Embed Size (px)

Citation preview

CHARITIES

CHARITY INSIGHT

MANAGING GROWTH & RISK IN NOT-FOR-PROFITS

AUTUMN 2016

Guest Interview 3

Be Risk Ready: Good Intentions Alone are No Protection 11

Davy Corporate Social Responsibility (CSR) Programme 14

US Election: Politics in the Age of Discontent 15

The Race To The White House 20

Asset Class Overview 26

EDITORS’ NOTE

About Charity Insight Charity Insight provides investment analysis from Davy Charities for discussion purposes only. It is not intended to constitute an offer or solicitation for the purchase or sale of any financial instruments, trading strategy, product or service and does not take into account the investment objectives, knowledge and experience or financial situation of any particular entity or person. You should obtain advice based on your own individual circumstances from your own tax, financial, legal and other advisers before making an investment decision, and only make such decisions on the basis of your own objectives, experience and resources. You may also contact a member of the Davy Charities team to discuss further any content of Charity Insight.

We are delighted to welcome you to the Autumn 2016 edition of Charity Insight.

Without doubt one of Ireland’s best known charities is Barretstown. For those of you who are not aware, Barretstown offers free, specially designed camps and programmes for children and their families living with serious illness – supported behind the scenes by 24-hour on site medical and nursing care. All of the children and families who attend Barretstown have their accommodation, food and medical assistance provided free of charge.

During the summer we were fortunate to visit the camp to interview the chief executive, Dee Ahearn and tour its facilities. We were amazed at the vibrancy, not least of the children but also of the staff at Barretstown. Dee talks passionately about Barretstown and its plans for the future.

The risks faced by charities today are broad and varied. It is necessary for charity trustees to regularly review and assess the risks faced in all areas of its work and plan for the management of those risks. It is a complex area but managing it effectively is essential if the trustees are to achieve their key objectives and safeguard their future.

Therefore we felt it appropriate to ask Paul Collins from Ecclesiastical Insurance to highlight some of the steps that can be taken to identify those risks and provide appropriate guidance on managing them.

As always, we hope you enjoy reading this edition of Charity Insight.

If you have any questions on any of the topics covered, please do not hesitate to contact any member of the Davy Charities team.

Ian Brady Head of Davy Charities

Adrienne Regan Senior Investment Adviser

2 Charity Insight Autumn 2016

Charity Focus

The story of growth at Barretstown Camp resonates at so many levels for the not-for-profit organisation today. Dee Ahearn, CEO of Barretstown, articulates both a strategic vision and practical roadmap for how to achieve that vision.

GUEST INTERVIEW

3Charity Insight Autumn 2016

Ian Brady: Dee, tell me a little about Barretstown?Dee Ahearn (DA): Barretstown was founded in 1994 by the late actor and philanthropist, Paul Newman, and based on his famous Hole in the Wall Gang Camp, which he established in Connecticut, USA.

We serve children affected by serious illnesses – primarily cancer and serious blood diseases and their families. Since Barretstown was founded, we have helped over 35,000 seriously ill children and their family members.

Everything we do is offered free of charge. Our specially designed camps and programmes are for children and their families living with a serious illness and this service is supported behind the scenes by 24-hour onsite medical and nursing care.

Barretstown is designed to respond directly to the needs of a child living with a serious illness – both clinical and psychological. Our Therapeutic Recreation model is recognised by paediatricians

and psychologists all over the world as an important and necessary component of a child’s treatment. We often say that the hospital treats the illness, we treat the child.

The Barretstown Therapeutic Recreation Programme provides fun activity-based challenges for children. Campers engage in a range of activities with various levels of challenges and are encouraged to achieve and to celebrate their successes. The activities are carefully directed through psychosocial support programmes which are now considered to be an integral part of treatment and recovery from serious illness.

And we know this programme is really successful. According to an evaluation conducted by the Yale Child Study Centre in the US, children with serious illness who attend a SeriousFun Camp showed improved confidence, higher self-esteem, a greater sense of independence and increased interest in social activities. The study also revealed that children’s stress related to their illness decreased as a result of the camp experience.

GUEST INTERVIEW BUILDING A SUSTAINABLE GROWTH PATH FOR BARRETSTOWN

Biography

As Chief Executive of Barretstown, Dee is responsible for managing and leading 80 employees and over 1,400 volunteers on an annual basis. She is also responsible for reaching Barretstown’s annual fundraising target of €5 million.

Dee’s background is in strategic and creative marketing. She has held senior management positions in Black & Decker Ireland, the Gunne Group and Treasury Holdings.

Dee has over a decade of board level experience having served on the boards of Barretstown, Treasury Holdings, Make a Wish Foundation, four years of which Dee held the position of Chairperson. Dee is currently Chairperson of the International CEO Council of the SeriousFun Children’s Network, of which Barretstown is a member.

Dee Ahearn

CEO Barretstown

"We often say that the hospital treats the illness, we treat the child."

Ian Brady and Adrienne Regan talk to Barretstown Chief Executive Officer (CEO) Dee Ahearn about the growth journey for the children's charity.

4 Charity Insight Autumn 2016

And how did you end up as CEO at Barretstown?DA: Before joining Barretstown I was on the Board of Treasury Holdings and while I was there my role involved communications, marketing, sales and corporate social responsibility (CSR). Given the role, and particularly the CSR element, I was well aware of the charity sector as a whole and the need for corporates to support charities, not only through the provision of funding, but also in terms of sharing expertise, knowledge and of course time.

Whilst there, I was chairperson of the Make a Wish Foundation for four years. I was on the board for seven years and through my involvement with them I became very familiar with Barretstown.

Then in 2010, I was approached about the role of CEO in Barretstown. It was a big decision, leaving the corporate sector to work here and so I thought long and hard about it, but deep down I felt I could make a real and lasting difference in this organisation and so I took a leap of faith.

One of my first priorities was to develop a long-term strategy for Barretstown that would focus on growth, expansion and reducing operating expenses through operational efficiencies and putting new structures in place for the future.

Clearly your strategy is working as I notice that the reach of Barretstown is growing and the number of campers is continuously increasing.DA: Yes, so far we are. Our strategic development plan is having real impact and is progressing as planned, which is fantastic.

It took us a little time to fine tune what we wanted to achieve and put plans in place. I carried out a complete strategic review of the organisation to identify what was working, what wasn’t working and to identify gaps and opportunities that I knew were there.

As a result of the strategic plan launched five years ago, we embarked on a major change programme. I’m proud to say that last November, I was able to present the outcomes to our board. In the past five years we have grown camper numbers by 165% and we have done that by increasing costs by less than 10%, a significant achievement considering the increase in activity during that time.

We have also invested heavily and extended nine of the existing cottages, built two new cottages, a multi-purpose indoor activity centre and undertook significant maintenance and upgrade work to the castle and existing buildings.

We are also in the middle of developing a new, modern dining hall. This involved a capital investment which was funded by a very generous legacy left to us in 2012 and the support of the Rory Foundation, John Fitzpatrick and Pioneer Investments who played a crucial role in allowing us to complete this much needed facility.

All of this work has resulted in improvements to our facilities for campers. For instance we have added some new and exciting activities, such as a mini golf course, indoor climbing wall, pet farm and a new archery range.

"In the past five years we have grown camper numbers by 165% and we have done that by increasing costs by less than 10% (...)"

Barretstown campers

DAVY CHARITIES | Guest Interview

5Charity Insight Autumn 2016

So you are now thinking of your next strategic plan?DA: Yes, absolutely. We’re now in the process of looking at the Barretstown 2020 vision and strategic plan. It’s a very exciting time and I’m really looking forward to the next phase of growth.

Our next plan will prioritise increasing the number of programmes we deliver, reducing our waiting lists and expanding our camp programmes to reach more seriously ill children and families who really need our services.

You talked about the satisfaction you get from working here and it’s obviously quite different from the corporate sector. Yet, you do operate quite a tight corporate-type ship.DA: Yes that’s entirely true. I don’t believe a charity should be run any differently to a business. My approach has always

been commercially minded with a view to growth and expansion. I came from an environment where you worked incredibly hard, everything was about reporting, key performance indicators (KPIs), budgets, delivering objectives and making sure that you got the best possible result. It shouldn’t be any different in Barretstown and we have worked hard to ensure it isn’t.

