Embed Size (px)

Citation preview

BARCLAYS CAPITAL CEO ENERGY-POWER CONFERENCECHESAPEAKE MIDSTREAM PARTNERS

PARTNERSHIP OVERVIEW

2

Partnership overview:Formed as Chesapeake Energy (“Chesapeake” or “CHK”) and Global Infrastructure Partners (“GIP”) joint venture in September 2009Provide midstream services in leading unconventional plays including the Barnett Shale, Haynesville Shale and Mid-Continent regionsCustomers include Chesapeake, Total E&P USA, Inc. (“Total”) and other third partiesPriced IPO in July 2010; NYSE: “CHKM”Expanded into the Haynesville Shale with December 2010 drop-down from CHK

Wellhead Customer

WellheadFacilities/Flowlines

GatheringSystem

GatheringFacilities

PipelineTransportation Distribution

Chesapeake Midstream PartnersValue Chain:

Central Delivery Points

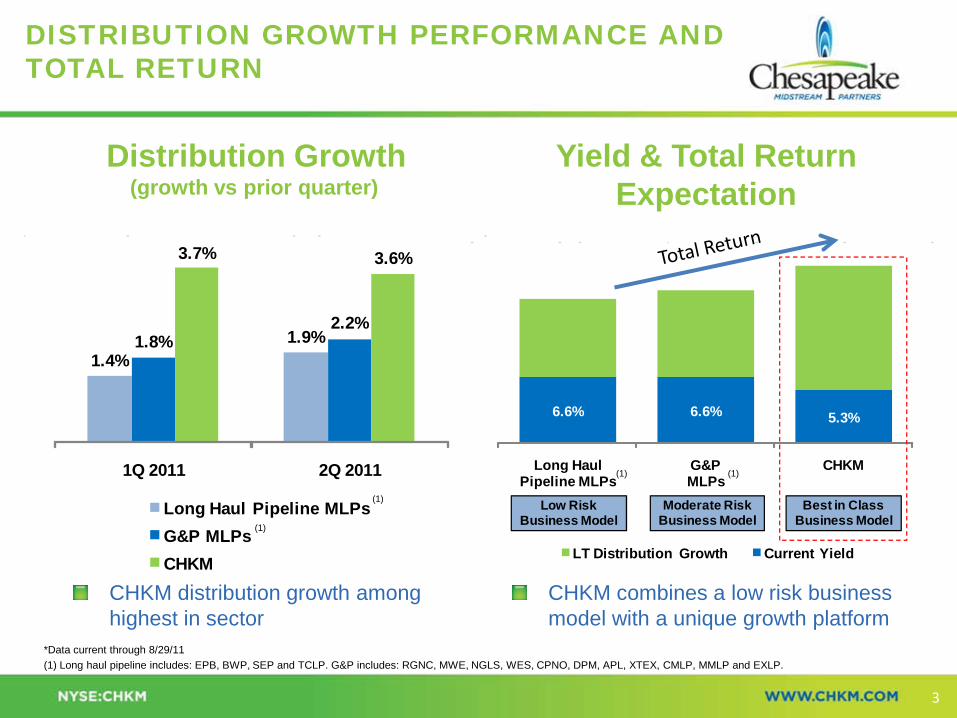

1.4%1.9%1.8%

2.2%

3.7% 3.6%

1Q 2011 2Q 2011

Long Haul Pipeline MLPsG&P MLPsCHKM

6.6% 6.6% 5.3%

Long HaulPipeline MLPs

G&PMLPs

CHKM

LT Distribution Growth Current Yield

Moderate RiskBusiness Model

Best in ClassBusiness Model

Low RiskBusiness Model

DISTRIBUTION GROWTH PERFORMANCE AND TOTAL RETURN

3

Distribution Growth (growth vs prior quarter)

Yield & Total Return Expectation

CHKM distribution growth among highest in sector

CHKM combines a low risk business model with a unique growth platform

*Data current through 8/29/11(1) Long haul pipeline includes: EPB, BWP, SEP and TCLP. G&P includes: RGNC, MWE, NGLS, WES, CPNO, DPM, APL, XTEX, CMLP, MMLP and EXLP.

