Embed Size (px)

Citation preview

1

WelcomeGreater Cincinnati/Northern Kentucky Apartment Association

2012 Apartment Market Overview2012 Apartment Market Overview

CBRE | Page 1

1

2012 Apartment Market

Distress Report / Capital Markets

Economic Fundamentals

Development Pipeline

Investment Market

Rents and Occupancies

Forecast for 2012

CBRE | Page 2

January 2011 January 2012

2012 Apartment MarketWhat a Difference a Year Makes

Average Temperature 26.1 Degrees 35.3 Degrees

January Snowfall 12.8 Inches 1.6 Inches

CBRE | Page 3

2

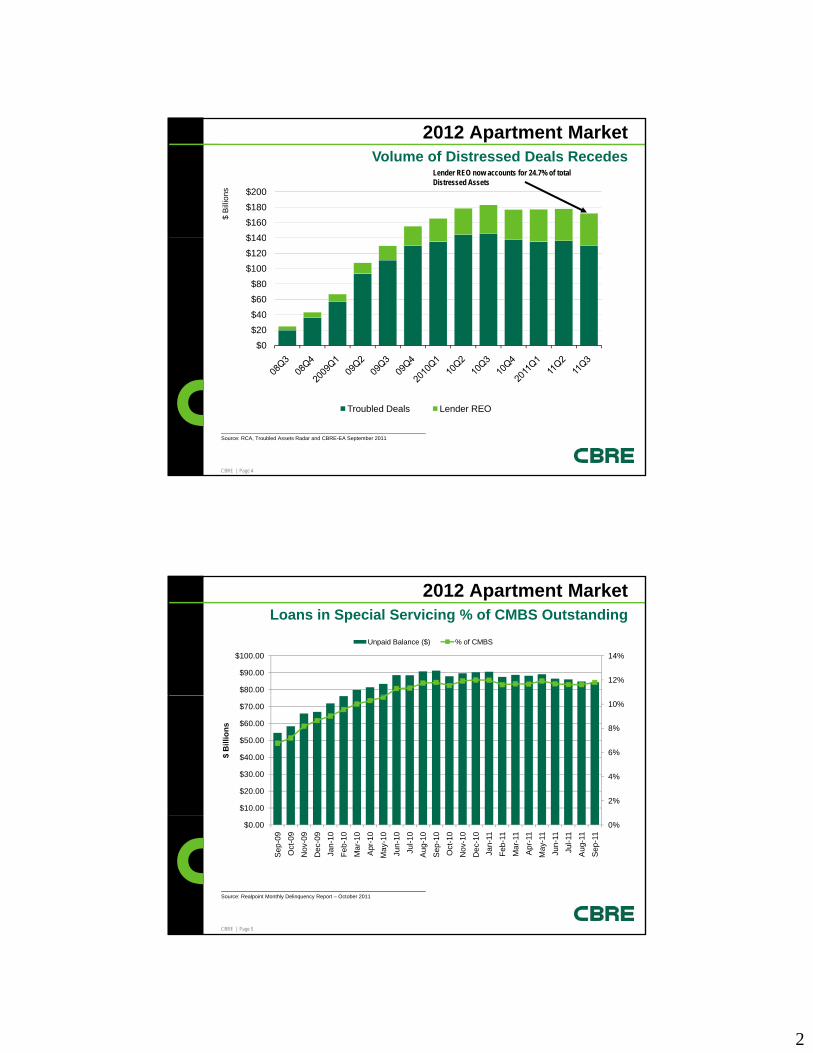

2012 Apartment MarketVolume of Distressed Deals Recedes

$140

$160

$180

$200

$ B

illio

ns

Lender REO now accounts for 24.7% of total Distressed Assets

$0

$20

$40

$60

$80

$100

$120

$140

CBRE | Page 4

Source: RCA, Troubled Assets Radar and CBRE-EA September 2011

Troubled Deals Lender REO

2012 Apartment MarketLoans in Special Servicing % of CMBS Outstanding

12%

14%

$80.00

$90.00

$100.00

Unpaid Balance ($) % of CMBS

2%

4%

6%

8%

10%

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$ B

illi

on

s

CBRE | Page 5

Source: Realpoint Monthly Delinquency Report – October 2011

0%$0.00

Se

p-0

9

Oct

-09

No

v-0

9

De

c-0

9

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-1

0

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-1

1

Au

g-11

Se

p-1

1

3

Substantial Loan Maturities will OccurIn the next 5 years, total amount is estimated to be $1.7 Trillion