I suppose the difference for me personally is that I am now ultimately responsible and accountable as the CEO of this organisation, whereas in the past I was a member of a large team. At the end of the day if I don’t raise sufficient funds it will impact our service delivery and camps, and children will suffer as a result. It’s very personal. I see the children and the families that come here to Barretstown and I know I have to bring in the funds for them. It’s a real motivator and one I take very seriously.

GUEST INTERVIEW: BARRETSTOWN

"My approach has always been commercially minded with a view to growth and expansion."

RORY’S DRIVE FOR CHARITIESBarretstown was among the charities supported by The Rory Foundation, the charity established by leading golfer Rory McIllroy. The Rory Foundation also supported the Jack & Jill Foundation and the Laura Lynn Children’s Hospice.

Through his foundation, Rory McIlroy donated a total of €317,000 to each of the three charities earlier this year from the proceeds of his win at the 2016 Dubai Duty Free Irish Open at The K Club in May, as well as tickets sales from related fundraising events at the tournament.

"While winning the Irish Open this year meant a lot to me, being able to give my prize money to three local children's charities made it all feel much more special.” Rory McIlroy

"Thanks to the events and initiatives that took place during the week of the Irish Open we were able to raise a huge amount of money for

three very worthy charities." Barry Funston, Chief Executive of the Rory Foundation

Barretstown will use the money to help pay for the fit out of its new dining hall, while Jack & Jill will pay for more than 19,800 hours of home nursing care. The LauraLynn hospice will use the funding to cover the cost of two clinical nurse specialists, as well as expenses and administration costs.

6 Charity Insight Autumn 2016

Over and above our three-five year strategic plan we work to a clearly defined work schedule and calendar of events annually. This helps us keep focused on achieving our targets and delivering above and beyond for our campers.

Since 2012 income has grown from €3.5 million a year to just under €5 million a year. We have achieved that at a time of significant challenges in the charity sector. I believe we achieved that because we operate to the highest standards. We have signed up to the Governance Code, which is a voluntary code developed for community, voluntary and charitable groups. In addition, our Annual Report incorporates statutory requirements as outlined in the Companies Act 2014. Barretstown has also adopted the Statement of Recommended Practice of Charities in accordance with FRS102, which is not yet mandatory in the Republic of Ireland, but is considered best practice. We also secured a National Standards Authority of Ireland (NSAI) Excellence Through People standard, achieving a score of 84% and placing Barretstown in the top 30% of companies audited in 2014/2015. Our next audit is due to take place this November.

We worked really closely with our board and its standing committees to ensure that we were managing the business appropriately and running a tight ship.

Would you say the role is more 24/7 than in the corporate world?DA: Yes, it really is 24/7. Our camps take place over weekends, school holidays and bank holiday weekends throughout the year.

I suppose like every CEO you need to have your finger on the pulse, both from an organisation point of view, but also a sectoral and category point of view. I also think that while the fundraising and other duties of running the organisation are important, what is truly important and at the heart of what we do is the quality of the programmes we offer the children and families that come here. Barretstown is part of a wider global network, called the SeriousFun Children’s Network, and so I’m in regular contact with other camps in the US and Europe and learn new practices and

"(...) what is truly important and at the heart of what we do is the quality of the programmes we offer the children and families that come here."

activities so that we can offer our campers cutting edge therapeutic recreation that will help them develop and recover fully.

How has the structure of the organisation changed lately?DA: It has changed a lot and so has the environment in which we operate. When I started we had just two standing committees of the board, a finance & audit committee and a childcare advisory committee. I worked with our chairman Maurice Pratt to establish additional standing committees; a nominations & remuneration committee, risk & governance committee and a development committee. These committees are made up of board members, external expertise and members of the senior leadership team here at Barretstown. Having a good structure which would operate at the highest corporate governance standards was a priority for me.

So too was strategy, which is why we developed a strategic plan. I think that over the past number of years we have also increased input from our board which has significantly bolstered our plans and helped us achieve and deliver at a higher level.

Would you say it was daunting? I am partly thinking that some smaller charities might be reading this in terms of resources.DA: Yes I would, but it’s important. It’s about accountability, transparency, reputation and credibility.

We invested a lot of time and effort into our governance structure, what it might look like and what we needed to have in place. Every board member agreed and supported the team in developing this governance framework. We had to ensure that Barretstown was positioned for success and we had to ensure that we could deliver and this was a key part of being successful.

Transparency and accountability are hugely important qualities?DA: Yes, in any business and for me, in any member of my team. It’s paying off. I recently presented our risk register to some of our board members, who work for big organisations and some said “wow, our processes aren’t as advanced as this.” It’s great to get that kind of feedback.

DAVY CHARITIES | Guest Interview

7Charity Insight Autumn 2016

In terms of the corporate plan – how do you frame it?DA: Every year we develop a master action plan and it’s really simple. It follows the FCOP model - finance, customer, operations and people.

We set out our financial objectives, customer objectives, which of course are our campers and families, objectives under operations and people objectives. We present them to our board every March for feedback and approval.

The plan is implemented by what we call internally the ‘map team’ here in Barretstown, which comprises members of our senior leadership team and our managers.

Every quarter we review how things are progressing to make sure we are on track. If there are any roadblocks, we identify them and propose solutions. At every board meeting I prepare a report which highlights successes, but also challenges we face. The board considers these reports, scrutinises them and offers support. I’m very lucky to have such an engaged board.

How do you ensure that income is sustainable?DA: That’s an ongoing challenge. When I joined the organisation in 2010, over 40% of our income was coming from the corporate sector. And of that, 70% was coming from three organisations. It’s a fundraising base that wasn’t sustainable and I knew I had to act quickly. We set up our development committee, comprising members of our board, senior leadership team and external experts who have the capacity to help us open doors and to help us raise awareness for Barretstown.

We recognised the need to widen the base and recruit more corporate and individual givers. We also focused on exploring multi-year partnerships with donors who had the capacity to enter into such agreements with us. We have had a particularly supportive partnership with Lidl for the past four years.

Our corporate partners support us in many ways, not only financially but through awareness raising initiatives, marketing and point of sale in stores. Their employees also get heavily involved by volunteering at camps and lending us support to maintain our gardens and even painting fences!

Engagement is so important to our corporate donors. Lidl, one of our big corporate partnerships, or indeed GSK and Pioneer Investments, often come down to Barretstown for corporate events. This ongoing and regular engagement allows our supporters to see first-hand how the money they raise is helping children and families affected by serious illness.

That’s how we approached it from a strategic point of view, but it’s also important not to forget the personal touch. Simply picking up the phone and thanking someone personally for a donation is so important. Inviting donors to Barretstown to see how that donation has made a real impact is also really important. These simple acts can have a profound effect and can result in enduring relationships with donors and partners.

We also looked at innovative ways to create new fundraising initiatives. For example, we have a wonderful facility here which is ideal for corporate events. Our castle is a unique place to host meetings and we have all the facilities onsite to provide for catering to large numbers. Over the past few years this is an income stream which we have developed around our camp calendar.

In terms of the children what would happen, in your mind, if there was no Barretstown?DA: We know from medical experts that cancer treatment for children can last for years. While such treatment now produces so many very positive outcomes medically, its intensiveness and duration can seriously disrupt childhood. Through the Barretstown camps and our Hospital Outreach Programme we enable children to just be children, even while undergoing such disruptive treatment.

"This ongoing and regular engagement allows our supporters to see first-hand how the money they raise is helping children and families affected by serious illness."

GUEST INTERVIEW: BARRETSTOWN

8 Charity Insight Autumn 2016

Take a boy who has been diagnosed with leukaemia, for example. His treatment can last up to three years if it goes as planned. Such lengthy treatment can have a significant developmental impact. That child will spend three years going in and out of hospital. They will be at home a lot, protected from public places for fear of infections and so naturally they are going to miss out on a significant chunk of the normal childhood experience. The child’s friends continue with their lives, going to football on Saturday or having friends over and sleepovers, which very often a seriously ill child can’t do. It can be very isolating. The child is also often the centre of their parents’ attention, they grow up too fast and lose a sense of independence.

