Embed Size (px)

Citation preview

CHARLIE CRIST

GOVERNOR HOLLY BENSON SECRETARY

Vis i t AHCA on l i ne a t h t tp : / / ahca .myf lo r i da .com

2727 Mahan Dr i ve , MS#15 Ta l l ahassee , F lo r ida 32308

July 30, 2008 Prospective Respondent: Subject: Solicitation Number: AHCA ITN 0810 Health Benefits Coverage for Cover Florida Addendum No. 1 This addendum is being issued to provide written answers to submitted vendor questions. All other terms and conditions of the solicitation remain in effect. To the extent this Addendum gives rise to a protest, failure to file a protest within the time prescribed in section 120.57(3), Florida Statutes, shall constitute a waiver of proceedings under chapter 120, Florida Statutes.

Sincerely, Cathy McEachron Cathy McEachron, PMP, CPPB Director, AHCA Procurement Office Enclosures:

Addendum #1 (58 pages)

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

Question: Agency Response: Submitted by: Superior Insurance

Solutions

1 Will limited coverage for many segments of medical care be acceptable?

Yes. Section 408.9091 (4)(a) (3), Florida Statutes, and ITN 0810 states, that plans may provide for cost containment through limits on the number of services, caps on benefits payments, and copayments for services.

2 May the carriers spell-out the state health care mandates they wish to eliminate from their new "limited benefit health plan" response to your ITN?

Yes. The Agency would like to see respondents list and define both covered and non-covered state health care mandates in both coverage plans, including catastrophic.

3 Must they have to cover specialty providers?

Yes. The ITN requires respondents to list and provide specialty providers in each county for which it has indicated intent to provide services.

4 What about medicines? Is coverage for generic only required? Where do brand name drugs fit in? Will there be limits on hospital bed days?

Section 408.9091 (4) (a) 8, Florida Statutes, requires a prescription drug benefit. The choice of generic versus brand names drugs is up to the respondent. Yes, a respondent may limit the number of hospital bed days.

5 Another area is annual exams. No where in my calculations should our government step in and force the issue.

Section 408.9091 (4) 6 a, Florida Statutes, requires that the benefit package provide access to annual health assessments.

6 How will these plans fit into full service individual and group coverage? Actually, how will the new plans fit into the creditable coverage scheme of things?

The Cover Florida Plan is intended to provide low cost coverage to those who currently do not have existing coverage. The Agency, in consultation with the Centers for Medicare and Medicaid Services and the U.S. Department of Labor, has determined that Cover Florida Plan coverage is creditable coverage. This would also mean that a certificate of prior creditable coverage would offset any pre-existing condition limitation that the plan might have.

Submitted by: Cat Adjusters Insurance Services

7 Is this Agency planning to release a census as part of the solicitation? The census would

No. Some information can be obtained from the U.S. Census Bureau website, as well as from the University of Florida 2004 report on the

AHCA ITN 0810, Addendum No. 1, Page 1 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

include DOB or Age, Zip Code, Gender & Status EE, EC, ES, FAM.

Uninsured in Florida.

Submitted by: Affinity Group Underwriters, Inc.

8 On page 30 of the Cover Florida ITN (Appendix I, Section III -Benefits), there is a reference to a requirement that one of the plans submitted must provide “catastrophic coverage”. Catastrophic coverage is defined on page 4 of the ITN in terms of the types of services required but there is no reference to any minimum benefit amounts. Can you provide further clarification as to what would and would not be considered catastrophic coverage? For example, what if a plan paid a fixed benefit of $500 per day of hospitalization for up to 180 days per year?

Chapter Law 2008-32 and ITN 0810 allow for flexibility and do not define specific minimums for catastrophic coverage. Each respondent’s submission will be evaluated on the most robust and comprehensive benefits for Floridians.

Submitted by: Capital City Consulting, LLC

9 In SB 2534, which is the Cover Florida Legislation, provides on page 11, line 302, paragraph (b) that, (4) “The agency and the office may announce an invitation to negotiate for the design of Cover Florida Plus products to companies that offer supplemental insurance, discount medical plan organizations licensed under part II of chapter 636, or prepaid health clinics licensed under part II of chapter 641.” My question is, does the current ITN 0810 allow for the use of licensed discount medical plans for ancillary supplemental services such as

Another ITN is anticipated to offer ancillary supplemental services after the award of this ITN.

AHCA ITN 0810, Addendum No. 1, Page 2 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

AHCA ITN 0810, Add

endum No. 1, Page 3 of 58

prescription, dental, vision, hearing, etc in conjunction with the insurance product? Paragraph (4) above suggests that the Agency can issue a separate ITN for such services. Is another ITN anticipated for supplemental insurance, prepaid health clinic services, and discount medical plans?

10 It seems as though an insurer can contract with a licensed discount medical plan and offer supplemental services as part of the Cover Florida Plan because there are several areas where ancillary services are referenced. For example, on page 22 the third bullet point references prescription discount cards. On page 24, tab F refers to “Diagnostic, Laboratory, Vision, Hearing, and Other Ancillary Services” Finally, in appendix III on the bottom of page 3 of the Benefit Grid there is a spot for “Discount Cards.”

Do these discount medical plan services need to be offered by an insurer bidding on this ITN, or can a licensed discount medical plan organization also submit a proposal separate from the insurance product?

Yes, a respondent may provide a response to this ITN including ancillary services within the benefits of the plan proposal. However, a separate ITN for ancillary supplemental services is anticipated and will allow for greater flexibility in design and benefits. Section 408.9091 (4) (a) 8, Florida Statutes, relating to prescription drugs is the only benefit where the use of a discount card is specifically permitted. The reference to page 24 is the listing of the network of providers which will be providing the minimum services required in accordance with the ITN. A discount medical plan organization licensed in accordance with Chapter 636, Part II Florida Statues will generally not qualify as a Cover Florida Plan entity unless it otherwise qualifies in accordance with section 408.9091 (3)(d), Florida Statutes.

Submitted by: Florida Health Care Plans 11 Will the Agency consider responses from carriers

on a County by County basis rather than a District/Area basis?

Yes.

12 Must maternity be covered? Respondents are required to provide the minimum benefits and services listed in Chapter Law 2008-32 and ITN 0810. The agency would like to see respondents list and define any additional state health care mandates that will be provided.

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

13 If so, how is pregnancy treated relative to the pre-existing exclusion? For example, does an over-the-counter pregnancy test result constitute medical advice, diagnosis or treatment?

Pregnancy would be treated the same as any other condition, if the respondent provides coverage for pregnancy. If the plan is written through a qualified employer, pregnancy may have to be covered as required under Federal laws. Over-the-counter tests do not constitute medical advice, diagnosis or treatment for purposes of the pre-existing condition exclusion.

14 Can the health plan vary rates by age / gender? Can the rates vary by other factors, such as industry, group size or participation percentage for small group? Can small group rates differ from individual?

As addressed in the ITN, rate proposals may be submitted under four separate options. Respondents may be flexible in rate design; however, an actuarial memorandum must be included with each proposal and the benefits must be reasonable in relationship to the premiums charged.

15 The eligibility requirements say, among other things, ages 19-64. Does that mean children are not covered at all, even as dependents under their parents coverage? What about newborns if maternity is covered?

The policyholder must enroll between the ages of 19 and 64. Nothing in the ITN precludes the policyholder from requesting coverage for children. See page 29 of the ITN – individual and family policies will qualify.

Submitted by: Broward Health/North Broward Hospital District

16 I am an executive with Broward Health / North Broward Hospital District. Upon my reading of the ITN, it is vague in saying whether a Health or Hospital District can submit a proposal if it does not have an insurance license.

In fact, page 15 of 35 states that "if a respondent is not an insurer...it must provide the following documentation: ... d. if a Health Care District, a copy of the enabling statutory citation."

While this would indicate we could submit, subsequent language indicates the contrary -- again, pg. 15, " a responded must submit

Section 408.9091 (3)(d), Florida Statutes, allows a health care district to respond to the ITN and if it is selected, may become a Cover Florida Plan entity without being licensed as an insurer or health maintenance organization as long as it meets the other requirements in the ITN and Florida Statutes. The reference to Tab B on page 15, the third paragraph beginning with the word “Examples” is only meant to serve as examples of documents to be provided and is not all inclusive. As indicated on the top of page 16, the respondent must submit documentation of whatever kind to support that it is appropriately organized to operate in Florida and authorized by the governing body to conduct business in the State of Florida as a Cover Florida Plan entity. The time line is only if the respondent is not currently or at the time of

AHCA ITN 0810, Addendum No. 1, Page 4 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

evidence of its authority to operate as proposed in Florida...examples of adequate evidence include... a copy of insurer's certificate of authority ... or ... a copy of Health Care Provider Certificate.. if respondent is not yet authorized to conduct business... in the manner proposed... the respondent must detail the timeline for compliance..."

I interpret this to mean that while we as a Health Care District can submit a response that response would need to indicate how and when we are to become a licensed insurer or HMO. Further, the products offered under Cover Florida are clearly insurance / managed care products that are full risk and will require OIR and AHCA approval.

So my question is whether a Health or Hospital District must receive an insurance license to participate as a Cover Florida plan.

submission of the response to the ITN, operational.

Submitted by: BlueCross BlueShield of Florida

17 The ITN indicates an Executive Officer of the Company must sign the ITN Bid Proposal. All company officers routinely sign legally binding proposals on behalf of the company. Would an officer’s signature satisfy this requirement? If not, please define the term “Executive Officer”.

Any company officer that has been granted the authority to bind the company by the governing body of the organization would be able to sign the ITN on behalf of the organization.

18 The ITN indicates an Executive Officer of the Company must sign the ITN Bid Proposal. All company officers routinely sign legally binding

Yes.

AHCA ITN 0810, Addendum No. 1, Page 5 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

proposals on behalf of the company. Would an officer’s signature satisfy this requirement? If not, please define the term “Executive Officer”.

19 The ITN requires that three references for similar services be provided. Because this program is unique we have no similar programs in the market. Would references from major clients satisfy this requirement?

Yes.

20 Are there concerns with offering the plan to active employees that are 18 or younger or older than 64 years of age?

The policyholder must enroll between the ages of 19 and 64. Nothing in the ITN precludes the policyholder from requesting coverage for children. See page 29 of the ITN – individual and family policies will qualify.

