Embed Size (px)

Citation preview

CHAPTER THIRTEEN

SPECIAL JOURNALS

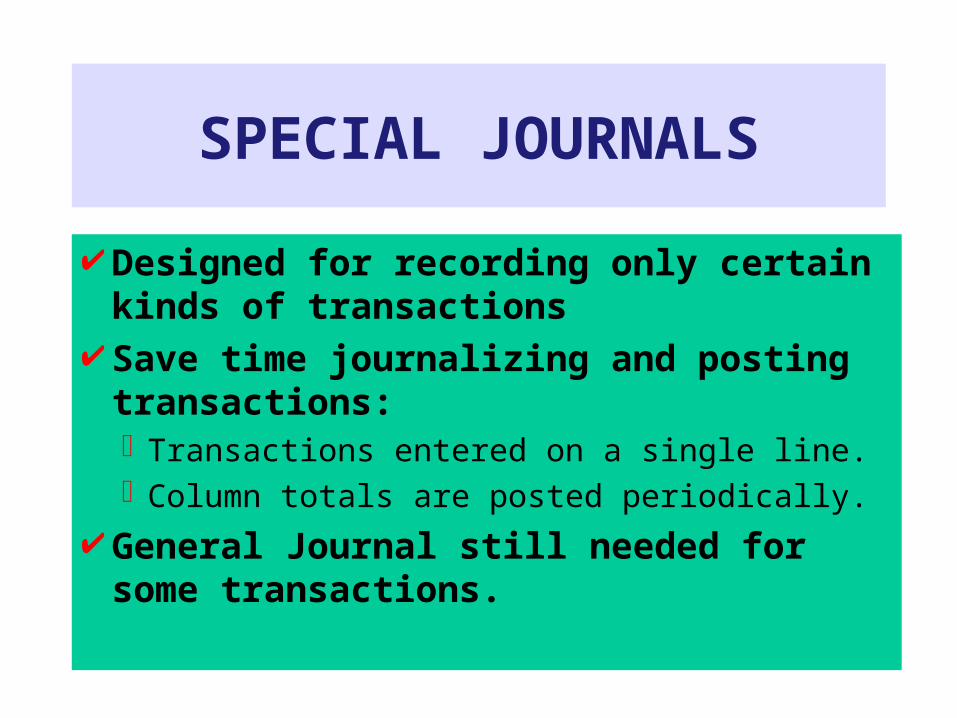

SPECIAL JOURNALS

Designed for recording only certain kinds of transactions

Save time journalizing and posting transactions:Transactions entered on a single line.Column totals are posted periodically.

General Journal still needed for some transactions.

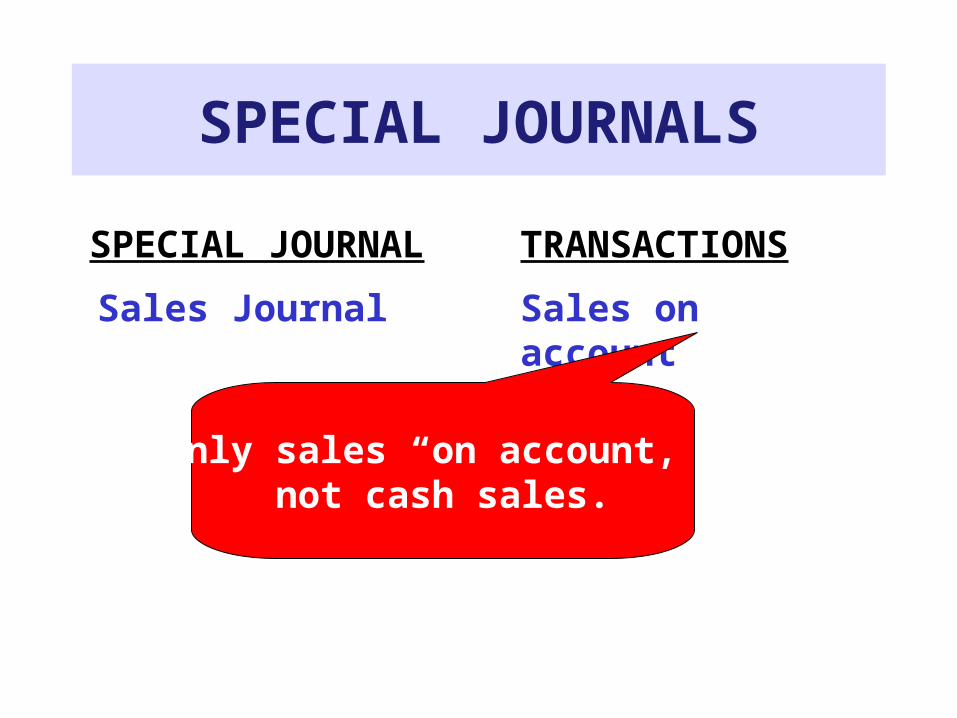

SPECIAL JOURNALS

SPECIAL JOURNAL TRANSACTIONS

Sales Journal Sales on account

Only sales “on account,” not cash sales.

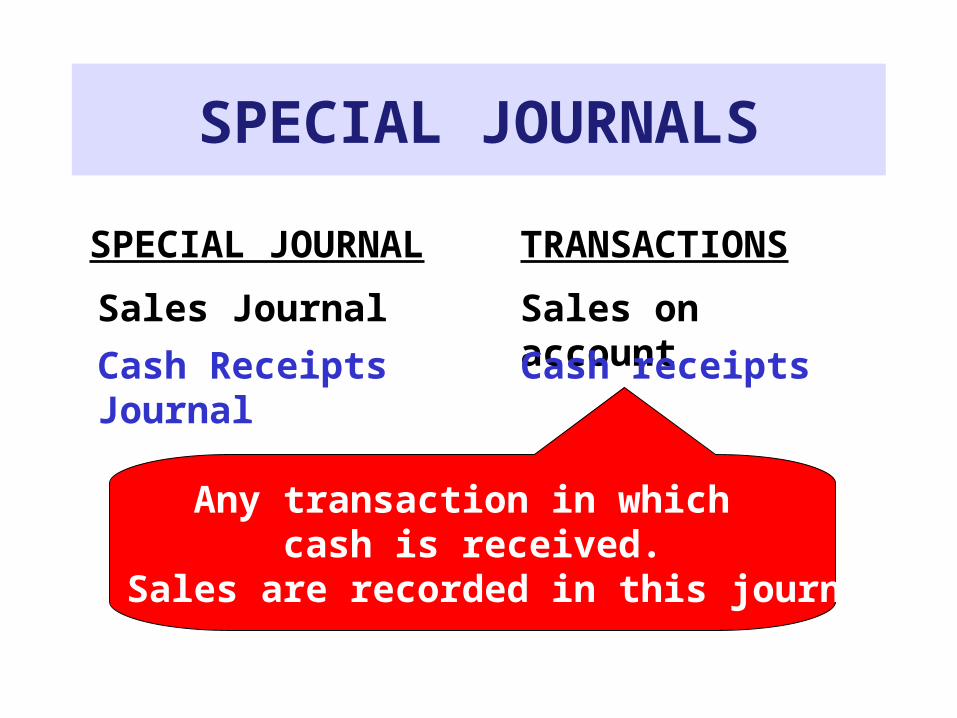

SPECIAL JOURNALS

SPECIAL JOURNAL TRANSACTIONS

Sales Journal Sales on account

Any transaction in which cash is received.

Cash Sales are recorded in this journal.

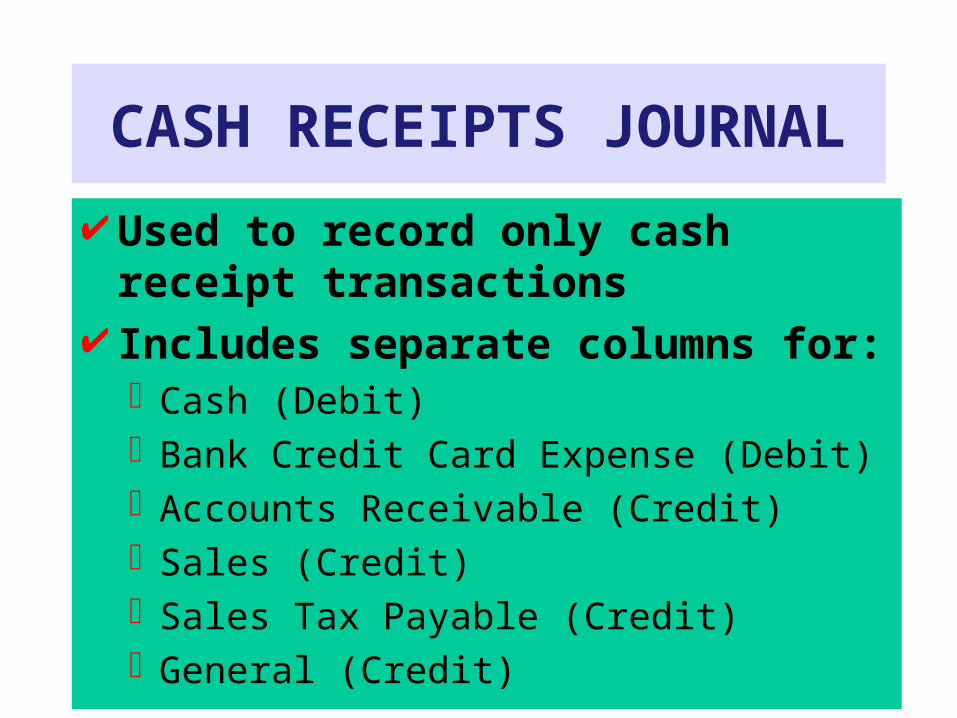

Cash Receipts Journal Cash receipts

SPECIAL JOURNALS

SPECIAL JOURNAL TRANSACTIONS

Sales Journal Sales on account

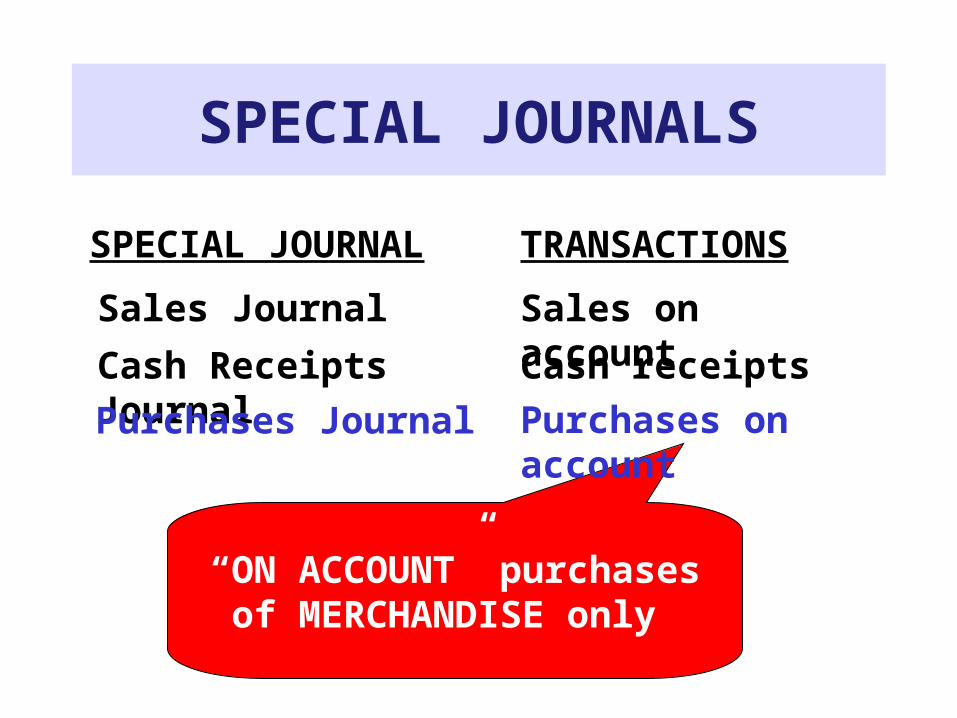

“ON ACCOUNT” purchasesof MERCHANDISE only

Cash Receipts Journal Cash receipts

Purchases Journal Purchases on account

SPECIAL JOURNALS

SPECIAL JOURNAL TRANSACTIONS

Sales Journal Sales on account

Cash Receipts Journal Cash receipts

Purchases Journal Purchases on account

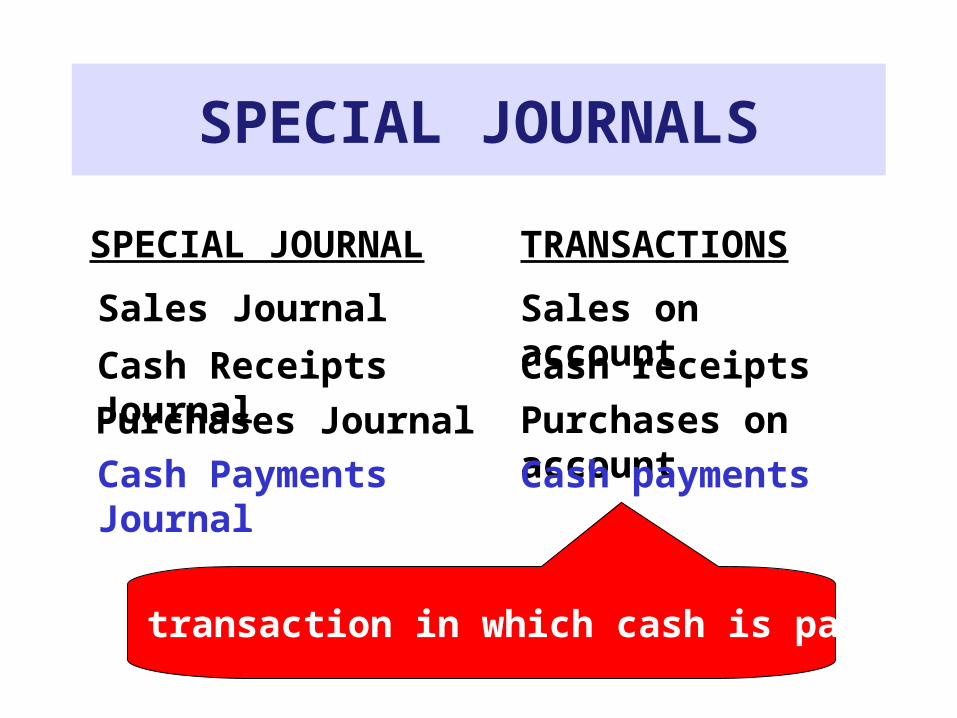

Cash Payments Journal Cash payments

Any transaction in which cash is paid.

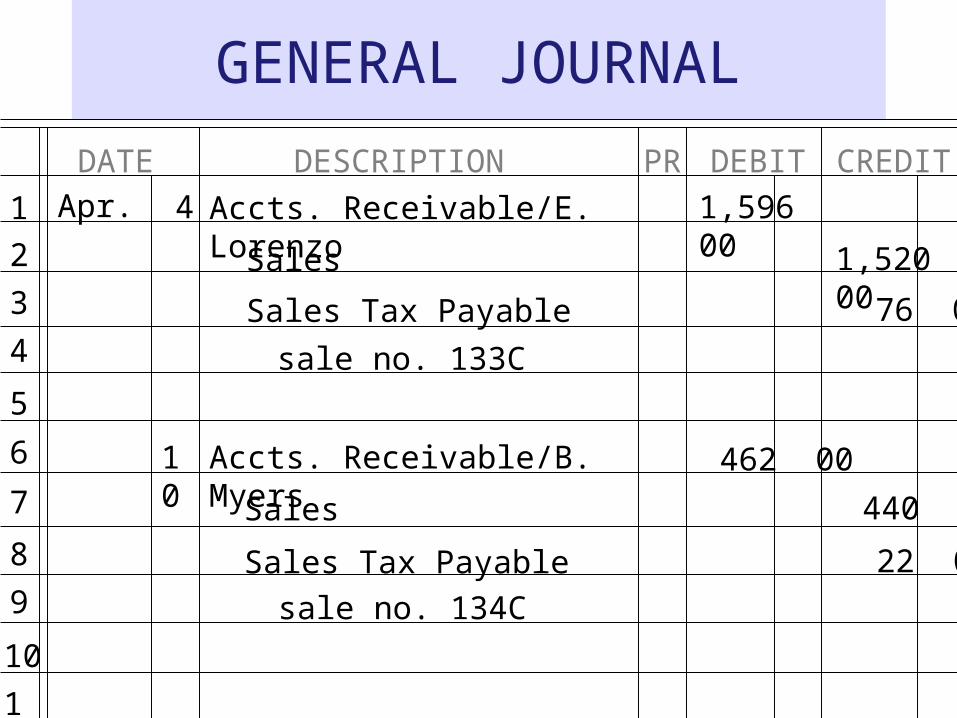

SALES TRANSACTIONS

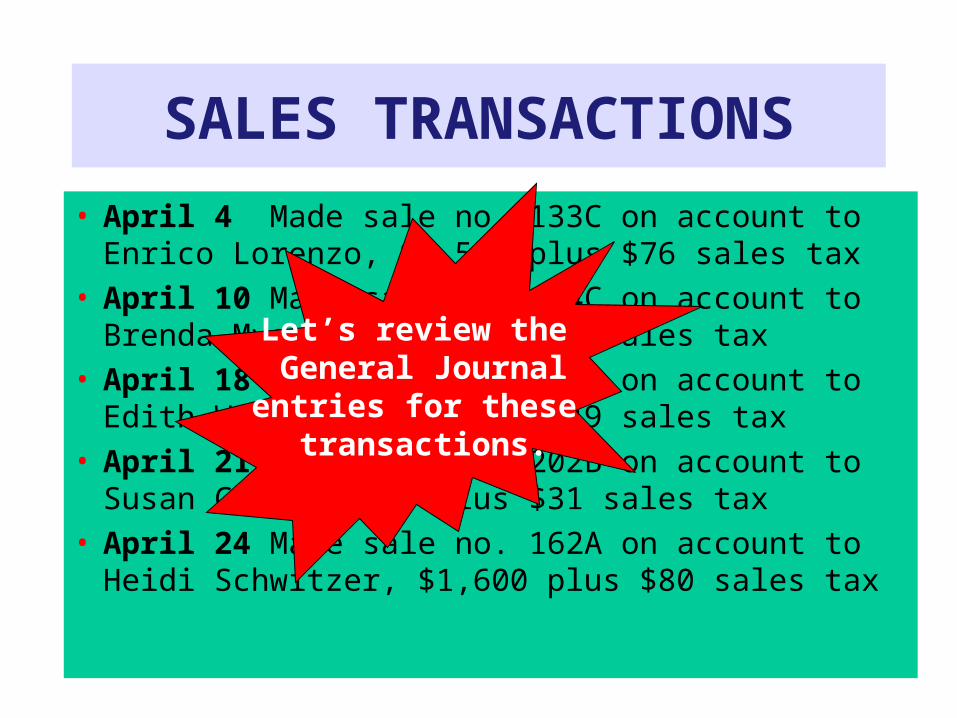

• April 4 Made sale no. 133C on account to Enrico Lorenzo, $1,520 plus $76 sales tax

• April 10 Made sale no. 134C on account to Brenda Myers, $40 plus $22 sales tax

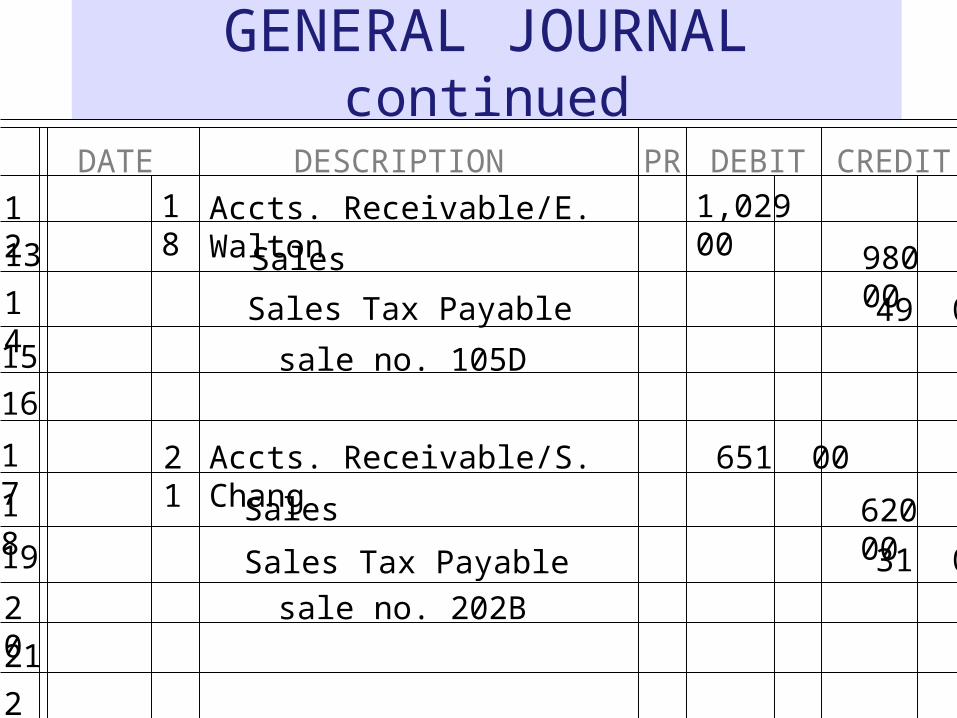

• April 18 Made sale no. 105D on account to Edith Walton, $980 plus $49 sales tax

• April 21 Made sale no. 202B on account to Susan Chang, $620 plus $31 sales tax

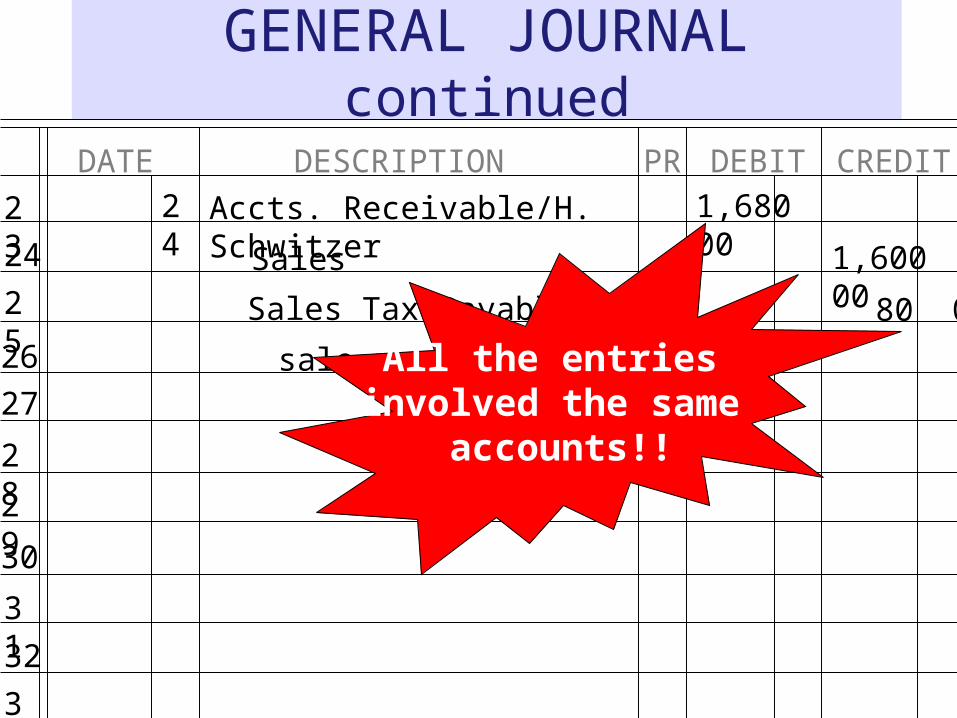

• April 24 Made sale no. 162A on account to Heidi Schwitzer, $1,600 plus $80 sales tax

Let’s review the General Journalentries for these

transactions.

GENERAL JOURNAL

DATE DESCRIPTION PR DEBIT CREDIT

1

2

3

4

5

6

7

8

9

10

11

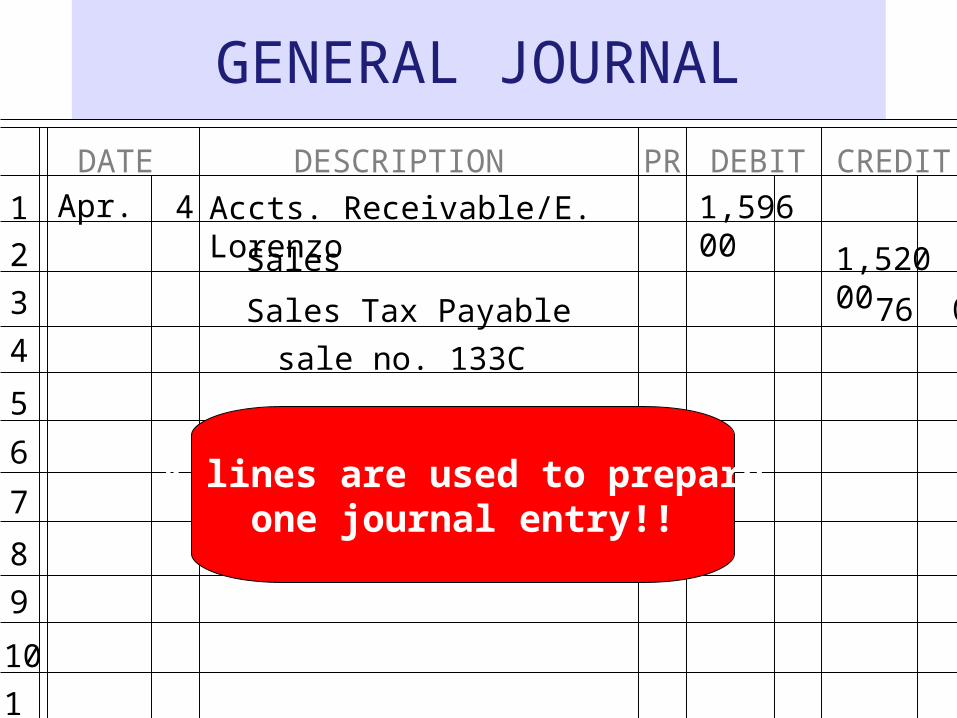

Apr. 4 Accts. Receivable/E. Lorenzo 1,596 00

Sales 1,520 00

Sales Tax Payable 76 00

sale no. 133C

4 lines are used to prepareone journal entry!!

GENERAL JOURNAL

DATE DESCRIPTION PR DEBIT CREDIT

1

2

3

4

5

6

7

8

9

10

11

Apr. 4 Accts. Receivable/E. Lorenzo 1,596 00

Sales 1,520 00

Sales Tax Payable 76 00

sale no. 133C

10 Accts. Receivable/B. Myers 462 00

440 00Sales

Sales Tax Payable

sale no. 134C

22 00

GENERAL JOURNAL continued

DATE DESCRIPTION PR DEBIT CREDIT

Accts. Receivable/E. Walton12

13

14

15

16

17

18

19

20

21

22

18

Sales

Sales Tax Payable

1,029 00

980 00

49 00

sale no. 105D

Accts. Receivable/S. Chang

Sales

Sales Tax Payable

sale no. 202B

651 00

620 00

31 00

21

GENERAL JOURNAL continued

DATE DESCRIPTION PR DEBIT CREDIT

Accts. Receivable/H. Schwitzer23

24

25

26

27

28

29

30

31

32

33

24

Sales

Sales Tax Payable

1,680 00

1,600 00

80 00

sale no. 162AAll the entries involved the same

accounts!!

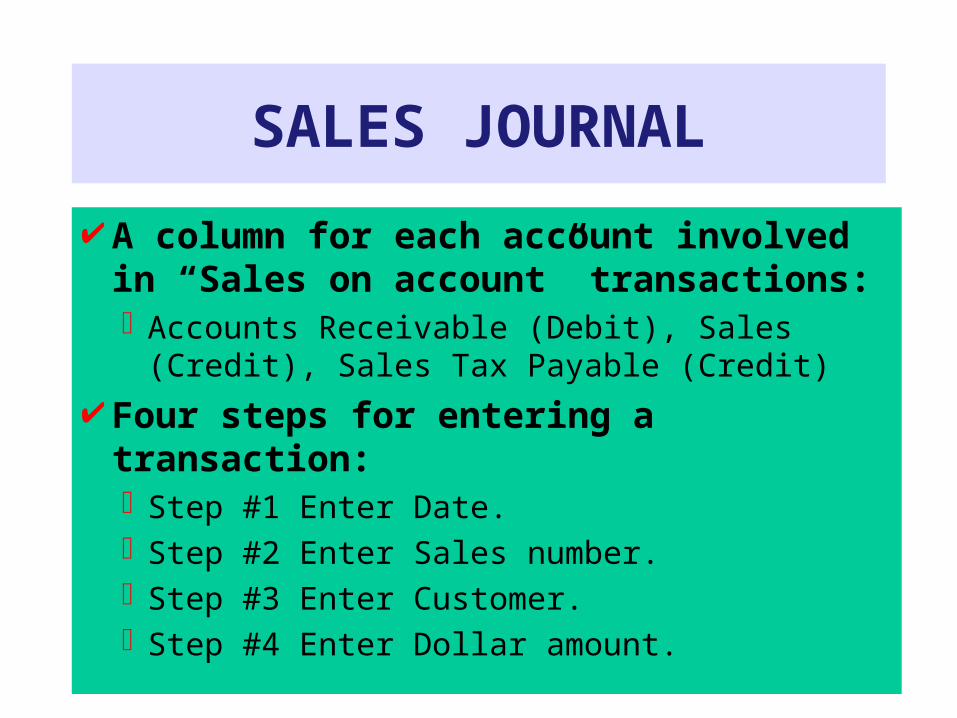

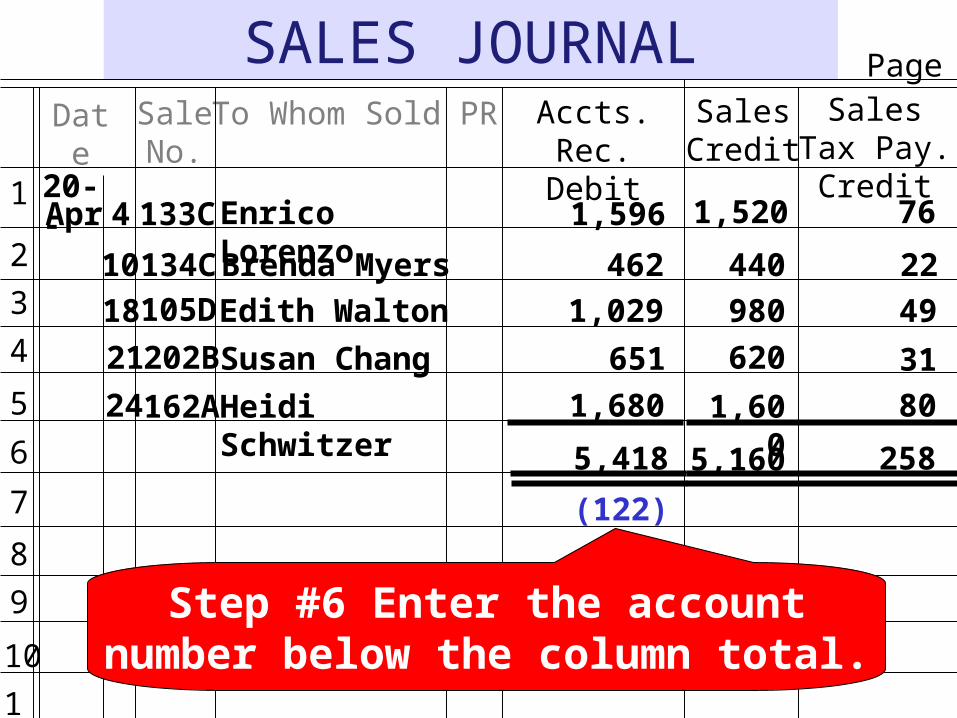

SALES JOURNAL

A column for each account involved in “Sales on account” transactions:Accounts Receivable (Debit), Sales (Credit),

Sales Tax Payable (Credit)

Four steps for entering a transaction:Step #1 Enter Date.Step #2 Enter Sales number.Step #3 Enter Customer.Step #4 Enter Dollar amount.