At Barretstown we try to turn that around. We try to give a seriously ill child a reminder of what childhood should be like and what it can be like post-illness. The children take part in activities whether it’s high ropes, archery, canoeing, or performing onstage. While this is a lot of fun, there is a serious, practical and evidence-based programme behind it. Each activity is designed to help rebuild a child’s confidence and self-esteem. So, for example, we might have a child who is absolutely petrified of heights. The camp

team, or Caras (Irish for Friend), as they are called here, will say to that child “Well look, why don’t you just try the small ropes because they are not too high?”.

And that night when they come back to their cottage, they’ll have a chat with their Caras who will say, “You were absolutely terrified to go on the small ropes today but do you realise that you did really well on them?” Very often over a few days the child will go higher and higher, until ultimately they end up at the highest level. And that child will say, “Oh my God, I did that.”

Bit by bit we aim to rebuild the child’s self-esteem and confidence during the eight days they spend with us.

What would give you most satisfaction to see in Barretstown, say by 2020, that you don’t have now? DA: We would dearly love to see Barretstown open all year round. In 2010, Barretstown’s camps were starting in April and finishing at the end of October which meant that this wonderful site was vacant for a third of the year. We’ve succeeded in expanding and extending the camp’s calendar. Next year the camp will start in February and it’s not going to end until December.

"We try to give a seriously ill child a reminder of what childhood should be like and what it can be like post-illness."

Dee Ahearn, chief executive of Barretstown

DAVY CHARITIES | Guest Interview

9Charity Insight Autumn 2016

Barretstown Talks is proud to present an afternoon with Orla Kiely

Orla will discuss life, inspiration and a hugely successful career in design with publisher and broadcaster Norah Casey.

Friday 25th November, 2016 from 12:30pm - 3pmThe Supper Room, The Mansion House, Dublin 2 (Fire Restaurant Entrance)€100 includes drinks reception, lunch & exclusive luxury goody bag for each guest.

All proceeds will go directly to Barretstown.Bookings can be made at www.barretstown.org, by email [email protected] or call 045 864 115

Orla KielySponsored by

So, what I would love to see is a move towards being open all year round with an increase in our camper numbers.

We would also like to grow our hospital outreach programme. Finally, I’d like to look at other illness groups and age groups that could really benefit from Barretstown’s programmes.

And the children’s hospital, does that help in terms of growing your outreach?DA: Yes, we have a very good relationship with Our Lady’s Children’s Hospital Crumlin and the vast majority of our campers are its patients. They are hugely supportive to us and the work we do because they recognise that the hospital treats the illness, but Barretstown treats the child.

One of their consultants, Professor Eoghan Smith, was quoted in The Irish Times saying that Barretstown is as important as the chemotherapy that these children receive. It’s so important from a developmental point of view.

Our outreach programme is in Our Lady’s Children’s Hospital Crumlin three days a month and we would love to expand that. We work closely with the team in the hospital and we know that they would really like us to expand the service we provide them. I really do hope that we can achieve that over the coming years.

Our outreach programme takes place in Dublin, Limerick, Cork and Belfast and is a very important part of the service we provide.

Barretstown’s mission is to rebuild the lives of these children and their families. To find out more visit www.barretstown.org, follow @Barretstown on Twitter or visit www.facebook.com/Barretstown.

WARNING: The opinions expressed in this interview are the views of the interviewee and do not reflect the views and opinions of Davy.

GUEST INTERVIEW: BARRETSTOWN

10 Charity Insight Autumn 2016

BE RISK READY: GOOD INTENTIONS ALONE ARE NO PROTECTION

"Organisations today need to devise innovative ways of raising funds."

Paul Collins

Paul is the Head of Risk Services Ireland for Ecclesiastical Insurance Office plc, a specialist insurer providing insurance and risk management solutions to the charity, faith, education and heritage sectors.

Managing risk has always been an important part of business. With a rise in litigation and the introduction of new compliance and health and safety legislation, this has placed an ever greater burden on businesses. Organisations in the charity sector are not immune to these developments.

While businesses never relish the onerous task of adhering to a myriad of legislation and regulation, the costs of non-compliance can be much higher. Those costs can come in the form of prosecutions, compensation payments, reputational damage and the withholding of funding. Having a robust risk management system in place is essential, as is understanding who has responsibility for its delivery – the directors and officers of the organisation.

Claims costs are the main drivers of insurance premiums and the rising volume and value of claims are primarily responsible for the premium hikes today.

Charities are exposed to a more adverse and severe range of risks than many other businesses; including reputational risk and risks associated with volunteers, fundraising and working with children or vulnerable adults. Risk management should therefore be one of the key focus areas for any charity business.

The Safety, Health and Welfare at Work Act 2005 aims to ensure that no one gets injured or ill because of their work, whether paid or voluntary. Preparing a Safety Statement and conducting detailed Risk Assessments help reduce the incidence and severity of accidents and ill-health at work. These are statutory requirements for any organisation which has three or more employees. Organisations with well managed health and safety policies have lower rates of absenteeism, lower costs and greater productivity levels. They are also less likely to be prosecuted under health and safety legislation, where penalties can be as high as a €3 million fine and/or up to two years imprisonment.

Let us now look at three risks common to the charity sector; namely fundraising, volunteering and working with children and/or vulnerable adults.

Fundraising Organisations today need to devise innovative ways of raising funds. Fundraising events such as sky-diving, parachute jumps, bungee-jumps and even abseiling down the side of buildings are commonplace. Whether you’re organising a low risk event such as a garden fête or a high risk experience like parachuting, all events need to be properly planned and thoroughly risk assessed by a “competent person”. Your risk assessments must be documented and any controls identified must be implemented. You also need to prepare a plan to cater for all eventualities and emergencies, which should be rigorously tested. The provision of first aid, emergency evacuation procedures, and appropriately trained marshals should be implemented.

Assistance should be sought from the bodies such as the Health & Safety Authority, www.hsa.ie. If you have no experience of organising events, particularly high hazard events, then you should give serious consideration to engaging experienced professionals to facilitate these events for you. Always look for documentary evidence that any contractors you use hold insurance protection and check that your own liability insurance policies will cover you for the proposed events.

What about fundraising events that are carried out of which you have no knowledge? Many people raise funds for their charities without advising the charity. Often, the first the charity knows about the fundraising is when they receive the funds. Such events are run to maximise the financial benefit for the charity with no resources invested in planning, security, first aid, insurance, electrics, safe access, emergency procedures, parking, toilet facilities or health and safety. These well intentioned fundraisers could have exposures to serious claims and need professional advice.

Volunteers An employer owes a duty of care to everyone on their premises, including employees, visitors, contractors, customers and volunteers. The Safety, Health and Welfare at Work Act 2005 requires you to do all that is reasonably practicable to

11Charity Insight Autumn 2016

protect the safety, health and welfare of all your employees, as well as any persons not in your employment who may be affected by your work. In our experience, supervising and managing volunteers is an area that is most often neglected by employers and does result in significant and serious claims.

Under health & safety legislation, persons working as volunteers are considered to be employees and persons making use of volunteers to be employers. The employer is obliged to carry out risk assessments on the activities and duties of all employees and volunteers. Volunteers should be treated in the same manner as employees, but could require more training, supervision and management than your employees. Rigorous training programmes should therefore be conducted regularly by suitably qualified trainers and documented evidence of the attendance by all staff and volunteers on these training courses must be completed and retained.

Organisations should also be aware they can be vicariously liable for the acts or omissions of their employees and volunteers, when these result in injuries to other persons or damage to their property.

Policies on the protection of children and vulnerable personsThose benefitting from charitable activity may include vulnerable children or adults. There are strict obligations attached to how they and their employees and volunteers interact with them. You will need to;

π Draft a Child Protection Policy and/or a Vulnerable Adult Protection Policy which should include details of;

- Allocation of responsibilities

- Recruitment of employees and volunteers, who must all be Garda vetted and reference checked

- Robust supervision procedures

- Reporting procedures

- Code of conduct for employees and volunteers

- General management & safety

π Communicate the policy to all staff and volunteers

π Appoint a designated liaison person(s)

π Train all staff and volunteers on child/vulnerable adult protection procedures.

Some vulnerable persons may have issues around challenging behaviour and can pose a threat to the safety of your staff and volunteers. It is essential that such issues are included in the risk assessments and that all relevant information is communicated to the employees and/or volunteers who may interact with persons who have challenging behaviour issues. Training in de-escalation techniques and strategies on how to deal with challenging behaviour should be provided. Lone working must never be permitted.

