Embed Size (px)

Citation preview

China’s National Rural Pension SchemeChina’s National Rural Pension Scheme

Matching Defined Contribution ConferencegMark Dorfman, Philip O’Keefe and Dewen Wang

The World Bank

Washington, DCJune 7, 2011

Organizationg

1. Background and Motivations for Reform2. Design of the National Rural Pension Scheme3. Initial Results4. Reflections on the Design and Remaining Challenges5. Lessons for Other Countries

Slide 2June 7, 2011

I. I. Background and Motivations for ReformBackground and Motivations for Reform

3

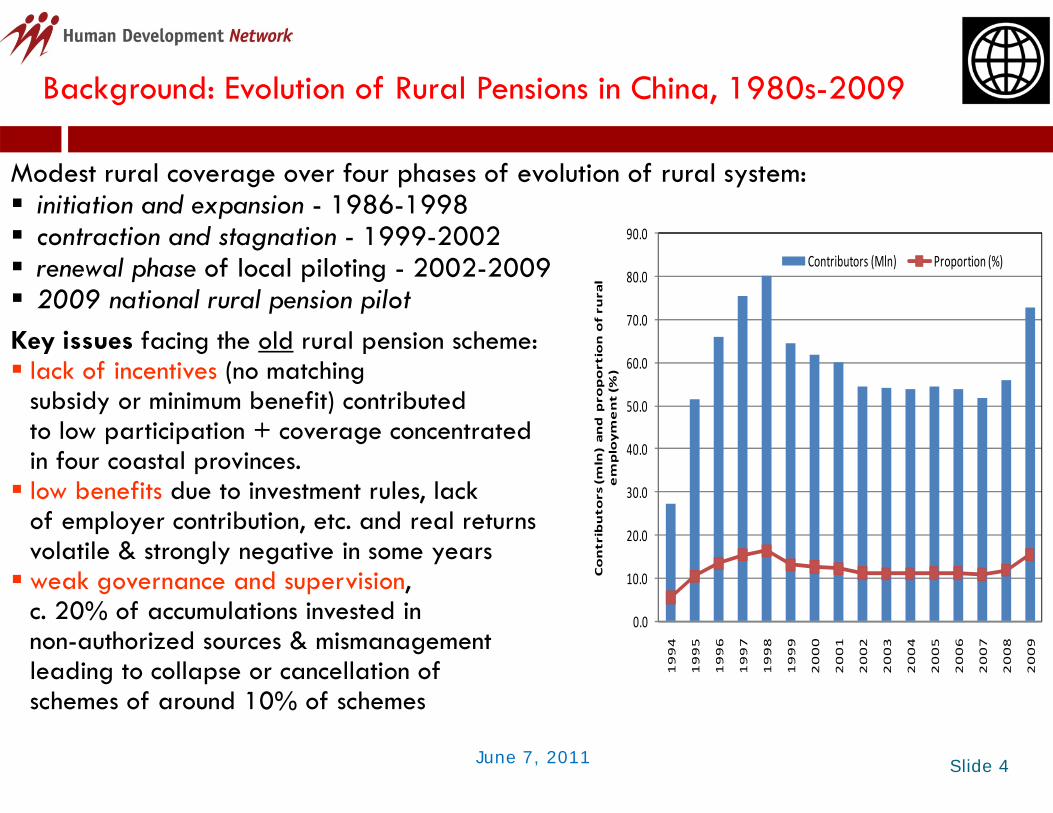

Background: Evolution of Rural Pensions in China, 1980s-2009

Modest rural coverage over four phases of evolution of rural system: initiation and expansion - 1986-1998initiation and expansion 1986 1998 contraction and stagnation - 1999-2002 renewal phase of local piloting - 2002-2009 2009 national rural pension pilot

80.0

90.0

ural

Contributors (Mln) Proportion (%)

2009 national rural pension pilotKey issues facing the old rural pension scheme: lack of incentives (no matching

subsidy or minimum benefit) contributed 50 0

60.0

70.0

proportion of r

nt (%

)

subsidy or minimum benefit) contributedto low participation + coverage concentratedin four coastal provinces. low benefits due to investment rules, lack 30.0

40.0

50.0

ors (mln) and p

employmen

of employer contribution, etc. and real returnsvolatile & strongly negative in some years weak governance and supervision,

20% f l i i d i 10.0

20.0

Contributo

c. 20% of accumulations invested in non-authorized sources & mismanagementleading to collapse or cancellation ofschemes of around 10% of schemes