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

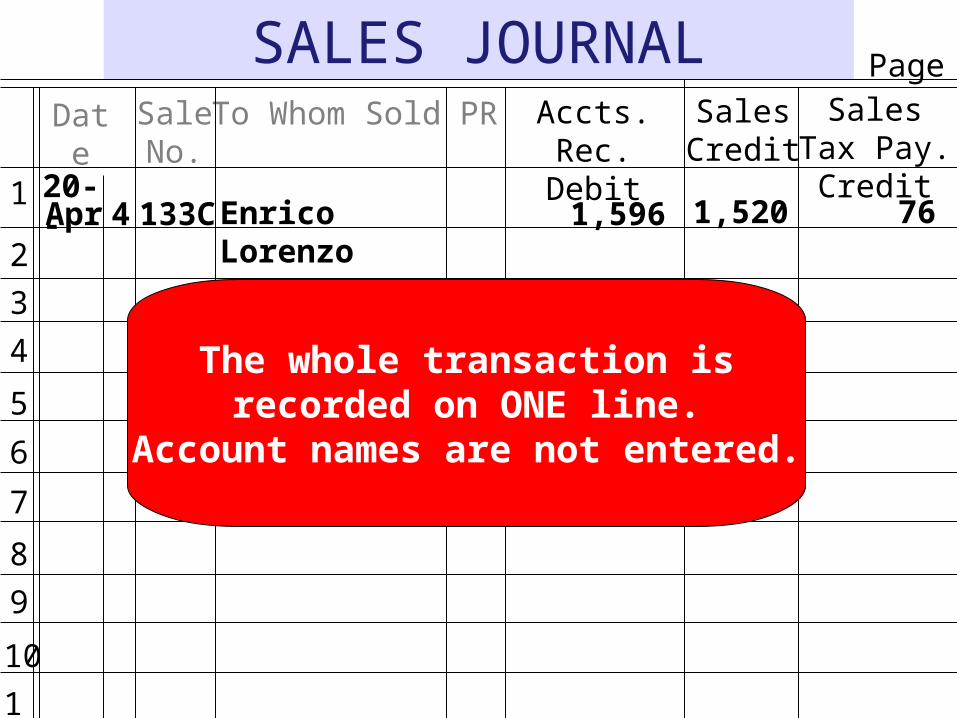

20--Apr 4 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 76

The whole transaction isrecorded on ONE line.

Account names are not entered.

Page 6

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

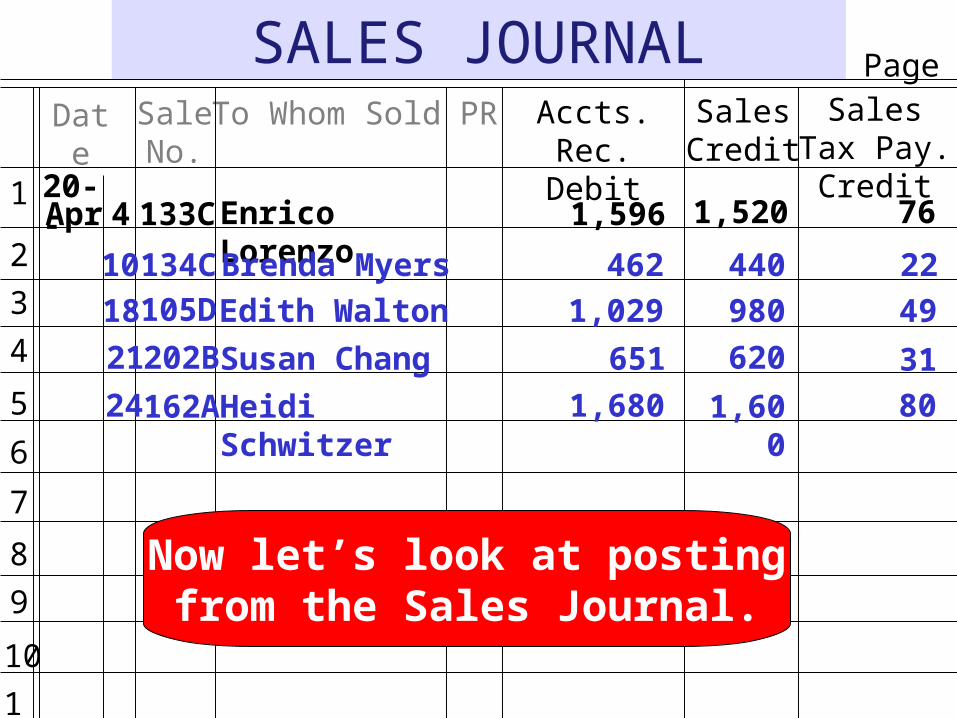

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

Now let’s look at posting from the Sales Journal.

Page 6

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

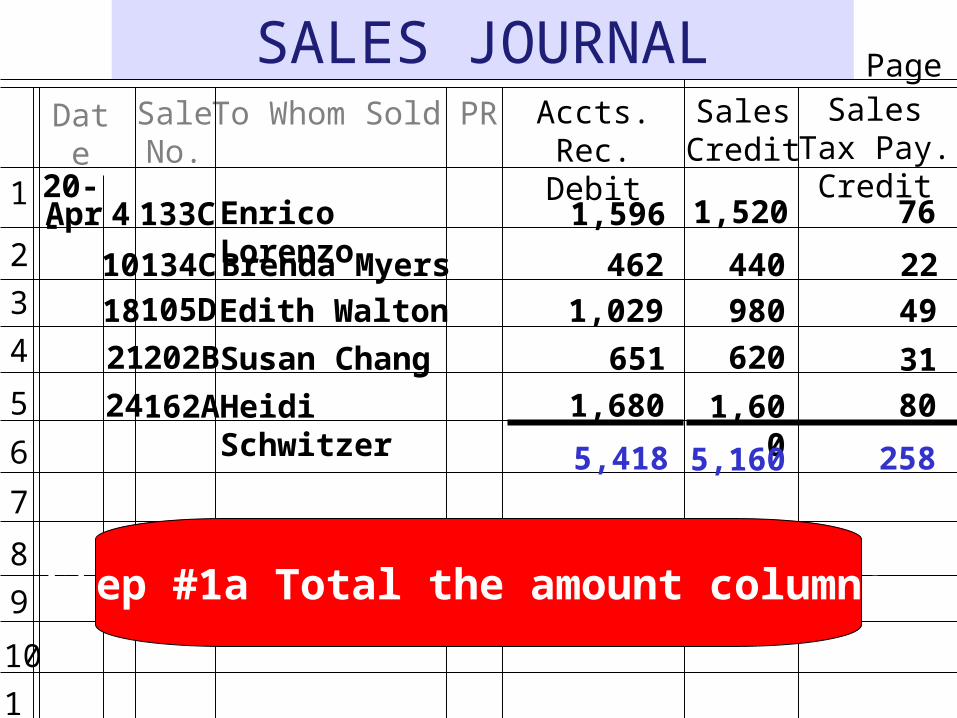

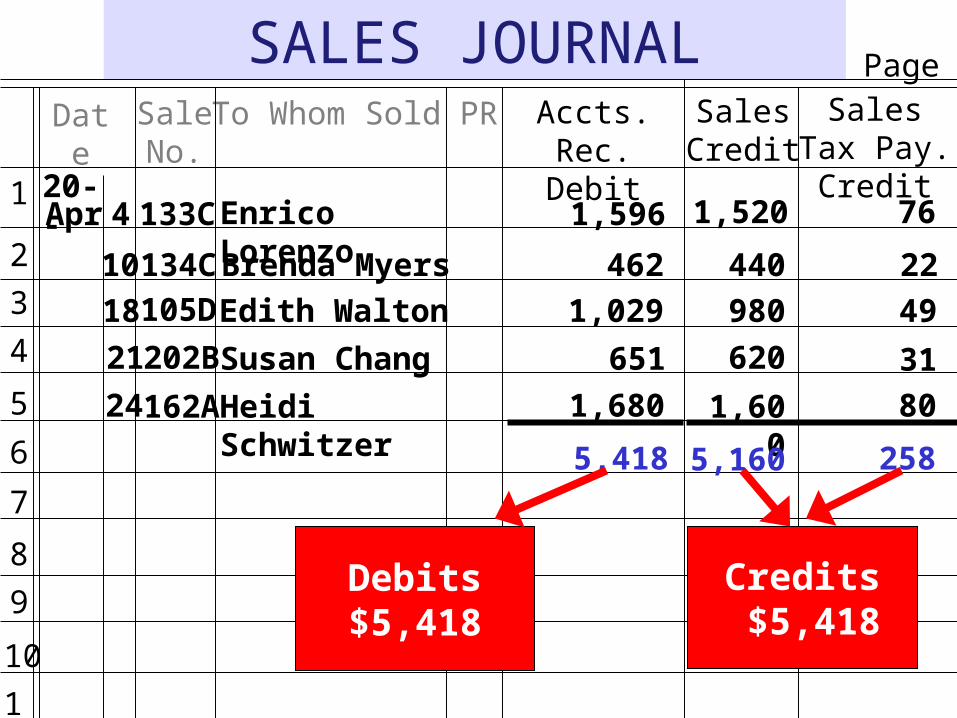

Step #1a Total the amount columns.

5,418 5,160 258

Page 6

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

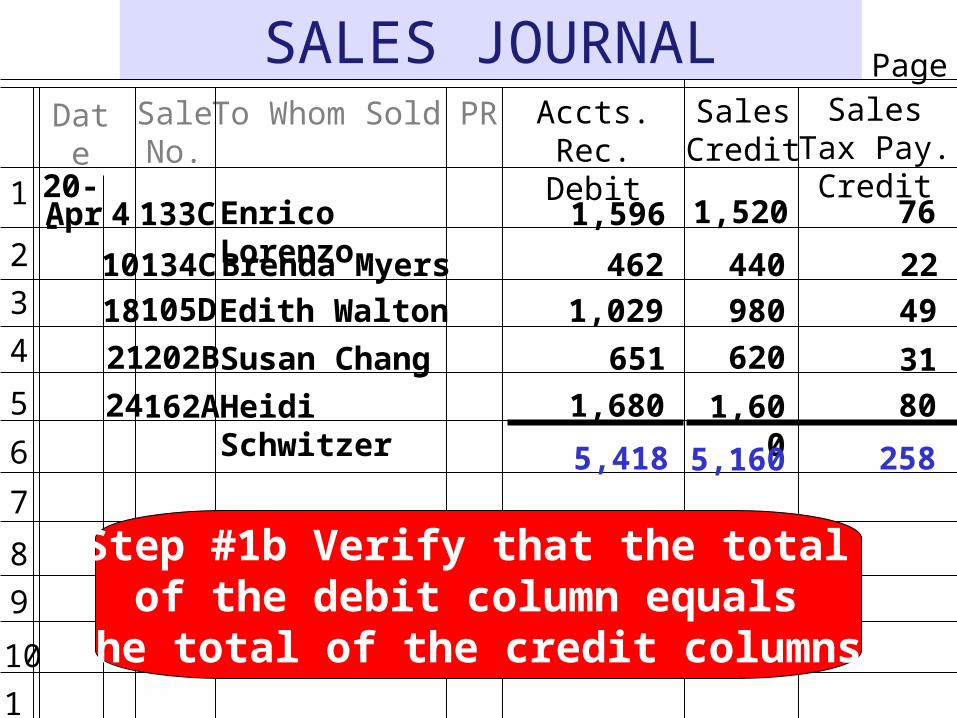

Step #1b Verify that the total of the debit column equals

the total of the credit columns.

5,418 5,160 258

Page 6

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

5,418 5,160 258

Debits$5,418

Credits $5,418

Page 6

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

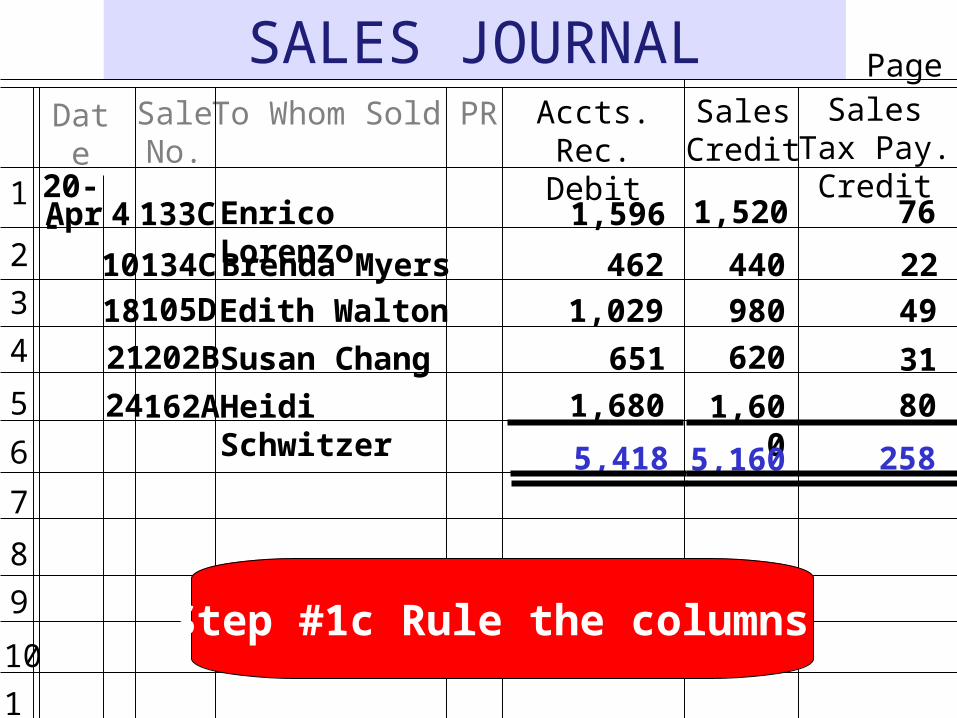

Step #1c Rule the columns.

5,418 5,160 258

Page 6

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

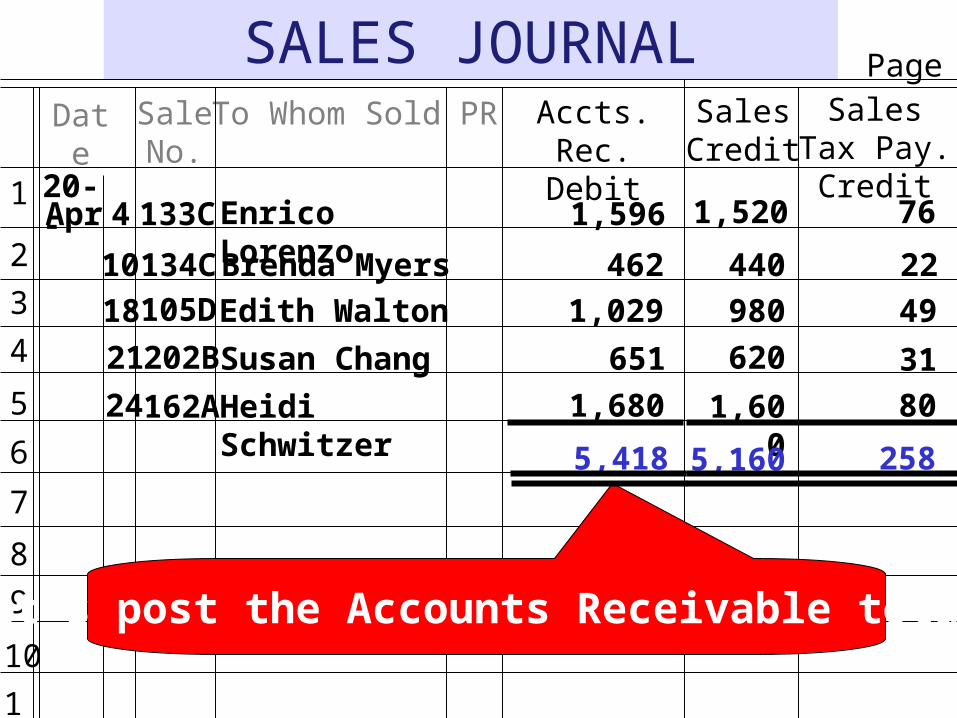

Let’s post the Accounts Receivable total.

5,418 5,160 258

Page 6

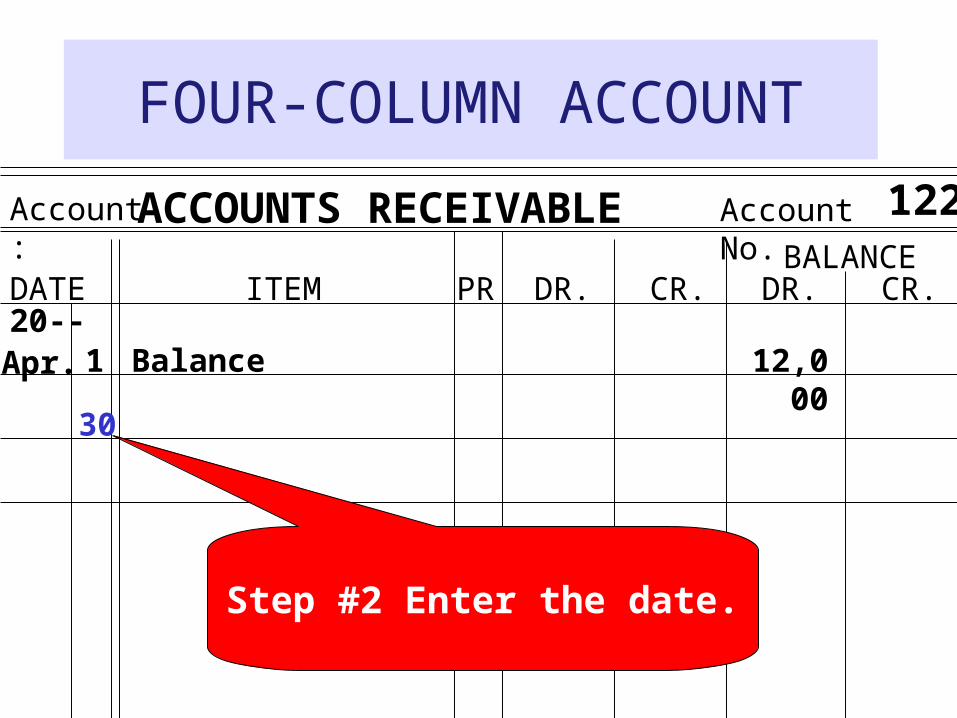

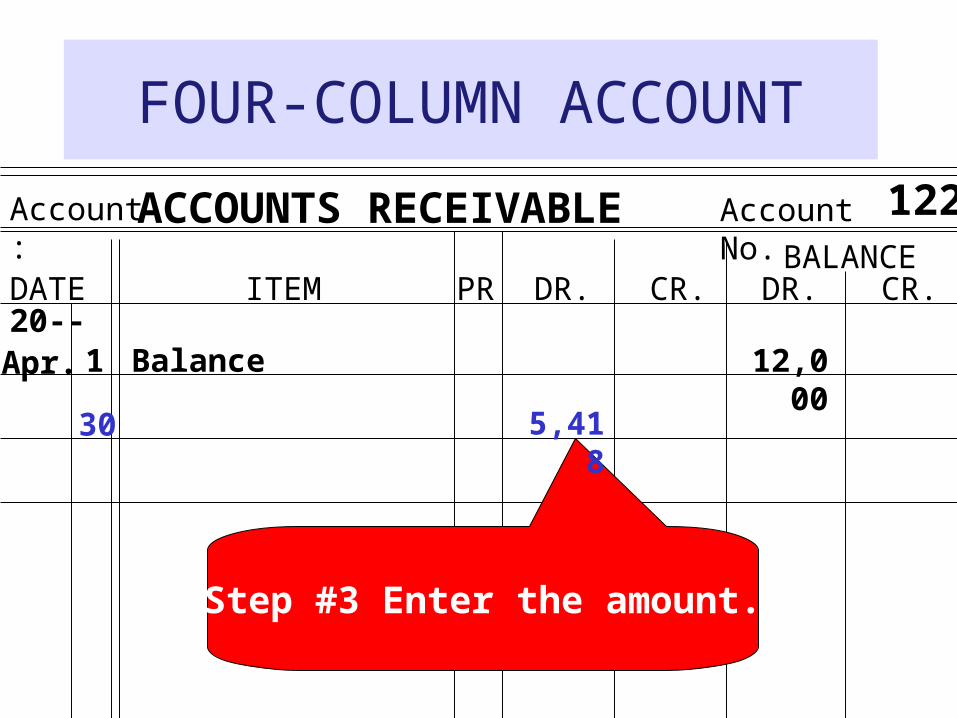

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

ACCOUNTS RECEIVABLE 122

20--Apr. 1 12,000

30

Balance

Step #2 Enter the date.

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

ACCOUNTS RECEIVABLE 122

20--Apr. 1 12,000

30

Balance

Step #3 Enter the amount.

5,418

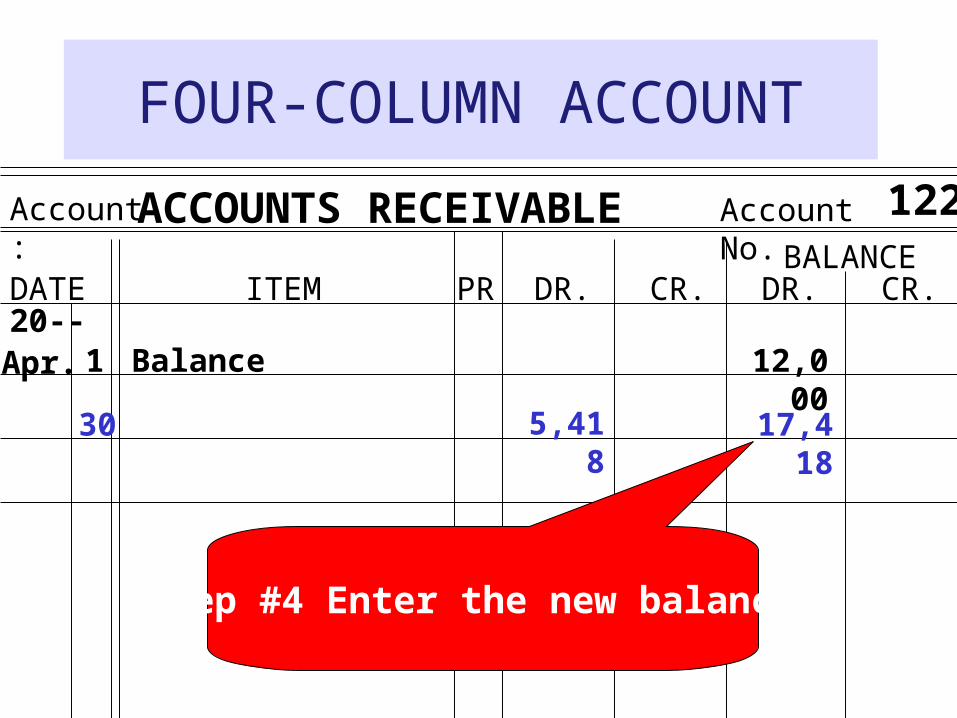

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

ACCOUNTS RECEIVABLE 122

20--Apr. 1 12,000

30

Balance

Step #4 Enter the new balance.

5,418 17,418

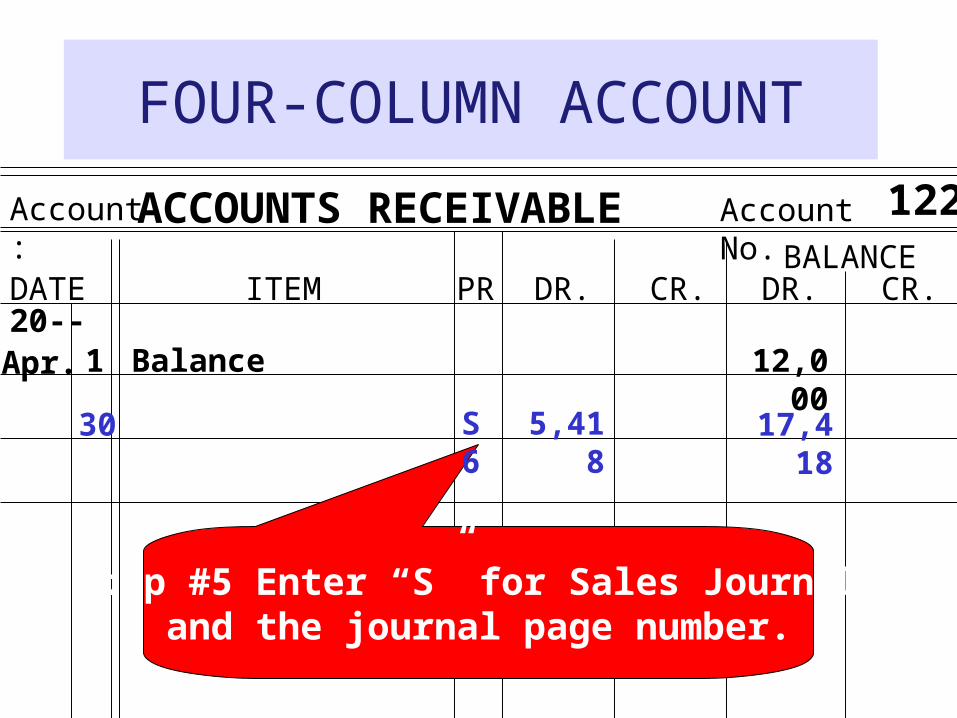

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

ACCOUNTS RECEIVABLE 122

20--Apr. 1 12,000

30

Balance

Step #5 Enter “S” for Sales Journal and the journal page number.

5,418 17,418S6

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

Step #6 Enter the accountnumber below the column total.

5,418 5,160 258

Page 6

(122)

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

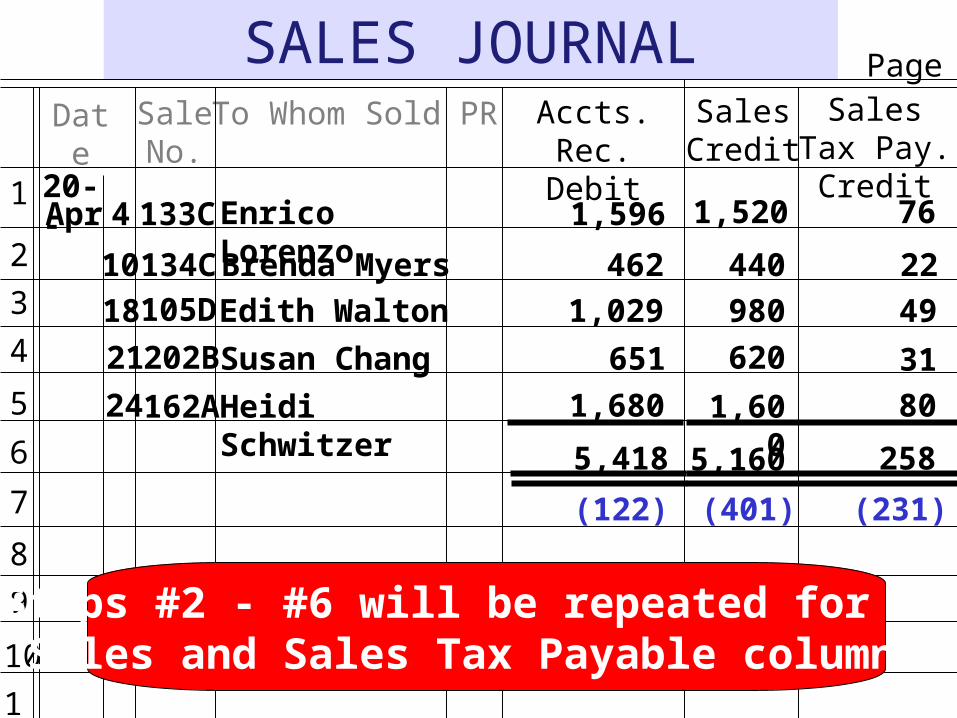

Steps #2 - #6 will be repeated for theSales and Sales Tax Payable columns.

5,418 5,160 258

Page 6

(122) (401) (231)

SALES JOURNALDate To Whom Sold PR Accts. Receivable

Debit/Sales Credit1

2

3

4

5

6

7

8

9

10

11

Sale No.

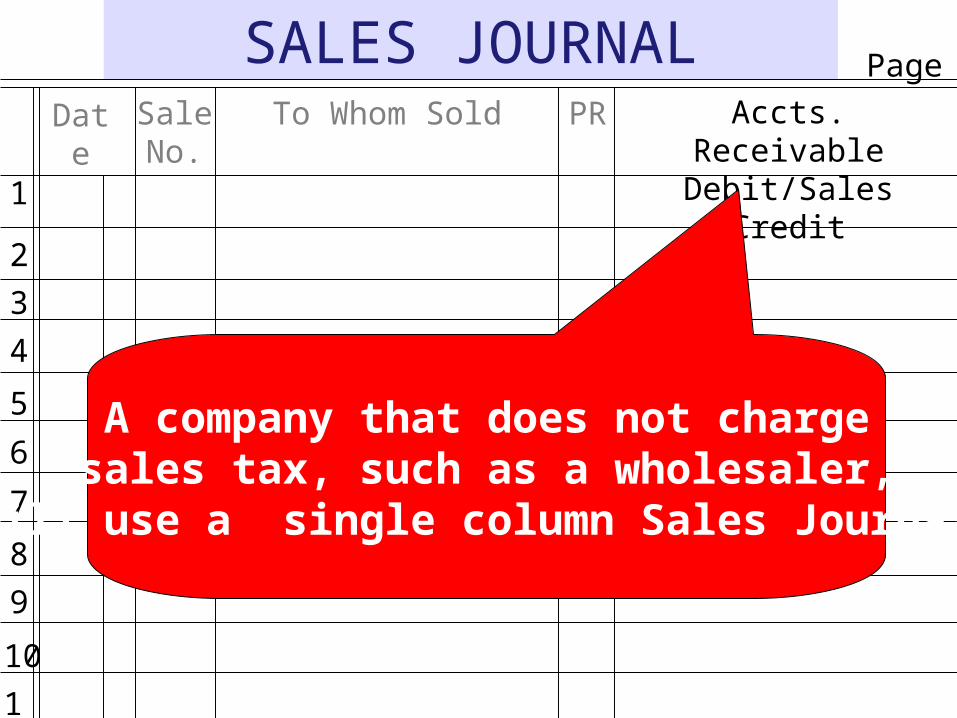

A company that does not chargesales tax, such as a wholesaler,

will use a single column Sales Journal.

