Embed Size (px)

Citation preview

ARTICLE IN PRESS

Contents lists available at ScienceDirect

Int. J. Production Economics

Int. J. Production Economics 115 (2008) 374– 387

0925-52

doi:10.1

� Cor

E-m

kimmo.

jukka.h

journal homepage: www.elsevier.com/locate/ijpe

Chinese ICT industry from supply chain perspective—A case study ofthe major Chinese ICT players

Lei Yu a, Kimmo Suojapelto b, Jukka Hallikas b, Ou Tang a,�

a Department of Management and Engineering, Linkoping Institute of Technology, SE-58183 Linkoping, Swedenb Technology Business Research Center, Lappeenranta University of Technology, P.O. Box 20, FI-53851 Lappeenranta, Finland

a r t i c l e i n f o

Article history:

Received 30 September 2006

Accepted 4 March 2008Available online 22 June 2008

Keywords:

ICT

Supply chain

Chinese case

73/$ - see front matter & 2008 Elsevier B.V. A

016/j.ijpe.2008.03.011

responding author. Tel.: +46 13 281773; fax: +

ail addresses: [email protected] (L. Yu),

[email protected] (K. Suojapelto),

[email protected] (J. Hallikas), [email protected] (O. T

a b s t r a c t

Having emerged in the middle of the 20th century, the information and communication

technology (ICT) industry has sprung up during the past 20 years. China plays a

significant role within the ICT segment in that it has become a major supplier and a fast

growing market in the world. This paper, based on interviews in 2006 with nine

important Chinese ICT companies, identifies the supply network structure for Chinese

ICT industry and its value-adding opportunities. The essential finding is that the

domestic operators are the focal companies within the Chinese ICT supply network. This

result is further verified by an alliance analysis using the UCINET software.

& 2008 Elsevier B.V. All rights reserved.

1. Introduction

The information and communication technology (ICT)sector has fostered the growth of several developed anddeveloping regional areas. One of the most interestingregional areas is China. According to a report by OECD(2004), the Organization for Economic Co-operation andDevelopment, the production of ICT goods and ICT-relatedservices are shifting towards China. Moreover, its largestpopulation in the world and fast economic developmentnowadays provide an enormous market for ICT-relatedproducts and services. For instance, Cisco, Ericsson, IBM,Intel, Nokia, Microsoft, Motorola, Samsung and Siemens,all have their subsidiaries in China where all of themoperate well in terms of revenues. For example, asmentioned by Guzman (2006), China is Nokia’s biggestmarket and its revenue in 2005 was h3.4 billion, followedby the USA with h2.7 billion. There are, however, alsonative Chinese ICT companies that play an important role

ll rights reserved.

46 13 281101.

ang).

within the global ICT industry. For instance, Huawei isacknowledged as the fourth largest GSM network providerin the world by Bengt Nordstrom, the branch analyzerin Incode Wireless (Andersson, 2006), according tothe market share of the GSM network. As the mostadopted 2G mobile standard in terms of the number ofsubscribers, GSM accounted for a growth of 53.2 millionsubscribers in China in 2005, which stands for more than1/8 of the growth in the global GSM subscribers(Andersson, 2006). China Mobile, the mobile networkoperator in China, is now the world’s largest ICTcompany in terms of its market capitalization (ThomsonONE Banker, 2006). Table 1 illustrates the key financialstatements of the four most important operators inChina and it further shows evidence of the fastgrowth in the development of ICT-related services inChina.

The ongoing convergence of various technologies andservices from traditional telecommunication, IT (informa-tion technology), media and the Internet is changing thestructure of the global ICT supply chain network. Forinstance, the emergence of 3G technologies not onlyinvolves providing the system equipment and operatingthe basic services such as voice services, which exist in thetraditional supply chain network, but also brings into the

ARTICLE IN PRESS

Table 1Key financial statements of major Chinese operators (1)

Key financial statements (2006-12-31)

Total assets (million h) 5-year growth (%) Annual sale (million h) 5-year growth (%) Net income (million h) 5-year growth (%)

China mobile 47,372 103 28,118 107 6286 65

China netcom 19,469 �22 8275 25 1061 5

China telecom 39,173 56 17,012 83 2637 182

China unicom 14,198 �18 8977 125 355 �41

IT(Goods & services

Telecommunications(Goods & services

including manufactures)

TransmissionNetworking

Onlineincluding

interactive

Offline

Informationcontent

(Film production,

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387 375

ICT supply chain more links in the form of content,applications, software, chips and tests, which makes theICT supply chain more complicated and leads to newbusiness models for value creating and adding within theICT sector. Therefore, studying the value creating andadding within the ICT sector becomes an interesting topic.In our viewpoint, the existing body of supply chainliterature provides an additional platform to identify therole of players, their interactions and the value creatingand adding opportunities in the ICT industry, which arealso the major objectives of this paper. Consequently, theICT development trends in China can be forecasted. Thus,in order to achieve the above objectives, we formulate thefollowing research questions:

includingmanufactures) multimedia information

services & themedia)

� What are the typical characteristics of the Chinese ICTindustry?

�Fig. 1. Overlap between the IT, telecommunications and information

What are the major driving forces and uncertaintiesthat influence the development of the Chinese ICTindustry?

content activities of firms (OECD, 2007).

� What are the future trends of the ICT industry inChina?The rest of the paper is arranged as follows: Section 2examines the ICT industry, reviews the supply chainframework adopted in this paper and introduces theconcept of alliance and networks; in Section 3, themethodology of identifying the Chinese ICT supply net-work structure is described in detail. The supply networkstructure of the Chinese ICT industry is addressed inSection 4, and the alliance analysis is adopted here inorder to verify the proposed supply network structure.Section 5 concludes our research findings and describesthe possible future research streams.

2. Literature

In this paper, the ICT sector is the research focus. Thesupply chain approach is adopted to identify the supplychain network structure of the Chinese ICT industry,which is then verified by an alliance analysis. Therefore,the definition of ICT, supply chain framework and allianceand networks are introduced in this section in order toprovide a theoretical background.

2.1. Defining ICT sector

The OECD categorizes the whole ICT industry into twosectors (OECD, 2002; Nielsen, 2000):

�

for the manufacturing industries, the products of acandidate industry:J must be intended to fulfil the function of informa-tion processing and communication includingtransmission and display;

�

must use electronic processing to detect, measure and/or record physical phenomena or to control a physicalprocess; � for the services industries, the products of a candidateindustry:J must be intended to enable the function of

information processing and communication byelectronic means.

OECD (2007) also illustrates the ICT sector as in Fig. 1and provides a literal interpretation by which the ICTsector can be viewed as the activities that fall within theunion of the IT and telecommunications activities in thediagram. It includes therefore the intersections between

ARTICLE IN PRESS

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387376

them and the information content activities. However, itexcludes those information content activities that falloutside those intersections; that is, those which have nodirect ICT association.

Similarly, Gruber (2001) defines ICT as the technologi-cal convergence of the IT and telecommunication technol-ogy. We adopt this definition of ICT in this paper.Additionally, the categorization of the ICT industry intothe manufacturing and service sectors is also consideredin this study.

