Embed Size (px)

Citation preview

Deductions under Chapter VIA

Institute of Chartered Accountants of India – WIRC

August 27, 2011

CA Chandresh Bhimani

Agenda

• Background

• Business deduction provisions under Chapter VIA

- Section 80-IA

- Section 80-IAB

- Section 80-IB

PwC

- Section 80-IB

- Section 80-IC

- Section 80-ID

- Section 80-JJA

- Section 80-JJAA

• Draft Direct Tax Code, 2010

• Appendix – Phased Out Deductions2

Provisions

Background

PwC 3

Background

• Gross Total Income (GTI)

- Total income computed in accordance with the provisions of the

Act, before making any deduction under Chapter VIA

• Total income = GTI less Applicable deductions under Chapter VI-A

(Section 80A)

PwC

(Section 80A)

• Chapter VI-A Deductions

- Section 80C to Section 80U

- Business Deductions

◦ Sections 80IA, 80IAB, 80IB, 80IC, etc

4

Basic Principles

• Aggregate deduction under Chapter VI-A not to exceed:

- gross total income of the assessee

- profits and gains of the undertaking or unit or enterprise or eligible

business

• Deduction to be calculated with reference to net income as computed

PwC

• Deduction to be calculated with reference to net income as computed

in accordance with the provisions of the Act

• No deduction to be allowed under any other provisions of the Act in

respect of the profits of an undertaking/unit/enterprise/ eligible

business to the extent of claim of deduction under Chapter VI-A

• Certain deductions to be computed with reference to income included

in GTI

5

Basic Principles

• Deduction not to be allowed unless:

- Claim of deduction made in the return of income

- Return of income filed within the due date

◦ Only section 80IA, 80IAB, 80IC, 80ID, 80IE

• Transfer price of goods and services between the undertaking or unit

PwC

• Transfer price of goods and services between the undertaking or unit

or enterprise or eligible business and any other undertaking or unit

or enterprise or business of the assessee to be determined at the

market value of such goods or services as on the date of transfer

• Where deduction in respect of profits or gains allowed under Chapter

VI-A is claimed and allowed in respect of profits of any business

specified under s 35AD of the Act, no deduction will be permitted

under s 35AD of the Act in relation to such specified business for the

same or any other assessment year6

Deduction under Chapter VIA

Section 80-IA

PwC 7

SECTION 80-IA

• Eligible activities for claiming deduction under Section 80-IA are

- Provision of infrastructure facilities

- Telecommunication services

- Development of Industrial park / special economic zone

PwC

- Power generation, transmission and distribution or substantial

renovation and modernization of existing distribution lines

- Reconstruction of a power unit

- Cross-country natural gas distribution network

8

Eligible

business

• Developing OR operating and maintaining OR developing,

operating and maintaining any “infrastructure facility”

• Infrastructure facility:

a) road including toll road, a bridge or a rail system;

b) highway project including housing or other activities

Section 80-IA – Infrastructure facility

PwC

b) highway project including housing or other activities

being an integral part of the highway project

c) a water supply project, water treatment system, irrigation

project, sanitation and sewerage system or solid waste

management system;

d) a port, airport, inland waterway, inland port or

navigational channel in the sea.

9

Other

Conditions

• Undertaking is owned by an Indian company / consortium

of such companies/ any Board / other authority established

under Central or State Act

• Entered into an agreement with Central Govt/ State Govt/

local authority etc

• Started or starts operating and maintaining Infrstructure

facility on or after 1st April, 1995

Section 80-IA – Infrastructure facility

PwC

facility on or after 1st April, 1995

Quantum • 100% deduction for 10 consecutive years in a block of 20

years except for d) wherein deduction is 100% for 10

consecutive years in a block of 15 years

10

Initial

Year

• Developing and beginning of operation of infrastructure

facility

Other

Points

• In case of transfer of an infrastructure facility by the

developer to another enterprise for operating and

maintaining the same on its behalf in accordance with the

agreement with the Central Government, State Government,

Section 80-IA – Infrastructure facility

PwC

agreement with the Central Government, State Government,

local authority or statutory body, deduction to be available to

transferee for the unexpired period

11

CBDT Circular - Widening of Road – Infrastructure facility Relaying of Road - No

Eligible

business

• Develops, develops and operates or maintains and operates

an industrial park notified during the period April 1, 1997 to

March 31, 2011

Quantum • 100% deduction for 10 consecutive years in a block of 15

years

Initial

Year

• Develops an industrial park

Section 80-IA – Industrial Park

PwC

Year

Other

Points

• Where an undertaking develops an industrial park and

transfers the operation and maintenance of this industrial

park to another undertaking, the deduction is available to

such a transferee undertaking for the balance period in the

10 consecutive years.

12

Eligible

business

• Undertaking engaged in

a) Generation or generation and distribution of power if

generation of power commenced during April 1, 1993 to

March 31, 2012

b) Transmission or distribution by laying a network of new

transmission or distribution lines during April 1, 1999 to

March 31, 2012

Section 80-IA – Power Generation

PwC

March 31, 2012

c) Substantial renovation and modernisation of existing

network of transmission or distribution lines during April

1, 2004 to March 31, 2012

Quantum • 100% deduction for 10 consecutive years in a block of 15

years

13

Initial

Year

• Begins to generates power or starts transmission or

distribution of power or undertakes substantial renovation

and modernisation of the existing transmission or

distribution lines

Other

Points

• Deduction to an undertaking referred to in (b) shall be

allowed only in relation to the profits derived from laying

such a network of new lines for transmission or distribution

Section 80-IA – Power Generation

PwC

such a network of new lines for transmission or distribution

• For undertaking referred to in (c), substantial renovation

and modernisation means an increase in the plant and

machinery in the network of transmission or distribution

lines by at least 50% of the book value of such plant and

machinery as on 01.04.2004

14

Eligible

business

Reconstruction or revival of a power generating plant by an

Indian company if:

• Such Indian company is formed before November 30,2005

with majority equity held by public sector companies and

such Indian company is notified before December 31, 2005

by the Central Government

• Generation or transmission or distribution of power before

Section 80-IA –Power Generation Plant Revival

PwC

• Generation or transmission or distribution of power before

March 31, 2011

Quantum • 100% deduction for 10 consecutive years in a block of 15

years

Initial

Year

• Develops an industrial park

Other

Points

• Begins to generate power or start transmission or

distribution of power

15

Issue – Work Contract

• Whether deduction available to sub-contractor

- Amendment to Explanation to section 80IA (w.r.e.f AY 2000-01)

◦ Deduction not available to works contracts awarded by any person and

executed by the undertaking

◦ M/s. B. T. Patil & Sons Belgaum, Construction Private Limited & Ors v.

PwC

ACIT (35 SOT 171)

› Deduction not available to sub-contractor

- Writ petition challenging constitutional validity of amendment made by

Finance Act 2009, admitted by Bombay High Court / Gujarat High Court

- JV Partner executing infrastructure development work eligible for section

80IA deduction, even if contract awarded to JV

◦ Transatory (India) Ltd [ ITA No. 540 /V/2009] – AY 2006-07

16

Recent Judicial precedents

• Rajkumar Exports Pvt. Ltd. v. ACIT [2009] 317 ITR 229

― amount disallowed are eligible for deduction under section 80IA

• CIT v. Chetak Enterprises (P.) Ltd. 176 Taxman 217 (Raj)

― Deduction u/s 80-IA will be allowed to the private limited company were contract was awarded to the erstwhile partnership firm by the Government

Associated Capsules Pvt. Ltd Vs Dy.CIT 2011-TIOL-28-HC-MUM-

PwC

• Associated Capsules Pvt. Ltd Vs Dy.CIT 2011-TIOL-28-HC-MUM-IT

― Deduction under section 80IA and 80HHC can be claimed simultaneously provided it should not exceeds profit of the undertaking

• CIT Vs M/s Dharampal Premchand Ltd 2010-TIOL-654-HC-DEL-IT

― No penalty is imposable if disallowance of deductions under Sections 80IA and 80IB is made

17

Issue: Treatment of Interest

Nature Deduction u/s?

Caselaw

Interest received from trade debtors

Yes – 80IA Advance Detergents Ltd. [2010] 228 CTR 356 (DEL)

Interest earned on FDRs No – 80IA, 80HH, 80I

Paras Oil Extraction Ltd.[1998] 230 ITR 266 (MP), Navbharat Explosives Co. (P.)Ltd. [2010] Tax LR 497

PwC

Ltd. [2010] Tax LR 497 (Chhattisgrah), Advance Detergents Ltd. [2010] 228 CTR 356 (DEL)

Interest received on letters of credit, bank guarantee money, deposits made under Sales Tax Rules, Kisan VikasPatras, Income-tax refund, Inter-corporate deposits

No – 80I Shri Ram Honda Power Equip [2007] 289 ITR 475 (DEL), Jay Bharat Maruti Ltd. [2010] 322 ITR 599 (DEL)

18

Provisions

Section 80-IAB

PwC 19

SECTION 80-IAB

• Deductions in respect of profits and gains from an undertaking or

enterprise engaged in development of SEZ

• Such SEZ should be notified on or after April 1, 2005

• Deduction is available of 100 percent of profits for ten consecutive

AYs

PwC

AYs

20

Issue - Characterisation of Developer’s income

• For tax purposes, income from lease of a real estate asset could be characterised as :

- Income from Business (“Business Profits”); or

- Income from House Property (“House Property”)

• Characterization of income to depend on nature of income

- Whether pure lease transaction or sophisticated business activity

PwC

- Whether pure lease transaction or sophisticated business activity

Composite letting – Business Income

• CIT v. National Storage Pvt Ltd (56 ITR 596)

• Manohar Singh v. CIT (58 ITR 592) (Punjab HC)

• Associated Building Co Ltd (137 ITR 339) (Bom HC)

Pure letting – House Property Income

• Shambhu Investment Pvt Ltd v. CIT (263 ITR 143) (SC)

• Karnani Properties Ltd. v. CIT (82 ITR 547) (SC)

21

Issue - Characterisation of Developer’s income

• For tax purposes, income from lease of a real estate asset could be characterised as :

- Income from Business (“Business Profits”); or

- Income from House Property (“House Property”)

PwC

Composite letting – Business Income

• CIT v. National Storage Pvt Ltd (56 ITR 596)

• Manohar Singh v. CIT (58 ITR 592) (Punjab HC)

• Associated Building Co Ltd (137 ITR 339) (Bom HC)

Pure letting – House Property Income

• Shambhu Investment Pvt Ltd v. CIT (263 ITR 143) (SC)

• Karnani Properties Ltd. v. CIT (82 ITR 547) (SC)

22

Issue - Characterisation of Developer’s income

• What if rent and service income recovered seperately from the lessee?

