Embed Size (px)

DESCRIPTION

Chapter Two. Determinants of Interest Rates. Interest Rate Fundamentals. Nominal interest rates - the interest rate actually observed in financial markets directly affect the value (price) of most securities traded in the market affect the relationship between spot and forward FX rates. - PowerPoint PPT Presentation

Citation preview

2-1McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Chapter TwoDeterminants of

Interest Rates

2-2McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Interest Rate Fundamentals

• Nominal interest rates - the interest rate actually observed in financial markets– directly affect the value (price) of most

securities traded in the market

– affect the relationship between spot and forward FX rates

• Nominal interest rates - the interest rate actually observed in financial markets– directly affect the value (price) of most

securities traded in the market

– affect the relationship between spot and forward FX rates

2-3McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Time Value of Money and Interest Rates

• Assumes the basic notion that a dollar received today is worth more than a dollar received at some future date

• Compound interest– interest earned on an investment is reinvested

• Simple interest– interest earned on an investment is not

reinvested

• Assumes the basic notion that a dollar received today is worth more than a dollar received at some future date

• Compound interest– interest earned on an investment is reinvested

• Simple interest– interest earned on an investment is not

reinvested

2-4McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Calculation of Simple Interest

Value = Principal + Interest (year 1) + Interest (year 2)

Example: $1,000 to invest for a period of two years at 12 percent

Value = $1,000 + $1,000(.12) + $1,000(.12)

= $1,000 + $1,000(.12)(2)

= $1,240

Value = Principal + Interest (year 1) + Interest (year 2)

Example: $1,000 to invest for a period of two years at 12 percent

Value = $1,000 + $1,000(.12) + $1,000(.12)

= $1,000 + $1,000(.12)(2)

= $1,240

2-5McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

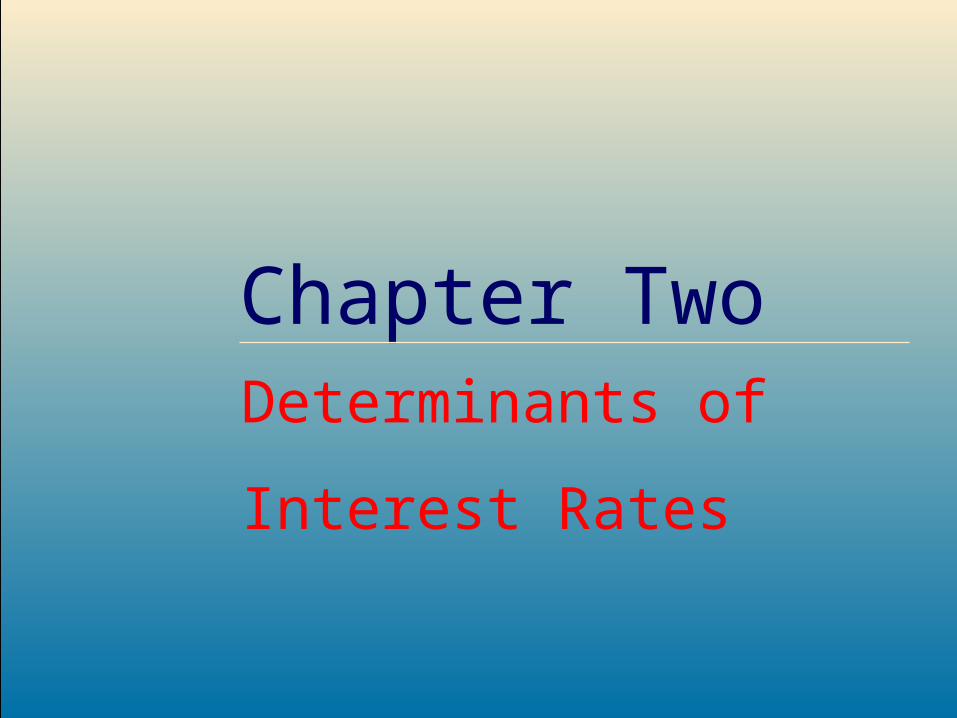

Value of Compound Interest

Value = Principal + Interest + Compounded interest

Value = $1,000 + $1,000(.12) + $1,000(.12) + $1,000(.12)

= $1,000[1 + 2(.12) + (.12)2]

= $1,000(1.12)2

= $1,254.40

Value = Principal + Interest + Compounded interest

Value = $1,000 + $1,000(.12) + $1,000(.12) + $1,000(.12)