Figure 1: Components of an effective health and safety management system

HEALTH & SAFETY POLICY

IDENTIFY HAZARDS

RISK ASSESSMENTS

DECIDE WHO MAY BE

HARMED AND HOW

IMPLEMENT CONTROLS

TO ELIMINATE OR REDUCE HAZARDS

RECORD FINDINGS

REVIEW AND REVISE

"Organisations should also be aware they can be vicariously liable for the acts or omissions of their employees and volunteers, when these result in injuries to other persons or damage to their property."

12 Charity Insight Autumn 2016

Additional advice and assistance on all health and safety matters can be obtained from your insurers or from the Health & Safety Authority, www.hsa.ie.

Further information on child protection is available from:

TUSLA, the Child and Family Agency T: 01 771 8500 www.tusla.ie

Department of Children & Youth Affairs T: 01 647 3000 www.dcya.gov.ie

ISPCC T: 01 676 7960 www.ispcc.ie

The benefits that accrue from carrying out the above will outweigh the effort and costs involved in developing and implementing good health and safety procedures in your business. Good risk management minimises the need to rely on luck to avoid serious accidents and the negative impacts that inevitably flow from them.

WARNING: The opinions expressed in this article are the views of the author and do not reflect the views and opinions of Davy.

DAVY CHARITIES | Be Risk Ready

13Charity Insight Autumn 2016

Davy is currently in the second year of a three year Corporate Social Responsibility (CSR) programme which supports HOPE, SOAR and a collaboration of homeless charities including Peter McVerry Trust, Focus Ireland and The Simon Community.

Each charity is represented by two Davy charity champions who raise awareness of their charity and hold or participate in various fundraising events in aid of their charities throughout the year.

HOPEOn 6th June this year many of our female colleagues took part in this year’s VHI Woman’s Mini Marathon to raise money on behalf of the HOPE Foundation.

A casino night was held in Davy in aid of the charity which raised an additional €1,350 for HOPE.

In November 2016, two Davy employees will make a trip to Kolkata to help the HOPE volunteers. They will visit various HOPE projects in Kolkata and work with a team to help paint some of the children’s crèches and homes.

DAVY CORPORATE SOCIAL RESPONSIBILITY (CSR) PROGRAMME

Davy employees participating in fundraising events.

SOARThere was a large Davy contingent representing SOAR in the Grant Thornton Corporate Challenge which took place on 13th September. Congratulations to our winning ladies team who are pictured above with their trophy.

HOMELESS CHARITIESPeter McVerry, Focus Ireland and Simon Community We had another very successful turnout for the Wexford cycle this year with many Davy employees enduring the long cycle in support of the Peter McVerry Trust. We also arranged a charity golf competition in aid of the homeless.

Other CSR Initiatives:In addition to our partner charities mentioned above, we are participating in the Time to Read programme run by Business in the Community. This is our third year to be involved with this great programme helping the children from O’Connell’s Boy’s School to improve their reading skills and confidence.

We have also recently launched our Davy Green Team which consists of employees from different areas of the company coming together with the aim of identifying and implementing solutions to help Davy operate in a more environmentally sustainable fashion.

14 Charity Insight Autumn 2016

US ELECTION:POLITICS IN THE AGE OF DISCONTENTOn 8th November US voters will be faced with the difficult decision of voting for two of the most unpopular presidential candidates in recent history. Republican candidate Donald Trump has tapped into a growing level of economic and political discontent while Democrat Hillary Clinton has failed to offer an inspiring alternative. Regardless of the outcome, the root causes of rising income inequality and declining public trust in government will continue to dog American leaders. The next president will need to address these domestic issues as well as a series of increasingly complex global challenges.

Election 2016 infographic on page

22

Economic and Investment Focus

15Charity Insight Autumn 2016

On 8th November Americans will go to the polls to vote for the next president of the United States in the same way they have 57 times over the past 228 years. And yet this election feels very different to any in recent history.

The rhetoric is more divisive. Voters are angry and discontent. Furthermore, the majority of the population has an unfavourable impression of Hillary Clinton and Donald Trump, the two final presidential nominees.

Regardless of whether it's Trump or Clinton, the issues that gave rise to this discord will persist. The next president of the United States will have to face these domestic challenges while navigating an ever more complex global economic and political environment.

The angry electorateAccording to the World Bank, the world is better off today than at any time in history. Globally people are wealthier, healthier, more democratic and better educated than they were a decade or two ago. It is widely accepted that globalisation and improved technology have resulted in a more socially and economically interconnected society. Yet large parts of the world’s population do not share such a positive assessment.

In the US, as in other advanced economies, the long-term impact of globalisation — free trade, offshoring, labour migration, market-oriented policies and relegation to supranational authorities — has come at a

cost to some parts of the population. This is a result of employment loss as jobs move overseas to cheaper labour markets, wage stagnation due to lower profits in the face of cheaper imports under trade agreements or lower cost labour from immigration.

Consumers in advanced economies have clearly benefited from lower priced imported goods. However, low and medium skilled workers have lost income and jobs as a result. One only needs to visit Rust Belt cities like Detroit and Cleveland to see the full impact of globalisation and deep recession.

An uneven recoveryTo make matters worse, the global financial crisis wreaked havoc on the American economy. It resulted in an unprecedented number of job losses, business failures, personal bankruptcies and loss of savings. Homeowners have witnessed the value of the equity in their homes decline and historic numbers have lost their homes.

Seven years into the slowest post-WWII recovery on record, many Americans feel there has been no real recovery from the worst recession in 75 years. In 2014, real median household income was lower than in 2007 - the year before the most recent recession - and US household income peaked back in 1999. The financial position of the middle class has not improved for the past 15 years; in fact it has deteriorated. Income inequality has surged close to levels witnessed before the Great Depression of the 1930s, as the average income of the top

US ELECTION: POLITICS IN THE AGE OF DISCONTENT

"It's the economy, stupid." James Carville, Presidential campaign manager to Bill Clinton

Alan Werlau

Senior Investment Strategist

16 Charity Insight Autumn 2016

"This wave of globalization has wiped out our middle class." Donald Trump, June 2016, on the campaign trail

1% of US households increased 7.7% in 2015 to $1.36 million, twice the rate of the other 99% whose pay averaged $48,768.

The rise of the protest candidateAgainst this troubled backdrop, this year’s field of presidential candidates was chock-a-block full of non-establishment protest candidates. Three out of four major candidates, Donald Trump, Bernie Sanders and Ted Cruz, did not have the full support of their respective parties and campaigned on issues well beyond their party’s official line.

Republican candidate Trump and Democratic candidate Senator Sanders proved how easy it is to win popular support by championing the cause of the evils of globalisation. Trump has found success tapping into the fear, whether real or perceived, of opportunities lost to migrants and jobs exported to cheaper overseas markets. Sanders garnered huge support from those who felt victimised by the growing disparity in wealth. While these issues are not new, they have never been as significant as they are in this election cycle. Nor are they solely American problems as evidenced by the recent successful Brexit vote.

Millennials outnumber baby boomers The concern about income inequality comes

at the same time as significant demographic shifts in the US. This election is the first time that Millennials (adults aged 18-35) will make up the majority of the population and registered voters. The American dream of a job for life, home ownership and economic prosperity seems to be fading with the decline of the Baby Boomers (adults aged 52-70). Younger voters have bleaker employment outlooks, stifling student loan burdens and a bankrupt social security system, which has mortgaged their future while paying benefits to retirees well above their actual contributions. Millennials were a verbal part of the election campaign and rallied around candidates such as Sanders, whose socialist leaning and promise of free university education and student loan forgiveness resonated.

The elephant in the roomTrump attempted to tap into the majority of Republicans looking for a significant change in the party after the unimpressive leadership of President George Bush and failed presidential candidate Mitt Romney. Trump has done this by moving towards a pragmatic centre position blending conservative and liberal elements of the party. His grassroots support is from voters who think he “tells it as it is…” and speaks to them rather than at them like other politicians.

