Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

28 July 2015

Asia Pacific/China

Equity Research

Automobile Distributors

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK)

INITIATION

From luxury dealer to high-end EV maker

■ Initiating with OUTPERFORM and a TP of HK$8.80 implying a 42% potential upside. Harmony Auto, a leading luxury dealer group in China, is transforming into a new energy vehicle (NEV) maker. It has tied up with Foxconn and Tencent and has acquired an 88% stake in Greenfield Motor (a NEV maker). Although the traditional car dealership operation remains the major near-term earnings contributor (97-99% in 2016-17) for Harmony, we think its new NEV operation is likely to provide it a decent long-term growth potential. After the 47% correction from its last peak, the stock is trading at 12.6/9x 2015/16E P/E and its risk-reward potential looks attractive.

■ Aftersales income to jump on expanding independent service network. By doubling its independent luxury car service centers from 43 in 2014 to 80 in 2015, Harmony auto has been able to capture the fast-growing luxury vehicles service and emerging electric vehicles after-sales market growth, resulting in a 40% earnings CAGR from independent service centers. The company thinks it

can offer outstanding balance between aftersales service quality and price.

■ The ambitious alliance is aiming to break into high-end EV market. We understand there are quite a few EV new entrants, but Foxconn-Tencent-Harmony alliance is most likely to work out, in our view. Our confidence stems from Foxconn's well-developed EV component supply chain, Tencent's internet expertise, and Harmony's dealership network. High-end EV operation is estimated to book Rmb408/974 mn in profit in 2019/20E after Rmb288 mn in

loss in 2018.

■ Valuation. Our HK$8.80 target price is DCF-based, as simple multiples cannot fully exhibit dealer business' long-term earnings power and Harmony's new endeavour in the electric vehicle market. Key risk: Weaker-than-expected

luxury car demand may ignite a price war, hurting dealers' margins.

Share price performance

60

80

100

120

140

4

6

8

10

12

Aug-13 Dec-13 Apr-14 Aug-14 Dec-14 Apr-15

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

MSCI CHINA F IDX which closed at 6741.44 on 27/07/15

On 27/07/15 the spot exchange rate was HK$7.75/US$1

Performance over 1M 3M 12M Absolute (%) -31.1 -37.9 40.5 — Relative (%) -18.6 -15.8 39.2 —

Financial and valuation metrics

Year 12/14A 12/15E 12/16E 12/17E Revenue (Rmb mn) 10,195.9 10,857.4 12,093.6 12,277.2 EBITDA (Rmb mn) 901.4 1,167.1 1,447.7 1,655.5 EBIT (Rmb mn) 790.8 1,007.5 1,236.0 1,391.6 Net profit (Rmb mn) 547.0 623.9 861.6 947.3 EPS (CS adj.) (Rmb) 0.50 0.40 0.55 0.60 Change from previous EPS (%) n.a. Consensus EPS (Rmb) n.a. 0.45 0.62 0.81 EPS growth (%) 33.4 -20.8 38.1 9.9 P/E (x) 10.0 12.6 9.1 8.3 Dividend yield (%) 1.9 1.5 2.1 2.3 EV/EBITDA (x) 10.4 6.2 5.2 4.6 P/B (x) 2.0 1.3 1.2 1.1 ROE (%) 22.1 14.6 13.9 13.6 Net debt/equity (%) 56.1 Net cash Net cash Net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* [V] Price (27 Jul 15, HK$) 6.21 Target price (HK$) 8.80¹ Upside/downside (%) 41.7 Mkt cap (HK$ mn) 9,785 (US$ 1,262) Enterprise value (Rmb mn) 7,225 Number of shares (mn) 1,575.70 Free float (%) 46.6 52-week price range 11.00 - 4.09 ADTO - 6M (US$ mn) 9.5

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

[V] = Stock considered volatile (see Disclosure Appendix).

Research Analysts

Bin Wang

852 2101 6702

Mark Mao

852 2101 6710

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 2

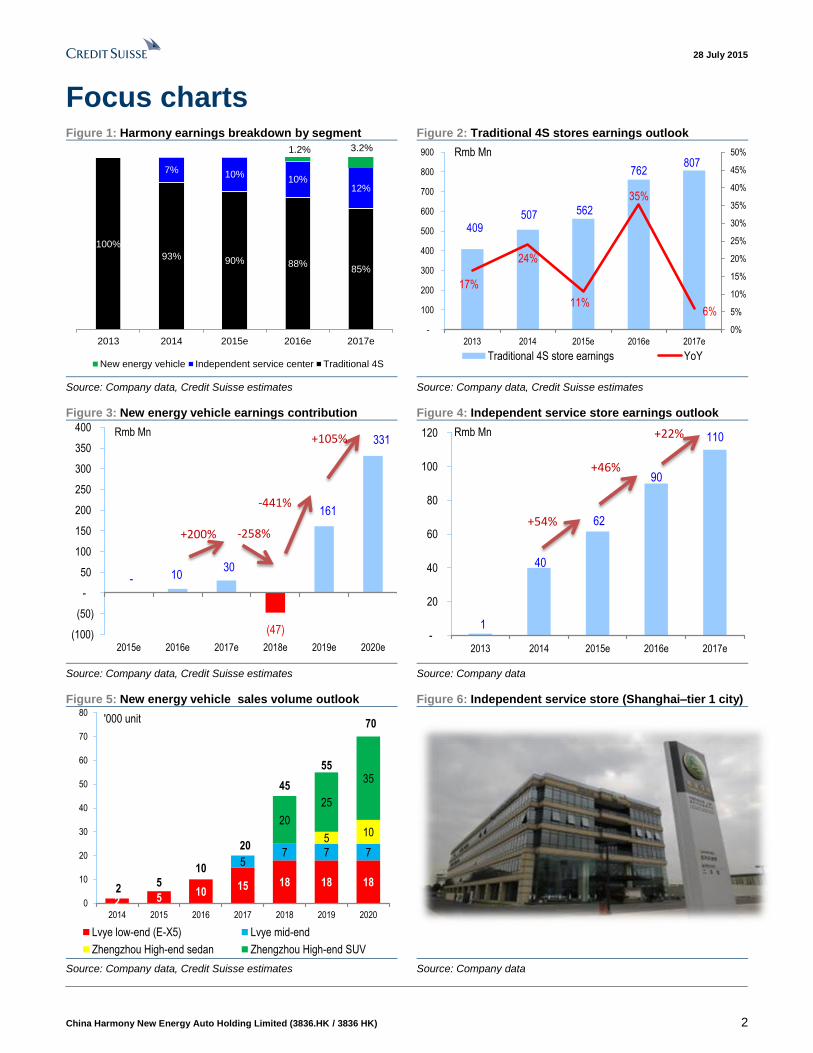

Focus charts Figure 1: Harmony earnings breakdown by segment Figure 2: Traditional 4S stores earnings outlook

100%

93% 90% 88%85%

7% 10%10%

12%

1.2% 3.2%

2013 2014 2015e 2016e 2017e

New energy vehicle Independent service center Traditional 4S

409 507 562

762 807

17%

24%

11%

35%

6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

-

100

200

300

400

500

600

700

800

900

2013 2014 2015e 2016e 2017e

Rmb Mn

Traditional 4S store earnings YoY

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 3: New energy vehicle earnings contribution Figure 4: Independent service store earnings outlook

- 10 30

(47)

161

331

(100)

(50)

-

50

100

150

200

250

300

350

400

2015e 2016e 2017e 2018e 2019e 2020e

Rmb Mn

+200% -258%

-441%

+105%

1

40

62

90

110

-

20

40

60

80

100

120

2013 2014 2015e 2016e 2017e

Rmb Mn

+54%

+46%

+22%

Source: Company data, Credit Suisse estimates Source: Company data

Figure 5: New energy vehicle sales volume outlook Figure 6: Independent service store (Shanghai–tier 1 city)

2 510

15 18 18 18

57 7 7

510

20

25

35

25

10

20

45

55

70

0

10

20

30

40

50

60

70

80

2014 2015 2016 2017 2018 2019 2020

'000 unit

Lvye low-end (E-X5) Lvye mid-end

Zhengzhou High-end sedan Zhengzhou High-end SUV

Source: Company data, Credit Suisse estimates Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 3

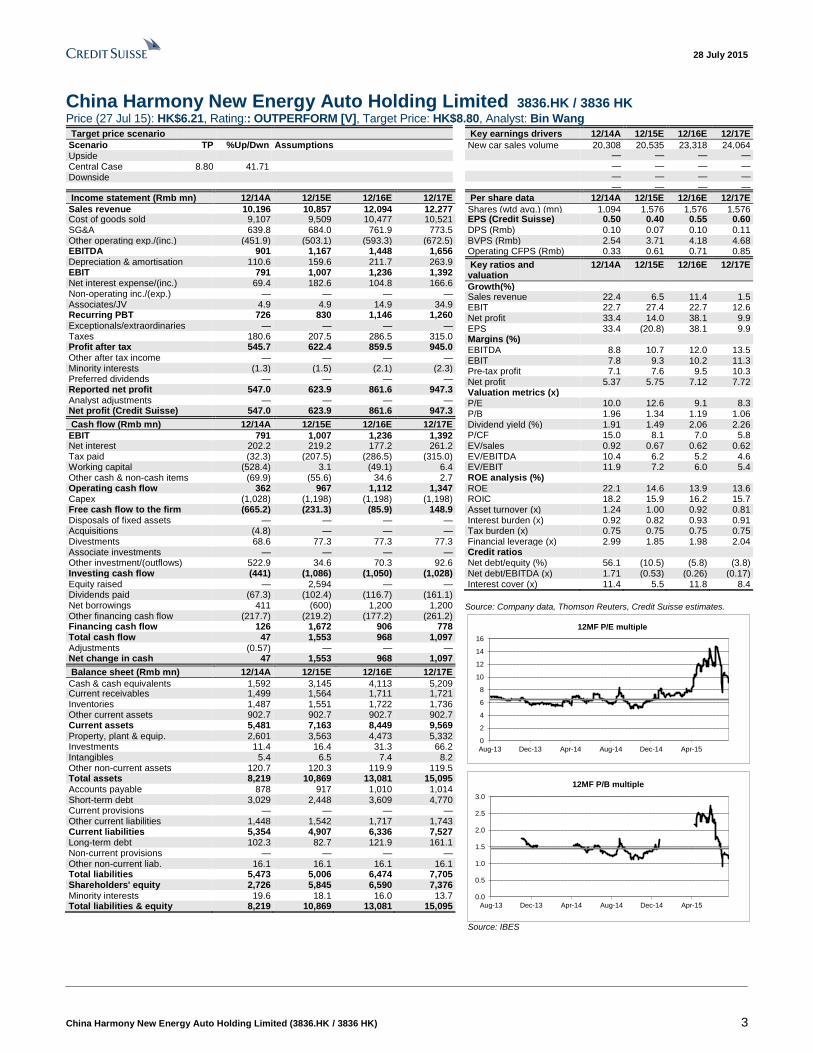

China Harmony New Energy Auto Holding Limited 3836.HK / 3836 HK Price (27 Jul 15): HK$6.21, Rating:: OUTPERFORM [V], Target Price: HK$8.80, Analyst: Bin Wang

Target price scenario

Scenario TP %Up/Dwn Assumptions Upside Central Case 8.80 41.71 Downside

Key earnings drivers 12/14A 12/15E 12/16E 12/17E

New car sales volume 20,308 20,535 23,318 24,064 — — — — — — — — — — — — — — — —

Income statement (Rmb mn) 12/14A 12/15E 12/16E 12/17E

Sales revenue 10,196 10,857 12,094 12,277 Cost of goods sold 9,107 9,509 10,477 10,521 SG&A 639.8 684.0 761.9 773.5 Other operating exp./(inc.) (451.9) (503.1) (593.3) (672.5) EBITDA 901 1,167 1,448 1,656 Depreciation & amortisation 110.6 159.6 211.7 263.9 EBIT 791 1,007 1,236 1,392 Net interest expense/(inc.) 69.4 182.6 104.8 166.6 Non-operating inc./(exp.) — — — — Associates/JV 4.9 4.9 14.9 34.9 Recurring PBT 726 830 1,146 1,260 Exceptionals/extraordinaries — — — — Taxes 180.6 207.5 286.5 315.0 Profit after tax 545.7 622.4 859.5 945.0 Other after tax income — — — — Minority interests (1.3) (1.5) (2.1) (2.3) Preferred dividends — — — — Reported net profit 547.0 623.9 861.6 947.3 Analyst adjustments — — — — Net profit (Credit Suisse) 547.0 623.9 861.6 947.3

Cash flow (Rmb mn) 12/14A 12/15E 12/16E 12/17E

EBIT 791 1,007 1,236 1,392 Net interest 202.2 219.2 177.2 261.2 Tax paid (32.3) (207.5) (286.5) (315.0) Working capital (528.4) 3.1 (49.1) 6.4 Other cash & non-cash items (69.9) (55.6) 34.6 2.7 Operating cash flow 362 967 1,112 1,347 Capex (1,028) (1,198) (1,198) (1,198) Free cash flow to the firm (665.2) (231.3) (85.9) 148.9 Disposals of fixed assets — — — — Acquisitions (4.8) — — — Divestments 68.6 77.3 77.3 77.3 Associate investments — — — — Other investment/(outflows) 522.9 34.6 70.3 92.6 Investing cash flow (441) (1,086) (1,050) (1,028) Equity raised — 2,594 — — Dividends paid (67.3) (102.4) (116.7) (161.1) Net borrowings 411 (600) 1,200 1,200 Other financing cash flow (217.7) (219.2) (177.2) (261.2) Financing cash flow 126 1,672 906 778 Total cash flow 47 1,553 968 1,097 Adjustments (0.57) — — — Net change in cash 47 1,553 968 1,097

Balance sheet (Rmb mn) 12/14A 12/15E 12/16E 12/17E

Cash & cash equivalents 1,592 3,145 4,113 5,209 Current receivables 1,499 1,564 1,711 1,721 Inventories 1,487 1,551 1,722 1,736 Other current assets 902.7 902.7 902.7 902.7 Current assets 5,481 7,163 8,449 9,569 Property, plant & equip. 2,601 3,563 4,473 5,332 Investments 11.4 16.4 31.3 66.2 Intangibles 5.4 6.5 7.4 8.2 Other non-current assets 120.7 120.3 119.9 119.5 Total assets 8,219 10,869 13,081 15,095 Accounts payable 878 917 1,010 1,014 Short-term debt 3,029 2,448 3,609 4,770 Current provisions — — — — Other current liabilities 1,448 1,542 1,717 1,743 Current liabilities 5,354 4,907 6,336 7,527 Long-term debt 102.3 82.7 121.9 161.1 Non-current provisions — — — — Other non-current liab. 16.1 16.1 16.1 16.1 Total liabilities 5,473 5,006 6,474 7,705 Shareholders' equity 2,726 5,845 6,590 7,376 Minority interests 19.6 18.1 16.0 13.7 Total liabilities & equity 8,219 10,869 13,081 15,095

Per share data 12/14A 12/15E 12/16E 12/17E

Shares (wtd avg.) (mn) 1,094 1,576 1,576 1,576 EPS (Credit Suisse) (Rmb)

0.50 0.40 0.55 0.60 DPS (Rmb) 0.10 0.07 0.10 0.11 BVPS (Rmb) 2.54 3.71 4.18 4.68 Operating CFPS (Rmb) 0.33 0.61 0.71 0.85

Key ratios and valuation

12/14A 12/15E 12/16E 12/17E

Growth(%) Sales revenue 22.4 6.5 11.4 1.5 EBIT 22.7 27.4 22.7 12.6 Net profit 33.4 14.0 38.1 9.9 EPS 33.4 (20.8) 38.1 9.9 Margins (%)

EBITDA 8.8 10.7 12.0 13.5 EBIT 7.8 9.3 10.2 11.3 Pre-tax profit 7.1 7.6 9.5 10.3 Net profit 5.37 5.75 7.12 7.72 Valuation metrics (x) P/E 10.0 12.6 9.1 8.3 P/B 1.96 1.34 1.19 1.06 Dividend yield (%) 1.91 1.49 2.06 2.26 P/CF 15.0 8.1 7.0 5.8 EV/sales 0.92 0.67 0.62 0.62 EV/EBITDA 10.4 6.2 5.2 4.6 EV/EBIT 11.9 7.2 6.0 5.4 ROE analysis (%) ROE 22.1 14.6 13.9 13.6 ROIC 18.2 15.9 16.2 15.7 Asset turnover (x) 1.24 1.00 0.92 0.81 Interest burden (x) 0.92 0.82 0.93 0.91 Tax burden (x) 0.75 0.75 0.75 0.75 Financial leverage (x) 2.99 1.85 1.98 2.04 Credit ratios Net debt/equity (%) 56.1 (10.5) (5.8) (3.8) Net debt/EBITDA (x) 1.71 (0.53) (0.26) (0.17) Interest cover (x) 11.4 5.5 11.8 8.4

Source: Company data, Thomson Reuters, Credit Suisse estimates.

