Embed Size (px)

Citation preview

Chicago Board of TradeInterest Rate Products Market Development

2003 Taipei Interest Rate Futures Conference

November 20 - 21, 2003

CBOT Interest Rate Product Line

• Family of Curves in the Interest Rate Complex– Treasury– Credit Curves

• LIBOR (A to AA)• Agencies (AAA)

– Tax Exempt (AAA)– Federal Funds

Major Trends

• Late 1970s ~ 1989– Inflation Peaks and then Declines– The Era of Deficit Spending

• 1990 ~ 2000– From Record Deficits to Record Surplus– Series of Market Crises:

Asia/Russia/LTCM• 2000 ~

– The LIBOR Era– The Electronic Trading Era

Major Factors Affecting Growth

• Growing Debt Level and Supply of Treasury Securities. Growth in cash market trading

• Benefits of Futures:– Markets are Open and Transparent– Standardized Products– One Centralized Marketplace

• Electronic Trading– Speed of Execution– Global Distribution– Cost Efficiencies

Historical Timeline of the CBOT Interest Rate Product Line

• 1975 – GNMA Futures (Government National Mortgage Association)

• 1977 – U.S. Treasury Bond Futures. • 1979 – “Saturday Night Special” FED

changes policy to target the money supply.

• 1982 – Options on U.S. T-Bond futures; 10-Year U.S. Treasury Note futures.

• 1983 – US budget deficit hits record $200 bn.

Historical Timeline of the CBOT Interest Rate Product Line

• 1984 - Options on 10-year T-notes• 1985 – Municipal Bond futures • 1986 - Oil collapses to $10. 30 year T-

Bond yield drops to 7.11 %. “Street” caught in a giant squeeze in cash 9 ¼ T- Bonds of 2016 – basis explodes to 350/32nds.

• 1987 - Open Outcry “Evening Session”

• 1987 - October 19 stock market crash – Dow falls 22 % - huge bond market rally.

Historical Timeline of the CBOT Interest Rate Product Line

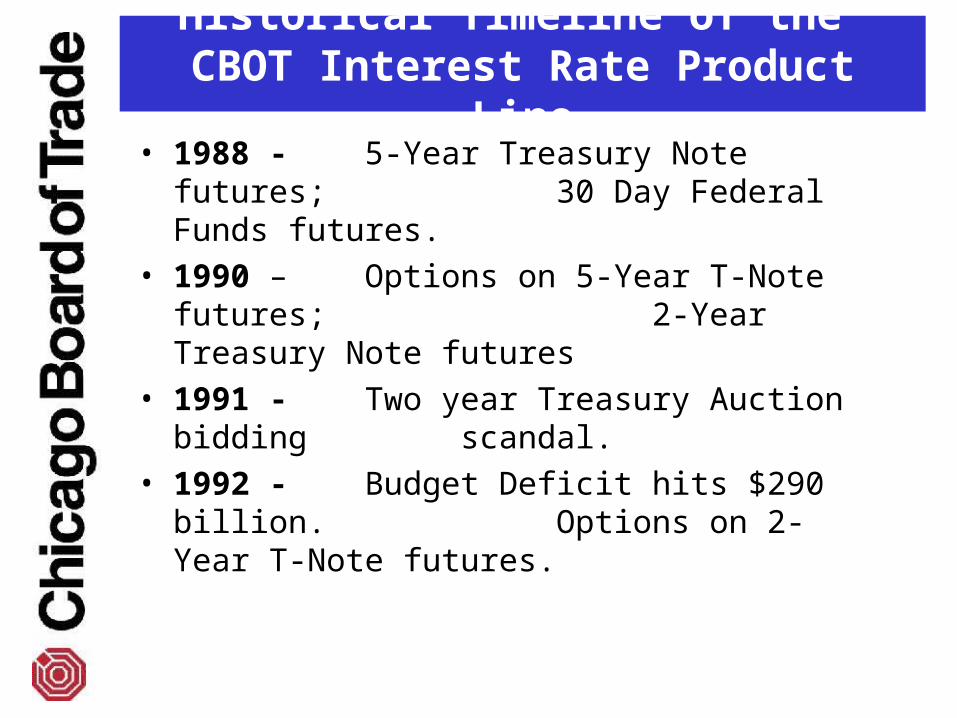

• 1988 - 5-Year Treasury Note futures; 30 Day Federal Funds

futures. • 1990 – Options on 5-Year T-Note

futures; 2-Year Treasury Note futures

• 1991 - Two year Treasury Auction bidding scandal.