Page 1

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

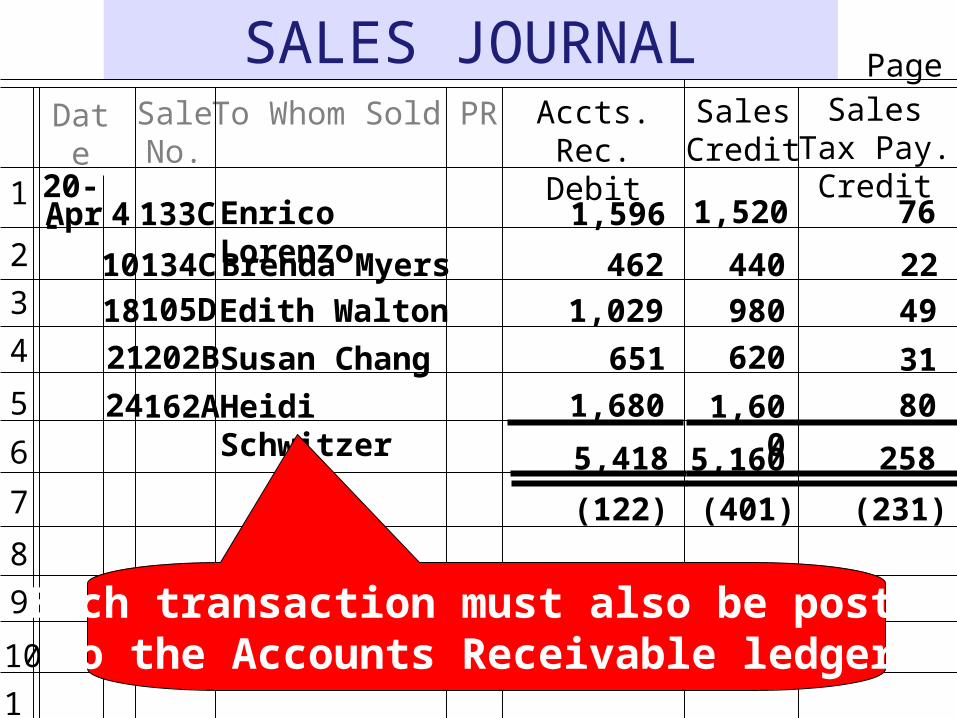

Each transaction must also be postedto the Accounts Receivable ledger.

5,418 5,160 258

Page 6

(122) (401) (231)

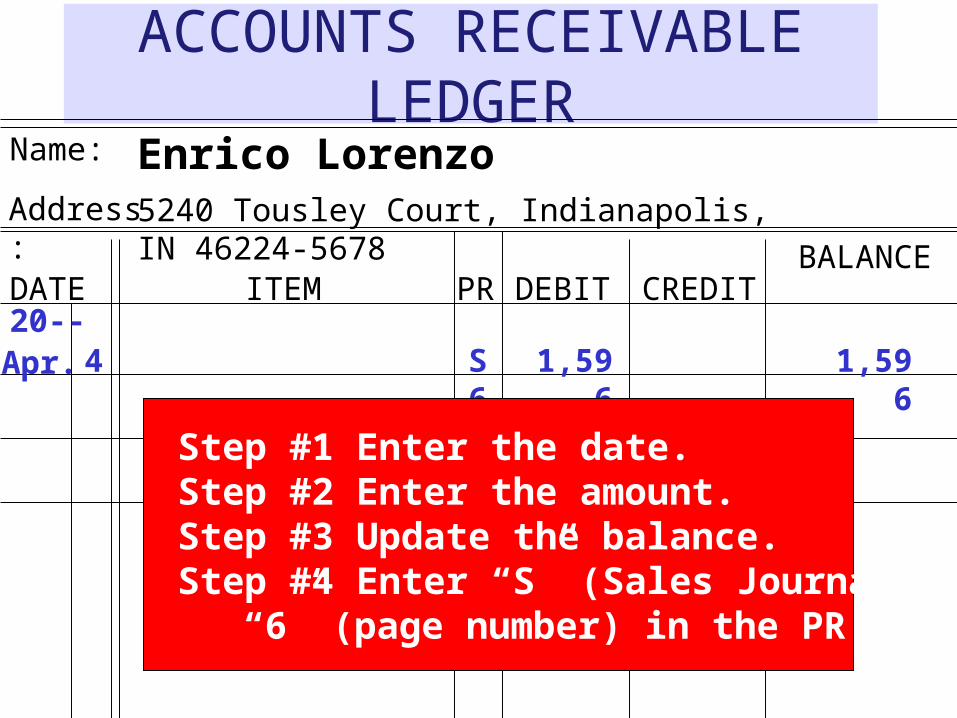

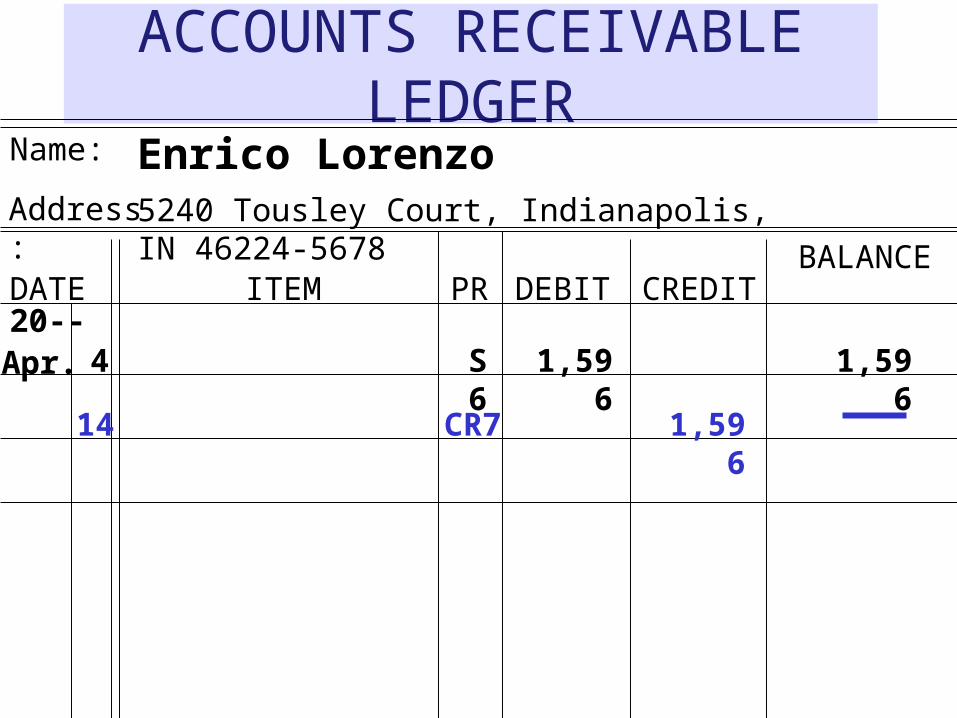

ACCOUNTS RECEIVABLE LEDGER

Name:

DATE ITEM PR DEBIT CREDITBALANCE

Enrico Lorenzo

20--Apr. 1,5964

Address: 5240 Tousley Court, Indianapolis, IN 46224-5678

1,596S6

Step #1 Enter the date.Step #2 Enter the amount.Step #3 Update the balance.Step #4 Enter “S” (Sales Journal) and “6” (page number) in the PR column.

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

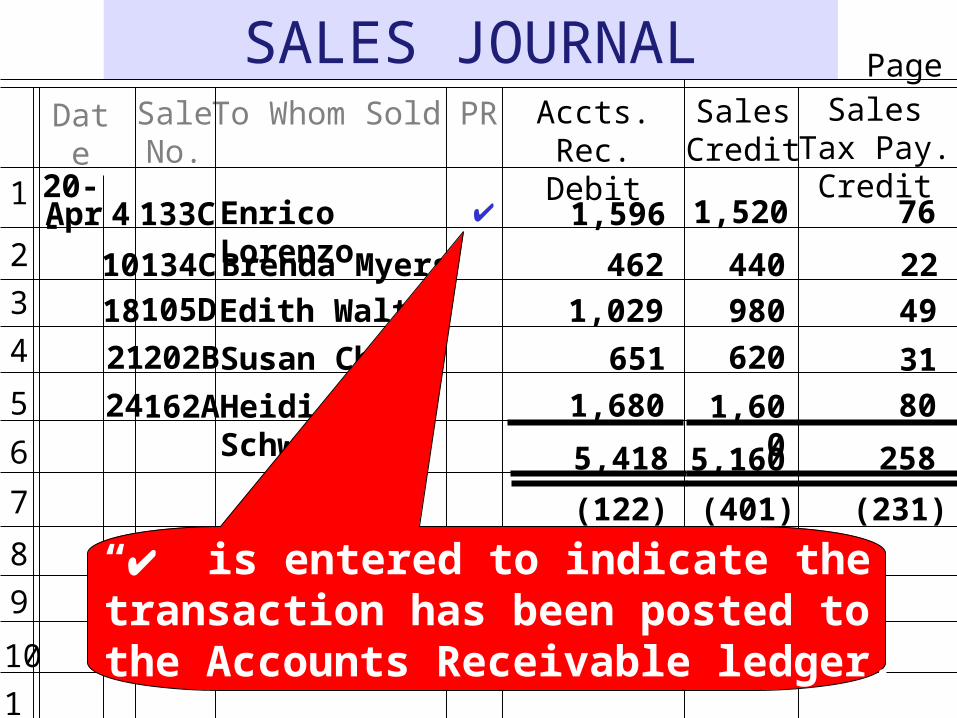

“” is entered to indicate thetransaction has been posted to

the Accounts Receivable ledger.

5,418 5,160 258

Page 6

(122) (401) (231)

SALES JOURNALDate To Whom Sold PR Accts. Rec.

DebitSales Tax

Pay. Credit

1

2

3

4

5

6

7

8

9

10

11

Sale No.

20--Apr 133C

Sales Credit

Enrico Lorenzo 1,596 1,520 764

10 134C Brenda Myers 462 440 22

18 105D Edith Walton 1,029 980 49

21 202B Susan Chang 651 620 31

24 162A Heidi Schwitzer 1,680 1,600 80

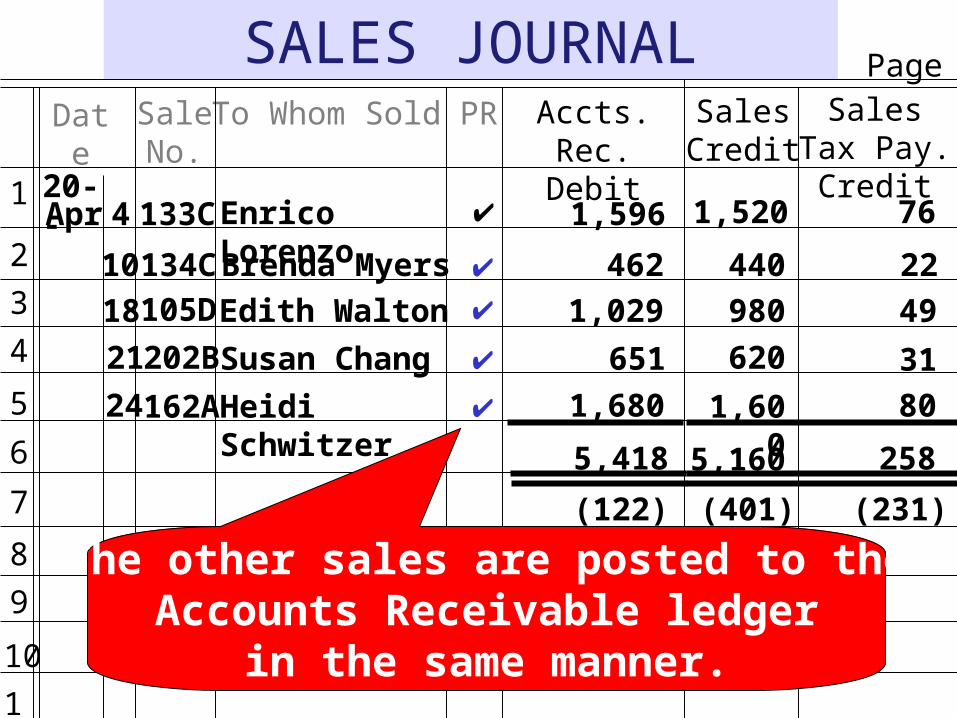

The other sales are posted to theAccounts Receivable ledger

in the same manner.

5,418 5,160 258

Page 6

(122) (401) (231)

CASH RECEIPTS JOURNAL

Used to record only cash receipt transactions

Includes separate columns for:Cash (Debit)Bank Credit Card Expense (Debit)Accounts Receivable (Credit)Sales (Credit)Sales Tax Payable (Credit)General (Credit)

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

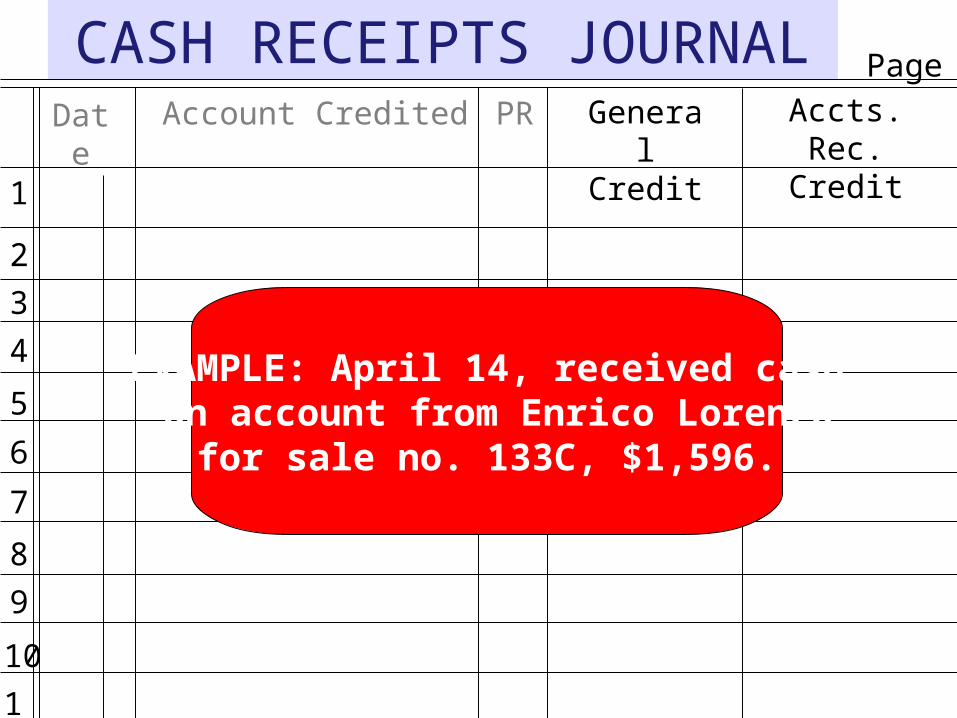

EXAMPLE: April 14, received cash on account from Enrico Lorenzo

for sale no. 133C, $1,596.

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

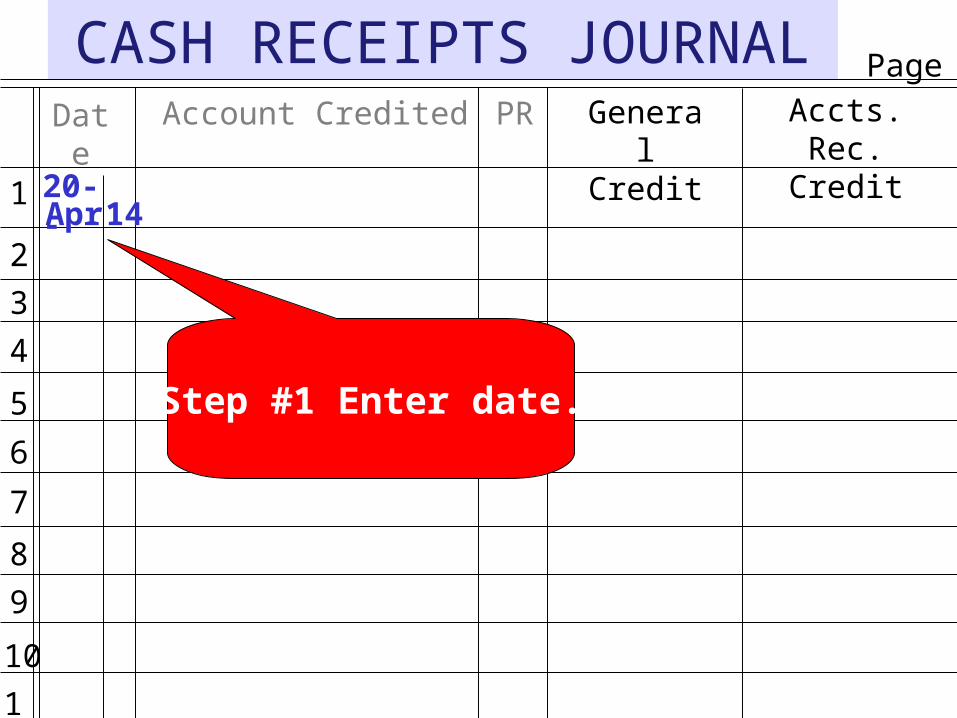

Step #1 Enter date.

Apr20--

14

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

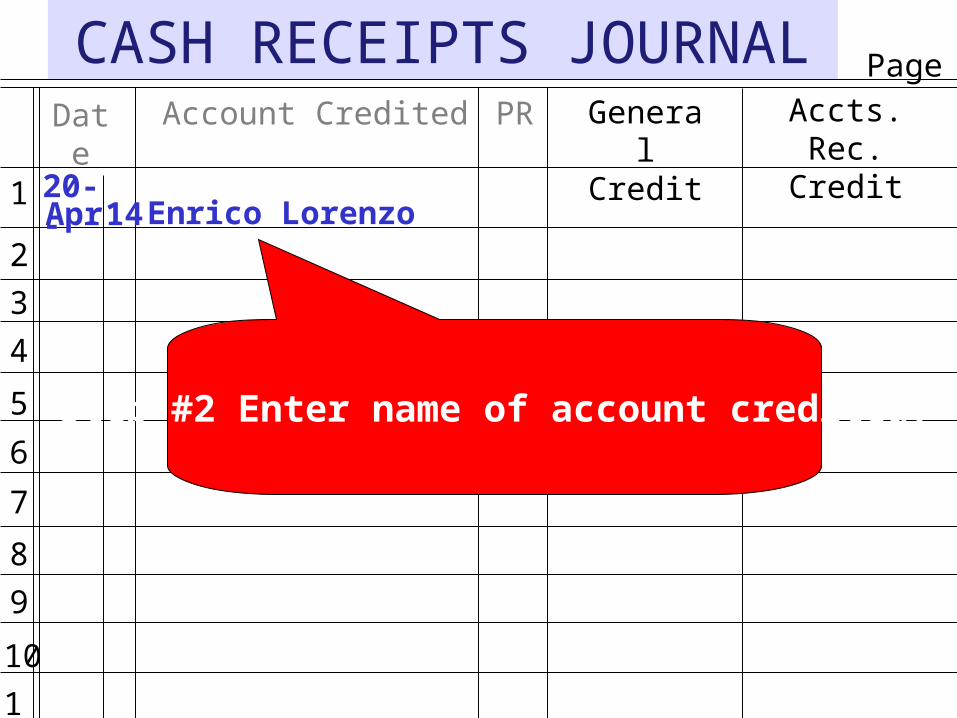

Step #2 Enter name of account credited.

Apr20--

14 Enrico Lorenzo

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo

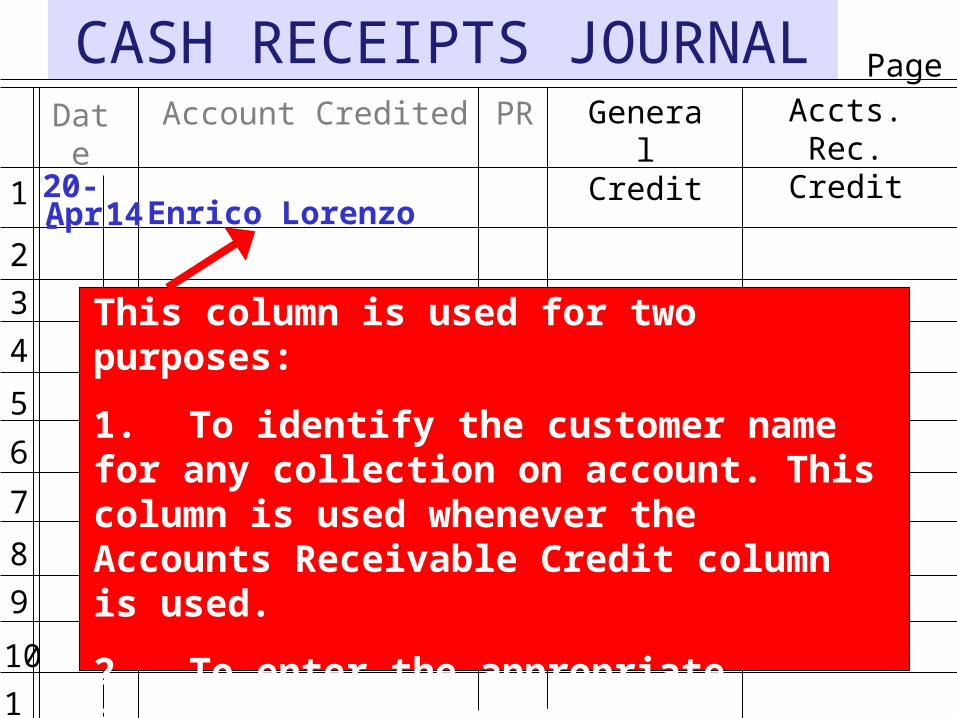

This column is used for two purposes:

1. To identify the customer name for any collection on account. This column is used whenever the Accounts Receivable Credit column is used.

2. To enter the appropriate account name whenever the General Credit column is used.

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

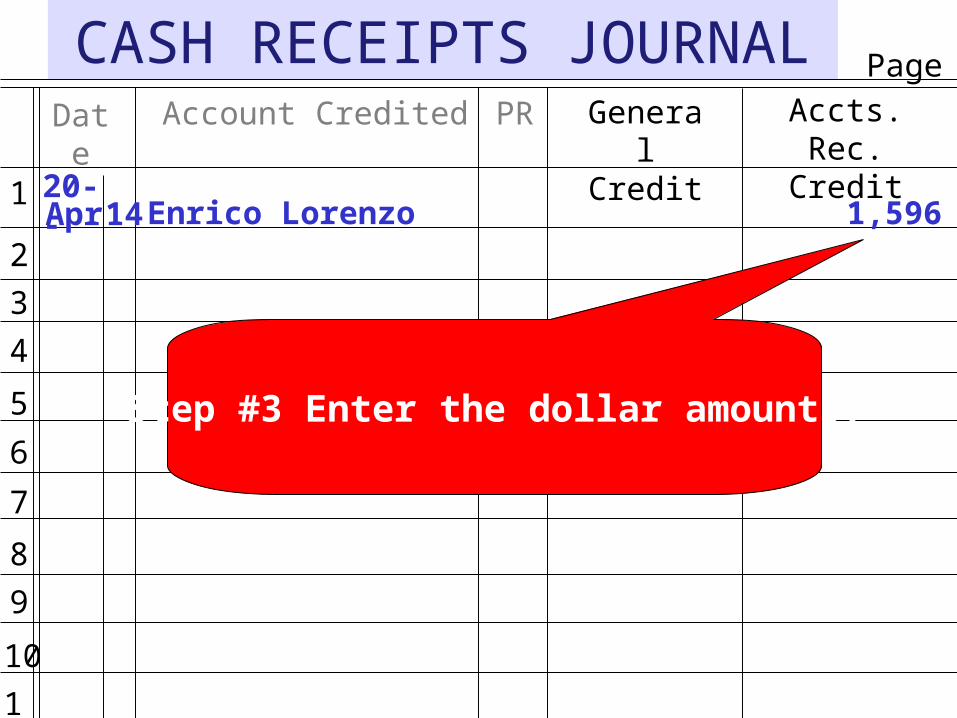

Step #3 Enter the dollar amounts.

Apr20--

14 Enrico Lorenzo 1,596

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

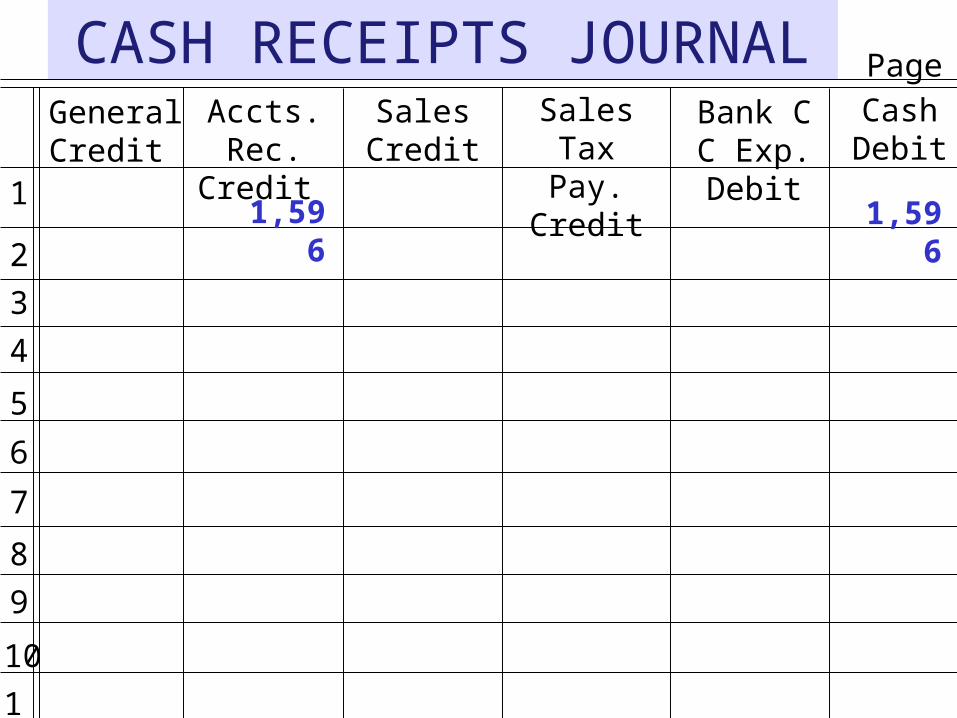

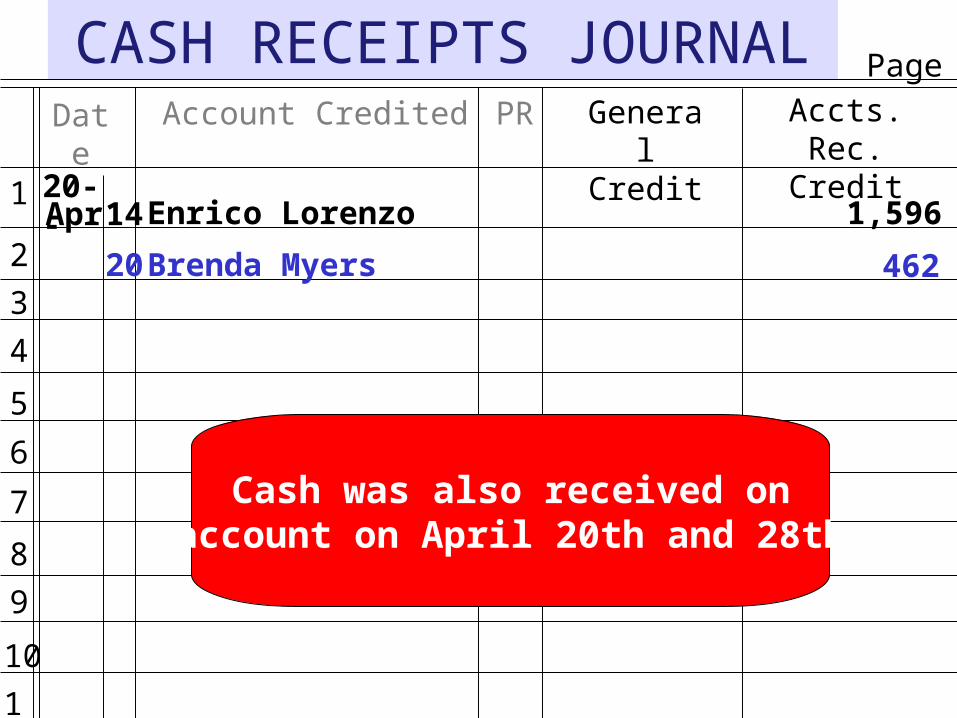

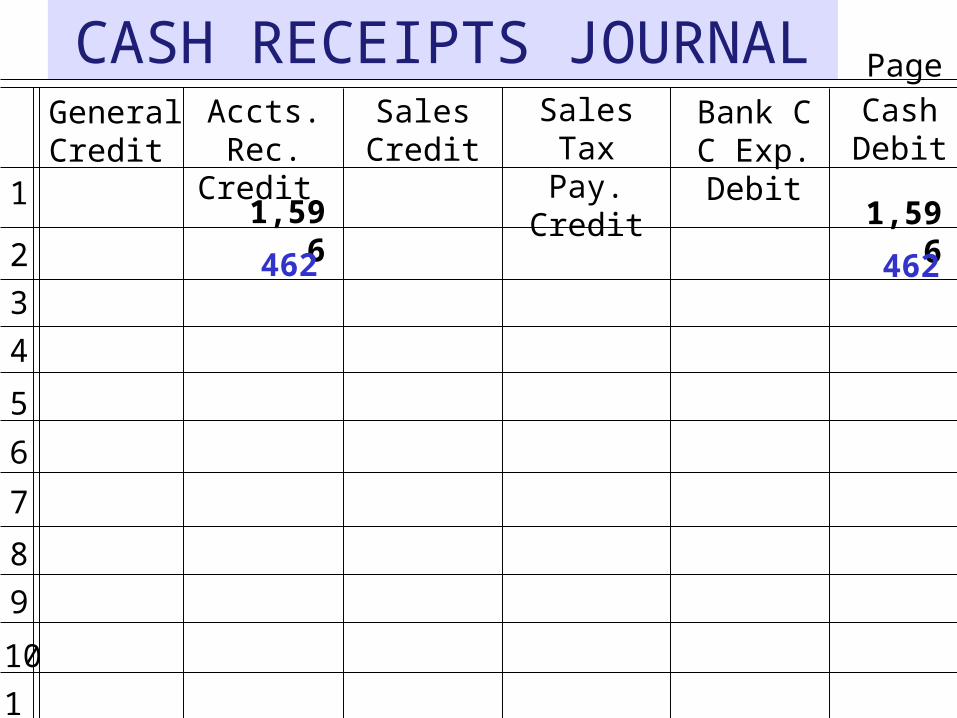

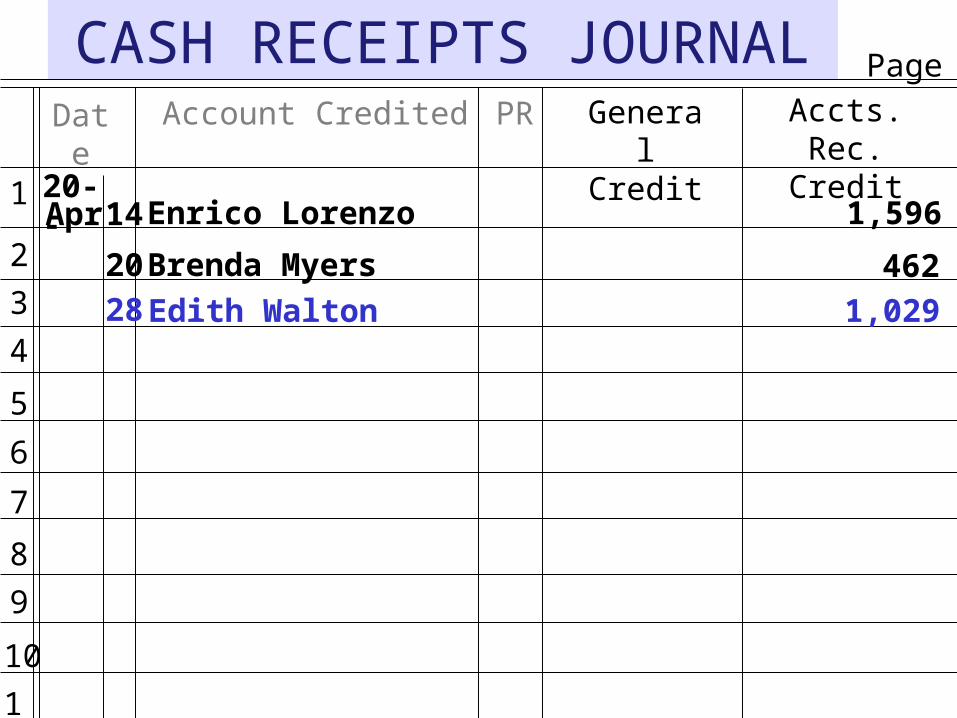

20 Brenda Myers 462

Cash was also received on account on April 20th and 28th.

