Embed Size (px)

Citation preview

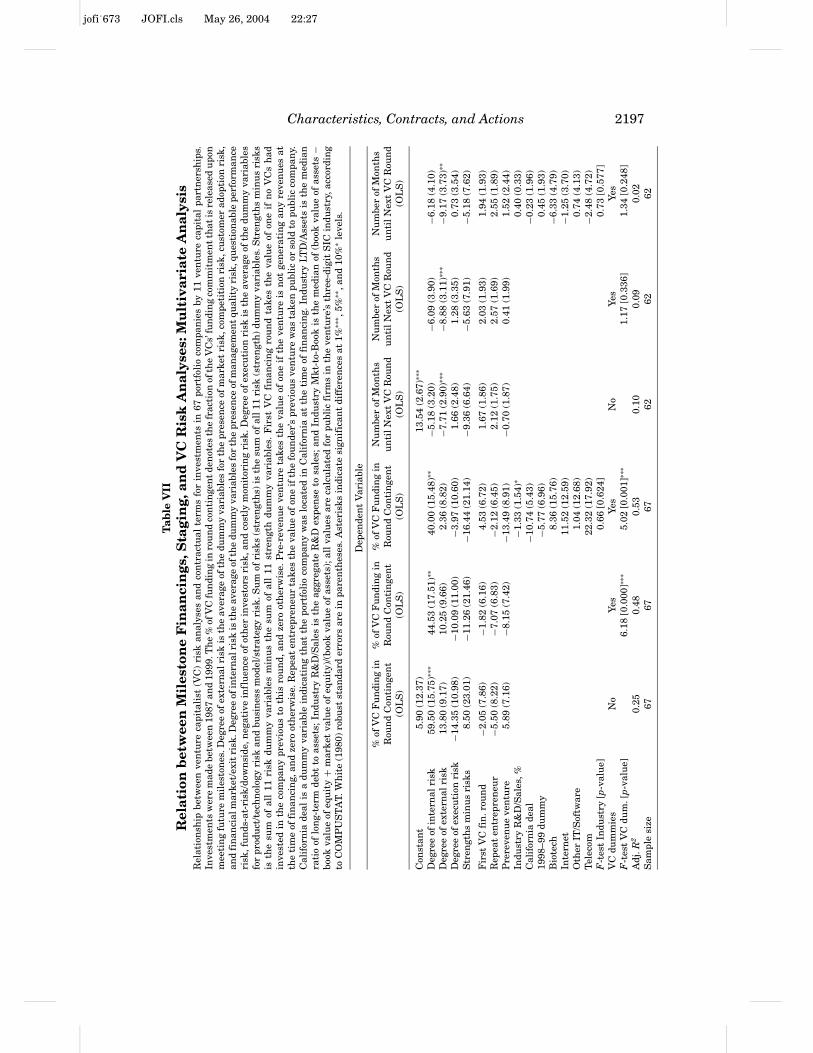

jofi˙673 JOFI.cls May 26, 2004 22:27

THE JOURNAL OF FINANCE • VOL. LIX, NO. 5 • OCTOBER 2004

Characteristics, Contracts, and Actions:Evidence from Venture Capitalist Analyses

STEVEN N. KAPLAN and PER STROMBERG∗

ABSTRACT

We study the investment analyses of 67 portfolio investments by 11 venture capital(VC) firms. VCs describe the strengths and risks of the investments as well as expectedpostinvestment actions. We classify the risks into three categories and relate them tothe allocation of cash flow rights, contingencies, control rights, and liquidation rightsbetween VCs and entrepreneurs. The risk results suggest that agency and hold-upproblems are important to contract design and monitoring, but that risk sharing isnot. Greater VC control is associated with increased management intervention, whilegreater VC equity incentives are associated with increased value-added support.

MOST FINANCIAL CONTRACTING THEORIES ADDRESS how conflicts between a principal/investor and an agent/entrepreneur affect ex ante information collection, con-tract design, and ex post monitoring. In this paper, we empirically test thepredictions of financial contracting theories using investments by venture cap-italists (VCs) in early stage entrepreneurs—real world entities that arguablyclosely approximate the principals and agents of theory.1

VCs face four generic (agency) problems in the investment process. First, theVC is concerned that the entrepreneur will not work hard to maximize valueafter the investment is made. In such a case, when the entrepreneur’s effort isunobservable to the VC, the traditional moral hazard approach, pioneered byHolmstrom (1979), predicts that the VC will make the entrepreneur’s compen-sation dependent on performance. The more severe the information problem,the more the contracts should be tied to performance.

∗University of Chicago Graduate School of Business and National Bureau of Economic Research.A previous version of this paper was titled “How Do Venture Capitalists Choose and Monitor Invest-ments?” We appreciate comments from Ulf Axelson, Douglas Baird, Francesca Cornelli, MathiasDewatripont, Douglas Diamond, Paul Gompers, Felda Hardymon, Josh Lerner; Frederic Martel,Bob McDonald (the editor), Kjell Nyborg, David Scharfstein, Jean Tirole, Lucy White, Luigi Zin-gales, an anonymous referee, and seminar participants at Amsterdam, Chicago, Columbia, ECARE,the 2001 European Finance Association meetings, Harvard Business School, HEC, INSEAD,London Business School, McGill, Michigan, New York University, North Carolina, Notre Dame,Ohio State, Purdue, Rochester, Stockholm School of Economics, Toulouse, Washington University,and Yale. This research has been supported by the Kauffman Foundation, by the Lynde and HarryBradley Foundation, and the Olin Foundation through grants to the Center for the Study of theEconomy and the State, and by the Center for Research in Security Prices. Alejandro Hajdenbergprovided outstanding research assistance. We are grateful to the venture capital partnerships forproviding data. Any errors are our own.

1 Hart (2001) concurs that this is a reasonable assumption.

2173

jofi˙673 JOFI.cls May 26, 2004 22:27

2174 The Journal of Finance

Second, the VC may also be concerned that the entrepreneur knows moreabout his or her quality/ability than the VC. The model in Lazear (1986) shows Q1that the VC can design contracts with greater pay-for-performance that goodentrepreneurs will be more willing to accept.2 Ross (1977) and Diamond (1991)show that investor liquidation rights—the ability to liquidate and the payoff inthe event of liquidation—can also be used to screen for good entrepreneurs.

Third, the VC also understands that after the investment, there will be cir-cumstances when the VC disagrees with the entrepreneur and the VC will wantthe right to make decisions. Control theories (such as Aghion and Bolton (1992)and Dessein (2002)) show that a solution to this problem is to give control tothe VC in some states and to the entrepreneur in others.

Fourth and finally, the VC is concerned that the entrepreneur can “hold-up”the VC by threatening to leave the venture when the entrepreneur’s humancapital is particularly valuable to the company. This is the hold-up problemanalyzed in Hart and Moore (1994). The VC can reduce the entrepreneur’sincentive to leave by vesting the entrepreneur’s shares.

The theories predict that characteristics of VC contracts will be related tothe extent of agency problems. As such problems increase, founder compensa-tion will be more performance sensitive, VCs will have stronger control andliquidation rights, and vesting will be more pronounced.

Most previous research, including our own, estimates the extent of agencyproblems using indirect measures, e.g., firm age, firm size, industry R&D inten-sity, and industry market-to-book ratio.3 These measures have two limitations.First, they may not measure the risks the VCs actually care about. Second, theymix different risks together when such risks may have different implicationsfor agency problems and therefore for the VC contracts and actions.

In this paper, we construct direct measures of risks and uncertainties thatVCs and entrepreneurs face, and then classify those risks depending on howthey relate to specific agency problems. We obtain these measures by readingand assessing the investment memoranda for investments in 67 companies by11 VC partnerships. We then consider whether the agency problems affect theVC contracts and actions in the ways predicted by the theories.