21 What are the State’s plans to market the Cover Florida program? What marketing assistance will the State provide to Statewide and Regional plans?

The Agency and the Executive Office of the Governor plan to aggressively market the Cover Florida program. A website and initial efforts are under development, including assistance and staffing through the Gubernatorial Fellows Program. In addition, the ITN requires that the respondent develop a marketing plan.

22 Page 6 references bonus points for proposals that provide a procedure for assisting enrollees in negotiating hospital charges upon exhaustion of benefits for any one individual admission. Please confirm that this would pertain only to the catastrophic plan that offers hospital benefits for covered services and not to the non-catastrophic plan.

Yes. The bonus points would apply only to catastrophic plans.

23 What is the maximum number of points a bidder’s proposal can receive?

50 points per evaluator, including bonus points.

24 Information received prior to the release of the ITN suggested an expectation of a single statewide rate. The ITN offers rating alternatives. Please clarify whether there is a preferred approach.

The “approaches” are specified in the rating section of the ITN; there is no preferred approach.

25 Is a company able to stop selling its Cover Florida product if financial losses for the product are excessive?

No. The respondent is required to continue selling Cover Florida plans through the contract period. However, respondents may control loss ratios through benefit design, including: mandates, number of services, caps on benefit payments, and co-payments for services. In addition,

AHCA ITN 0810, Addendum No. 1, Page 6 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

respondents/contractors will be able to submit data on an annual basis to support modifications to rates. This will be specified in the contract and is subject to regulatory oversight by the Agency.

26 How will renewal rating be handled? Are their any restrictions on renewal rates?

The rating renewal process will generally be the same as the process outlined in the ITN. Rate adjustments at renewal are allowed if supported by the actuarial memorandum. Rate changes are subject to regulatory oversight by the Agency.

27 What is the State’s thinking and leaning with regard to promoting consumer choice and stimulating competition by offering many different Statewide and Regional plans?

The Agency has not made any predetermination on the number of contracts to be awarded. However, the agency looks forward to receiving many proposals and the ultimate goal is multiple, affordable plans that maximize consumer choice and stimulate competition.

28 Please explain and clarify the expectation on page 22 regarding "a detailed business plan including a proforma income statement covering the contract period for this line of business". This is difficult to do because of assumptions regarding enrollment, the number of companies that may be offered, the number of years of business results, etc required.

The Agency believes that the respondents would have a reasonable feel for how the marketplace, both competitors and purchasers, is going to react to this product. The respondent could conservatively assume that the competitive factors for this market will be the same as any other market a commercial program operates in.

29 Are the Cover Florida Plans selected by AHCA exempt from the standard OIR filing and renewal requirements/procedures for commercial health insurance products?

Chapter Law 2008-32 and ITN 0810 list specific Cover Florida filing and reporting requirements; however, these reporting requirements do not meet every aspect of the Insurance Code.

30 What are the procedures for an insurer to end participation in the Cover Florida program?

The contract will spell out the termination rights of each of the contracting parties.

31 What is the process for making benefit coverage changes for Cover Florida policies?

Benefit changes will be submitted to OIR in the same manner as those submitted with the ITN.

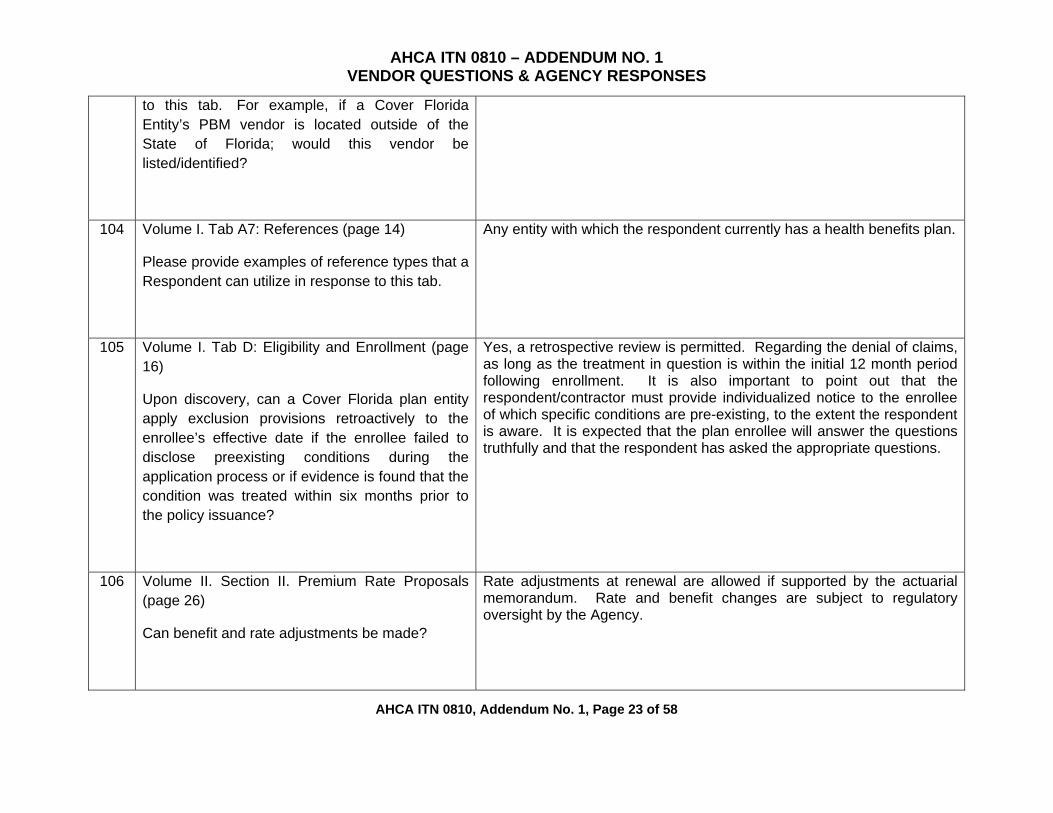

32 Please confirm that anyone meeting only those conditions identified in 408.9091 (7)(c) 1,2,3 or 4 can enroll outside of the insurer’s open enrollment periods.

That is partially correct; in addition children born to or adopted by the policyholder, and those persons in a Medicare, Medicaid or Kidcare program that are no longer eligible for those programs, can enroll outside of the entity’s open enrollment periods.

33 Would the State consider modifying the open enrollment period provisions on page 17 of the ITN to create a uniform time period for open enrollment?

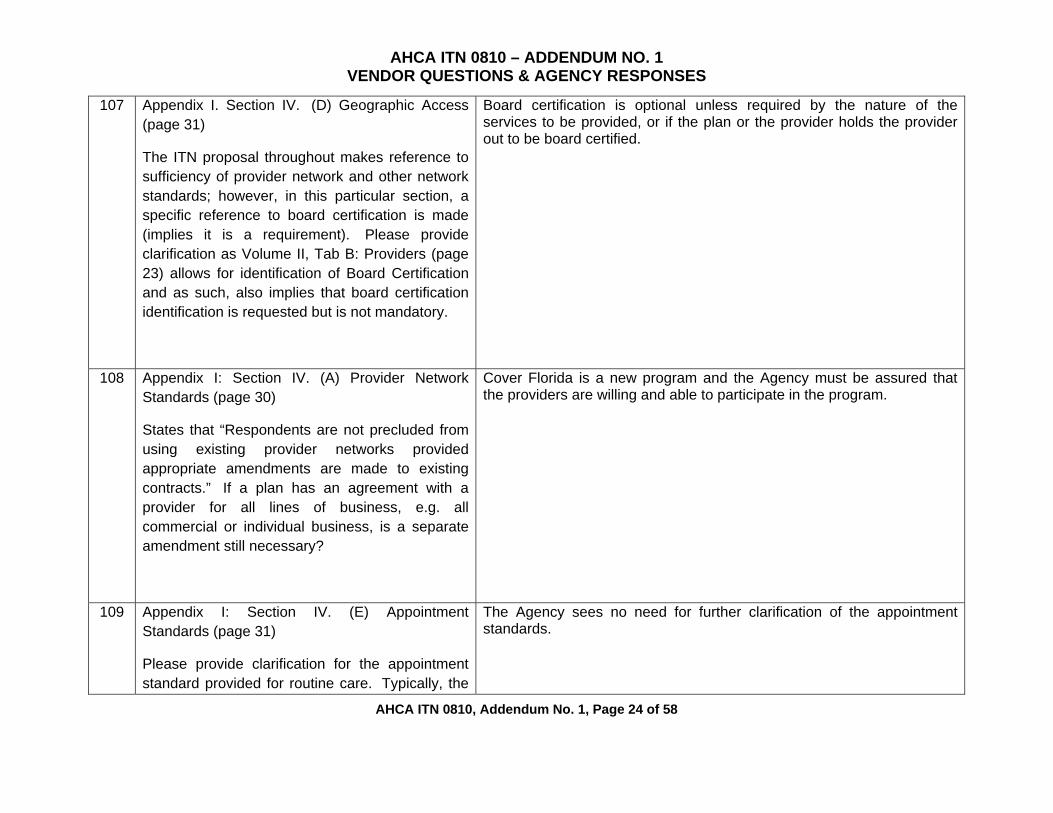

Yes.