0.0

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Slide 4June 7, 2011

schemes of around 10% of schemes

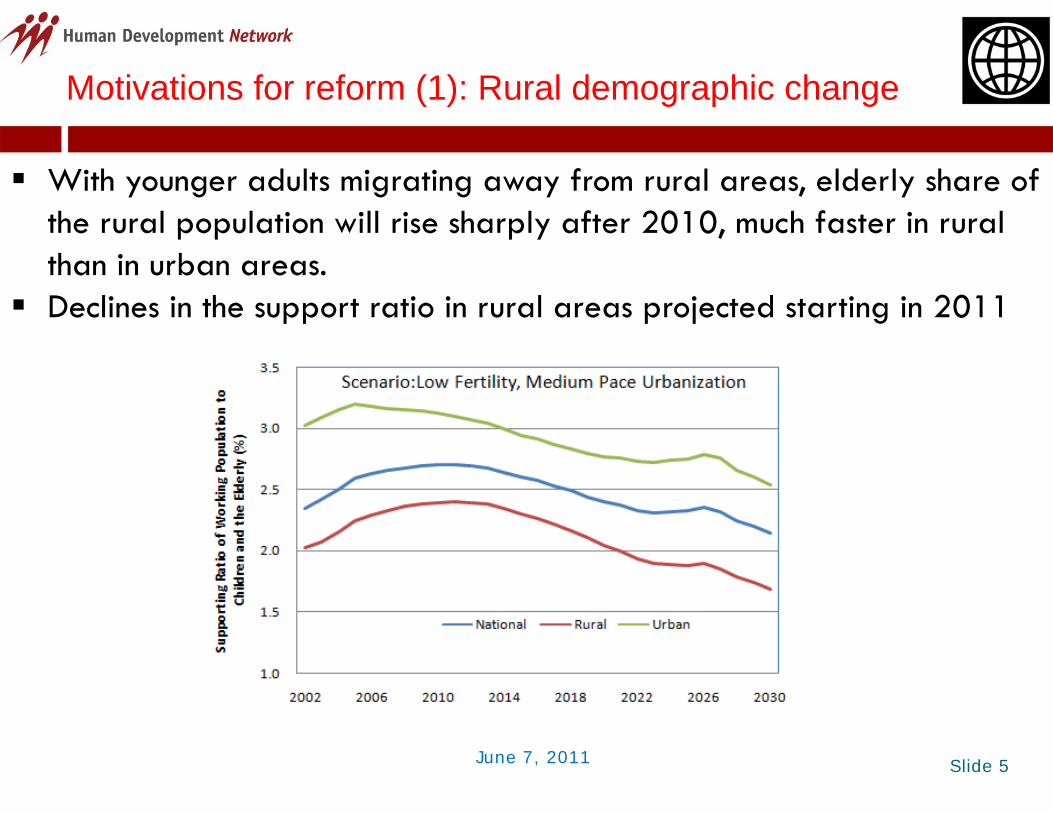

Motivations for reform (1): Rural demographic change

With younger adults migrating away from rural areas, elderly share of the rural population will rise sharply after 2010, much faster in rural than in urban areas.

Declines in the support ratio in rural areas projected starting in 2011 Declines in the support ratio in rural areas projected starting in 2011