(1) (1)

(1)

(1)

Established Basins with Low Development RiskHaynesville and Barnett are #1 and #2 U.S. gas shales by production, respectivelyDiversity of plays in Mid-Continent, enhanced focus on unconventional resources

Leading CHK PositionCHK #1 producer in Barnett and Haynesville and a leading producer in Mid-Continent

Attractive Downstream Market AccessAccess to multiple pipeline interconnects and downstream markets in all regions

Scale Volumes1.0 Bcf/d Barnett + 0.6 Bcf/d Haynesville + 0.5 Bcf/d Mid-Continent = 2.1 Bcf/d +

Capital Expenditure/Infrastructure Maturity60-70% of major infrastructure built out across regions

LEADING MIDSTREAM BUSINESS

Unique portfolio with leading positions in Barnett Shale, Haynesville Shale and Mid-Continent Region

4

BUSINESS RISK CONSIDERATIONS AND MITIGANTS

5

MitigantsConsiderations

MVC and long-term acreage dedicationsRate redeterminationConservative maintenance capital

Volume & Capital

100% fixed-fee revenuesCommitment to maintain contract structure / business model as business growsConcentrated in low cost basins

Total and other 3rd parties today – ~18 % revenueImproving CHK financial profile (25/25 Plan)Core basins to CHK for cash flow generation

Arms-length, 10-20 year contracts at market ratesCritical infrastructure providing access to marketDedicated acreage

Commodity & Basin

Counterparty Concentration

Re-contracting

1) Data for the three-month period ended 06/30/2011

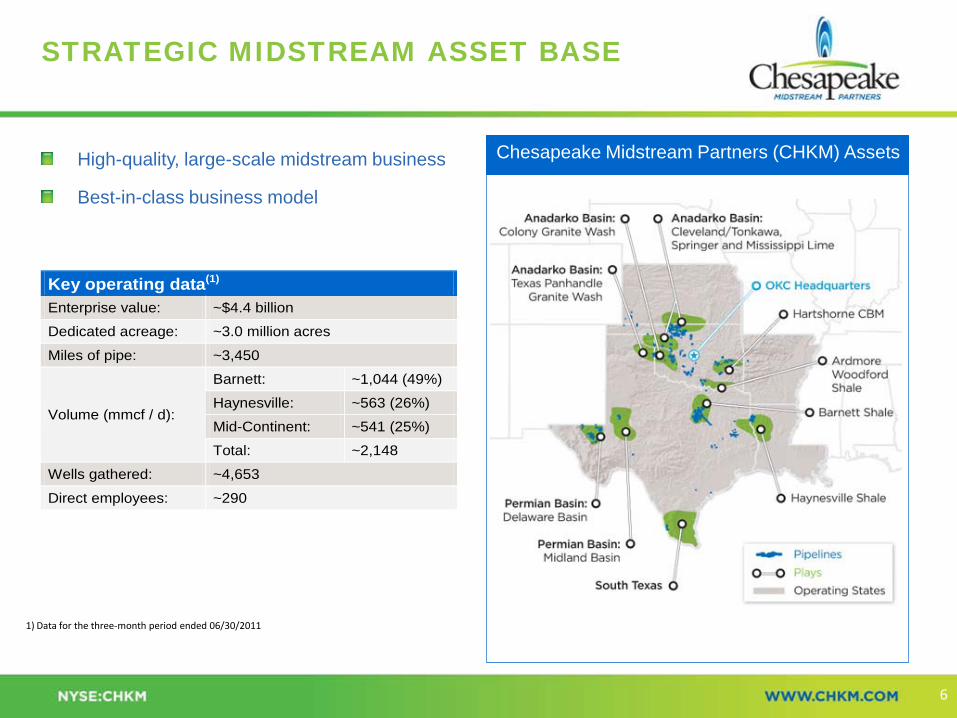

STRATEGIC MIDSTREAM ASSET BASE

High-quality, large-scale midstream business

Best-in-class business model

6

Key operating data(1) Enterprise value: ~$4.4 billion

Dedicated acreage: ~3.0 million acres

Miles of pipe: ~3,450

Volume (mmcf / d):

Barnett: ~1,044 (49%)

Haynesville: ~563 (26%)

Mid-Continent: ~541 (25%)

Total: ~2,148

Wells gathered: ~4,653

Direct employees: ~290

Chesapeake Midstream Partners (CHKM) Assets

Barnett Shale proved to be an excellent basin to pioneer best practices for use throughout Midstream