Sour

ce: T

he N

ew Y

ork

Tim

es

PER

CEN

T

0

10

20

30

40

50

60

48.2%

36.2%24.2%

228 301 423

608 531 777

992 1,048

1,337

1,675

1,974

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

50

100

150

200

250

300

350

Jan

2009

A

pr 2

009

Jul 2

009

Oct

200

9 Ja

n 20

10

Apr

201

0 Ju

l 201

0 O

ct 2

010

Jan

2011

A

pr 2

011

Jul 2

011

Oct

201

1 Ja

n 20

12

Apr

201

2 Ju

l 201

2 O

ct 2

012

Jan

2013

A

pr 2

013

Jul 2

013

Oct

201

3 Ja

n 20

14

Apr

201

4 Ju

l 201

4 O

ct 2

014

Jan

2015

A

pr 2

015

Jul 2

015

Val

ue o

f €10

0 in

vest

ed o

n 31

st J

anua

ry 2

00

9

PERC

ENT

ELECTION 2016 POLL OF POLLS

49

47

45

43

41

37

35

31

Jan 2016 Jun 2016 Jul 2016 Aug 2016 Sept 2016

16

17

18

18

20

20

9.0

9

9

9

9

9

61

61

56

54

51

50

10

10

12

11

12

12

4

4

5

7

8

9

0% 10% 20% 30% 40%

ADULT POPULATION BY INCOME TIER (MILLIONS)

50% 60% 70% 80% 90% 100%

1971

1981

1991

2001

2011

2015

CLINTON TRUMP

DAVY | US Election: Politics in the Age of Discontent

Figure 1: Clinton in the lead but the public remains divided

Election 2016 poll of polls

17Charity Insight Autumn 2016

The most remarkable aspect of Trump’s candidacy is that his supporters overlook his crudeness and radical positions because they believe he can solve what they consider to be the most pressing issue facing America today — the economy. His antagonistic positions on trade, immigration and economic growth appeal to voters who feel discontent and disenfranchised.

Same issues, different approachesThe uneven nature of the economic recovery and rising income inequality are the leading issues in this election. However, several other issues follow closely behind, including the cost of healthcare, immigration, globalisation and trade. Even the issue of security and terrorism are often intentionally woven into the anti-immigration rhetoric.

Democratic candidate Hillary Clinton has only reluctantly recognised the issue of income inequality as a response to Sanders’ socialist-leaning platform which highlighted the issue. Clinton has pledged more money for the lower and middle classes by promising to raise taxes on the wealthy, increase the federal minimum wage, offer tuition-free university and boost infrastructure spending.

Trump in contrast claims the system is rigged against the average American. He pledges to bring back jobs by renegotiating trade deals, spending more on infrastructure than Clinton and running a higher budget deficit. Trump’s tax proposals would allow the wealthiest Americans to keep more money.

The stakes are highUS presidential elections always carry high stakes and this one is no exception. For the first time in several decades, the US’s influence as the world’s sole superpower has faded and lost some of its lustre. Both candidates have acknowledged as much, but they plan to exercise leadership very differently. Trump’s “America First” approach would view America’s alliances and coalitions in terms of their net benefit to national interests, while Clinton considers international coalitions and partnerships as essential tools to use American influence overseas.

This election will also have a long-lasting impact on the fabric of American society. The death of conservative Supreme Court Justice, Antonin Scalia, earlier this year means the majority vote between liberals and conservative justices has come into play. The next president will choose his replacement. In addition, two other justices are nearing retirement. So a historic opportunity exists for the next president to alter the composition of the Supreme Court which will impact major decisions for decades to come. A Clinton victory could lead to a significant liberal shift on issues such as abortion, affirmative action, voting rights and the president’s powers on immigration and deportation.

Surely Clinton will win, right?Clinton represents the Democratic establishment and has the full backing of her party’s apparatus, while Trump does not represent the Republican establishment and has not benefited from their support. One could easily conclude that Clinton

"You can’t just talk someone into trusting you. You’ve got to earn it." Hillary Clinton

PER

CEN

T

0

10

20

30

40

50

60

48.2%

36.2%24.2%

228 301 423

608 531 777

992 1,048

1,337

1,675

1,974

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

50

100

150

200

250

300

350

Jan

2009

A

pr 2

009

Jul 2

009

Oct

200

9 Ja

n 20

10

Apr

201

0 Ju

l 201

0 O

ct 2

010

Jan

2011

A

pr 2

011

Jul 2

011

Oct

201

1 Ja

n 20

12

Apr

201

2 Ju

l 201

2 O

ct 2

012

Jan

2013

A

pr 2

013

Jul 2

013

Oct

201

3 Ja

n 20

14

Apr

201

4 Ju

l 201

4 O

ct 2

014

Jan

2015

A

pr 2

015

Jul 2

015

Val

ue o

f €10

0 in

vest

ed o

n 31

st J

anua

ry 2

00

9

PERC

ENT

ELECTION 2016 POLL OF POLLS

49

47

45

43

41

37

35

31

Jan 2016 Jun 2016 Jul 2016 Aug 2016 Sept 2016

16

17

18

18

20

20

9.0

9

9

9

9

9

61

61

56

54

51

50

10

10

12

11

12

12

4

4

5

7

8

9

0% 10% 20% 30% 40%

ADULT POPULATION BY INCOME TIER (MILLIONS)

50% 60% 70% 80% 90% 100%

1971

1981

1991

2001

2011

2015

LOWEST LOWER MIDDLE MIDDLE INCOME UPPER MIDDLE HIGHEST

Figure 2: The middle class is shrinking

Middle income Americans no longer in the majority

Sour

ce: P

ew R

esea

rch

anal

ysis

of t

he

Cur

rent

Pop

ulat

ion

Surv

ey, A

nnua

l Soc

ial

and

Econ

omic

Sup

plem

ents

, 197

1 an

d 20

15

18 Charity Insight Autumn 2016

will win by a large margin as the cards are stacked in her favour and the current polls reflect this. But as we saw in the UK’s Brexit vote, raw public opinion is only modestly indicative of likely results.

Election Day is when Americans vote for the president, senators, representatives in Congress, state governors, mayors and other local officials who in many ways have a much greater impact on their day-to-day lives. A typical ballot is organised in columns dividing Democratic and Republican Party candidates with the option to simply check one box or move one lever and vote ‘the party line’. The majority of voters tend to vote for all of their party’s candidates rather than cross party lines to vote for the opposing candidate. As unpalatable as either of the candidates may be, they tend to get the votes given to the Democratic or Republican ticket.

Voter turnout is important Another significant factor will be voter turnout. American presidential election turnout ranges from 48% in 1996, when Bill Clinton was re-elected, to 57% in 2008, when Barack Obama won the race to the White House. The result in November will be influenced not just by the number of voters but critically by who turns out. The anti-establishment protest vote which

supported Sanders may protest by not voting since Clinton is not their candidate. Republican protest voters will turn out to vote for Trump. Given the political polarisation which has increased over the past decade and the high disapproval of each candidate inside and outside their own parties, the coming weeks promise to bring one the most negative campaigns the US has seen. The rest of the world will remain on edge until the votes are counted and the dust settles.

Control of the Senate is also up for grabs in this election. The expectation is for the presidential winner to also gain control of the Senate. Consensus is for the House of Representatives to remain under Republican control. Therefore, a Trump victory could see Republicans control the Executive and Legislative branches. Financial markets are likely to favour a Clinton presidency, not due to any preference for her policy platform, but on the expectation that the House of Representatives remains Republican. This underlying preference for a divided government and the gradualism it brings, compared to an abrupt pivot in policy, could mean the markets reward a Clinton victory. A Trump sweep of the White House, Senate and House would probably be met with a greater level of uncertainty and volatility.

"The result in November will be influenced not just by the number of voters but critically by who turns out."

HOW AMERICA’S ELECTORAL COLLEGE WORKS

The American electorate system is called the Electoral College. This essentially is a group of 538 people who choose the winner, meaning 270 are needed to elect a president. When the public cast their vote they are actually voting for these “electors”. Each state has a certain number of electors based on their population in the most recent census. The candidate with the most votes in each state becomes the candidate which that state supports for president. Almost every state adopts a winner-takes-all system meaning that the person who wins the most electors in California, for example, will get all of the state’s 55 electoral votes. This means that it is possible, as in the case of Al Gore vs. George W. Bush in 2000 that the winner of the election may actually receive a lower percentage of the popular vote.