0

2

4

6

8

10

12

14

16

Aug-13 Dec-13 Apr-14 Aug-14 Dec-14 Apr-15

12MF P/E multiple

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Aug-13 Dec-13 Apr-14 Aug-14 Dec-14 Apr-15

12MF P/B multiple

Source: IBES

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 4

From luxury dealer to high-end EV maker Initiating with OUTPERFORM; HK$8.80 TP implies

42% potential upside Harmony Auto, a leading luxury dealer group in China, is transforming into a new energy

vehicle (NEV) maker. It has tied up with Foxconn and Tencent, and has acquired an 88%

stake in Greenfield Motor (an NEV maker). Although traditional car dealership operation

remains the major near-term earnings contributor (97-99% in 2016-17) for Harmony, we

think its new NEV operation is likely to provide decent long-term growth potential. After a

47% correction from its last peak, the stock is trading at 12.6/9x 2015/16E P/E and its risk-

reward potential looks attractive.

Aftersales income to jump on expanding

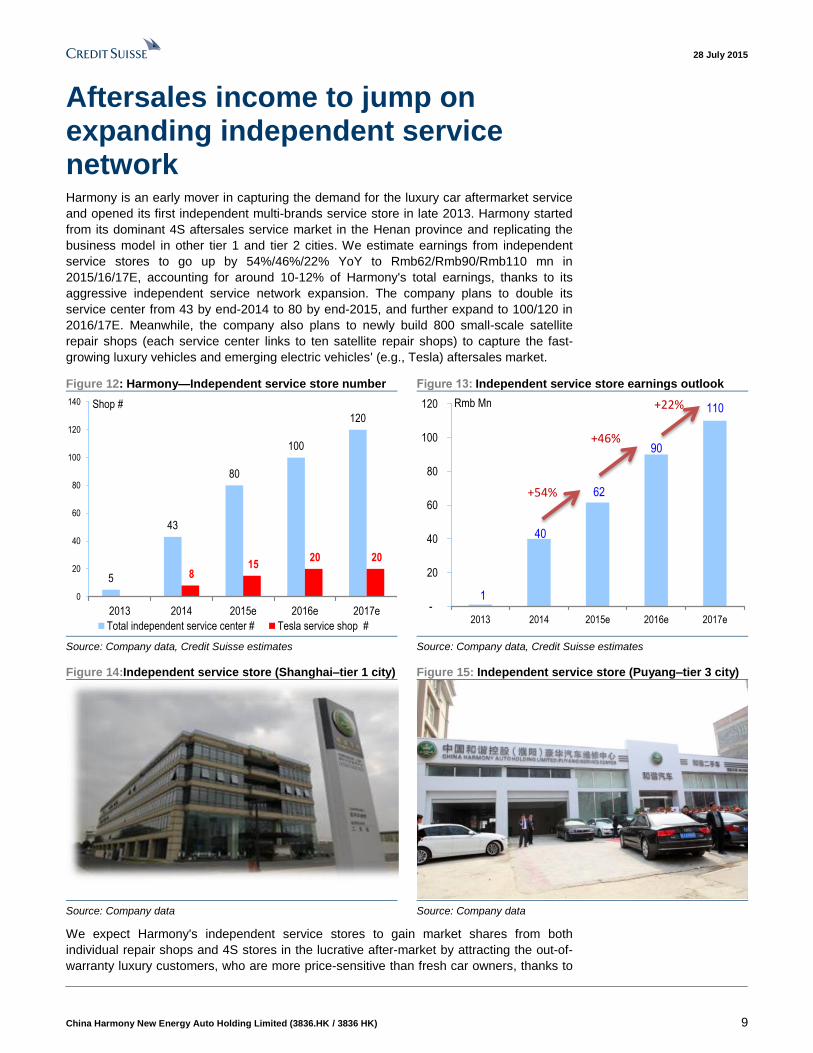

independent service network Harmony auto is doubling its independent luxury car serve centers from 43 in 2014 to 80 in 2015. Meanwhile, the company is also planning to newly build 800 small-scale satellite repair shops (each service center links to ten satellite repair shops) to capture the fast-growing luxury vehicles and emerging electric vehicles' aftersales market. We expect Harmony's independent service stores to gain market shares from both individual repair shops and 4S stores in the lucrative after-market by attracting the out-of-warranty and more price-sensitive luxury customers, thanks to Harmony's offering of outstanding balance between service quality and price. We estimate earnings from independent service stores to go up by 54%/46%/22% YoY to Rmb62 mn/Rmb90 mn/Rmb110 mn in 2015/16/17E, respectively, to account for around 10-12% of Harmony's total earnings, thanks to its aggressive independent service network expansion.

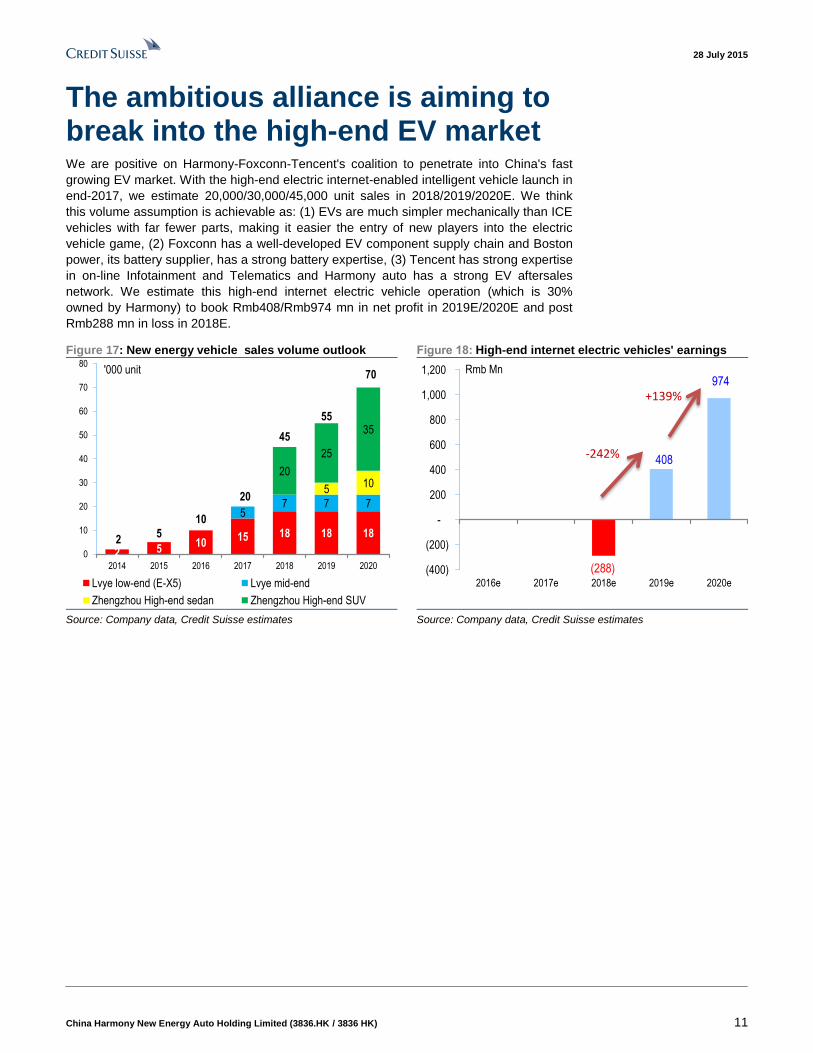

The ambitious alliance is aiming to break into the high-end EV market We understand there are quite a few EV new entrants, but Foxconn-Tencent-Harmony alliance is most likely to work out. With the high-end electric internet intelligent vehicle launch in end-2017, we estimate 20,000/30,000/45,000 unit sales in 2018/2019/2020E, respectively. We think this volume assumption is achievable because: (1) EVs are much simpler mechanically than ICE vehicles, with far fewer parts, making it much easier for new entrants to get into the electric vehicle game, (2) Foxconn's well-developed EV component supply chain along with the strong battery expertise of Boston power, its battery supplier (3) Tencent's expertise in on-line Infotainment and Telematics and Harmony auto's strong EV aftersales network. We believe the ambitious alliance will be able to offer high-quality high-end EVs series and estimate that this operation to book

Rmb408/974 mn in net profit in 2019/20E after booking Rmb288 mn in loss in 2018.

Valuation

We derive our HK$8.80 target price from a DCF-based methodology, as simple multiples do not fully exhibit a dealer business's long-term earnings power and Harmony's new endeavour in the electric vehicle market. Our target price implies 12.9x/11.7x 2016/17E P/E, a premium to Chinese auto dealer's average of 8.0x 12-month forward P/E, which is

justified by the company's penetration into the high growth EV segment, in our view.

Risks

Key downside risks are: (1) Weaker luxury car demand, (2) failure to receive a new energy vehicle license, and (3) intensified competition in the independent service market. Key upside risks are: (1) Integrating internet into the auto aftersales market and (2) government extending the application of new energy vehicle subsidy to lead-acid battery low-speed electric vehicles.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 5

Initiating with OUTPERFORM; HK$8.80 TP implies 42% upside Harmony Auto, a leading luxury dealer group in China (the 36

th largest dealer group by

revenue in 2014), is transforming into a new energy vehicle (NEV) maker, after tying up

with Foxconn and Tencent, and acquiring an 87.6% stake in Greenfield Motor (a NEV

maker). Harmony Auto guided that it will acquire the rest of the Greenfield Motor's stake,

12.4%, in the near future. Although its traditional car dealership operation remains the

major near-term earnings contributor (97-99% in 2016-17) for Harmony, we think its new

NEV operation is likely to provide a decent long-term growth potential. After the 47%

correction from its last peak, the stock is trading at 12.6/9x 2015/16E P/E and its risk-

reward potential looks attractive.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 6

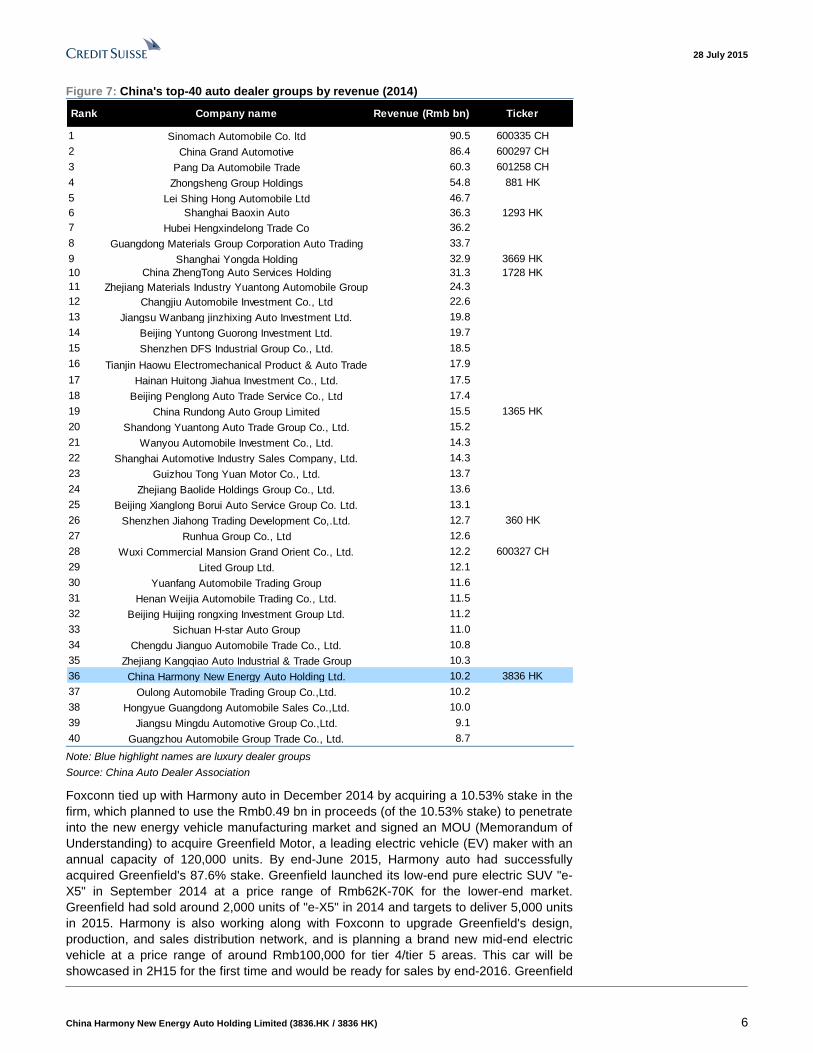

Figure 7: China's top-40 auto dealer groups by revenue (2014)