Most agency problems are directly related to asymmetric information, i.e.,uncertainties about which the entrepreneur is better informed than the VC.For example, agency problems will be more severe when the entrepreneur’sability is unknown because of inexperience, when the operations of the ventureare hard to observe and monitor, and when the entrepreneur has more discre-tion in actions and in the use of funds. We denote such types of uncertaintiesas internal risks. When internal risks are larger, moral hazard problems, ad-verse selection risks, and the likelihood of future conflicts of interest will alsobe larger. As a result, the theories predict that performance-sensitive and con-tingent compensation should be more pronounced, the VC should get control in

2 Hagerty and Siegel (1988) point out that the solution to the screening problem is observationallysimilar to that for the moral hazard problem.

3 Smith and Watts (1992), Gompers (1995), and Kaplan and Stromberg (2003), e.g., all use suchindirect measures.

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2175

more states of the world, and the VC should have greater ability to liquidatethe venture upon poor performance.

VCs and founders also face risks that are equally uncertain for both parties.Examples are the extent of future demand for an undeveloped product, theresponse of competitors upon the product’s introduction, and the receptivity offinancial markets when investors try to sell the company or bring it public. Wedenote such uncertainties as external risks.

Unlike the clear predictions for internal risks, financial contracting theorieshave ambiguous predictions with respect to external risks. According to tra-ditional moral hazard theories like Holmstrom (1979), when risks—such asexternal risks—are not under the entrepreneur’s control, pay-for-performancecompensation and other contingent payoffs are less desirable because a risk-averse entrepreneur has to be compensated for taking on such risks.

Alternatively, in a world of incomplete contracting, external uncertaintiesmay increase the likelihood of unforeseen contingencies and the concomitantVC-entrepreneur conflicts. Theories such as Aghion and Bolton (1992) implythat the VC will get control in more states of the world. It also is plausible thatexternal uncertainty makes direct monitoring more difficult. For this reason,Prendergast (2002) predicts that pay-for-performance compensation should in-crease with external uncertainty, and Dessein (2002) implies that VC controlshould increase.

Finally, some uncertainties are neither solely internal (because they areequally uncertain for the VC and the entrepreneur), nor solely external (be-cause they are at least partly under the entrepreneur’s control). The VC maybe happy with the quality and work of the management team, and all partiesmay agree that there will be a great market for the product once developed,but it may be very difficult to make the technology or the strategy work. Wedenote such uncertainties, which are related to the venture’s complexity andthe importance of the entrepreneur’s human capital, as difficulty of executionrisks. The hold-up problem of Hart and Moore (1994) is likely to be greater insuch cases because the entrepreneur can credibly threaten to leave. As a result,we would expect to see greater use of vesting provisions in such ventures.4

In our empirical analysis, we first describe the strengths and risks of theinvestments as well as expected postinvestment monitoring. We then form em-pirical measures of the three different types of risks and relate those measuresto the contracts.

Consistent with the agency explanation, internal uncertainty is significantlyrelated to many of the incentive and control mechanisms in the contracts.Higher internal risk is associated with more VC control, more contingent

4 Another possibility is that for such complex ventures, it is difficult to find proper benchmarksor signals on which to base contingent compensation. Execution risks are likely to be present inventures where the tasks that the entrepreneur has to perform are very complex and multidimen-sional. Basing compensation on a signal correlated with a particular aspect of the task may lead theentrepreneur to put too much effort on this aspect, as opposed to other areas. Multitasking theoriessuch as Holmstrom and Milgrom (1991) and Baker (1992) predict that contingent compensationbased on performance benchmarks will be used less in these cases.

jofi˙673 JOFI.cls May 26, 2004 22:27

2176 The Journal of Finance

compensation for the entrepreneur, and more contingent financing in a givenround. The exceptions are that the overall fraction of founder cash flow rightsand some VC liquidation rights are not related to internal risk.

Similar to internal risks, external risk is associated with more VC controland more contingent compensation. External risk is also associated with in-creases in the strength of VC liquidation rights, and tighter staging, in thesense of a shorter period between financing rounds. These findings are highlyinconsistent with optimal risk-sharing between risk-averse entrepreneurs andrisk-neutral investors. In contrast, the results are supportive of the argumentsin Prendergast (2002) and Dessein (2002).

Risk related to difficulty of execution shows a (weakly) negative relation withmany contractual terms such as contingent compensation and VC liquidationrights. These results suggest that for highly complex environments, where thefounder’s human capital is particularly important, standard incentive mecha-nisms are less effective. Furthermore, consistent with hold-up theories, execu-tion risk is positively related to founder vesting provisions.

Next, we test two additional theoretical predictions by relating the financialcontracts to VC actions. First, control theories like Aghion and Bolton (1992)imply that intervening actions are more likely when the VC has greater controlrights. Second, the “double sided moral hazard” theories like Casamatta (2003)emphasize that VCs also provide value-added support activities. Since both theVC and the entrepreneur benefit from value-added services, these activities areless likely to be resisted by the entrepreneur. Rather, the problem is to providethe VC incentives to undertake supporting actions. These theories suggest thatsupporting actions will be more likely as the VC’s equity stake in the companyincreases.5

We use the investment analyses to measure actions that the VCs took beforeinvesting and expected to undertake afterward. We then classify these actionsinto intervening and supporting ones. In at least half of the investments, theVC expected to play a role in recruiting management or some other interveningaction that the entrepreneur is likely to view as a conflict. Consistent withthe control theories, VCs are more likely to intervene as VC control increases.Second, in more than one-third of the investments, the VC expects to providevalue-added services such as strategic advice or customer introductions. Aspredicted, we find that VC’s value-added services increase with the VC’s equitystake, but are not related to VC control.

Overall, we believe this paper makes three contributions. First, the paperis novel in using investors’ direct assessments of risks rather than the indi-rect proxies used in most previous research. The internal risk results suggestthat agency problems are very important to contract design. The external riskresults suggest that risk-sharing concerns are unimportant relative to otherconcerns such as monitoring. Second, we show that VCs expect to take actionswith their investments and those actions are related to the contracts. Expected

5 We are able to measure these effects separately because control rights in VC contracts areseparate and distinct from cash flow rights. See Kaplan and Stromberg (2003).

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2177

VC intervention is related to VC board control, while VC support or advice isrelated to VC equity ownership. Finally, the paper adds to existing work bydescribing the characteristics and risks that VCs consider in actual deals. Ourresults are consistent with those in MacMillan, Siegel and Subbanarasimha(1985) and MacMillan, Zemann, and Subbanarasimha (1987) who rely largelyon survey evidence.

The paper proceeds as follows. Section I describes our sample. Section IIdescribes the VC analyses. Section III presents the relation between the con-tracts and the VC analyses. Section IV considers the relation between VC ac-tions and the contracts. Section V summarizes our results and discusses theirimplications.

I. Sample

A. Description

We analyze VC investments in 67 companies by 11 VC firms. This is a subsam-ple of the 119 companies from 14 VC firms analyzed in Kaplan and Stromberg(2003), who obtained their sample by asking the VCs to provide detailed infor-mation on their investments. For each company and for each financing roundfor the company, the VC was asked to provide the (1) term sheet; (2) stock andsecurity purchase agreements; (3) the company’s business plan; and (4) the VC’sinternal analysis of the investment.

Most VC firms have a process in which the partner responsible for a potentialinvestment writes up an analysis or memorandum for that investment. Theentire partnership group uses the analysis to help decide whether to make theinvestment. If the VC invests in the company, the memorandum then serves asa guide for postinvestment actions.

VCs at 11 of the 14 VC firms provided an investment analysis for at least onecompany investment. The analyses vary in detail. Some are brief, two-page,write-ups while others are in-depth descriptions exceeding twenty pages. Aconsequence of this is that our results may understate the extent of analysesthat the VCs perform.