WHAT ARE SWING STATES?

Many states tend to vote for one party almost all of the time. For example, New York votes Democrat, Texas votes Republican. So in the race to get to the magic number - 270 - it's the swing states that often matter most. The winner-takes-all system of electoral voting, that is adopted by all states except Maine and Nebraska, has led to the existence of ‘battleground’ or ‘swing’ states. These are the states where recent presidential elections have been decided by a narrow margin and are thus viewed as very important in determining the result of the election. Candidates will tend to focus their energy on campaigning in the swing states.

DAV | US Election: Politics in the Age of Discontent

19Charity Insight Autumn 2016

THE RACE TO THE WHITE HOUSE

THE INTERVIEW

Alan Werlau: Let’s start with the most obvious question: Who do you think will win the election?Mona Sutphen: The fundamental contours of this presidential cycle remain unchanged: this election is Clinton’s to lose with a 75%+ likelihood of victory. Our current poll-of-polls model projects Clinton receiving 323 electoral votes, with 215 for Trump.

This is because Clinton has multiple paths to reach 270 electoral votes, but Trump must accomplish three goals simultaneously: prevent Clinton from winning Arizona, Georgia and North Carolina — all states Romney won in 2012; also he needs to win one of New Hampshire, Iowa or Nevada; and finally Trump needs to sweep the remaining toss-ups: Ohio, Florida and Pennsylvania. This is a difficult, but not impossible, task.

AW: Non-establishment candidates have played a large role in this election. Why do you think candidates like Donald Trump and Bernie Sanders have done so well?MS: In my view, there are two fundamental reasons for the appeal of Trump and Sanders. The American electorate is frustrated and dissatisfied with their politicians after more than six years of partisan gridlock in Washington. Second, the post-financial crisis economy has improved for many Americans, with nearly every indicator — job quality, satisfaction, unemployment — trending in the right direction. However, the outlook is very uneven depending on geography, education level and socioeconomic status.

Trump and Sanders have effectively tapped into the fear and frustration among the

segments of society which worry most about dwindling economic opportunity. Their anti-status quo and “outsider” message resonate deeply with voters left behind by globalisation.

AW: The US political system seems more divided and partisan than ever. What does that gridlock mean for future US domestic and global policy?MS: In order to understand the partisanship in politics, it is essential to understand the increasing political divide within the general public. Pew Research Center conducted in-depth research on this issue in mid-June, and it showed that Americans are deeply divided on policy, moral and philosophical grounds. Further, Americans are increasingly likely to assign highly negative traits to those who do not share their political views. In sum, political partisanship is as much a reflection of broader social and cultural trends as it is a driver.

If this trend line continues without interruption, the rising partisanship on both the right and left will likely gain ground. Although the extreme ends of the political spectrum have some common concerns, such as corporate subsidies and globalisation, the room for finding compromise will be very narrow — and policy progress will likely be made only on the margins.

However, the US has overcome strong divisions in the past such as the civil rights movement, the Vietnam War and the dynamics has a tendency to ebb and flow, so the recent past is only a limited predictor of future trends. The pull towards extremes may create room for more third-party candidacies or changes

Mona Sutphen

Ahead of the US presidential election, Alan Werlau spoke with Mona Sutphen, former White House Deputy Chief of Staff for Policy, to hear her views on the possible implications of the result.

Ms. Sutphen served as White House Deputy Chief of Staff for Policy in the Obama administration from 2009-2011, working on a range of policy issues including economic, regulatory and international matters. She currently serves on the President’s Intelligence Advisory Board and is a Partner at New York-based Macro Advisory Partners. Ms. Sutphen also spent three years at UBS AG as Managing Director, covering geopolitical and policy risk. She has also previously held positions as an American diplomat and served on the National Security Council during the Clinton administration.

20 Charity Insight Autumn 2016

in the electoral process like California’s open primary system. These shifts, alongside demographic trends, can in turn change political incentives. While most commentators rightly focus on the dysfunction in Washington, the lack of progress nationally has unleashed a wave of public innovation at the state and local level, often on a bipartisan basis.

AW: The state of the US economy has figured large in this election cycle — and not for shorter-term issues, but rather longer-term issues, like the impact of globalisation and trade. What can the next president do to address these issues?MS: The “what next”, in the face of a historically long recovery and lack of counter-cyclical tools, has ultimately led policymakers back to fiscal policy. The fact that both Trump and Clinton showcase major infrastructure investment programmes as the central pillars of their respective economic plans is striking —though not surprising. Public support for such initiatives tends to be high. A recent Gallup poll suggests that approximately 75% of Americans agree that more federal spending is needed to improve infrastructure (though not necessarily about how to pay for it). Further, a major infrastructure programme would accelerate job creation, improve productivity and boost wages in the construction sector. Clinton’s plan contains several elements that would help direct activity to economically distressed areas, such as multimodal transportation, water rehabilitation and highway/rail transport.

Interestingly, both candidates are hostile to the free-trade agenda, but I believe these attitudes will likely extend beyond the political season and may spill over into policy choices, whether in seeking more support for communities negatively impacted by trade (Clinton) or in more

assertive postures in addressing trade disputes (Trump/Clinton).

AW: What do you think the consequences would be of a Trump victory?MS: The policy and political uncertainty that would flow from a Trump victory is difficult to fathom, and would likely roil financial markets and geopolitics until observers have a clearer sense of Trump's policies, preferences and leadership style.

This presidential cycle has been largely substance-free, and the media has found it difficult to pin Trump down on a range of core issues — for example, taxes, immigration, tariffs and US/Russia ties. As a result, very few of the traditional guideposts are evident in this cycle, whether on specific policy issues or even on the question of who sits inside his inner circle beyond his family. It is not at all clear that Trump has the interest or patience needed to manage bureaucratic wrangling in Washington. His non-politician background is an important source of his political support but may ultimately make for choppy and erratic decision making as he tries to navigate the beltway.

AW: What do you see as the single largest challenge (whether domestic or global) for the next administration?MS: Migration. The political, geopolitical and economic consequences of the global migration challenge will be the biggest challenge. While issues like North Korea or cyber-attacks will be difficult to navigate and may lead to conflict, the migration challenge is unique in its ability to animate domestic and global politics simultaneously. There is no other threat that can so quickly destabilise the developing world, upset the politics of Western Europe and North America, foment humanitarian crises, and facilitate cross-border terrorism and crime all at once.

The race for the White House is getting tighter

"The fundamental contours of this presidential cycle remain unchanged: this election is Clinton’s to lose with a 75%+ likelihood of victory."

WARNING: The opinions expressed in this article are the views of the interviewee and do not reflect the views and opinions of Davy.

