Embed Size (px)

Citation preview

f i n a n c i n g t h e p l a c e s w h e r e p e o p l e l i v e a n d w o r k

c o m m u n i t y r e p o r t 2 0 0 4 c o l o r a d o h o u s i n g a n d f i n a n c e a u t h o r i t y

celebrating 30 years of financing the placeswhere people live and work

By now, you have seen the pearls on the front cover of ColoradoHousing and Finance Authority’s (CHFA’s) 2004 community report.CHFA chose the pearl as the theme for this year’s report in partbecause it represents the traditional 30th anniversary gift. The pri-mary reason, however, was because it symbolizes CHFA’s gem-stones… its customers and partners.

The pearl, formed inside a shellfish, results from an irritant enteringthe shellfish, causing a reaction. The shellfish isolates the matterand coats it with layer after layer of mother of pearl. It is a very longprocess, but the end result is a thing of great beauty and greatvalue.

Like the pearl, CHFA was created in 1973 by the ColoradoLegislature due to a bothersome problem in the state… a lack ofaffordable housing for low and moderate income families. In 1982,when the need for additional business capital was also identified,CHFA’s mission expanded to include financing of businesses.

Today CHFA, a valuable Colorado entity, stands as a leader in theaffordable housing industry through its financing of single familymortgages and multi-family apartment units for low and moderateincome residents. It also develops and creates growth opportuni-ties for small businesses in Colorado. In 2004, CHFA prioritized cus-tomer service and efficiency. The results are described in the follow-ing pages. Some highlights:

> Small Business portfolio exceeded $100 Million in assetsoutstanding

> CHFA was recognized as one of the top five best Coloradocompanies for working families

> $131.8 million in Single Family mortgage prepayments wererecycled

Since CHFA opened in 1974, CHFA’s commitment to its mission hasnever wavered. Just like the pearl, the result is a thing of greatvalue… financing the places where people live and work inColorado.

This community report chronicles some of our major initiatives in2004 and successes over the years. It is presented as a public serv-ice to all interested persons. We hope you find it engaging anduseful.

from theboard chairand ceo

M. Michael CookeBoard Chair

Roy AlexanderChief Executive Officer

Merced de las Animas - Durango, Colorado

meeting our mission

CHFA’s mission is to:

> Increase the availability of affordable, decent, andaccessible homes for lower income Coloradans

> Strengthen the state’s economy by providing financialassistance to businesses

CHFA, an independent and self sustaining financial enterprise,maintains an A1/A+ credit rating with Moody’s and Standard &Poor’s. Its bonds are rated “A” through “AAA”. CHFA is not astate agency, nor does it utilize taxpayer dollars for programadministration. Rather, CHFA sells bonds in the capital marketsand uses the proceeds for program funds.

CHFA’s has built its reputation on integrity, expertise, fiscalresponsibility and dedication to its mission. Staff continues tomake service a top priority through its focus on customers, whorange from families just starting out in a modest apartment orhouse, to developers of affordable housing, to bankers, to smallbusiness owners and to nonprofits. The CHFA team pledges topursue greater efficiency and effectiveness so that it may betterserve Colorado.

mission

Reyna and Martin Chacón

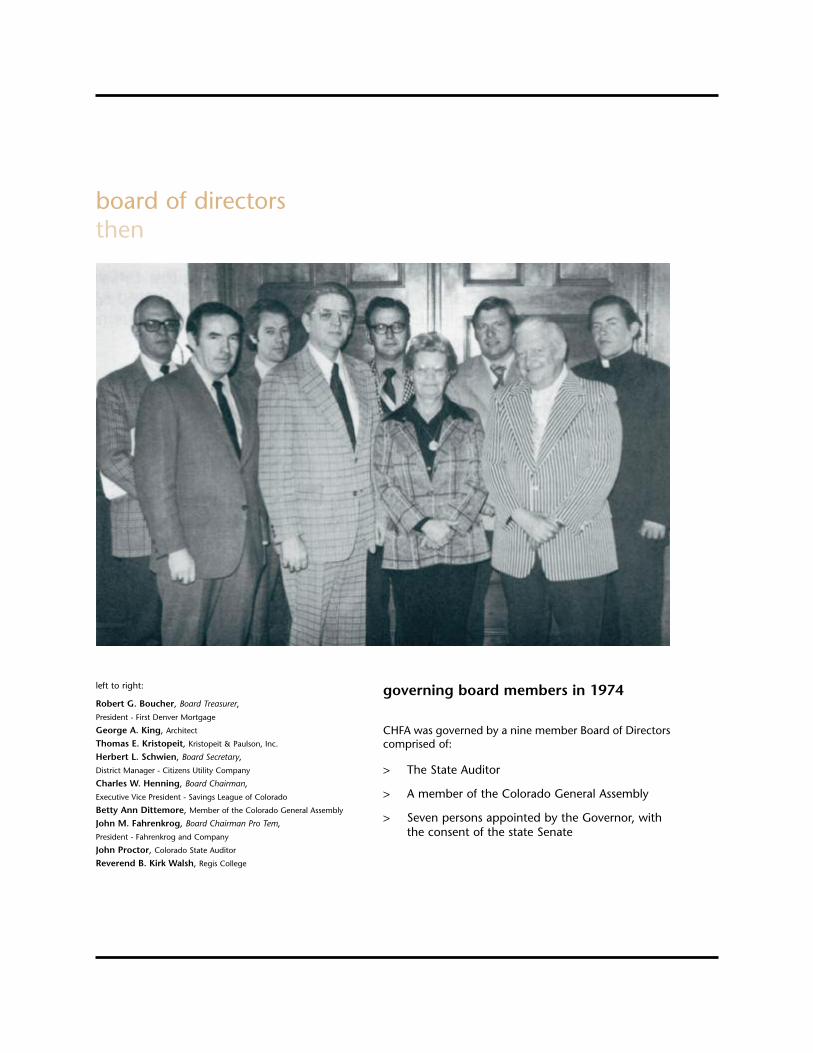

governing board members in 1974

CHFA was governed by a nine member Board of Directorscomprised of:

> The State Auditor

> A member of the Colorado General Assembly

> Seven persons appointed by the Governor, withthe consent of the state Senate

board of directorsthen

left to right:

Robert G. Boucher, Board Treasurer,President - First Denver Mortgage

George A. King, Architect

Thomas E. Kristopeit, Kristopeit & Paulson, Inc.