Table I presents sample summary information. We study the first investmentmade by the VC in these companies. Panel A indicates that of the 67 invest-ments, 25 are prerevenue—the firms either did not have revenues or were notyet operating. We refer to these as early stage rounds. The remaining invest-ments are rounds in which the firms had revenues and were already operating.For 44 companies, the investment is the first investment any VC ever madein the company; in the remaining 23, another VC had invested before our VCacquired a stake.

Panel B shows that the sample investments were relatively recent when col-lected. All but 11 of the 67 companies were initially funded by the VCs between1996 and 1999.

Panel C indicates that the companies represent a wide range of industries.The largest group is in information technology and software (24 companies),

jofi˙673 JOFI.cls May 26, 2004 22:27

2178 The Journal of Finance

Tab

leI

Su

mm

ary

Info

rmat

ion

Su

mm

ary

info

rmat

ion

for

inve

stm

ents

in67

port

foli

oco

mpa

nie

sby

11ve

ntu

reca

pita

lpar

tner

ship

s.In

vest

men

tsw

ere

mad

ebe

twee

n19

87an

d19

99.P

rere

ven

ue

stag

ero

un

dsar

efi

nan

cin

gro

un

dsfo

rco

mpa

nie

sth

ath

adn

ore

ven

ues

befo

reth

efi

nan

cin

g.F

irst

VC

inve

stm

ents

refe

rto

obse

rvat

ion

sw

her

ew

eh

ave

the

inve

stm

entm

emor

andu

mfo

rth

efi

rstt

ime

any

ven

ture

capi

talf

un

din

vest

edin

the

com

pan

y.R

epea

ten

trep

ren

eur

refe

rsto

obse

rvat

ion

sw

her

e,be

fore

fou

ndi

ng

this

part

icu

lar

port

foli

oco

mpa

ny,

the

fou

nde

rh

adsu

cces

sfu

lly

gon

epu

blic

wit

ha

prev

iou

sve

ntu

reor

sold

such

ave

ntu

reto

apu

blic

com

pan

y.T

otal

fin

anci

ng

com

mit

ted

isth

eto

tala

mou

nto

fequ

ity

fin

anci

ng

com

mit

ted

toby

the

ven

ture

capi

tali

sts

atth

eti

me

ofth

efi

nan

cin

gro

un

d.V

Cfi

rmlo

cati

onin

clu

des

Cal

ifor

nia

(CA

),M

idw

este

rnU

nit

edS

tate

s(M

W),

Nor

thea

ster

nU

nit

edS

tate

s(N

E),

and

dive

rse

loca

tion

s(D

IV).

Dat

aon

capi

talm

anag

edan

dfu

nds

rais

edby

VC

firm

sco

me

from

Ven

ture

Eco

nom

ics.

A.

NN

um

ber

ofpo

rtfo

lio

com

pan

ies

67P

rere

ven

ue

25F

irst

VC

inve

stm

ents

44R

epea

ten

trep

ren

eur

14M

emo

wri

tten

byle

adin

vest

or57

Loc

ated

inC

alif

orn

ia25

Loc

ated

inN

orth

-Eas

tU

nit

edS

tate

s13

Loc

ated

inM

idw

est

11

B.B

yye

arin

itia

lro

un

dfi

nan

ced

:P

re-1

995

1996

1997

1998

1999

#co

mpa

nie

s11

1412

291

C.B

yin

du

stry

Bio

tech

Inte

rnet

IT/S

oftw

,Oth

erT

elec

omH

ealt

hca

reR

etai

lO

ther

Inds

.#

com

pan

ies

714

1010

1010

6

D.B

yV

Cfi

rm1

23

45

67

89

1011

#po

rtfo

lio

com

pan

ies

incu

rren

tdr

aft

73

315

44

210

210

7L

ocat

ion

CA

MW

NE

MW

CA

MW

CA

DIV

MW

DIV

DIV

Ran

kin

term

sof

capi

talm

anag

ed20

02,<

=to

p50

100

2515

015

050

550

2525

025

100

E.V

Cfi

rmch

arac

teri

stic

s:M

ean

Med

ian

By

fin

anci

ng

rou

nd

(N=

67):

VC

firm

age

atti

me

offi

nan

cin

gro

un

d,ye

ars

13.3

12.0

Nu

mbe

rof

fun

dsra

ised

byfi

rmsi

nce

fou

nda

tion

5.9

5.0

Am

oun

tra

ised

bypa

rtn

ersh

ipsi

nce

fou

nda

tion

($m

illi

ons)

448.

928

9.7

By

VC

firm

(N=

11):

VC

firm

age,

Nov

embe

r20

0216

.715

.0N

um

ber

offu

nds

rais

edby

Nov

embe

r20

0211

.28.

5C

apit

alu

nde

rm

anag

emen

t,N

ovem

ber

2002

($m

illi

ons)

1747

.284

6.7

F.F

inan

cin

gA

mou

nts

Mea

nM

edia

nT

otal

fin

anci

ng

com

mit

ted

($m

illi

ons)

9.7

6.0

Tot

alfi

nan

cin

gpr

ovid

ed($

mil

lion

s)5.

54.

8G

.Ou

tcom

esas

of10

/31/

02P

riva

teP

ubl

icS

old

Liq

uid

ated

#of

com

pan

ies

2315

1613

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2179

with 14 internet-related and 10 noninternet related. The sample also includesbiotech, telecom, healthcare, and retail ventures.

Panel D shows that the portfolio companies were funded by 11 U.S.-basedVC firms with no more than 15 companies from any one VC. Three VCs arebased in California, four in the Midwest, one in the Northeast, and three havemultiple offices. Five VCs are among the top 50 VC firms in the United Statesin capital under management; all but two are among the top 150.

Panel E shows that at the time of financing, the VC for the median investmentin our sample was 12 years old and had raised five funds amounting to $290million.

Panel F reports the financing amounts. The VCs committed a median of$6.0 million with a median of $4.8 million disbursed at closing and the restcontingent on milestones.

Finally, panel G indicates that by October 31, 2002, 15 of the 67 companieswere public, 16 had been sold, and 13 had been liquidated. The remaining 23companies were still private.

B. Sample Selection Issues

In this section, we discuss potential selection issues. The sample is not ran-dom in that we obtained the data from VC firms with whom we have a rela-tionship.

One possible bias is that the three VCs from our previous paper that did notprovide investment memoranda are different from the others. While possible,the terms and the outcomes of the investments made by those VCs appearsimilar to those for the investments made by the other 11 VCs.

It is also possible that the VCs provided us with memos on their better invest-ments. Several factors suggest that this is not the case. Many of the investmentsthe VCs provided us were their most recent. In addition, 6 of the 11 VCs pro-vided all of their investments in the relevant period. The terms for the six VCsare similar to those for the entire sample. Finally, investments with memos areinsignificantly less likely to have gone public than those without memos.

Another possible bias is that memoranda are written only for more contro-versial investments. The results in the previous paragraph argue against this.Furthermore, four of the six VCs who gave us all their investments gave usmemoranda for all of them.

There do not appear to be industry or geographic biases as the industries andlocations of the sample companies are in line with those of all VC investmentsover the same period.

Finally, because we contacted successful VCs, it is possible that our VCsare of above-average ability. We do not think this bias is of much concern forour analyses because we are interested in understanding how VCs choose andstructure their investments rather than how well they perform. If anything,a bias towards more successful VCs would be helpful because we are morelikely to have identified the methods used by sophisticated, value-maximizingprincipals.

jofi˙673 JOFI.cls May 26, 2004 22:27

2180 The Journal of Finance

Overall, we acknowledge that the sample is selected, and it is difficult toknow the extent of any bias. We have discussed the more likely biases and havenot found any obvious red flags.