Sarabhai Pvt Ltd (263 ITR 197) (Guj HC)Where the rental and the service arrangement are separable, (i.e. the one is not so integral to the other such that it cannot be separated) having regard to the overall purpose of the agreement, then the rental income should be characterized as

PwC

agreement, then the rental income should be characterized as HP income and the service income should be regarded as Business Income

Sultan Bros P Ltd. v. CIT (51 ITR 353) (SC)… …has held that where the two arrangements are per se inseparable (i.e. letting of one without other is not possible); then despite the fact that the income streams have been bifurcated in the agreement, the same would be characterized on an aggregate basis

23

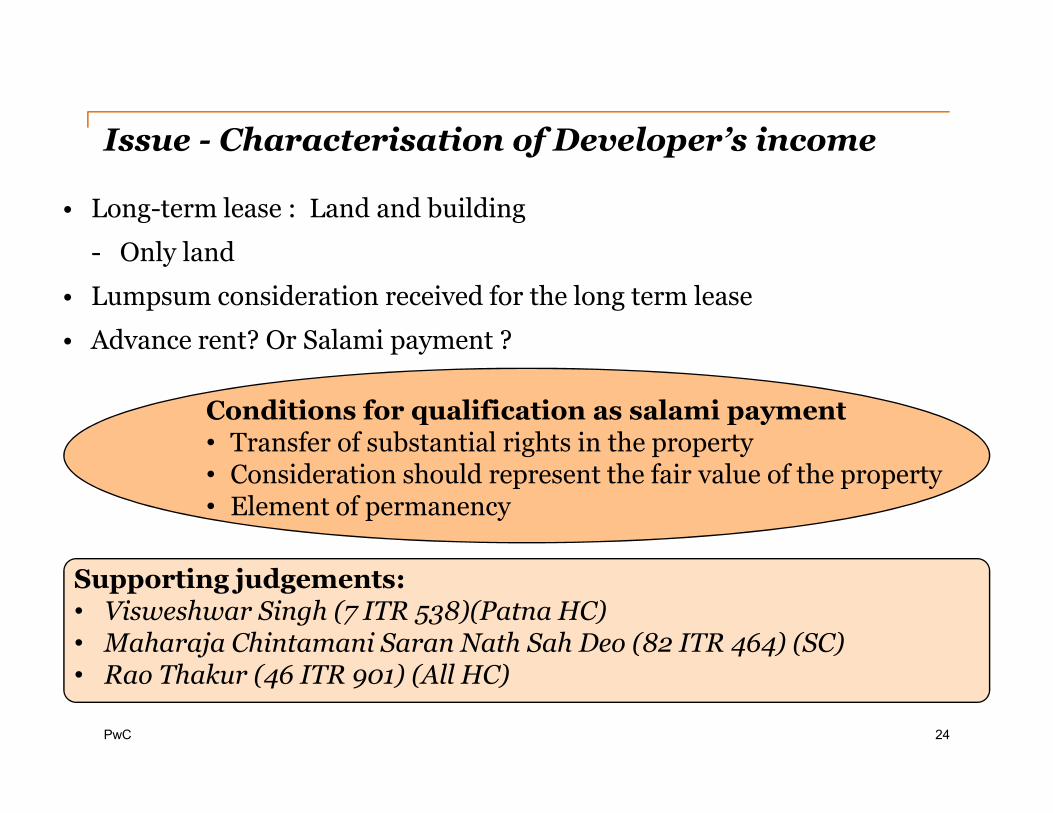

Issue - Characterisation of Developer’s income

• Long-term lease : Land and building

- Only land

• Lumpsum consideration received for the long term lease

• Advance rent? Or Salami payment ?

Conditions for qualification as salami payment

PwC

Supporting judgements:• Visweshwar Singh (7 ITR 538)(Patna HC)• Maharaja Chintamani Saran Nath Sah Deo (82 ITR 464) (SC)• Rao Thakur (46 ITR 901) (All HC)

Conditions for qualification as salami payment• Transfer of substantial rights in the property• Consideration should represent the fair value of the property• Element of permanency

24

Issue - Characterisation of Developer’s income

• Deduction under section 80IAB available if developer’s income classified as house property income?

- Section 80IAB does not indicate head of income

- Deduction should be available

PwC

• Lease of land to co-developer for carrying on developing activity-deduction available?

- Section 80IAB mentions business of developing a SEZ

- What constitutes “development of SEZ” not clear

- Strict interpretation-deduction not available

25

Issue - Characterisation of Developer’s income

• Developer develops land in part and leases the same to co-developer for balance development and operating and maintenance

• Developer receives lease rentals from co-developer

• Co-developer receives lease rentals from units

• Whether Developer eligible for 80IAB deduction for part development of

PwC

• Whether Developer eligible for 80IAB deduction for part development of land?

• Will Co-Developer be entitled to claim 80IAB deduction?

Deduction should be available

26

Provisions

Section 80-IB

PwC 27

SECTION 80-IB

• Deduction in respect of profits and gains from certain industrial

undertakings other than infrastructure development undertakings

• Eligible activities for claiming deduction under Section 80IB are

- Business of an industrial undertaking (Refer Annexure for details)

- Operation of ship

PwC

- Hotels

- Industrial research

- Production of mineral oil

- Developing and building housing projects

- Business of processing, preservation and packaging of fruits or

vegetables or integrated handling, storage and transportation of

food grains units

28

SECTION 80-IB

- Multiplex theaters

- Convention centre

- Operating and maintaining a hospital in rural area

- Hospital located in certain areas

PwC 29

Eligibility • Undertaking developing and building housing projects

approved before March 31, 2008 by local auhority

•Housing project –

• Min land area – one acre

• Max built up area for each unit- 1000 sq ft for Delhi/

Section 80-IB – Housing Projects

PwC

Mumbai (1500 sq ft for others)

•Commercial built up area < 3% of the aggregate built up

area or 5,000 sq ft, whichever is higher (from AY 2005-

06)

• One unit to an individual

• Deduction not available for execution of housing projects on

works contract basis

Quantum • 100% deduction for profits derived from such project

30

Issue – Cap on Commercial Space – Retrospective ?