Submitted by: Total Health Choice, Inc. AHCA ITN 0810, Addendum No. 1, Page 7 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

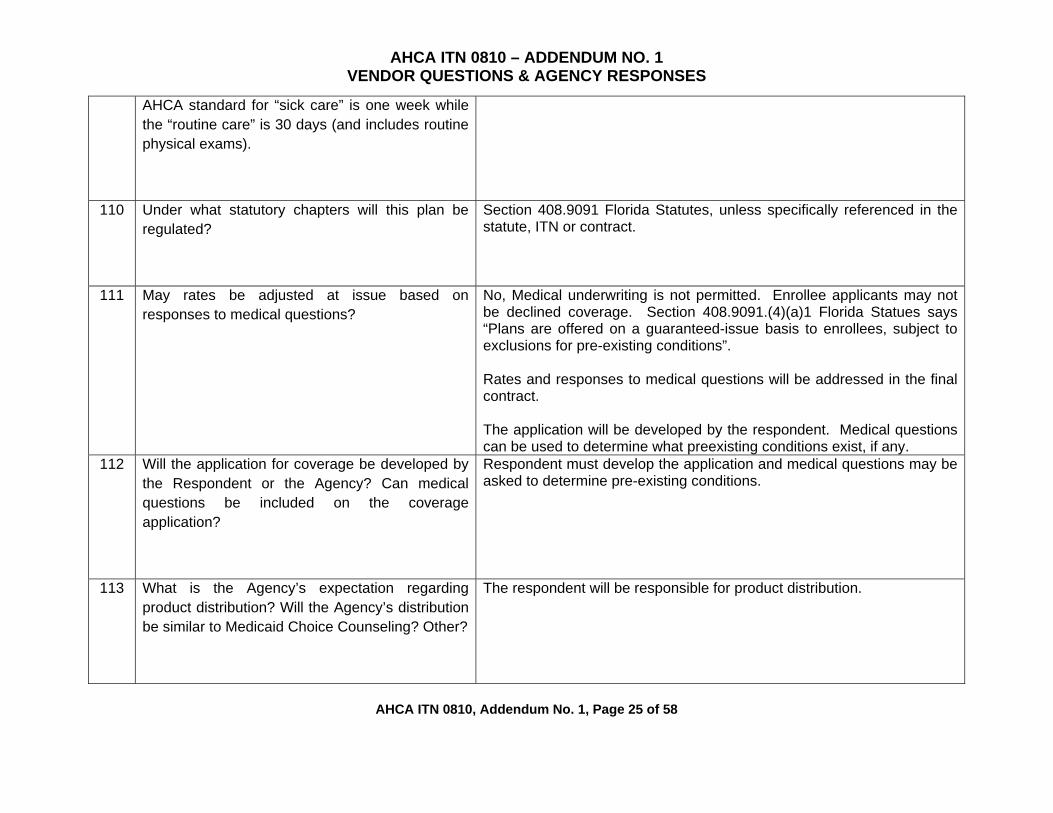

34 Page 3 of the ITN seems to indicate that non-statewide contracts will be issued based on AHCA District (“Agency anticipates issuance of additional contracts regionally, based on the existing Medicare Area structure”). The rate sections of the ITN (page 26, #4) reference rates by county. What is the smallest geographic area a proposal must cover? A District? A county? Other?

A county is the smallest geographic area a respondent can choose.

35 Is the policyholder responsible for 100% of the premium (assuming no employer contribution) or will the Agency/State subsidize the premium? If so, to what level?

No, state subsidization should not be anticipated during the initial contract period. However, 408.9091(4)(e), Florida Statutes, allows public or private entities to design programs to encourage Floridians to participate in Cover Florida or encourage employers to co-sponsor some share of the premium.

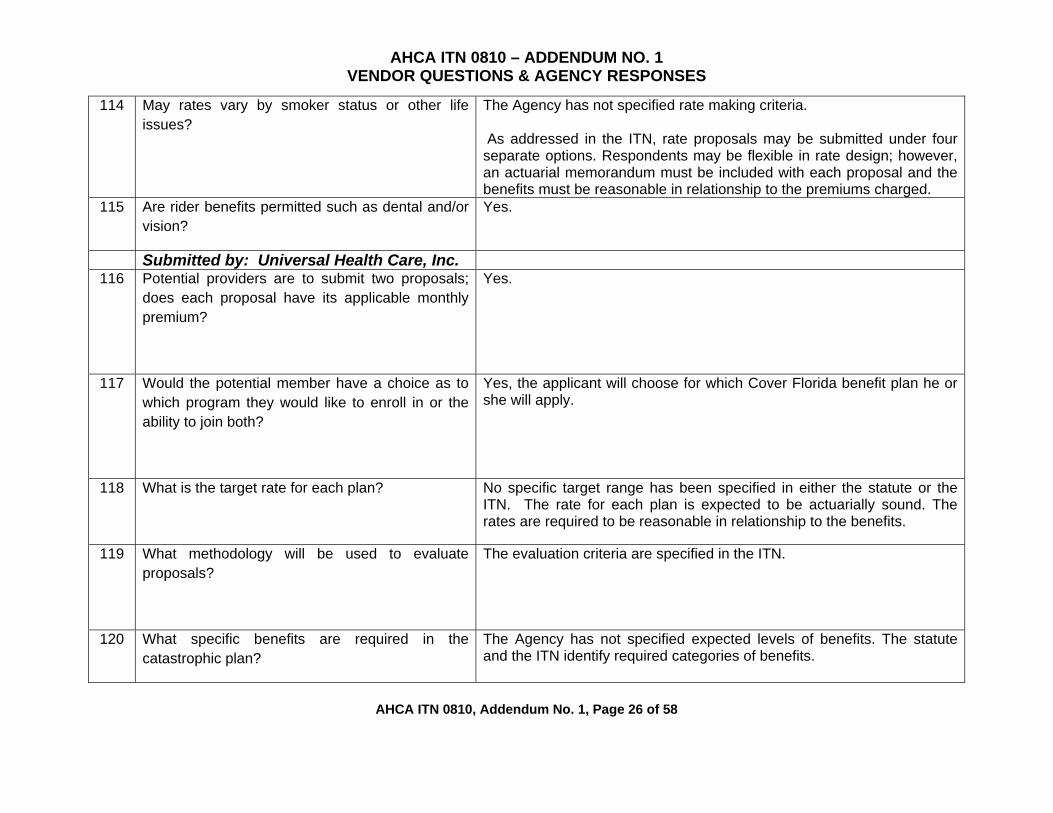

36 Page 22 of the ITN (first bullet) states that plans shall be issued on a guarantee renewable basis. Page 16, Tab D of the ITN, Section I states that coverage is guaranteed issue. Is any medical underwriting permitted? May applicants be declined based on responses to medical questions in the application? May rates be adjusted at issue based on responses to medical questions?

No, Medical underwriting is not permitted. Enrollee applicants may not be declined coverage. Section 408.9091.(4)(a)1 Florida Statues says “Plans are offered on a guaranteed-issue basis to enrollees, subject to exclusions for pre-existing conditions”. Rates and responses to medical questions will be addressed in the final contract.

37 Will the application for coverage be developed by the Respondent or the Agency? Can medical questions be included on the coverage application?

The application will be developed by the respondent. Medical questions can be used to determine what preexisting conditions exist, if any.

AHCA ITN 0810, Addendum No. 1, Page 8 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

38 Is a minimum required loss ratio defined for the product? If so, what is the minimum required loss ratio?

No.

39 What is the Agency’s expectation regarding product distribution? Broker/Agent distribution by Respondent? Agency distribution similar to Choice Counseling? Other?

The Agency has no expectations regarding marketing other than the respondent must submit a marketing plan and the implementation of that plan must be approved by OIR. The marketing plan must also comply with Part IX of Chapter 626, Florida Statutes.

40 Will retrospective review of pre-existing conditions be permitted? Specifically if a policyholder presents herself for treatment or if treatment is provided within twelve months of policy issuance and the Respondent subsequently reviews the case and finds evidence that the condition was treated within six months prior to policy issuance (but was not disclosed in the application), may the claim be denied?

Yes, a retrospective review is permitted. Regarding the denial of claims, as long as the treatment in question is within the initial 12 month period following enrollment. It is also important to point out that the respondent/contractor must provide individualized notice to the enrollee of which specific conditions are pre-existing, to the extent the respondent is aware. It is expected that the plan enrollee will answer the questions truthfully and that the respondent has asked the appropriate questions.

41 May applicants be required to pre-pay premium for several months? In other words may Respondent require the first six months of premium be paid at policy issuance?

Applicants may be offered a prepayment option for several months if appropriate discounts or other financial incentives to do so are offered and are included in the rate filing and are actuarially sound. Prepayment may not be required; however, if the policyholder terminates the coverage, any unearned premium must be refunded.

AHCA ITN 0810, Addendum No. 1, Page 9 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

42 May Respondents require premium payment be made by automatic bank transfer from the policyholder’s account? Alternatively, may the Respondent charge an additional (to the premium) fee for manual billing?

The respondent may not require premium payment by automatic transfer from policyholder account. However, they may offer it as an option to the applicant/policyholder. The respondent may not charge additional fees for administrative functions.

43

Is there a required rate format within a proposal? May rates vary by age and gender (which is a requirement for individual policies)? May rates vary by smoker status or other lifestyle issues?

As addressed in the ITN, rate proposals may be submitted under four separate options. Respondents may be flexible in rate design; however, an actuarial memorandum must be included with each proposal and the benefits must be reasonable in relationship to the premiums charged..

44 It is clear that at least two benefit plans must be offered; one benefit including the catastrophic benefit and one not including the catastrophic. May addition plans be offered within the same area? May 3 non-catastrophic and 2 with catastrophic be submitted by a single respondent in a single area?

While the statue and the ITN call for two plans, the agency will consider plans that provide additional options and choice for Florida consumers

45 May a Respondent offer a different rate for a policyholder covering dependents? In other words may a mother and dependent child be charged a different rate than the combined rate for an unrelated female and child?

Neither the statute nor the ITN specify specific rate structures. The only requirement is that the rates be actuarially sound.

46 Will the agency make available demographic data available showing the population by age, gender, county, etc. for the population eligible for

No. Some information can be obtained from the U.S. Census Bureau website, as well as from the University of Florida 2004 report on the Uninsured in Florida.

AHCA ITN 0810, Addendum No. 1, Page 10 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

coverage under Cover Florida?

47 Will a transcript of the bidders conference be made available?

No.

48 Are rider benefits permitted? With different eligibility/waiting periods than the policy benefits – such as a maternity rider with a 12-month waiting period?

Yes, except as it pertains to coverage through a qualified employer and requirements under federal law.

49 Who will determine whether or not an applicant meets the Cover Florida eligibility criteria?

The respondent/plan entity will be responsible for determining eligibility.

Submitted by: Medica Health Plans of Florida

50 Is there a possibility for an extension on the deadline for Receipt of Responses to the ITN?

It is not currently the Agency’s intent to change the timeline.

51 Plan design, could the carrier create an outpatient /preventive care only and an outpatient and catastrophic only? Or do they have to include professional services in both?

At least one proposal must include both.