2012 Apartment Market

CBRE | Page 6

Source: CBRE Investors, Foresight Analytics 3Q 2010 Update

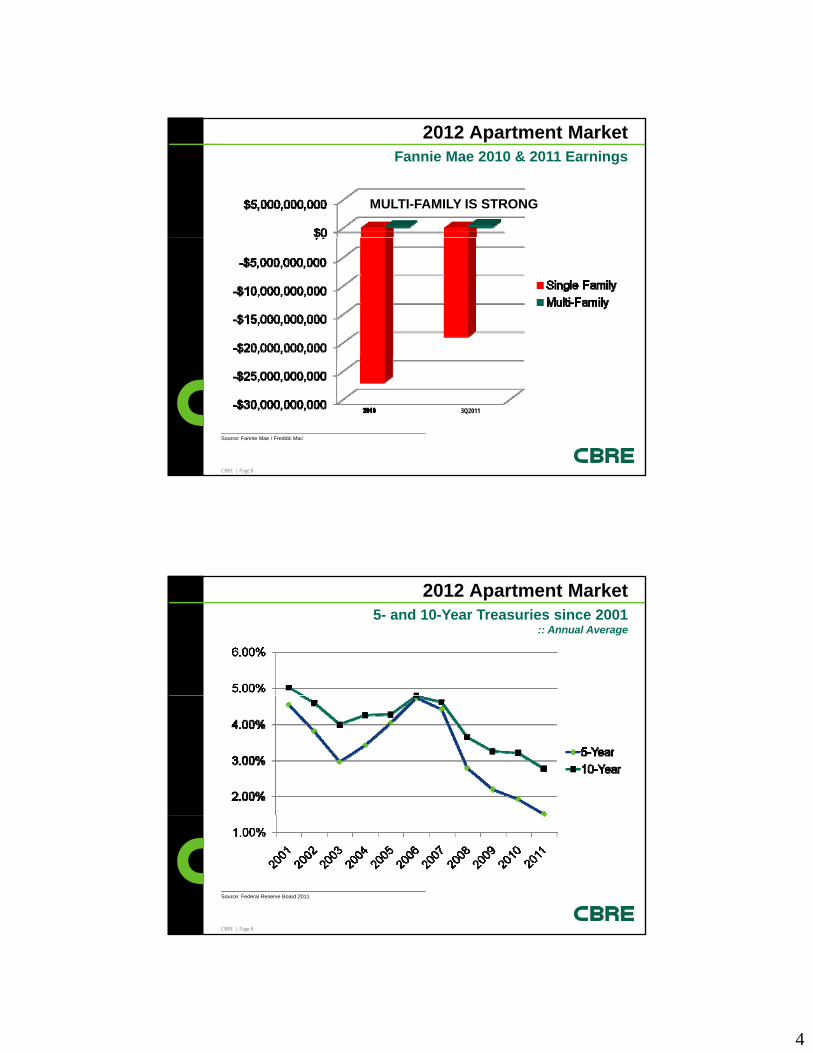

2012 Apartment MarketFreddie Mac 2010 & 2011 Earnings

MULTI-FAMILY IS STRONG

CBRE | Page 7

Source: Fannie Mae / Freddic Mac

3Q2011

4

2012 Apartment MarketFannie Mae 2010 & 2011 Earnings

MULTI-FAMILY IS STRONG

CBRE | Page 8

Source: Fannie Mae / Freddic Mac

3Q2011

2012 Apartment Market5- and 10-Year Treasuries since 2001

:: Annual Average

CBRE | Page 9

Source: Federal Reserve Board 2011

5

2012 Apartment MarketKey Rates

:: Historical and Current

2/2006 2/2007 2/2008 2/2009 2/2010 2/2011 2/2012*

Prime Rate 7.50% 8.25% 6.00% 3.25% 3.25% 3.25% 3.25%

5-Year Treasuries 4.59% 4.68% 2.74% 1.87% 2.25% 2.33% 0.875%

10-Year Treasuries 4.60% 4.69% 3.68% 2.89% 3.63% 3.60% 2.00%

LIBOR (3-mo) 4.77% 5.36% 3.09% 1.24% 0.25% 0.31% 0.49%

CBRE | Page 10

*Source: Bloomberg.com as of 2/21/2012 @ 7:57 AM

2012 Apartment MarketHomeownership Rate is Likely to Continue Declining in 2012

38

40

42

69

70

71

Homeownership Rate, % Renter Households, Millions

22

24

26

28

30

32

34

36

61

62

63

64

65

66

67

68

CBRE | Page 11

Source: Bureau of the Census (Housing Vacancy Survey), CBRE Econometric Advisors, Q3 2011

2060

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

F

Homeownership Rate, % Renter Households, Millions

6

2012 Apartment MarketFannie Mae | Freddie Mac REO Inventory

CBRE | Page 12

Source: Fannie Mae / Freddic Mac

2012 Apartment MarketCincinnati MSA Housing Market

Number of Single Family Sales

30,000

35,000

10,000

15,000

20,000

25,000

CBRE | Page 13