CIT V.M/.s Brahma Associates ( 333 ITR 289) (Bom) (AY 2003-04)

• Assessee undertook a construction project which consisted of 15 residential buildings and 2 commercial buildings

• Local authority had approved the project as “residential plus commercial”. Project commenced on 14 August 2000 and was completed on 3 October 2005

PwC

completed on 3 October 2005

• Claimed deduction under section 80IB (10) on the profits derived from the sale of the residential units in the project

• AO rejected the claim on the ground that the project was approved by the local authority as “residential plus commercial‟ and hence was not a project of residential units only

• CIT(Appeals) dismissed the appeal filed by the taxpayer

• On further appeal, the matter was referred to a Special Bench of the Tribunal which ruled partly in favour of the taxpayer

31

Issue before the High Court

• Whether deduction under section 80IB(10) as applicable prior to 1 April 2005 allowable to a housing project approved by a local authority with commercial user to the extent permitted under the rules framed by the local authority?

• Whether the limit on commercial use of built-up area as prescribed by clause (d) of section 80-IB(10) is prospective and hence applicable from assessment year 2005-06 onwards?

PwC

Conclusion

• a project with residential and commercial user to the extent permitted under Development Control Rules would be a “housing project” eligible for deduction under section 80-IB(10) of the Act upto assessment year 2004-05

• With effect from the assessment year 2005-06, the deduction under section 80-IB(10) of the Act would be available subject to the fulfilment of commercial user criteria set out in clause (d) to section 80-IB(10)

32

August 2011

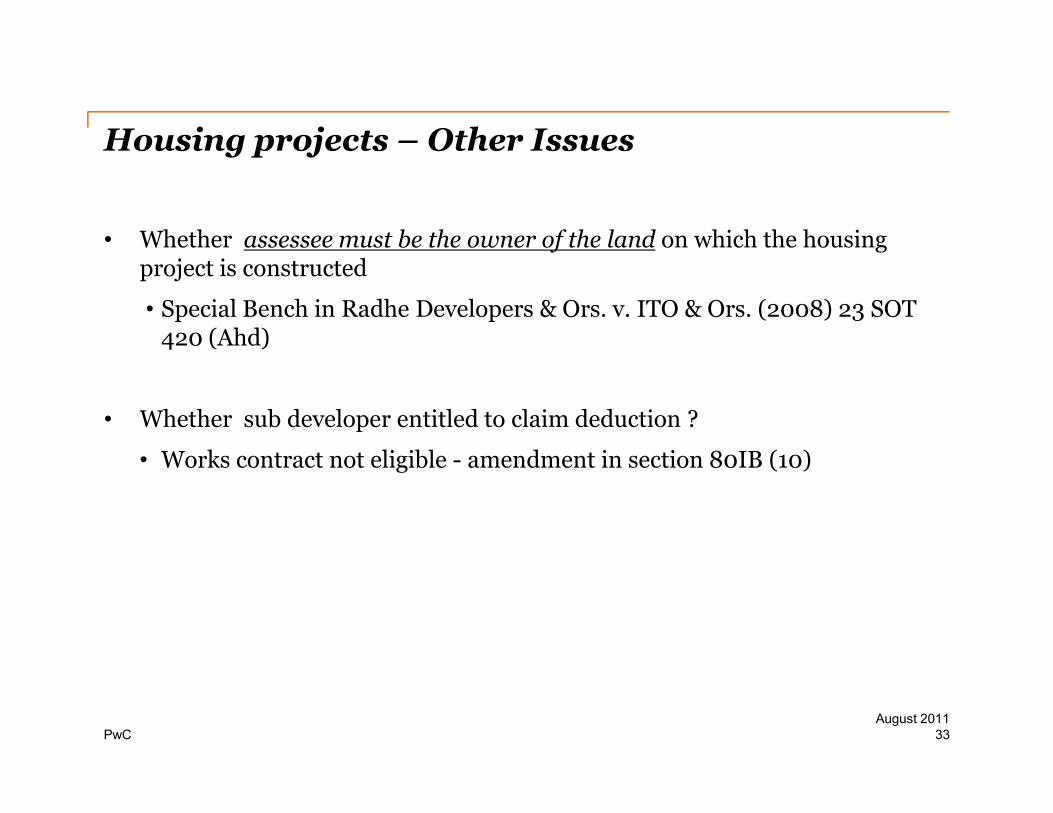

Housing projects – Other Issues

• Whether assessee must be the owner of the land on which the housing project is constructed

• Special Bench in Radhe Developers & Ors. v. ITO & Ors. (2008) 23 SOT 420 (Ahd)

• Whether sub developer entitled to claim deduction ?

PwC

• Whether sub developer entitled to claim deduction ?

