Embed Size (px)

Citation preview

Chp 2foreign exchange parity

relations

organization

Foreign exchange fundamentals, in particular the balance of payment and foreign exchange regimes

International parity relations

Forex Fundamental Balance of payments it tracks all financial flows crossing a country’s borders

during a given period (one year). it is an accounting of all cash flows between residents

and nonresidents of a country.Conventions: treat all inflows (exports or sale of domestic

assets) as a credit to the BOP.International transaction are grouped into 2 main

categories Current account Financial account

Current account

Covers all current transaction that take place in the normal business of residents of a country, and be dominated by the trade balance, the balance of all exports and imports. CA is made up of Exports and imports of goods (trade balance) Services income (interest, dividends, and various investment

income from cross-border investments) Current transfer (gift and other flows without quid pro

quo compensation)

Financial account

Covers investments by residents abroad and investments by nonresidents in the home country, it includes Direct investments made by companies Portfolio investments in equity, bonds, and

other securities of any maturity Other investments and liabilities (deposits or

borrowing with foreign bank and vice versa)

CA+FA=overall balance IF overall balance is not zero, the

monetary authority must use reserve assets (official reserves) to fill the gap

As long as foreign investors are willing to finance this difference by net capital flows into the country, the trade deficits poses no economic problem.

CA<0 depreciation of home currency

FA>0 appreciation of home currency

as a result, the two effects can cancel each other

Frequently, CA deficit can be deemed as bad politically.

External financing of a country also increases the risk of crisis

CA deficits is bad?

Factors that affect Forex rate

In a flexible exchange rate system, the value of a currency is driven by changes in fundamental economic factors, amongst the factors are Differences in national inflation rates Changes in real interest rates Differences in economic performance Changes in investment climate

Effect of Government policies on Forex and BOP

Monetary policy and Forex rate

an expansionary monetary policy will lead to a depreciation of the home currency, while a restrictive monetary policy will lead to an appreciation of the home currency

Fiscal policy and Forex rate many economists believe that the net result of a more re

strictive policy will be a depreciation of the home currency.

a more expansionary fiscal policy has the reverse effect. the reaction will be somewhat stronger if the shift in fis

cal policy is expected to be permanent rather than temporary.

Exchange rate regimes

Historically, there are three different regimes Flexible exchange rates Fixed exchange rates Pegged exchange rates

Flexible exchange rates

It is one in which the exchange rate between two currencies fluctuates freely in the foreign exchange market (government intervene only to smooth temporary imbalances).

Advantage a market-determined price that reflects economic funda

mentals at each point in time government got independent domestic monetary and fisc

al policies Decrease speculation against Forex

Disadvantage Be quite volatile and bad for agents engaged in trade

and investments

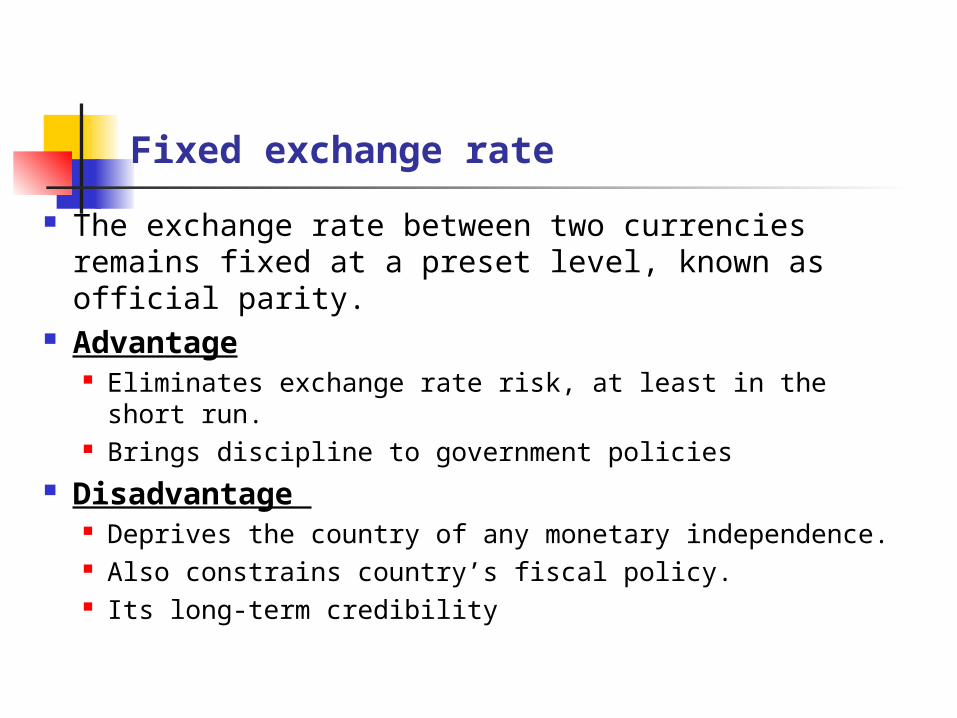

Fixed exchange rate

The exchange rate between two currencies remains fixed at a preset level, known as official parity.

Advantage Eliminates exchange rate risk, at least in the short run. Brings discipline to government policies

Disadvantage Deprives the country of any monetary independence. Also constrains country’s fiscal policy. Its long-term credibility

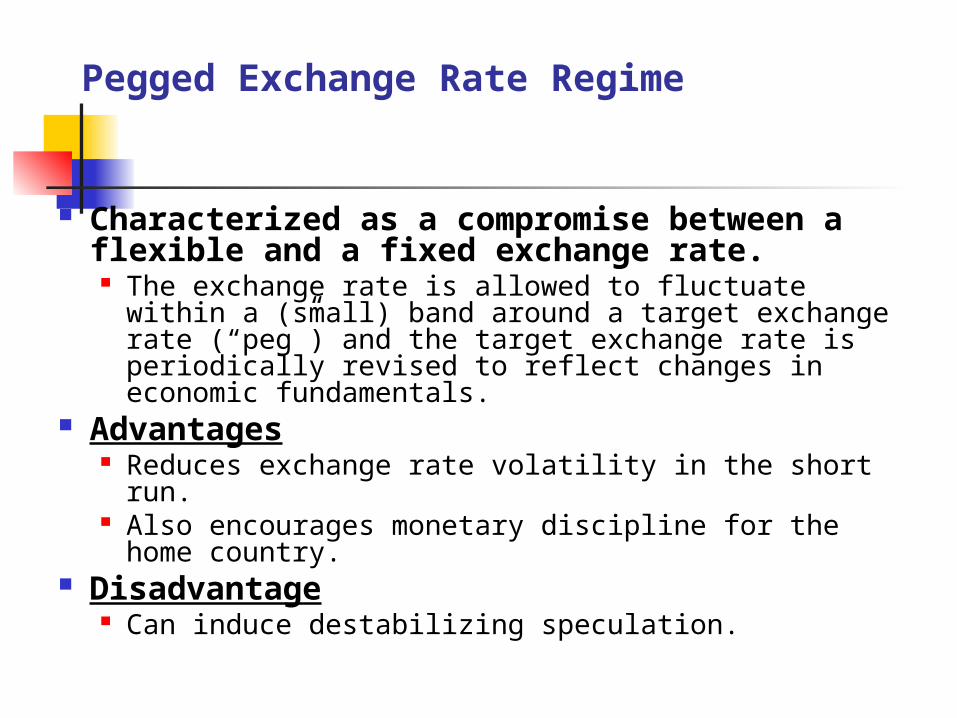

Pegged Exchange Rate Regime

Characterized as a compromise between a flexible and a fixed exchange rate. The exchange rate is allowed to fluctuate within a (small)

band around a target exchange rate (“peg”) and the target exchange rate is periodically revised to reflect changes in economic fundamentals.

