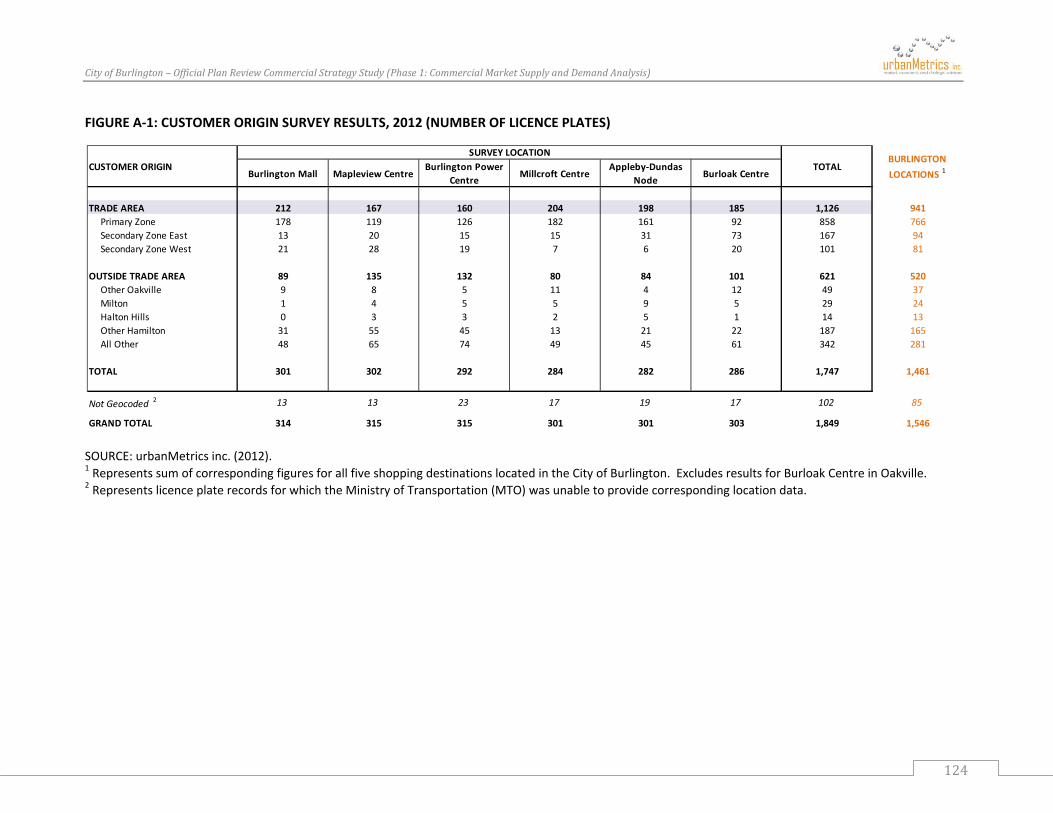

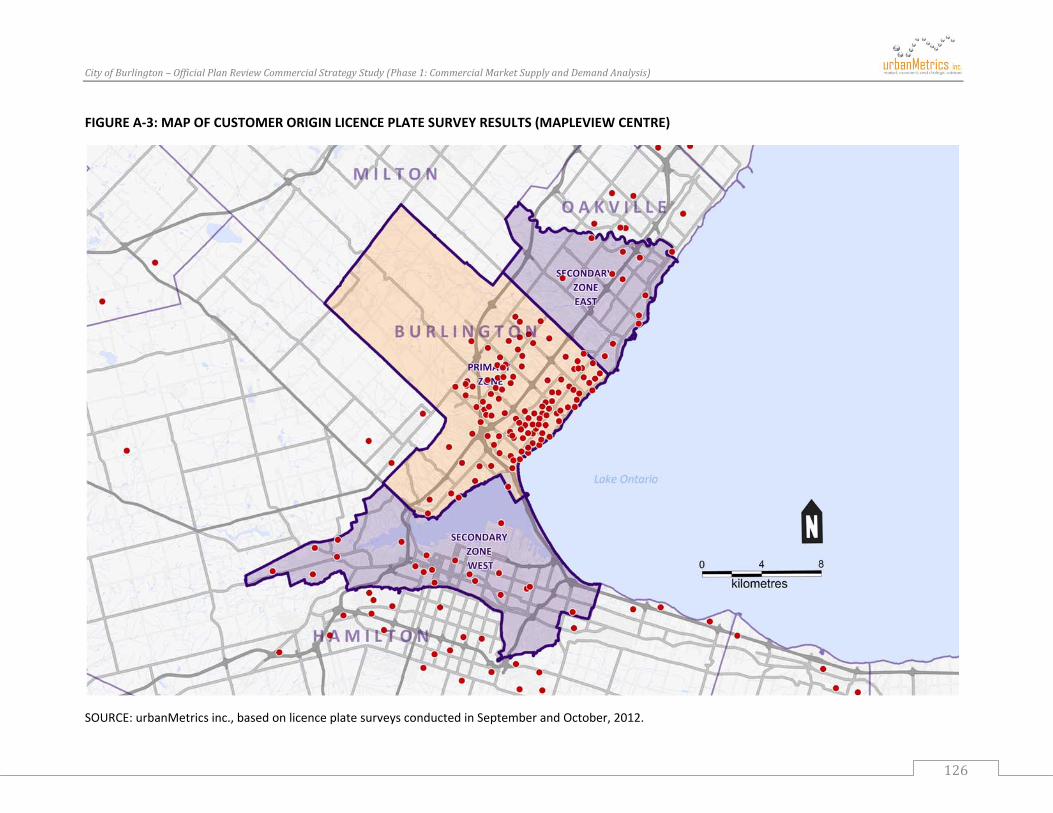

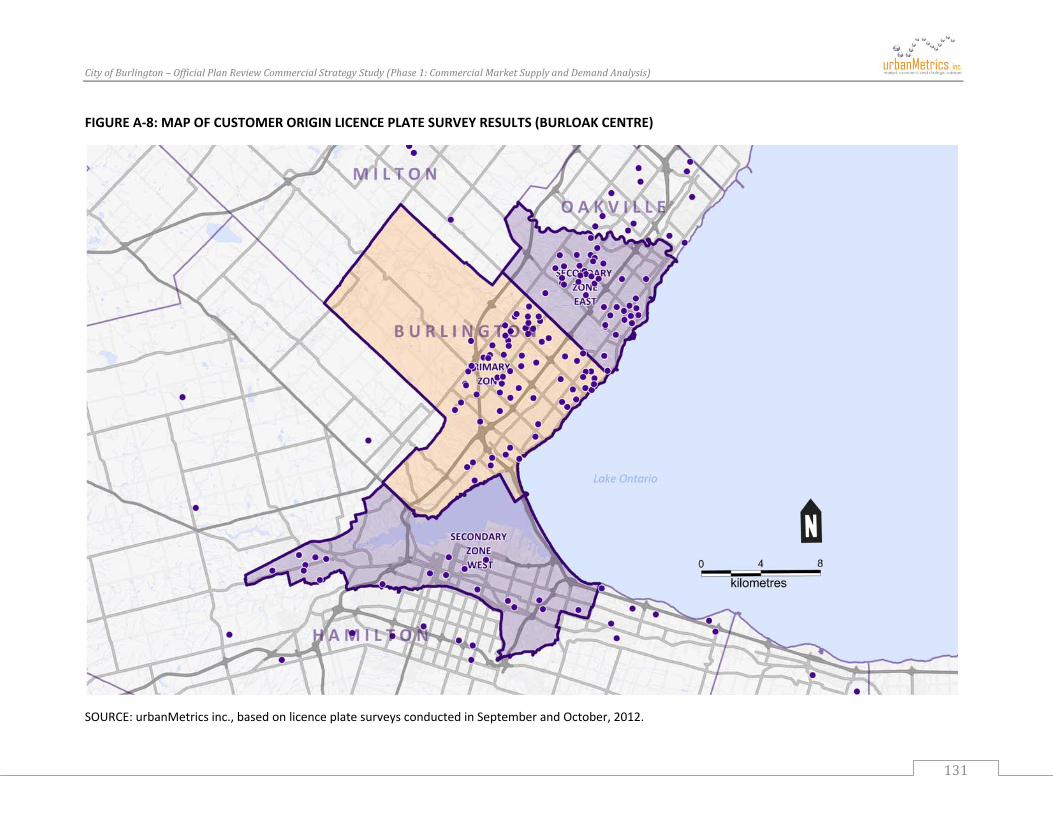

LicencePlateSurveys–atotalofsome1,849uniquelicenceplaterecordswerecollectedoverathreeweekperiodintheFallof2012(i.e.SeptemberandOctober)atsixmajorshoppingdestinationslocatedinorneartheedgesoftheCityofBurlington.(i.e.,BurlingtonMall,MapleviewCentre,BurlingtonPowerCentre(BrantStreet&theQueenElizabethWay),MillcroftCentre,theAppleby‐DundasPowerNodeandBurloakCentreinOakville).Theresultsofthesesurveyshavebeenusedtodeterminethegeographicdraw–orTradeArea–ofcommercialfacilitieslocatedintheCityofBurlington.

On‐StreetInterceptSurveys–approximately300on‐streetinterceptsurveyswerecompletedwithlocalresidents,employees,visitorsandotherpatronsofDowntownBurlingtonbetweenSeptemberandOctober2012.Theresultsofthesesurveyshavebeenusedtoidentifyshoppingpatterns,modesoftransportationandcustomeroriginsforthedowntown.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