II. Description of VC Investment Analyses

In this section, we present our classification scheme for investment strengthsand risks, describe those strengths and risks, and describe the actions the VCstake and expect to take.

A. Classification Scheme

Previous work on VC company characteristics distinguishes among factorsthat relate to the opportunity (the company’s market, product/service, technol-ogy, strategy, and competition), the management team, the deal terms, and thefinancing environment.6 We include these factors, but group them into threecategories motivated by the theories described in the introduction.

The first category includes internal factors—management quality, perfor-mance to date, downside risk, influence of other investors, VC investment fitand monitoring costs, and valuation. These factors are related to managementactions and/or the quality of the management team. We believe these factorsare more likely to be subject to asymmetric information and moral hazard withrespect to the management team.

The second category includes those factors we view as external to the firm.We classify market size, customer adoption, competition, and exit conditionrisks as such factors. Because these are external to the firm and largely beyondthe control of the management team, we believe that the VC and the foundershould be more or less equally informed about these factors.

The third category measures factors related to difficulty of execution orimplementation—product/technology and business strategy/model. These fac-tors are designed to capture the complexity of the task and the reliance on theentrepreneur’s human capital.

We recognize that there are alternative interpretations of our categories. Wepostpone a discussion of these alternatives until later when we present ourresults.

Table II summarizes the classifications, investment theses, and risks.

B. Investment Strengths/Theses

Panel A confirms that internal factors are important. The VCs cite manage-ment quality as a reason for investing in almost 60% of the investments. The

6 MacMillan et al. (1987, 1987, 1988); Sapienza (1992); and Sapienza et al. (1996) rely largelyon survey evidence to obtain these results.

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2181

Tab

leII

Inve

stm

ent

Th

eses

and

Ris

ks

inV

entu

reC

apit

alis

tA

nal

yses

Exp

lici

tly

men

tion

ed(1

)re

ason

sfo

rin

vest

ing

and

(2)

risk

sof

inve

stm

ent,

acco

rdin

gto

ven

ture

capi

tali

stan

alys

esfo

rin

vest

men

tsin

67po

rtfo

lio

com

pan

ies

by11

ven

ture

capi

talp

artn

ersh

ips.

Inve

stm

ents

wer

em

ade

betw

een

1987

and

1999

.

Rea

son

toIn

vest

/Str

engt

hR

isk

ofIn

vest

men

t/W

eakn

ess

N%

Exa

mpl

esN

%E

xam

ples

A.I

nte

rnal

Fact

ors:

Man

agem

ent,

Pre

viou

sP

erfo

rman

ce,F

un

dsat

Ris

k,O

ther

Inve

stor

s

Qu

alit

yof

man

agem

ent

4059

.7•

Man

agem

ent

team

has

exte

nsi

vein

tern

etan

dw

ebsi

tem

anag

emen

tex

peri

ence

.•

Man

agem

ent

team

isbe

liev

edto

bego

odin

scie

nce

,an

dat

rais

ing

and

con

serv

ing

mon

ey.

•E

xper

ien

ced

man

ager

sou

tof

succ

essf

ulv

entu

reba

cked

com

pan

y.•

Hig

hly

sou

ght-

afte

ren

trep

ren

eur/

fou

nde

r,w

ho

co-f

oun

ded

com

pan

yth

atw

ent

publ

ic.

•E

xper

ien

ced,

prov

enan

dh

igh

-pro

file

CE

O.

•F

oun

der

has

hig

hm

arks

from

exis

tin

gin

vest

ors

•K

now

nC

EO

for

alo

ng

tim

e.•

Tea

mh

asac

quir

edsi

gnif

ican

tle

velo

fpen

etra

tion

and

rela

tion

ship

sin

afa

irly

shor

tti

me.

•C

EO

/fou

nde

ris

capa

ble

ofat

trac

tin

gn

eces

sary

empl

oyee

s.H

asde

velo

ped

exce

llen

tpr

odu

ctw

hil

eco

nsu

min

gm

odes

tam

oun

tsof

capi

tal.

•C

EO

isve

ryfr

uga

lan

dw

illn

otsp

end

un

wis

ely.

•F

oun

der

very

com

mit

ted:

quit

job

atco

mpe

tito

ran

dm

ortg

aged

his

hou

se.

•T

eam

isw

ell-

bala

nce

d,yo

un

gan

dag

gres

sive

.

4161

.2•

CE

Ois

a“r

ath

erdi

ffic

ult

pers

on.”

Act

ive

invo

lvem

ent

ofch

airm

anw

illb

ecr

uci

al.

•C

EO

/fou

nde

rh

asa

stro

ng

desi

refo

rac

quis

itio

ns.

VC

sh

ave

tode

vote

subs

tan

tial

tim

eev

alu

ate.

•M

anag

emen

th

asn

otsh

own

inth

epa

stth

atit

can

effe

ctiv

ely

fore

cast

fin

anci

alpr

ogre

ss.

•C

ompa

ny

isin

man

yse

emin

gly

disp

arat

ebu

sin

esse

s;a

refl

ecti

onof

man

agem

ent’s

lack

offo

cus?

•W

illm

anag

emen

tbe

able

toin

tegr

ate

acqu

isit

ion

s?•

Th

eC

EO

’sch

oice

ofpa

stco

mpa

nie

squ

esti

onab

le.

•M

anag

emen

tis

you

ng

and

rela

tive

lyin

expe

rien

ced.

•M

anag

emen

tte

amis

inco

mpl

ete.

•C

ompa

ny

ish

igh

lyre

lian

ton

one

indi

vidu

al(t

he

CE

O).

•C

ompa

ny

nee

dsC

EO

,CF

O,C

OO

,an

dco

ntr

ol(o

pera

tin

g,re

port

ing,

and

bill

ing)

syst

ems.

•N

eed

seas

oned

indu

stry

exec

uti

ve.

•In

com

plet

em

anag

emen

tte

am.A

mil

esto

ne

for

furt

her

fun

din

gis

hir

ing

VP

ofsa

les

and

mar

keti

ng.

•M

ust

stre

ngt

hen

man

agem

ent

and

ensu

rein

volv

emen

tof

VC

asch

airm

an.W

illh

ave

toh

ire

CE

O.

jofi˙673 JOFI.cls May 26, 2004 22:27

2182 The Journal of Finance

Tab

leII

—C

onti

nu

ed

Rea

son

toIn

vest

/Str

engt

hR

isk

ofIn

vest

men

t/W

eakn

ess

N%

Exa

mpl

esN

%E

xam

ples

Per

form

ance

toda

te18

26.9

•D

emon

stra

ted

prof

itab

ilit

yof

busi

nes

sm

odel

.•

Com

pan

yh

asa

man

agea

ble

cash

burn

rate

and

isex

pect

edto

beca

sh-f

low

brea

k-ev

enin

12m

onth

s.•

Sig

nif

ican

tsa

les

grow

than

dm

omen

tum

.•

Has

deve

lope

dpr

odu

ct,w

ell-

posi

tion

edto

ach

ieve

reve

nu

eta

rget

.

57.

5•

Com

pan

yis

mak

ing

loss

esan

dpe

rfor

min

gbe

low

plan

.•

Bad

debt

prob

lem

,wh

ich

sign

ific

antl

ych

ange

dth

epr

ofit

abil

ity

ofth

eco

mpa

ny,

beca

use

ofpa

stbu

sin

ess

proc

edu

res.

Fu

nds

atri

sk/

dow

nsi

de13

19.4

•P

arti

cipa

tin

gpr

efer

red

prot

ects

VC

ifm

edio

cre

perf

orm

ance

.•

Equ

ipm

ent

can

befu

nde

dw

ith

debt

.•

Inve

stor

sh

ave

abil

ity

toco

ntr

olgr

owth

.•

Min

imiz

edo

wn

side

byon

lypr

ovid

ing

lim

ited

fun

dsu

nti

lmil

esto

nes

met

.•

VC

com

mit

men

tw

illb

ein

vest

edov

erti

me.