Slide 5June 7, 2011

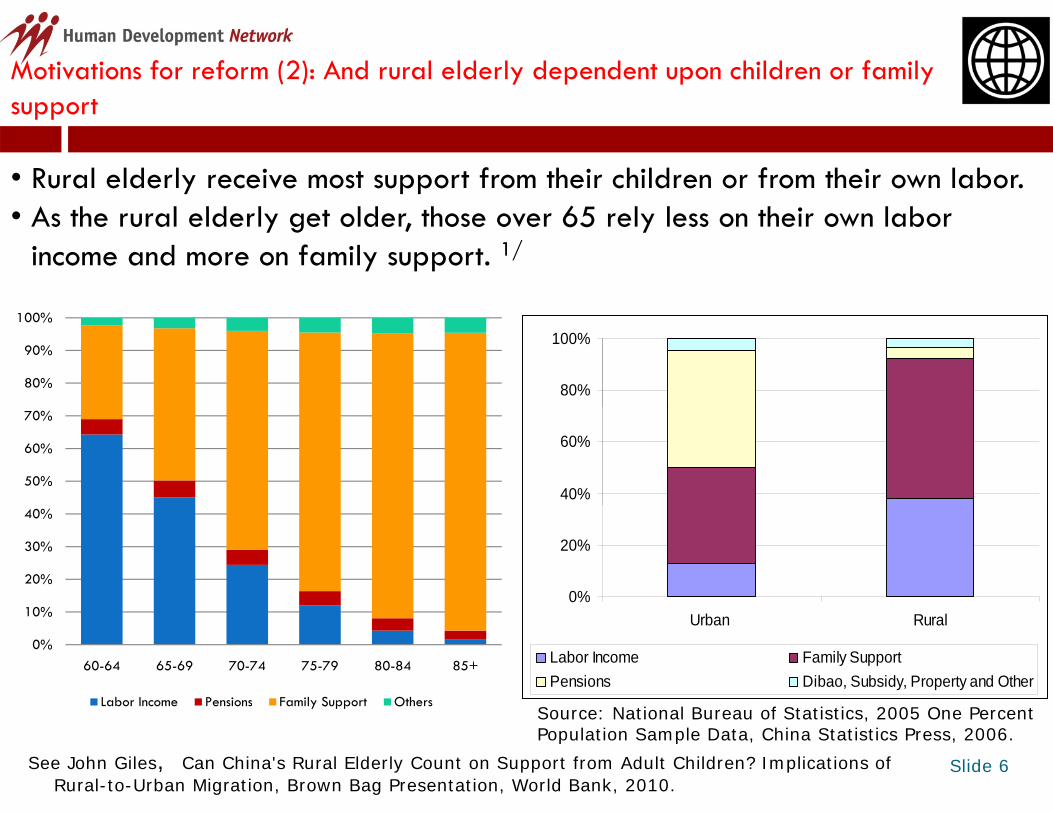

Motivations for reform (2): And rural elderly dependent upon children or family supportsupport

• Rural elderly receive most support from their children or from their own labor.A h l ld l ld h 65 l l h i l b • As the rural elderly get older, those over 65 rely less on their own labor income and more on family support. 1/

80%

100%

80%

90%

100%

40%

60%

50%

60%

70%

0%

20%

20%

30%

40%

Urban Rural

Labor Income Family SupportPensions Dibao, Subsidy, Property and Other

0%

10%

60-64 65-69 70-74 75-79 80-84 85+

Labor Income Pensions Family Support Others

Slide 6

Source: National Bureau of Statistics, 2005 One Percent Population Sample Data, China Statistics Press, 2006.

Labor Income Pensions Family Support Others

See John Giles, Can China's Rural Elderly Count on Support from Adult Children? Implications of Rural-to-Urban Migration, Brown Bag Presentation, World Bank, 2010.

Motivation for Reform (3): An important share of the rural elderly are poor or vulnerable particularly as they get very oldpoor or vulnerable, particularly as they get very old.

1991 1993 1997

Poverty Incidence by Age of Eldest Resident of the Household.5

.6.7

.81991 1993 1997

0.1

.2.3

.4

hare

5.6

.7.8

2000 2004Sh

0.1

.2.3

.4.

25-60 Years Old 60-70 Years Old71-80 80 and Above

Graphs by survey year

Slide 7Source: CHNS, Various Years

June 7, 2011

Motivations for reform (4): Addressing broader policy concerns

• Weak rural poverty protection mechanisms.p y p• Growing urban/rural income disparities.• Increasingly mobile population, often with little or no social

protection.