Route developmentEnvironmental permitting Construction techniques

Barnett solutions in action – At the end of 2Q 2011, the Barnett represented

50% of total CHKM volume60% of CHKM revenue65% of invested capital

Overcoming the most difficult challenges translates into competitive advantage

Difficult Challenges Establish Best Practices

COMPETITIVE ADVANTAGE FROM BARNETTEXECUTION

7

Meeting the challenges of operating in an urban environmentCHESAPEAKE MIDSTREAM PARTNERS

8

Maintaining good relationships with neighbors

Meeting the challenges of operating in an urban environmentCHESAPEAKE MIDSTREAM PARTNERS

9

Managing operations near homes and recreational areas

The Barnett ShaleCHESAPEAKE MIDSTREAM PARTNERS

10

Successfully coexisting in Fort Worth while providing reliable delivery of natural gas to market

CHKM Urban OperationsConservative designRigorous construction inspectionRisk assessmentIntegrity Management philosophyPublic Awareness

Application of Latest TechnologyForward Looking Infrared (FLIR) camerasHelicopter flyoversSmart Pig

Innovative & Conservative OperationsBEST IN CLASS OPERATIONS

11

-

100

200

300

400

500

600

700

Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

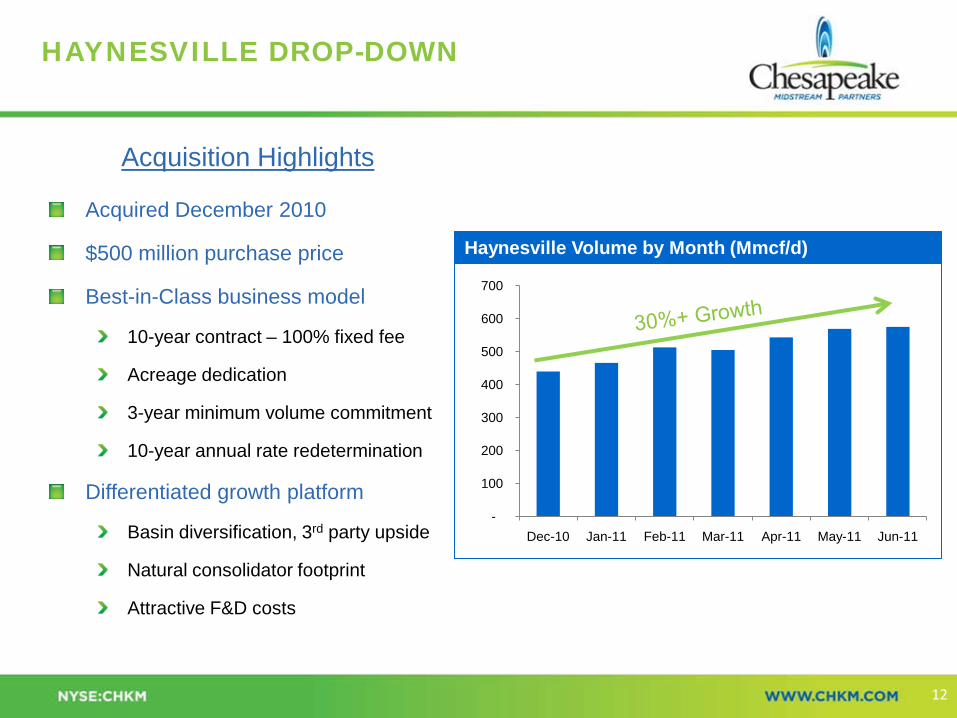

Acquired December 2010

$500 million purchase price

Best-in-Class business model

10-year contract – 100% fixed fee

Acreage dedication

3-year minimum volume commitment

10-year annual rate redetermination

Differentiated growth platform

Basin diversification, 3rd party upside

Natural consolidator footprint

Attractive F&D costs

HAYNESVILLE DROP-DOWN

12

Acquisition Highlights

Haynesville Volume by Month (Mmcf/d)

CHKM’s unique relationship with CHK provides multiple benefitsLargest drilling company in the U.S.Increasing focus in oil and liquids rich playsSignificant Natural Gas Liquids (NGL) production in multiple basinsCHK serves as the anchor tenant for processing plants and NGL pipeline projectsDiversification of supply provides secure returns on investmentMinimum of five years of potential liquids projects