• Works contract not eligible - amendment in section 80IB (10)

33

August 2011

Eligible

business

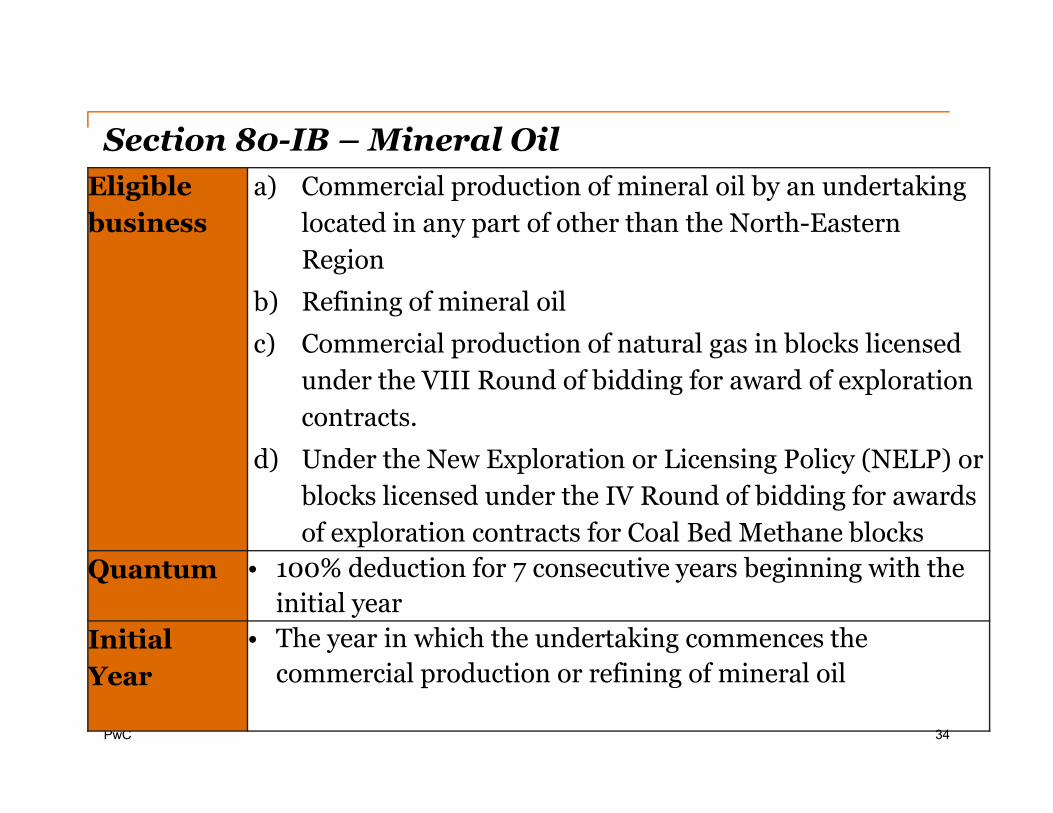

a) Commercial production of mineral oil by an undertaking

located in any part of other than the North-Eastern

Region

b) Refining of mineral oil

c) Commercial production of natural gas in blocks licensed

under the VIII Round of bidding for award of exploration

contracts.

Section 80-IB – Mineral Oil

PwC

contracts.

d) Under the New Exploration or Licensing Policy (NELP) or

blocks licensed under the IV Round of bidding for awards

of exploration contracts for Coal Bed Methane blocks

Quantum • 100% deduction for 7 consecutive years beginning with the

initial year

Initial

Year

• The year in which the undertaking commences the

commercial production or refining of mineral oil

34

Other

Points

• the commercial production of mineral oil should have

begun or begins on or after 01.04.1997

• In the case of (a), deduction shall not be available to blocks

licensed under a contract awarded after the 31st day of

March 2011,under NELP announced by the Resolution No.

O-19018/22/95 – ONG.DO.VL,dated 10th February, 1999

or in pursuance of any law for the time being in force or by

Section 80-IB – Mineral Oil

PwC

or in pursuance of any law for the time being in force or by

the Central or a State Government in any other manner;

• In the case of (b), the refining of mineral oil should be

commenced by the undertaking not later than 01.04.2012;

• In the case of (c), the commercial production of natural gas

should be commenced on or after 01.04.2009

35

Eligible

business

a) Processing preservation and packaging of fruits or

vegetables

b) Processing, preserving and packaging of meat and meat

products or poultry, marine or dairy products

c) The integrated business of handling, storage and

transportation of food grains

Quantum • 100% deduction for 5 years beginning with the initial year

Section 80-IB –Food Processing

PwC

Quantum • 100% deduction for 5 years beginning with the initial year

• 25% (or 30% where the assessee is a company) for next 5

years

• Total period is 10 consecutive years

Initial

Year

• The year in which the undertaking begins such business

36

Other

Points

• Undertaking begins to operate such business on or after

April 1, 2001

• Deduction in case of (b) would be eligible to the undertaking

commencing its operations on or after April 1, 2009

•

Section 80-IB –Food Processing

PwC 37

Eligible

business

• Operating and maintaining a hospital located anywhere in

rural areas, other than the excluded area

Quantum • 100% deduction for 5 consecutive years beginning with the

initial year

Initial

Year

• The year in which the hospital starts functioning

Section 80-IB –Hospitals

PwC

Year

Other

Points

• The hospital is constructed and has started or starts

functioning at any time during the period beginning on the

01.04.2008 and ending on the 31.03.2013

• The hospital has at least 100 beds for patients

• The construction of the hospital is in accordance with the

regulations or bye-laws of the local authority

• “Excluded area” shall mean specified areas in specified cities

38

Eligible

business

• Engaged in the business of hotel located in the specified

district having a World Heritage Site

Quantum • 100% deduction for 5 years beginning with the initial year

Initial

Year

• Hotel is constructed and has started or starts functioning at

any time during the period beginning on the April 1, 2008

and ending on the March 31, 2013

Section 80-ID –Heritage Hotels

PwC

and ending on the March 31, 2013

39

Issue - Operating & Management Arrangement

Constructs and

starts functioning

O & M

arrangement

A Ltd. (owning co.)