Advantages Reduces exchange rate volatility in the short run. Also encourages monetary discipline for the home country.

Disadvantage Can induce destabilizing speculation.

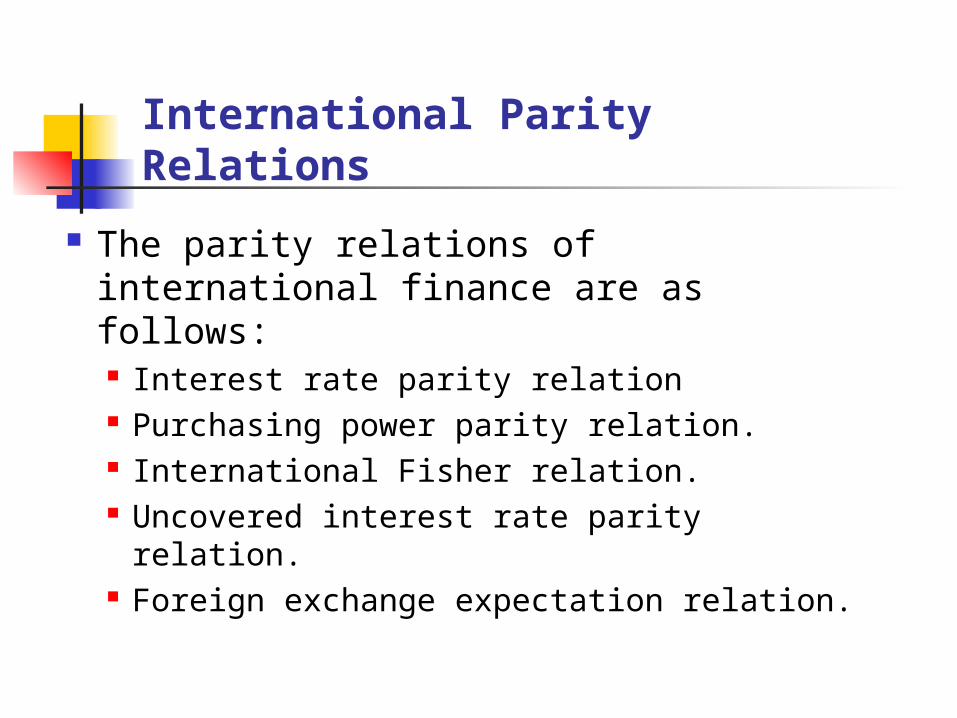

International Parity Relations

The parity relations of international finance are as follows: Interest rate parity relation Purchasing power parity relation. International Fisher relation. Uncovered interest rate parity relation. Foreign exchange expectation relation.

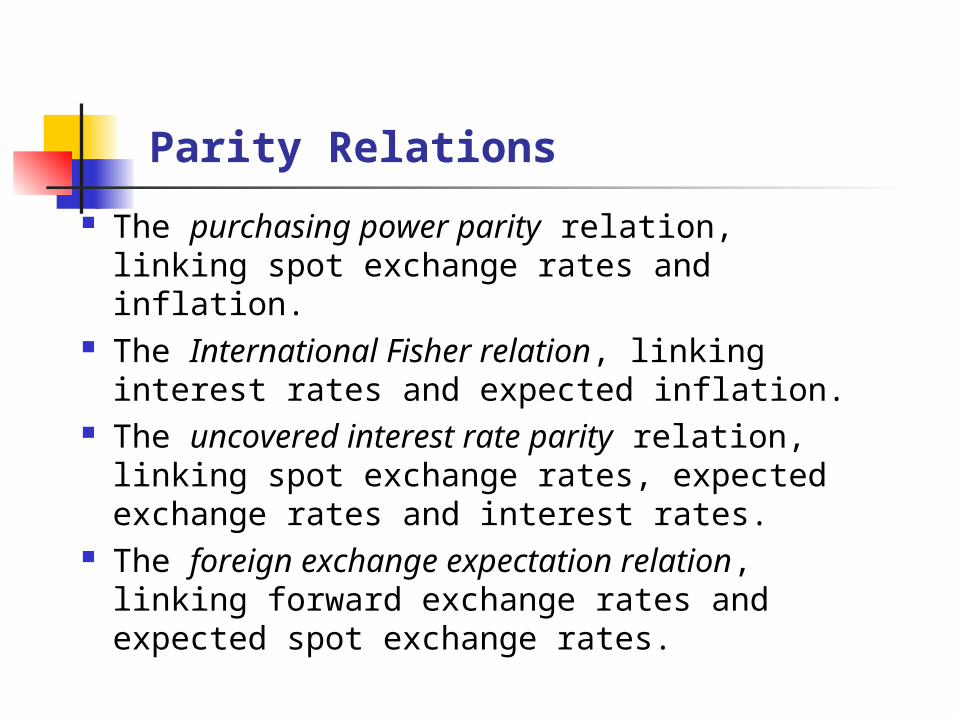

Parity Relations

The purchasing power parity relation, linking spot exchange rates and inflation.

The International Fisher relation, linking interest rates and expected inflation.

The uncovered interest rate parity relation, linking spot exchange rates, expected exchange rates and interest rates.

The foreign exchange expectation relation, linking forward exchange rates and expected spot exchange rates.

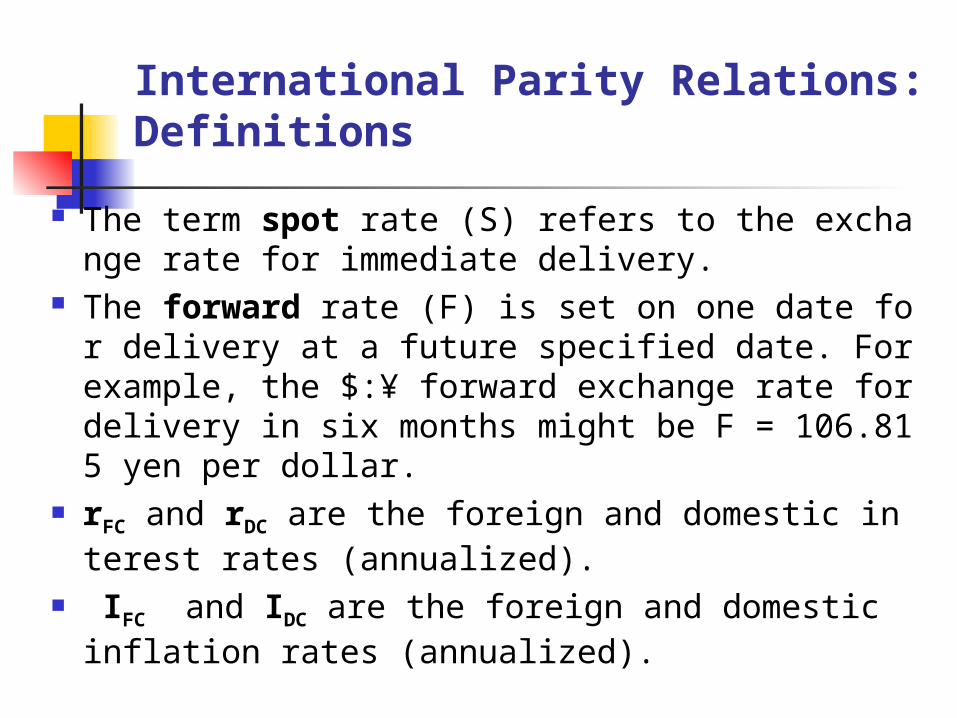

International Parity Relations: Definitions

The term spot rate (S) refers to the exchange rate for immediate delivery.

