Embed Size (px)

Citation preview

CHILEAN EXPERIENCE IN INVESTMENT REGULATION

International Conference “The Private Pension System in the Context of the Development of the Financial Services Market”

UkraineJanuary 2003

Guillermo Arthur E., President of FIAP

Author: Asociación de AFP de Chile

IndexIndex

Chilean Pension System

Investment Scheme

Results

Impact on the Economy

Some lessons from the Chilean experience

Chilean Pension System

Chilean Pension System

OLD SYSTEM AFP SYSTEM

FUNDING Pay-as-you-go Individual Capitalization

MANAGEMENT State Private

BENEFITS Discrimination Uniformity

MEMBERSHIP Inflexibility Individual Freedom

Framework of Laws and Regulations

Supervision Subsidiary

• Minimum Pension

• Insurance Company Bankruptcy

• Minimum Yield

Role of the StateRole of the State

Characteristics of the Pension SystemCharacteristics of the Pension System

Benefits:

Funding:

Mode of Pension Payment: Programmed Withdrawal (AFP)

Life Annuity (Insurance Company)

Temporary Withdrawal with Deferred Life Annuity (AFP and Ins. Company)

- Old-Age Pensions (Legal Age and Early)

- Disability Pension (Total and Partial)

- Survivorship Pension

- Savings: Mandatory 10% Gross Wage

- Disability and Survivorship Insurance

- Recognition Bond

Investment SchemeInvestment Scheme

OBJECTIVES:

- Yield

- Security

RESULTS:

- Better Pensions

- Contribution to Economic Development

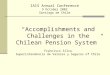

YIELD : Key Factor

94%

167%

55%

0%

50%

100%

150%

200%

3% 5% 7%

Real Annual Yield

Pension / Last Income

Source : The Private Pension System CEP-1988

Assumptions-Male member, married with a wife 5 years younger.- Age when working life begins : 18 years.- He contributes during 85% of his working lifel.-Growth in earnings : 2% per year until the age of 50, and then stable.-He retires at 65 years of age

Effect of Yield on Pensions

Impact of Yield on the Total of the Accumulated Pension Fund

0

2

4

6

8

10

12

14

16

18

20

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01

YIELD

CONTRIBUTIONS

In December 2001, 63% of the accumulated fund was

accounted for by the yield of the investments.

MM$

Note: in order to obtain a pure measurement of the impact of the yield on the accumulated fund, an uninterrupted monthly contribution of $30.000 was taken, with a fixed commission of $534. The real annual yield obtained by the Pension Funds on average during the period was used, deflated by the UF. In the year 2021 (40 years) contributions represent 84% of the fund and contributions only 16%, with n average projected yield of 6% per annum.

How can adequate yield and security be achieved?How can adequate yield and security be achieved?

Investment in Instruments Authorized by the Law: Bonds, Shares, Mortgage-Backed Securities, Fund Shares, Foreign, etc.

Diversification: Instrument class; Issuer (risk, net worth or asset, issue, concentration, liquidity); Group of instruments, etc.

Competition between AFPs.Single Corporate Purpose.Net Worth Separation: AFP and Pension FundRisk Rating Process.Trading in Formal Markets (Primary and Secondary)Physical Custody of 90% of the Securities.Guaranteed Minimum Yield.Conflicts of Interest.Supervision by the Superintendency of AFPs.

Diversification: By InstrumentDiversification: By Instrument

28%

62%

9% 1%

45%

17%

16%

11%

11%

31%

21%11%

9%

2%

16%

10%

1981 1990 2002

State Time Dep. MBS. Corp. Bonds Shares Inv. Funds Abroad

Diversification: By FundDiversification: By Fund

Fund Maximum L. Minimum L.

Fund A 80% 40%

Fund B 60% 25%

Fund C 40% 15%

Fund D 20% 5%

Fund E 0% 0%

Limits on Equities:

Distribution Multifunds (31.XII.2003)Distribution Multifunds (31.XII.2003)

Fund Millions US$ % Equities

Fund A 489,22 72,49%

Fund B 3.936,13 41,34%

Fund C 25.275,25 24,04%

Fund D 3.769,14 14,75%

Fund E 2.045,53 0%

TOTAL 35.515,27 24,25%

SINGLE CORPORATE PURPOSESINGLE CORPORATE PURPOSE

D.L. N° 3.500 Art. N° 23

The AFPs shall be corporations whos “exclusive purpose” shall be the management of Pension Funds...

• Concentrates efforts on achieving the best social security benefits for members

• Facilitates supervision• Minimizes the risk of conflicts of interests

Guaranteed Minimum YieldGuaranteed Minimum Yield

The Law ensures a Minimum Yield

Each AFP is responsible for obtaining it and it is calculated on the basis of the average yield of the P.F. (36)

Calculation: The lower of the following yields ...

Real Average Annualized Yield minus 50%

Real Average Annualized Yield minus 2 % (Funds C,D and E) and 4% (Funds A and B)

Financing of Difference: Yield Fluctuation Reserve, Mandatory Reserve Fund and State as a last resort (Bankruptcy of AFP).

CONFLICTS OF INTERESTCONFLICTS OF INTEREST

Responsibility of the AFP: The AFP is answerable for any harm to the

P.F.; Legal actions, compensation, not revealing investments or confidential

information etc.

Activities forbidden to the AFPs: Using information, charging the

P.F. for services; obtaining unlawful benefits with P. F. operations; etc.