Herbert L. Schwien, Board Secretary,District Manager - Citizens Utility Company

Charles W. Henning, Board Chairman,Executive Vice President - Savings League of Colorado

Betty Ann Dittemore, Member of the Colorado General Assembly

John M. Fahrenkrog, Board Chairman Pro Tem,President - Fahrenkrog and Company

John Proctor, Colorado State Auditor

Reverend B. Kirk Walsh, Regis College

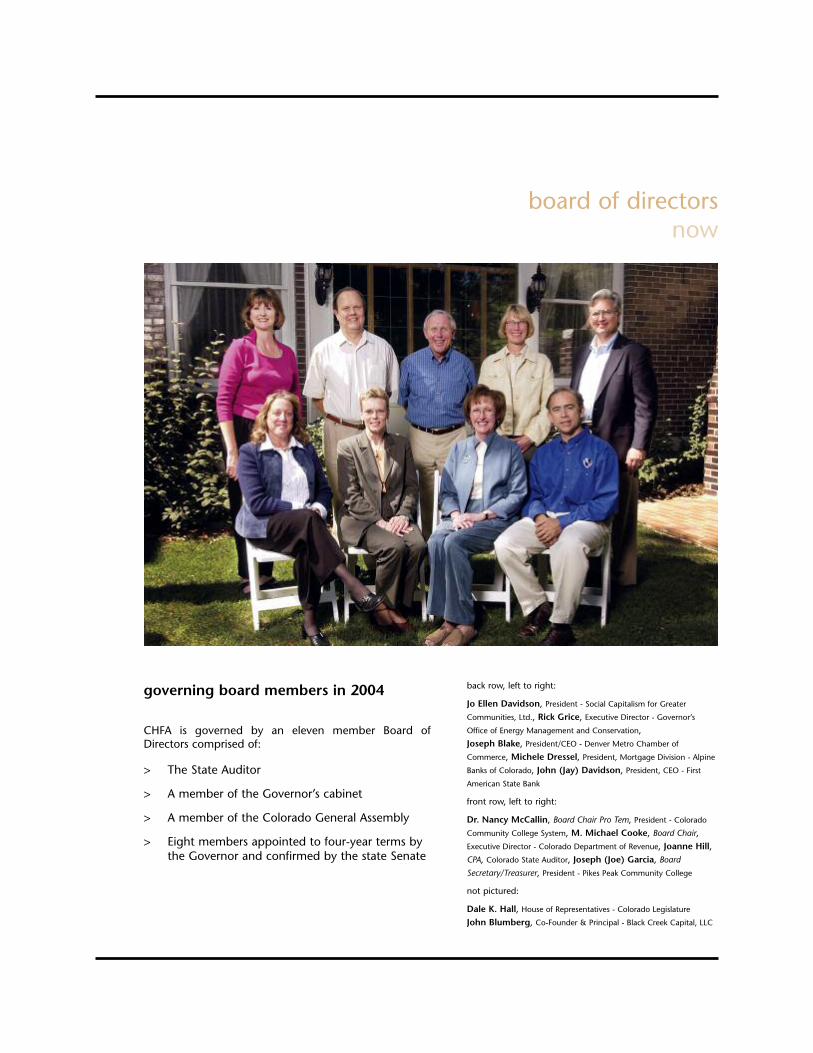

governing board members in 2004

CHFA is governed by an eleven member Board ofDirectors comprised of:

> The State Auditor

> A member of the Governor’s cabinet

> A member of the Colorado General Assembly

> Eight members appointed to four-year terms bythe Governor and confirmed by the state Senate

board of directorsnow

back row, left to right:

Jo Ellen Davidson, President - Social Capitalism for Greater

Communities, Ltd., Rick Grice, Executive Director - Governor’s

Office of Energy Management and Conservation,Joseph Blake, President/CEO - Denver Metro Chamber of

Commerce, Michele Dressel, President, Mortgage Division - Alpine

Banks of Colorado, John (Jay) Davidson, President, CEO - First

American State Bank

front row, left to right:

Dr. Nancy McCallin, Board Chair Pro Tem, President - Colorado

Community College System, M. Michael Cooke, Board Chair,Executive Director - Colorado Department of Revenue, Joanne Hill,CPA, Colorado State Auditor, Joseph (Joe) Garcia, Board

Secretary/Treasurer, President - Pikes Peak Community College

not pictured:

Dale K. Hall, House of Representatives - Colorado Legislature

John Blumberg, Co-Founder & Principal - Black Creek Capital, LLC

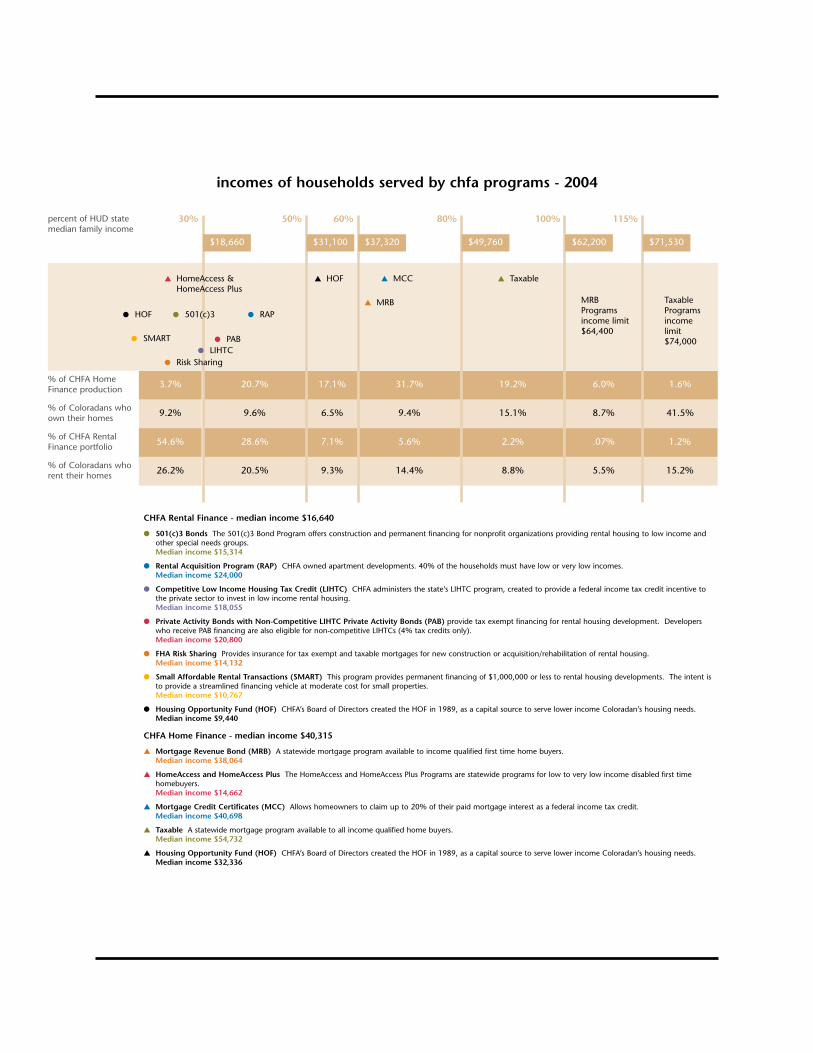

Each year, CHFA staff examines the characteristics of peopleserved by CHFA’s rental housing and homeownership programsto understand who benefits from its housing production. Thechart on the following page is from the 2004 report and showsthe percentage of households benefiting from CHFA programs,compared with the total percentage of households in Coloradoby income group. The data show CHFA’s programs reach work-ing households, including teachers, firefighters and construc-tion workers, as well as households receiving federal assistance.