= $1,000[1 + 2(.12) + (.12)2]

= $1,000(1.12)2

= $1,254.40

2-6McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Present Value of a Lump Sum

• PV function converts cash flows received over a future investment horizon into an equivalent (present) value by discounting future cash flows back to present using current market interest rate

– lump sum payment

– annuity

• PVs decrease as interest rates increase

• PV function converts cash flows received over a future investment horizon into an equivalent (present) value by discounting future cash flows back to present using current market interest rate

– lump sum payment

– annuity

• PVs decrease as interest rates increase

2-7McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

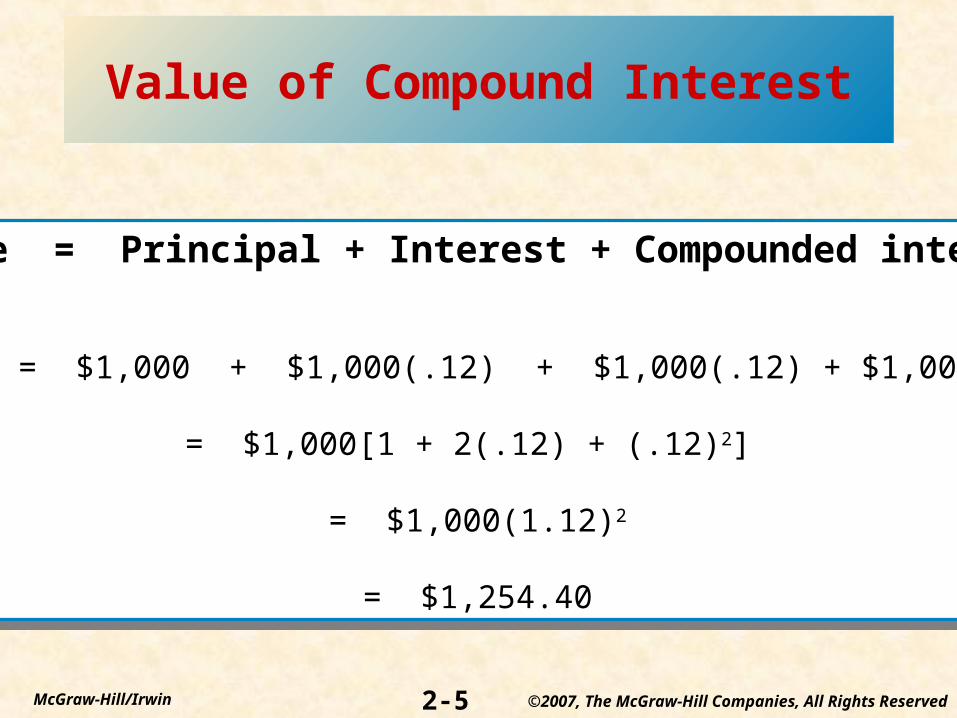

Calculating Present Value (PV) of a Lump Sum

PV = FVn(1/(1 + i/m))nm = FVn(PVIFi/m,nm)

where:PV = present valueFV = future value (lump sum) received in n years i = simple annual interest rate earned n = number of years in investment horizon m = number of compounding periods in a year

i/m = periodic rate earned on investments nm = total number of compounding periods PVIF = present value interest factor of a lump sum

PV = FVn(1/(1 + i/m))nm = FVn(PVIFi/m,nm)

where:PV = present valueFV = future value (lump sum) received in n years i = simple annual interest rate earned n = number of years in investment horizon m = number of compounding periods in a year

i/m = periodic rate earned on investments nm = total number of compounding periods PVIF = present value interest factor of a lump sum

2-8McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Calculating Present Value of a Lump Sum

• You are offered a security investment that pays $10,000 at the end of 6 years in exchange for a fixed payment today.

• PV = FV(PVIFi/m,nm)

• at 8% interest - = $10,000(0.630170) = $6,301.70

• at 12% interest - = $10,000(0.506631) = $5,066.31

• at 16% interest - = $10,000(0.410442) = $4,104.42

• You are offered a security investment that pays $10,000 at the end of 6 years in exchange for a fixed payment today.