CHKM’s liquids strategyOwn and operate processing plants for CHK and third-party gasBuild or pursue joint ventures for NGL and crude oil pipelines to premium marketsParticipate in downstream fractionation and NGL upgrade opportunity

LIQUIDS UPDATELeveraging the relationship with CHK

13

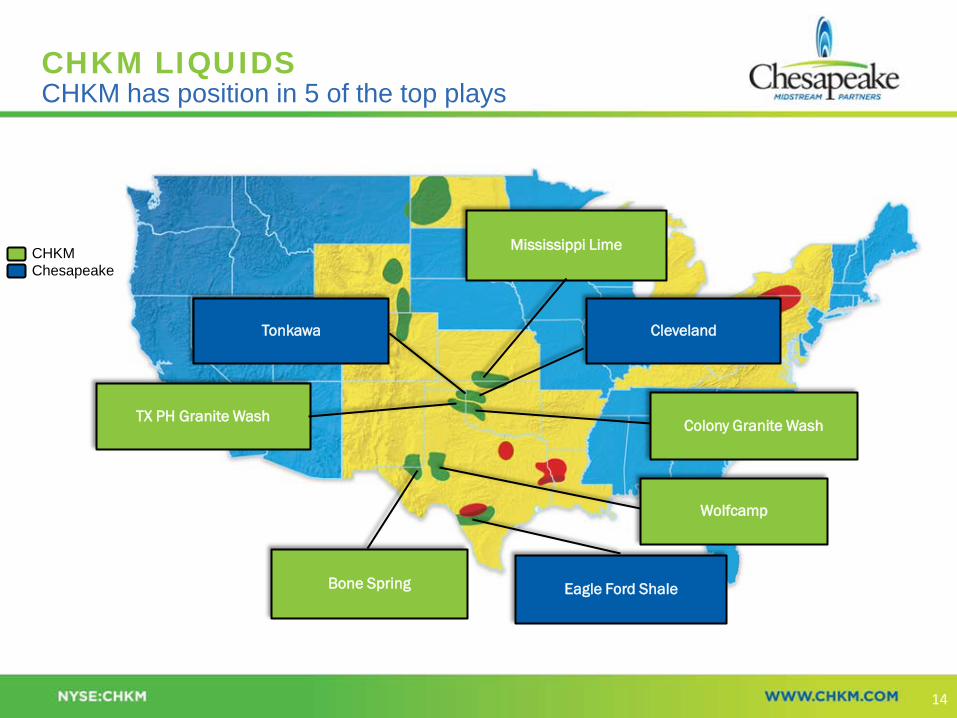

CHKM LIQUIDSCHKM has position in 5 of the top plays

Wolfcamp

Eagle Ford ShaleBone Spring

TX PH Granite Wash

Tonkawa

Mississippi Lime

Cleveland

Colony Granite Wash

CHKMChesapeake

14

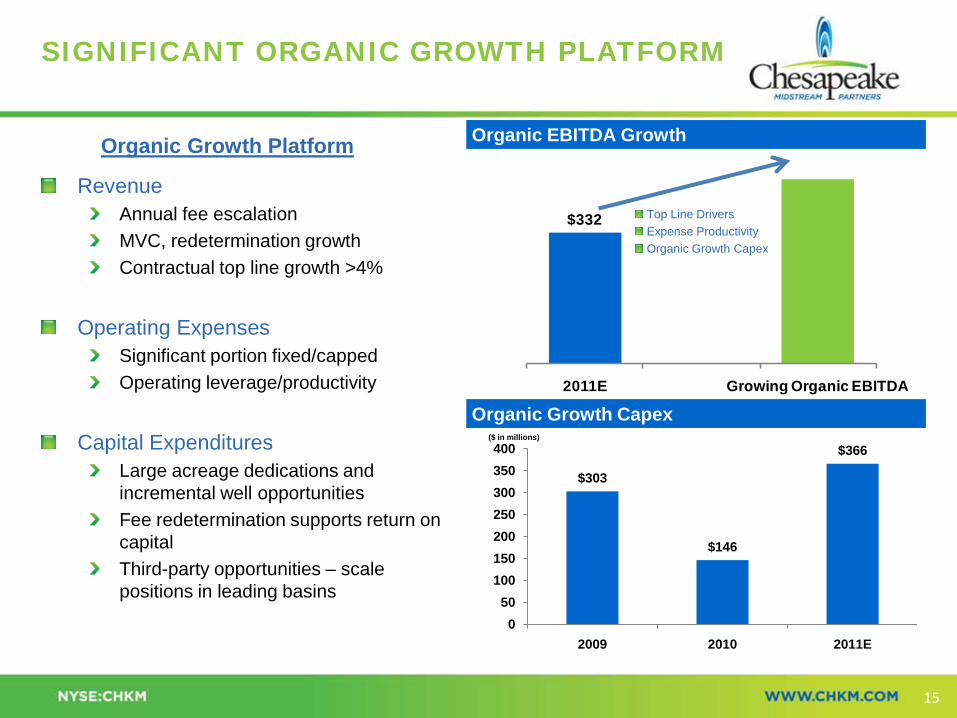

SIGNIFICANT ORGANIC GROWTH PLATFORM

15

RevenueAnnual fee escalationMVC, redetermination growthContractual top line growth >4%

Operating ExpensesSignificant portion fixed/cappedOperating leverage/productivity

