Embed Size (px)

DESCRIPTION

A presentation to the Canadian Bar Association (BC) by Gib van Ert, 28 November 2013.

Citation preview

Charity revocation appeals: Process and

prospects

Gib van Ert Hunter Litigation Chambers

CBABC Charity Law Section • 28 November 2013

• Stages of revocation

• Appeals to Federal Court of Appeal

• Record creation

• Grounds: generally

• Grounds: adequacy of documents

• Prospects of success

Stages of revocation

• Audit

• Administrative Fairness Letter

• Notice of Intention to Revoke

• Notice of Objection

• Notice of Confirmation

• Appeal to Federal Court of Appeal

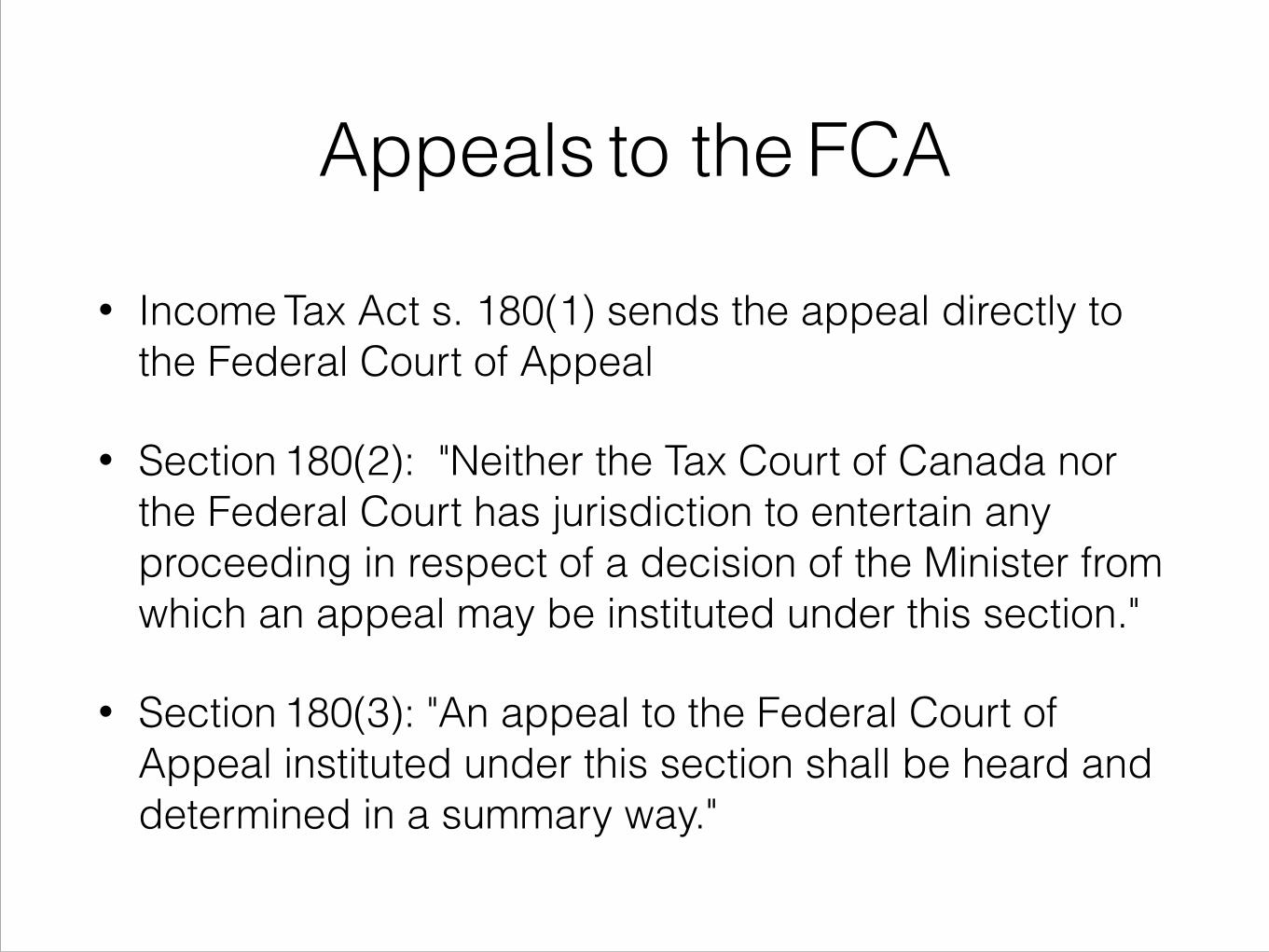

Appeals to the FCA

• Income Tax Act s. 180(1) sends the appeal directly to the Federal Court of Appeal

• Section 180(2): "Neither the Tax Court of Canada nor the Federal Court has jurisdiction to entertain any proceeding in respect of a decision of the Minister from which an appeal may be instituted under this section."

• Section 180(3): "An appeal to the Federal Court of Appeal instituted under this section shall be heard and determined in a summary way."

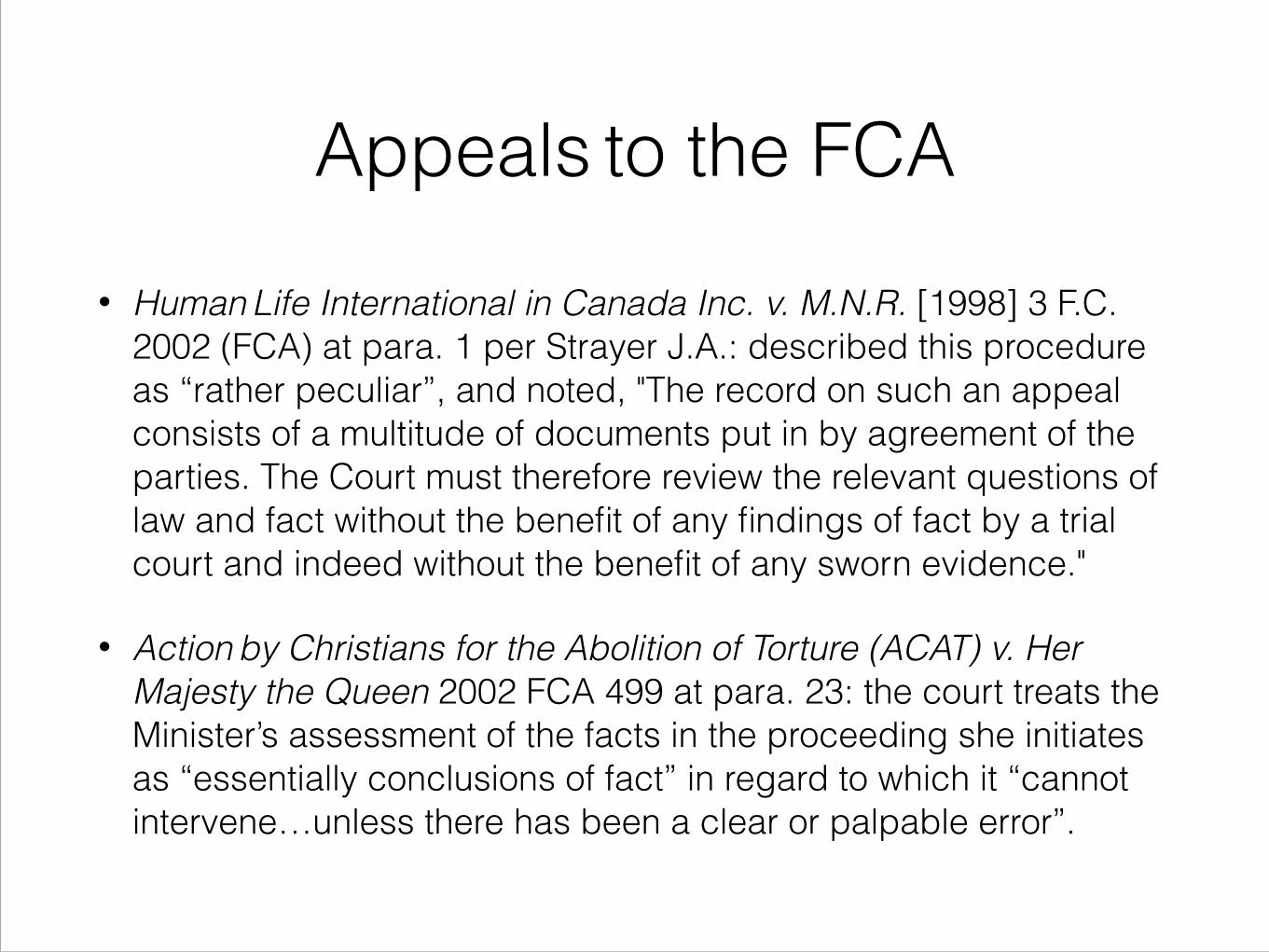

Appeals to the FCA

• Human Life International in Canada Inc. v. M.N.R. [1998] 3 F.C. 2002 (FCA) at para. 1 per Strayer J.A.: described this procedure as “rather peculiar”, and noted, "The record on such an appeal consists of a multitude of documents put in by agreement of the parties. The Court must therefore review the relevant questions of law and fact without the benefit of any findings of fact by a trial court and indeed without the benefit of any sworn evidence."

• Action by Christians for the Abolition of Torture (ACAT) v. Her Majesty the Queen 2002 FCA 499 at para. 23: the court treats the Minister’s assessment of the facts in the proceeding she initiates as “essentially conclusions of fact” in regard to which it “cannot intervene…unless there has been a clear or palpable error”.

