Embed Size (px)

Citation preview

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 1/34

From Enterprise

Protection to Social ProtectionPension Reform in China

P E T E R W H I T E F O R DDirectorate of Education, Employment, Labour and Social Affairs, Organisation for Economic Co-operation and Development

abstract The Chinese system of social protection has been subjectto significant reforms over the past 25 years, but it can still be regardedas a system in transition. These reforms have been impressive in scopeand much has been achieved in extending coverage, pooling resources,improving administration of payments, and in starting to address theissue of future financing requirements. Nevertheless, the system is not

yet fully appropriate for the challenges facing China over the nextdecade and beyond. This article assesses the main features of thedevelopment of the Chinese pension system, and identifies a numberof issues to be addressed as part of future reforms. The articlecompares the Chinese system with those operating in other worldregions, and also in other parts of Asia. Chinese developments are alsodiscussed in the context of global social policy developments and therole of international organizations. The article also discusses possibleapproaches to dealing with future challenges.

keywords ageing, China, pensions, social security

A RT I C L E 45

Global Social Policy Copyright © 2003SAGE Publications (London, Thousand Oaks, ca and New Delhi)

vol. 3(1): 45–77. [1468-0181 (200304) 3:1; 45–77; 032011]

gsp

Introduction

This article assesses developments in retirement income policies in China, with an emphasis on reforms over the past decade. China is facing a numberof transitions, including the transition from a centrally planned to a‘socialist market’ economy; the transition from a rural society to a moreurbanized and industrialized society; the transition accompanying rapid

economic growth from a low income to a middle income, but more unequalsociety; and the demographic transition that will result in a substantially higher proportion of older people in the population in the next 25 to 50

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 2/34

years. Not unexpectedly, the institutions promoting social protection are notnecessarily appropriate for a society experiencing complex transitions inthese and other areas. Overlaying this is the fact that China is the largestsociety in the world, so that the scope of the challenges to be addressed often

appears daunting if not overwhelming. Complexity is further increased by the fact that changes are linked in important respects, so that, for example,reforms to social protection are a component of reforms to state ownedenterprises (SOE) and collectively owned enterprises (COE). In this sense,reforms involve more complex linkages than is common in assessing socialpolicy issues in OECD countries.

The article is structured as follows. The next section outlines the historicaldevelopment of the current system since the 1950s. This is followed by a

description of the current system. After examining trends in spending andrecipient numbers, the article compares the characteristics of the pensionsystem in China with those applying in other regions of the world, as well asother significant Asian economies. This is followed by a discussion of themain policy challenges facing China in this area, and a range of possibleapproaches to deal with these challenges.

A number of caveats should be noted. The Chinese system of socialprotection has been subject to significant change and experimentation overthe past 10 years, and is still in the process of transition. The pension system

was reformed in 1997, with changes being phased in across the country overthe subsequent two to three years. Those already retired were not affectedby these changes, while those already employed have transitional rules toprotect their entitlements. The discussion below describes the rules of thepost-1997 system, but in fact the vast majority of current pensioners are stillbeing paid under the old rules, which were more generous in terms of replacement rates, for example. The situation is further complicated by therapidity of changes in outcomes (e.g. coverage) as the result of these reforms.

Moreover, the most recent data generally refer to 1999 or 2000, so that thephasing-in process itself was not necessarily complete in the period coveredby the data.

The Chinese social insurance system involves central governmentguidelines, which are adapted by provincial and city or county governmentsto local conditions. Actual rules may differ across regions – for example,replacement rates have ranged from 65 percent to 102 percent (Stanton and

Whiteford, 1998). Due to these variations of time and space, rather than

being one system, the Chinese pension system could be thought of as anumber of systems. This is not necessarily surprising in a country the size of China.

As a result of these complexities, the discussion that follows should not beregarded as definitive. At this stage it may be more appropriate to talk of directions and tendencies. This situation may continue for many years, withfurther modifications of the system in the light of new challenges.

46 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 3/34

Main Historical Developments

In 1951 the Communist government introduced Regulations on Labour Insurance, providing the framework for the provision of various benefits

based on the principle of lifetime employment and association with a stateowned enterprise. The Regulations were patterned after the Soviet model.

Although in theory they covered only SOE and COE employees, they wereapplicable to nearly all urban workers including government employees andthose in related sectors such as schools, youth organizations, universities,health care, etc. Significantly, they did not apply to the majority of the

workforce in China, the rural peasants. Male workers became eligible for apension at 60 years of age after 25 years continuous employment. For female

workers the qualifying age was either 50 or 55 after 20 years employment.(In the 1955–60 period, average life expectancy at birth was 43.1 years formen and 46.2 years for women.) The pension was typically 50 to 70 percentof the standard wage depending on the number of years in employment.

The scheme was administered at the local level by trade union committeesunder the umbrella of the All China Federation of Trade Unions (ACFTU).

The ACFTU became responsible for administration at the national level in1954. The scheme was funded through employer contributions set at 3percent of the total enterprise wage bill, out of which 30 percent was paid

into a special ACFTU controlled fund responsible for the payment of pensions. As the workforce was then relatively young, there were fewdemands on the fund and throughout the 1950s and early 1960s, asubstantial surplus was built up.

This system practically ceased to exist during the Cultural Revolution when trade unions were abolished and the funds were used for otherpurposes. Individual enterprises became responsible for paying pensions andother benefits out of current revenues. This practice continued after the

Cultural Revolution ended. The labour insurance pension scheme that hadexisted before was not re-established and individual SOE continued to besolely responsible for pension provision and other benefits including healthand housing.

During the Cultural Revolution many older workers had the grant of theirretirement pension postponed and continued to work beyond retirementage. In 1978 the State Council amended the retirement component of theLabour Insurance Regulations providing these and other workersapproaching retirement age with incentives to leave the labour force. This

was to secure employment for younger workers who had been sent to ruralareas during the Cultural Revolution and who were now returning to thecities. The 1978 amendments relaxed the eligibility criteria to permitpensions after 10 instead of 20 years of continuous employment. They alsointroduced higher pension rates, ranging from 60 percent of standard wagesfor workers with 10–15 years of employment up to 75 percent for those who

Whiteford: Social Protection: Reform in China 47

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 4/34

had worked for 20 years or more. They also extended the ‘substitute’ (‘dingti’) option to all state employees. A job in a state sector was promised to onechild per retiree. The parent would get full pension; the child would secure afull state salary and benefits (Davis, 1988). In addition, the 1978

amendments formalized the practice of enterprises bearing full responsibility for all of the labour insurance benefits (including old retirement pensions)due to their employees (Fuery et al., 1996).

The number of pensioners nearly doubled in the year after the 1978regulations. Expenditure increased almost 19 times between 1978 and 1988.

The increase in the number of pensioners after 1978 substantially changedthe ratio of pensioners to workers. In 1978, there were 30.3 workers perpensioner; by 1988 the ratio had fallen to 6.4:1 (Chai, 1992). In recognition

of these emerging problems, in 1986 the Government introducedregulations requiring all new SOE employees to make contributions of up to3 percent of their basic wages, along with employer contributions of 15percent of the enterprise’s pre-tax wages bill. Contributions were paid intocollective funds operated by newly established Social Insurance Agencies(SIA). These funds superseded the practice of leaving individual enterprisessolely responsible for pension payments. By the end of 1991 all counties andcities had set up their own SIA to administer the funds and two third of

workers in SOE were covered. In 1992 the establishment of pension funds was extended to COE. It was also not uncommon for some enterprises torequire contributions from both new recruits and those employed before 1October 1986 when the new scheme was introduced.

Although the major portion of contributions still came from employers,the 1986 reforms introduced the concept of individual contributions into thepension system. Another important innovation was the establishment of agencies that managed pension funds independent of employing enterprises.

As a result enterprises gradually ceased to be seen by their employees as the

main provider of social security benefits. The reforms in the mid-1980s wereaimed at reducing costs for enterprises and establishing a more effectivefunding base. They were initially introduced on an experimental basis withlocal variations. As with the establishment of special economic zones, theChinese government chose to allow certain provinces to test a number of new programmes. Two approaches gradually evolved. One was outlined inthe 1991 State Council Resolution on the Reform of the Pension System for

Enterprise Workers, promoting the integration of local programs at the

provincial level and eventually at a national level. Alternatively, some citiesand provinces were developing new programs that differed from the nationalnorm, setting up fully funded pension programs that often extendedcoverage to include private and joint-venture enterprises.

The 1991 Resolution constituted a significant step in the furtherdevelopment of the system. It aimed to bring all workers in SOE into auniform pension scheme with three tiers. These were a basic pension for all

48 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 5/34

retirees jointly financed by the state, enterprises and the workers; asupplementary scheme funded by the enterprise from its trading surplus; andan account funded by individual worker, on a voluntary basis, and payable atretirement as a lump sum. As on previous occasions, the 1991 Resolution

laid down guidelines rather than binding directives. The Resolutionrecommended that social insurance funds should be set up at the provinciallevel and once established, the distinction between the permanent andcontract workers’ fund should be abolished and they should be unified undera system of pooling. The old practice of requiring individual enterprises topay the pensions of their retired workers was now to be replaced by collective funds where the responsibility was shared between the state, theenterprise and individual worker. Some provinces also began experimenting

with a more individually-focused, two tiered approach funded by employeeand employer contributions without the guaranteed government-backedbasic pension. This approach was particularly popular with employees inprivate and joint-venture enterprises. They often had few retirees on theirpayrolls and thus saw pooling as a form of subsidising state-sector retirees.Furthermore because contributions represented a percentage of payroll,private firms that paid higher salaries had to shoulder a greater burden.

The Government attempted to broaden coverage by introducing pensionschemes for the rural population, initially on an experimental basis. In

January 1991, under the ‘Basic Plan for Old Age Social Insurance in theCountryside’ the State Council decided to develop old-age social insurancein rural areas and designated the Ministry of Civil Affairs to be responsiblefor the project.

In the 1990s the success of various experimental approaches, together withthe sustained growth of the economy, encouraged the authorities to continuetheir efforts to reform the pension system, but in more unified way thanbefore. The two crucial policy documents were the 1995 State Council

Circular on Deepening the Reform of the Old Age Pension System for Enterprise Employees and the 1997 State Council Document No. 26 . In the first, the StateCouncil offered provinces a choice of two plans. Despite the fact that theprovinces, in fact, adopted a wider range of variants the regulationestablished the principle that policy on pension design was a Government,and not an enterprise, responsibility. The 1997 Document approved a planto finally establish a unified nationwide basic pension insurance system toreplace all pilot programmes in each province by the end of the century.

Current Social Security Arrangements

OVERVIEW

China now has a range of social protection mechanisms, including socialinsurance programmes, as well as social assistance and welfare programmes.

