Embed Size (px)

Citation preview

CHAPTER - V I

MARKETING OF FOOTWEAR IN ATHANI. AGRA AND MADRAS

CHAPTER YI

MARKETIN0 OF FOOTWEAR IN IITH~III, A G R ~ AND mOmS

6 . 0 INTRODUCTION

J n this Chapter, an attempt ls made to study tire

marketing practices followed, znvalvement of middlemen in tile

market channels, the price mark UP rlght from the producer level

until they reach the ultimate consumers, the made of payments,

the problems in credit and advance payment systems, the market

cost6 involved and the instltutional assistance provided to the

footwear artisans In selling the footwear

The shoes produced in Agra are marketed all over ~ndia

mainly through the wholesale dealel-s o f the Hing-ki-mandl market,

partly by 'Bata' and 'Carona' through their chain of retail

market outlet6 and by ths Government agencies like charma Kuteer

of KVIC, LAMCO, Bharat Leather Corporation (BLC) and the non-

governmental organisation of Bharatiya Charmadyog Sangh (BCS).

Apart from meeting the domestic consumptun, the shoes and shoe

uppers made I" the semi-mechanised factories o f A g r a , are

exported to USSR, ern any, UK and Netherlands. similarly, the

kalhapuri chappals made in ~thani find their market all over

India through Chalnalaya (KVIC), the Xhadi ~andars o f KVIC.

and by L I D ~ R through ~ t s emporias and then by the wholesale

dealers in the cities. The mixed leather fnatwcar

made in xadras m , , , n , y cater to the needs of the local plntform

shops and retail dealers in Medras market. Data provided in Table

6.1 the mode selling of foat*tear by these agenctes.

&THAN1

Of the total faotwear produced i n the household ,,nit+

~f Athani centre, 6 0 % 1s procured by the G~~~~~~~~~

the Charmalaya, a Departmental unit of KVIC and itle procurement

centres of LIDWR (Table 6.1). Wlthln this 6 0 8 , the share of

chamalaya work* out to 45% and the LIDXAR 1 5 % . Both these

centres are located I" the midst of the footwear

artisan units concentrated in xalgalli area. 35% ai the faatwear

in the artisan units are procured by the outside

wholesale dealers stationed in Bombay, ~ u n e , ~yderabad,

Bangalare, Trivandrum and the remaining 5 % goes directly t o the

retail dealers who plaoe orders.

In the case of household warkshopa, 57% of their output

is supplied to autslde wholesale dealers and 39% to the

government aqr 'nr l r? of Charmalaya and LIDl<hR and 4 % of the

footwear produced are sold dlrectly to the outside retail

dealers . Thus, institut~onal agencles emerged as the leading

marketers of footwear in Athani centre. It 1s evident from the

fact that the outside dealers procure these footwear against

advances to the artrsan units.

6.1.1 MODE OF PAYMENT

production units, which are given each a code

number, charmalap, takes the orders and specifications

regarding the design, materials to be used, purchase the

raw material., fabricate the footwear In their houses and EuPPlY

them to charmalaya weekly. ~t the time of supply, the quality Of

the pairs, the materials used in fabrication, the uniformity

within the pairs, are inspected visually by the Quality

lnspectnr and paymen: f o r t h e acceiited footwear are w,ii , , l ,

one t o two h o u r s time. The Charmalaya's p ~ . ~ c ~ ~ ~ ~ ~ ~ , t on

~ ~ ~ k t n g day s t a r t s a t 1 0 AM and gars u p t a 2 PM dlsburspmrt,t

of t akes P l a c e a f t e r 2 PM I f t h e value of t h e footweat

i s l e s s t h a n Rs.2 ,000/- tilo a r t i s n ~ l s are p s i 6 with o = ~ ,

and t f i t e x c e e d s Rs.2 ,000/- t h e y are paid i n t h e form a cheque.

a r t i s a n s a f t e r r e c e i v i n g t h e amount/cheque, a l s o g e t orders

far t h e s u b s e q u e n t week and t h i s modus a p e r a n d i is b e i n g

~ ~ s t e m a t ~ c a l l y fol lowed s i n c e i t s inception. he r e l e c t i o n r a t e

a t t h e i n s p e c t l a " var i e s from 2 t o 5 % . These r e l e c t e d footwear

are a g a i n r e c t i f i e d by replacing t h e p a r t i c u l a r p a r t s and

l e d s u b s e q u e n t l y .

The market ing p r a c t i c e s and t h e made of payment f a r

these i n f o r m a l s e c t o r footwear u n i t s have made t h e market ing

~ n s t i t u t i a n s v e r y p a p u l a r among t h e household a r t i s a n s . T h i s

p r a c t l c e h a s c r e a t e d enormous degree of consciousness among t h e

a r t i s a n s which is unknown t o them e a r l i e r . These changes i n

r a r k e t i n g p r a c t i c e s i n Athani c e n t r e has opened t h e f l o o d g a t e s

of m a r k e t i n g o f t h e s e t r a d i t i o n a l chappals t o modern market ing

techniques . I t has a g r e a t bear ing on t h e marketing of footwear

in t h e o t h e r areas also. he g r w t h of i n r t r t u t i o n a l c h a n n e l s

l i k e Charmalaya and i t s performance i s shown In Annexure 3 3 of

Chapter 111.

he LIDKAR oentre a l s o l n t h e midst o f t h e

l o c a l i t y procure t h o footwear from t h e a r t l s a n s s i m i l a r on t h e

l i n e s o f Charmalaya. he mode of payment i n LIDYAR is o n l y by

cheque b u t in cash. whi le giving t h e o r d e r s the a r t i s a n s are

instructed to follow the Pattern ac s lae s f o l every 12 t o

be made in each si2e as shown b c l o r , ~ :

size in inches No of pairs ---------.--..--..------..---. Gents Chappala 1,adios Chsppnls

1 2 3 ____-------------------..--...--.---...---.---....