• PV = FV(PVIFi/m,nm)

• at 8% interest - = $10,000(0.630170) = $6,301.70

• at 12% interest - = $10,000(0.506631) = $5,066.31

• at 16% interest - = $10,000(0.410442) = $4,104.42

2-9McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

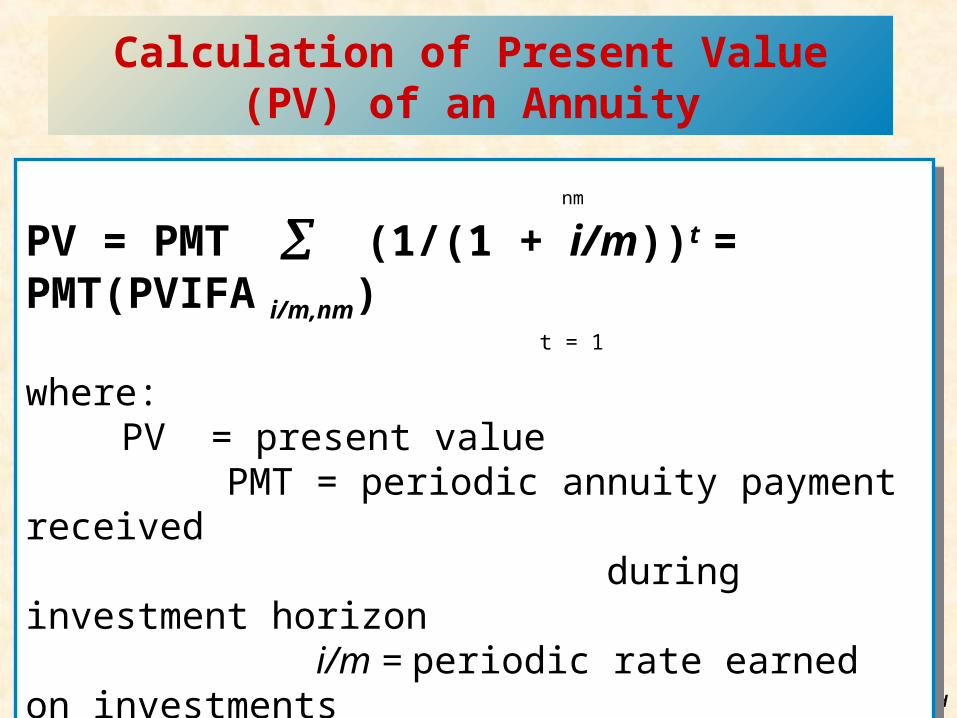

Calculation of Present Value (PV) of an Annuity

nm

PV = PMT (1/(1 + i/m))t = PMT(PVIFA i/m,nm)

t = 1

where:PV = present value

PMT = periodic annuity payment received during investment horizon i/m = periodic rate earned on investments nm = total number of compounding periods PVIFA = present value interest factor of an annuity

nm

PV = PMT (1/(1 + i/m))t = PMT(PVIFA i/m,nm)

t = 1

where:PV = present value

PMT = periodic annuity payment received during investment horizon i/m = periodic rate earned on investments nm = total number of compounding periods PVIFA = present value interest factor of an annuity