The social insurance programmes cover many of the contingencies usually

Whiteford: Social Protection: Reform in China 49

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 6/34

50 Global Social Policy 3(1)

t a b l e

1

A n o v e r v i e w

o f s o c i a l p r o t e c t i o n p r o g r a m m

e s i n C h i n a

E x p e n d i t u r e

E x p e n d i t u r e

R

e v e n u e

R e v e n u e

R e c i p i e n t s

C o n

t r i b u t o r s

P r o g r a m m e

( m i l l i o n y u a n

)

% G D P

( m i l l i o n y u a n )

% G D P

( m i l l i o n )

( m i l l i o n )

O l d A g e I n s u r a n c e

1 9 2 , 4 8 5 . 4 3

2 . 3 5 0

1 9 6 , 5 1 1 . 5 1

2 . 3 9 9

2 9 . 8 4

9 5 . 0 2

O c c u p a t i o n a l I n j u r y

1 , 5 4 1 . 6 4

0 . 0 1 9

2 , 0 8 7 . 8 1

0 . 0 2 5

–

3 9 . 1 2

M a t e r n i t y

7 1 2 . 7 4

0 . 0 0 9

1 , 0 7 4 . 8 8

0 . 0 1 3

–

2 9 . 3 0

H e a l t h i n s u r a n c e *

6 , 9 0 7 . 3 5

0 . 0 8 4

8 , 9 8 6 . 6 0

0 . 1 1 0

5 . 5 6

1 5 . 0 9

U n e m p l o y m e n t I n s u r a n c e

9 , 1 6 0 . 0 0

0 . 1 1 2

1 2 , 5 2 0 . 0 0

0 . 1 5 3

1 . 0 1

9 8 . 5 2

T o t a l S o c i a l I n s u r a n c e

2 1 0 , 8 0 7 . 2 0

2 . 5 7 0

2 2 1 , 1 8 0 . 8 0

2 . 7 0 0

–

–

D i s a s t e r R e l i e f

3 , 4 0 5 . 0 0

0 . 0 4 2

–

–

–

–

S o c i a l W e l f a r e a n d R

e l i e f F u n d s

4 , 8 5 2 . 0 0

0 . 0 5 9

–

–

–

–

L o w e s t C o s t o f L i v i n g G u a r a n t e e

–

–

–

–

5 . 3 2

–

U r b a n

–

–

2 . 6 6

–

R u r a l

–

–

2 . 6 6

–

P e r s o n s i n r u r a l h o u

s e h o l d s

–

–

–

–

1 6 . 6 0

–

r e c e i v i n g r e l i e f f u n d s

P e r s o n s i n u r b a n h o u s e h o l d s

–

–

–

–

1 . 5 7

–

r e c e i v i n g r e l i e f f u n d s

R e c i p i e n t s o f t h e 5 g

u a r a n t e e s

–

–

–

–

3 . 0 4

–

P e n s i o n s f o r h a n d i c a p p e d a n d

5 , 4 6 0 . 0 0

0 . 0 6 7

–

–

–

–

b e r e a v e d f a m i l i e s

O t h e r

4 , 2 8 0 . 0 0

0 . 0 5 2

–

–

–

–

T o t a l s o c i a l s e c u r i t y

a n d w e l f a r e

1 7 , 9 9 0 . 0 0

0 . 2 2 0

–

–

–

–

M e m o r a n d u m :

S u b s i d i e s t o s o c i a l s e c u r i t y

3 2 , 5 3 6 . 7 2

0 . 3 9 7

p r o g r a m m e s

P r i c e S u b s i d i e s

3 8 , 3 7 1 . 2 0

0 . 4 6 8

E x p e n d i t u r e o n R e t i r e d i n

3 6 , 0 1 5 . 3 5

0 . 4 4 0

A d m i n i s t r a t i v e D e p a

r t m e n t s

P u b l i c H e a l t h E x p e n d i t u r e

4 3 , 8 4 9 . 3

0 . 5 3 5

* I n a d d i t i o n t o t h o s e a c t i v e l y c o n t r i b u t i n g t o h e a l t h i n s u r a n c e t h e r e a r e a f u r t h e r 5 . 5

6 m i l l i o n r e t i r e d p e o p l e w i t h h

e a l t h i n s u r a n c e c o v e r a g e , g i v i n g t o t a l

c o v e r a g e o f 2 0 . 6 5 m i l l i o n p e o p l e

S o u r c e : M i n i s t r y o f L a b

o u r a n d S o c i a l S e c u r i t y , 2 0 0 0 a n d N a t i o n a l B u r e a u o f S t a t i s t i c s , 2 0 0 0 .

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 7/34

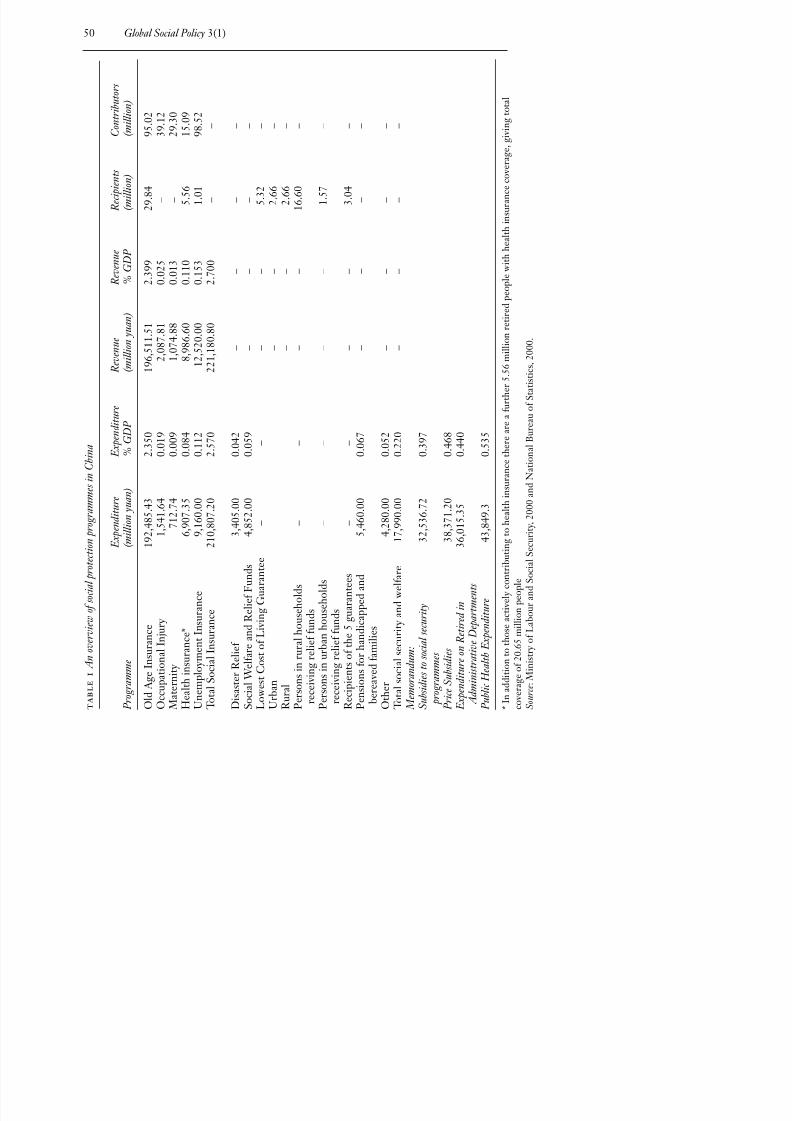

covered in OECD countries, including old age, unemployment, health care,maternity and occupational injury. Table 1 shows the main social insuranceand assistance programmes in 1999, together with the level of spending andrecipient and contributor numbers where relevant. Overall, spending on

social insurance programmes in 1999 amounted to 2.57 percent of GDP (notincluding civil servant’s pensions). Social assistance programmes are muchless significant (about 0.2% of GDP), and include disaster relief plus anumber of restrictive schemes for the very poor who have no other forms of support from their families.

Administration of social protection programmes is divided across anumber of Ministries. Since 1997, social insurance has been theresponsibility of the former Ministry of Labour, now called the Ministry of

Labour and Social Security (MOLSS). Rural issues are largely theresponsibility of the Ministry of Agriculture (although there is a Departmentof Rural Social Insurance under MOLSS.). The Ministry of Civil Affairs(MOCA) supervises social assistance.

RETIRMENT PENSIONS

Retirement pensions are by far the most significant social protectionprogramme in China. In 1999 expenditure was around 2.35 percent of GDP.

There were around 95m contributors to the system and around 30mpensioners. The urban pension system now covers 90 percent of all active

workers within the groups for whom it is compulsory. As a proportion of estimated total urban employment, the pension system has covered about 45percent of the urban labour force since the early 1990s, or around 60 percentincluding civil servants.

The main features of the system are as follows. Most importantly, thesystem involves central government guidelines, which are adapted by provincial, city or county governments to local conditions. The basic old-

age pension has two components: a notional defined contribution plan withan individual account established for each worker, and a defined benefit planknown as the social pension, based on a social pooling account. Pools arebased on location (cities, prefectures or provinces) or industry (civil aviation,railroads). The current level of employee contributions to individualaccounts is increasing to 8 percent. The maximum enterprise contribution isset at 20 percent of total payroll, but in practice there is substantial variationranging from 15–30 percent.

The retirement age is 60 (men) and 55 (women in salaried positions) and50 (women in blue-collar jobs). Those working in designated harsh ordangerous conditions may retire five years earlier; senior professionals may retire five years later. The recommended consecutive length of service toqualify for a pension is not less than 15 years, although practice varies. Early retirement is allowed at 50 for men or 45 for women who have 10 years’coverage and are totally disabled.

Whiteford: Social Protection: Reform in China 51

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 8/34

A basic pension is payable from the pooling fund. This is 20 percent of thecity-wide or countywide average wage of the preceding year. No pension ispayable for those with less than 15 years’ contributions, except in the case of approved early retirement. On retirement, the accumulated contributions

and interest in individual accounts will be translated into monthly benefitsequal to 1/120th of the total balance. The combination of social pooling andannuities from individual accounts could be expected to provide areplacement rate of around 60 percent.

By definition, those who live for more than 10 years after retirement willbenefit from redistribution. This is because they will continue to receivepensions even though their individual accounts have ‘run out’. Workers withless than 15 years’ contributions receive a lump sum of the balance in their

account. A disability pension is payable for those who have total incapacity for work and are ineligible for early retirement. This is payable at 40 percentof wages, with provincial and city or country governments setting minimumbenefits according to local standards of living. The basic payment forsurvivors involves a lump sum of between 6 and 12 months wage (dependingon the number of surviving dependants) if the deceased was in coveredemployment or a pensioner. The legal heir also receives a lump sum equal tothe balance of the employee’s total contributions, plus interest.

OTHER RETIREMENT INCOME SYSTEMS

There is also an enterprise supplementary insurance scheme that isemployer-sponsored but voluntary. Involvement in supplementary occupational pension plans is very limited in scope. An enterprise must firstmeet its obligations to the basic pension scheme before it can offer anoccupational pension. All contributions by employees and employers go intoindividual accounts, which on retirement can be drawn on either as a lumpsum or in regular withdrawals. This scheme, which was introduced in 1991,

covers some 5m workers with a total accumulation of 6.4bn yuan (about 0.08percent of GDP).

There are a number of other relevant systems. There is a differentprogramme for civil servants and employees of State organizations andinstitutions. This is a pay-as-you go system, financed by government or the

working units, with no individual contributions. For civil servants, all theirbasic wage and seniority wage is paid after retirement, with the proportionof their position wage and their post wage paid increasing from 40 percent

for those with less than 10 years service to 88 percent for those with morethan 35 years service. For employees in State institutions, a proportion of their basic wage and post wage is paid – ranging from 50 percent for those

with less than 10 years service to 90 percent for those with 35 years or moreof service. This system covers 30m people (MOLSS, 2000). Expenditure in1999 is estimated at 0.44 percent of GDP.