Source: Cincinnati Board of Realtors & Northern Kentucky Association of Realtors

0

5,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

7

6.9% 7.2% 7.6%

9.9% 10.5%

8.0%

10.0%

12.0%

2012 Apartment MarketNational House Price Appreciation

:: House Price Appreciation Over Previous Four Quarters | USA(Seasonally Adjusted, Purchase-Only Index)

4.8%

‐0.2%

‐4.7%‐3.0%

‐3.7%

‐8.0%

‐6.0%

‐4.0%

‐2.0%

0.0%

2.0%

4.0%

6.0%

CBRE | Page 14

‐8.3%

‐12.0%

‐10.0%

Source: Federal Housing Finance Agency, Nov. 29, 2011 News Release

20

01

Q3

20

02

Q3

20

03

Q3

20

04

Q3

20

05

Q3

20

06

Q3

20

07

Q3

20

08

Q3

20

09

Q3

20

10

Q3

20

11

Q3

2012 Apartment MarketJobs – Statewide Unemployment Rate

:: Current / Low / High (Seasonally Adjusted)

Current* Low Year High Year

Nationwide 8.7%

Indiana 9.0% 2.6% 1999 12.7% 1983

Ohio 8.5% 3.8% 2001 13.8% 1983

Kentucky 9.4% 4.1% 2000 12.0% 1983

CBRE | Page 15

Source: Bureau of Labor Statistics

* As of November 2011p

8

2012 Apartment MarketGreater Cincinnati MSA Unemployment Rate

(Not Seasonally Adjusted)

CBRE | Page 16

Source: Bureau of Labor Statistics

2012 Apartment Market

10,000

20,000

Greater Cincinnati Net Job Growth

-40,000

-30,000

-20,000

-10,000

0

CBRE | Page 17

-50,000

,

De

c-02

De

c-03

De

c-04

De

c-05

De

c-06

De

c-07

De

c-08

De

c-09

De

c-10

De

c-11

201

2 Pro

j.

201

3 Pro

j.

201

4 Pro

j.

201

5 Pro

j.

201

6 Pro

j.Source: CBRE Econometric Advisors

9

2012 Apartment Market

6 9%

6.6%

Cleveland OH

Columbus, OH

Jobs | Local MSA Unemployment Rates(Not Seasonally Adjusted as of November 2011p)

