Embed Size (px)

Citation preview

healthy convenient fresh chiquita

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

CH

IQU

ITA

BR

AN

DS

INT

ER

NA

TIO

NA

L, IN

C. 2

00

6 A

NN

UA

L R

EP

OR

T

www.chiquita.comwww.freshexpress.com

278879_Cover 4/12/07 2:48 PM Page 1

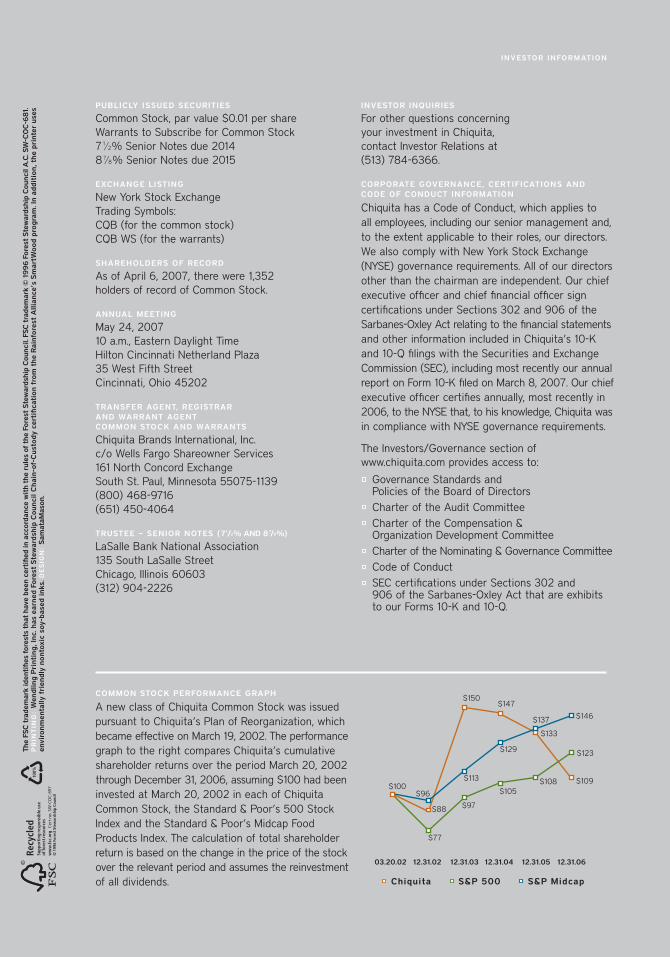

PUBLICLY ISSUED SECURITIES

Common Stock, par value $0.01 per shareWarrants to Subscribe for Common Stock71/2% Senior Notes due 201487/8% Senior Notes due 2015

EXCHANGE LISTING

New York Stock ExchangeTrading Symbols:CQB (for the common stock)CQB WS (for the warrants)

SHAREHOLDERS OF RECORD

As of April 6, 2007, there were 1,352holders of record of Common Stock.

ANNUAL MEETING

May 24, 200710 a.m., Eastern Daylight TimeHilton Cincinnati Netherland Plaza35 West Fifth StreetCincinnati, Ohio 45202

TRANSFER AGENT, REGISTRAR AND WARRANT AGENT COMMON STOCK AND WARRANTS

Chiquita Brands International, Inc.c/o Wells Fargo Shareowner Services161 North Concord ExchangeSouth St. Paul, Minnesota 55075-1139(800) 468-9716(651) 450-4064

TRUSTEE – SENIOR NOTES (71/2% AND 87/8%)

LaSalle Bank National Association135 South LaSalle StreetChicago, Illinois 60603(312) 904-2226

COMMON STOCK PERFORMANCE GRAPH

A new class of Chiquita Common Stock was issuedpursuant to Chiquita’s Plan of Reorganization, whichbecame effective on March 19, 2002. The performancegraph to the right compares Chiquita’s cumulativeshareholder returns over the period March 20, 2002through December 31, 2006, assuming $100 had beeninvested at March 20, 2002 in each of ChiquitaCommon Stock, the Standard & Poor’s 500 StockIndex and the Standard & Poor’s Midcap FoodProducts Index. The calculation of total shareholderreturn is based on the change in the price of the stockover the relevant period and assumes the reinvestmentof all dividends.

INVESTOR INQUIRIES

For other questions concerning your investment in Chiquita, contact Investor Relations at (513) 784-6366.

CORPORATE GOVERNANCE, CERTIFICATIONS ANDCODE OF CONDUCT INFORMATION

Chiquita has a Code of Conduct, which applies to all employees, including our senior management and,to the extent applicable to their roles, our directors.We also comply with New York Stock Exchange(NYSE) governance requirements. All of our directorsother than the chairman are independent. Our chiefexecutive officer and chief financial officer sign certifications under Sections 302 and 906 of theSarbanes-Oxley Act relating to the financial statementsand other information included in Chiquita’s 10-K and 10-Q filings with the Securities and ExchangeCommission (SEC), including most recently our annualreport on Form 10-K filed on March 8, 2007. Our chiefexecutive officer certifies annually, most recently in2006, to the NYSE that, to his knowledge, Chiquita wasin compliance with NYSE governance requirements.

The Investors/Governance section ofwww.chiquita.com provides access to:

Governance Standards and Policies of the Board of DirectorsCharter of the Audit CommitteeCharter of the Compensation & Organization Development CommitteeCharter of the Nominating & Governance CommitteeCode of ConductSEC certifications under Sections 302 and 906 of the Sarbanes-Oxley Act that are exhibits to our Forms 10-K and 10-Q.

INVESTOR INFORMATION

Cert

no.

SW

-CO

C-89

7 $100

$88

$77

$96

$150

$97

$113

$147

$105

$129

$133

$108

$137

$109

$123

$146

03.20.02 12.31.02 12.31.03 12.31.04 12.31.05 12.31.06

Chiquita S&P 500 S&P Midcap

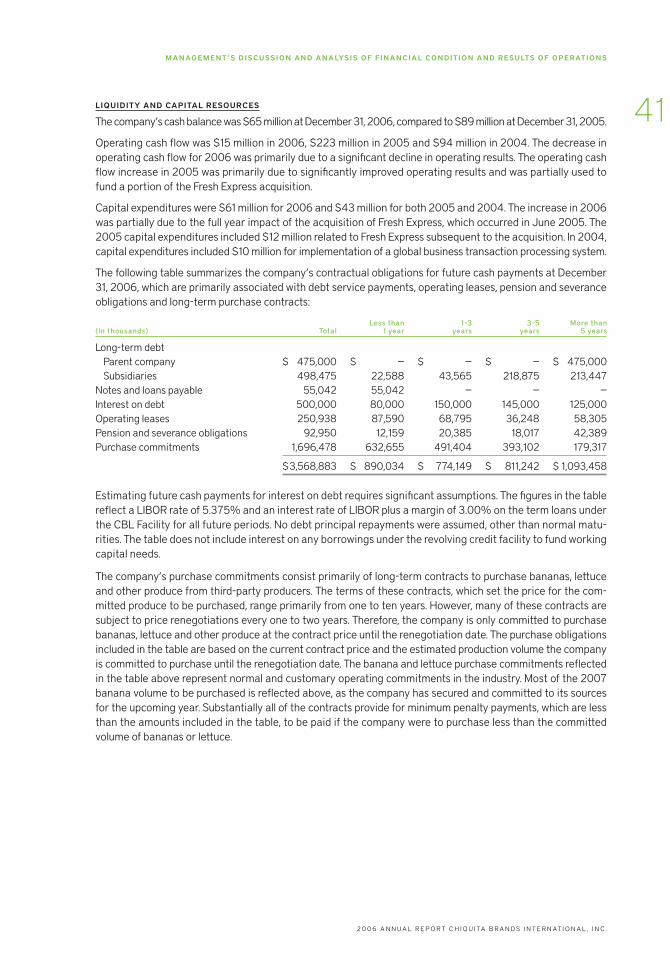

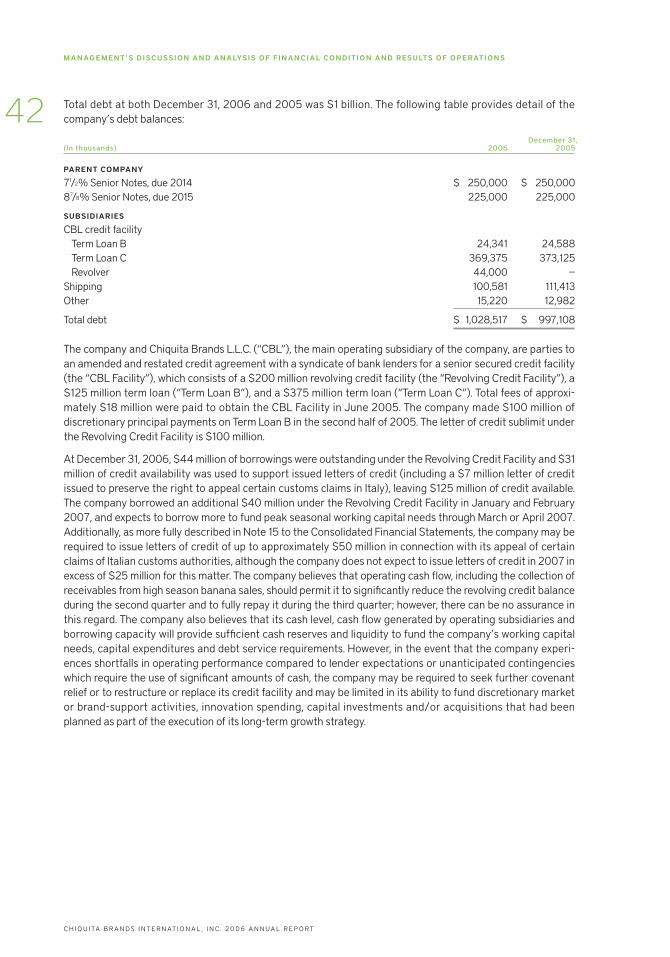

(In millions, except per share amounts) 2006 2005* 2004

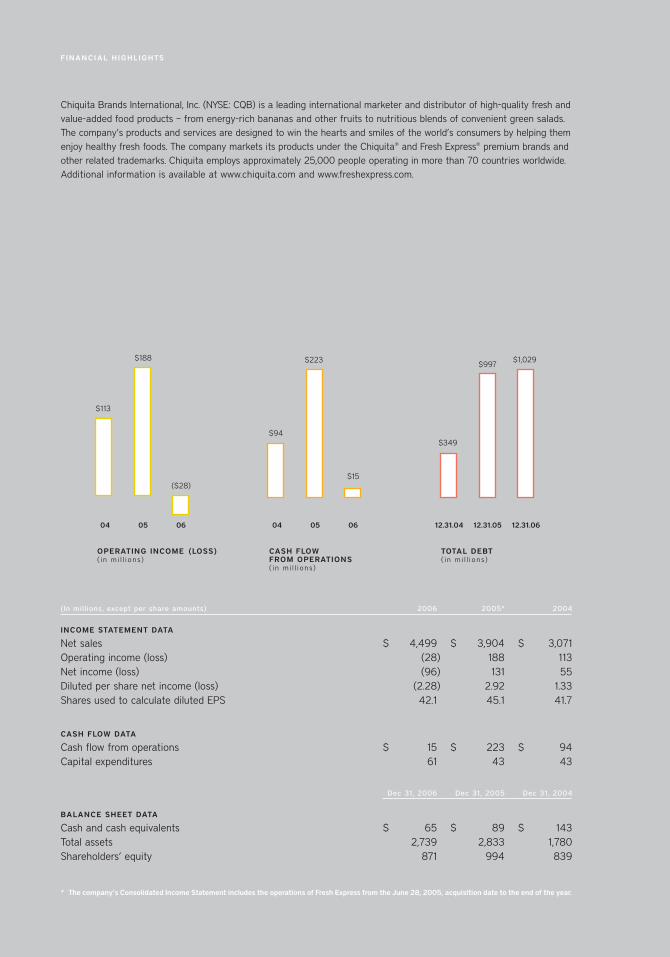

INCOME STATEMENT DATA

Net sales $ 4,499 $ 3,904 $ 3,071Operating income (loss) (28) 188 113Net income (loss) (96) 131 55Diluted per share net income (loss) (2.28) 2.92 1.33Shares used to calculate diluted EPS 42.1 45.1 41.7

CASH FLOW DATA

Cash flow from operations $ 15 $ 223 $ 94Capital expenditures 61 43 43

Dec 31, 2006 Dec 31, 2005 Dec 31, 2004

BALANCE SHEET DATA

Cash and cash equivalents $ 65 $ 89 $ 143Total assets 2,739 2,833 1,780Shareholders’ equity 871 994 839

* The company’s Consolidated Income Statement includes the operations of Fresh Express from the June 28, 2005, acquisition date to the end of the year.