4 N11 1

5 Nil 3

6 1 4

7 2 3

8 4 1

9 4 Nil

10 1 Nil

Total pairs 12 12

Aaart from the aovernnent aaencies menttoned above the

wholesale dealers stationed in major metropolitan olties and

towns also place orders mainly with the household workshops, At

the time of placing order they give advances to the proprietor,

either partly or fully to the value of the orders. This advance

payments again depend upon the mutual understanding and the

confidence built up on either side aver the years. The wholesale

dealers stationed in Bombay, Pune, Calcutta, Hyderabad, Delhi

send thelr representative or place arders In the form of letter

accompanied by the &emend draft. mile procuring, they inepect

the pairs, and arrange to settle the full payment. Earlier, the

artisans used to the footwear and wait for weeks and

months together to receive the payments from the dealers. Rut due

LO the procurement centres started by KVIC and I.IIIKRR, tiip r.l,nln

trend has reversed and today the Production rlnlts t h e

payments before exec~ting the ordcvs. There are Instances t h a t

the wholesale dealers after paying the advances have to for

one o r two weeks far Procurement of f o o t w e a r ~ e c a u s ~ t h e

continuous orders Placed by the Charmalaya. LIDKAR and the

,utaide wholesale dealers, an the whole the lnfomal of

~thani have very few marketing problems. Whenever there has been

an increase in the raw material prices like bag tanned leathers,

the marketing centres also enhance the procurement prices of

the footwear by leaving sufficient margin to the workers.

1 .1 .2 KhRKET COST6

After procuring the footwear, the Charmalays arranges

for stamping its brand "CHARMALAYA" on each chappal. Depending

upon the orders they have from various Kbadi Cramodyog

Bhavans/Bandar. and the KVIC registered institutional retail

outlets, they assort the footwear designwise, sizewise, arranges

for colouring by dipping the footwear rn spindle oil and

transport the footwear to the respectrve addresses of the retail

outlets far which they receive the demand drafts as well as

subsequent orders. The Charmalaya adds around 20% aver its

procurement price in order to meet the expenditure an stamping

1 0 . 2 5 ) , oiling (1.00), packing ( 0 25) per pair and the transport.

costs including loading and unload~nq charges. Tire selling rates

of Charmalaya for different items of Kolhspuri chappals that vary

from design to design are shown in Annexure 3 . 2 of the Third

Chapter.

While LIDI(AR also operates more less on the .+ i m i l a r

lines of the Charnalaya, the wholesale dealcrs add more by o f

costs and include the interest on the advances

taxes and pass an the barden to the retailers and ultimately to

the consumers As a result the price of K O I I ~ ~ ~ ~ ~ ~ chappais in the

~ I C outlets are leas when compared to the retail prjceq i n the

footwear shops.

6 , 2 EXPORT8 OF XOLHAPURI FOOTWEAR

As mentioned earlier, the major production centres of

Kolhapuri chappals, ViZ. Athani, Nlppani, Madhubavi, Kalhapur and

Miraj and the surrounding villages I" Xarnataka and ~aharashtra

states produce around 41 lakh parrs per year valued at Rs 14.35

crores at an average procurement price of Rs.35 per pair. out of

41 lakh pairs produced by the informal sector of the footwear

units, 12.56 lakh pairs valued around Rs.203 millions have b w n

from Indla durlng 1991-92 as shown in Chart 1.2. A small

fraction of embraldered footwear is also included in this export

value. The export price of a pair of Kalhapuri chappal works out

to Rs.115/- per pair as against around R s 50/- I" the domestic

retall market. ~ h e s e exports are effected through the merchant

exporters stationed in omb bay. The Kalhapurl footwear is widely

accepted during the months of September. October, November in

countries llke USA.

~h~ marketing channels of Kolha~uri chappals

are depicted in the F l o w Chart 6.1.

3 AGE?+

6 , 3 . 1 MARKETING OF SHOE8

1t is avident from the d m g~vcll 11, ~ ~ b l ~ th,t r,,,i

~f the 45 household units covered under this study, 84s, o f tl,a,l

are ~upplylnq therr shoes to tlw cammisa~o~~ n g e n t q / w ~ , ~ ~ ~ ~ ~ l ~

traders stationed In the Hlng-kl-"sand1 market of R ~ ~ ~ , 11% o~

them directly supplied to the retailers of the nearby towns a,,d

5% to the government agencies like Bcs o r W ~ C O In the case of

household workshops, 75% of the units covered supply their shoes

to wholesale dealers in Hlng-ki-mandi market, 2 5 % to the

qovernnent procurement centres llke LRMCO, BCS and directly to

the retailers Whlle the household units are not regular in

getting orders from traders, the household workshops almost qet

orders regularly either from the traders or from the government

while issuing the orders, the traders specify the norms

like colour o f the leather, sizes and other product descriptions

and sccordingly the warkehaps effect the supplies. The household

unlts, lacking orders, are at the mercy of the traders in

bargaining the prlces and hence the 'Purcha System' has been in

force over the decades in Agra market.