2-10McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

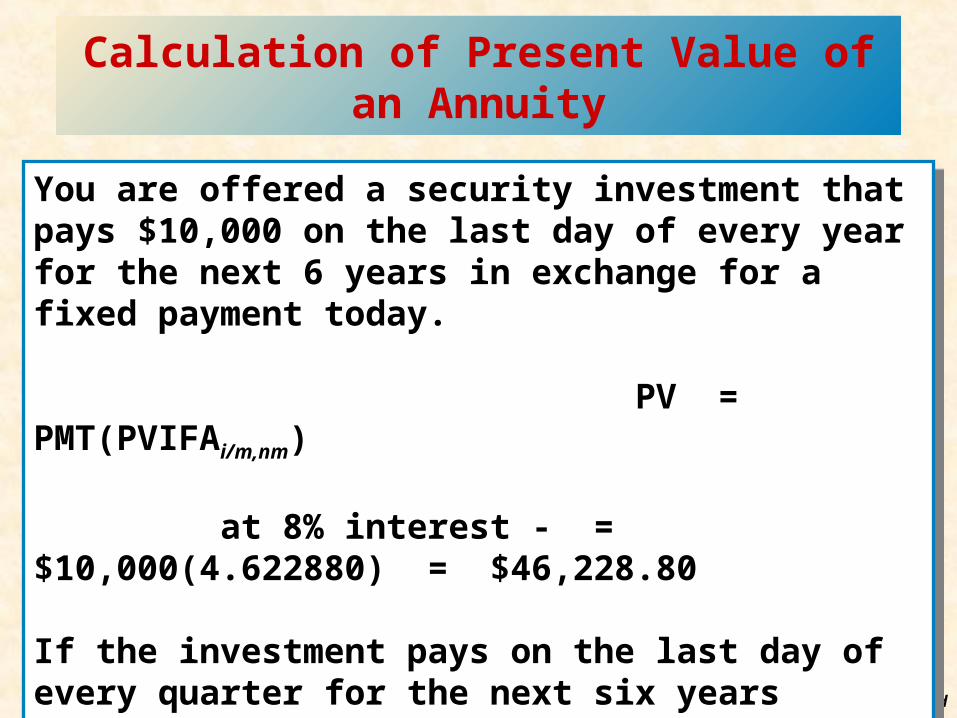

Calculation of Present Value of an Annuity

You are offered a security investment that pays $10,000 on the last day of every year for the next 6 years in exchange for a fixed payment today.

PV = PMT(PVIFAi/m,nm)

at 8% interest - = $10,000(4.622880) = $46,228.80

If the investment pays on the last day of every quarter for the next six years

at 8% interest - = $10,000(18.913926) = $189,139.26

You are offered a security investment that pays $10,000 on the last day of every year for the next 6 years in exchange for a fixed payment today.

PV = PMT(PVIFAi/m,nm)

at 8% interest - = $10,000(4.622880) = $46,228.80

If the investment pays on the last day of every quarter for the next six years

at 8% interest - = $10,000(18.913926) = $189,139.26

2-11McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Future Values

• Translate cash flows received during an investment period to a terminal (future) value at the end of an investment horizon

• FV increases with both the time horizon and the interest rate

• Translate cash flows received during an investment period to a terminal (future) value at the end of an investment horizon

• FV increases with both the time horizon and the interest rate

2-12McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Future Values Equations

FV of lump sum equation

FVn = PV(1 + i/m)nm = PV(FVIF i/m, nm)

FV of annuity payment equation

(nm-1)

FVn = PMT (1 + i/m)t = PMT(FVIFAi/m, mn) (t = 0)

FV of lump sum equation

FVn = PV(1 + i/m)nm = PV(FVIF i/m, nm)

FV of annuity payment equation

(nm-1)

FVn = PMT (1 + i/m)t = PMT(FVIFAi/m, mn) (t = 0)

2-13McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

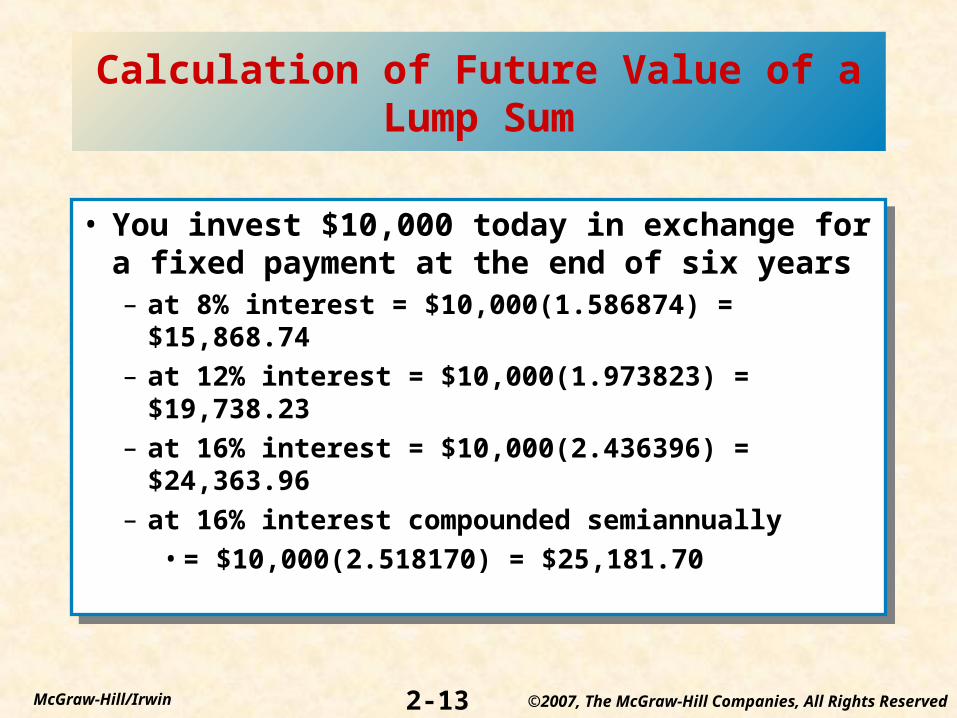

Calculation of Future Value of a Lump Sum

• You invest $10,000 today in exchange for a fixed payment at the end of six years– at 8% interest = $10,000(1.586874) = $15,868.74

