Embed Size (px)

Citation preview

Presale:

Chase Issuance Trust (Class A(2020-1))February 10, 2020

Preliminary Rating

Class Preliminary Rating Interest rate (%) Preliminary amount (mil. $) Credit support (%)

A(2020-1) AAA (sf) Fixed 500 14.0

Note: This presale report is based on information as of Feb. 10, 2020. The rating shown is preliminary. This report does not constitute arecommendation to buy, hold, or sell securities. Subsequent information may result in the assignment of a final rating that differs from thepreliminary rating. (i)The interest rates will be determined on the pricing date.

Profile

Expected Closing date Feb. 18, 2020.

Expected maturity date Jan. 17, 2023.

Legal maturity date Jan. 15, 2025.

Distribution date The 15th day of each calendar month, beginning March 16, 2020.

Issuer trust collateral Credit card receivables that are generated by revolving credit card accounts owned byJPMorgan Chase Bank N.A. or one of its affiliates.

Issuing entity Chase Issuance Trust.

Originator, sponsor, administrator,and servicer

JPMorgan Chase Bank N.A. (A+/Stable/A-1).

Depositor and transferor Chase Card Funding LLC.

Indenture trustee and collateralagent

Wells Fargo Bank N.A.

Underwriter J.P. Morgan Securities LLC.

Rationale

The preliminary rating assigned to Chase Issuance Trust's class A(2020-1) CHASEseries notesreflects:

- The 14.0% credit support that the subordinated class B and C notes provide, which we believeis sufficient to withstand the simultaneous stresses we apply to our 5.5% base-case loss rate,20.0% base-case payment rate, 15.0% base-case yield, and 3.0% purchase rate assumptionsfor the notes. In addition, we used stressed excess spread and note interest rate assumptions

Presale:

Chase Issuance Trust (Class A(2020-1))February 10, 2020

PRIMARY CREDIT ANALYST

Trang Luu

Dallas

+ 1 (214) 765 5887

SECONDARY CONTACTS

Romil Chouhan, CFA

New York

+ 1 (212) 438 3512

Jonathan Zimmerman

New York

(1) 212-438-1002

www.standardandpoors.com February 10, 2020 1

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

to assess whether, in our view, sufficient credit support is available for the notes. We base all ofthe above stress assumptions on our current criteria and assumptions (see "U.S. Credit CardSecuritizations: Methodology And Assumptions," published Aug. 24, 2017.

- Our view that the 5.0% minimum seller's interest is sufficient in our stress scenarios to absorbdilutions or noncash reductions in the receivables.

- Our expectation that under a moderate ('BBB') stress scenario, all else being equal, ourpreliminary rating on the class A(2020-1) notes will remain within one rating category of theassigned preliminary 'AAA (sf)' rating during the next 12 months, which is in line with our creditstability criteria (see "Methodology: Credit Stability Criteria," May 3, 2010).

- The inherent credit risk in the collateral loan pool, based on our economic forecast, the mastertrust portfolio's historical performance, the collateral characteristics, and vintage performancedata.

- JPMorgan Chase Bank N.A.'s (Chase's; A+/Stable/A-1) servicing experience and our view of itsaccount origination, underwriting, account management, collections, and general operationalpractices.

- Our expectation for timely interest and ultimate principal payments by the legal final maturitydate, based on stressed cash flow modeling scenarios using assumptions that arecommensurate with the assigned preliminary 'AAA (sf)' rating.

- Our view of the notes' underlying payment structure, cash flow mechanics, and legal structure.

Changes From Class A(2018-1)

The class A(2020-1) note structure is similar to that of the class A(2018-1) notes issued out of thetrust.

In May 2019, Chase Bank USA N.A. merged with JPMorgan Chase Bank, with JPMorgan ChaseBank as the surviving entity. Prior to the merger, Chase USA was the sponsor, originator,administrator and servicer of the issuing entity. Post-merger, JPMorgan Chase Bank assumed andagreed to perform all covenants and obligations of Chase USA as sponsor, originator,administrator and servicer of the issuing entity.