Rank Company name Revenue (Rmb bn) Ticker

1 Sinomach Automobile Co. ltd 90.5 600335 CH

2 China Grand Automotive 86.4 600297 CH

3 Pang Da Automobile Trade 60.3 601258 CH

4 Zhongsheng Group Holdings 54.8 881 HK

5 Lei Shing Hong Automobile Ltd 46.7

6 Shanghai Baoxin Auto 36.3 1293 HK

7 Hubei Hengxindelong Trade Co 36.2

8 Guangdong Materials Group Corporation Auto Trading 33.7

9 Shanghai Yongda Holding 32.9 3669 HK

10 China ZhengTong Auto Services Holding 31.3 1728 HK

11 Zhejiang Materials Industry Yuantong Automobile Group 24.3

12 Changjiu Automobile Investment Co., Ltd 22.6

13 Jiangsu Wanbang jinzhixing Auto Investment Ltd. 19.8

14 Beijing Yuntong Guorong Investment Ltd. 19.7

15 Shenzhen DFS Industrial Group Co., Ltd. 18.5

16 Tianjin Haowu Electromechanical Product & Auto Trade 17.9

17 Hainan Huitong Jiahua Investment Co., Ltd. 17.5

18 Beijing Penglong Auto Trade Service Co., Ltd 17.4

19 China Rundong Auto Group Limited 15.5 1365 HK

20 Shandong Yuantong Auto Trade Group Co., Ltd. 15.2

21 Wanyou Automobile Investment Co., Ltd. 14.3

22 Shanghai Automotive Industry Sales Company, Ltd. 14.3

23 Guizhou Tong Yuan Motor Co., Ltd. 13.7

24 Zhejiang Baolide Holdings Group Co., Ltd. 13.6

25 Beijing Xianglong Borui Auto Service Group Co. Ltd. 13.1

26 Shenzhen Jiahong Trading Development Co,.Ltd. 12.7 360 HK

27 Runhua Group Co., Ltd 12.6

28 Wuxi Commercial Mansion Grand Orient Co., Ltd. 12.2 600327 CH

29 Lited Group Ltd. 12.1

30 Yuanfang Automobile Trading Group 11.6

31 Henan Weijia Automobile Trading Co., Ltd. 11.5

32 Beijing Huijing rongxing Investment Group Ltd. 11.2

33 Sichuan H-star Auto Group 11.0

34 Chengdu Jianguo Automobile Trade Co., Ltd. 10.8

35 Zhejiang Kangqiao Auto Industrial & Trade Group 10.3

36 China Harmony New Energy Auto Holding Ltd. 10.2 3836 HK

37 Oulong Automobile Trading Group Co.,Ltd. 10.2

38 Hongyue Guangdong Automobile Sales Co.,Ltd. 10.0

39 Jiangsu Mingdu Automotive Group Co.,Ltd. 9.1

40 Guangzhou Automobile Group Trade Co., Ltd. 8.7 Note: Blue highlight names are luxury dealer groups

Source: China Auto Dealer Association

Foxconn tied up with Harmony auto in December 2014 by acquiring a 10.53% stake in the

firm, which planned to use the Rmb0.49 bn in proceeds (of the 10.53% stake) to penetrate

into the new energy vehicle manufacturing market and signed an MOU (Memorandum of

Understanding) to acquire Greenfield Motor, a leading electric vehicle (EV) maker with an

annual capacity of 120,000 units. By end-June 2015, Harmony auto had successfully

acquired Greenfield's 87.6% stake. Greenfield launched its low-end pure electric SUV "e-

X5" in September 2014 at a price range of Rmb62K-70K for the lower-end market.

Greenfield had sold around 2,000 units of "e-X5" in 2014 and targets to deliver 5,000 units

in 2015. Harmony is also working along with Foxconn to upgrade Greenfield's design,

production, and sales distribution network, and is planning a brand new mid-end electric

vehicle at a price range of around Rmb100,000 for tier 4/tier 5 areas. This car will be

showcased in 2H15 for the first time and would be ready for sales by end-2016. Greenfield

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 7

plans to sell 5,000 units of this new mid-end electric vehicle in 2017, thanks to its

refreshed stylish design, higher efficient battery, and stronger dynamics.

Figure 8: Greenfield "e-X5" electric SUV

Source: Company data

Tencent joined the Foxconn–Harmony alliance in March 2015 by pencilling in an

agreement on developing a smart electric car platform to integrate electric vehicles to the

internet. The coalition established "Harmony Futeng", a 40:30:30 investment management

company formed by Harmony:Foxconn:Tencent, in that proportion, in June 2015, aiming at

internet and intelligent electric vehicle opportunities. Harmony guided that this ambitious

alliance plans to build a new high-end electric vehicle plant in Zhengzhou city, with

200,000 units of annual capacity. This plant will be used to launch high-end products

(priced at around Rmb300,000), such as a pure-electric internet-enabled intelligent vehicle

by end-2017, which could drive 300 km on a single charge with 180 km/hour of maximum

speed. The alliance will invest Rmb4 bn in the next three years for the new plant and the

development of new high-end EV models (a sedan and an SUV), per Harmony's guidance.

Figure 9: Foxconn-Tencent-Harmony alliance history

(Dec. 22 2014) Foxconn

subscribed 129 mn shares in

Harmony and became its 2nd

largest shareholder

(May 11 2015) Harmony

acquired 64.64% stake in

Greenfield Motor, an EV

manufacturer

(Jun. 26 2015) Harmony acquired

additional 22.93% stake in

Greenfield Motor, to a total 87.6%

(Jun. 18 2015) Harmony (40%), Foxconn

(30%) Tencent (30%) formed an investment

management company to develop “Internet

+ Intelligent Electric Vehicle”

(Jun. 28 2015) Foxconn

bought 40 mn shares (or

2.5% stake) in Harmony

from the Chairman

(Dec. 30 2014) Harmony signed

a MOU to acquire Greenfield

Motor, an EV manufacturer

(Mar. 23 2015) Harmony-Foxconn-Tencent pencil an

agreement on jointly developing a smart electric car

platform to integrate the internet with electric vehicles

(End-2016) Brand

new mid-end electric

vehicle launch

(End-2017) New

high-end internet

intelligent electric

vehicle launch

Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 8

Figure 10: Foxconn-Tencent-Harmony alliance to penetrate into China's intelligent electric vehicle market

Source: Company data

Figure 11: Terry Gou (Foxconn), Changge Feng (Harmony) and Pony Ma (Tencent)

Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 9

Aftersales income to jump on expanding independent service network Harmony is an early mover in capturing the demand for the luxury car aftermarket service

and opened its first independent multi-brands service store in late 2013. Harmony started

from its dominant 4S aftersales service market in the Henan province and replicating the

business model in other tier 1 and tier 2 cities. We estimate earnings from independent

service stores to go up by 54%/46%/22% YoY to Rmb62/Rmb90/Rmb110 mn in

2015/16/17E, accounting for around 10-12% of Harmony's total earnings, thanks to its

aggressive independent service network expansion. The company plans to double its

service center from 43 by end-2014 to 80 by end-2015, and further expand to 100/120 in

2016/17E. Meanwhile, the company also plans to newly build 800 small-scale satellite

repair shops (each service center links to ten satellite repair shops) to capture the fast-

growing luxury vehicles and emerging electric vehicles' (e.g., Tesla) aftersales market.

Figure 12: Harmony—Independent service store number Figure 13: Independent service store earnings outlook

5

43

80

100

120

8 15

20 20

0

20

40

60

80

100

120

140

2013 2014 2015e 2016e 2017e

Shop #

Total independent service center # Tesla service shop #

1

40

62

90

110

-

20

40

60

80

100

120

2013 2014 2015e 2016e 2017e

Rmb Mn

+54%

+46%

+22%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 14:Independent service store (Shanghai–tier 1 city) Figure 15: Independent service store (Puyang–tier 3 city)

Source: Company data Source: Company data

We expect Harmony's independent service stores to gain market shares from both

individual repair shops and 4S stores in the lucrative after-market by attracting the out-of-

warranty luxury customers, who are more price-sensitive than fresh car owners, thanks to

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 10

Harmony's reputation for service quality and price. Meanwhile, we expect a rising demand

for new energy vehicle aftersales service to help Harmony capture the emerging

opportunities, thanks to its strong EV service expertise via its partnership with Tesla for its

aftersales service.

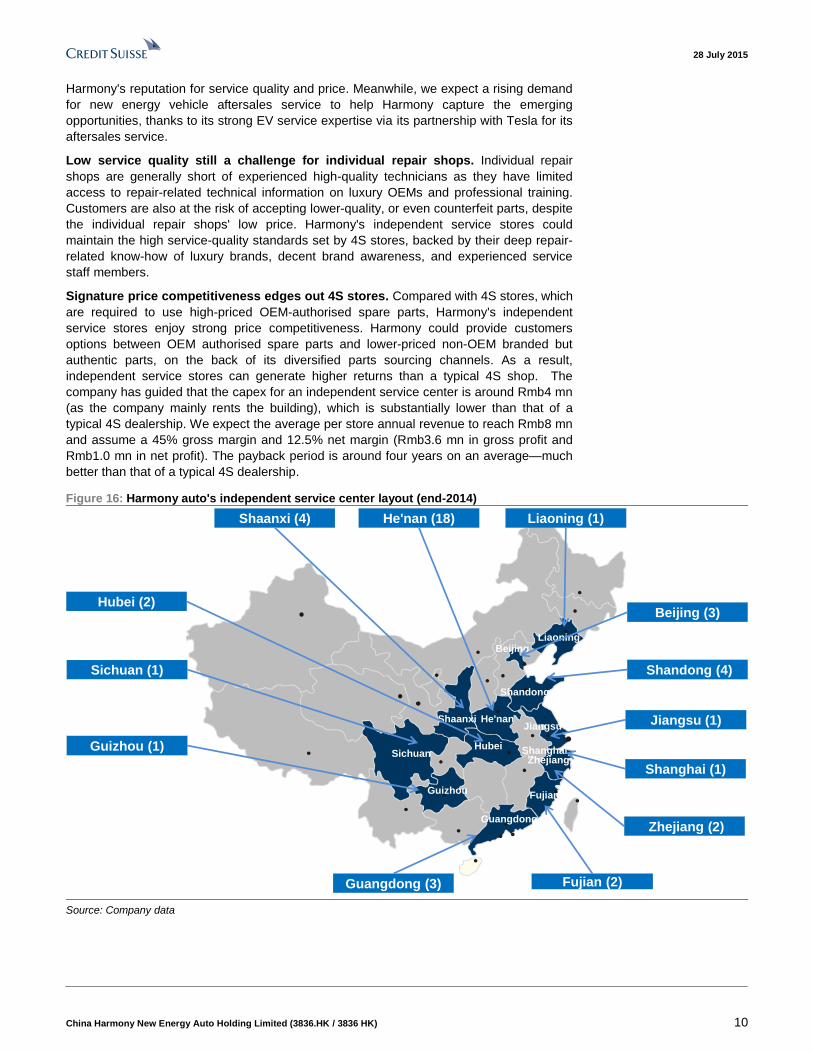

Low service quality still a challenge for individual repair shops. Individual repair

shops are generally short of experienced high-quality technicians as they have limited

access to repair-related technical information on luxury OEMs and professional training.

Customers are also at the risk of accepting lower-quality, or even counterfeit parts, despite

the individual repair shops' low price. Harmony's independent service stores could

maintain the high service-quality standards set by 4S stores, backed by their deep repair-

related know-how of luxury brands, decent brand awareness, and experienced service

staff members.

Signature price competitiveness edges out 4S stores. Compared with 4S stores, which

are required to use high-priced OEM-authorised spare parts, Harmony's independent

service stores enjoy strong price competitiveness. Harmony could provide customers

options between OEM authorised spare parts and lower-priced non-OEM branded but

authentic parts, on the back of its diversified parts sourcing channels. As a result,

independent service stores can generate higher returns than a typical 4S shop. The

company has guided that the capex for an independent service center is around Rmb4 mn

(as the company mainly rents the building), which is substantially lower than that of a

typical 4S dealership. We expect the average per store annual revenue to reach Rmb8 mn

and assume a 45% gross margin and 12.5% net margin (Rmb3.6 mn in gross profit and

Rmb1.0 mn in net profit). The payback period is around four years on an average—much

better than that of a typical 4S dealership.

Figure 16: Harmony auto's independent service center layout (end-2014)

Beijing (3)

Shandong (4)

He'nan (18)

Shaanxi

Hubei

Beijing

Shandong

Jiangsu

Zhejiang

Guangdong

Shanghai

He'nan

Guizhou

Sichuan

Liaoning

Shaanxi (4)

Guangdong (3)

Shanghai (1)

Jiangsu (1)

Zhejiang (2)

Hubei (2)

Liaoning (1)

Guizhou (1)

Sichuan (1)

Fujian (2)

Fujian

Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 11

The ambitious alliance is aiming to break into the high-end EV market We are positive on Harmony-Foxconn-Tencent's coalition to penetrate into China's fast

growing EV market. With the high-end electric internet-enabled intelligent vehicle launch in

end-2017, we estimate 20,000/30,000/45,000 unit sales in 2018/2019/2020E. We think

this volume assumption is achievable as: (1) EVs are much simpler mechanically than ICE

vehicles with far fewer parts, making it easier the entry of new players into the electric

vehicle game, (2) Foxconn has a well-developed EV component supply chain and Boston

power, its battery supplier, has a strong battery expertise, (3) Tencent has strong expertise

in on-line Infotainment and Telematics and Harmony auto has a strong EV aftersales

network. We estimate this high-end internet electric vehicle operation (which is 30%

owned by Harmony) to book Rmb408/Rmb974 mn in net profit in 2019E/2020E and post

Rmb288 mn in loss in 2018E.

Figure 17: New energy vehicle sales volume outlook Figure 18: High-end internet electric vehicles' earnings

2 510

15 18 18 18

57 7 7

510

20

25

35

25

10

20

45

55

70

0

10

20

30

40

50

60

70

80

2014 2015 2016 2017 2018 2019 2020

'000 unit

Lvye low-end (E-X5) Lvye mid-end

Zhengzhou High-end sedan Zhengzhou High-end SUV

(288)

408

974

(400)

(200)

-

200

400

600

800

1,000

1,200

2016e 2017e 2018e 2019e 2020e

Rmb Mn

-242%

+139%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 12

Figure 19: New high-end internet electric vehicle plant blueprint in Zhengzhou

Source: Company data, DaHe Daily

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 13

Much easier for new entrants to assemble EVs than

ICEs

EVs are mechanically much simpler than ICE vehicles, with far fewer parts, making it

much easier for new entrants to get into the electric vehicle game. The supply chain of a

conventional OEM is a very lengthy and complex operation – a typical global OEM would

require more than 1,000 suppliers to supply over 20,000-30,000 components, including

engine, fuel system, transmission, drive train, exhaust, etc., that make up an internal

combustion engine (ICE) vehicle.