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

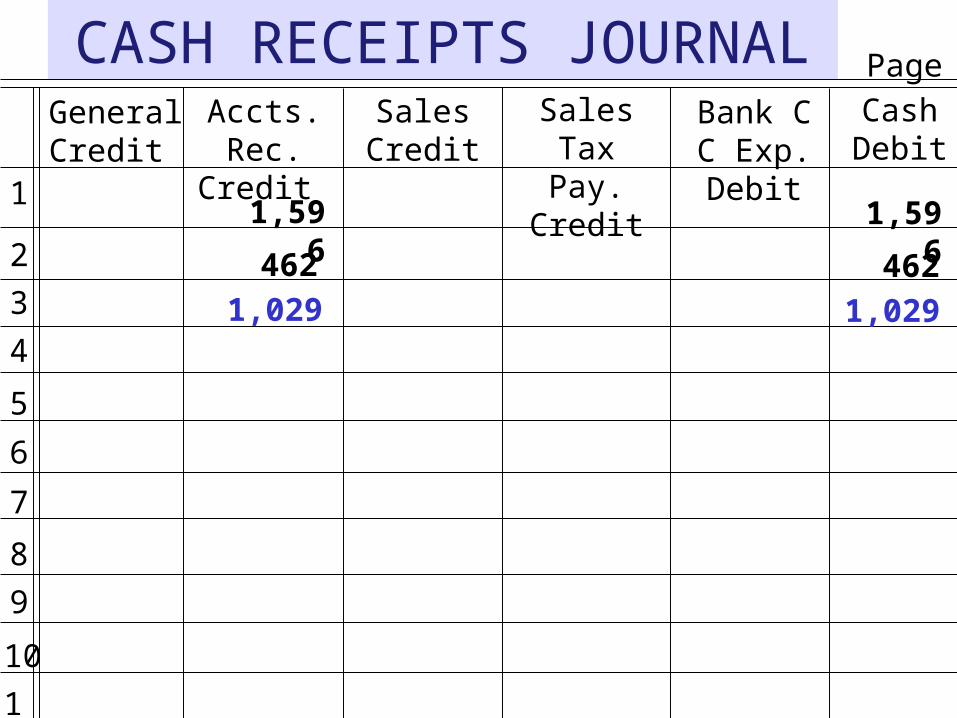

Accts. Rec. Credit

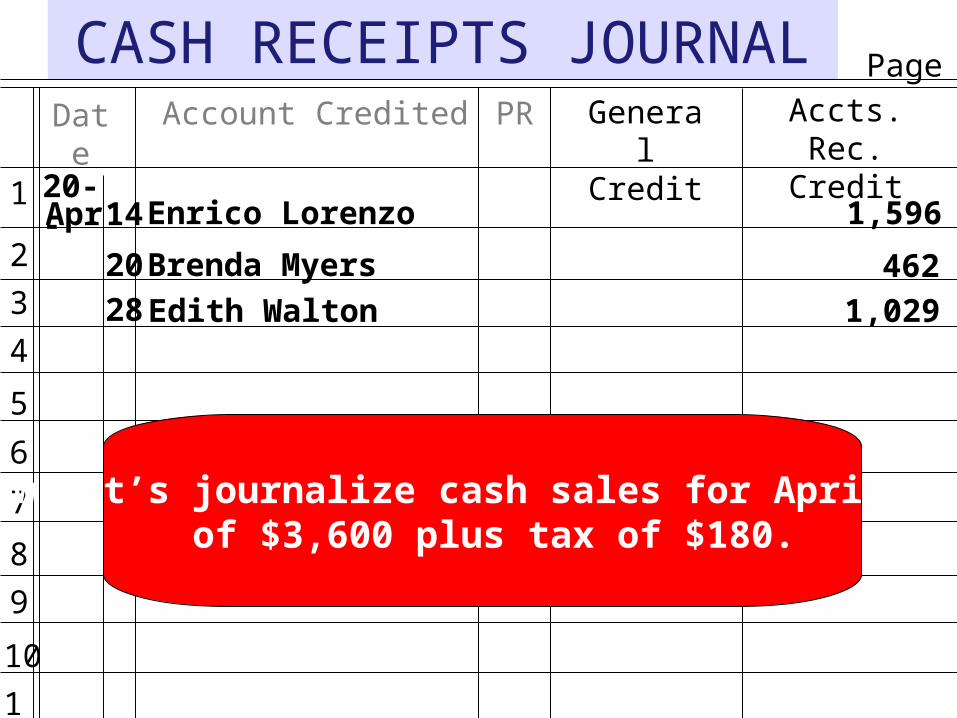

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

Now let’s journalize cash sales for April 30th of $3,600 plus tax of $180.

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

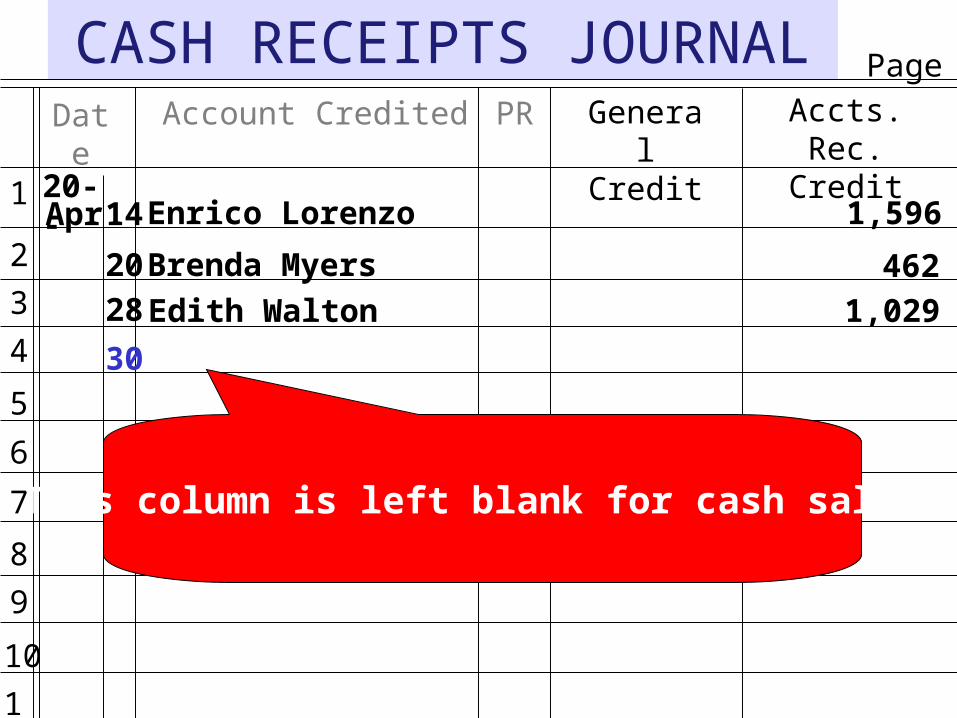

20 Brenda Myers 46228 Edith Walton 1,029

This column is left blank for cash sales.

30

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

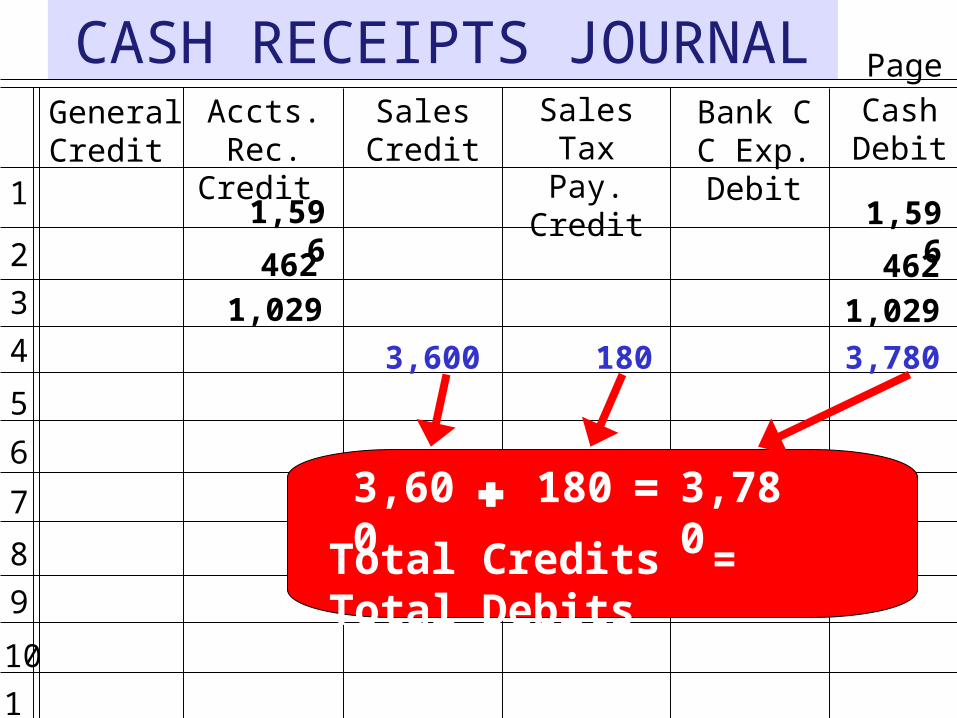

3,600 180 3,780

3,600 180 = 3,780

Total Credits = Total Debits

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

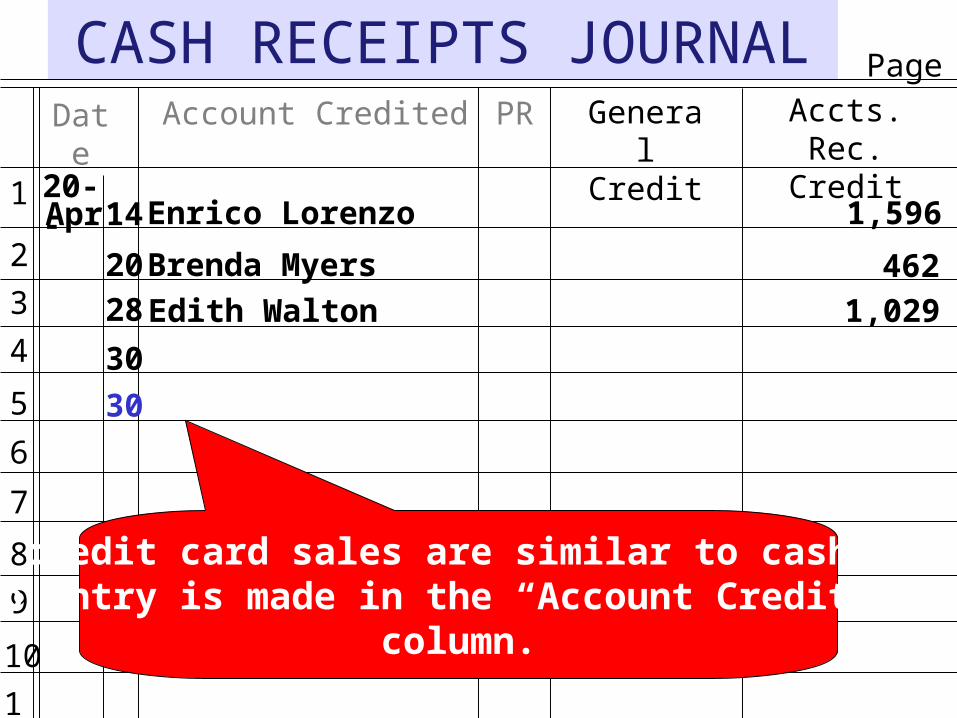

Bank credit card sales are similar to cash sales,no entry is made in the “Account Credited”

column.

30

30

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

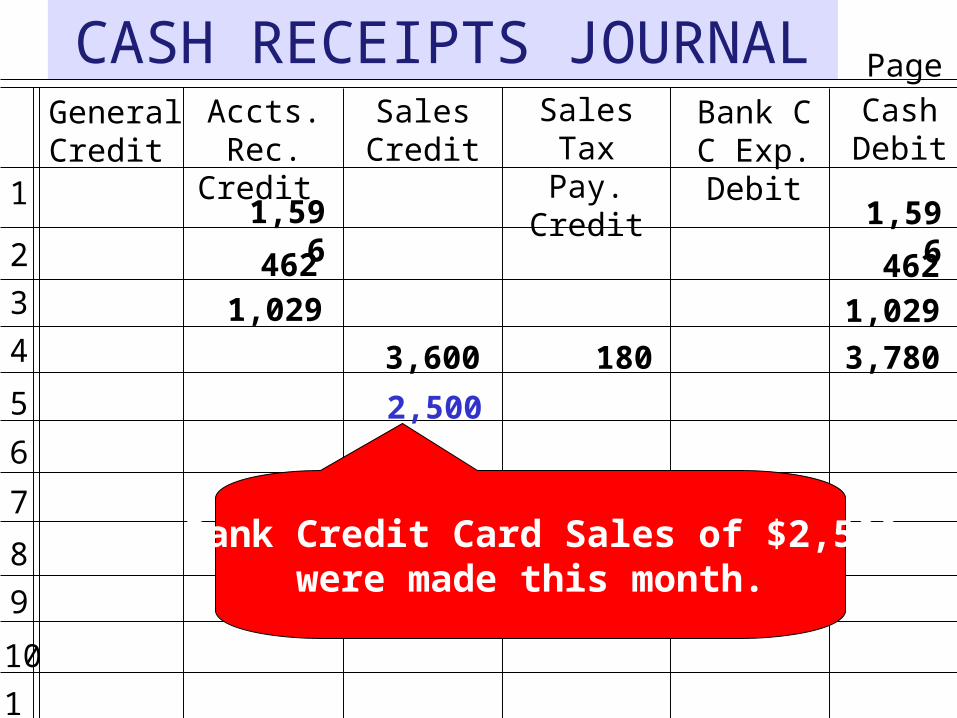

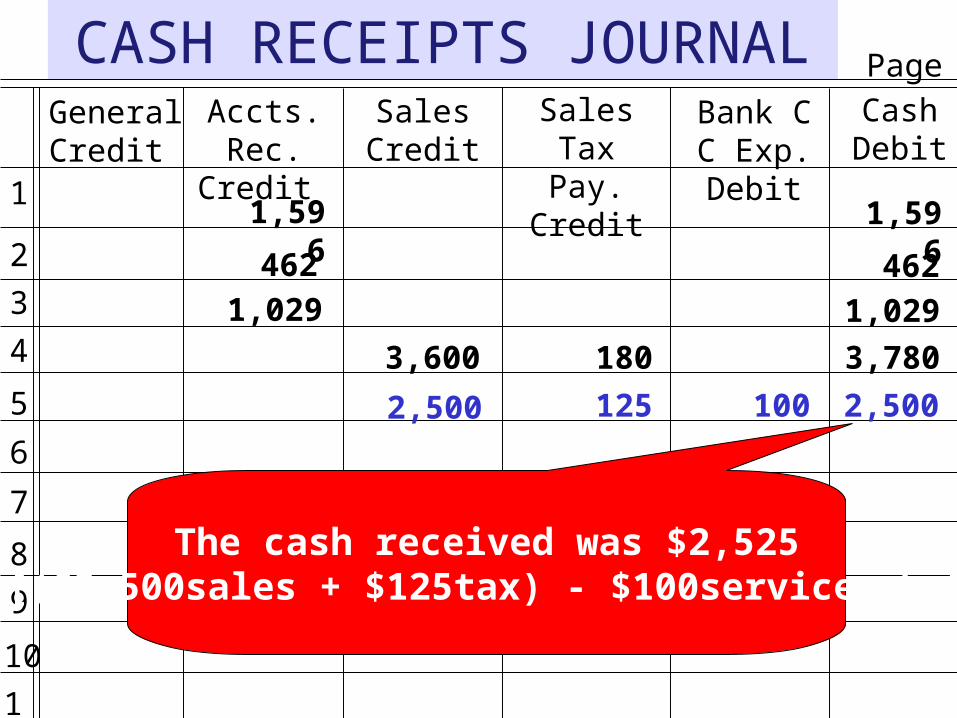

Bank Credit Card Sales of $2,500were made this month.

2,500

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

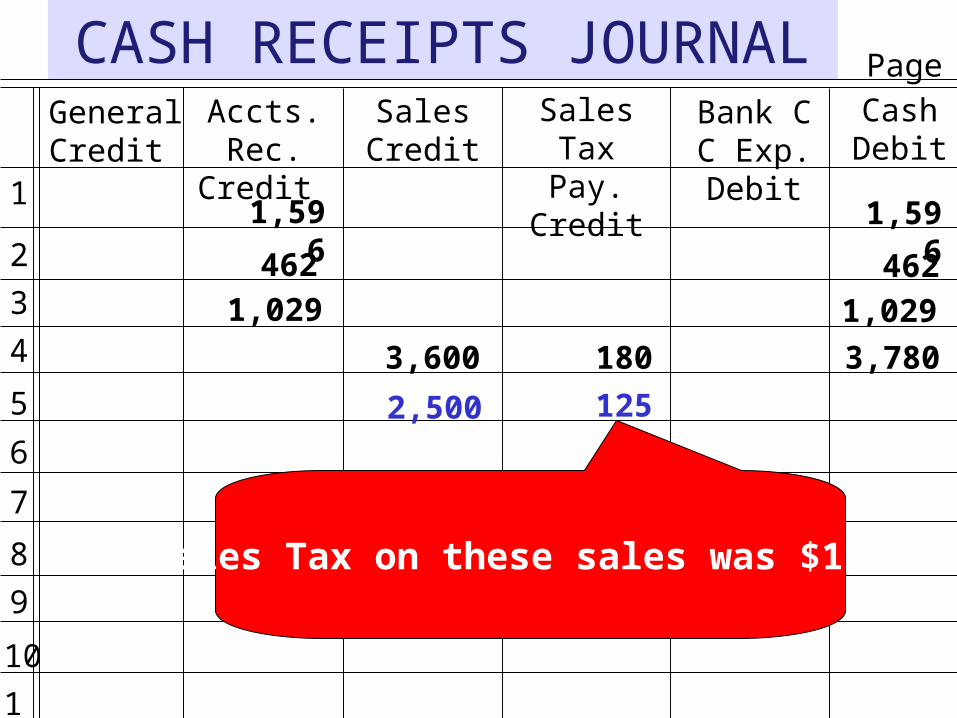

Sales Tax on these sales was $125.

2,500 125

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

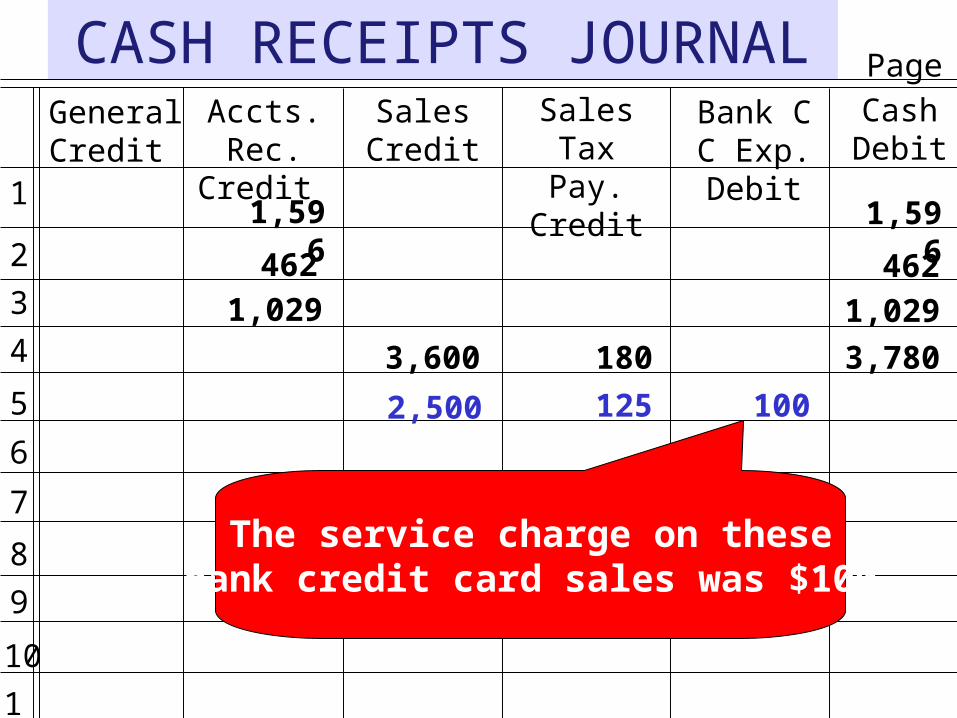

The service charge on these bank credit card sales was $100.

2,500 125 100

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

The cash received was $2,525 [($2,500sales + $125tax) - $100service chg].

2,500 125 100 2,500

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

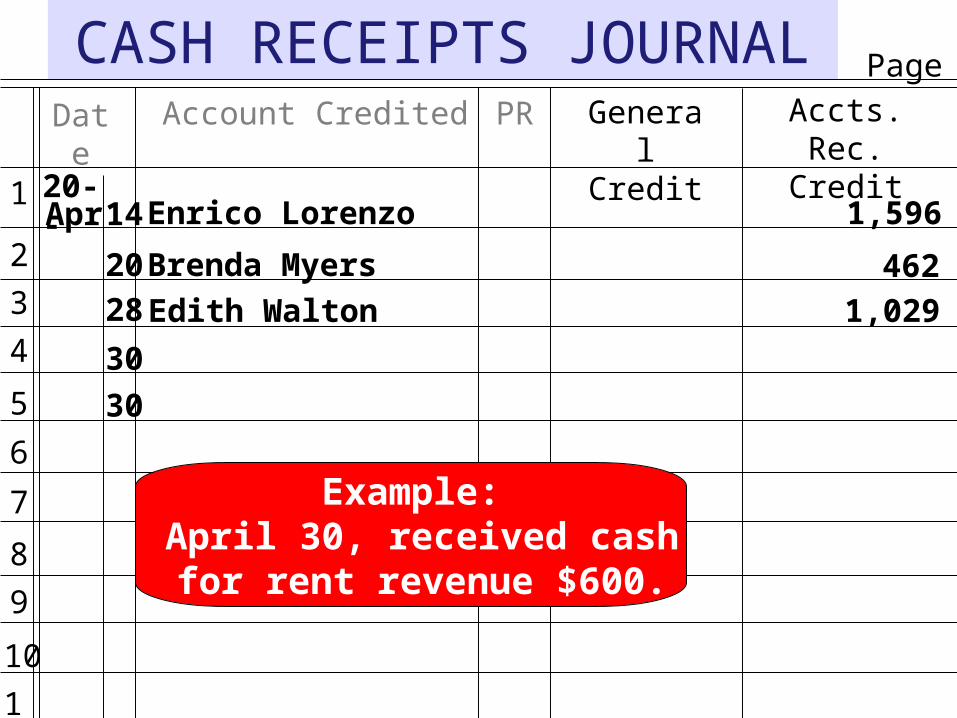

Example: April 30, received cash for rent revenue $600.

30

30

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

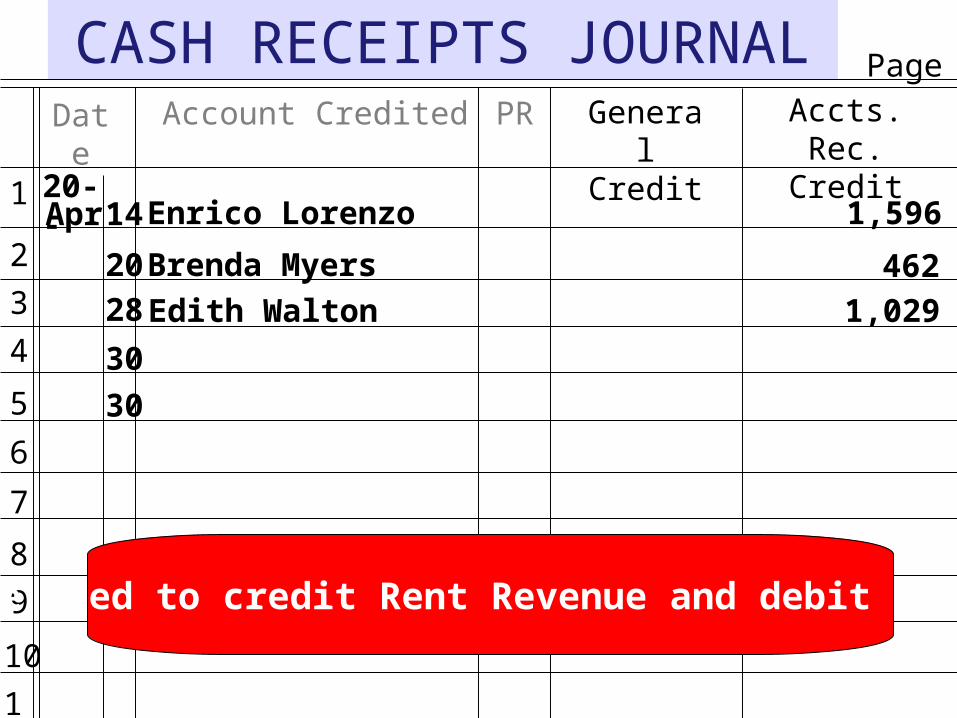

We need to credit Rent Revenue and debit Cash.

30

30

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

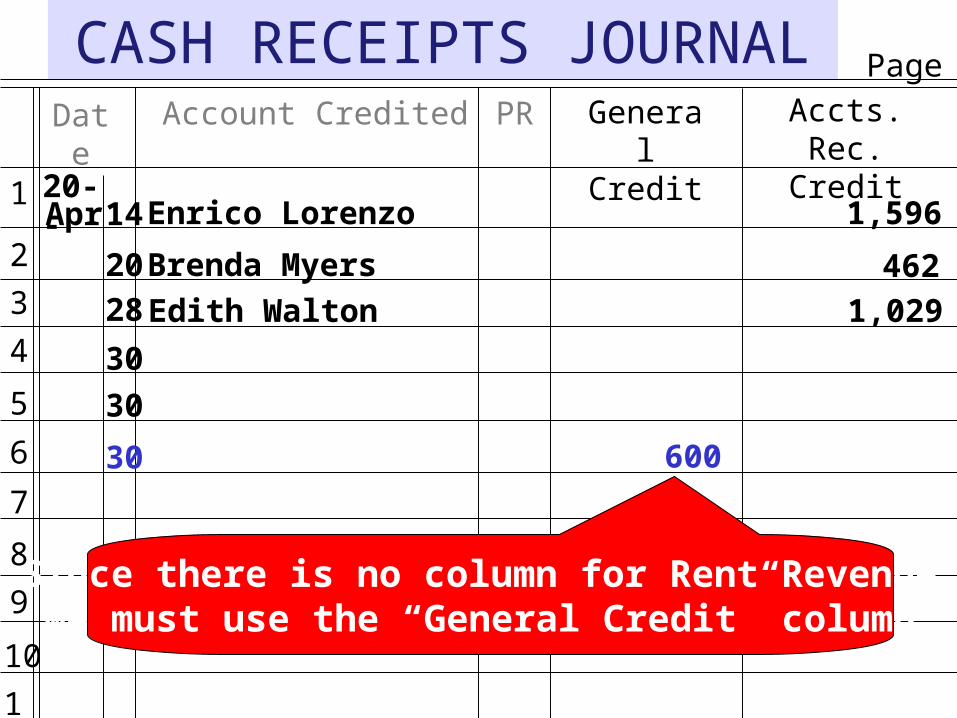

Since there is no column for Rent Revenue,we must use the “General Credit” column.

30

30

30 600

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

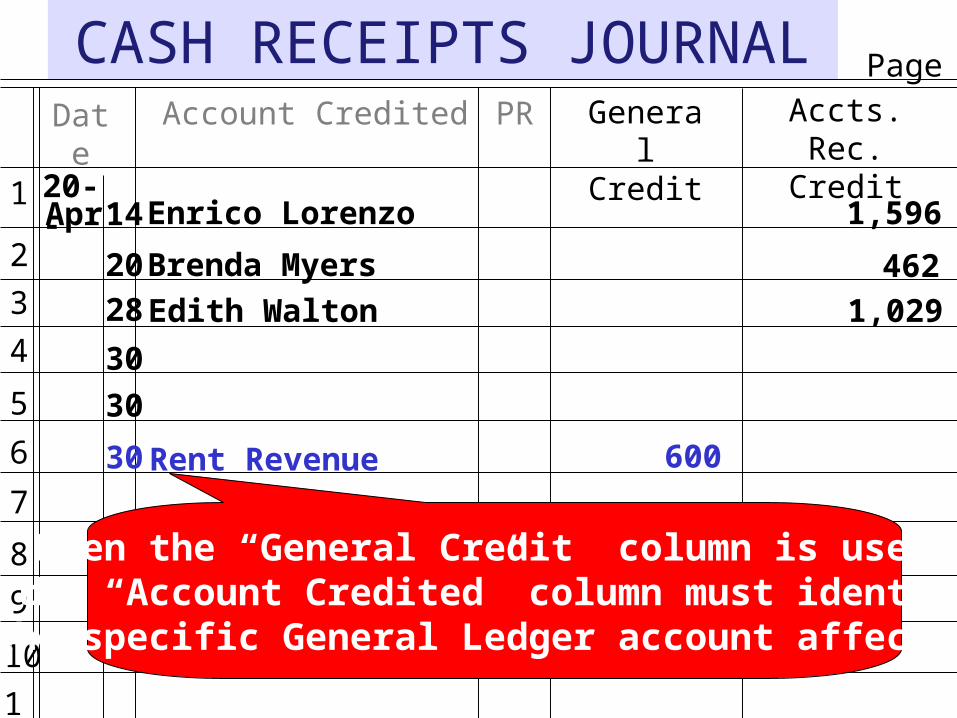

When the “General Credit” column is used,the “Account Credited” column must identifythe specific General Ledger account affected.