Chiquita Brands International, Inc. (NYSE: CQB) is a leading international marketer and distributor of high-quality fresh andvalue-added food products – from energy-rich bananas and other fruits to nutritious blends of convenient green salads.The company’s products and services are designed to win the hearts and smiles of the world’s consumers by helping themenjoy healthy fresh foods. The company markets its products under the Chiquita® and Fresh Express® premium brands andother related trademarks. Chiquita employs approximately 25,000 people operating in more than 70 countries worldwide.Additional information is available at www.chiquita.com and www.freshexpress.com.

F INANCIAL H IGHL IGHTS

04

OPERATING INCOME (LOSS)( i n m i l l i ons )

05 06

$113

($28)

$188

04

CASH FLOW FROM OPERATIONS( i n m i l l i ons )

05 06

$94

$15

$223

12.31.04

TOTAL DEBT( i n m i l l i ons )

12.31.05 12.31.06

$349

$1,029$997

The

FSC

tra

dem

ark

iden

tifi

es f

ores

ts t

hat

have

bee

n ce

rtifi

ed in

acc

orda

nce

wit

h th

e ru

les

of t

he F

ores

t S

tew

ards

hip

Cou

ncil.

FS

C t

rade

mar

k ©

19

96

For

est

Ste

war

dshi

p C

ounc

il A

.C. S

W-C

OC

-68

1.P

RIN

TIN

G:

Wen

dlin

g P

rint

ing

, In

c. h

as e

arn

ed F

ore

st S

tew

ard

ship

Co

unci

l Ch

ain

-of-

Cus

tod

y ce

rtifi

cati

on

fro

m t

he

Rai

nfo

rest

Alli

ance

’s S

mar

tWo

od

pro

gra

m. I

n a

dd

itio

n, t

he

prin

ter

uses

envi

ron

men

tally

frie

ndl

y n

ont

oxic

soy

-bas

ed i

nks

. DE

SIG

N:

Sam

ataM

ason

.

278879_Cover 4/13/07 4:49 PM Page 2

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

LETTER FROM CHAIRMAN & CEO

01

D E A R S TA K E H O L D E R S ,

2006 was a difficult, transitional year for Chiquita.

We achieved a number of operational and strategic

targets and made progress towards achieving our

vision of becoming an innovative global leader in

branded, healthy, fresh foods. However, we also

faced many challenges during the year. We faced

these head-on and have recently begun to recover,

but these factors had a significant impact on our

overall financial performance.

W E D E L I V E R E D T H E FO L LO W I N G R E S U LT S I N 2 0 0 6 :

Net sales grew by 15 percent to a new record

of $4.5 billion. The increase in annual sales

reflects the positive full-year impact of the

acquisition of Fresh Express in mid-year 2005.

We incurred an operating loss of $28 million,

compared to operating income of $188 million

in 2005 and a net loss of $96 million, or

($2.28) per diluted share, compared to net

income of $131 million the prior year.

Operating cash flow was $15 million, compared

to $223 million in 2005, reflecting the decline

in operating income.

A D D R E S S I N G I N D U S T RY W I D E C H A L L E N G E S T H R O U G H O U T 2 0 0 6

We were not satisfied with our results in 2006,

a year in which we faced what many investors

called a “perfect storm.” We confronted significant

headwinds from higher tariffs and increased com-

petition in the E.U. banana market, U.S. consumer

concerns about the safety of fresh spinach, higher

industry costs and other competitive pressures.

However, we firmly believe our 2006 results are

not indicative of the underlying strengths of

Chiquita’s business or our long-term potential.

We are encouraged by a promisingfuture, as we reach to achieve ourvision as an innovative global leader in branded, healthy, fresh foods.

278879_text 4/12/07 3:17 PM Page 01

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

LETTER FROM CHAIRMAN & CEO

02

At the beginning of 2006, the European

Commission imposed a tariff rate of ¤176 per

metric ton of bananas imported from Latin

America, up from ¤75 per metric ton, and

eliminated the volume quota that previously

applied to Latin American banana imports. This

unilateral regulatory change resulted in a net

increase of $75 million in higher tariff costs to

Chiquita and contributed to a decline of

$110 million in banana pricing in core European

markets. As expected, several Latin American

governments have strongly objected to the

current E.U. banana regime as illegal. In March

2007, Ecuador’s request for an arbitration

panel under expedited Article 21.5 World Trade

Organization procedures was approved, and

a ruling is expected late in 2007. While such a

challenge does not guarantee success, we

believe the Latin Americans have strong legal

arguments and, this challenge has the potential

to lead Europe to negotiate a lower tariff rate or

other constructive changes to the current regime.

In September, the fresh-cut industry was affected

by an E. coli outbreak that has had a negative

impact on U.S. consumer confidence. The U.S.

Food and Drug Administration’s investigation of

this outbreak did not link any confirmed cases of

illness to the company’s products. In fact, Fresh

Express has a stellar food-safety record for the

19 years during which we have produced retail

value-added salads. Nevertheless, we estimate

that operating results were $21 million lower in

our Fresh Cut segment due to reduced sales and

decreased margins as consumption of packaged

salads declined. Although we have been rebounding

faster than others in the category, we believe the

impact on consumer confidence is likely to con-

tinue to negatively affect our Fresh Cut segment

results through at least the third quarter 2007.

Our costs for fuel, fruit, ship charters, paper and

resin increased by $54 million in 2006, reflecting

increases affecting the entire industry. In addition,

we recorded a one-time, noncash charge of $43

million related to goodwill impairment at Atlanta

AG, our German fresh produce distributor, and a

$25 million reserve for settlement of a previously

disclosed investigation by the U.S. Department

of Justice. Lastly, to enhance financial flexibility,

we suspended Chiquita’s quarterly cash dividend

in September.

278879_text 4/12/07 3:18 PM Page 02

At the beginning of 2006, the European Commission imposed a tariff rate of

¤176 per metric ton of bananas imported from Latin America, up from ¤75 per

metric ton, and eliminated the volume quota that previously applied to Latin

American banana imports. This unilateral regulatory change resulted in higher tariff

costs to Chiquita and contributed to a decline in banana pricing in core European

markets. As expected, several Latin American governments have strongly objected

to the current E.U. banana regime as illegal. In March 2007, Ecuador’s request for

an arbitration panel under expedited World Trade Organization procedures was

approved, and a ruling is expected late in 2007.

“Latin Americanbanana-producing countries rejectnew EU tariff”X I N H U A G E N E R A L N E W S S E R V I C E

H E A D L I N E :

sep1406

278879_text 4/12/07 7:15 PM Page 03

We are committed to bringing healthy, safe products to consumers, and food safety

has always been our No. 1 priority. As an example of our leadership, we formed an

independent scientific advisory panel in May 2006 to further explore how food-safety

practices might be enhanced. In fact, we committed $2 million to fund nine innovative

research projects recommended by this panel in an effort to better understand and

mitigate the threat posed by E. coli O157:H7 in lettuce and leafy greens. We plan to

share any research findings as widely as possible to stimulate the development of

advanced safeguards within the fresh-cut industry.

“Fresh Expressleads the pack inproduce safety”U S A TO D AY – J U L I E S C H M I T

oct2306

H E A D L I N E :

278879_text 4/12/07 6:34 PM Page 04

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

LETTER FROM CHAIRMAN & CEO

05

Despite these challenges, we sustained our

leadership position in the premium-quality segment

of the European banana market, expanding

sales of Chiquita-brand bananas by 4 percent,

and maintained all of our significant customer

relationships in Europe. Banana pricing in North

America continued to improve, generating an

additional $21 million in 2006 income. Further,

our Fresh Express business expanded its market

leadership position, while strengthening

Chiquita’s reputation for food safety.

We are encouraged by a promising future. Our

vision is to enhance our position as an innovative

global leader in branded, healthy, fresh foods.

We aim to double revenue from our 2005 base and

more than double profitability during the next five

years. To achieve this goal, we are focused on two

key objectives: to pursue profitable growth by

delivering innovative, higher-margin products

and to build a high-performance organization.

D E L I V E R I N G I N N O VAT I V E , H I G H E R - M A R G I N P R O D U CT S

Our company is enhancing its leadership position

in branded, healthy, fresh foods by focusing on

meeting consumer needs with differentiated,

value-added products and making them more

available to consumers.

Fresh Express expanded its market leadership

in retail value-added salads, growing its dollar

share to approximately 48 percent in 2006,

compared to approximately 43 percent in

2005. Fresh Express successfully introduced

12 new higher-margin products during 2006,

including “Sweet Butter” and “5 Lettuce Mix”

salad blends. These two salad blends were

the top two new items across all categories

introduced in U. S. supermarkets in the third

quarter, beating out all new products from

other leading brands such as Pepsi, Frito-Lay,

Kraft and Campbell Soup.

Chiquita minis are also achieving success.

These higher-margin “baby” bananas meet

consumer needs for healthy, portable snacks.

We are currently serving several large retail

customers in North America. Following a

successful market test in Finland, we are

expanding across Europe in 2007.

278879_text 4/12/07 7:50 AM Page 05

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

LETTER FROM CHAIRMAN & CEO

06

Chiquita Apple Bites remain the No. 1 brand

of sliced apples in the United States with a

49 percent value share at year-end. We continue

to expand distribution aggressively, both at

retail, where we have increased distribution

to about 38 percent, and through our quick-

service restaurant partners. In March 2007,

Subway began offering co-branded Chiquita

Apple Bites nationally, expecting to reach

more than 14,500 restaurants in 2007.

Chiquita Just Fruit in a Bottle, a line of all-

natural chilled fruit smoothies, has excelled

in its initial European market introduction in

Belgium last June. This product is available at

major grocery retailers, as well as in various

out-of-home channels. After only six months,

Just Fruit in a Bottle is the leading fresh smoothie

in Belgium with 70 percent distribution among

major retailers.