Compared with the complexity to develop and produce an ICE vehicle, which requires

sophisticated assembling skills to deal with massive precision spare parts, electric vehicles

that have remarkably far fewer parts are much easier to manufacture and assemble. In

particular, engine and transmission, the two most complicated systems in an ICE vehicle

no longer exist in an EV. Propelled by an electric motor and a battery pack, an EV's

propulsion system is less complex, as there are fewer moving parts. Transmission also

becomes unnecessary, as the electric motor's output characteristic does not require a

transmission to adapt. The electrification of the powertrain system eliminates a number of

control and connection parts specific to ICE such as starters, spark plugs, clutch valves,

tailpipe, fuel injection, distributor, fuel tank, among others, leaving an electric motor to

match the battery pack – the single biggest cost component in a typical electric vehicle.

In addition, an EV's simplified powertrain system and spare parts reduce its supply-chain

complexity, enabling modular design applicable for its mass production. Modularity could

largely lower the barrier of entry for EV manufacturing, as new entrants may source core

EV components, such as electric motor, battery from multiple component suppliers.

Therefore, we see a rising trend of ambitious new players entering the EV industry, such

as internet giant Google.

Figure 20: Typical ICE vehicle chassis structure Figure 21: Typical electric vehicle chassis structure

Battery pack

Electric motorSteering system

Coil springShock absorbers

Radiator

Source: Company data Source: Company data

We expect the Foxconn-Tencent-Harmony alliance to get into EV assembly, thanks to not

only Greenfield's electric vehicle experience and Foxconn's well-developed EV component

supply chain but also Foxconn's superior production management expertise. Foxconn, as

the key assembler of Apple products, has built an outstanding track record in

manufacturing and is undoubtedly a world class assembler. We believe Foxconn would

bring its superior production management into the EV production.

BYD was a good example of EV market penetration: The Foxconn-Tencent-Harmony

alliance is at a similar situation that BYD was in, over 12 years ago, including its lack of

experience and track record in car manufacturing and its beginnings by acquiring a vehicle

manufacturing company, among others. When BYD set its mind into entering the electric

vehicle business as a green hand, many people jumped into the conclusion that BYD

would fail. Now, BYD has become the largest new energy vehicle maker in China, with a

28% market share. We think Foxconn-Tencent-Harmony alliance enjoys better timing—

China's EV industry take off.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 14

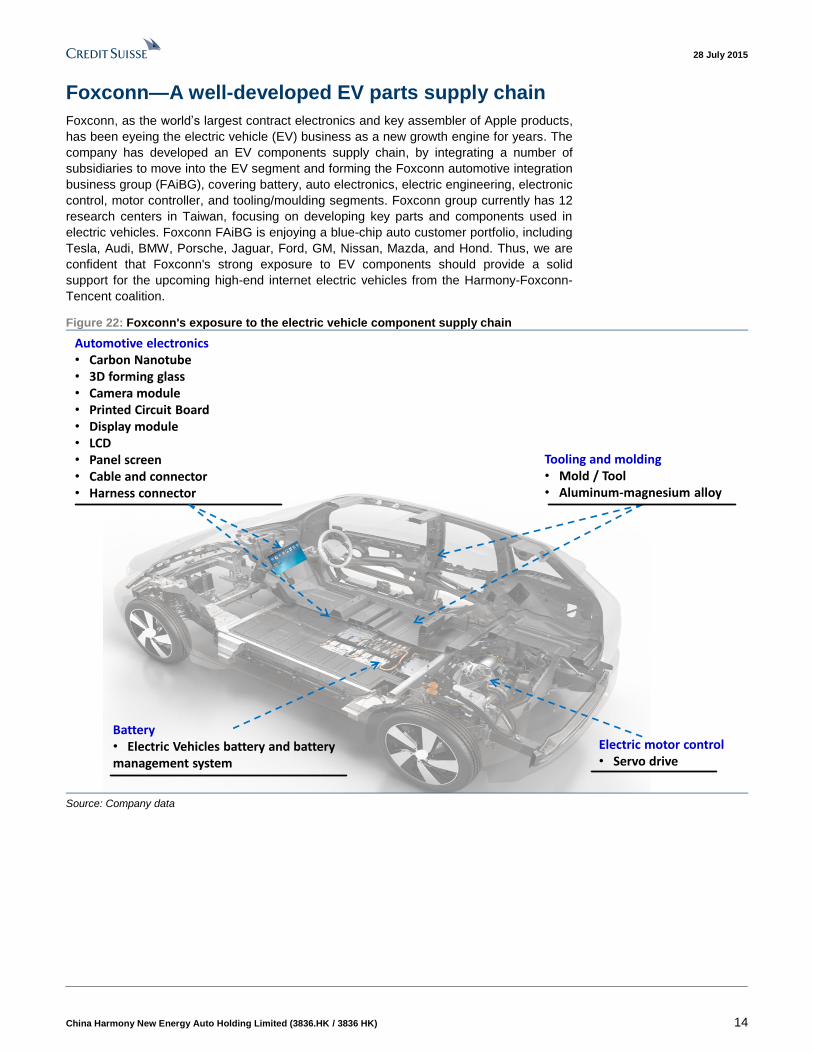

Foxconn—A well-developed EV parts supply chain

Foxconn, as the world’s largest contract electronics and key assembler of Apple products,

has been eyeing the electric vehicle (EV) business as a new growth engine for years. The

company has developed an EV components supply chain, by integrating a number of

subsidiaries to move into the EV segment and forming the Foxconn automotive integration

business group (FAiBG), covering battery, auto electronics, electric engineering, electronic

control, motor controller, and tooling/moulding segments. Foxconn group currently has 12

research centers in Taiwan, focusing on developing key parts and components used in

electric vehicles. Foxconn FAiBG is enjoying a blue-chip auto customer portfolio, including

Tesla, Audi, BMW, Porsche, Jaguar, Ford, GM, Nissan, Mazda, and Hond. Thus, we are

confident that Foxconn's strong exposure to EV components should provide a solid

support for the upcoming high-end internet electric vehicles from the Harmony-Foxconn-

Tencent coalition.

Figure 22: Foxconn's exposure to the electric vehicle component supply chain

Tooling and molding• Mold / Tool • Aluminum-magnesium alloy

Automotive electronics• Carbon Nanotube• 3D forming glass• Camera module • Printed Circuit Board• Display module • LCD• Panel screen• Cable and connector• Harness connector

Battery• Electric Vehicles battery and battery management system

Electric motor control• Servo drive

Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 15

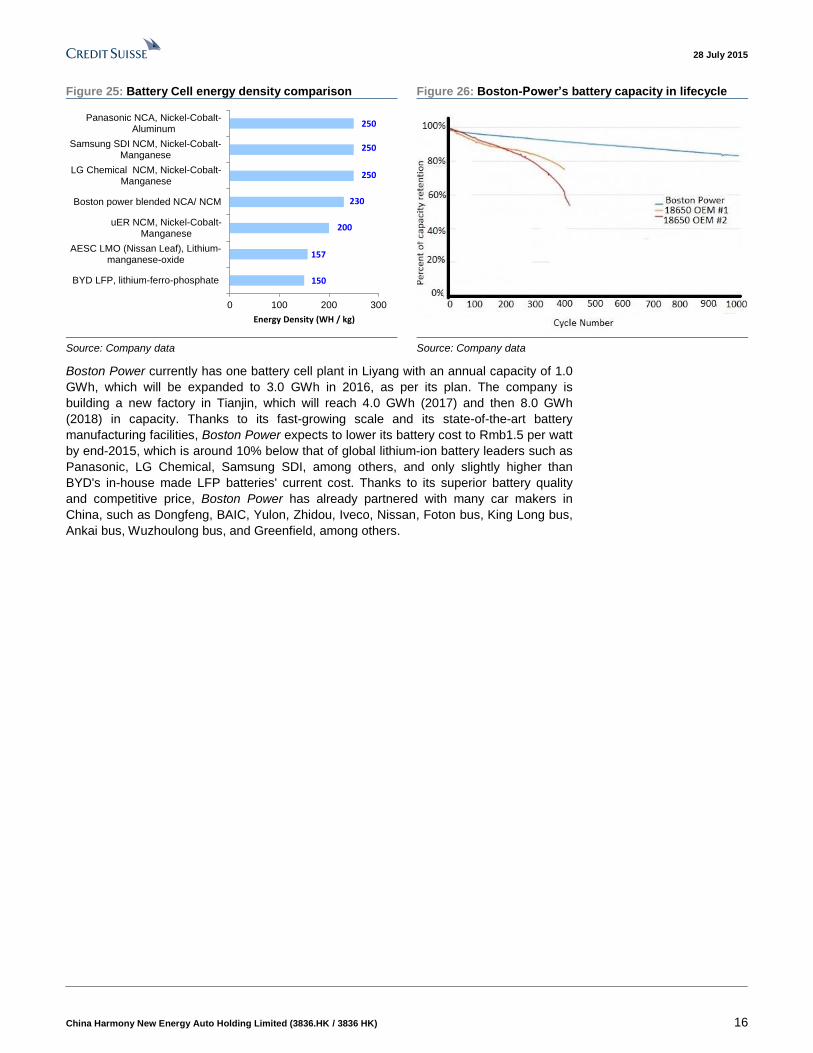

Strong and diversified partnership to break battery hurdle

Battery is the most crucial part of electric vehicles and the single-biggest cost factor holding up

EVs is the battery cost, which accounts for around 40% of the total cost of a typical electric

vehicle. We think Foxconn-Tencent-Harmony alliance could leverage not only Greenfield

Motor's exiting partnership with Boston Power—a leading lithium-ion battery supplier, but also

a potential tie-up with uER Technology—a lithium battery subsidiary of Foxconn Group and the

major e-bus battery supplier in Taiwan (nominated by Taiwan government).

Figure 23: Boston-Power’s flagship product "Swing 5300" Figure 24: uER Technology lithium battery products

Source: Company data Source: Company data

While most of the Chinese EV makers chose to go with large battery cells (BYD chose in-

house made large-size prismatic LFP battery), Greenfield Motor went against the grain to

use smaller cells manufactured by Boston Power. Boston Power's strength derives from its

unique chemistry formulations (blended NCA/NCM), its mechanical engineering, and

electrical designs. In particular, its cells are based on a flat, oval-shaped design with

dimensions equivalent to two conventional 18650 lithium-ion cells. This unique cell design

supports high energy density, dependable cycle-life, a broad operating temperature range,

fast charge, and multiple safety features.

High energy density. Boston Power battery cells offer 230 wh/kg gravimetric energy

density, significantly outperforming lithium-ion pouch (157 wh/kg) and BYD's LFP

battery (150 wh/kg), though slightly behind global leaders (250 wh/kg from Panasonic

/ LG Chemical / Samsung SDI). Boston Power plans to introduce its fourth generation

battery cells with energy density of 250 wh/kg in 2016, in cooperation with global

leading battery material suppliers, such as BASF. High energy density directly

equates to more miles travelled, as well as reduced battery weight and size, and,

therefore, cost.

Long cycle-life. Boston Power battery cells can undergo over 3,000 charge/discharge

cycles at 90% depth of discharge (DOD), delivering greater than ten years of reliable

calendar life. This is much longer than the conventional lithium-ion batteries, which

begin to fade noticeably after only 300 charges and have to be replaced after about 2-

3 years. Thus Boston power enjoys superior advantage in the long-range electric

vehicle (EV) application.

Broad operating temperature range. Boston Power 's patented chemistry supports

one of industry's widest operating temperature ranges—a discharge temperature

range from -40°C to 70°C and a charge temperature range from -20°C to 60°C. By

achieving high performance at both high and low temperature extremes, Boston

Power battery supports all-weather performance for electric vehicles (EV) where low

temperature performance is critical.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 16

Figure 25: Battery Cell energy density comparison Figure 26: Boston-Power’s battery capacity in lifecycle

150

157

200

230

250

250

250

0 100 200 300

BYD LFP, lithium-ferro-phosphate

AESC LMO (Nissan Leaf), Lithium-manganese-oxide

uER NCM, Nickel-Cobalt-Manganese

Boston power blended NCA/ NCM

LG Chemical NCM, Nickel-Cobalt-Manganese

Samsung SDI NCM, Nickel-Cobalt-Manganese

Panasonic NCA, Nickel-Cobalt-Aluminum

Energy Density (WH / kg)

Source: Company data Source: Company data

Boston Power currently has one battery cell plant in Liyang with an annual capacity of 1.0

GWh, which will be expanded to 3.0 GWh in 2016, as per its plan. The company is

building a new factory in Tianjin, which will reach 4.0 GWh (2017) and then 8.0 GWh

(2018) in capacity. Thanks to its fast-growing scale and its state-of-the-art battery

manufacturing facilities, Boston Power expects to lower its battery cost to Rmb1.5 per watt

by end-2015, which is around 10% below that of global lithium-ion battery leaders such as

Panasonic, LG Chemical, Samsung SDI, among others, and only slightly higher than

BYD's in-house made LFP batteries' current cost. Thanks to its superior battery quality

and competitive price, Boston Power has already partnered with many car makers in

China, such as Dongfeng, BAIC, Yulon, Zhidou, Iveco, Nissan, Foton bus, King Long bus,

Ankai bus, Wuzhoulong bus, and Greenfield, among others.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 17

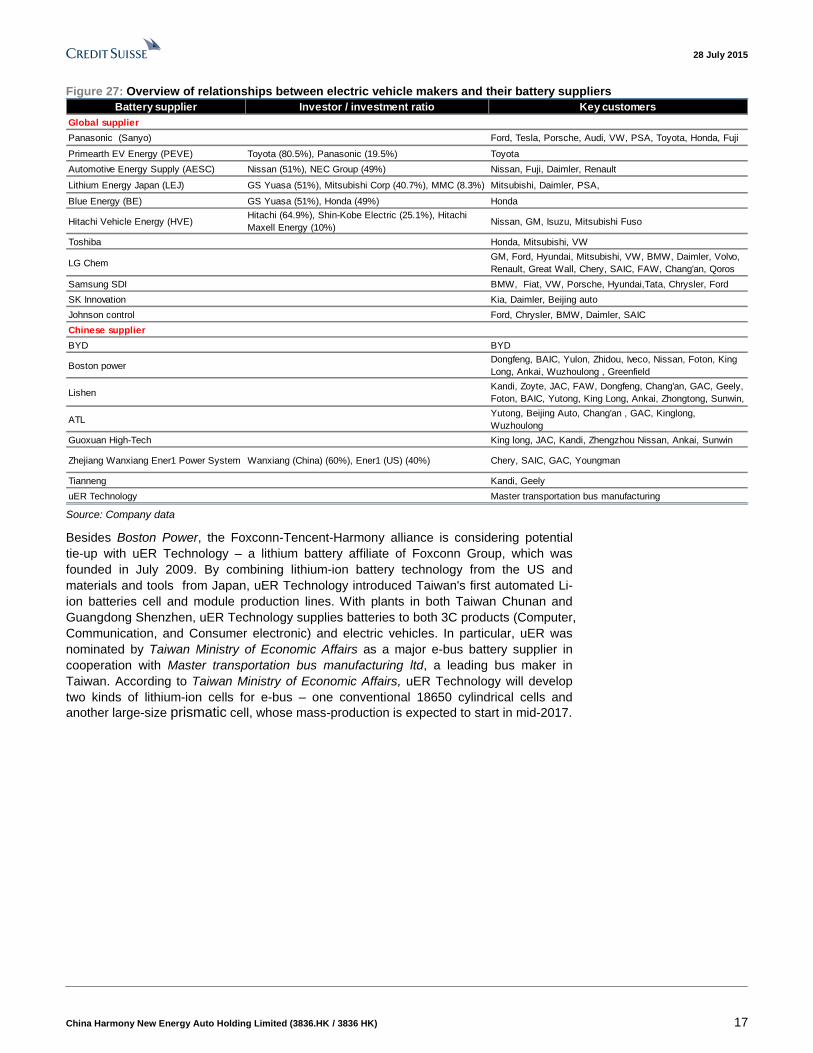

Figure 27: Overview of relationships between electric vehicle makers and their battery suppliers