The forward rate (F) is set on one date for delivery at a future specified date. For example, the $:¥ forward exchange rate for delivery in six months might be F = 106.815 yen per dollar.

rFC and rDC are the foreign and domestic interest rates (annualized).

IFC and IDC are the foreign and domestic inflation rates (annualized).

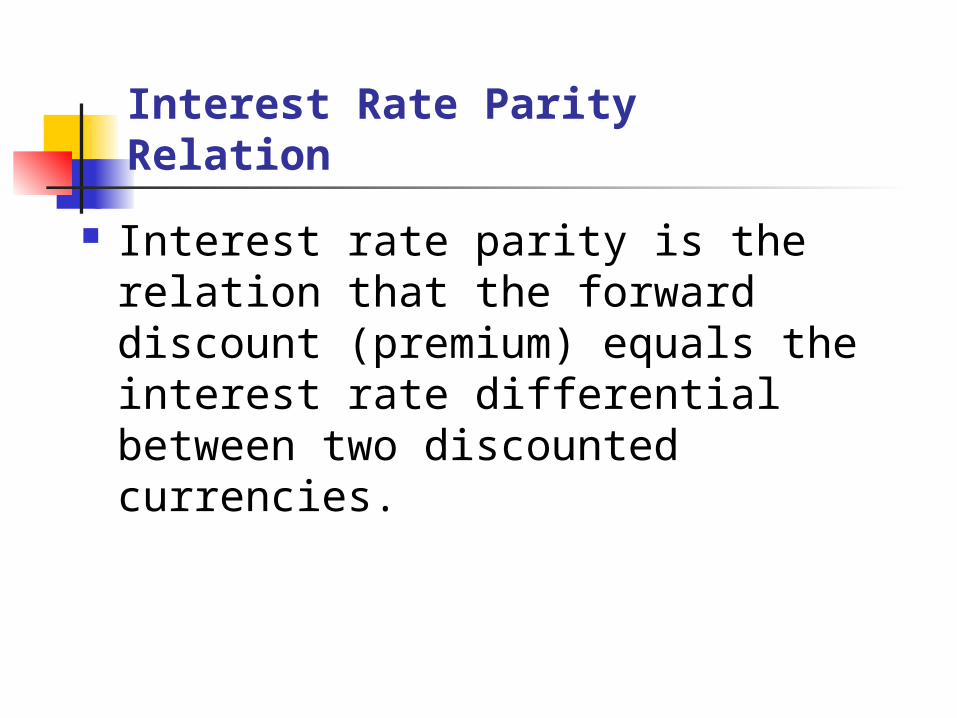

Interest Rate Parity Relation

Interest rate parity is the relation that the forward discount (premium) equals the interest rate differential between two discounted currencies.

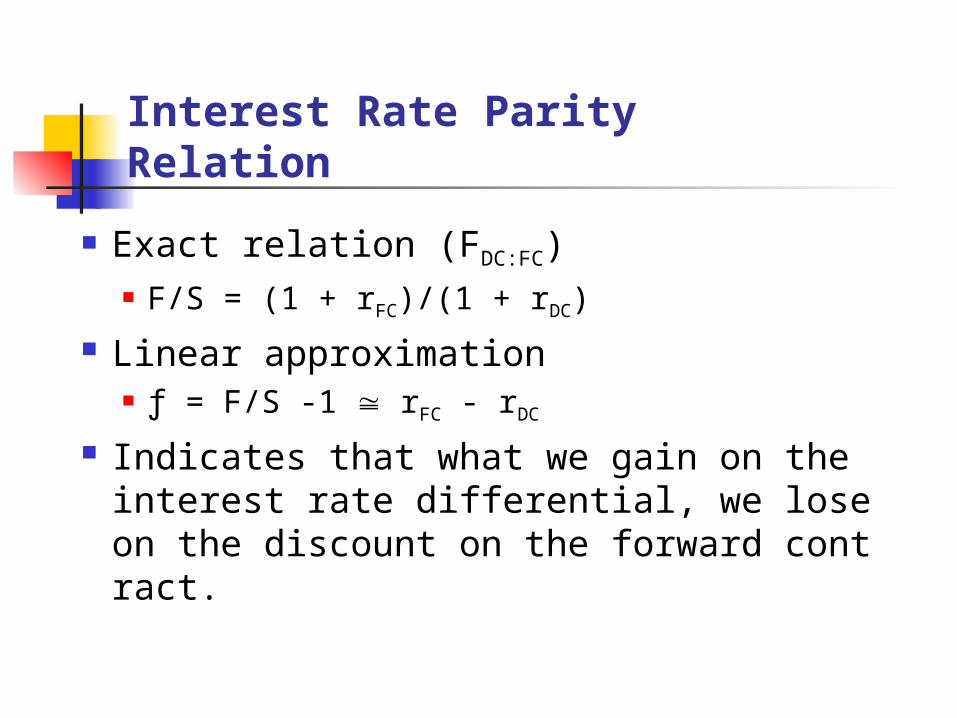

Interest Rate Parity Relation

Exact relation (FDC:FC) F/S = (1 + rFC)/(1 + rDC)

Linear approximation ƒ = F/S -1 rFC - rDC

Indicates that what we gain on the interest rate differential, we lose on the discount on the forward contract.