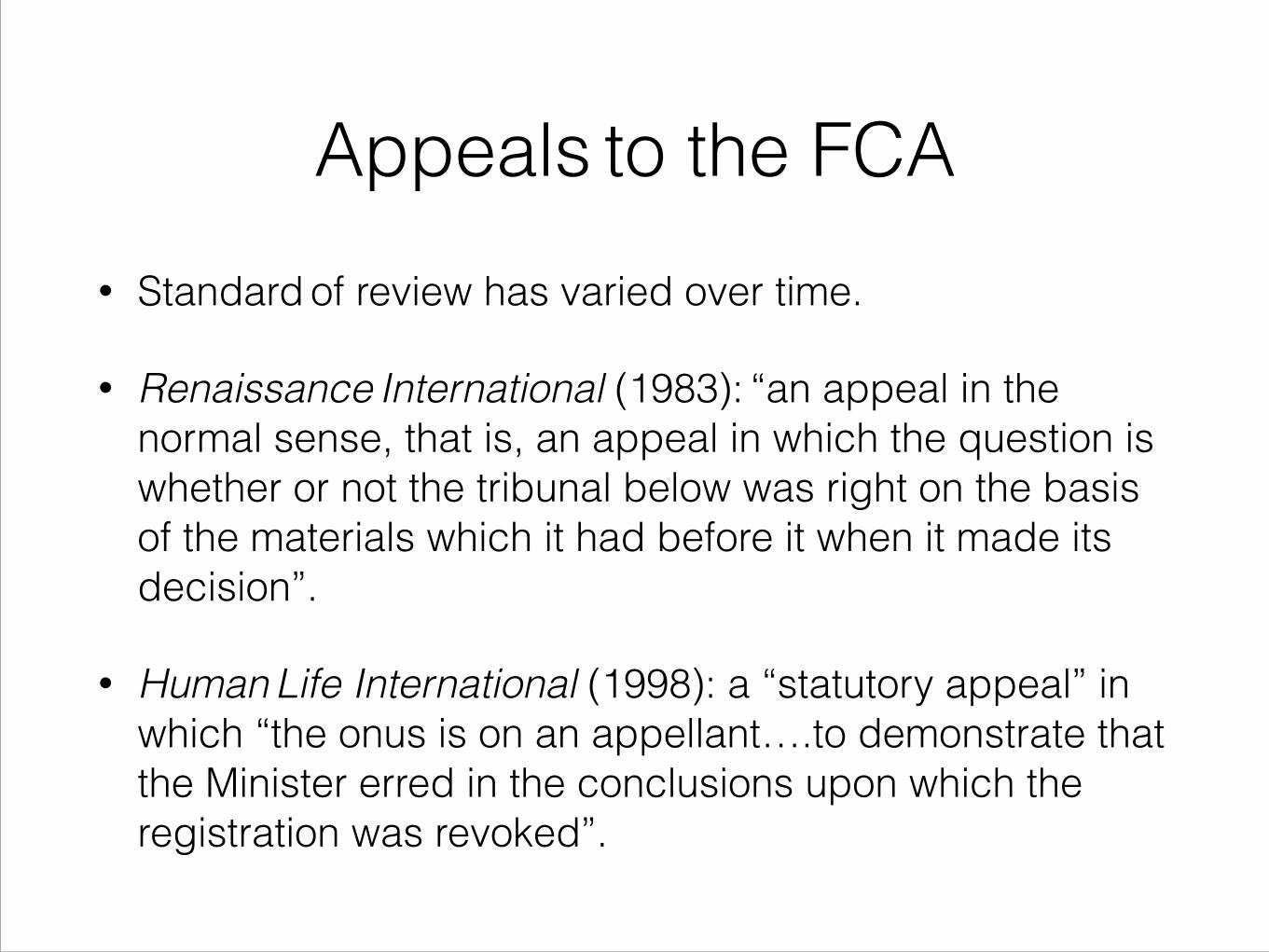

Appeals to the FCA• Standard of review has varied over time.

• Renaissance International (1983): “an appeal in the normal sense, that is, an appeal in which the question is whether or not the tribunal below was right on the basis of the materials which it had before it when it made its decision”.

• Human Life International (1998): a “statutory appeal” in which “the onus is on an appellant….to demonstrate that the Minister erred in the conclusions upon which the registration was revoked”.

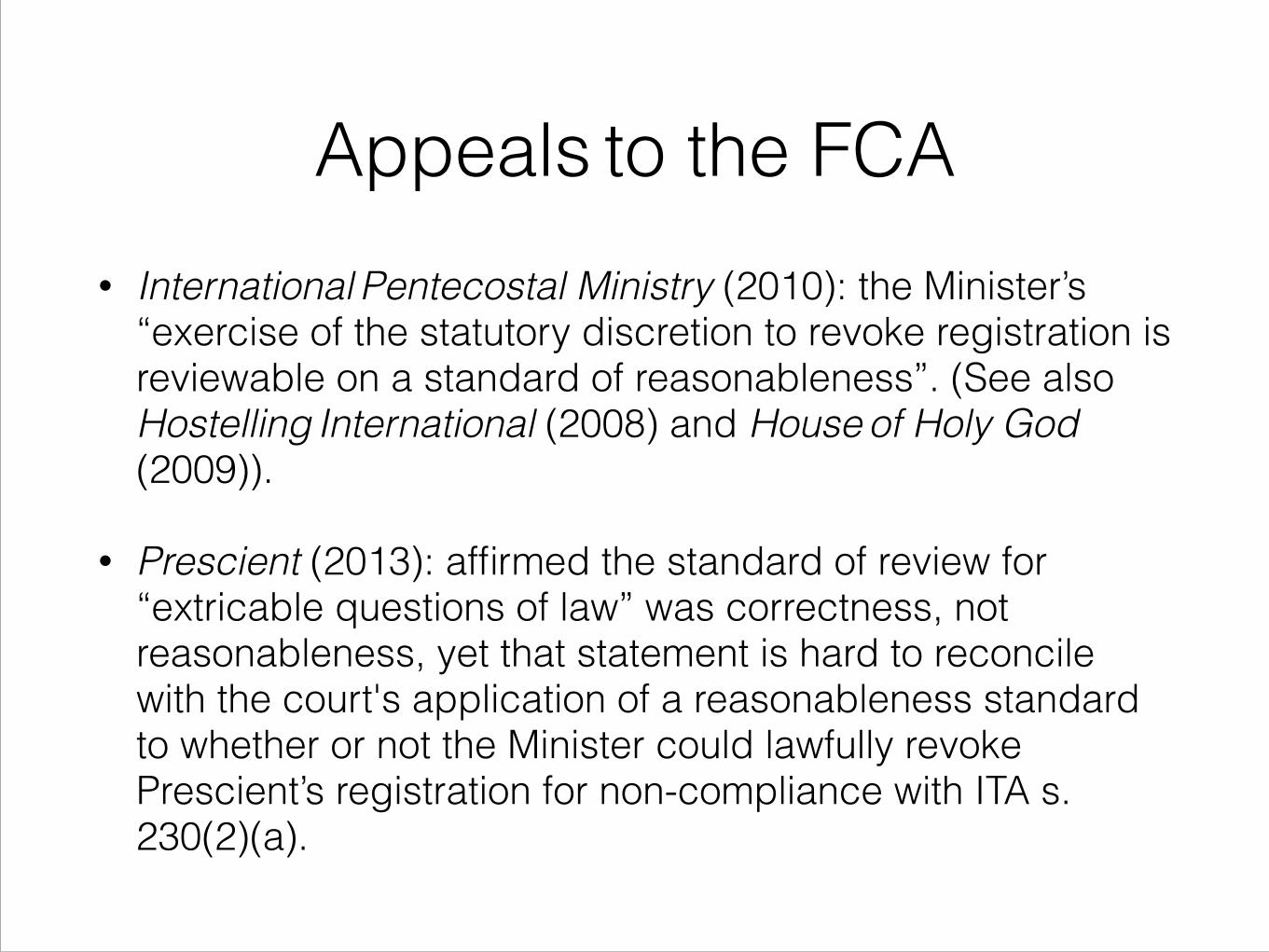

Appeals to the FCA• International Pentecostal Ministry (2010): the Minister’s

“exercise of the statutory discretion to revoke registration is reviewable on a standard of reasonableness”. (See also Hostelling International (2008) and House of Holy God (2009)).

• Prescient (2013): affirmed the standard of review for “extricable questions of law” was correctness, not reasonableness, yet that statement is hard to reconcile with the court's application of a reasonableness standard to whether or not the Minister could lawfully revoke Prescient’s registration for non-compliance with ITA s. 230(2)(a).