1t is interesting to ohserve that the famous Rgra shoe

market is dominated by the wholesale dealers and mrddlenen in the

marketing of shoes. ~"rther, it was found that the institutional

agencies have not been developed ~n this market and their share

in the marketing of shoes is not that much significant. However,

in v i e w of the huge size the Agra market, the role af these

institutional agencjes is very meagre and they have not developed

to a very significant level. The poor performance of these

, n e t i ~ ~ i f l ' " ~ ' h a s been a g r e a t h a n d i c a p to tile a r t l s ans i l l

,.rketlng t h e shoes. As such, i t was found t h a t the i n f o r m a l

a r t i s a n s are n o t corlscious o f same of t l le d isadvantnqes

f o e them due t o t h e ineffective p e r f o r m a n c e o f t h e s e

i n s t l t u t i a n s .

The busy s c h e d u l e i n Hing-ki-mandl market s t a r t s from

3 . 0 0 PM and t r a n s a c t i o n s t a k e place upto 8 .30 PM d a i l y . on a n

average worklng day, t h e 350 wholesale t r a d e r s s t a t i o n e d i n t h i s

market procure around 3 . 0 0 l a k h p a i r s of shaes valued a t ~ s . 3 . 6 0

crorss and 0 . 3 0 lalih P a i r s of chappals valued a t Rs.9.on lakhs.

~ ~ c h d e a l e r p r o c u r e s s h o e s tram a minimum of 10 t o 12 s u p p l i e r s

( ~ h ~ l i y a w a l l a h s ) each c a r r y l n g around 7 2 p a i r s . The shaes

produced i n t h e whole week a re brought i n head loads c a l l e d

"Ohallyan" or by engaging rickshaws.

A f t e r procurement , t h e wholesale d e a l e r s a s s o r t t h e

shoe5 p u t t h e i r brand names, pack them i n boxcs and despatch t o

var ious r e t a i l e r s s t e t i o l i e d a l l over India . In t h e same way, t h e

BCS, a r e g l r t e r e d K V I C i n s t i t u t i o n and t h e LAMCO p l a c e orders to

the Workshops w i t h a l l specifications and procure t h e shoes a t

a l ready a g r e e d p r i c e s . A f t e r procurement they t r a n ~ p o r t t h e shoes

with t h e i r r e s p e c t i v e brand names t o var ious r e t a l l o u t l e t s . The

BCS s u p p l i e s t o XVIC r e g i s t e r e d r e t a i l o u t l e t s Khndi

Bhandars/shavans/charm Kuteers/Charma S h i l p a s and U M C O t o i t s

elnporias and t o t h e government departments

mta and carom having a l a r g e network of r e t a i l shops

i n t h e c o u n t r y a l s o plaoe orders with the illformal s e c t o r u n i t s

i n Agra. w h i l e issuing t h e o r d e r s , they s p e c i f y t h e raw m a t e r i a l s

to be used, colour, size and designs. After fabrlcatlon shoes

are inspected by their quality control ~ n ~ ~ ~ ~ t ~ ~ . and arra,,s. fo r

with their respective brand names.

6.1.2 MODE OF PAYMENT

It can be seen from Table 6.1 that 32% of the hm,+rhold

~nlts get the PaYmellt in terms of cash mereas 501 of tllem by

both cash and credit. In case of household workshops 2 2 %

effect their supplies On cah payment and 61% both cash and

oredit In Aqra, the 'Purcha System' prevailing in "ing-ki-mandi

market affect the the household units in selling their shoes. he

modus operandi is that at the tlme of supplying the shoes, the

manufacturer is issued with a credit slip for the value of the

suppl~ed. ~ h l s credit slip called "Purcha" has to he

submitted to the financier of the whole8ale dealer who pays the

amount after deducting 2 to 3 months lnterest at 2% on the total

vallie of the blll. That is, if Lire value of the shoes supplied is

Rs.l,ooO/- an Interest rate of 2% for 3 months that works out to

R5.60/- is deducted from the total amount of Rs.1,000/- alld

the remaining ~ ~ 9 4 0 only 1s p a l r l to the household

owner/supplier. As the manufacturer h a + to invest the sale

proceeds in purchasing raw materials and accessories for

continuing the production on the subsequent days, and to maintain

the camily they are bound to accept this kind of

reduced payment.. mr no fault ofthe hou3ehald owner, his margin

on the is curtailed due to the system o f involving

middlemen and the of "Purcha" system. Hence, the

prevai l ing operation Purcha system of payment in the Hing-ki-

~ a n d i shoe market Aqra clearly indicates the degree

by the informal footwear artlsans the

the middlemen v i z . the commissloil agents, W I I O I P S ~ ~ ~ dealcrl iil,d

the unauthorlsed flnanclers.

In case o f workshops enplayinq hired ti,.