The Government in its Basic Plan for Old Age Social Insurance in the

52 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 9/34

Countryside (1991) outlined plans to introduce pension schemes for the ruralpopulation. Individual contributions are made monthly or annually, at one of 10 levels (between 2 and 20 yuan a month), according to the member’sfinancial capacity. This represents 80 percent of the total contribution, with

the member’s employer (rural collective or township village enterprise)paying the remaining 20 percent. Contributions are paid into individualaccounts managed by the local social insurance fund and invested in banksand government bonds at set rates of return. Pensions are payable from age60, but individual contributions are made at a very low rate and only marginally supplemented by employers, so pensions represent only a very basic form of protection for the rural aged. There are around 82.25m ruralpeople covered by this system. Current payments are made to around

500,000 rural people (MOLSS, 2000). Accumulated funds have reachednearly 120bn yuan (Zhou Jianguo, 2001). There is also a range of social assistance programmes, including the

minimum living guarantee, a means-tested programme. While programmesexist in rural areas, the greatest policy attention is paid to urban areas, wherebenefit amounts are higher and where the need for a last resort is seen ashigher because of rising unemployment. The reported number of urbanbeneficiaries in 2000 was 3.8m, up from 2.7m in 1999 (MOLSS, 2001).

MOLSS has estimated that a further 10m urban workers were eligible butdid not receive benefits in 2000. About 80 percent of the reportedbeneficiaries in 2000 belonged to groups, such as the laid-off, retired persons

with low pensions and disabled persons.In rural areas, the biggest social support programme assists poor farmers

after natural disasters. In practice, such support is largely concentrated inregions that are not only poor but also characterized by frequent droughts.

Another rural programme is the ‘ five guarantees ’ (meals, clothes, housing,funeral and education), which essentially is locally financed. It applies to

persons suffering ‘three noes’: no children, no family, and no resources. Most beneficiaries are elderly persons and orphans, and they typically stay innursing homes or receive grain.

Trends in Spending and Recipient Numbers

Table 2 shows trends in spending on the main social insurance benefits, plussocial assistance and relief payments over the period 1989 to 1999. In brief,

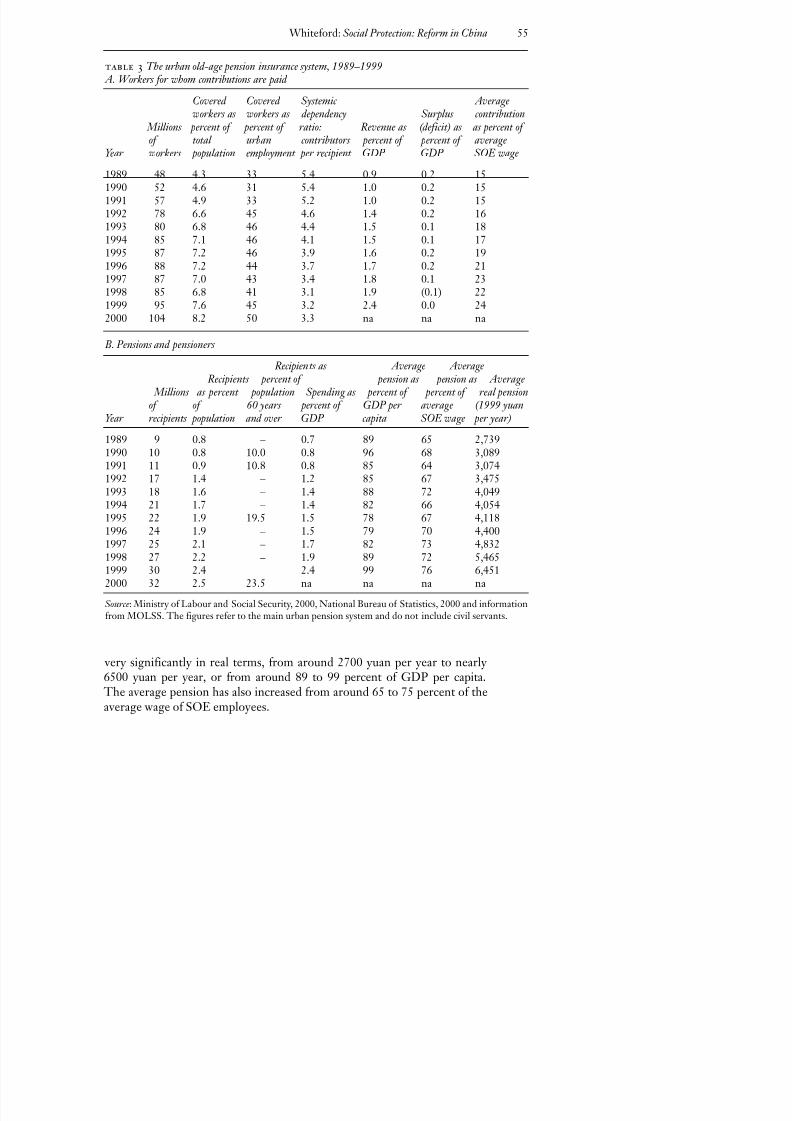

for the periods for which data are available, all the contributory programmesshow very significant increases in spending. In every period, however, it isspending on retirement pensions that predominates. Table 3 shows trends inthe urban pension system. Between 1989 and 2000 spending increased from0.7 percent to 2.35 percent of GDP. The number of retirement pensionersincreased from around 9m to 32m, or from about 0.8 percent to 2.5 percentof the Chinese population. Average benefits per recipient have increased

Whiteford: Social Protection: Reform in China 53

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 10/34

54 Global Social Policy 3(1)

t a b l e

2

S p e n d i n g o n

s o c i a l s e c u r i t y i n C h i n a , 1 9 8 9 t o 1 9 9 9 ( % o f G D P )

S o c i a l

P e n s i o n s f o r

O c c u p a t i o n a l

T o t a l

w e l f a r e

h a n d i c a p p e d

A g e

H e a l t h

i n j u r y

M a t e r n i t y

U n e m p l o y m e n t s o c i a l

a n d

D i s a s t e r

a n d b e r e a v e d

Y e a r

p e n s i o n s

i n s u r a n c e

i n s u r a n c e

I n s u r a n c e

i n s u r a n c e

i n s u r a n c e r e l i e f f u n d s

r e l i e f

f a m i l i e s

O t h e r T o t a l

1 9 8 9

0 . 7 0

–

–

–

–

0 . 7 0

0 . 0 6 4

0 . 0 7 6

0 . 0 8 5

0 . 0 1 7

0 . 9 5

1 9 9 0

0 . 8 1

–

–

–

–

0 . 8 1

0 . 0 6 5

0 . 0 7 2

0 . 0 8 9

0 . 0 1 8

1 . 0 5

1 9 9 1

0 . 8 0

–

–

–

–

0 . 8 0

0 . 0 6 1

0 . 1 0 4

0 . 0 8 0

0 . 0 1 9

1 . 0 6

1 9 9 2

1 . 2 1

–

–

–

–

1 . 2 1

0 . 0 5 4

0 . 0 6 0

0 . 0 6 9

0 . 0 2 0

1 . 4 1

1 9 9 3

1 . 3 6

0 . 0 0 4

0 . 0 0 1

0 . 0 0 1

–

1 . 3 7

0 . 0 4 9

0 . 0 4 4

0 . 0 6 0

0 . 0 2 3

1 . 5 4

1 9 9 4

1 . 4 1

0 . 0 0 6

0 . 0 0 2

0 . 0 0 2

–

1 . 4 2

0 . 0 4 4

0 . 0 4 1

0 . 0 5 3

0 . 0 2 2

1 . 5 8

1 9 9 5

1 . 4 5

0 . 0 1 2

0 . 0 0 3

0 . 0 0 3

–

1 . 4 7

0 . 0 4 1

0 . 0 4 7

0 . 0 5 0

0 . 0 2 1

1 . 6 3

1 9 9 6

1 . 5 2

0 . 0 2 4

0 . 0 0 5

0 . 0 0 5

–

1 . 5 5

0 . 0 4 3

0 . 0 5 8

0 . 0 4 8

0 . 0 2 4

1 . 7 3

1 9 9 7

1 . 6 8

0 . 0 5 4

0 . 0 0 8

0 . 0 0 7

–

1 . 7 5

0 . 0 4 9

0 . 0 4 6

0 . 0 5 0

0 . 0 2 7

1 . 9 2

1 9 9 8

1 . 9 3

0 . 0 6 8

0 . 0 1 2

0 . 0 0 9

0 . 0 6 6

2 . 0 8

0 . 0 4 5

0 . 0 6 7

0 . 0 5 2

0 . 0 3 4

2 . 2 8

1 9 9 9

2 . 3 5

0 . 0 8 4

0 . 0 1 9

0 . 0 0 9

0 . 1 1 2

2 . 5 7

0 . 0 5 9

0 . 0 4 2

0 . 0 6 7

0 . 0 2 8

2 . 7 7

S o u r c e : C a l c u l a t e d f r o m

M i n i s t r y o f L a b o u r a n d S o c i a l S e c u r i t y , 2 0 0 0 a n d N a t i o n a l B u r e a u o f S t a t i s t i c s , 2 0 0 0 .

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 11/34

very significantly in real terms, from around 2700 yuan per year to nearly 6500 yuan per year, or from around 89 to 99 percent of GDP per capita.

The average pension has also increased from around 65 to 75 percent of theaverage wage of SOE employees.

Whiteford: Social Protection: Reform in China 55

table 3 The urban old-age pension insurance system, 1989–1999 A. Workers for whom contributions are paid

Covered Covered Systemic Averageworkers as workers as dependency Surplus contribution

Millions percent of percent of ratio: Revenue as (deficit) as as percent of of total urban contributors percent of percent of average

Year workers population employment per recipient GDP GDP SOE wage

1989 48 4.3 33 5.4 0.9 0.2 151990 52 4.6 31 5.4 1.0 0.2 151991 57 4.9 33 5.2 1.0 0.2 151992 78 6.6 45 4.6 1.4 0.2 161993 80 6.8 46 4.4 1.5 0.1 181994 85 7.1 46 4.1 1.5 0.1 17

1995 87 7.2 46 3.9 1.6 0.2 191996 88 7.2 44 3.7 1.7 0.2 211997 87 7.0 43 3.4 1.8 0.1 231998 85 6.8 41 3.1 1.9 (0.1) 221999 95 7.6 45 3.2 2.4 0.0 242000 104 8.2 50 3.3 na na na

B. Pensions and pensioners

Recipients as Average Average

Recipients percent of pension as pension as Average Millions as percent population Spending as percent of percent of real pensionof of 60 years percent of GDP per average (1999 yuan

Year recipients population and over GDP capita SOE wage per year)

1989 9 0.8 – 0.7 89 65 2,7391990 10 0.8 10.0 0.8 96 68 3,0891991 11 0.9 10.8 0.8 85 64 3,0741992 17 1.4 – 1.2 85 67 3,4751993 18 1.6 – 1.4 88 72 4,0491994 21 1.7 – 1.4 82 66 4,0541995 22 1.9 19.5 1.5 78 67 4,1181996 24 1.9 – 1.5 79 70 4,4001997 25 2.1 – 1.7 82 73 4,8321998 27 2.2 – 1.9 89 72 5,4651999 30 2.4 – 2.4 99 76 6,4512000 32 2.5 23.5 na na na na

Source: Ministry of Labour and Social Security, 2000, National Bureau of Statistics, 2000 and informationfrom MOLSS. The figures refer to the main urban pension system and do not include civil servants.