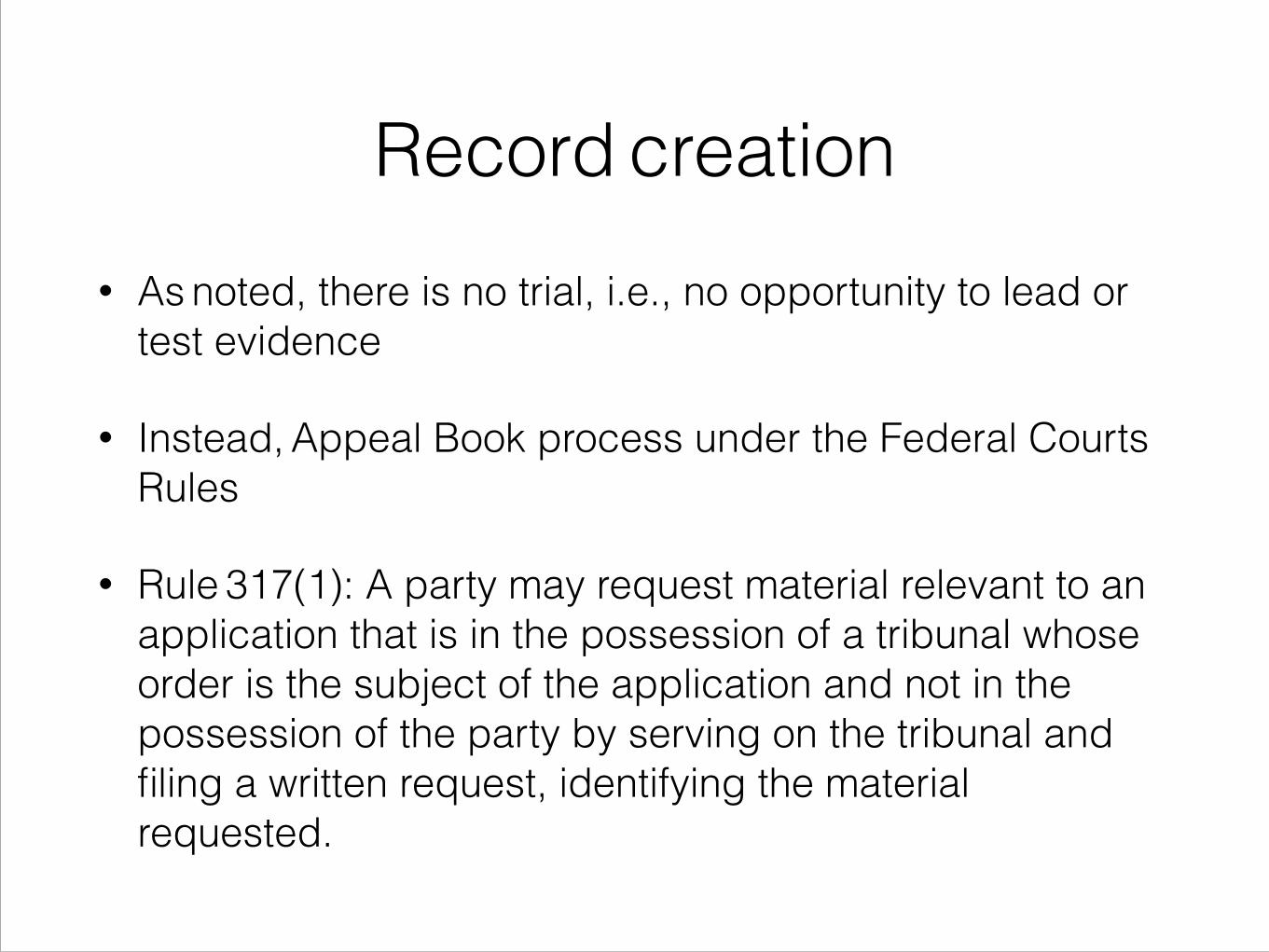

Record creation• As noted, there is no trial, i.e., no opportunity to lead or

test evidence

• Instead, Appeal Book process under the Federal Courts Rules

• Rule 317(1): A party may request material relevant to an application that is in the possession of a tribunal whose order is the subject of the application and not in the possession of the party by serving on the tribunal and filing a written request, identifying the material requested.

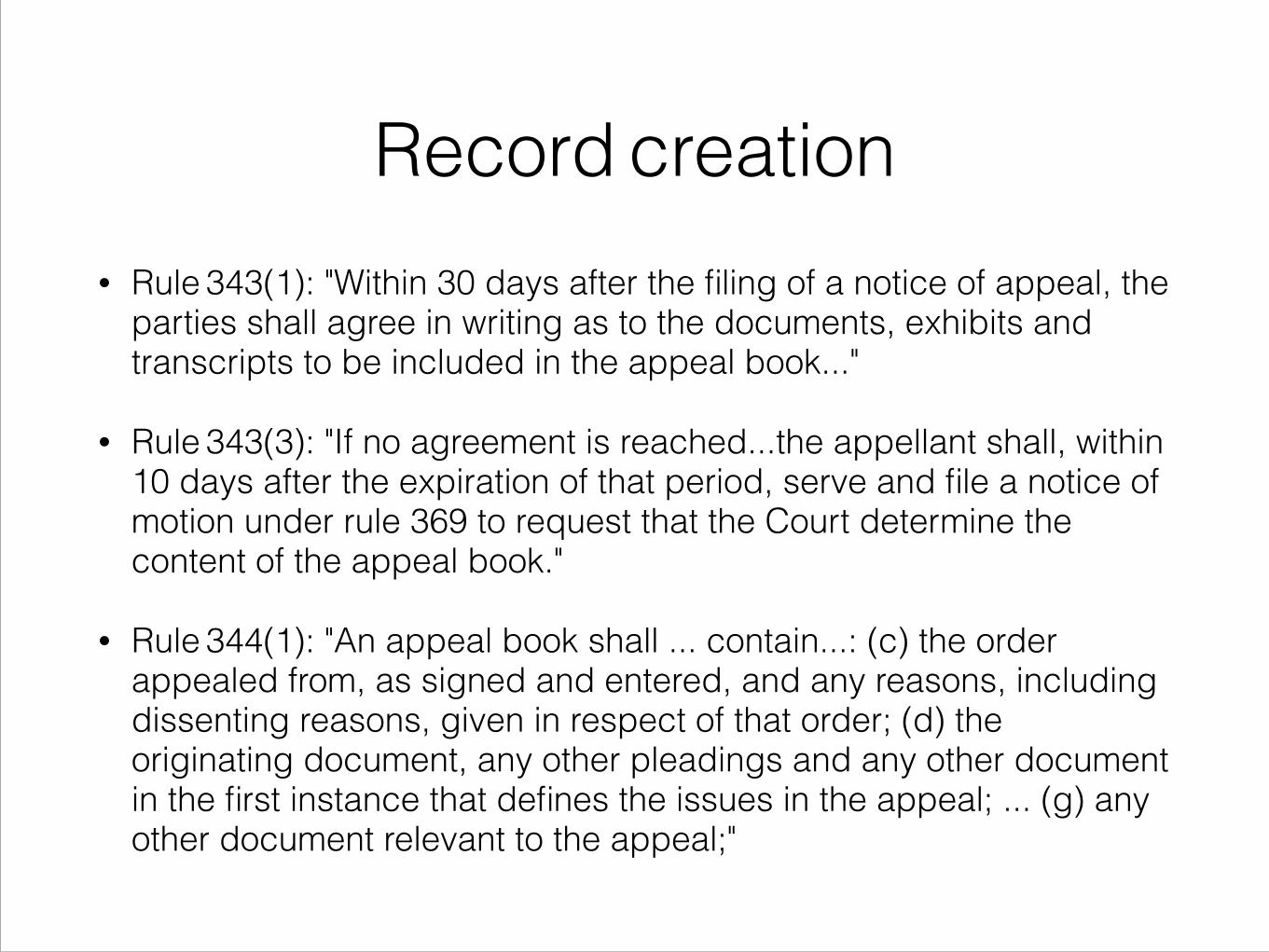

Record creation• Rule 343(1): "Within 30 days after the filing of a notice of appeal, the

parties shall agree in writing as to the documents, exhibits and transcripts to be included in the appeal book..."

• Rule 343(3): "If no agreement is reached...the appellant shall, within 10 days after the expiration of that period, serve and file a notice of motion under rule 369 to request that the Court determine the content of the appeal book."

• Rule 344(1): "An appeal book shall ... contain...: (c) the order appealed from, as signed and entered, and any reasons, including dissenting reasons, given in respect of that order; (d) the originating document, any other pleadings and any other document in the first instance that defines the issues in the appeal; ... (g) any other document relevant to the appeal;"

