Embed Size (px)

Citation preview

AGENDA City Council Special Meeting Tuesday, September 8, 2020

1102 Lohmans Crossing Road, Lakeway, TX 78734 6:30 PM

VIA VIDEOCONFERENCE

This meeting of the Lakeway City Council will be conducted via videoconference, pursuant to Governor Abbott’s Temporary Suspension of Open Meetings Laws issued on March 16, 2020. As always, you may watch the meeting using the city’s live stream at: https://www.lakeway-tx.gov/1062/Videos---Meetings-Events. There will be no in-person attendance at this meeting. Citizen Participation on posted agenda items will occur via telephone. If you wish to provide comments on a specific agenda item via telephone during the meeting, submit a public comment form on the city website before 3:00 pm Tuesday, September 8, 2020. Go to https://lakeway-tx.civicweb.net/Portal/CitizenEngagement.aspx to complete the form. Email [email protected] if you have any questions regarding citizen participation. City staff will send an email providing instructions for commenting during public participation via videoconference directly to those registered to comment. The same rules apply to telephone comments as to in-person comments. They must be on the topic of the agenda item, and they must be no more than 3 minutes in length.

Page 1 ESTABLISH QUORUM AND CALL TO ORDER. 2 PLEDGE OF ALLEGIANCE. 3 FY 2021 BUDGET.

• Presentation by City Manager Julie Oakley. • Public hearing. • Council discussion/action.

Draft Budget 3 - 65 4 HAMILTON GREENBELT WILDFIRE FUELS REDUCTION PROJECT.

Page 1 of 161

• Presentation by Forrester Carrie Burns. • Citizen participation. • Council discussion/action.

Presentation 66 - 70 5 HOT TAX POLICY.

• Presentation by Finance Director Shereen Gendy. • Citizen participation. • Council discussion/action.

Staff Report Proposed HOT Policy - DRAFT HOT Policy Current HOT Application Tax Code Chapter 351

71 - 161

6 ADJOURN. Signed this 3rd day of September, 2020. ________________________________ Sandra L. Cox, Mayor All items may be subject to action by City Council pursuant to Ordinance No. 2001-10-29-1, Article VI. The City Council may adjourn into Executive Session at any time during the course of this meeting to discuss any matters listed on the agenda, as authorized by the Texas Government Code including, but not limited to, Sections: 551.071 (Consultation with Attorney), 551.072 (Deliberations about Real Property), 551.073 (Deliberations about Gifts and Donations), 551.074 (Personnel Matters), 551.076 (Deliberations about Security Devices), 551.087 (Economic Development), 418.183 (Deliberations about Homeland Security Issues) and as authorized by the Texas Tax Code including, but not limited to, Section 321.3022 (Sales Tax Information). Certification: I certify that the above notice of meeting was posted on the City of Lakeway Official Community Bulletin Board on the 4th day of September, 2020 at 3:00 p.m. Council approved agendas and action minutes are available on line at http://www.lakeway-tx.gov/. The City of Lakeway Council meetings are available to all persons regardless of ability. If you require special assistance, please contact Jo Ann Touchstone, City Secretary, at 512-314-7506 at least 48 hours in advance of the meeting. _________________________________ Jo Ann Touchstone, City Secretary

Page 2 of 161

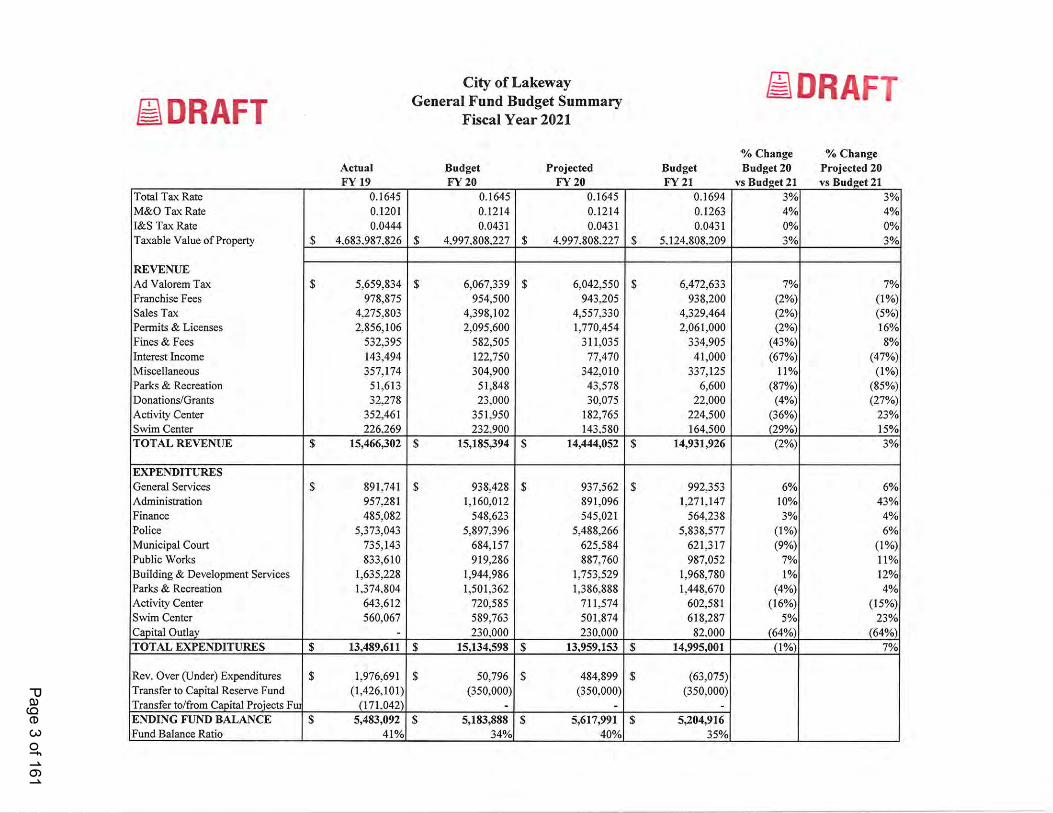

City of Lakeway DRAFTE DR General Fund Budget SummaryI Fiscal Year 2021

% Change % ChangeActual Budget Projected Budget Budget 20 Projected 20FY 19 FY 20 FY 20 FY 21 vs Budget 21 vs Budget 21

Total Tax Rate 0.1645 0.1645 0.1645 0.1694 3% 3%M&O Tax Rate 01201 0.1214 0.1214 0.1263 4% 4%1&5 Tax Rate 0.0444 0.0431 0.0431 0.0431 0% 0%Taxable Value of Property 39 4.683.987.8215 $ 4.997.808.2227 $ 4.997.808.227 $ 5.1Z4.808.209 3% 3%

REVENUEAd Valorem Tax $ 5,659,834 $ 6.067.339 $ 6.042.550 $ 6.472.633 7% 7%Franchise Fees 978.875 954,500 943.205 938,200 (2%) (1%)Sales Tax 4.275,803 4,398,102 4,557,330 4,329,464 (2%) (5%)Permits & Licenses 2,856,106 2,095,600 1,770,454 2,061,000 (2%) 16%Fines & Fees 532,395 582,505 311,035 334,905 (43%) 8%

Interest Income 143,494 122,750 77,470 41,000 (67%) (47%)Miscellaneous 357,174 304.900 342,010 337.125 11% (1%)Parks & Recreation 51.613 51,848 43.578 6.600 (87%) (85%)Donations/Grants 32.278 23.000 30.075 22.000 (4%) (27%)Activity Center 352,461 351,950 182,765 224,500 (36%) 23%Swim Center 226.269 232.900 143.580 164.500 (29%) 15%TOTAL REVENUE $ 15,466,302 S 15,185,394 $ 14,444,052 5 14,931,926 (2%) 3%

EXPENDITURESGeneral Services 3:‘ 891,741 $ 938,428 $ 937,562 5 992,353 6% 6%Administration 957,281 1,160,012 891,096 1.271.147 10% 43%Finance 485.082 548,623 545,021 564,238 3% 4%Police 5,373,043 5,897,396 5,488,266 5,838,577 (1%) 6%Municipal Court 735.143 684.157 625.584 621.317 (9%) (1%)Public Works 833,610 919,286 887,760 987,052 7% 11%

Building & Development Services 1,635,228 1,944,986 1.753.529 1,968,780 1% 12%Parks & Recreation 1,374,804 1,501.362 1,386.888 1,448,670 (4%) 4%Activity Center 643.612 720,585 711,574 602,581 (16%) (15%)Swim Center 560,067 589.763 501.874 618.287 5% 23%Capital Outlay - 230.000 230.000 82.000 (64%) (64%)TOTAL EXPENDITURES $ 13,489,611 $ 15,134,598 S 13,959,153 $ 14.995,001 ( 1%) 7%

Rev. Over (Under) Expenditures $ 1,976,691 $ 50,796 $ 484,899 $ (63,075)Transfer to Capital Reserve Fund (1,426,101) (350000) (350000) (350000)Transfer to/from Capjtal ProiectsFur (171.042) - - -

ENDING FUND BALANCE 5 5,483,092 $ 5,183,888 $ 5,617,991 $ 5,204,916Fund Balance Ratio 41% 34% 40% 35%

Page 3 of 161

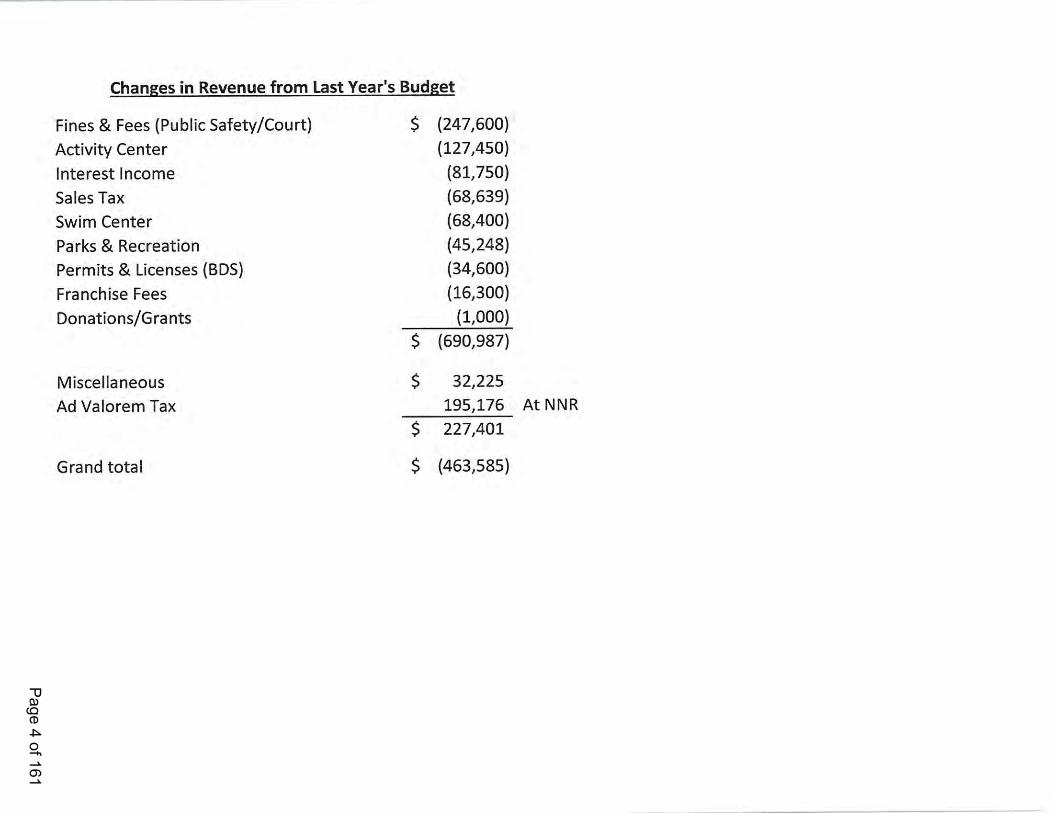

Changes in Revenue from Last Year's Budget

Fines 8: Fees (Public Safety/Court) S (247,600)

Activity Center (127,450)

Interest Income (81,750)

Sales Tax (68,639)

Swim Center (68,400)

Parks & Recreation (45,248)

Permits & Licenses (BDS) (34,600)

Franchise Fees (16,300)

Donations/Grants (1,000)

$ (690,987)

Miscellaneous S 32,225

Ad Valorem Tax 195,176

S 227,401

Grand total S (463,585)

At NNR

Page 4 of 161

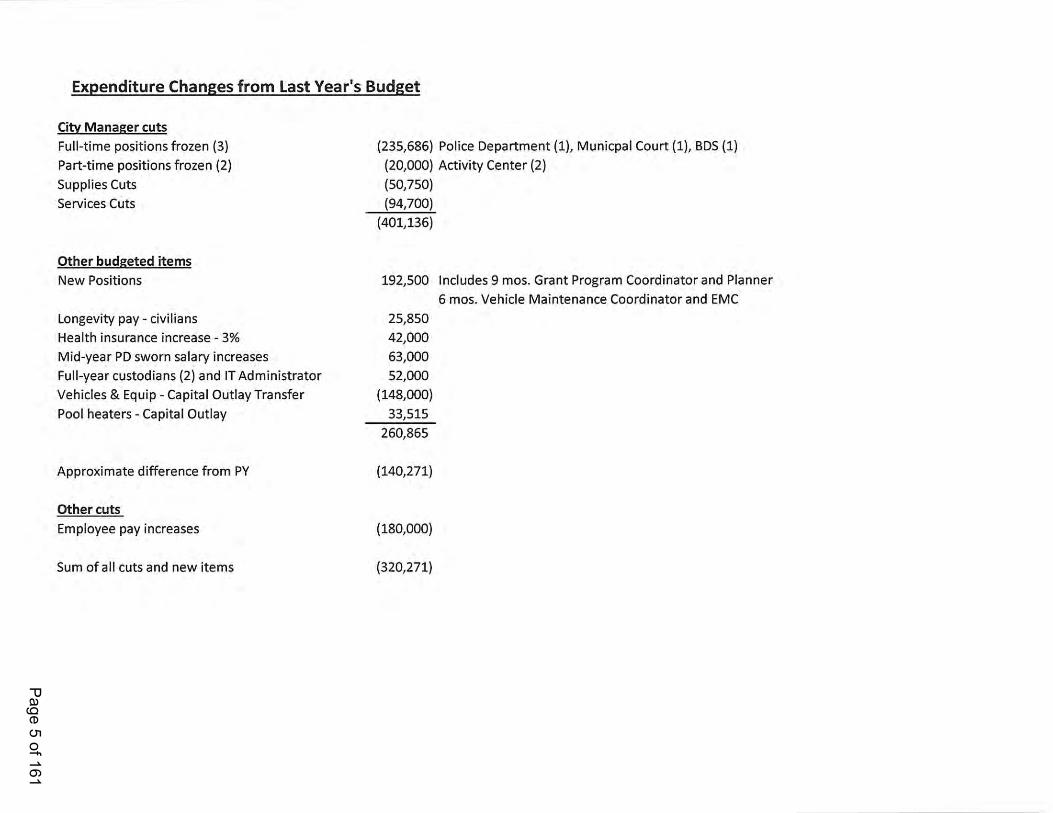

Expenditure Changes from Last Year's Budget

Cig Manager cuts

Fu||—time positions frozen (3) (235,686) Police Department (1), Municpal Court (1), BDS(1)

Part«time positions frozen (2) (20,000) Activity Center (2)

Supplies Cuts (50,750)

Services Cuts (94,700)

(401,136)

Other budgeted items

New Positions 192,500 Includes 9 mos. Grant Program Coordinator and Planner6 mos. Vehicle Maintenance Coordinator and EMC

Longevity pay - civilians 25,850

Health insurance increase — 3% 42,000Mid—yearPD sworn salary increases 63,000Full-year custodians (2) and ITAdministrator 52,000

Vehicles & Equip — Capital Outlay Transfer (148,000)

Pool heaters - Capital Outlay 33,515

260,865

Approximate difference from PY (140,271)

Other cuts

Employee pay increases (180,000)

Sum of all cuts and new items (320,271)

Page 5 of 161

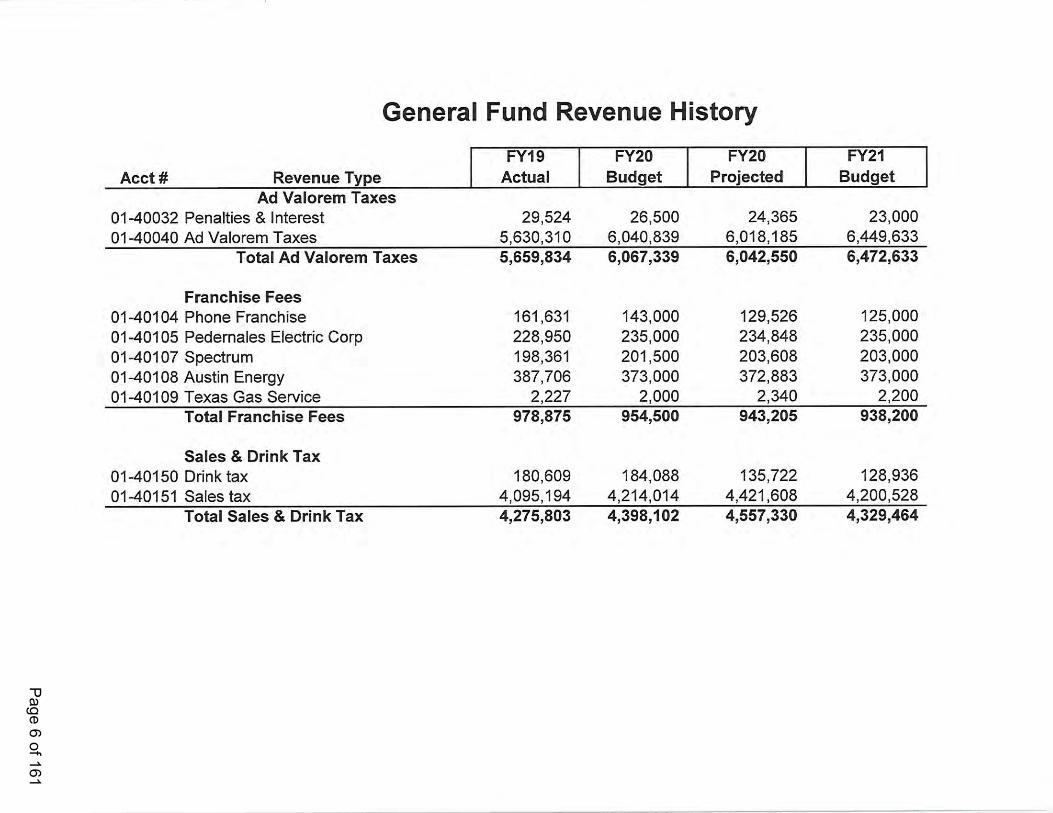

General Fund Revenue History

FY19 FY20 FY20 FY21Acct # Revenue Type Actual Budget Projected Budget

Ad Valorem Taxes01-40032 Penalties & Interest 29,524 26,500 24,365 23,00001-40040 Ad Valorem Taxes 5,630,310 6,040,839 6,018,185 6,449,633

Total Ad Valorem Taxes 5,659,834 6,067,339 6,042,550 6,472,633

Franchise Fees01-40104 Phone Franchise 161,631 143,000 129,526 125,00001-40105 Pedernales Electric Corp 228,950 235,000 234,848 235,00001-40107 Spectrum 198,361 201,500 203,608 203,00001-40108 Austin Energy 387,706 373,000 372,883 373,00001-40109 Texas Gas Service 2,227 2,000 2,340 2,200

Total Franchise Fees 978,875 954,500 943,205 938,200

Sales & Drink Tax01-40150 Drink tax 180,609 184,088 135,722 128,93601-40151 Sales tax 4,095,194 4,214,014 4,421,608 4,200,528

Total Sales & Drink Tax 4,275,803 4,398,102 4,557,330 4,329,464

Page 6 of 161

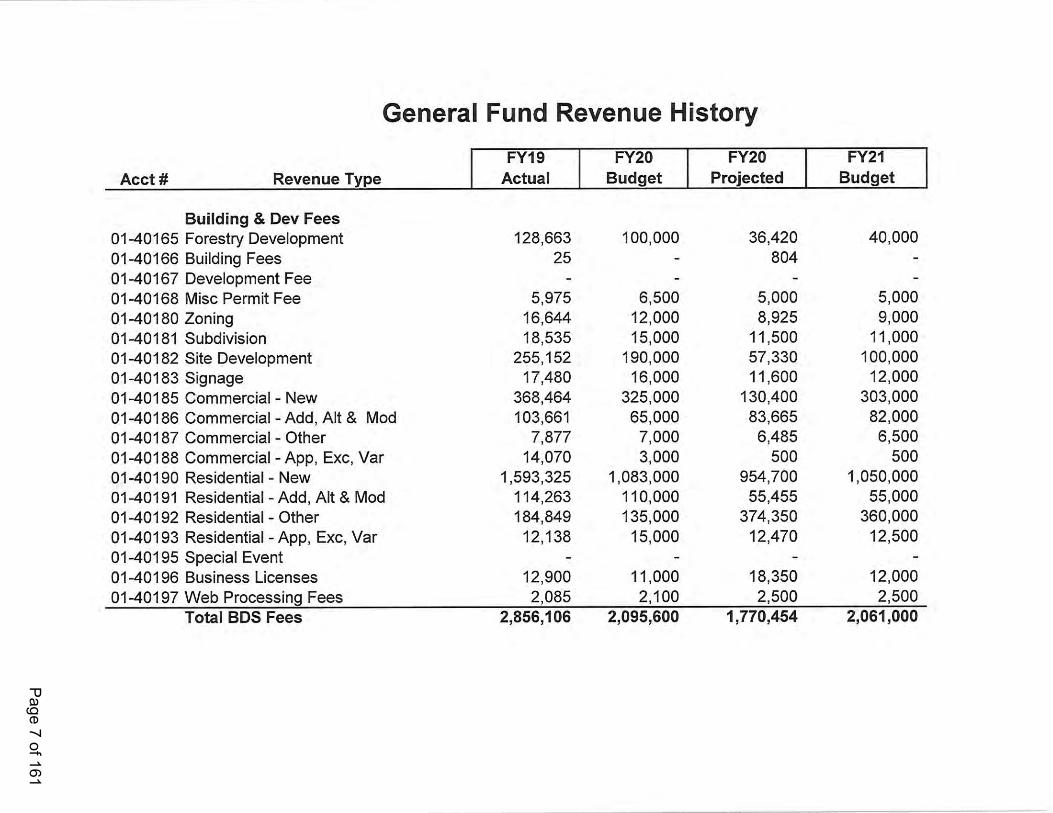

General Fund Revenue History

FY19 FY20 FY20 FY21

Acct # Revenue Type Actual Budget Projected Budget

Building & Dev Fees01-40165 Forestry Development 128,663 100,000 36,420 40,00001-40166 Building Fees 25 - 804 -