6

Online/TelephoneConsumerSurveys–atotalof885onlineandtelephoneconsumersurveyshavebeencompleted2todetermineBurlingtonresidents’shoppingpatterns,aswellastheirperceptionsofandsatisfactionlevelswiththevarioustypeandformatofcommercialfacilitiesinBurlington.

Public/StakeholderConsultation

Inadditiontothevariousempiricalresearchthathasbeenundertakenasinputtoourcommercialmarketanalysis,urbanMetricsandThePlanningPartnershiphavealsoengagedlocalresidents,businessownersandothermembersofthepublictoobtainfeedbackastotheiropinionsregardingthecurrentandfuturestateofDowntownBurlington.Forexample,aDowntownPublicWorkshoppublicconsultationeventwasheldonNovember7,2012,attheBurlingtonArtsCentrewithmorethan130membersofthepublic.Thiseventincludedaninteractive“visioning”exercisethatpolledparticipantsbasedonanumberofquestionsrelatingtotheirsatisfactionwithdowntownandthespecificimprovementsthattheythoughtcouldbemade,aswellassmallerbreak‐outsessionsthatdealtwithspecific“tabletopics”intendedtofurtherdeveloptheideasandissuespresentedearlierintheevent.

TheresultsofthistypeofpublicconsultationhavebeenusedtoassessthecurrentstateofDowntownBurlington,thevariousfunctionsitserves,howwellitiscurrentlymeetingtheneedsoftheCity,andhowwellcurrentlanduseplanningpoliciesaresupportingitsvibrancy,asdetailedintheaccompanyingInterimCommercialStrategyDiscussionPaperonDowntownBurlington,whichwaspreparedbyurbanMetricsinc.andThePlanningPartnershipearlier.

AnalysisofBurlingtonMarketDimensionsandConditions

Relyingonthelicenseplate,on‐street,telephoneandon‐linesurveys;theinventoryofcompetition;andthepopulationanalysis,aTradeAreahasbeenfortheCityofBurlingtonasawhole,andthedowntowncore.Thesegeographicareashaveservedasthebasisforourmarketsupplyanddemandanalysis.

Withintheseareas,wehavealsoestimatedfuturepopulationgrowthanddeterminedtheuniqueincomeandexpenditurecharacteristicsofTradeArearesidents;whichhaveservedasimportantinputstoourmarketanalysis.

