Embed Size (px)

Citation preview

April 14, 2015

Alliance Pipeline

CIBC Fixed Income Conference

Forward-Looking Information

Certain information contained in this presentation constitutes forward-

looking statements. The words “anticipate”, “expects” and “expected to”

and similar expressions are intended to identify such forward-looking

statements. Although Alliance believes that these statements are based on

information and assumptions which are current, reasonable and complete,

these statements are necessarily subject to a variety of risks and

uncertainties including, but not limited to, future operating performance,

regulation, economic conditions and fundamentals affecting the oil and gas

producing and marketing industries. Should one or more of these risks or

uncertainties materialize or fail to materialize, or should underlying

assumptions prove incorrect, actual results may vary materially from those

expected.

2

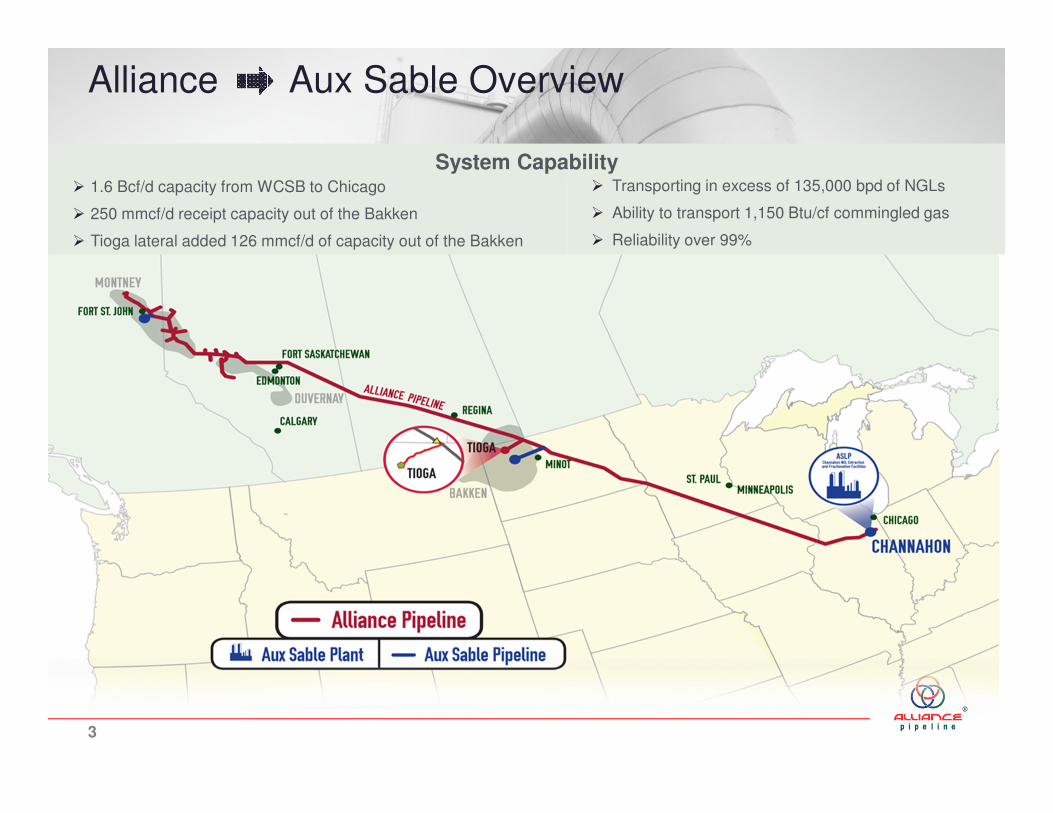

Alliance Aux Sable Overview

� 1.6 Bcf/d capacity from WCSB to Chicago

� 250 mmcf/d receipt capacity out of the Bakken

� Tioga lateral added 126 mmcf/d of capacity out of the Bakken

� Transporting in excess of 135,000 bpd of NGLs

� Ability to transport 1,150 Btu/cf commingled gas

� Reliability over 99%

System Capability

3

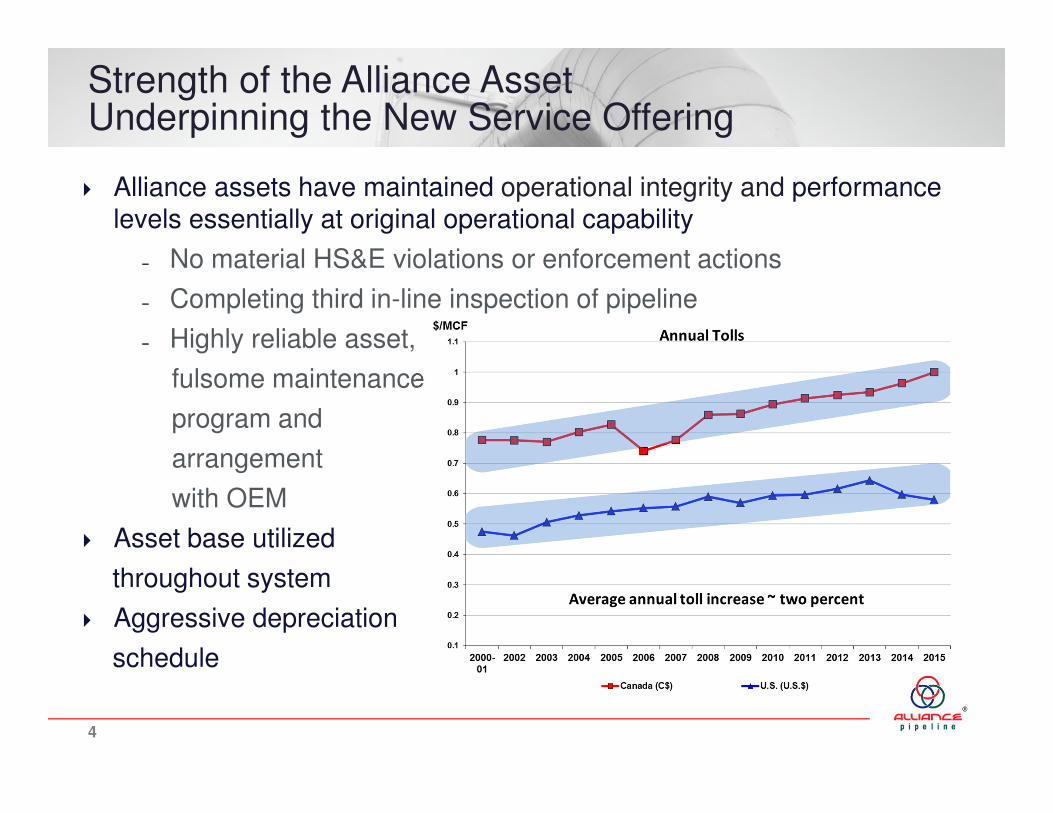

Strength of the Alliance AssetUnderpinning the New Service Offering

� Alliance assets have maintained operational integrity and performance levels essentially at original operational capability

˗ No material HS&E violations or enforcement actions

˗ Completing third in-line inspection of pipeline

˗ Highly reliable asset,

fulsome maintenance

program and

arrangement

with OEM

� Asset base utilized

throughout system

� Aggressive depreciation

schedule

4

Competitive Advantages

� Unique and growing Natural Gas Liquid (“NGL”) transport capability

– Only pipe carrying natural gas and NGLs to U.S.