Slide 8

III. Design of the National Rural Pension SchemeIII. Design of the National Rural Pension Scheme

9

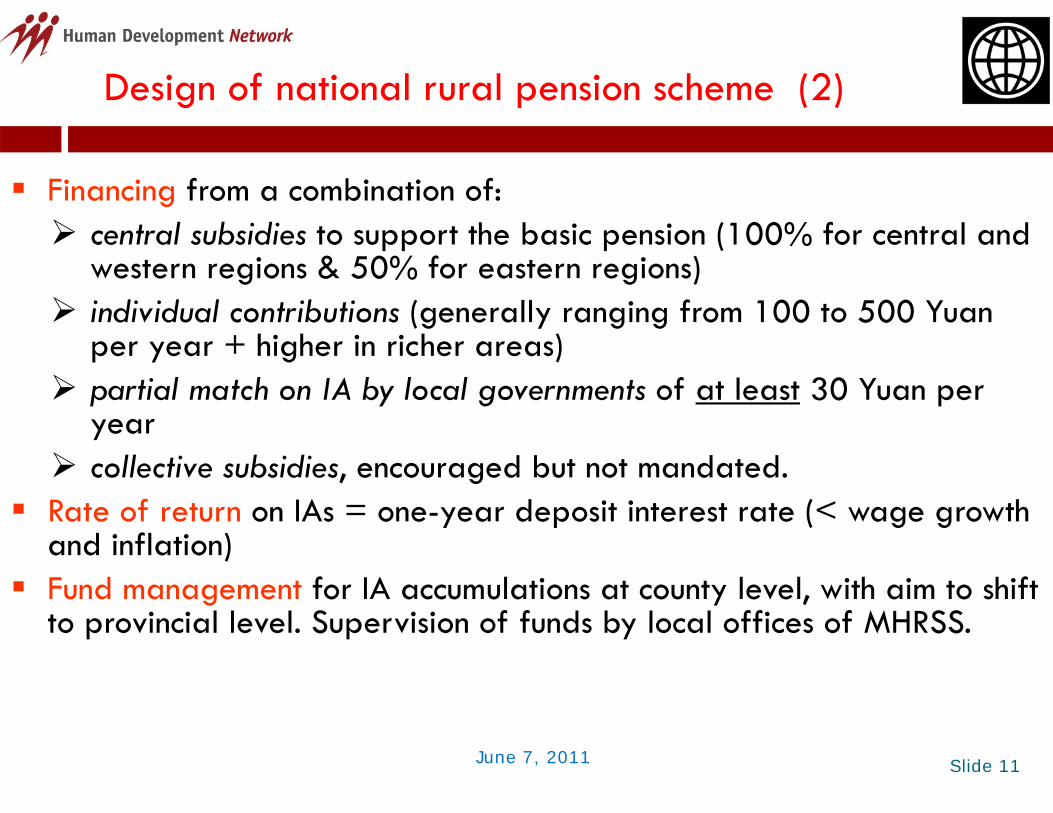

Design of national rural pension scheme (1)g p ( )

Two components:p Individual accounts with matching contributions (MDC)Basic (flat) pension at age 60 for workers who contribute 15 years.

“Family binding” provisions for those over 60 to receive basic pension provided children are contributing. Those aged 45-59 contribute during their working lives and pay lump sum to cover shortfall on during their working lives and pay lump sum to cover shortfall on vesting contributions.

Contributions for dibao beneficiaries are supposed to be covered by pp ylocal governments.

Slide 10June 7, 2011

Design of national rural pension scheme (2)

Financing from a combination of: central subsidies to support the basic pension (100% for central and

western regions & 50% for eastern regions) indi id al c ntrib ti ns (generally ranging from 100 to 500 Yuan individual contributions (generally ranging from 100 to 500 Yuan

per year + higher in richer areas) partial match on IA by local governments of at least 30 Yuan per

year collective subsidies, encouraged but not mandated.

R t f t IA = d it i t t t (< th Rate of return on IAs = one-year deposit interest rate (< wage growth and inflation)

Fund management for IA accumulations at county level, with aim to shift g y ,to provincial level. Supervision of funds by local offices of MHRSS.

Slide 11June 7, 2011

III. Initial ResultsIII. Initial Results

12

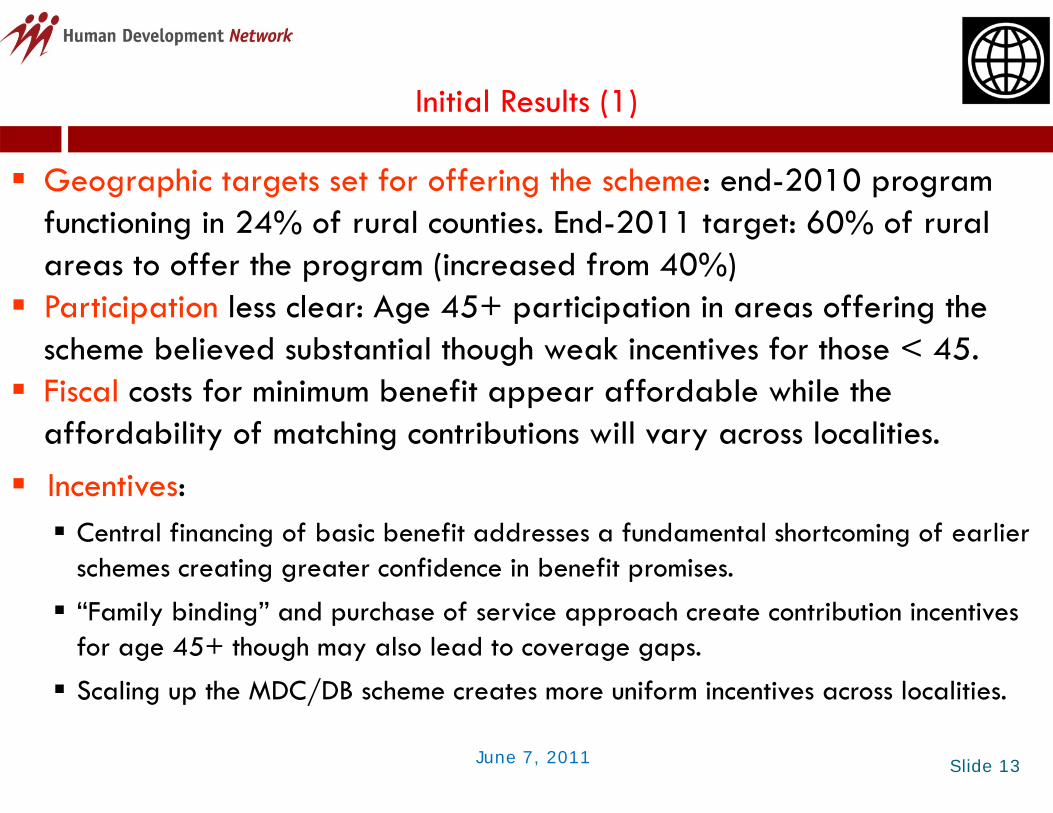

Initial Results (1)Initial Results (1)