• 1992 - Budget Deficit hits $290 billion. Options on 2-Year T-Note

futures.

Historical Timeline of the CBOT Interest Rate Product Line

• 1994 - Project A Afternoon Session• 1995 - Project A Night Session• 1997 - Asian currency crisis. • 1998 - Russia debt default. Long Term

Capital Management collapse. Credit spreads widen, treasury cross hedges lose some effectiveness.

• 1998 - Start of 4 years of budget surpluses.

• 2000 – 10-Year & 5-Year Agency Debt futures & options.

• 2000 - a/c/e platform replaces Project A.

Historical Timeline of the CBOT Interest Rate Product Line

• 2000 - Record budget surplus of $236 bn. FASB 133 – Hedge Accounting.

• 2001 - Treasury ends of 30-year bond. • 2001 – 10-Year & 5-Year Interest Rate

Swap futures and options. • 2001 - Electronic trading in treasury

futures at 25 % of total. • 2002 - Electronic trading in treasury

futures at 50% of total. • 2003 - Electronic trading in treasury

futures surpasses 75% of total volume.

• 2003 - Begin e-cbot Liffe Connect platform.

CBOT Product Lines by Share of Volume

82%

3%

15%

Interest Rates Equity index Commodity

Growth of U.S. Debt US Treasury Debt - US$ Billions

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Mar

-92

Sep

-92

Mar

-93

Sep

-93

Mar

-94

Sep

-94

Mar

-95

Sep

-95

Mar

-96

Sep

-96

Mar

-97

Sep

-97

Mar

-98

Sep

-98

Mar

-99

Sep

-99

Mar

-00

Sep

-00

Mar

-01

Sep

-01

Mar

-02

Sep

-02

Mar

-03

Total Treasury Debt

FED & US Govt Held

Foreign Held

Growth of U.S. Debt

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ma

r-9

2

Se

p-9

2

Ma

r-9

3

Se

p-9

3

Ma

r-9

4

Se

p-9

4

Ma

r-9

5

Se

p-9

5

Ma

r-9

6

Se

p-9

6

Ma

r-9

7

Se

p-9

7

Ma

r-9

8

Se

p-9

8

Ma

r-9

9

Se

p-9

9

Ma

r-0

0

Se

p-0

0

Ma

r-0

1

Se

p-0

1

Ma

r-0

2

Se

p-0

2

Ma

r-0

3

Se

p-0

3

Ma

r-0

4

Foreign Held as Percent of Total Privately Held

US FED & Govt Held as a Percent of Total Debt

CBOT Treasury Futures Average Daily Volume - Contracts

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

Jan-

80

Jan-

82

Jan-

84

Jan-

86

Jan-

88

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

2yr

5yr

10yr

30yr

CBOT Treasury Options Average Daily Volume - Contracts

0

100,000

200,000

300,000

400,000

500,000

Jan-

80

Jan-

81

Jan-

82

Jan-

83

Jan-

84

Jan-

85

Jan-

86

Jan-

87

Jan-

88

Jan-

89

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

5yr

10yr

30yr

CBOT Treasury Futures vs. Cash

$Dollar Volume Comparisons Average Daily $volume June ~ Sept 2003In US$ Millions source: NY Fed , CBOT

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2y 5y 10y 30y

Futures Cash

CBOT Treasury Futures Electronic Platform Share of Volume

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1998 1999 2000 2001 2002 2003

CBOT Credit & LIBOR Futures Average Daily Volume

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Oct

-88

Oct

-89

Oct

-90

Oct

-91

Oct

-92

Oct

-93

Oct

-94

Oct

-95

Oct

-96

Oct

-97

Oct

-98

Oct

-99

Oct

-00

Oct

-01

Oct

-02

Oct

-03

10 Yr Muni

10 Yr Agency

10 Yr Swap

CBOT 30 Day Federal Funds Futures & Options - Average Daily Volume

0

20,000

40,000

60,000

80,000

100,000

120,000

Oc

t-8

8

Oc

t-8

9

Oc

t-9

0

Oc

t-9

1

Oc

t-9

2

Oc

t-9

3

Oc

t-9

4

Oc

t-9

5

Oc

t-9

6

Oc

t-9

7

Oc

t-9

8

Oc

t-9

9

Oc

t-0

0

Oc

t-0

1

Oc

t-0

2

Oc

t-0

3

Fed Funds Options

Fed Funds Futures

• pension funds• bankers• cash managers• governments• insurance

companies• mortgage bankers• thrifts• underwriters

• bond dealers• corporate treasurers• hedge fund

managers• investment bankers• mutual fund mangers• portfolio mangers• trust fund managers• arbitrage firms