Chiquita to Go, single Chiquita bananas in pro-

prietary packaging that keeps bananas perfectly

ripe for seven days or more, has generated

tremendous enthusiasm. This packaging inno-

vation enables us to reach consumers through

new higher-margin convenience outlets. At

year-end, Chiquita to Go was already in more

than 8,000 outlets, and we will significantly

increase the size of this business in 2007, as

we add new distribution points every month.

These are just some of the new, innovative higher-

margin products Chiquita is introducing, and we

see significant opportunity to expand our offerings

and profitability by meeting consumer demand

for healthy, on-the-go, fresh foods. Throughout

2007, more innovative products like these will

be tested and introduced into the marketplace.

B U I L D I N G A H I G H - P E R FO R M A N C E O R GA N I Z AT I O N

Our second key objective is to continue to build

a high-performance organization. This means

optimizing our efforts to become a consumer-

centric and customer-preferred company. For

example, we are working to make value-selling

a key capability across our organization. We

continue to excel in cold-chain management,

lead with innovation and technology to expand

margins, and apply best-in class people practices

across Chiquita.

278879_text 4/12/07 7:50 AM Page 06

Our products are the perfect fit to address consumers’ needs for health, convenience

and great taste. Chiquita is enhancing its leadership position in branded, healthy,

fresh foods by focusing on meeting consumer needs with value-added products

and making them more available to consumers. To help parents find easy ways to

incorporate fruits into their children’s diets and meet the USDA’s recommended

two cups of fruit a day, we have introduced smaller and pre-packaged snack

options. Chiquita minis and Chiquita Apple Bites are excellent examples of ready-

to-eat choices for parents that are ideal for lunchboxes and snack time.

“Want fast food?Now you can have fast fruit”T U C S O N C I T I Z E N – B R U C E H O R O V I TZ

jan0806

H E A D L I N E :

278879_text 4/12/07 6:34 PM Page 07

To achieve our vision as an innovative global leader in branded, healthy, fresh foods,

we are focused on two key objectives: to pursue profitable growth by delivering

innovative, higher-margin products and to build a high-performance organization.

We believe we made a great deal of progress in both areas during 2006, and we are

prepared to further take advantage of these opportunities in 2007. We are building a

steady stream of innovations, transitioning from a commodity focus to profitable

value-added products with higher margins, while expanding into adjacent product

categories. Chiquita is on the right path to profitable, sustainable growth.

“A recipe for profits”T H E I R I S H T I M E S – BY A L I S O N H E A LY

H E A D L I N E :

aug3106

278879_text 4/12/07 6:35 PM Page 08

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

LETTER FROM CHAIRMAN & CEO

09

For example, in September 2006, we announced

that we were exploring strategic alternatives

for the sale and long-term management of our

ocean shipping operations. We believe there is

an opportunity to enhance shareholder value

while maintaining high quality and competitive

long-term operating costs by partnering with

expert shipping service providers that can grow with

Chiquita. Potential opportunities such as these

will allow us to focus our efforts and resources

even more on strengthening customer relationships

and generating capital, which will primarily be

used to reduce debt, as well as to invest in new

growth opportunities.

We are continuously evaluating how to make our

business more efficient and drive synergies. We

exceeded our cost savings and synergy targets

in 2006, achieving $47 million in gross cost

savings across our tropical production and supply

chain, which mitigated some of the cost increases

affecting the entire industry. In addition, we

achieved our target of a $20 million run-rate in

acquisition synergies within 18 months of acquiring

Fresh Express, in half the time we had committed.

We expect to make further progress and have

set a goal to deliver an additional $40 million in

gross cost savings in 2007.

We are focused on becoming a customer-preferred

company by excelling in category management,

product quality, customer service and in-store

execution. In fact, Progressive Grocer magazine

recognized Chiquita and Fresh Express as

“Category All-Stars” in 2006 for exceptional

category management, honoring companies that

have been Category Captains in at least five of the

last 10 years.

A D D I N G L E A D E R S H I P TA L E N T

We have made enhancements to our management

team to support our goal to grow Chiquita into an

innovative global leader in branded, healthy, fresh

foods. James Thompson now serves as our general

counsel and secretary with responsibility for

Chiquita’s global law department. We appointed

Vanessa Vargas-Land to serve as our chief com-

pliance officer, as we continue our commitment

to full regulatory compliance and transparency in

all of our activities. Additionally, we named two

newly created global product leader positions to

better manage our pipeline of innovative products

across all segments and develop a growth platform

for our key products on a global basis.

278879_text 4/12/07 7:51 AM Page 09

LETTER FROM CHAIRMAN & CEO

10

F E R N A N D O AG U I R R E

Chairman & Chief Executive OfficerApril 12, 2007

We are also integrating the strengths of our

Chiquita and Fresh Express sales teams to better

leverage our value-selling capability and have

already begun producing results. We are pleased

that Mike Holcomb has joined our management

team as vice president of corporate sales and

customer development to lead this effort.

Individually and as a team, we have ensured

that our management is well-prepared to grow

our businesses profitably through innovation and

build a high-performance organization. Consistent

with our deep commitment to innovation, 2007

marks the first year that a portion of our man-

agement team’s incentive compensation will be

based on achieving certain revenue targets for

new higher-margin products.

M O V I N G TO W A R D A S T R O N G F U T U R E

I have confidence that Chiquita is on the right

path to return to profitable, sustainable growth.

We are focused on diversification and innovation

to ensure we capitalize on opportunities to

strengthen our business and brand. Our team is

working together to share new product ideas and

create efficiencies and profitable growth across our

operation. We believe the strategic initiatives we

are executing will revitalize our company in 2007.

I want to thank our employees for their tremendous

dedication to Chiquita in leading this effort. I am

confident we will successfully transform Chiquita

into an innovative global leader in branded,

healthy, fresh foods, and I look forward to updating

you on our progress as we move through the year.

278879_text 4/12/07 3:20 PM Page 10

Chiquita has a clearvision, focused on innovation with higher-margin products that fit perfectly with consumer needs forhealthy, convenient and fresh foods.

278879_text 4/12/07 6:35 PM Page 11

278879_text 4/12/07 7:52 AM Page 12

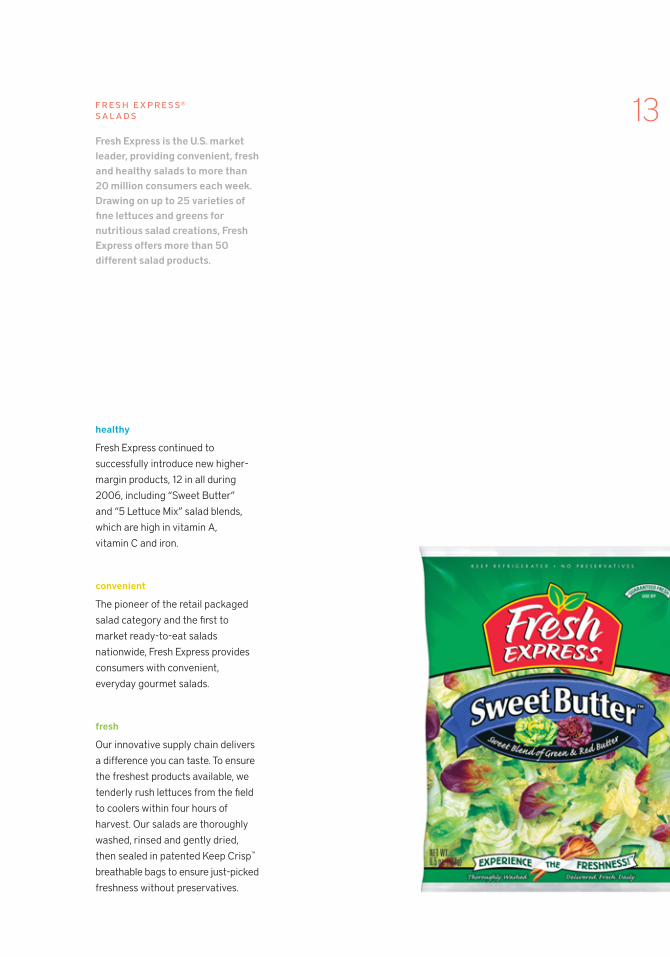

13

healthy

Fresh Express continued to

successfully introduce new higher-

margin products, 12 in all during

2006, including “Sweet Butter”

and “5 Lettuce Mix” salad blends,

which are high in vitamin A,

vitamin C and iron.

convenient

The pioneer of the retail packaged

salad category and the first to

market ready-to-eat salads

nationwide, Fresh Express provides

consumers with convenient,

everyday gourmet salads.

fresh

Our innovative supply chain delivers

a difference you can taste. To ensure

the freshest products available, we

tenderly rush lettuces from the field

to coolers within four hours of

harvest. Our salads are thoroughly

washed, rinsed and gently dried,

then sealed in patented Keep Crisp™

breathable bags to ensure just-picked

freshness without preservatives.

F R E S H E X P R E S S ®

S A L A D S

Fresh Express is the U.S. marketleader, providing convenient, freshand healthy salads to more than20 million consumers each week.Drawing on up to 25 varieties offine lettuces and greens for nutritious salad creations, FreshExpress offers more than 50 different salad products.

278879_text 4/12/07 3:21 PM Page 13

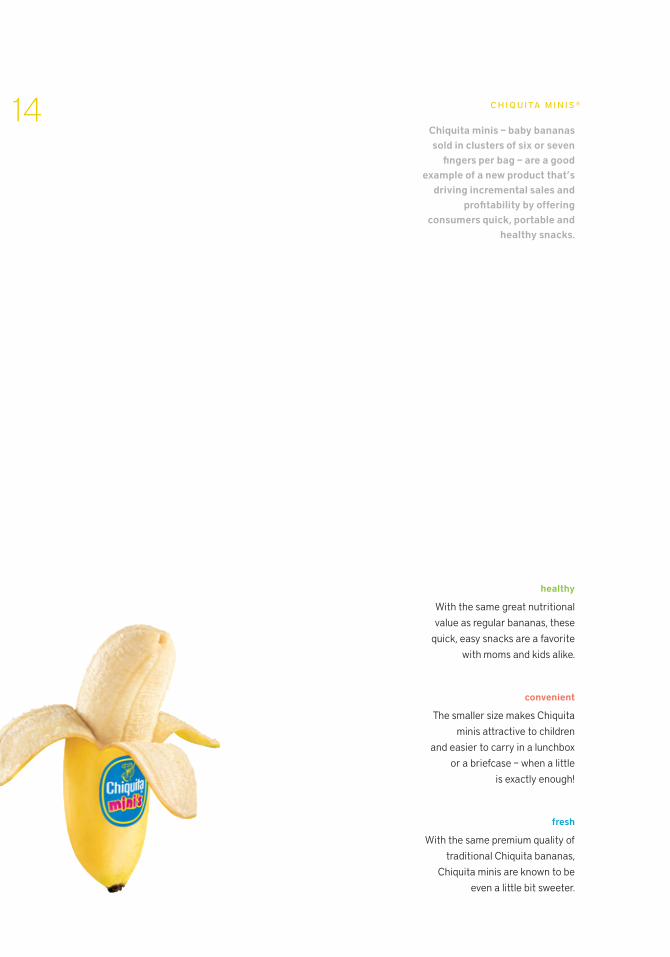

14

healthy

With the same great nutritional

value as regular bananas, these

quick, easy snacks are a favorite

with moms and kids alike.

convenient

The smaller size makes Chiquita

minis attractive to children

and easier to carry in a lunchbox

or a briefcase – when a little

is exactly enough!

fresh

With the same premium quality of

traditional Chiquita bananas,

Chiquita minis are known to be

even a little bit sweeter.