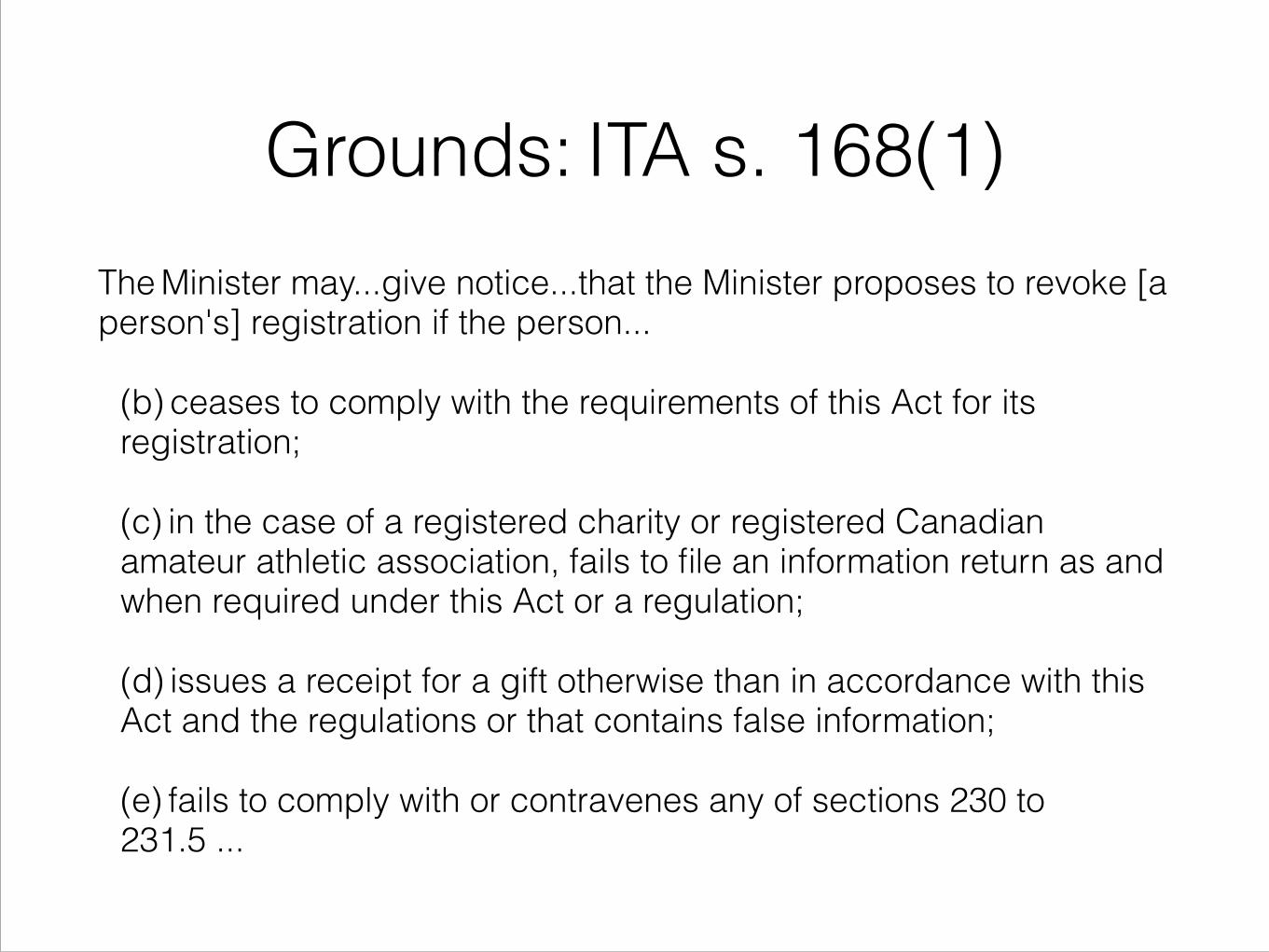

Grounds: ITA s. 168(1)The Minister may...give notice...that the Minister proposes to revoke [a person's] registration if the person...

(b) ceases to comply with the requirements of this Act for its registration;

(c) in the case of a registered charity or registered Canadian amateur athletic association, fails to file an information return as and when required under this Act or a regulation;

(d) issues a receipt for a gift otherwise than in accordance with this Act and the regulations or that contains false information;

(e) fails to comply with or contravenes any of sections 230 to 231.5 ...

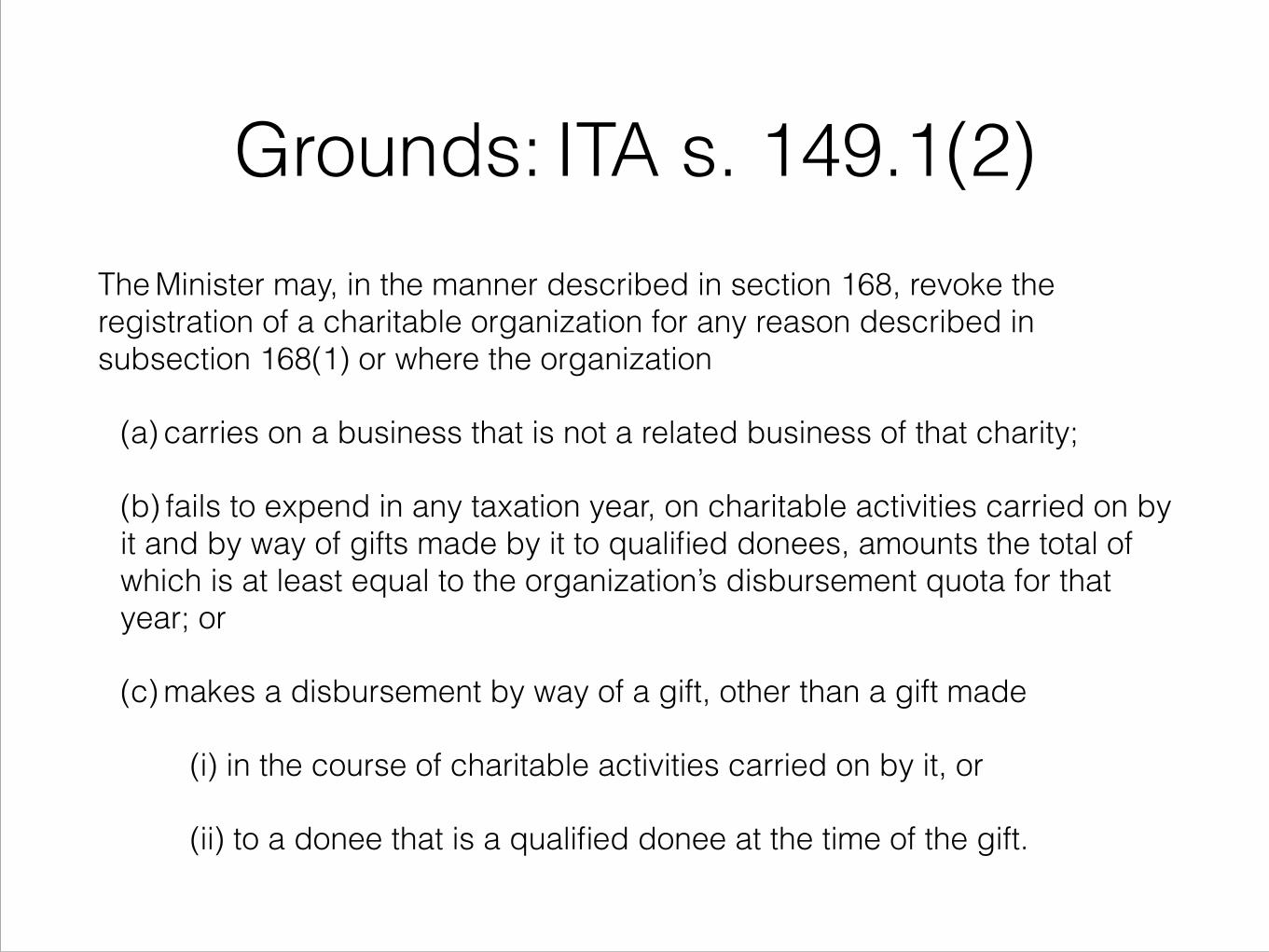

Grounds: ITA s. 149.1(2)The Minister may, in the manner described in section 168, revoke the registration of a charitable organization for any reason described in subsection 168(1) or where the organization

(a) carries on a business that is not a related business of that charity;

(b) fails to expend in any taxation year, on charitable activities carried on by it and by way of gifts made by it to qualified donees, amounts the total of which is at least equal to the organization’s disbursement quota for that year; or

(c) makes a disbursement by way of a gift, other than a gift made

(i) in the course of charitable activities carried on by it, or

(ii) to a donee that is a qualified donee at the time of the gift.