52 Could the carrier offer a limited network (similar to an EPO) or do the HMO requirements still stand? In the Geographic Access section (pg.31), it indicates the 30/60 rule, is there a possibility that the 30/60 rule can be waived in areas other than

Yes, a network similar to an EPO is permissible; however it must have sufficient providers to provide benefits to be offered. Generally a waiver of the 30/60 measure is not granted in other than rural areas.

AHCA ITN 0810, Addendum No. 1, Page 11 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

rural residences?

53 Rating, if the policies are guaranteed issue, could the carrier adjust the rates up based medical experience (substandard rating)?

No. However the respondent does have the right to exclude pre-existing conditions as well as create a benefit design which provides for market flexibility. The experience of all of the Cover Florida coverage will be considered in the renewal rating.

54 Upon renewal, could the carrier adjust the rate table as the carriers do today with small group?

Rate adjustments at renewal are allowed if supported by the actuarial memorandum. Rate changes are subject to regulatory oversight by the Agency.

55 5 bonus points, if the interpretation is correct with regards to exhaustion of benefits, the carrier will assist in negotiating with the hospitals, such as attempt to reduce charges or balance billing? Or is the carrier required to offer a set rate or maximum charges allowable when the provider is participating?

The bonus points are for respondents who agree to provide plan enrollees with assistance in negotiating fees or charges with hospitals in the event that a hospital stay is longer than the benefit coverage provided by the respondent.

56 Could the references in Tab A7 (pg14), be either small group or individual currently enrolled in street plans?

Yes.

57 Tab (pg16), it appears that the proposed plan is similar to HIPPA in terms of eligibility? How is the eligibility validated and what is accepted/required in terms of evidence?

Yes, it is required by Federal Law that a preceding carrier must provide a certificate of creditable coverage.

AHCA ITN 0810, Addendum No. 1, Page 12 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

AHCA ITN 0810, Addendum No. 1, Page 13 of 58

58 Could the carrier use the HIPPA model to create the enrollment application and forms? Or will there be a universal Cover Florida enrollment form?

Each contractor will provide their own application form.

59 How are terminations handled when member is no longer eligible or loses eligibility/out of service area/non payment of premiums? Could the carrier rescind for misrepresentation? Is the carrier allowed re-verify eligibility upon renewal?

A plan enrollee must be given notice of non-renewal for whatever the reason. A carrier may rescind coverage for material misrepresentation. The Cover Florida Plan coverage is guaranteed issue and guaranteed renewable. Once the policy is issued it is renewable regardless of the change in initial eligibility. In addition, respondents/contractors will be able to submit data on an annual basis to support modifications to rates. This will be specified in the contract and is subject oversight by the Agency.

60 Page 17, regarding the open enrollment period in 2010, would this be similar to 1-life groups at point of renewal? How will the carriers restrict the enrollment period during various times during a calendar year? Need more clarification as to the “90day of open enrollment”.

Open enrollment is to accept applications for new enrollment and has nothing to do with renewal. The ITN specifies that the plan entity must have a cumulative 90 days of open enrollment in the calendar year. Each enrollment period must be at least 30 days long. For example a plan could have open enrollment for 90 consecutive days any time during the year. It could have 3 different open enrollment periods each one lasting 30 days.

61 Pg 18, regarding marketing material, would adding Creole qualify?

The ITN and the Statute require the marketing and benefit materials to be in English and Spanish. If the respondent chooses to add Creole it is certainly permitted.

62 Enrollment cutoffs, what are they? There are no enrollment cutoffs. Cover Florida plans must be offered on

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

a guaranteed issue basis.

63 Page 11, references employer qualified plans s.125, yet it must be individually portable. Does this plan fall under a group or individual policy?

Both. If the plan enrollee is initially enrolled in a group plan and leaves the group, they must be able to continue coverage outside the group as long as the premium is paid.

64 TabA (pg21) Benefits- this section speaks to plans offered through qualified employer groups. Currently Individual coverage is not considered to be valid waiver for employees applying for group coverage. Would this be a product such as the old Champus be considered a legitimate waiver?

The Agency is unclear as to the nature of the information sought. However, generally, an employer may designate a Cover Florida plan as a group health plan for purposes of the Internal Revenue Code (Section 125) and the employee may pay premiums on a pre-tax basis.

65 How would the applicant qualify for this product if they are currently employed? This section contradicts with the program eligibility section (pg29). Please clarify?

If the applicant is currently employed and has group coverage, then he or she would not qualify unless there is a qualifying event which makes the person eligible. However, if he or she is employed but has no insurance, he or she would qualify for coverage

66 Regarding prescription benefits, could the carrier offer a limited benefit (such as high caps and generic only)?

The statue and the ITN require provision of a prescription drug benefit. The respondent chooses how to structure the benefit. Section 408.9091 (4)(a)3 allows cost containment through limits in services, caps on benefit payments and copayments.

AHCA ITN 0810, Addendum No. 1, Page 14 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

67 Section V (pg. 32), regarding the issuance of Id cards, is the carrier required to issue the id and handbook with in 5 days of acceptance or effective date? In other words if the carrier accept an application on 1/15/09, is the carrier required to have it delivered by 1/20/09? Please clarify if the acceptance is the same as the effective date of the policy?

Within 5 days of acceptance. That is not generally the same as the effective date of coverage although it could be.

68 Why must the carrier issue a separate contract or amendment to providers for the Cover Florida plan when the Commercial contracts include “all payer” language? Is the Cover Florida plan a commercial or Medicaid line of business?

The Agency needs reasonable assurance that the providers submitted as part of a respondent’s network have in fact agreed to participate in the Cover Florida Health Access Program. Cover Florida is not a Medicaid line of business.

69 If so, does it include Hospitals, ancillaries?

It would include any provider that is presented to the Agency as part of the respondent’s response to the ITN.

70 What reporting requirements are necessary (pg6)? Monthly/ quarterly?

All reporting requirements will be spelled out in the contract. Some examples are updated network files, grievances received, and the number of covered lives by county.

71 Competitiveness of premium rate, what is the premium range (ex. $100-150, not to exceed X)?

Neither the ITN nor the statute specify a rate range. The purpose of the Cover Florida Plan is to provide affordable coverage to the uninsured.

AHCA ITN 0810, Addendum No. 1, Page 15 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

AHCA ITN 0810, Addendum No. 1, Page 16 of 58

as previous noted in the Bill Analysis.

72 Page 10, is the Agency considering awarding contracts to multiple respondents statewide and in Medicaid service areas?

The Agency has not made any predetermination on the number of contracts to be awarded. However, the agency looks forward to receiving many proposals and the ultimate goal is affordable plans that maximize consumer choice and stimulate competition.

73 Regarding the GEO Access data file, are the providers required to be board certified or is the data file simply asking the status “if yes, or no”?

The data file asks for the status only.

74 What is the contract period? 1/1/09-1/1/10?

The contract period has not been finalized; however, it will likely be a two year contract.

75 Regarding the business plan on pg.22, what is implied by detail plan? Complete business plan or specific to this product?

The Agency believes that the respondents would have a reasonable feel for how the marketplace, both competitors and purchasers, is going to react to this product. The respondent could conservatively assume that the competitive factors for this market will be the same as any other market a commercial program operates in. The business plan should cover the Cover Florida product only.

76 If a complete business plan is required, what are the elements the State is looking for?

The elements should be those elements the respondent deems appropriate to allow the Agency to understand the goals of the plan and evaluate the network based upon that plan. Any material underlying assumptions should also be described in the response.

77 Regarding the Performa, is this for the entity or the Cover Florida plan only? And for how many years?

Cover Florida Plan only and for a minimum of the contract period which is likely to be two years.

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

AHCA ITN 0810, Add

endum No. 1, Page 17 of 58

78 Page 29, indicates eligibility is between 19-64, however it also states that families could apply through a qualified employer? Please clarify if this an individual policy, how will dependent or family coverage be administered?

The policyholder must enroll between the ages of 19 and 64. Nothing in the ITN precludes the policyholder from requesting coverage for children. See page 29 of the ITN – individual and family policies will qualify.

79 Page 3 of the ITN seems to indicate that non-statewide contracts will be issued based on AHCA District (“Agency anticipates issuance of additional contracts regionally, based on the existing Medicare Area structure”). The rate sections of the ITN (page 26, #4) reference rates by county. What is the smallest geographic area a proposal must cover? A District? A county? Other?

The smallest geographic service area is a county.

80 Is the policyholder responsible for 100% of the premium (assuming no employer contribution) or will the Agency/State subsidize the premium? If so, to what level?

No, state subsidization should not be anticipated during the initial contract period. However, 408.9091(4)(e), Florida Statutes, allows public or private entities to design programs to encourage Floridians to participate in Cover Florida or encourage employers to co-sponsor some share of the premium.

81 Page 22 of the ITN (first bullet) states that plans shall be issued on a guarantee renewable basis. Page 16, Tab D of the ITN, Section I states that coverage is guaranteed issue. Is any medical underwriting permitted? May applicants be

No, Medical underwriting is not permitted. Enrollee applicants may not be declined coverage. Section 408.9091.(4)(a)1 Florida Statues says “Plans are offered on a guaranteed-issue basis to enrollees, subject to exclusions for pre-existing conditions”. Rates and responses to medical questions will be addressed in the final

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

declined based on responses to medical questions in the application? May rates be adjusted at issue based on responses to medical questions?

contract.

82 Will the application for coverage be developed by the Respondent or the Agency? Can medical questions be included on the coverage application?

The application will be developed by the respondent. Medical questions can be used to determine what preexisting conditions exist, if any.