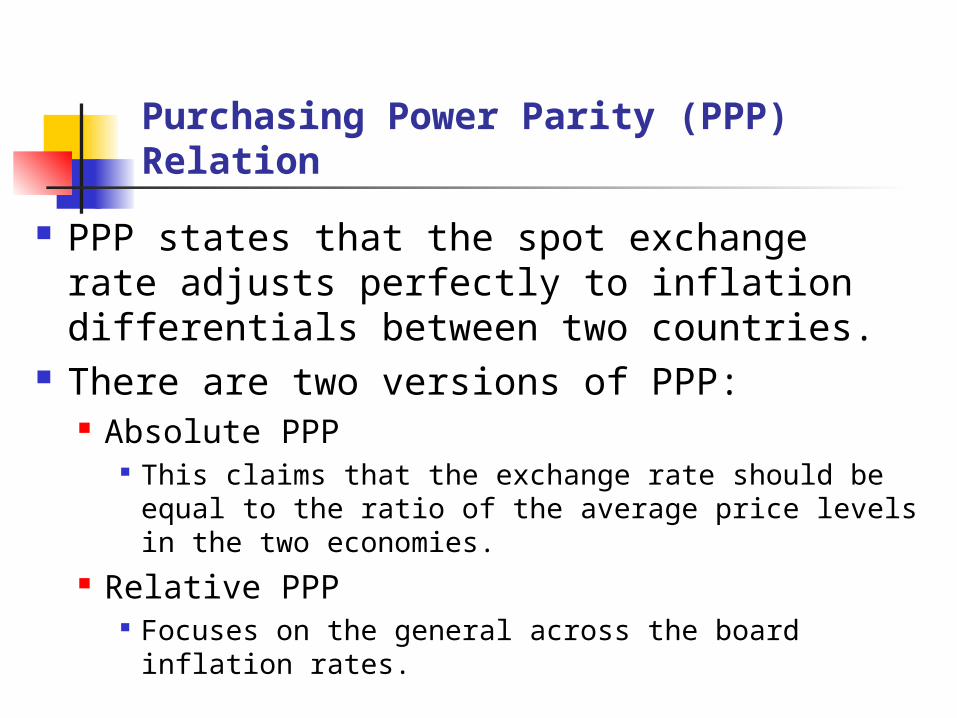

Purchasing Power Parity (PPP) Relation

PPP states that the spot exchange rate adjusts perfectly to inflation differentials between two countries.

There are two versions of PPP: Absolute PPP

This claims that the exchange rate should be equal to the ratio of the average price levels in the two economies.

Relative PPP Focuses on the general across the board inflation rates.

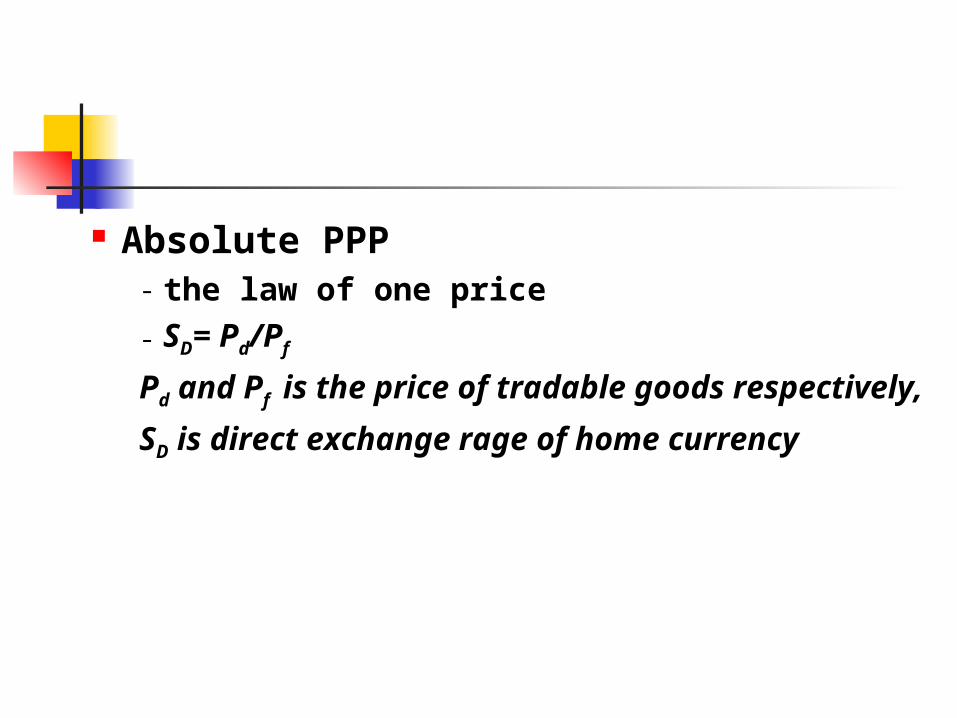

Absolute PPP the law of one price SD= Pd/Pf

Pd and Pf is the price of tradable goods respectively,

SD is direct exchange rage of home currency

Purchasing Power Parity (PPP) Relation

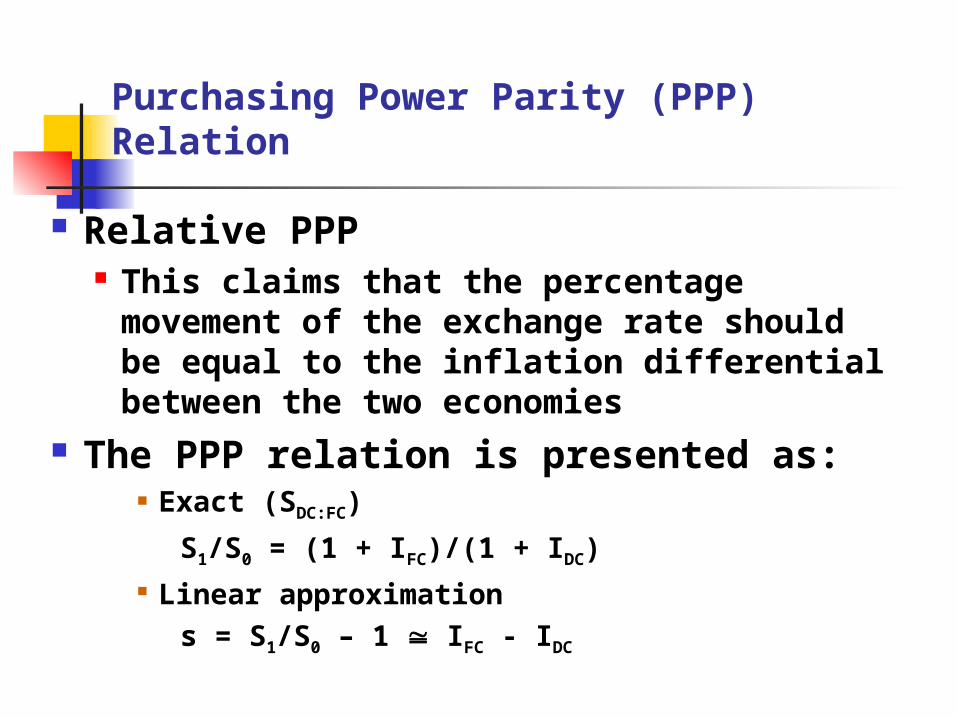

Relative PPP This claims that the percentage movement of

the exchange rate should be equal to the inflation differential between the two economies

The PPP relation is presented as: Exact (SDC:FC)