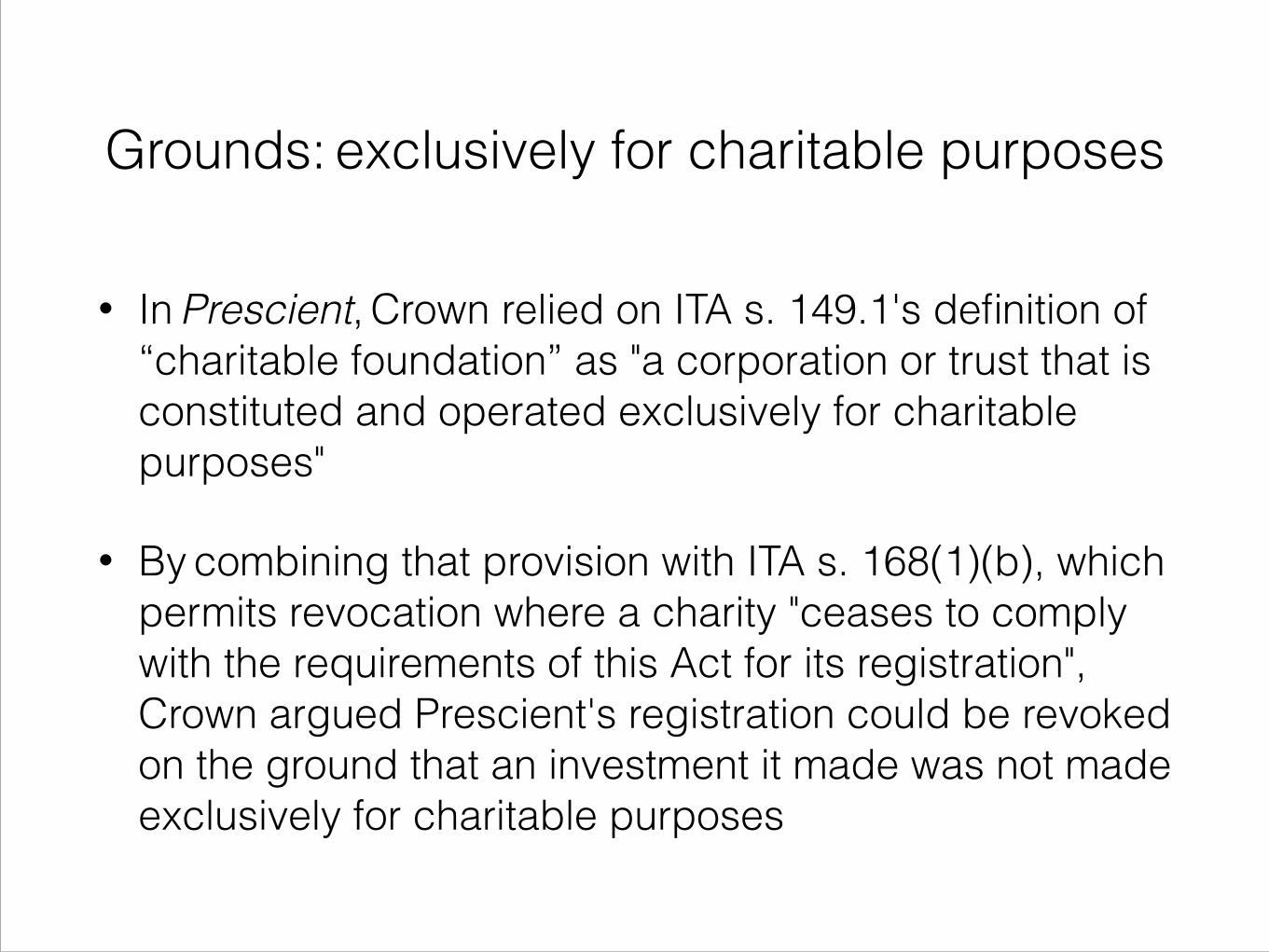

Grounds: exclusively for charitable purposes

• In Prescient, Crown relied on ITA s. 149.1's definition of “charitable foundation” as "a corporation or trust that is constituted and operated exclusively for charitable purposes"

• By combining that provision with ITA s. 168(1)(b), which permits revocation where a charity "ceases to comply with the requirements of this Act for its registration", Crown argued Prescient's registration could be revoked on the ground that an investment it made was not made exclusively for charitable purposes

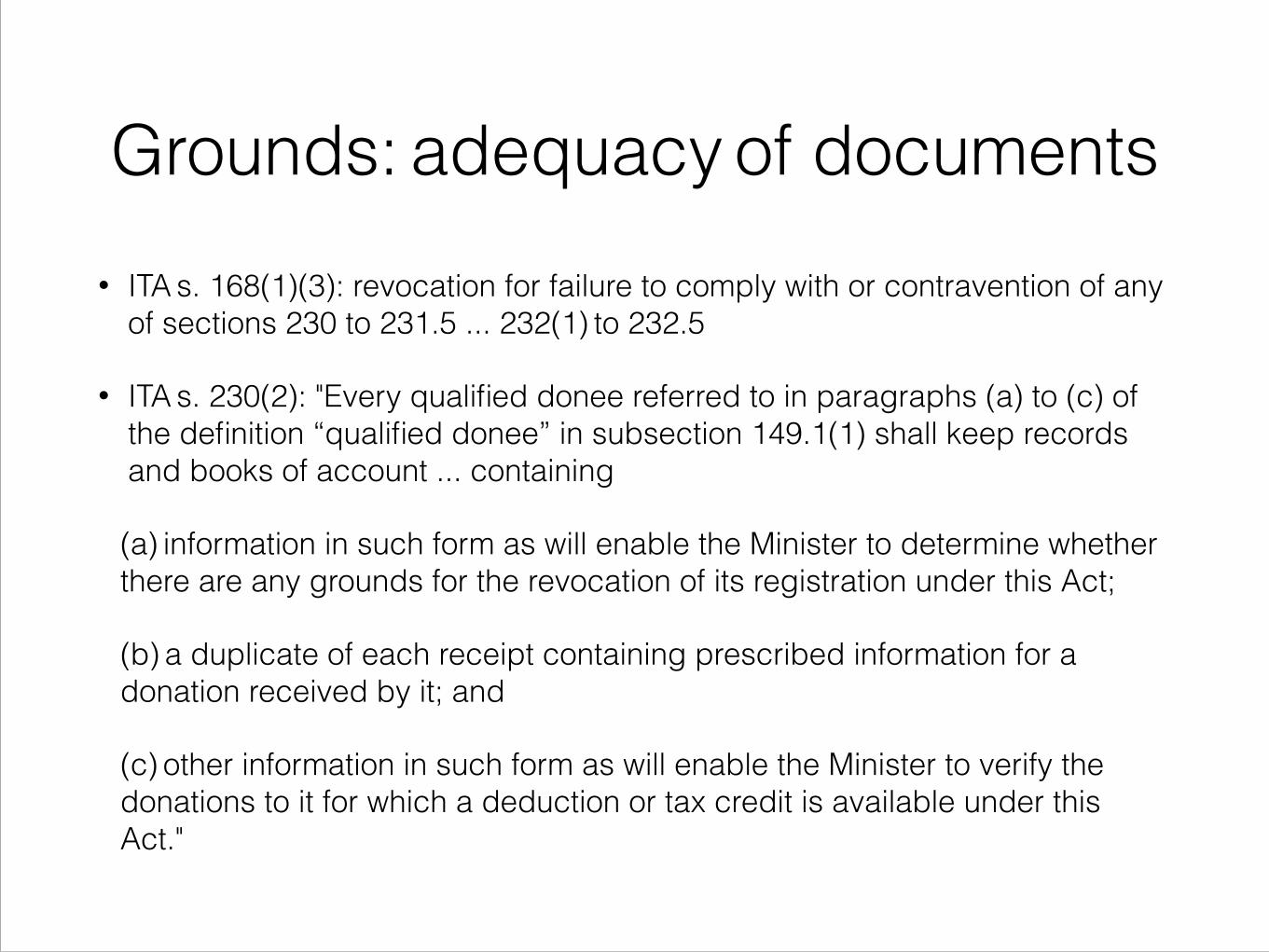

Grounds: adequacy of documents• ITA s. 168(1)(3): revocation for failure to comply with or contravention of any

of sections 230 to 231.5 ... 232(1) to 232.5

• ITA s. 230(2): "Every qualified donee referred to in paragraphs (a) to (c) of the definition “qualified donee” in subsection 149.1(1) shall keep records and books of account ... containing

(a) information in such form as will enable the Minister to determine whether there are any grounds for the revocation of its registration under this Act;

(b) a duplicate of each receipt containing prescribed information for a donation received by it; and

(c) other information in such form as will enable the Minister to verify the donations to it for which a deduction or tax credit is available under this Act."

Grounds: adequacy of documents

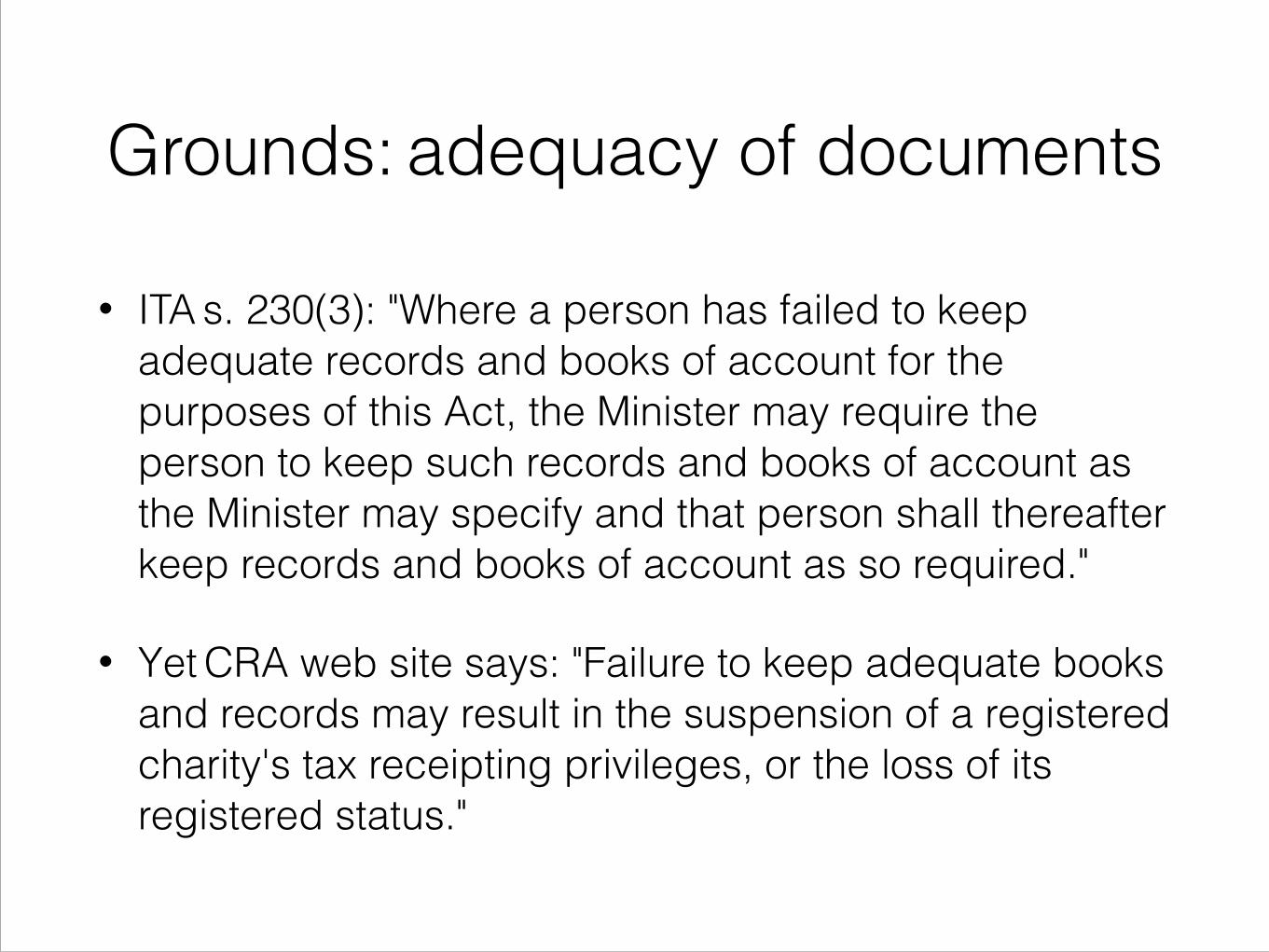

• ITA s. 230(3): "Where a person has failed to keep adequate records and books of account for the purposes of this Act, the Minister may require the person to keep such records and books of account as the Minister may specify and that person shall thereafter keep records and books of account as so required."