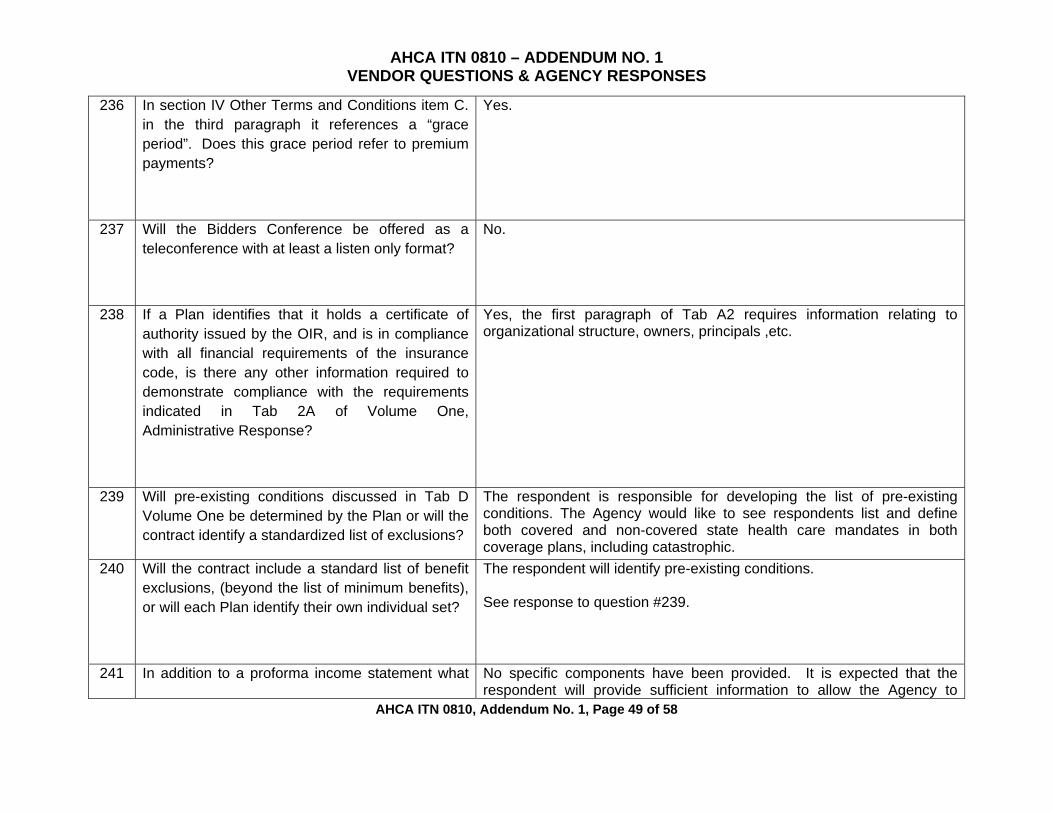

83 Is a minimum required loss ratio defined for the product? If so, what is the minimum required loss ratio?

No.

84 What is the Agency’s expectation regarding product distribution? Broker/Agent distribution by Respondent? Agency distribution similar to Choice Counseling? Other?

The Agency has no expectations regarding marketing other than the respondent must submit a marketing plan and the implementation of that plan must be approved by OIR. The marketing plan must also comply with Part IX of Chapter 626, Florida Statutes.

85 Will retrospective review of pre-existing conditions be permitted? Specifically if a policyholder presents herself for treatment or if treatment is provided within twelve months of policy issuance and the Respondent subsequently reviews the case and finds evidence that the condition was

Yes, a retrospective review is permitted. Regarding the denial of claims, as long as the treatment in question is within the initial 12 month period following enrollment. It is also important to point out that the respondent/contractor must provide individualized notice to the enrollee of which specific conditions are pre-existing, to the extent the respondent is aware. It is expected that the plan enrollee will answer the questions truthfully and that the respondent has asked the appropriate questions. .

AHCA ITN 0810, Addendum No. 1, Page 18 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

treated within six months prior to policy issuance (but was not disclosed in the application), may the claim be denied?

86 May applicants be required to pre-pay premium for several months? In other words may Respondent require the first six months of premium be paid at policy issuance?

Applicants may be offered a prepayment option for several months if appropriate discounts or other financial incentives to do so are offered and are included in the rate filing and are actuarially sound. Prepayment may not be required; however, if prepayment occurs and the policyholder terminates the coverage, any unearned premium must be refunded.

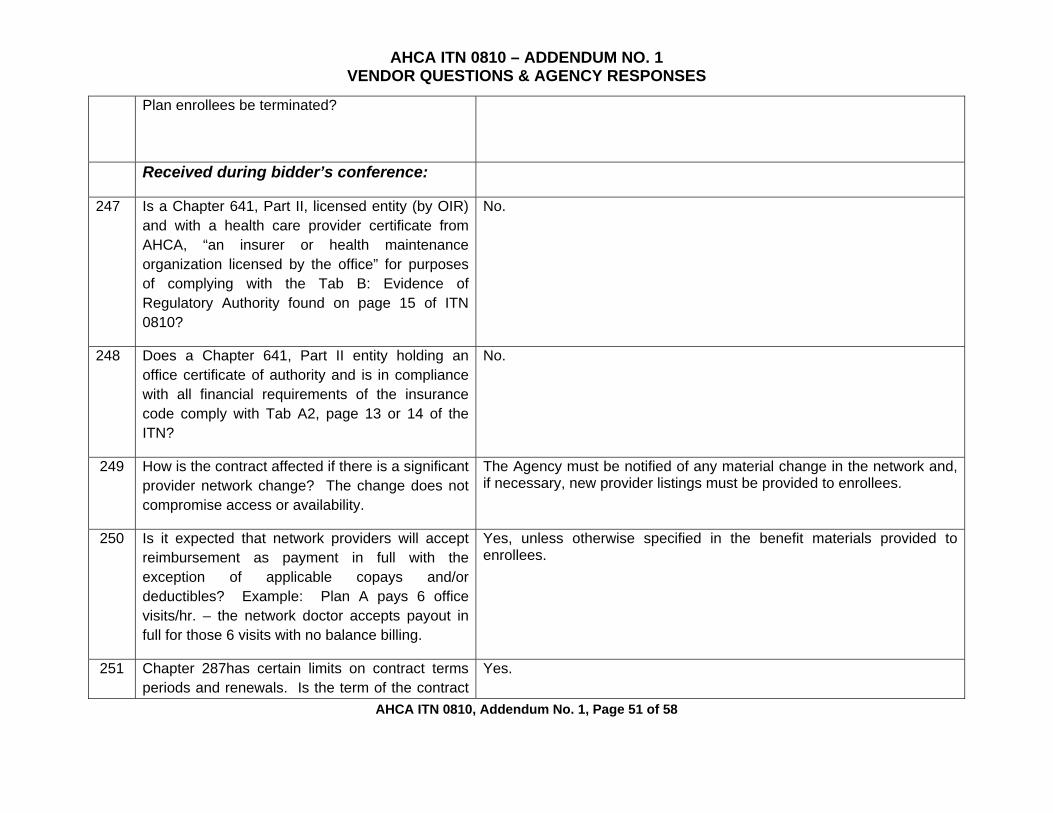

87 May Respondents require premium payment be made by automatic bank transfer from the policyholder’s account? Alternatively, may the Respondent charge an additional (to the premium) fee for manual billing?

The respondent may not require premium payment by automatic transfer from policyholder account. However, they may offer it as an option to the applicant/policyholder. The respondent may not charge additional fees for administrative functions.

88 Is there a required rate format within a proposal? May rates vary by age and gender (which is a requirement for individual policies)? May rates vary by smoker status or other lifestyle issues?

As addressed in the ITN, rate proposals may be submitted under four separate options. Respondents may be flexible in rate design; however, an actuarial memorandum must be included with each proposal and the benefits must be reasonable in relationship to the premiums charged.

89 It is clear that at least two benefit plans must be offered; one benefit including the catastrophic benefit and one not including the catastrophic. May addition plans be offered within the same area? May 3 non-catastrophic and 2 with

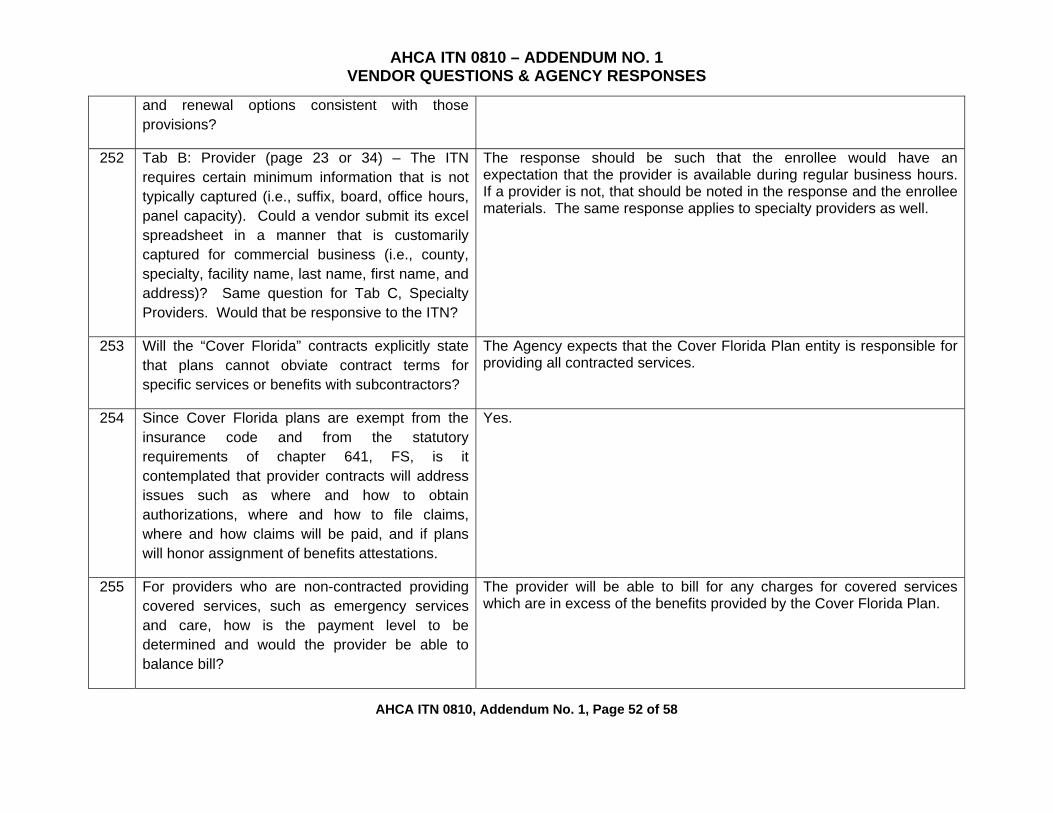

While the statue and the ITN call for two plans, the agency will consider plans that provide additional options and choice for Florida consumers

AHCA ITN 0810, Addendum No. 1, Page 19 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

catastrophic be submitted by a single respondent in a single area?