01-40167 Development Fee - - - -

01-40168 Misc Permit Fee 5,975 6,500 5,000 5,00001-40180 Zoning 16,644 12,000 8,925 9,00001-40181 Subdivision 18,535 15,000 11,500 11,00001-40182 Site Development 255,152 190,000 57,330 100,00001-40183 Signage 17,480 16,000 11,600 12,00001-40185 Commercial - New 368,464 325,000 130,400 303,00001-40186 Commercial - Add, Alt & Mod 103,661 65,000 83,665 82,00001-40187 Commercial - Other 7,877 7,000 6,485 6,50001-40188 Commercial - App, Exc, Var 14,070 3,000 500 50001-40190 Residential — New 1,593,325 1,083,000 954,700 1,050,00001-40191 Residential - Add, Alt & Mod 114,263 110,000 55,455 55,00001-40192 Residential - Other 184,849 135,000 374,350 360,00001-40193 Residential - App, Exc, Var 12,138 15,000 12,470 12,50001-40195 Special Event - - - -

01-40196 Business Licenses 12,900 11,000 18,350 12,00001-40197 Web Processing Fees 2,085 2,100 2,500 2,500

Total BDS Fees 2,856,106 2,095,600 1,770,454 2,061,000

Page 7 of 161

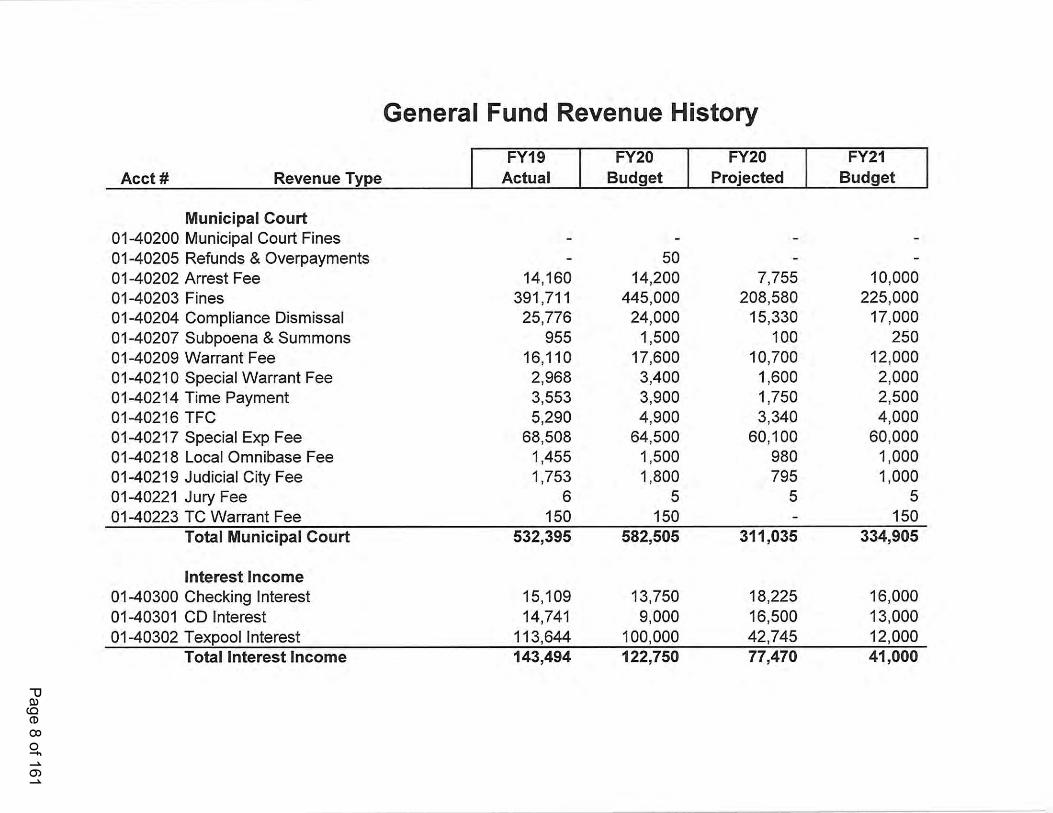

General Fund Revenue History

FY19 FY20 FY20 FY21Acct # Revenue Type Actual Budget Projected Budget

Municipal Court01-40200 Municipal Court Fines -

5001-40205 Refunds & Overpayments - - -

01-40202 Arrest Fee 14,160 14,200 7,755 10,00001-40203 Fines 391,711 445,000 208,580 225,00001-40204 Compliance Dismissal 25,776 24,000 15,330 17,00001-40207 Subpoena & Summons 955 1,500 100 25001-40209 Warrant Fee 16,110 17,600 10,700 12,00001-40210 Special Warrant Fee 2,968 3,400 1,600 2,00001-40214 Time Payment 3,553 3,900 1,750 2,50001-40216 TFC 5,290 4,900 3,340 4,00001-40217 Special Exp Fee 68,508 64,500 60,100 60,00001-40218 Local Omnibase Fee 1,455 1,500 980 1,00001-40219 Judicial City Fee 1,753 1,800 795 1,00001-40221 Jury Fee 6 5 5 501-40223 TC Warrant Fee 150 150 - 150

Total Municipal Court 532,395 582,505 311,035 334,905

Interest Income01-40300 Checking Interest 15,109 13,750 18,225 16,00001-40301 CD Interest 14,741 9,000 16,500 13,00001-40302 Texpool Interest 113,644 100,000 42,745 12,000

Total Interest Income 143,494 122,750 77,470 41,000

Page 8 of 161

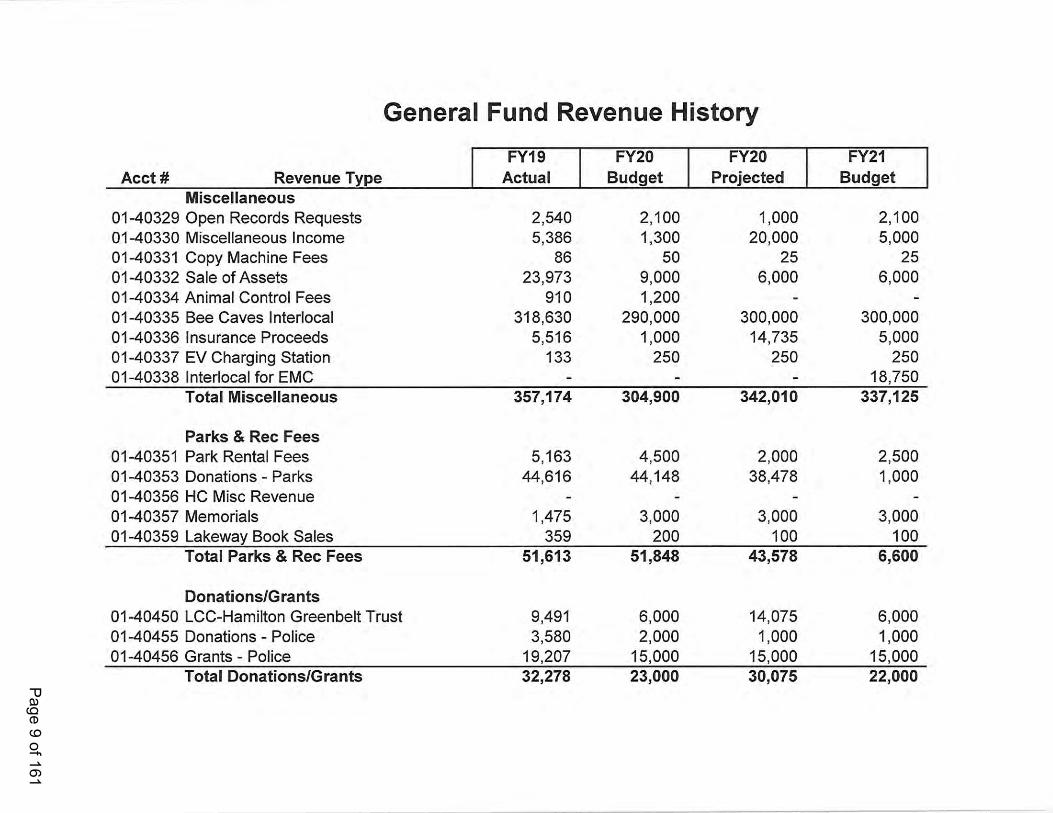

General Fund Revenue History

FY19 FY20 FY20 FY21Acct # Revenue Type Actual Budget Projected Budget

Miscellaneous01-40329 Open Records Requests 2,540 2,100 1,000 2,10001-40330 Miscellaneous Income 5,386 1,300 20,000 5,00001-40331 Copy Machine Fees 86 50 25 2501-40332 Sale of Assets 23,973 9,000 6,000 6,00001-40334 Animal Control Fees 910 1,200 - —

01-40335 Bee Caves lnterlocal 318,630 290,000 300,000 300,00001-40336 Insurance Proceeds 5,516 1,000 14,735 5,00001-40337 EV Charging Station 133 250 250 25001-40338 lnterlocal for EMC - - - 18,750

Total Miscellaneous 357,174 304,900 342,010 337,125

Parks & Rec Fees01-40351 Park Rental Fees 5,163 4,500 2,000 2,50001-40353 Donations - Parks 44,616 44,148 38,478 1,000O1-40356 HC Misc Revenue - - - -

01-40357 Memorials 1,475 3,000 3,000 3,00001-40359 Lakeway Book Sales 359 200 100 100

Total Parks & Rec Fees 51,613 51,848 43,578 6,600

DonationsIGrants01-40450 LCC-Hamilton Greenbelt Trust 9,491 6,000 14,075 6,00001-40455 Donations - Police 3,580 2,000 1,000 1,000O1-40456 Grants - Police 19,207 15,000 15,000 15,000

Total DonationslGrants 32,278 23,000 30,075 22,000Page 9 of 161

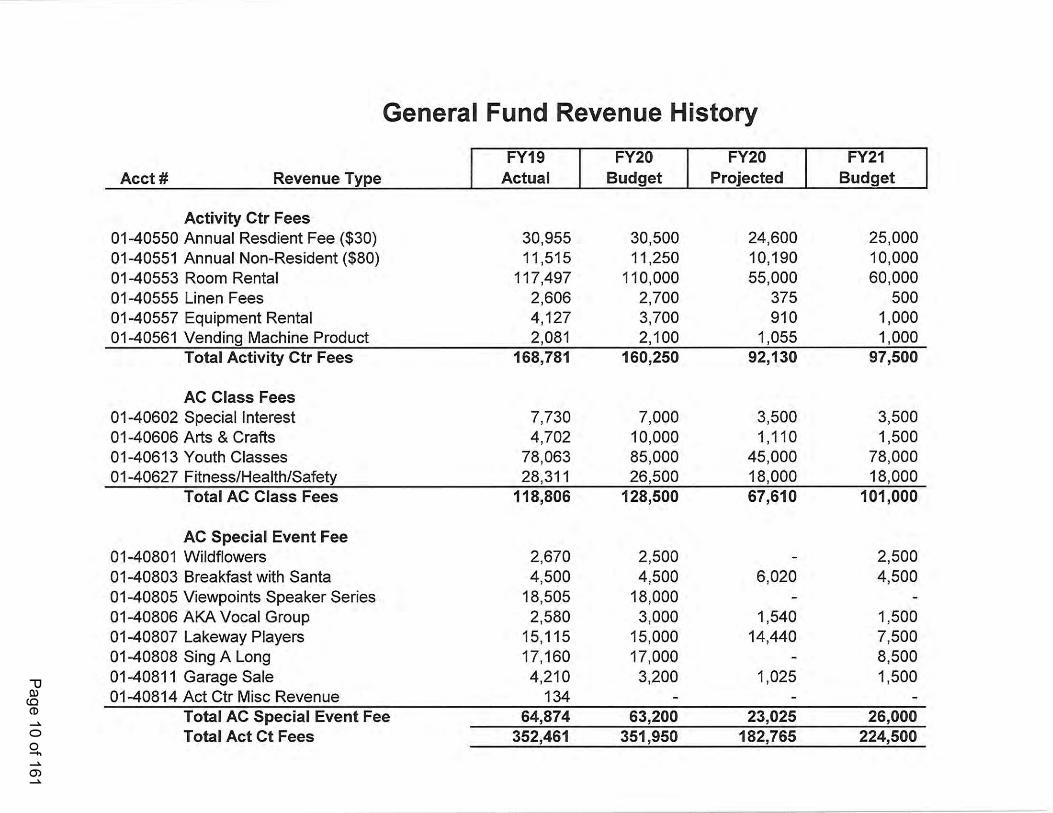

General Fund Revenue History

FY19 FY20 FY20Acct # Revenue Type Actual Budget Projected

Activity Ctr Fees01-40550 Annual Resdient Fee ($30) 30,955 30,500 24,60001-40551 Annual Non-Resident ($80) 11,515 11,250 10,19001-40553 Room Rental 117,497 110,000 55,00001-40555 Linen Fees 2,606 2,700 37501-40557 Equipment Rental 4,127 3,700 91001-40561 Vending Machine Product 2,081 2,100 1,055

Total Activity Ctr Fees 168,781 160,250 92,130

AC Class Fees01-40602 Special Interest 7,730 7,000 3,50001-40606 Arts & Crafts 4,702 10,000 1,11001-40613 Youth Classes 78,063 85,000 45,00001-40627 Fitness/Health/Safety 28,311 26,500 18,000

Total AC Class Fees 118,806 128,500 67,610

AC Special Event Fee01-40801 Wildflowers 2,670 2,500 -

01-40803 Breakfast with Santa 4,500 4,500 6,02001-40805 Viewpoints Speaker Series 18,505 18,000 -

01-40806 AKAVocal Group 2,580 3,000 1,54001-40807 Lakeway Players 15,115 15,000 14,44001-40808 Sing A Long 17,160 17,000 -

01-40811 Garage Sale 4,210 3,200 1,02501-40814 Act Ctr Misc Revenue 134 - -

Total AC Special Event Fee 64,874 63,200 23,025Total Act Ct Fees 352,461 351,950 182,765

FY21Budget

25,00010,00060,000

5001,0001,000

97,500

3,5001,500

78,00018,000

101,000

2,5004,500

1,5007,5008,5001,500

26,000224,500

Page 10 of 161

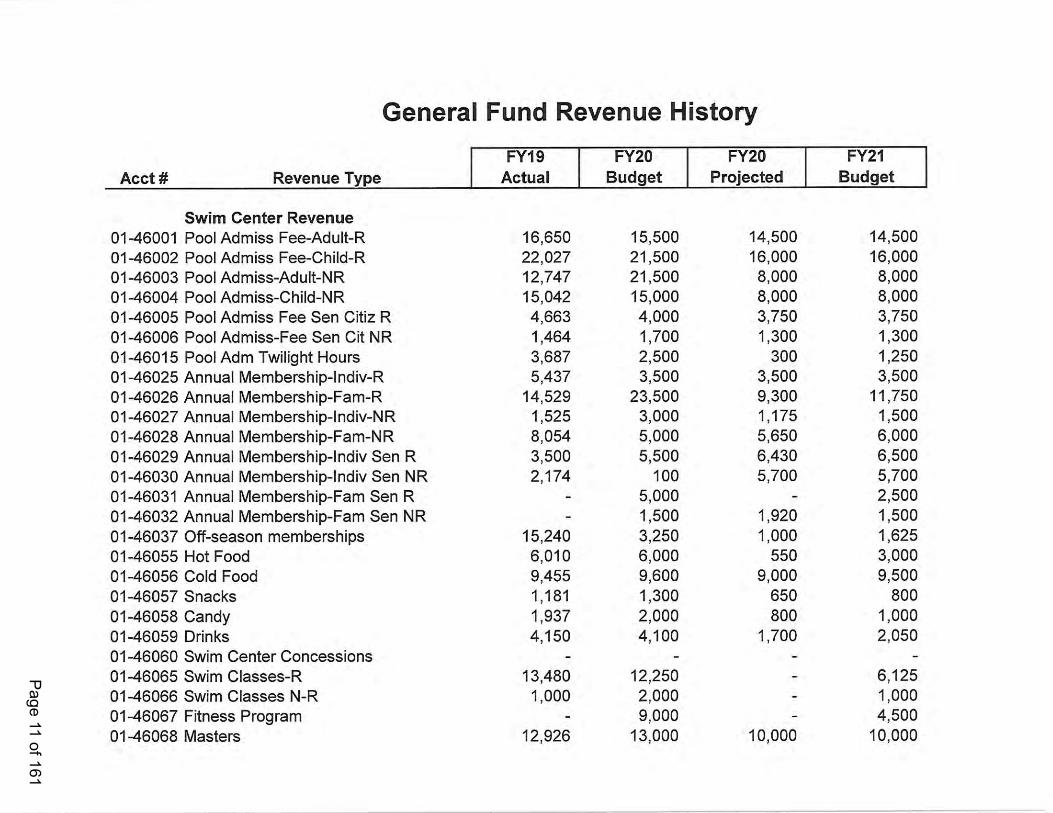

General Fund Revenue History

FY19 FY20 FY20 FY21Acct # Revenue Type Actual Budget Projected Budget

Swim Center Revenue01-46001 Pool Admiss Fee-Adult-R 16,650 15,500 14,500 14,50001-46002 Pool Admiss Fee-Child-R 22,027 21,500 16,000 16,00001-46003 Pool Admiss-Adult-NR 12,747 21,500 8,000 8,00001-46004 Pool Admiss-Child-NR 15,042 15,000 8,000 8,00001-46005 Pool Admiss Fee Sen Citiz R 4,663 4,000 3,750 3,75001-46006 Pool Admiss-Fee Sen Cit NR 1,464 1,700 1,300 1,30001-46015 Pool Adm Twilight Hours 3,687 2,500 300 1,25001-46025 Annual Membership-lndiv-R 5,437 3,500 3,500 3,50001-46026 Annual Membership—Fam-R 14,529 23,500 9,300 11,75001-46027 Annual Membership-lndiv-NR 1,525 3,000 1,175 1,50001-46028 Annual Membership-Fam-NR 8,054 5,000 5,650 6,00001-46029 Annual Membership-lndiv Sen R 3,500 5,500 6,430 6,50001-46030 Annual Membership-lndiv Sen NR 2,174 100 5,700 5,70001-46031 Annual Membership-Fam Sen R - 5,000 - 2,50001-46032 Annual Membership-Fam Sen NR - 1,500 1,920 1,50001-46037 Off-season memberships 15,240 3,250 1,000 1,62501-46055 Hot Food 6,010 6,000 550 3,00001-46056 Cold Food 9,455 9,600 9,000 9,50001-46057 Snacks 1,181 1,300 650 80001-46058 Candy 1,937 2,000 800 1,00001-46059 Drinks 4,150 4,100 1,700 2,05001-46060 Swim Center Concessions - - - -

01-46065 Swim Classes-R 13,480 12,250 - 6,12501-46066 Swim Classes N-R 1,000 2,000 - 1,00001-46067 Fitness Program - 9,000 4,500O1-46068 Masters 12,926 13,000 10,000 10,000