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 12/34

The number of contributors to old-age insurance more than doubled toaround 104m in 2000, rising from 4.3 to 8.2 percent of the total population.Coverage correspondingly increased from one third to one half of the urban

workforce. However, as the number receiving pensions has more than

trebled, the ratio of contributors to pensioners has fallen from around 5.4 to1 to 3.3 to 1. Revenues for retirement pensions have increased from 0.9 to2.4 percent of GDP, with the result that there have been small surpluses formost years. The average payment per person contributing to the pensionsystem has increased from around 20 percent of GDP per capita to nearly 32percent, with the increase as a percent of the average SOE wage being from15 to 24 percent.

Overall, these figures suggest a rapid increase in pension spending, albeit

from a low base. While the number of contributors has increasedsignificantly, the system dependency ratio (recipients per contributor) hasincreased. As pension benefits have also increased – in real terms, as apercentage of GDP per capita, and relative to average wages – the level of contributions per worker has also risen, both as a percentage of average

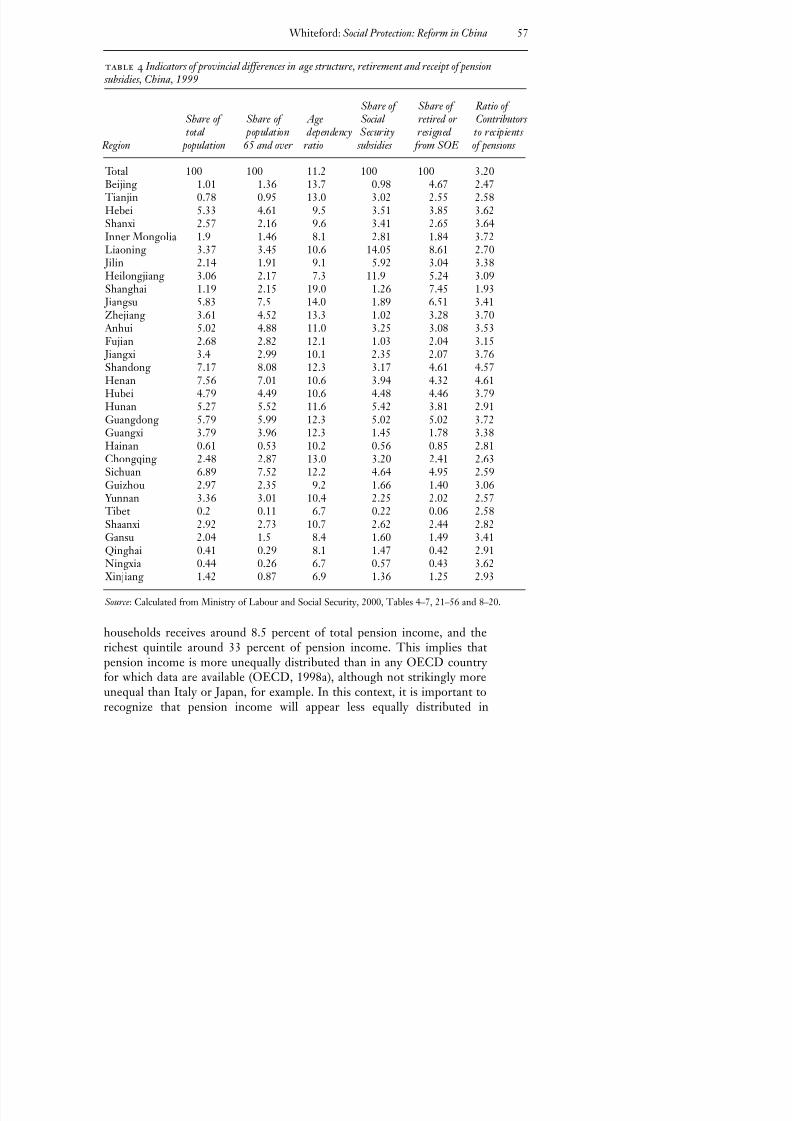

wages and relative to GDP per capita. There are important differences between regions, shown in Table 4. For

example, the age dependency ratio varies between 7.7 in Ningxia and Tibetto 19.0 in Shanghai. The ratio of contributors to pension recipients also

varies widely across provinces, from more than 4.5 to 1 in Henan andShandong to around 2.5 to 1 in Sichuan and less than 2 to 1 in Shanghai.

While Shanghai has only just over 1 percent of the national population, ithas more than 2 percent of the population aged over 65 years, and more than7 percent of the population of those retired or resigned from SOE. Thesituation in Beijing is similar, with it having an above average share of olderpeople and an even higher share of those retired from SOE. It is theprovinces of Liaoning and Heilongjian that show the most marked

discrepancies in relation to the costs of pensions. For example, Liaoning has just over 3 percent of the national population and a slightly higher share of the population over 65 years. However, the province has nearly 9 percent of those retired or resigned from SOE. It also receives 14 percent of the socialsecurity subsidies from central government, designed to make up shortfallsin the pooling funds.

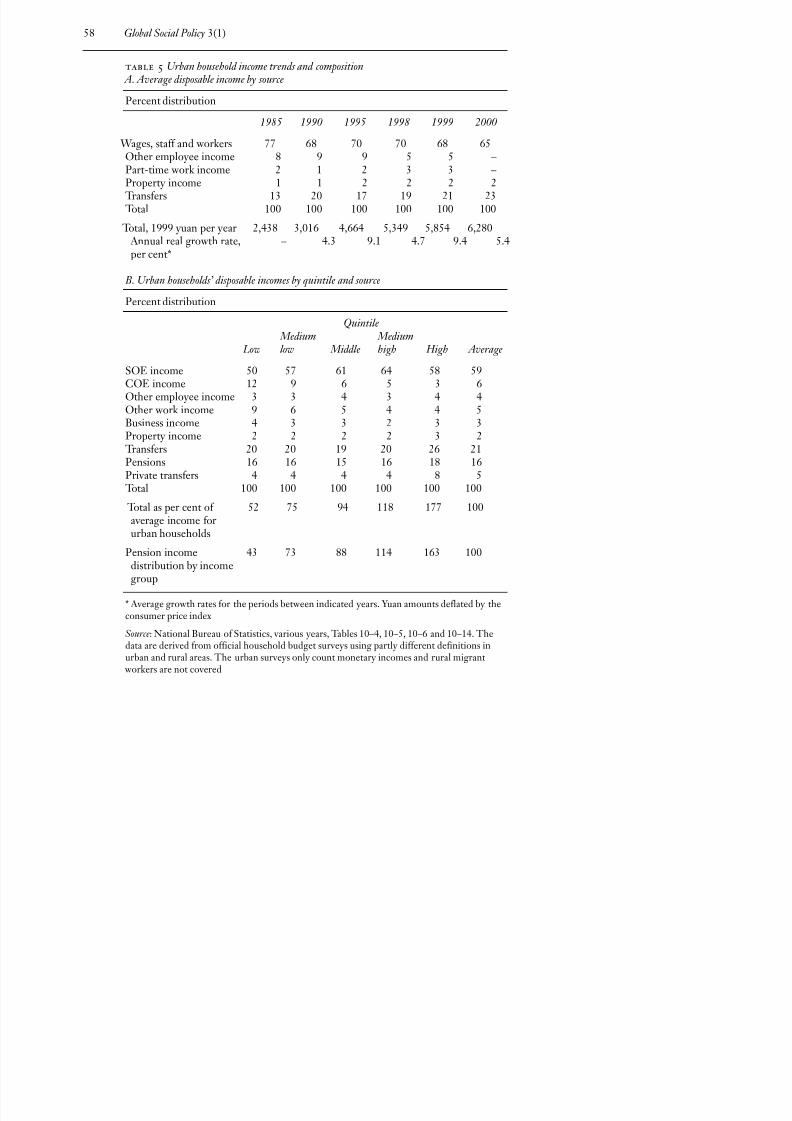

Table 5 shows trends in the role of transfer income, including pensions, inthe income distribution of urban households. Between 1985 and 2000

transfer income increased from 13 to 23 percent of average urban householddisposable income. Most of this increase occurred in the 1980s, with the roleof transfer income fluctuating around the 20 percent level over the 1990s.

The second part of the table shows the distribution of transfer income,separating out pensions from private transfers. Pension income is around 15to 18 percent of household income per capita for each income quintile,being slightly more for the richest quintile. The poorest quintile of urban

56 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 13/34

households receives around 8.5 percent of total pension income, and therichest quintile around 33 percent of pension income. This implies thatpension income is more unequally distributed than in any OECD country for which data are available (OECD, 1998a), although not strikingly moreunequal than Italy or Japan, for example. In this context, it is important torecognize that pension income will appear less equally distributed in

Whiteford: Social Protection: Reform in China 57

table 4 Indicators of provincial differences in age structure, retirement and receipt of pension subsidies, China, 1999

Share of Share of Ratio of Share of Share of Age Social retired or Contributors total population dependency Security resigned to recipients

Region population 65 and over ratio subsidies from SOE of pensions

Total 100 100 11.2 100 100 3.20Beijing 1.01 1.36 13.7 0.98 4.67 2.47

Tianjin 0.78 0.95 13.0 3.02 2.55 2.58Hebei 5.33 4.61 9.5 3.51 3.85 3.62Shanxi 2.57 2.16 9.6 3.41 2.65 3.64Inner Mongolia 1.9 1.46 8.1 2.81 1.84 3.72

Liaoning 3.37 3.45 10.6 14.05 8.61 2.70 Jilin 2.14 1.91 9.1 5.92 3.04 3.38Heilongjiang 3.06 2.17 7.3 11.9 5.24 3.09Shanghai 1.19 2.15 19.0 1.26 7.45 1.93

Jiangsu 5.83 7.5 14.0 1.89 6.51 3.41Zhejiang 3.61 4.52 13.3 1.02 3.28 3.70

Anhui 5.02 4.88 11.0 3.25 3.08 3.53Fujian 2.68 2.82 12.1 1.03 2.04 3.15

Jiangxi 3.4 2.99 10.1 2.35 2.07 3.76Shandong 7.17 8.08 12.3 3.17 4.61 4.57Henan 7.56 7.01 10.6 3.94 4.32 4.61Hubei 4.79 4.49 10.6 4.48 4.46 3.79Hunan 5.27 5.52 11.6 5.42 3.81 2.91Guangdong 5.79 5.99 12.3 5.02 5.02 3.72Guangxi 3.79 3.96 12.3 1.45 1.78 3.38Hainan 0.61 0.53 10.2 0.56 0.85 2.81Chongqing 2.48 2.87 13.0 3.20 2.41 2.63Sichuan 6.89 7.52 12.2 4.64 4.95 2.59Guizhou 2.97 2.35 9.2 1.66 1.40 3.06

Yunnan 3.36 3.01 10.4 2.25 2.02 2.57 Tibet 0.2 0.11 6.7 0.22 0.06 2.58Shaanxi 2.92 2.73 10.7 2.62 2.44 2.82Gansu 2.04 1.5 8.4 1.60 1.49 3.41Qinghai 0.41 0.29 8.1 1.47 0.42 2.91Ningxia 0.44 0.26 6.7 0.57 0.43 3.62

Xinjiang 1.42 0.87 6.9 1.36 1.25 2.93

Source: Calculated from Ministry of Labour and Social Security, 2000, Tables 4–7, 21–56 and 8–20.