In the homeownership programs, a high number of loansserved households with incomes between 30% and 60% of themedian.

In the rental housing programs, the data show 90% of CHFAserved households fall well below 50% of median income, andmany reach down to households below 30% of median.

homeownership demographics at a glance

> Median income of CHFA single family borrowers was$40,315 ($19.38 per hour) or 35% below the HUD statemedian income of $62,200

> 22% of homeownership loans were made to minorities

> 12% of homeownership loans were made in rural Colorado

rental housing demographics at a glance

> Median income of renter families in CHFA developments was$16,640, ($8.00 per hour) or 73% below the HUD statemedian family income of $62,200

> 10% of all CHFA rental units served disabled households

> The percentage of single parents benefiting from CHFA’srental programs was 24%, surpassing the single parentpopulation for Colorado which was 8%

demographics

CHFA Rental Finance - median income $16,640

l 501(c)3 Bonds The 501(c)3 Bond Program offers construction and permanent financing for nonprofit organizations providing rental housing to low income andother special needs groups.Median income $15,314

l Rental Acquisition Program (RAP) CHFA owned apartment developments. 40% of the households must have low or very low incomes.Median income $24,000

l Competitive Low Income Housing Tax Credit (LIHTC) CHFA administers the state’s LIHTC program, created to provide a federal income tax credit incentive tothe private sector to invest in low income rental housing.Median income $18,055

l Private Activity Bonds with Non-Competitive LIHTC Private Activity Bonds (PAB) provide tax exempt financing for rental housing development. Developerswho receive PAB financing are also eligible for non-competitive LIHTCs (4% tax credits only).Median income $20,800

l FHA Risk Sharing Provides insurance for tax exempt and taxable mortgages for new construction or acquisition/rehabilitation of rental housing.Median income $14,132

l Small Affordable Rental Transactions (SMART) This program provides permanent financing of $1,000,000 or less to rental housing developments. The intent isto provide a streamlined financing vehicle at moderate cost for small properties.Median income $10,767

l Housing Opportunity Fund (HOF) CHFA’s Board of Directors created the HOF in 1989, as a capital source to serve lower income Coloradan’s housing needs.Median income $9,440

CHFA Home Finance - median income $40,315

s Mortgage Revenue Bond (MRB) A statewide mortgage program available to income qualified first time home buyers.Median income $38,064

s HomeAccess and HomeAccess Plus The HomeAccess and HomeAccess Plus Programs are statewide programs for low to very low income disabled first timehomebuyers.Median income $14,662

s Mortgage Credit Certificates (MCC) Allows homeowners to claim up to 20% of their paid mortgage interest as a federal income tax credit.Median income $40,698

s Taxable A statewide mortgage program available to all income qualified home buyers.Median income $54,732

s Housing Opportunity Fund (HOF) CHFA’s Board of Directors created the HOF in 1989, as a capital source to serve lower income Coloradan’s housing needs.Median income $32,336