•C

ash

-eff

icie

nt

earl

yst

age

than

ksto

futu

reco

mpa

ny

acqu

isit

ion

sw

ith

stoc

k.•

Can

take

com

pan

yto

lead

ing

indu

stry

posi

tion

wit

ha

min

imu

mof

capi

tal.

913

.4•

Un

cert

ain

tyab

out

wh

atpr

oper

mil

esto

nes

shou

ldbe

.•

Lar

geam

oun

tof

capi

talf

ora

star

t-u

pen

terp

rise

.W

illr

equ

ire

stro

ng

man

agem

ent

over

sigh

t.•

Agg

ress

ive

ban

klo

anas

sum

ptio

ns.

Mig

ht

requ

ire

eith

ersl

ower

expa

nsi

onor

mor

eeq

uit

yca

pita

l.•

Com

pan

yh

asli

ttle

inth

ew

ayof

un

derl

yin

gas

set

valu

ean

dth

us

offe

rsli

mit

eddo

wn

side

prot

ecti

on.

•C

ompa

ny

expe

cts

ton

eed

addi

tion

alfi

nan

cin

gn

ext

year

.No

asse

tsof

valu

eex

cept

for

empl

oyee

s.•

Nee

dsu

ffic

ien

tch

ecks

and

bala

nce

sre

gard

ing

draw

dow

nof

fun

ds.

Infl

uen

ceof

oth

erin

vest

ors

46.

0•

Inve

stin

gpa

rtn

ers

incl

ude

inve

stor

sw

ho

prev

iou

sly

inve

sted

earl

yin

som

eex

trem

ely

succ

essf

ulc

ompa

nie

s.•

Co-

inve

stor

also

invo

lved

asac

tive

chai

rman

and

inte

rim

CE

O.

46.

0•

Lea

dV

Cw

illn

oth

ave

un

ilat

eral

con

trol

,bu

th

ave

tore

ach

agre

emen

tw

ith

thre

eot

her

VC

s.•

Pre

viou

sin

vest

or(w

ho

isse

llin

gal

lsh

ares

toV

Cs)

isan

xiou

sto

get

out

ata

deep

disc

oun

t.•

Oth

erV

Cpr

evio

usl

yde

cide

dn

otto

fin

ance

deal

.V

Cpo

rtfo

lio

fit

and

mon

itor

ing

cost

1217

.9•

Add

sad

diti

onal

brea

dth

toV

Cpo

rtfo

lio

wit

hin

this

mar

ket

segm

ent.

•V

Cis

stro

ng

inth

isge

ogra

phic

regi

on.

•G

ood

stra

tegi

cfi

tw

ith

VC

.•

VC

has

boar

dse

aton

com

pan

yin

com

plem

enta

rybu

sin

ess;

mar

keti

ng

part

ner

ship

poss

ible

.

1014

.9•

Com

plic

ated

lega

lan

dfi

nan

cial

due

dili

gen

cen

eede

d.•

May

requ

ire

too

mu

chti

me

from

VC

.•

Geo

grap

hic

alri

sk—

US

corp

orat

ean

dov

erse

asR

&D

.•

VC

sh

ave

tode

vote

subs

tan

tial

tim

eto

eval

uat

eac

quis

itio

ns.

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2183

•N

ewm

arke

tse

gmen

tfo

rV

C,w

hic

hsh

ould

stim

ula

teso

me

addi

tion

alop

port

un

itie

s.•

Pot

enti

alfo

r(N

on-C

alif

orn

ia)

VC

tole

ada

Sil

icon

Val

ley

deal

.

•H

eavy

invo

lvem

ent

ofin

vest

oras

inte

rim

CE

O,

(rep

laci

ng

fou

nde

r)is

crit

ical

tosu

cces

s.•

Hav

eto

ensu

reac

tive

invo

lvem

ent

ofon

eof

VC

inve

stor

sas

chai

rman

.V

alu

atio

n14

20.9

•L

owva

luat

ion

:IR

Rof

46%

inco

nse

rvat

ive

case

.•

Exi

tm

ult

iple

sar

esh

ooti

ng

up.

1319

.4•

Are

the

valu

atio

nan

dfi

nan

cial

proj

ecti

ons

real

isti

c?•

Hig

hva

luat

ion

beca

use

ofco

mpe

titi

onbe

twee

nV

Cs.

B.E

xter

nal

Fact

ors:

Mar

ket

Siz

e,C

ompe

titi

on,C

ust

omer

s,F

inan

cial

Mar

kets

,an

dE

xit

Con

diti

ons.

Mar

ket

size

and

grow

th46

68.7

%•

Lar

gem

arke

tam

enab

leto

rapi

dgr

owth

.•

Ver

yla

rge

mar

ket

inw

hic

hin

cum

ben

tsea

rnh

igh

prof

itm

argi

ns.

•C

ompa

ny

cou

lddr

amat

ical

lyim

pact

the

evol

uti

onof

the

com

pute

rin

dust

ry.

2131

.3%

•R

egu

lato

ryu

nce

rtai

nty

.•

Cou

ntr

yri

sk.

•C

urr

ency

risk

.•

New

,lar

gely

un

prov

en,m

arke

tpla

ce.

•G

ener

aldo

wn

turn

inin

dust

ry.

Com

peti

tion

and

barr

iers

toen

try

2232

.8%

•S

tron

gpr

opri

etar

yan

dpa

ten

tpo

siti

on.

•C

ompa

ny

ista

rget

ing

asi

gnif

ican

tm

arke

tse

gmen

tth

atis

un

ders

erve

dby

incu

mbe

nts

.•

Ear

lym

over

adva

nta

ges

from

bein

gpi

onee

rof

con

cept

and

larg

est

play

er.

•H

igh

lyfr

agm

ente

din

dust

ry,w

hic

hm

akes

itri

pefo

rco

nso

lida

tion

.•

No

com

peti

tors

.•

Th

ere

ism

ore

than

enou

ghro

omfo

rse

vera

lco

mpe

tito

rs.

2740

.3%

•C

ust

omer

sm

igh

tbe

com

eco

mpe

tito

rson

ceth

eyle

arn

com

pan

y’s

busi

nes

sm

odel

•P

aten

tpr

otec

tion

alon

em

igh

tn

otpr

ovid

een

ough

barr

iers

toen

try.

•M

any

new

entr

ants

-pri

ceco

mpe

titi

onco

uld

driv

edo

wn

mar

gin

s.•

Com

peti

tive

and

tigh

tla

bor

mar

ket,

com

peti

ng

wit

hla

rger

esta

blis

hed

firm

sfo

rem

ploy

ees.

•N

ewte

chn

olog

ym

igh

tbe

lon

g-te

rmth

reat

.•

Low

barr

iers

toen

try.

Low

swit

chin

gco

sts.

•P

rodu

ctca

nbe

copi

edby

larg

een

tren

ched

firm

s.L

ikel

ihoo

dof

cust

omer

adop

tion

2029

.9%

•C

once

ptu

alac

cept

ance

bypr

ofes

sion

alco

mm

un

ity.

•B

eta

arra

nge

men

tsw

ith

larg

ecu

stom

ers.

•S

olid

base

ofcu

stom

ers.

•C

ust

omer

sar

epo

siti

vere

gard

ing

the

prod

uct

and

the

man

agem

ent

team

.

1522

.4%

•U

nce

rtai

nw

het

her

can

con

vin

cecu

stom

ers

tobe

ton

anu

npr

oven

tech

nol

ogy.