Geographic targets set for offering the scheme: end-2010 program functioning in 24% of rural counties. End-2011 target: 60% of rural areas to offer the program (increased from 40%)

Participation less clear: Age 45+ participation in areas offering the Participation less clear: Age 45+ participation in areas offering the scheme believed substantial though weak incentives for those < 45.

Fiscal costs for minimum benefit appear affordable while the ppaffordability of matching contributions will vary across localities.

Incentives: Central financing of basic benefit addresses a fundamental shortcoming of earlier

schemes creating greater confidence in benefit promises.

“F il bi di ” d h f i h ib i i i “Family binding” and purchase of service approach create contribution incentives for age 45+ though may also lead to coverage gaps.

Scaling up the MDC/DB scheme creates more uniform incentives across localities.

Slide 13June 7, 2011

g p /

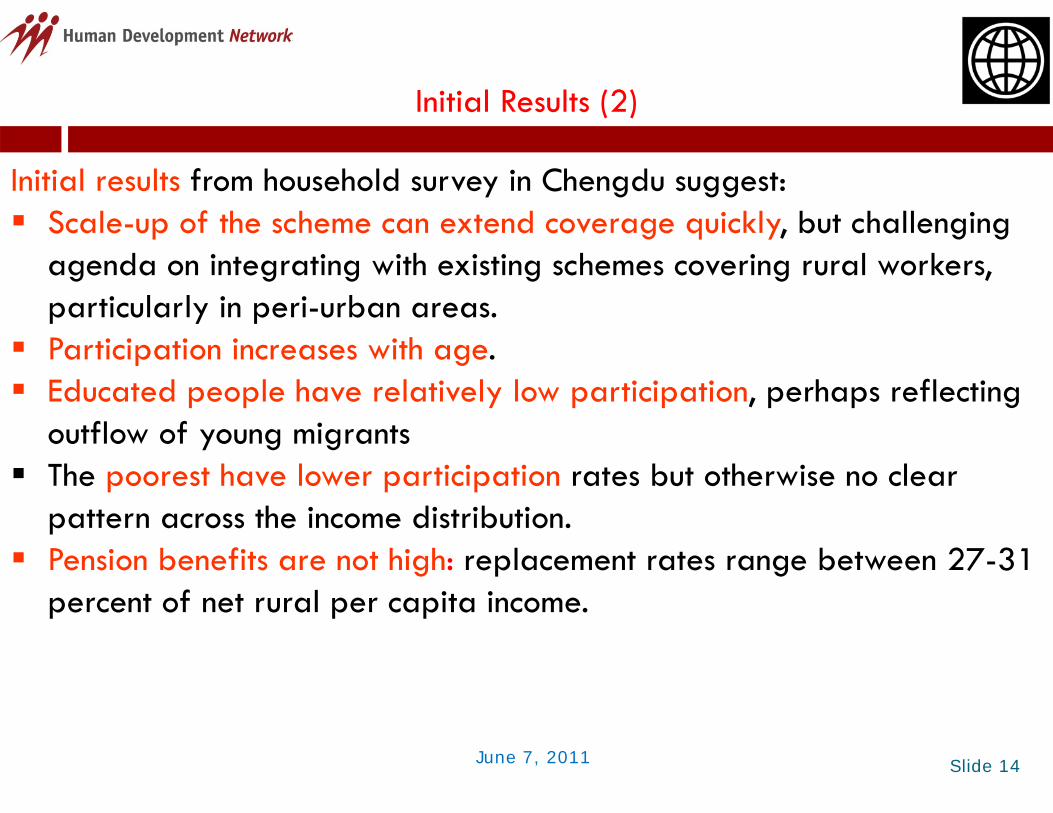

Initial Results (2)Initial Results (2)

Initial results from household survey in Chengdu suggest: Scale-up of the scheme can extend coverage quickly, but challenging

agenda on integrating with existing schemes covering rural workers, particularly in peri urban areasparticularly in peri-urban areas.