CommercialNeedsAssessment

Usingtheresultsofthepreviousworksteps,wehaveundertakenadetailedmarketdemandanalysisbymajorstoretype;includingFoodStoreRetail(FSR)andNon‐FoodStoreRetail(NFSR).Inparticular,thisanalysishasreliedonTradeAreapopulationestimates,incomeandexpenditurecharacteristicsofTradeArearesidents,commercialinventoryinformation,aswellastheresultsofthe

2Includes364completedtelephonesurveys,261fullycompleteon‐linesurveys,and260partiallycompletedon‐linesurveys.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

7

online/telephoneconsumersurveysandlicenseplatesurveys,whichhavebeenusedtodevelopmarketsharesandinflowratiosforourexpenditureanalysis.WhereStatisticsCanadaexpendituredataisnotavailable,wehavereliedonapercapitaspacemethodologyforselectedotherretailandservicecategories.

ThisanalysishasbeenusedtoprojectcommercialspaceneedsintheCityofBurlingtonto2031.Similarly,thisanalysishasalsobeenusedtodeterminehowwelltheexistingsupplyofcommerciallandandspacewillbeabletoaccommodateexistingandfutureretailandservicecommercialneedsthroughoutthisperiod.

DevelopmentofConclusionsandRecommendations

Basedontheresultsofthevariousresearchandanalysisdescribedinthepreviousworksteps,wehaveprovidedasummaryofourkeyresearchfindingsandconclusions.WehavealsodevelopedanumberofrecommendationsastohowtheCity’sfuturespacerequirementscanbeaccommodatedwithintheexistingurbansystemofBurlington.

1.5 ASSUMPTIONS

Inanyanalysisrequiringestimatesoffutureconditions,itisnecessarytomakecertainbasicassumptions,asfollows:

Overtheforecastperiod,totheyear2031,areasonabledegreeofeconomicgrowthandstabilitywillprevailinCanada,OntarioandspecificallyinHaltonRegion.Itisexpectedthatoverthisperiodcyclicaldownturnandupturnwilloccur.

Thepopulationforecasts,whicharebasedonHaltonRegion’sBestPlanningEstimatesareassumedreasonableandwillnotvarysignificantlyfromactualcountsinthefuture.

Thevarioussourcesemployedinouranalysistocalculateretailexpenditures,baseyearBurlingtonsharesorcapturerates,andsalespersquaremetre/footperformancelevelsforthevariousretailstoretypesanalyzedareconsideredsufficientlyreliable.

Commercialusesexaminedinthisreportincluderetail,servicecommercial,andlocalserving/streetfrontofficeuses.Forthepurposesofourmarketanalysis,certaincommercialuseshavenotbeenevaluated,includingautomotivesales,carrentalfirms,servicestations,funeralservicesandhotel/motelaccommodationuses.

Alldollarreferencesarein2012dollars,whichexcludeinflation,unlessnotedotherwise.Ourresearchandanalysishasbeenconductedinaccordancewiththetermsofreferenceforthisassignmentandourauthorizedscopeofwork.Thefindingsandrecommendationspresentedinthisreportrepresentourbestjudgmentbasedupontheinformationavailabletousasofthedateofourresearch.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

8

Accordingly,thefindingsandrecommendationspresentedhereinshouldbereviewedandinterpretedwithreferencetoevolvingcircumstancesandeconomicconditions.If,foranyreason,therearesignificantdeviationsfromanyoftheseassumptions,thereportanditsconclusionsshouldbereviewedorre‐examined.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

9

2 CITYOFBURLINGTON–GEOGRAPHYANDDEMOGRAPHICCHARACTERISTICS

2.1 LOCATIONALCHARACTERISTICS

2.1.1 REGIONALCONTEXT

BurlingtonisstrategicallysituatedwithintheWesternGTAhighwaynetwork,withexceptionalconnectivitytoOakville,Mississauga,andtheCityofTorontototheeast;HamiltonandtheNiagaraRegiontothesouth;andHamiltonandBrantfordtothewest.Asaresult,theCityiswellpositionedtodrawretailsalesinflowfromwellbeyonditsbordersandtoattractretailersseekingaregionalmarketexposure.

FIGURE 2‐1: CITY OF BURLINGTON REGIONAL CONTEXT

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

10

Basedon2006StatisticsCanadaPlaceofWorkdata,Burlingtoniswellbalancedintermsofcommuterflows,withsome41,300BurlingtonresidentsworkingoutsidetheCityand39,805non‐BurlingtonresidentsworkingintheCity.Approximately60%ofnon‐residentsworkinginBurlingtonliveinHamilton.Toamuchlessextent,BurlingtondrawsemploymentfromOakville,MississaugaandtheCityofToronto.