Page 11 of 161

General Fund Revenue History

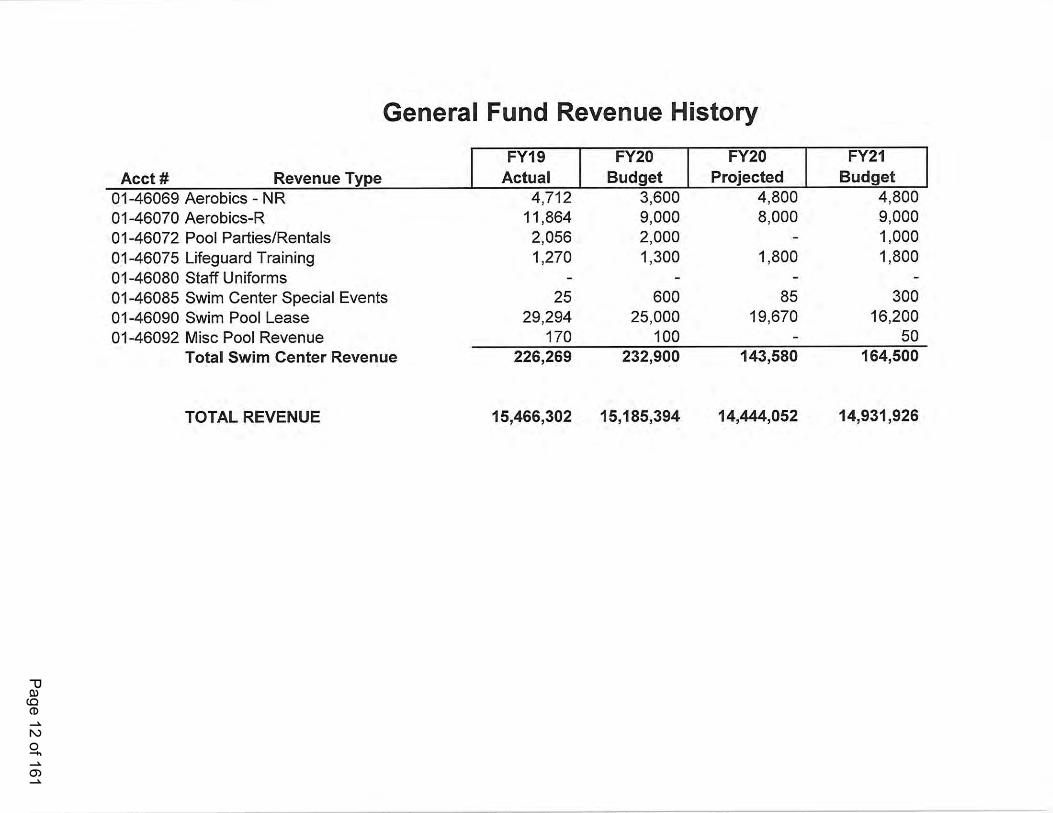

FY19 FY20 FY20 FY21Acct # Revenue Type Actual Budget Projected Budget

01-46069 Aerobics - NR 4,712 3,600 4,800 4,80001-46070 Aerobics-R 11,864 9,000 8,000 9,00001-46072 Pool Parties/Rentals 2,056 2,000 - 1,00001-46075 Lifeguard Training 1,270 1,300 1,800 1,80001-46080 Staff Uniforms - — - -

01-46085 Swim Center Special Events 25 600 85 30001-46090 Swim Pool Lease 29,294 25,000 19,670 16,20001-46092 Misc Pool Revenue 170 100 - 50

Total Swim Center Revenue 226,269 232,900 143,580 164,500

TOTAL REVENUE 15,466,302 15,185,394 14,444,052 14,931,926

Page 12 of 161

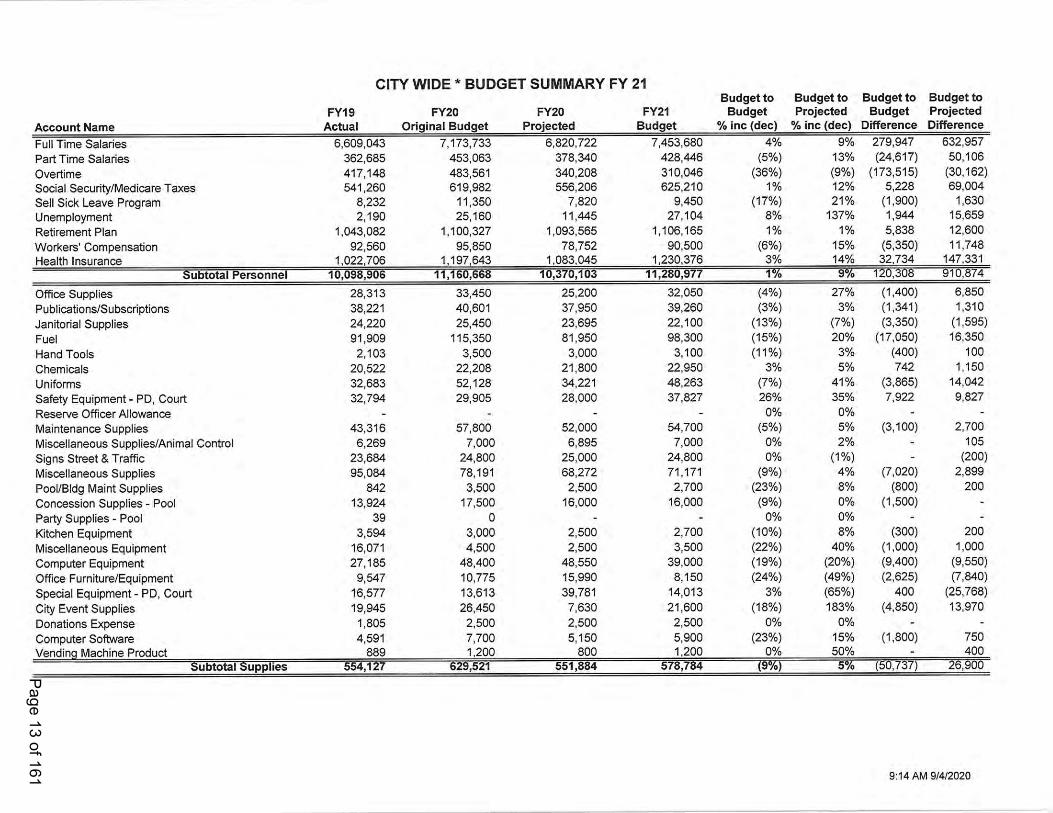

CITY WIDE * BUDGET SUMMARY FY 21Budget to Budget to Budget to Budget to

FY19 FY20 FY20 FY21 Budget Projected Budget Projected

Account Name Actual Original Budget Projected Budget % inc (dec) % inc (dec) Difference Difference

Full Time Salaries 6,609,043 7,173,733 6,820,722 7,453,680 4% 9% 279,947 632,957

Part Time Salaries 362,685 453,063 378,340 428,446 (5%) 13% (24,617) 50,106

Overtime 417,148 483,561 340,208 310,046 (36%) (9%) (173,515) (30,162)

Social Security/Medicare Taxes 541,260 619,982 556,206 625,210 1% 12% 5,228 69,004

Sell Sick Leave Program 8,232 11,350 7,820 9,450 (17%) 21% (1,900) 1,630

Unemployment 2,190 25,160 11,445 27,104 8% 137% 1,944 15,659

Retirement Plan 1,043,082 1,100,327 1,093,565 1,106,165 1% 1% 5,838 12,600

Workers‘ Compensation 92,560 95,850 78,752 90,500 (6%) 15% (5,350) 11,748

Health Insurance 1,022,706 1,197,643 1,083,045 1,230,376 3% 14% 32,734 147,331Subtotal Personnel 10,098,906 11,160,668 10,370,103 11,280,977 1% 9% 120,308 910,874

Of?ce Supplies 28,313 33,450 25,200 32,050 (4%) 27% (1,400) 6,850

Publications/Subscriptions 38,221 40,601 37,950 39,260 (3%) 3% (1,341) 1,310

Janitorial Supplies 24,220 25,450 23,695 22,100 (13%) (7%) (3,350) (1,595)

Fuel 91,909 115,350 81,950 98,300 (15%) 20% (17,050) 16,350

Hand Tools 2,103 3,500 3,000 3,100 (11%) 3% (400) 100

Chemicals 20,522 22,208 21,800 22,950 3% 5% 742 1,150

Uniforms 32,683 52,128 34,221 48,263 (7%) 41% (3,865) 14,042

Safety Equipment - PD, Court 32,794 29,905 28,000 37,827 26% 35% 7,922 9,827

Reserve Of?cer Allowance - ~ — - 0% 0% — —

Maintenance Supplies 43,316 57,800 52,000 54,700 (5%) 5% (3,100) 2,700

Miscellaneous Supplies/Animal Control 6,269 7,000 6,895 7,000 0% 2% - 105

Signs Street &Traf?c 23,684 24,800 25,000 24,800 0% (1%) - (200)

Miscellaneous Supplies 95,084 78,191 68,272 71,171 (9%) 4% (7,020) 2,899

Pool/Bldg Maint Supplies 842 3,500 2,500 2,700 (23%) 8% (800) 200

Concession Supplies - Pool 13,924 17,500 16,000 16,000 (9%) 0% (1,500) —

Party Supplies - Pool 39 0 — - 0% 0% - -

Kitchen Equipment 3,594 3,000 2,500 2,700 (10%) 8% (300) 200

Miscellaneous Equipment 16,071 4,500 2,500 3,500 (22%) 40% (1,OOO) 1,000

Computer Equipment 27,185 48,400 48,550 39,000 (19%) (20%) (9,400) (9,550)

Of?ce Furniture/Equipment 9,547 10,775 15,990 8,150 (24%) (49%) (2,625) (7,840)

Special Equipment - PD, Court 16,577 13,613 39,781 14,013 3% (65%) 400 (25,768)

City Event Supplies 19,945 26,450 7,630 21,600 (18%) 183% (4,850) 13,970

Donations Expense 1,805 2,500 2,500 2,500 0% 0% — —

Computer Software 4,591 7,700 5,150 5,900 (23%) 15% (1,800) 750

Vending Machine Product 889 1,200 800 1,200 0% 50% - 400Subtotal Supplies 554,127 629,521 551,884 578,784 (9%) 5% (50,737) 26,900

9:14 AM 9/4/2020

Page 13 of 161

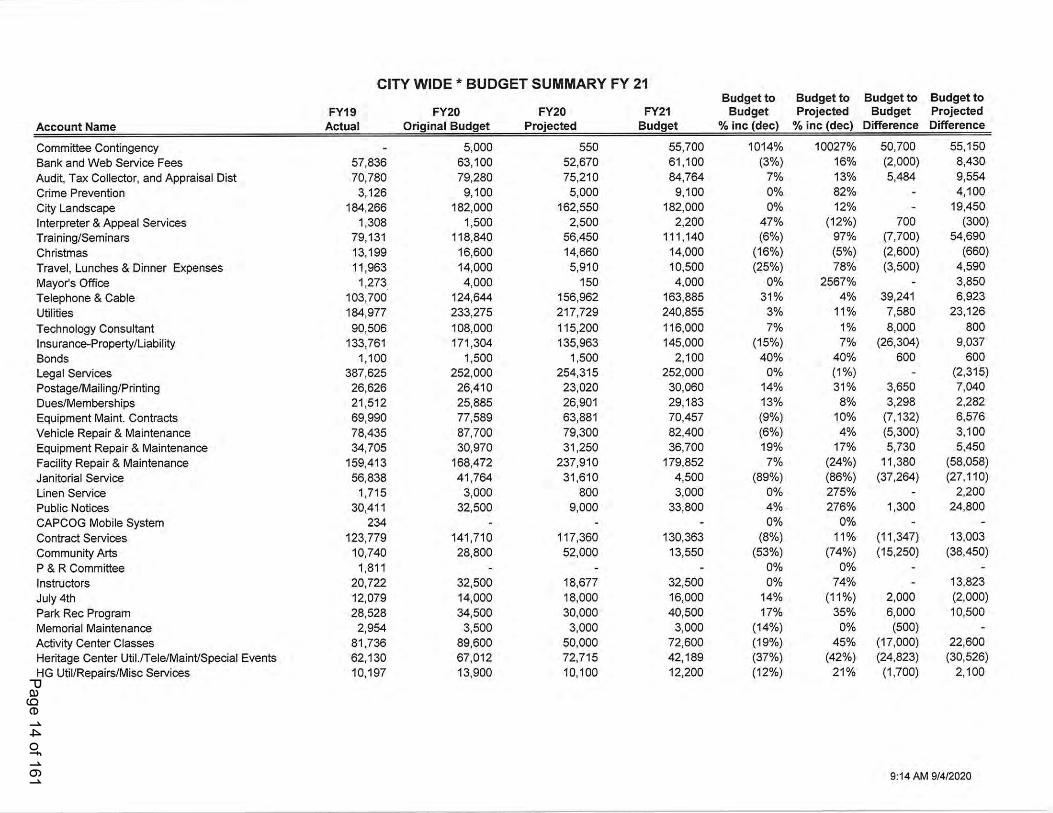

CITY WIDE * BUDGET SUMMARY FY 21Budget to Budget to Budget to Budget to

FY19 FY20 FY20 FY21 Budget Projected Budget Projected

Account Name Actual Original Budget Projected Budget % inc (dec) % inc (dec) Difference Difference

Committee Contingency - 5,000 550 55,700 1014% 10027% 50,700 55,150

Bank and Web Service Fees 57,836 63,100 52,670 61,100 (3%) 16% (2,000) 8,430

Audit, Tax Collector, and Appraisal Dist 70,780 79,280 75,210 84,764 7% 13% 5,484 9,554

Crime Prevention 3,126 9,100 5,000 9,100 0% 82% - 4,100City Landscape 184,266 182,000 162,550 182,000 0% 12% - 19,450

Interpreter &Appeal Services 1,308 1,500 2,500 2,200 47% (12%) 700 (300)

Training/Seminars 79,131 118,840 56,450 111,140 (6%) 97% (7,700) 54,690

Christmas 13,199 16,600 14,660 14,000 (16%) (5%) (2,600) (660)

Travel, Lunches & Dinner Expenses 11,963 14,000 5,910 10,500 (25%) 78% (3,500) 4,590

Mayor's Of?ce 1,273 4,000 150 4,000 0% 2567% - 3.850Telephone & Cable 103,700 124,644 156,962 163,885 31% 4% 39,241 6,923

Utilities 184,977 233,275 217,729 240,855 3% 11% 7,580 23,126

Technology Consultant 90,506 108,000 115,200 116,000 7% 1% 8,000 800Insurance—Property/Liability 133,761 171,304 135,963 145,000 (15%) 7% (26,304) 9,037

Bonds 1,100 1,500 1,500 2,100 40% 40% 600 600

Legal Services 387,625 252,000 254,315 252,000 0% (1%) — (2,315)

Postage/Mailing/Printing 26,626 26,410 23,020 30,060 14% 31% 3,650 7,040

Dues/Memberships 21,512 25,885 26,901 29,183 13% 8% 3,298 2,282Equipment Maint. Contracts 69,990 77,589 63,881 70,457 (9%) 10% (7,132) 6,576Vehicle Repair & Maintenance 78,435 87,700 79,300 82,400 (6%) 4% (5,300) 3,100

Equipment Repair & Maintenance 34,705 30,970 31,250 36,700 19% 17% 5,730 5,450Facility Repair & Maintenance 159,413 168,472 237,910 179,852 7% (24%) 11,380 (58,058)

Janitorial Service 56,838 41,764 31,610 4,500 (89%) (86%) (37,264) (27,110)

Linen Service 1,715 3,000 800 3,000 0% 275% — 2,200

Public Notices 30,411 32,500 9,000 33,800 4% 276% 1,300 24,800CAPCOG Mobile System 234 — - — 0% 0% - —

Contract Services 123,779 141,710 117,360 130,363 (8%) 11% (11,347) 13,003Community Arts 10,740 28,800 52,000 13,550 (53%) (74%) (15,250) (38,450)

P & R Committee 1,811 - - - 0% 0% — —

Instructors 20,722 32,500 18,677 32,500 0% 74% - 13,823July 4th 12,079 14,000 18,000 16,000 14% (11%) 2,000 (2,000)

Park Rec Program 28,528 34,500 30,000 40,500 17% 35% 6,000 10,500Memorial Maintenance 2,954 3,500 3,000 3,000 (14%) 0% (500) —

Activity Center Classes 81,736 89,600 50,000 72,600 (19%) 45% (17,000) 22,600

Heritage Center Util./Tele/Maint/Special Events 62,130 67,012 72,715 42,189 (37%) (42%) (24,823) (30,526)

HG Util/Repairs/Misc Services 10,197 13,900 10,100 12,200 (12%) 21% (1,700) 2,100

9:14 AM 9/4/2020

Page 14 of 161

CITY WIDE * BUDGET SUMMARY FY 21Budget to Budget to Budget to Budget to

FY20 FY20 FY21 Budget Projected Budget ProjectedAccount Name Actual Original Budget Projected Budget °/a inc (dec) % inc (dec) Difference Difference

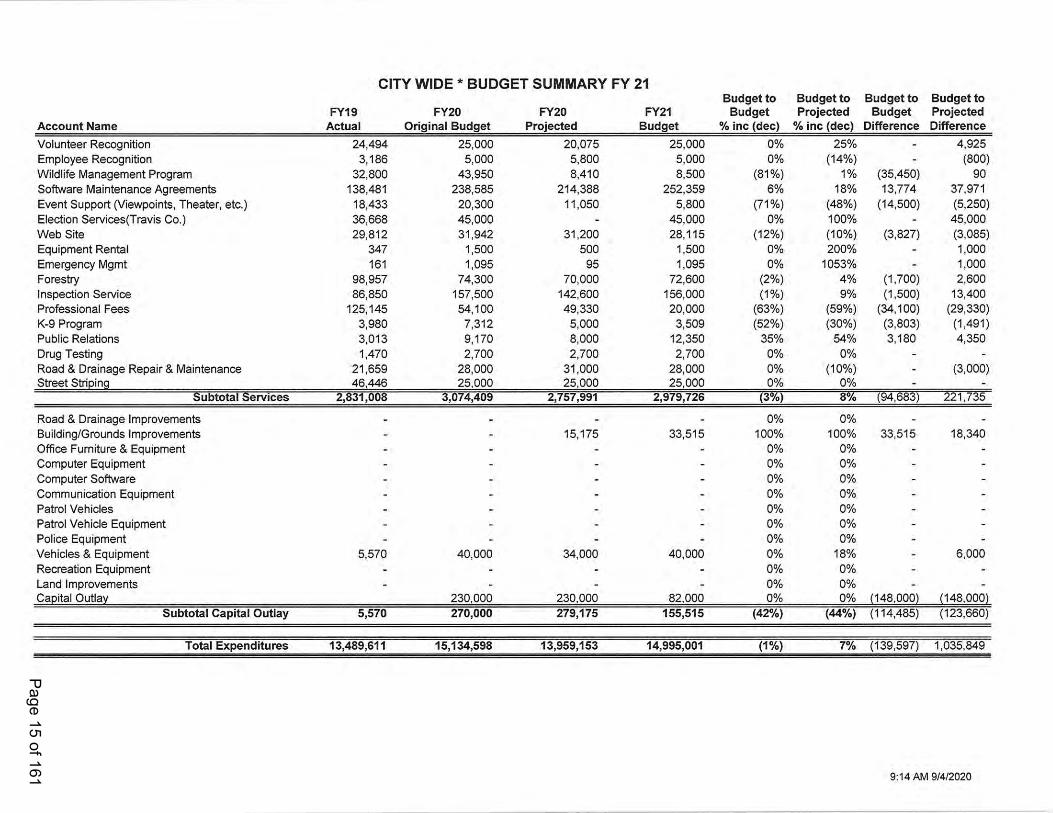

Volunteer Recognition 24,494 25,000 20,075 25,000 0% 25% - 4,925Employee Recognition 3,186 5,000 5,800 5,000 0% (14%) — (800)Wildlife Management Program 32,800 43,950 8,410 8,500 (81%) 1% (35,450) 90Software Maintenance Agreements 138,481 238,585 214,388 252,359 6% 18% 13,774 37,971Event Support (Viewpoints, Theater, etc.) 18,433 20,300 11,050 5,800 (71%) (48%) (14,500) (5,250)Election Services(Travis Co.) 36,668 45,000 — 45,000 0% 100% - 45,000Web Site 29,812 31,942 31,200 28,115 (12%) (10%) (3,827) (3,085)Equipment Rental 347 1,500 500 1,500 0% 200% - 1,000Emergency Mgmt 161 1,095 95 1,095 0% 1053% - 1,000Forestry 98,957 74,300 70,000 72,600 (2%) 4% (1,700) 2,600Inspection Service 86,850 157,500 142,600 156,000 (1%) 9% (1,500) 13,400Professional Fees 125,145 54,100 49,330 20,000 (63%) (59%) (34,100) (29,330)K-9 Program 3,980 7,312 5,000 3,509 (52%) (30%) (3,803) (1,491)Public Relations 3,013 9,170 8,000 12,350 35% 54% 3,180 4,350Drug Testing 1,470 2,700 2,700 2,700 0% 0% - -

Road & Drainage Repair & Maintenance 21,659 28,000 31,000 28,000 0% (10%) — (3,000)Street Striping 46,446 25,000 25,000 25,000 0% 0% - ~

Subtotal services 2,831,008 3,074,409 2,757,991 2,979,726 (3%) 3% (94,683) 221,735

Road & Drainage Improvements - - - - 0% 0% — —

Building/Grounds Improvements - - 15,175 33,515 100% 100% 33,515 18,340Of?oe Furniture & Equipment - - - - 0% 0% - —

Computer Equipment - — - - 0% 0% — —

Computer Software - - - — 0% 0% - -

Communication Equipment - ~ - - 0% 0% - -

Patrol Vehicles - - — - 0% 0% - -

Patrol Vehicle Equipment — - — — 0% 0% - -

Police Equipment ~ - - - 0% 0% - —

Vehicles & Equipment 5,570 40,000 34,000 40,000 0% 18% - 6,000Recreation Equipment - - - - 0% 0% — —

Land Improvements - - - - 0% 0% - -

Capital Outlay 230,000 230,000 82,000 0% 0% (148,000) (148,000)Subtotal capital Outlay 5,570 270,000 279,175 155,515 (42%) (44%) (114,485) (123,660)

Total Expenditures 13,489,611 15,134,598 13,959,1 53 14,995,001 (1%) 7% (139,597) 1,035,849