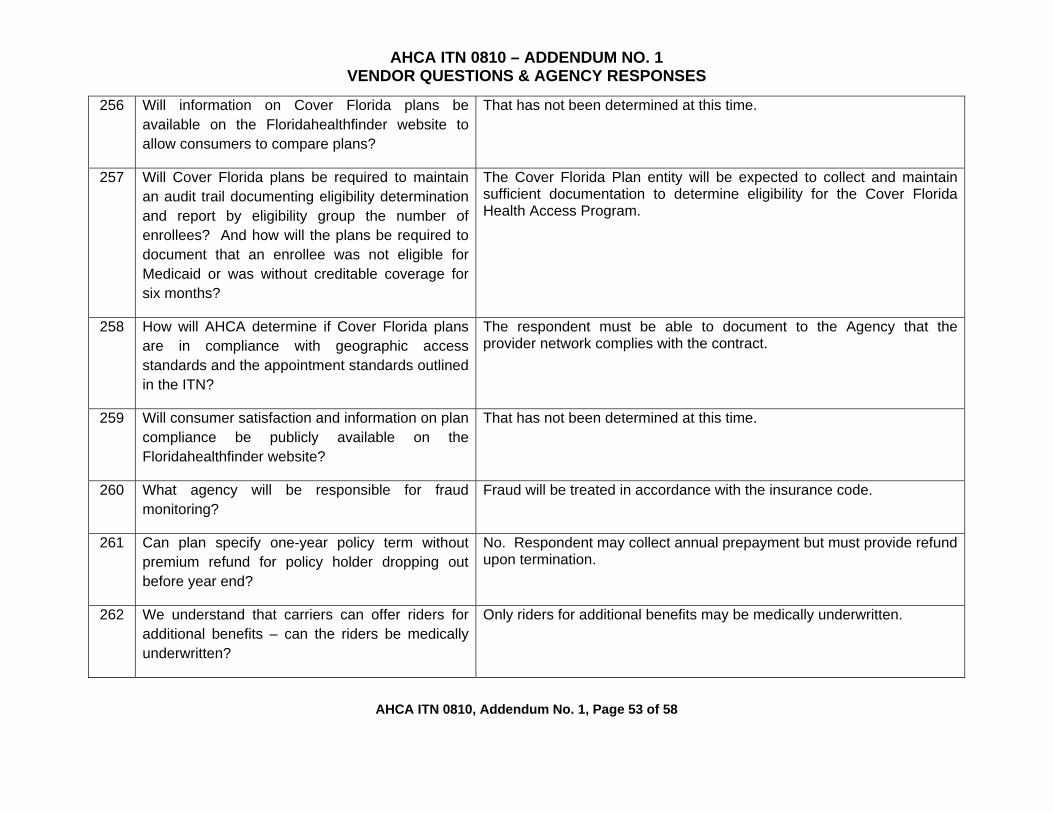

90 May a Respondent offer a different rate for a policyholder covering dependents? In other words may a mother and dependent child be charged a different rate than the combined rate for an unrelated female and child?

Neither the statute nor the ITN specify rate structures. The only requirement is that the rates be actuarially sound.

91 Will the agency make available demographic data available showing the population by age, gender, county, etc. for the population eligible for coverage under Cover Florida?

No. Some information can be obtained from the U.S. Census Bureau website, as well as from the University of Florida 2004 report on the Uninsured in Florida.

92 Will a transcript of the bidder’s conference be made available?

No.

93 Are rider benefits permitted? With different eligibility/waiting periods than the policy benefits – such as a maternity rider with a 12-month waiting period?

Yes, except as it pertains to coverage through a qualified employer and requirements under federal law.

Submitted by: Preferred Medical Plan 94 Volume II. Tab E: Proposed Pharmacy Network

(page 24) For pharmacies that are part of a major/retail chain, in lieu of listing each individual pharmacy location/address, would it suffice to list only the name of the pharmacy chain, e.g. Walgreens,

Yes, as long as all locations in Florida honor the contract. The respondent must affirmatively state that in the response to the ITN.

AHCA ITN 0810, Addendum No. 1, Page 20 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

CVS, etc.?

95 Section III. Procurement Process- Factors to be

evaluated (page 5)

How will the “sufficiency of the proposed provider network” be tested or determined? Will the AHCA method for determining network sufficiency be utilized or another method?

The evaluators will review the network in relation to the benefits offered and the expected numbers of enrollees projected to participate.

96 Section III. Procurement Process- Factors to be evaluated (page 6)

What are the reporting requirements that the Respondent must comply with?

All reporting requirements will be spelled out in the contract. Some examples are updated network files, grievances received, number of covered lives by county.

97 Appendix I: Background Information, Section II. Enrollment (page 29)

Please clarify which entity will manage the on-line application process.

Each respondent will be responsible for processing applications for coverage including on-line application processing.

98 Volume II. Tab A: Benefits (page 23)

Will State resources be provided for the marketing of approved Cover Florida products?

The Agency and the Executive Office of the Governor plan to aggressively market the Cover Florida program. A website and initial efforts are under development, including assistance and staffing through the Gubernatorial Fellows Program. In addition, the ITN requires that the respondent develop a marketing plan.

AHCA ITN 0810, Addendum No. 1, Page 21 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

99 Volume I. Tab E: Program Management (page 17)

What are the specific marketing guidelines for the Cover Florida plan entities? Can an employee of the Cover Florida plan entity enroll an applicant?

The Agency has no expectations regarding marketing other than the respondent must submit a marketing plan and the implementation of that plan must be approved by OIR. The marketing plan must also comply with Part IX of Chapter 626, Florida Statutes.

100 Volume I. Tab G: Contract (page 20)

What is the length of the Contract period for the initial inception and subsequent renewals?

The initial contract period is expected to be two years with the possibility of three (3) one (1) year renewals as agreed upon.

101 If a Cover Florida plan entity wishes to terminate the Contract, what is the notification period?

The contract will provide information on the termination rights.

102 Volume I. Tab D: Eligibility and Enrollment (page 16)

Will enrollees be allowed to dis-enroll and re-enroll between Cover Florida plan entities at any time?

No. Any enrollee that terminates voluntarily may not re-apply for coverage more than once per calendar year.

103 Volume I. Tab A4: Contracted services and locations(page 14)

Please clarify which services with vendors/subcontractors must be listed in response

Yes, any administrative services which are provided by a subcontractor must be listed in this section.

AHCA ITN 0810, Addendum No. 1, Page 22 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

to this tab. For example, if a Cover Florida Entity’s PBM vendor is located outside of the State of Florida; would this vendor be listed/identified?

104 Volume I. Tab A7: References (page 14)

Please provide examples of reference types that a Respondent can utilize in response to this tab.

Any entity with which the respondent currently has a health benefits plan.

105 Volume I. Tab D: Eligibility and Enrollment (page 16)

Upon discovery, can a Cover Florida plan entity apply exclusion provisions retroactively to the enrollee’s effective date if the enrollee failed to disclose preexisting conditions during the application process or if evidence is found that the condition was treated within six months prior to the policy issuance?

Yes, a retrospective review is permitted. Regarding the denial of claims, as long as the treatment in question is within the initial 12 month period following enrollment. It is also important to point out that the respondent/contractor must provide individualized notice to the enrollee of which specific conditions are pre-existing, to the extent the respondent is aware. It is expected that the plan enrollee will answer the questions truthfully and that the respondent has asked the appropriate questions.

106 Volume II. Section II. Premium Rate Proposals (page 26)

Can benefit and rate adjustments be made?

Rate adjustments at renewal are allowed if supported by the actuarial memorandum. Rate and benefit changes are subject to regulatory oversight by the Agency.

AHCA ITN 0810, Addendum No. 1, Page 23 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

107 Appendix I. Section IV. (D) Geographic Access (page 31)

The ITN proposal throughout makes reference to sufficiency of provider network and other network standards; however, in this particular section, a specific reference to board certification is made (implies it is a requirement). Please provide clarification as Volume II, Tab B: Providers (page 23) allows for identification of Board Certification and as such, also implies that board certification identification is requested but is not mandatory.

Board certification is optional unless required by the nature of the services to be provided, or if the plan or the provider holds the provider out to be board certified.

108 Appendix I: Section IV. (A) Provider Network Standards (page 30)

States that “Respondents are not precluded from using existing provider networks provided appropriate amendments are made to existing contracts.” If a plan has an agreement with a provider for all lines of business, e.g. all commercial or individual business, is a separate amendment still necessary?

Cover Florida is a new program and the Agency must be assured that the providers are willing and able to participate in the program.

109 Appendix I: Section IV. (E) Appointment Standards (page 31)

Please provide clarification for the appointment standard provided for routine care. Typically, the

The Agency sees no need for further clarification of the appointment standards.

AHCA ITN 0810, Addendum No. 1, Page 24 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

AHCA standard for “sick care” is one week while the “routine care” is 30 days (and includes routine physical exams).

110 Under what statutory chapters will this plan be regulated?

Section 408.9091 Florida Statutes, unless specifically referenced in the statute, ITN or contract.

111 May rates be adjusted at issue based on responses to medical questions?

No, Medical underwriting is not permitted. Enrollee applicants may not be declined coverage. Section 408.9091.(4)(a)1 Florida Statues says “Plans are offered on a guaranteed-issue basis to enrollees, subject to exclusions for pre-existing conditions”. Rates and responses to medical questions will be addressed in the final contract. The application will be developed by the respondent. Medical questions can be used to determine what preexisting conditions exist, if any.

112 Will the application for coverage be developed by the Respondent or the Agency? Can medical questions be included on the coverage application?

Respondent must develop the application and medical questions may be asked to determine pre-existing conditions.

113 What is the Agency’s expectation regarding product distribution? Will the Agency’s distribution be similar to Medicaid Choice Counseling? Other?

The respondent will be responsible for product distribution.

AHCA ITN 0810, Addendum No. 1, Page 25 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

114 May rates vary by smoker status or other life issues?

The Agency has not specified rate making criteria. As addressed in the ITN, rate proposals may be submitted under four separate options. Respondents may be flexible in rate design; however, an actuarial memorandum must be included with each proposal and the benefits must be reasonable in relationship to the premiums charged.