9.2% 9.6% 6.5% 9.4% 15.1% 8.7% 41.5%

3.7% 20.7% 17.1% 31.7% 19.2% 6.0%

26.2% 20.5% 9.3% 14.4% 8.8% 5.5% 15.2%

54.6% 28.6% 7.1% 5.6% 2.2% .07% 1.2%

1.6%

30% 50% 60% 80% 100% 115%

$71,530$62,200$49,760$37,320$31,100$18,660

percent of HUD statemedian family income

s HomeAccess &HomeAccess Plus

s HOF s MCC s Taxable

MRBProgramsincome limit$64,400

TaxableProgramsincomelimit$74,000

% of CHFA HomeFinance production

% of Coloradans whoown their homes

% of CHFA RentalFinance portfolio

% of Coloradans whorent their homes

incomes of households served by chfa programs - 2004

s MRBl HOF l 501(c)3 l RAP

l LIHTCl PAB

l Risk Sharing

l SMART

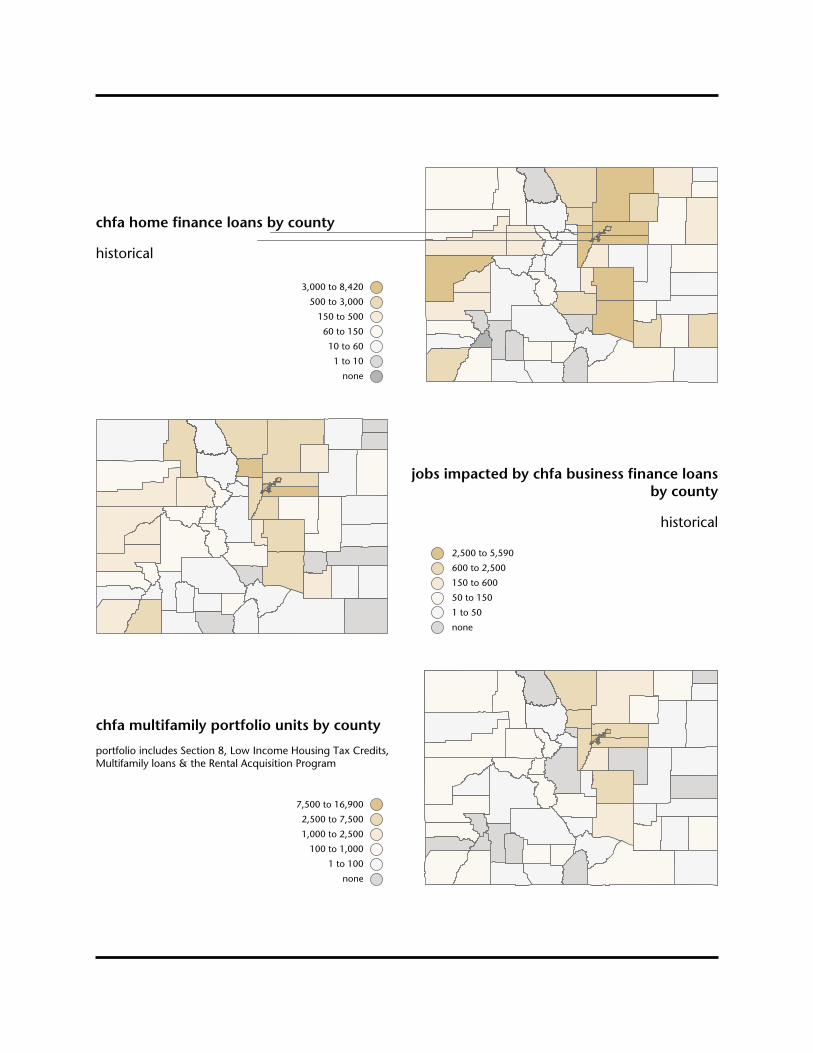

chfa home finance loans by county

historical

7,500 to 16,900

2,500 to 7,500

1,000 to 2,500

100 to 1,000

1 to 100

none

2,500 to 5,590

600 to 2,500

150 to 600

50 to 150

1 to 50

none

3,000 to 8,420

500 to 3,000

150 to 500

60 to 150

10 to 60

1 to 10

none

jobs impacted by chfa business finance loansby county

historical

chfa multifamily portfolio units by county

portfolio includes Section 8, Low Income Housing Tax Credits,Multifamily loans & the Rental Acquisition Program

Imprints Wholesale - Denver, Colorado

In 2003, CHFA combined its Loan Servicing Department with itsHome Finance Division. This change improved efficiency andhelped streamline processes, ultimately benefiting our singlefamily borrowers. In the summer of 2004, CHFA conducted asurvey of all home finance borrowers in our single family port-folio to capture feedback for areas of focus. The survey was sentto over 11,000 households, asking questions about CHFA’shomeownership programs and loan servicing options. CHFAreceived over 2,200 responses. The majority of the responseswere from borrowers receiving an MRB First Step loan.

CHFA’s MRB First Step Program, a statewide first mortgage pro-gram available to income qualified first time homebuyers, offersbelow market interest rates, as well as an optional second mort-gage to assist with down payment and closing costs. Thisoptional 30 year second mortgage loan is available for up to 3%of the first mortgage loan amount at an interest rate of 0%. Nopayment is due on the second mortgage until the first mort-gage is paid in full, the property is sold, or the property nolonger serves as the homeowner’s primary residence.

Survey responses indicated:

> 98% of respondents said homeownership gave them asense of pride

> 97% of those with children said they felt better abouttheir children’s future as a result of homeownership

> 91% said they felt better or much better about theirquality of life

One quote in particular captures the feelings of customersregarding their CHFA loan:

“CHFA allowed me, as a single working woman, to become a firsttime homebuyer. I can’t tell you what a sense of pride I feel everytime I come home. I love being able to work in my own yard. I cantake care of things on my own. I don’t depend on anyone to helpme. That is a great feeling. Thank you CHFA.”

In 2004, CHFA assisted 3,198 families in purchasing homesequaling $437 million dollars. Since its inception, cumulativehome ownership production is $6,375,417,874 serving 55,146families.

stability

Robert and Christina Aldridge, and theirchildren Brylee and Blakely of Arapahoe,

Colorado purchased their first homethrough CHFA’s MRB First Step Program

The CHFA Servicing Team recognizes the enormous role they playin helping borrowers succeed. With each loan, CHFA makes a com-mitted partnership with borrowers, which is why the team makesservice its number one priority. In 2004, the Servicing Staff serviceda portfolio of 17,564 single family loans, 300 business finance loansand 352 rental finance loans.

The survey of single family borrowers conducted in 2004 was cru-cial in helping staff understand possible areas for improvement anddetermine what new products and/or services customers would liketo see from CHFA in the future.

Using the survey responses, the CHFA Servicing Team developed aset of customer service best practices. For example:

> CHFA provides cheerful encouragement to borrowersexperiencing hard times, to give them hope things willimprove.

> CHFA’s customer service center, located in CHFA’s lobby,allows borrowers to talk face to face with customer servicerepresentatives. Not a lot of mortgage companies offer thisservice to their borrowers. This makes CHFA unique andshows its dedication to customer service.

The following letter from customer Theresa Y. Godinez demon-strates CHFA’s commitment and dedication to service:

Dear Ms. Harkin,

I am writing this letter to offer my thanks and to let you andyour staff know that the work you do in assisting home ownersdoes not go unnoticed. I was blessed by having CHFA help mebuy my first home about seven years ago. During my youth, myfamily moved quite frequently from here to there. My parentswere never in a position to purchase a home. Therefore, to thinkthat I might be able to was a far-fetched dream that seemedcompletely out of reach, until a friend told me about CHFA.

Recently, I had to refinance which, as you know, means I will nolonger be sending my coupon to CHFA.

I was quite sad that my relationship with your agency has cometo an end; however, I wanted to send my deepest thanks foryour careful and courteous assistance through the years. I justwanted you to know that your company helped to change mylife for the better. I will always be eternally grateful.

Best regards,Theresa Y. Godinez

dependability

Borrowers who completed the survey becameeligible for a grand prize drawing of one

complimentary month’s mortgageKristy and Ernest Hale, along with their children,

Cassie and Nathan, were the lucky winners

CHFA assumed a leadership position in the business financemarketplace in 1982, when the Colorado General Assemblyamended CHFA’s enabling legislation, permitting CHFA to uti-lize bond proceeds to finance small and moderate sized busi-nesses in Colorado. CHFA created the Business Finance Team todevelop and administer various lending programs targeted tomeet the needs of diverse businesses.

Today, the Business Finance Team is the state’s leading resourcepartner in the area of economic development finance. CHFAprograms offer long term, fixed rate financing to all regions ofthe state, for small and medium sized businesses, manufactur-ers and most recently, nonprofit organizations.

Nonprofit organizations face tremendous difficulty accessingfunds due to often unpredictable cash flow situations. CHFA’sprograms offer more flexible underwriting standards that workbetter for nonprofits.

Children’s ARK is a nonprofit that benefited from CHFA financ-ing. A residential treatment center for youths between the agesof nine and 18, Children’s ARK is located approximately 25miles west of Colorado Springs. In the early 90s, Eric and JeanAnn West sold their home in California to follow their calling toserve kids suffering from family, emotional and physical prob-lems. Children’s ARK provides a home, educational opportuni-ties and emotional support from Eric, Jean Ann and their dedi-cated staff. They provide these services in a quiet, peaceful set-ting, aimed at pointing the troubled youths at Children’s ARK inthe right direction.