9:14 AM 9/4/2020

Page 15 of 161

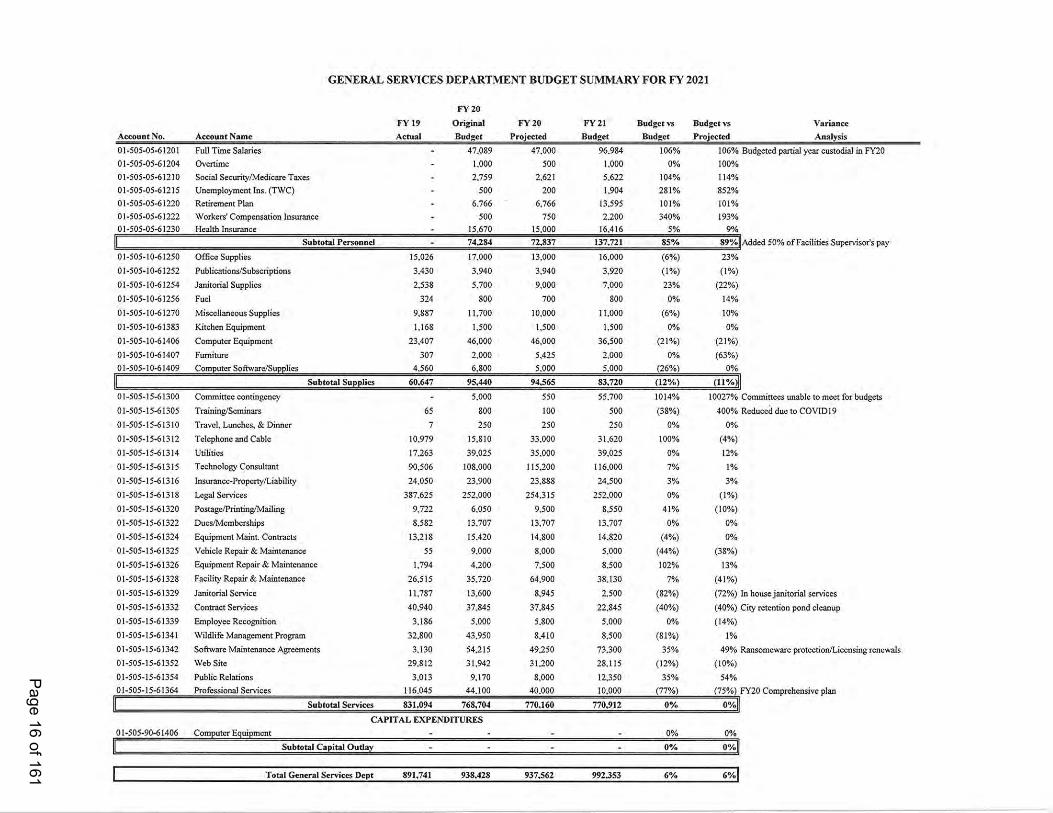

GENERAL SERVICES DEPARTMENT BUDGET SUMMARY FOR FY 2021

1=)( 20

1w 19 Original 1w 20 FY 21 Budget vs Budget vs variance

Account No. Account Name Actual Budget Projected Budget Budget Projected Analysis

01.50s.05-61201 Full Time sa1nries - 47.039 47.000 96.934 106% 106% Budgeted partisi year eustodia1in FY20

01-505.05.61204 Ovcnimc . 1,000 500 1.000 0% 100%

01-505-05-61210 sociai Security/MedicaxeTaxes . 2.759 2.621 5.622 104% 114%

01-505-0561215 unernp1eyrnent1ns. (TWC) . 500 200 1.904 231% 352%

01-505-05-61220 Retirement 1>1an - 6.766 6.766 13.595 101% 101%

01-S05-05-61222 Wurkcrs’ compensation insurance - 500 750 340% 193%

01.505-05-61230 Health Insumnce - 15.670 15.000 5% 9%

Subtotal 1>ersonne1 - 74,234 7 Add¢d 50% of Faei1iu'esSupervisor's pay

01-505-1061250 Of?ce Supplies 15.026 17.000 13.000 16.000 (6%) 23%

01-505-10-61252 Publications/Subscriptions 3.430 3.940 3.940 3.920 (1%) (1%)

01.505.10.61254 Janitorialsuppiics 2.533 5.700 9.000 7.000 23% (22%)

01.505.10-61256 1=uc1 324 300 700 300 0% 14%

01-505-10-61270 Misce11anecussupp1ies 9.337 11.700 10.000 11.000 (6%) 10%

01-505-10-61333 KitchenEquipment 1.163 1.500 1.500 1.500 0% 0%

o1.505.10-61406 computer Equipment 23.407 46.000 46.000 36.500 (21%) (21%)

01.505-10-61407 Fumiturc 307 2.000 5.425 2.000 0% (63%)

01-505-10-61409 computer So?waxe/Supplies 4.560 6.800 5.000 5.000 (26%) 0%

subtotai supniies 60.647 95.440 94.565 33.720 (12%) (11%)

01.505.15.61300 cemrnittee contingency . 5.000 550 55.700 1014% 10027% committees unable to meet for budgets

01-505-15.61305 1-raining/seminars 65 300 100 500 (33%) 400% Reduced due to cov11>19

01-505-15.61310 Travel. Lunches.3; Dinner 7 250 250 250 0% 0%

01-505-1561312 Te1ep1i6neand Cable 10.979 15.310 33.000 31.620 100% (4%)

01.505.1561314 Utiliiics 17.265 39.025 35.000 39.025 0% 12%

01.505.1561315 Technology censuitant 90.506 103.000 115.200 116.000 7% 1%

01-505-15.61316 Insumnc:-Property/Liability 24.050 23.900 23.333 24.500 3% 3%

01-505-15-61313 1.ega1services 337.625 252.000 254.315 252.000 0% (1%)

01.505.15.61320 Paslage/Printing/Mailing 9.722 6.050 9.500 3.550 41% (10%)

01.505.15-61322 Dues/Memberships 3.532 13.707 13.707 13.707 0% 0%

01.505.15-61324 Equipment Maint. contracts 12.213 15.420 14.300 14.320 (4%) 0%

01-505.15-61325 Vehicle Repair 5: Maintenance 55 9.000 3,000 5.000 (44%) (33%)

01-50545-61326 Equipment Repair 3; Mnintenanee 1.794 4.200 7.500 3.500 102% 13%

01-505-15-61323 FacilityRepair & Mainlcncu-ice 26.515 35.720 64,900 33.130 7% (41%)

01-505-1561329 Janitorialservice 11.737 13.600 3.945 2.500 (32%) (72%) In house janitorial services

01-505-1561332 contract services 40.940 37.345 37.345 22.345 (40%) (40%) city retention pond ciennup

01-505-1561339 Employee Recognition 3.136 5.000 5.300 5.000 0% (14%)

01-505.1561341 Wildlife Management Program 32.300 43.950 3.410 3.500 (31%) 1%

01.505.15-61342 So?ware Maintenance Agrccmcnls 3.130 54.215 49.250 73.300 35% 49% Rnnsoroevvare protection/Licensingre-nevva1s

01.505.15-61352 web site 29.312 31,942 31.200 23.115 (12%) (10%)

01.505.15-61354 Public Re1a6ens 3.013 9.170 3.000 12,350 35% 54%

01-505.15-61364 Professional services 116.045 44.100 4()£9_0 10.000 (77%) (75%) FY20 Comprehensive p1an

__ Subtotal services 331.094 768.704 770.160 770.912 0% 0%

CAPITAL EXPENDITURES

01-505-90-61406 computer Equipment . . - - 0% 0%

Subtotal Capital oug - - - - 0% 0%

Page 16 of 161

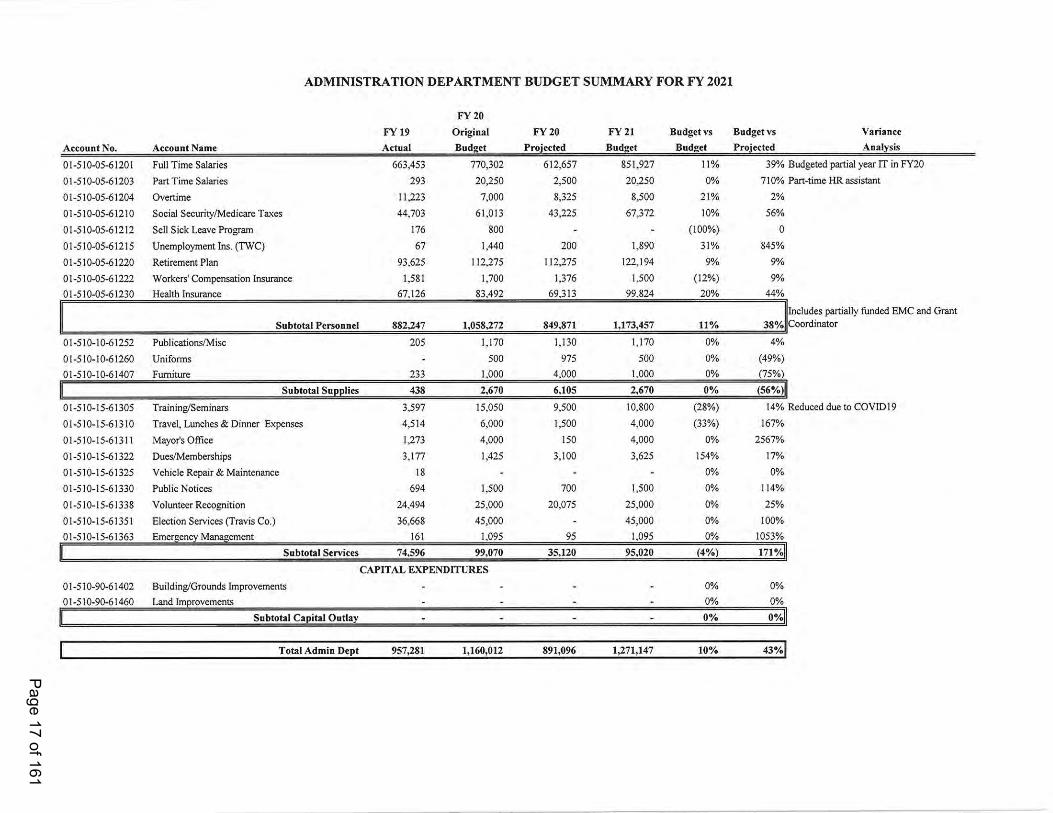

ADMINISTRATION DEPARTMENT BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 Original FY 20 FY 21 Budget vs Budget vs Variance

Account No. Account Name Actual Budget Projected Budget Budget Proiccted Analysis

01-510-05-61201 Full Time Salaries 663.453 770,302 612,657 851,927 11% 39% Budgetedpartial year IT in FY20

01-510-05-61203 Part Time Salaries 293 20.250 2.500 20,250 0% 710% Part-timeHR assistant

01-510-05-61204 Overtime 11.223 7.000 8,325 8,500 21% 2%

01-510-05-61210 Social Security/MedicareTaxes 44.703 61.013 43,225 67,372 10% 56%

01-510-05-61212 Sell Sick Leave Program 176 800 - - (100%) 0

01-510-05-61215 Unemployment Ins. (TWC) 67 1.440 200 1.890 31% 845%

01-510—05-61220 RetirementPlan 93.625 112.275 112,275 122,194 9% 9%

01-510-05-61222 Workers’ CompensationInsurance 1.581 1.700 1,376 1.500 (12%) 9%

01-510-05-61230 Health Insurance 67.126 83.492 69,313 99.824 20% 44%

Includespartially funded EMC and Grant

Subtotal Personnel 882,247 1,058,272 849,871 1,173,457 11% 38% C00|'dina1-01“

01-510-10-61252 Publications/Misc 205 1.170 1,130 1,170 0% 4%

01-510-10-61260 Unifonns - 500 975 500 0% (49%)

01-510-10-61407 Furniture 233 1.000 4.000 1.000 0% (75%)

Subtotal Supplies 438 2,670 6,105 2,670 0% (56%)

01-510-15-61305 Training/Seminars 3,597 15,050 9.500 10.800 (28%) 14% Reduced due to COVUJ19

01-510-15-61310 Travel.Lunches& Dinner Expenses 4,514 6,000 1.500 4.000 (33%) 167%

01-510-15-61311 Mayors O?lce 1,273 4.000 150 4.000 0% 2567%

01-510-15-61322 Dues/Memberships 3,177 1,425 3.100 3,625 154% 17%

01-510-15-61325 Vehicle Repair & Maintenance 18 - ~ - 0% 0%

01-510-15-61330 Public Notices 694 1,500 700 1,500 0% 114%

01-51045-61338 Volunteer Recognition 24.494 25,000 20,075 25,000 0% 25%

01-510-15-61351 ElectionServices(Travis Co.) 36,668 45,000 - 45,000 0% 100%

01-510-15-61363 Emergency Management 161 1.095 95 1,095 0% 1053%

Subtotal Services 74,596 99,070 35.120 95.020 (4%) 171%

CAPITAL EXPENDITURES

01-510-90-61402 Bui1dinyGroundsImprovements - - - - 0% 0%

01-510-90-61460 Land Improvements - - - - 0% 0%

Subtotal Capital Outlay - - — - 0% 0%

Page 17 of 161

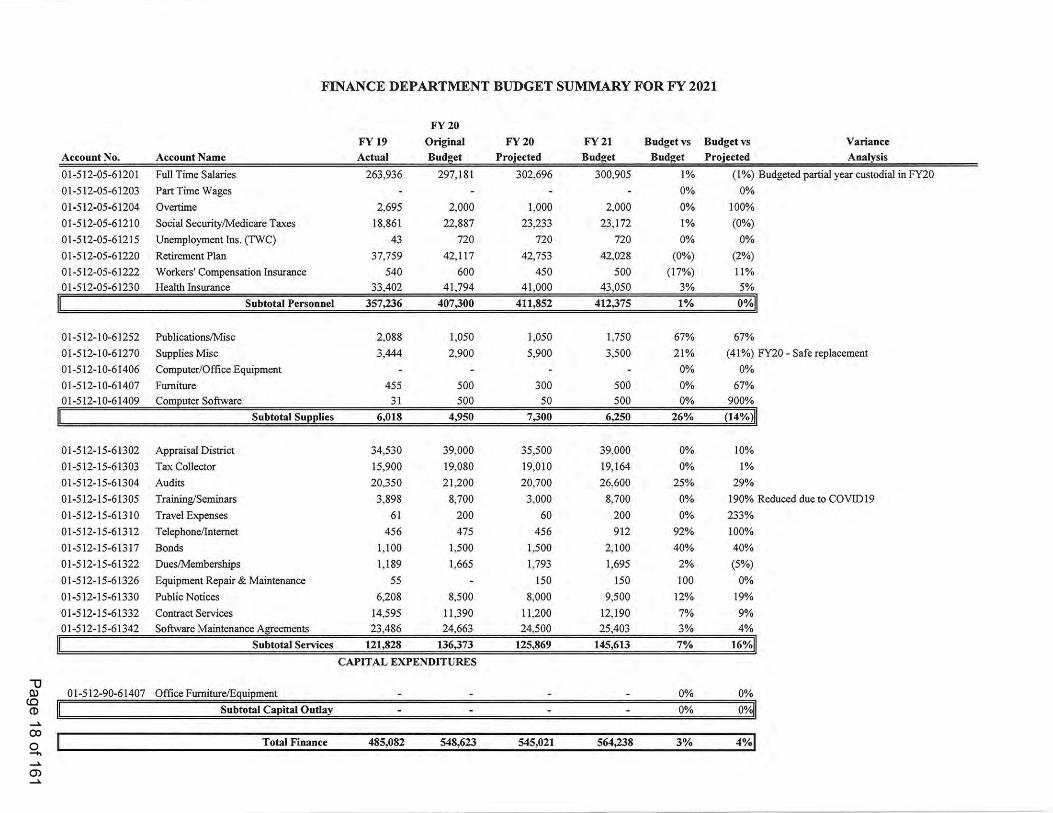

FINANCE DEPARTMENT BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 Original FY 20 FY 21 Budget vs Budget vs Variance

Account No. Account Name Actual Budget Projected Budget Budget Projected Analysis

01-512-05-61201 Full Time Salaries 263,936 297,181 302.696 300,905 1% (1%) Budgeted partialyear custodial in FY20

01-512-05-61203 Part Time Wages - - - - 0% 0%

01-512-05-61204 Overtime 2.695 2,000 1,000 2,000 0% 100%

01-512-05-61210 Social Security/Medicare Taxes 18,861 22,887 23,233 23,172 1% (0%)

01-512-05-61215 Unemployment Ins. (TWC) 43 720 720 720 0% 0%

01-512-05-61220 Retirement Plan 37.759 42.117 42.753 42.028 (0%) (2%)

01-512-05-61222 Workers‘ Compensation Insurance 540 600 450 500 (17%) 11%

01-512-05-61230 Health Insurance 33.402 41.794 41,000 43.050 3% 5%

Subtotal Personnel 357,236 407,300 411,852 412,375 1% 0%

01-512-10-61252 Publicxations/Misc 2.088 1.050 1.050 1.750 67% 67%

01-512-10-61270 Supplies Misc 3,444 2,900 5.900 3,500 21% (41%) FY20 - Safe replacement

0 1-5 12-10-61406 Computer/Office Equipment - - - - 0% 0%

01-512-10-61407 Fumiture 455 500 300 500 0% 67%

01-512-10-61409 Computer Software 31 500 50 500 0% 900%

Subtotal Supplies 6,018 4,950 7,300 6,250 26% (14%)

01-512-15-61302 AppraisalDistrict 34530 39,000 35,500 39.000 0% 10%

01-512-15-61303 Tax Collector 15,900 19,080 19,010 19,164 0% 1%

01-512-15-61304 Audits 20.350 21.200 20.700 26.600 25% 29%

01-512-15-61305 Traininyseminars 3.898 8.700 3,000 8.700 0% 190% Reduced due to COVIDI9

01-512-15-61310 Travel Expenses 61 200 60 200 0% 233%

01-512-15-61312 Telephone/Intemet 456 475 456 912 92% 100%

01-512-15-61317 Bonds 1.100 1.500 1.500 2.100 40% 40%

01-512-15-61322 Dues/‘Memberships 1.189 1,665 1.793 1,695 2% (5%)

01-512-15-61326 EquipmentRepair & Maintenance 55 - 150 150 100 0%

01-512-15-61330 Public Notices 6,208 8,500 8.000 9,500 12% 19%

01-512-15-61332 Contract Services 14,595 11,390 11,200 12,190 7% 9%01-512-15-61342 Software Maintenance Agreements 23,486 24,663 24.500 25.403 3% 4%

Subtotal Services 121,828 136,373 125,869 145,613 7% 16%

CAPITAL EXPENDITURES

01-512-90-61407 Office Fumiture/Equipment - - - - 0% 0%

Subtotal Capital Outlay - - - - 0% 0%

Page 18 of 161

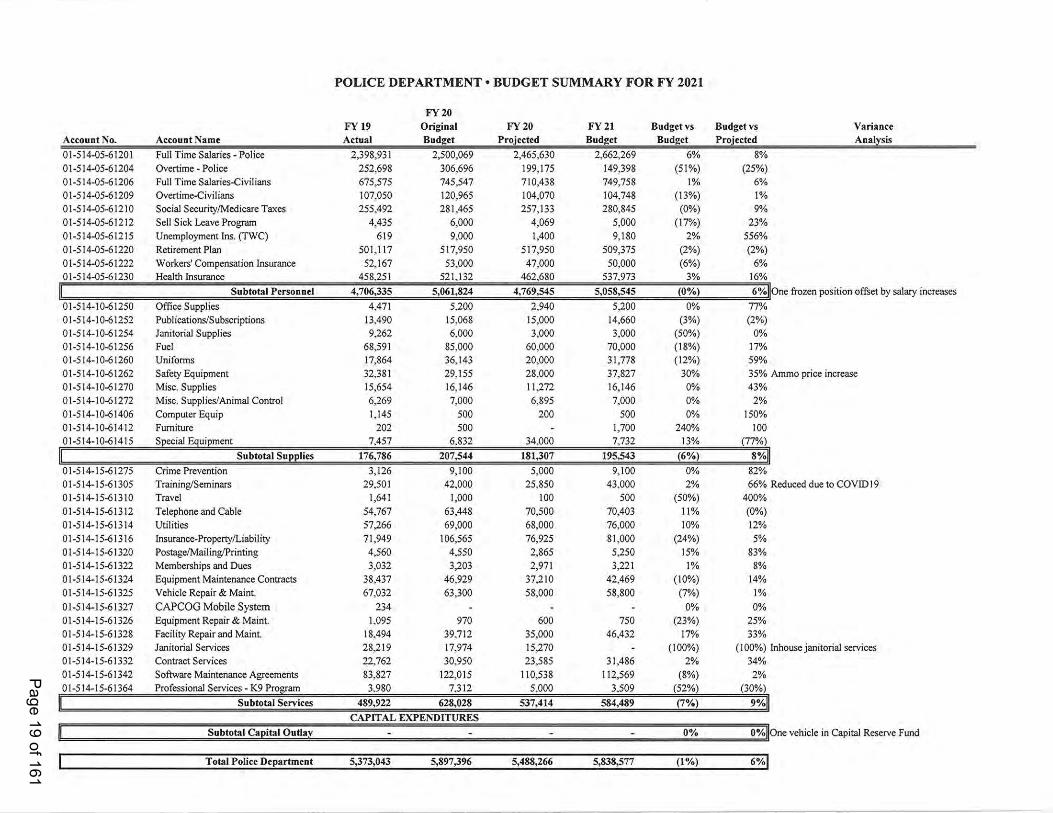

POLICE DEPARTMENT - BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 Original FY 20 FY 21 Budget vs Budget vs Variance

Account No. Account Name Actual Budget Projected Budget Budget Proiected Analysis

01-514-05-61201 Full Time Salaries - Police 2,398,931 2,500,069 2.465,63O 2,662,269 6% 8%01-514-05-61204 Overtime - Police 252,698 306,696 199,175 149,398 (51%) (25%)01-514-05-61206 Full Time Salaries-Civilians 675,575 745,547 710,438 749,758 1% 6%