2.2. Supply chain framework

The supply chain, a society (a network of members,termed a group) formed by autonomous entities (andtheir systems) by bonding together to solve a commonproblem (Chandra and Kumar, 2001), has been a keentopic for both the academia and the practitioners for along time (Cousins et al., 2006). Supply chain manage-ment (SCM) is defined by the Global Supply Chain Forumas the integration of key business processes from endusers through original suppliers that provide products,services and information, which add value for customersand other stakeholders (Lambert et al., 1998; Lambert andCooper, 2000). Christopher (1998) defines SCM as themanagement of upstream and downstream relationshipswith suppliers and customers to deliver superior customervalue at less cost to the supply chain as a whole. The scopeof SCM could be either the management of the internalsupply chain within an organization which provides valueto its customers, or the management of the supply chainwhich involves a set of organizations that deliver valuethrough original suppliers to the end customers.

Lambert et al. (1998), Lambert and Cooper (2000) andCooper et al. (1997) provide an SCM framework thatconsists of three interrelated elements within the supplychain: the network structure, business processes andmanagement components. The implementation of SCMinvolves identifying the supply chain members, withwhom it is critical to link, what processes need to belinked with each of these key members and what type orlevel of integration applies to each process link. From theabove, we can deduce that identifying the supply chainnetwork structure is the basis within SCM: only after thesupply chain network structure has been identified, theother two elements can be further analyzed. Therefore,this paper focuses on finding out the supply chainnetwork structure of the ICT industry in China. Twoissues are outlined here:

�

the individual supply chain members; � and the configuration of the supply chain memberswithin the supply chain as well as their commonobjective.

Tan (2001) classifies the studies on SCM into twofunctional trends, the purchasing and supply perspective,and the transportation and logistics perspective fromwhich the research of SCM originates (Christopher, 1998).The denotations of these two concepts imply their

different emphases. The former perspective focuses onimproving the efficiency and competitive advantage ofmanufacturers by taking advantage of the immediatesupplier’s capability and technology, while the latter one’sprimary focus is the efficient physical distribution of finalproducts from the manufacturers to the end users in anattempt to replace inventories with information. In thispaper, we emphasize the purchasing and supply perspec-tive and construct the supply chain network according tothe supply–demand relationships of the different supplychain members for the Chinese ICT industry.

The contextual focus of the supply chain literature ismostly related to manufacturing (Burgess et al., 2006).Although there are also papers using the supply chainframework to deal with manufacturing issues in the ICTindustry, for example, electronics (Berry et al., 1994),mobile infrastructure (Collin and Lorenzin, 2006), mobilehandsets (Olhager et al., 2002; Catalan and Kotzab, 2003)and risk management of the telecommunication manufac-turing segment (Agrell et al., 2004; Norrman and Jansson,2004), there is only little supply chain literature describingthe entire ICT industry including the service sector.Kemppainen and Vepsalainen (2003) present the industrialscope of supply chain as one of the interesting themes forboth academia and practitioners. Our study focuses on theindustrial scope of the supply chain regarding the wholeICT industry instead of merely concentrating on the ICTmanufacturing sector or the supply chain for a single ICTcompany. In this case, a holistic view concerning the entireICT industry could be obtained.

2.3. Alliances and networks

It can be argued that industries emerge from networksof relationships with various interdependent organiza-tions. A network analysis focuses on the relations amongactors, and not individual actors and their attributes(Hanneman and Riddle, 2005). In this paper, we alsoinvestigate the alliance relationships between organiza-tions since a lot of inter-firm collaboration takes place inalliance relationships with actors in industry networks.According to Doz and Hamel (1999), alliance relationshipsdiffer from the traditional market transactions in that theycan be characterized as strategic collaborative relation-ships with companies. They state that alliance relation-ships are essential in global competition since they allowthe sharing of complementary resources between organi-zations. Furthermore, the inherent uncertainty in thebusiness environment requires the formulation of alli-ances and collaborative learning processes. Recent alli-ance research has indicated that firms are utilizingstrategic alliances in the execution of specific businessstrategies (Yasuda and Iijima, 2005). Thus the explorationof structural position in the industry alliance network isabout to provide interesting insights into the strategicpositioning of the companies on an industrial level.

There are several methods to analyze collaborationactivities and network centrality. Degree centrality can beused as a comparison to measure the absolute number ofalliances formed by firms. The alliance degree measure

ARTICLE IN PRESS

Table 2The categorization of the ICT supply chain members

Supply chain

members

Functionality

Within ICT industry

EP Providing equipment: network infrastructure,

handsets, etc.

AP Providing applications: software etc.

SP Providing service platforms

CP Providing contents: music, pictures, mobile games,

etc.

Operator The government has authorized owning the basic

network infrastructure, through which various

services can be provided to end users

Outside ICT industry

Regulator The organization to constitute the various industrial

regulations

End user Ultimate customers who consume the devices and

various services

Intermediary Selling the handsets or SIM cards to the customers

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387 377

represents the scale and volume of network formation;however, it does not take into account the structuralimportance of alliance partners, i.e. with whom thealliance is formed in a network. Betweenness can beemployed as a measure to analyze the actors’ orcompanies’ structural position in the network (see e.g.Wasserman and Faust, 1994;). By following Borgatti(2005), betweenness is defined as the share of times theactor k is needed to the shortest (geodesic) pathwaysbetween other pairs of actors i and j. Here, if gij isthe number of geodesic paths from i to j, and gikj is thenumber of these geodesics that pass through node k, thebetweenness of node k is

X

i

X

j

gikj

gij

; iajak (1)

Based on the above-mentioned betweenness and degreecentrality calculations, the UCINET analysis can finally beused to formulate the structural network analysis. UCINETalso includes a graphical illustration tool based on thissoftware. For example, Borgatti et al. (1992) havepresented a profound introduction to the UCINET softwarein their network research.

3. Methodology and data collection

The methodology of this study contains both qualitativeand quantitative methods. Principal data for identifying thesupply chain network structure of the Chinese ICT industrycome from the interviews with nine essential Chinese ICTplayers (see Table 3). In addition, we use alliance analysis, aquantitative method, to verify the network structuredeveloped for the Chinese ICT industry. Since the methodof alliance analysis has been presented in Section 2.3, herewe focus on the details of the interviews.

3.1. Methodology and limitations

The interviews were conducted in China in July 2006.There were nine interviews and the average duration ofeach interview was 3 h. The interviews were documentedand transcribed for analysis.

In order to make the interviews more efficient, thespecific situation for the Chinese ICT industry was pre-studied before the interviews. The categorization of thedifferent roles within the ICT industry provided byHallikas et al. (2005) was condensed from 25 groups tofive key categories: the equipment provider (EP), applica-tion provider (AP), service provider (SP), content provider(CP) and operator, which are attributed to as supply chainmembers within the ICT industry. The supply chainmembers outside the ICT industry include the regulator,end user and intermediary. The major functions of thesesupply chain members are collected in Table 2, and thesesupply chain members are described in more detail inSection 4. It should be mentioned, however, that for thesupply chain members within the ICT industry, the EPsometimes also acts as an application provider, while theSP often covers what the CP does. Therefore, we note themas EP/AP and SP/CP in this paper.

Due to confidentiality, the quantitative data obtainedfrom the interviews cannot be published, and becausetime and resources were limited, the supply chainmembers cannot be divided into a more detailed level.On the other hand, the scope of this research has beenlimited geographically within the Chinese mainland,which does not include Hong Kong, Macau and Taiwan.These three areas have their special policies and situationsin the ICT industry, which should be studied individually.