Chiquita minis – baby bananassold in clusters of six or seven

fingers per bag – are a good example of a new product that’s

driving incremental sales and profitability by offering

consumers quick, portable andhealthy snacks.

C H I Q U I TA M I N I S ®

278879_text 4/12/07 7:53 AM Page 14

278879_text 4/12/07 3:21 PM Page 15

278879_text 4/12/07 7:54 AM Page 16

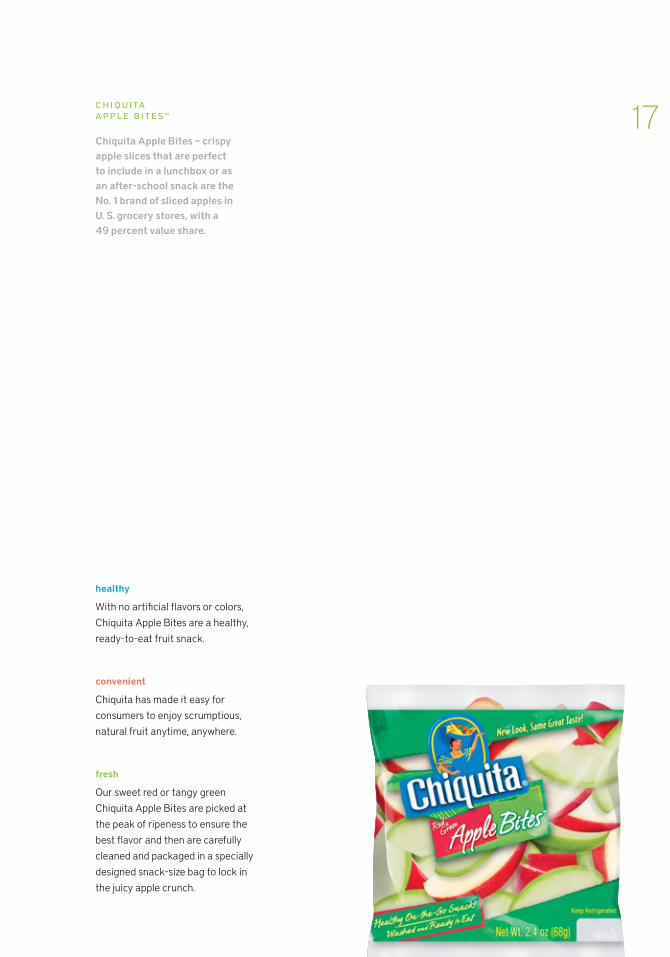

17

healthy

With no artificial flavors or colors,

Chiquita Apple Bites are a healthy,

ready-to-eat fruit snack.

convenient

Chiquita has made it easy for

consumers to enjoy scrumptious,

natural fruit anytime, anywhere.

fresh

Our sweet red or tangy green

Chiquita Apple Bites are picked at

the peak of ripeness to ensure the

best flavor and then are carefully

cleaned and packaged in a specially

designed snack-size bag to lock in

the juicy apple crunch.

C H I Q U I TA

A P P L E B I T E S™

Chiquita Apple Bites – crispyapple slices that are perfect to include in a lunchbox or as an after-school snack are the No. 1 brand of sliced apples in U. S. grocery stores, with a 49 percent value share.

278879_text 4/12/07 7:54 AM Page 17

18

healthy

We have just put whole fruits into a

bottle and added nothing else: no

additives, no preservatives and no

added sugar. Pure fruit, pure pleasure!

convenient

Chiquita Just Fruit in a Bottle

brings the natural goodness of

fresh fruits to European retail

outlets in a single-serve bottle

that consumers can enjoy at

any time or place.

fresh

The intense natural fruit taste and

the rich texture make Chiquita Just

Fruit in a Bottle delicious, while the

fresh fruit ingredients make it a

nutritious, healthy snack.

J U S T F R U I T

I N A B OT T L E™

Chiquita’s Just Fruit in a Bottleoffers European consumers a new

way to enjoy fresh fruits. Thesenondairy smoothies are a

chilled mix of fresh fruits andfreshly squeezed juice in three

flavors: strawberry-banana, banana-pineapple-orange and

mango-passion fruit.

278879_text 4/12/07 7:54 AM Page 18

19

278879_text 4/12/07 3:22 PM Page 19

278879_text 4/12/07 3:23 PM Page 20

21C H I Q U I TA TO G O ®

B A N A N A S

Our single Chiquita bananas arepacked in conveniently sized boxes sealed with a proprietarypatch that perfectly regulates air flow, enabling a longer shelflife and distribution through nontraditional and higher-marginretail outlets. At year-end,Chiquita to Go was in more than 8,000 outlets, and we willsignificantly increase the size of this business in 2007.

convenient

Using proprietary packaging

technology that keeps bananas at

their peak of ripeness for more

than seven days, Chiquita to Go

brings healthy, fresh fruit to

consumers every day of the week,

any time of day.

healthy

Chiquita bananas are vitamin-rich,

heart-healthy and perfectly fat-free.

In fact, a single Chiquita banana

supplies 20 percent and 11 percent

of the U.S. Recommended Daily

Allowances of vitamin B6 and

potassium, respectively.

fresh

Selected for their ideal size, color,

shape and ripeness, Chiquita to Go

bananas are perfectly ripe every

day of the week and offer a healthy

alternative snack to consumers.

278879_text 4/12/07 7:56 AM Page 21

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

22

Gourmet Café Salads™

The pioneer of the retail packaged salad category, Fresh Express continues

its commitment to quality and innovation through a new line of full-meal

salads in convenient, single-serve packaging.

These are just some of the new, innovative higher-margin products Chiquita isintroducing, and we see significant opportunity to expand our offerings andprofitability by meeting consumer demand for healthy, on-the-go, fresh foods.Throughout 2007, more innovative products like these will be tested and introduced into the marketplace.

Chiquita Fresh & Ready™

Chiquita Fresh & Ready offers bananas that stay fresh for twice as long

as regular bananas. Taking the Chiquita to Go technology from the

convenience store to the produce department at your local grocer,

Chiquita Fresh & Ready provides consumers a convenient, healthy snack

at home. At year-end 2006, Chiquita Fresh & Ready was in test with

several major retailers in three U.S. states.

Chiquita Fruit Bar

Chiquita Fruit Bar offers a wide array of high-quality Chiquita fresh

produce and tasty fruit-based drinks that are made on demand in a fun and

friendly retail atmosphere. A natural extension to meet consumers’ needs

for healthy and convenient food choices, Chiquita Fruit Bar continues

to build our brand equity with European consumers and is currently at four

locations in Germany.

Healthy Snacking

To meet the demand from today’s consumers for convenient, healthy and

great-tasting food choices, we are expanding on the success of Chiquita

Apple Bites by introducing ready-to-eat mini carrots, snap peas and grapes

that are ideal for lunchboxes and snack time. These healthy, bite-sized

products are fun for kids and adults alike and provide essential vitamins

and minerals in consumer-friendly, on-the-go packages.

EVEN MORE INNOVATIVE PRODUCTS

278879_text 4/12/07 3:23 PM Page 22

nov17

06“Chiquita cleans up its act”F O R T U N E M AG A Z I N E – J E N N I F E R A LS E V E R

H E A D L I N E :

We manage all of our operations in accordance with our Core Values – Integrity,

Respect, Opportunity and Responsibility – and the Chiquita Code of Conduct,

which guide our daily decisions and define our standards for corporate respon-

sibility. In addition to strict legal compliance, we define corporate responsibility

to include social responsibilities, such as respect for the environment and the

communities where we do business, the health and safety of our workers, labor

rights and food safety. We see a positive link between our Core Values and our

company’s vision, mission and sustainable growth strategy.

278879_text 4/12/07 6:36 PM Page 23

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

24

CORPORATE RESPONSIB IL ITY

M A I N TA I N I N G 1 0 0 % C E R T I F I C AT I O N O N O W N E D FA R M S I N L AT I N A M E R I C A

We have selected industry standards that are most

relevant to each segment of our business. In most

cases, we have been the industry pioneer seeking

credible third-party certification of our performance.

For example, in the mid-1990s, we committed

to achieve certification on all company banana

farms to the rigorous standards of the Rainforest

Alliance, a leading international conservation

organization. The Rainforest Alliance (www.ra.org)

certifies farms that follow its 10 stringent environ-

mental and social standards for agriculture,

designed to protect the environment, wildlife,

workers and local communities.

During 2006, all of our Latin American banana

divisions earned recertification by the Rainforest

Alliance for the seventh straight year based on

farm-by-farm audits, despite more rigorous

standards. Moreover, 84 percent of acreage of

independent grower farms in Latin America from

which we source bananas also had achieved

Rainforest Alliance certification at year-end.

In addition, 100 percent of our owned banana

farms in Latin America were certified to the Social

Accountability 8000 labor and human rights

standard (www.sa-intl.org) and to the EurepGAP

food-safety standard (www.eurepgap.org).

C O N S E R V I N G B I O D I V E R S I T Y W I T H C O M M U N I T Y S U P P O R T

A highlight of our corporate responsibility efforts

in 2006 occurred when President Oscar Arias

of Costa Rica presented the 2006 Contribution

to the Community Award to Chiquita Brands

International on behalf of the American-Costa

Rican Chamber of Commerce, in recognition of

the company’s Nature & Community Project,

an initiative designed to preserve biodiversity,

promote nature conservation awareness among

the local population and create new sources of

income for people in the community.

Chiquita’s Nature and Community Project –

developed with the support and cooperation of

independent partners, including Swiss retailer

Migros (www.migros.ch), the Rainforest Alliance,

and German Technical Cooperation – GTZ

(www.gtz.de) – contributes to the protection of

the exceptional biodiversity of the region by

encouraging local communities and farmers to

actively participate in the protection of rainforests

and the many species which depend on them.

The project, which started in September 2003,

is based at Chiquita’s Nogal farm in the Sarapiquí

region in northeastern Costa Rica. More than 100

hectares (250 acres) of protected rainforest on

this farm were designated as a private wildlife

refuge by the Costa Rican government in January

2006. To facilitate the migration and survival of

endangered species, this forest will be connected

with other forest areas of the region, including

the Braulio Carrillo national park, 8 kilometers

(5 miles) away. To date, the creation of this biological

corridor has involved the planting of 10,000 trees

of more than 40 native species. Local farmers are

contributing to this effort by providing land for

reforestation.

278879_text 4/12/07 5:23 PM Page 24

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

CORPORATE RESPONSIB IL ITY

25Environmental education for schoolchildren,

neighbors and Chiquita’s own employees plays

an important role in this work, since the support

of the local population is essential for long-term

environmental conservation. Nearly 3,000

visitors have already participated in workshops

provided at the Nogal project center.