– at 12% interest = $10,000(1.973823) = $19,738.23

– at 16% interest = $10,000(2.436396) = $24,363.96

– at 16% interest compounded semiannually

• = $10,000(2.518170) = $25,181.70

• You invest $10,000 today in exchange for a fixed payment at the end of six years– at 8% interest = $10,000(1.586874) = $15,868.74

– at 12% interest = $10,000(1.973823) = $19,738.23

– at 16% interest = $10,000(2.436396) = $24,363.96

– at 16% interest compounded semiannually

• = $10,000(2.518170) = $25,181.70

2-14McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

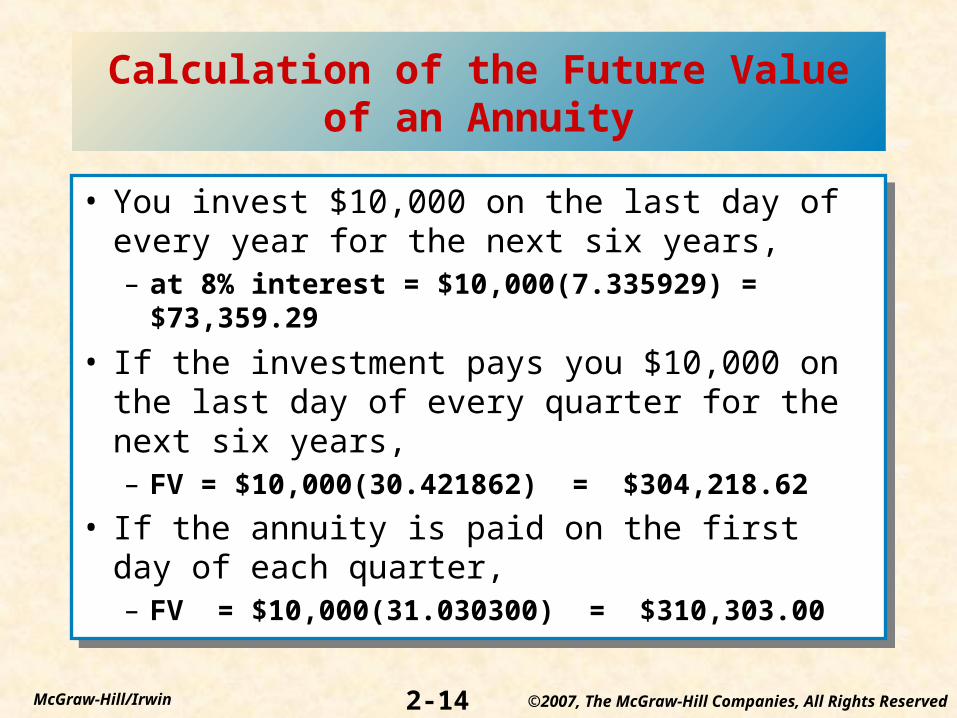

Calculation of the Future Value of an Annuity

• You invest $10,000 on the last day of every year for the next six years,– at 8% interest = $10,000(7.335929) = $73,359.29

• If the investment pays you $10,000 on the last day of every quarter for the next six years,– FV = $10,000(30.421862) = $304,218.62

• If the annuity is paid on the first day of each quarter, – FV = $10,000(31.030300) = $310,303.00

• You invest $10,000 on the last day of every year for the next six years,– at 8% interest = $10,000(7.335929) = $73,359.29

• If the investment pays you $10,000 on the last day of every quarter for the next six years,– FV = $10,000(30.421862) = $304,218.62

• If the annuity is paid on the first day of each quarter, – FV = $10,000(31.030300) = $310,303.00

2-15McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Relation between Interest Rates and Present and Future Values

Present Value(PV)

Interest Rate

FutureValue(FV)

Interest Rate

2-16McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Effective or Equivalent Annual Return (EAR)

Rate earned over a 12 – month period taking the compounding of interest into account.

EAR = (1 + r) c – 1

Where c = number of compounding periods per year

Rate earned over a 12 – month period taking the compounding of interest into account.