,holesale dealers place orders wlth I,teilxcd rat... ,,,,#I

accordingly the Procurements are eflected. ?he price ttte

shoes produced in workshops always rule higher than those mnde in

the household units. Knowing fully well, that the traders reduce

the r ~ t e s of the shoes supplied by the housetlnld units, they

resort to purchase low quallty raw materials and fabricate tile

shoes in accordance with the rates offered to them. 1n this case,

except labour, the margin per pair 1s very meagre to the

household units. Various marketing channels operatinq far shoes

produced j n Agra are depicted In Flow chart (,..'.The dominant role

of the wholesale traders of Hing-XI-Mandl has adversely affected

the hausehold artisans. The poor performance of institutional

agencies ~n marketing of shoes emphasises the need to develop

same institutional agency which wlll reduce the role of wholesale

traders. This requires several pallcy measures and urgent action

to serve the household workers in the lnformal sector.

the case of BCS and Charma Kuteer (started in 1991)

o f KVIC, after procurement the payment is paid in cash uPto

RS Z,OOO/- and in the form of cheque if the amount exceed* more

than R~.~,ooo/-. ~h~ w c o C s payments are delved and not regular

and the artisans have to wait for one or two weeks.

worksbops that undertake orders for production and

supply to sata, caronas Liberty shoes etc. receive payments after

two t o t h r e e months. Thlf a c t o f delayed paynents ranginq from

two t o t h r e e nonth4 by t h e country's leading cs tahl ished tVn,iels

like ' B a t e ' and 'Carona' c l e a r l y e x i r i b l t t h e d e g r n e o f

e x p l o i t a t i o n w h i l e Procuring t h e shoes from t h e i n f o m a l sector

footwear u n i t s i n Agra. However, t h e s e u n i t s y e t cnnt~nuouc

o r d e r s f r o m t h e n a s long a s t h e y a d h e r e t o t h e q l l n ~ i t y

a n d s p e c i f i c a t i o n s g i v e n . The B L C and t h e u n i t s

making i n d u s t r i a l s h o e s g e t t h e orders from t h e government

.gencies l i k e Deience or P u b l i c Linl ted Undertakings and e f f e c t

the supplies. BLC l n s l s t s a d v a n c e s f o r t h e i n d u s t r i a l s h o e s

whereas t h e p r l v a t e u n i t s supply a g a i n s t g u o t a t l o n s .

6 . 3 . 3 KIRKETING C06TS

The w h o l e s a l e d e a l e r s , government agencies l i k e BCS,

Charmakuteer, LAMCO and t h e leading shoe companies of ~ a t s and

CarOna h a v e t o m e e t t h e m a r k e t c o s t s i n v o l v e d i n p a c k i n g ,

t r a n s p o r t a t i o n , l o a d i n g and unlaadlny charges a p a r t from meet ing

the C e n t r a l S a l e s Tax of 4 % and s t a t e S a l e s Tax of 6% t h a t are

o p e r ~ t l n g i n t h e d o m e s t i c n a r k e t . I n t h e case of shoes produced

in workshops employing more than 40 workers and using 2 H P power,

an e x c i s e d u t y af 10% is l e v i e d on t h e value of t h e s h o e s .

However, i n t h e r e c e n t budget , t h e levy of e x o i s e duty is l i m i t e d

t o footwear costing more t h a n Rs.120 per p a i r and hence t h e

e a r l i e r norm o f l i m i t i n g t o workers and power has been waived o f f

6.4 EXPORT OF FULL SHOES

R~ has a l r e a d y heen mentioned i n Chapter 111, t h a t o u t

of R9.11252 worth of footwear and footwear oomponents

exported tram l n d i a d u r i n g 1991-92, t h e f u l l shoes and open

footwear constitute ~ ~ . 4 , 2 5 4 n i l l i o n s and t h e remaining

~ ~ . 6 . 9 4 8 m l l l l o n s are through shoe upper and components. I t i s

i n t e r e s t i ng t o "OtP here t h a t a l l tile shoo oppers t h a t are

,xported a r e made from t h e mechaniaed and seni-mechnnired

whereas a l l t h e f u l l shoes are made both in the formal

and informal s e c t o r u n i t s . I t i s estimated t h a t out of the t o t a l

t u rnove r of 108 mi l l l an p a i r s valued a t 115.12,960 m i l l i o n s

i n ag ra , a lmost R s . 1 , 9 4 4 mi l l i ons worth of shoes are exported by

the wholesale d e a l e r s of Xing-ki-mandi market e i t h e r through

direct e x p o r t or through the merchant exporters s t a t i oned i n

bay and o e l h i . Most of t he se shoes are made ~n t he ~ n f a r r n ~ l

,ectar of t h e shoe u n i t s i n Agra and t h e rest of t he shoes

from I n d i a are made i n t he semi-mechanlsed or m r r l i a n i s ~ d

sector sp read rn Agra and Tamilnadu wherein again t he inform~l

o f t h e l abour play a v r t a l r o l e as piece r a t e workel-s Tor

l abou r l n t e n s l v e operat lone For instance, t he country 's

l e ad i l i g e x p o r t e r i n Lad ie s B e l l a r i n a s v i r . "TEJOMALS" p l a c r

orde r s to semi-meclianised workshops i n Agra each employlnq

around 2 0 rrarkers.