CommutingtripsbyBurlingtonresidentsoutsidetheCityaremuchmoreevenlydistributedamongthesesamemunicipalities,withabout24%ofcommutingoutflowdestinedforOakville;and21%destinedforeachMississaugaandTorontorespectively.

ThesecommutingflowpatternsprovideaguidetotheretailinflowsandoutflowstoandfromtheCity.

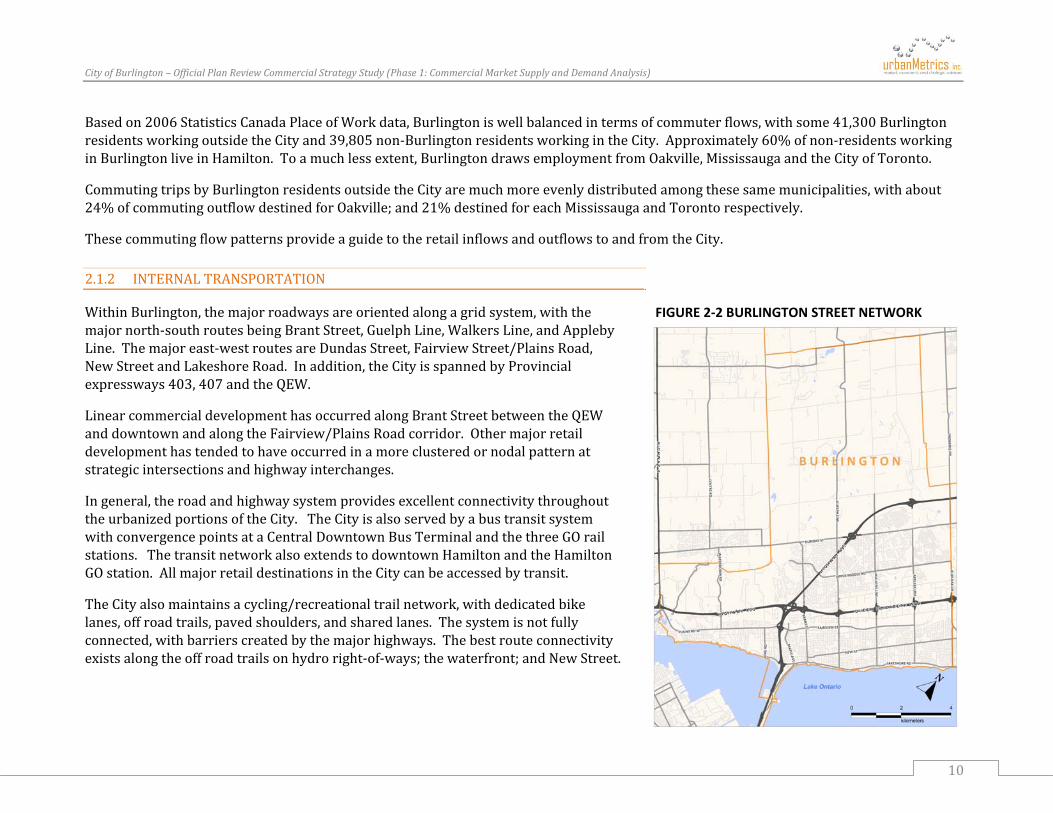

2.1.2 INTERNALTRANSPORTATION

WithinBurlington,themajorroadwaysareorientedalongagridsystem,withthemajornorth‐southroutesbeingBrantStreet,GuelphLine,WalkersLine,andApplebyLine.Themajoreast‐westroutesareDundasStreet,FairviewStreet/PlainsRoad,NewStreetandLakeshoreRoad.Inaddition,theCityisspannedbyProvincialexpressways403,407andtheQEW.

LinearcommercialdevelopmenthasoccurredalongBrantStreetbetweentheQEWanddowntownandalongtheFairview/PlainsRoadcorridor.Othermajorretaildevelopmenthastendedtohaveoccurredinamoreclusteredornodalpatternatstrategicintersectionsandhighwayinterchanges.