• Yet CRA web site says: "Failure to keep adequate books and records may result in the suspension of a registered charity's tax receipting privileges, or the loss of its registered status."

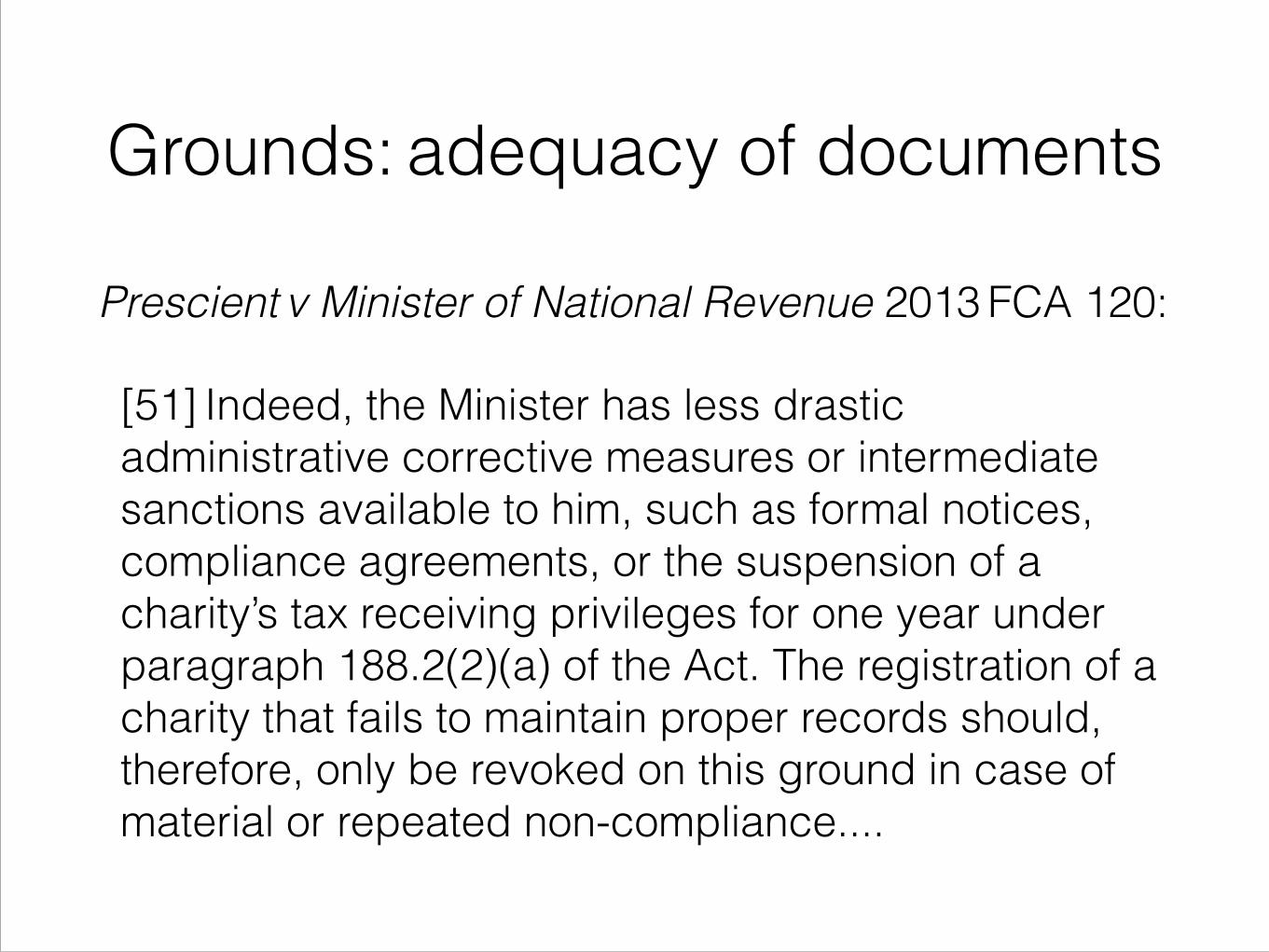

Grounds: adequacy of documents

Prescient v Minister of National Revenue 2013 FCA 120:

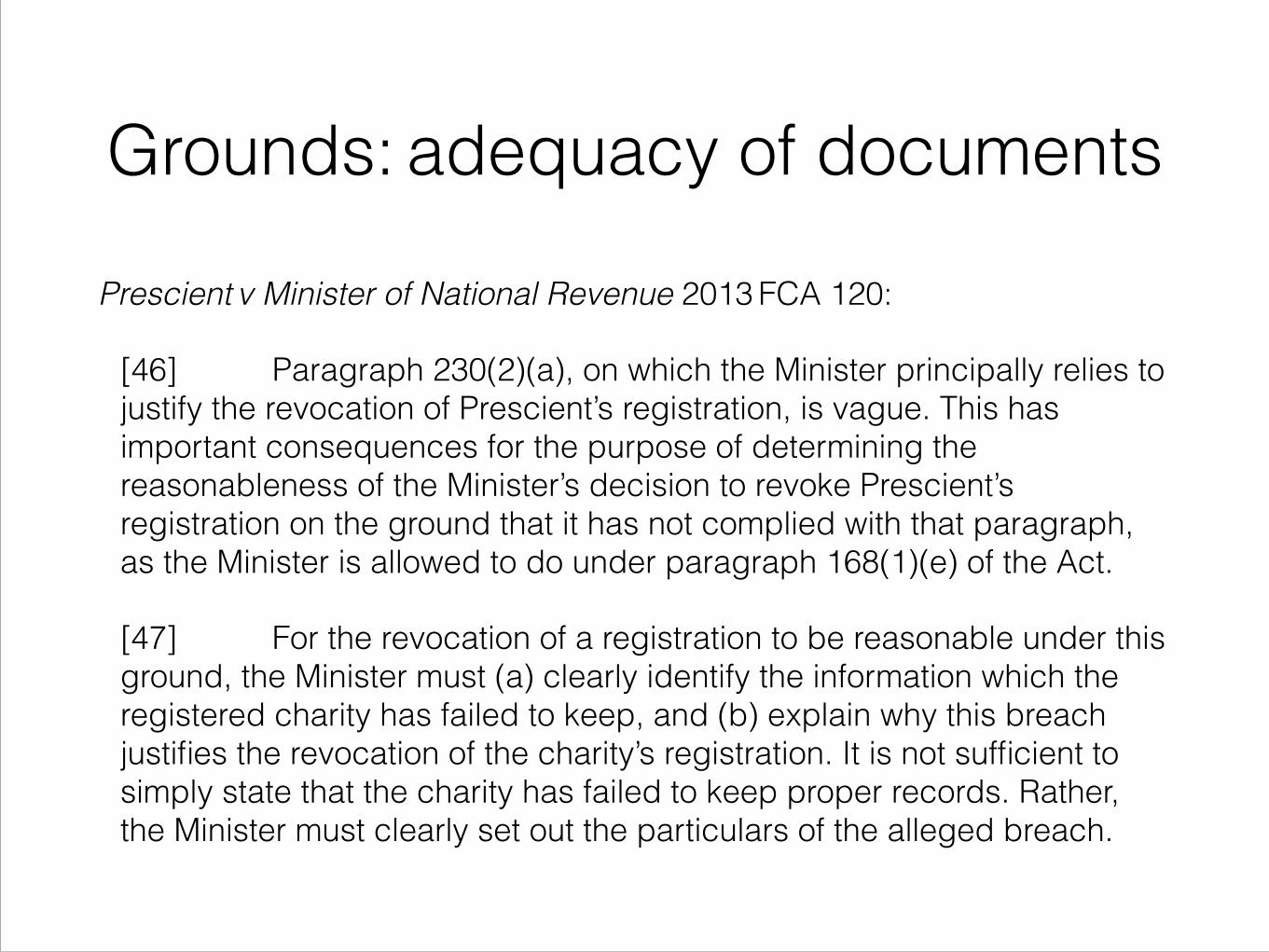

[46] Paragraph 230(2)(a), on which the Minister principally relies to justify the revocation of Prescient’s registration, is vague. This has important consequences for the purpose of determining the reasonableness of the Minister’s decision to revoke Prescient’s registration on the ground that it has not complied with that paragraph, as the Minister is allowed to do under paragraph 168(1)(e) of the Act.