8.0%

7.8%

7.2%

7.0%

6.9%

Springfield, OH

Cincinnati, OH

Akron, OH

Lexington, KY

Cleveland, OH

CBRE | Page 18

9.5%

8.3%

8.2%

Detroit, MI

Dayton, OH

Indianapolis, IN

Source: Bureau of Labor Statistics

2012 Apartment MarketCincinnati MSA Population Growth

9.1%

3.0%

8.9%

CBRE | Page 19

Source: CBRE

10

2012 Apartment MarketGreater Cincinnati Building Permits Issued

2011 Single Family Permits Issued: 2,4902011 Multi-Family Permits Issued: 743

CBRE | Page 20

Source: US Census

2012 Apartment MarketGreater Cincinnati Multi-Family Permits*

*Multi-Family Defined as 5+ Units

CBRE | Page 21

Source: US Census

11

2012 Apartment MarketGreater Cincinnati Multi-Family Units Built and Projected

CBRE | Page 22

Source: CBRE

2012 Apartment Market

Current @ The Banks | Completed 2011300 Units in Downtown Cincinnati

Studio, 1- and 2- BR Units | Average $1.80/SF Rents

Development

CBRE | Page 23

Source: CBRE

12

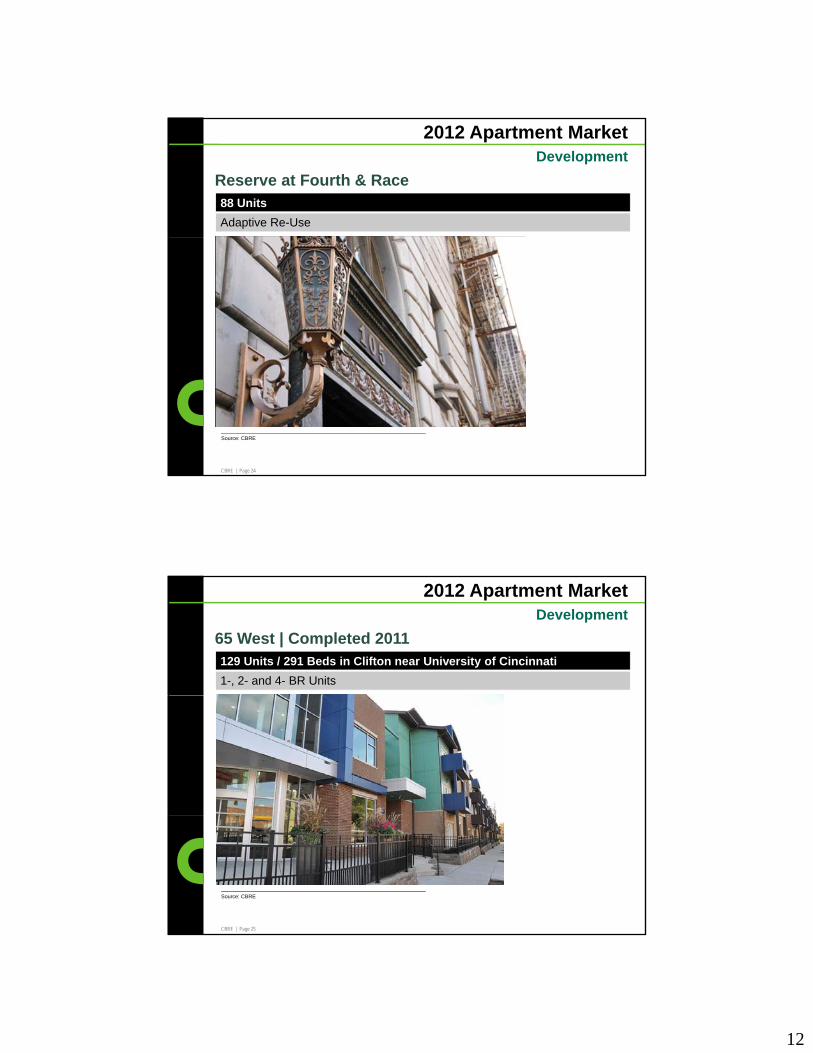

2012 Apartment MarketDevelopment

Reserve at Fourth & Race88 Units

Adaptive Re-Use

CBRE | Page 24

Source: CBRE

2012 Apartment MarketDevelopment

65 West | Completed 2011129 Units / 291 Beds in Clifton near University of Cincinnati

1-, 2- and 4- BR Units

CBRE | Page 25

Source: CBRE

13

2012 Apartment Market

Euclid SquareVine Street Flats

Development

36 Units on Short Vine

Opening September 2012

36 Units on Short Vine