EAR = (1 + r) c – 1

Where c = number of compounding periods per year

2-17McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Loanable Funds Theory

• A theory of interest rate determination that views equilibrium interest rates in financial markets as a result of the supply and demand for loanable funds

• A theory of interest rate determination that views equilibrium interest rates in financial markets as a result of the supply and demand for loanable funds

2-18McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

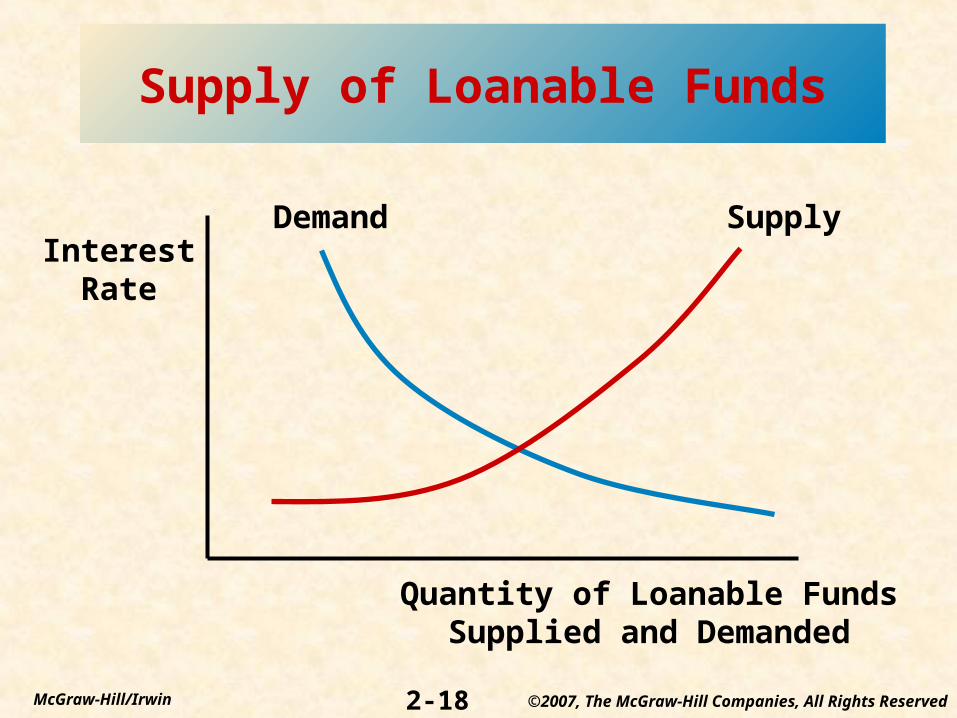

Supply of Loanable Funds

InterestRate

Quantity of Loanable FundsSupplied and Demanded

Demand Supply

2-19McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Funds Supplied and Demanded by Various Groups (in billions of dollars)

Funds Supplied Funds Demanded Net

Households $34,860.7 $15,197.4 $19,663.3Business - nonfinancial 12,679.2 30,779.2 -12,100.0Business - financial 31,547.9 45061.3 -13,513.4Government units 12,574.5 6,695.2 5,879.3Foreign participants 8,426.7 2,355.9 6,070.8

Funds Supplied Funds Demanded Net

Households $34,860.7 $15,197.4 $19,663.3Business - nonfinancial 12,679.2 30,779.2 -12,100.0Business - financial 31,547.9 45061.3 -13,513.4Government units 12,574.5 6,695.2 5,879.3Foreign participants 8,426.7 2,355.9 6,070.8