1.5 mDms

In Madras, 5 5 % of t h e household u n l t s c o n t a c t e d

d i r ec t ly s e l l t h e i r mixed l ea the r footwear t o t he r e t a i l e r s v i z .

the platform shops l oca t ed i n busy carnmerclal places i n t he c i t y

and 35% t o t h e r e t a l l d e a l e r s o f the Parry's market and 10% only

supply t o TALC0 ( ~ ~ b l e 6 . 1 ) . 1n the case of household workshops

also, 4 7 % supp ly to platform shops, 2 9 % t o r e t a i l dea l e r s and

the remaining 24% t o t h e TALCO. I n Madras cen t r e , the middlemen

i n t he market cha ln are mrninised and manufacturers themselves

d i r e c t l y sell t h e footvear t o t h e r e t a i l e r s catering to

~ a d r R s c i t y . Thus , i n Madras mixed l e a t h e r footwear markek q,lnws

the d i s t i n c t i o n of reducing t h e middlemen to tiie minimum lev+,l

" i th l o w e s t c o n t r o l over t h e Producers , rspecla l ly houc.nl,oid

~ " ~ t s . T h u s , t h e n a t u r e o f demanri TOT C I I ( . + ~ Pl.OdUCtE 4 m R F l y

c o n t r i b u t e d €Or t h e d e v e l a ~ m e n t o f a i p e c z a l malket,ng C1,al,llP,

in t h e i n f o r m a l sector o f Madras c i t y .

6.5.1 MODE OF PAYMENT

Most of t h e footwear manufacturers i n ~ a d r a ~

t h e i r f o o t w e a r against o r d e r s p l a c e d by t h e p l a t f o r m shops

located i n P a r r y s . ' P r l p l l c a n e , T.Nagar, Mylapore, Purasawalkam

areas. The f i e l d r e s u l t s show t h a t 46% of t h e m a n u f a c t u r e r s

t h e i r f o o t w e a r a g a i n s t c a s h , 14% both by cash and c r e d i t

and t h e remaining 2 2 % on c r e d i t . I n t h e case of h o u s e h o l d

workshope a b o u t 3 3 % of t h e u n l t s g e t cash and equal number o f

u n i t s s u p p l y on c r e d i t as w e l l a s both on cash and c r e d l t . At t h e

time of s u p p l y 5 0 1 o f t h e value of t h e footwear s u p p l i e d i s p a i d

t o t h e a r t i s a n s and t h e r e s t i n equal i n s t a l m e n t s w i t h i n a week's

t i n e . ~t RE been o b s e r v e d t h a t t h e shop owners always keep an

o u t s t a n d i n g b a l a n c e of RS.~OQ/- due t o t h e a r t i s a n s , wi th an

a p p r e h e n s i o n t o h a v e assured s u p p l y iron them. Whenever t h e

a r t i s a n s r e c e i v e a d v a n c e s from t h e shop owners, t h e supply p r i c e

i s a lways be l e s s by Re.11- p e r p a i r compared t o t h e r u l i n g

p r i c e . j u s t l i k e i n Agra, t h i s a g a i n forms a c l e a r c u t example

of e x p l o i t a t i o n of t h e informal footwear u n i t s i n t h e hands of

the r e t a i l e r s .

To sum up, it can be oencluded t h a t t h e middlemen In

the market chain ~ i . . t h e comnrsslan a g e n t s and t h e wholeeale

dealers operating l n accordance wlth the ,Purc l ,a System. jn.

,,ntloned earlier) in Hing-ki-Mandi shoe o f Agra, p,ns , ,,,y sisniflcant and vital role it1 erplolting the producers nf

the informal sector. Further, inordinate delay in payment. from

the leading traders 1Ike 'Beta' and 'Carann' and even flom tile

~~vernment agency called ' W I C O ' Indicates a clear example of

exploitation In marketing of shoes. Finally, partial

settlement o f bills by the Pavement shops/retailers in ~ndras

,ity resulted in mast exploitation of the informal producers.

wnce, it can be lnferred that the middlemen in the market chain

play a mast vital role r n explalt~ng the informal sector artisans

while marketrng the footwear in Aqra and Madrae centres.

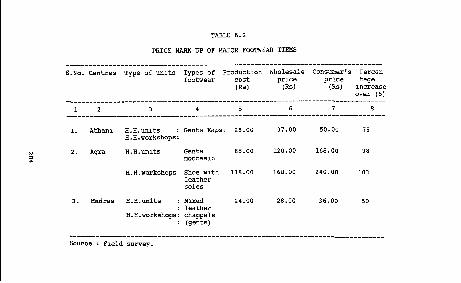

6 . 6 PRICE MIIRK-UP

an account of involvement of commlsrion agents,

wholesale dealers I " the main markets and then the outside

wholesale dealers ~n the respective states/major towns, and the

retail shop owners, the prices of footwear are increased from its

supplying level by the time ~t reaches the consumers. This price

mark-up is due to packing costs, transport casts,

laading/unloading charges, taxes prevailing in the market,

establishment charges at eve ry stage like sleutriclty,

gadaun/shop rents and the individual's Profit f o r t h e amount

invested in the business.

T~ study this price mark-up, the fast moving

xapsi type footwear made in Athanl, all leather moccasin shoe

made i n and the mixed leather gent's chappal made in Madras

are considered for their prices at different level of

PRICE MARK UP OF MAJOR FOOTWEAR ITEMS

S.No. Centres Type of unlts Types of Product~an Wholesale Consumer's Percen footwear cost prlce prlce tage

1x5) (Rs) (Rs) lncrease over (5)

1. Athanl H.H.unrts : Gents Xapsl 28.00 37.00 50.00 79 H.H.vorkshops:

N 7. hgra H.H.unlts Gents 55.00 120.00 168.00 98 rn noccas1n

H . H . ~ ~ ~ k ~ h ~ p s Shoe wlth 118.00 160.00 740.00 103 leather soles

3. Madras H.H.units : Mired 24.00 28.00 36.00 50 : leather

H.H.wor!csho~s: ChaDDals

Source : Fzeld surrey.