[47] For the revocation of a registration to be reasonable under this ground, the Minister must (a) clearly identify the information which the registered charity has failed to keep, and (b) explain why this breach justifies the revocation of the charity’s registration. It is not sufficient to simply state that the charity has failed to keep proper records. Rather, the Minister must clearly set out the particulars of the alleged breach.

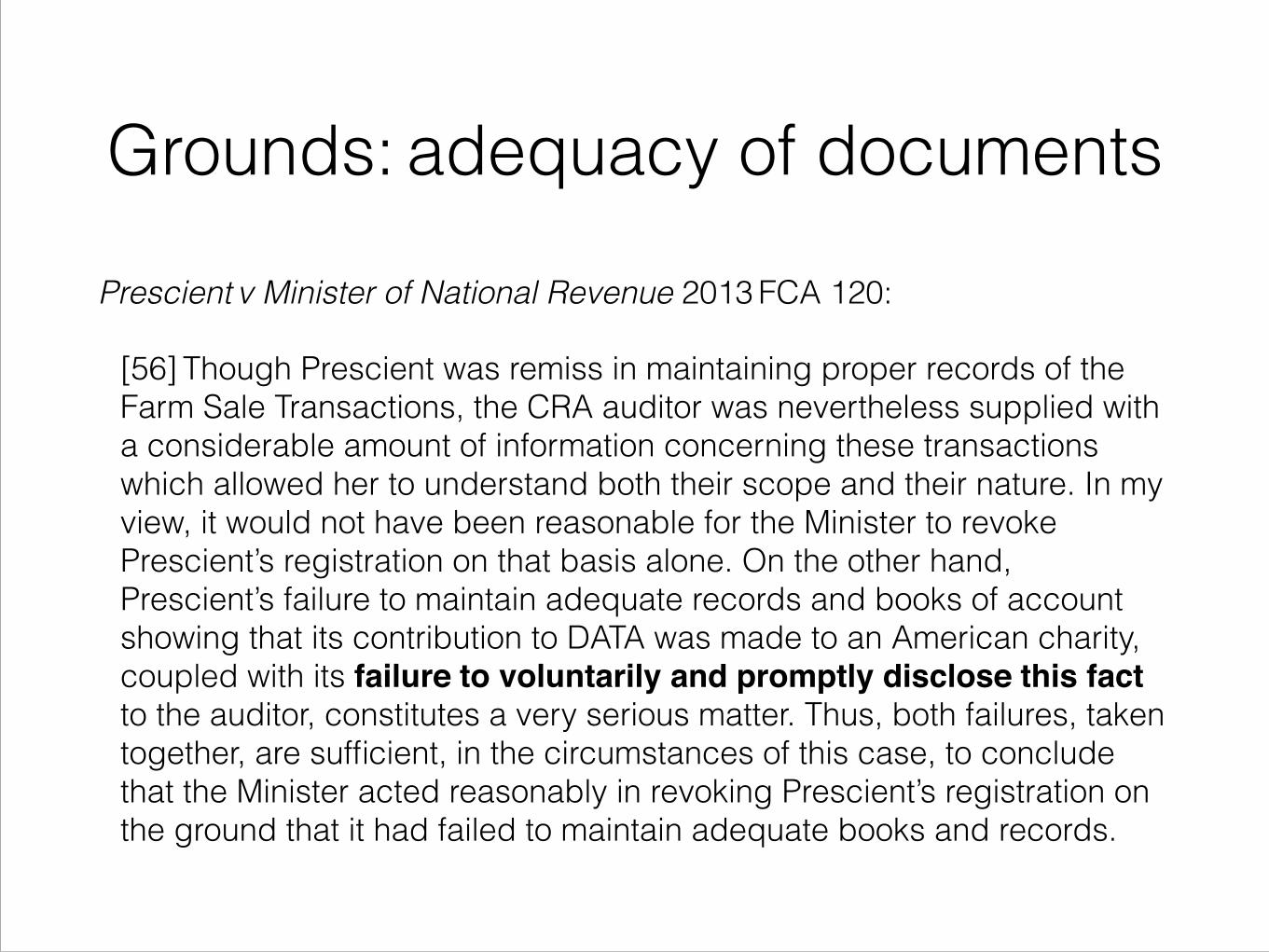

Grounds: adequacy of documents

Prescient v Minister of National Revenue 2013 FCA 120:

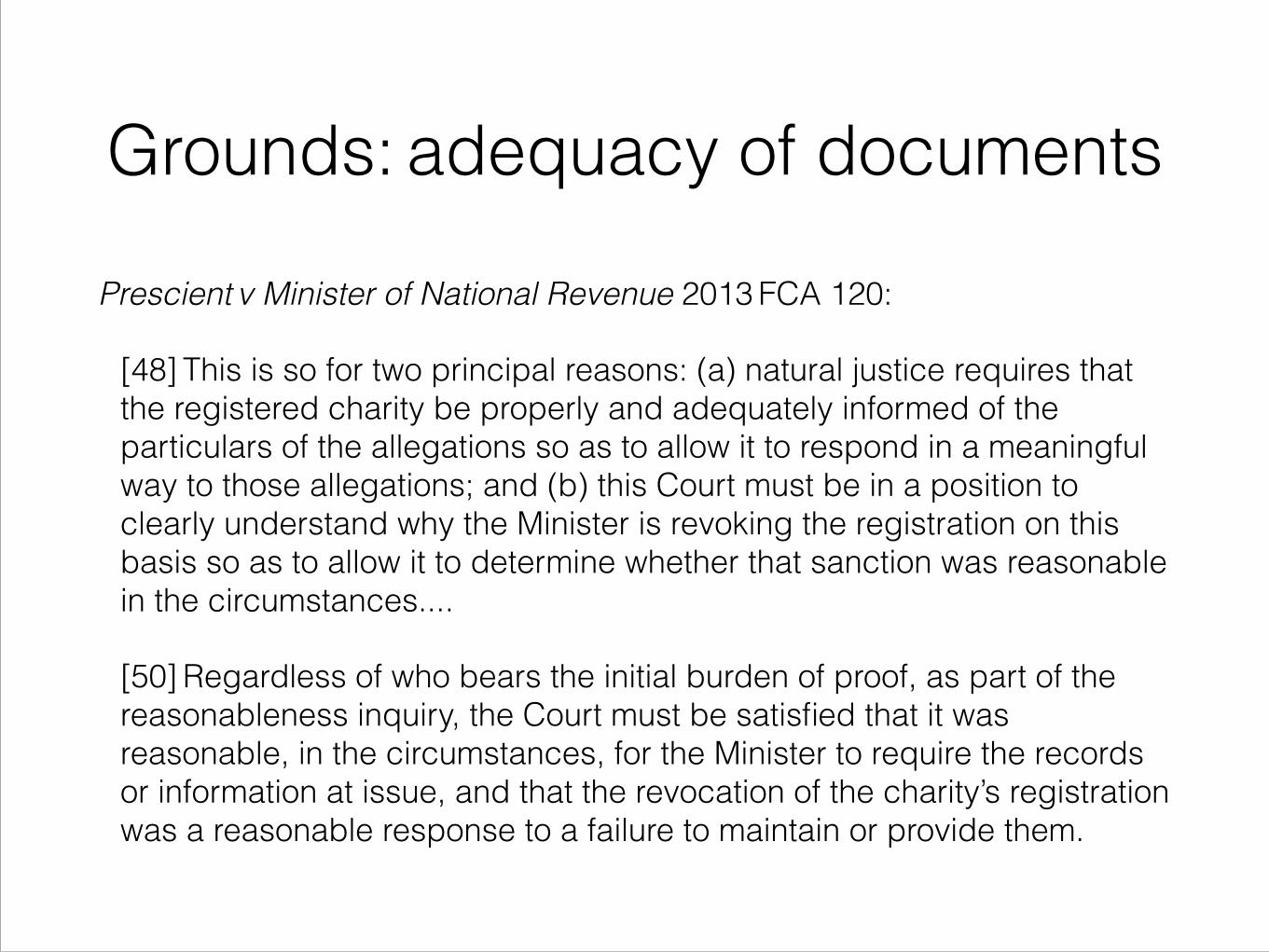

[48] This is so for two principal reasons: (a) natural justice requires that the registered charity be properly and adequately informed of the particulars of the allegations so as to allow it to respond in a meaningful way to those allegations; and (b) this Court must be in a position to clearly understand why the Minister is revoking the registration on this basis so as to allow it to determine whether that sanction was reasonable in the circumstances....

[50] Regardless of who bears the initial burden of proof, as part of the reasonableness inquiry, the Court must be satisfied that it was reasonable, in the circumstances, for the Minister to require the records or information at issue, and that the revocation of the charity’s registration was a reasonable response to a failure to maintain or provide them.

Grounds: adequacy of documents

Prescient v Minister of National Revenue 2013 FCA 120:

[51] Indeed, the Minister has less drastic administrative corrective measures or intermediate sanctions available to him, such as formal notices, compliance agreements, or the suspension of a charity’s tax receiving privileges for one year under paragraph 188.2(2)(a) of the Act. The registration of a charity that fails to maintain proper records should, therefore, only be revoked on this ground in case of material or repeated non-compliance....