Opening September 2012

Schiel School

CBRE | Page 26

Schiel School

Source: CBRE

102 Units on Short Vine

Opening September 2013

2012 Apartment MarketDevelopment

University Edge120 Units in Clifton

Opening September 2012

CBRE | Page 27

Source: CBRE

14

2012 Apartment MarketDevelopment

U Square at the Loop160 Units adjacent to UC Campus

Mixed Use

CBRE | Page 28

Source: CBRE

2012 Apartment MarketDevelopment

Palmera 360 Units at Butler-Warren Road & Bethany Road

1-, 2-, and 3-Bedroom Class “A+” Garden & TH Units

CBRE | Page 29

Source: CBRE

15

2012 Apartment MarketGreater Cincinnati Effective Rents

CBRE | Page 30

Source: CBRE, Year End Rent & Occupancy Survey

2012 Apartment MarketGreater Cincinnati Historical Occupancy

CBRE | Page 31

Source: CBRE, Year End Rent & Occupancy Survey

16

December July Dec.

2005 2006 2007 2008 2009 2010 2011 2011

2012 Apartment MarketRents & Occupancy | Overall Market

2005 2006 2007 2008 2009 2010 2011 2011

Occupancy 89.7% 90.9% 91.5% 90.6% 88.4% 91.8% 93.8% 93.1%

EffectiveRent

$637 $666 $680 $666 $675 $690 $709 $718

EffectiveRent Per SF

$0.71 $0.74 $0.75 $0.75 $0.74 $0.77 $0.77 $0.79

CBRE | Page 32

Source: CBRE, Year End Rent & Occupancy Survey

2012 Apartment MarketOccupancy by Submarket

December July Dec.

2005 2006 2007 2008 2009 2010 2011 2011

O ll 89 7% 90 9% 91 5% 90 6% 88 4% 91 8% 93 8% 93 1%Overall 89.7% 90.9% 91.5% 90.6% 88.4% 91.8% 93.8% 93.1%