30

30

30 600Rent Revenue

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

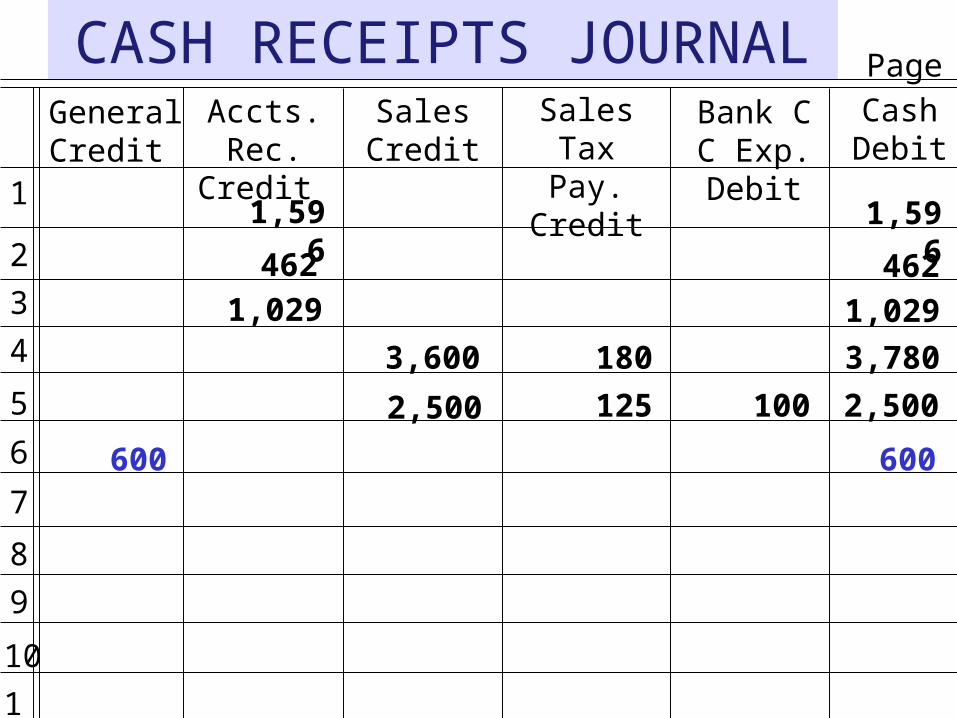

600 600

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

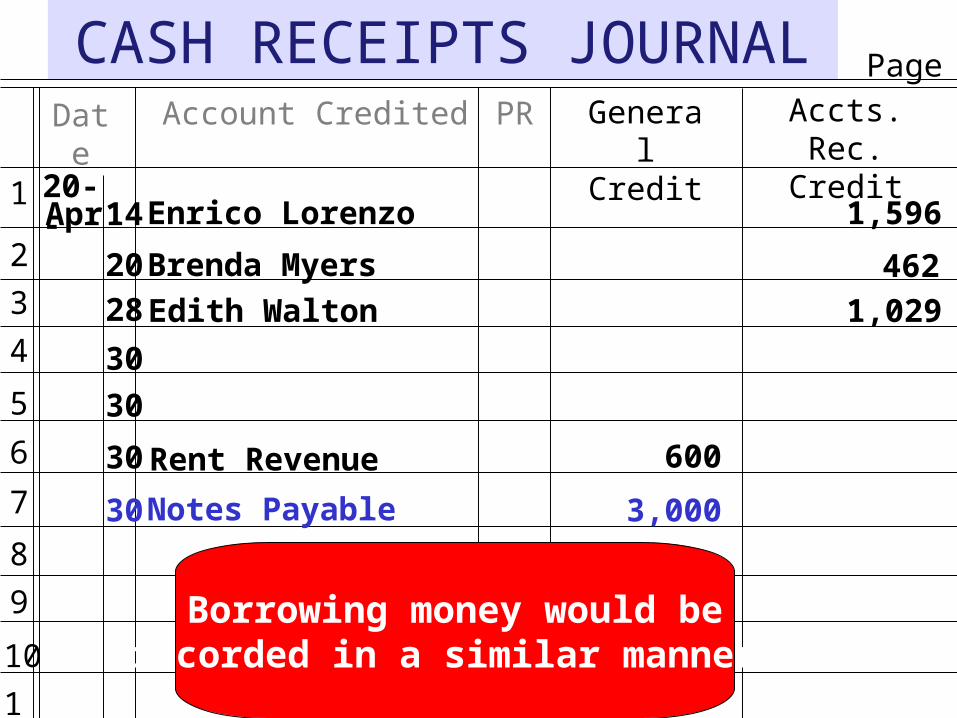

Borrowing money would berecorded in a similar manner.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

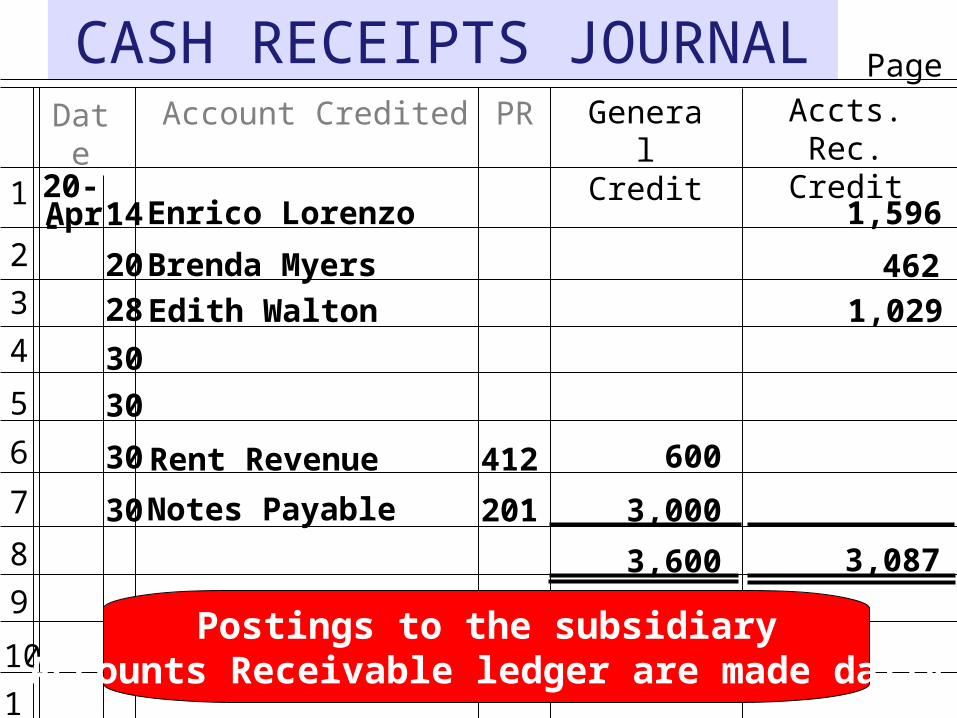

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

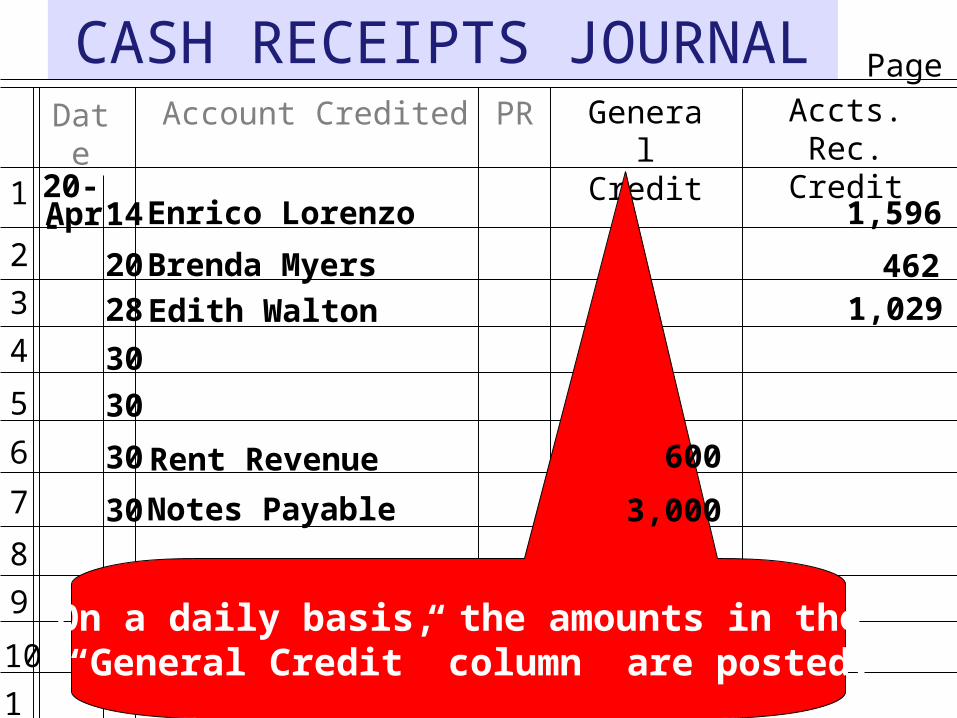

On a daily basis, the amounts in the “General Credit” column are posted.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

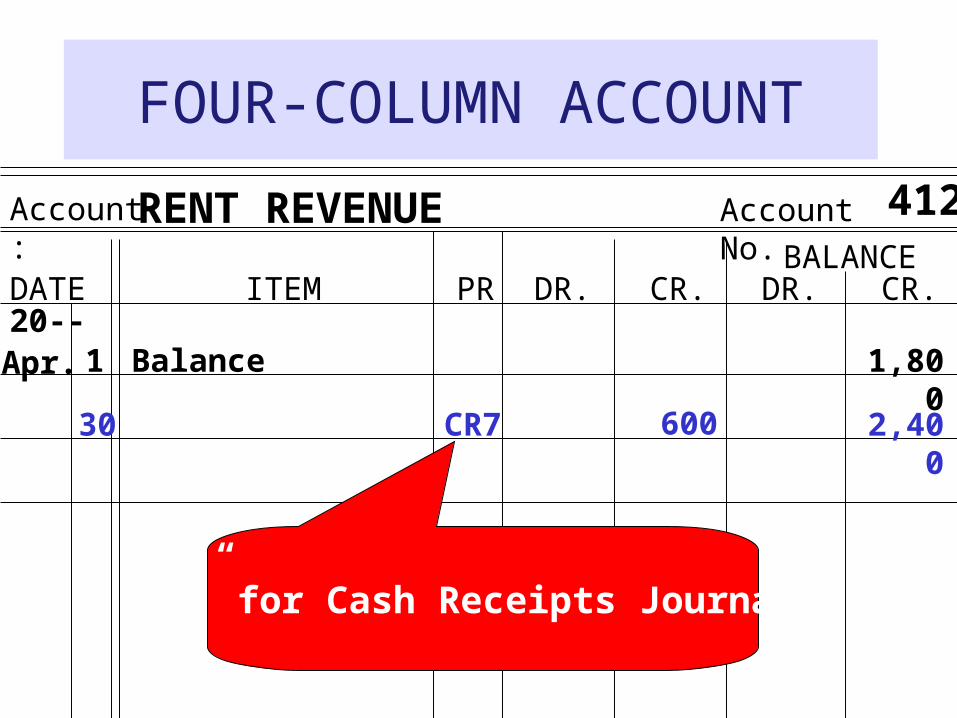

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

RENT REVENUE 412

20--Apr. 1 1,800

30

Balance

“CR” for Cash Receipts Journal.

600 2,400CR7

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

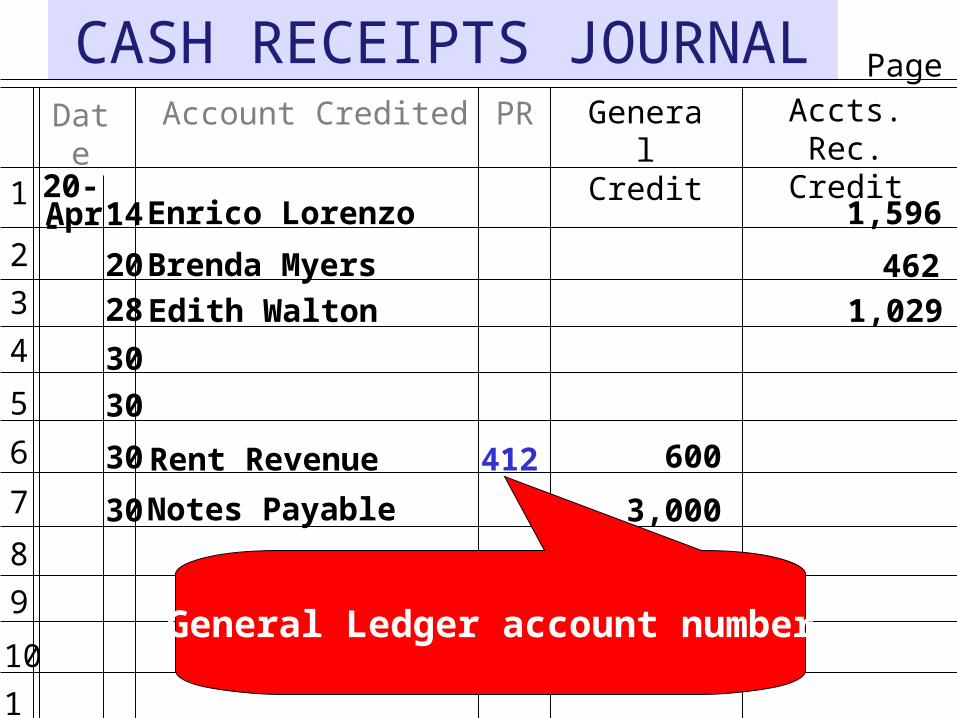

General Ledger account number

30

30

30 600Rent Revenue

30 Notes Payable 3,000

412

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

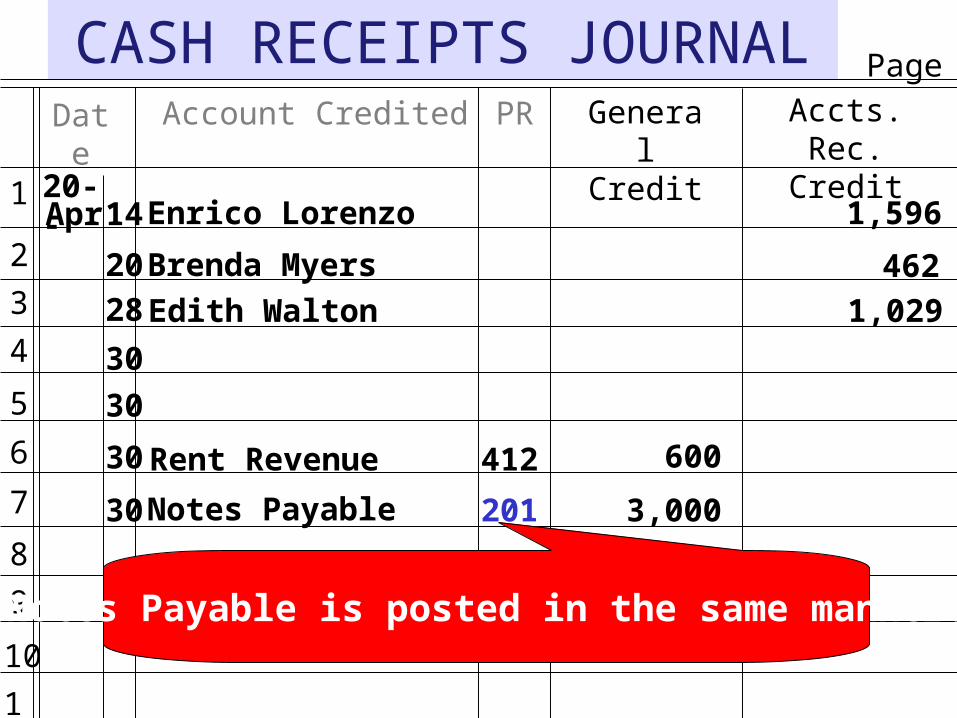

Notes Payable is posted in the same manner.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

412

201

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

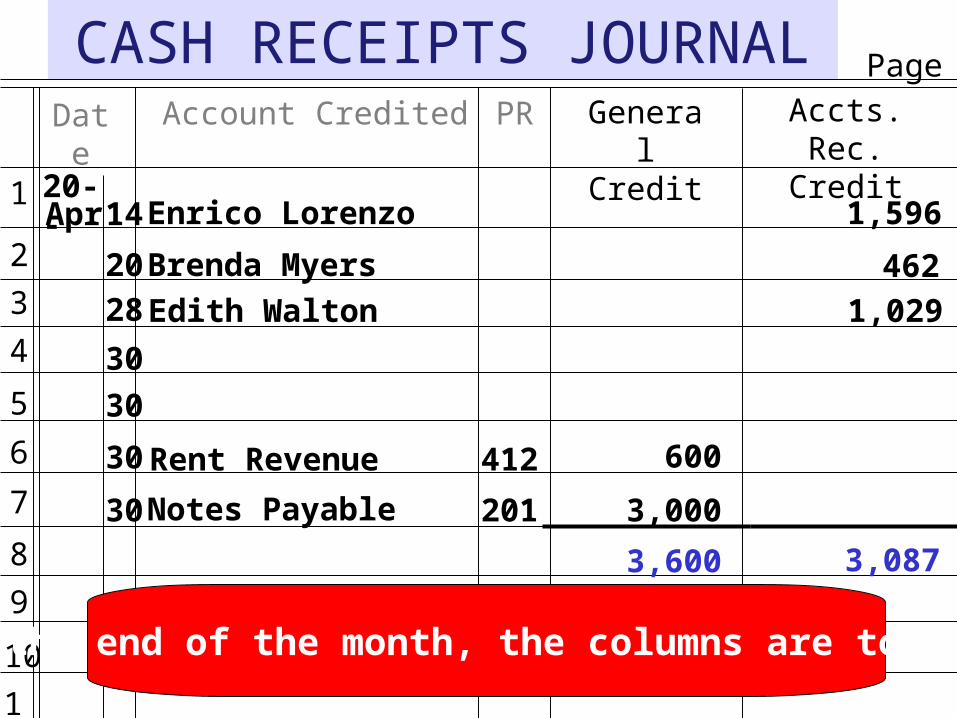

At the end of the month, the columns are totaled.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

412

201

3,600 3,087

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

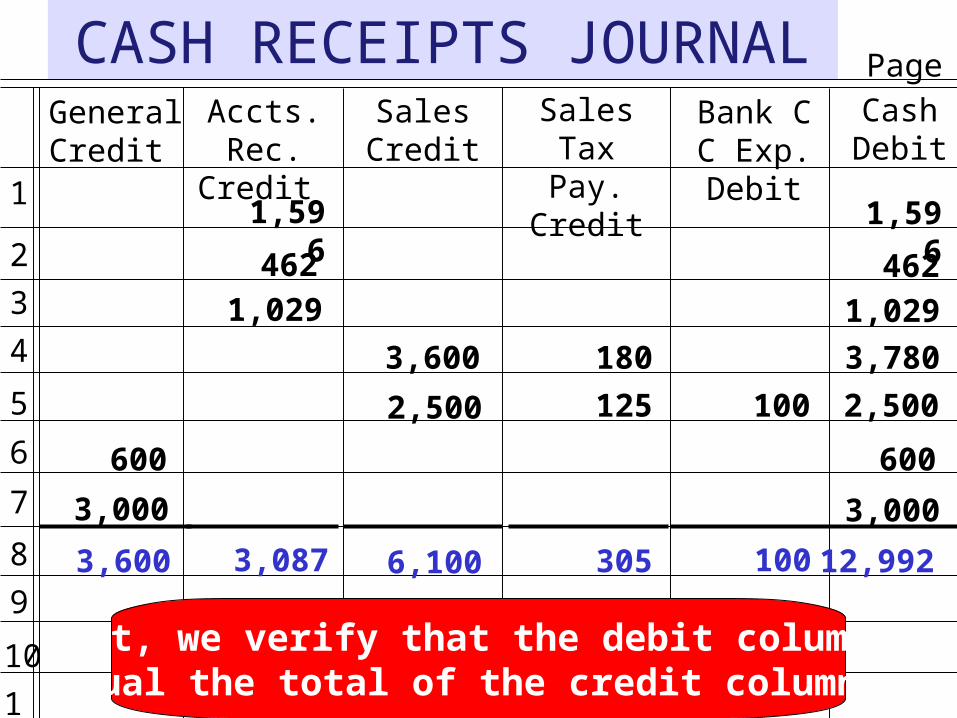

3,600 3,087 6,100 305 100 12,992

Next, we verify that the debit columns equal the total of the credit columns.

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

3,600 3,087 6,100 305 100 12,992

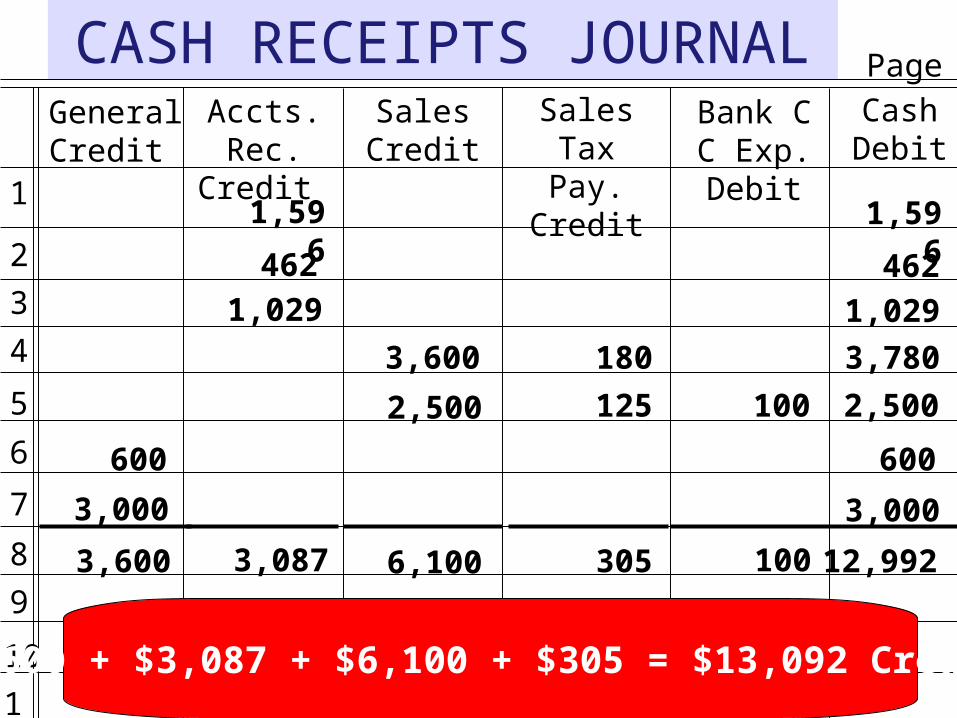

$3,600 + $3,087 + $6,100 + $305 = $13,092 Credits

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

3,600 3,087 6,100 305 100 12,992

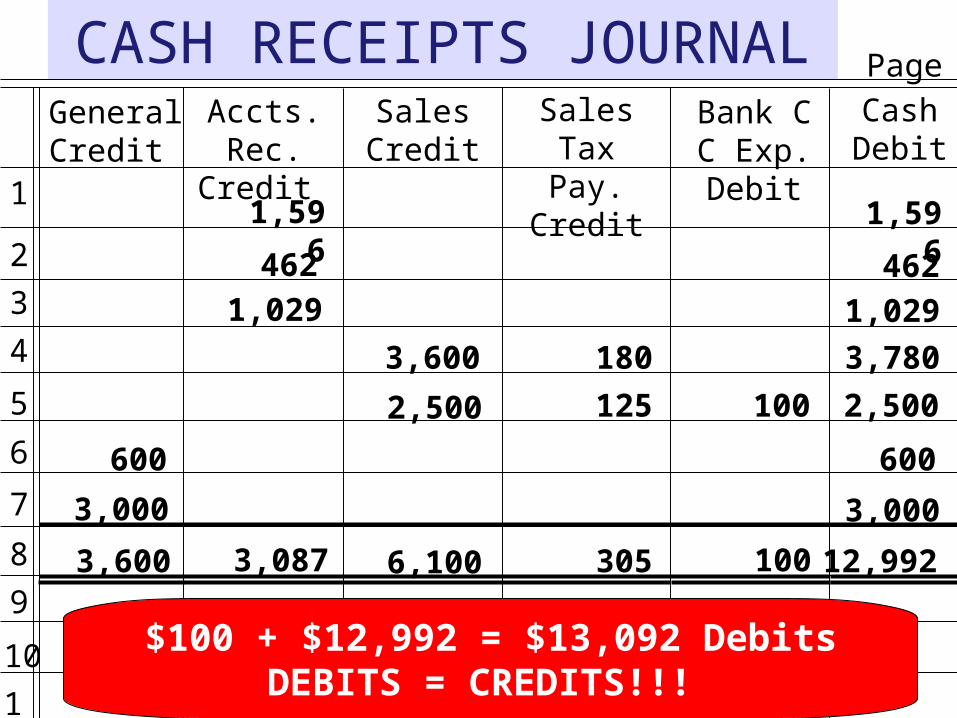

$100 + $12,992 = $13,092 DebitsDEBITS = CREDITS!!!

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

3,600 3,087 6,100 305 100 12,992

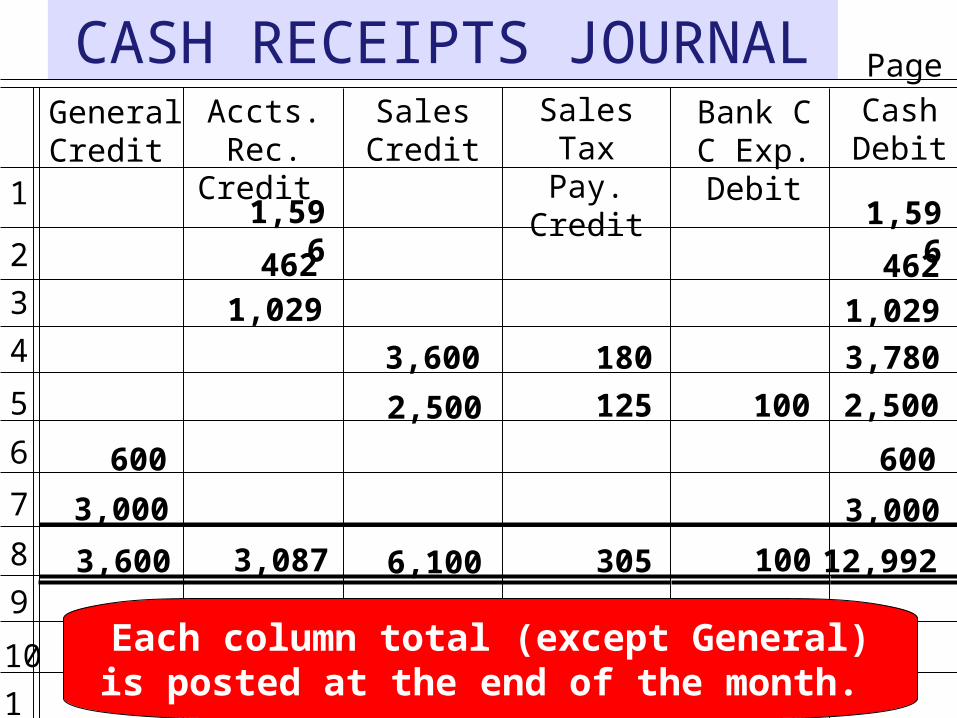

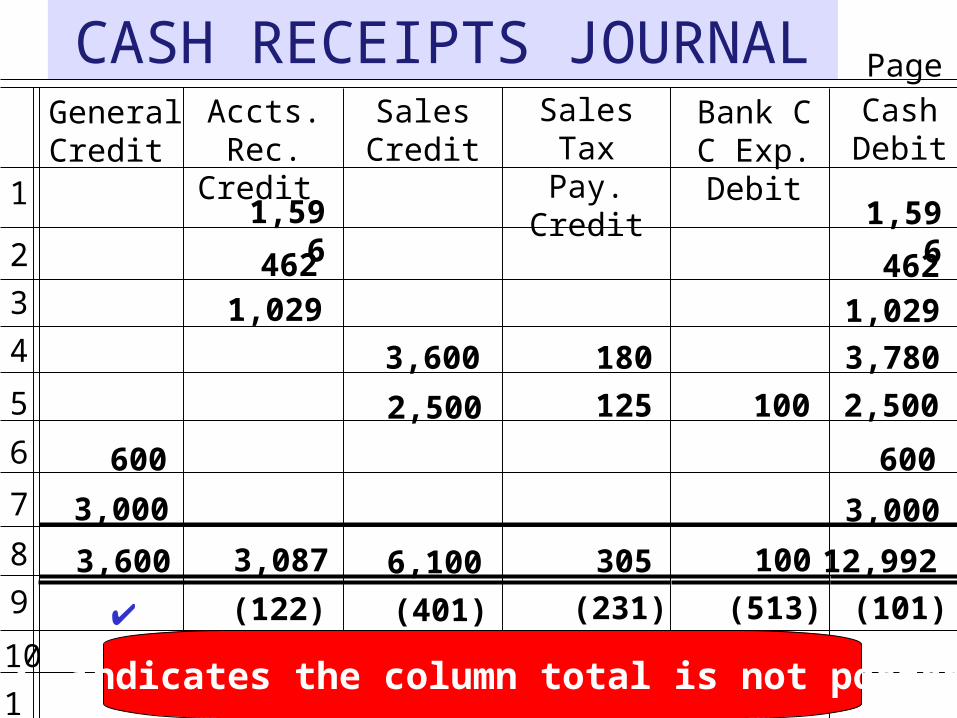

Each column total (except General)is posted at the end of the month.

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

ACCOUNTS RECEIVABLE 122

20--Apr. 1 12,000

30

Balance

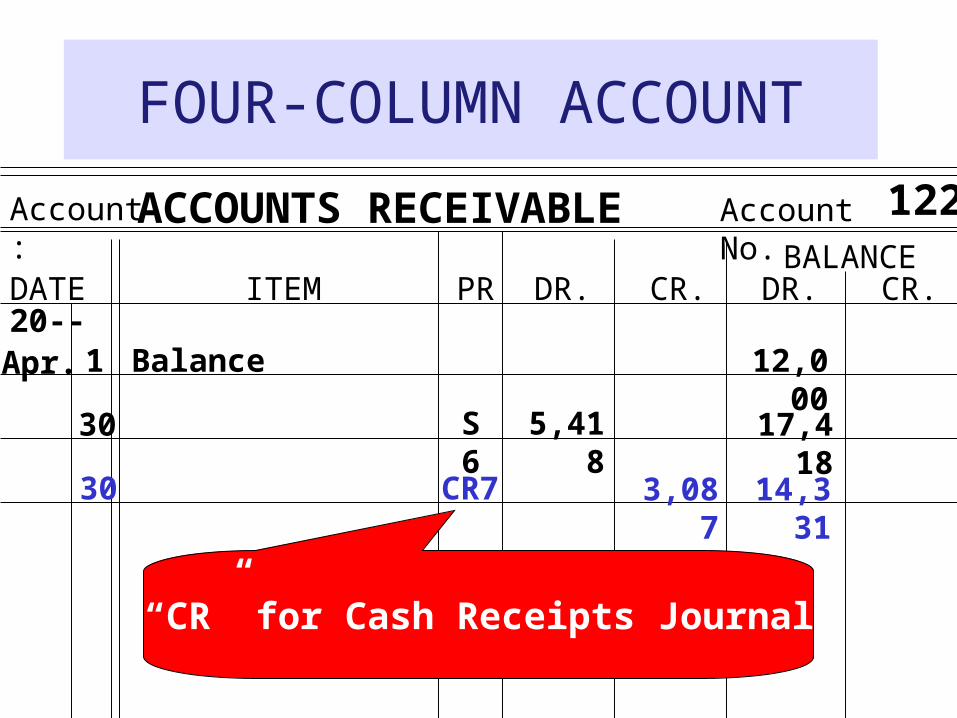

“CR” for Cash Receipts Journal

5,418 17,418S6

30 CR7 3,087 14,331

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

3,600 3,087 6,100 305 100 12,992

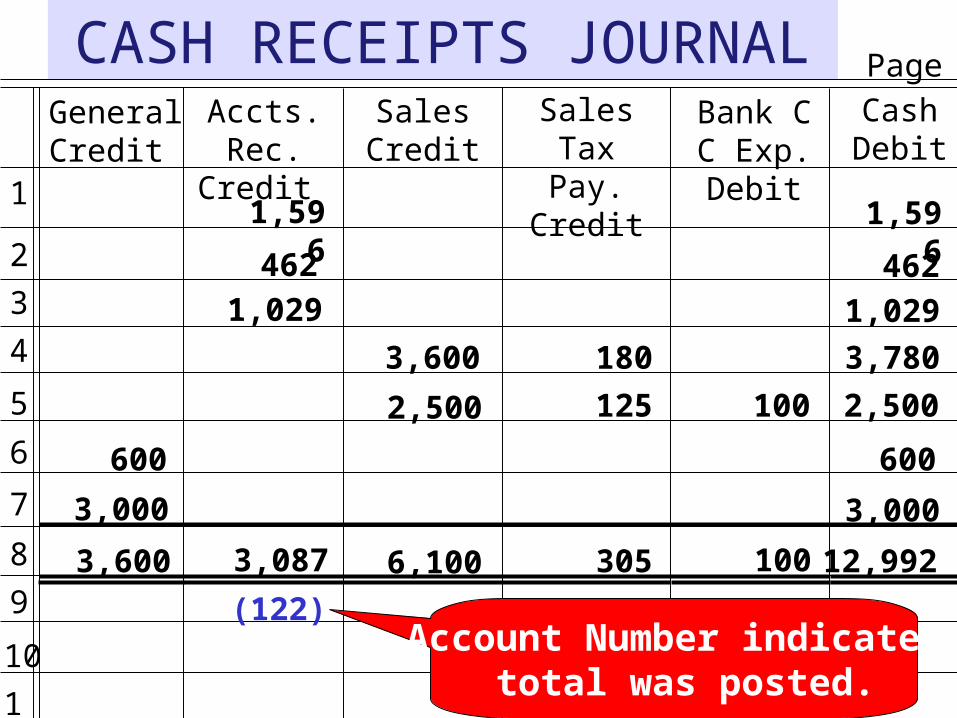

(122)Account Number indicates

total was posted.