Grounds: adequacy of documents

Prescient v Minister of National Revenue 2013 FCA 120:

[56] Though Prescient was remiss in maintaining proper records of the Farm Sale Transactions, the CRA auditor was nevertheless supplied with a considerable amount of information concerning these transactions which allowed her to understand both their scope and their nature. In my view, it would not have been reasonable for the Minister to revoke Prescient’s registration on that basis alone. On the other hand, Prescient’s failure to maintain adequate records and books of account showing that its contribution to DATA was made to an American charity, coupled with its failure to voluntarily and promptly disclose this fact to the auditor, constitutes a very serious matter. Thus, both failures, taken together, are sufficient, in the circumstances of this case, to conclude that the Minister acted reasonably in revoking Prescient’s registration on the ground that it had failed to maintain adequate books and records.

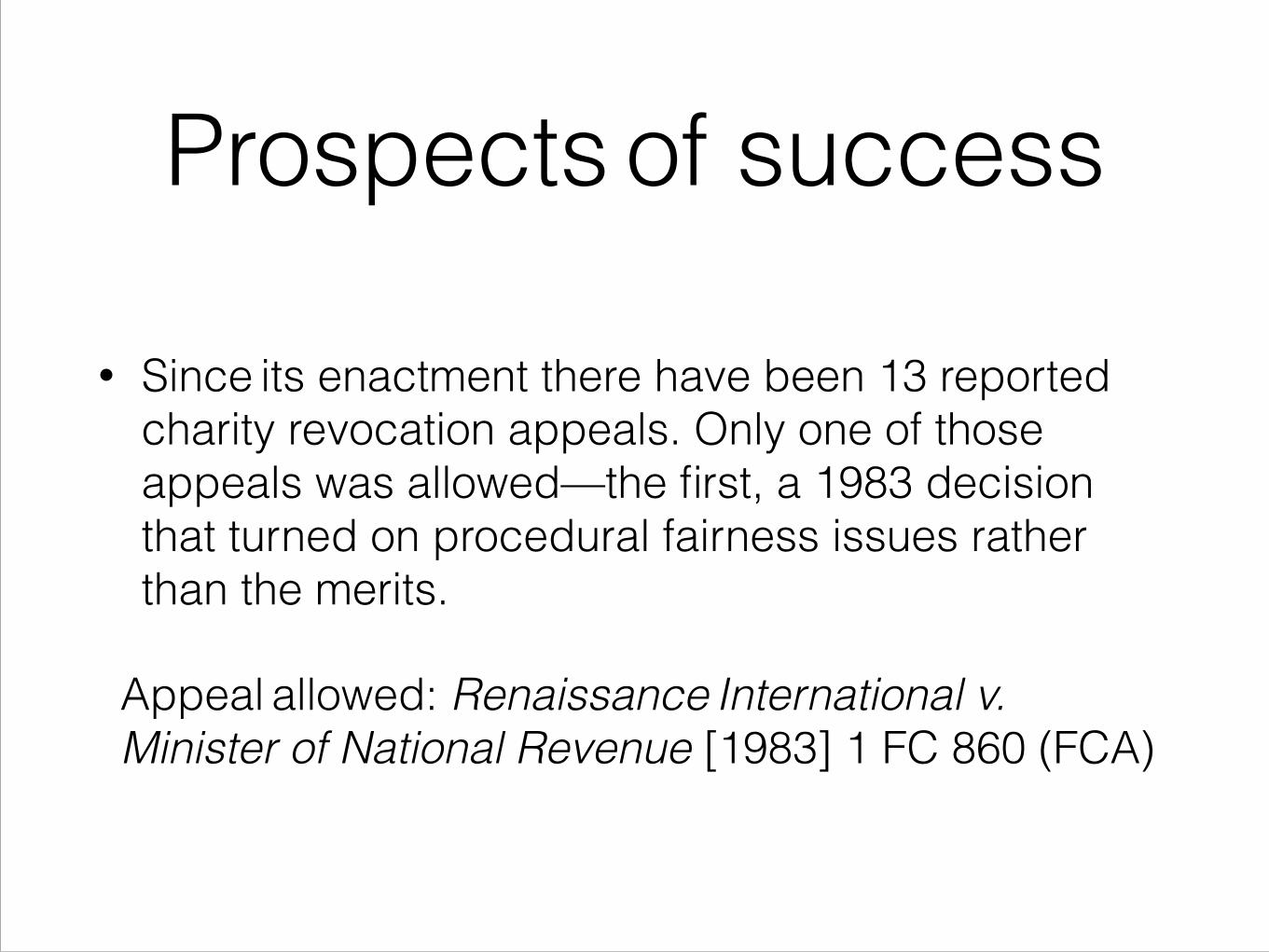

Prospects of success

• Since its enactment there have been 13 reported charity revocation appeals. Only one of those appeals was allowed—the first, a 1983 decision that turned on procedural fairness issues rather than the merits.

Appeal allowed: Renaissance International v. Minister of National Revenue [1983] 1 FC 860 (FCA)

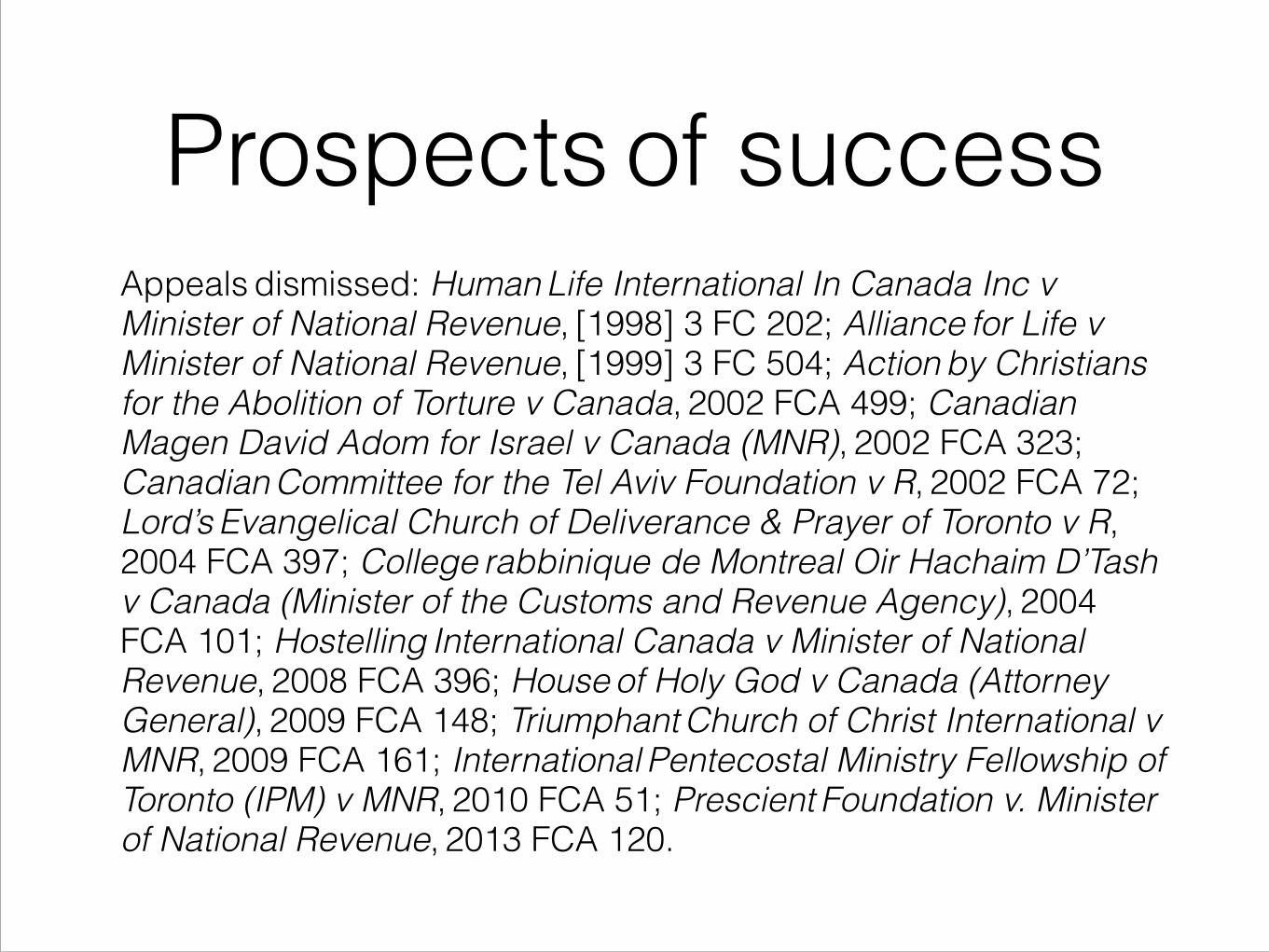

Prospects of successAppeals dismissed: Human Life International In Canada Inc v Minister of National Revenue, [1998] 3 FC 202; Alliance for Life v Minister of National Revenue, [1999] 3 FC 504; Action by Christians for the Abolition of Torture v Canada, 2002 FCA 499; Canadian Magen David Adom for Israel v Canada (MNR), 2002 FCA 323; Canadian Committee for the Tel Aviv Foundation v R, 2002 FCA 72; Lord’s Evangelical Church of Deliverance & Prayer of Toronto v R, 2004 FCA 397; College rabbinique de Montreal Oir Hachaim D’Tash v Canada (Minister of the Customs and Revenue Agency), 2004 FCA 101; Hostelling International Canada v Minister of National Revenue, 2008 FCA 396; House of Holy God v Canada (Attorney General), 2009 FCA 148; Triumphant Church of Christ International v MNR, 2009 FCA 161; International Pentecostal Ministry Fellowship of Toronto (IPM) v MNR, 2010 FCA 51; Prescient Foundation v. Minister of National Revenue, 2013 FCA 120.