3.2. Selection of interviews

Because of the limited time and resources, the criteriafor the selection of the companies to be interviewedbecame essential. The following three aspects wereconsidered within the company selection procedure:

�

Selection of the geographical regions: there are three mostimportant regions in China concerning the ICT industry:Pearl River Delta Area, Yangtze River Delta Area and BoSea Gulf Area. The Pearl River Delta Area is the high-techarea for the ICT industry with the largest scale, the fastestrate of development and the highest proportion ofexporting within China. The focal products within thisarea include telecommunication equipment, PCs and theircomponents. The Yangtze River Delta Area, with Shanghaias its center, is major in producing laptops, personal digitalassistants, mobile handsets and electronic fittings. Thecompetence of the Bo Sea Gulf Area lies in the researchand development (R&D) of the IT industry. For exampleBeijing, the center of the Bo Sea Gulf Area, has universitiesand research institutes that provide the resources fortechnology research. The interviewed companies weretherefore limited into these three areas. � Selection of the interviewed company: as mentioned inSection 2, the supply chain members within the ICTindustry include five sectors: EP, AP, SP, CP and operator.It was imperative to have at least one representativefrom each of the five sectors. The selection alsodepended on the company’s size and importance for

ARTICLE IN PRESS

TabList

EP/

SP/

Ope

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387378

the industry. One of the three drivers that cause thechanges within business models for the ICT industry, as(Bouwman and MacInnes, 2006) state, is regulation.Therefore, the relationship between the selected com-pany and the government is also an important criterion.As discussed in Section 1, because there are many worldleading companies operating in China, the interviewedcompanies should include these global players.

� Selection of the interviewees: the interviewees wereselected so that they are experts within the ICTindustry in terms of their working experience andpositions.

According to the criteria above, the selected interviewedcompanies for this case study were located in Beijing,Shanghai, Shenzhen and Zhuhai, which cover all of thethree most important areas for the ICT industry in China.In addition, Beijing and Shanghai are the centers for the BoSea Gulf Area and Yangtze River Area, while Shenzhen andZhuhai are among the important cities for the ICT industrywithin the Pearl River Area.

The selected companies cover all the five sectors for theChinese ICT industry: EP, AP, SP, CP and operator. They haveeither large economies of scale or close relationship withthe Chinese government and include both native Chinesecompanies and a subsidiary of a foreign company. How theindividual selected companies fit the various selectioncriteria is shown in Table 3. Although there is only onecompany from the category SP/CP because of contactingdifficulties, we obtained enough information on the SP/CP’sperspective from some of the most experienced intervie-wees, who had worked for many other SP/CPs in Chinabesides Altra Information Technology.

Most of the interviewees from the interviewed com-panies have worked for the ICT industry for more than 10years. The interviewees are all above mid-level manage-ment and most of them are from top-level management.

3.3. Interview framework

Following the purpose of this case study stated inSection 1, the interviews were conducted enclosing thefollowing four aspects:

�

General information about the entire ICT industry fromall the five sectors’ viewpoint. From this aspect, theinterviewed ICT companies within different sectorsoutlined the whole Chinese ICT industry from theirpoint of view. In this way, the Chinese ICT industrycould be sketched more objectively. � General information about each ICT sector from theinterviewed companies allocated by sectors. Here the

le 3of interviewed companies in terms of selection criteria

Economies of scale Close

AP Huawei; ZTE; Nokia Beijing Shan

CP Altra Information Technology Ltd.

rator China Mobile; China Telecom; China Unicom Chin

contents were disaggregated into each of the five ICTsectors, namely EP, AP, SP, CP and operator. The purposewas to obtain information about how each sectorwithin the Chinese ICT industry operates.

� The interaction among each interviewed company andthe other ICT players to provide information foridentifying the supply chain network structure forthe Chinese ICT industry.

� The future of the Chinese ICT industry from all the fivesectors’ viewpoint. Similar to the first aspect, the futuretrends of the Chinese ICT industry are going to berevealed by the players from all the five sectors withinICT industry.

The outline of the interviews is shown in Appendix A.

4. Chinese ICT industry supply chain networkstructure

4.1. General structure of the Chinese ICT supply chain

network

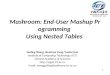

Based on the interview results, we illustrate the supplychain network structure for the Chinese ICT industry inFig. 2. As mentioned in Section 3, the Chinese ICT playerscould be sorted into five groups: operator, EP, AP, SP andCP. Besides, there are also three important ICT-relatedsupply chain members: regulator, end user and inter-mediary. Regulator in this case is MII (the Ministry ofInformation Industry of the People’s Republic of China),the governmental organization which superintends thewhole Chinese information industry.

In Fig. 2, the ICT industry is limited within the dash-dotted rectangular. The thin line stands for the supplier–customer relationship, while the heavy line represents theregulated power relationship. The arrows of the thin linespoint from the suppliers to the customers. The heavy linesgo from the controllers to the controlled members due tothe existence of regulation. As mentioned in the previoussection, the boundaries between AP and EP as well asbetween CP and SP are not distinct, which is alsoillustrated in Fig. 2 with dash-dotted ovals. For instance,in our case companies, Huawei, ZTE and Nokia Beijing areEPs as well as APs; Shanghai CINTel and Digi Moc actprimarily as APs, while they outsource the equipmentfrom EPs; and Altra Information Technology Ltd. acts asboth SP and CP.

In general, CPs supply SPs with contents includingtexts, pictures and music/video clips. SPs provide theoperators with various service platforms. Operatorspurchase applications, network infrastructures and tai-lored terminals from EP/APs. AP and EP always outsource

relationship with the government Global company

ghai CINtel; Digi Moc Nokia Beijing

a Mobile; China Telecom; China Unicom

ARTICLE IN PRESS

Operator

EP Inter-mediary

CP SP

AP End User

ServicePlatform

Content

Application

Terminal

Basic &value-added service

Tailored terminalSIM-card

SIM-card

Network infrastructure& Tailored terminal

Application

Terminalor SIM-card

Regulator(MII)

Equipment

Supply-customer relationship

Control relationship

Fig. 2. Supply chain network for the Chinese ICT industry.

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387 379

the applications or ICT equipments from each other. Manyterminals are also wholesaled to the intermediaries andthen sold further to the end users. Besides terminals, theintermediaries purchase SIM cards from the operators andsell to the end users. The operators, like the intermediariesas well, face the end users directly. Operators providetailored terminals, SIM cards, basic voice services andother services such as short message services (SMS) to theend users. The whole ICT industry in China is undersurveillance of the governmental organization MIIthrough its direct control over the operators. Moreover,the operators are empowered to supervise the SP/CPs tosustain the industrial regulations.

4.2. Supply chain members within ICT industry

4.2.1. Operator

As seen in Fig. 2, the most important supply chainmembers within the ICT industry are the operators, whichcorrespond to a focal company within a supply chain.Operators in China are authorized by the governmentaldepartment MII to own the base network infrastructuresand to operate the respective fixed-line telephone, mobiletelephone and Internet-related services. They face the endusers directly and can be seen as the portal that connectsthe AP, EP and SP with the end users. They are also theprolocutor of the MII. The operators transmit and executethe regulations that the MII has defined, while the MIIconsults the operators when it constitutes the regulations.