Market Participants

CME/CBOT Common Clearing Link

• The Common Clearing Link (CCL) agreement was signed in April 2003 by the CBOT and the CME.

• The CCL will follow the same timetable as the switch to the new e-CBOT Powered by Liffe Connect®. When a product begins trading on the new e-CBOT platform, it will also begin clearing through the new CCL.

• The CCL will clear approximately 85 % of all U.S. futures and futures options.

CME/CBOT Common Clearing Link

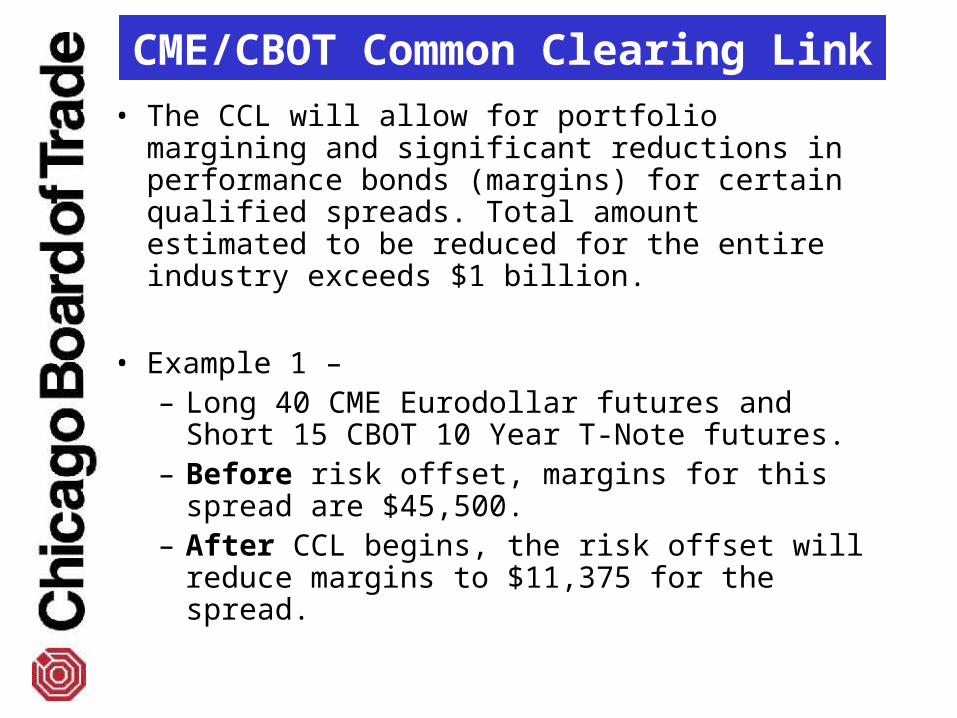

• The CCL will allow for portfolio margining and significant reductions in performance bonds (margins) for certain qualified spreads. Total amount estimated to be reduced for the entire industry exceeds $1 billion.

• Example 1 – – Long 40 CME Eurodollar futures and Short

15 CBOT 10 Year T-Note futures. – Before risk offset, margins for this spread

are $45,500. – After CCL begins, the risk offset will reduce

margins to $11,375 for the spread.

• State of the art electronic platform. – Host + Gateway + Network

• Over 110 Firms in 181 locations are participating in the migration to the new e-CBOT platform.

• Increased built-in functionality – – 32 option spread strategies – 6 futures strategies.

• Multiple trade matching algorithms: Price-Time and Pro-Rata.

e-CBOT Powered by LIFFE CONNECT®

e-CBOT Powered by LIFFE CONNECT®

• Timetable for transition– November 24, 2003

• Interest Rate Swap products• Federal Funds products• Municipal bond products• Dow Equity Index products

– January 2, 2004• Treasury complex products• Agency complex products• Agricultural complex products