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

3,600 3,087 6,100 305 100 12,992

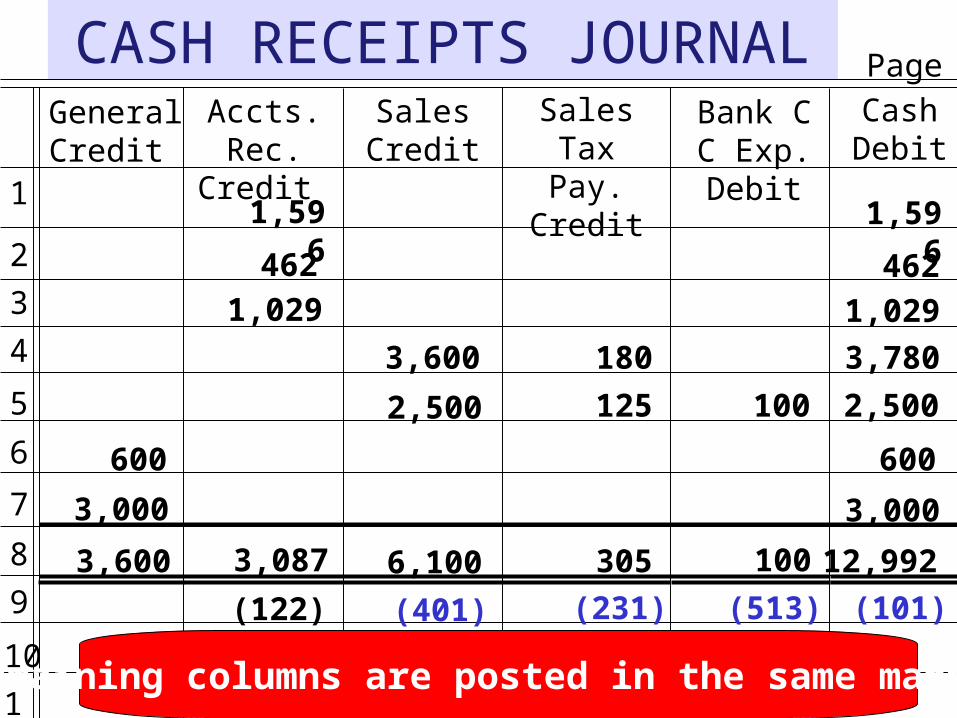

(122) (401) (231) (513) (101)

Remaining columns are posted in the same manner.

CASH RECEIPTS JOURNALBank C C Exp. Debit

1

2

3

4

5

6

7

8

9

10

11

Page 7

Cash Debit

1,596

Sales Tax Pay. Credit

Sales Credit

Accts. Rec. Credit

General Credit

1,596

462462

1,0291,029

3,600 180 3,780

2,500 125 100 2,500

600 600

3,000 3,000

3,600 3,087 6,100 305 100 12,992

(122) (401) (231) (513) (101)

“” indicates the column total is not posted.

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

Postings to the subsidiary Accounts Receivable ledger are made daily.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

412

201

3,600 3,087

ACCOUNTS RECEIVABLE LEDGER

Name:

DATE ITEM PR DEBIT CREDITBALANCE

Enrico Lorenzo

20--Apr. 1,5964

Address: 5240 Tousley Court, Indianapolis, IN 46224-5678

1,596S6

14 1,596CR7

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

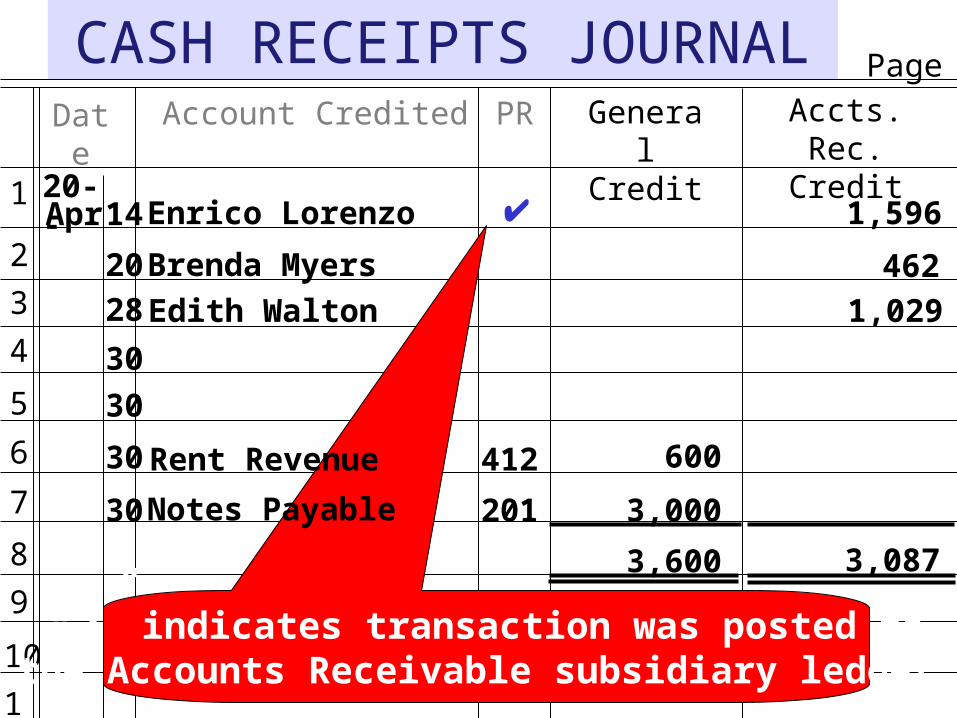

“” indicates transaction was posted tothe Accounts Receivable subsidiary ledger.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

412

201

3,600 3,087

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

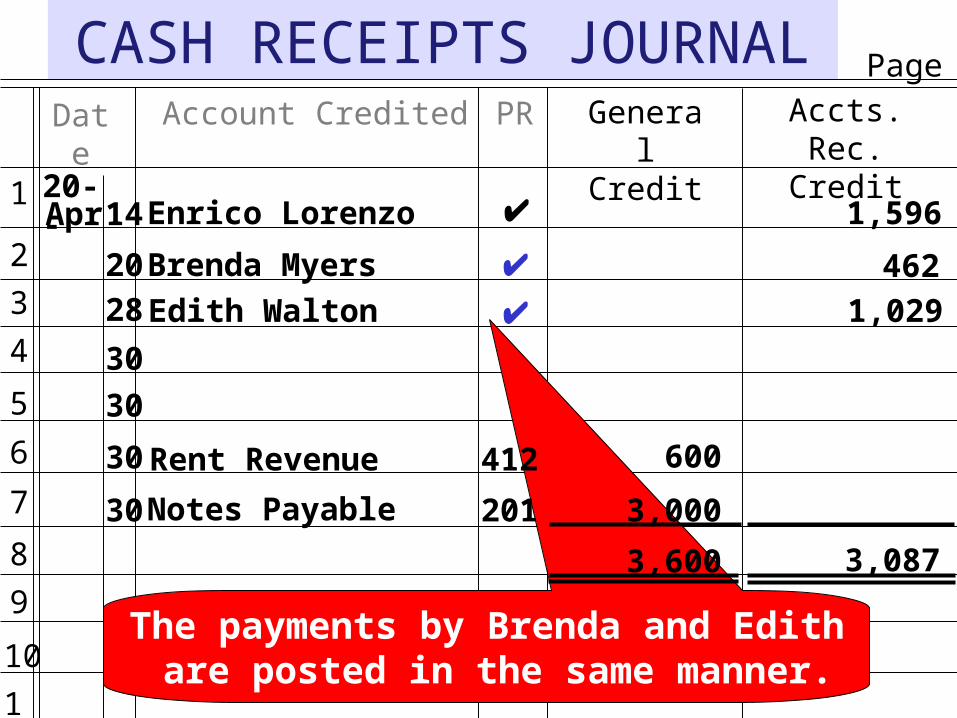

The payments by Brenda and Edith are posted in the same manner.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

412

201

3,600 3,087

CASH RECEIPTS JOURNALDate Account Credited PR General

Credit1

2

3

4

5

6

7

8

9

10

11

Page 7

Accts. Rec. Credit

Apr20--

14 Enrico Lorenzo 1,596

20 Brenda Myers 46228 Edith Walton 1,029

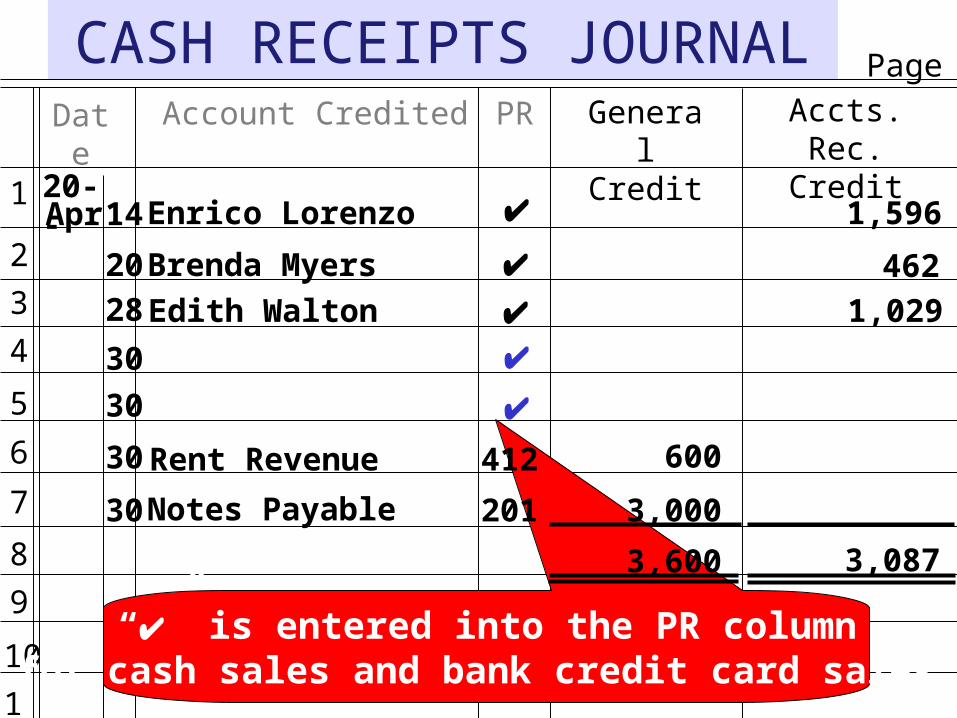

“” is entered into the PR columnfor cash sales and bank credit card sales.

30

30

30 600Rent Revenue

30 Notes Payable 3,000

412

201

3,600 3,087

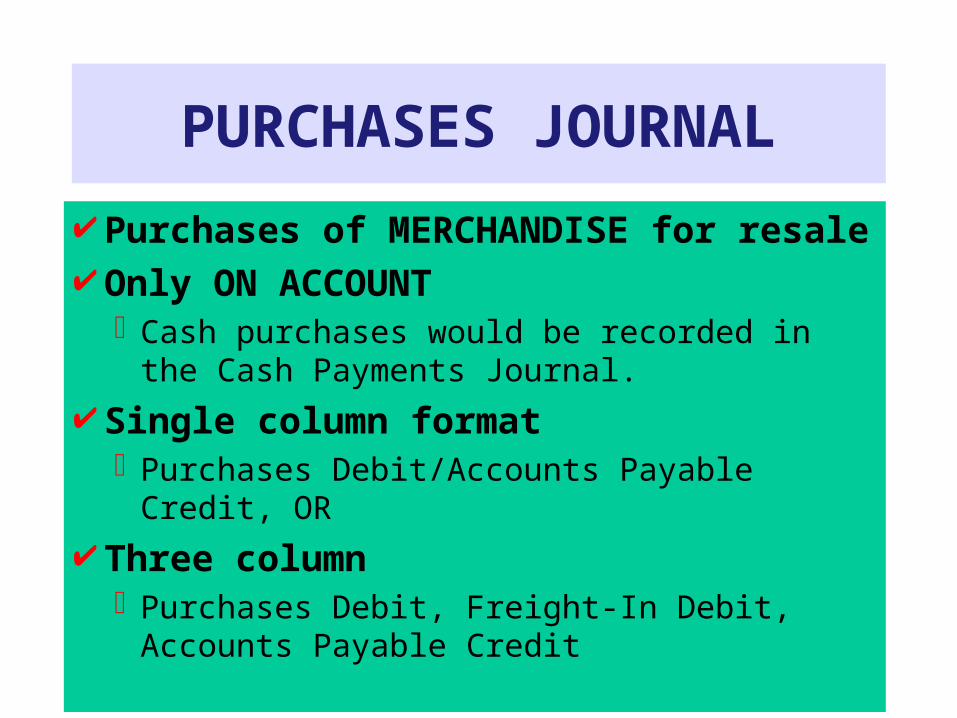

PURCHASES JOURNAL

Purchases of MERCHANDISE for resale Only ON ACCOUNT

Cash purchases would be recorded in the Cash Payments Journal.

Single column formatPurchases Debit/Accounts Payable Credit, OR

Three columnPurchases Debit, Freight-In Debit, Accounts

Payable Credit

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

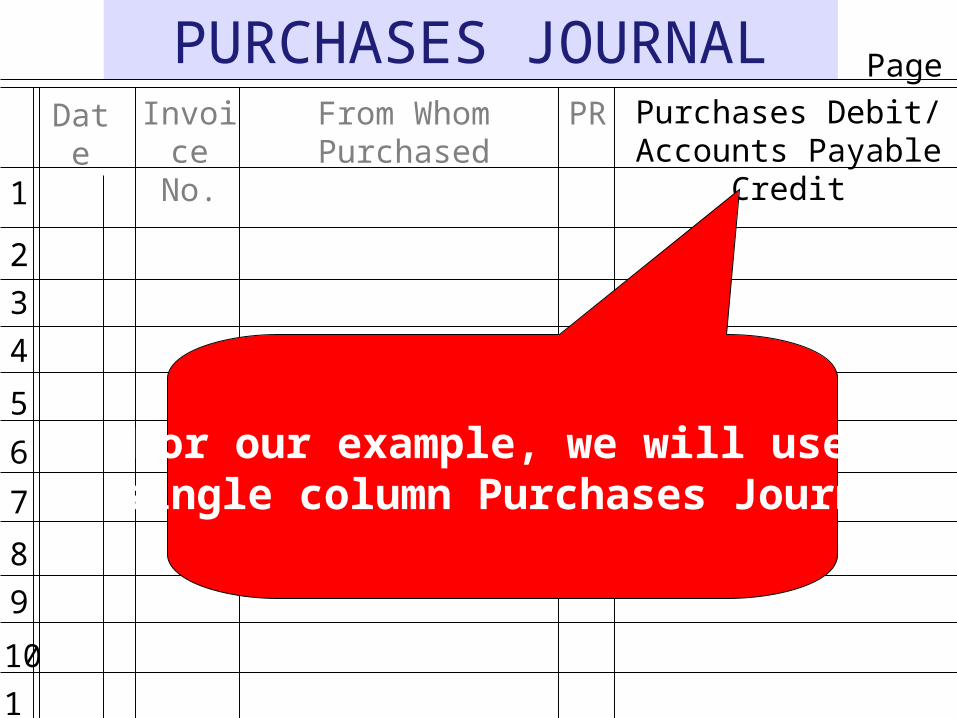

For our example, we will use a single column Purchases Journal.

Page 8

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

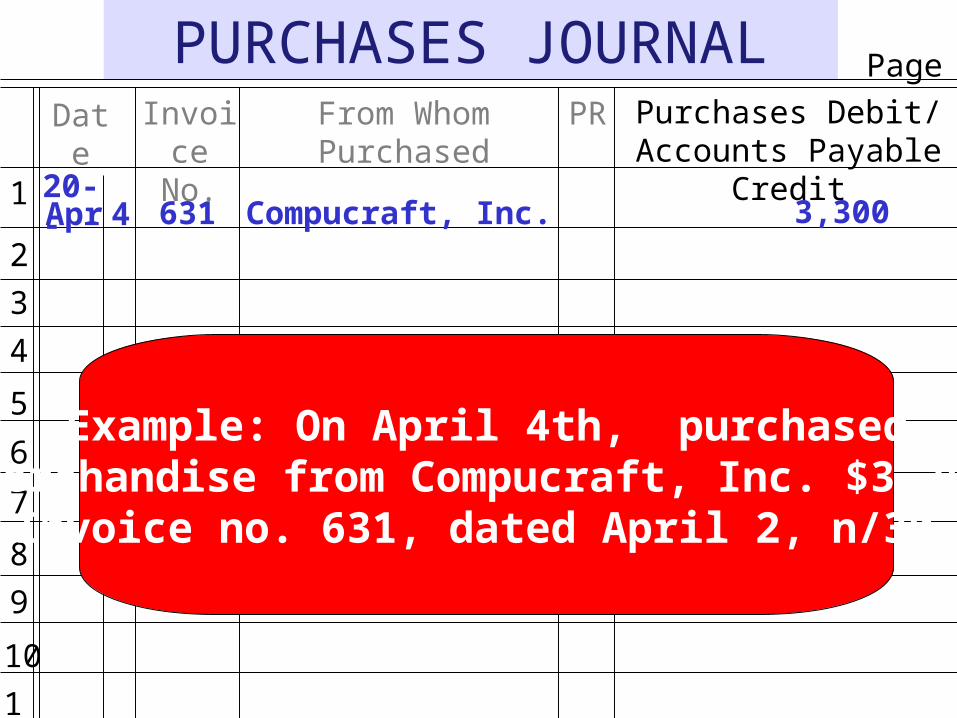

Example: On April 4th, purchasedmerchandise from Compucraft, Inc. $3,300

Invoice no. 631, dated April 2, n/30.

Page 8

20--Apr 4 631 Compucraft, Inc. 3,300

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

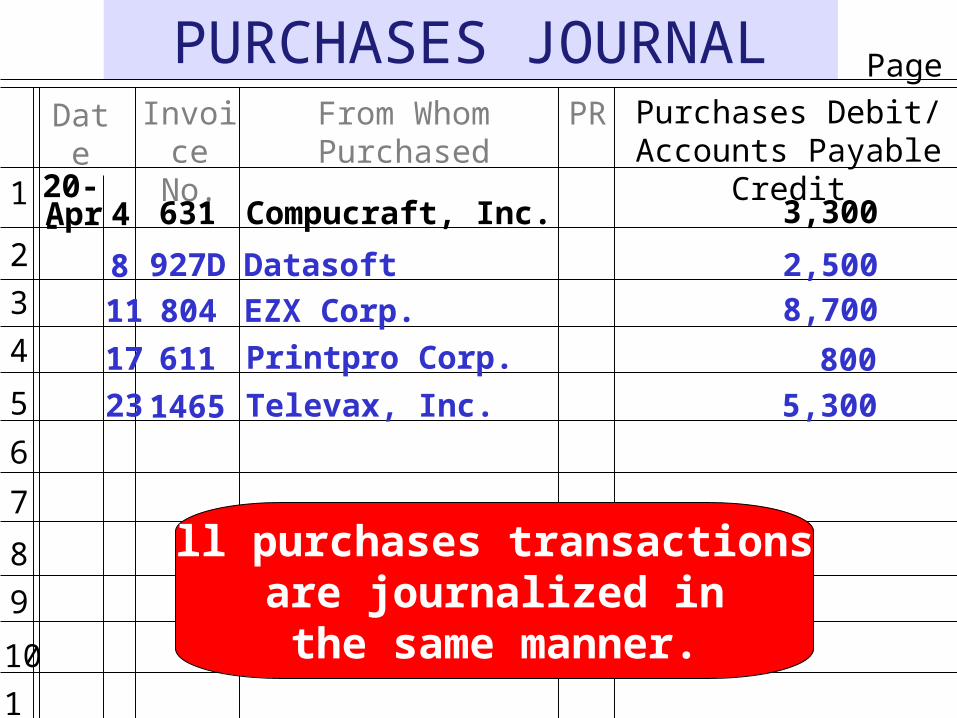

All purchases transactions are journalized inthe same manner.

Page 8

20--Apr 4 631 Compucraft, Inc. 3,300

8 927D Datasoft 2,500

11 804 EZX Corp. 8,700

17 611 Printpro Corp. 800

23 1465 Televax, Inc. 5,300

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

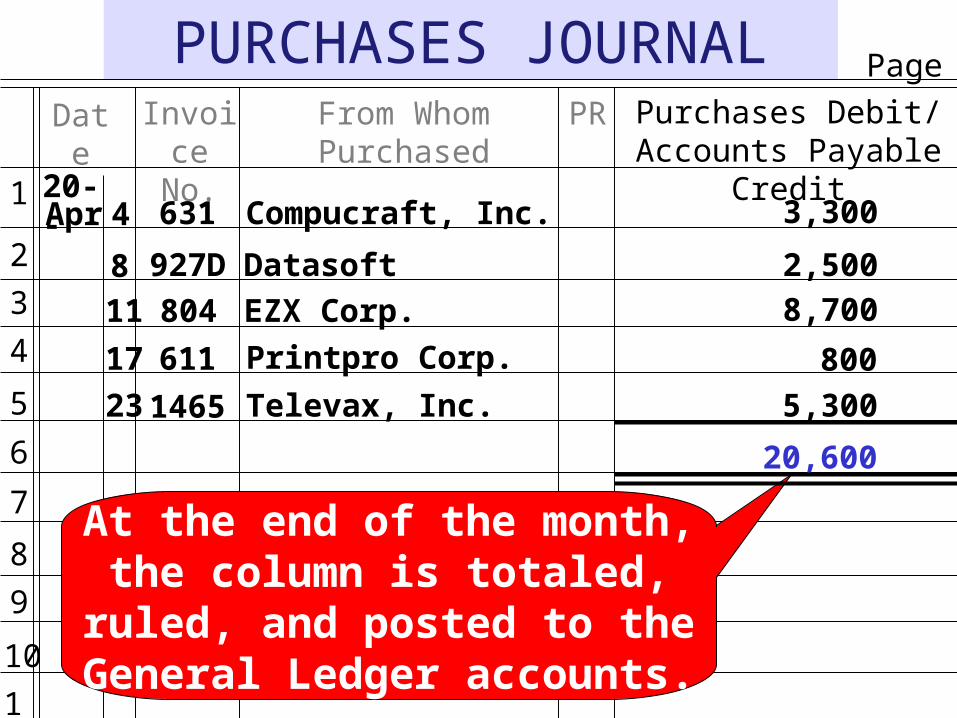

At the end of the month,the column is totaled,

ruled, and posted to theGeneral Ledger accounts.

Page 8

20--Apr 4 631 Compucraft, Inc. 3,300

8 927D Datasoft 2,500

11 804 EZX Corp. 8,700

17 611 Printpro Corp. 800

23 1465 Televax, Inc. 5,300

20,600

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

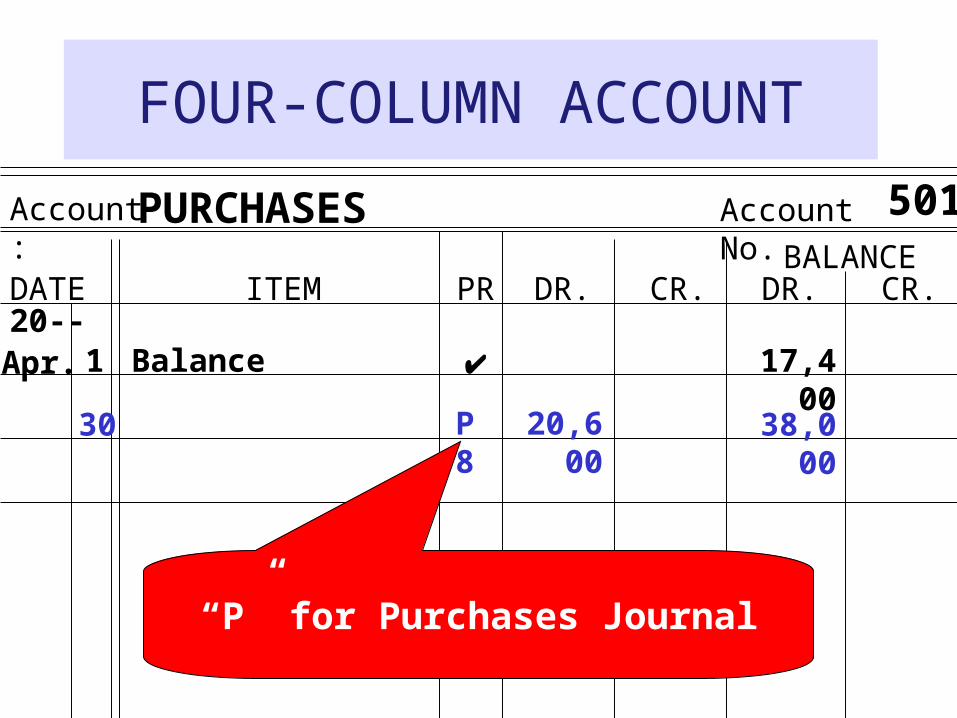

PURCHASES 501

20--Apr. 1 17,400

30

Balance

“P” for Purchases Journal

20,600 38,000P8

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

Page 8

20--Apr 4 631 Compucraft, Inc. 3,300

8 927D Datasoft 2,500

11 804 EZX Corp. 8,700

17 611 Printpro Corp. 800

23 1465 Televax, Inc. 5,300

20,600

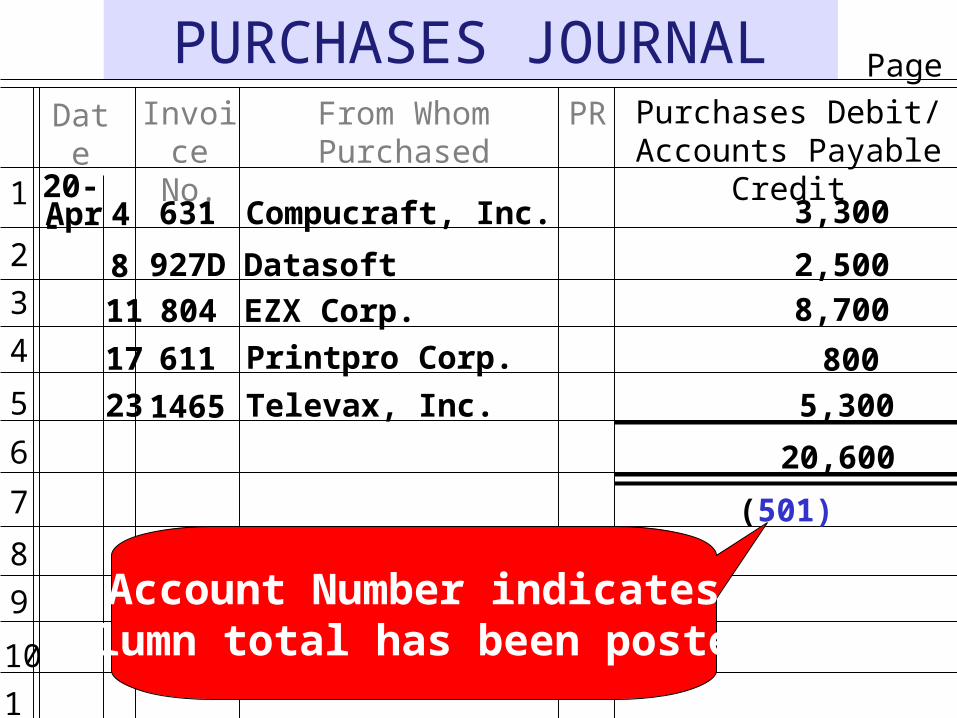

(501)

Account Number indicatescolumn total has been posted.

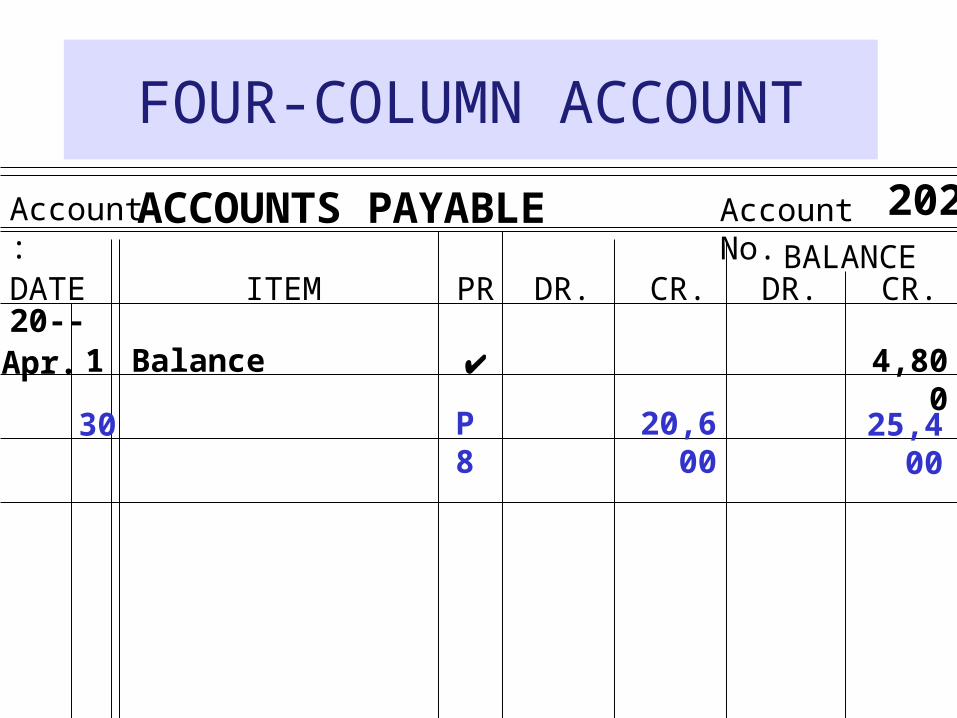

FOUR-COLUMN ACCOUNT

Account: Account No.

DATE ITEM PR DR. CR.BALANCE

DR. CR.