•C

ust

omer

sm

ayn

otw

ant

topa

yen

ough

ofa

prem

ium

for

prod

uct

.•

Tar

get

cust

omer

sh

ave

not

his

tori

call

ybe

ensp

eedy

adop

ters

.•

Fin

anci

alvi

abil

ity

ofcu

stom

ers

and

exis

tin

gco

ntr

acts

ques

tion

able

.•

Ch

alle

nge

isto

broa

den

the

prod

uct

beyo

nd

the

init

ialc

ust

omer

segm

ent.

jofi˙673 JOFI.cls May 26, 2004 22:27

2184 The Journal of Finance

Tab

leII

—C

onti

nu

ed

Rea

son

toIn

vest

/Str

engt

hR

isk

ofIn

vest

men

t/W

eakn

ess

N%

Exa

mpl

esN

%E

xam

ples

Fin

anci

alm

arke

tan

dex

itco

ndi

tion

s

1116

.4%

•If

succ

essf

ul,

poss

ibil

ity

for

earl

yex

itor

acqu

isit

ion

.•

Exp

ect

toh

ave

acce

ssto

both

publ

icde

btan

deq

uit

yon

attr

acti

vete

rms.

•Q

uic

kfl

ippo

ten

tial

for

the

inve

stm

ent.

•M

any

stra

tegi

cbu

yers

avai

labl

e.•

Rec

ent

publ

icm

arke

ten

thu

sias

mfo

re-

com

mer

ceco

mpa

nie

sm

igh

ten

able

publ

iceq

uit

yfi

nan

cin

gto

mit

igat

efu

ture

fin

anci

ng

risk

s.•

Giv

enth

esi

zeof

the

mar

ket

oppo

rtu

nit

yan

dco

mpa

ny’

sst

rate

gy,c

apit

alm

arke

tsw

illb

ere

cept

ive

give

nth

atco

mpa

ny

ach

ieve

sbu

sin

ess

plan

.Als

o,a

con

soli

dati

ontr

end

shou

ldem

erge

inin

dust

ryas

mor

eco

mpa

nie

sen

ter

mar

ket.

57.

5%•

Wh

atw

illt

he

leve

rage

bean

dw

hat

hap

pen

sto

leve

rage

ifth

eIP

Ois

dela

yed?

•W

ould

may

bebe

bett

erto

sell

com

pan

y.•

Fin

anci

alm

arke

tan

dpo

liti

calf

luct

uat

ion

s.•

How

wil

lpu

blic

mar

kets

trea

tth

eco

mpa

ny?

C.D

iffi

cult

yof

Exe

cuti

on:P

rodu

ctan

dT

ech

nol

ogy,

Str

ateg

y

Pro

duct

and/

orte

chn

olog

y27

40.3

•L

ate

stag

esof

prod

uct

deve

lopm

ent

(fir

stpr

odu

ctla

un

chpl

ann

edin

15–1

8m

onth

s).

•S

upe

rior

tech

nol

ogy

wit

hla

rge

mar

ket

pote

nti

al.

•R

evol

uti

onar

yn

ewte

chn

olog

y.•

Has

deve

lope

dex

cell

ent

prod

uct

.•

Has

buil

ta

robu

st,s

cala

ble

syst

emth

atca

nm

eet

the

curr

ent

mar

ket

dem

ands

.•

Bes

tpr

odu

cton

the

mar

ket.

•W

ellt

este

dte

chn

olog

y/pr

odu

ct.

•E

arly

-sta

geco

mpa

ny

wit

hpo

st-b

eta

prod

uct

wit

hco

mpe

ten

t/ex

peri

ence

dte

chn

olog

yte

am.

2131

.3•

Ou

tcom

eof

clin

ical

test

san

dde

velo

pmen

t:M

ust

prov

eth

atte

chn

olog

yis

supe

rior

toot

her

mar

kete

dal

tern

ativ

es,i

nte

rms

ofef

fici

ency

and

side

effe

cts.

•E

arly

stag

ere

sear

chpr

ojec

t:P

roje

ctis

eleg

ant,

ambi

tiou

san

d,co

nse

quen

tly,

diff

icu

lt.

•A

bili

tyto

mak

ete

chn

olog

yw

ork

atta

rget

cost

poin

t.•

No

guar

ante

epr

odu

ctw

illw

ork

ina

full

prod

uct

ion

envi

ron

men

t.•

Iden

tifi

cati

onan

dde

velo

pmen

tof

am

ore

com

pell

ing

prod

uct

.•

Pro

duct

scal

abil

ity

isto

befu

lly

test

ed.

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2185

Bu

sin

ess

stra

tegy

/m

odel

3653

.7•

Com

pan

ysi

gnif

ican

tly

redu

ces

cost

sw

hil

em

ain

tain

ing

qual

ity.

•C

ompe

llin

gbu

sin

ess

stra

tegy

.Pre

sen

ceor

like

lih

ood

ofva

lida

tin

gco

rpor

ate

alli

ance

s.•

Ou

tsou

rcin

gm

ean

sle

ssfo

rco

mpa

ny

tom

anag

e.•

Att

ract

ive

and

dem

onst

rate

dpr

ofit

abil

ity

ofbu

sin

ess

mod

el.

•E

xcel

len

tn

ewco

nce

pt.

•Fa

vora

ble

acqu

isit

ion

oppo

rtu

nit

ies,

wh

ich

wil

lbe

driv

erof

grow

th.

•D

isti

nct

ive

stra

tegy

.•

Hig

hva

lue-

adde

d,h

igh

mar

gin

stra

tegy

for

very

litt

leca

pita

lupf

ron

t.•

“Lea

nan

dm

ean

”op

erat

ion

wit

hfe

wem

ploy

ees

and

good

cust

omer

focu

s.•

Pu

repl

ay/f

ocu

sed.

3450

.7•

Rea

lsal

esef

fort

nee

dsto

bem

oun

ted,

wh

ich

isve

ryre

lian

ton

man

agem

ent

team

’sex

peri

ence

tom

anag

epr

ofit

ably

.Tra

nsf

erab

ilit

yof

busi

nes

sm

odel

toot

her

mar

kets

?•

Are

ther

een

ough

can

dida

tes

avai

labl

efo

rac

quis

itio

n?

•W

illc

ompa

ny

beab

leto

ensu

requ

alit

yw

hil

epu

rsu

ing

agr

owth

-th

rou

gh-a

cqu

isit

ion

stra

tegy

?•

How

scal

able

isth

ebu

sin

ess?

Isth

ere

any

oper

atin

gle

vera

gein

the

busi

nes

sm

odel

?•

Lac

kof

focu

s.•

Vu

lner

able

stra

tegy

.•

Exe

cuti

onof

busi

nes

sm

odel

has

yet

tobe

prov

en.

•W

illc

ompa

ny

beab

leto

attr

act

empl

oyee

s?•

VC

due

dili

gen

cesh

owed

that

mar

gin

san

dex

pen

sepe

rcen

tage

sof

exis

tin

gst

ores

hav

eto

bebr

ough

tin

toli

ne

wit

hpr

otot

ype

mod

el.

•K

eypa

rtn

ersh

ips

not

nai

led

dow

n.

•G

eogr

aph

ical

risk

—U

.S.c

orpo

rate

and

fore

ign

R&

D.

jofi˙673 JOFI.cls May 26, 2004 22:27

2186 The Journal of Finance

VCs cite good performance to date in almost 27% and a favorable valuation ora low amount of capital at risk in roughly 20%.

Panel B shows that external factors are also important. VCs cite large andgrowing markets as attractive in almost 69% of the investments; a favorablecompetitive position and a high likelihood of customer adoption, in roughly30%; and favorable exit conditions, in 16%.

Panel C shows that factors related to execution are important as well. In atleast 40% of investments, VCs were attracted by the product/technology or bythe strategy/business model.