Ingeneral,theroadandhighwaysystemprovidesexcellentconnectivitythroughouttheurbanizedportionsoftheCity.TheCityisalsoservedbyabustransitsystemwithconvergencepointsataCentralDowntownBusTerminalandthethreeGOrailstations.ThetransitnetworkalsoextendstodowntownHamiltonandtheHamiltonGOstation.AllmajorretaildestinationsintheCitycanbeaccessedbytransit.

TheCityalsomaintainsacycling/recreationaltrailnetwork,withdedicatedbikelanes,offroadtrails,pavedshoulders,andsharedlanes.Thesystemisnotfullyconnected,withbarrierscreatedbythemajorhighways.Thebestrouteconnectivityexistsalongtheoffroadtrailsonhydroright‐of‐ways;thewaterfront;andNewStreet.

FIGURE 2‐2 BURLINGTON STREET NETWORK

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

11

2.2 DEMOGRAPHICCHARACTERISTICS

Thesocio‐demographiccharacteristicsofacommunitycaninfluencethemarketdemandforretailspace,includingconsumers’preferencesforcertaintypesofretailfacilitiesandtheattractionofretailbusinessestoacommunity.Changesinthedemographicsofacommunityandlifestylepatternscanalterthedemandfordifferenttypesofretailandservicecommercialfacilities,withpopulationgrowthandincomelevelstheultimateinfluencersofdemand.Someofthekeydriversofchangeincludethecompositionalvariationsinapopulation(i.e.,aginganddeclininghouseholdsizes),percapitaincomelevelsandlifestylechangesassociatedwithanagingpopulation.

ThefollowingsectionofthereportprovidesanevaluationofthefollowingcharacteristicsoftheCityofBurlington’spopulation:

Currentandhistoricpopulation;

Forecastpopulationgrowth;

Agestructure;

Incomelevels;

Ethnicity;

Familystructure;

Currentandhistoricemploymentlevels;and,

Forecastemploymentgrowth.

Section4.5ofthisreportfurtherexaminesthepopulationprojectionsfortheCityofBurlingtonanditsTradeAreatoassistindeterminingfutureretailspaceneeds.