ACCOUNTS PAYABLE 202

20--Apr. 1 4,800

30

Balance

20,600 25,400P8

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

Page 8

20--Apr 4 631 Compucraft, Inc. 3,300

8 927D Datasoft 2,500

11 804 EZX Corp. 8,700

17 611 Printpro Corp. 800

23 1465 Televax, Inc. 5,300

20,600

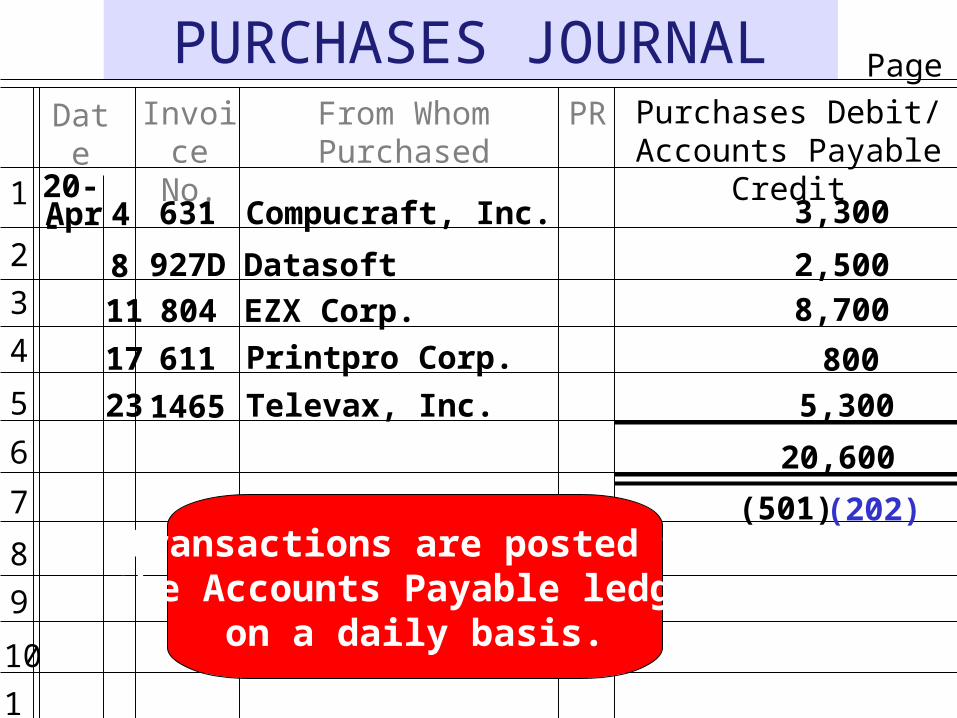

(501) (202)Transactions are posted to

the Accounts Payable ledgeron a daily basis.

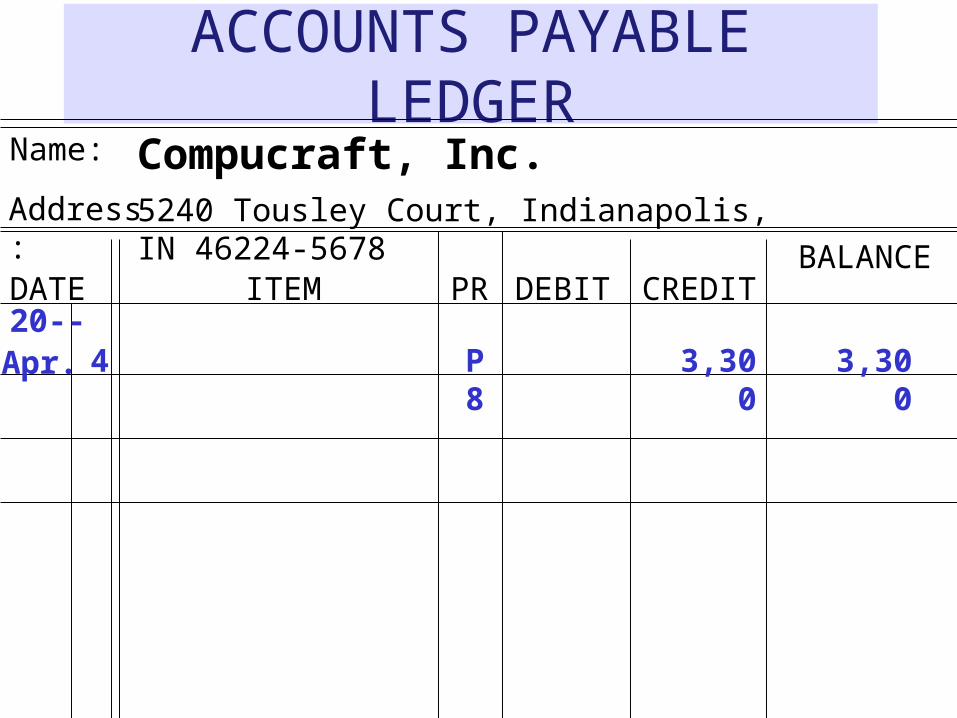

ACCOUNTS PAYABLE LEDGER

Name:

DATE ITEM PR DEBIT CREDITBALANCE

Compucraft, Inc.

20--Apr. 3,3004

Address: 5240 Tousley Court, Indianapolis, IN 46224-5678

3,300P8

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

Page 8

20--Apr 4 631 Compucraft, Inc. 3,300

8 927D Datasoft 2,500

11 804 EZX Corp. 8,700

17 611 Printpro Corp. 800

23 1465 Televax, Inc. 5,300

20,600

(501) (202)

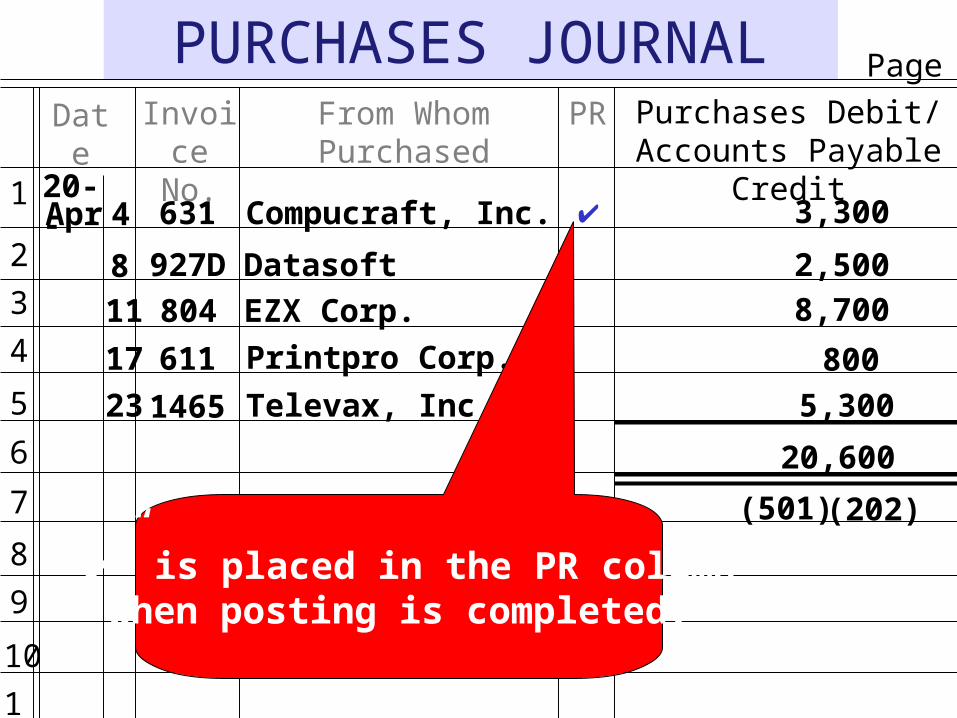

“” is placed in the PR columnwhen posting is completed.

PURCHASES JOURNALDate From Whom Purchased PR Purchases Debit/

Accounts Payable Credit1

2

3

4

5

6

7

8

9

10

11

Invoice No.

Page 8

20--Apr 4 631 Compucraft, Inc. 3,300

8 927D Datasoft 2,500

11 804 EZX Corp. 8,700

17 611 Printpro Corp. 800

23 1465 Televax, Inc. 5,300

20,600

(501) (202)

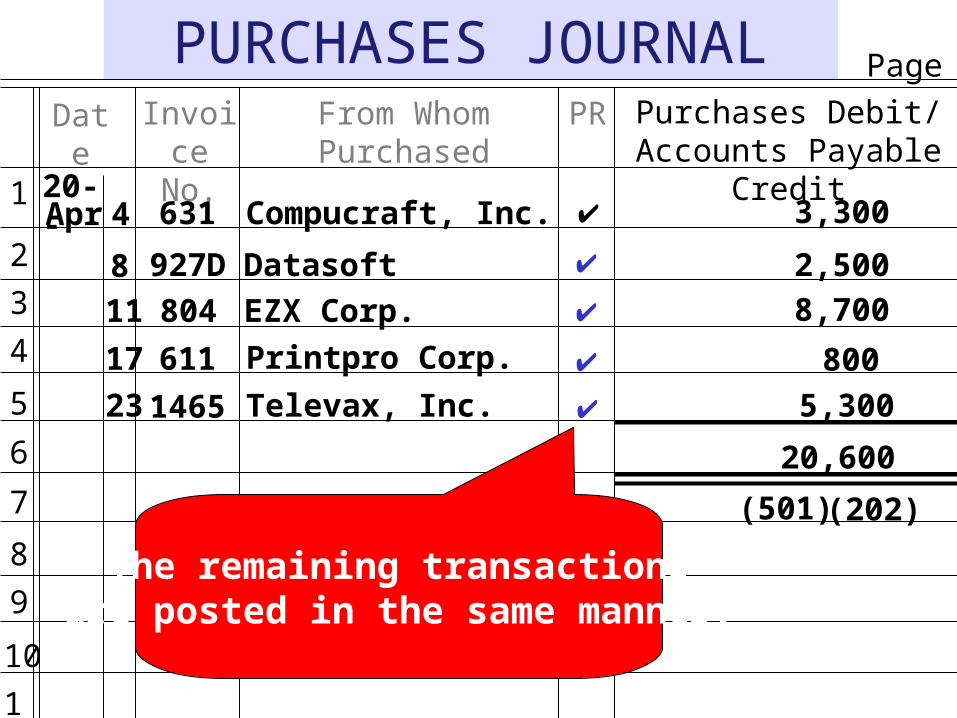

The remaining transactionsare posted in the same manner.

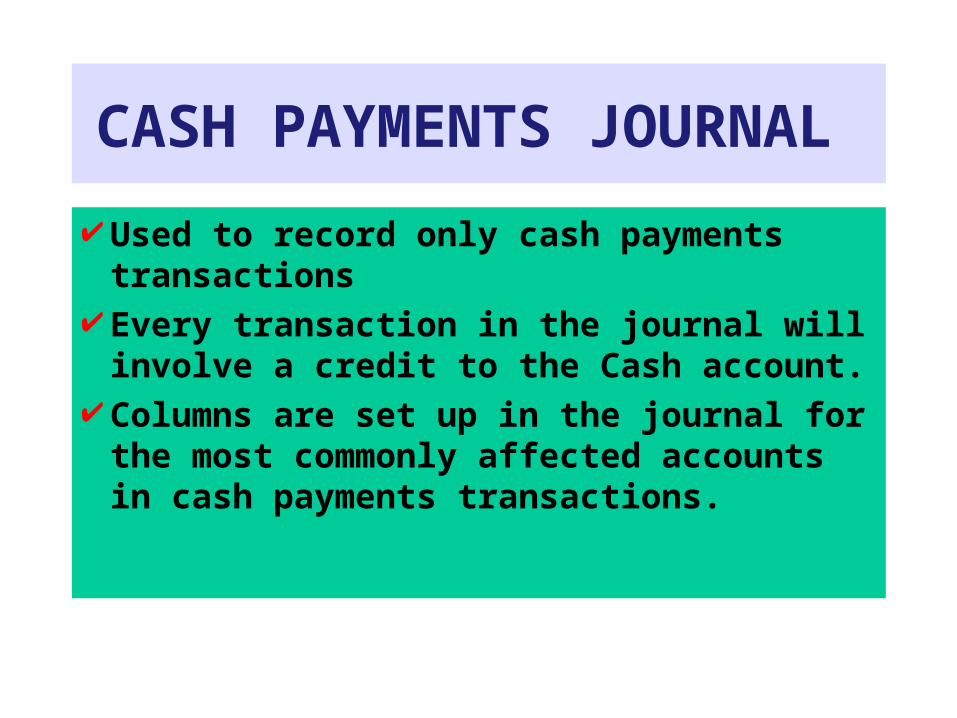

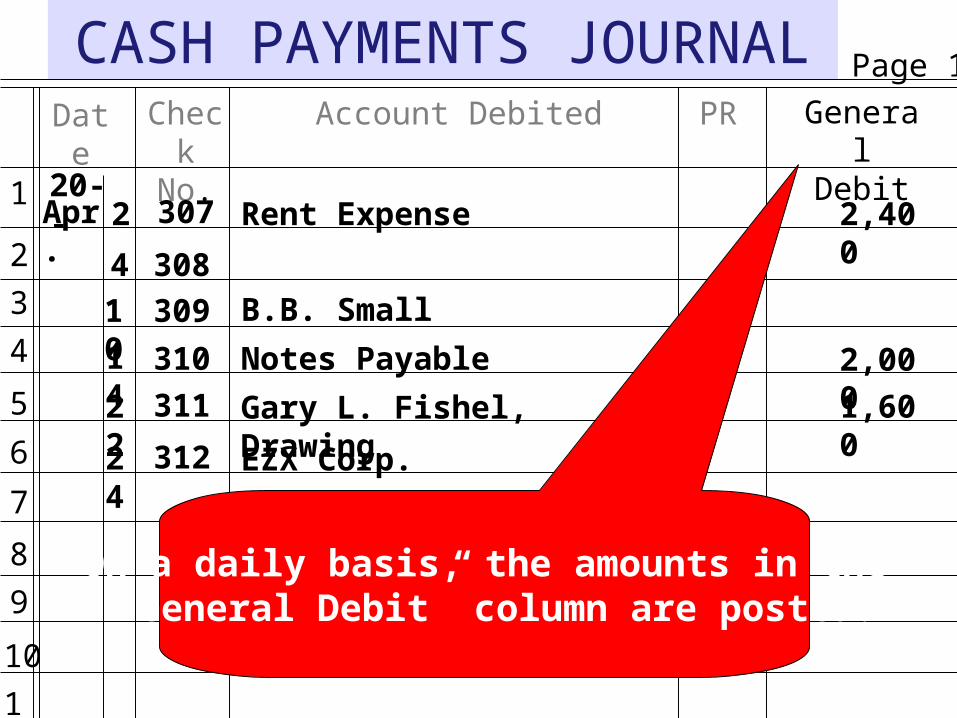

CASH PAYMENTS JOURNAL

Used to record only cash payments transactions

Every transaction in the journal will involve a credit to the Cash account.

Columns are set up in the journal for the most commonly affected accounts in cash payments transactions.

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

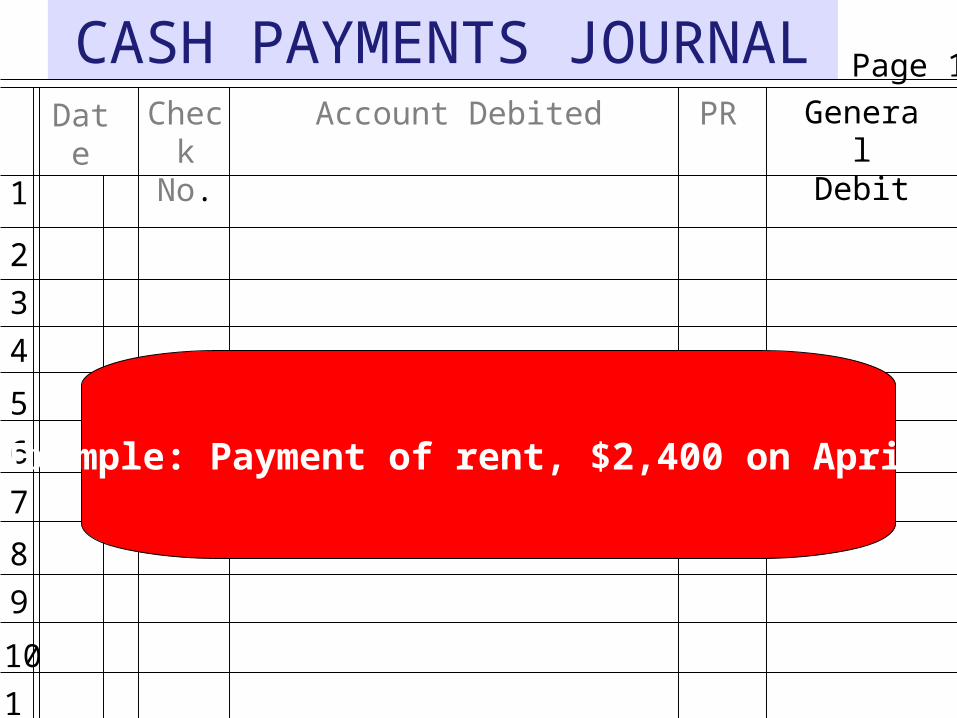

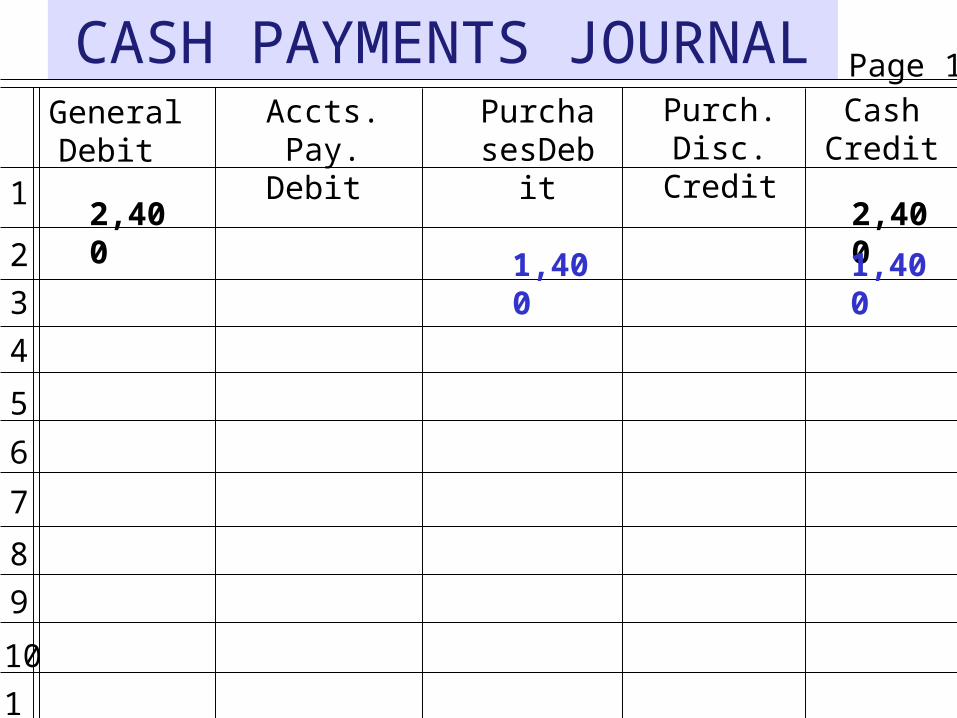

Example: Payment of rent, $2,400 on April 2

Check No.

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

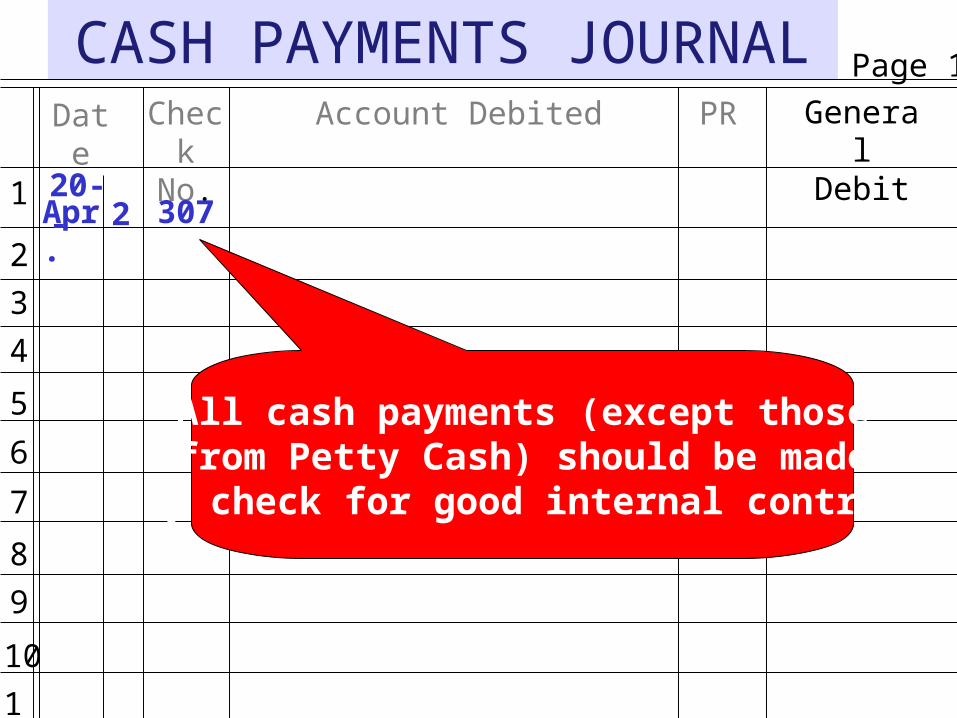

All cash payments (except thosefrom Petty Cash) should be made

by check for good internal control.

20--Apr. 2

Check No.

307

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

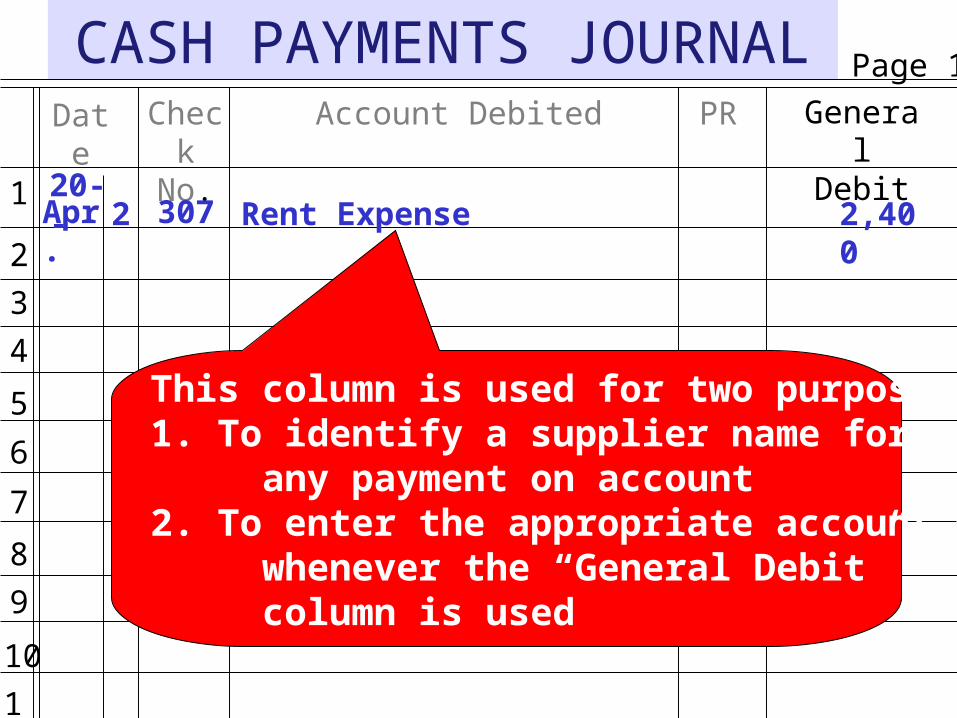

This column is used for two purposes:1. To identify a supplier name for any payment on account2. To enter the appropriate account name whenever the “General Debit” column is used

20--Apr. 2

Check No.

307 2,400Rent Expense

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

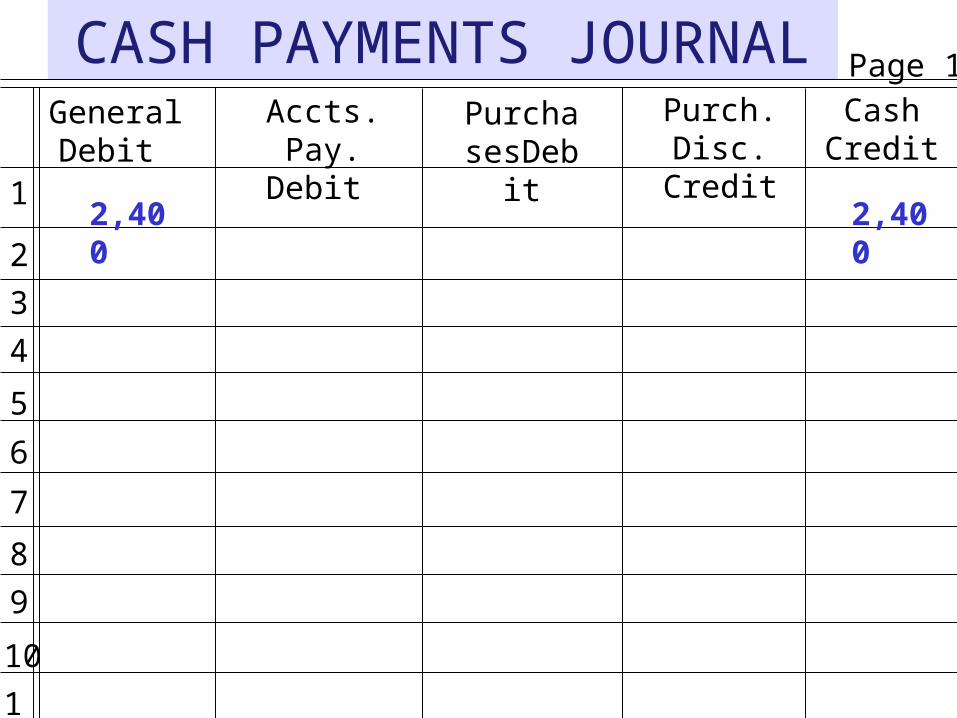

2,4002,400

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

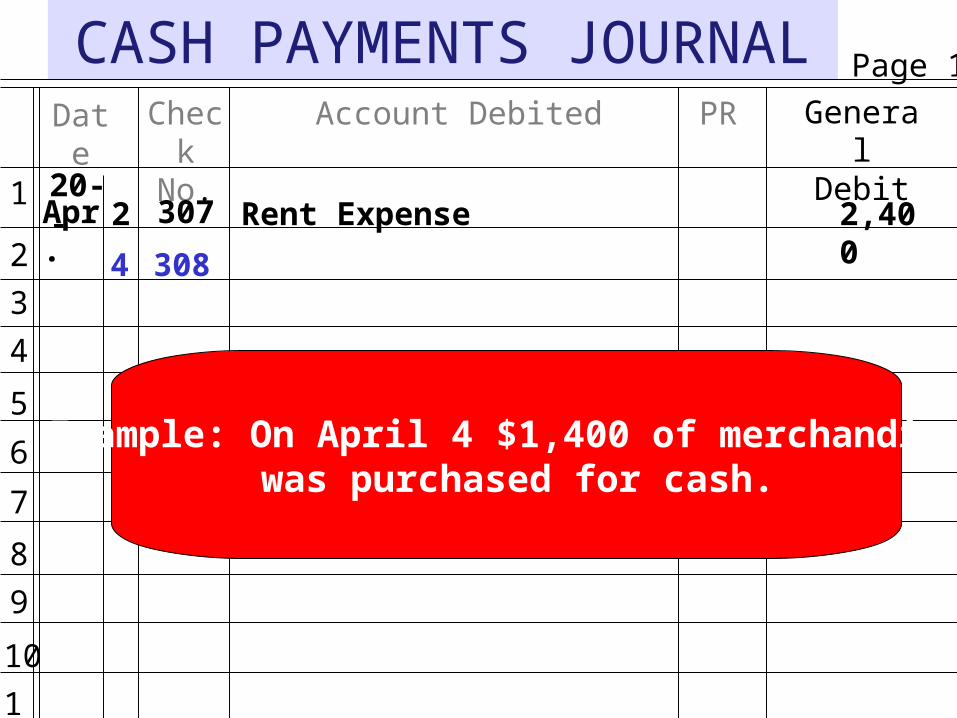

Example: On April 4 $1,400 of merchandise was purchased for cash.

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

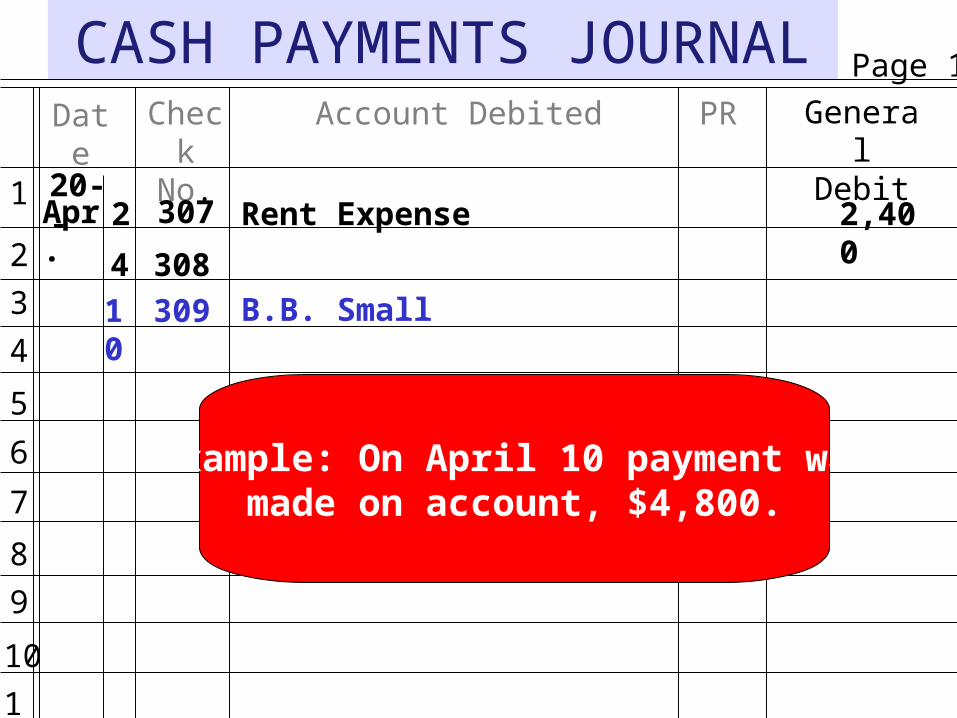

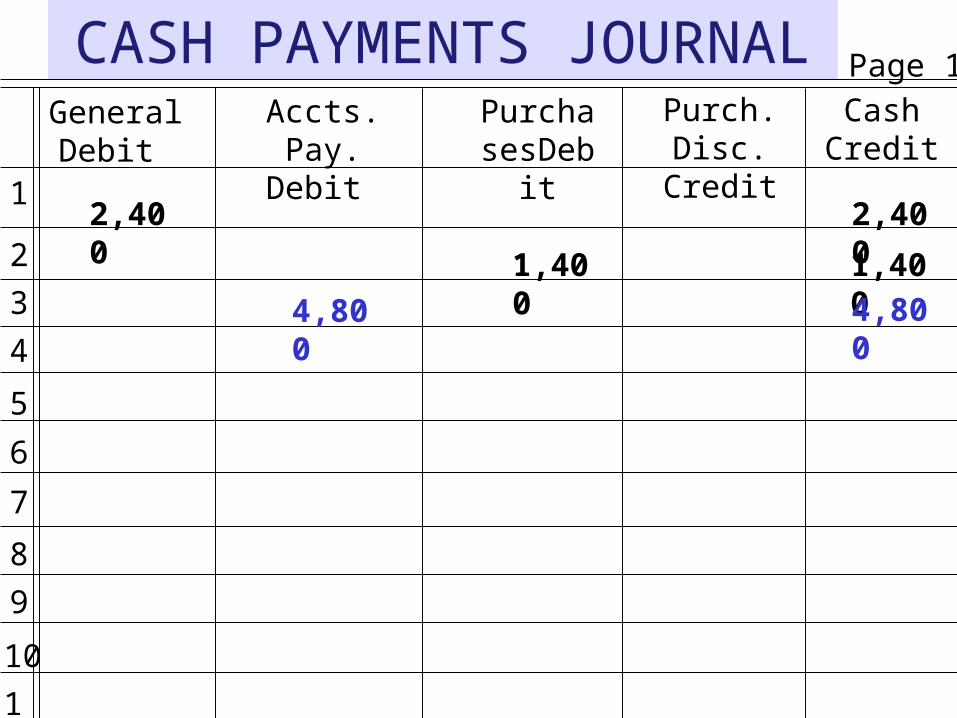

Example: On April 10 payment wasmade on account, $4,800.