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 14/34

58 Global Social Policy 3(1)

table 5 Urban household income trends and composition A. Average disposable income by source

Percent distribution

1985 1990 1995 1998 1999 2000 Wages, staff and workers 77 68 70 70 68 65Other employee income 8 9 9 5 5 –Part-time work income 2 1 2 3 3 –Property income 1 1 2 2 2 2

Transfers 13 20 17 19 21 23 Total 100 100 100 100 100 100

Total, 1999 yuan per year 2,438 3,016 4,664 5,349 5,854 6,280 Annual real growth rate, – 4.3 9.1 4.7 9.4 5.4

per cent*

B. Urban households’ disposable incomes by quintile and source

Percent distribution

Quintile Medium Medium

Low low Middle high High Average

SOE income 50 57 61 64 58 59COE income 12 9 6 5 3 6Other employee income 3 3 4 3 4 4Other work income 9 6 5 4 4 5Business income 4 3 3 2 3 3Property income 2 2 2 2 3 2

Transfers 20 20 19 20 26 21Pensions 16 16 15 16 18 16Private transfers 4 4 4 4 8 5

Total 100 100 100 100 100 100

Total as per cent of 52 75 94 118 177 100average income forurban households

Pension income 43 73 88 114 163 100distribution by incomegroup

* Average growth rates for the periods between indicated years. Yuan amounts deflated by theconsumer price index

Source: National Bureau of Statistics, various years, Tables 10–4, 10–5, 10–6 and 10–14. Thedata are derived from official household budget surveys using partly different definitions inurban and rural areas. The urban surveys only count monetary incomes and rural migrant

workers are not covered

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 15/34

countries where higher proportions of pensioners share households withadult children. This will be the case in China. Having said this, the moreimportant disparity is that this income source is not generally available tothe rural majority in China. For example, in 2000 average transfer income in

rural households was only 79 yuan per year, or 3.5 percent of average netrural household income, and only 5.4 percent of the average transfersreceived by urban households (National Bureau of Statistics [NBS], 2001).

The Chinese System in Comparative Perspective

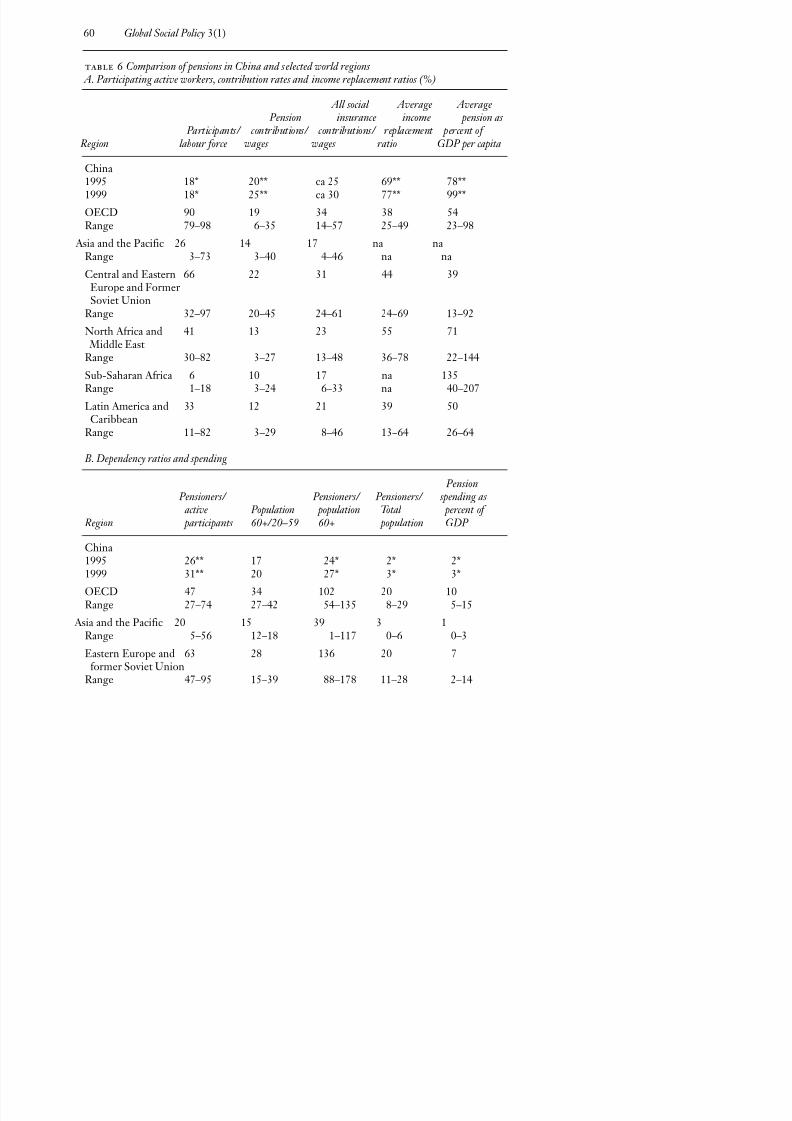

How does the Chinese system compare with other areas of the world and with other Asian economies? Table 6 provides a range of comparisons of the

Chinese pension system with those in other major regions of the world.1

Onthe basis of these comparisons, a number of conclusions can be reached. Inthe mid-1990s, China still had a relatively low ratio of pensioners to the totalpopulation, below the average for the Asia-Pacific region, and well below theaverage for other world regions apart from Sub-Saharan Africa. This wasdespite the fact that the older population share was above the average for itsown and a number of other regions. This is because pension receipt amongthe older population in China is relatively low, because coverage is limited tothe urban population.

Despite the fact that Chinese pensioners are a relatively low proportion of the total population, spending is nearly two to three times the average forthe Asia-Pacific region, and approaches the average level in North Africaand the Middle East and Latin America and the Caribbean. An index of standardized spending – the average pension as a percentage of GDP percapita – suggests that spending in China was nearly the highest of all worldregions, apart from Sub-Saharan Africa. However, many individual countries

will also be higher than their regional average, as is shown in subsequent

discussion of the Asian region. Pension replacement rates in China (averagemonthly benefits as a percent of average monthly wages) also appear to beamong the highest in the world, although some countries of North Africaand the Middle East are higher. Given the high level of replacement ratesand the fact that covered workers are among the higher income groups inChina, it is not surprising that average pensions are comparatively high.

Coverage of social security among the labour force and the working agepopulation is relatively low, however, although the difference between the

two measures of coverage is less than in many other regions. This impliesthat a relatively low percentage of the labour force is required to contributetowards the costs of relatively expensive pension benefits. As a consequence,it is not surprising that the level of employer pension taxes and of all socialinsurance taxes are high. The level of employer pension taxes, for example, isclose to the OECD average and to those of the countries of Eastern Europeand the Former Soviet Union (FSU). This is despite the fact that the share

Whiteford: Social Protection: Reform in China 59

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 16/34

60 Global Social Policy 3(1)

table 6 Comparison of pensions in China and selected world regions A. Participating active workers, contribution rates and income replacement ratios (%)

All social Average Average Pension insurance income pension as

Participants/ contributions/ contributions/ replacement percent of Region labour force wages wages ratio GDP per capita

China1995 18* 20** ca 25 69** 78**1999 18* 25** ca 30 77** 99**

OECD 90 19 34 38 54Range 79–98 6–35 14–57 25–49 23–98

Asia and the Pacific 26 14 17 na naRange 3–73 3–40 4–46 na na

Central and Eastern 66 22 31 44 39Europe and FormerSoviet Union

Range 32–97 20–45 24–61 24–69 13–92

North Africa and 41 13 23 55 71 Middle EastRange 30–82 3–27 13–48 36–78 22–144

Sub-Saharan Africa 6 10 17 na 135Range 1–18 3–24 6–33 na 40–207

Latin America and 33 12 21 39 50Caribbean

Range 11–82 3–29 8–46 13–64 26–64

B. Dependency ratios and spending

Pension

Pensioners/ Pensioners/ Pensioners/ spending as active Population population Total percent of Region participants 60+/20–59 60+ population GDP

China1995 26** 17 24* 2* 2*1999 31** 20 27* 3* 3*

OECD 47 34 102 20 10Range 27–74 27–42 54–135 8–29 5–15

Asia and the Pacific 20 15 39 3 1Range 5–56 12–18 1–117 0–6 0–3

Eastern Europe and 63 28 136 20 7former Soviet Union

Range 47–95 15–39 88–178 11–28 2–14

Whi f d S i l P i R f i Chi 61

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 17/34

of the population aged 60 and over is only around half the average forOECD countries.

In summary, the Chinese pension system is marked by relative generosity to a narrow share of older population and the total population. Therelatively low number of contributors as a percentage of the labour force hasmeant that the contributions required to finance these benefits are relatively high, compared to other world regions.

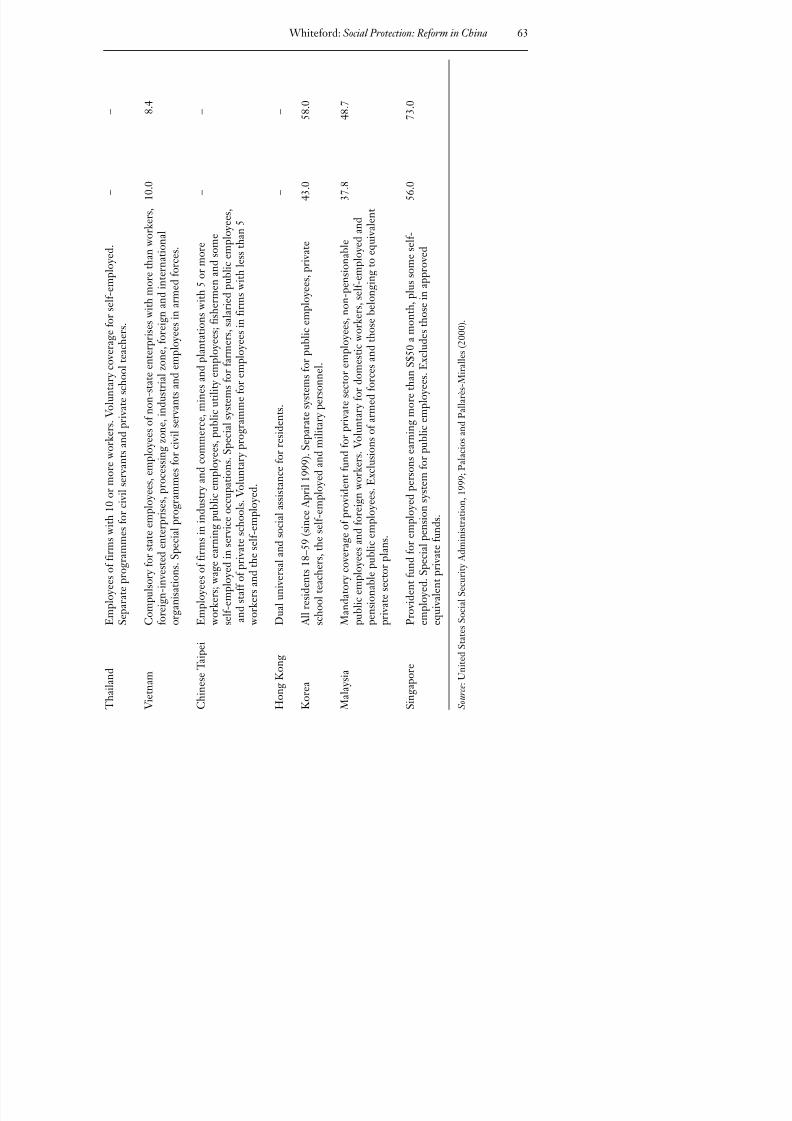

Table 7 sets out details of the coverage of retirement pensions in a range of

significant Asian economies, including some at much higher levels of national income. The higher income economies – Korea, Malaysia andSingapore – all have much higher levels of coverage among the labour forceand those of working age. The other lower income countries generally havepension systems restricted to those in firms or businesses with a minimumnumber of employees. Generally speaking, it is quite common to haveseparate schemes for those in the government sector, the military or those

working on railways, for example. It is also worth noting that China appears

to have higher levels of coverage of persons of working age than does India,Indonesia, Bangladesh, Pakistan or the Philippines.