Battery supplier Investor / investment ratio Key customers

Global supplier

Panasonic (Sanyo) Ford, Tesla, Porsche, Audi, VW, PSA, Toyota, Honda, Fuji

Primearth EV Energy (PEVE) Toyota (80.5%), Panasonic (19.5%) Toyota

Automotive Energy Supply (AESC) Nissan (51%), NEC Group (49%) Nissan, Fuji, Daimler, Renault

Lithium Energy Japan (LEJ) GS Yuasa (51%), Mitsubishi Corp (40.7%), MMC (8.3%) Mitsubishi, Daimler, PSA,

Blue Energy (BE) GS Yuasa (51%), Honda (49%) Honda

Hitachi Vehicle Energy (HVE)Hitachi (64.9%), Shin-Kobe Electric (25.1%), Hitachi

Maxell Energy (10%)Nissan, GM, Isuzu, Mitsubishi Fuso

Toshiba Honda, Mitsubishi, VW

LG Chem GM, Ford, Hyundai, Mitsubishi, VW, BMW, Daimler, Volvo,

Renault, Great Wall, Chery, SAIC, FAW, Chang'an, Qoros

Samsung SDI BMW, Fiat, VW, Porsche, Hyundai,Tata, Chrysler, Ford

SK Innovation Kia, Daimler, Beijing auto

Johnson control Ford, Chrysler, BMW, Daimler, SAIC

Chinese supplier

BYD BYD

Boston powerDongfeng, BAIC, Yulon, Zhidou, Iveco, Nissan, Foton, King

Long, Ankai, Wuzhoulong , Greenfield

LishenKandi, Zoyte, JAC, FAW, Dongfeng, Chang'an, GAC, Geely,

Foton, BAIC, Yutong, King Long, Ankai, Zhongtong, Sunwin,

ATLYutong, Beijing Auto, Chang'an , GAC, Kinglong,

Wuzhoulong

Guoxuan High-Tech King long, JAC, Kandi, Zhengzhou Nissan, Ankai, Sunwin

Zhejiang Wanxiang Ener1 Power System Wanxiang (China) (60%), Ener1 (US) (40%) Chery, SAIC, GAC, Youngman

Tianneng Kandi, Geely

uER Technology Master transportation bus manufacturing Source: Company data

Besides Boston Power, the Foxconn-Tencent-Harmony alliance is considering potential

tie-up with uER Technology – a lithium battery affiliate of Foxconn Group, which was

founded in July 2009. By combining lithium-ion battery technology from the US and

materials and tools from Japan, uER Technology introduced Taiwan's first automated Li-

ion batteries cell and module production lines. With plants in both Taiwan Chunan and

Guangdong Shenzhen, uER Technology supplies batteries to both 3C products (Computer,

Communication, and Consumer electronic) and electric vehicles. In particular, uER was

nominated by Taiwan Ministry of Economic Affairs as a major e-bus battery supplier in

cooperation with Master transportation bus manufacturing ltd, a leading bus maker in

Taiwan. According to Taiwan Ministry of Economic Affairs, uER Technology will develop

two kinds of lithium-ion cells for e-bus – one conventional 18650 cylindrical cells and

another large-size prismatic cell, whose mass-production is expected to start in mid-2017.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 18

Figure 28: uER's headquarter in Taiwan Chunan Figure 29: uER's Shenzhen batter factory

Source: Company data Source: Company data

Figure 30: uER e-bus battery product – 18650 & prismatic Figure 31: uER 3C battery product – power bank

Source: Company data Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 19

Tencent—Internet expertise plug-into the electric vehicles

Tencent, as the internet giant in China and the maker of popular messaging App "WeChat",

could bring its internet expertise into the car, enabling the EV products to capture the trend

of "Internet of Things" (IoT). By incorporating Tencent's internet platform, car drivers can

access services such as messaging, mapping, music, and payment via telematics platform.

Figure 32: Tencent's "WeDrive" vehicle internet total solution

News

Stock

QQSports

Music

Dianping.com

Fun-drive navigation

Fun-drive T services

Source: Company data

In particular, Tencent's "WeDrive" system could help electric vehicle makers to collect car

owners' information and improve customer relation management, thus increase brand

reputation and loyalty. "WeDrive" is a vehicle internet total solution which integrates

Tencent QQ, QQ music, Tencent news, Dianping, Optional share, Tencent watch the

game, NavInfo Fun Drive navigation, and Fun Drive T service. "WeDrive" enables users to

enjoy the experience of a multi-terminal synchronisation vehicle internet product during

driving and provides safety, entertainment, social and life services for the driving life.

"WeDrive" can also help car owners check vehicle conditions such as mileage, fuel

consumption and tire pressure, tele-control the vehicle's door switch, lighting switch and

air conditioning switch, and send to the vehicle remote POI position info and car automatic

navigation.

Tencent is eager to move into the nascent market for electric internet intelligent vehicle as

its internet peers have already established tie-ups with major auto makers, such as

Alibaba, Baidu, and Letv, among others. For example, Alibaba signed a partnership

agreement with SAIC to co-develop connected cars in July 2014, which will enable SAIC

to use Alibaba's AliYun operating system, its mapping and music services, and big data

and cloud computing technologies. Baidu, a Chinese internet search giant, also launched

its in-car infotainment platform, "CarLife", which enables car users to link their

smartphones with in-vehicle infotainment screens, in order to access all of the connected

car services based on Baidu Maps. Meanwhile, Baidu also hopes to introduce an

autonomous car in collaboration with its artificial intelligence-focused Deep Learning

Institute and BMW. Other examples, include Letv's partnership with BAIC Motor, Pateo &

Yongche with Chery, Sina with Weichai Enranger, etc.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 20

Figure 33: Leading internet giantss effort in electric vehicles

Connected electric vehicle• Invested in U.S. based battery maker Atieva

Inc. in 2014

• Built a R&D team based in Silicon Valley

Connected vehicle• Jointly invested Rmb1 bn in a fund to

develop a connected car in Mar. 2015

• First model will debut in 2016

Electric smart vehicle• Established a joint venture to build electric

smart cars for a car sharing service in Feb. 2015

Self-driving vehicle• Develop a highly automated car

• Plan to launch first model in 2015

High-end connected electric vehicle• Harmony (40%), Foxconn (30%) and Tencent

(30%) formed a joint venture investment management company to develop high-end “Internet + Intelligent Electric Vehicle”

Connected vehicle• Partnered to develop interconnected cars

• Plan to launch first model in Sep. 2015

Connected vehicle• Partnered to develop interconnected cars

with incorporation of Huawei’s telematics system

Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 21

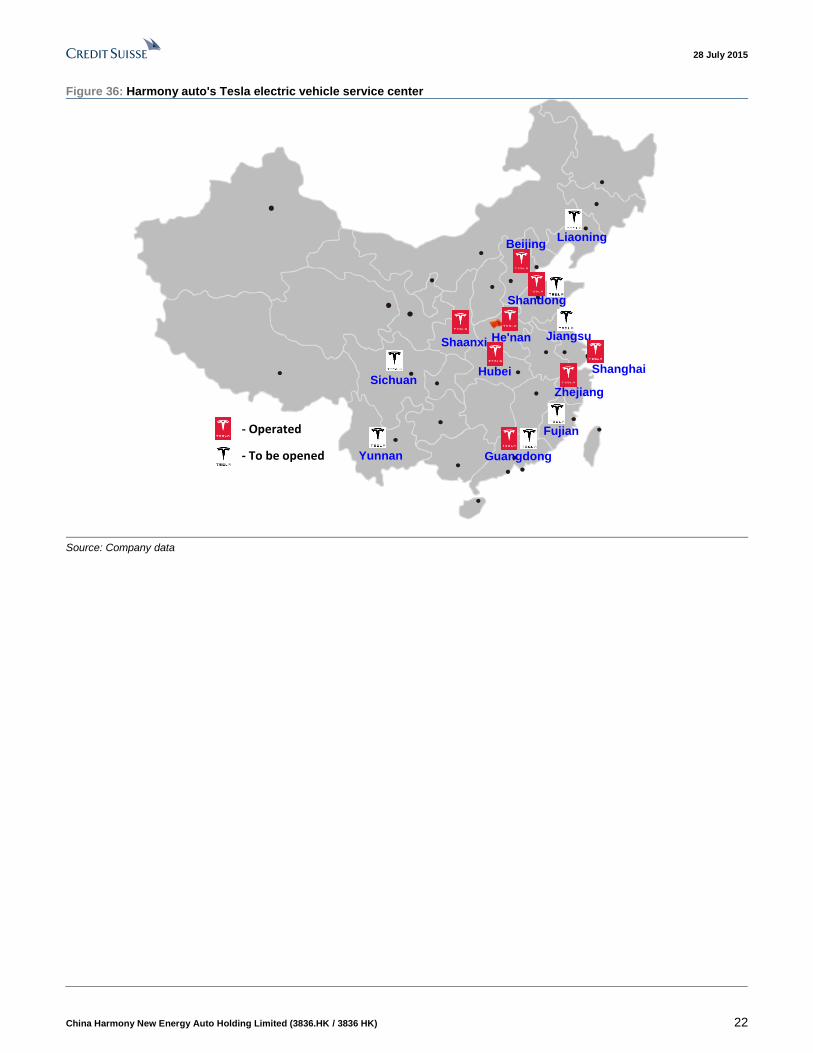

Harmony—A strong EV aftersales expertise and

network

In the EV aftersales market, Harmony has accumulated rich experience through its

exclusive partnership with Tesla for plate work and paint spraying in China (other components

Tesla staff will handle by themselves). Harmony had eight EV aftersales outlets by end-2014

and is expanding rapidly to establish another eight EV aftersales by end-2015 via its

independent aftersales center. We believe Harmony's well-developed independent

network could provide solid support to its high-end electric vehicle development.

Figure 34: Beijing Tesla after-service service center Figure 35: Tesla plate work and paint spraying center

Source: Company data Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 22

Figure 36: Harmony auto's Tesla electric vehicle service center

Shaanxi

Hubei

Beijing

Shandong

Zhejiang

Guangdong

Shanghai

He'nan

Sichuan

Liaoning

Jiangsu

Fujian

Yunnan- To be opened

- Operated

Source: Company data

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 23

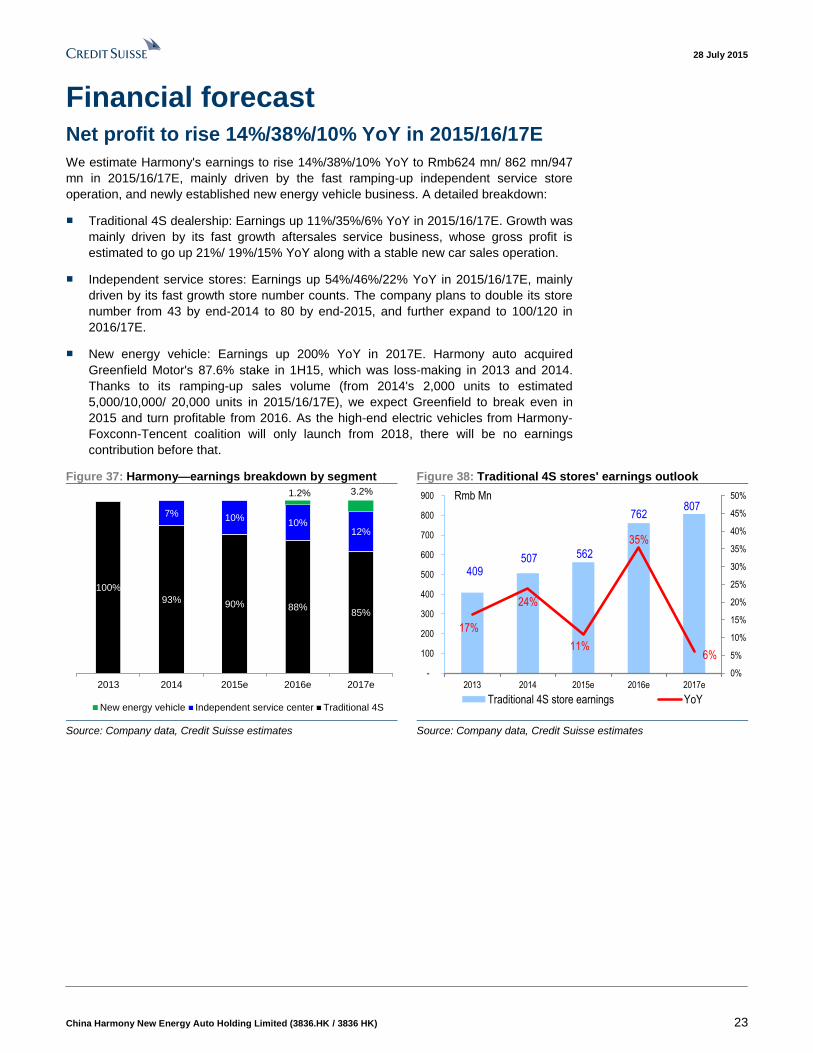

Financial forecast Net profit to rise 14%/38%/10% YoY in 2015/16/17E

We estimate Harmony's earnings to rise 14%/38%/10% YoY to Rmb624 mn/ 862 mn/947

mn in 2015/16/17E, mainly driven by the fast ramping-up independent service store

operation, and newly established new energy vehicle business. A detailed breakdown:

■ Traditional 4S dealership: Earnings up 11%/35%/6% YoY in 2015/16/17E. Growth was

mainly driven by its fast growth aftersales service business, whose gross profit is

estimated to go up 21%/ 19%/15% YoY along with a stable new car sales operation.

■ Independent service stores: Earnings up 54%/46%/22% YoY in 2015/16/17E, mainly

driven by its fast growth store number counts. The company plans to double its store

number from 43 by end-2014 to 80 by end-2015, and further expand to 100/120 in

2016/17E.

■ New energy vehicle: Earnings up 200% YoY in 2017E. Harmony auto acquired

Greenfield Motor's 87.6% stake in 1H15, which was loss-making in 2013 and 2014.