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

4,800 4,800

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

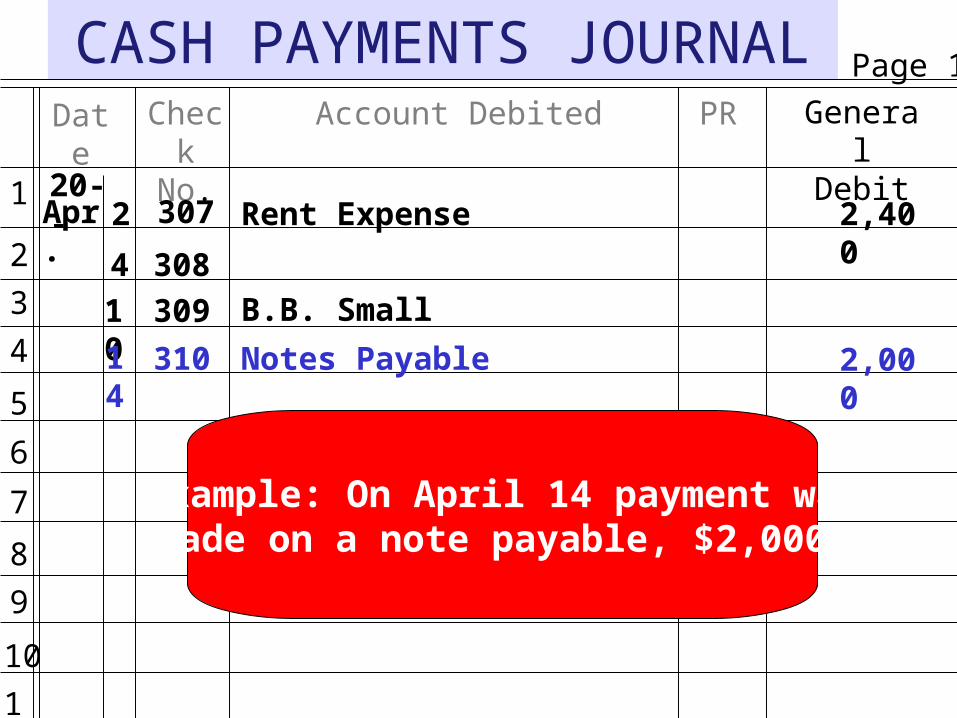

14 310 Notes Payable

Example: On April 14 payment wasmade on a note payable, $2,000.

2,000

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

4,800 4,800

2,0002,000

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

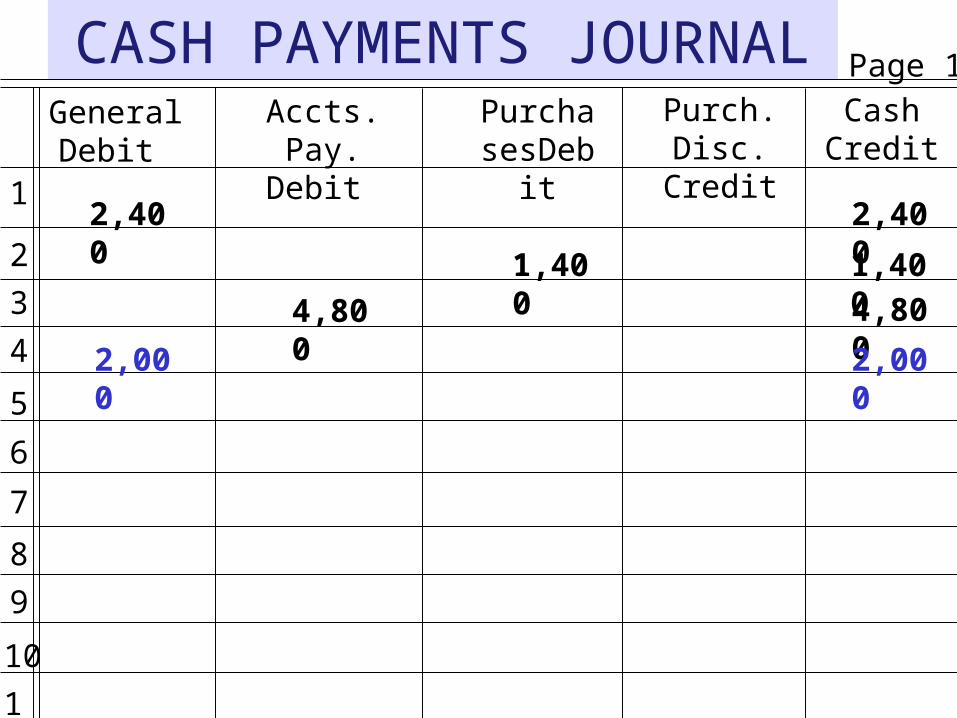

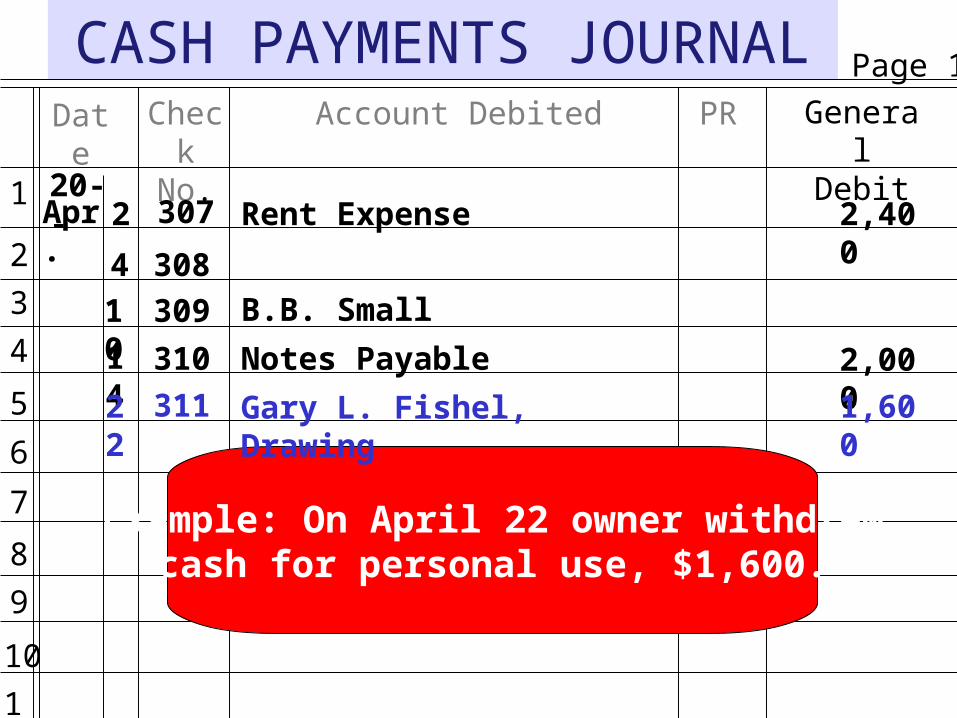

Example: On April 22 owner withdrewcash for personal use, $1,600.

2,000

22 311 Gary L. Fishel, Drawing 1,600

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

4,800 4,800

2,0002,000

1,6001,600

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

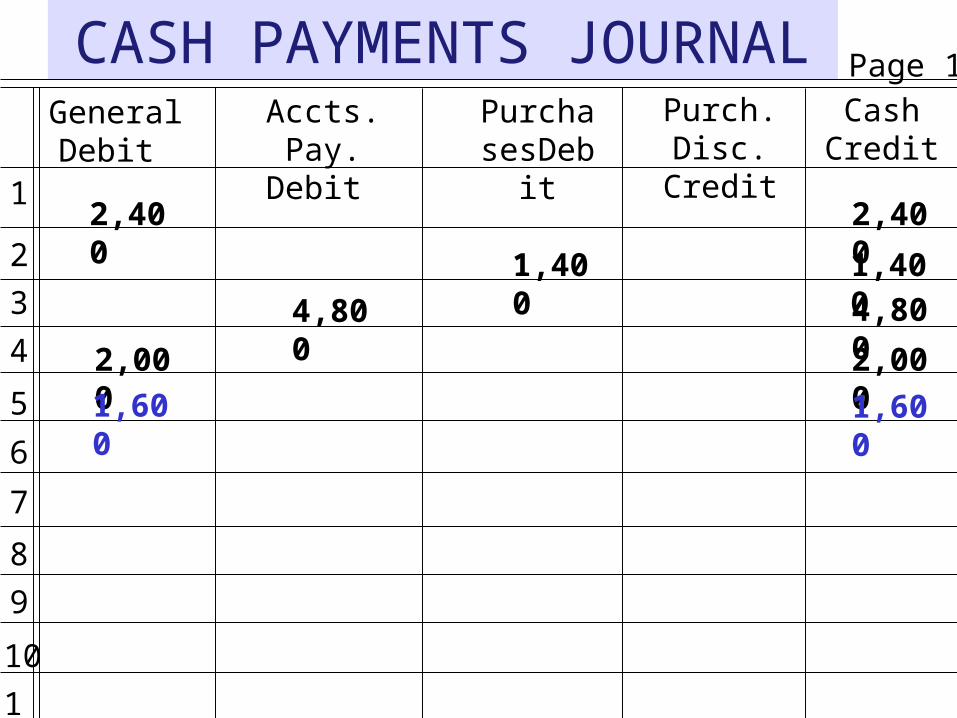

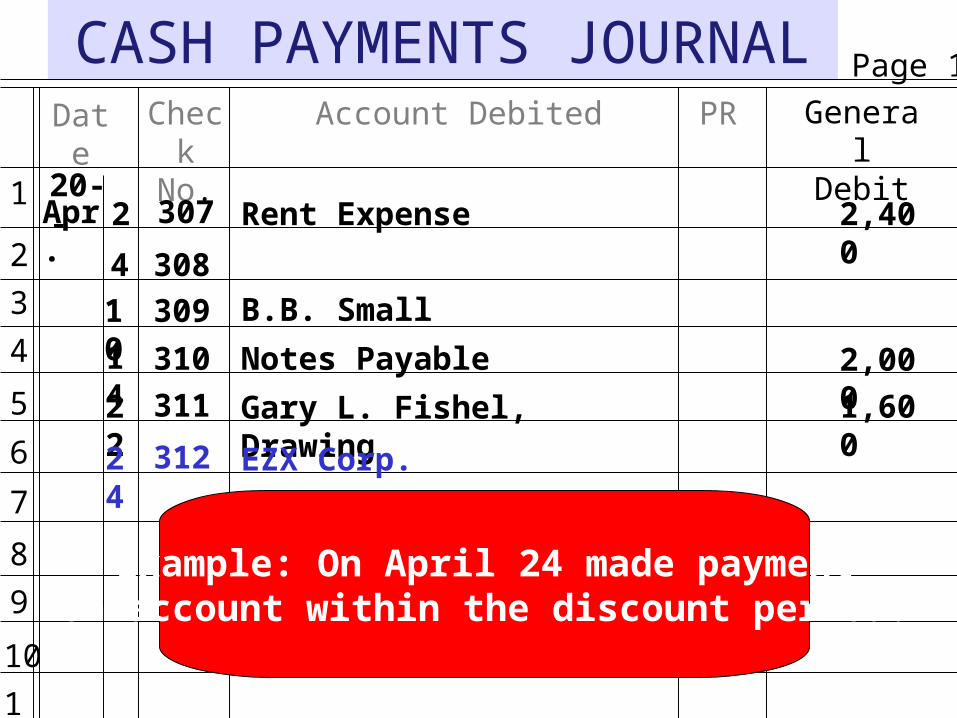

Example: On April 24 made paymenton account within the discount period.

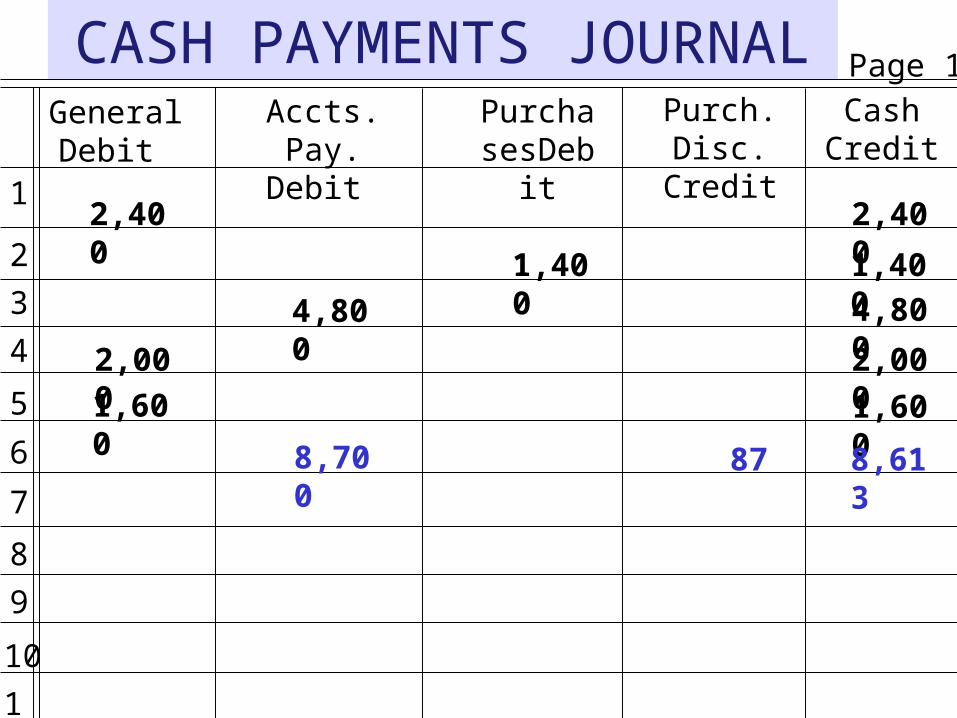

2,000

22 311 Gary L. Fishel, Drawing 1,600

24 312 EZX Corp.

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

4,800 4,800

2,0002,000

1,6001,600

8,700 87 8,613

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

On a daily basis, the amounts in the “General Debit” column are posted.

2,000

22 311 Gary L. Fishel, Drawing 1,600

24 312 EZX Corp.

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

“CP” for Cash Payments journal is entered in the ledger account’s PR column,and the account number is entered

in the journal’s PR column.

2,000

22 311 Gary L. Fishel, Drawing 1,600

24 312 EZX Corp.

521

201

312

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

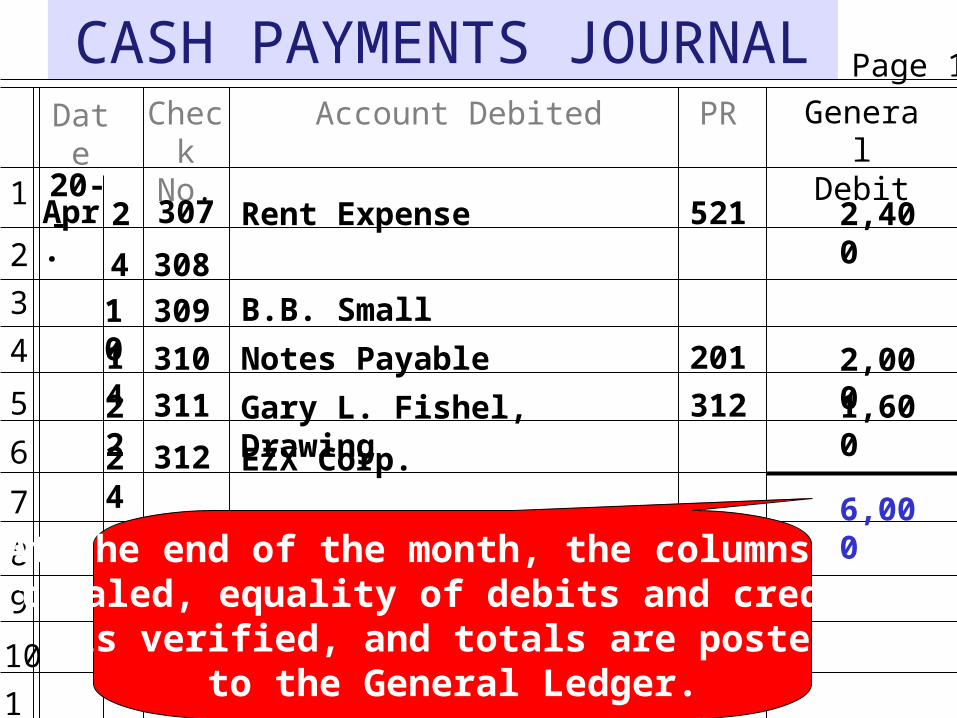

At the end of the month, the columns aretotaled, equality of debits and credits

is verified, and totals are postedto the General Ledger.

2,000

22 311 Gary L. Fishel, Drawing 1,600

24 312 EZX Corp.

521

201

312

6,000

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

4,800 4,800

2,0002,000

1,6001,600

8,700 87 8,613

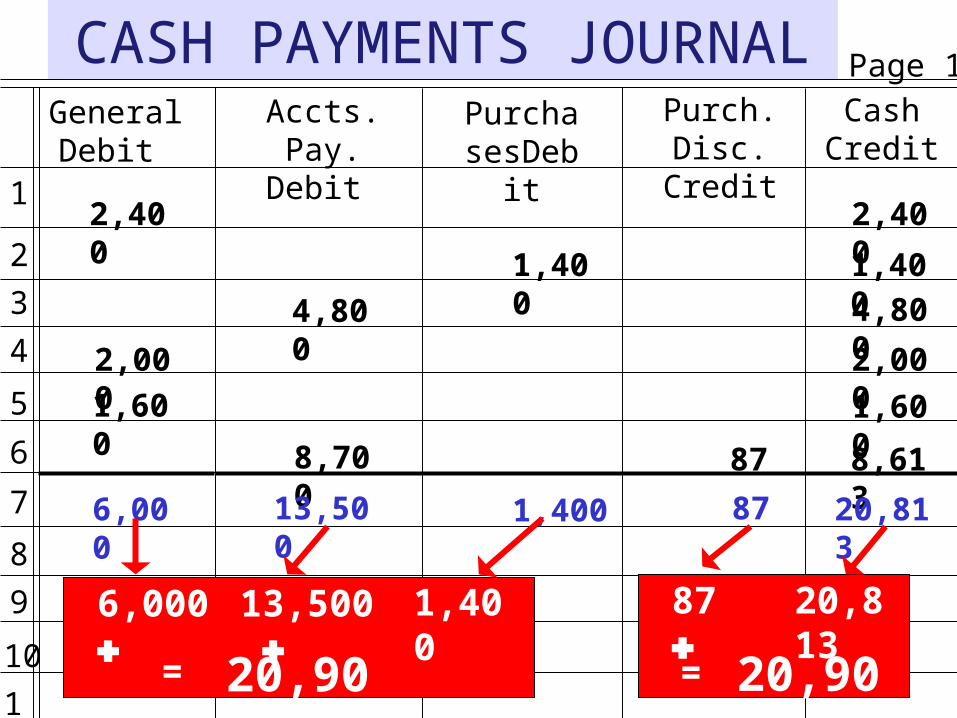

6,000 13,500 1,400 87 20,813

6,000 13,500 1,400

= 20,900

87 20,813

= 20,900

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

4,800 4,800

2,0002,000

1,6001,600

8,700 87 8,613

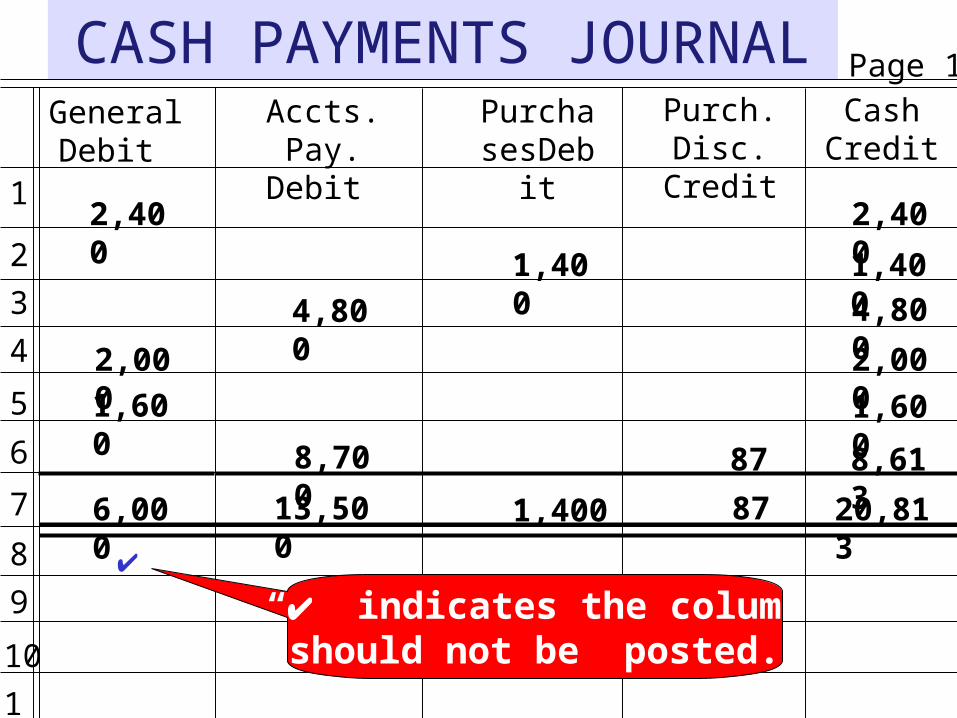

6,000 13,500 1,400 87 20,813

“” indicates the column

should not be posted.

CASH PAYMENTS JOURNAL

1

2

3

4

5

6

7

8

9

10

11

Page 12

Cash Credit

Purch. Disc. Credit

PurchasesDebit

Accts. Pay. Debit

General Debit

2,4002,400

1,400 1,400

4,800 4,800

2,0002,000

1,6001,600

8,700 87 8,613

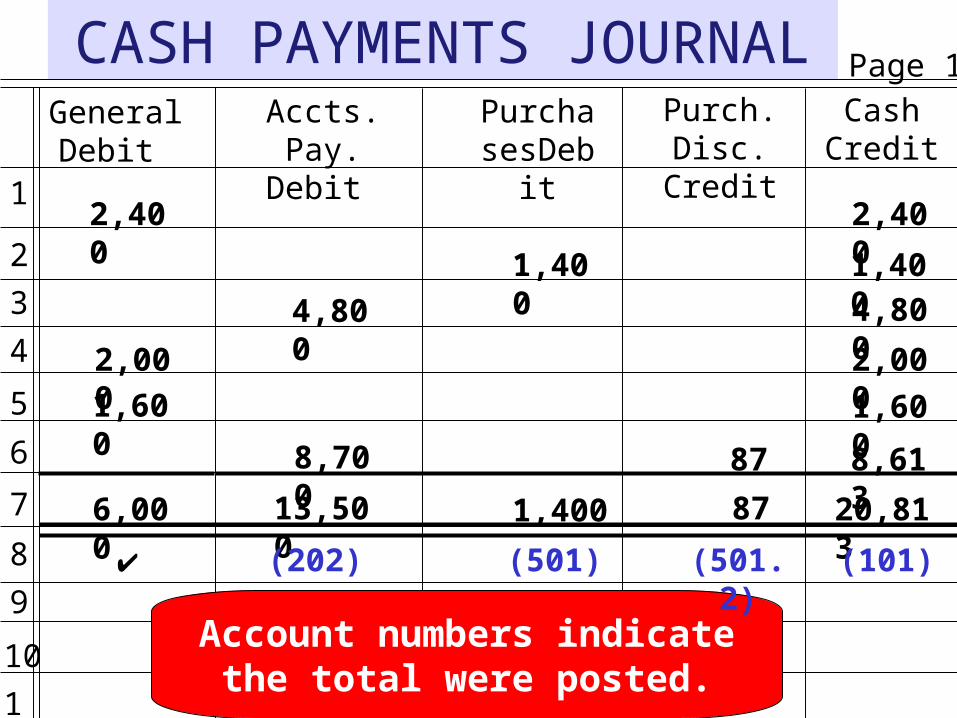

6,000 13,500 1,400 87 20,813

Account numbers indicatethe total were posted.

(202) (501) (501.2) (101)

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

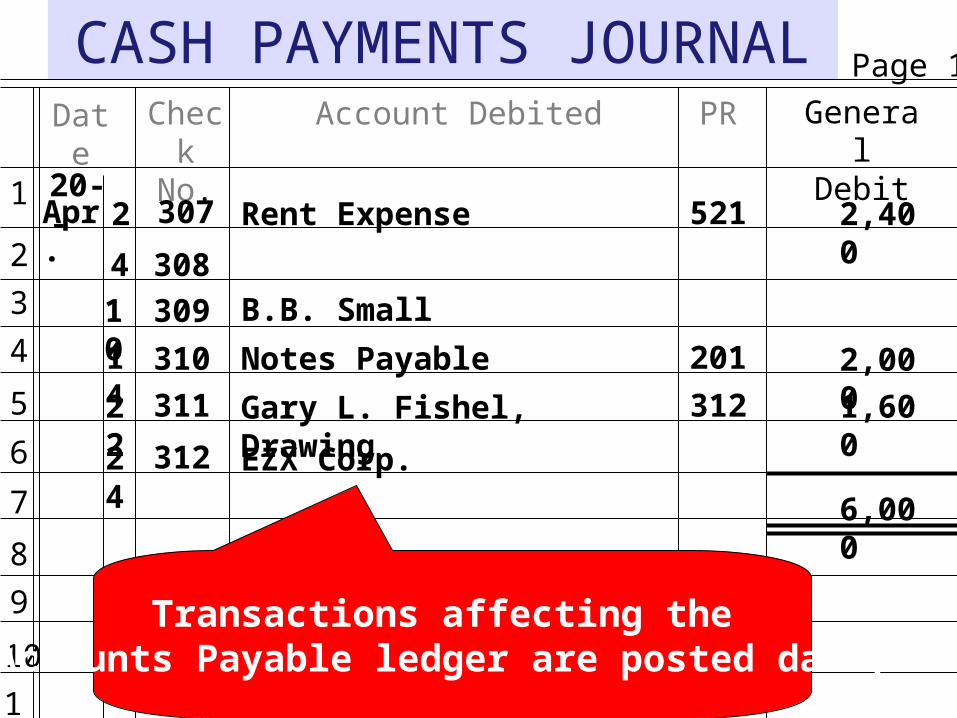

Transactions affecting the Accounts Payable ledger are posted daily.

2,000

22 311 Gary L. Fishel, Drawing 1,600

24 312 EZX Corp.

521

201

312

6,000

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

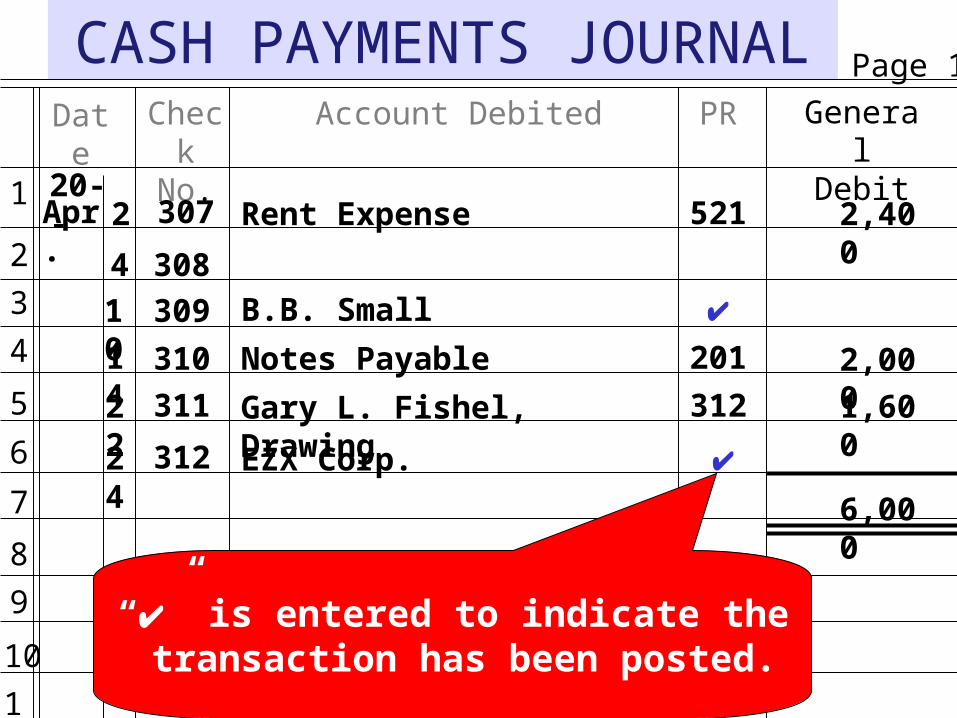

“” is entered to indicate the transaction has been posted.

2,000

22 311 Gary L. Fishel, Drawing 1,600

24 312 EZX Corp.

521

201

312

6,000

CASH PAYMENTS JOURNALDate Account Debited PR General

Debit1

2

3

4

5

6

7

8

9

10

11

Page 12

20--Apr. 2

Check No.

307 2,400Rent Expense

4 308

10 309 B.B. Small

14 310 Notes Payable

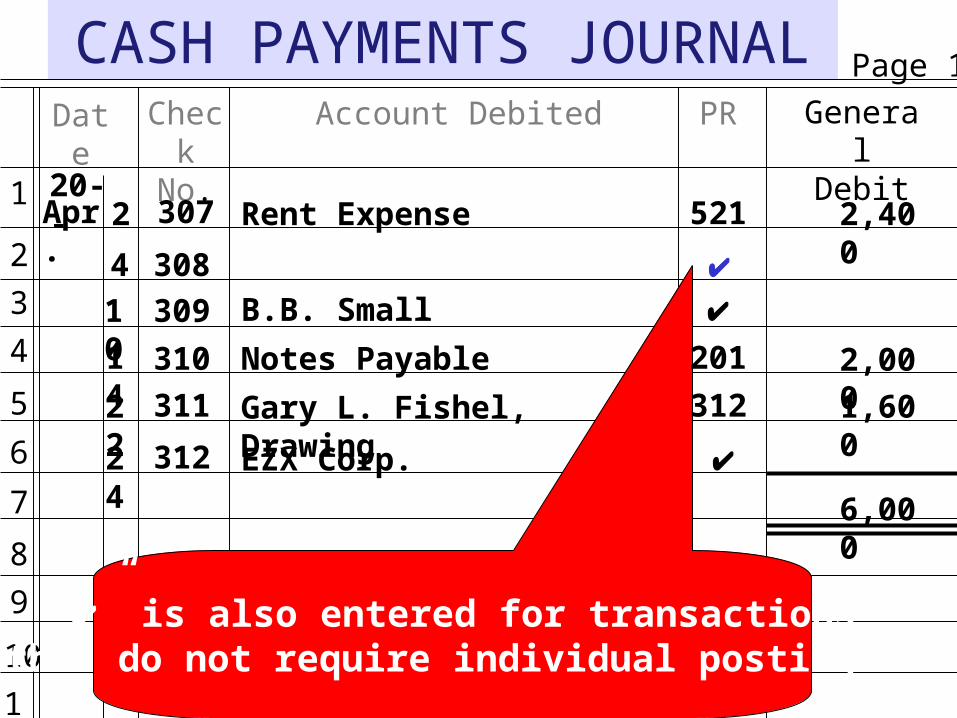

“” is also entered for transactionsthat do not require individual postings.

2,000

22 311 Gary L. Fishel, Drawing 1,600

24 312 EZX Corp.

521

201

312

6,000