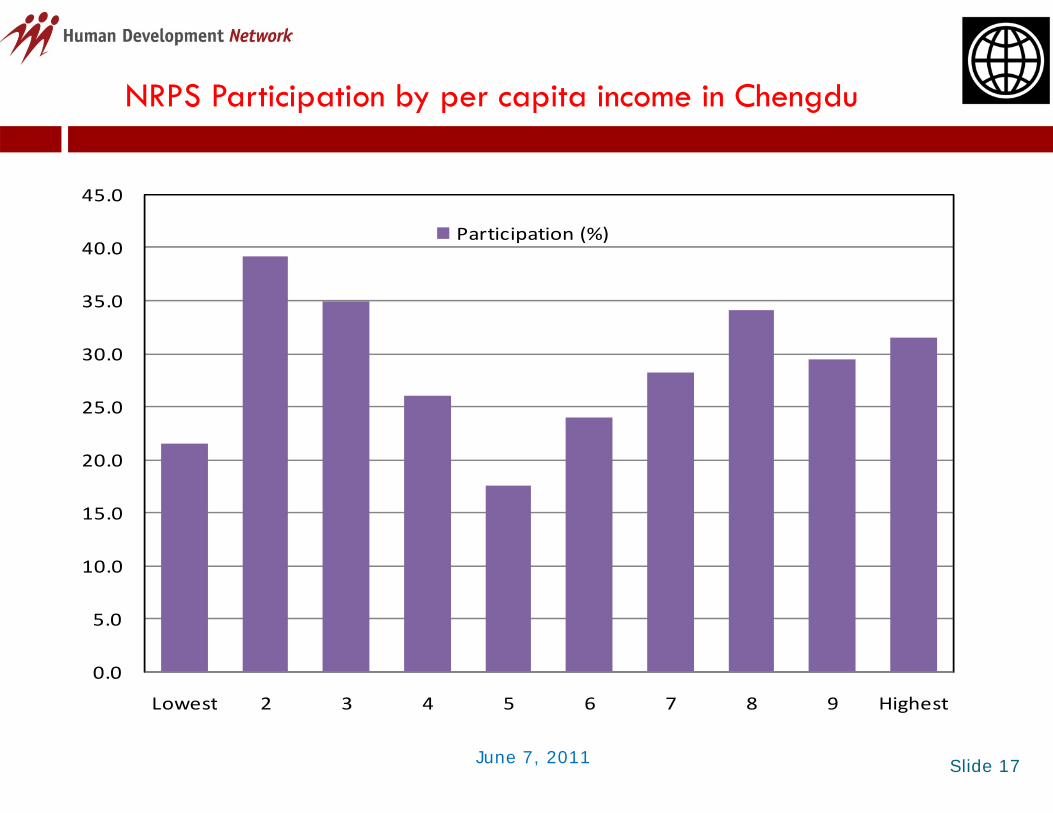

Participation increases with age. Educated people have relatively low participation, perhaps reflecting p p y p p , p p g

outflow of young migrants The poorest have lower participation rates but otherwise no clear