– Ability for producers to optimize field capital requirements and time to market

� Responsive new services framework

– Manage contract duration and staging, choose rich gas services and have toll certainty over contract term

� Connected to growing rich gas supply regions

� Value add of Aux Sable access to U.S. NGL markets

5

Competitive Advantages

� Access to growing demand markets

– Evolving U.S. Midwest gas market

– Growing U.S. NGL demand and export capacity

� Complementary rich gas bridge to potential B.C. Liquefied Natural Gas (“LNG”) export facilities

� Alliance Chicago Exchange (“ACE”) services provide value during market events

Strategically positioned rich gas pipeline providing

timely and economic access to premium markets

6

US MidwestMarket Hub

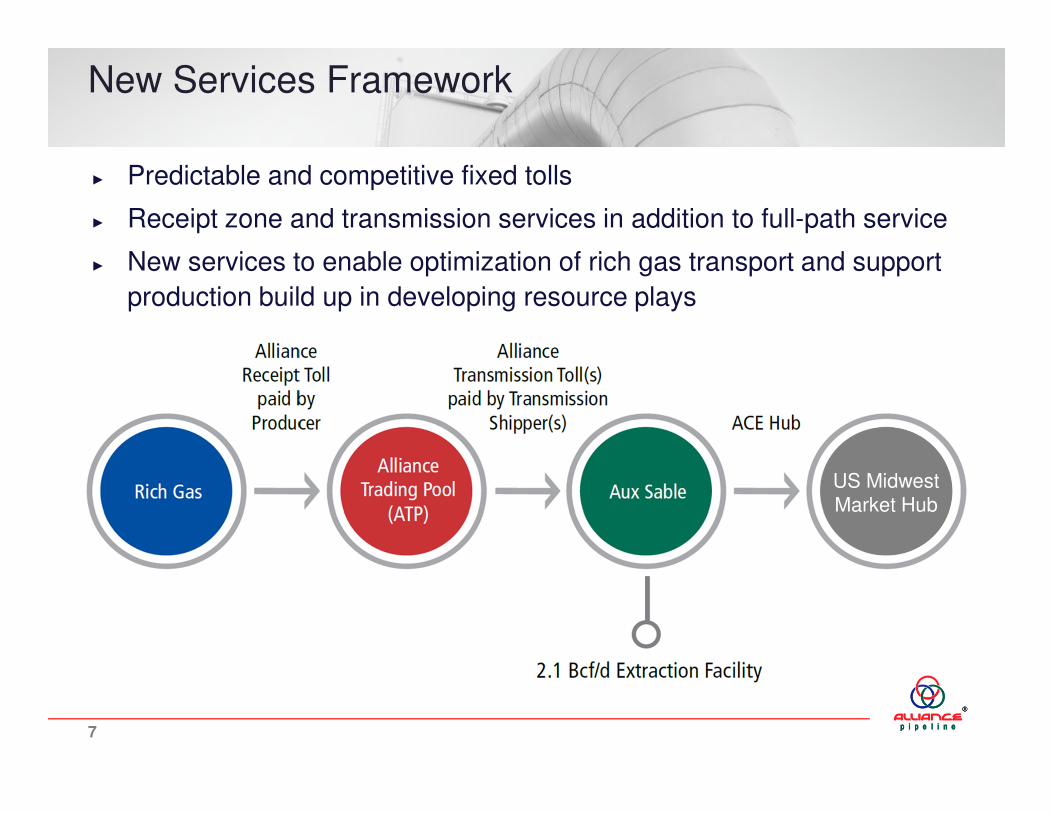

New Services Framework

► Predictable and competitive fixed tolls

► Receipt zone and transmission services in addition to full-path service

► New services to enable optimization of rich gas transport and support

production build up in developing resource plays

7

National Energy Board (“NEB”) Application for New Services

� Application Filed May 22, 2014

– General Terms and Conditions, Service Agreements, and Toll Schedules

– Fixed tolls for long-term firm receipt, delivery, and full path services

– Interruptible and Seasonal Firm Service (with full tolling flexibility)

– Hydrocarbon Dewpoint (“HCDP”) specification revised to -5°C

� NEB issued Hearing Order on August 20, 2014, adopting Alliance’s request for a written hearing format

– Five rounds of Information Requests from NEB and two rounds from Intervenors have been completed

– Alliance filed Reply Evidence on April 1, 2015.

– Oral Final Argument scheduled for April 15 – 16, 2015

– NEB decision expected mid-July 2015

� Alliance plans to file application with Federal Energy Regulatory Commission (“FERC”) in June 2015