S1/S0 = (1 + IFC)/(1 + IDC) Linear approximation

s = S1/S0 – 1 IFC - IDC

Purchasing Power Parity (PPP) Relation

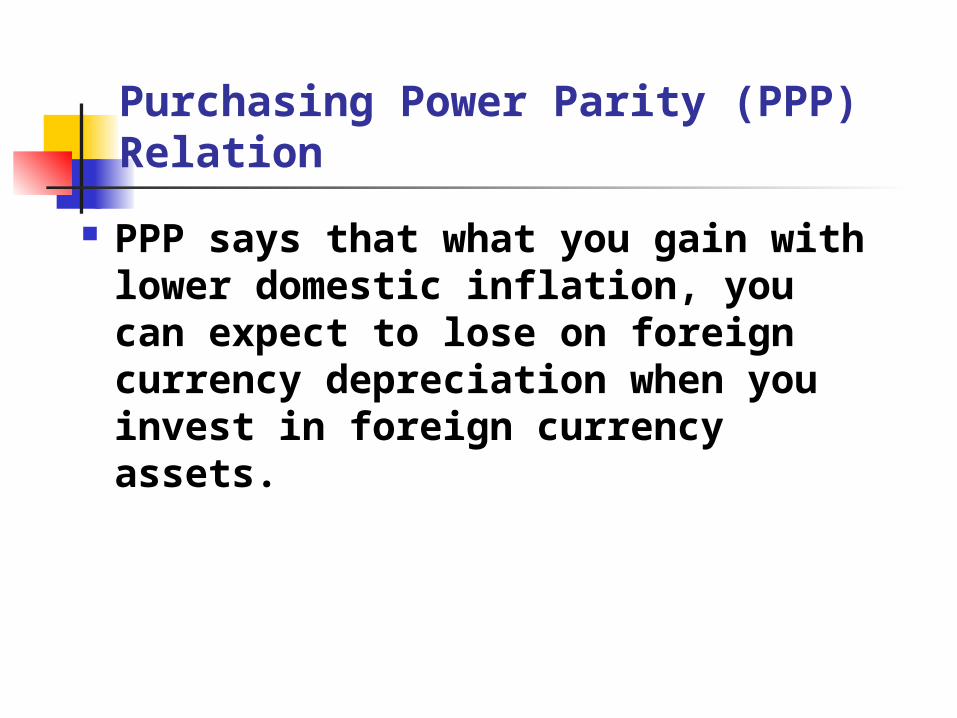

PPP says that what you gain with lower domestic inflation, you can expect to lose on foreign currency depreciation when you invest in foreign currency assets.

International Fisher Relation

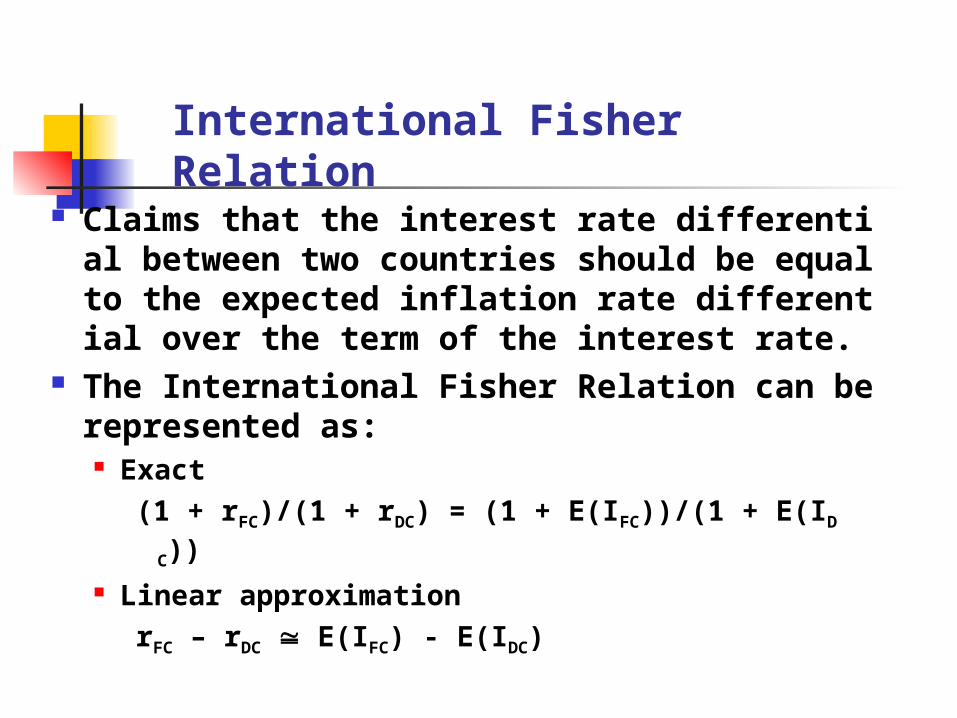

Claims that the interest rate differential between two countries should be equal to the expected inflation rate differential over the term of the interest rate.

The International Fisher Relation can be represented as: Exact

(1 + rFC)/(1 + rDC) = (1 + E(IFC))/(1 + E(IDC)) Linear approximation

rFC – rDC E(IFC) - E(IDC)

Example

Question: How are the nominal and real interest rates calculated?

Answer: Nominal interest rate is observed in the marketplace. The real interest rate is calculated from the observed interest rate and forecasted inflation.

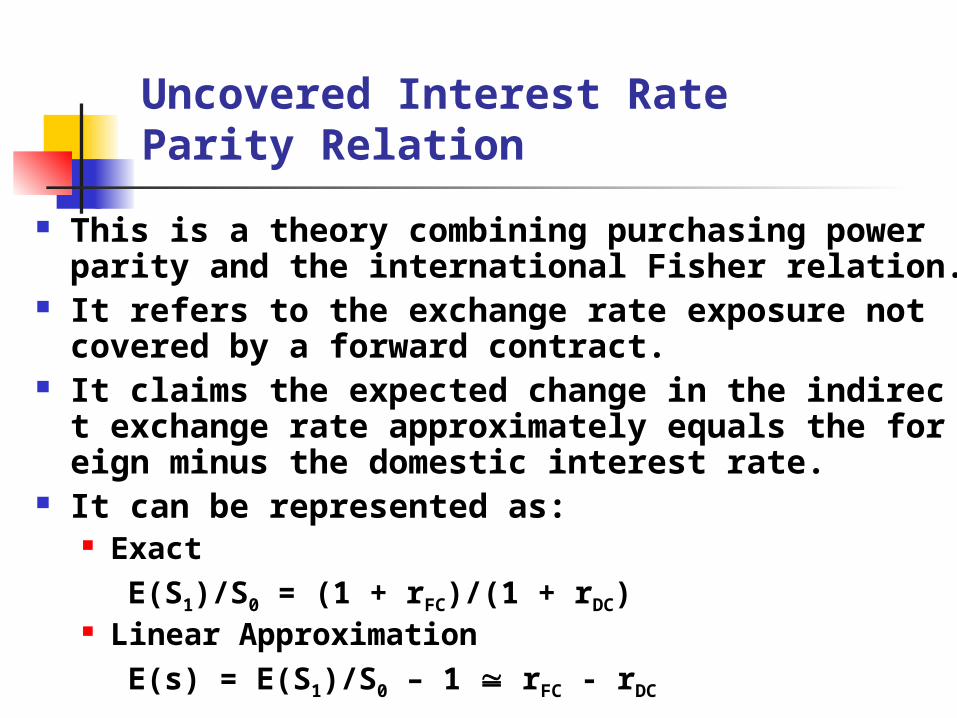

Uncovered Interest Rate Parity Relation

This is a theory combining purchasing power parity and the international Fisher relation.