In 2004, Eric and Jean Ann realized they needed to expand theirfacility into something more manageable. Being a nonprofit,they were not sure where to go for the necessary funding.“When we heard about the CHFA nonprofit loan program, weknew our prayers had been answered,” Eric said. CHFA built afinancing package for Children’s ARK that allowed them to savesubstantially. “I had agreed to what I considered a fair interestrate,” West said. “When I opened up my contract, I saw that therate quoted on the contract was considerably lower than the com-mitment letter’s loan rate. I struggled a bit with my conscience anddecided to do the right thing and call CHFA to tell them of the mis-take. To my surprise and delight, I was told there was no error. Myloan officer had worked with CHFA’s finance department to comeup with a rate a struggling nonprofit could handle.”

community support

Children’s ARK

timeline

1989

1988

1987

1986

1985

1984

1983

1982

1981

1980

1979

1978

1977

1976

1975

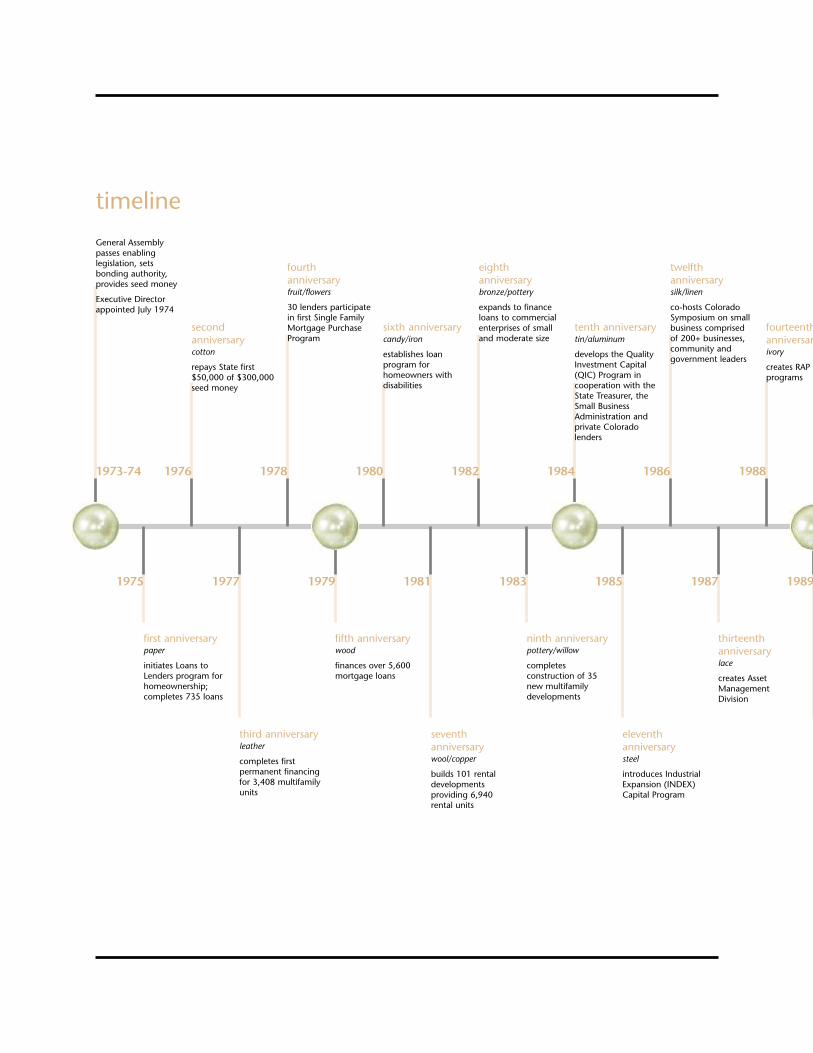

1973-74

General Assemblypasses enablinglegislation, setsbonding authority,provides seed money

Executive Directorappointed July 1974

secondanniversarycotton

repays State first$50,000 of $300,000seed money

first anniversarypaper

initiates Loans toLenders program forhomeownership;completes 735 loans

fourthanniversaryfruit/flowers

30 lenders participatein first Single FamilyMortgage PurchaseProgram

sixth anniversarycandy/iron

establishes loanprogram forhomeowners withdisabilities

eighthanniversarybronze/pottery

expands to financeloans to commercialenterprises of smalland moderate size

tenth anniversarytin/aluminum

develops the QualityInvestment Capital(QIC) Program incooperation with theState Treasurer, theSmall BusinessAdministration andprivate Coloradolenders

twelfthanniversarysilk/linen

co-hosts ColoradoSymposium on smallbusiness comprisedof 200+ businesses,community andgovernment leaders