8

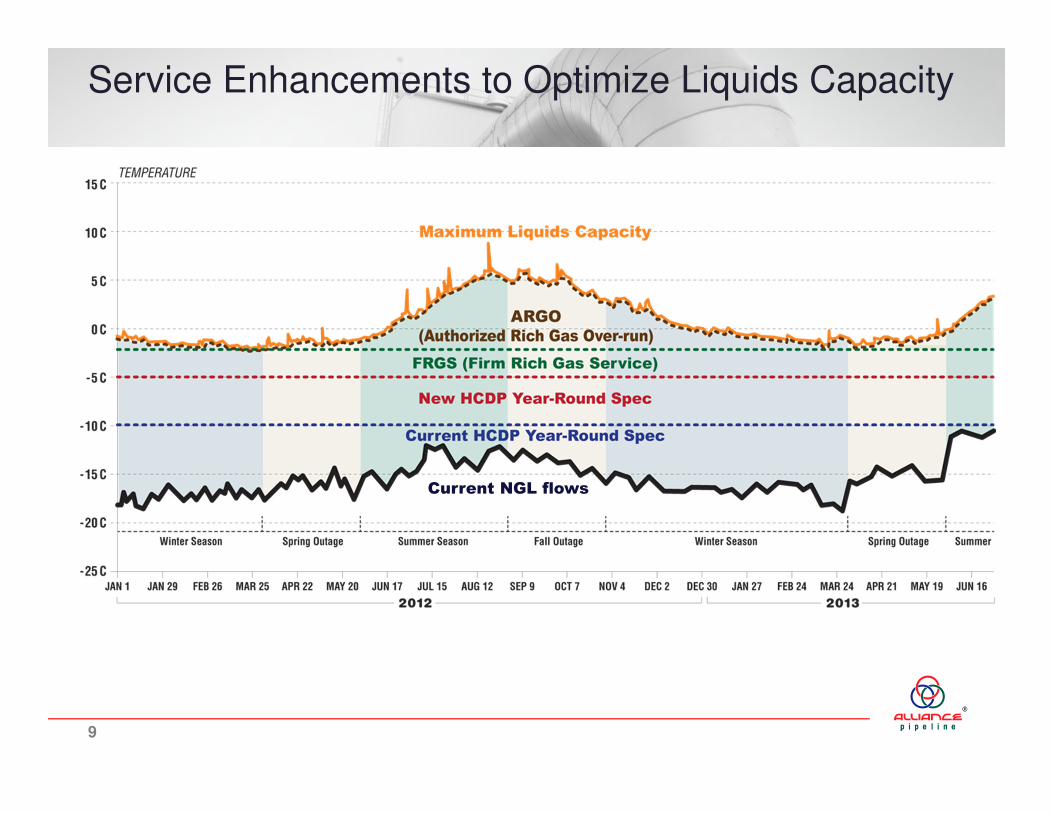

Service Enhancements to Optimize Liquids Capacity

Current NGL flows

9

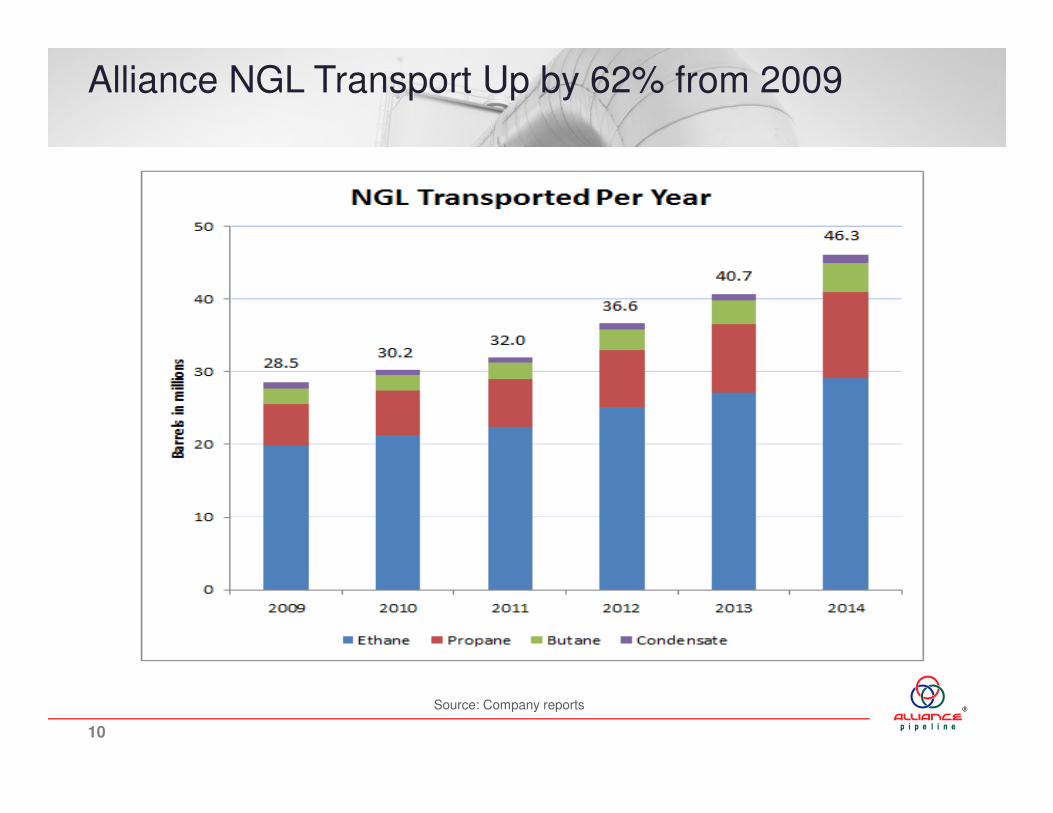

Alliance NGL Transport Up by 62% from 2009

Source: Company reports

10

Aux Sable adds Fractionation Capacity

� $130 million expansion will add 24,500 barrels a day in processing capacity

� Target in service date is mid-2016 and will be supported by Rich Gas Premium agreements

� Indicative that Alliance’s owners expect even more rich gas to flow on Alliance post 2015

11

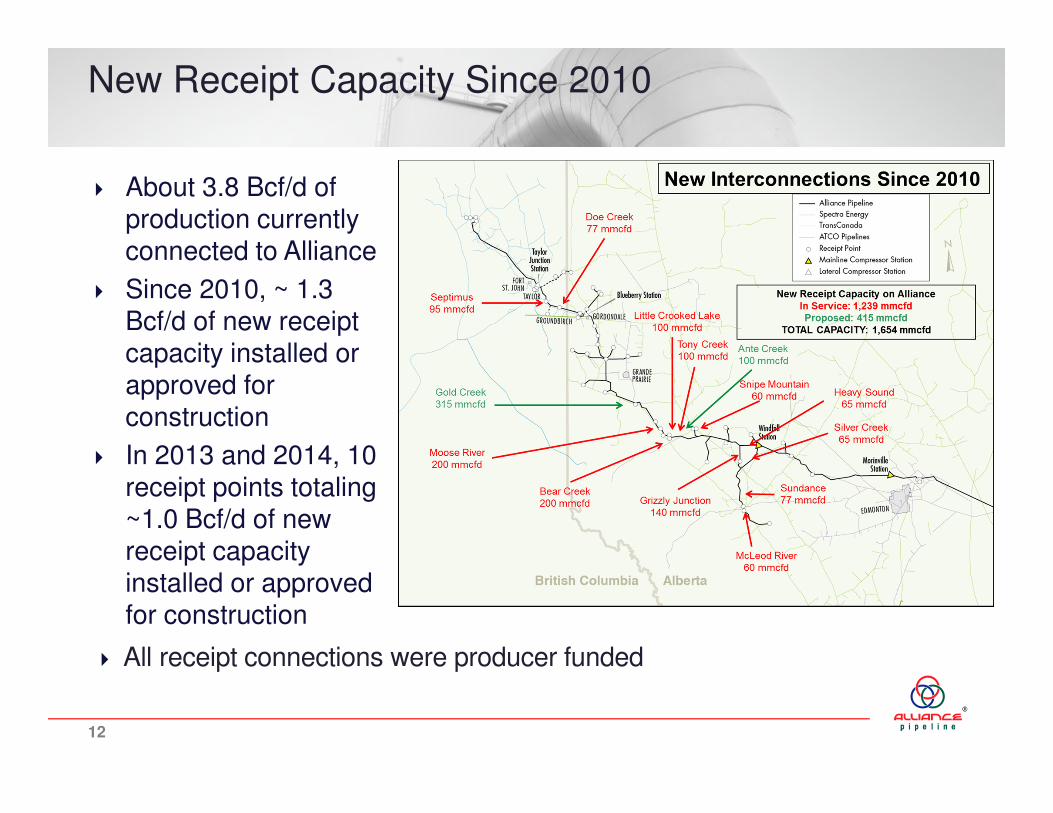

New Receipt Capacity Since 2010

� About 3.8 Bcf/d of production currently connected to Alliance

� Since 2010, ~ 1.3 Bcf/d of new receipt capacity installed or approved for construction

� In 2013 and 2014, 10 receipt points totaling ~1.0 Bcf/d of new receipt capacity installed or approved for construction

� All receipt connections were producer funded

12

Canadian Shipper Progression

� 2013 & 2014 were focused on attracting new rich gas supply to the pipe

– Producers seeing benefits of capital avoidance, staging commitments, rich gas flexibility and time to market

– Significant Montney and Duvernay interest

� Alliance is pleased with progress to date and NGL content of the executed deals