The creation of new economic opportunities, such

as ecotourism and arts and crafts based on envi-

ronmental protection, is another important aspect

of the project. So far, five small businesses have

been established with assistance of the project, and

their sales have contributed to the income of many

families in neighboring communities.

A G R E E M E N T W I T H U . S . D E PA R T M E N T O F J U S T I C E

In April 2003, Chiquita voluntarily informed the

U.S. Department of Justice (DOJ) that in order to

protect the lives and safety of its employees, its

banana-producing subsidiary in Colombia had

been forced to make protection payments to local

right- and left-wing paramilitary groups. Chiquita

approached the DOJ when senior management

became aware that payments to these groups

were prohibited under a U.S. antiterrorism law that

had changed in September 2001.

The payments made by the company were always

motivated by our good faith concern for the safety of

our employees. Since disclosing this information

four years ago, Chiquita has cooperated with the

DOJ investigation, sold its Colombian operations and

enhanced its compliance programs and procedures.

The aim of the company’s enhanced programs is to

foster transparency and to reinforce a strong culture

of ethics and compliance with our obligations under

U.S. law and in the jurisdictions around the world in

which we do business.

In March 2007, Chiquita reached an agreement

with the DOJ relating to the investigation. Under

terms of the agreement, Chiquita will pay a fine of

$25 million over five years and pleaded guilty to

one count of violating a U.S. law in connection with

payments made from 2001 to 2004 by its former

subsidiary to entities affiliated with “Autodefensas

Unidas de Colombia,” which had been designated

as a foreign terrorist organization. In anticipation

of this settlement, the company recorded a reserve

for $25 million in its financial statements for the

quarter and year ended Dec. 31, 2006.

C O R E VA L U E S C O N T I N U E T O G U I D EB U S I N E S S D E C I S I O N S

We are proud of our corporate responsibility

progress. In many parts of our company, such as in

the banana divisions and in the supply chain, our

corporate responsibility programs have generated

benefits in productivity and employee morale. As

a result, corporate responsibility is largely integrated

into the culture and daily life of these operations.

At the same time, we recognize that there is always

more that can be done. We have new businesses

and new employees who do not have a long history

with our corporate responsibility programs. So, it’s

important to help all our employees to understand

our Core Values, our ethical and legal obligations

and the benefits of our programs. We must continue

to integrate compliance and values into our decision-

making, and we need to implement these efforts

more consistently across the company.

While there will be many challenges and opportu-

nities ahead, our Core Values and Code of Conduct

will continue to guide management’s decisions.

For more information, please visit www.chiquita.comunder the “Corporate Responsibility” tab.

278879_text 4/12/07 3:24 PM Page 25

27

28

50

51

5253

54

55

5681

82

83

S TAT E M E N T O FM A N AG E M E N T R E S P O N S I B I L I T Y

M A N AG M E N T ’ S D I S C U S S I O N A N D A N A LYS I S O F F I N A N C I A L C O N D I T I O N A N D R E S U LT S O F O P E R AT I O N S

R E P O R T O F I N D E P E N D E N T R E G I S T E R E D P U B L I C AC C O U N T I N G F I R M O N F I N A N C I A L S TAT E M E N T S

R E P O R T O F I N D E P E N D E N T R E G I S T E R E D P U B L I C AC C O U N T I N G F I R M O N I N T E R N A L C O N T R O L O V E R F I N A N C I A L R E P O R T I N G

C O N S O L I D AT E D S TAT E M E N T O F I N C O M E

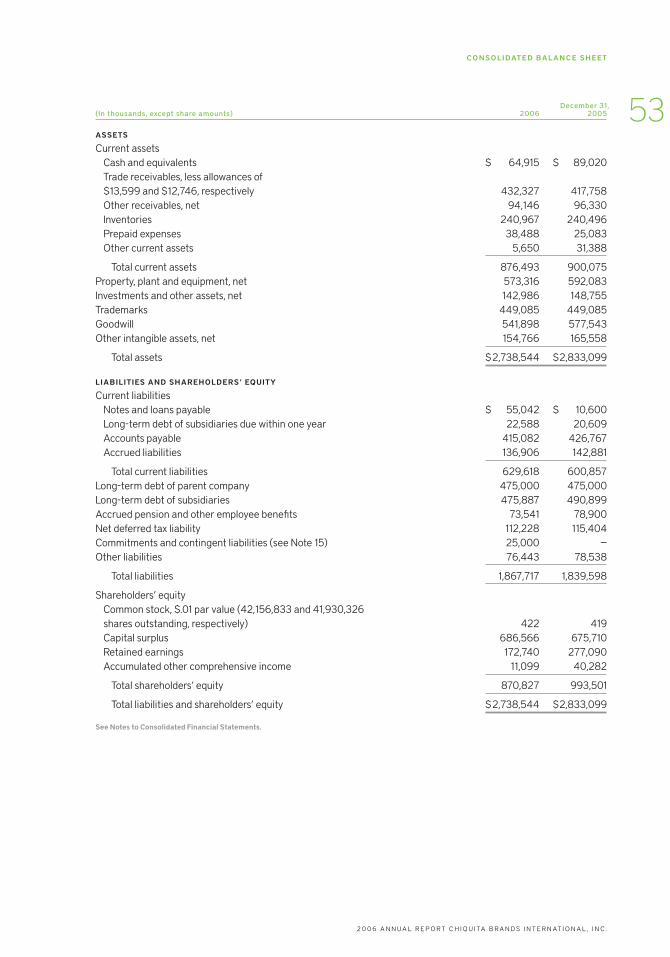

C O N S O L I D AT E D B A L A N C E S H E E T

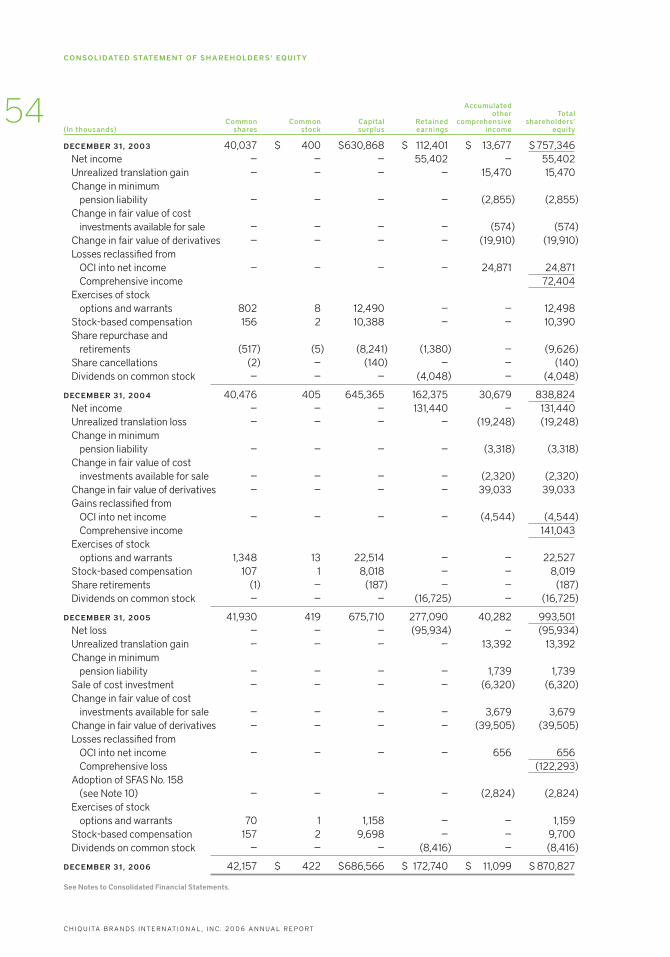

C O N S O L I D AT E D S TAT E M E N T O F S H A R E H O L D E R S ’ E Q U I T Y

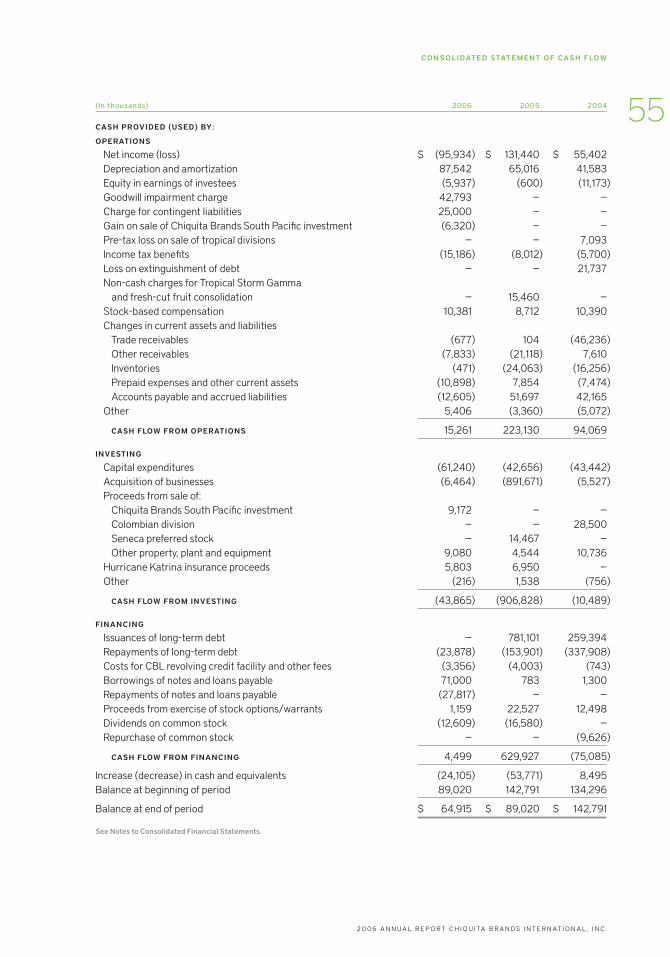

C O N S O L I D AT E D S TAT E M E N T O F CA S H F LO W

N OT E S TO C O N S O L I D AT E D F I N A N C I A L S TAT E M E N T S

S E L E CT E D F I N A N C I A L D ATA

B OA R D O F D I R E CTO R S , O F F I C E R S A N D S E N I O R O P E R AT I N G M A N AG E M E N T

I N V E S TO R I N FO R M AT I O N A N DC O M M O N S TO C KP E R FO R M A N C E G R A P H

F INANCIAL TABLE OF CONTENTS

278879_text 4/12/07 6:36 PM Page 26

The financial statements and related financial information presented in this Annual Report are the responsibility ofChiquita Brands International, Inc. management, which believes that they present fairly the company’s consol-idated financial position and results of operations in accordance with generally accepted accounting principles.

The company’s management is responsible for establishing and maintaining adequate internal controls. Thecompany has a system of internal accounting controls, which includes internal control over financial reportingand is supported by formal financial and administrative policies. This system is designed to provide reasonableassurance that the company’s financial records can be relied on for preparation of its financial statements andthat its assets are safeguarded against loss from unauthorized use or disposition.

The company also has a system of disclosure controls and procedures designed to ensure that material infor-mation relating to the company and its consolidated subsidiaries is made known to the company representativeswho prepare and are responsible for the company’s financial statements and periodic reports filed with theSecurities and Exchange Commission (“SEC”). The effectiveness of these disclosure controls and procedures isreviewed quarterly by management, including the company’s Chief Executive Officer and Chief FinancialOfficer. Management modifies these disclosure controls and procedures as a result of the quarterly reviews oras changes occur in business conditions, operations or reporting requirements.