~t can be seen from the data given i n Table 6 z that In case of

shoes made I n Agra, ii marketed through ~ i ~ ~ - k ~ - ~ ~ ~ ~ i i ,

fallowed by outside wholesale dealers and then to retailers, itlp

price increment by the time lt reaches the ultimate

be around 100% over the cost of production. 1f the cast of

production of a pair of shoes in the household workshops works

,,t at ~s.lla/- by the time it reaches the ultimate cansunier in

any town in South India, works out to Rs.210/- for the same pair.

I" the same way, the price mark-up in case of Kalhapuri (Kapsij

chappals works out to 79%. Although the production cost in Athani

is R6.28/- per pair, the consumer In Madras has to pay ns.50/-

f o r the same pair. In Madras oentre, the price mark up is not

~ig~lficant because of the mlnlmum role oC mrddlemen in the

chain. In most cases, the producers directly sell their

footwear to the retailers, in which case the price mark up

including the profit of the producer and the retailer goes only

to the extent of 501. Thus, the presence of middlemen greatly

influence the price mark up and these agents at times influence

the price mark up to the tune of 100% mostly In Agra followed by

Athsnl.

6.7 DEUNIND FOR FOOTWEAR

The demand far footwear bath in domestlc and

international market depends on a host of factors like climirtlc

conditions, income levels of the consumers, fashlan changes and

dresslng habits and awareness of iiearing footwear to protect

their fcrt. per wplta consunptlon of leather footwear of 0.5

pairs in zndie is expected to grow I n future, due to the

improvement in the standard of livlng, lnoome levels, dress

consciousness and fashion changes . I t i s l n t e r e s t i l i g to note t h a t

.bout 60 t o 10% of t h e l e a t h e r produced i n t h e world goes towards

the manufacture of foot*-ear. In o t h e r words, footwear industry is

the s i n g l e l a r g e s t consumer of f i n i s h e d l e a t h e r produced in t h e

and a l s o i n India. Although i n I n d i a , l e a t h e r producks l i k e

g a r m e n t s , t r a v e l g o o d s , handbags a r e made t h e y a re m a i n l y

intended f o r e x p o r t s .

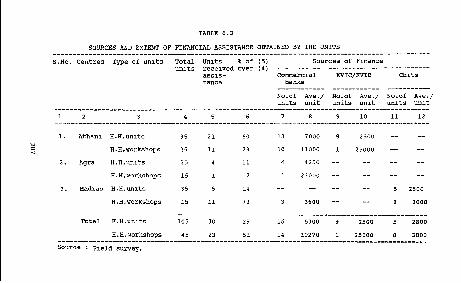

6.8 FINANCIAL A8818TANCE OBTAINED BY THE UNITS

Although v a r i o u s developmental o r g a n i s a t i o n s c la imed

that t h e y had a s s i s t e d t h e household e n t e r p r i s e s f i n a n c i a l l y ,

the f l e l d survey r e s u l t s shown i n Table 6.3 r e v e a l s a d ismal

p i c t u r e . Only ln t h e case o f Athanl c e n t r e , 60% of t h e household

uni ts and 73% of t h e household workshops have a v a i l e d f i n a n c i a l

assistance e i t h e r t h r o u g h l o c a l commercial banks or througli SC/ST

c o r p o r a t i o n s and KVIB. At t h e lns t i ince of t h e Kvrc " ~ h a r r n a l a y a " ,

the commercial banks and t h e IWIB of Karnataka i n Athani came

forward and p r o v l d e d on an average Rs.? ,oao/- and Rs.2,500/-

r e s p e c t i v e l y per household u n ~ t t h a t has a u a l l e d t h e a s s i s t a n c e .

Whereas i n t h e case of household workshops t h e cammerclal banks

have p r o v i d e d an amount of ~s.11,000/- p e r u n l t and t h e K V I B

Rb.25,000. 1t h a s been r e p o r t e d by t h e banks t h a t repayment

schedule from t h e u l r i t ~ is almost regular and t h e r e are c e r t a l n

i l l s tances where t h e units have taken loans f o r mare than t w o o r

three t i m e s .

I,, A ~ ~ ~ , 11% O E t h e household u n i t s and 7% o f t h e

workshops have a v a i l e d t h e f i n a n c l s l a s s i s t a n c e from t h e

commercial b a n k s .

TABLE 6.3

SOURCES AND EXTENT OF FINANCIAL ASSISTANCE OBTAINED BY THE UNITS -------------------.---.-.-------.--------------------------------------.----------------------- ~.NO. Centres Type of units Total Units % of (51 sources of finance

units recelve& over ( 4 ) ---.----..-----.--------.--------------

a5515- Commercxal KVIc/KvIB Chlts tance banks ------------ ------------ -----------

No.of Ave./ N O . ~ ave./ No.of Ave./ unlts unit units unlt unlts unlt

--------.-------------------------------------------------------- Total H.H.unlts 105 30 29 16 6300 9 2500 5 2800

In Madras city, the sources finance f o r the fnatwenr

,,its are the conventional chit that are i n

However, the interest for this amount exhorbitant lo

the bank interest. The evils of the system are too well known to

be repfated here. Hence, t.hr.r~ I,. nn urql.nt n r l ~ c ~ ti, I,,, , proper

institutional support for these units.