DAVY | The Interview: The Race to the White House

21Charity Insight Autumn 2016

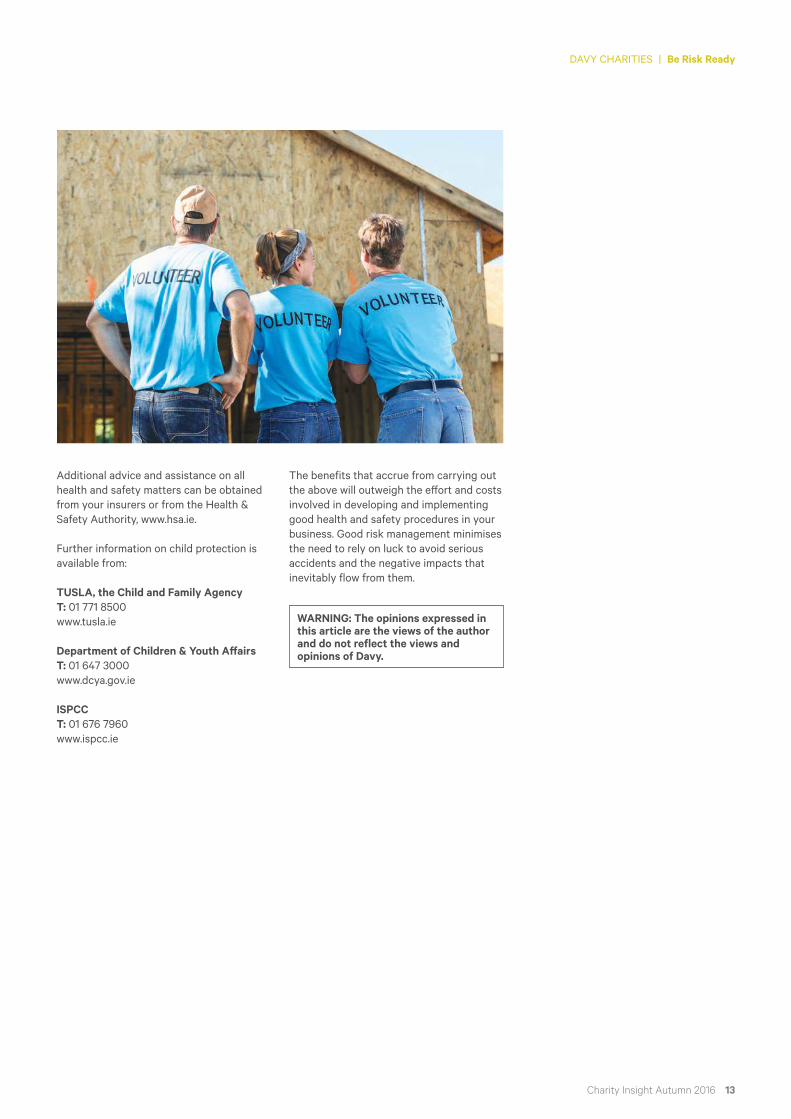

ELECTION 2016 ...what the american people are saying

Donald TRUMP

unfavourable favourable

58% 38%

Hillary CLINTON

unfavourable favourable

55% 42%

ELECTION 2016 ...what the American people are saying

FAVOURABILITY RATINGS TACKLING THE KEY ISSUES

5 KEY POINTS

CLINTON IS FAVOURED TO TACKLE EDUCATION BY A MARGIN OF

26%20%

ECONOMY

5343 50

466135

5640

5245

EDUCATION

TRUMP +10% TRUMP +7% TRUMP +4% CLINTON +26% CLINTON +16%

EMPLOYMENT AND JOBS

TERRORISM AND NATIONAL

SECURITY

HEALTHCARE AND AFFORDABLE

CARE ACT

VOTERS CONSISTENTLY RANK THE ECONOMY AS THEIR TOP CONCERN

WHO THE PUBLIC THINKS IS BEST EQUIPPED

BOTH TRUMP AND CLINTON ARE CONSIDERED UNFAVOURABLE

TRUMP IS THE PREFERRED CANDIDATE ON ISSUES OF ECONOMY, EMPLOYMENT AND NATIONAL SECURITY

IMMIGRATION IS A KEY ISSUE FOR MANY VOTERS

CLINTON PUTS MORE EMPHASIS ON SOCIAL ISSUES SUCH AS EDUCATION AND HEALTHCARE

IDEOLOGICAL DIVIDE WIDENS

DEMOCRATS AND REPUBLICANS ARE MORE IDEOLOGICALLY DIVIDED THAN IN THE PAST

Sour

ce: P

EW R

esea

rch

Cen

ter

Sour

ce: G

allu

p, 1

8-22

May

201

6

Sour

ce: R

ealc

lear

polit

ics,

ave

rage

s 26

/08-

08/0

9/20

16

1994 2004 2014

DEMOCRAT

ConsistentlyLiberal

MEDIAN MEDIAN

ConsistentlyConservative

ConsistentlyLiberal

ConsistentlyConservative

ConsistentlyLiberal

ConsistentlyConservative

REPUBLICAN DEMOCRATMEDIAN MEDIAN

REPUBLICAN DEMOCRATMEDIAN MEDIAN

REPUBLICAN

$

V I S A

PUBLIC TRUST IN THE GOVERNMENT HIT A

RECORD LOWOF LESS THAN

REPUBLICANDEMOCRAT

22 Charity Insight Autumn 2016

ELECTION 2016 ...what the american people are saying

Donald TRUMP

unfavourable favourable

58% 38%

Hillary CLINTON

unfavourable favourable

55% 42%

ELECTION 2016 ...what the American people are saying

FAVOURABILITY RATINGS TACKLING THE KEY ISSUES

5 KEY POINTS

CLINTON IS FAVOURED TO TACKLE EDUCATION BY A MARGIN OF

26%20%

ECONOMY

5343 50

466135

5640

5245

EDUCATION

TRUMP +10% TRUMP +7% TRUMP +4% CLINTON +26% CLINTON +16%

EMPLOYMENT AND JOBS

TERRORISM AND NATIONAL

SECURITY

HEALTHCARE AND AFFORDABLE

CARE ACT

VOTERS CONSISTENTLY RANK THE ECONOMY AS THEIR TOP CONCERN

WHO THE PUBLIC THINKS IS BEST EQUIPPED

BOTH TRUMP AND CLINTON ARE CONSIDERED UNFAVOURABLE

TRUMP IS THE PREFERRED CANDIDATE ON ISSUES OF ECONOMY, EMPLOYMENT AND NATIONAL SECURITY

IMMIGRATION IS A KEY ISSUE FOR MANY VOTERS

CLINTON PUTS MORE EMPHASIS ON SOCIAL ISSUES SUCH AS EDUCATION AND HEALTHCARE

IDEOLOGICAL DIVIDE WIDENS

DEMOCRATS AND REPUBLICANS ARE MORE IDEOLOGICALLY DIVIDED THAN IN THE PAST

Sour

ce: P

EW R

esea

rch

Cen

ter

Sour

ce: G

allu

p, 1

8-22

May

201

6

Sour

ce: R

ealc

lear

polit

ics,

ave

rage

s 26

/08-

08/0

9/20

16

1994 2004 2014

DEMOCRAT

ConsistentlyLiberal

MEDIAN MEDIAN

ConsistentlyConservative

ConsistentlyLiberal

ConsistentlyConservative

ConsistentlyLiberal

ConsistentlyConservative

REPUBLICAN DEMOCRATMEDIAN MEDIAN

REPUBLICAN DEMOCRATMEDIAN MEDIAN

REPUBLICAN

$

V I S A

PUBLIC TRUST IN THE GOVERNMENT HIT A

RECORD LOWOF LESS THAN

REPUBLICANDEMOCRAT

DAVY | US Election: Politics in the Age of Discontent

23Charity Insight Autumn 2016

IN THE NEWS

JAPAN RUNNING OUT OF ARROWSIn the run up to the Bank of Japan’s (BoJ) July meeting, market participants were expecting an increase in the country’s bond purchase programme and potentially the provision of “helicopter money” - direct injection of capital into the real economy. The BoJ approved a fiscal stimulus package of $73 billion for infrastructure spending and cash handouts to low income citizens. This was not the monetary bazooka the market expected. The central bank announced a small increase in the state’s purchases of Exchange Traded Funds (ETFs), maintained its current pace of purchase of other assets - at ¥80 trillion (c.$800 billion)- per annum and held its base rate at -0.1%.

TURKEY'S COUP D’ÉTATOn 15th July a faction of the Turkish armed forces attempted to seize control of several key targets in Istanbul and Ankara in an attempt to overthrow President Erdogan. A curfew, martial law and the preparation of a new constitution were announced. Protesters were shot at and government buildings were fired upon. Over 300 people were killed and 2,100 injured in the clashes. The army faction did not receive public support or wider military backing and so surrendered in the early hours. The government blamed members of the Gülen movement (supporters of Fethullah Gülen, a Turkish cleric based in the United States) and arrested around 6,000 people, including 2,839 soldiers and 2,745 judges. Turkish citizens may have had a feeling of déjà vu as it was not the first time there has been a coup in Turkey. There have been five coup attempts since 1960.

FED DIVIDEDMuch of the market commentary over the last year has centred on the ‘will they, won’t they’ interest rate hike saga in the US. Following the move to raise interest rates by 0.25% in December, the US Federal Reserve (Fed) was expected to raise rates four times during 2016. This has not been the case. Global macroeconomic uncertainty along with some inconsistent or slow-to-improve data points domestically have put the Fed on hold, with just one hike now expected before year end. Fed Chair Janet Yellen has continuously cited slack in the labour market and a lack of productivity growth as reasons for holding off, but with unemployment now below 5% and core inflation approaching target levels, influential Fed members such as Stanley Fischer and William Dudley have stated recently that a rate hike may be justified.