The company’s worldwide internal audit function, which reports to the Audit Committee, reviews the adequacyand effectiveness of controls and compliance with the company’s policies.

Chiquita has published its Core Values and Code of Conduct which establish the company’s high standards forcorporate responsibility. The company maintains a hotline, administered by an independent company, thatemployees can use confidentially and anonymously to communicate suspected violations of the company’sCore Values or Code of Conduct, including concerns regarding accounting, internal accounting control or auditingmatters. Any reported accounting, internal accounting control or auditing matters are also forwarded directlyto the Chairman of the Audit Committee of the Board of Directors.

The Audit Committee of the Board of Directors consists solely of directors who are considered independentunder applicable New York Stock Exchange rules. One member of the Audit Committee, Roderick M. Hills, hasbeen determined by the Board of Directors to be an “audit committee financial expert” as defined by SEC rules.The Audit Committee reviews the company’s financial statements and periodic reports filed with the SEC, aswell as the company’s internal control over financial reporting including its accounting policies. In performingits reviews, the Committee meets periodically with the independent auditors, management and internal auditors,both together and separately, to discuss these matters.

The Audit Committee engages Ernst & Young, an independent registered accounting firm, to audit the company’sfinancial statements and its internal control over financial reporting and express opinions thereon. The scopeof the audits is set by Ernst & Young, following review and discussion with the Audit Committee. Ernst & Younghas full and free access to all company records and personnel in conducting its audits. Representatives ofErnst & Young meet regularly with the Audit Committee, with and without members of management present,to discuss their audit work and any other matters they believe should be brought to the attention of theCommittee. Ernst & Young has issued an opinion on the company’s financial statements. This report appearson page 50. Ernst & Young has also issued an audit report on management’s assessment of the company’sinternal control over financial reporting. This report appears on page 51.

MANAGEMENT’S ASSESSMENT OF THE COMPANY’S INTERNAL CONTROL OVER FINANCIAL REPORTING

The company’s management assessed the effectiveness of the company’s internal control over financialreporting as of December 31, 2006. Based on management’s assessment, management believes that, as ofDecember 31, 2006, the company’s internal control over financial reporting was effective based on the criteriain Internal Control – Integrated Framework, as set forth by the Committee of Sponsoring Organizations of theTreadway Commission (COSO).

FERNANDO AGUIRRE JEFFREY M . ZALLA BRIAN W. KOCHER

Chief Executive Officer Chief Financial Officer Chief Accounting Officer

27

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

STATEMENT OF MANAGEMENT RESPONSIB IL ITY

278879_Fin.qxp 4/9/07 3:57 PM Page 27

28

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

OVERVIEW

Chiquita Brands International, Inc. (“CBII”) and its subsidiaries (collectively, “Chiquita” or the company) operateas a leading international marketer and distributor of high-quality fresh and value-added produce, which is soldunder the Chiquita® premium brand, the Fresh Express® brand and other related trademarks. The company isone of the largest banana producers in the world and a major supplier of bananas in Europe and NorthAmerica. In June 2005, Chiquita acquired Fresh Express, the U.S. market leader in value-added salads, a fast-growing food category for grocery retailers, foodservice providers and quick-service restaurants. Theacquisition of Fresh Express increased Chiquita’s consolidated annual revenues by about $1 billion. The companybelieves that the acquisition diversified its business, accelerated revenue growth in higher margin value-addedproducts, and provided a more balanced mix of sales between Europe and North America, which makes thecompany less susceptible to risks unique to Europe, such as the European Union (“EU”) banana import regimeand foreign exchange risk. See Note 2 to the Consolidated Financial Statements for further information on thecompany’s 2005 acquisition of Fresh Express.

Significant financial items in 2006 included the following:

Net sales for 2006 were $4.5 billion, compared to $3.9 billion for 2005. The increase resulted from theacquisition of Fresh Express in June 2005.

The operating loss for 2006 was $28 million, compared to $188 million of operating income for 2005. The2006 results included a $43 million goodwill impairment charge related to Atlanta AG and a $25 millioncharge related to a potential settlement of a previously disclosed U.S. Department of Justice investigation.Operating income for 2005 included flood costs of $17 million related to Tropical Storm Gamma and a $6million charge related to the consolidation of fresh-cut fruit facilities in the Midwestern United States.

Operating cash flow was $15 million in 2006, compared to $223 million in 2005. The decline was primarilydue to the significant decline in operating results in 2006.

The company’s debt at both December 31, 2006 and 2005 was $1 billion. The balance at December 31, 2006included $44 million of borrowings on the company’s revolving credit facility to fund working capital needs.

In September 2006, the board of directors suspended the company’s quarterly cash dividend of $0.10 pershare on its outstanding shares of common stock.

Operating results in 2006 were significantly affected by regulatory changes in the European banana market,which resulted in lower local pricing and increased tariff costs, and by higher fuel and other industry costs.Neither the company nor the industry has been able to pass on the increased tariff costs to customers or consumers, although the company has been able to maintain its price premium in the European market.Comparisons to 2005 are also affected by the fact that 2005 was an unusually good year for banana pricing inEurope. Additionally, the company recorded a charge in 2006 in its Banana segment related to the U.S.Department of Justice investigation and a goodwill impairment charge related to Atlanta AG that affectedboth the Banana and Fresh Select segments. The Fresh Cut segment was significantly affected by consumerconcerns regarding the safety of packaged salad products, after discovery of E. coli in certain industry spinachproducts in September 2006 and the resulting investigation by the U.S. Food and Drug Administration (“FDA”).Although the FDA investigation linked no cases of illness to the company’s Fresh Express products, the industryissues related to fresh spinach products will likely continue to have a significant impact on Fresh Cut segmentresults through at least the third quarter of 2007.

278879_Fin.qxp 4/9/07 3:57 PM Page 28

29

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

In 2006, the company outlined its vision to become a global leader in branded, healthy, fresh foods, and refinedits strategic objectives to (i) become a consumer-driven, customer-preferred organization, (ii) be an innovative,high-performance organization, and (iii) deliver leading food industry shareholder returns. The company is continuing to focus on becoming a more consumer-centric organization and launching innovative products tomeet consumers’ growing desire for healthy, fresh and convenient food choices. In 2006, the company expandedits distribution of convenient, single “Chiquita-To-Go” bananas into 8,000 non-grocery convenience outlets.“Chiquita Fresh and Ready” was also introduced for testing in late 2006 in traditional grocery stores, as aninnovative way to keep bananas fresher four days longer. During the year, Fresh Express added 12 new offerings,including “5-Lettuce Mix” and “Sweet Butter” blends, to its line of ready-to-eat salad kits and premium value-added salads. Chiquita intends to continue providing value-added products and services in ways it believes better satisfy consumers, increase retailer profitability and boost the in-store presence of Chiquita and FreshExpress branded products.

The major risks facing the business include the EU tariff-only regime and related industry and pricing dynamics, weather and agricultural disruptions, consumer concerns regarding the safety of packaged salads, exchangerates, industry cost increases, risks of governmental investigations and other contingencies, and financing.

In January 2006, the European Commission implemented a new regime for the importation of bananas intothe EU. It eliminated the quota that was previously applicable and imposed a higher tariff on bananasimported from Latin America, while imports from certain African, Caribbean and Pacific (“ACP”) sources areassessed zero tariff on the first 775,000 metric tons imported. The new tariff, which increased to ¤176 from¤75 per metric ton, equates to an increase in cost of approximately ¤1.84 per box for bananas imported by the company into the EU from Latin America, Chiquita’s primary source of bananas. In 2006, the company incurred a net $75 million in higher tariff-related costs, which is the sum of $116 million in incremental tariffcosts minus $41 million in lower costs to purchase banana import licenses, which are no longer required. Inpart due to the elimination of the quota, the volume of bananas imported into the EU increased in 2006,which contributed to a decrease in the company’s average banana prices in core European markets of 11%on a local currency basis compared to 2005. The negative impact of the new regime has been substantialand is expected to continue indefinitely.

In 2006, the company incurred $25 million of higher sourcing, logistics and other costs for replacementfruit due to banana volume shortfalls caused by Hurricane Stan and Tropical Storm Gamma, whichoccurred in the fourth quarter of 2005. These storms, along with Hurricane Katrina in 2005, causedsignificant damage to banana cultivations and port facilities and resulted in increased costs for alternativebanana sourcing, logistics and farm rehabilitation, and write-downs of damaged farms. Additionally, in2007, Fresh Cut segment results for the first quarter are expected to be impacted by up to $4 million from arecord January freeze in Arizona which affected lettuce sourcing.

The company could be adversely affected by actions of regulators or a decline in consumer confidence inthe safety and quality of certain food products or ingredients, even if the company’s practices and proce-dures are not implicated. For example, consumer concerns regarding the safety of packaged salads in theUnited States, after discovery of E. coli in certain industry spinach products in September 2006, adverselyimpacted Fresh Express operations in the third and fourth quarters of 2006, resulting in lower sales andunforeseen costs, even though Fresh Express products were not implicated in these issues. As a result, thecompany may also elect or be required to incur additional costs aimed at restoring consumer confidence inthe safety of its products. The company incurred $9 million of direct costs in 2006, such as abandoned rawproduct inventory and non-cancelable purchase commitments, related to this spinach issue. In addition tothese direct costs, the company believes that 2006 operating income was approximately $12 million lowerthan it otherwise would have been, as a result of reduced sales and decreased margins. The companyexpects this issue will continue to negatively impact Fresh Cut segment results through at least the thirdquarter of 2007.

278879_Fin.qxp 4/9/07 3:57 PM Page 29

30

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

In 2006, the euro strengthened against the dollar, causing the company’s sales and profits to increase as aresult of the favorable exchange rate conversion of euro-denominated sales to U.S. dollars. The company’sresults are significantly affected by currency changes in Europe and, should the euro weaken against thedollar, it would adversely affect the company’s results. The company seeks to reduce its exposure toadverse effects of euro exchange rate movements by purchasing euro put option contracts. Currently, thecompany has hedging coverage for approximately 70% of its estimated net euro cash flow in 2007 at averageput option strike rates of $1.28 per euro and approximately 65% of its estimated net euro cash flow in thefirst half of 2008 at average strike rates of $1.27 per euro.

Transportation costs are significant in the company’s business, and the price of bunker fuel used in shippingoperations is an important variable component of transportation costs. The company’s fuel costs haveincreased substantially since 2003, and may increase further in the future. In addition, fuel and transportationcosts are a significant cost component of much of the produce that the company purchases from growersor distributors, and there can be no assurance that the company will be able to pass on such increased coststo its customers. The company enters into hedge contracts which permit it to lock in fuel purchase prices forup to three years on up to 75% of the fuel consumed in its ocean shipping fleet, and thereby minimize thevolatility that fuel prices could have on its operating results. However, these hedging strategies cannot fullyprotect against continually rising fuel rates and entail the risk of loss if market fuel rates decline (see Note 8to the Consolidated Financial Statements). At December 31, 2006, the company had 55% hedging coveragethrough the end of 2009 on fuel consumed in its banana shipments to core markets in North America andEurope; in relation to market forward fuel prices at December 31, 2006, these hedge positions entailedlosses of $3 million in 2007, $5 million in 2008, and $2 million in 2009.