– No available capacity in Zone 1

– Less than 2% of target capacity available in Zone 2

� 2015 has seen increased engagement of downstream transmission zone shippers

13

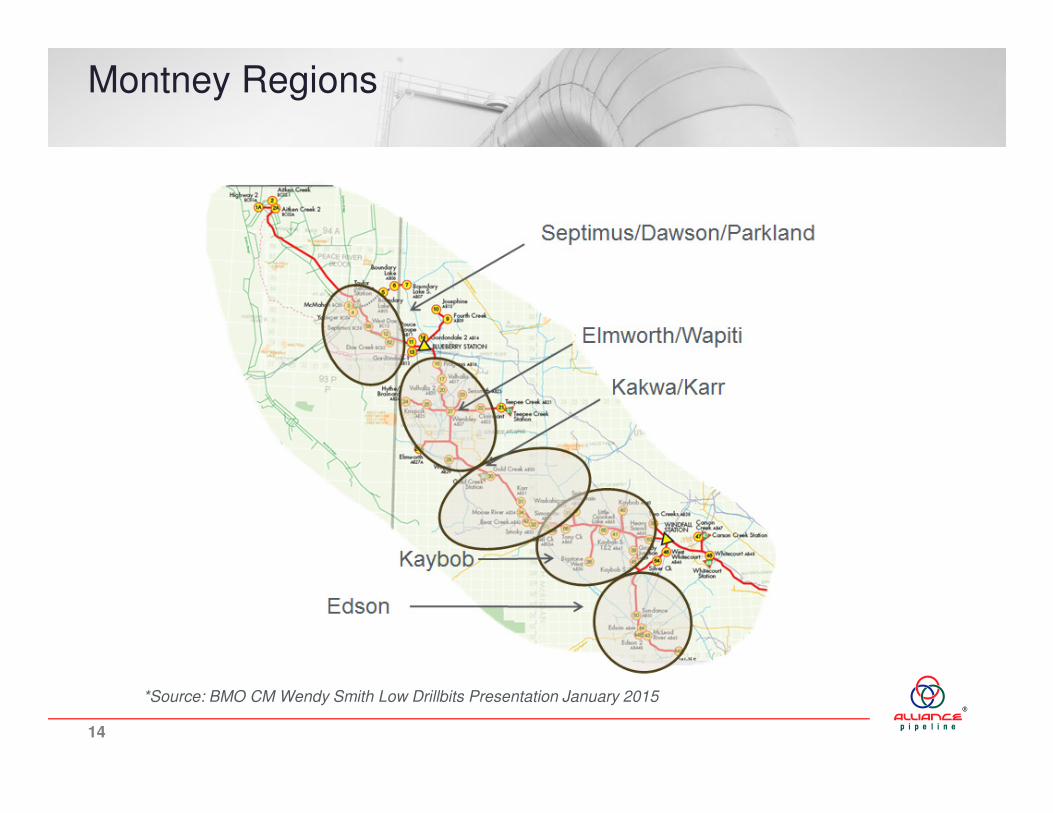

Montney Regions

*Source: BMO CM Wendy Smith Low Drillbits Presentation January 2015

14

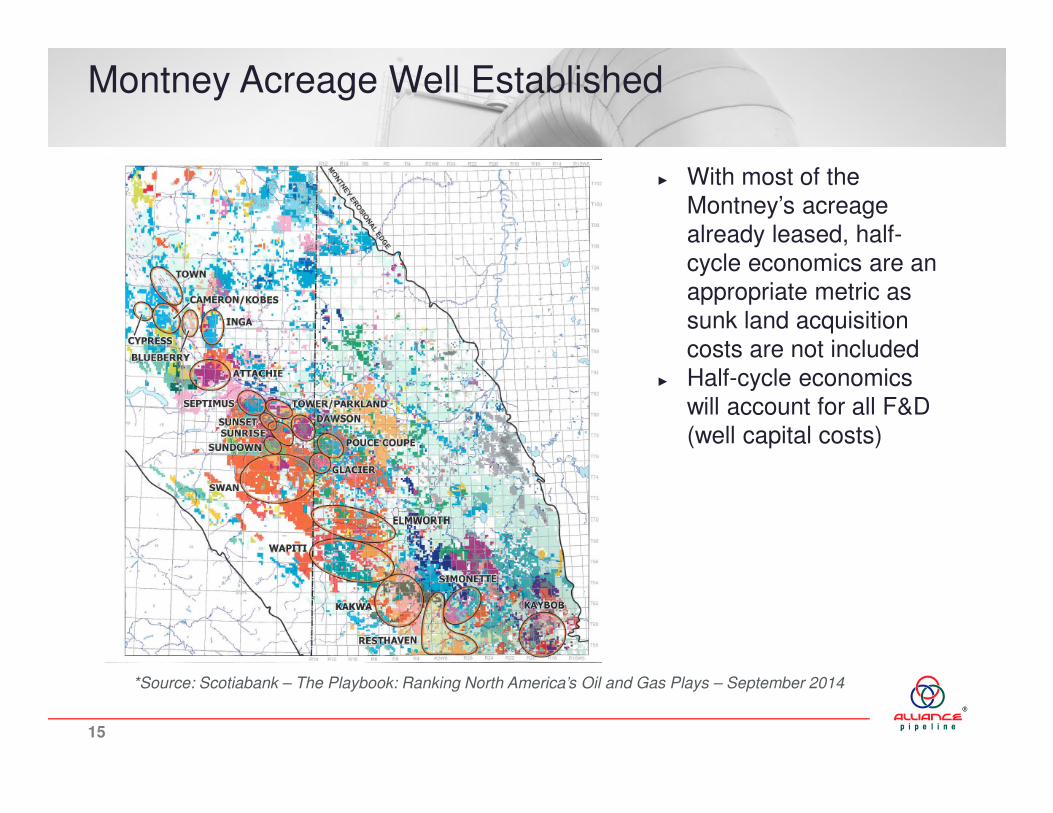

Montney Acreage Well Established

► With most of the Montney’s acreage already leased, half-cycle economics are an appropriate metric as sunk land acquisition costs are not included

► Half-cycle economics will account for all F&D (well capital costs)

*Source: Scotiabank – The Playbook: Ranking North America’s Oil and Gas Plays – September 2014

15

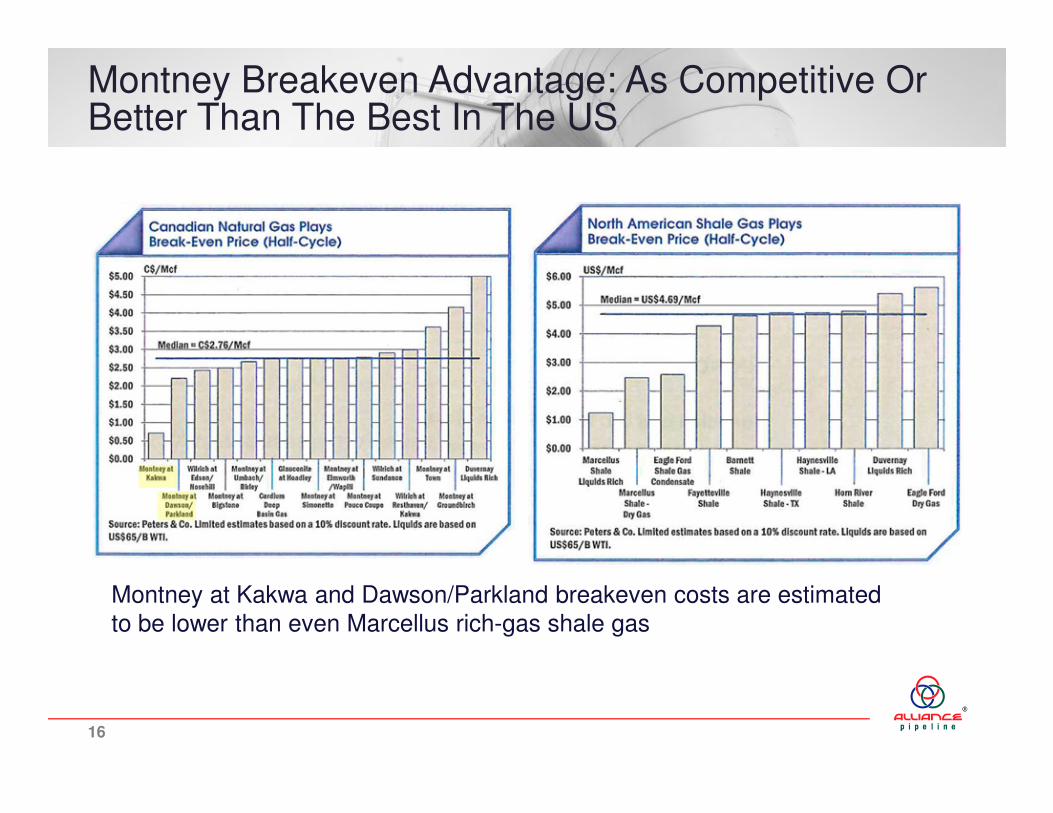

Montney Breakeven Advantage: As Competitive Or Better Than The Best In The US

Montney at Kakwa and Dawson/Parkland breakeven costs are estimated to be lower than even Marcellus rich-gas shale gas