fourteenthanniversaryivory

creates RAP and SSPprograms

third anniversaryleather

completes firstpermanent financingfor 3,408 multifamilyunits

fifth anniversarywood

finances over 5,600mortgage loans

seventhanniversarywool/copper

builds 101 rentaldevelopmentsproviding 6,940rental units

ninth anniversarypottery/willow

completesconstruction of 35new multifamilydevelopments

eleventhanniversarysteel

introduces IndustrialExpansion (INDEX)Capital Program

thirteenthanniversarylace

creates AssetManagementDivision

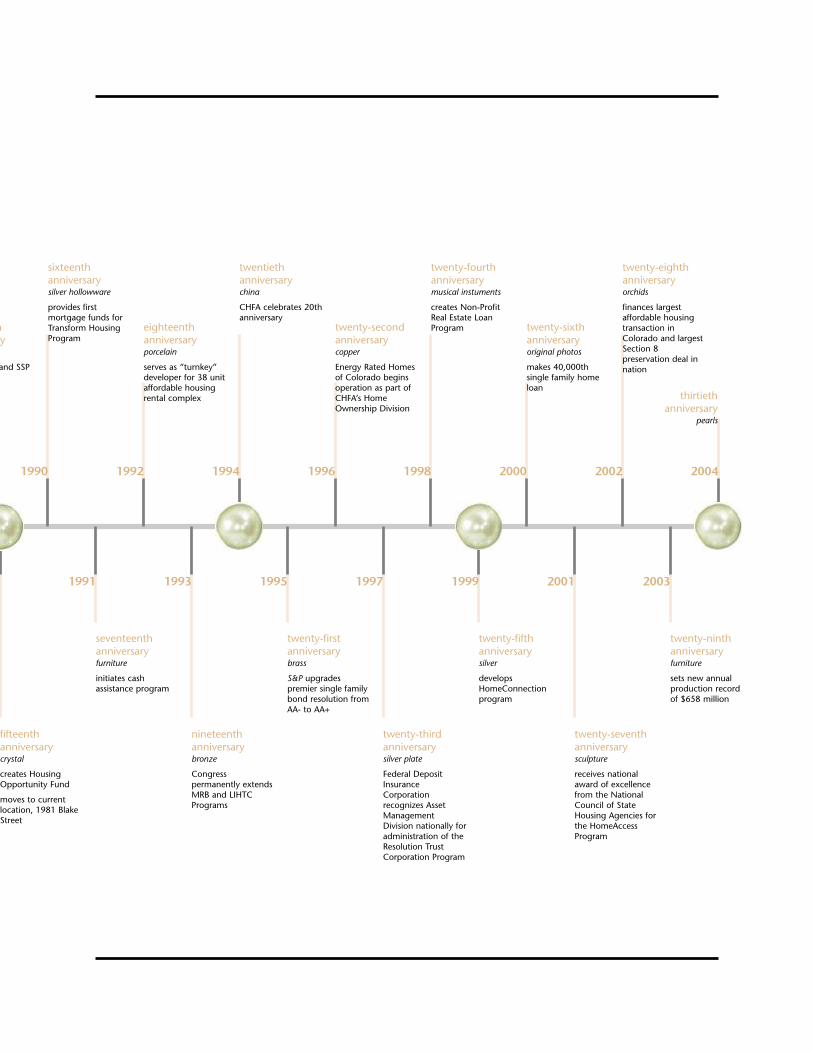

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

thy

and SSP

sixteenthanniversarysilver hollowware

provides firstmortgage funds forTransform HousingProgram

eighteenthanniversaryporcelain

serves as “turnkey”developer for 38 unitaffordable housingrental complex

twentiethanniversarychina

CHFA celebrates 20thanniversary

twenty-secondanniversarycopper

Energy Rated Homesof Colorado beginsoperation as part ofCHFA’s HomeOwnership Division

twenty-fourthanniversarymusical instuments

creates Non-ProfitReal Estate LoanProgram twenty-sixth

anniversaryoriginal photos

makes 40,000thsingle family homeloan

twenty-eighthanniversaryorchids

finances largestaffordable housingtransaction inColorado and largestSection 8preservation deal innation

thirtiethanniversary

pearls

fifteenthanniversarycrystal

creates HousingOpportunity Fund

moves to currentlocation, 1981 BlakeStreet

seventeenthanniversaryfurniture

initiates cashassistance program

nineteenthanniversarybronze

Congresspermanently extendsMRB and LIHTCPrograms

twenty-firstanniversarybrass

S&P upgradespremier single familybond resolution fromAA- to AA+

twenty-thirdanniversarysilver plate

Federal DepositInsuranceCorporationrecognizes AssetManagementDivision nationally foradministration of theResolution TrustCorporation Program

twenty-fifthanniversarysilver

developsHomeConnectionprogram

twenty-seventhanniversarysculpture

receives nationalaward of excellencefrom the NationalCouncil of StateHousing Agencies forthe HomeAccessProgram

twenty-ninthanniversaryfurniture

sets new annualproduction recordof $658 million

In addition to working with nonprofits, CHFA provides financ-ing to businesses in rural communities. Loans made under itsBusiness and Industry Programs may be used for real estate orrelated equipment. In 2004, CHFA closed a loan with theDurango and Silverton Narrow Gauge Railroad. The loan repre-sents CHFA’s largest business finance transaction.

The railroad, in operation for over 120 years, is one of the mostimportant historical narrow gauge rail lines in the world. Thetrain, a National Historic Landmark, significantly impacts theregion’s economy. In 2002, Al and Carol Harper, who own therailroad, found themselves with a very difficult decision tomake, one that would have a four million dollar economicimpact. Unfortunately, due to the extreme drought inSouthwest Colorado and the resulting wildfires, they wereforced to discontinue passenger service to Silverton.

“CHFA was there for us,” said Jeff Jackson, Senior Vice Presidentof the railroad. “First, CHFA approved a one million dollar loan tohelp the railroad get through the hard times and then at the endof 2004, they refinanced the railroad’s entire debt.”

The railroad infuses approximately $100,000,000 each year intosouthwestern Colorado and directly impacts one out of everysix employees in La Plata and San Juan counties. The trainmaintains year-round employment of approximately 80employees. Seasonal employment increases the number ofemployees to over 150.

CHFA provided a 20 year fixed rate loan used to refinance debtand reduce annual loan payments by almost 60%. The resultassures this enterprise, so vital to the southwest region of thestate, will be financially stable for many years to come. AlHarper sums it up well “This loan will ensure continued operationof the railroad for future generations.”

Both the Children’s ARK and the Durango and Silverton NarrowGauge Railroad loans demonstrate how CHFA’s business financeefforts bring positive economic opportunities to communitiesthroughout Colorado. To date, CHFA’s economic developmentprograms have financed more than $500 million to businessesthroughout Colorado and have impacted 26,153 jobs.

economic growth

CHFA offers several production tools to multifamily developersto support their development and redevelopment effortsthroughout Colorado neighborhoods. These tools include debtor equity for the rental developments through loans or tax cred-its.

CHFA is the state agency designated by the Governor to admin-ister the Low Income Housing Tax Credits (LIHTC) Programwhich encourages the construction and rehabilitation of lowincome rental housing. Created by the 1986 Tax Reform Act,the program provides a federal income tax incentive which isused as equity by investors developing qualified low incomerental housing. CHFA allocates the credits to eligible develop-ments, which must reserve a specified proportion of housingunits for low income occupancy for a minimum of 30 years.Each year, CHFA publishes a Qualified Allocation Plan, whichdescribes a process for allocating the tax credits and for deter-mining the amount of credit to be allocated to each develop-ment. CHFA also monitors compliance with the low income userequirements. Since 1987, CHFA has allocated more than $84million tax credits that have created over 30,870 rental house-holds. In 2004 alone, CHFA reserved $10.5 million in tax cred-it, which impacted approximately 1,230 units.

If a developer seeks a loan, CHFA Housing DevelopmentOfficers have the skills to assess the situation and provide thebest possible financing solution. In 2004, the team closed$32,251,425 in loans, allowing the production or preservationof 908 units, and bringing cumulative rental production to48,662 units.

Often, both LIHTC and CHFA loan products are necessary tobuild a successful rental project. An excellent example is PalomaVillas I, a newly constructed, 80-unit multi-family project locat-ed in Denver, Colorado.

According to Greg Glade, CFO of Black Creek Communities (theproject's developer and owner), "CHFA's flexible equity and debtprograms enabled us to seamlessly fill Paloma's entire capital struc-ture on terms that were very competitive with the broader capitalmarkets. We anticipate working with both the equity and debtgroups on our future residential developments."

neighborhooddevelopment

Mary Lou Rodriguez and family,residents of Paloma Villas I

The CHFA Asset Management Division’s primary responsibility isto monitor CHFA loans. Asset Management assesses the overallfinancial condition and performance of all the developments inCHFA’s commercial portfolio. In doing so, it balances CHFA’sfiduciary responsibility of maintaining a sound financial struc-ture with its public purpose goals of providing affordable hous-ing and economic opportunity.

The division also operates the Housing Assistance Payment(HAP) contract administration for the federal office of Housingand Urban Development (HUD). Under the HAP program, res-idents pay 30% of their income toward rent and the rest is paidby HUD. In 2004, Asset Management monitored 53,696 rentalunits in over 700 developments around Colorado.