01-514-05-61209 Overtime—Civilia.ns 107,050 120,965 104.070 104.748 (13%) 1%

01-514-05-61210 Social Security/MedicareTaxes 255.492 281.465 257,133 280.845 (0%) 9%01-514-05-61212 Sell Sick Leave Program 4.435 6,000 4,069 5.000 (17%) 23%01-514-05-61215 Unemployment Ins. (TWC) 619 9,000 1.400 9,180 2% 556%

01-514-05-61220 RetirementPlan 501,117 517,950 517.950 509.375 (2%) (2%)01-514-05-61222 Workers’ Compensation Insurance 52.167 53.000 47.000 50,000 (6%) 6%

01-514-05-61230 Health Insurance 458.251 521.132 462.680 537,973 3% 16%

Subtotal Personnel 4,706,335 5,061,824 4.769,545 5,058,545 (0%) 6% One frozen position offset by salary increases

01-514-10-61250 O?ice Supplies 4,471 5.200 2.940 5,200 0% 77%01-514-10-61252 Publications/Subscriptions 13,490 15.068 15,000 14,660 (3%) (2%)01-514-1061254 Janitorial Supplies 9,262 6.000 3,000 3,000 (50%) 0%

01-514-10-61256 Fuel 68,591 85.000 60,000 70,000 (18%) 17%

01-514—l0«61260 Unifomis 17,864 36.143 20,000 31,778 (12%) 59%

01-514-10-61262 Safety Equipment 32,381 29,155 28,000 37.827 30% 35% Ammo price increase01-514-10-61270 Misc.Supplies 15,654 16,146 11,272 16,146 0% 43%01-514-10-61272 Misc. Supplies/Animal Control 6,269 7,000 6,895 7.000 0% 2%01-514-10-61406 Computer Equip 1,145 500 200 500 0% 150%

01-514-10-61412 Fumiture 202 500 - 1,700 240% 10001-514-10-61415 Special Equipment 7.457 6832 34.000 7.732 13% (77%)

Subtotal Supplies 176.786 207,544 181.307 195.543 (6%) 8%

01-514-15-61275 Crime Prevention 3.126 9.100 5.000 9,100 0% 82%01-514-15-61305 Training/Seminars 29.501 42.000 25.850 43.000 2% 66% Reduced due to COVIDI901-514-15-61310 Travel 1.641 1.000 100 500 (50%) 400%01-514-15-61312 Telephone and Cable 54.767 63.448 70,500 70,403 11% (0%)01-514-15-61314 Utilities 57,266 69.000 68.000 76.000 10% 12%01-514-15-61316 Insurance-Property/Liability 71,949 106,565 76,925 81,000 (24%) 5%01-514-15-61320 Postage/Mailing/Printing 4,560 4.550 2,865 5.250 15% 83%01-514-15-61322 Memberships and Dues 3,032 3.203 2.971 3.221 1% 8%01-514-15-61324 Equipment MaintenanceContracts 38,437 46,929 37,210 42,469 (10%) 14%01-514-15-61325 VehicleRepair & Maint. 67,032 63,300 58,000 58,800 (7%) 1%01-514-15-61327 CAPCOGMobile System 234 - - - 0% 0%01-51445-61326 EquipmentRepair & Maint. 1,095 970 600 750 (23%) 25%01-514-15-61328 FacilityRepairand Maint. 18.494 39.712 35,000 46.432 17% 33%01-514-15-61329 JanitorialServices 28.219 17.974 15,270 - (100%) (100%) lnhousejanitorial services01-514-15-61332 Contract Services 22.762 30.950 23,585 31.486 2% 34%01-514-15-61342 SoftwareMaintenanceAgreements 83,827 122,015 110,538 112,569 (8%) 2%01-514-15-61364 ProfessionalServices A K9 Program 3,980 7.312 5,000 3.509 (52%) (30%)

Subtotal Services 489,922 628,028 537,414 584,489 (7%) 9%CAPITAL EXPENDITURES

Subtotal Capital Outlay - - - - 0% 0% One vehiclein Capital ReserveFund

Page 19 of 161

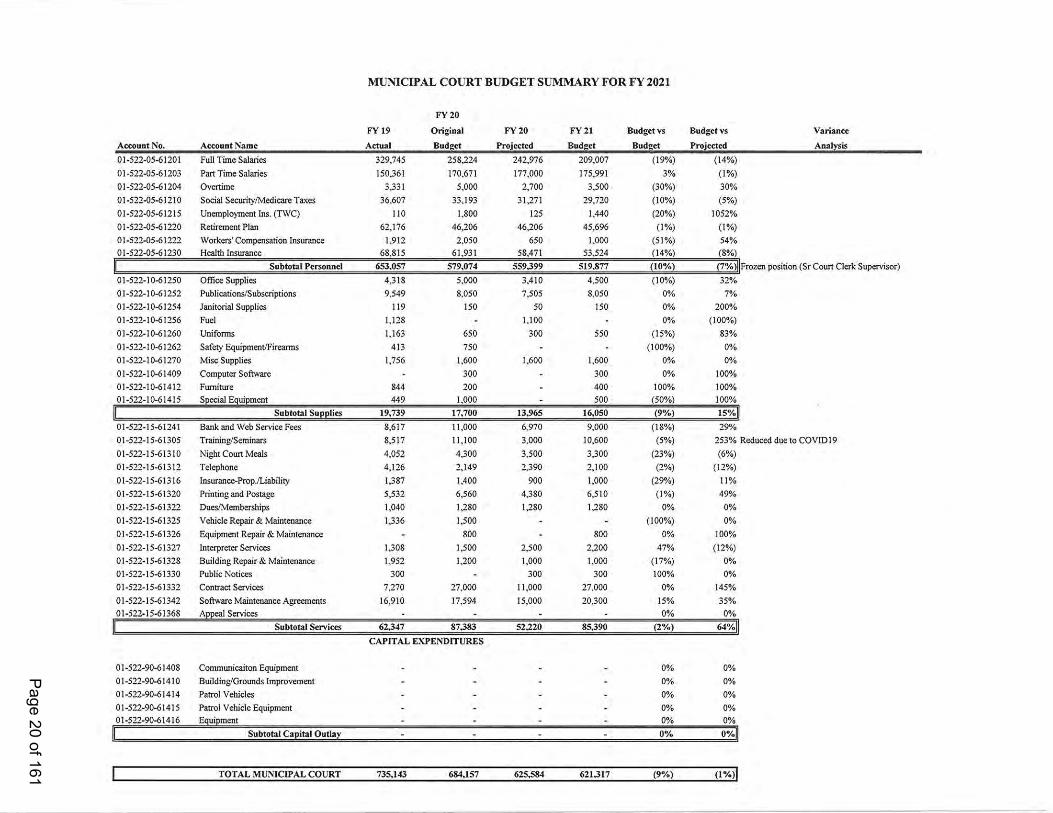

MUNICIPAL COURT BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 Original FY 20 FY 21 Budget vs Budget Vs Variance

Account No. Account Name Actual Budget Projected Budget Budoct Projected Analysis

2-05-61201 FullTime Salaries 329.745 258.224 242.976 209.007 (19%) (14%)

.. 05-61203 Part Time Salaries 150.361 170,671 177.000 175,991 3% (1%)

2-05-61204 Overtime 3.331 5.000 2.700 3.500 (30%) 30%

01-5'77-05-61210 SocialSecurity/Medicare Taxes 36,607 33.193 31,271 29,720 (10%) (5%)

05-61215 Unemployment Ins. (TWC) 110 1,800 125 1,440 (20%) 1052%

01-57" 05-61220 RetirementPlan 62.176 46.206 46.206 45.696 (1%) (1%)

05-61222 Workers‘ Compensation Insurance 1.912 2,050 650 1.000 (51%) 54%

01-522-05-61230 Health Insurance 68.815 61.931 58.471 53.524 (14%) (8%)

Subtotal Personnel 653.057 579.074 559.399 519.877 (10%) (7%) Frozen position(Sr Court Clerk Supervisor)

01-522-10-61250 Office Supplies 4.318 5.000 3.410 4.500 (10%) 32%

01-522-10-61252 Publications/Subscriptions 9.549 3.050 7.505 8.050 0% 7%

01-522-10-61254 Jmitorial Supplies 119 150 50 150 0% 200%

01-52 10-61256 Fuel 1.128 - 1.100 v 0% (100%)

01-522-10-61260 Uniforms 1.163 650 300 550 (15%) 83%

01-522-10-61262 Safety Equipment/Fireanns 413 750 - - (100%) 0%

01-522-10-61270 Misc Supplies 1.756 1,600 1.600 1.600 0% 0%

01-522-10-61409 Computer So?ware - 300 - 300 0% 100%

01-522-10-61412 Furniture 844 200 - 400 100% 100%

01 72vl0-61415 Special Equipment 449 1.000 - 500 (50%) 100%

Subtotal Supplies 19.739 17.700 13.965 16.050 (9%) 15%

0l-52 15-61241 Bank and Web Service Fees 8.617 11.000 6.970 9.000 (18%) 29%

01-52.. 15-61305 Training/Seminars 8.517 11.100 3.000 10.600 (5%) 253% Reduced due to COVIDI9

01-522-15-61310 Night Court Meals 4.052 4.300 3.500 3.300 (23%) (6%)

01-522-15-61312 Tcleplmne 4.126 2.149 2.390 2,100 (2%) (12%)

01-522-15-61316 Insurance-Prop./Liability 1.387 1.400 900 1.000 (29%) 11%

01-522-15-61320 Printing and Postage 5.532 6.560 4.380 6.510 (1%) 49%

01-522-15-61322 Dues/Memberships 1,040 1.280 1.280 1,280 0% 0%

01-522-15-61325 Vehicle Repair ELMaintenance 1.336 1,500 - - (100%) 0%

01-522-15-61326 Equipment Repair & Maintenance - 800 - 800 0% 100%

01-522-15-61327 Interpreter Services 1.308 1.500 2.500 2.200 47% (12%)

01-522-15-61328 Building Repair & Maintenance 1.952 1.200 1.000 1.000 (17%) 0%

01-522-15-61330 PublicNotices 300 - 300 300 100% 0%

01—522—15-61332 Contmct Services 7.270 27.000 11.000 27 000 0% 145%

01-522-15-61342 So?warc MaintenanceAgreements 16.910 17.594 15.000 20.300 15% 35%

01-522-15-61368 Appeal Services - — - - 0% 0%

Subtotal Services 62.347 87.383 52.220 85.390 (2%) 64%

CAPITAL EXPENDITURES

01-522-90-61408 CommunicaitonEquipment - - - - 0% 0%

01-522-90-61410 Building/Grounds Improvement - - - - 0% 0%

01-522-90-61414 Patrol Vehicles - v - - 0% 0%

01-522-90-61415 Patrol Vehicle Equiprnent - - - — 0% 0%

01-522-90-61416 Equipment — — — — 0% 0%

Subtotal Capital Outlay - - - - 0% 0%

1 TOTAL MUNICIPAL COURT 735.143 684.157 625.584 621.317 (9%) (l?

Page 20 of 161

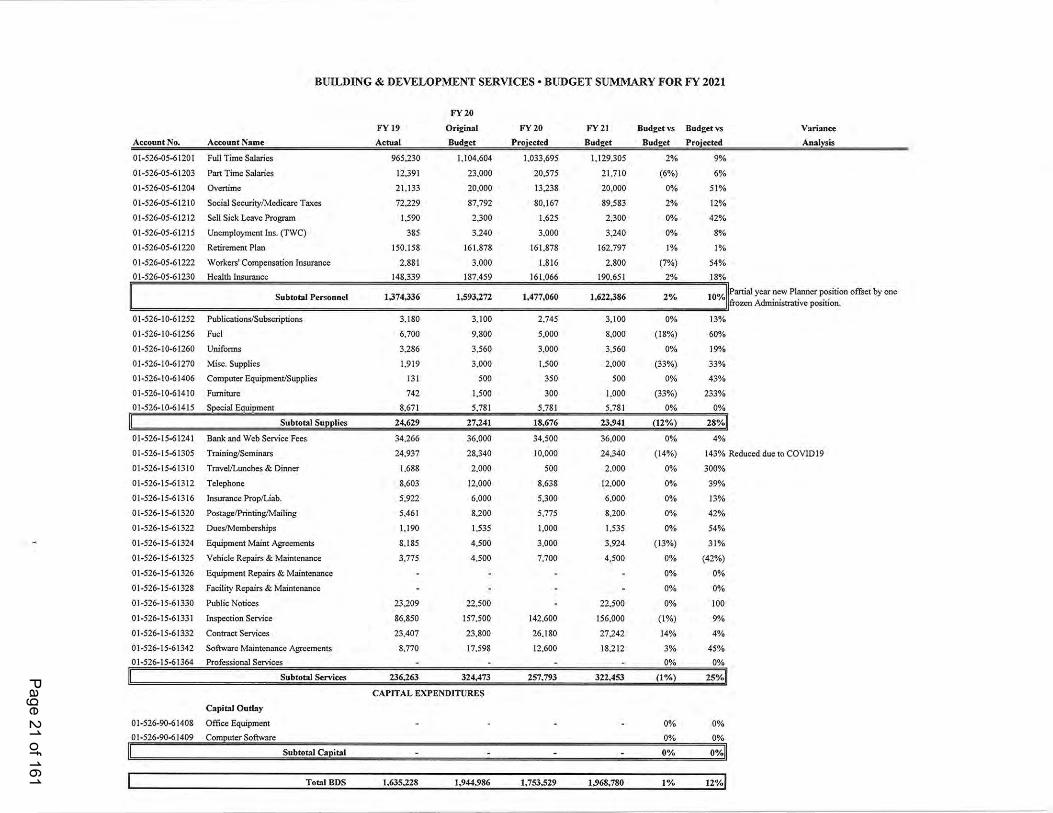

BUILDING & DEVELOPMENT SERVICES - BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 oi-iginai FY 20 FY 21 Budget vs Budget vs Variance

Account No. Account Name Aeniai Budge: Projected Budge: Budget Projected Analysis

01.526-05-61201 1=u11TimeSalaries 965.230 1.104.604 1.033.695 1.129.305 2% 9%

01-526-05-61203 Pan Timc Salaries 12.391 23.000 20.575 21.710 (6%) 6%

01-526-05-61204 ovenisne 21.133 20.000 13.238 20.000 0% 51%

01-526-05-61210 soeia1Security/McdicarcTaxcs 72.229 87.792 80.167 89.583 2% 12%

01-526-05-61212 se11Sick Leave Piogxain 1.590 2.300 1.625 2.300 0% 42%

01-526~D5-61215 Unemployment 1ns.(TWC) 385 3.240 3.000 3.240 0% 8%

01-526-05-61220 Retirement Plan 150.158 161.878 161.878 162.797 1% 1%

01-526~l)5-61222 Workers‘ Compensation Xnsurancc 2.881 3.000 1,816 2.800 (7%) 54%

01-526-05-61230 Health Xnsuranc: 148339 187.459 161.066 190.651 2% __ 18%

subzomi Personnel 1,374,336 1,593,272 1,477,060 1.622386 2% 10% 2:: H::1.“‘:‘c“;:".‘t’:::I‘_""°?‘°' by °"°

01-526-10-61252 Publications/Subscriplions 3.180 3.100 2.745 3.100 0% 13%

01-526-10-61256 Fuel 6.700 9.800 5.000 8.000 (18%) 60%

01-526-10-61260 unifei-ins 3.286 3.560 3.000 3.560 0% 19%

O1-526-10-61270 Mise. suppiies 1.919 3.000 1.500 2.000 (33%) 33%

O1-526-10-61406 Computer Equipment/Supplies 131 500 350 500 0% 43%

0l~526-10-61410 1-‘ui-nizure 742 1.500 300 1.000 (33%) 233%

01-526-10-61415 special Equipment 8.671 5.781 5.781 5.781 0% 0%

Subtotal Supplies 24,629 27241 18,676 23.941 (12%) 28%

01-526-15-61241 Bank and Web Service Fees 34.266 36.000 34.500 36.000 0% 4%

01—526—15-61305 Tnining/Seminars 24.937 28.340 10.000 24.340 (14%) 143% Reduced due to cov1D19

OI-516-15-61310 Travel/Lunches52Dinner 1638 2.000 500 2.000 0% 300%

01-526-15-61312 Tclcphonc 8.603 12.000 8.638 12.000 0% 39%

01-526-15-61316 Insumncc Prop/Liab. 5.922 6.000 5.300 6.000 0% 13%

O1-526-15-61320 Postage/Printing/Mailing 5.461 8.200 5.775 8.200 0% 42%

01-526-15-61322 Dues/Memberships 1.190 1.535 1.000 1.535 0% 54%

01-526-15-61324 Equipinem Maint Agreemems 8.185 4.500 3.000 3.924 (13%) 31%

01-526-15-61325 Vehicle Rcpairs & Maintenanoe 3.775 4.500 7.700 4.500 0% (42%)

01-52645-61326 Equipment Repairs & Maintenance - - - - 0% 0%

01-526-15-61328 FacilityRepairs & Maintenance - - —. 0% 0%

01-526-15-61330 PublicNotices 23209 22.500 - 22.500 0% 100

01-526-15-6133] 1nspeeu'nnService 86850 157.500 142.600 156.000 (1%) 9%

01-526-15-61332 Contract seiviees 23.407 23.800 26.180 27.242 14% 4%

0 1-526-1 5—6134Z So?warc Maintenance Agccmcnts 8.770 17.598 12.600 18.212 3% 45%

01-526-15.61364 Professional serviees - — — — 0% 0%

S Services 236.263 324.473 257.793 322.453 (1%) 25%

CAPITAL EXPENDITURES

Capital Outlay

01-526-90-61408 o?iee Equipmcnl - - - - 0% 0%

01-526-90-61409 Compulcr So?ware 0% 0%

- - - — 0% 0%Subtotal Capiul

Page 21 of 161

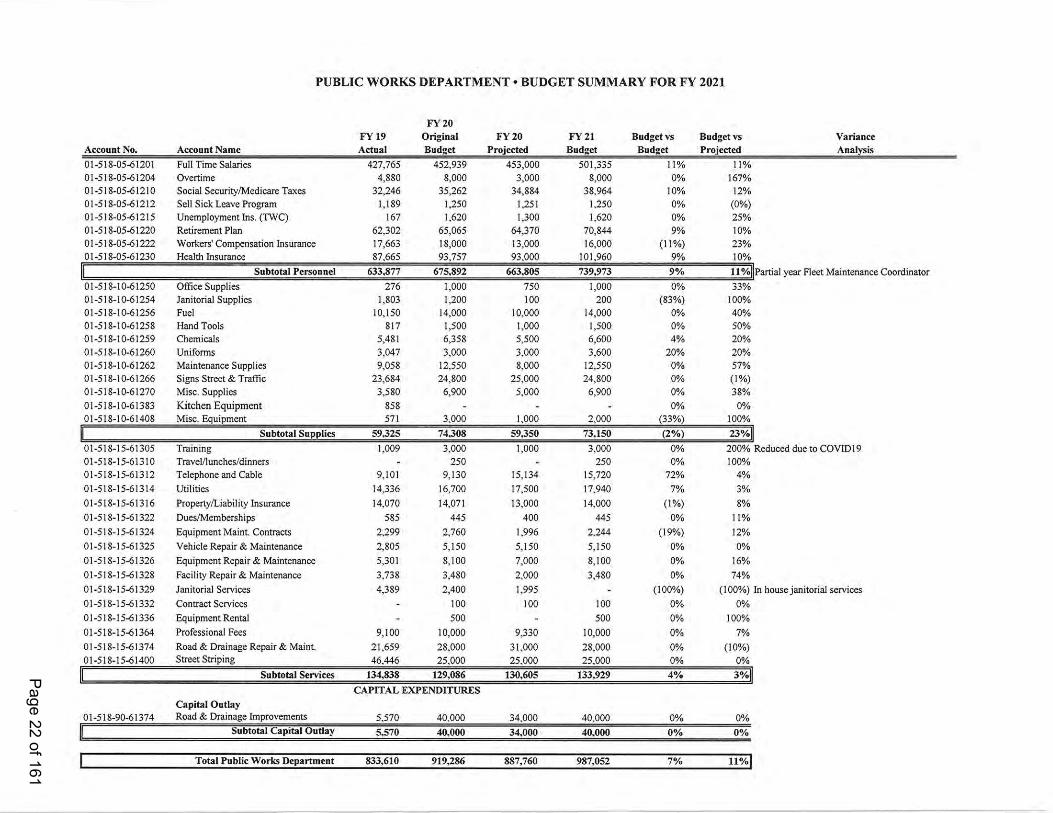

PUBLIC WORKS DEPARTMENT - BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 Original FY 20 FY 21 Budget vs Budget vs VarianceAccount No. Account Name Actual Budget Projected Budget Budget Projected Analysis

01-518-05-61201 Full Time Salaries 427.765 452.939 453,000 501.335 11% 11%

01-518-05-61204 Overtime 4,880 8.000 3.000 8.000 0% 167%

01-518-05-61210 Social Security/Medicare Taxes 32,246 35.262 34,884 38.964 10% 12%

01-518-05-61212 Sell Sick Leave Program 1.189 1.250 1.251 1.250 0% (0%)01-518-05-61215 Unemployment Ins. (TWC) 167 1,620 1,300 1.620 0% 25%

01-518-05-61220 RetirementPlan 62.302 65,065 64,370 70,844 9% 10%01-518-05-61222 Workers‘ Compensation Insurance 17.663 18.000 13,000 16.000 (11%) 23%01-518-05-61230 Health Insurance 87,665 93,757 93,000 101,960 9% 10%

Subtotal Personnel 633.877 675.892 663.805 739.973 9% 11% Partial year Fleet Maintenance Coordinator01-518-10-61250 Office Supplies 276 1,000 750 1,000 0% 33%