Thanks to its ramping-up sales volume (from 2014's 2,000 units to estimated

5,000/10,000/ 20,000 units in 2015/16/17E), we expect Greenfield to break even in

2015 and turn profitable from 2016. As the high-end electric vehicles from Harmony-

Foxconn-Tencent coalition will only launch from 2018, there will be no earnings

contribution before that.

Figure 37: Harmony—earnings breakdown by segment Figure 38: Traditional 4S stores' earnings outlook

100%

93% 90% 88%85%

7% 10%10%

12%

1.2% 3.2%

2013 2014 2015e 2016e 2017e

New energy vehicle Independent service center Traditional 4S

409 507 562

762 807

17%

24%

11%

35%

6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

-

100

200

300

400

500

600

700

800

900

2013 2014 2015e 2016e 2017e

Rmb Mn

Traditional 4S store earnings YoY

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 24

Figure 39: Independent service stores earnings outlook Figure 40: New energy vehicle operation earnings outlook

1

40

62

90

110

-

20

40

60

80

100

120

2013 2014 2015e 2016e 2017e

Rmb Mn

+54%

+46%

+22%

-

10

30

-

5

10

15

20

25

30

35

2013 2014 2015e 2016e 2017e

Rmb Mn

+200%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

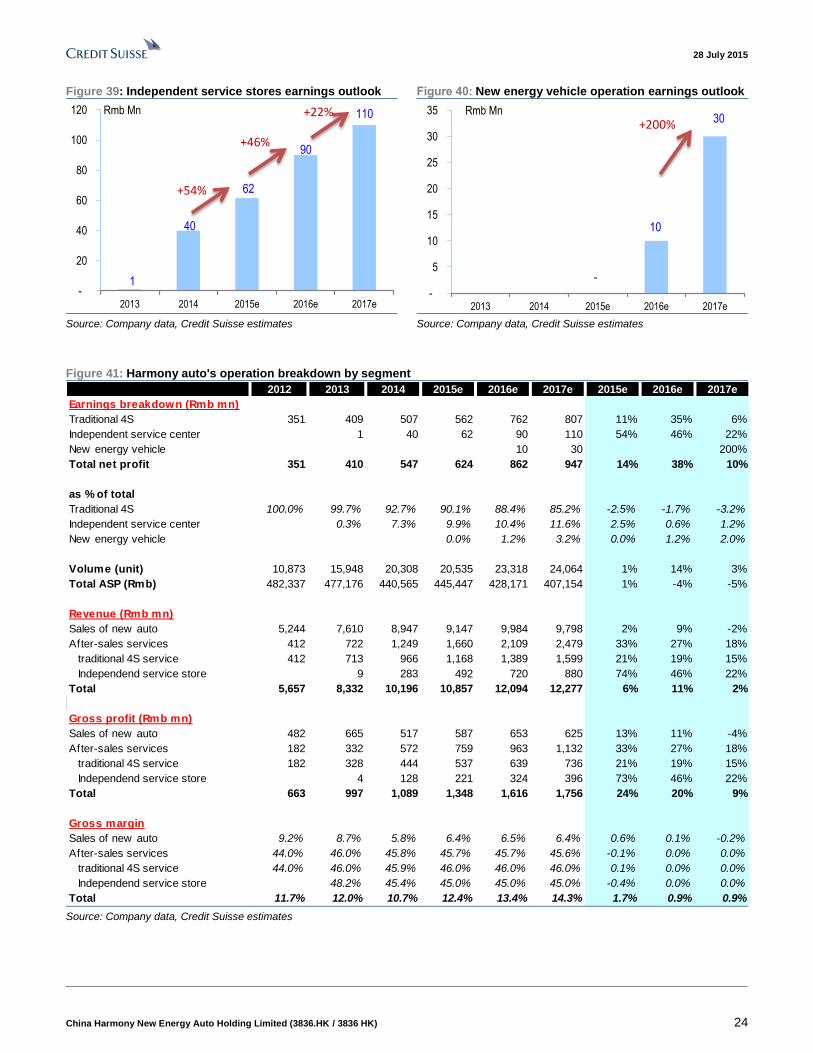

Figure 41: Harmony auto's operation breakdown by segment

2012 2013 2014 2015e 2016e 2017e 2015e 2016e 2017e

Earnings breakdown (Rmb mn)

Traditional 4S 351 409 507 562 762 807 11% 35% 6%

Independent service center 1 40 62 90 110 54% 46% 22%

New energy vehicle 10 30 200%

Total net profit 351 410 547 624 862 947 14% 38% 10%

as % of total

Traditional 4S 100.0% 99.7% 92.7% 90.1% 88.4% 85.2% -2.5% -1.7% -3.2%

Independent service center 0.3% 7.3% 9.9% 10.4% 11.6% 2.5% 0.6% 1.2%

New energy vehicle 0.0% 1.2% 3.2% 0.0% 1.2% 2.0%

Volume (unit) 10,873 15,948 20,308 20,535 23,318 24,064 1% 14% 3%

Total ASP (Rmb) 482,337 477,176 440,565 445,447 428,171 407,154 1% -4% -5%

Revenue (Rmb mn)

Sales of new auto 5,244 7,610 8,947 9,147 9,984 9,798 2% 9% -2%

After-sales services 412 722 1,249 1,660 2,109 2,479 33% 27% 18%

traditional 4S service 412 713 966 1,168 1,389 1,599 21% 19% 15%

Independend service store 9 283 492 720 880 74% 46% 22%

Total 5,657 8,332 10,196 10,857 12,094 12,277 6% 11% 2%

Gross profit (Rmb mn)

Sales of new auto 482 665 517 587 653 625 13% 11% -4%

After-sales services 182 332 572 759 963 1,132 33% 27% 18%

traditional 4S service 182 328 444 537 639 736 21% 19% 15%

Independend service store 4 128 221 324 396 73% 46% 22%

Total 663 997 1,089 1,348 1,616 1,756 24% 20% 9%

Gross margin

Sales of new auto 9.2% 8.7% 5.8% 6.4% 6.5% 6.4% 0.6% 0.1% -0.2%

After-sales services 44.0% 46.0% 45.8% 45.7% 45.7% 45.6% -0.1% 0.0% 0.0%

traditional 4S service 44.0% 46.0% 45.9% 46.0% 46.0% 46.0% 0.1% 0.0% 0.0%

Independend service store 48.2% 45.4% 45.0% 45.0% 45.0% -0.4% 0.0% 0.0%

Total 11.7% 12.0% 10.7% 12.4% 13.4% 14.3% 1.7% 0.9% 0.9% Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 25

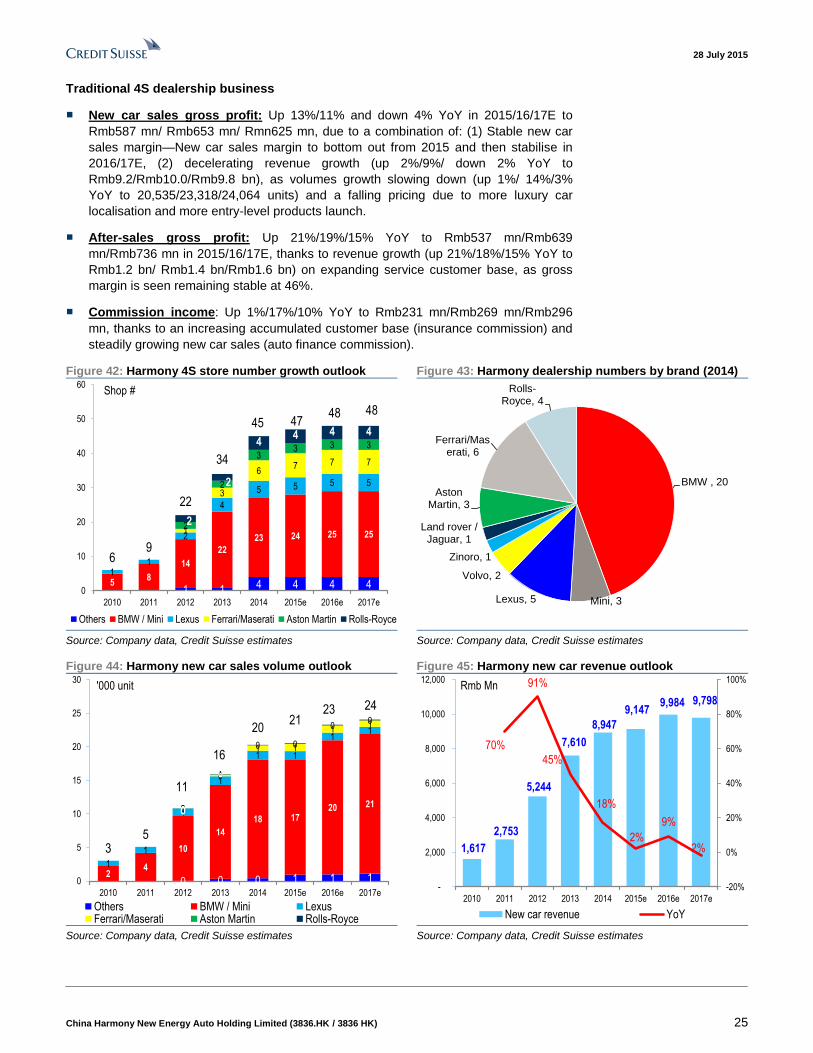

Traditional 4S dealership business

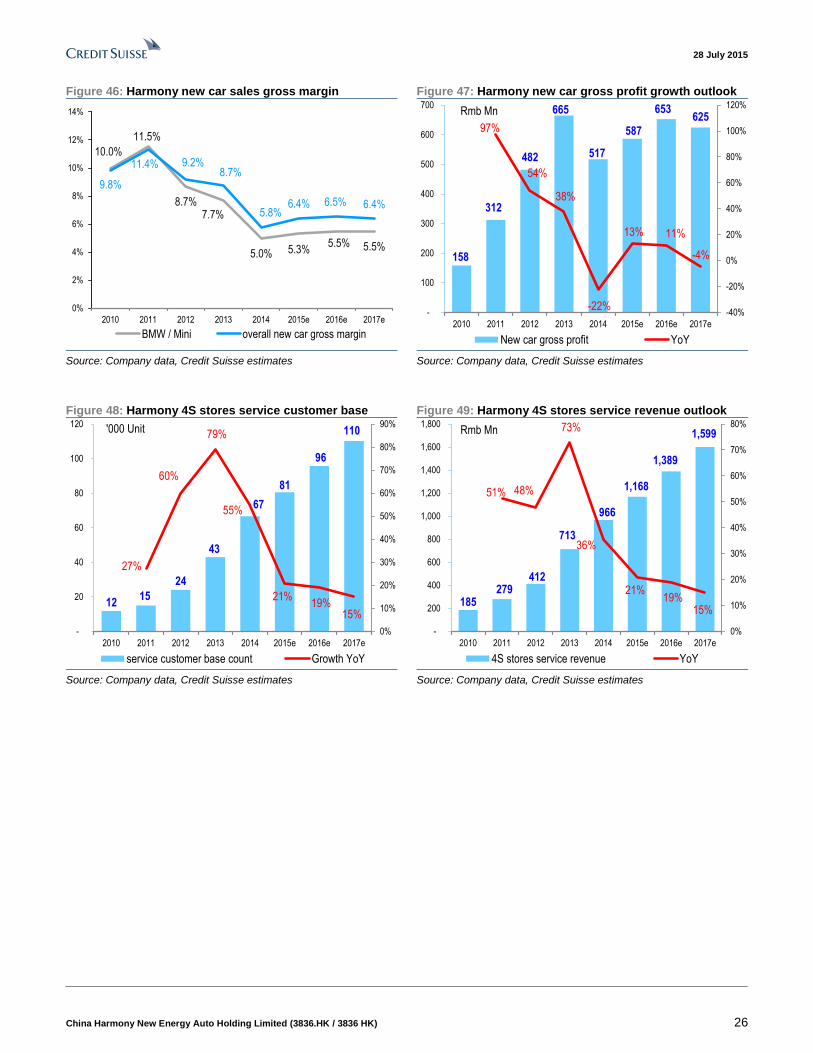

■ New car sales gross profit: Up 13%/11% and down 4% YoY in 2015/16/17E to

Rmb587 mn/ Rmb653 mn/ Rmn625 mn, due to a combination of: (1) Stable new car

sales margin—New car sales margin to bottom out from 2015 and then stabilise in

2016/17E, (2) decelerating revenue growth (up 2%/9%/ down 2% YoY to

Rmb9.2/Rmb10.0/Rmb9.8 bn), as volumes growth slowing down (up 1%/ 14%/3%

YoY to 20,535/23,318/24,064 units) and a falling pricing due to more luxury car

localisation and more entry-level products launch.

■ After-sales gross profit: Up 21%/19%/15% YoY to Rmb537 mn/Rmb639

mn/Rmb736 mn in 2015/16/17E, thanks to revenue growth (up 21%/18%/15% YoY to

Rmb1.2 bn/ Rmb1.4 bn/Rmb1.6 bn) on expanding service customer base, as gross

margin is seen remaining stable at 46%.

■ Commission income: Up 1%/17%/10% YoY to Rmb231 mn/Rmb269 mn/Rmb296

mn, thanks to an increasing accumulated customer base (insurance commission) and

steadily growing new car sales (auto finance commission).