24 Charity Insight Autumn 2016

DAVY | In the News

EUROPE TAKES A BITE

OUT OF APPLEIn August the result of a three-year European Commission (EC) investigation into Apple’s tax arrangement with Ireland was released. The EC ruled that Apple was given an unfair advantage over other companies and thus owes €13 billion in tax to the Irish Revenue. Most commentators expected the ruling to go this way, but no one imagined the tax bill would be so large. Due to the potential negative knock-on effects to foreign direct investment, Ireland and Apple will appeal the ruling. The appeal process could take a number of years. In addition, the EC specifically said that tax authorities from other nations could examine its findings and lay claim to a portion of the €13 billion. Both Apple and Ireland say they are confident of winning the legal battle.

RIO OLYMPICSOver the summer we witnessed one of the most controversial Olympic Games in recent memory. The Brazilian economy is on its knees due to slumping commodity prices and the wide-reaching political scandal that has resulted in President Rousseff being impeached. The large swathes of public money spent on the Olympics and the 2014 FIFA World Cup have understandably annoyed many Brazilians. There is divided opinion over whether the games were a success. Multiple world records were broken, but there were noticeably thousands of empty seats with many stadiums barely half full. The legacy of these games may linger in the minds of the Brazilian public for years to come for all the wrong reasons.

BAD DAY FOR ELON MUSKSeptember started badly for visionary entrepreneur Elon Musk. On day one his personal wealth took a hit to the tune of $779 million. There were two main reasons for this. Firstly, a Space X rocket exploded during a test firing. Thankfully, nobody was injured but it was a sizeable setback for the company which is attempting to make reusable rockets. To add fuel to the fire (pardon the pun), the share price of both Tesla, where he is CEO and chairman, and solar panel manufacturer SolarCity, where he has a considerable shareholding, plummeted. The reason: news of a potential merger between the two led to rumours that he was simply trying to bailout SolarCity which is burning through cash at a rate of knots. Musk has a long history of throwing money at his grand visions and we doubt losing $800 million for a man worth over $11 billion will throw him off course.

25Charity Insight Autumn 2016

Investment Strategy

ASSET CLASS OVERVIEWBoth Clinton and Trump have different ideas about how the economy should be run. Trump wants to roll back on some of Obama’s healthcare reforms; Clinton wants to turn America into a renewable energy superpower. One thing they have in common is that they both want to spend big on Infrastructure. This could not only help kick-start the economy but present good opportunities for investors.

Equities 27

Infrastructure 28

Active versus Passive investing 30

26 Charity Insight Autumn 2016

REPUBLICANS OR DEMOCRATS: WHO IS BETTER FOR THE STOCK MARKET?DAVID COLLINS Investment Strategist

EQUITIES:

There is a perceived ‘wisdom’ among investors that having a Republican in the Oval Office is better for business and ergo stock market returns. But looking back over 72 years since World War II, there is no conclusive evidence that this is the case. In fact the data shows that the opposite is true.

Figure 1 shows that returns for the S&P 500 have been much better when a Democrat has been president. On average, markets have returned 24.2% when a Republican

has been in power compared to 48.2% for a Democrat since 1944.

Take the last two presidencies for example. George W. Bush presided during two of the worst bear markets ever recorded: the bursting of the technology bubble at the turn of the century and the global financial crisis in 2008 at the end of his tenure. Obama’s first term started near the bottom of the fallout following the global financial crisis and stock markets have more than doubled during his tenure.

"...the stock market’s performance is much more complex than who sits in the Oval Office."

DAVY | Asset Class Overview

Figure 1: Is a Democratic president better for the stock market?

S&P 500 average return under Republican and Democratic presidencies; 1944-2016

WARNING: Past performance is not a reliable guide to future performance. The value of investments may go down as well as up. Returns on investments may increase or decrease as a result of currency fluctuations.

So it would seem that the stock market’s performance is much more complex than who sits in the Oval Office. That’s not to say that whoever wins in November will not influence economic policy, and that some industries will be impacted more than others depending on whether Trump or Clinton wins.

Beware Trump’s protectionist agendaTrump’s campaign is full of protectionist promises. His ‘make America great again’ slogan encapsulates his belief that America

should reject the free trade policy it has pursued under previous governments and introduce tariffs to protect American industry. Trump, using a mix of insults and inflammatory rhetoric, has somehow tapped into a deep vein of unhappiness running through white Middle America with his followers even supporting the construction of a wall between the US and Mexico to keep immigrants out.

In theory these policies would help domestic US companies by reducing competition and also freeing up more jobs

PER

CEN

T

0

10

20

30

40

50

60

48.2%

36.2%24.2%

228 301 423

608 531 777

992 1,048

1,337

1,675

1,974

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

50

100

150

200

250

300

350

Jan

2009

A

pr 2

009

Jul 2

009

Oct

200

9 Ja

n 20

10

Apr

201

0 Ju

l 201

0 O

ct 2

010

Jan

2011

A

pr 2

011

Jul 2

011

Oct

201

1 Ja

n 20

12

Apr

201

2 Ju

l 201

2 O

ct 2

012

Jan

2013

A

pr 2

013

Jul 2

013

Oct

201

3 Ja

n 20

14

Apr

201

4 Ju

l 201

4 O

ct 2

014

Jan

2015

A

pr 2

015

Jul 2

015

Val

ue o

f €10

0 in

vest

ed o

n 31

st J

anua

ry 2

00

9

PERC

ENT

ELECTION 2016 POLL OF POLLS

49

47

45

43

41

37

35

31

Jan 2016 Jun 2016 Jul 2016 Aug 2016 Sept 2016

16

17

18

18

20

20

9.0

9

9

9

9

9

61

61

56

54

51

50

10

10

12

11

12

12

4

4

5

7

8

9

0% 10% 20% 30% 40%

ADULT POPULATION BY INCOME TIER (MILLIONS)

50% 60% 70% 80% 90% 100%

1971

1981

1991

2001

2011

2015

Sour

ce: B

loom

berg

AVERAGE - DEMOCRATIC PRESIDENT AVERAGE AVERAGE - REPUBLICAN PRESIDENT

Note: Average returns over 4-year presidential term

27Charity Insight Autumn 2016

THE FOUNDATION OF GROWTHDAVID HILLERY Investment Strategist

INFRASTRUCTURE:

ASSET CLASS OVERVIEW

for Americans. In reality, raising import tariffs would not only raise the prices of those goods, but many other prices too – stopping what little economic growth America has and plunging the country into recession.

Healthcare in Hillary’s sightsLike Obama, healthcare reform is one of the pillars of Hillary Clinton’s agenda. She has promised to crack down on high pricing by drug companies, and has floated the idea of capping the price of prescription drugs. She also favours maintaining (although modifying) the Affordable Care Act, which Trump favours repealing. Clinton’s stance could cause the pharmaceuticals and biotech sector to come under pressure as it has done in the run up to the election.

Different energy policiesClinton has also stated that she wants to turn America into a renewable energy superpower. Any policies to subsidise the likes of solar or wind energy could be negative for coal and fossil fuel companies. Trump, on the other hand, wants to revive the Keystone XL Pipeline, which runs from

Canada to Texas and has been a long standing cause for Republicans in Congress. This would be a substantial boon to energy stocks.

Rebuild AmericaOne area where the candidates agree is America’s need to invest in infrastructure. According to a recent report by the American Society of Civil Engineers (ASCE), the US’s failure to address its infrastructure deficit is set to cost the country trillions of dollars in lost economic output in the coming decades. In its report the ASCE projected $3.32 trillion of infrastructure investment will be needed between 2016 and 2025, and with both candidates in favour of increased spending in this area, a number of sectors stand to benefit.

Congress has already passed a $305 billion highway act and we think more large scale infrastructure projects will be announced in the coming year regardless who wins. Below, Investment Strategist David Hillery, looks at infrastructure as an emerging investment theme both in the US and elsewhere around the world.

"We will no longer surrender this country or its people to the false song of globalism (…) And under my administration; we will never enter America into any agreement that reduces our ability to control our own affairs." Donald Trump during a foreign policy address at the Center for the National Interest, Washington, April 2016

We are about to witness a massive global building boom. After eight years of austerity, governments around the world are beginning to realise that they need to invest in their economies if they are to retain their competitive advantage and build an infrastructure that is fit for the 21st century.