The cost of paper and plastics are also significant to the company because bananas and some other produceitems are packed in cardboard boxes for shipment, and packaged salads are shipped in sealed plastic bags.If the price of paper and/or plastics increases, or results in a higher cost to the company to purchase freshproduce, and the company is not able to effectively pass these price increases along to its customers, thenthe company’s operating income will decrease. Increased costs of paper and plastics have negativelyimpacted the company’s operating income in the past, and there can be no assurance that these costs willnot adversely affect the company’s operating results in the future.

The company has international operations in many foreign countries, including in Central and SouthAmerica, the Philippines and the Ivory Coast. These activities are subject to risks inherent in operating inthose countries, including government regulation, currency restrictions and other restraints, burdensometaxes, risks of expropriation, threats to employees, political instability, terrorist activities, including extortion,and risks of U.S. and foreign governmental action in relation to the company. Should such circumstancesoccur, the company might need to curtail, cease or alter activities in a particular region or country and maybe subject to fines or other penalties. The company’s ability to deal with these issues may be affected byapplicable U.S. or other applicable law. See Note 15 to the Consolidated Financial Statements for a descriptionof (i) a $25 million financial sanction contained in a plea agreement offer made by the company to the U.S.Department of Justice and relating to payments made by the company’s former banana producing subsidiary in Colombia to certain groups in that country which had been designated under United Stateslaw as a foreign terrorist organization, (ii) an investigation by EU competition authorities relating to priorinformation sharing in Europe and (iii) customs proceedings in Italy.

278879_Fin.qxp 4/9/07 3:57 PM Page 30

31

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

The company has $1 billion outstanding in total debt, most of which is issued under debt agreements thatrequire continuing compliance with financial covenants. The most restrictive of these covenants are in thecompany’s bank credit facility, which includes a $200 million revolving credit facility and $394 million ofoutstanding term loans (the “CBL Facility”). In 2006, after seeking prospective covenant relief in June, thecompany needed to seek further covenant relief later in the year. In October, the company obtained a temporary waiver, for the period ended September 30, 2006, from compliance with certain financialcovenants in the CBL Facility, with which the company otherwise would not have been in compliance. InNovember, the company obtained a permanent amendment to the CBL Facility to cure the covenant violations that would have otherwise occurred when the temporary waiver expired. In March 2007, thecompany obtained further prospective covenant relief with respect to a proposed financial sanction contained in a plea agreement offer made by the company to the U.S. Department of Justice and otherrelated costs. If the company’s financial performance were to decline compared to lender expectations, thecompany could in the future be required to seek further covenant relief from its lenders, or to restructure orreplace its credit facility, which would further increase the cost of the company’s borrowings, restrict itsaccess to capital, and/or limit its operating flexibility.

As of February 28, 2007, the company had borrowed $84 million under its revolving credit facility, andexpects to make additional draws to fund peak seasonal working capital needs through March or April2007. Another $29 million of capacity was used to issue letters of credit, including a $7 million letter ofcredit issued to preserve the right to appeal certain customs claims in Italy. During 2007, the company maybe required to issue up to an additional $25 million of letters of credit for appeal bonds relating to litigationof additional customs claims in Italy. The company believes that operating cash flow, including the collectionof receivables from high season banana sales, should permit it to significantly reduce the revolving creditbalance during the second quarter and to fully repay it during the third quarter; however, there can be noassurance in this regard. In order to ensure adequate liquidity, in the event that the company experiencesshortfalls in operating performance or unanticipated contingencies which require the use of significantamounts of cash, the company may be limited in its ability to fund discretionary market or brand-supportactivities, innovation spending, capital investments and/or acquisitions that had been planned as part ofthe execution of its long-term growth strategy.

278879_Fin.qxp 4/9/07 3:57 PM Page 31

32

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

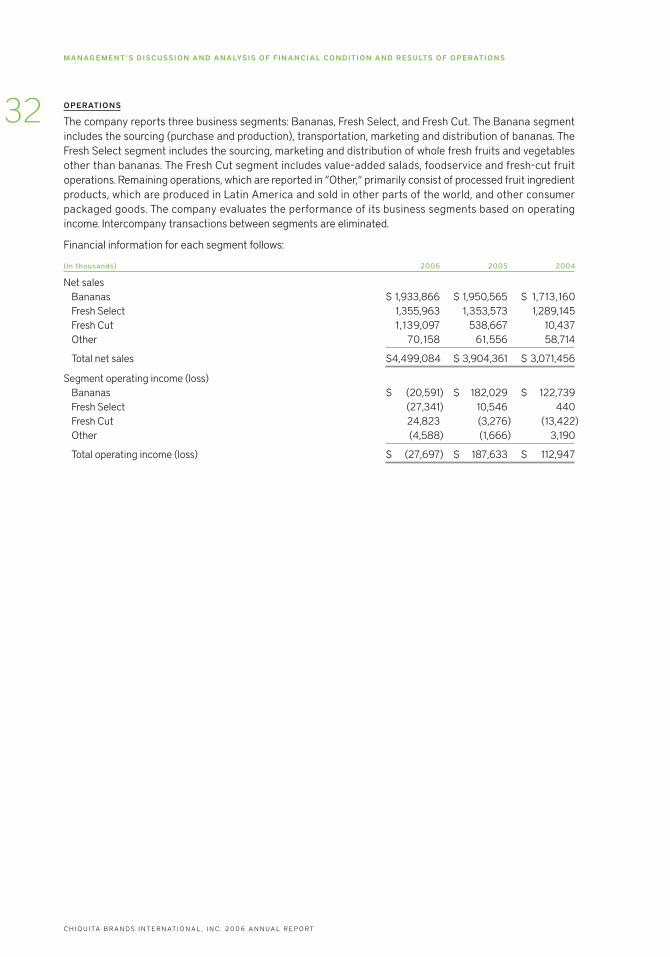

OPERATIONS

The company reports three business segments: Bananas, Fresh Select, and Fresh Cut. The Banana segmentincludes the sourcing (purchase and production), transportation, marketing and distribution of bananas. TheFresh Select segment includes the sourcing, marketing and distribution of whole fresh fruits and vegetablesother than bananas. The Fresh Cut segment includes value-added salads, foodservice and fresh-cut fruit operations. Remaining operations, which are reported in “Other,” primarily consist of processed fruit ingredientproducts, which are produced in Latin America and sold in other parts of the world, and other consumer packaged goods. The company evaluates the performance of its business segments based on operatingincome. Intercompany transactions between segments are eliminated.

Financial information for each segment follows:

(In thousands) 2006 2005 2004

Net salesBananas $ 1,933,866 $ 1,950,565 $ 1,713,160Fresh Select 1,355,963 1,353,573 1,289,145Fresh Cut 1,139,097 538,667 10,437Other 70,158 61,556 58,714

Total net sales $4,499,084 $ 3,904,361 $ 3,071,456

Segment operating income (loss)Bananas $ (20,591) $ 182,029 $ 122,739Fresh Select (27,341) 10,546 440Fresh Cut 24,823 (3,276) (13,422)Other (4,588) (1,666) 3,190

Total operating income (loss) $ (27,697) $ 187,633 $ 112,947

278879_Fin.qxp 4/9/07 3:57 PM Page 32

33

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

BANANA SEGMENT

Net sales

Banana segment net sales for 2006 decreased 1% versus 2005. The decrease resulted from lower bananapricing in Europe, which was mostly offset by higher volume in Europe and improved pricing in North America.

Net sales for 2005 increased 14% versus 2004. The increase resulted primarily from improved banana pricingin both Europe and North America.

Operating income

2006 compared to 2005. The Banana segment operating loss for 2006 was $21 million, compared to operatingincome of $182 million for 2005. Banana segment operating results were adversely affected by:

$110 million from lower European local banana pricing, attributable in part to increased banana volumesthat entered the market, encouraged by regulatory changes that expanded the duty preference for Africanand Caribbean suppliers and eliminated quota limitations for Latin American fruit, as well as reduced consumption driven by unseasonably hot weather in many parts of Europe during the third quarter.

$75 million of net incremental costs associated with higher banana tariffs in the European Union. This consisted of approximately $116 million of incremental tariff costs, reflecting the duty increase to ¤176from ¤75 per metric ton effective January 1, 2006, offset by approximately $41 million of expensesincurred in 2005 to purchase banana import licenses, which are no longer required.

$54 million of industry cost increases for fuel, fruit, paper and ship charters.

$25 million of higher sourcing, logistics and other costs for replacement fruit due to banana volume shortfalls caused by Hurricane Stan and Tropical Storm Gamma, which occurred in the fourth quarter 2005.

$25 million charge for potential settlement of a contingent liability related to the Justice Department investigation related to the company’s former Colombian subsidiary.

$14 million goodwill impairment charge related to Atlanta AG.

$12 million in higher professional fees related to previously-reported legal proceedings, including theJustice Department investigation, the EU competition law investigation, and U.S. anti-trust litigation.

These adverse items were offset in part by:

$23 million of net cost savings in the Banana segment, primarily related to efficiencies in the company’ssupply chain and tropical production operations.

$21 million from higher pricing in North America.

$20 million from lower marketing costs, primarily in Europe.

$17 million impact from 2005 flooding in Honduras as a result of Tropical Storm Gamma, which did notrecur in 2006.

$13 million benefit from the impact of European currency, consisting of a $23 million favorable variancefrom balance sheet translation and a $1 million increase in revenue, partially offset by $9 million ofincreased hedging costs and $2 million of higher European costs due to a stronger euro.

$11 million of costs related to flooding in Costa Rica and Panama in the first half of 2005 that did not repeatin 2006.

$10 million from lower accruals for performance-based compensation due to lower operating results relative to targets.