C. Investment Risks

While the VCs found the investments attractive on a number of dimensions,Table II also indicates that the VCs viewed the investments as having substan-tial risks.

Panel A shows that the primary internal risk was management, cited asrisky in 61% of the analyses. For example, one CEO was “difficult,” while sev-eral teams were incomplete. This 61% roughly equals the 60% of analysesfor which management was a reason to make the investment. The apparentcontradiction can be reconciled by observing that a VC might think highly ofthe founder, but be uncertain whether the founder can build the rest of theteam.

Panel A also indicates that the other internal factors of valuation, VC mon-itoring cost, downside risk, performance to date, and other investor influenceare concerns in, respectively, 19, 15, 13, 7.5, and 6% of the investments. Twoobservations are worth making about these risks. First, the risks of VC moni-toring costs show that in several instances, the VC worried that the investmentmight require too much time. This indicates that while VCs regularly play amonitoring and advisory role, they do not intend to become excessively involvedin the company. Second, because valuation is endogenous to the contracts, wewill not include it as a risk in the regressions.

Panel B reports external factors that the VCs viewed as risks. In 40, 31, and22%, of the investments, respectively, the VCs perceived competitive, marketsize, and customer adoption risks. Exit conditions were viewed as a risk in fewerthan 8% of the investments.

Panel C reports that execution difficulties are also important risks. In justover 50% of the investments, the VC viewed the strategy or business model asrisky. In 31%, the VC viewed the product and or technology as risky.

In general, the strengths and risks we identify are similar to those empha-sized in the VC strategy and management literature, as well as in anecdotalaccounts.

D. Relation of Strengths, Risks, and Firm Characteristics

Table III explores the relation of strengths and risks to each other and then toexogenous investment characteristics—pre- or postrevenue, first or subsequent

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2187

Tab

leII

IR

elat

ion

sb

etw

een

VC

Str

engt

hs,

Ris

ks,

and

Fir

mC

har

acte

rist

ics

Exp

lici

tly

men

tion

edst

ren

gth

san

dri

sks

inin

vest

ing

acco

rdin

gto

ven

ture

capi

tali

stan

alys

esan

dth

eir

rela

tion

toex

ogen

ous

firm

char

acte

rist

ics

for

67po

rtfo

lio

com

pan

ies

by11

ven

ture

capi

tal

part

ner

ship

s.In

vest

men

tsw

ere

mad

ebe

twee

n19

87an

d19

99.

Inte

rnal

risk

isth

eav

erag

eof

the

dum

my

vari

able

sfo

rth

epr

esen

ceof

man

agem

ent

qual

ity,

prev

iou

spe

rfor

man

ce,

fun

ds-a

t-ri

sk/d

own

side

,in

flu

ence

ofot

her

inve

stor

s,an

dco

stly

mon

itor

ing

risk

s(s

tren

gth

s).

Ext

ern

alri

sks

(str

engt

hs)

isth

eav

erag

eof

the

dum

my

vari

able

sfo

rth

epr

esen

ceof

mar

ket,

com

peti

tion

,cu

stom

erad

opti

on,a

nd

fin

anci

alm

arke

t/ex

itri

sks

(str

engt

hs)

.Exe

cuti

onri

sks

(str

engt

hs)

isth

eav

erag

eof

the

dum

my

vari

able

sfo

rpr

odu

ct/t

ech

nol

ogy

and

busi

nes

sm

odel

/str

ateg

yri

sks

(str

engt

hs)

.S

um

ofri

sks

(str

engt

hs)

isth

esu

mof

all

11ri

sk(s

tren

gth

)du

mm

yva

riab

les.

Str

engt

hs

min

us

risk

sis

the

diff

eren

cebe

twee

nsu

mof

risk

san

dsu

mof

stre

ngt

hs.

Pre

reve

nu

est

age

rou

nds

are

fin

anci

ng

rou

nds

for

com

pan

ies

that

had

no

reve

nu

esat

the

tim

eof

the

fin

anci

ng.

Fir

stV

Cin

vest

men

tsre

fer

toth

ero

un

dsin

volv

ing

the

firs

tti

me

any

ven

ture

capi

tal

fun

din

vest

edin

the

com

pan

y.In

dust

ryR

&D

/Sal

esis

the

aggr

egat

eR

&D

expe

nse

tosa

les

for

publ

icfi

rms

inth

eve

ntu

re’s

thre

e-di

git

SIC

indu

stry

,acc

ordi

ng

toC

OM

PU

ST

AT.

CA

(Non

-CA

)in

vest

men

tin

dica

tes

that

the

port

foli

oco

mpa

ny

was

(not

)lo

cate

din

Cal

ifor

nia

atth

eti

me

offi

nan

cin

g.L

ead

inve

stor

indi

cate

dth

atth

em

emo

was

wri

tten

byth

eV

Cfi

rmpr

ovid

ing

the

larg

est

amou

nt

offi

nan

cin

gam

ong

the

VC

sin

vest

ing

inth

ero

un

d.D

ata

onfu

nds

rais

edby

VC

firm

sar

eta

ken

from

ven

ture

econ

omic

s.In

pan

elB

,ast

eris

ksin

dica

tesi

gnif

ican

tdi

ffer

ence

su

sin

gei

ther

aM

ann

–Wh

itn

eyor

aK

rusk

al–W

alli

s(f

orV

Cdu

mm

ies)

test

,wh

ile

inpa

nel

Aas

teri

sks

indi

cate

sign

ific

ant

corr

elat

ion

coef

fici

ents

at1%

∗∗∗ ,

5%∗∗

,an

d10

%∗

leve

ls.

A.C

orre

lati

ons

betw

een

Str

engt

hs

and

Ris

ks(B

ivar

iate

Pea

rson

Cor

rela

tion

Coe

ffic

ien

ts)

Str

engt

hs

No.

ofIn

tern

alIn

tern

alE

xter

nal

Ext

ern

alE

xecu

tion

Exe

cuti

onM

inu

sP

ages

inS

tren

gth

sR

isks

Str

engt

hs

Ris

ksS

tren

gth

sR

isks

Ris

ksM

emo

Inte

rnal

stre

ngt

hs

1.00

00.

051

0.02

2−0

.095

0.00

5−0

.038

0.52

7∗∗∗

0.13

2In

tern

alri

sks

0.05

11.

000

0.31

5∗∗∗

0.29

1∗∗

−0.1

25−0

.012

−0.4

7∗∗∗

0.55

8∗∗∗

Ext

ern

alst

ren

gth

s0.

022

0.31

5∗∗∗

1.00

00.

334∗

∗∗−0

.002

−0.0

060.

256∗

∗0.

442∗

∗∗E

xter

nal

risk

s−0

.095

0.29

1∗∗

0.33

4∗∗∗

1.00

00.

089

0.08

9−0

.45∗

∗∗0.

215∗

Exe

cuti

onst

ren

gth

s0.

005

−0.1

25−0

.002

0.08

91.

000

0.26

4∗∗

0.25

4∗∗

−0.0

25E

xecu

tion

risk

s−0

.038

−0.0

12−0

.006

0.08

90.

264∗

∗1.

000

−0.2

84∗∗

0.02

4S

tren

gth

sm

inu

sri

sks

0.52

7∗∗∗

−0.4

7∗∗∗

0.25

6∗∗

−0.4

5∗∗∗

0.25

4∗∗

−0.2

84∗∗

1.00

0−0

.085

No.

ofpa

ges

inm

emo

0.13

20.

558∗

∗∗0.

442∗

∗∗0.

215∗

−0.0

250.

024

−0.0

851.

000

jofi˙673 JOFI.cls May 26, 2004 22:27

2188 The Journal of Finance

Tab

leII

I—C

onti

nu

ed

B.R

elat

ion

ofR

isk

Fact

ors

and

Str

engt

hs

toD

ealC

har

acte

rist

ics

CA

Lea

d1st

(N=

44)/

Ind.