The issuer, eligible accounts and receivables, payment priority, collection and allocationmechanics, credit support and usage mechanics, early redemption events, and events of defaulthave not changed. There have been no material changes in collateral performance since theprevious transaction. Our base-case and stress assumptions have not changed since January2019, when we completed our shelf review of all U.S. bank credit card trusts that we rate (see"2019 U.S. And Canadian Credit Card ABS Review," published Jan. 14, 2019).

Notably, in June 2019, a lawsuit was brought against the special-purpose entities of Chase'scredit card securitization program, alleging that interest rates charged to New York cardholdersviolate New York's usury laws. The defendants filed a motion to dismiss the complaint in August2019; and, in January 2020, the magistrate judge reviewing the case issued a report andrecommendation that the defendants' motion be granted. The case is in its early stages, and theoutcome is uncertain at this time. We will continue to monitor the development of this case, aswell as pending Madden-related cases brought against other securitization entities and reassesswhat affect, if any, this may have on the trust assets (for more details, see "With The OngoingLawsuits Against Two Securitization Entities, How Will Credit Card Receivables Asset-BackedSecurities Be Affected?," published Oct. 15, 2019).

www.standardandpoors.com February 10, 2020 2

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

Class A(2020-1) Note Terms Summary

The class A(2020-1) issuance has the following key features:

- The notes pay fixed interest per year on the 15th day of each month, beginning March 16, 2020.The preliminary rating addresses the full principal payment by the legal final maturity daterather than the expected maturity date.

- All outstanding class B and C notes will provide credit support to the class A(2020-1) notes.Based on the transaction documents, Chase Issuance Trust may issue additional class A notetranches as long as the class B and C notes' minimum required amounts are outstanding tosupport them.

- The class B and C notes will each provide 8.14% minimum subordination--when expressed as apercentage of the class A(2020-1) principal balance--to support the class A(2020-1) notes,giving 16.28% total credit support for the class A(2020-1) notes. Based on the capital structure,these credit support levels translate to 7.00% credit support each from the class B and C notes,which is 14.0% total credit support for the class A(2020-1) notes.

Collateral Overview

We believe the receivables designated to the trust reflect a geographically diverse portfolio ofwell-seasoned prime accounts. The average credit limit and balance have been relatively stablefor the past several years. As of fourth-quarter 2019, accounts older than 60 months generated100% of the total receivables. In addition, the receivables representing FICO scores greater than720 have generally risen during the past several years, and FICO scores less than 660 havegenerally declined. As of Dec. 31, 2019, FICO scores greater than 720 comprised about 71.0% ofthe total trust, and FICO scores below 660 only represented about 8.58%. Assuming this pool'scollateral composition does not change, we believe the receivables will continue to perform well in2020 (see charts 1-3).

www.standardandpoors.com February 10, 2020 3

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

Chart 1

www.standardandpoors.com February 10, 2020 4

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

Chart 2

www.standardandpoors.com February 10, 2020 5

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

Chart 3

S&P Global Ratings' Credit Rating Assumptions

Generally, our base-case assumptions reflect our expectations for the trust's performance duringthe revolving period, based on trust-specific performance trends (i.e., delinquency, delinquencyroll rates, pool stratification quality and consistency, underwriting, and account management),trust performance relative to peers, and trust sensitivity to our forecast economic variables, suchas unemployment and bankruptcy rates (see table 1). For more information on our economicforecast, see "Global Structured Finance Outlook 2020: Another $1 Trillion-Plus Year On Tap,"published Jan 6, 2020, and for a more detailed description of credit card receivables performanceand collateral data for this trust compared with our credit card quality index (CCQI) and othertrusts we monitor, see "Quarterly U.S. Credit Card Quality Index: Stable Performance And IssuanceDecline Continues In Third-Quarter 2019," Dec. 5, 2019.