278879_Fin.qxp 4/9/07 3:57 PM Page 33

34

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

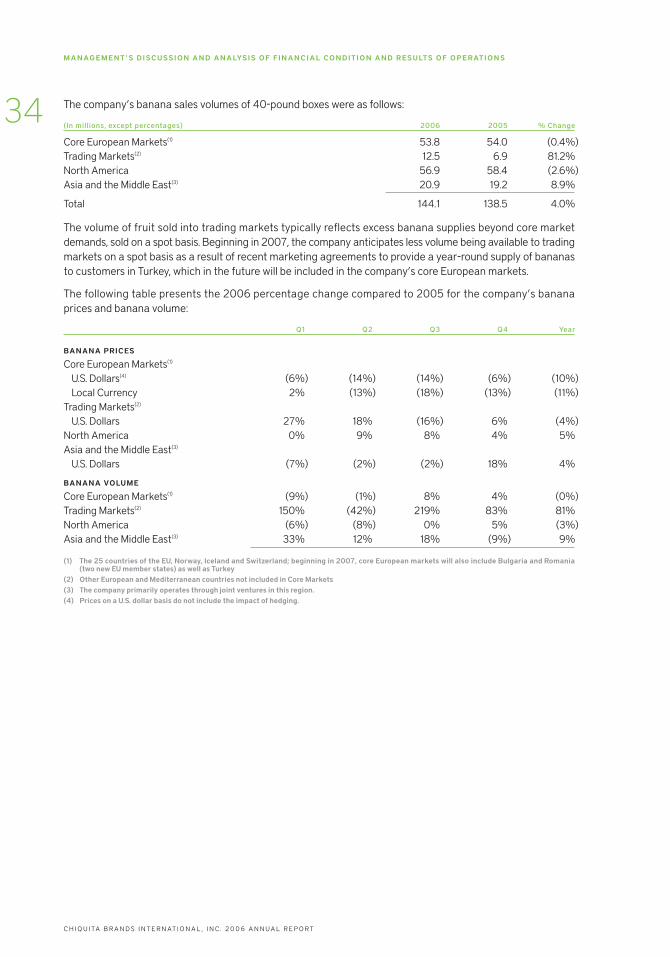

The company’s banana sales volumes of 40-pound boxes were as follows:

(In millions, except percentages) 2006 2005 % Change

Core European Markets(1) 53.8 54.0 (0.4%)Trading Markets(2) 12.5 6.9 81.2%North America 56.9 58.4 (2.6%)Asia and the Middle East(3) 20.9 19.2 8.9%

Total 144.1 138.5 4.0%

The volume of fruit sold into trading markets typically reflects excess banana supplies beyond core marketdemands, sold on a spot basis. Beginning in 2007, the company anticipates less volume being available to tradingmarkets on a spot basis as a result of recent marketing agreements to provide a year-round supply of bananasto customers in Turkey, which in the future will be included in the company’s core European markets.

The following table presents the 2006 percentage change compared to 2005 for the company’s bananaprices and banana volume:

Q1 Q2 Q3 Q4 Year

BANANA PRICES

Core European Markets(1)

U.S. Dollars(4) (6%) (14%) (14%) (6%) (10%)Local Currency 2% (13%) (18%) (13%) (11%)

Trading Markets(2)

U.S. Dollars 27% 18% (16%) 6% (4%)North America 0% 9% 8% 4% 5%Asia and the Middle East(3)

U.S. Dollars (7%) (2%) (2%) 18% 4%

BANANA VOLUME

Core European Markets(1) (9%) (1%) 8% 4% (0%)Trading Markets(2) 150% (42%) 219% 83% 81%North America (6%) (8%) 0% 5% (3%)Asia and the Middle East(3) 33% 12% 18% (9%) 9%

(1) The 25 countries of the EU, Norway, Iceland and Switzerland; beginning in 2007, core European markets will also include Bulgaria and Romania(two new EU member states) as well as Turkey

(2) Other European and Mediterranean countries not included in Core Markets(3) The company primarily operates through joint ventures in this region.(4) Prices on a U.S. dollar basis do not include the impact of hedging.

278879_Fin.qxp 4/9/07 3:57 PM Page 34

35

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

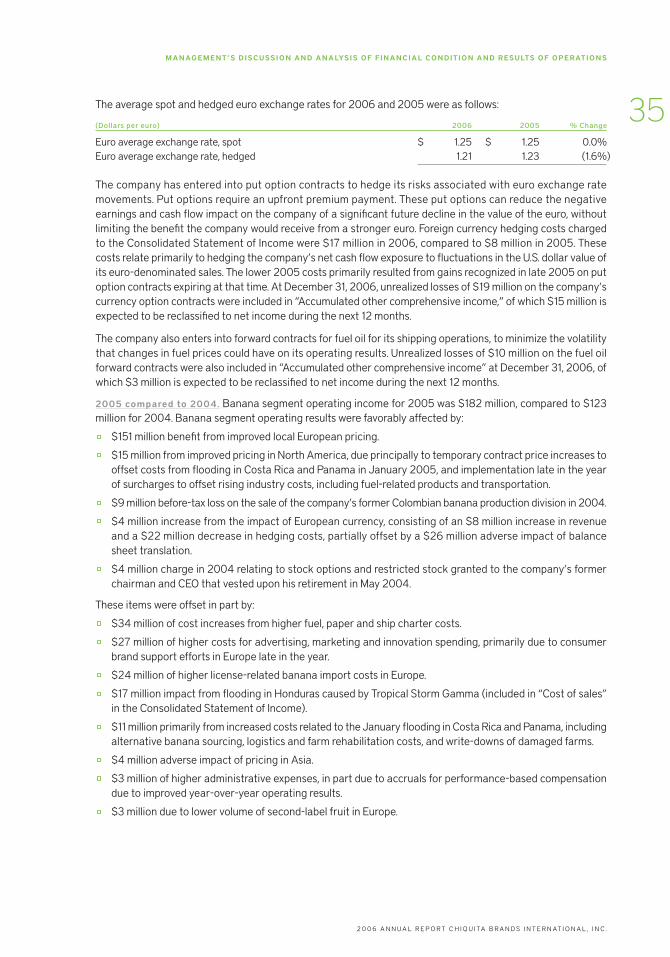

The average spot and hedged euro exchange rates for 2006 and 2005 were as follows:

(Dollars per euro) 2006 2005 % Change

Euro average exchange rate, spot $ 1.25 $ 1.25 0.0%Euro average exchange rate, hedged 1.21 1.23 (1.6%)

The company has entered into put option contracts to hedge its risks associated with euro exchange ratemovements. Put options require an upfront premium payment. These put options can reduce the negativeearnings and cash flow impact on the company of a significant future decline in the value of the euro, withoutlimiting the benefit the company would receive from a stronger euro. Foreign currency hedging costs chargedto the Consolidated Statement of Income were $17 million in 2006, compared to $8 million in 2005. Thesecosts relate primarily to hedging the company’s net cash flow exposure to fluctuations in the U.S. dollar value ofits euro-denominated sales. The lower 2005 costs primarily resulted from gains recognized in late 2005 on putoption contracts expiring at that time. At December 31, 2006, unrealized losses of $19 million on the company’scurrency option contracts were included in “Accumulated other comprehensive income,” of which $15 million isexpected to be reclassified to net income during the next 12 months.

The company also enters into forward contracts for fuel oil for its shipping operations, to minimize the volatilitythat changes in fuel prices could have on its operating results. Unrealized losses of $10 million on the fuel oil forward contracts were also included in “Accumulated other comprehensive income” at December 31, 2006, ofwhich $3 million is expected to be reclassified to net income during the next 12 months.

2005 compared to 2004. Banana segment operating income for 2005 was $182 million, compared to $123million for 2004. Banana segment operating results were favorably affected by:

$151 million benefit from improved local European pricing.

$15 million from improved pricing in North America, due principally to temporary contract price increases tooffset costs from flooding in Costa Rica and Panama in January 2005, and implementation late in the yearof surcharges to offset rising industry costs, including fuel-related products and transportation.

$9 million before-tax loss on the sale of the company’s former Colombian banana production division in 2004.

$4 million increase from the impact of European currency, consisting of an $8 million increase in revenueand a $22 million decrease in hedging costs, partially offset by a $26 million adverse impact of balancesheet translation.

$4 million charge in 2004 relating to stock options and restricted stock granted to the company’s formerchairman and CEO that vested upon his retirement in May 2004.

These items were offset in part by:

$34 million of cost increases from higher fuel, paper and ship charter costs.

$27 million of higher costs for advertising, marketing and innovation spending, primarily due to consumerbrand support efforts in Europe late in the year.

$24 million of higher license-related banana import costs in Europe.

$17 million impact from flooding in Honduras caused by Tropical Storm Gamma (included in “Cost of sales”in the Consolidated Statement of Income).

$11 million primarily from increased costs related to the January flooding in Costa Rica and Panama, including alternative banana sourcing, logistics and farm rehabilitation costs, and write-downs of damaged farms.

$4 million adverse impact of pricing in Asia.

$3 million of higher administrative expenses, in part due to accruals for performance-based compensationdue to improved year-over-year operating results.

$3 million due to lower volume of second-label fruit in Europe.

278879_Fin.qxp 4/9/07 3:57 PM Page 35

36

C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C . 2 0 0 6 A N N U A L R E P O R T

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

FRESH SELECT SEGMENT

Net sales

Fresh Select net sales were flat at $1.4 billion in 2006 compared to 2005. Net sales for 2005 increased by 5%compared to 2004, primarily due to higher volume from Atlanta AG.

Operating income

2006 compared to 2005. The Fresh Select segment had an operating loss of $27 million in 2006, comparedto operating income of $10 million in 2005. The 2006 operating results included a $29 million charge for goodwillimpairment at Atlanta AG. Aside from the impairment charge, year-over-year improvements in the company’sNorth American Fresh Select operations were more than offset by a decline in profitability at Atlanta AG, andlower pricing and currency-related declines in the company’s Chilean operations. The decline in profitability ofAtlanta AG resulted from intense price competition in its primary market of Germany, as well as $3 million ofcharges late in 2006 related to rationalization of its distribution network, including the closure of one facility.

During the 2006 third quarter, due to the decline in Atlanta AG’s business performance in the period followingthe implementation of the new EU banana import regime as of January 1, 2006, the company accelerated thetesting of Atlanta’s goodwill and fixed assets for impairment. As a result, the company recorded a goodwillimpairment charge in the 2006 third quarter for the full amount, of which $29 million was included in the FreshSelect segment and $14 million in the Banana segment.

2005 compared to 2004. The Fresh Select segment had operating income of $10 million in 2005, comparedto breakeven results for 2004. The improvement resulted primarily from a restructured melon program andother improvements in North America, and operational improvement at Atlanta, partially offset by weather andcurrency-related declines in the company’s Chilean operations.

278879_Fin.qxp 4/9/07 3:57 PM Page 36

37

2 0 0 6 A N N U A L R E P O R T C H I Q U I TA B R A N D S I N T E R N AT I O N A L , I N C .

MANAGEMENT’S D ISCUSSION AND ANALYSIS OF F INANCIAL CONDIT ION AND RESULTS OF OPERATIONS

FRESH CUT SEGMENT

Net sales

Net sales in 2006 for the company’s Fresh Cut segment were $1.1 billion, up from $539 million in 2005 due to theFresh Express acquisition in mid-2005. Substantially all of the revenue in this segment is from Fresh Express.

Operating income

2006 compared to 2005. The Fresh Cut segment had operating income of $25 million in 2006, compared toan operating loss of $3 million for 2005. Fresh Cut segment results were favorably affected by:

$31 million increase in operating income from Fresh Express, as a result of Chiquita owning Fresh Express fora full year in 2006 versus a half year in 2005, as well as normal operating improvements.

$6 million of mostly non-cash charges in 2005 from the shut-down of Chiquita’s fresh-cut fruit facility inManteno, Illinois following the acquisition of Fresh Express, which had a facility servicing the sameMidwestern area.

These items were offset in part by:

$9 million of direct costs in 2006, including lost raw product inventory and non-cancelable purchase commitments, related to consumer concerns about the safety of packaged salads after discovery of E. coliin certain industry spinach products in September 2006 and the resulting investigation by the U.S. Food andDrug Administration.

In addition to the direct costs resulting from the fresh spinach issue, the company believes that 2006 operatingincome was at least $12 million lower than it otherwise would have been as a result of reduced sales anddecreased margins during the final four months of 2006. Although the FDA investigation linked no cases of illness to the company’s Fresh Express products, consumer concerns are likely to continue to have an impact onFresh Cut segment results through at least the third quarter of 2007.