Figure 42: Harmony 4S store number growth outlook Figure 43: Harmony dealership numbers by brand (2014)

1 1 4 4 4 458

14

22

23 24 25 25

11

2

4

5 5 5 5

1

3

67 7 7

2

2

33 3 3

2

2

44 4 4

69

22

34

45 4748 48

0

10

20

30

40

50

60

2010 2011 2012 2013 2014 2015e 2016e 2017e

Shop #

Others BMW / Mini Lexus Ferrari/Maserati Aston Martin Rolls-Royce

BMW , 20

Mini, 3Lexus, 5

Volvo, 2

Zinoro, 1

Land rover / Jaguar, 1

Aston Martin, 3

Ferrari/Maserati, 6

Rolls-Royce, 4

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 44: Harmony new car sales volume outlook Figure 45: Harmony new car revenue outlook

0 0 0 1 1 124

10

14

18 1720 21

1

1

1

1

1 1

11

0

0

1 1

11

0

0

0 0

00

0

0

0 0

0 0

35

11

16

2021

23 24

0

5

10

15

20

25

30

2010 2011 2012 2013 2014 2015e 2016e 2017e

'000 unit

Others BMW / Mini LexusFerrari/Maserati Aston Martin Rolls-Royce

1,617

2,753

5,244

7,610

8,947

9,147 9,984 9,798

70%

91%

45%

18%

2%

9%

-2%

-20%

0%

20%

40%

60%

80%

100%

-

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015e 2016e 2017e

Rmb Mn

New car revenue YoY

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 26

Figure 46: Harmony new car sales gross margin Figure 47: Harmony new car gross profit growth outlook

10.0%

11.5%

8.7%7.7%

5.0% 5.3%5.5% 5.5%

9.8%

11.4% 9.2%8.7%

5.8%6.4% 6.5% 6.4%

0%

2%

4%

6%

8%

10%

12%

14%

2010 2011 2012 2013 2014 2015e 2016e 2017e

BMW / Mini overall new car gross margin

158

312

482

665

517

587

653 625

97%

54%

38%

-22%

13% 11%

-4%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

-

100

200

300

400

500

600

700

2010 2011 2012 2013 2014 2015e 2016e 2017e

Rmb Mn

New car gross profit YoY

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 48: Harmony 4S stores service customer base Figure 49: Harmony 4S stores service revenue outlook

12 15

24

43

67

81

96

110

27%

60%

79%

55%

21%19%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015e 2016e 2017e

'000 Unit

Tho

usan

ds

service customer base count Growth YoY

185 279

412

713

966

1,168

1,389

1,599

51% 48%

73%

36%

21%19%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2010 2011 2012 2013 2014 2015e 2016e 2017e

Rmb Mn

4S stores service revenue YoY

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 27

Figure 50: Harmony 4S stores service gross margin Figure 51: Harmony 4S stores service gross profit outlook

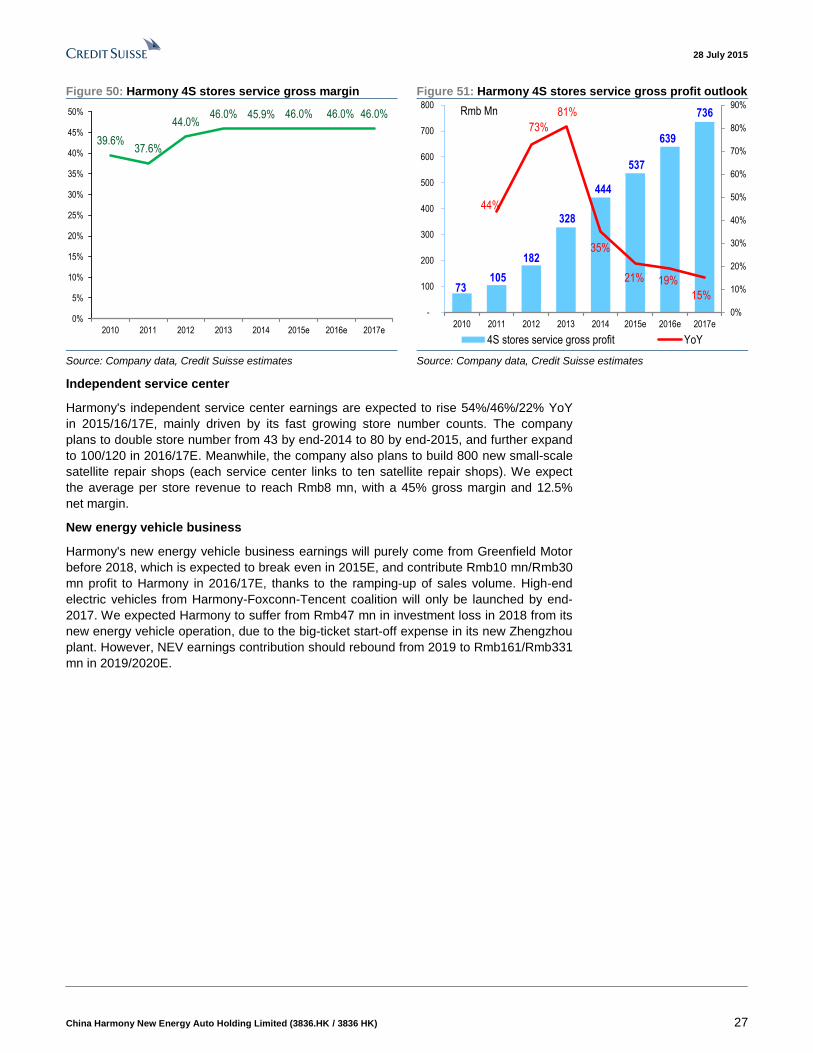

39.6%37.6%

44.0%46.0% 45.9% 46.0% 46.0% 46.0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2010 2011 2012 2013 2014 2015e 2016e 2017e

73 105

182

328

444

537

639

736

44%

73%

81%

35%

21% 19%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 2015e 2016e 2017e

Rmb Mn

4S stores service gross profit YoY

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Independent service center

Harmony's independent service center earnings are expected to rise 54%/46%/22% YoY

in 2015/16/17E, mainly driven by its fast growing store number counts. The company

plans to double store number from 43 by end-2014 to 80 by end-2015, and further expand

to 100/120 in 2016/17E. Meanwhile, the company also plans to build 800 new small-scale

satellite repair shops (each service center links to ten satellite repair shops). We expect

the average per store revenue to reach Rmb8 mn, with a 45% gross margin and 12.5%

net margin.

New energy vehicle business

Harmony's new energy vehicle business earnings will purely come from Greenfield Motor

before 2018, which is expected to break even in 2015E, and contribute Rmb10 mn/Rmb30

mn profit to Harmony in 2016/17E, thanks to the ramping-up of sales volume. High-end

electric vehicles from Harmony-Foxconn-Tencent coalition will only be launched by end-

2017. We expected Harmony to suffer from Rmb47 mn in investment loss in 2018 from its

new energy vehicle operation, due to the big-ticket start-off expense in its new Zhengzhou

plant. However, NEV earnings contribution should rebound from 2019 to Rmb161/Rmb331

mn in 2019/2020E.

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 28

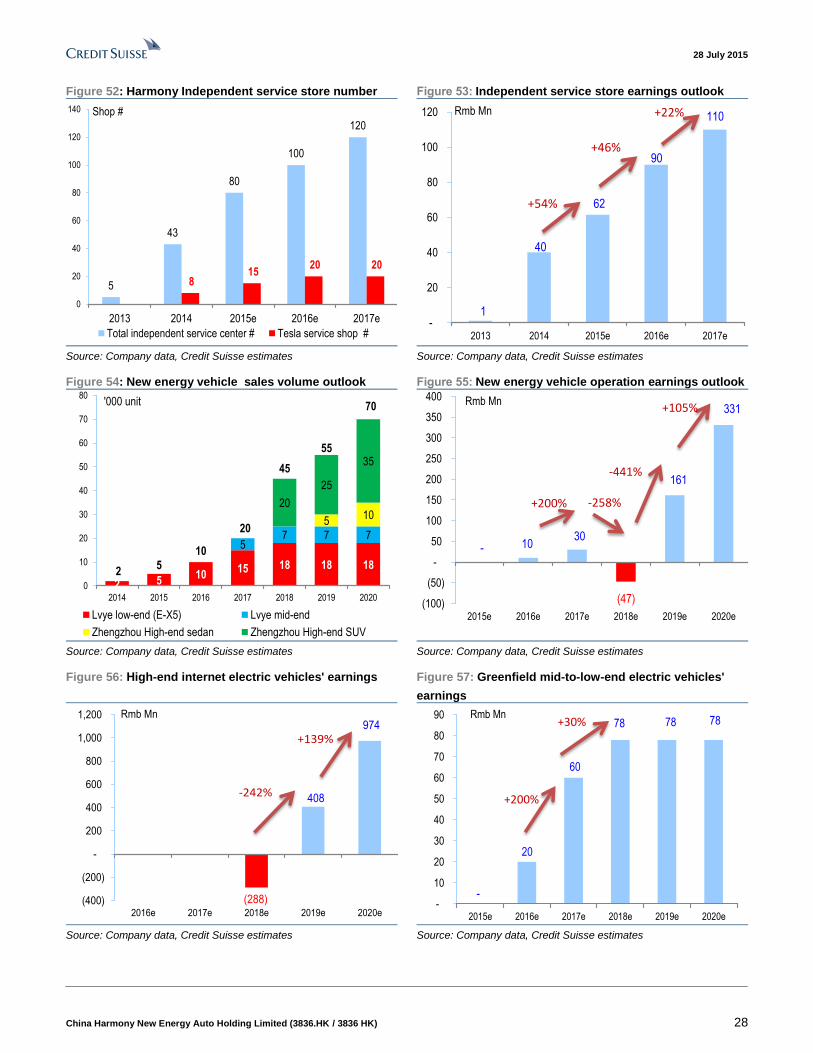

Figure 52: Harmony Independent service store number Figure 53: Independent service store earnings outlook

5

43

80

100

120

8 15

20 20

0

20

40

60

80

100

120

140

2013 2014 2015e 2016e 2017e

Shop #

Total independent service center # Tesla service shop #

1

40

62

90

110

-

20

40

60

80

100

120

2013 2014 2015e 2016e 2017e

Rmb Mn

+54%

+46%

+22%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 54: New energy vehicle sales volume outlook Figure 55: New energy vehicle operation earnings outlook

2 510

15 18 18 18

57 7 7

510

20

25

35

25

10

20

45

55

70

0

10

20

30

40

50

60

70

80

2014 2015 2016 2017 2018 2019 2020

'000 unit

Lvye low-end (E-X5) Lvye mid-end

Zhengzhou High-end sedan Zhengzhou High-end SUV

- 10 30

(47)

161

331

(100)

(50)

-

50

100

150

200

250

300

350

400

2015e 2016e 2017e 2018e 2019e 2020e

Rmb Mn

+200% -258%

-441%

+105%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 56: High-end internet electric vehicles' earnings Figure 57: Greenfield mid-to-low-end electric vehicles'

earnings

(288)

408

974

(400)

(200)

-

200

400

600

800

1,000

1,200

2016e 2017e 2018e 2019e 2020e

Rmb Mn

-242%

+139%

-

20

60

78 78 78

-

10

20

30

40

50

60

70

80

90

2015e 2016e 2017e 2018e 2019e 2020e

Rmb Mn

+200%

+30%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 29

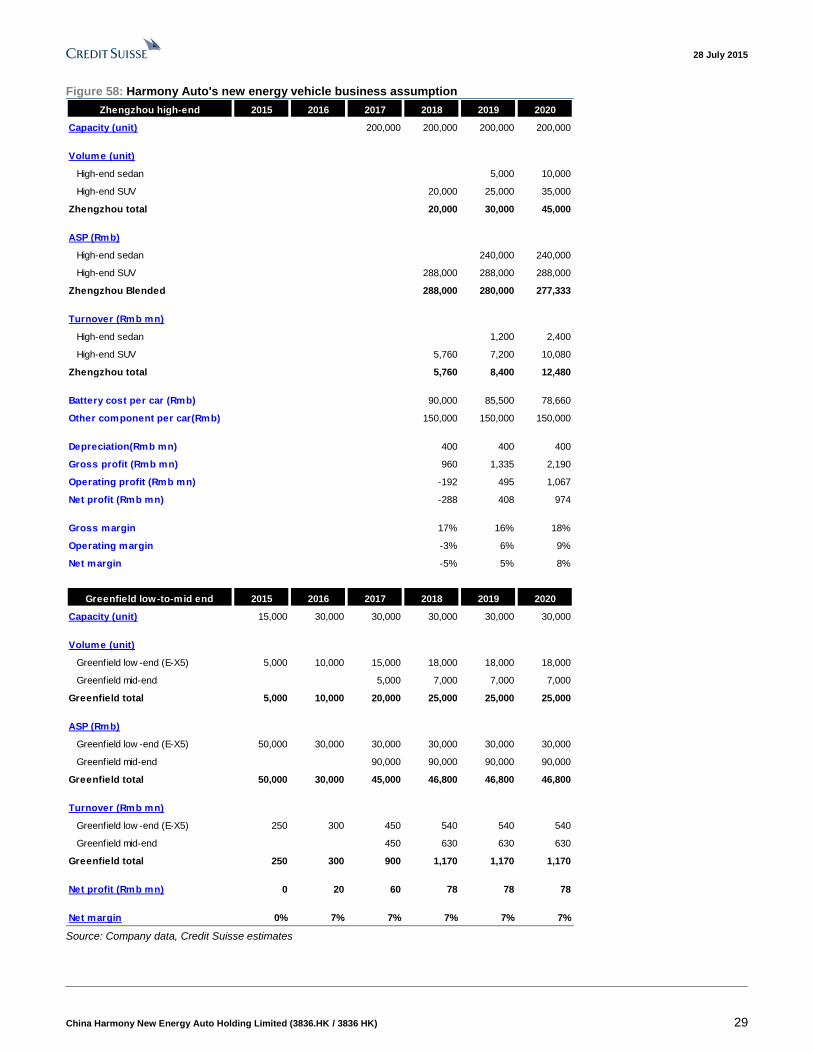

Figure 58: Harmony Auto's new energy vehicle business assumption

Zhengzhou high-end 2015 2016 2017 2018 2019 2020

Capacity (unit) 200,000 200,000 200,000 200,000

Volume (unit)

High-end sedan 5,000 10,000

High-end SUV 20,000 25,000 35,000

Zhengzhou total 20,000 30,000 45,000

ASP (Rmb)

High-end sedan 240,000 240,000

High-end SUV 288,000 288,000 288,000

Zhengzhou Blended 288,000 280,000 277,333

Turnover (Rmb mn)

High-end sedan 1,200 2,400

High-end SUV 5,760 7,200 10,080

Zhengzhou total 5,760 8,400 12,480

Battery cost per car (Rmb) 90,000 85,500 78,660

Other component per car(Rmb) 150,000 150,000 150,000

Depreciation(Rmb mn) 400 400 400

Gross profit (Rmb mn) 960 1,335 2,190

Operating profit (Rmb mn) -192 495 1,067

Net profit (Rmb mn) -288 408 974

Gross margin 17% 16% 18%

Operating margin -3% 6% 9%

Net margin -5% 5% 8%

Greenfield low-to-mid end 2015 2016 2017 2018 2019 2020

Capacity (unit) 15,000 30,000 30,000 30,000 30,000 30,000

Volume (unit)

Greenfield low -end (E-X5) 5,000 10,000 15,000 18,000 18,000 18,000

Greenfield mid-end 5,000 7,000 7,000 7,000

Greenfield total 5,000 10,000 20,000 25,000 25,000 25,000

ASP (Rmb)

Greenfield low -end (E-X5) 50,000 30,000 30,000 30,000 30,000 30,000

Greenfield mid-end 90,000 90,000 90,000 90,000

Greenfield total 50,000 30,000 45,000 46,800 46,800 46,800

Turnover (Rmb mn)

Greenfield low -end (E-X5) 250 300 450 540 540 540

Greenfield mid-end 450 630 630 630

Greenfield total 250 300 900 1,170 1,170 1,170

Net profit (Rmb mn) 0 20 60 78 78 78

Net margin 0% 7% 7% 7% 7% 7% Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 30