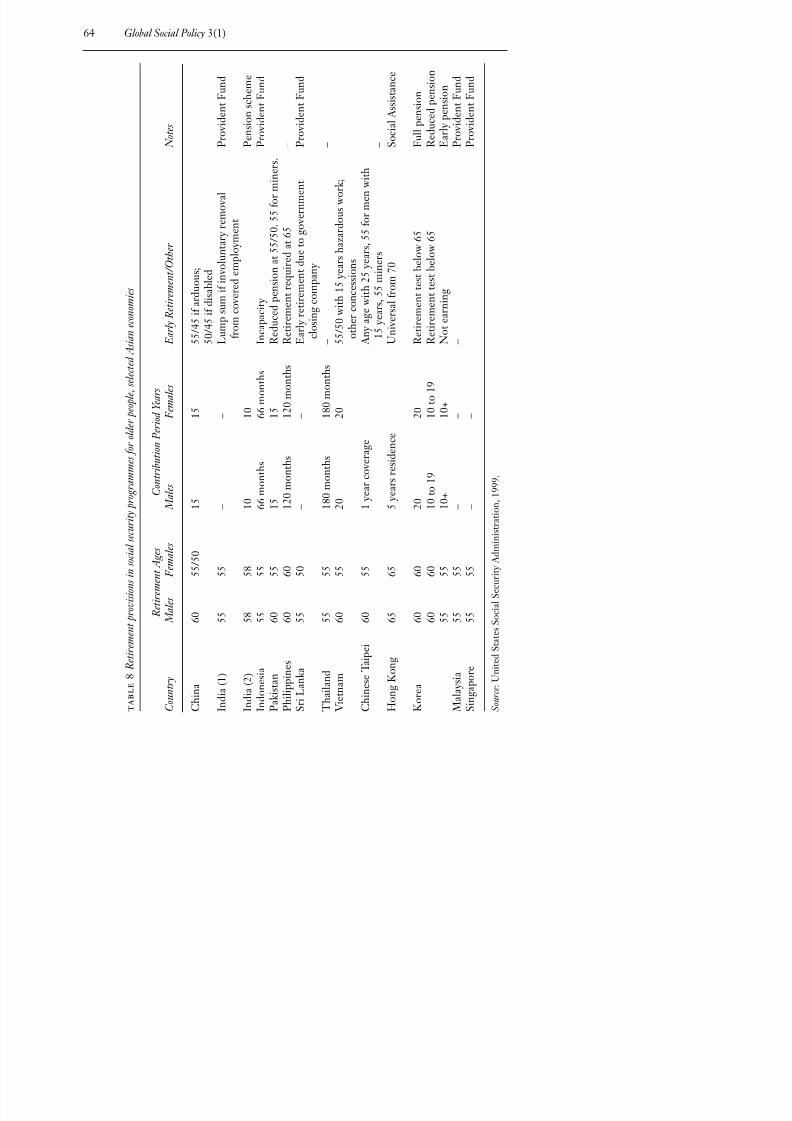

Table 8 shows retirement ages and contribution periods. Retirement agesfor men and women are not notably lower in China than in other significant

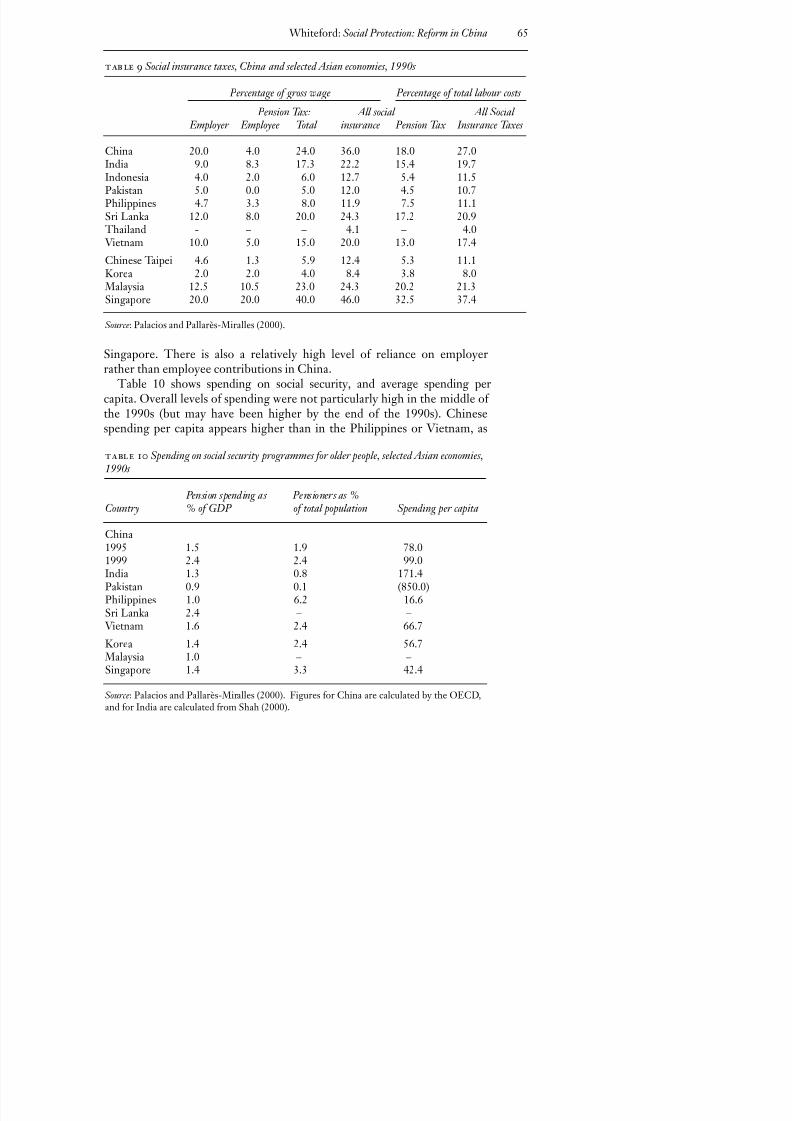

Asian economies. Hong Kong has the highest retirement age, but this is ageneral-revenue financed social assistance scheme. Similarly, thecontribution periods are broadly similar across countries, with theexceptions of the Republic of Korea and Vietnam. Table 9 compares thelevel of social insurance taxes across the region. China has the highest levelof social security contributions among the lower income Asian countries.Generally speaking, only Singapore among the high-income group has asubstantially higher level of social security contributions, although in thecase of Singapore this is to a provident fund, rather than to a PAYG socialinsurance system. As a result, social insurance taxes are a higher proportionof total labour costs in China than in any other economy, apart from

Whiteford: Social Protection: Reform in China 61

North Africa and 30 15 58 4 3 Middle EastRange 19–50 9–29 5–94 0–10 0–6

Sub-Saharan Africa 7 12 15 1 1

Range 0–37 10–16 0–121 0–10 0–3Latin America and 25 17 46 4 3Caribbean

Range 4–70 12–35 5–152 1–26 0–13

* The regular urban pension system and that for civil servants. ** The regular urban pension system.N.B. employee contribution rates increased every year 1997-2001.

Source: Figures for China are calculated by the OECD. Calculations for other regions based on WorldBank data in Palacios and Pallarès-Miralles (2000).

62 Global So ial Poli 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 18/34

62 Global Social Policy 3(1)

t a b l e

7

C o v e r a g e o f s o c i a l s e c u r i t y p r o g r a m m e s f o r o l d e r p e o p l e , s e l e c t e d A s i a n e c o n o m i e s

% o f p e r s o n s o f

% o f l a b o u r

C o u n t r y

P

e r s o n s C o v e r e d

w o r k i n g a g e

f o r c e

C h i n a

E m p l o y e e s i n s t a t e - r u n e n t e r p r i s e s . C o l l e c t i v e , p r i v a t e , a n d f o r e i g n - i n v e s t e d ( C h i n e s e

1 7 . 4 ( 1 9 9 4 )

1 7 . 6

n a t i o n a l s o n l y ) a n d t h e s e l f - e m p l o y e d m a y p r o v i d e s i m i l a r o r s e p a r a t e p r o g r a m m e s .

E m p l o y e e s o f g o v e r n m e n t a n d p a r t y o r g a n i s a t i o n s , a n d

c u l t u r a l , e d u c a t i o n a l a n d s c i e n t i f i c

i n s t i t u t i o n s a r e c o v e r e d u n d e r g o v e r n m e n t - f u n d e d , e m p

l o y e r - a d m i n i s t e r e d s y s t e m .

I n d i a

P r o v i d e n t f u n d , p e n s i o n a n d

d e p o s i t i n s u r a n c e s c h e m e s

f o r e m p l o y e e s o f e s t a b l i s h m

e n t s

7 . 9

1 0 . 6

w i t h 2 0 o r m o r e e m p l o y e e s i n 1 7 7 c a t e g o r i e s o f i n d u s t r y . E x c l u d e s t h o s e e a r n i n g m o r e t h a n

5 0 0 0 r u p e e s a m o n t h . C o n t r

a c t i n g o u t f o r t h o s e c o v e r e d b y e q u i v a l e n t p r i v a t e p l a n s . S p e c i a l

s y s t e m f o r m i n e r s , r a i l w a y a n d p u b l i c e m p l o y e e s . G r a t u i t y s c h e m e f o r e m p l o y e e s o f

f a c t o r i e s , m i n e s a n d f i r m s w i t h 1 0 o r m o r e e m p l o y e e s .

I n d o n e s i a

E s t a b l i s h m e n t s w i t h 1 0 o r m

o r e e m p l o y e e s o r p a y r o l l o f R p 1 m i l l i o n o r m o r e a m o

n t h .

7 . 0

8 . 0

C o v e r a g e b e i n g g r a d u a l l y e x

t e n d e d t o s m a l l e r e s t a b l i s h m

e n t s a n d c a s u a l a n d s e a s o n

a l

w o r k e r s . S p e c i a l s y s t e m s f o r

p u b l i c e m p l o y e e s a n d m i l i t a r y .

B a n g l a d e s h

P u b l i c e m p l o y e e s o n l y .

2 . 6

3 . 5

P a k i s t a n

E m p l o y e e s i n f i r m s w i t h 1 0 o r m o r e w o r k e r s . S p e c i a l s y

s t e m f o r p u b l i c e m p l o y e e s , a r m e d

2 . 1

3 . 5

f o r c e s , p o l i c e , s t a t u t o r y b o d i e s , l o c a l a u t h o r i t i e s , b a n k s a n d r a i l w a y e m p l o y e e s . E x c l u d e s

f a m i l y l a b o u r a n d t h e s e l f - e m

p l o y e d .

P h i l i p p i n e s

C o m p u l s o r y f o r a l l p r i v a t e e

m p l o y e e s u n d e r 6 0 , h o u s e h

e l p e r s e a r n i n g a t l e a s t 1 0 0 0

p e s o s

1 3 . 6

2 8 . 3

a m o n t h , a n d a l l s e l f - e m p l o y

e d w i t h 1 0 0 0 p e s o s o r m o r e m o n t h l y i n c o m e . S p e c i a l s y s t e m

f o r g o v e r n m e n t e m p l o y e e s a

n d m i l i t a r y .