Northwest 90.8% 90.4% 90.1% 89.0% 87.8% 91.0% 93.2% 91.9%

N. KY 91.3% 92.8% 93.9% 91.1% 88.0% 92.2% 94.2% 94.1%

West 82.3% 89.2% 89.0% 87.1% 84.8% 89.9% 90.7% 91.3%

East 91.0% 91.2% 91.7% 92.8% 90.8% 92.7% 94.3% 93.5%

Central 89.5% 89.4% 90.1% 90.5% 88.4% 90.3% 93.7% 91.6%

Northeast 90 3% 91 6% 93 2% 92 9% 89 8% 93 5% 95 1% 94 9%

CBRE | Page 33

Source: CBRE, Year End Rent & Occupancy Survey

Northeast 90.3% 91.6% 93.2% 92.9% 89.8% 93.5% 95.1% 94.9%

17

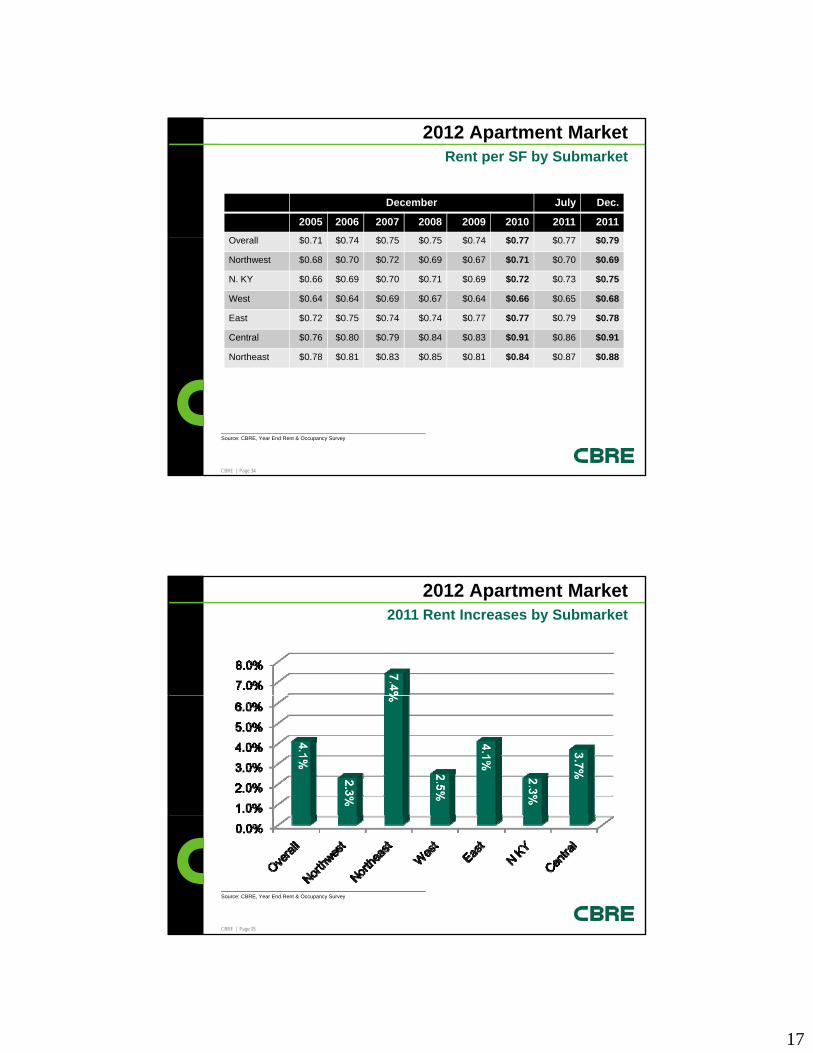

2012 Apartment MarketRent per SF by Submarket

December July Dec.

2005 2006 2007 2008 2009 2010 2011 2011

O ll $0 71 $0 74 $0 75 $0 75 $0 74 $0 77 $0 77 $0 79Overall $0.71 $0.74 $0.75 $0.75 $0.74 $0.77 $0.77 $0.79

Northwest $0.68 $0.70 $0.72 $0.69 $0.67 $0.71 $0.70 $0.69

N. KY $0.66 $0.69 $0.70 $0.71 $0.69 $0.72 $0.73 $0.75

West $0.64 $0.64 $0.69 $0.67 $0.64 $0.66 $0.65 $0.68

East $0.72 $0.75 $0.74 $0.74 $0.77 $0.77 $0.79 $0.78

Central $0.76 $0.80 $0.79 $0.84 $0.83 $0.91 $0.86 $0.91

Northeast $0 78 $0 81 $0 83 $0 85 $0 81 $0 84 $0 87 $0 88

CBRE | Page 34

Source: CBRE, Year End Rent & Occupancy Survey

Northeast $0.78 $0.81 $0.83 $0.85 $0.81 $0.84 $0.87 $0.88

2012 Apartment Market2011 Rent Increases by Submarket

CBRE | Page 35

Source: CBRE, Year End Rent & Occupancy Survey

18

2012 Apartment MarketVacancy vs. Rent Inflation

CBRE | Page 36

Source: CBRE, Year End Rent & Occupancy Survey

Dec ‘0

1

Dec ‘0

2

Dec ‘0

3

Dec ‘0

4

Dec ‘0

5

Dec ‘0

6

Dec ‘0

7

Dec ‘0

8

Dec ‘0

9

Dec ‘1

0

Dec ‘1

1

2012 Apartment Market

Percentage of Properties

Offering Concessions:

Avg. Monthly Concessions

by Style:

Greater Cincinnati Concession Summary

December 2010 2011

Efficiency $25 $27

1 Bedroom $48 $43

2 Bedroom $57 $51

31%

40%

36%

25%

CBRE | Page 37

3 Bedroom $72 $50

2008 2009 2010 2011

Source: CBRE, Year End Rent & Occupancy Survey

19

2012 Apartment Market

$400

$600

$800

1 Bedroom / 1 Bath Effective Rents by Submarket

$0

$200

$400

2007 2008 2009 2010 2011

East $555 $549 $569 $579 $586

West $461 $454 $445 $439 $449

CBRE | Page 38

Source: CBRE, Year End Rent & Occupancy Survey

N. East $676 $701 $649 $664 $744

N. West $561 $549 $539 $548 $566

Central $572 $577 $610 $672 $652

N. Ky. $552 $564 $551 $569 $600

Overall $569 $566 $573 $601 $612

2012 Apartment Market2 Bedroom / 1 Bath Effective Rents by Submarket

$400

$600

$800

$0

$200

$400

2007 2008 2009 2010 2011

East $558 $566 $609 $587 $590

West $544 $526 $499 $530 $542

CBRE | Page 39

Source: CBRE, Year End Rent & Occupancy Survey

N. East $739 $719 $660 $694 $704

N. West $612 $624 $618 $610 $637

Central $653 $660 $683 $651 $699

N. Ky. $603 $594 $587 $600 $639

Overall $624 $604 $599 $606 $631

20

2012 Apartment Market

$600

$900

$1,200

2 Bedroom / 2 Bath Effective Rents by Submarket

$0

$300

$600

2007 2008 2009 2010 2011

East $794 $819 $818 $825 $856

West $694 $642 $734 $697 $701

CBRE | Page 40

Source: CBRE, Year End Rent & Occupancy Survey

N. East $887 $926 $879 $901 $952

N. West $778 $785 $733 $724 $763

Central $940 $987 $980 $1,181 $1,120

N. Ky. $759 $758 $763 $783 $805

Overall $831 $849 $822 $850 $888

2012 Apartment Market

$900

$1,200

3 Bedroom Effective Rents by Submarket

$0

$300

$600

2007 2008 2009 2010 2011

East $757 $780 $848 $851 $856

West $783 $732 $654 $735 $770

CBRE | Page 41

Source: CBRE, Year End Rent & Occupancy Survey

N. East $1,289 $1,199 $1,089 $1,243 $1,253

N. West $807 $846 $839 $852 $849

Central $1,001 $981 $864 $975 $963

N. Ky. $752 $756 $844 $913 $848

Overall $919 $927 $904 $897 $913

21

2012 Apartment Market

$250,000,000

$300,000,000

Greater Cincinnati Multi-Housing Sales Volume

$50 000 000

$100,000,000

$150,000,000

$200,000,000

CBRE | Page 42

$0

$50,000,000

Source: CBRE

2012 Apartment MarketApartment Units Sold in Greater Cincinnati

5,422 5,210

6,450

5,450

6,819

5,1015,443

4,5984,293

2,0442,346

CBRE | Page 43

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: CBRE

22

2012 Apartment MarketMarket Activity is a “Barbell”

UNDER $20K PER UNIT OVER $50K PER UNIT

967 Units

$45 Million

1,575 Units

$112 Million

2,901 Units

$35 Million

CBRE | Page 44

Source: CBRE

2012 Apartment Market

$50,000

$60,000

Average Price Per Unit

$10,000

$20,000

$30,000

$40,000

CBRE | Page 45

$0

Source: CBRE

23

LAKOTA LAKE(FKA: WOODBRIDGE ON THE LAKE)