6 . 8 . 1 DISTRIBUTION OF UNITS RCCORDING TO PIXED C ~ P I T ~ L

The distribution of small enterprises according to the

value of their fixed assets Obned (Table 6.4) reveals that 52%

of the household unlts in Athani, each owned less than ~s.l,ooo/-

worth of tools and irrplements, whereas the remaining 48% ha".

equipments each worth ranging Rs 1.000 to R S . ~ , O O O by way o f

possessing the seulng machines. In the case o f household

W O T ~ S ~ O ~ S . 66% of the unlts have each a fixed capital of less

than R8.5.000 and the remaining 31% have more than Rs.5,Oon. l'he

above analysis clearly indicate that the small enterprises ill

hthani mostly depend an hand operations l n tbe fabrlcatioll of

~ ~ l h ~ ~ ~ r i footwear with an exception of utrl~sing only the sewlng

nachlnes and hence have less flxed capital The correlation

coefficient (0.43) worked out between the production of footwear

and the fixed capital among the household units of ~thani and the

test procedure callowed to know the extent of significance reveal

that there is relationship between ~roductjan of

footwear and the flaed capital r n these units. Similarly with a

correlation coefficient of 0.11 between the production and fixed

capital, there exists significant relationship between them among

the household workshops of Athani centre^

In Agra. 10% o f the llousehold have each than

R, ~,ooo/- worth of fixed capital. 40% of the ,,,,it.

r u e d assets ranging from Rs.1,Ouo to RS.B,OOO In tile of

household workshops, about 45% of the units each fixed

assets worth more than Rs.15.000/- mainly beoaiise of having

indigenous machinery such as swing, pasting compresior. .phe

correlation coefficients worked out t o stlldy the relat~on~hip

between shoe production and flxed capital in both types of units

in ngra Indicate that there is no significant relationship

between the productIan of shoes and Iixed capital. ~ h l a can bp

explained that some unlts although do not passes. n e c e s s a r y

machines they depend on other job work units for such maciline

operations. As has been nentloned earlier, thls centre has surtl

strong linkages among different types of units.

In Madras, 67% o f the household anits ilave very l o w

fixed assets of less than Rs.1,000/- each, 2 3 % have a c s a t a

ranging from ~s.1.000 to 5,000 and only 10% of the unlts hold

each ~s.5.000 to 10,000 worth of assets. With a correlation

coeffic~ent of 0.9 between the p~aductlan a n d flxed capital in

household units and 0.7 in household workshops of Madras centre.

there exists significant relationship betweell the production and

fixed capital. the production unlts in Madras involve in mined

leather footwear, introduction of small improved tools, sewing

and buffing machines make a blg differrence ~n them volume of

production. It can be deduced that the hausehold units in all the

centres hold less f ixed capital compared to the household

workshops which are fairly blg due to the introduction Of

indigenous machines.

6 . 8 . 2 DISTRIBUTION OF UNITS ACCORDIND TO WORKINO CnPTTnl,

The amount o f warking c a p ~ t a l t h e holds i t -

~ a p a c i t y to t u r n I t over on i t s bnsrnes;, p lays % " i t e l roip <,, , , i n t a m i n g t h e m a n u f a c t u r i n g a c t i v r t y w , t h o u t any g , rp or

~ l a c k n e s i The t u r n aver of working c a p i t a l by t h e ,,nibr. i s

weekly o r d a i l y depending on t h e node O L narket i l lq 71,.

dsta on d i s t r i b u t i o n of u n i t s according t o t h e range of workilll

,.pita1 i n v e s t e d on t h e i r b u s i n e s s i s shown ~n vabie 6.5. ~t war

found t h a t a b o u t 90% of t h e household u n i t s and 41% of t h e

household wnrkahops In A t h a n i have l l n l t e d r o C a t ~ o r i of ~ s . 5 . 0 0 0

each as worklng c a p i t a l t o w a r d s purchase of raw materials. 1n t h e

case of h o u s e h o l d workshops . 24% had working c a p i t a l ranginq from

Rs.5.000 t o 1 5 , 0 0 0 , 19% between Ra.15.000 and 20,000 and 10% had

a maxirnllm working c a p i t a l of more than Rs.D0,000 each. wi th a

c o e r e r l a t l o n c o e f f l c l e n t of 0 . 8 7 between t h e p r o d u c t i o n o f

footwear and t h e worklng c a p i t a l among t h e household u n i t s and

0.86 i n case of household workshops i n Athani c e n t r e , t h e r e

e u s t s v e r y s i g n i f i c a n t r e l a t i o n s h i p b e t v e e n p r o d u c t i o n a n d

working c a p i t a l i n b o t h c a t e g o r i e s of t h e u n i t s . It

may be n o t e d t h a t t h e market ing suppor t provided by Charmalaya

~ n d LIDmR h a v e g r e a t l y c o n t r i b u t e d for t h e effective t u r n o v e r of

working capi tal weekly among t h e s e u n i t s . Hence, it can be

concluded t h a t e f f e c t i v e turnover of working c a p i t a l has a s t r o n g

bearlng on t h e and r e g u l a r i t y of product ion ill Athani

centre .