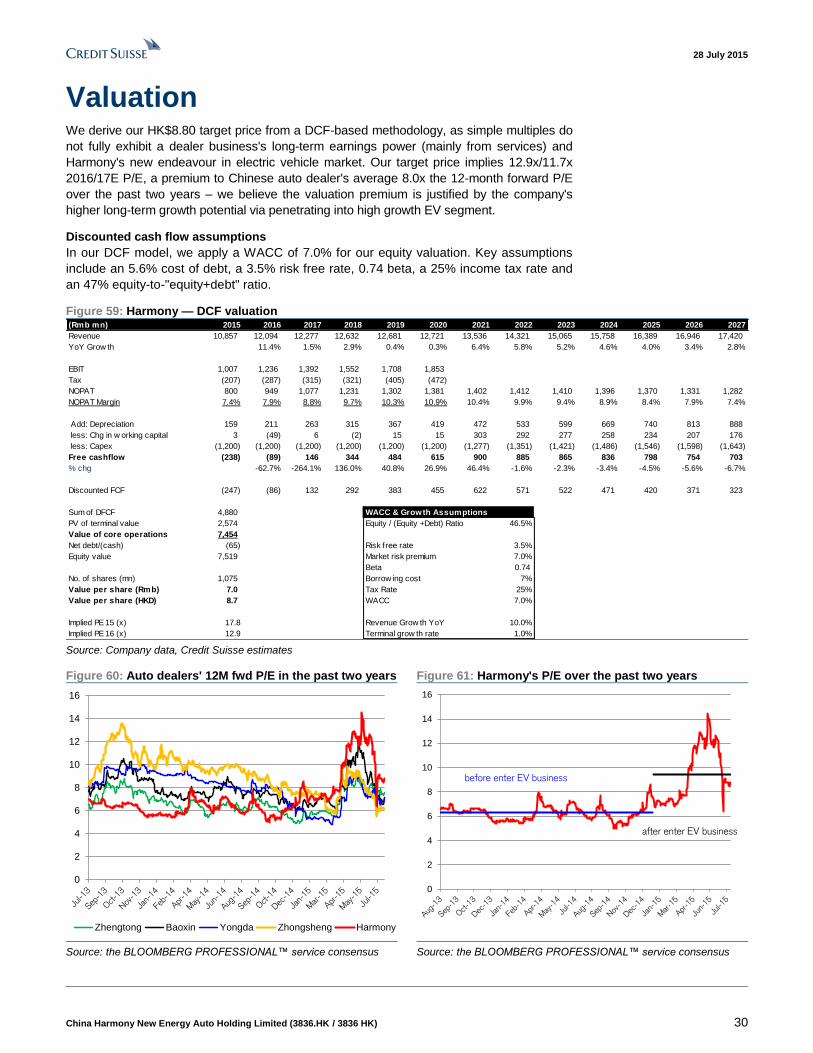

Valuation We derive our HK$8.80 target price from a DCF-based methodology, as simple multiples do

not fully exhibit a dealer business's long-term earnings power (mainly from services) and

Harmony's new endeavour in electric vehicle market. Our target price implies 12.9x/11.7x

2016/17E P/E, a premium to Chinese auto dealer's average 8.0x the 12-month forward P/E

over the past two years – we believe the valuation premium is justified by the company's

higher long-term growth potential via penetrating into high growth EV segment.

Discounted cash flow assumptions

In our DCF model, we apply a WACC of 7.0% for our equity valuation. Key assumptions

include an 5.6% cost of debt, a 3.5% risk free rate, 0.74 beta, a 25% income tax rate and

an 47% equity-to-"equity+debt" ratio.

Figure 59: Harmony — DCF valuation (Rmb mn) 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Revenue 10,857 12,094 12,277 12,632 12,681 12,721 13,536 14,321 15,065 15,758 16,389 16,946 17,420

YoY Grow th 11.4% 1.5% 2.9% 0.4% 0.3% 6.4% 5.8% 5.2% 4.6% 4.0% 3.4% 2.8%

EBIT 1,007 1,236 1,392 1,552 1,708 1,853

Tax (207) (287) (315) (321) (405) (472)

NOPAT 800 949 1,077 1,231 1,302 1,381 1,402 1,412 1,410 1,396 1,370 1,331 1,282

NOPAT Margin 7.4% 7.9% 8.8% 9.7% 10.3% 10.9% 10.4% 9.9% 9.4% 8.9% 8.4% 7.9% 7.4%

Add: Depreciation 159 211 263 315 367 419 472 533 599 669 740 813 888

less: Chg in w orking capital 3 (49) 6 (2) 15 15 303 292 277 258 234 207 176

less: Capex (1,200) (1,200) (1,200) (1,200) (1,200) (1,200) (1,277) (1,351) (1,421) (1,486) (1,546) (1,598) (1,643)

Free cashflow (238) (89) 146 344 484 615 900 885 865 836 798 754 703

% chg -62.7% -264.1% 136.0% 40.8% 26.9% 46.4% -1.6% -2.3% -3.4% -4.5% -5.6% -6.7%

Discounted FCF (247) (86) 132 292 383 455 622 571 522 471 420 371 323

Sum of DFCF 4,880 WACC & Growth Assumptions

PV of terminal value 2,574 Equity / (Equity +Debt) Ratio 46.5%

Value of core operations 7,454

Net debt/(cash) (65) Risk free rate 3.5%

Equity value 7,519 Market risk premium 7.0%

Beta 0.74

No. of shares (mn) 1,075 Borrow ing cost 7%

Value per share (Rmb) 7.0 Tax Rate 25%

Value per share (HKD) 8.7 WACC 7.0%

Implied PE 15 (x) 17.8 Revenue Grow th YoY 10.0%

Implied PE 16 (x) 12.9 Terminal grow th rate 1.0% Source: Company data, Credit Suisse estimates

Figure 60: Auto dealers' 12M fwd P/E in the past two years Figure 61: Harmony's P/E over the past two years

0

2

4

6

8

10

12

14

16

Zhengtong Baoxin Yongda Zhongsheng Harmony

0

2

4

6

8

10

12

14

16

before enter EV business

after enter EV business

Source: the BLOOMBERG PROFESSIONAL™ service consensus Source: the BLOOMBERG PROFESSIONAL™ service consensus

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 31

Risks Downside risks

Luxury car demand slowdown may ignite price wars and hurt dealers’ margins

Historical data shows a clear correlation between the dealer's new car margins and

market-wide luxury dealer per store sales volumes. If luxury demand decelerates due to a

weaker-than-expected macro-economy and more intensified government anti-corruption

campaign, we see downside risk to dealers' new car sales margins. A slowdown in luxury

car sales and fast-expanding dealership number might drag down per dealership sales

and increase pricing pressure.

The company's NEV development plan may be delayed if it fails to receive a

passenger vehicle production license

The company plans to deliver its sample electric vehicles to Ministry of Industry and

Information Technology (MIIT) in 2H15 as one of the process to apply for new energy

vehicle production license. Any delay in sample EV delivery or failure in passenger vehicle

production license application may impose negative impact on company's new energy

vehicle development plan (both mid-end lithium-ion battery EV and high-end EV models).

Intensified competition in independent service market may result in lower margin or

sales growth of company's independent service business

Given the relatively low entry barriers for independent service market, new entrants,

especially those leading dealers group's foraying into the market may impose margin

depression or sales growth slowing down to company's independent service business.

Upside risks

Integrating internet into auto aftersales market could be a new growth engine

By incorporating internet companies' online platforms with dealers' offline networks, auto

aftersales market may find a new growth engine driver to fuel the online-to-offline (O2O)

segment. The company has established a broad strategic cooperation with many domestic

internet platforms, such as Tencent, Tmall.com, JD.com, and could benefit from the rising

O2O trend.

The government may extend the application of new energy vehicle subsidy to lead-

acid battery low-speed electric vehicle

Currently, only lithium-ion battery electric vehicles are eligible for the government's new

energy vehicle subsidies. With the loosening of government's restriction on low speed

electric vehicles, the government may extend subsidy application and grant subsidy to

lead-acid battery electric vehicle. Company's "Green field" subsidiary could be one of the

key beneficiaries.

Company background

China Harmony New Energy Auto is a leading luxury dealership group in China in terms of

the number of 4S stores (45 by end-2014). Its main focus is on luxury and ultra-luxury auto

brands, such as Rolls-Royce, Aston Martin, Ferrari, Maserati, BMW, Land Rover, Jaguar,

Lexus, MINI, Volvo, and Zinoro. Harmony also operated 43 independent after-sales

service stores by end-2014. The company is transforming into a new energy vehicle (NEV)

maker, after its tie-up with Foxconn and Tencent and after acquiring an 87.6% stake in

Greenfield Motor (a NEV maker).

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 32

Figure 62: Company key milestones

Year Key milestones

2015 Acquired 87.57% equity interests in Greenfield Motor Co., Ltd.

Formed a joint venture investment management company, Harmony auto (40%

stake), Foxconn (30% stake) and Tencent (30% stake) to invest in “internet +

intelligent electric vehicle” project

2014 Hon Hai Group acquired 10% stake in Harmony Auto

Entered into a strategic cooperation framework agreement in respect of

“internet + intelligent electric car” with Tencent and Foxconn Technology

Group

Entered into aftersales collaboration with Tesla Motors, Inc. for plate work and paint

spraying

Acquired Shanghai Goocar Pre-owned Automobile Co., Ltd to develop used car

business

2013 Listed in Hong Kong Stock Exchange

Commenced independent aftersales service business

2012 First Aston Martin store in Zhengzhou, Henan

First Rolls Royce store in Xi'an, Shaanxi

First Jaguar Land Rover store in Zhengzhou, Henan

First Maserati & Ferrari store in Suzhou, Jiangsu

2010 First Mini store in Zhengzhou, Henan

2006 First Lexus store in Zhengzhou, Henan

2005 First BMW store in Zhengzhou, Henan

Source: Company data, Credit Suisse estimates

Figure 63: Company structure

Harmony New Energy Auto

(3836.HK)

Foxconn

(Far East)

Ultra luxury / Luxury auto dealership (45) Used car and independent service

8.17%

H-share public

shareholder

44.25%

BMW (20) Independent aftersales

service store (43)

Electric vehicle

Green Field Motor

(87.57%)

Managements

1.21%

Chairman FENG

Changge

43.83%

Mini (3)

Lexus (5)

Volvo (2) Zinoro (1)

Jaguar Land

Rover (1)

Aston Martin (3)

Ferrari /

Maserati (6)

Used car service (1)

Investment management

JV company (stake:

Harmony 40%, Foxconn

30%, Tencent 30%)

High-end “Internet +

Intelligent Electric Vehicle”

To be confirmed

Hon Hai Precision

Industry (2317.TW)

Foxconn Technology

Co., Ltd (2354.TW)

2.54%

29%100%

Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 33

Figure 64: Management profile

Name Position Experience

FENG Changge Chairman

Executive Director

FENG is the founder of the Group and is responsible for the overall strategic and business

direction of the Group.

FENG graduated with a bachelor’s degree in economic law from Central South Institute of Law

(now known as Zhongnan University of Economics and Law) in 1992 and received a master's

degree in law from the same institution in 2001.

From 1992-2002, he served as an assistant judge and a judge in Henan's judicial system.

He started a law firm and was involved in real estate investment since 2002;

He is also the controlling shareholder of Hexie Industrial Group, whose business interests focus

on branded and luxury lifestyle goods and services, including property development, golf courses

and automobile sales.

YU Feng CEO

Executive Director

YU oversees the day-to-day business and management of the Group

YU graduated from Central South Institute of Law (now known as Zhongnan University of

Economics and Law) with a bachelor's degree in law in 1992 and completed a postgraduate

course in criminal law from China University of Political Science and Law in 2000.

From 1992 to 2001, he worked in the courts in Luoshan county of Henan province.

From June 2003 to July 2005 he was with Yuanda Investment.

In July 2005, he joined Henan Zhongdebao, where he was involved in obtaining the dealership

rights for automobile brands such as Land Rover, Lexus, Rolls Royce, and Aston Martin.

YANG Lei COO Executive Director

YANG is responsible for overseeing and managing the Group's automobile business.

YANG graduated in 2002 from Henan University, College of Foreign Languages majoring in

English.

YANG joined the Group in April 2005 in the sales department of our BMW business, during which

he gained extensive sales and marketing experience in the automobile industry.

Qian Yewen CFO Qian has extensive experience in corporate finance and capital markets.

Qian graduated from Peking University with a master degree in economics (majored in finance) in

July 2006 and a bachelor degree in philosophy in June 2004. He is a Chartered Financial Analyst

(CFA).

Prior to joining the Group, Qian served as Vice President of China Investment Banking at

Citigroup Global Market Asia Limited from July 2014 to June 2015. Between September 2007

and July 2014, Qian worked at China International Capital Corporation Limited where his last

position was that of Executive Director of the Investment Banking Department. He also served as

an analyst in the Corporate Finance Department of Cazenove Asia Limited (now known as

Standard Chartered Securities (Hong Kong) Limited) from July 2006 to August 2007.

CUI Ke Vice president

Executive Director

CUI is responsible for overseeing the network development and operation supervision of BMW

and Land Rover brands.

CUI graduated in economics and business management from the Henan Institute of Finance and

Economics (now known as Henan University of Economics and Law) in 2008.

CUI joined the Group in July 2009 as the general manager of Luoyang Yuedebao Automobile

Sales & Services Co., Ltd. He was promoted as a vice president of the company in February

2011. He was appointed as the general manager of Huadebao in February 2011.

MA Lintao Head of administration Executive Director

MA is responsible for the Group’s overall administrative matters and public relationships.

MA graduated from Henan Institute of Finance and Economics (now known as Henan University

of Economics and Law with a bachelor's degree in national economic planning and statistics in

June 1992.

From July 1992 to December 2003 MA worked in China Construction Bank's Henan branch in

various positions.

MA joined the Group in September 2006 as the chairman of Yuanda Lexus, Harmony's wholly-

owned subsidiary.

MA is the wife of FENG Changge.

Source: Company data, Credit Suisse estimates

28 July 2015

China Harmony New Energy Auto Holding Limited (3836.HK / 3836 HK) 34

Companies Mentioned (Price as of 27-Jul-2015)

Alibaba Group Holding Limited (BABA.N, $83.02) BAIC Motor Corporation Limited (1958.HK, HK$6.95) BMW (BMWG.DE, €89.08) Baidu Inc (BIDU.OQ, $206.25) Baoxin Auto Group Ltd (1293.HK, HK$3.7) China Harmony New Energy Auto Holding Limited (3836.HK, HK$6.21, OUTPERFORM[V], TP HK$8.8) China Yongda Automobiles Services Holding limited (3669.HK, HK$4.59) China Zhengtong Auto Services Holding limited (1728.HK, HK$4.14) Foxconn Technology Corp (2354.TW, NT$93.0) General Motors Corp. (GM.N, $31.06) Hon Hai Precision (2317.TW, NT$90.1) SAIC Motor Corp Ltd (600104.SS, Rmb19.2) Sina Corporation (SINA.OQ, $42.51) Tencent Holdings (0700.HK, HK$145.6) Tesla Motors Inc. (TSLA.OQ, $265.41) Weichai Power Co. Ltd (2338.HK, HK$10.7) Zhongsheng Group Holding limited (0881.HK, HK$4.53)

Disclosure Appendix

Important Global Disclosures

I, Bin Wang, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.