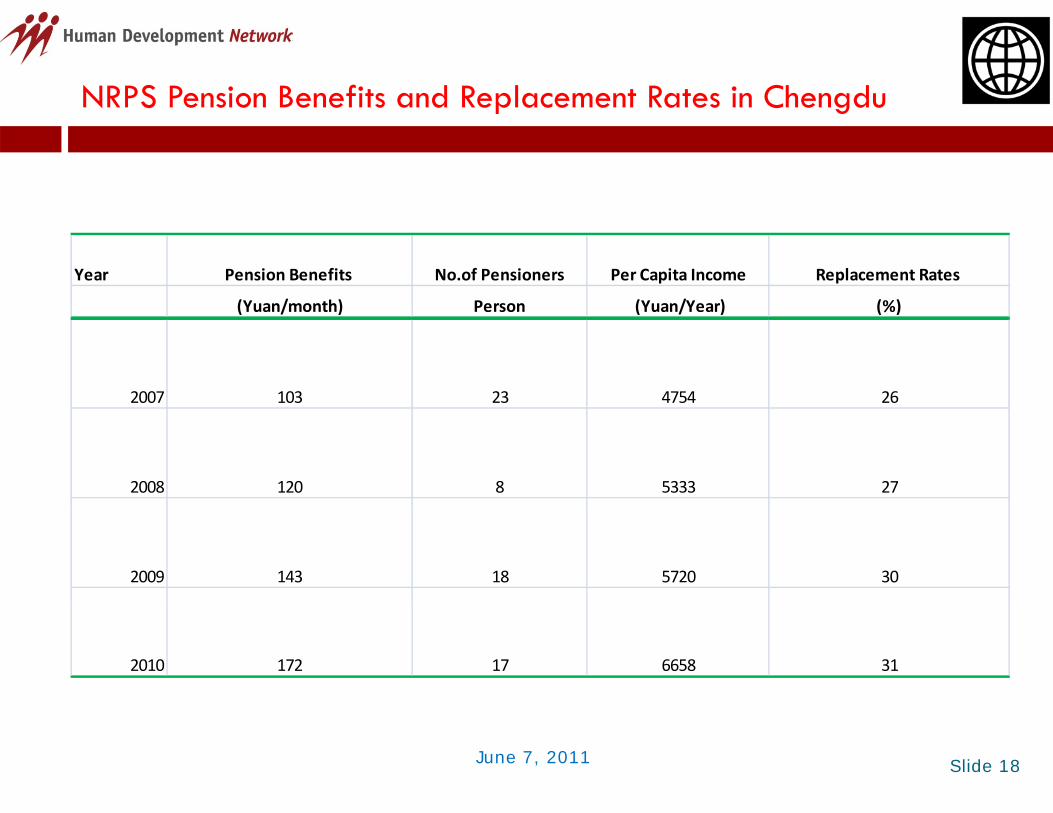

pattern across the income distribution. Pension benefits are not high: replacement rates range between 27-31

percent of net rural per capita incomepercent of net rural per capita income.

Slide 14June 7, 2011

NRPS is only part of the coverage story - Pension coverage by different schemes & by countydifferent schemes & by county

Country Jintang Congzhou Shuanliu TotalCountry Jintang Congzhou Shuanliu Total

National Rural Pension Scheme 27.8 4.1 0.4 9.8

Urban Worker Pension Scheme 3.3 3.8 5.0 4.1

Landless Farmers Pension Scheme 0.4 4.5 53.6 23.6

Mi C h i I 0 8 1 6 2 5 1 7Migrant Comprehensive Insurance 0.8 1.6 2.5 1.7

Other Schemes 0.2 0.8 0.2 0.4

Total 32.5 14.9 61.6 39.7

Slide 15June 7, 2011

NRPS Participation by Age and Education in Chengdup y g g

1

Slide 16June 7, 2011

NRPS Participation by per capita income in Chengdup y p p g

45.0

35.0

40.0Participation (%)

25 0

30.0

20.0

25.0

10.0

15.0

0.0

5.0

Lowest 2 3 4 5 6 7 8 9 Highest

Slide 17June 7, 2011

Lowest 2 3 4 5 6 7 8 9 Highest

NRPS Pension Benefits and Replacement Rates in Chengdup g

1 Year Pension Benefits No.of Pensioners Per Capita Income Replacement Rates

(Yuan/month) Person (Yuan/Year) (%)(Yuan/month) Person (Yuan/Year) (%)

2007 103 23 4754 26

2008 120 8 5333 27

2009 143 18 5720 30

2010 172 17 6658 31

Slide 18June 7, 2011

And there remain implementation challenges…p g

Establishing adequate service delivery networks at county level & g q y ybelow. Developing fund/budgetary management systems at a local level

to monitor the revenue streams from multiple parties and avoid the urban problem of “empty” accounts.

k f Linking up information systems to ensure necessary communication between and across levels of government. E t bli hi i bl h t t bilit f i ht d Establishing a viable approach to portability of rights and

linkages with urban pension arrangements.

Slide 19June 7, 2011

IV. Reflections on the Design and Remaining ChallengesIV. Reflections on the Design and Remaining Challenges

20

Reflections – link between design and objectivesg j

Does the design suit the objectives? Should alternatives be considered? Low target income replacement, largely flat benefits and subsidy

structure suggests elderly poverty protection is the core objective. Yet design largely a contributory flat defined-benefit social insurance Yet design largely a contributory flat defined-benefit social insurance

scheme. Achieving universal elderly poverty protection will require additional

b f d h dminimum benefit guarantees under the current design.

Alternatively establishing a non contributory social pension (pensions tested with Alternatively, establishing a non-contributory social pension (pensions tested with a low benefit target) might better achieve the objective of poverty protection with greater economic and operational efficiency.

An MDC arrangement with greater matching contributions and an annuitized An MDC arrangement with greater matching contributions and an annuitized benefit could provide basic income support, serve as a savings vehicle for smoothing consumption in retirement (and a stronger savings incentive for those <45) and pro ide a basis for adding p entitlements for China’s mobile

Slide 21June 7, 2011

<45), and provide a basis for adding up entitlements for China’s mobile workforce.

Reflections on new scheme design – Coverage incentives (1)g g ( )

Will combined subsidies and the basic benefit be sufficient invite id d i i i ? widespread participation?