Our stress assumptions reflect our view of how performance variables could deteriorate in anearly amortization scenario (see table 1). The stresses we use are commensurate with 'AAA' levelrating scenarios and are based on our criteria (see "U.S. Credit Card Securitizations: MethodologyAnd Assumptions," published Aug. 24, 2017).

www.standardandpoors.com February 10, 2020 6

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

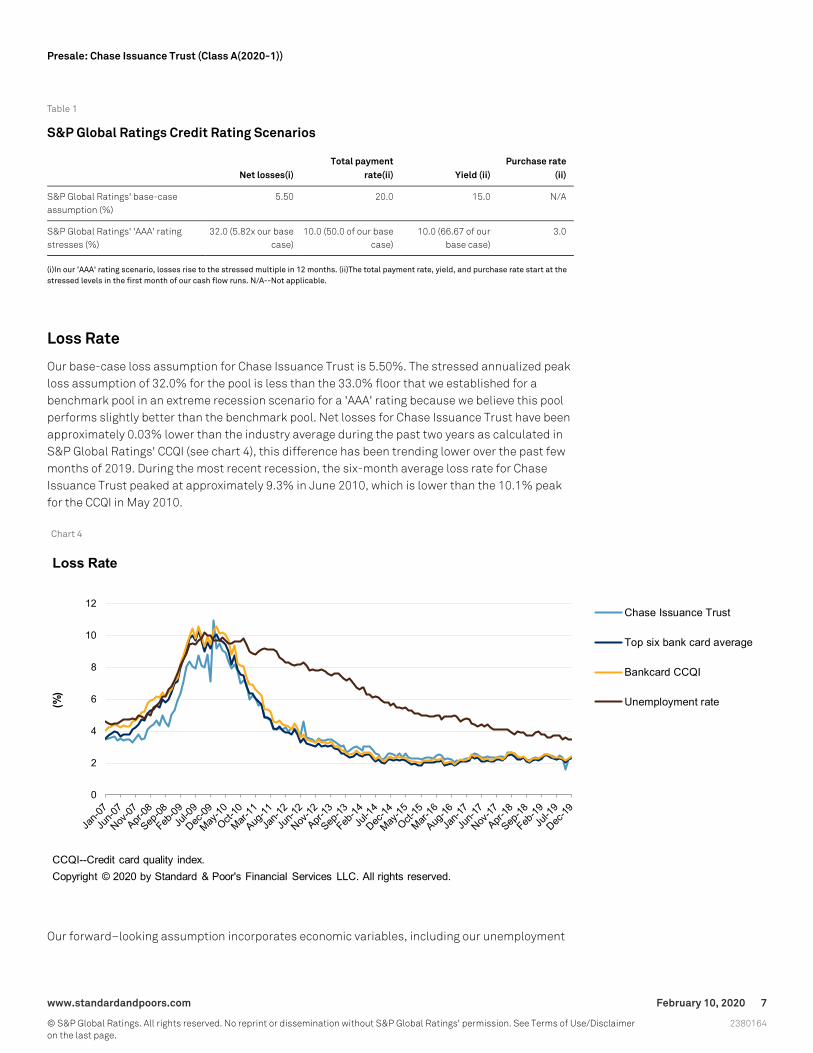

Table 1

S&P Global Ratings Credit Rating Scenarios

Net losses(i)Total payment

rate(ii) Yield (ii)Purchase rate

(ii)

S&P Global Ratings' base-caseassumption (%)

5.50 20.0 15.0 N/A

S&P Global Ratings' 'AAA' ratingstresses (%)

32.0 (5.82x our basecase)

10.0 (50.0 of our basecase)

10.0 (66.67 of ourbase case)

3.0

(i)In our 'AAA' rating scenario, losses rise to the stressed multiple in 12 months. (ii)The total payment rate, yield, and purchase rate start at thestressed levels in the first month of our cash flow runs. N/A--Not applicable.