After the reorganization of the Chinese telecommuni-cation operators in 2002, there are now six basic operatorsin China: China Telecom, China Mobile, China Unicom,China Netcom, China Railcom and China Satcom. Origin-ally, there was just one operator, China Telecom, whichoperated the services embedded in fixed-line telephony,1G (analog) mobile handsets, the Internet and later on thepersonal handy phone (PHS), a condensed mobile phoneand available only within the range of certain geographi-cal areas. The PHS costs less than a normal mobile phonein terms of the network infrastructure; on the other hand,the quality of the PHS is notably poorer than the normalmobile services. In effect, China Telecom was separatedfrom the former China Posts and TelecommunicationsBureau in 1998. When the government realized themonopoly situation of Chinese telecommunications, theyestablished China Unicom in 1994 in order to break thissituation. China Unicom had all the licenses for operatingfixed-line telephony, mobile phone, PHS and Internetservices. But the monopoly situation was not broken asintended. In 1998, the assets and turnovers of ChinaUnicom were just 1/260 and 1/112, respectively, of thoseof China Telecom. Therefore, in the late 1999 China Mobilewas separated from the China Telecom to concentrate onoperating the mobile service. From then on, ChinaTelecom has not owned the license for mobile handsets.This move was intended to weaken the monopoly withintelecommunication, but even though the governmentbestowed a lot of preferential policy on China Unicom,as a newcomer to the sector China Unicom has hardlybeen able to compete with China Mobile and cannot pay

ARTICLE IN PRESS

Table 4The market areas of the major Chinese operators

Establishing year Market area

Major business sector Geographical area

China Mobile 1999 Mobile network related services (GSM) China

China Netcom 2002 Fixed network, internet related services and PHS North China

China Telecom 1998 Fixed network, internet related services and PHS South China

China Unicom 1994 Mobile network-related services (CDMA) China

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387380

attention to the fixed-line telephony service, which istheir major business area. In order to break the monopolyin this area, a new operator, China Netcom, came out in2002. It has the same business sectors as China Telecom,while China Telecom’s major geographical business areaslie in the South, and China Netcom mostly operates inNorth China. The business areas of these four largestChinese operators are listed in Table 4.

As the names indicate, the networks of China Railcom(established in 1999) and China Satcom (established in2001) were originally used especially for railway commu-nication and national defence. With the fast developmentof ICT, there were spare networks left which could be usedfor commercial purposes. Therefore, China Railcom andChina Satcom were established. These special conditionsconstrain the business scale of the two operators andtherefore they are not as popular as the other fouroperators in China.

Tables 1 and 4 show that there is almost no competi-tion between the major Chinese operators currently. BothChina Telecom and China Netcom operate within thebusiness areas including fixed-line and Internet connec-tion services. Their business areas in terms of geographyare however rather different. The situation is similar forthe operating of the mobile services: although only ChinaMobile and China Unicom compete within the mobileservices sector, China Mobile is more than three timeslarger than China Unicom in terms of total assets and theannual sale in 2006 (see Table 1). When looking at thenumber of subscribers (until June, 2007)), China Mobileexceeds 5 billion, which is over 10 times more than thenumber of subscribers (0.4 billion) for China Unicom(Global Sources, 2007).

The price of telecommunications is defined by the MII.Before the operators push out preferential menus or give theend users discounts, they need to obtain an approval fromthe Ministry. In this aspect, China Unicom gets the absolutefavour of authorities because of their weak competitivenessin mobile phone business compared with China Mobile. Thegovernment empowers China Unicom, for example, withlower call charges than those at China Mobile.

In addition, as the issuing of the three 3G licenses inChina is still under processing, another reorganization ofthe operators is probably going to be carried out. Thischange will affect the ICT industry in China. The futurenumber of the operators directly affects the economicbenefit of the EP/APs concerning the selling of thenetworks or applications. For instance, if there were justone operator for 3G, the EPs and APs could just sell one set

of the network infrastructures or applications, it would bethe worst scenario for them. On the other hand, this willbe the most cost saving situation regarding the infra-structure for the country, as they just pay for one setinstead of several. But if there were just one operator, theend users would be the victim. Nevertheless, ChinaTelecom is claimed to obtain one of the 3G licenses. SinceChina Telecom is the largest fixed-line operator in China.When the government issued the license of operating thePHS service, which is mobile service in nature, thisimplied that it is letting China Telecom to prepare forthe operating of 3G-related services.

4.2.2. EP/AP

An AP offers the software or solutions for the specificrequirements the operators needed, while an EP suppliesthe operators with the equipment needed, for examplenetwork infrastructure or tailored handsets. Although theboundary between the APs and EPs is not obvious, theyoften outsource from each other with their respectivefocal products. The two largest Chinese EPs are Huaweiand ZTE, which also act as APs in China and evenworldwide. Huawei and ZTE compete in the almost samebusiness sectors as well as geographical areas. The onlydifference lies in the form of ownership. Huawei is atotally private-owned company, while ZTE is state owned.There are also a lot of subsidiaries of the foreign EPs/APs inChina, as mentioned in Section 1, Cisco, Ericsson, Motor-ola, Nokia, Samsung and Siemens. They all have bigmarket shares in China. For instance, the market share ofthe foreign brand mobile handsets in 2005 accounted forabout 60% (Global Sources, 2006). Besides, there are alsosome joint-ventured EP/APs that operate within thissector. For instance, TD Tech Co. Ltd. was co-founded bySiemens and Huawei on March 18, 2005 in Beijing and isfocused on the network infrastructures related to TD-SCDMA. Most of the EP/APs currently have been concen-trating on the products that relate to TD-SCDMA, which isdeveloped by China and is among the world’s threeapproved 3G wireless interface specifications.

4.2.3. SP/CP

CP supplies the SPs with music, video clips, etc. The SPconstructs the service platforms in order to provide theend users with specific services through the operators, forexample SMS, interactive voice response and multimediamessage services. Besides the supplier–customer relation-ship between the SPs and the operators, as mentioned inSection 4.1, the operator has also the control power over

ARTICLE IN PRESS

Table 5Descriptive statistics of China telecommunication network (1999– H1/

2007)

Time horizon of alliance announcements 1999–H1/2007

Number of alliances 201

Number of relationships 307

Number of nodes (companies) 178

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387 381

the SPs. The operators are empowered by the MII with theright to permit or prohibit the SPs running their business.The operators admit the SPs to offer the platforms for theservices to the end users, but the operators face the endusers directly and calculate the flux and take in thecharges from the end users. Then the SPs receive theirshares from the operators.

SMS is the most successful value-added service (VAS)in China. Yan et al. (2006) argue that, as one of thesimplest VASs based on the GSM and CDMA standards, inChina SMS offers real growth in mobile data services.NEWS.CN (2006) pronounced that during the ChineseNew Year 2006 (8 days), the number of SMSs in Chinareached 12.6 billion! During the 8 days, the average SMSssent per person was over 30 and the earnings from SMSfor the two Chinese mobile operators, China Mobile andChina Unicom together, exceeded h0.13 billion.

In China, several SPs also act as CPs. There are morethan 1000 SPs in China and because of the immaturemarket and their irregular operating within this sector,the operators have improved the regulations for thissector and reorganizing the SPs in terms of reducing theirnumbers and eliminating unqualified SP/CPs in 2006.

4.3. Supply chain members outside ICT industry

4.3.1. Regulator

The regulator for the Chinese ICT industry is the MII. Itwas established in 1998 and is the governmental depart-ment that constitutes the information industry-relatedregulations and deals with the affairs within the informa-tion industry in China. The MII directly appoints orreorganizes the operators and superintends them. Onthe other hand, MII indirectly controls the whole ICTindustry through constituting industrial regulations,common standards and even the respective service fees.Although the MII administrates the ICT-related affairs, it isa governmental organization and therefore it cannot becategorized within the boundaries of the ICT industry.From the Chinese ICT supply network structure illustratedin Fig. 2, it can be seen that the Chinese government hasabsolute control over the whole Chinese ICT industrythrough its directly controlling of the operators.