R&

D/

Bef

ore

(N=

25)/

(N=

57)/

VC

Rai

sed

Pre

-(N

=21

)/S

ubs

equ

ent

Sal

es<

9%(N

=37

)/N

on-C

AN

on-L

ead

>6

(N=

33)/

VC

All

Obs

.P

ost-

(N=

46)

(N=

23)

(N=

32)/

Aft

er(N

=30)

(N=

42)

(N=

10)

<=6

Fu

nds

Du

mm

ies

(N=

67)

Rev

enu

eR

oun

d>

=9%

(N=

34)

Jan

.1,1

998

Inve

stm

ent

Inve

stor

(N=

34)

χ2(1

0)=

Inte

rnal

stre

ngt

hs

26.0

26.7

/25.

624

.6/2

8.7

23.1

/28.

224

.1/2

8.6

27.2

/25.

225

.3/3

0.0

25.4

/26.

58.

6In

tern

alri

sks

20.9

22.9

/20.

023

.2/1

6.5

29.4

/12.

4∗∗∗

19.0

/23.

612

.8/2

5.7∗

∗22

.1/1

4.0

21.2

/20.

632

.4∗∗

∗E

xter

nal

stre

ngt

hs

36.9

38.1

/36.

439

.2/3

2.6

39.8

/34.

637

.8/3

5.7

28.0

/42.

3∗∗

38.2

/30.

039

.6/3

5.3

20.5

∗∗E

xter

nal

risk

s25

.021

.4/2

6.6

27.8

/19.

631

.2/1

9.8∗

∗25

.6/2

4.1

17.0

/29.

8∗∗∗

26.3

/17.

524

.2/2

5.7

27.1

∗∗∗

Exe

cuti

onst

ren

gth

s47

.033

.3/5

3.2∗

∗44

.3/5

2.2

37.5

/55.

9∗∗

46.2

/48.

252

.0/4

4.0

49.1

/35.

047

.0/4

7.1

7.7

Exe

cuti

onri

sks

41.0

31.0

/45.

6∗40

.9/4

1.3

35.9

/45.

641

.0/4

1.1

40.0

/41.

742

.1/3

5.0

43.9

/38.

213

.6

Su

mof

stre

ngt

hs

3.72

3.52

/3.8

03.

68/3

.78

3.50

/3.9

23.

64/3

.82

3.52

/3.8

33.

77/3

.40

3.76

/3.6

816

.1∗

Su

mof

risk

s2.

872.

62/2

.98

3.09

/2.4

33.

44/2

.32∗

∗∗2.

79/2

.96

2.12

/3.3

1∗∗∗

3.00

/2.1

02.

91/2

.82

37.8

∗∗∗

Str

engt

hs

min

us

risk

s0.

850.

90/0

.83

0.59

/1.3

5∗0.

06/1

.59∗

∗∗0.

85/0

.86

1.40

/0.5

20.

77/1

.30

0.85

/0.8

525

.2∗∗

∗N

o.of

page

sin

mem

o6.

237.

14/5

.82

6.91

/4.9

67.

66/4

.92

6.69

/5.6

14.

80/7

.10∗

∗6.

84/2

.80∗

∗5.

79/6

.68

43.7

∗∗∗

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2189

round, industry research and development, pre- or post-1998, California or non-California investment, lead or nonlead investor, and VC firm experience.

We measure strengths and risks as the average of the dummy variables foreach type of strength and risk. Internal risk (strength) is the average of thedummy variables for the presence of management quality, previous perfor-mance, funds-at-risk/downside, influence of other investors, and costly mon-itoring risk (strength). External risk (strength) is the average of the dummyvariables for the presence of market, competition, customer adoption, and fi-nancial market/exit risk (strength). Execution risk (strength) is the averageof the dummy variables for product/technology and business model/strategyrisk (strength). These definitions normalize the measures to lie between zeroand one. While these variables may not capture all available information, theyreduce the extent to which we subjectively interpret the investment analyses.

Panel A shows that internal risks are correlated with external strengths andrisks. External strengths and risks are correlated with each other, as are exe-cution strengths and risks. While the length of the investment memo capturessome relevant information, it is significantly related to only half the risks andstrengths.

Panel B relates strengths and risks to other investment characteristics. Mostof the significant differences are found across different industries and geogra-phies. These effects are hard to disentangle from particular VCs because VCstend to concentrate in particular industries and in particular geographies.7 Insubsequent regressions, we control for these effects using the investment char-acteristic variables and VC dummies. Panel B also shows that memos are longerfor non-California investments and those in which the VC is the lead investor(57 investments.)

Finally, it is worth pointing out that measures of stage of development—pre-or postrevenue and first VC round—are not particularly correlated with ourrisk measures, suggesting that the risk measures pick up risks that are notdriven by stage.

E. VC Actions

Many papers have studied the role of VCs in assisting and monitoring theirportfolio companies. Gorman and Sahlman (1989), MacMillan, Kulow, andKhoylian (1988), Sapienza (1992), and Sapienza, Manigart, and Vermeir (1996)survey VCs and find that VCs spend substantial time and effort monitoring andsupporting their investments. Using data provided by start-ups, Hellman andPuri (2000 and 2002) find that firms financed by VCs bring products to mar-ket more quickly and are more likely to professionalize their human resourcefunctions. Lerner (1995) and Baker and Gompers (2001) find that VCs play animportant role on the board of directors.

7 For example, all our retail deals come from one VC who specializes in retail deals, and the sameis true for our healthcare ventures.

jofi˙673 JOFI.cls May 26, 2004 22:27

2190 The Journal of Finance

Table IVVenture Capitalist Actions

Venture capitalist (VC) actions before investment and anticipated at the time of investment forinvestments in 67 portfolio companies by 11 venture capital partnerships. Investments were madebetween 1987 and 1999.

Number (%)of Companies

ManagementVC active in recruiting or changing management team before investing 11 (16%)VC expects to be active in recruiting or changing management team after 29 (43%)

investingAny of the above 34 (51%)

Strategy/Business ModelVC explicitly active in shaping strategy/business model before investing 6 (9%)VC explicitly expects to be active in shaping strategy/business model after 20 (30%)

investingAny of the above 23 (34%)Examples:

Design employee compensationArrange vendor financing agreementsInstall information and internal accounting systemsHelp company exit noncore businessesImplement currency hedging programHire market research firm to help with new store locationsAssist with development of marketing planAssist with mergers and acquisitionsDevelop business plan, budget, financial forecastsMonitor R&D and product management effortsRefine pricing model and work on major account strategyAssist technical service teamLeverage VC strategic relationships

The results in previous work are all either survey-based or indirect. We usethe VC analyses to complement and corroborate that previous work by reportingthe actions that the VC took before investing and the actions the VC expectedto undertake after investing.

Table IV confirms that VCs help shape and recruit the management team.In 16% of the investments, the VC plays such a role before investing; in 43%,the VC expects to play such a role afterward. VCs also help shape the strat-egy and the business model before investing (in 9% of the investments) andexpect to be active in these areas afterward (in 30%). These actions includedesign of employee compensation, development of business plans and budgets,implementation of information and accounting systems, and assistance withacquisitions.8

8 Although not reported in a table, the extent of VC actions is highly correlated with the VCsand with industry.

jofi˙673 JOFI.cls May 26, 2004 22:27

Characteristics, Contracts, and Actions 2191

Our results likely understate the actions VCs take because we observe onlythose actions the VCs (a) reported as important and (b) had done or planned atthe time of investment. Even so, the results support and complement those inHellman and Puri (2002). In addition to actions traditionally associated withmonitoring (replacing management after poor performance), our results con-firm that VCs assist founders in running and professionalizing the business.

III. The Relationship between VC Risk Factorsand Contractual Terms