Loss Rate

Our base-case loss assumption for Chase Issuance Trust is 5.50%. The stressed annualized peakloss assumption of 32.0% for the pool is less than the 33.0% floor that we established for abenchmark pool in an extreme recession scenario for a 'AAA' rating because we believe this poolperforms slightly better than the benchmark pool. Net losses for Chase Issuance Trust have beenapproximately 0.03% lower than the industry average during the past two years as calculated inS&P Global Ratings' CCQI (see chart 4), this difference has been trending lower over the past fewmonths of 2019. During the most recent recession, the six-month average loss rate for ChaseIssuance Trust peaked at approximately 9.3% in June 2010, which is lower than the 10.1% peakfor the CCQI in May 2010.

Chart 4

Our forward–looking assumption incorporates economic variables, including our unemployment

www.standardandpoors.com February 10, 2020 7

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

forecasts of 3.5% and 3.6% for 2020 and 2021, respectively, under our baseline economicscenario. We expect Chase's master trust loss rates to remain stable in 2020 based on the currentpool composition, low delinquency rates, and our macroeconomic forecasts.

Yield

Our 'AAA' stressed yield is 10.0%, which is 66.67% of the base case. The haircut applied to thistrust's yield is lower, relative to the example of the general range of stresses we publish in ourcriteria, because our cash flow yield input typically assumes 10.0%-13.0% in the 'AAA' stresslevel, and applying a higher haircut would result in an input well below that range. Our typicalrange of 10.0%-13.0% yield input at the 'AAA' stress level reflects our view that yield willimmediately decline in an amortization scenario because of competitive pressures, lowintroductory and promotional rates, and restrictive pricing regulations. Similar to other pools thatinclude high-quality prime cardholders, we believe this pool is less likely to experience a sharpincrease in delinquencies, resulting in less volatility in stressed yield than pools that include ahigher portion of nonprime accounts.

During the economic downturn, yield declined to 15.95% in 2008 from more than 18.0% in 2007and then increased to 20.22% in 2010. We believe the increase likely resulted from asset repricingin anticipation of the Credit Card Accountability, Responsibility, and Disclosure Act (The CARDAct), which took effect in 2009, and the 1.50% discount of principal receivables that began on June1, 2009. After the discount-option receivables were discontinued on July 1, 2010, yield declined to17.88% in 2011 and 17.51% in 2012 (see chart 5). We believe this pool's receivables historicallyhave not generated high yields because the pool includes mainly prime accounts, about 91.42% ofwhich have FICO scores higher than 660.