4.3.2. End user

Another very important member for the ICT industry,which cannot be counted in the ICT industry, is the enduser. End users are situated at the very end of the supplynetwork and are, therefore, a gold mine for the whole ICTindustry. To continuously develop new technology or newservices, the ultimate goal of the various supply chainmembers within the Chinese ICT industry is to obtain orretain more end users. Although handsets, different SIMcard or preferential menus and different services are allcreated to fulfil the end users’ needs, they actually do nothave any bargaining power in terms of, for example, theservice fee. The end users just have to accept the amountthe MII has prescribed. On the other hand, the cardinalnumber of the end users and the potential end users inChina is the advantaged precondition for the commercial

profit of the Chinese ICT industry. The successful runningof SMS in China is among the examples that confirm theproposition.

4.3.3. Intermediary

According to the definition for the ICT industry, theintermediaries cannot be ascribed to the ICT category. InChina, the ICT intermediaries’ major tasks include sellingof terminals (including accessories such as batteries,headphones and so on) and SIM cards to the end users.However, the operators have started to take over the roleand sell tailored handsets (with their logos and names inthe font of the handsets) in order to adapt their specialservices or prepaid cards they provided to the end users.

4.4. ICT network development in China—Collaboration view

We have formulated a case network in order to providean overview of the formation of the collaborative relation-ships for the Chinese ICT supply chain network. Thenetwork is based on the information of strategic alliancesformed from the beginning of 1999 to June 2007 of 10Chinese focal companies (Haier Group, Huawei Technol-ogies, Lenovo, Vimicro, Dtmobile, ZTE, China Mobile,China Telecom, China Unicom and Hutchison Telecom),and their global and local alliance relationships. Thesefocal companies are large Chinese companies fromdifferent sides of the ICT industry and represent heretheir industry sectors.

Altogether 307 valued relationships were included in theanalysis and the case network consists of 178 companies(nodes). The alliance relationships of these companiesillustrate the industrial ICT network; nevertheless, thestructure of the network is in some sense egocentric sinceit is described through few focal companies. The informationof the alliances was gathered from the SDC Platinumalliance database through searching alliances, where focusgroup firms were as one of the participants. The useddatabase, SDC Platinum, is a Thomson Financial admini-strated database, which has information of approximately60,000 alliances globally since 1988. This database isdetailed, systematically gathered and updated regularlyand therefore it is a good source for extensive analysis offirms’ alliance activities. Chinese ICT network statistics ofalliances (focal firms) is presented in Table 5.

Because some of the alliances were between severalfirms, for this analysis it was necessary that theseparticipations in the alliances were disaggregated intopairs of relationships eventually creating over 50% morefirm-to-firm relationships than the number of originalalliances. This was necessary for the UCINET analysis that

ARTICLE IN PRESS

Table 6Top companies’ structural position in China ICT network

Company name Category nBetweenness Alliance degree Company name Category nBetweenness Alliance degree

China Unicoma OP 54.02 47 Hewlett-Packard EP/AP 1.53 3

China Telecoma OP 29.76 56 SingTel OP 1.31 17

Lenovoa EP 26.32 11 Nokia EP/AP 1.12 5

SunMicrosystems AP 25.69 3 NTT OP 1.12 12

China Mobilea OP 18.08 35 Korea Telecom OP 1.12 13

Huaweia EP/AP 17.49 22 Chunghwa OP 1.09 13

Haiera EP/AP 17.23 18 Huawei-3com EP 1.07 2

Microsoft AP 17.22 2 Shenzhen Digital AP 1.07 2

ZTEa EP/AP 16.94 23 Lucent (Alcatel) EP/AP 0.33 6

Ericsson EP/AP 7.88 5 Telekom Malaysia OP 0.12 13

QUALCOMM SP 6.87 5 StarHub AP 0.10 5

Nortel EP/AP 6.20 4 China Netcom OP 0.06 3

Vodatel OP 5.27 6 KDD OP 0.05 9

Siemens EP/AP 4.06 4 HK Telecomm OP 0.02 9

Motorola EP/AP 3.40 8 Qingdao EP/AP 0.02 3

Telstra OP 2.94 12 Alcatel EP/AP 0 5

Cisco EP/AP 2.61 2

a Focal company.

34 %

15 %17 %

8 %

26 %

OP

EP

AP

SP/CP

OTHER

Fig. 3. Chinese ICT alliance target sectors (based on SIC codes).

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387382

was used finally in order to formulate the structuralnetwork analysis.

The results of the analysis are shown in Table 6.Betweenness, as one of the measures of centrality,assesses the extent to which a particular actor lies between

the various other actors in the graph. The principle of themeasure is to indicate actors that are between other actorsin a network, thus describing their dependency. Strongbetweenness facilitates the actors’ power position orbroker position in a network. It may also provide actorswith more control over others in the network. It should benoted that the illustrated betweenness measures are onlycomparable within the case network and cannot becompared directly with other networks. The graphicalpresentation of the core parts of the case ICT network isillustrated later in Fig. 4.

We also used degree centrality as a comparison tomeasure the absolute number of alliances formed byfirms. As shown later in Table 6, a firm may obtain a highbetweenness result even if it has only few alliances,because alliances may be formed with central nodes of thenetwork (and vice versa). In this network in question, SunMicrosystems is a good example of such a company.

Betweenness in this context can be seen as an indicatorfor exposing the central nodes within the value network.It can be assumed that firms primarily tend to seekcollaboration relationships with firms or industries, whichhave the most central role in the value network andgenerate most value into it. As shown in Table 6,telecommunication operators seem to be the most centralcompanies (or industry) in the Chinese ICT network, whenstudying the firms’ collaboration activeness. Regardless ofthe smaller size (see Fig. 1), China Unicom is by far themost central single company (betweenness result is 82%greater than the second one’s) in the network. This can bepartly explained by the direct connection between SunMicrosystems and China Unicom, which is the main singlereason for both of the firm’s high betweenness result,because no other centrally positioned Chinese firm has

formed a link with Sun Microsystems. This connection isillustrated clearly in the upper right section in Fig. 4.

In some cases, the alliance degree result also correlateswith betweenness. However, there are exceptions, espe-cially the above-mentioned Sun Microsystems and Micro-soft, which can be seen as centrally positioned firms in thenetwork, although they have formed very few alliances. Onthe other hand, firms like SingTel, NTT, Korean Telecom,Chunghwa and Telekom Malaysia have formed severalalliances, but not directly (or exclusively) with the mostcentral firms, which explains the low betweenness results.

In addition to structural analysis, we examined thetargets of the formed alliances. The SDC Platinumdatabase also includes a feature to track what the firmsare really doing with their alliances and what their targetsare. This alliance target is described with a SIC code(US based Standard Industry Classification system) andthe division of these alliance targets (converted to ICTsupply chain industries) can be seen in Fig. 3.

Fig. 3 shows that, similarly to betweenness, the biggestsingle alliance target is the telecommunication operator

ARTICLE IN PRESS

Fig. 4. Graphical illustration of the China alliance ICT network.