S r i L a n k a

P r o v i d e n t f u n d f o r e m p l o y e d p e r s o n s , e x c l u d i n g f a m i l y l a b o u r a n d t h o s e i n a p p r o v e

d

2 0 . 8

2 8 . 8

p r i v a t e f u n d s . S p e c i a l p e n s i o

n f o r p u b l i c a n d l o c a l g o v e r

n m e n t e m p l o y e e s .

Whiteford: Social Protection: Reform in China 63

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 19/34

Whiteford: Social Protection: Reform in China 63

T h a i l a n d

E m p l o y e e s o f f i r m s w i t h 1 0

o r m o r e w o r k e r s . V o l u n t a r y

c o v e r a g e f o r s e l f - e m p l o y e d

.

–

–

S e p a r a t e p r o g r a m m e s f o r c i v i l s e r v a n t s a n d p r i v a t e s c h o

o l t e a c h e r s .

V i e t n a m

C o m p u l s o r y f o r s t a t e e m p l o y e e s , e m p l o y e e s o f n o n - s t a t e e n t e r p r i s e s w i t h m o r e t h a n

w o r k e r s , 1 0 . 0

8 . 4

f o r e i g n - i n v e s t e d e n t e r p r i s e s , p r o c e s s i n g z o n e , i n d u s t r i a l z o n e , f o r e i g n a n d i n t e r n a t i o n a l

o r g a n i s a t i o n s . S p e c i a l p r o g r a m m e s f o r c i v i l s e r v a n t s a n d

e m p l o y e e s i n a r m e d f o r c e s

.

C h i n e s e T a i p e i

E m p l o y e e s o f f i r m s i n i n d u s t r y a n d c o m m e r c e , m i n e s a n d p l a n t a t i o n s w i t h 5 o r m o r e

–

–

w o r k e r s ; w a g e e a r n i n g p u b l i c e m p l o y e e s , p u b l i c u t i l i t y e m p l o y e e s ; f i s h e r m e n a n d s o

m e

s e l f - e m p l o y e d i n s e r v i c e o c c u p a t i o n s . S p e c i a l s y s t e m s f o

r f a r m e r s , s a l a r i e d p u b l i c e m

p l o y e e s ,

a n d s t a f f o f p r i v a t e s c h o o l s .

V o l u n t a r y p r o g r a m m e f o r e

m p l o y e e s i n f i r m s w i t h l e s s

t h a n 5

w o r k e r s a n d t h e s e l f - e m p l o y

e d .

H o n g K o n g

D u a l u n i v e r s a l a n d s o c i a l a s s i s t a n c e f o r r e s i d e n t s .

–

–

K o r e a

A l l r e s i d e n t s 1 8 – 5 9 ( s i n c e A p r i l 1 9 9 9 ) . S e p a r a t e s y s t e m s

f o r p u b l i c e m p l o y e e s , p r i v a

t e

4 3 . 0

5 8 . 0

s c h o o l t e a c h e r s , t h e s e l f - e m p l o y e d a n d m i l i t a r y p e r s o n n

e l .

M a l a y s i a

M a n d a t o r y c o v e r a g e o f p r o v

i d e n t f u n d f o r p r i v a t e s e c t o r e m p l o y e e s , n o n - p e n s i o n a b

l e

3 7 . 8

4 8 . 7

p u b l i c e m p l o y e e s a n d f o r e i g n w o r k e r s . V o l u n t a r y f o r d o

m e s t i c w o r k e r s , s e l f - e m p l o y e d a n d

p e n s i o n a b l e p u b l i c e m p l o y e e s . E x c l u s i o n s o f a r m e d f o r c

e s a n d t h o s e b e l o n g i n g t o e q u i v a l e n t

p r i v a t e s e c t o r p l a n s .

S i n g a p o r e

P r o v i d e n t f u n d f o r e m p l o y e d p e r s o n s e a r n i n g m o r e t h a n S $ 5 0 a m o n t h , p l u s s o m e s e l f -

5 6 . 0

7 3 . 0

e m p l o y e d . S p e c i a l p e n s i o n s y s t e m f o r p u b l i c e m p l o y e e s . E x c l u d e s t h o s e i n a p p r o v e d

e q u i v a l e n t p r i v a t e f u n d s .

S o u r c e : U n i t e d S t a t e s S o c i a l S e c u r i t y A d m i n i s t r a t i o n , 1 9 9 9 ; P a l a c i o s a n d P a l l a r è s - M

i r a l l e s ( 2 0 0 0 ) .

64 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 20/34

64 Global Social Policy 3(1)

t a b l e

8

R e t i r e m e n t

p r o v i s i o n s i n s o c i a l s e c u r i t y p r o g r a m m e s f o r o l d e r p e o p l e , s e l e c t e d A s i a n e c o n o m i e s

R e t i r e m e n t A g e s

C o n t r i b u t i o n P e r i o d Y e a r s

C o u n t r y

M a l e s

F e m a l e s

M a l e s

F e m a l e s

E a r l y R e t i r e m e n t / O t h e r

N o t e s

C h i n a

6 0

5 5 / 5 0

1 5

1 5

5 5 / 4 5 i f a r d u o u s ;

5 0 / 4 5 i f d i s a b l e d

I n d i a ( 1 )

5 5

5 5

–

–

L u m p s u m i f i n v o l u n

t a r y r e m o v a l

P r o v

i d e n t F u n d

f r o m c o v e r e d e m p l o y m e n t

I n d i a ( 2 )

5 8

5 8

1 0

1 0

P e n s

i o n s c h e m e

I n d o n e s i a

5 5

5 5

6 6

m o n t h s

6 6 m o n t h

s

I n c a p a c i t y

P r o v

i d e n t F u n d

P a k i s t a n

6 0

5 5

1 5

1 5

R e d u c e d p e n s i o n a t 5 5 / 5 0 . 5 5 f o r m i n e r s .

P h i l i p p i n e s

6 0

6 0

1 2

0 m o n t h s

1 2 0 m o n t h s

R e t i r e m e n t r e q u i r e d

a t 6 5

–

S r i L a n k a

5 5

5 0

–

–

E a r l y r e t i r e m e n t d u e

t o g o v e r n m e n t

P r o v

i d e n t F u n d

c l o s i n g c o m p a n y

T h a i l a n d

5 5

5 5

1 8

0 m o n t h s

1 8 0 m o n t h s

–

–

V i e t n a m

6 0

5 5

2 0

2 0

5 5 / 5 0 w i t h 1 5 y e a r s h a z a r d o u s w o r k ;

o t h e r c o n c e s s i o n s

C h i n e s e T a i p e i

6 0

5 5

1 y e a r c o v e r a g e

A n y a g e w i t h 2 5 y e a r

s , 5 5 f o r m e n w i t h

1 5 y e a r s , 5 5 m i n e r s

–

H o n g K o n g

6 5

6 5

5 y e a r s r e s i d e n c e

U n i v e r s a l f r o m 7 0

S o c i a l A s s i s t a n c e

K o r e a

6 0

6 0

2 0

2 0

R e t i r e m e n t t e s t b e l o w 6 5

F u l l p e n s i o n

6 0

6 0

1 0

t o 1 9

1 0 t o 1 9

R e t i r e m e n t t e s t b e l o w 6 5

R e d u c e d p e n s i o n

5 5

5 5

1 0

+

1 0 +

N o t e a r n i n g

E a r l y p e n s i o n

M a l a y s i a

5 5

5 5

–

–

–

P r o v

i d e n t F u n d

S i n g a p o r e

5 5

5 5

–

–

P r o v

i d e n t F u n d

S o u r c e : U n i t e d S t a t e s S o c i a l S e c u r i t y A d m i n i s t r a t i o n ,

1 9 9 9 .

Whiteford: Social Protection: Reform in China 65

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 21/34

Singapore. There is also a relatively high level of reliance on employerrather than employee contributions in China.

Table 10 shows spending on social security, and average spending percapita. Overall levels of spending were not particularly high in the middle of the 1990s (but may have been higher by the end of the 1990s). Chinesespending per capita appears higher than in the Philippines or Vietnam, as

f

table 9 Social insurance taxes, China and selected Asian economies, 1990s

Percentage of gross wage Percentage of total labour costs

Pension Tax: All social All Social

Employer Employee Total insurance Pension Tax Insurance Taxes

China 20.0 4.0 24.0 36.0 18.0 27.0India 9.0 8.3 17.3 22.2 15.4 19.7Indonesia 4.0 2.0 6.0 12.7 5.4 11.5Pakistan 5.0 0.0 5.0 12.0 4.5 10.7Philippines 4.7 3.3 8.0 11.9 7.5 11.1Sri Lanka 12.0 8.0 20.0 24.3 17.2 20.9

Thailand - – – 4.1 – 4.0 Vietnam 10.0 5.0 15.0 20.0 13.0 17.4

Chinese Taipei 4.6 1.3 5.9 12.4 5.3 11.1Korea 2.0 2.0 4.0 8.4 3.8 8.0

Malaysia 12.5 10.5 23.0 24.3 20.2 21.3Singapore 20.0 20.0 40.0 46.0 32.5 37.4

Source: Palacios and Pallarès-Miralles (2000).

table 10 Spending on social security programmes for older people, selected Asian economies,1990s

Pension spending as Pensioners as %Country % of GDP of total population Spending per capita

China1995 1.5 1.9 78.01999 2.4 2.4 99.0India 1.3 0.8 171.4Pakistan 0.9 0.1 (850.0)Philippines 1.0 6.2 16.6Sri Lanka 2.4 – –

Vietnam 1.6 2.4 66.7Korea 1.4 2.4 56.7

Malaysia 1.0 – –Singapore 1.4 3.3 42.4

Source: Palacios and Pallarès-Miralles (2000). Figures for China are calculated by the OECD,and for India are calculated from Shah (2000).

66 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 22/34

well as in Korea and Singapore. In contrast, spending per capita appears tohave been significantly greater in India and Pakistan (although the figures forPakistan are calculated from numbers that have been rounded in the source).

To sum up these comparisons with other Asian economies, it can be noted

that China is less unusual compared to other parts of Asia than compared toother large regions of the world. China has comparatively high levels of coverage among the workforce, but its contribution rates are higher than inmost other Asian economies. This appears to be because it is significantly more generous in relative terms than are the high-income Asian economies,but it covers a significantly higher proportion of the aged than do India orPakistan, for example.

The Chinese System in the Global Policy Context The reform of the Chinese pension system is of considerable significance tofuture global social policy developments. At one level, this simply reflectsthe sheer size of China. China is already the seventh-largest economy in the

world (OECD, 2002), and its relative growth rate suggests that it willincrease this ranking over the next 20 to 30 years. It is also forecast that by 2030 more than a quarter of the world’s older people will live in China(James, 2001). Thus, how China adapts its pension system to make it

sustainable and equitable will potentially be directly relevant to more peoplethan any other national social protection system in the world.

The indirect effects of the reforms could also be significant. Depending onthe extent to which they are successful in managing the transition from asystem protecting a minority of the Chinese population to one providingsustainable coverage for the majority of the population, Chinese reformscould become a model for other developing countries – either positive ornegative. In addition, if there is a successful transition to an advance-funded,

multi-pillar pension system with a broader coverage of the population thenit is possible that China would also have one of the largest accumulatedpension funds in the world by the middle of the 21st century.