The Asset Management Team fulfills their responsibilitiesthrough regular visits to each development in the portfolio.The Team also holds training sessions for onsite property man-agement and owners of developments across Colorado. Thetraining sessions cover topics to ensure owners provide safe,decent rental housing to Colorado families. In 2004, CHFA heldover ten training sessions attended by approximately 300 prop-erty managers, developers and owners of rental properties.

maintainingrelationships

The CHFA Asset ManagementTeam conducting a training session

Through its Rental Acquisition Program (RAP), CHFA purchasesapartment developments, rehabilitates them and insures that atleast 40% of the units are affordable to low income familieswithout federal subsidies. CHFA currently owns 15 rental devel-opments totaling 1,586 units and contracts with private entitiesto manage the properties. The properties range in size from 12to 492 units, located in eight different cities and townsthroughout Colorado.

The newest addition to the RAP portfolio is Mountain TerraceApartments, purchased in 2004. Mountain Terrace has 152units and is located in Westminster. CHFA purchased MountainTerrace from Rocky Mountain Mutual Housing Association.CHFA’s purchase of the property maintained its affordabilitywhile providing RMMHA, a non profit affordable housing devel-oper and owner which partners with CHFA, a fair market price.It was a “win-win” situation.

Mountain Terrace is an exciting addition to the portfolio. It wasacquired with an established set of unique resident services andactivities broader than that which currently exist at the other 14RAP properties.

Within its RAP portfolio, CHFA fosters and encourages a sense ofcommunity at each of the properties by hosting family and res-ident activities including trainings and informal social events.CHFA intends to use Mountain Terrace as a model for the restof its RAP developments in the near future.

chfa ownedrental portfolio

A resident of Mountain Terrace Apartmentsenjoying the activity center

CHFA created its Supportive Services Program (SSP) in 1988,with grants provided by the Robert Woods Johnson Foundationand the Administration on Aging. The program places trainedACE (Access, Coordination and Empowerment) ServiceCoordinators in independent senior and family facilitiesthroughout the state. Research shows that when services suchas housekeeping, personal care, meals, etc., are made availableto seniors and monitored by trained personnel, seniors maintaintheir independence longer. Currently 40 facilities with approxi-mately 4,500 rental units participate in CHFA’s SSP.

One property utilizing the SSP is Simon Center, a 104-unit,Section 8 property in Englewood. Simon Center’s residentsreceive a wide variety of services, as well as educational andsocial programs. Frequent presentations cover assistance withentitlements, safety, elderly fraud and illness prevention. Manyevents such as barbecues, day trips and picnics help serve thesocial needs of the Center’s residents.

CHFA’s SSP staff also participates in community developmentefforts to create interaction between residents and their neigh-borhoods, helping families understand what services andresources are available to them near where they live.

supportive services

Two residents from Simon Centerin Englewood, Colorado

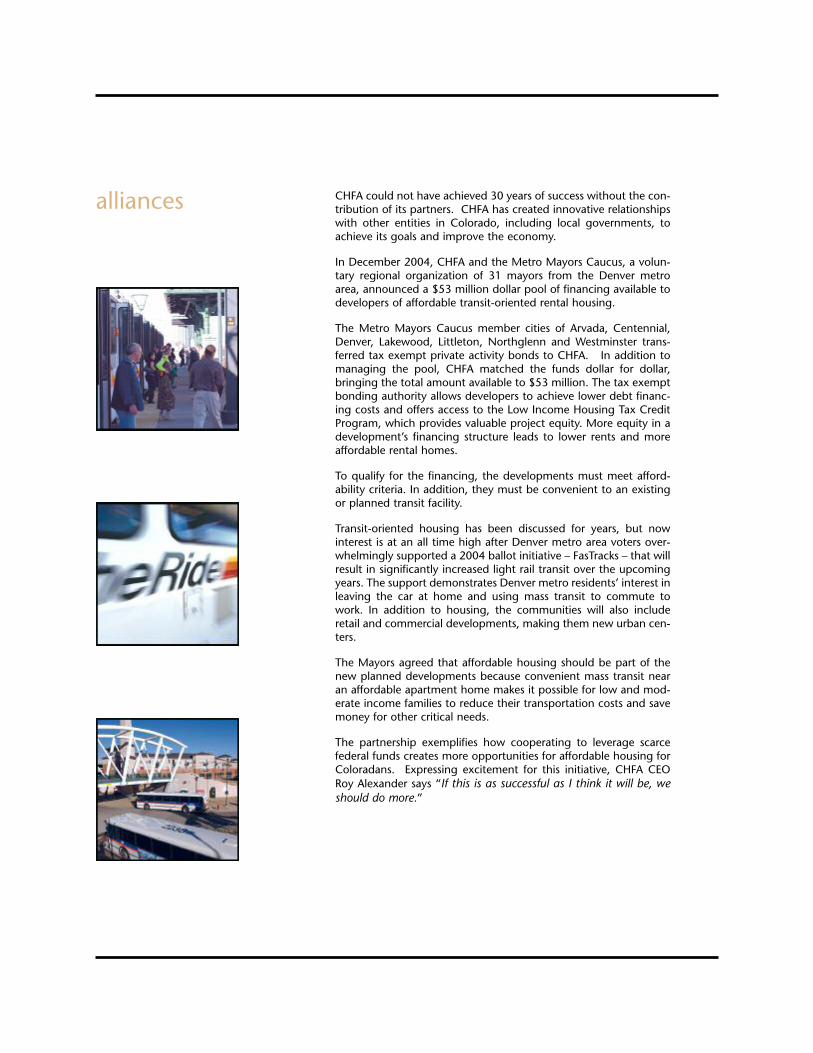

CHFA could not have achieved 30 years of success without the con-tribution of its partners. CHFA has created innovative relationshipswith other entities in Colorado, including local governments, toachieve its goals and improve the economy.

In December 2004, CHFA and the Metro Mayors Caucus, a volun-tary regional organization of 31 mayors from the Denver metroarea, announced a $53 million dollar pool of financing available todevelopers of affordable transit-oriented rental housing.

The Metro Mayors Caucus member cities of Arvada, Centennial,Denver, Lakewood, Littleton, Northglenn and Westminster trans-ferred tax exempt private activity bonds to CHFA. In addition tomanaging the pool, CHFA matched the funds dollar for dollar,bringing the total amount available to $53 million. The tax exemptbonding authority allows developers to achieve lower debt financ-ing costs and offers access to the Low Income Housing Tax CreditProgram, which provides valuable project equity. More equity in adevelopment’s financing structure leads to lower rents and moreaffordable rental homes.

To qualify for the financing, the developments must meet afford-ability criteria. In addition, they must be convenient to an existingor planned transit facility.