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387 383

sector with 34% of all the alliances. EPs’ and APs’ business-related alliances are also relatively common (17% and 15%,respectively). The SP/CP sector is the most uncommontarget, with only 8% share of all alliances, reflecting alsothe immaturity and incoherence of this sector in China. Inaddition, remarkable is the big number of other alliancestargeted outside the ICT industry (26%). This groupincludes a wide range of targets across industries, butnearly half of them are aimed at consulting services andpatenting, which may well be related to the ICT industryin the end, but it cannot be verified from the data.

The above analysis revealed the central role of theoperators within the Chinese ICT network. Both structuraland alliance target analyses strongly support this conclu-sion. Although this is not very surprising, we have to notethat the centrality of the operators is not as dominant inmost of the other market areas, and therefore this result isimportant and relevant. The underlying reason for thisresult is most probably due to the MII’s role and itsrelationship with the operators described in Section 4. InFig. 4, a graphical illustration of the Chinese ICT alliancenetwork based on the UCINET analysis is shown.

4.5. Discussion

4.5.1. Characteristics of Chinese ICT industry

The most remarkable characteristic of the Chinese ICTindustry is the centralized control of the government over

the operators, and due to the operators occupying the bestposition within the supply chain network this leads to theindirect control over the whole ICT industry in China bythe MII.

Since the ICT industry is an industry with very fastclockspeed, the centralized control of the governmentcould, to some extent, create obstacles for technologyupdates. In the short term, this may lead to certaineconomic benefits for the supply network members, butin the long term, it may delay the application of newtechnologies in China. Therefore, it is almost impossiblefor China to catch up with the adoption of the newtechnologies in other developed countries. For instance,3G has already been commercially operated in Japan for6 years and Sweden has been updating its existing 3Gnetwork to the turbo 3G network since the end of 2006,but it is still under commercial tests in China and no 3Glicenses will be issued before 2008.

Also by appointment from the MII, China has devel-oped its own 3G standard, TD-SCDMA. This gives a betterpossibility for Chinese companies to be involved intechnology development already in the early stage, whichat the cost of foreign EPs causes relative advantage fornational firms when the networks are to be built in thefuture. Own standard gives the regulator a betterpossibility to regulate its own markets also in the future,if it so chooses. In addition on a bigger scale, this has beenseen as a way to reduce the country’s dependence onforeign technology and to run China’s own interest;

ARTICLE IN PRESS

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387384

therefore, it has also been a political choice. Actually, thereason why China delays issuing its 3G licenses is waitingfor the TD-SCDMA to be ready for commercial use. At thebeginning of 2007, China Mobile, under the authorizationof the MII, started purchasing the TD-SCDMA networkinfrastructure in the form of a beauty contest for thepurpose of commercial trials before the issuing of 3Glicenses. ZTE became the biggest winner with about 50%of the business, which is worth about h3 billion. Thismove further convinces the importance of TD-SCDMA inChina. In this sense, it is very important for the individualICT supply network members to follow or keep soundrelations with the Chinese government, which results inneglecting the end users’ needs.

Moreover, the investment in a new set of networkinfrastructures or the updating of the existing networkinfrastructures within the ICT industry could be enor-mous. In this way, the decision of issuing 3G licenses bythe MII could directly affect the revenues of variousinvolved EP/APs and SP/CPs.

The ICT industry is also full of new business opportu-nities. In China, which is an immature ICT market in termsof incomplete industrial regulations, centralized controlcould reduce the unwarrantable management resort. Thebanning of the irregularly operated SP/CPs in 2006illustrates this advantage of government control.

Another issue concerning the Chinese ICT industry isthat the business environment is extraordinary tough forboth the small-sized EP/APs and SP/CPs. They competevery intensely with the famous global firms as well as thegiant Chinese companies within their business areas. Theglobal firms have their competitive advantage with theirbrands, for example, Ericsson and Nokia, whereas thecompetitive advantage for the giant Chinese companieslies mostly with the price. The small EP/APs and SP/CPshave neither a famous brand nor the economies of scale,and therefore they can hardly win customers from theglobal firms or giant Chinese companies. Therefore, thesurvival conditions for small EP/APs and SP/CPs are thateither they have unique or creative products that theircompetitors do not have, or they try to win the orders thattheir giant competitors do not want or do not care about.

4.5.2. Major driving forces and uncertainties

When concerning the development of the ICT industryin China, the main power comes from the EP/APs or SP/CPstogether with the end users. Since the operators areempowered to occupy the best position within the supplynetwork structure of the Chinese ICT industry, they dolittle for the renewing of the technology. It is always thecase that the EP/APs or SP/CPs bring a new technology orservice idea to the operator and persuade them to testwithout paying. The operators pay for the new technologyor service only after they have got enough profit from theend users. Before finding a new technology or a newservice, the EP/APs or SP/CPs always conduct marketresearch in order to obtain accurate feedback from the endusers. Therefore, it is the EP/APs or SP/CPs together withthe end users who initiate the development of the ICTindustry.

The major uncertainty of the Chinese ICT industry lies inthe change of regulations and diversification of end userneeds. Since the Chinese government has the absolutecontrol power over the ICT industry, the transformation ofthe regulations regarding the ICT industry affects the wholeindustry. For example, along with the releasing of the 3Glicense, the structure of the operators is going to be totallychanged. On the other hand, uncertainty is also accompa-nied with end users, since they are the ones that pay for thevarious products and services. In China, the large number ofend users and the inequality in economic developmentwithin different geographical areas all lead to differentconsumption patterns for different groups of end users,which increases uncertainty in the Chinese ICT industry.

4.5.3. Future trends

Nokia Corporation (2004) has noted that regarding thedevelopment trend of the technology, the direction istoward more mobility together with higher data compres-sing. As voice matures, the future of operator businessgrowth and profitability lies in multimedia services andmobility. This also applies in the Chinese context.However, the mobile penetration level in China is stillrather low (around 35% by the end of the year 2006)compared to, for example, EU which is already closing inon 100%. Therefore it can be assumed that this trend issomewhat lagging in the Chinese market, and the maingrowth driver will still be voice services and traditionalpenetration growth, at least for the next few years.

Related to 3G network licenses, there are couple ofquestions that are connected with their release. Thereorganization of the operators is planned to be carriedout together with the release of the 3G licenses. The firstquestion is technological, whether China grants operatinglicenses for two or three 3G technologies (TD-SCDMA,WCDMA and CDMA2000). The main issue is whether ornot CDMA2000 technology will receive a license togetherwith two other technologies. Another question linked tothis is timing. The delay on unfinished TD-SCDMAtechnology development may delay 3G license grantingin general. However, this technology and its full develop-ment is of such high importance within China that thedelay in the license granting is seen justifiable. The othermain issue is that 3G license granting will also reorganizethe Chinese operator landscape: which current operatorswill be granted with the license, where they will operategeographically in the future, and whether new operatorsare formed in addition to the current ones. The question ofopening the markets to foreign operators will also be putout herewith. Finally, this reorganization will also affectSP/CPs so that the new organized operators couldreorganize SP/CPs as well and the complete landscapewithin the SP/CP sector could be greatly changed.