Participation of the AFPs in the election of the

directors of a Corporation: Vote in person, AFP Board decides

votes, not to vote for the controller or related person, not to vote for executives or

directors of the AFP, etc.

The directors of the AFPs: May not take part in investment decisions

in financial firms, give opinions on matters involving conflicts of interest, etc.

Daily information.

a) Balances in current accounts b) Operations carried out (purchases and sales)

c) Mandatory reserve required and held d) Value of the investment portfolio

e) Fund and mand. reserve in custody f) Inflow and outflow of custody from

in the C.S.D. and abroad. the Central Securities Depository.

Periodic Information.– Financial Statements of the Fund.

– Financial Statements of the AFP.

– Quarterly balances.

– Publication of the investment portfolio.

– Etc... $$AFPAFPFundFund

Supervision of the Superintendency of A.F.P.Supervision of the Superintendency of A.F.P.

RESULTS

223 702 1.2741.661

2.3213.041

3.7254.543

5.6147.445

10.537

11.74915.098

18.22519.183

20.31922.229

23.055

28.01730.129

33.134

35.515

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 ´01 ´02

PENSION FUNDS In December of each year in Millions of Dollars as of 31 Dec.2002

PENSION FUNDS In December of each year in Millions of Dollars as of 31 Dec.2002

Evolution in the Number of Contributors ( Thousands )

1.0601.230

1.3601.558

1.774

2.0242.168

2.268

2.6432.487

2.6962.7922.8802.962

3.1213.296

3.1503.2623.197

3.450

0

500

1000

1500

2000

2500

3000

3500

4000

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01 '02Agosto

3.465

12,9

28,5

13,4

5,46,9

15,6

-1,1

16,3

4,46,7

21,2

3,6

12,3

6,5

29,7

3,02

16,218,2

-2,5

3,5 4,73,0

-5

0

5

10

15

20

25

30

35

%

10,3%

4% 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98

99 00 01 02 (*1)

YEAR

( *1) Average accumulated yield July 81- December 02

REAL ANNUAL YIELD OF THE PENSION REAL ANNUAL YIELD OF THE PENSION FUNDSFUNDS

Monthly Social Security Cost Monthly Social Security Cost For an Average Contributor For an Average Contributor (Includes fixed commission and cost paid (Includes fixed commission and cost paid

under the item Disability and Survivorship Insurance)under the item Disability and Survivorship Insurance)

0%

1%

2%

3%

4%

5%

6%

82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01 '02

2,43%

% Commission: 2,26% (Includes the cost of the Insurance)Fixed Commission: $ 538 Average

August

Impact on the EconomyImpact on the Economy

IN THE FISCAL – FINANCIAL ASPECT: The pension reform deactivated the crisis that would have occurred in the future due to demographic changes.

INCREASE OF G.D.P.: 26,5% of the increase in the growth rate of G.D.P. in the period 1985 – 1997, is explained by the pension reform.

DEVELOPMENT OF THE CAPITAL MARKET:Creation of new institutions and financial instruments, accumulation of long-term resources, growth of the stock market, etc.

ECONOMIC EFFECTS OF THE PENSION REFORMECONOMIC EFFECTS OF THE PENSION REFORM Source: Klaus Schmidt-Hebbel, Head of Economic Research

Banco Central de Chile

EFFECTS ON UNEMPLOYMENT

DECREASE IN STRUCTURAL UNEMPLOYMENT - permanent, long-term - BY 2 PERCENTAGE POINTS

EFFECTS ON EMPLOYMENT

• INCREASE IN COVERAGE: 1980 - 51% of the Work Force Active contributors (Old System)

1998 - 65% of the Work Force All Contributors - ( 4% Old System and 61% Present System)

• INCREASE IN FORMAL WORK – Reduces the incentives of informality in Production and Employment

Participation of the Informal Sector in GDP in the 1990s: Chile - 18%; Argentina - 22%, Bolivia - 66%

IMPACT OF THE PRIVATE PENSION SYSTEM IMPACT OF THE PRIVATE PENSION SYSTEM ON THE LABOR MARKET ON THE LABOR MARKET

Fiscal Impact of the ReformFiscal Impact of the Reform

Social Security Deficit(% of GDP)

1982 1999 2037

Pension Payment 2,0% 3,1% 0,2%

Recognition Bonds 0,1% 1,1% 0,0%

Minimum Pensions 0,0% 0,0% 0,6%

TOTAL DEFICIT 2,1% 4,2% 0,8%

The Pension Funds are invested in various

sectores of our Economy

The Pension Funds are invested in various

sectores of our Economy

PENSION FUND INVESTMENT PENSION FUND INVESTMENT

SECTOR MMUS$ % P.F. Electricity 1,305 3.73% Telecommunications 1,025 2.92% Sanitation 90 0.26% Natural Resources 1,119 3.20% Real Estate 4,786 13.63% Infrastructure 613 1.76% Financial 7,573 21.58% Foreign 5,389 15.36% Government 11,572 32.99% Various Industries 1,613 7.64%

TOTAL 35,085 100%

Some lessons from the Chilean experience

Advantages of the individual capitalization system compared with the PAYG systems.

Private, competitive management.

Freedom of members: Choice of AFP and freedom to change

Amount contributed (above the minimum)

Age and mode of retirement

Type of Fund

Ensure professional and technical supervision.

(Continued)

Diversified investments. Without minimum limits.

Regulate the capital market.

Carry out the reform without waiting for all the conditions to be fulfilled that are theoretically necessary for its success.

Take the discussion from the political to the technical plane.

Some lessons from the Chilean experience