Capital ExpendituresLarge acreage dedications and incremental well opportunitiesFee redetermination supports return on capitalThird-party opportunities – scale positions in leading basins

Organic Growth Platform Organic EBITDA Growth

Organic Growth Capex

Top Line DriversExpense ProductivityOrganic Growth Capex

$332

2011E Growing Organic EBITDA

$303

$146

$366

050

100150200250300350400

2009 2010 2011E

($ in millions)

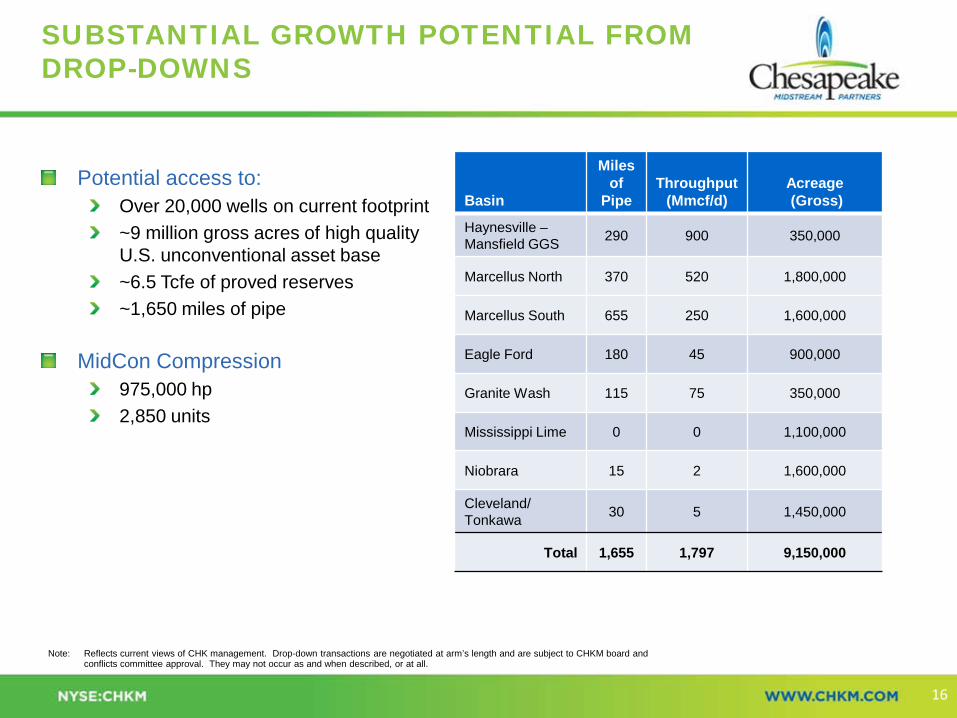

Potential access to:Over 20,000 wells on current footprint~9 million gross acres of high quality U.S. unconventional asset base ~6.5 Tcfe of proved reserves~1,650 miles of pipe

MidCon Compression975,000 hp2,850 units

SUBSTANTIAL GROWTH POTENTIAL FROM DROP-DOWNS

16

Note: Reflects current views of CHK management. Drop-down transactions are negotiated at arm’s length and are subject to CHKM board and conflicts committee approval. They may not occur as and when described, or at all.