On a more general level these decisions have an effecton the Chinese trade policy, or are affected by it. Forinstance, the WTO’s opinion on free trade in general mayplay a role in the question of whether and when foreignoperators are accepted in the Chinese markets. Similarly,the WTO’s attitude towards intellectual property rights(IPRs) issues and pressure on the Chinese government cancause changes on a general level. Currently, IPRs are

ARTICLE IN PRESS

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387 385

followed rather loosely in the Chinese markets and, forexample, product piracy business is extensive. China isprobably the biggest exporter of these products in theworld. If the Chinese government would change itsattitude towards IPR, it would cause great changes inmany industries. These changes would also have a notableeffect within the ICT industry, especially on the SP/CPs andconsequently the operators’ role. If IPR owners, especiallyCPs in this case, would be more recognized, the compen-sation from their work would become higher and there-fore their position in the ICT network would becomestronger. This would be firstly and mostly at the cost of theoperators, because they are the direct customers of CPs.Therefore, the choices made in these different politicalstages may quite rapidly affect the ICT network environ-ment and its power structure.

4.5.4. Some remarks of the value-adding opportunities of

the ICT players

After answering the three core questions of this paper,some of the value-adding opportunities for each group ofthe Chinese ICT players can be identified.

EP/APs are responsible for the development of newtechnologies within the ICT supply chain. Therefore, themastery of the core technologies or standardizations is themost important value-adding opportunity for EP/APs. Thisis valid not only in China but also worldwide. The owningof the core technology of CDMA by Qualcomm illustratestheir value-adding opportunities. Qualcomm has beendeducting a percentage from the revenues the othercompanies gained, only if the profitable technologies thecompanies developed are embedded in the Qualcomm’score technology of CDMA.

Similar for SP/CPs, the continuous researching anddeveloping of new services and contents provides value-adding opportunities for them. The considerations for EP/APs and SP/CPs in China are not only to seize the endusers’ needs, but also to forecast and follow the govern-ment’s intent.

The operators, who have the best position within theChinese ICT supply chain, should utilize their advantage ofhaving close relationships with both the regulator MII andthe end users in order to find out the end users’requirements. They should also take initiative to sharethe information together with the EP/APs and SP/CPs, sothat these three supply chain members could togetherprovide value to the end users.

4.5.5. Some remarks on ICT in china and other important ICT

regions

Regarding the Chinese supply chain network structurewhen compared to other market regions, the maindifference comes from the role of the regulators. TheChinese regulator MII has continuously chosen an active(strict) role in the supply network. Although the operatorsare the focal supply network members within the ChineseICT supply network, they are appointed by the MII andthey involuntarily divide the country more or less toregional monopolies between each other. There is no freecompetition within the network operator sector, nor are

foreign operators allowed to operate directly in theChinese market.

In Japan, the regulator in the 1990s imposed anoperator-led telecom supply chain network, and sincethen the regulator has been a more passively influentialbody. This created the boom of i-mode, and through thisdecision the Japanese market has been the forerunner oftelecom development. However, this has given a muchsmaller role for EPs in the supply network, since they havebeen forced to follow the operators’ (e.g. NTT DoCoMo)specified paths, often at the cost of EPs’ own profitability.

In Europe in the 1990s, the regulator decided on thefavoured technology, GSM, which was heavily lobbied bystrong EPs (especially Ericsson and Nokia). Ever since, theregulator has had a relatively passive observer role. Thisdevelopment path has given EPs a much stronger rolewith regard to operators than in Japan, for example.

In the USA, the regulator Federal CommunicationsCommission has chosen a rather open and liberal role andgives free hands for technologies to develop, favouring thetechnology developers and EPs (Qualcomm). However,this has caused confusion among the users about whichtechnology to choose, because different technologies donot roam between each other (mostly by the choice ofoperators). This partially explains the smaller revenues ofall the parties in the value network and a slowerpenetration of mobile technology in the USA in generalthan in Europe and Japan.

5. Conclusions and future study

In this paper, we examined the Chinese ICT industryfrom the perspective of its supply chain network structureand identified the relationship between the individualsupply chain members. By using a collaborative study, wehave verified the major finding from the supply chainnetwork that the Chinese operators are the focal compa-nies of the whole Chinese ICT industry.

The value-adding opportunities for each group of theICT players were pointed out in this paper. The mastery ofthe core technologies and standardizations are importantfor EP/APs, whereas innovation is critical for SP/CPs. Theessential issue for the operators is to balance between theregulator’s intent and the needs of the end users.

In order to adequately utilize the resources to makeprofits at the introducing of the 3G in China, developingmore VASs which satisfy the end users is among the mostimportant trends for the Chinese ICT. Along with the 3Gpenetration, the landscape of the Chinese operators isgoing to change. Although all of the three 3G technologies,approved by International Telecommunication Union, areaccepted in China, the Chinese initiated technology TD-SCDMA is going to be the dominant one in China.Moreover, with the globalization of China including theChinese ICT industry, the IPR problem is going to gainmore attention, and therefore the importance of eachChinese ICT supply chain member is going to change inthe future.

The result of the qualitative mapping of the ICTindustry provides a basis for quantitatively identifying

ARTICLE IN PRESS

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387386

the value adding of each supply chain member within theICT industry. For instance, (Yu et al., 2007) identify theglobal ICT supply chain network, based on which theyquantitatively obtain the most value-adding sectors with-in the whole ICT industry.

Although we have discussed the regulators’ role invarious countries in paper, it is also interesting in thefuture research to investigate ICT industry from otheraspects between China and other countries. In addition,collaborative analysis can be extended to include morefocal firms in order to better understand the developmentof Chinese ICT industry. Finally, we believe the roles ofdifferent players can be further analyzed if supply chainmembers can be disaggregated to an extent. For instance,EP could be further divided into terminal providers,network providers and component providers.

Acknowledgments

The authors would like to thank the Finnish organiza-tion TEKES for funding this study. The personnel fromFinchi office in Shanghai, Mr. Jaani Heinonen and Ms.Karen Jiang also provided great help. We would also like toexpress our appreciation to the Chinese companies whogranted opportunities for the interviews.

Appendix A. Interview outline for Chinese ICT firms(July, 2006)

Prologue (interviewer initiative)

�

Introduction of the background and purpose ofSirmakka project and the interviewDemographic information

�

Firm’s name and sector � Interviewee’s name � Interviewee’s position � Interviewee’s experience � Interview time duration � Interview placeInformation related to the interviewed company

�

How does the firm develop during recent years? Whatis the growth potential of the business?J Suppliers and customersJ Business areasJ Geographical areasJ Major alliancesJ R&D � What is (are) your firm’s competitive advantage(s)compared to the companies within the same sector asyour firm? What is (are) the disadvantage(s) of yourfirm?

� Has your firm faced any crises?J If yes, what are them and how did you handlethem?

J If not, can you point out any crises that mightthreaten your firm or even your sector in thefuture?

J What are the causes behind the crises?

� How do you position your firm within the ICT industryin China? How do you position the business sector inwhich your firm residents within the ICT industry inChina?

� What are the major driving forces and hinders for yourfirm or your business sector?

� How, as a single actor, can your firm create value in thenetwork?

� How can you describe the business processes youadopted in your firm and even in your business sector,if possible?

� What capabilities and assets become critical in thefuture, both for your firm and your business sector?

� What capabilities and assets are in danger of loosingtheir value, both for your firm and your businesssector?

� What kinds of relationships or connections that yourfirm has withJ other ICT players that residence in the same sector

as your firm?J other ICT players that do not residence in the same

business sector as your firm?

� How do/does you/your firm know about Supply ChainManagement (SCM)?

� How does SCM approach adopt in your firm, yoursector and even the whole Chinese ICT industry?