As the footwear ",,its in Agra are specia l i -d i n shoe

f a b r i c a t i o n , t h e i r t u r n o v e r of working c a p i t a l on t h e raw

nater ia la /accessor ies is t h a n t h e o t h e r two centres. About

PERCENTAGE DISTRIBUTION OF UNITS ACCORDING TO WORKING CAPITAL

S.No. Centres Type of unlts Range of working capltal (Rs.) ................................................................ < 5000 5001 10001 15001 20001 25001 30000 Total

to to to to to and 10000 15000 20000 25000 30000 above

1. Athanl H.H.unlts

H.H.workshops w

2. Ama H.H.unrts

H.B.warkshops

3. Madras H.H.unlts

B.H.irorksbops

Total H.H.unlts

A.H.~ork~hops

------------------------------------.-----------..----..-.-----.---.--------~-----------.---.--- St urce : Pleld survey.

45% of the household units in Agra had a capital mn,,

than n s . 3 0 , 0 0 0 each I n contrast t o n 4 a of the llou?chold wn,~.-~,nl,..

having the working capital in tho range oc ns .n .30 I~Y.I,. t o

R s . z , 5 n lakhs. The correlatron corificjrnts and the test r f

~ignliicance procedures followed ~n relation t o <,r

.hoes and the working capital ln bath Ihousehold units and

household workshops of Agra indicate that there is no slgniflrant

relationship between the ProductIan and working capital in the-e

,,its. The operation of 'Purcha system' a.; has been mentioned

,arlier in the Hlng-ki-mandi market and tho delayed payments hy

the leading companies a £ 'Bata' and 'Carona' might be stroilg

reasons far ineffective turnover of working capital which has a

hearing I" the productron schedule among the shoe units in

Agra.

In Madras. 65% of the household unlts and 47% a€ the

household Workshops had a ?:orking capital of Rs.5,000 to 15,onn

each whereas 2 6 % o f the household workshops have a working

capital of more than Rs.30 ,000 each. The correlation coefficients

worked out and the procedure for testlng thelr significance

between the productron and working capltal among the two

categories of units reveal that there 1 s no significant

relationship between production and working capital among the

mlxed leather footwear production units in Madras. The system of

payments in instalment basis by the pavement sI>op owners has been

the major reason attributable for this phenomenon. The delayed

payments by the shop owners have a definite bearing on the

working capital turnover and thereby the production.

The w o r k i n g c a p i t a l r o t n t i a n amollg t h e

o f A t h a n i i s v e r y low because o f t h e weekly t,,rnovrr

and a s s u r e d m a r k e t i n g a s s r s t a n c e provided by charlnalaya (KVI(.I

and t h e a d v a n c e s o f f e r e d by t h e whalesale dealers .

( , g CONCLUSION

TO sum UP, t h e continuous assured marketlnq

p v i d e d by Charmalaya a g a i n s t almost cash t r a n s a c t i o n and I.IDKPIR

, g a i n s t ~ F G U B of cheques is g r e a t l y r e s p o n s i b l e i n r e l i e v l t l g t h e

a r t i s a n s o f h t h a n i c e n t r e from tlie e x p l o i t a t l a n o f middlemen i n

the market c h a i n . Such a system of markatmy a s s i s t a n c e i n i i t h a n i

has made t h e i n f o r m a l producers t o concentra te on t h e product ion

of footwear and t h e r e b y e a r n i n g higher incomes and r e g u l a r work.

r p o s i t i v e t r e n d of wholesale d e a l e r s p r o v i d r n g advances t o t h e

producers h a s s e t i n d u e t o t h e i n s t i t u t i o n a l marketing

i n t e r v e n t i o n s o p e r a t i n g i n Athalli

Al though such i n t e r r e n t i o n s e x i s t ID Aqra, they could

not make an inpact I" reducing t h e e n p l o i t a t l o r ~ ol middlemen.

s t i l l t h e i n i o r n l a l footwear u n l t s 1" Aqrs are being e x p l o i t e d by

the middlemen o p e r a t i n g i n t h e market chain r i g h t from Hing-ki-

nandi market u n t i l t h e y r e a c h t h e consumers The 'Purrha eystem'

of deducting t h e amount by way of i n t e r e s t on t h e value o[ t h e

#hoes s u p p l i e d a vital role i n reducing t h e p r o f i t margin

which is due to t h e small producers. Added t o t h i s , t h e delayed

payment by l e a d i n g companies of ' n a t a ' and 'Cerona' i s a l s o a

g r e a t h indrance f o r t h e informal u n i t s I n marketing ehaes in

Aqra.

The delayed payment I n t e r n s o r i n - t a l m e t l t r TII~I

r,duct~on 1" prices are same of t h n evils tllp i i r t i s d ~ , ~ far." i l l

t h e ~ a f l r a ~ centre. Hence, t o protect ti?^ artlqnns f r n t , t l lo

eyplDlration of mldZllemen In t h e market chain, a serira nf

, t r e o t ~ v e lnatltutional marketlaq Intervont~on. a- l l a i bnnn

experimented in Athani may be set up and popul' ir~sed among t i ) "

producers In the lnformal unlts of Agra and Madras.