It is not straightforward to identify the role of international organizationsin influencing the reforms chosen by China. As is well known, the WorldBank (1994) proposed a ‘three pillar’ model as a basis for pension reform.

This approach has been most influential in Latin America, and in some of the transition countries of Central and Eastern Europe. This ‘new pensionorthodoxy’ is commonly regarded as involving the downsizing of the publicpension tier and the introduction of mandatory individual accounts – inshort, the privatization or partial privatization of pensions (Müller, 2003).

The main arguments put by the World Bank for reforms of this type are thatchanges are needed to make social security systems more fiscally sustainable,and to avoid increasing social security contribution rates as populations age.It is also argued that pre-funding can be used to increase saving that is

Whiteford: Social Protection: Reform in China 67

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 23/34

committed for long-term investments, and pension funds can be used asengines of financial market development and to improve corporategovernance (James, 2001).

The World Bank supports a range of projects on pension reform in China.

In the social protection area, there are currently three ongoing World Bank projects: a pension reform project (cost US$5m), an enterprise housing andsocial security project (a commitment of US$350m), and a labour marketdevelopment project (a commitment of US$30m), plus direct technicalassistance and training on pension reform issues. However, these are only a

very small component of the Bank’s overall activities in China. At 30 June2001, World Bank commitments in China approached US$35bn for 234projects.2

The Asian Development Bank has also funded a range of activities onpension reform in China. In 1999 the ADB approved a US$2.4m technicalassistance grant to China to support the formulation and implementation of the various administrative frameworks for the new pension system. In 2001,the ADB agreed to provide technical assistance of around US$1m to supportthe social security pilot reform programme in Liaoning, and to strengthenthe institutional capacity of the National Council for the Social Security Fund.3 While the ADB has been promoting pension reform in Asia for some

years, it has recently developed a wider social protection policy (Ortiz,

2001), which emphasizes the positive role of effective social protection inachieving sustained poverty reduction, now one of the main focuses of the

work of the ADB. The strategy also includes a chapter on the operation of pension systems written by Lawrence Thompson, critical of many of thearguments put by some proponents of privatization and advance funding.

The position adopted by the OECD differs again. The OECD report on Reforming China’s Enterprises (2000) identified pension reform as an essentialpart of the process of reducing financial burdens on enterprises. For

example, in its opening paragraphs, the report noted that ‘. . . a thirdcomponent [of enterprise reforms] is provision of supporting institutionsand infrastructure needed for a market based enterprise economy. Key inthis regard is the development of social benefit programmes to deal with theeconomy adjustments entailed by reforms, allow enterprises to focus on theircommercial objectives, and provide for the longer-term needs of thepopulation.’ (OECD, 2000: 7) This emphasis has been continued in morerecent studies (OECD, 2002). Thus, pension reform has been placed in thecontext of the need for broader industrial changes and associated labourmarket reforms.

It should also be noted that in making recommendations on pension issuesto member countries the OECD does not necessarily endorse ‘privatization’of social security. For example, the OECD (1998b) sets out a range of principles for pension reform, including that ‘retirement income should beprovided by a mix of tax and transfer systems, advance-funded systems,

68 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 24/34

private savings and earnings. The objective is risk-diversification, a betterbalance of burden-sharing between generations, and to give individualsmore flexibility over retirement decisions.’

The approach adopted by China appears to have been influenced by

aspects of all these analyses, but it seems fair to say that China has not simply adopted the multi-pillar pension model in an uncritical fashion. While thenew system has adopted features that make it appear to be a three-pillarmodel, the fact is that the pension system basically remains a PAYG scheme,

where current contributions are used to pay for current benefits. Wherefunding is in operation, revenues are mainly invested in government bonds.

Moreover, even if the individual contributions were actually being paid intoindividual accounts, they would still amount to less than a third of the totallevel of contributions. That is, the contributory, social insurance approachremains predominant. Indeed, the basic pension remains highly redistributive, and the design of the second pillar also contains many redistributive features, with the proviso that this is redistribution within arelatively small and privileged group. In fact, the system is subject tocontinuing criticisms by the World Bank, on the basis that the system may be creating unrealistic expectations by pretending to have funded elements(James, 2001).

Overall, the Chinese government has consistently adopted a cautious

approach to pension reform. The evidence for this is provided by thegradual reforms introduced, and the use of provincial experiments to testreform proposals before their wider implementation. As noted by Tang andNgan (2001), ‘the model that has emerged is not a market-based retirementsystem. It is not an endorsement for the privatisation of social security.Rather, the continued involvement of government in the system represents apragmatic approach to deal with the social security issue’ (pp. 256–7).

Issues and Questions IS THE SYSTEM APPROPRIATE FOR CHINA’S CIRCUMSTANCES?

China’s social security system dates back to the 1950s and in part reflects thedifferent economic reality of state ownership of virtually all enterprises,

where the State was practically the only employer. In a sense, the institutionsof society were mutually supportive, but with the consequence that thesolutions to some problems themselves become problems when otherinstitutions changed. For example, the traditional social welfare system inChina guaranteed urban SOE workers a wide range of social benefits,including pensions, health care and housing. During the pre-reform period,these benefits were partly borne by employees in the form of low nominal

wages (OECD, 2000), but there was no unemployment, and there was theguarantee of state employment for one child of a retiree. These and otherfeatures embodied the principle of the ‘iron rice bowl’ (tiefanwan), the

Whiteford: Social Protection: Reform in China 69

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 25/34

government’s commitment to ensure employment and incomes for urban workers. The system was marked by security for workers, but lowproductivity.

Even so, rural residents did not enjoy the same privileges. Under the

household registration system (hukou) they were specifically excluded fromthe urban workforce and its privileges, originally as a response to the need toration scarce resources. However, under the rural Household ProductionResponsibility system, which replaced collective farms in 1984, every agricultural household had a right to cultivate a small plot of land, currently averaging around one-half a hectare. The land entitlement constitutes theprincipal element of social security in rural areas. However, oneconsequence of the replacement of collective farms with the HouseholdProduction Responsibility system was the effective phasing-out of the ruralco-operative medical system (including so-called barefoot doctors).

According to the World Bank (1997b), only 10 percent of the ruralpopulation had access to subsidised health care by the mid-1990s comparedto 90 percent in 1978.

While replacement of collective farms substantially increased agriculturalproductivity for an extended period, it appears to have subsequently reachedits limits. The average household farm of about 0.5 ha is too small to giveproductive full-time employment to all individuals reported to work there.

Many must be underemployed unless they have off-farm jobs in addition.Depending on the assumption of what level of productivity is regarded asacceptable, rural hidden unemployment can be estimated to be between170m and 250m (OECD, 2002). Thus, the principal form of social security for the rural majority of the Chinese population can be regarded as thesource of one of the country’s major economic problems.

Economic reforms from the late 1970s created a new private sector withalternative job opportunities, as well as new forms of employment in SOE

based on contracts. Nevertheless, in the 1980s and most of the 1990s, the‘work unit’ was the chief vehicle for delivering social benefits. This systemhas become an increasing impediment to modernization of China’senterprise sectors in several ways. The system imposes benefit expenses onSOE that are relatively high on average and unevenly distributed. Totaloutlays by SOE for social benefits have averaged around 30 percent of theirpayrolls, but are 50 percent or higher in the most heavily burdened cases.4

These burdens have increased over time as the ratio of retired to activeemployees has risen with the ageing of the population.

Despite major reforms to the pension system for enterprise workers, anumber of key problems remain. Financial burdens on SOE remain high,partly because the new arrangements with reduced replacement rates apply to new workers while current retirees continue to receive higher pensions.Burdens have been shifted, but mainly from loss-making and low profit SOEthat are unable to meet their obligations to more profitable SOE, which in

70 Global Social Policy 3(1)

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 26/34

some cases are required to pay more than the theoretical maximum of 20percent of salaries. Moreover, because the pooling of contributions occursonly within municipalities or provinces there are disincentives for newbusinesses to establish themselves in the regions most affected by SOE

restructuring, precisely where new job opportunities are most needed. Thus,the pension system in its current form continues to provide impediments to wider economic reform.

IS THE SYSTEM SUSTAINABLE?

The World Bank (World Bank, 1997a) identifies the longer-termpredicament arising from a rapidly ageing population and the urgent andimmediate problem of the pension burden placed on SOE as the two mostsevere difficulties facing China’s pension system. Although China has arelatively young population, this will change over the next 20 years andbeyond, as a result of increasing life expectancy and the impact of the ‘onechild policy’. It is projected that the proportion of the older population inChina will rise from around 10 percent in 2000 to 15.8 percent in 2020 and

just under 25 percent by 2040. The proportion of the urban population aged60 and over to the population aged 20–59 will increase to 34 percent by 2040. While a much smaller group, the ‘old old’ (over 75) will increase at amuch faster rate, increasing the share of the most vulnerable, particularly

older women. The share of the population over 60 in China is projected toincrease from around half the OECD average to nearly three-quarters the(higher) OECD average in 2040. China will have one of the highest sharesof older people of any Asian economy, apart from much higher incomeeconomies, such as Korea, Hong Kong, Singapore and Japan.

In considering these future pressures it is important to bear in mind thatpension spending trebled over the past 10 years, from 0.8 to 2.4 percent of GDP. It can be calculated that if everything else had remained equal, the

increase in the value of pensions relative to GDP per capita would haveincreased spending by around 11 percent, and population ageing would haveincreased spending by around 15 percent. This means that the main factorcontributing to increased spending has been the increase in coverage of theolder population, which has more than doubled. The factors impacting onspending are multiplicative. Thus, the more significant increase in the futureshare of the older population due to demographic ageing might be expectedto increase spending at an even faster rate. In a ‘worst case’ scenario, pensionspending in 2040 could exceed 12 percent of GDP. However, for this to

happen the average benefit level would have to stay at its current high level,and coverage rates would have to double from their current level.

While it is true that spending has been increasing at a very rapid rate, thisseems unlikely to continue over the next decade. Recent reforms can beexpected to reduce replacement rates over time. It also seems unlikely thatcoverage will increase as rapidly as in the past decade. A more conservative

Whiteford: Social Protection: Reform in China 71

8/9/2019 China_from Enterprise Protection to Social Protection

http://slidepdf.com/reader/full/chinafrom-enterprise-protection-to-social-protection 27/34

estimate is that pension spending could reach around 3 percent of GDP by 2010. While this overall level is modest by the standards of OECDcountries, most OECD countries provide retirement income support to themajority of their aged population in a way that substantially alleviates

poverty. Moreover, this represents a large share of overall governmentresources in China, and it is important to ensure that the need to financepensions does not ‘crowd-out’ other important social priorities.

The social pooling component of the pension is now indexed tocontemporary wages. While this may not have had a significant impact todate, it is likely in the future to exercise upward pressure on spending.

Having said this, expansions in coverage are likely to reduce the averagelevel of benefits simply as a result of the fact that new contributors will belower in the wage distribution than current contributors. As a result, thesame target replacement rate would produce lower pensions relative to GDPper capita, and moderate the average cost of the scheme. At the same time,the fact that China has experienced rapid economic growth and growth inreal wages means that pensions should be more adequate in real terms.

Nevertheless, expanded coverage, while it has alleviated the near-termsqueeze on funds, increases pension obligations over the longer term. Thesystem dependency ratio has actually become less favourable over the pastdecade. This is a serious problem, as the average contribution has risen