Basin

Miles of

PipeThroughput

(Mmcf/d)Acreage(Gross)

Haynesville –Mansfield GGS 290 900 350,000

Marcellus North 370 520 1,800,000

Marcellus South 655 250 1,600,000

Eagle Ford 180 45 900,000

Granite Wash 115 75 350,000

Mississippi Lime 0 0 1,100,000

Niobrara 15 2 1,600,000

Cleveland/Tonkawa 30 5 1,450,000

Total 1,655 1,797 9,150,000

Organic growth capital

Significant opportunities

Mid-teens return

CHK drop-down portfolio

Leading basins

#1 acreage positions

Third-party acquisitions

Opportunistic

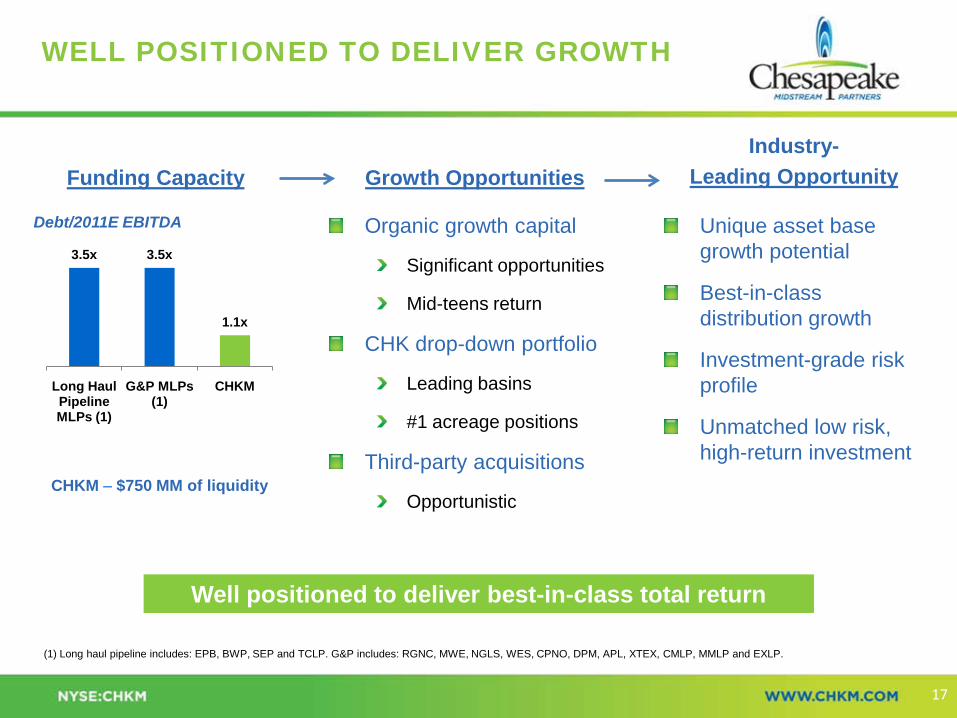

WELL POSITIONED TO DELIVER GROWTH

Funding Capacity

Well positioned to deliver best-in-class total return

Unique asset base growth potential

Best-in-class distribution growth

Investment-grade risk profile

Unmatched low risk, high-return investment

Growth OpportunitiesIndustry-

Leading Opportunity

Debt/2011E EBITDA

(1) Long haul pipeline includes: EPB, BWP, SEP and TCLP. G&P includes: RGNC, MWE, NGLS, WES, CPNO, DPM, APL, XTEX, CMLP, MMLP and EXLP.

17

CHKM – $750 MM of liquidity

3.5x 3.5x

1.1x

Long Haul Pipeline MLPs (1)

G&P MLPs (1)

CHKM

Chesapeake Midstream Partners remains committed to:Protecting our country’s natural resourcesEncouraging our employees, contractors, suppliers and vendors to work in the safest and most environmentally-friendly manner possibleContinually evaluating and improving our operating practices to minimize our environmental footprintBeing a good neighbor in the areas in areas where we live and work

Commitment to Safety and Environmental ExcellenceSAFE AND RESPONSIBLE OPERATIONS

18