16

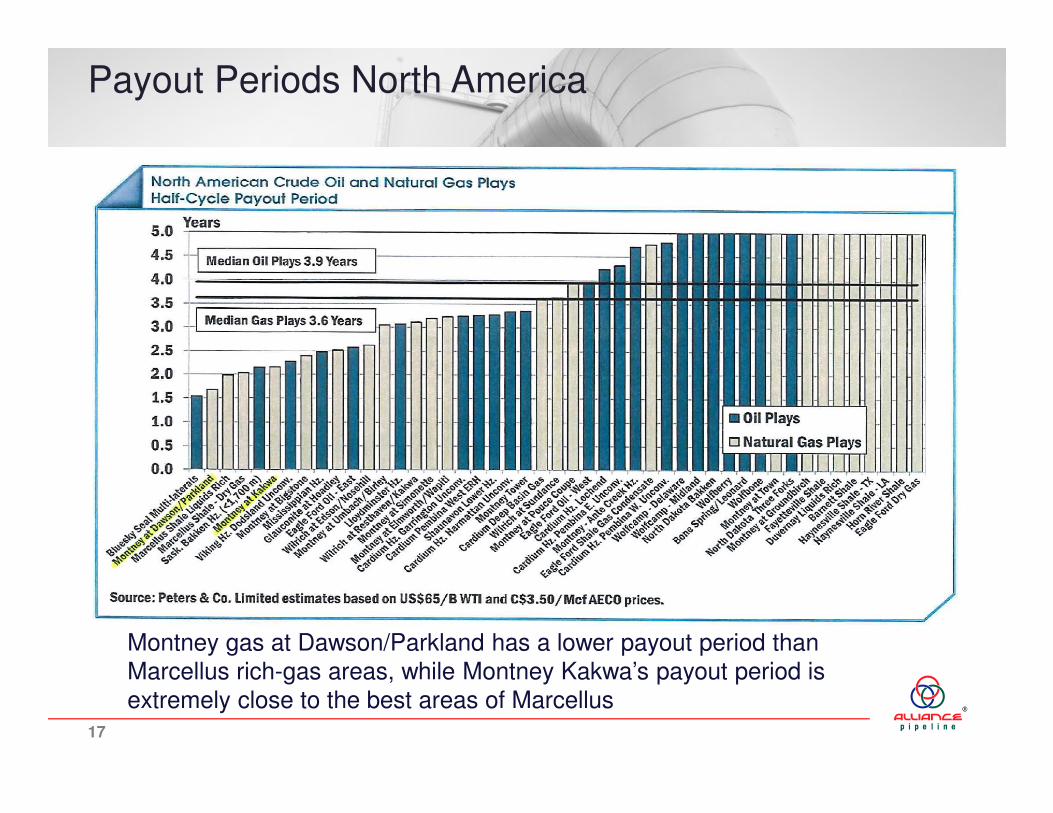

Payout Periods North America

Montney gas at Dawson/Parkland has a lower payout period than Marcellus rich-gas areas, while Montney Kakwa’s payout period is extremely close to the best areas of Marcellus

17

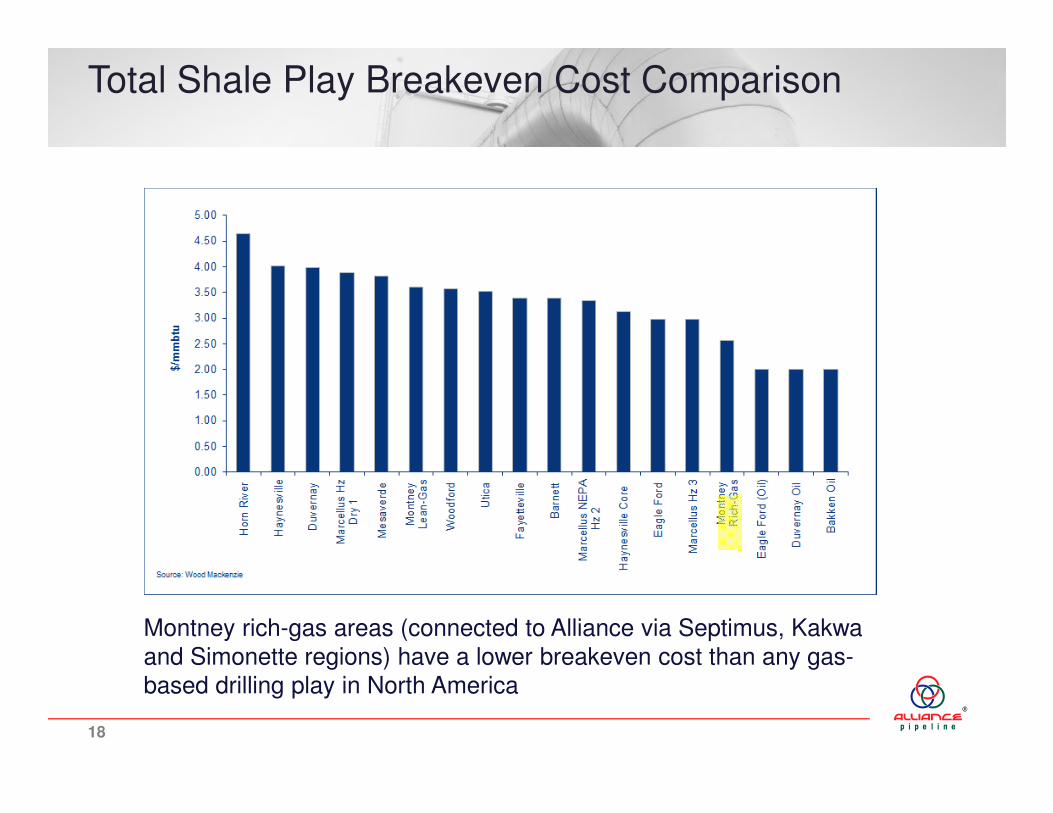

Total Shale Play Breakeven Cost Comparison

Montney rich-gas areas (connected to Alliance via Septimus, Kakwa and Simonette regions) have a lower breakeven cost than any gas-based drilling play in North America

18

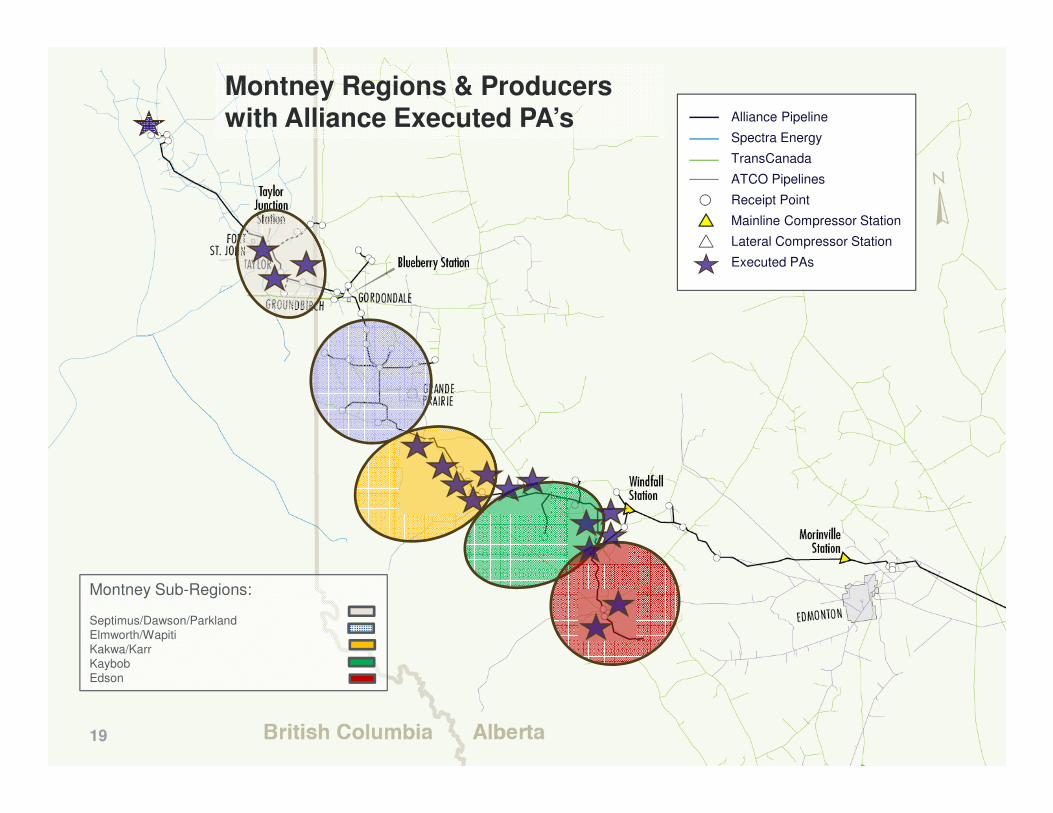

Montney Sub-Regions:

Septimus/Dawson/ParklandElmworth/WapitiKakwa/KarrKaybobEdson

Montney Regions & Producers with Alliance Executed PA’s Alliance Pipeline

Spectra Energy

TransCanada

ATCO Pipelines

Receipt Point

Mainline Compressor Station

Lateral Compressor Station

Executed PAs

19

Immediate and Economic Bridge for LNG Facilities

� Alliance an existing, economic solution with immediate access to market

� Capital avoidance and predictable rich gas transportation through 2020 and beyond

� First B.C. LNG projects still awaiting investment decisions

� Optionality while LNG outcomes get sorted

� Long-term market portfolio alternative for rich gas plays

� Increasing exports from U.S. Gulf Coast

20

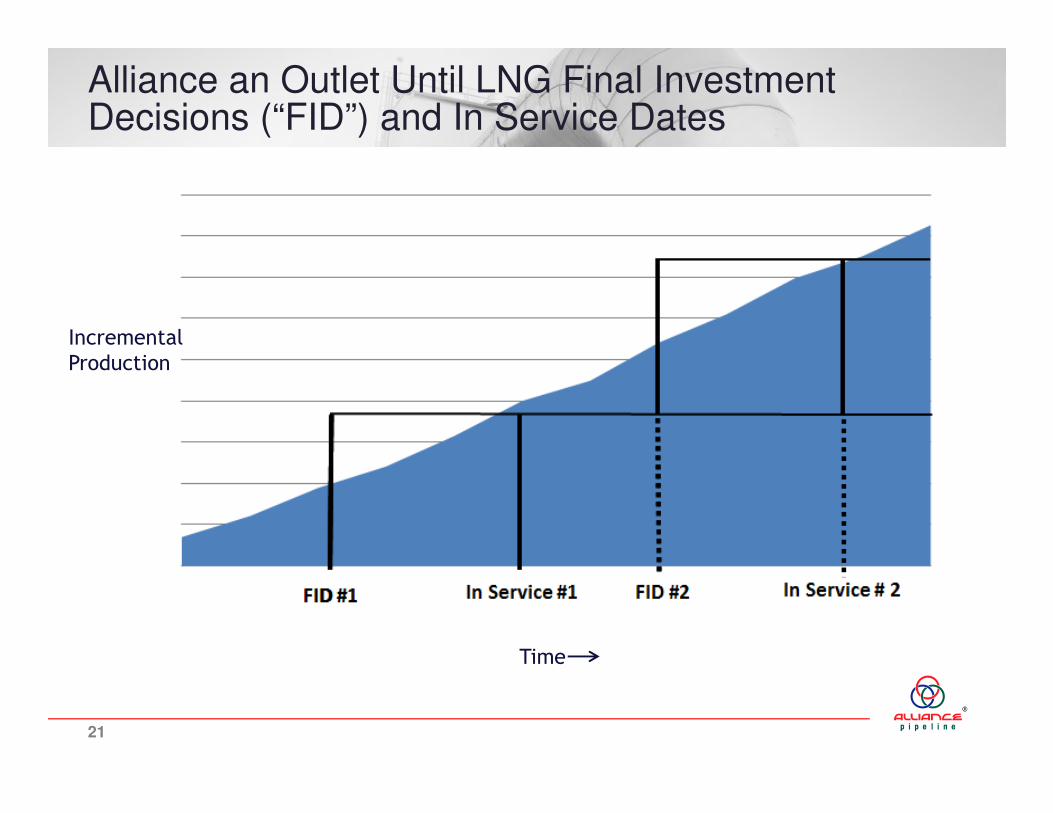

Alliance an Outlet Until LNG Final Investment Decisions (“FID”) and In Service Dates