2-20McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

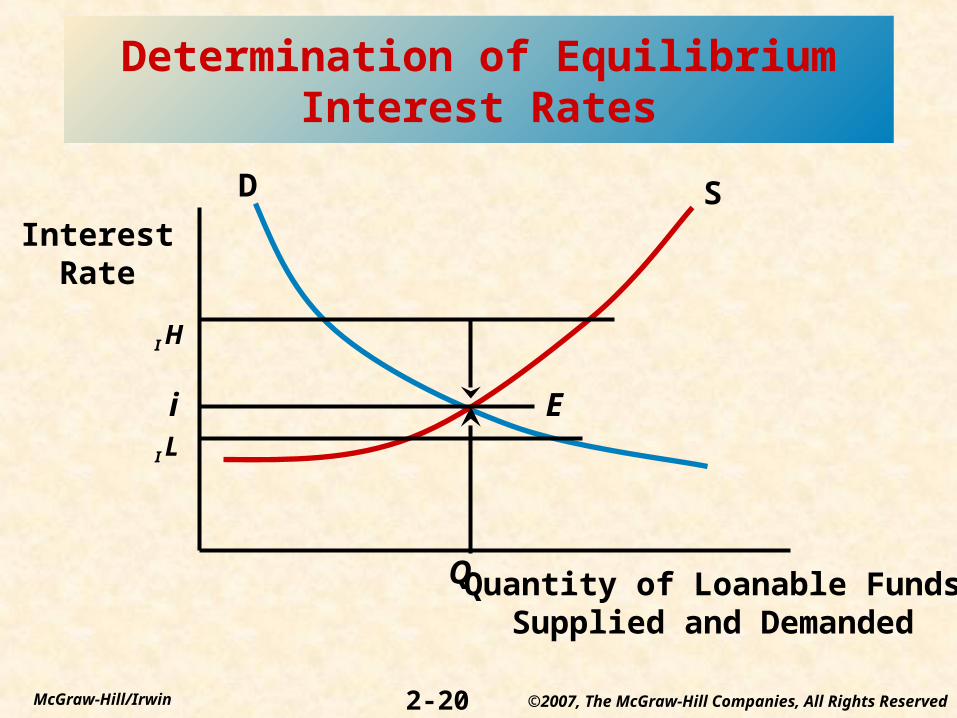

Determination of Equilibrium Interest Rates

InterestRate

Quantity of Loanable FundsSupplied and Demanded

D S

I H

i

I L

E

Q

2-21McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Effect on Interest rates from a Shift in the Demand Curve for or Supply curve of

Loanable FundsIncreased supply of loanable funds

Quantity ofFunds Supplied

InterestRate DD SS

SS*

EE*

Q*

i*

Q**

i**

Increased demand for loanable funds

Quantity of Funds Demanded

DDDD* SS

EE*

i*

i**

Q* Q**

2-22McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Factors Affecting Nominal Interest Rates

• Inflation

• Real Interest Rate

• Default Risk

• Liquidity Risk

• Special Provisions

• Term to Maturity

• Inflation

• Real Interest Rate

• Default Risk

• Liquidity Risk

• Special Provisions

• Term to Maturity

2-23McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

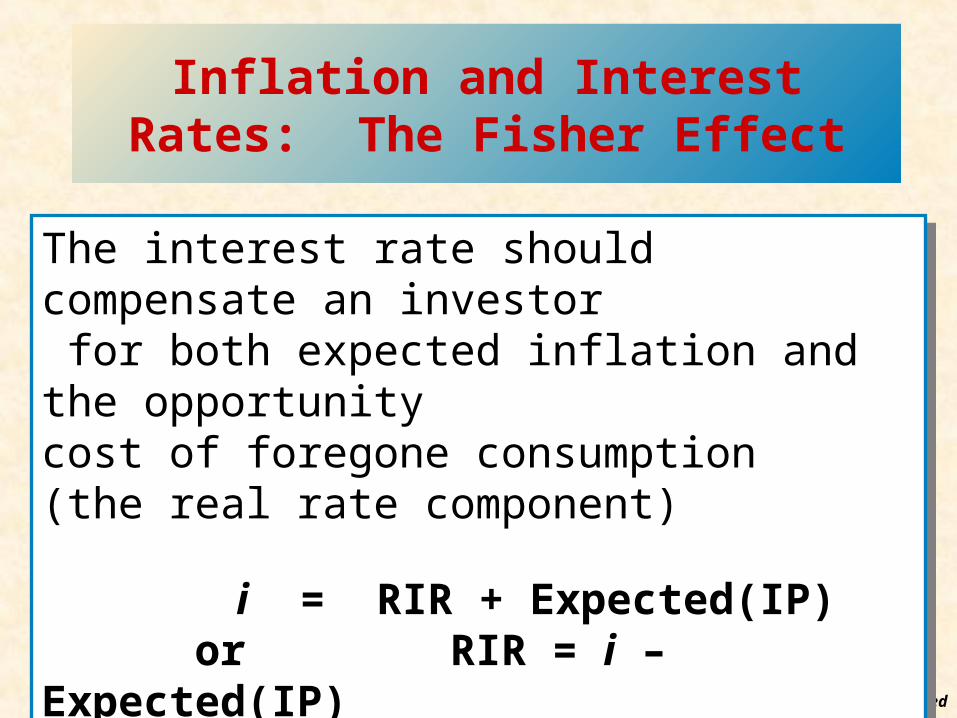

Inflation and Interest Rates: The Fisher Effect

The interest rate should compensate an investor for both expected inflation and the opportunity cost of foregone consumption (the real rate component)

i = RIR + Expected(IP) or RIR = i – Expected(IP)