115 Are rider benefits permitted such as dental and/or vision?

Yes.

Submitted by: Universal Health Care, Inc. 116 Potential providers are to submit two proposals;

does each proposal have its applicable monthly premium?

Yes.

117 Would the potential member have a choice as to which program they would like to enroll in or the ability to join both?

Yes, the applicant will choose for which Cover Florida benefit plan he or she will apply.

118 What is the target rate for each plan?

No specific target range has been specified in either the statute or the ITN. The rate for each plan is expected to be actuarially sound. The rates are required to be reasonable in relationship to the benefits.

119 What methodology will be used to evaluate proposals?

The evaluation criteria are specified in the ITN.

120 What specific benefits are required in the catastrophic plan?

The Agency has not specified expected levels of benefits. The statute and the ITN identify required categories of benefits.

AHCA ITN 0810, Addendum No. 1, Page 26 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

121 What are the specific benefits required for the regular plan?

The Agency has not specified expected levels of benefits. The statute and the ITN identify required categories of benefits.

122 Will maternity be covered? If so, how is pregnancy treated relative to the pre-existing exclusion? For example, does an over-the-counter pregnancy test result constitute medical advice, diagnosis or treatment? The eligibility requirements say, among other things, ages 19-64. Does that mean children are not covered at all, even as dependents under their parent’s coverage? What about newborns if maternity is covered?

Respondents are required to provide the minimum benefits and services listed in Chapter Law 2008-32 and ITN 0810. The agency would like to see respondents list and define any additional state health care mandates that will be provided. Pregnancy would be treated the same as any other condition, if the respondent provides coverage for pregnancy. If the plan is written through a qualified employer, pregnancy may have to be covered as required under Federal laws. Over-the-counter tests do not constitute medical advice, diagnosis or treatment for purposes of the pre-existing condition exclusion. The age requirement applies to the policyholder. If the policyholder and respondent wish to have spouse and children included that would be permitted. The policyholder must enroll between the ages of 19 and 64. Nothing in the ITN precludes the policyholder from requesting coverage for children. See page 29 of the ITN – individual and family policies will qualify.

AHCA ITN 0810, Addendum No. 1, Page 27 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

AHCA ITN 0810, Addendum No. 1, Page 28 of 58

123 What are the expectations for potential members that have HIV/AIDS?

Pre-existing conditions may be excluded as specified in the ITN. Once any applicable exclusion period expires, the Agency expects the respondent to provide coverage up to the limits specified in the benefit package.

124 What are the guidelines for co-payments?

The Agency has not specified any expected level of copayments.

125 Can the health plan vary rates by age / gender? Can the rates vary by other factors, such as industry, group size or participation percentage for small group? Can small group rates differ from individual?

The Agency has not specified a rating methodology. As addressed in the ITN, rate proposals may be submitted under four separate options. Respondents may be flexible in rate design; however, an actuarial memorandum must be included with each proposal and the benefits must be reasonable in relationship to the premiums charged.

126 The ITN references a bid by Medicaid Area but later references bid by county; are bids by county acceptable?

Yes.

127 What are the guidelines for home and community base services?

The Agency has not specified any expected level of benefits.

128 What are the guidelines for persons in an ALF?

The applicant’s place of residence has no impact on eligibility except that Cover Florida policyholders must be Florida residents.

129 There is only a two week window from the date the responses to the questions will be available and the bid due date. Is it possible to move up the question response date or move back the bid due date in order to allow more time for our actuaries to consider your answers in their rate analysis?

The responses to the written questions will be posted as quickly as possible. It is not currently anticipated that any changes will be made in the procurement timeline.

Submitted by: UnitedHealth Group 130 On page 3, Introduction: Definition 4. “Behavioral

health”, please confirm that Substance Abuse diagnosis and treatments are not included within the definition of Behavioral health, thus are not a

Substance abuse is not a required benefit.

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

minimum requirement for services the Cover Florida plan. If the state expects Substance Abuse to be covered, what are the detailed benefit requirements for Substance Abuse diagnosis and treatment?

131 On page 4, Definition 10. “Enrollee”, please clarify whether spouses and dependents are eligible or excluded under Cover Florida plan. If they are to be included, please provide the following clarification.

Are Spouse and Children included as eligible dependents? What sort of dependent or family definitions accompany the definition of enrollee and policyholder? What are the terms for dependent eligibility? How do those relate to individual coverage? Are plan entities required to offer coverage to spouse and children under age 19? Can a spouse be covered as an individual?

Spouses and children would be considered enrollees if covered by the policyholder. Yes, spouses and children are eligible dependents. The definitions are those generally used by the health insurance industry. Dependent eligibility is the same as that for traditional health insurance coverage. The respondents may offer coverage to spouse and dependents under 19. A spouse could be covered as an individual, as long as they meet the general eligibility requirements.

132 What is the process and requirements if a Cover Florida Plan Entity elects to cease participation in the Cover Florida program?

Termination rights will be spelled out in the contract.

133 Are all of the Program Eligibility requirements for applicants also requirements to remain covered under Cover Florida, including age and

No, the Cover Florida Plan benefit is a guaranteed issue and guaranteed renewable product. Once a person qualifies for coverage he or she remains eligible for coverage as long as the appropriate premium is paid. In addition, respondents/contractors will be able to submit data on an

AHCA ITN 0810, Addendum No. 1, Page 29 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

obtainment of other coverage? If yes, what process is required by the Cover Florida Plan Entities on an ongoing basis to ensure that the requirements are met? If not, please specify which requirements are continuing and which ones are not.

annual basis to support modifications to rates. This will be specified in the contract and is subject oversight by the Agency.

134 If an employer enters the Cover Florida plan, is the employer required to choose just one Cover Florida Plan Entity, can the employer choose more than one Cover Florida Plan Entity to make available for employee choice, or do employees of that employer automatically have open choice of any Cover Florida Plan Entity including both statewide Entities and applicable county Entities?

An employer has the right to contract with more than one Cover Florida Plan entity if it chooses. The employees of that employer would then have the ability to choose between or among the coverages offered. Employees would also have the right to choose a different Cover Florida Plan entity as an individual. In this circumstance, the employee would lose the tax advantages of a Section 125 plan.

135 On page 5 and 6, the ITN references “Factors to be evaluated during the process include....Ability to comply with all reporting requirements”. Please specify or define “all reporting requirements” that will be required as specified.

All reporting requirements will be spelled out in the contract. Some examples are updated network files, grievances received, number of covered lives by county.

136 On page 11, under Other Terms and Conditions – the ITN references reinstatement for Cover Florida enrollees:

What is the effective date of the reinstatement? If an enrollee seeks reinstatement after 63 days, is the enrollee eligible to reapply before which time the enrollee has been without coverage for 6 months? (Part of

The effective date of the reinstatement would be the 1st day of the month for which the premium has been paid. Yes, if an enrollee seeks reinstatement after 63 days, the application would be treated as a new application and the enrollee must wait until the next open enrollment period. Any enrollee that terminates voluntarily may not re-apply for coverage more than once per calendar year.

AHCA ITN 0810, Addendum No. 1, Page 30 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

the eligibility criteria for Cover Florida)

137 On page 11, under Conditions pertaining to the statement of portability, if an individual is insured via a Cover Florida group policy, and then terminates employment, would the individual be offered COBRA coverage, individual continuation coverage or be offered an individual Cover Florida policy?

In this circumstance a plan enrollee would be entitled to an individual Cover Florida policy.

138 On page 19, pertaining to Written and Verbal grievance process, what is the timeline for which a Cover Florida enrollee has to file an appeal?

Six months after the denial notice is received by the plan enrollee. Such notice must be in writing.

139 What type of eligibility verification is expected? Does the state intent to audit eligibility verification, if yes, what is the process for auditing? What is the performance metric for eligibility verification that is expected to be met? What, if any, are the penalties expected to be levied if the performance metrics have not been met?

Eligibility verification is the responsibility of the plan entity. Should the Agency become aware that the plan entity may be operating contrary to law, the ITN or the contract, an investigation may be initiated.

140 On page 22, Volume Two: Plan Proposal, what are the requirements of “a detailed business plan” required under Section 1 Tab A.

The Agency believes that the respondents would have a reasonable feel for how the marketplace, both competitors and purchasers, is going to react to this product. The respondent could conservatively assume that the competitive factors for this market will be the same as any other market

141 On page 25, Section II Premium Rate Proposals – can rates be trended during a plan year, or may rates be adjusted only once per year on the plan anniversary? If allowed, can a monthly or

Rates may only be adjusted once per year on the anniversary date of the policy. The rating renewal process will generally be the same as the process outlined in the ITN. Rate adjustments at renewal are allowed if

AHCA ITN 0810, Addendum No. 1, Page 31 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

AHCA ITN 0810, Addendum No. 1, Page 32 of 58

quarterly rate of trend be submitted with the proposed rates?

supported by the actuarial memorandum. Rate changes are subject to regulatory oversight by the Agency.

142 On page 25, the first sentence under Section II, heading, "Premium Rate Proposals", says “1. Any proposed premium rate that includes conditions for acceptance or contingencies will be disqualified". Does that mean the following are not allowed?

the loading factor varying by the group participation level individual medical underwriting minimum employer contribution

No, if a respondent says that they will only participate if they achieve a specific overall enrollment in the program, their response will be disqualified from participation.

143 Top of page 26, Item 6 references carriers submitting annual rate adjustment requests. Please describe the rate adjustment process. If a rate adjustment request is denied, is a Cover Florida Plan Entity required to continue participation in the Cover Florida program?

The rating renewal process will generally be the same as the process outlined in the ITN. Rate adjustments at renewal are allowed if supported by the actuarial memorandum. Rate changes are subject to regulatory oversight by the Agency.

144 Per ” the “Rate Presentation Options”, Pages 26 & 27, respondents may present “any actuarially sound rate structure “ please confirm that commonly used rating variable such as age, sex, tobacco usage, geographical area are acceptable. Are there any rating variables which may not be utilized? Is the UW discounts/loading allowed from the manual rate? If so, are there any restrictions?

As addressed in the ITN, rate proposals may be submitted under four separate options. Respondents may be flexible in rate design; however, an actuarial memorandum must be included with each proposal and the benefits must be reasonable in relationship to the premiums charged. General individual rating and UW discounts/loading will be considered.