Incremental

Production

Time

21

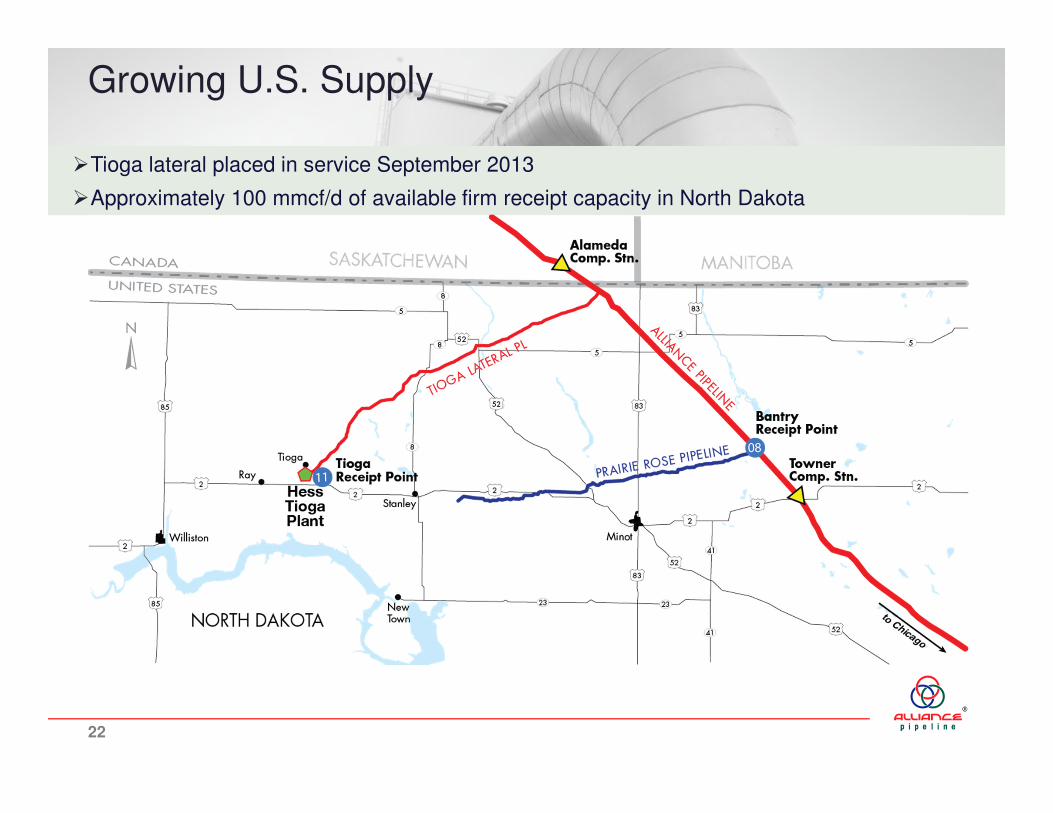

Growing U.S. Supply

�Tioga lateral placed in service September 2013

�Approximately 100 mmcf/d of available firm receipt capacity in North Dakota

22

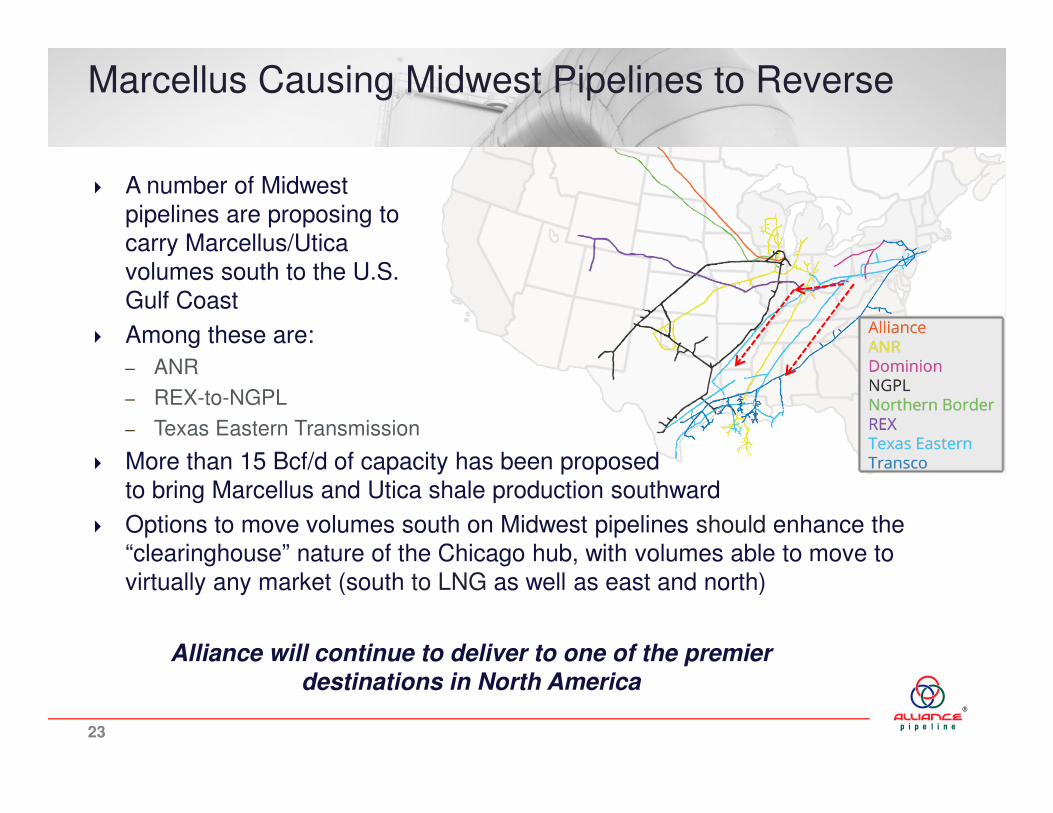

Marcellus Causing Midwest Pipelines to Reverse

� A number of Midwest pipelines are proposing to carry Marcellus/Utica volumes south to the U.S. Gulf Coast

� Among these are:

– ANR

– REX-to-NGPL

– Texas Eastern Transmission

� More than 15 Bcf/d of capacity has been proposed to bring Marcellus and Utica shale production southward

� Options to move volumes south on Midwest pipelines should enhance the “clearinghouse” nature of the Chicago hub, with volumes able to move to virtually any market (south to LNG as well as east and north)

Alliance will continue to deliver to one of the premier destinations in North America