01-518-10-61254 Janitorial Supplies 1.803 1.200 100 200 (83%) 100%

01-518-10-61256 Fuel 10.150 14.000 10.000 14.000 0% 40%

01-518-10-61258 HandTools 817 1.500 1.000 1,500 0% 50%

01-518-10-61259 Chemicals 5.481 6.358 5,500 6.600 4% 20%

01-518-10-61260 Uniforms 3.047 3.000 3,000 3.600 20% 20%

01-518-10-61262 MaintenanceSupplies 9.058 12.550 8.000 12.550 0% 57%

01-518-10-61266 Signs Street & Traffic 23.684 24,800 25,000 24,800 0% (1%)

01-518-10-61270 Misc. Supplies 3.580 6.900 5.000 6.900 0% 38%

01-518-10-61383 Kitchen Equipment 858 - - - 0% 0%

01-518-10-61408 Misc. Equipment 571 3,000 1.000 2,000 (33%) 100%

Subtotal Supplies 59.325 74.308 59.350 73.150 (2%) 23%

01-518-15-61305 Training 1,009 3.000 1.000 3.000 0% 200% Reduced due to COVIDI901-518-15-61310 Travel/lunches/dinners - 250 - 250 0% 100%01-518-15-61312 Telephone and Cable 9,101 9.130 15.134 15.720 72% 4%

01-518-15-61314 Utilities 14.336 16.700 17.500 17.940 7% 3%01-518-15-61316 Property/Liability Insurance 14.070 14.071 13.000 14.000 (1%) 8%01-518-15-61322 Dues/Memberships 585 445 400 445 0% 11%01-518-15-61324 EquipmentMaint. Contracts 2.299 2.760 1.996 2.244 (19%) 12%01-518-15-61325 Vehicle Repair & Maintenance 2,805 5.150 5.150 5.150 0% 0%

01-518-15-61326 Equipment Repair & Maintenance 5,301 8.100 7,000 8.100 0% 16%01-518-15-61328 Facility Repair & Maintenance 3.738 3.480 2,000 3,480 0% 74%O1-518-15-61329 JanitorialServices 4,389 2,400 1.995 - (100%) (100%) In housejanitorial services01-518-15-61332 Contract Services - 100 100 100 0% 0%

01-518-15-61336 Equipment Rental - 500 - 500 0% 100%

01-518-15-61364 Professional Fees 9.100 10.000 9.330 10.000 0% 7%01-518-15-61374 Road& Drainage Repair & Maint. 21.659 28.000 31.000 28.000 0% (10%)01-518-15-61400 Street Striping 46.446 25.000 25.000 25,000 0% 0%

Subtotal Services 134,838 129.086 130.605 133.929 4% 3%

CAPITAL EXPENDITURES

Capital Outlay

01-518-90-61374 Road & Drainage Improvements 5,570 40.000 34.000 40.000 0% 0%51151091 Ciliiml011319)’ 5.570 40.000 34.000 40.000 0% 0%

Page 22 of 161

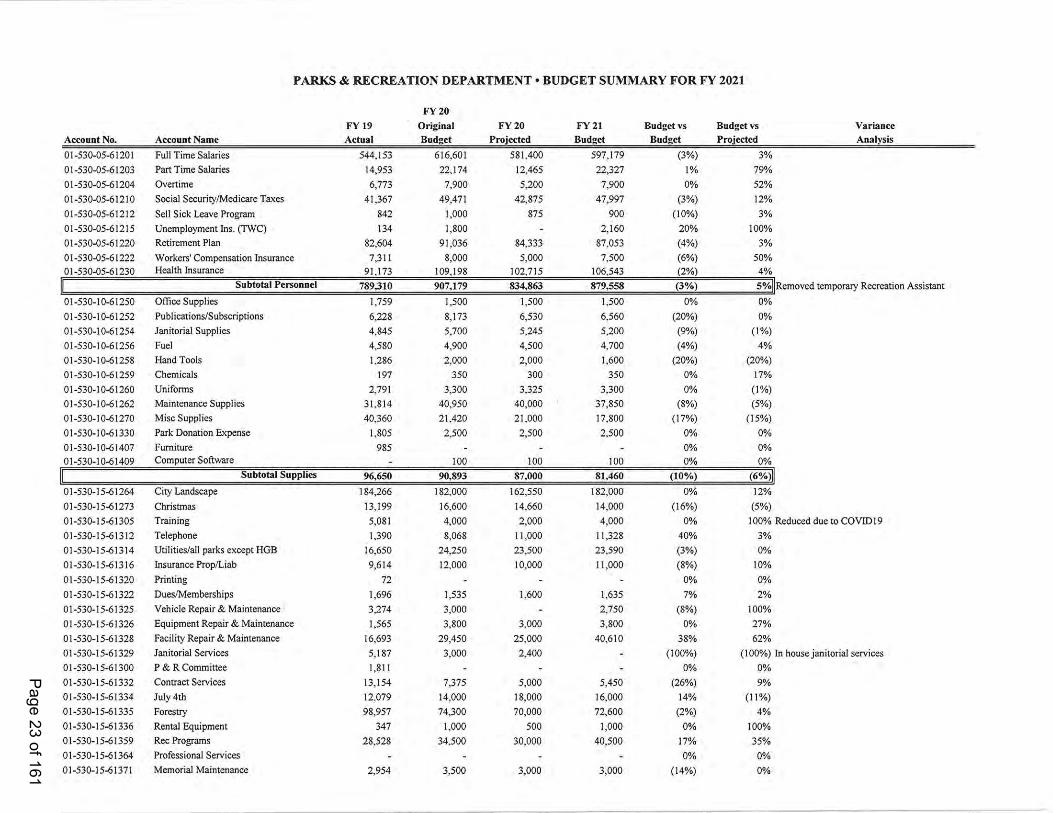

PARKS & RECREATION DEPARTMENT ° BUDGET SUMMARY FOR FY 2021

FY 20

FY 19'

Original FY 20 FY 21 Budget vs Budget vs Variance

Account No. Account Name Actual Budget Projected Budget Budget Projected Analysis

01-530-05-61201 Full Time Salaries 544.153 616,601 581.400 597,179 (3%) 3%

01-530—05—61203 Part Time Salaries 14,953 22,174 12.465 22,327 1% 79%

01-530-05-61204 Overtime 6,773 7,900 5,200 7.900 0% 52%

01-530-05-61210 Social Security/Medicare Taxes 41.367 49,471 42.875 47,997 (3%) 12%

01-530-05-61212 Sell Sick Leave Program 842 1,000 875 900 (10%) 3%

01-530-05-61215 Unemployment lns. (TWC) 134 1.800 - 2,160 20% 100%

01-530-05-61220 RetirementPlan 82604 91 ,036 84.333 87,053 (4%) 3%

01-530-05-61222 Workers‘ Compensation Insurance 7,31 1 8.000 5.000 7.500 (6%) 50%01-530-05-61230 Health Insurance 91.173 109.198 102.715 106.543 (2%) 4%

Sllb?ll?l P9'S0'|||el 789.310 907.179 834.863 879.558 (3%) 5% Removedtemporary RecreationAssistant

01-530-10-61250 Office Supplies 1.759 1.500 1,500 1.500 0% 0%

01-530-10-61252 Publications/Subscriptions 6.228 8.173 6,530 6.560 (20%) 0%

01-530-10-61254 Janitorial Supplies 4.845 5.700 5.245 5.200 (9%) (1%)

01-530-10-61256 Fuel 4.580 4.900 4,500 4.700 (4%) 4%

01-530-10-61258 Hand Tools [.286 2.000 2.000 1.600 (20%) (20%)

01-530-10-61259 Chemicals 197 350 300 350 0% 17%

01-530-10-61260 Uniforms 2.791 3.300 3.325 3.300 0% (1%)

01-530-10-61262 Maintenance Supplies 31.814 40,950 40.000 37,850 (8%) (5%)

01-530-10-61270 MiscSupplies 40,360 21,420 21.000 17,800 (17%) (15%)

01-530-10-61330 Park DonationExpense 1805 2.500 2.500 2.500 0% 0%

01-530-1 0-61407 Furniture 985 - - - 0% 0%

01-530-1 0-61409 COMPUWYS0?7W3Y9 - 100 100 100 0% 0%Subtotal Supplies 96.650 90.393 87.000 81.460 (10%) (6%)

01-530-15-61264 City Landscape 184.266 182.000 162.550 182.000 0% 12%

01-530-15-61273 Christmas 13.199 16.600 14,660 14.000 (16%) (5%)

01-530-15-61305 Training 5.081 4.000 2.000 4.000 0% 100% Reduced due to COVIDI901-S30-15-61312 Telephone 1.390 8.068 11,000 11,328 40% 3%

O1-530-15-61314 Utilities/all parks except HGB 16.650 24.250 23.500 23.590 (3%) 0%

01-530-15-61316 InsuranceProp/Liab 9.614 12,000 10,000 I 1,000 (8%) 10%

01-530-15-61320 Printing 72 — - - 0% 0%

01-530-15-61322 Dues/Memberships 1.696 1,535 1.600 1,635 7% 2%

01-S30-15-61325 Vehicle Repair & Maintenance 3,274 3,000 - 2.750 (8%) 100%

01-530-15-61326 Equipment Repair & Maintenance 1.565 3.800 3.000 3.800 0% 27%01-530-15-61328 Facility Repair & Maintenance 16,693 29.450 25.000 40.610 38% 62%

01-530-15-61329 Janitorial Services 5,187 3.000 2.400 - (100%) (100%) In housejanitorial services01-530-15-61300 P & R Committee 1,811 - - - 0% 0%

01-530-15-61332 Contract Services 13.154 7.375 5.000 5.450 (26%) 9%

01-530-15-61334 July 4t.h 12.079 14.000 18.000 16,000 14% (11%)

01-530-15-61335 Forestry 98.957 74,300 70.000 72,600 (2%) 4%

01-530-[5-61336 Rental Equipment 347 1,000 500 1,000 0% 100%

01-530-15-61359 Rec Programs 28,528 34,500 30.000 40.500 17% 35%

01-530-15-61364 Professional Services - - - - 0% 0%

01-530-15-61371 MemorialMaintenance 2.954 3.500 3,000 3.000 (14%) 0%

Page 23 of 161

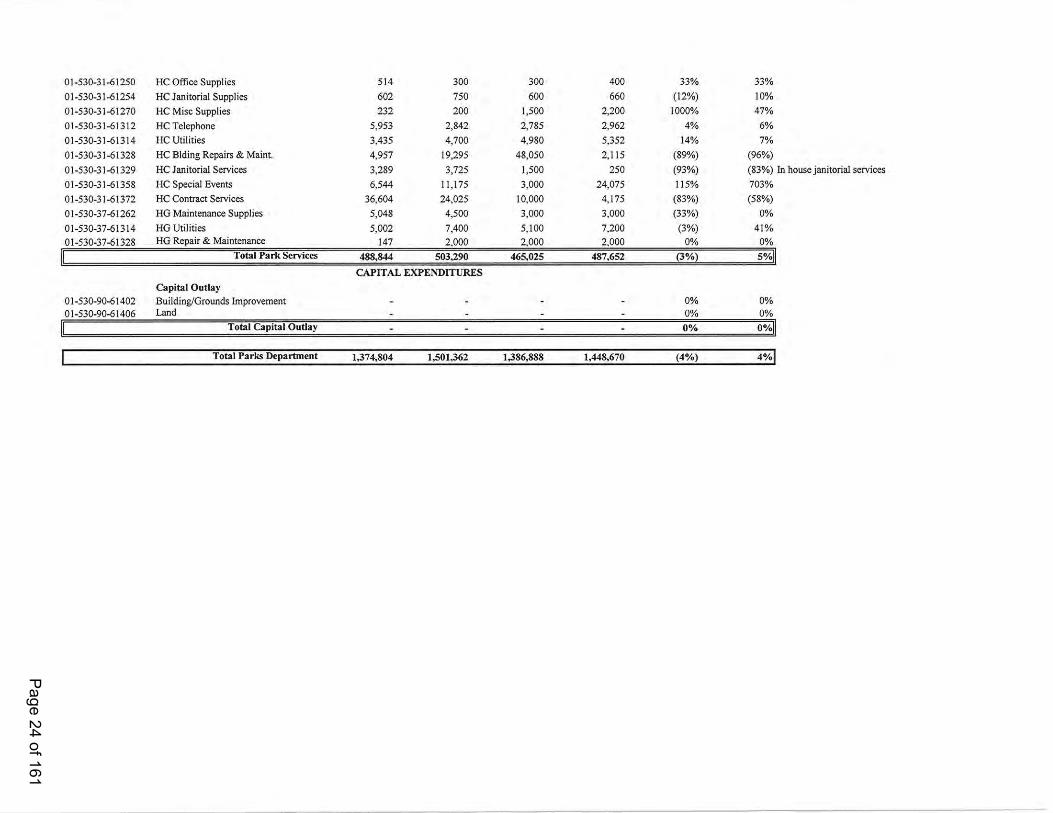

01-530-31-61250 HC Office Supplies 514 300 300 400 33% 33%

01-530-31-61254 HC JanitorialSupplies 602 750 600 660 (12%) 10%

0l—530»31—6l270 I-{C Misc Supplies 232 200 1,500 2.200 l000% 47%

01-530-31-61312 HC Telephone 5,953 2,842 2.785 2.962 4% 6%

01-530-31-61314 I-{C Utilities 3,435 4.700 4,980 5.352 14% 7%

01-530-31-61328 I-ICBlding Repairs & Maint. 4.957 19,295 48.050 2.115 (89%) (96%)

01v530-31-61329 I-ICJanitorial Services 3.289 3,725 1.500 250 (93%) (83%) In housejanitorial services01-530-31-61358 I-1CSpecial Events 6.544 11,175 3.000 24.075 115% 703%

01-530-31-61372 I-ICContract Services 36,604 24,025 10,000 4.175 (83%) (58%)

01-530-37-61262 HG MaintenanceSupplies 5,048 4,500 3,000 3,000 (33%) 0%

01-530-37-61314 HG Utilities 5002 7.400 5,100 7.200 (3%) 41%01-530-37-61328 HG Repair & Maintenan?e 147 2.000 2.000 2.000 0% 0%

Total Park Services 488,844 503,290 465.025 487.652 (3%) 5%

CAPITAL EXPENDITURES

Capital OutlayD1-530-90-61402 Building/Grounds Improvement - v - — 0% 0%

01-530-90-61406 Land .— - - 0% 0%

Total Capital Outlay . . . . 00/. 0%

Page 24 of 161

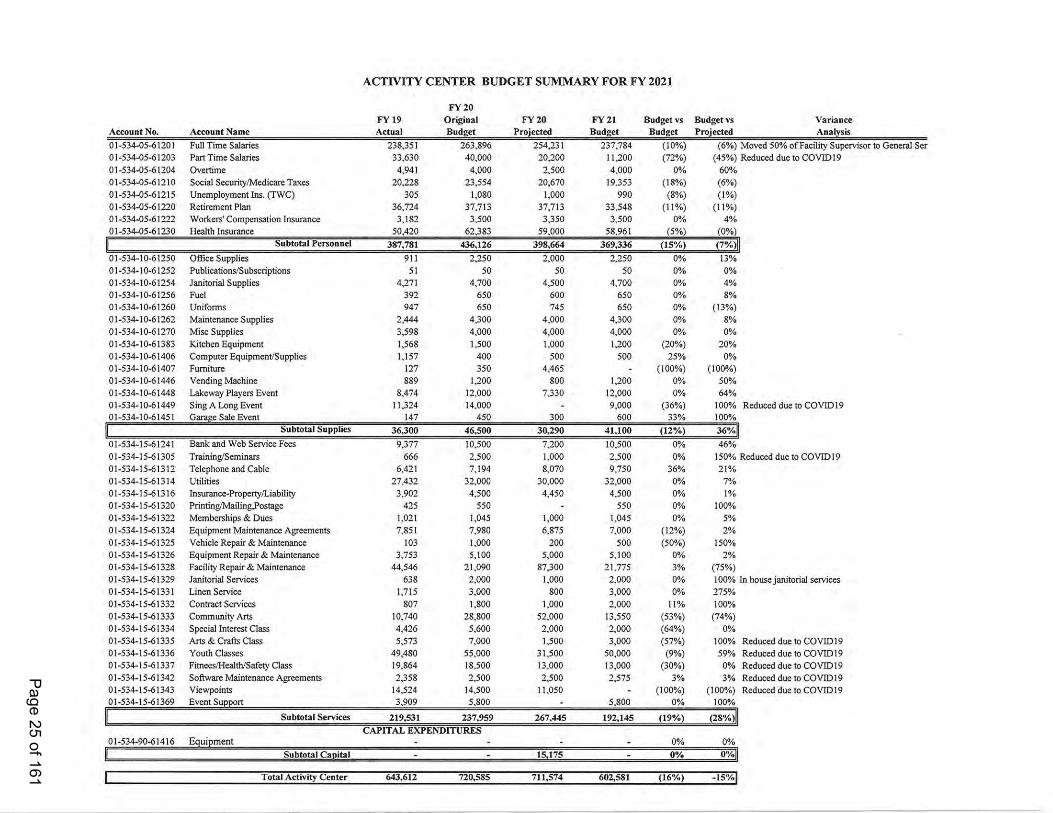

ACTIVITY CENTER BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 Original FY 20 FY 21 Budget vs Budget vs VarianceAccount N0. Account Name Actual Budget Proicctcd Budget Budget Projected Analysis

01-S34-05-61201 Full Time Salaries 238.351 263.896 254.231 237,784 (10%) (6%) Moved 50% of Facility Supervisor to General Scr01-534-05-61203 Part Time Salaries 33,630 40.000 20,200 11,200 (72%) (45%) Reduced due to COV1D19

01—534—05—61204Overtime 4.941 4.000 2,500 4.000 0% 60%01-534-05-61210 Social Security/Medicare Tavcs 23.554 20.670 19.353 (18%) (6%)01-534-05-61215 Unemployment lns. (TWC) 305 1.080 1,000 990 (8%) (1%)01—534—05-61220 Retirement Plan 36,724 37,713 37,713 33.548 (11%) (11%)01-S34-05-612-2 Workers‘Compensation Insurance 3.182 3.500 3,350 3.500 0% 4%01—534—05-61230Health lnsurance 50,420 62.383 59.000 58.961 (;V3) (0%)

S||bWW1P4~'|'S0nn¢l 387.781 436.126 398.664 369.336 (15%) (7%)

01—534—10-61250 Office Supplies 911 2,250 2.000 2.250 0% 13%01-534-I 0~61252 Publications/Subscriptions 51 50 S0 50 0% 0%01-534-10-61254 Janitorial Supplies 4.271 4.700 4.500 4.700 0% 4%01-534-10-61256 Fuel 392 650 600 650 0% 8%01-534-10-61260 Uniforms 947 650 745 650 0% (13%)01-534—10~61262 Maintenance Supplies 2.444 4,300 4.000 4,300 0% 8%

01-534-10«61Z70 Misc Supplies 3.598 4,000 4,000 4.000 0% 0%01-534-10-61383 Kitchen Equipment 1.568 1.500 1.000 1.200 (20%) 20%01»534-10-61406 Computer Equipment/Supplies 1.157 400 500 500 25% 0%

01-534-10-61407 Furniture 127 350 4.465 — (100%) (100%)01-534-10-61446 Vending Machine 889 1.200 800 1.200 0% 50%01-534-10-61448 Lakcway Players Event 8.474 12.000 7,330 12.000 0% 64%01-534-10-61449 Sing A Long Event 11,324 14.000 — 9.000 (36%) 100% Reduced due to COV1Dl901-534-10—61451 Gge &_:LeEvent

‘. 147 450 300 600 33% 100%

5“ b‘‘~°'3l 5“PPl"55 36.300 46.500 30.290 41.100 (12%) 36%

01~534-15»61241 Bank and Web Service Fees 9,377 10,500 7.200 10,500 0% 46%

01-534-15-61305 Training/Seminars 666 2.500 1.000 2.500 0% 150% Reduced due to COVTDI901-534-15-61312 Telephone and Cable 6,421 7.194 8,070 9.750 36% 21%01-534-15-61314 Utilities 27,432 32.000 30.000 32,000 0% 7%01-534-15-61316 1nsurance»Froperty/Liability 3.902 4,500 4.450 4,500 0% 1%01-534-15-61320 Printing/Mailing.1’ostage 425 550 — 550 0% 100%

01-534-15-61322 Memberships & Dues 1.021 1.045 1.000 1.045 0% 5%01-534-15-61324 Equipment Maintenance Agreements 7.851 7.980 6,875 7.000 (12%) 2%01-534-15-61325 Vehicle Repair & Maintenance 103 1.000 200 500 (50%) 150%01A534-15-61326 Equipment Repair & Maintenance 3.753 5.100 5.000 5.100 0% 2%01-534-15-61328 FacilityRepair & Maintenance 44.546 21.090 87.300 21.775 3% (75%)01-534-1 5—61329 Janitorial Sendces 638 2,000 1.000 2.000 0% 100% In house janitorial services01-534-15-61331 Linen Service 1,715 3,000 800 3,000 0% 275%

01»534-15-61332 Contract Services 807 1.800 1.000 2.000 11% 100%01-534-15-61333 CommunityArts 10.740 28.300 52.000 13.550 (53%) (74%)01-534-15-61334 Special Interest Class 4,426 5,600 2,000 2,000 (64%) 0%01~534~15—61335 Arts & Crak Class 5.573 7.000 1.500 3.000 (57%) 100% Reduced due to COVID1901-534-15—61336 Youth Classes 49.480 55,000 31.500 50.000 (9%) 59% Reduced due to COVID1901-534-15-61337 Fitnees/Health/SafetyClass 19.864 18.500 13.000 13.000 (30%) 0% Reduced due to COVID1901-534-15—61342 So?ware Maintenance Agreements 2.358 2.500 2,500 2.575 3% 3% Reduced due to COVIDI901-534-15-61343 Viewpoints 14.524 14.500 11.050 — (100%) (100%) Reduced clue to COWD1901-534-15-61369 Event Support 3.909 5.800 - 5.800 0% 100%