# of Units Sale Date

492 1/2011

2012 Apartment MarketInvestment Market – 2011 Sales

492 1/2011

CBRE | Page 46

BAVARIAN WOODS / RENATA / FERNCREST / PARK VALLEY

# of Units Sale Date Price per Unit

806 6/2011 $12,775

2012 Apartment MarketInvestment Market – 2011 Sales

CBRE | Page 47

24

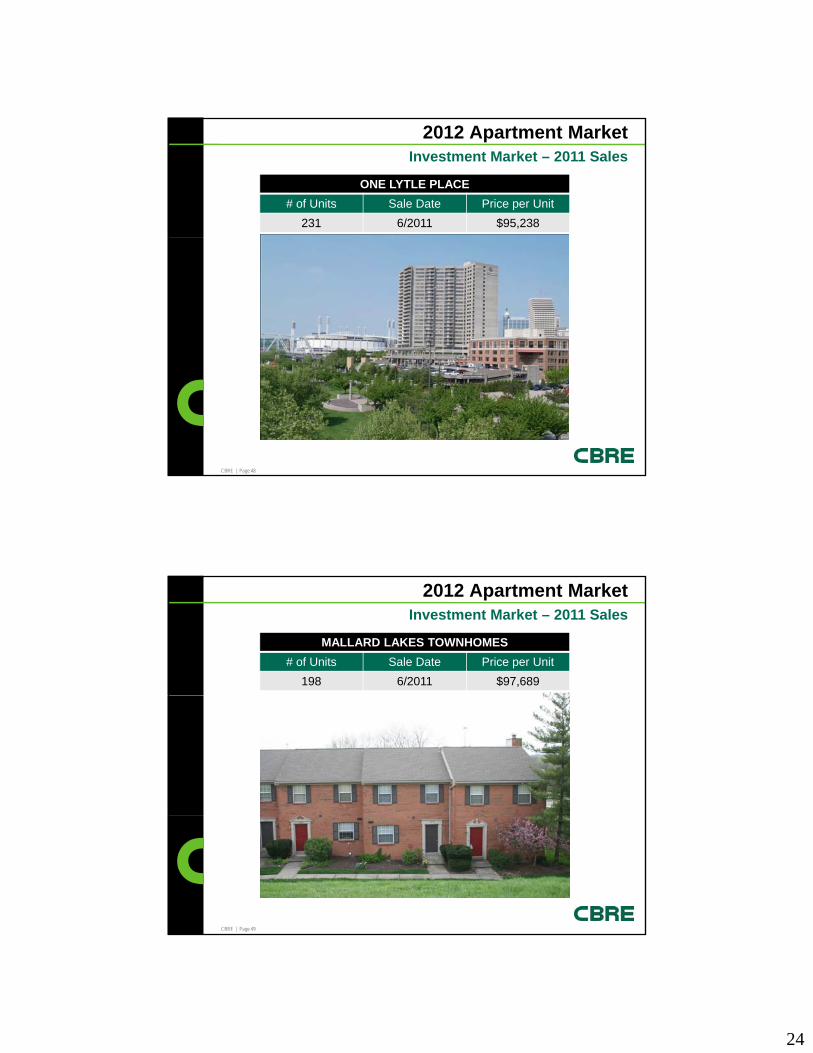

ONE LYTLE PLACE

# of Units Sale Date Price per Unit

231 6/2011 $95,238

2012 Apartment MarketInvestment Market – 2011 Sales

CBRE | Page 48

MALLARD LAKES TOWNHOMES

# of Units Sale Date Price per Unit

198 6/2011 $97,689

2012 Apartment MarketInvestment Market – 2011 Sales

CBRE | Page 49

25

GRANDVIEW SUMMIT

# of Units Sale Date Price per Unit

192 8/2011 $91,667

2012 Apartment MarketInvestment Market – 2011 Sales

CBRE | Page 50

REMINGTON PLACE

# of Units Sale Date Price per Unit

234 10/2011 $53,419

2012 Apartment MarketInvestment Market – 2011 Sales

CBRE | Page 51

26

MAYRIDGE / LAFEUILLE / WESTBROOK

# of Units Sale Date Price per Unit

393 3/2011 – 10/2011 $16,349

2012 Apartment MarketInvestment Market – 2011 Sales

CBRE | Page 52

TIMBER HOLLOW

# of Units Sale Date Price per Unit

368 11/2011 $63,859

2012 Apartment MarketInvestment Market – 2011 Sales

CBRE | Page 53

27

2012 Apartment Market2008-2010 Cap Rates

CBRE | Page 54

Source: CBRE

2012 Apartment Market2008-2011 Cap Rates

CBRE | Page 55

Source: CBRE

28

2012 Apartment Market

Effective rents will increase 3.0%

Most new units will be “purpose-built”

Occupancy will be 93.5% at mid-year and remain

Recap of Dave’s 2011 Forecast

steady through year end

Cap rates will remain steady for “A” and “B-”grade assets. Class “C” cap rates will rise

Energy/Resource Cost Control will move to the forefront

CBRE | Page 56

2012 Apartment Market

Effective rents will increase 2.5%

Occupancy will remain above 93.0% and climb to 95.0%

2012 Forecast

Development pipeline will accelerate, weighted toward in-fill

Sale market will be active; At least $250 Million in trades

CBRE | Page 57

29

2012 Apartment Market

Dave Lockard, CCIMFirst Vice President

Steve LaMotte, Jr., CCIMSenior Vice President

Dane Wilson Senior Associate

Indianapolis-Cincinnati Multi-Housing Group

David EnglertFinancial Analyst

Emily CantleySales Assistant

Carrie BallardClient Services Specialist

CBRE | Page 58

2012 Apartment Market

To download a copy of today’s presentation, please visit our team website at:

b / h i

For more information

• www.cbre.com/mhgic –“Market Reports & Rent Surveys” Tab

If you would like to receive a hardcopy of the presentation please email:

CBRE | Page 59