Chart 5

www.standardandpoors.com February 10, 2020 8

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

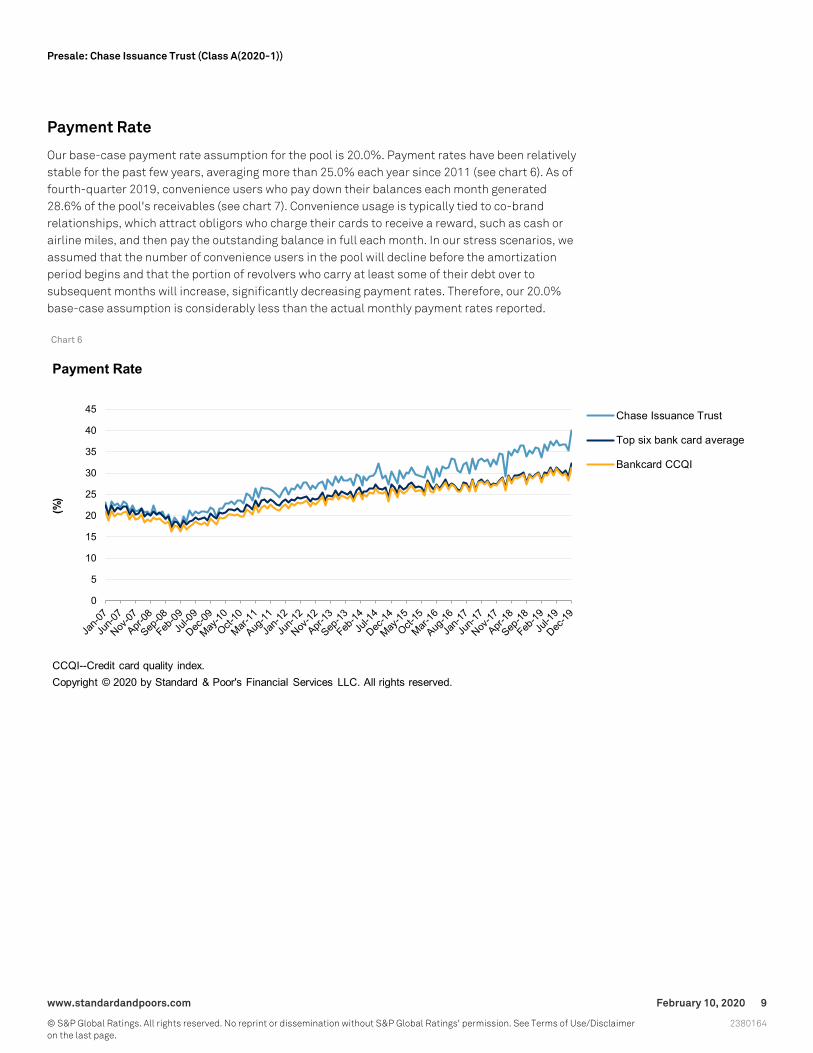

Payment Rate

Our base-case payment rate assumption for the pool is 20.0%. Payment rates have been relativelystable for the past few years, averaging more than 25.0% each year since 2011 (see chart 6). As offourth-quarter 2019, convenience users who pay down their balances each month generated28.6% of the pool's receivables (see chart 7). Convenience usage is typically tied to co-brandrelationships, which attract obligors who charge their cards to receive a reward, such as cash orairline miles, and then pay the outstanding balance in full each month. In our stress scenarios, weassumed that the number of convenience users in the pool will decline before the amortizationperiod begins and that the portion of revolvers who carry at least some of their debt over tosubsequent months will increase, significantly decreasing payment rates. Therefore, our 20.0%base-case assumption is considerably less than the actual monthly payment rates reported.