Subtotal Services 219,531 237,959 267.445 192,145 (19%) (28%)

CAPITAL EXPENDITURES01-534-90-61416 Equipment ~ - - - 0% 0%

1 Subtotal Capital — — 15 175 — 0% 0%

Total Activity Center 643.612 720,585 711,574 602.581 (16%)

Page 25 of 161

SWIM CENTER - BUDGET SUMMARY FOR FY 2021

FY 20

FY 19 Original FY 20 FY 21 Budget vs Budget vs Variance

Account No. Account Name Actual Budget Projected Budget Budget Projected Analysis

01-538-05-61201 Full Time Salaries 101,904 117.281 117.000 117.227 (0%) 0%

01-538-05-6 1203 Part Time Salaries 151.057 176.968 145.600 176.968 0% 22%

01-538-05-61204 Overtime 2,424 1,000 500 1.000 0% 100%01-538-05-61210 Social Security/Medicare Taxes 19.527 22.587 20,127 22.582 (0%) 12%

01-538-05-61215 Unemployment Ins. (TWC) 360 3.960 3,500 3.960 0% 13%

01-538-05-61220 Retirement Plan 16,617 19,321 19,321 19,036 (1%) (1%)

01-53 8-05-61222 Workers‘ Compensation Insurance 5.323 5.500 5,360 5.500 0% 3%01-538-05-61230 Health Insurance 17.515 20.828 20,800 21.477 3% 3%

SubtotalPersonnel 314,727 367,445 332,208 367.750 0% 11%

01-53 8-10-61250 O?ice Supplies 1.552 1,500 1.600 1,600 7% 0%

01-538-10-61254 JanitorialSupplies 1.382 2,000 1,800 1,850 (8%) 3%

01-538-10-61256 Fuel 44 200 50 150 (25%) 200%

01-538-10-61259 Chemicals 14.844 15,500 16.000 16,000 3% 0%

01-538-10-61260 Unifonns 3.585 4.325 2,876 4,325 0% 50%

01-538-10-61270 Miscellaneous Supplies 14.886 10,525 8.000 8,225 (22%) 3%

01-538-10-61271 Pool/Building Maint. Supplies 842 3.500 2,500 2,700 (23%) 8%

01-538-10-61272 Concession Supplies 13.924 17.500 16.000 16.000 (9%) 0%

01-538-10-61273 Party Supplies 39 - - - 0% 0%

01-538-10-61406 Computer Equipment/Supplies 1.345 1.000 1.500 1.000 0% (33%)

01-538-10-61407 Furniture 5.081 4,725 1,500 1.550 (67%) 3%01-538-10-61408 Misc. Equipment 16.071 1.500 1.500 1.500 0% 0%

5" biota! supplies 73,595 62.275 53.326 54.900 (12%) 3%

01-538-15-61241 Bank and Web Service Fees 5.576 5.600 4,000 5.600 0% 40%

01-538-15-61305 Training/Seminars 1.860 3.350 1,000 3.700 10% 270% Reduced due to COV1D1901-538-15-61306 Drug Testing 1.470 2.700 2.700 2.700 0% 0%

01-538-15-61312 Telephone and Cable 7,857 6.370 7.774 10.052 58% 29%

01-538-15-61314 Utilities 52.030 52.300 43.729 52.300 0% 20%01-538-15-61316 insurance-Property/Liability 2,867 2.868 1,500 3.000 5% 100%

01-538-15-61320 Printing and Marketing 854 500 500 1.000 100% 100%

01-538-15-61322 Dues & Memberships - 45 50 995 2111% 1890%

01-538-15-61325 Vehicle Repair & Maintenance 37 250 250 5,700 2180% 2180% Refurbishing recycled police vehicle

01-53 8-15-61326 Equipment Repair & Maintenance 21_.142 8,000 8,000 9.500 19% 19%

01-538-15-61328 Facility Repair & Maintenance 47,475 37,820 22,710 28,425 (25%) 25%

01-53 8-15-61329 Janitorial Services 6,618 2,790 2.000 - (100%) (100%) In housejanitorial services01-538-15-61332 Contract Services 844 1,450 1.450 2.050 41% 41%

01-538-15-61359 Pool Programs 2,393 3,500 2.000 4.600 31% 130%01-538-15-61374 Instructors 20,722 32.500 18.677 32.500 0% 74%

5" M0331 3¢|'V|N-‘S 171.745 160,043 116,340 162.122 1% 39%

CAPITAL EXPENDITURES01-538-90-61402 Building & grounds improvement - — - 33,515 100% 100%

T051 UIPIW — - - 33,515 100% 100%

Total S 589,763 501,874 5% 23%

Page 26 of 161

o__m.moocm

?m2...;

moz<

a<m

nzamU

ZZ

HZ

H

ouzsmm U

:_._n—E99.20

nvnm

._£m__F.,H

£m.:~.~

$§m_.~

m.:.:s.~

mm

mabazm

axmA

<,H

O.—

.

8282

SSE

a..:om

< _mom

E

$2.::33

3??325

55

833..8o.8~._

o8.o8.__m

&o_E

n_5oQ

mm

mptnzam

xa

.Rw

.E~.~

.§.§_.~m

5zm>

mm

1—<

._.O,~.

2:m

an...oE

8£.m

o.§.:_

S3 _~.~o8.:s.~

moxah

EP_£a>

c<

m5zm

>m

m

muz<

q<m

975%oz_zzG

mm

am.:£U

3>

r._2

>r._

2>

7.-

«:au.Sm.om

_:_m_..2uu.?..m

_.=:u<

:323>

_.§E

SusanU

??rmoo_>

..omE

on

»a>»$_su—

mo56

Page 27 of 161

no?mm

ow~.m

m3a.:

mm

u.:_.=.:2_xuo.£.:=

V\..o>

em

o==

o>3—

..

mam

m._&

m:s.£._

£m.__~.~

m:s.?_.$

32.33m

8282

SSsum

v__am§s.§.S

W2

33$5.5

?aaam

a?a.

522:.£m

$.§.o_W

2:2

:_.sm@

363.m

an$.25

Soda.

2332%

33%.

233_.am

8o.8~._o8,8S

o8.o8._oo?i

.:3

o_&u:_._._

m;G

.§.o_W

2scam

25.8;.

23E

5Sega

.23

3am898%

.«E

ua_._...m

m?_=

.=:.2_xm

§.£~.~m

$a.B_.~

m§.ao.~

m

2:3.

£3oE

ou:_aw

ake..83.:

$Ss~.~$~.cm

_.~§,w

S.~vars E

o._o_w>

3253.2

835

«SKm

2.3m

_aA

.E

o._o_m>

u<N

821:

ma=

:o>uM

_u>

.._on

>.._

E>

..—=

£:__..umoQ

25.2.=

=3...<

.ez...=

=3u<

euueamu2ae_.o..m

_..::o<

:3>

hM

OH

1=<

,HH

GH

HU

QD

Q.

ezE>

Fm<

.:EH

DZ

Z;

mo_>

E_m

Sam3

975%

Page 28 of 161

32%..

EE

Kuoca?m

2...”.

Azo_.:m

o._

FHZ

G...=

.U_~—

.—.w

My_Z

Dw

~?DZ

<cmJ.

w..~.a$._

m$.:a._

23.3..

8” _w _was

.§._:e._

uM..=

2_U

.=8._e.~

cmcan:2.3

33%..

5?_

.uu_:_n_ w

366

8838283:3

w

2in

3.3_.o..m

Swd

E3...:

93~S.8m._

:.-s..._~

RQ

SNPH

Znm

.5E.~m

m=

z:

a.>

,..~

_.::o<

_~cN.E

u>.55

.,..m_.=

m_:._i323

_.__..m

zs>o3_nA

.3»:O

8=s_um

_c:=

m=

_»m

=m

__U

mB

_:::zm._v.u

A4...—

.O.H

_s_%o

mm

m:bnzm

._v.m

mazm

rémA

<._.O

._.

oEoo:_

.m..:o:__

280m

m3o<

Eco

moon.

2.3

mean.

m:_m

m3oi

Em

u5.20

u:=o>

3_833

E_am

m:zu>

5_

5:05.3

.2:2m:o

anB

um

Page 29 of 161

$53..3,... .3..

.:.~.E.5

Suns:E

ms:

Q....O

mA

<,..O

...

$n.se....am

.~G..

2a.:m..

§_>.am

.EP..

weed.

vmm

d.m

mono.

m=

_=£

2___:oE

a8.55.55:

_.=:_=

<3.8:.

m_=

2=8.u<

8E=

_2:_£>.

Bsscom

~..mE

.m..~.

W8

ooodvooo.o..

mm

wdm

m=

_mm

8o:_Ea=

a_.8__80.92.

m_.o..:aN

E.

.._o__8=o...

b.2».

23>»

Nu...E

.=.uw

=o...

.em.w

.m..~.m

.~o

..

._2E

oE2.

.QE

o9:u...m

8..:um.u_:E

oU~m

m.o.m

..~.m.~o

coedm

monm

ma?a

$8..3.3.

bst?...E

a8:a:o=

_.m=

__S=

=_£

.55..22:

amazon.

m:_o_:o2w

<..=

_a.>. .:uE

...__.%n...~m

.c.m..~.m.~o

eaSm

..9392

3.59% m

.._..m_2.E

oS.-2o.2.~_m

.~c

25.225.:

5.:m

.__=3a_§_..__

.8u.__.___:_

E;

oms§_

m______w

2\m=

__=_..Sw

s8._o~m$.2.~:.S

Sm.

w?

mum

comzm

.amu..w. m

s.m_.~_m

.~o

o2om

.co.

mean 22.5

mzsm

:.q.s.2.~_m

.~o

SN8.

:::o§._a

u=o_.n.

2.21.9.9...~:G

.m_.~_

m.~o

SNcm

3m

=___.E

.:5:._o...o.o>

E...

3:25.95....

2m

s.2.~:.8

83com

.m

._2_e__o3\E____5m

_2§tE=

_..amn=

____sF8m

s.2.~:,8

$5:?ag

83.”3».

£3.35

_:aU....u._O

moon.

8.2%$3

a.ism..&

....m..N

.m

.~o

33325.123

30.3....325m

38:50._88..oU

23>»

2.8o .O

8...“ ..~. vs...w

.u.=:m

m.

2:4:5

8m;

3=._._._m

.599

comm

am.

.5..:o:..._2_=

.Eoo

muzzm

om.eo_.5._2_=

_Sm€25

EoE

.._=..m

.55:50oo3o.o..~.

m.~o

8m8.

won

.2u...E

.o.o:...o§=

yen..=

2_a_=_.m

<2____._=

:350§.5.o_.~_

m.~o

..

...o=

ow=

_Eo0

=_:o8<

8:2.K

u.o.o..~.m

.~o

SN.

.m

:Em

29.m

::o...=... 8~s.2.~:,S

O8

2:33

.m.E

.:_u.aUdeem..5:o...

$=.a_.m

350%

~s.o_.~:.S

§.i~.~=.m

.

:3:?m

?.w

s?..a=

_5m._u.—

.593

.m=

==

.§wk

.~?.

an3.

m..5.

.:._.d_:mX

.2:5/.

:_=Su<

dz.:_:.......<

.uw.:._m

...u.3.?.....E

:o<

:3.5.

K0,».

A.<

...HA

. emunam

97...:H

.._m<

>>

niom

Page 30 of 161

_2.£m.m

m5.5....

wo:.Sm

.nm

8234::29.

uzEzm

83::m _5.8.

35.3»W

_s_%uu. 3=

_€_§_xmE

_=_5E

>_.

3.2.3.

2m.e2._

mm

ama

w33m

mm

><

..:.DD

A<

,:.—<

01_<

.—.O

.—.

Sam~33

~9...m~

_5..a._=E

Ea

mu_uE

u>m

in;

..

Su?=

s=a_=

_umE...»

mu_uE

u>£53

23:“.

89%98$

23%m

2oEm

>_D

._—?A

_

.m

oo...».

_=v::__=

vm_

um 8_uEu>

.m

vnhwm

.m

.=o:_u>

o:E:

umu_.__SDumuuoz

o8.2a._.w

_..%.~£

m?nm

?w

m.=

o=_o>

o.aE_m

in;aw.m

v==

c.D .u=

=m

.r<A

,HD

O_.~<

.HT

—<

U

2.n.$m

85...m

.343m

mm

zatnzmaxm

a<._.oa

..

ooo.Eou=

m=

o:.__u28

imam

ESan

Snow.

25,2.:62

son_a=

o_m3..8n_

83m

83w

3?.m

m8__oz

3.5

m5S.:nzu._xm

39.24.m

328M

mm

5§.._m

u:zm_:.E

A<

._.D._.

0550-:$225

83$.O

85?_.=

.£E

sau52..

E25:

MD

Z?>

Hw

—

E32%

muz§<

aQ

ZD

Ruz_zz_um

m

«N>

..~8

.23

>,._

.&_.__m

_.u:a_.o..m_a=

_u<

:2.E

o>.535

n.==

.m Piomow

u _a:._sU

5.3.53

55

Page 31 of 161

8._._=.m

m.

w.

m

Ooodom

..

:o__a>oco~_.350

0253.

83:..

.as... =

w_$u.2n_

<02.»

2._2.a>oas_

m_._=

_2oum w.__2_=

m8.._o.oo.8m

.-

3:5_.=

=_5

SQS

m_..a.:.

mSE

3m

m3_.E

m.55

..

8933.§_2____»2

a. zaum$_=

__8.._m

~m_c.2.w

mm

.-

..

.§_>

sm3.2

~mm

_e.2.8m.-

838o.~

EN

...2s_.8_z.a

Em

325233.5

on:e.2.Em

.-

830W

8a.?m

2%.:

m5.;

5.358%

”3:

_Eo_ae.E

$mE

.2.8m.-

=30

.m.o2E

u=.. .m__E

2._m5

._=o=

.mm

omm

a€32

3=_.__:§_§

83....m

233m

23%..

m,

o8.~m..

892$_o_,o~.2

5_em

.:....~887$

com.»

.am:

...$,~o:22...

_8._§.~~oS...-

83w

32W

8.m

:22...m

=E

8._U88...~N

na==

u>u~—

—NPH

>w

—¢—

~?n—=

o_=__.5m

aQB

EN

Z.=

=euo<

.cZ:=

.3u<3m

1=m

——

..2ou_.c\..—_.=

:u<

:3>

,mM

OE

..=<

.Hm

_GH

HU

DD

H

DZ

DK

m>

E_m

mE

J<.:n_<

U,

Nu nzam

Page 32 of 161

w.G

.=..._

m23.5»

w

?m.._2..

mm

a?am

wunam

u

.m

$3».

w

.w

..

w.

m.

.w

.._8.8m332

32:w

u:_m:8.__E

;2_>.m

0o.,.$>

._om .=5: .20

m_5E

o>oa=

:m

in;

n?_=.__.:.=

_xuA._a_E

3\._~>ama=

=u>

3_

:25__%

_.G.53.

._.2_a_._3§.aE

ou8..$.8.m

om.-

x..::m.uS.>

=.n

.5=a_.am

o__.S.o$mm

.-

.=2=

2sa=__

2..__.2on__§_=m

~$_w.8.o$.-

Sanam

uuaqmm

~33w

.$....o_

..35:

£5

.an:

.22.?

.:___53:

.22:5

O33

W:93

mam

am

m2u.=

_~>.§.._82._3_

=§_a_.__.m

E2u_o_€>

..S_e.om.om

m.~N

.m

.m

Summ

m.

..

33:23.5

.m

.m

.m

.5=..._=

_.mE

a$_oEm

>..o3§$:m

.~N

.§_.a.m

Sci.w

Ew

m?

m.

.:.~.3.

3_o.3:=o2

Sank

ooqa.W

8:3m

32.2m

$_u.=_~>

_e_£$2.5m

$_u_€>.25

.;.;o.8..;m.-

.m

5&2

m.