It refers to the exchange rate exposure not covered by a forward contract.

It claims the expected change in the indirect exchange rate approximately equals the foreign minus the domestic interest rate.

It can be represented as: Exact

E(S1)/S0 = (1 + rFC)/(1 + rDC) Linear Approximation

E(s) = E(S1)/S0 – 1 rFC - rDC

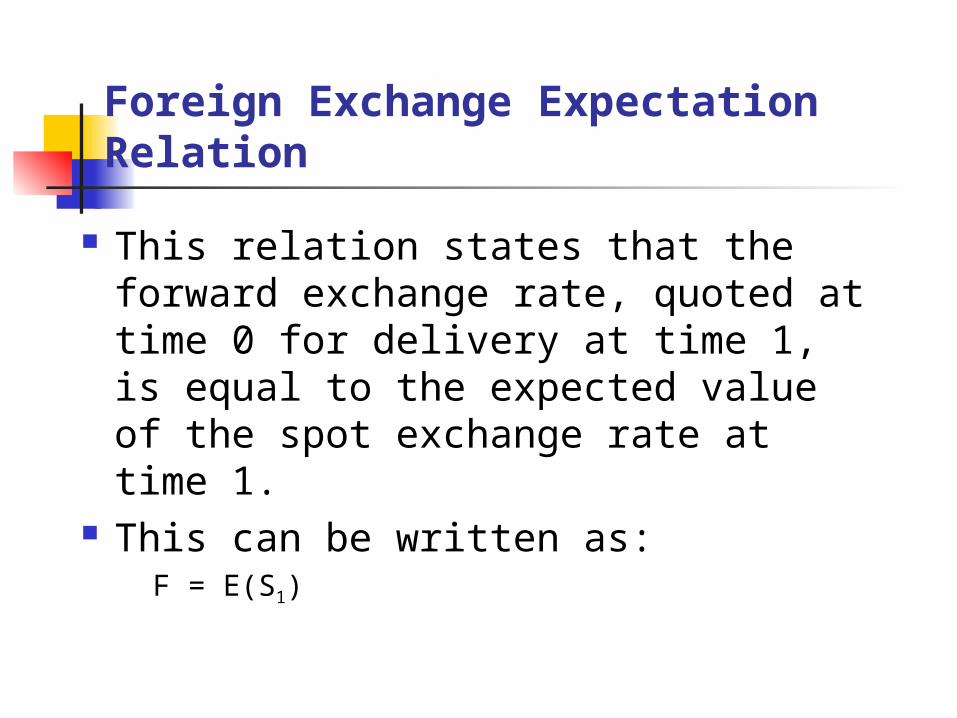

Foreign Exchange Expectation Relation

This relation states that the forward exchange rate, quoted at time 0 for delivery at time 1, is equal to the expected value of the spot exchange rate at time 1.

This can be written as:F = E(S1)

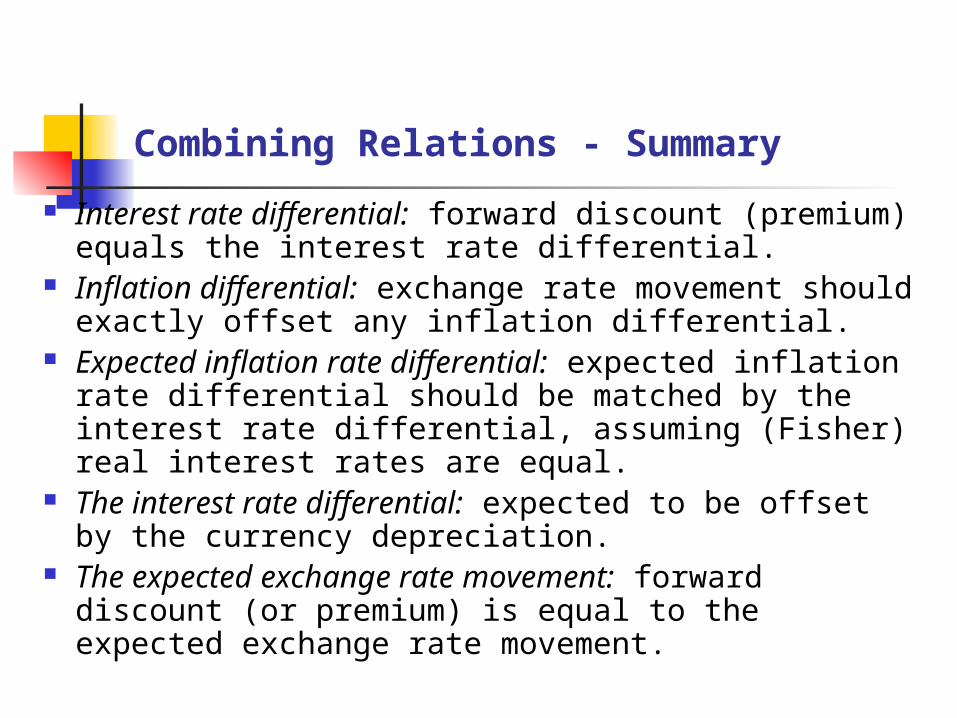

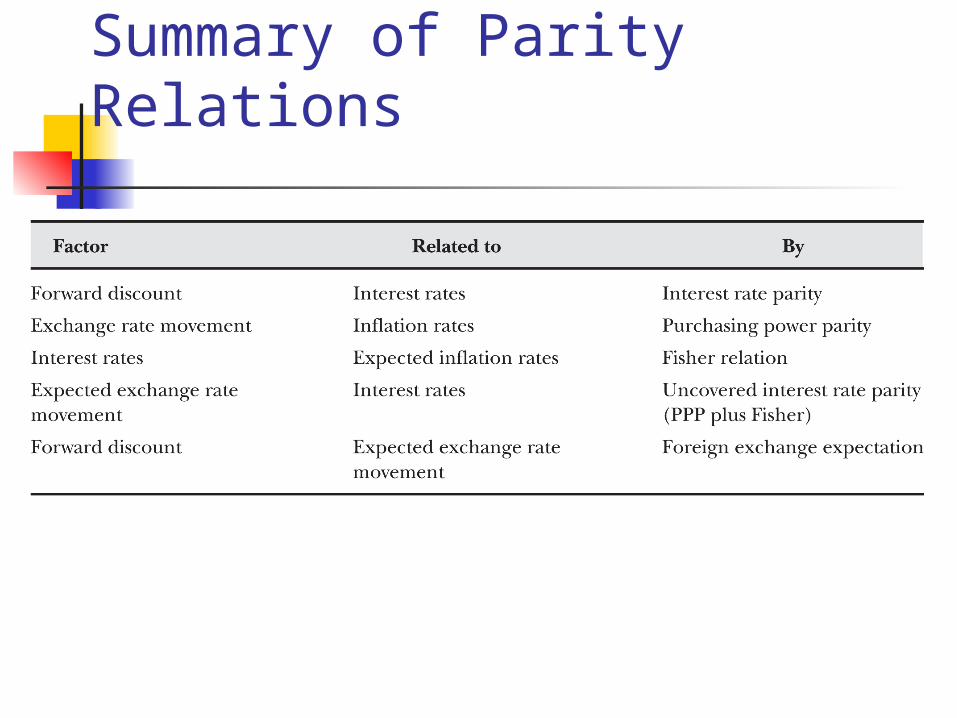

Combining Relations - Summary

Interest rate differential: forward discount (premium) equals the interest rate differential.