23

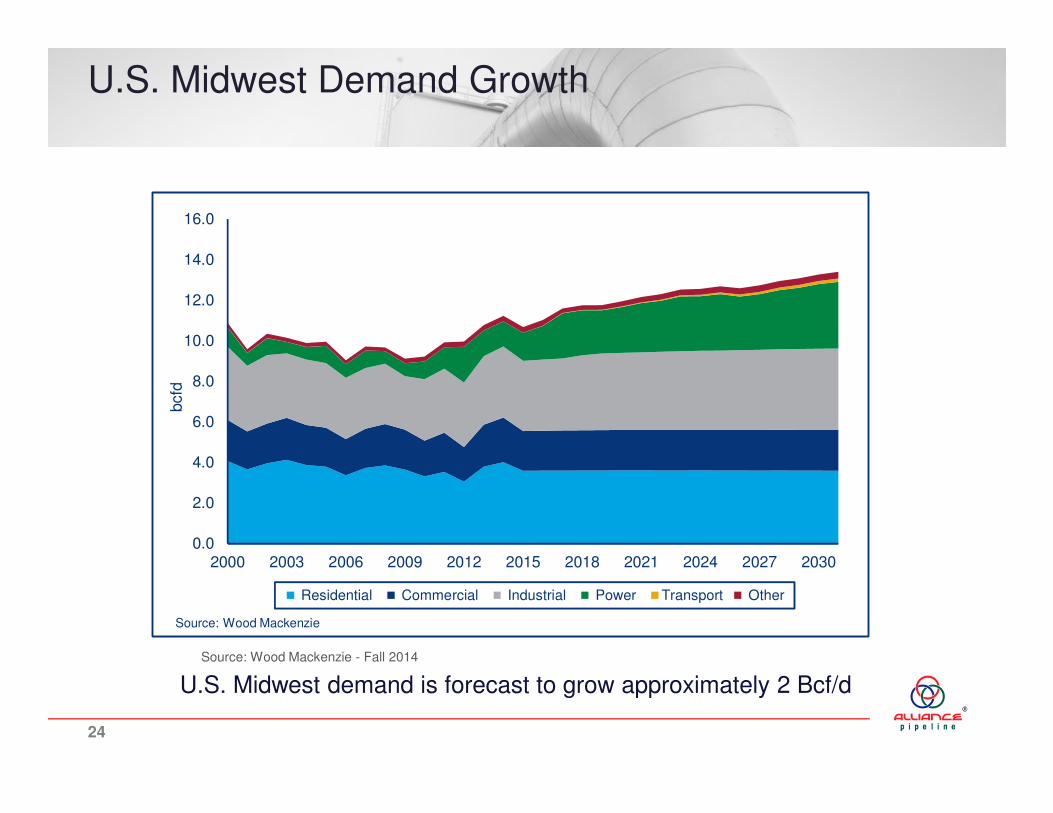

U.S. Midwest Demand Growth

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030

bcfd

Residential Commercial Industrial Power Transport Other

Source: Wood Mackenzie

Source: Wood Mackenzie - Fall 2014

U.S. Midwest demand is forecast to grow approximately 2 Bcf/d

24

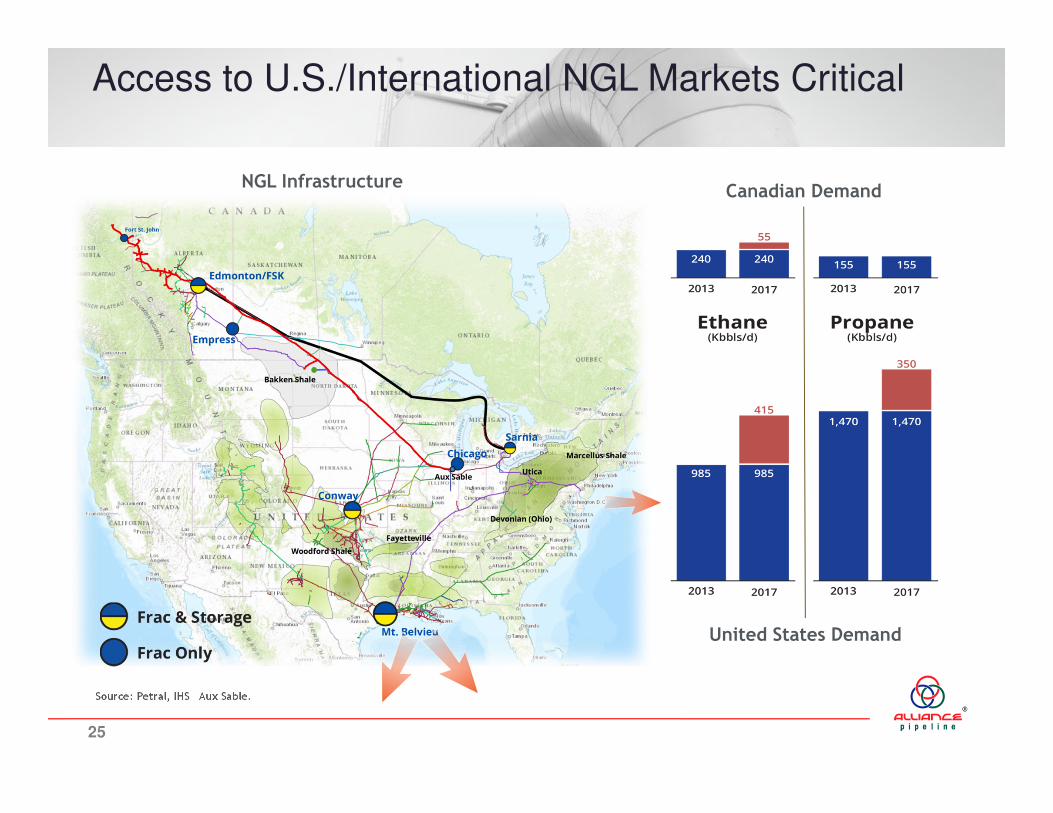

2012

Source: Petral, IHS Aux Sable.

Canadian Demand

United States Demand

NGL Infrastructure

Access to U.S./International NGL Markets Critical

25

Summary

� Customer-oriented approach

� Rich gas advantage, focus capital on the drill bit

� Flexible suite of toll and service options providing access to premium markets

� “Known cost” and contract terms provide optionality

� Immediate and economic bridge for LNG facilities

� Re-contracting efforts are progressing well

26

Contacts

www.alliancepipeline.com

Keith PalmerSenior Vice President & CFODirect: (403) 517-6369Email: [email protected]

Kevin SundvallTreasurerDirect: (403) 517-7711Email: [email protected]

Terrance KutrykPresident & CEODirect: (403) 517-6500Email: [email protected]

27

� Hydrocarbon Dewpoint (“HCDP”) Change

– HCDP tariff specification rises to -5°C (23°F) from -10°C (14°F)

– Enables greater access to Alliance’s liquids carrying capability

– Only long haul, natural gas pipeline shipping to U.S. at -5°C HCDP

� Flexible, full-path and segmented tolling options

– Fixed, term differentiated firm tolls

– Index based tolls offering basis sharing for terms greater than five years

– Flexible pricing for interruptible services and seasonal services

Supplemental InformationNew Services Offering

28

Supplemental InformationNew Services Offering

� Firm Rich Gas Service (“FRGS”)

– Allows shippers to flow gas hotter than -5°C year round

– Customers can ship gas with more liquids than specification

– Surcharge of 1¢ for each °C/mcf in excess of -5°C

– Offered on a first-come, first-served basis

� Shipper Paired Gas (“SPG”)

– Shippers of lean and rich gas pair to meet HCDP specification

– Alliance can help facilitate pairing

– Eliminates need for pre-pipeline gas processing facilities

– Creates value proposition for lean gas

29

Supplemental InformationNew Services Offering

� Authorized Rich Gas Overrun (“ARGO”)

– Optimal system conditions and warm temperatures enable shipments of hotter gas (above -5°C)

– When conditions allow, shippers could flow additional hot gas

– Posted / offered daily as available

– Value-add opportunity for shippers, offered free of charge

� Priority Interruptible Transportation Service (“PITS”)

– Available for firm receipt and full path shippers with 3+ year terms at contracted receipt point

– Provides for an additional 25% of firm contracted capacity to be utilized as PITS

– Scheduled after firm service but before Interruptible Transportation (“IT”)

– First 10% at 110% of associated firm service toll, further 15% available at 125% of associated firm service toll

30

Supplemental InformationNew Services Offering

� Staging of Contracted Capacity

– Available to firm receipt service and firm full path service shippers that:

• Have firm service terms of five years or more

• An aggregate contracted capacity averaging at least 1,400 103m3/d over contracted term (~50 mmcf/d)

– Allow for staging of contract volumes to match production targets

– Pay a weighted average toll over term of transportation service agreements utilizing 1, 3 and 5 year tolls as applicable

� Alliance Trading Pool and Ace Hub Services

– Enables other market participants to transact on the pipe

– Broadens customer base and economic opportunities for shippers

31

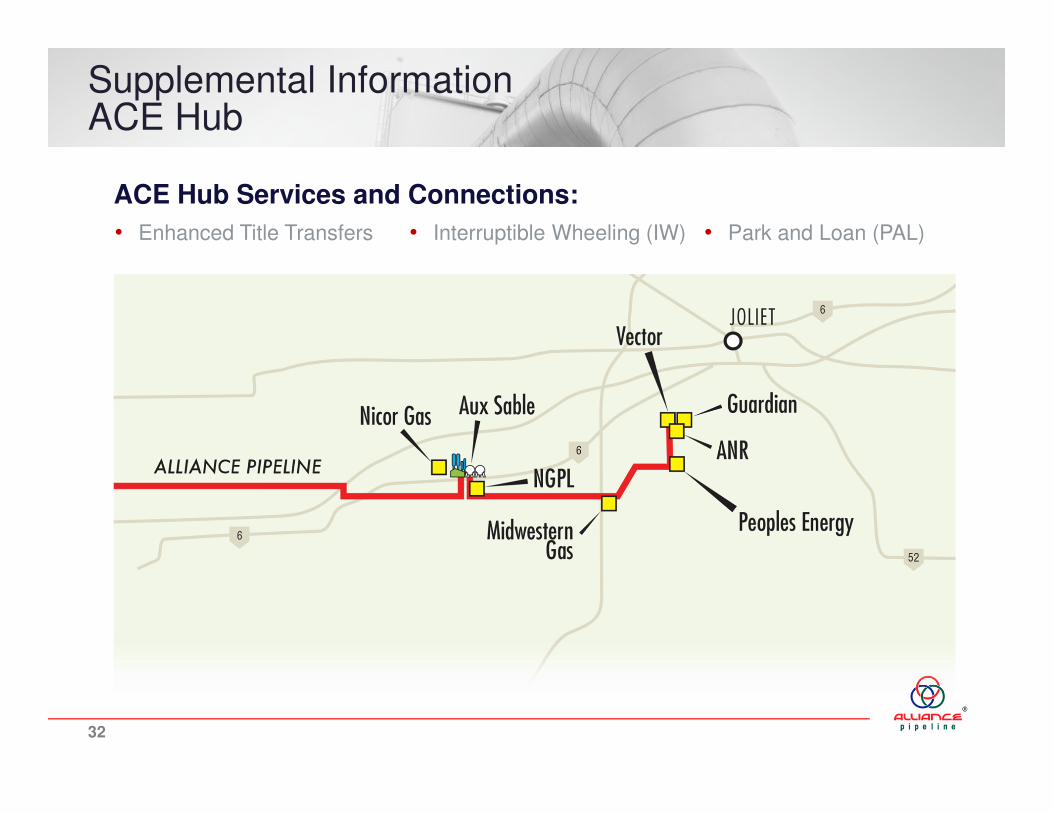

Supplemental InformationACE Hub

ACE Hub Services and Connections:

• Enhanced Title Transfers • Interruptible Wheeling (IW) • Park and Loan (PAL)

32