m

..335

5.8:Se

~..~.~mm

:55_?s3_.J

©w

:_mm

EU=

.E_m

uvumm

_=m

=_o>

oa:__uum

:_ED

ow gemm

o3w.om

.mom

.-

3Fa

cu>

.._3

?m:o_:.__.5m

u:uE

aZ=

=.3..<

éz..=

E3<

Suns:cu.uu_.e._.m

_.=:o<

Page 33 of 161

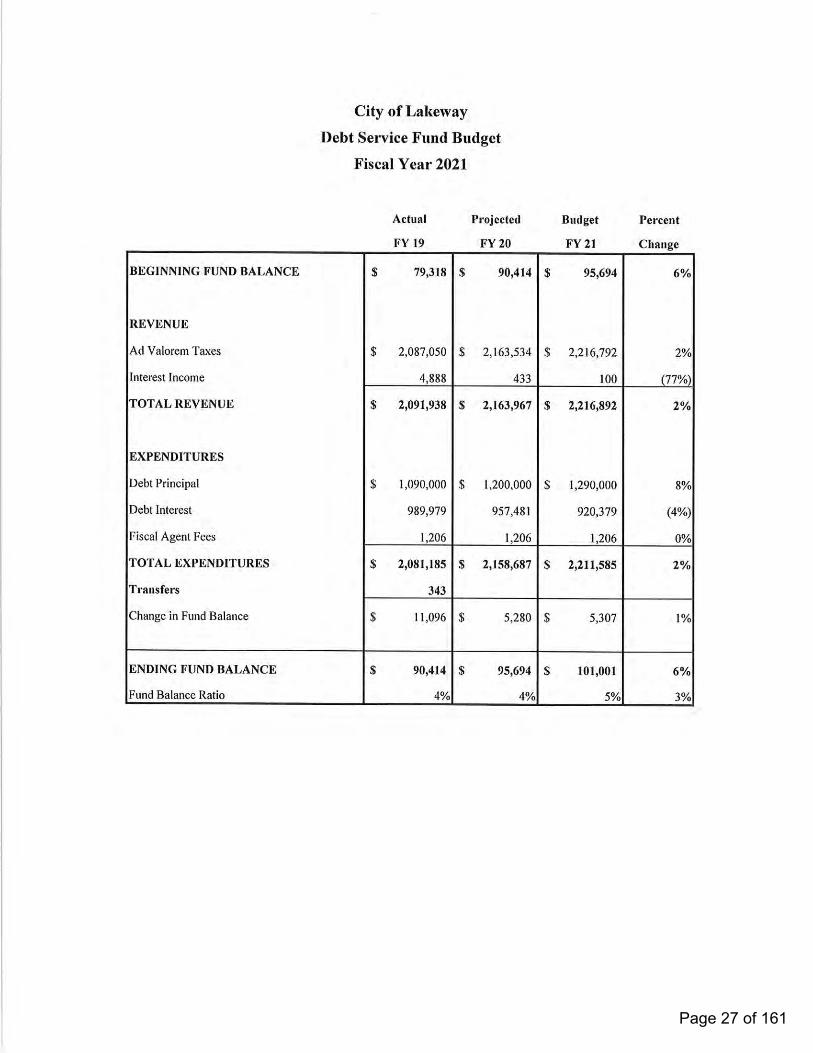

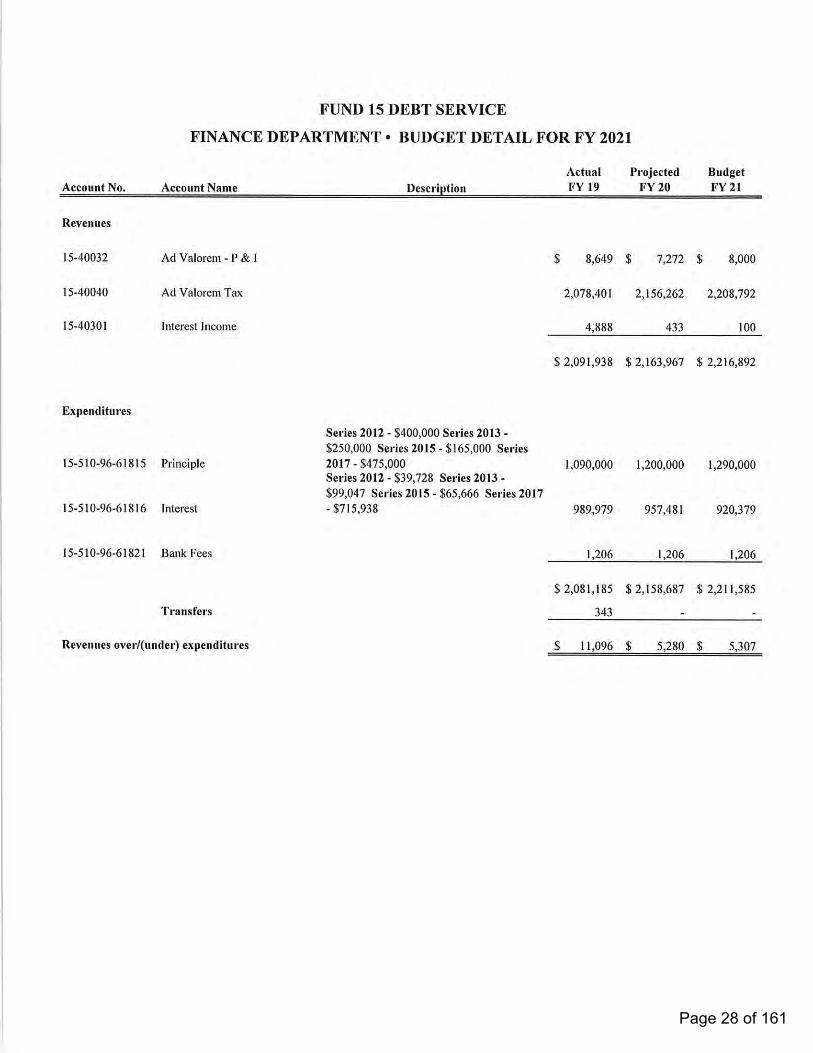

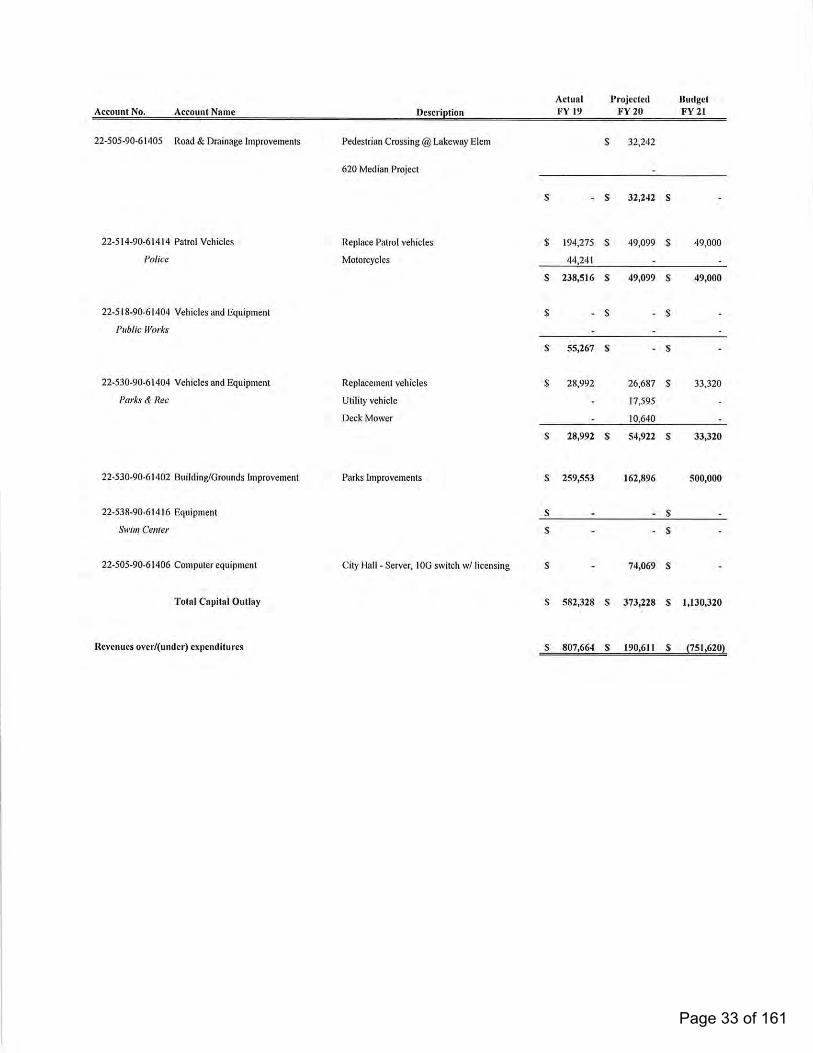

CAPITAL RESERVE FUND BUDGET PROJECTION

Revenue

Interest

Transfer in ~ fundbalance surplus

Transfer in - capital outlay budget

Total Revenue

Expenditures

PublicNotices

Hofessional fees

Building& Grounds Improvements

City Hall RenovationsConversionof PD to house EDS

City Park restroom - lower level

YMCA Pre—designphase

Park Improvements

SwimCenter Restoration

City Park - asphalt overlay of trails & parking. includesstriping

City Park - Pavilionand Upper restroom rehab

Heritage Center - asphaltoverlay and restripe parking lot

Activity Center - re?irbishing project

ResurfaoeSailmastersport court for pickleball

Resurfacebasketballcourt ~ City Park

Total

Road & Drainage Improvements

PedestrianCrossing @ Lakeway Elementary

620 Median project

Lakeway Blvd - East medianirrigation

Total

Vehicles and Equipment

City Hall - Server and 10GBswitchw/ licensing

Motorcycles

Replacement vehicles - PD

Replacement vehicles - Parks & Rec

Replacement vehicles- PublicWorks

Replacementvehicles - BDS

Replacement mower - Parks & Rec

Equipment - Parks

SecuritySystem - SwimCtr

Total Expenditures

Change in Fund Balance

Fund balance - beginning

Fund balance . ending

Projected Budget

FY18 FY19 FY20 FY21 FY22 FY23

42,934 62.652 23.739 9.000 40.000 30,000

350,000 1_115.101 350.000 350.000 350.000 350.000— 310.000 230.000 32.000 350,000 350,000

392,984 1,483,753 503,739 441,000 740,000 730,000

1,323 4.214 2.000 2.000 2,000 2,000

» 33.547 42.900 50.300 —.

.323 37.751 44.900 52.300 2.000 2,000

. . . 310.000 .- . . 500.000 1.200.000 .

104,186 259.553 37.325 — — —

— - — 43.000 — -

— . 500.000 500.000 500,000

159,313 51.000 - .—

. — 75.090 — —.

. . 21,500 — —.

. . 5,573 — —.

. . 2.100 — —.

. . 13.900 — —.

.— 7,403 — - »

254.004 320.553 152.395 1,043,000 2.010.000 500.000

- — 32.242 - —.

201,2-2 - - — —

201,22- » 32,242 - - —

. . 74.059 — —

— 44,241 — 45,000 .. 194.275 49.099 49.000 150,000 150,000

— 23,992 25.537 33.320 . 25,000

- 55.257 . . 35.000 35.000- - — . 50.000 50.000— — 10.540 — - -

— - 17.595 .—

.23.793 - — - . .23.793 322,775 173,090 32.320 290.000 270.000

495,352 531,039 413,123 1,192,520 2,302,000 772,000

(102,353) 307,554 190,511 (751,520) (1,552,000) (42,000)

3.242.374 3.139.505 3.947.170 4,137,731 3,335,151 1,324,151

3,139,505 3.947.170 4,137,731 3,335,151 1.324.151 1.732.151

Page 34 of 161

SE

muamum

moaoi«N

omi

muz<

a<m

975%U

Z—

QZ

m—

Ezam

o um. €.__:€§%

m€ov:5\.$>

oo:=

o>om

><

w:.D

OJ<

,:m<

UJ<

,—.O

,H

mE

uEo>

o.&::om

mi?m on98%

m~:®

_.co>O

._Q-;m

c:=o.:U umm

?czzm

><

w=

.DO

H<

.:n—<

U

mum

stnzmzxm

A<

._.O._.

mw

um_mm

o_mm

£o._m

sesz23$

mm

zsbnzamxm

m:zm

>m

EJ<

._.O,_.

0:52:.m

o._2E

wash. w

:_v:=m262

ouzomEoc

.£m:m

..r_.

m—

DZ

H>

HM

muz<

a<m

9755-uz_zz_©

mm

_N>

rA8

Vm

E?_

.0935c2uo_.9_m

_n:.u<

G3

53%_§E

2:5.8.=

:.__§%

u.s§w

_._22_.:.__3

353.3m

o56

Page 35 of 161

Nn

amuam 8..§§n_

wN

oN>

u_

§...§§m

_$.S~m

.m

3:_.==

:._.aA

..o_.=_5\..o.5:_:§sm

=.K

,.=:

m23.8

m.

m3:_o_.._.;o

_..s.n

..

.m

=.2=

u>a=

__=_ow

m:_E

Dm

oEc.oa.om

m...~

ooho?m

as?m

.A

3.5.$_:_€:uo£

m.:oE

u>E

._.Em

_:=::O

~oEo.oo.om

m...~

.25.E

u==

§_.5

3:26333.

B_.:.;_3

?=_.o

_.£___G

3:4w

.m

..m

,.:_.:.m_E

e,H

83.

.séoz

33.5o$$.2.o%

._.N

.w

.m

.a

mu»...

_a:o_mm

u.«oE3:o.2.¢$.§

mu.._:=

:a._.§

e?m

:33m

.m

.8°52

.22...... E

50E

OE

.o.«mcE

._._%

e..X

..

..85.:

_oo%$._.

~omo...w

~

o?M

amw

.»

E225

w=

_._§_o8§..§

3::9$z

5>

mon

5.3

>2

..o:.::$QuE

sz:..:.3<.oz.=

_.aZ¢

.§_._.m_.::.=

:.._§.:<

:3>

.mK

OK

1=<

,Hm

_DH

HO

GD

M

nzamH

UH

HO

MA

»—<

,:.—<

UZ

O~.—

.<U

:.=Z

mE

..:E§>

.3

975%

Page 36 of 161

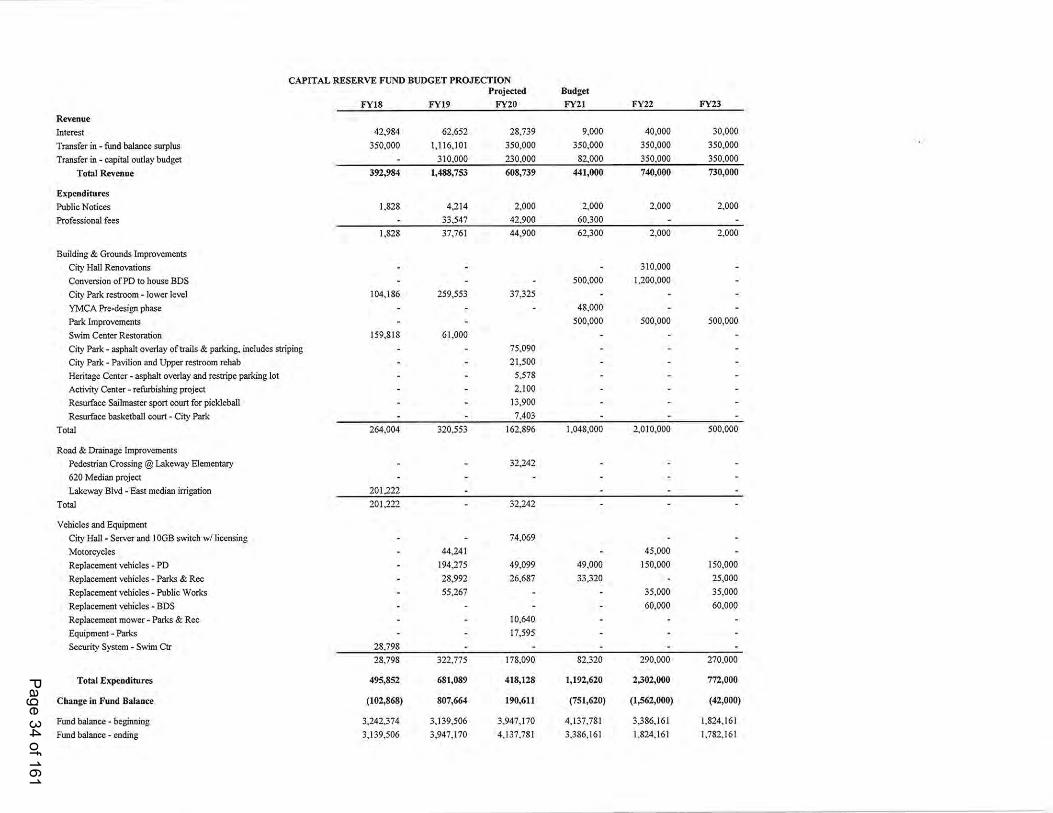

852.3.

Eggs“.

_.mo~>

n_

cramouzim

mU

ZZ

E

uoz?é:23

U./E

QZ

N

uu:.n_mmw

cam =_0w=

N£Q

mnisbnzm

axmA

<.H

O.H

muo_>

.om65:50

»u=m

:o=__£>

_.9___oP_

.5=a_.am

_s_o2_m

2:25...:=

a.m

mm

EFE

zmA

..z.m

m.:za>

m:

A<

._.O._.

o=_ouE

Beau:

£30.590

_a&o_=

:E

m5zm

>m

m

mu./:54:

nzbmuz_zz5m

m

au:.:_U_u

>,.—

3>

.._3

E

.=3._o._

.uu_.:m=

23.?._.~_s_:o<

:323>

.55

Ew

czmc:=m

»=..=

8mw

=:.=

=m

2.50

zs>»3_aA

ma~05

Page 37 of 161

X”

amuam um

moqoaE

SE

comm

mi

mn~_m

._vn$.:::.:u58

Toc:=v\..u>

e 3==

u>o~—

.§..mm

muqm

mSE

:a

832%

%~.2

m8E

ou_2.§m

=oo

Bt_.£w

=5:

Q___um

.su__:%§::_oo

#2ca

_.-m.8

..

S8.535

a. _=_8m

om?

o.B.-m

.8

..

2m

azeo-$.B

.-m.8

..

mu..8__x.s<

<oE

2~S.3.-m.8

.w

.w

M:

m2...§_xm

t___«mc88.3.-m

.§

nu..=_=

.:a._xm

=¢m

.mw

2%m

3...m

uu

mo:_ooE

.mo.5.:_

—cm

O?.©

O

83m

2%m

33m

amenE

au:,a§:=

2~_~o...8

3=:a>

um

3.7.

on5%

3>

m=

o_::._u3Qu=

:..Z.::3u<

.eZ.=

=3o<

.vMU

=m

uu.uu_..:.__§:a<

Ea

MPHM

GR

_.:<,H

HQ

emunzm

QZ

PH>

.5mD

UH

moz?dbm

HM

DO

U-

8nzam

Page 38 of 161

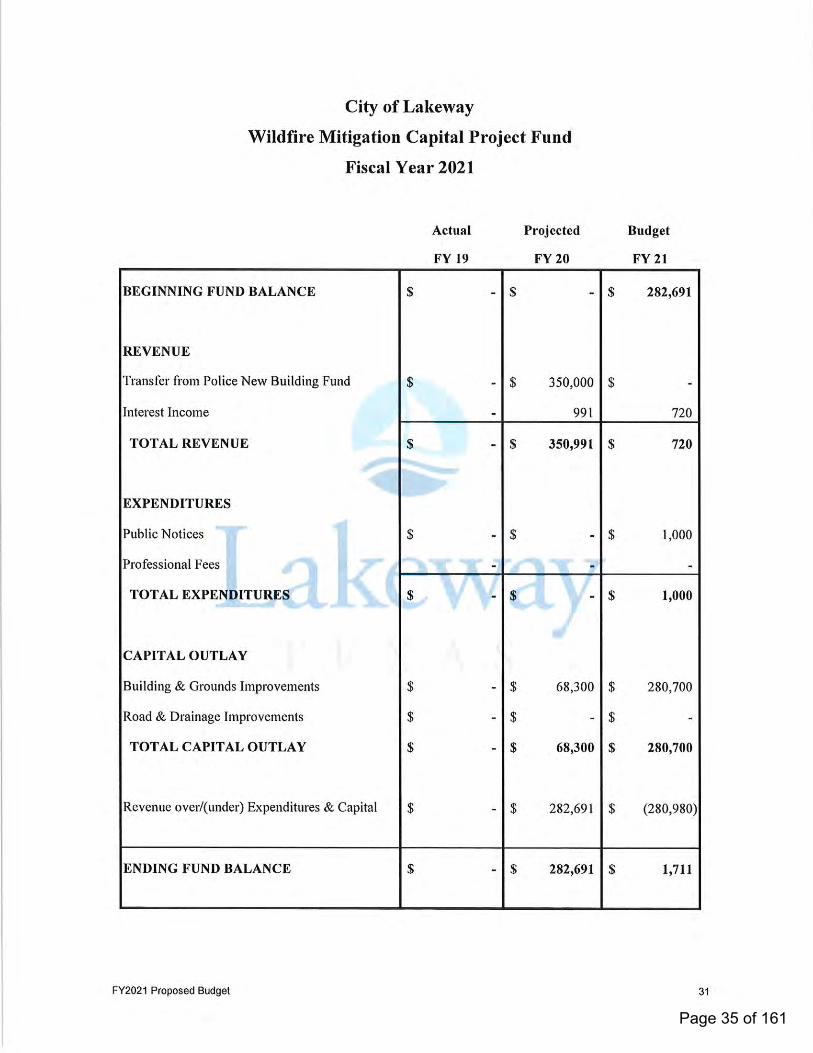

$3.5.u?aoi

FNoN

>u_

moz3<

mD

./5hU

ZH

HZ

H

ouzsnm E_=

.._E

uwsaso

mm

E::=

zm.:.E

A<

._.O._.

:_o=a_.am.2:m

EoU

=§_a_=

_.m:=

oU

m.uE

.:oUE

EE

.E=

a_=_.m

wm

uabnzmm

xa

n_:zm>

mm

AA

FOH

.

2:853225

Bum

goo...E80

m5Z

H>

H-

muza?am

nzamoz_zz_um

_m

&.=

=_o

GE

8E

SE

.:3.:..—.ou_.=

mc2uu_..:.~

_E:e<

Ea

53>_aum

E

«owc=

mc.:.,m

mw

o_c::uo,_.2.50

.€.$3_«Ano.05

Page 39 of 161

onE

muzmuom

oaoi53>“.

53.a

3:5m

55m

_.2:1.;_.__=<

.§=.

:_=a:m

SW3

m#3.

mE

ns.m

m:=

.=...2E

__.a§

«S...33

NE

;E

___§m8:.E

«E.

N

835:3

.52.

§s:____=__v<

Esp

.E__a__...m.2_.._=

_oo§.s.2.§.3

as>

ezoom

Eau

.=2_a____.mE

50o:.G

._:.-m.3

=3.»

mac.»

w$.m

$33w

snzzou .=_aE

:5_.:&=

cmv~m

_c.mT

~~m.3

5.8893

+2&

5.§$T

mw

%3%

....._._ou

no....=u:2_xm

_

$3a

saww

95.2m

SNSN

3:2:85

.mo.§=

_3838

.53w

83m

8%:

an33.

=89

Sac233.8

m2_:9$~—

—N

onkm

3>

m:o_:.:..um

oDoE

aZ.:=

aua<dz

.:_.Euu<

_E3......

_.3:...:.__.:_:<

:3>

,mm

om1?<

.HH

QH

HU

QD

Q

QZ

DE

VU

OA

OZ

EU

HH

H1500

-be

Qzbh

Page 40 of 161

B

uu:§_UE

>m

ca>

.._3

>m

.:3..u.—33...:

—.33_..:.m

_E:u<

Ea

53>_§r_

sw.=

_m2.3.baam

EE

O

.§>»3_nA

.8.30

68amu$8_2n_

ESE

035%ooz?w

mw

:=r._

moz<

a<m

G./5h

cz?zm

ouz?umu=

=n_:_ow

sazo

mm

istnzmm

xmA

<.—

.O.—

.

EE

Om

:_mm

o.UBegum

mm

zabnzmt?

m:zm

>m

:..—

<H

Oh

2:85~m

0._0~=—

mo./25¢:

DZ

D,.~

ozwzz?m

m

Page 41 of 161

an332m

3835_.~oN

>u_

83.9m

32.6a

ova...”u

nu\_=.=

u=a53

A..3..:3\.$.5

mo=

:o>o~_

83:m

83m

Rn:

»

83com

33o,=

3__uu2\<U

Eo:$.8.-E

a

8...:33

:~.m_

E20

m:_m

mo._U

_8__omQ

.~s.3.-m.8

n?_=.=

.=a._zm

8%:

M~32

a83:

m

.m

29:52:

.mE

2=_

_omo.1w

o

83..m

.2.m..?

m9:

Em

W3;

.903B

ED

~_~$.wo

$_.:?6.z

E>

..~ow>

.m3

?m:e_::._o3D

~EsZ

.:=e3<

57..:=

e3<E

wezm

=3ua_9.m

_:=.u<

Ea

MFAM

OE

..=<

.Hm

~QH

HU

DD

M

nzam>

?r_<w

AW

EE

O-

2Q

ZPH

Page 42 of 161

mm

amaze 88._o_n_

52>“.

moz3<

mm

zauU

ZH

GZ

M

&_=

=_o

:.uo..a.~

3>

.._

=u_.=

m

oozsamvszmE®

w:w

:U

mm

E:._:za.§m

A<

._.O._.

m._E

__=.um

\w=

_=_a..r~

$=&

=m

8E0

EE

:2:oM\u.uu_voS_\b::oum

Eoow

uEF

tam.m

ums?

uE:.___£

.m

2._£aw

mum

:§azm._xm

_

m:zm

>5_

44,50...

uEoo=

_522.:

meow .sw

a=m

E350u::o.::.

m:zm

>m

m

muz<

q<m

DZ

DE

uz_zz5mm

8.€—

3w

k

_.23_......__.=

:u<

:253>

_§E

.owc=

m c:=,m

..owE

EE

omm

b u=:o>

=_.

§=3_5

no 55

Page 43 of 161

3

E...._:

m$8.5

W33.3

m

mm

uam 8..,8en_E

NE

ma..:.=

.:2_v.aA

._oc:=<

._u>e8=

:a_5.=

35:m

25:m

2.m.:

a

8m8m

.m

.a=_E

um\m

___=_.§

8mG

.m _.§.:

..

.3__._%

w850%

~s.o_.§.:

2_.~

2 _.~.

._.2__2:.éo-s.8.§.__

$2$1.

.28_B

2E_=

aumE

082

~$.8.-m.:

25.225.:

83.2::

:5.m

oms:8~$.8.-m

.:

.m

.m

.W

2.._..___:_.3:%m