Information related to the entire ICT industry in China

�

How ICT industry has developed during last few yearsin China and worldwide? � Are there any remarkable events nowadays within theChinese ICT industry?J CausesJ Influences (to your firm, your business sector and

the whole ICT industry)J Consequences

� What are main differences between market areas/regions (Europe, Asia, USA etc.)?J How the regulation is expected to develop in these

areas?J What is the role of regulation in different market

areas?

� What kind of supply chain network structure does itexist in the Chinese ICT industry?

� Point out some ICT players that you think are runningwell within their business sectors:J ChineseJ GlobalJ What, do you think, are the success factors for

them?

The future of the Chinese ICT industry

�

What are the current trends and signals in the industrydevelopment?

ARTICLE IN PRESS

L. Yu et al. / Int. J. Production Economics 115 (2008) 374–387 387

�

What are the key uncertainties in the industrydevelopment?J External uncertainties (macro-economical)J Internal uncertainties (micro-economical) � What are the major driving and restricting forces in theindustry development?J CatalystsJ Inhibitors

� What plausible future development paths can beidentified in the industry?

� What incidents or indicators of change can bediscovered from the business environment? (turningpoints, points where alternative futures become ap-parent, important milestones)

� Is it possible to proactively identify and influence theregulation?J What are the major influence means?J Are there any regional differences?

� How the industry competition is about to change in thefuture?J The power of customers & suppliersJ The threat of new entrants & substitutes

References

Agrell, P.J., Lindroth, R., Norrman, A., 2004. Risk, information andincentives in telecom supply chains. International Journal ofProduction Economics 90 (1), 1–16.

Andersson, G., 2006. Rekordtillvaxt: 404 Miljoner Nya GSM-Abonnenter iFjol. Computer, Sweden, 2006-01-27.

Burgess, K., Singh, P.J., Koroglu, R., 2006. Supply chain management: Astructured literature review and implications for future research.International Journal of Operations & Production Management 26(7), 703–729.

Berry, D., Towill, D.R., Wadsley, N., 1994. Supply chain management inthe electronics products industry. International Journal of PhysicalDistribution & Logistics Management 24 (10), 20–32.

Borgatti, S.P., 2005. Centrality and network flow. Social Networks 27 (1),55–71.

Borgatti, S.P., Everett, M.G., Freeman, L.C., 1992. Ucinet-Guide-Ucinet forWindows: Software and Social Network Analysis Harvard. AnalyticTechnologies.

Bouwman, H., MacInnes, I., 2006. Dynamic Business Model Frameworkfor Value Webs. In: Proceedings of the 39th Hawaii InternationalConference on System Sciences.

Catalan, M., Kotzab, H., 2003. Assessing the responsiveness in the Danishmobile phone supply chain. International Journal of PhysicalDistribution & Logistics Management 33 (8), 668–685.

Chandra, C., Kumar, S., 2001. Enterprise architecture framework forsupply chain integration. Industrial Management and Data Systems101 (6), 290–303.

Christopher, M., 1998. Logistics and Supply Chain Management:Strategies for Reducing Cost and Improving Service, second ed.Financial Times Professional Limited, London.

Collin, J., Lorenzin, D., 2006. Plan for supply chain agility at Nokia:Lessons from the Mobile Infrastructure Industry. International

Journal of Physical Distribution & Logistics Management 36 (6),418–430.

Cooper, M.C., Lambert, D.M., Pagh, J.D., 1997. Supply chain management:More than a new name for logistics. The International Journal ofLogistics Management 8 (1), 1–14.

Cousins, P.D., Lawson, B., Squire, B., 2006. Supply chain management:Theory and practice—The emergence of an academic discipline?International Journal of Operations & Production Management 26(7), 697–702.

Doz, Y., Hamel, G., 1999. Alliance Advantage: The Art of Creating ValueThrough Partnering. Harvard Business School Press, USA.

Global Sources, 2006. /http://www.esmchina.com/ART_8800068963_617671_a0751953200605.HTMS.

Global Sources, 2007. /http://www.esmchina.com/ART_8800079069_1300_2300_3300_0_e044d422.HTM?click_fro-m=0,0,2007-10-24,ESMCOL,ARTICLE_ALERTS.

Gruber, H., 2001. The Diffusion of Information Technology in Europe. Info3 (5), 419–434.

Guzman, R., 2006. Nokias Mobiler Saljer som Smor. Computer, Sweden,2006-01-27.

Hanneman, R.A., Riddle, M., 2005. Introduction to Social NetworkMethods. Riverside, University of California, USA.

Hallikas, J., Suojapelto, K., Savolainen, P., 2005. Industrial Analysis Report.Working paper, Technology Business Research Center, LappeenrantaUniversity of Technology, Finland.

Kemppainen, K., Vepsalainen, A.P.J., 2003. Trends in industrial supplychains and networks. International Journal of Physical Distribution &Logistics Management 33 (8), 701–719.

Lambert, D.M., Cooper, M.C., 2000. Issues in supply chain management.Industrial Marketing Management 29 (1), 65–83.

Lambert, D.M., Cooper, M.C., Pagh, J.D., 1998. Supply chain management:Implementation issues and research opportunities. The InternationalJournal of Logistics Management 9 (2), 1–20.

NEWS.CN, 2006. /http://news.xinhuanet.com/newmedia/2006-02/08/content_4149558.htmS.

Nielsen, P.B., (chairman), 2000. The ICT sector in the Nordic Countries,Statistics Finland, Statistics Denmark, Statistics Iceland, StatisticsNorway, Statistics Sweden. Denmark, /http://www.dst.dk/ict1998S.

Nokia Corporation, 2004. Nokia Intelligent Edge: Adding Value in theNew Multimedia Age. Contra/Libris/06/2004, Nokia Code: 11189,Nokia Corporation.

Norrman, A., Jansson, U., 2004. Ericsson’s proactive supply chain riskmanagement approach after a serious sub-supplier accident. Inter-national Journal of Physical Distribution & Logistics Management 34(5), 434–456.

OECD, 2002. Reviewing the ICT Sector Definition: Issues for Discussion./http://www.oecd.org/dataoecd/3/8/20627293.pdfS.

OECD, 2004. OECD Information Technology Outlook 2004. /http://www.oecd.org/dataoecd/20/47/33951035.pdfS.

OECD, 2007. ANNEX 1B: OECD Definition of the ICT Sector. /http://www.oecd.org/dataoecd/49/44/35930616.pdfS.

Olhager, J., Persson, F., Berne, P., Rosen, S., 2002. Supply chain impacts atEricsson—From production units to demand-driven supply units.International Journal of Technology Management 23 (1–3), 40–59.

Tan, K.C., 2001. A framework of supply chain management literature.European Journal of Purchasing & Supply Management 7 (1), 39–48.

Thomson ONE Banker, 2006. /http://banker.thomsonib.comS.Wasserman, S., Faust, K., 1994. Social Network Analysis. Cambridge

University Press, Cambridge.Yan, X., Gong, M., Thong, J.Y.L., 2006. Two tales of one service: User

acceptance of short message service (SMS) in Hong Kong and China.Info 8 (1), 16–28.

Yasuda, H., Iijima, J., 2005. Linkage between strategic alliances and Firm’sbusiness strategy: The case of semiconductor industry. Technovation25 (5), 513–521.

Yu, L., Tang, O., Grubbstrom, R.W., 2007. Application of a Leontief Modelto the ICT Industry. Presented in the 19th ICPR, Valparaiso, Chile.