Inflation differential: exchange rate movement should exactly offset any inflation differential.

Expected inflation rate differential: expected inflation rate differential should be matched by the interest rate differential, assuming (Fisher) real interest rates are equal.

The interest rate differential: expected to be offset by the currency depreciation.

The expected exchange rate movement: forward discount (or premium) is equal to the expected exchange rate movement.

Summary of Parity Relations

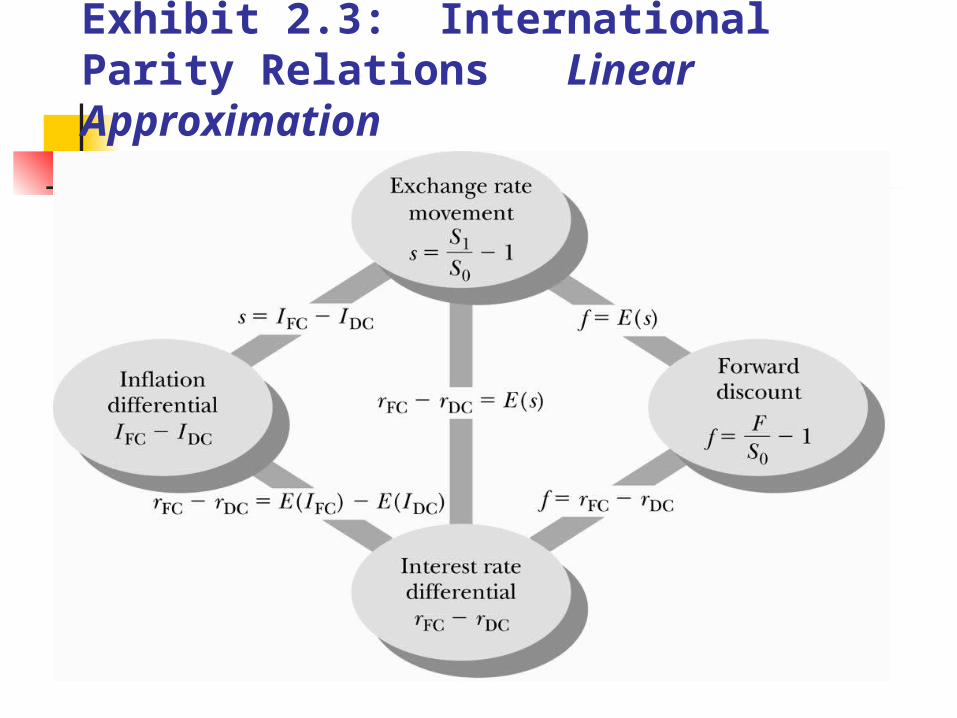

Exhibit 2.3: International Parity Relations Linear Approximation

Exchange Rate Determination

The following approaches are proposed: Fundamental value based on relative PPP Balance of Payments Approach Asset Market Approach

Fundamental Value Based on Relative PPP

Fundamental value based on relative PPP Select an inflation index for each country Select an historical period for which to

compute long-run PPP Determine the fundamental PPP value of

the exchange rate and hence the current amount of over-or undervaluation of the currency

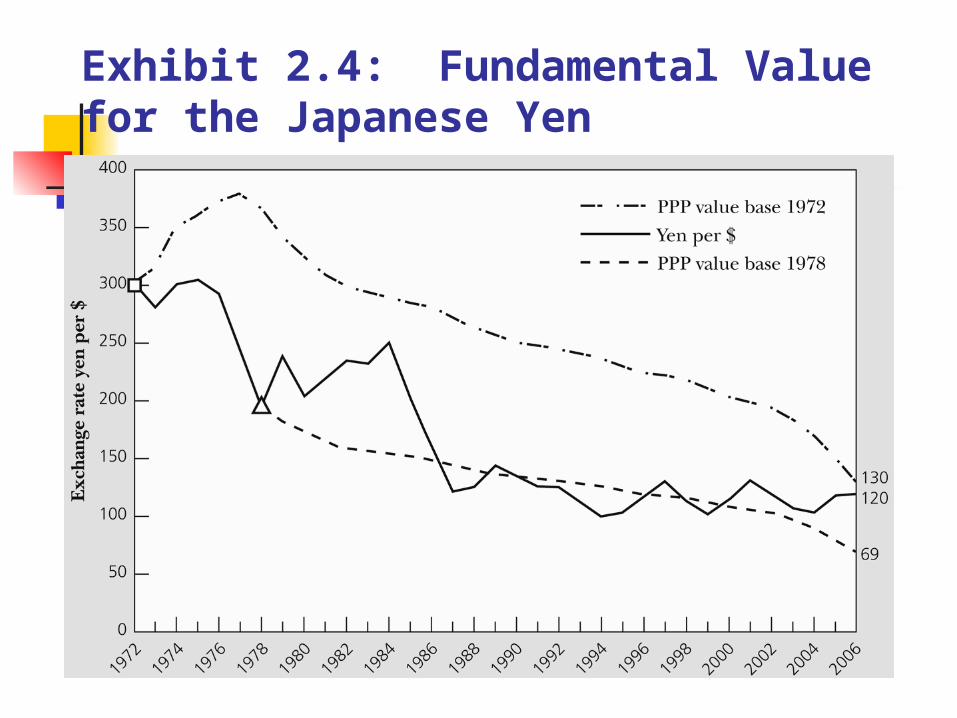

Exhibit 2.4: Fundamental Value for the Japanese Yen

Such estimation is not an easy task and exchange rates can become grossly misaligned and remain so for several years without a correction.

This correction will usually take place, but it may take several years and its timing is unclear.

Additional models are needed to provide a better understanding of exchange rate movements.