Transit-oriented housing has been discussed for years, but nowinterest is at an all time high after Denver metro area voters over-whelmingly supported a 2004 ballot initiative – FasTracks – that willresult in significantly increased light rail transit over the upcomingyears. The support demonstrates Denver metro residents’ interest inleaving the car at home and using mass transit to commute towork. In addition to housing, the communities will also includeretail and commercial developments, making them new urban cen-ters.

The Mayors agreed that affordable housing should be part of thenew planned developments because convenient mass transit nearan affordable apartment home makes it possible for low and mod-erate income families to reduce their transportation costs and savemoney for other critical needs.

The partnership exemplifies how cooperating to leverage scarcefederal funds creates more opportunities for affordable housing forColoradans. Expressing excitement for this initiative, CHFA CEORoy Alexander says “If this is as successful as I think it will be, weshould do more.”

alliances

Englewood CityCenter Light Rail station

To celebrate its 30th anniversary, CHFA found some innovativeways to give back to the community while also remembering itshistory:

First, on September 24, 2004, CHFA held its 15th annual J.David Barba golf tournament at the Heritage Eagle Bend Golfand Country Club in Aurora, Colorado. This year’s event servedas a fundraiser for the Colorado Coalition for the Homeless(CCH). CHFA donated $30,000 and raised an additional$24,000 at the tournament to benefit CCH.

The tournament was a tremendous success thanks in large partto CHFA’s many partners: Lehman Brothers, Wells Fargo, Zion’sBank, UBS Paine Webber, Newman and Associates andGuaranty Bank to name a few. Former Bronco wide receiver EdMcCaffrey’s appearance also contributed a great deal to thetournament’s success.

Second, on December 24th, CHFA donated one turkey fromeach CHFA staff member to the Food Bank of the Rockies tofeed needy families and individuals throughout Colorado. Theidea came from an old CHFA story…

… In 1983, Congress made some significant changes to theMortgage Revenue Bond program resulting in a sudden drop insingle family loan production. Costs had to be cut quickly. Thetraditional Christmas turkey given to staff was a luxury CHFAcouldn’t afford. One of the senior staff members decided toinject some humor into the situation. He gathered all staffmembers in the board room for a small holiday celebration andpresented each staff member with a Cornish game hen, thebird’s reduced size reflecting CHFA’s reduced profits. The ges-ture is fondly remembered, even after all these years.

giving back

2004 CHFA J. David Barba Golf Tournament

The staff and employees of CHFA are critical to our success andwill continue to create innovative and unique solutions toaddress the affordable housing and small business needs of thestate of Colorado.

2004 staff

Roy Alexander • Kiza Amatya • Paul Ammon • Norma Andersen • Shelia Anderson• Cathy Arambula • Ram Balaraman • Terry Barnard • Kay Barnes • Deona Barr •Monique Bartolo • Rachel Basye • Kelly Becker • Robin Bienek • Linda Bessinger •Art Birky • Karen Black • Gene Blauth • Richelle Bliss • Check Borgman • DarceyBorzileri • Cindy Bradley • Jessica Bugarin • Emily Bullard • Karen Calderon • LizCameron • Todd Campos • Joe Capello • Larissa Carlson • William Carlson •William Carter • Susann Comer • Laura Coyle • Connie Cronin • DeDe Cross • JohnCurlin • Dwan Daniels • Julie Deffert • Sheri Lowrance • Tim Dolan • John Dolton• Kathy Dominguez • Kimberly Duignan • Adelaida Escalante • Claire Fagan • MarkFeilmeier • Anthony Fernandez • Peggy Fernandez • Tom Fleming • Janine Flores •Susan Forsman • Iris Foster • Priscilla Fox • Irma Fransua • Shannon Friel • MonteFrihauf • Louise Gallegos • Roque Gallegos • Juan Garcia • Zenobia Garcia •Michele Gentry • Amelia Georgiou • Jaime Gomez • Yvonne Gonzales • MikeGuertin • Jose Gutierrez • Karen Gutjahr • Lynn Gylling • Stephen Hagen • SteveHalbrook • Karen Harkin • Paula Harrison • Helena Haynes • Kendall Hays • PamHeath • Thomas Hemming • Nikki Hendrich • Debbie Herrera • Matt Hertzfeld •Dolores Higgins • Jim Hooper • Robert Horn • Rhonda Housden • Ann Hugh •Roger Hughes • Andrea Jenkins • Jeff Johnson • Steve Johnson • Wyatt Jones • AndiKaup • Lorrie Keller-Garcia • Jill Klosterman • Kathi Koehn • Delrae Korczak • RobKorosec • Ron Lafollette • Paul Lago • Theresa Lee • Elfriede Leicht • Rene LeJeune• Tracy Lew • D. Mark Livingston • Kimberly Longworth • Ann Lowery • Lisa Lunger• Melissa Martinez • Roni Martinez • Susan Mazzulla • Megan McCarthy • MarionMcGruder • Kris McLain • Dan McMahon • Brian Miller • Jason Miller • DesireeMiniel • Bud Minzenmayer • Bob Munroe • Jim Nelly • Kathy Nguyen • TrinaNguyen • Debra Norborg • Alan Nuss • Don O’Brien • John O’Brien • MasoudaOmar • JoAnn Onweller • Denise O’Rourke • Doreen Padilla • Starr Padilla • VickyePalmer • Thomas Parra • Brian Phetteplace • John Plakorus • Candace Polk •Tamme Polson • Rita Poundstone • James Roberts • June Robertson • ShawnRomero • Brenda Saewert • Nedra San Filippo • Bob Sandridge • Barbara Schmitt• Debra Sgambati • Jana Sizemore • Aaron Sleezer • Liz Smith • YuDania Sparks •Elena Spinks • Heather Staggs • Adam Stricker • Denise Tamulis • Martha Taylor •Kathryn Teets • Linda Thomas • Michael Trofi • Annette Trujillo • Susan Vaho • RoseVasquez • Diane Walton • Joyce Ware • Eron Weaver • Tasha Weaver • Janelle Welch• Cris White • Pat Whitfield • Rich Wilke • Gaylene Wilson • Brian Windley • EvaWinslett • Mary Wolf • Eileen Wood • Frances Zambrano • Jorge Zavala • Li Zhang

in memory of Steve Halbrook

Colorado Housing and Finance Authority

1981 Blake StreetDenver, Colorado 80202

303.297.2432800.877.2432 toll free303.297.7305 tdd

www.colohfa.org

CHFA is not a state agency. Its bonds and notes are notobligations of the state of Colorado, and are notrepaid with tax dollars. CHFA is self supporting.

This report was written and designed by the CHFAMarketing and Strategic Development Team, and wasprinted without the use of general fund dollars.

All photos copyright 2004, 2005 Scott Dressel-Martin.

financing the places where people live and work