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

145 What is the process and timeline for approval of rate and form filings?

Rates and forms will have to be approved prior to implementation of the program.

146 Are Cover Florida plans required to provide coverage for enrollees traveling outside of the United States?

No.

147 Will premium taxes be levied on Cover Florida plans?

No.

148 Will the state conduct any retro rating?

No.

149 Will the Cover Florida plans be required to offer Out of Network coverage? If yes, for what categories of services, which types of providers and what is the permissible cost sharing?

Yes, emergency coverage only. Yes, a network similar to an EPO is permissible; however it must have sufficient providers to provide benefits to be offered. Generally a waiver of the 30/60 measure is not granted in other than rural areas..

150 May respondents utilize the Governor’s Discount Drug card/program as one option for Prescription drug coverage for Cover Florida?

No.

151 On pages 32-33, the ITN indicates that coverage offered under Cover Florida is deemed to be "creditable coverage" under the relevant portions of ERISA, the Public Services Act and the Internal Revenue Code. . . .and that Respondents are responsible for issuing a certificate of creditable coverage to all enrollees. Clarification of these points is requested:

Does each plan proposed have to meet the federal standard for "creditable coverage"? Has the State received a waiver from the

We have been advised by the appropriate Federal authorities that the minimum benefits required of a Cover Florida Plan benefit are creditable coverage.

AHCA ITN 0810, Addendum No. 1, Page 33 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

respective federal government agencies declaring all Cover Florida plans "creditable coverage?" Is meeting the standard for "creditable coverage" under federal law a minimum requirement for responding to the ITN? For each plan proposed? If one or more plans do not meet the federal criteria for "creditable coverage", how will Respondents be able to issue certificates of creditable coverage as required by the ITN?

152 The ITN requires Respondents to accept applications during all of 2009 and allows a more restrictive enrollment/application window beginning 1/1/10. Clarification is requested on the following:

What are the permissible limitations for re-enrollment during 2009? Are Respondents required to allow persons to enroll in a Cover FL plan in 2009, allow that same person to terminate coverage, and then re-enroll at a later date?

What limitations are acceptable to impose on re-enrollment? Will it be permissible to impose surcharges, waiting periods for re-enrollment, waiting periods for full benefits, or some combination thereof to be

Grace period and reinstatement language is included in the ITN.

Surcharges will not be permitted. If a plan enrollee seeks re-instatement after 63 days, the application is treated as a new application and the re-instatement or re-application may be restricted to open enrollment periods.

As it relates to open enrollment for group plans, section 125 of the IRC takes precedence. Any section 125 plan open enrollment period must comply with federal law and regulation. Any enrollee that terminates voluntarily may not re-apply for coverage more than once per calendar year.

AHCA ITN 0810, Addendum No. 1, Page 34 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

imposed?

The requirement to accept applications/enrollments for all of 2009 appears to be in conflict with the requirements of Section 125 of the Internal Revenue Code, at least as the requirement pertains to employer groups under a cafeteria plan. How will this apparent conflict be resolved?

Submitted by: Paragon Case Management

153 Where may I list our company, Paragon Case Management, as a subcontractor for medical and vocational field case management?

This is outside the scope of this ITN.

Submitted by: Celtic Insurance and Centene Corp.

154 In addition to the county of residence, please describe any other criteria by which rates may vary (i.e. age, gender, non-smoker, build, etc.). If no additional rate variance is acceptable, would health plans be able to offer incentives or discounts to lower risk applicants?

As addressed in the ITN, rate proposals may be submitted under four separate options. Respondents may be flexible in rate design; however, an actuarial memorandum must be included with each proposal and the benefits must be reasonable in relationship to the premiums charged.

155 Is there a 12 month rate guarantee, or can rate changes occur more frequently?

A minimum of 12 month rate guarantee. Rate adjustments at renewal are allowed if supported by the actuarial memorandum. Rate changes are subject to regulatory oversight by the Agency. .

AHCA ITN 0810, Addendum No. 1, Page 35 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

156 What are the requirements for approval of future rate actions when needed?

Upon renewal of the policy. Rate adjustments at renewal are allowed if supported by the actuarial memorandum. Rate changes are subject to regulatory oversight by the Agency.

157 Is there a minimum loss ratio requirement?

No.

158 Other than pre-existing conditions, will built in benefit waiting periods be acceptable?

No.

159 Please describe any enrollment functions or marketing activities that AHCA or other State agencies are planning to offer in addition to those performed by the contractors. How would AHCA allocate enrollment applications received directly from applicants and would contractors be responsible for any commission in return?

The Agency and the Executive Office of the Governor plan to aggressively market the Cover Florida program. A website and initial efforts are under development, including assistance and staffing through the Gubernatorial Fellows Program. In addition, the ITN requires that the respondent develop a marketing plan.

160 Would successful Respondents be allowed to provide discounts or other incentives to members that elect to receive correspondence (i.e. monthly statements, EOBs, newsletters, etc.) from the health plan in electronic format?

Yes.

AHCA ITN 0810, Addendum No. 1, Page 36 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

161 Has AHCA performed any market research that would assist Respondents in formulating their assumptions to develop more accurate enrollment expectations?

No. Some information can be obtained from the U.S. Census Bureau website, as well as from the University of Florida 2004 report on the Uninsured in Florida.

Submitted by: Aetna Health Inc. and Aetna Life Insurance Company

162 What is to be the term of the Cover Florida Program bid?

It is expected that the Contract will be for a two year period, with three (3) one (1) year renewal options.

163 Over what period of time will the contract extend? It is expected that the Contract will be for a two year period, with three (3) one (1) year renewal options.

164 Can a plan propose a specific time period for participation in the Cover Florida Program (such as a two year term)?

Yes. Also, see response to question #163.

165 Under what circumstances can the plan terminate its participation in the Cover Florida Program?

See response to question #101. Termination rights will be specified in the contract.

166 What will be the role of Cover Florida Plus in comparison to the catastrophic coverage of the current ITN?

It is expected to be supplemental in nature.

167 With different respondents potentially providing benefits in different regions, how will member movement from one region to another be handled? If a member enrolls in one region with

If a plan enrollee moves from one region to another where coverage is not provided by the enrollee’s current plan, then the enrollee would apply for coverage with a Cover Florida Plan entity in the new location.

AHCA ITN 0810, Addendum No. 1, Page 37 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

one carrier and then moves to a region in which that carrier does not provide coverage, will that member be disenrolled from the first respondent’s plan and have an opportunity to select the second?

168 Is it contemplated that a policyholder may be an entity other than an individual or a family?

Yes, the policyholder may be a qualifying employer.

169 Where are the minimum benefits package specifications set forth? What limits (if any) can there be on deductibles, service limits, plan limits, etc.?

Chapter Law 2008-32 and ITN 0810 allow for flexibility and do not define a specific minimum benefit package. Each respondent’s submission will be evaluated on the most robust and comprehensive benefits for Floridians. Section 408.9091 (4) (a) 3, Florida Statutes states “provide cost containment through limits on the number of services, caps on benefit payments, and copayments”.

170 What tools will be made available to the carrier to verify eligibility, especially in the context of eligibility or participation in government programs?

Respondent may set reasonable documentation standards.

171 How will “respondent’s compliance status with requirements of other regulatory agencies in Florida” be determined?

The Agency will be responsible for verification.

172 What falls within the term “regulatory action” by the state of Florida?

Any action taken by a regulator for which a fine or other sanction has been levied and all appeals, settlements or other method for resolving the issue has been completed.

173 How will the sufficiency of the proposed provider network be evaluated?

The Agency evaluation team will review the projected enrollment, service area covered and network and determine sufficiency based upon those criteria.

174 What are the reporting requirements? All reporting requirements will be spelled out in the contract. Some examples are updated network files, grievances received, and the number of covered lives by county.

AHCA ITN 0810, Addendum No. 1, Page 38 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

175 What is the State’s expectation regarding the “procedure for assisting enrollees in negotiating hospital charges upon exhaustion of benefits?”

This is an optional service; no minimum standards have been developed.

176 What criteria will be used to determine which respondent to invite to negotiate?

As specified in the ITN, the Agency will make the final determination once all the evaluations have been completed.

177 What does the State contemplate regarding the offering of plans through a qualified employer and meeting section 125 requirements?

Section 408.9091 (4)(a) 10, Florida Statutes requires any plan offered through a qualified employer must meet the requirements of section 125 of the Internal Revenue Code.

178 Is this viewed as a positive for which additional scoring will take place?

No.

179 How will the grace period work? Will plans have the ability to deny claims incurred during the grace period if the premium is not paid by the end of the grace period?

Yes.

180 If an individual is enrolled in a Cover Florida Plan and thereafter becomes covered under another health insurance plan outside the Cover Florida arrangement, does he/she have the right to continue in the Cover Florida Plan?

Yes, the Cover Florida Plan benefit is a guaranteed issue and guaranteed renewable product.

181 What claim payment timeliness requirements apply?

This will be delineated in the contract.

182 What is meant by the term “affiliated plans?” Those plans that have common ownership, control or management.

183 Is th request for information limited to litigation in the state of Florida or limited to operations of the

No.

AHCA ITN 0810, Addendum No. 1, Page 39 of 58

AHCA ITN 0810 – ADDENDUM NO. 1 VENDOR QUESTIONS & AGENCY RESPONSES

respondent in the state of Florida?

184 What services are subject to the ban on offshoring? Does this apply to incidental services (such as the production of ID cards), or does it pertain solely to the provision of the specific benefits that are referenced elsewhere in the ITN?

All services related to a Cover Florida Plan must be provided by employees or contractors within the United States.

185 What is meant by the term “services of the same nature?”

Providing health insurance coverage.

186 What tools will be made available to a respondent for determining eligibility for its applicants and enrollees? How will the respondent be able to determine whether the applicant was enrolled in or eligible for other governmental programs? How will the respondent be expected to determine whether the applicant was not covered within the past six months under any other health insurance program?

Respondents will be able to ask for reasonable documentation during the application process.

187 What is the expectation regarding the administration of the pre-existing condition exclusion? Will the exclusion apply if the condition existed during the preceding twelve months but the member was not seen by a physician during that time?

The definition of preexisting conditions is spelled out in the ITN.