Likely yes for those age 45+. Overall returns on contributions make for a very high 16% IRR on contributions (with low direct make for a very high 16% IRR on contributions (with low direct matching subsidies, low rates of return on individual accounts, basic benefits, generous annuity factors and survivors’ benefits). 2/

Minimum contributions affordable for most rural citizens.Overall, 15 years of contributions of 8.33 yuan/month (US$1.28) yields a benefit of 73 yuan/month (US$11 20) for 19 2 years (+ yields a benefit of 73 yuan/month (US$11.20) for 19.2 years (+ survivorship benefits) … a good deal for those who can afford it.While those under age 45 may only contribute on behalf of g y yparents.

Slide 22June 7, 2011

2/ See Larry Thompson, Guangdong Pension System Development, Preliminary Draft, 2011.

Reflections on new scheme design – Coverage incentives (2)g g ( )

Will contribution incentives lead to coverage gaps for those with lowest incomes or inability to meet the family binding/purchase of service requirements? Fi l it t t t ib ti b h lf f dib i i t Fiscal capacity to support contributions on behalf of dibao recipients

limited, but dibao recipients only about 6% of rural population. Local fiscal capacity for 30% match may be difficult in poorest Local fiscal capacity for 30% match may be difficult in poorest

localities. Migration may prove a barrier to meeting family binding g y p g y g

requirements. Uncovered elderly beneficiaries may or may not receive dibao

benefits.

Slide 23June 7, 2011

Reflections on new scheme design – Benefit adequacy

Will a benefit of 73 yuan (US$11.20) per month be adequate to protect the rural elderly from poverty? Adequacy low by most measures though depends upon the benchmark. 17% of rural per capital income (2009) 17% of rural per capital income (2009) 29% of $1.25/day73% of national poverty line & dibao threshold (2009)p y ( )

Effectiveness of the NRPS in achieving elderly poverty protection will depend upon the amount of supplementary financing provided by the

A f flocality. Additional financing and benefit guarantees likely needed in most of China. Further reducing income disparities may require committing to a higher Further reducing income disparities may require committing to a higher

minimum income target which is centrally financed.

Slide 24June 7, 2011

Looking ahead …g

How can policies and systems develop to ensure full portability of pension rights across space and occupation as the system matures?Wh i h i l f “ l” “i f l ” What is the potential to move from “rural” to “informal sector” pensions through parallel expansion of urban resident pensions and integration of rural and urban schemes for those outside the and integration of rural and urban schemes for those outside the formal sector? How will the NRPS be integrated with the recently announced national expansion of the urban resident pensions?announced national expansion of the urban resident pensions?

Slide 25June 7, 2011

V. Lessons for Other CountriesV. Lessons for Other Countries

26

Lessons for Other Countries

• Linking social pension eligibility with MDC contributions C iti l i t i ti th h ti & “f il bi di ” Can positively impact incentives through vesting req. & “family binding”

provisions. But poses institutional challenges & can come at the expense of coverage gapsWhile the same effect could be achieved by a much larger match which also

provides stronger incentives for younger workers.• Strong rural coverage through the NRPS compared with countries of comparable Strong rural coverage through the NRPS compared with countries of comparable

income and economic composition. A strong fiscal position and central fiscal transfers which guarantee a minimum

b fit ti i ti d dibilitbenefit can encourage participation and credibility. Yet need a unified institutional infrastructure is needed for mobilizing, managing

and disbursing pension savings in rural areas.• Portability - An MDC design can form the foundation for consolidating acquired

rights in a rapidly urbanizing economy where labor mobility is key to growth.

Slide 27June 7, 2011

References

1. Giles, John, Wang, Dewen, and Changbao Zhao, Can China's Rural Eld l C t S t f Ad lt Child ? I li ti f R lElderly Count on Support from Adult Children? Implications of Rural-to-Urban Migration, PPT Presentation, World Bank, 2010.

2. O’Keefe, Philip, Wang, Dewen, Closing the Coverage Gap –E l ti d I f R l P i i Chi PPT P t ti Evolution and Issues for Rural Pensions in China, PPT Presentation, Ageing in Asia Conference, Beijing, December 2010.

3. Poverty is No Simple Matter, Caixin online, May 11, 2011.h ll h h ’ l h4. Shen, Ce, Williamson, John B., China’s new rural pension scheme: can

it be improved? International Journal of Sociology and Social Policy, Vol. 30 Nos. 5/6, 2010.

5. Thompson, Larry, Guangdong Pension System Development, Preliminary Draft, 2011.

6. World Bank, China: A Vision for Pension Policy Reform, Draft, 2011.7. World Bank, China: From Poor Areas to Poor People - China’s Evolving

Poverty Reduction Agenda, 2009.8. World Bank, The Well-Being of China’s Rural Elderly and Old Age

Slide 28

Support, 2011.June 7, 2011