Example: 3.49% - 1.60% = 1.89%

The interest rate should compensate an investor for both expected inflation and the opportunity cost of foregone consumption (the real rate component)

i = RIR + Expected(IP) or RIR = i – Expected(IP)

Example: 3.49% - 1.60% = 1.89%

2-24McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Default Risk and Interest Rates

The risk that a security’s issuer will default on that security by being late on or missing an interest or principal payment

DRPj = ijt - iTt

Example for December 2003: DRPAaa = 5.66% - 4.01% = 1.65%DRPBaa = 6.76% - 4.01% = 2.75%

The risk that a security’s issuer will default on that security by being late on or missing an interest or principal payment

DRPj = ijt - iTt

Example for December 2003: DRPAaa = 5.66% - 4.01% = 1.65%DRPBaa = 6.76% - 4.01% = 2.75%

2-25McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

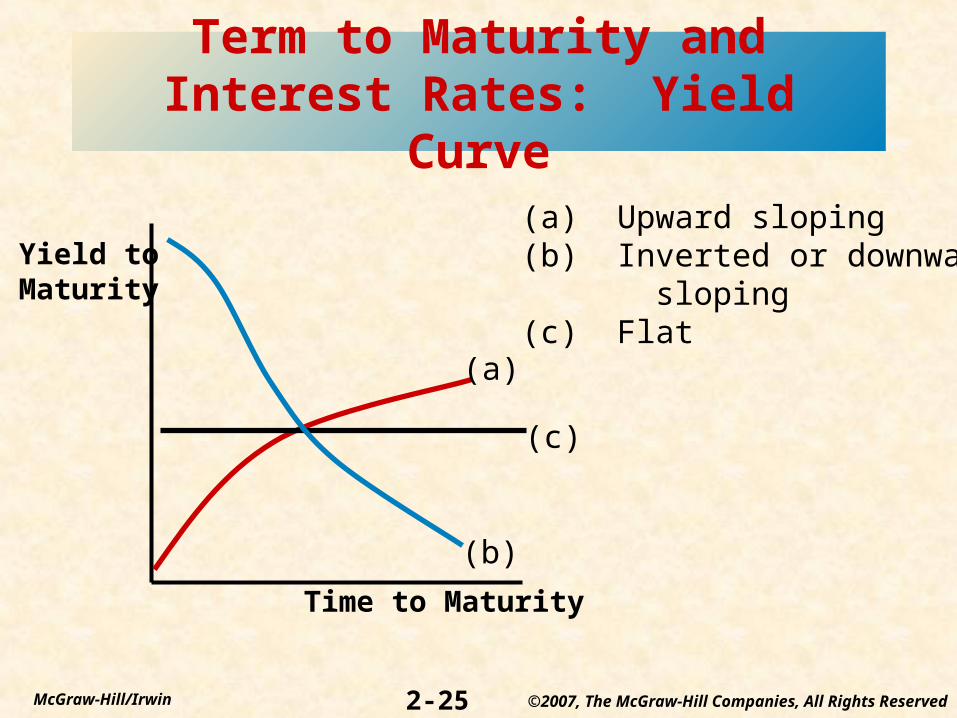

Term to Maturity and Interest Rates: Yield Curve

Yield toMaturity

Time to Maturity

(a)

(b)

(c)

(a) Upward sloping(b) Inverted or downward sloping(c) Flat

2-26McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Term Structure of Interest Rates

• Unbiased Expectations Theory

• Liquidity Premium Theory

• Market Segmentation Theory

• Unbiased Expectations Theory

• Liquidity Premium Theory

• Market Segmentation Theory

2-27McGraw-Hill/Irwin ©2007, The McGraw-Hill Companies, All Rights Reserved

Forecasting Interest Rates

Forward rate is an expected or “implied” rate on a security that is to be originated at some point in the future using the unbiased expectations theory _ _ 1R2 = [(1 + 1R1)(1 + (2f1))]1/2 - 1

where 2 f1 = expected one-year rate for year 2, or the implied forward one-year rate for next year

Forward rate is an expected or “implied” rate on a security that is to be originated at some point in the future using the unbiased expectations theory _ _ 1R2 = [(1 + 1R1)(1 + (2f1))]1/2 - 1

where 2 f1 = expected one-year rate for year 2, or the implied forward one-year rate for next year