Management

fees

PwC

Hotel

B Ltd. (operating co.)

Operating revenueO & M

arrangement

fees

A Ltd. appoints B Ltd for operating and managing the hotel

40

Issue - Operating & Management Arrangement

• Income-tax implications in the hands of A Ltd.

- Eligible for 80ID deduction

◦ engaged in business of hotel

- O & M fees paid to B Ltd. is an allowable deduction - subject to tax

withholding u/s. 194J / 195

PwC

withholding u/s. 194J / 195

• Income-tax implications in the hands of B Ltd.

- O & M fees – Business or Other Sources

- Eligible for 80ID deduction ?

A Ltd. and B Ltd. can claim 80ID deduction on same undertaking ?

41

Section 80ID (contd.)

Issues

• Engaged in “business of hotel” – meaning

- Construction and operation by same entity?

- Deduction to hotel operating entities?

◦ Radhe Developers & Ors. 113 TTJ 300 (Ahd)

Slide 42

◦ Radhe Developers & Ors. 113 TTJ 300 (Ahd)

◦ Shakti Corpn [2009] 32 SOT 438 (Ahd)

• Deduction available on “business income” – meaning?

• Amalgamation and demerger – deduction available ?

- rigors of section 80IA(12A) not present

Provisions

Section 80-IE

PwC 43

SECTION 80-IE

• Deduction in respect of certain undertakings in North-Eastern

States

• The deduction is available if the assessee begins manufacture or

production of eligible goods or undertakes substantial expansion or

begins to provide the eligible services during April 1, 2007 to March

31, 2017

PwC

31, 2017

• These activities should be undertaken in North-Eastern states

44

SECTION 80-IE

• Eligible business includes

- Hotels

- Adventure and leisure sports

- Nursing home

- Old age homes

PwC

- Old age homes

- Vocational training institutes

- IT related training institutes

- It hardware units and bio-technology

• Substantial expansion means increase in investment in the plant and

machinery by at least 25 percent of the book value of plant and

machinery (before depreciation), as on the first day of the year in

which expansion takes place

45

Provisions

Section 80-JJA, 80-JJAA

PwC 46

Eligible

business

• Business of collecting and processing or treating of bio-

degradable waste:

• for generating power; or

• for producing bio-fertilizers, bio-pesticides or other

biological agents; or

SECTION 80-JJA - Collecting and Processing of Bio-degradable Waste

PwC

biological agents; or

• for producing bio-gas; or

• making pellets or briquettes for fuel or organic manure

Quantum • 100% deduction for 5 years beginning with the initial year

Initial

Year

• Year of commencement of business

47

Eligible

business

• Employment by any industrial undertaking engaged in the

manufacture or production of articles or thing, of new

regular workmen

• A “regular workman” does not include:

• a casual workman; or

• a workman employed through contract labour; or

SECTION 80-JJAA - Employment of New Workmen

PwC

• a workman employed through contract labour; or

• any other workman employed for a period of less than 300

days during the financial year

Quantum • 30% of additional wages paid to the new regular workmen

employed by the assessee in the financial year for the period

of three years, starting from the initial year

Initial

Year

• Year in which the employment is provided to new regular

workmen

48

Provisions

Other Points

PwC 49

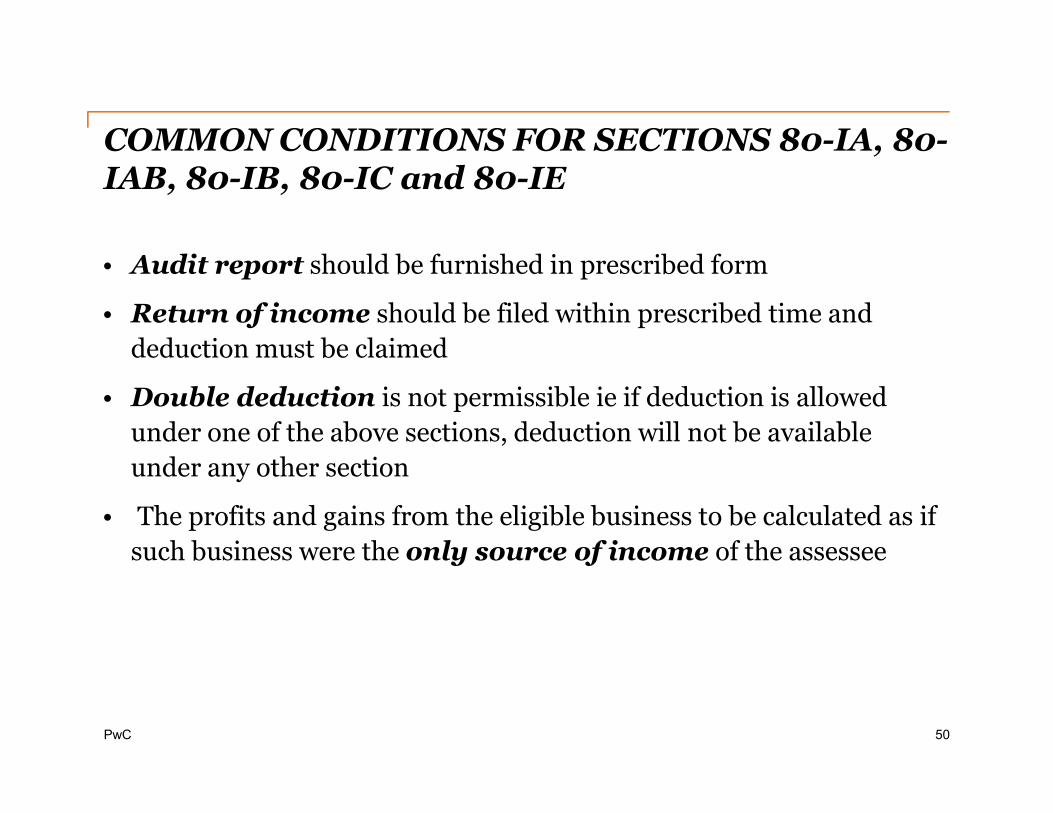

COMMON CONDITIONS FOR SECTIONS 80-IA, 80-IAB, 80-IB, 80-IC and 80-IE

• Audit report should be furnished in prescribed form

• Return of income should be filed within prescribed time and

deduction must be claimed

• Double deduction is not permissible ie if deduction is allowed

PwC

• Double deduction is not permissible ie if deduction is allowed

under one of the above sections, deduction will not be available

under any other section

• The profits and gains from the eligible business to be calculated as if

such business were the only source of income of the assessee

50

COMMON CONDITIONS FOR SECTIONS 80-IA, 80-IAB, 80-IB, 80-IC and 80-IE

• The AO has power to recompute profits if

- The taxpayer carries on two or more businesses out of which

atleast one is qualified for deductions in the above-mentioned

sections

- Some goods are transferred from the business eligible for

PwC

- Some goods are transferred from the business eligible for

deduction to the other business

- Some goods are transferred from the business eligible for

deduction to the other business

• If the undertaking entitled for deduction is

amalgamated/demerged, then the amalgamated/resulting

company can avail the benefit for the unexpired period of the tax

holiday

51

DRAFT DIRECT TAX CODE, 2010 (DTC)

PwC 52

DRAFT DIRECT TAX CODE, 2010 (DTC)

• Sections 80-IA, 80-IAB, 80-IB, 80-IC,80-ID, 80-IE, 80-JJA or 80-

JJA grandfathered subject to following conditions:

- Assessee eligible to claim such deduction for AY 2012-13

- Eligible profits computed as per DTC with specified exclusions

PwC

- Deduction not allowed for period otherwise not allowable under

the Act

- Capital expenditure not to be allowed as deduction while

computing GTI

- Other conditions prescribed in relevant sections continue to be

satisfied

53

Thank You

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, [insert legal name of the PwC firm], its

members, employees and agents do not accept or assume any liability, responsibility or duty of

care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2011 PricewaterhouseCoopers Private Ltd. All rights reserved. “PwC”, a registered

trademark, refers to PricewaterhouseCoopers Private Limited (a limited company in India) or,

as the context requires, other member firms of PwC International Limited, each of which is a

separate and independent legal entity.

Appendix – Phased out Deductions

PwC 55

Section 80-IA – Past Deductions

S.

No.Eligible business

Sunset date

(the last date

up to which

the

deduction is

allowed)

Period of

deduction

Deduction

available (if

set-up in the

year of sunset

date) until

financial year

1 An undertaking which starts March 31, 2005 100% deduction 2013-14 to 2018-

PwC

providing

telecommunication services,

whether basic or cellular,

including radio paging,

domestic satellite service,

network of trunking,

broadband network and

internet services during the

period 01.04.1995 to

31.03.2005

for the first five

years and 30%

for the next five

years

Total 10

consecutive

years in a

block of 15

years

19 depending

upon the initial

year opted

56

Section 80-IA – Past Deductions

S.

No.Eligible business

Sunset date

(the last date

up to which

the deduction

is allowed)

Period

of

deducti

on

Deduction

available (if

set-up in the

year of sunset

date) until

financial year

2 An undertaking which develops,

develops and operates or maintains and

operates an SEZ, notified by the Central

March 31, 2005 100%

deduction

for the 10

2013-14 to 2018-

19 depending

upon the initial

PwC

operates an SEZ, notified by the Central

Government in accordance with the

scheme framed and notified by that

Government during the period

01.04.1997 to 31.03.2005.

In a case where an undertaking develops

an SEZ and transfers the operation and

maintenance of such SEZ to another

undertaking (the transferee undertaking),

the deduction is available to the transferee

undertaking for the remaining period in

the 10 consecutive years.

for the 10

consecutive

years in a

block of 15

years

upon the initial

year opted

57

Section 80-IA – Past Deductions : Conditions

S.

No.Conditions Remarks

1. The undertaking is owned by a company registered

in or by a consortium of such companies or by an

authority or a board or a corporation or any other

body established or constituted under any Central or

State Act

2. The undertaking has entered into an agreement with

the Central Government or a State Government or a

PwC

the Central Government or a State Government or a

local authority or any other statutory body for (i)

developing; or (ii) operating and maintaining; or

(iii) developing, operating and maintaining a new

infrastructure facility

3. The undertaking has started or starts operating and

maintaining the infrastructure facility on or after

01.04.1995

58

Section 80-IA – Past Deductions : Conditions

S.

No.Conditions Remarks

4. In the case of a highway project, where housing or

other activities are an integral part of the highway

project, the deduction will be made available only

where the profits from housing or other activities

are transferred to a special reserve and the reserve is

actually utilised for the highway project excluding

housing and other activities before the expiry of

The amount remaining unutilised would

be charged to tax as income of the year in

which the transfer to reserve account took

place

PwC

housing and other activities before the expiry of

three years following the year in which the amount

was transferred to the reserve.