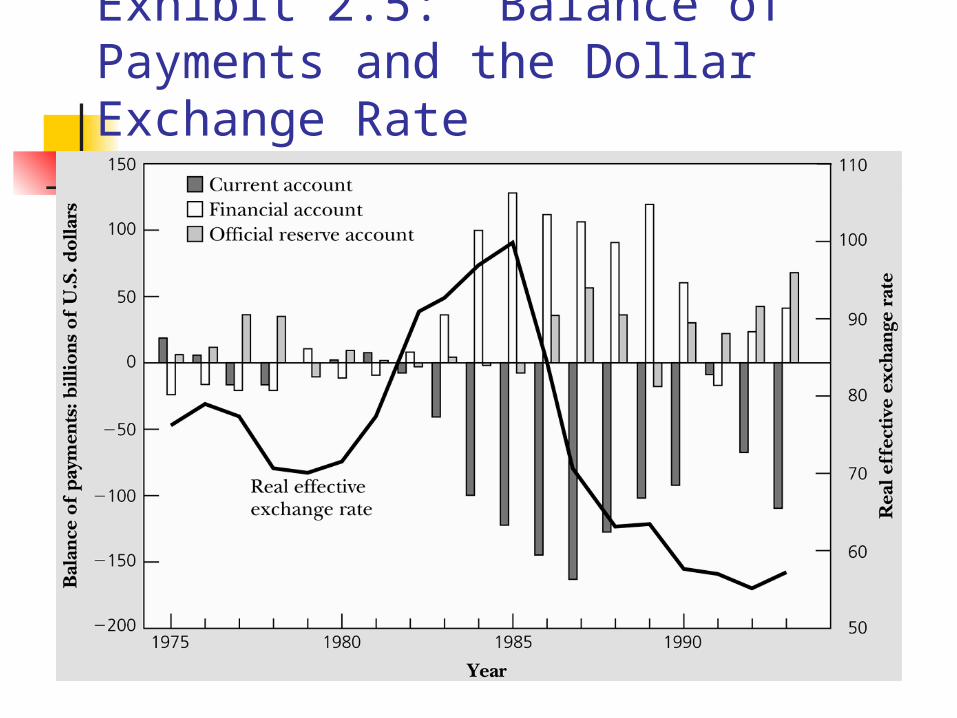

Balance of Payments Approach

An analysis of balance of payments provided the first approach to the economic modeling of the exchange rate.

The four component groups include the current account, financial account, capital account and official reserves account.

An imbalance in some account could lead to a depreciation or appreciation of the home currency.

Exhibit 2.5: Balance of Payments and the Dollar Exchange Rate

Asset Market Approach The asset market approach is generally used

to estimate the impact of some disturbance on the current value of a currency

This approach claims that the exchange rate is the relative price of two currencies, determined by investors’ expectations about the future, not by current trade flows.(eg.P62)

“News” (unexpected information) about future economic prospects should affect the current exchange rate.

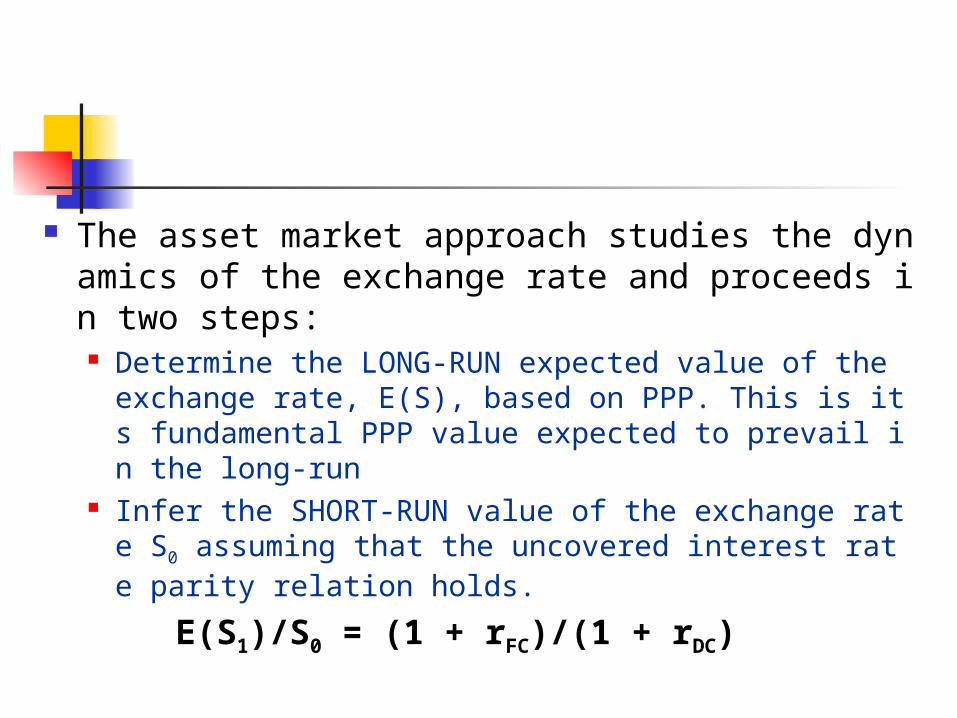

The asset market approach studies the dynamics of the exchange rate and proceeds in two steps: Determine the LONG-RUN expected value of the exch

ange rate, E(S), based on PPP. This is its fundamental PPP value expected to prevail in the long-run

Infer the SHORT-RUN value of the exchange rate S0 assuming that the uncovered interest rate parity relation holds.

E(S1)/S0 = (1 + rFC)/(1 + rDC)

Asset Market Approach: A Simple Example

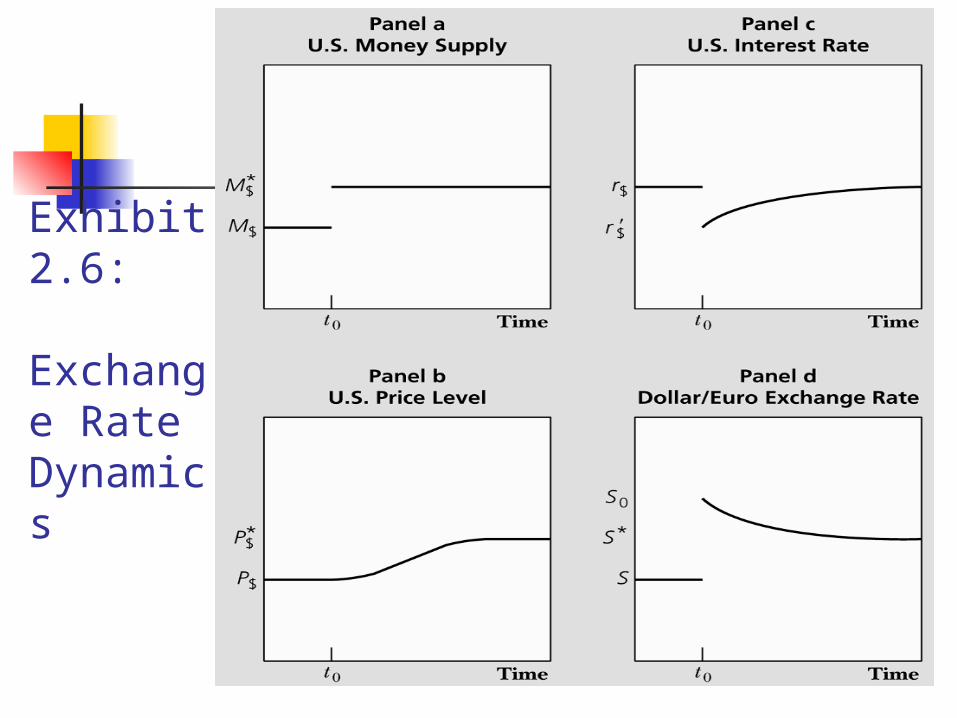

Let’s consider a one-time sudden and unexpected increase in the domestic money supply that will lead to higher home inflation.

The long-run exchange rate effect is a depreciation of the home currency so that purchasing power parity is maintained as the percentage increase in the price level matches the percentage increase in the money supply.

Given sticky-goods prices, the short-run exchange rate effect is an immediate drop in the real interest rate and more depreciation of the currency than the depreciation implied by purchasing power parity.

Exhibit 2.6:

Exchange Rate Dynamics