Chart 6

www.standardandpoors.com February 10, 2020 9

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

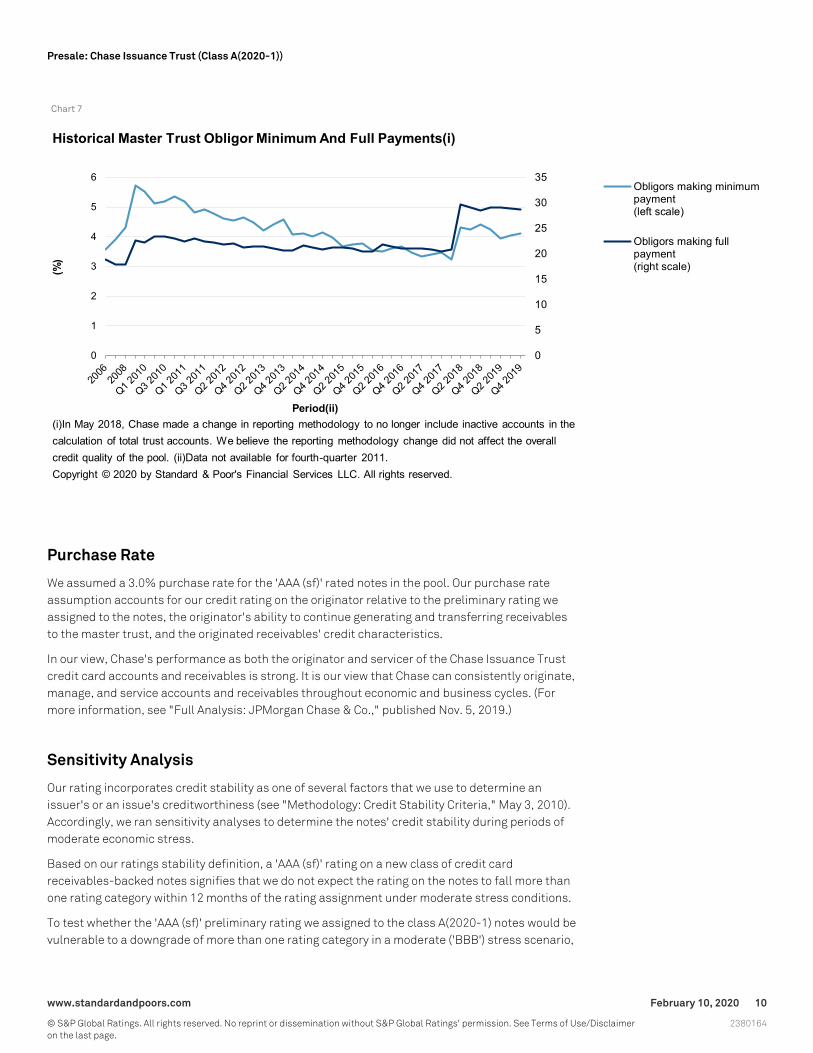

Chart 7

Purchase Rate

We assumed a 3.0% purchase rate for the 'AAA (sf)' rated notes in the pool. Our purchase rateassumption accounts for our credit rating on the originator relative to the preliminary rating weassigned to the notes, the originator's ability to continue generating and transferring receivablesto the master trust, and the originated receivables' credit characteristics.

In our view, Chase's performance as both the originator and servicer of the Chase Issuance Trustcredit card accounts and receivables is strong. It is our view that Chase can consistently originate,manage, and service accounts and receivables throughout economic and business cycles. (Formore information, see "Full Analysis: JPMorgan Chase & Co.," published Nov. 5, 2019.)

Sensitivity Analysis

Our rating incorporates credit stability as one of several factors that we use to determine anissuer's or an issue's creditworthiness (see "Methodology: Credit Stability Criteria," May 3, 2010).Accordingly, we ran sensitivity analyses to determine the notes' credit stability during periods ofmoderate economic stress.

Based on our ratings stability definition, a 'AAA (sf)' rating on a new class of credit cardreceivables-backed notes signifies that we do not expect the rating on the notes to fall more thanone rating category within 12 months of the rating assignment under moderate stress conditions.

To test whether the 'AAA (sf)' preliminary rating we assigned to the class A(2020-1) notes would bevulnerable to a downgrade of more than one rating category in a moderate ('BBB') stress scenario,

www.standardandpoors.com February 10, 2020 10

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

we ran sensitivity analyses assuming that the pool's base-case loss rate would increase toapproximately 2.23x the current base-case loss rate. In this scenario, we believe that our 'AAA (sf)'rating on the notes would not become vulnerable to a downgrade of more than one rating categorywithin 12 months of the rating assignment based on the 14.0% credit support available to thenotes.

Structural Overview

These notes are part of the CHASEseries, in which delinked tranches can be issued as long as theissuer meets certain conditions, such as ensuring sufficient subordination to provide the requiredcredit support. The notes are secured by credit card receivables generated by revolving credit cardaccounts owned by Chase or one of its affiliates.

Payment Priority

The issuer allocates available finance charge collections to the CHASEseries notes on eachdistribution date in the priority shown below (see table 2).