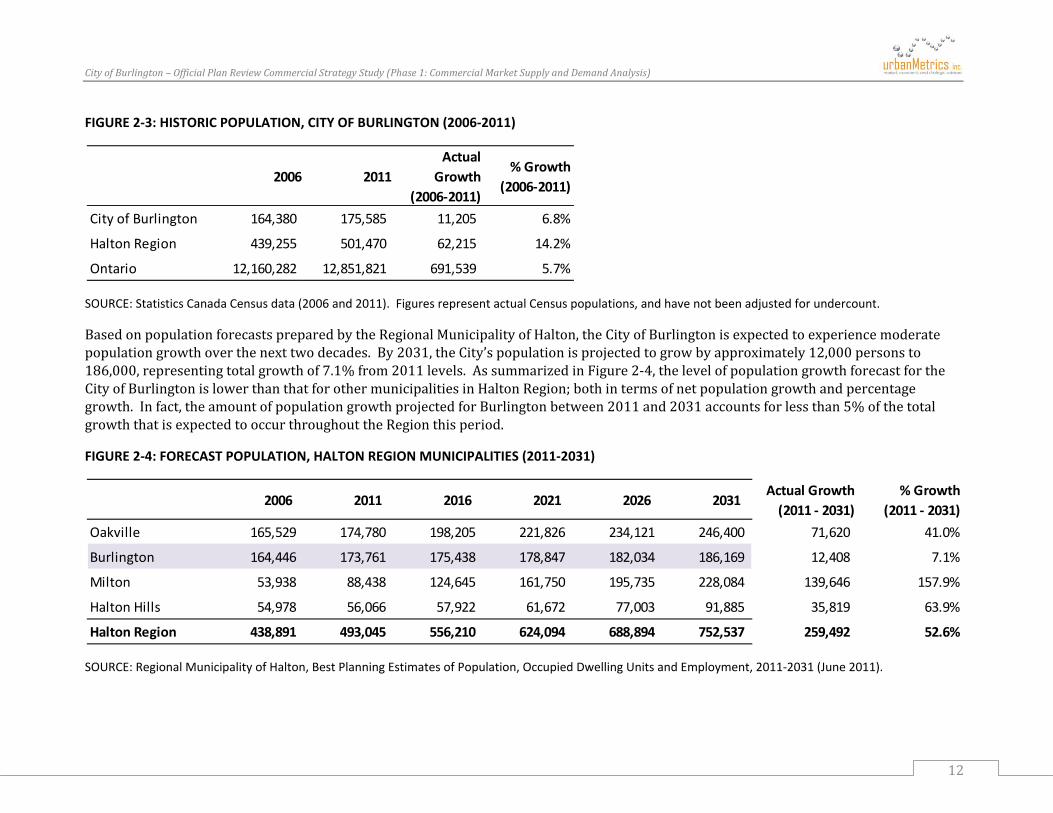

2.2.1 HISTORICANDFORECASTPOPULATIONGROWTH

BasedonStatisticsCanadaCensusdata,thepopulationoftheCityofBurlingtonreachedanestimated175,585personsin2011.Thisrepresentsagrowthrateofapproximately6.8%from2006,oranaverageannualgrowthrateof1.4%.Thisisslightlyhigherthantheprovincialpopulationgrowthrateduringthisperiod(i.e.,2006to2011)andbelowthatfortheentireRegionalMunicipalityofHalton(i.e.,CityofBurlington,TownofOakville,TownofMiltonandTownofHaltonHills).

Figure2‐3illustratesthehistoricchangeinpopulationbetween2006and2011fortheCityofBurlington,aswellasfortheRegionalMunicipalityofHaltonandtheProvinceofOntarioasawhole.

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

12

FIGURE 2‐3: HISTORIC POPULATION, CITY OF BURLINGTON (2006‐2011)

SOURCE: Statistics Canada Census data (2006 and 2011). Figures represent actual Census populations, and have not been adjusted for undercount.

BasedonpopulationforecastspreparedbytheRegionalMunicipalityofHalton,theCityofBurlingtonisexpectedtoexperiencemoderatepopulationgrowthoverthenexttwodecades.By2031,theCity’spopulationisprojectedtogrowbyapproximately12,000personsto186,000,representingtotalgrowthof7.1%from2011levels.AssummarizedinFigure2‐4,thelevelofpopulationgrowthforecastfortheCityofBurlingtonislowerthanthatforothermunicipalitiesinHaltonRegion;bothintermsofnetpopulationgrowthandpercentagegrowth.Infact,theamountofpopulationgrowthprojectedforBurlingtonbetween2011and2031accountsforlessthan5%ofthetotalgrowththatisexpectedtooccurthroughouttheRegionthisperiod.

FIGURE 2‐4: FORECAST POPULATION, HALTON REGION MUNICIPALITIES (2011‐2031)

SOURCE: Regional Municipality of Halton, Best Planning Estimates of Population, Occupied Dwelling Units and Employment, 2011‐2031 (June 2011).

2006 2011Actual

Growth (2006‐2011)

% Growth (2006‐2011)

City of Burlington 164,380 175,585 11,205 6.8%

Halton Region 439,255 501,470 62,215 14.2%

Ontario 12,160,282 12,851,821 691,539 5.7%

2006 2011 2016 2021 2026 2031Actual Growth (2011 ‐ 2031)

% Growth (2011 ‐ 2031)