59

Section 80-IB – Past Deductions

S. No.

Eligible business

Sunset date(the last date up to which the deduction is allowed)

Period of deduction

Deduction available (if set-up

in the year of sunset date) tillfinancial year

1 A small-scale industrial undertaking which begins to manufacture or produce articles or things or operate a cold storage plant

March 31, 2002 10 years (12years in case of aco-operativesociety)

2010/11 (2012/13 in case of co-operative society)

PwC

[s 80-IB(3)(ii)]2 An industrial undertaking in

a industrially backward state which begins to manufacture or produce articles or things or operate a cold storage plant [s 80-IB(4)]

March 31, 2004 10 years (12years in case of aco-operativesociety)

2012/13 (2014/15 in case of co-operative society)

60

Section 80-IB – Past Deductions

S. No.

Eligible business

Sunset date(the last date up to which the deduction is allowed)

Period of deduction

Deduction available (if set-up

in the year of sunset date) tillfinancial year

3 An Industrial undertaking in an industrially backward district which begins to manufacture or produce articles or things or operate

March 31, 2004 8–10 years (12 years in case of a co-operative society) depending on

2010-11/2012/13 (2014/15 in case of a co-operative society) depending on the category of district.

PwC

a cold storage plant [s 80-IB(5)]

the category of district.

4 Company carrying on Scientific Research & Development [s 80-IB(8A)]

March 31, 2007 10 years 2015/16

5 Undertaking developing and building Housing Projects [s 80-IB(10)]

Project approved before March 31, 2008

Deduction allowed up to 5 years for projects approved after 01.04.2005.

2011/12

61

Section 80-IB – Past Deductions

S. No.

Eligible business

Sunset date(the last date up to which the deduction is allowed)

Period of deduction

Deduction available (if set-up

in the year of sunset date) tillfinancial year

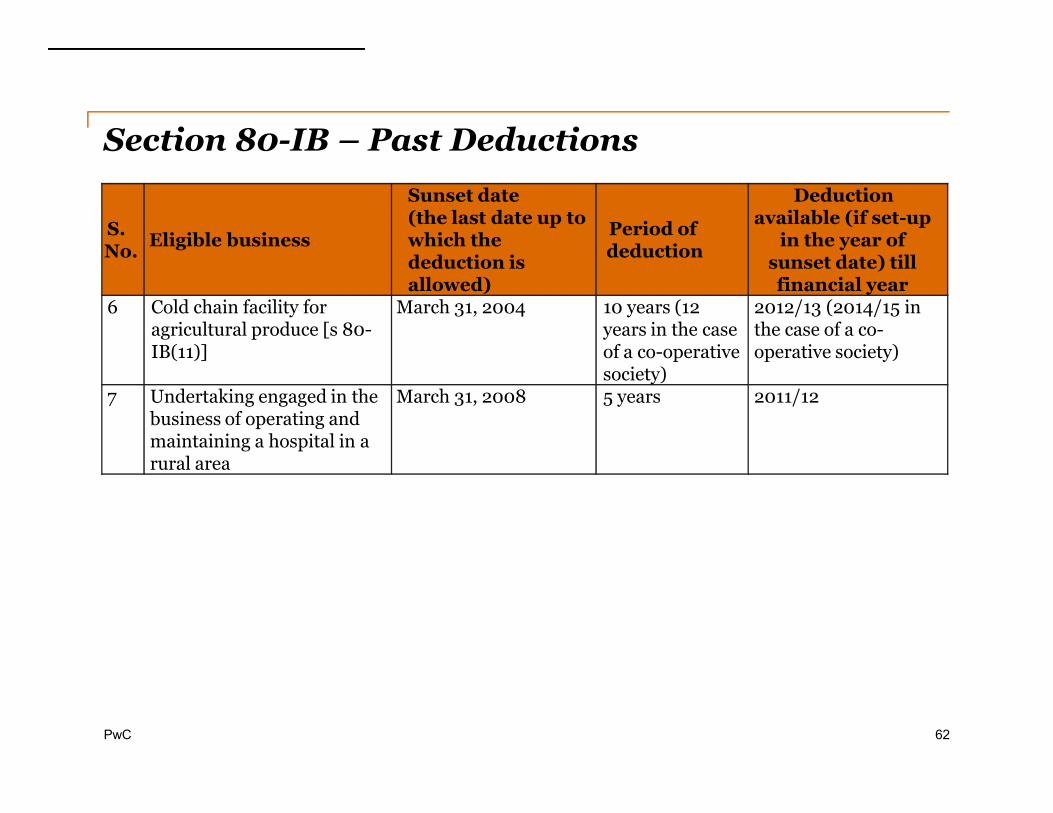

6 Cold chain facility for agricultural produce [s 80-IB(11)]

March 31, 2004 10 years (12 years in the case of a co-operative society)

2012/13 (2014/15 in the case of a co-operative society)

7 Undertaking engaged in the March 31, 2008 5 years 2011/12

PwC

business of operating and maintaining a hospital in a rural area

62

Section 80-ID – Past Deductions

S.

No.Eligible business Quantum of

deductionInitial year Remarks

1. Engaged in the business

of hotels located in

specified areas

100% deduction

for 5 years

beginning with

the initial year

Year in which

the business of

the hotel starts

functioning

Hotel is constructed and

starts functioning during

the period 01.04.2007 to

31.07.2010

2. Engaged in the business

of building, owning and

operating a convention

100% deduction

for 5 years

beginning with

Year in which

the convention

centre starts

Convention Centre is

constructed during the

period 01.04.2007 to

PwC

operating a convention

centre located in a specified area

beginning with

the initial year

centre starts

operating on a commercial

basis

period 01.04.2007 to

31.07.2010

63