Table 2

Finance Charge Waterfall

Priority Payment

1 Accrued and unpaid interest on each class A note tranche.

2 Accrued and unpaid interest on each class B note tranche.

3 Accrued and unpaid interest on each class C note tranche.

4 Due and unpaid servicing fees.

5 Treat as available principal collections to cover the CHASEseries default amount.

6 Treat as available principal collections to cover the nominal liquidation amount deficit.

7 Deposit into the class C reserve account, if necessary.

8 Any other payments or deposits required for any tranche of notes.

9 Treat as shared excess available finance charge collections to cover finance charge shortfalls for otherseries, if any.

10 Treat as unapplied excess finance charge collections to cover finance charge shortfalls in anydesignated master trusts.

11 Pay to Chase Card Funding LLC as the transferor.

If an early redemption event occurs, all of the principal collections that the issuer allocates to theCHASEseries notes, in addition to the series' finance charge amounts available to reimbursecharged-off receivables and the subordinated notes' nominal liquidation amount deficits, will beavailable to make payments subject to the indenture supplement's cash flow provisions in thepriority outlined in the principal waterfall (see table 3).

www.standardandpoors.com February 10, 2020 11

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

Table 3

Principal Waterfall

Priority Payment

1 Cover interest shortfalls for each class A note tranche until their nominal liquidation amount or unusedsubordinated amount equals zero.

2 Cover interest shortfalls for each class B note tranche until their nominal liquidation amount or unusedsubordinated amount equals zero.

3 Cover servicing fee shortfalls for each class A and B note tranche until their nominal liquidation amounts orunused subordinated amounts equal zero.

4 Targeted deposits to the principal funding account for each class A note tranche.

5 Targeted deposits to the principal funding account for each class B note tranche.

6 Targeted deposits to the principal funding account for each class C note tranche.

7 Treat as shared excess available principal collections to cover principal shortfalls for other series, if any.

8 Deposit into an excess funding account until the required transferor amount and minimum pool balance arereached.

9 Pay to Chase Card Funding LLC as the transferor.

The early redemption events include:

- For any month, the three-month average excess spread percentage is less than zero.

- Chase fails to designate additional collateral certificates or credit card receivables for theissuer to include, or fails to increase an existing collateral certificate investment included in theissuing entity when either action is required.

- Any issuing entity servicer default occurs that has a materially adverse effect on thenoteholders.

- Chase's or Chase Card Funding LLC's ability to designate additional credit card receivables toinclude in the issuing entity or to designate additional credit card receivables for inclusion in asecuritization special-purpose entity that has issued a collateral certificate included in theissuing entity becomes restricted, causing either the pool balance to not meet the minimumpool balance or the transferor amount to not meet the required transferor amount, and theissuing entity fails to meet those tests for 10 days.

- An event of default occurs that causes a class or tranche of notes to accelerate.

- The issuing entity fails to fully pay a tranche of notes by its scheduled principal payment date.

- A scheduled principal payment date of a tranche of notes occurs.

- The issuing entity becomes an "investment company" under the Investment Company Act of1940 as amended.

- Chase experiences insolvency, conservatorship, or receivership.

Events of default include:

- The issuing entity fails to pay interest for 35 days on any tranche of notes when that interestbecomes due and payable.

- The issuing entity fails to pay the stated principal amount of any tranche of notes on itsapplicable legal maturity date.

www.standardandpoors.com February 10, 2020 12

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

- The issuing entity defaults in performance or breaches any of its covenants or warranties in theindenture for 90 days after either the indenture trustee or the holders of 25% of the affectedoutstanding note class' or tranche's aggregate outstanding dollar principal amount hasprovided written notice requesting that breach's remedy. In addition, the default materially andadversely affects the related noteholders' interests and continues to materially and adverselyaffect them during the 90-day period.

- The issuing entity becomes bankrupt or insolvent.