Oakville 165,529 174,780 198,205 221,826 234,121 246,400 71,620 41.0%

Burlington 164,446 173,761 175,438 178,847 182,034 186,169 12,408 7.1%

Milton 53,938 88,438 124,645 161,750 195,735 228,084 139,646 157.9%

Halton Hills 54,978 56,066 57,922 61,672 77,003 91,885 35,819 63.9%

Halton Region 438,891 493,045 556,210 624,094 688,894 752,537 259,492 52.6%

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

13

2.2.2 AGESTRUCTURE

Ashouseholdsage,theirneedsandspendinghabitsshift.Inverybroadterms,youngadultstendtospendahigherproportionoftheirincomeonfashion,entertainmentandrecreationmerchandise.Astheseindividualsgetmarriedandhavechildren,spendingpatternstendtoshifttowardsitemsandservicesrelatedtohousingandchildrearing.Similarly,whenfamilysizesincreaseandchildrenage,housing,homefurnishingsandhomedécoritemsoccupyamuchgreatershareinhouseholdexpenditures.Followingretirement,housingandfurnishingsneedsaretypicallyreduced,althoughinmanycasesthequantityisreplacedbyhigherquality.Inaddition,asconsumersage,thereisagreateremphasisonservice‐relatedexpenditures.

Basedon2011Censusdata,themedianageoftheBurlingtonpopulationwas41.8,whichrepresentsaslightincreasefromtheCity’s2006medianageof40.3.Itisalsointerestingtonotethatthe2011medianageofBurlingtonresidentsissomewhathigherthanthatoftheOntariopopulation(40.4)andneighbouringcommunitiessuchasOakville(40.2).Overall,therefore,itisevidentthatBurlingtonhasarelativelymaturepopulationincomparisontootherareasoftheProvinceandGreaterTorontoArea.

ThechartinFigure2‐5providesasummaryofthecurrentandhistoricagedistributionoftheBurlingtonpopulationbyfive‐yearagegroup.Asshown,theCity’spopulationiswellrepresentedinallagegroups,withthelargestshareconcentratedinthe35to59agerange.ItisalsoimportanttonotethatBurlington’smiddle‐ageandseniorpopulationshavecontinuedtoincreaseoverthe2006to2011period,withgrowthrecordedinallagecategoriesforpersons45yearsandover.

AlthoughtheBurlingtonpopulationhascontinuedtoage,therehasalsobeensomegrowthintheyoungermarketpopulationaswell;withincreasesofmorethan5%ineachofthe15‐19,20‐24and25‐29agecategories.

FIGURE 2‐5: CITY OF BURLINGTON AGE DISTRIBUTION (2006 – 2011)

SOURCE: urbanMetrics inc., based on Statistics Canada Census data (2006 and 2011).

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000

0 to 4 years5 to 9 years

10 to 14 years15 to 19 years20 to 24 years25 to 29 years30 to 34 years35 to 39 years40 to 44 years45 to 49 years50 to 54 years55 to 59 years60 to 64 years65 to 69 years70 to 74 years75 to 79 years80 to 84 years

85 years and over

Burlington (2011) Burlington (2006)

CityofBurlington–OfficialPlanReviewCommercialStrategyStudy(Phase1:CommercialMarketSupplyandDemandAnalysis)

14

2.2.3 INCOMESTRUCTURE

Incombinationwithfuturepopulationlevels,percapitaincomeisanimportantelementindeterminingthecurrentandfutureretailexpenditurepotentialofBurlingtonresidents.AssummarizedinFigure2‐6,incomelevelsaregenerallyquitehighthroughouttheentireRegionalMunicipalityofHalton,andparticularlysointheTownofOakvilleandCityofBurlington.Basedon2006Censusdata,percapitaincomelevelsintheCityofBurlingtonareapproximately5%belowtheRegionalaverage;howevertheyaremorethan23%abovetheProvincialaverage.

FIGURE 2‐6: PER CAPITA INCOME, HALTON REGION MUNICIPALITIES (2006)

SOURCE: Statistics Canada Census data (2006). Figures represent 2005 income levels.

ThemapinFigure2‐7onthefollowingpageprovidesanillustrationofpercapitaincomelevelsindexedtotheProvincialaveragefortheentireCityofBurlington,aswellaspartsofneighbouringmunicipalitiessuchasOakville,Milton,andHamilton.Asshown,percapitaincomelevelsaregenerallygreaterthanorequaltotheProvincialaverageforthevastmajorityofdisseminationareasidentifiedinBurlington,OakvilleandsouthernMilton.Moreover,therelativelylimitednumbersoflowincomepocketsinthesemunicipalitiesareconcentratedalongtheQueenElizabethWayhighwaycorridor,whichconsistsprimarilyofnon‐residentiallanduses.