Related Criteria

- Criteria | Structured Finance | Legal: U.S. Structured Finance Asset Isolation AndSpecial-Purpose Entity Criteria, May 15, 2019

- Criteria | Structured Finance | General: Incorporating Sovereign Risk In Rating StructuredFinance Securities: Methodology And Assumptions, Jan. 30, 2019

- Criteria | Structured Finance | ABS: U.S. Credit Card Securitizations: Methodology AndAssumptions, Aug. 24, 2017

- Criteria | Structured Finance | General: Methodology: Criteria For Global Structured FinanceTransactions Subject To A Change In Payment Priorities Or Sale Of Collateral Upon ANonmonetary EOD, March 2, 2015

- Criteria - Structured Finance - General: Criteria Methodology Applied To Fees, Expenses, AndIndemnifications, July 12, 2012

- General Criteria: Global Investment Criteria For Temporary Investments In TransactionAccounts, May 31, 2012

- Criteria | Structured Finance | General: Methodology For Servicer Risk Assessment, May 28,2009

Related Research

- Global Structured Finance Outlook 2020: Another $1 Trillion-Plus Year On Tap, Jan. 6, 2020

- Quarterly U.S. Credit Card Quality Index: Stable Performance And Issuance Decline Continues InThird-Quarter 2019, Dec. 5, 2019

- Economic Research: Fewer Signs Of Scrooge-ing Up U.S. Growth In The New Year, Dec. 4, 2019

- Credit Conditions North America: Recession Risk Has Eased For Now, Dec. 3, 2019

- JPMorgan Chase & Co., Nov. 5, 2019

- With The Ongoing Lawsuits Against Two Securitization Entities, How Will Credit CardReceivables Asset-Backed Securities Be Affected?, Oct. 15, 2019

- 2019 U.S. And Canadian Credit Card ABS Review, Jan. 14, 2019

- Global Structured Finance Scenario And Sensitivity Analysis 2016: The Effects Of The Top FiveMacroeconomic Factors, Dec. 16, 2016

In addition to the criteria specific to this type of security (listed above), the following criteriaarticles, which are generally applicable to all ratings, may have affected this rating action:

www.standardandpoors.com February 10, 2020 13

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

"Counterparty Risk Framework: Methodology And Assumptions," March 8, 2019; "Post-DefaultRatings Methodology: When Does Standard & Poor's Raise A Rating From 'D' Or 'SD'?," March 23,2015; "Global Framework For Assessing Operational Risk In Structured Finance Transactions,"Oct. 9, 2014; "Methodology: Timeliness of Payments: Grace Periods, Guarantees, And Use of 'D'And 'SD' Ratings," Oct. 24, 2013; "Criteria For Assigning 'CCC+', 'CCC', 'CCC-', And 'CC' Ratings,"Oct. 1, 2012; "Methodology: Credit Stability Criteria," May 3, 2010; and "Use of CreditWatch AndOutlooks," Sept. 14, 2009.

www.standardandpoors.com February 10, 2020 14

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors.S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributedthrough other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available atwww.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respectiveactivities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has establishedpolicies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed andnot statements of fact. S&P's opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase,hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation toupdate the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment andexperience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not actas a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable,S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-relatedpublications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limitedto, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certainregulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Partiesdisclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damagealleged to have been suffered on account thereof.

Copyright © 2020 Standard & Poor's Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any partthereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrievalsystem, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not beused for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees oragents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are notresponsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or forthe security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESSOR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE ORUSE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THECONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct,indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, withoutlimitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advisedof the possibility of such damages.

Standard & Poor’s | Research | February 10, 2020 15

2380164

Presale: Chase Issuance Trust (Class A(2020-1))

![Garage Policy Issuance Guidelines Ed 0313 - … · Garage Policy Issuance Guidelines Ed. 01/13 [1]$ $ GARAGE POLICY ISSUANCE GUIDELINES 2013 Issuance Changes ... 32 As defined by](https://img.pdfslide.us/doc/110x75/5b91c6dd09d3f277288c7415/garage-policy-issuance-guidelines-ed-0313-garage-policy-issuance-guidelines.jpg)