Embed Size (px)

Citation preview

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

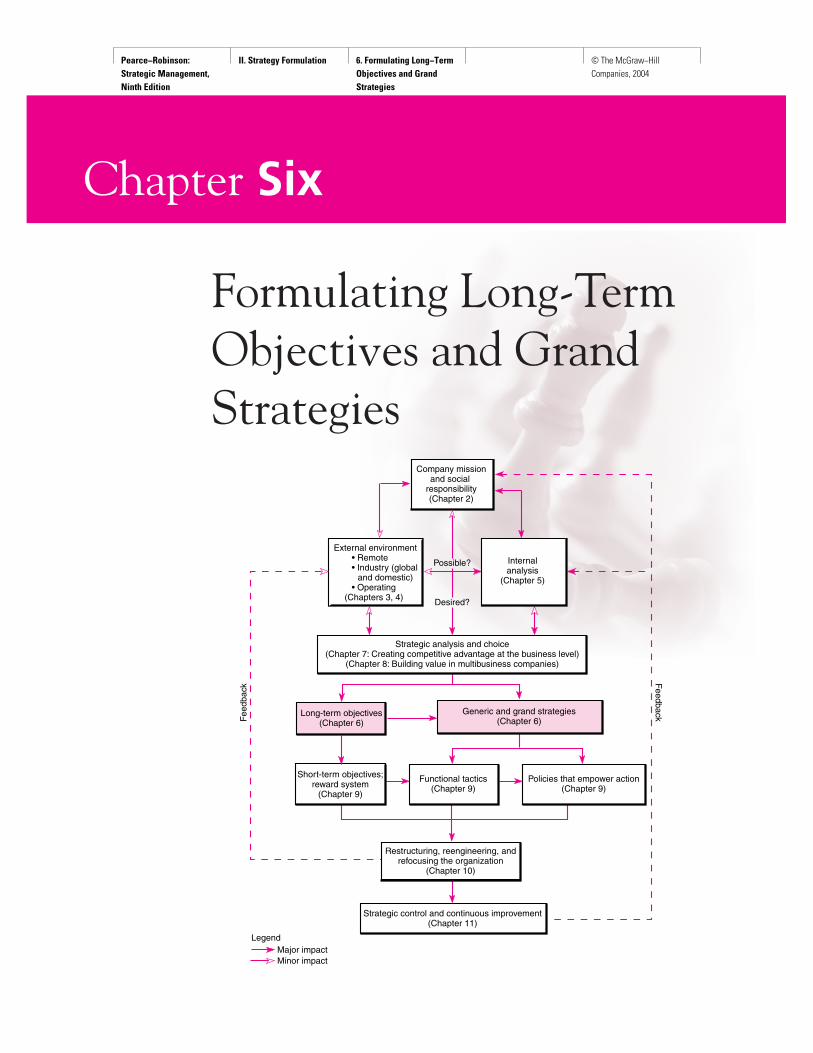

External environment• Remote• Industry (global and domestic)• Operating

(Chapters 3, 4)

Strategic analysis and choice(Chapter 7: Creating competitive advantage at the business level)

(Chapter 8: Building value in multibusiness companies)

Long-term objectives (Chapter 6)

Generic and grand strategies(Chapter 6)

Short-term objectives;reward system

(Chapter 9)

Functional tactics(Chapter 9)

Policies that empower action(Chapter 9)

Strategic control and continuous improvement(Chapter 11)

Fee

dbac

k Feedback

Possible?

Desired?

LegendMajor impactMinor impact

Restructuring, reengineering, andrefocusing the organization

(Chapter 10)

Internalanalysis

(Chapter 5)

Company missionand social

responsibility(Chapter 2)

Chapter Six

Formulating Long-TermObjectives and GrandStrategies

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 191

The company mission was described in Chapter 2 as encompassing the broad aims of thefirm. The most specific statement of aims presented in that chapter appeared as the goalsof the firm. However, these goals, which commonly dealt with profitability, growth, andsurvival, were stated without specific targets or time frames. They were always to be pur-sued but could never be fully attained. They gave a general sense of direction but were notintended to provide specific benchmarks for evaluating the firm’s progress in achieving itsaims. Providing such benchmarks is the function of objectives.1

The first part of this chapter will focus on long-term objectives. These are statements ofthe results a firm seeks to achieve over a specified period, typically three to five years. Thesecond part will focus on the formulation of grand strategies. These provide a comprehen-sive general approach in guiding major actions designed to accomplish the firm’s long-termobjectives.

The chapter has two major aims: (1) to discuss in detail the concept of long-term objec-tives, the topics they cover, and the qualities they should exhibit; and (2) to discuss the con-cept of grand strategies and to describe the 15 principal grand strategy options that areavailable to firms singly or in combination, including three newly popularized options thatare being used to provide the basis for global competitiveness.

LONG-TERM OBJECTIVES

1The terms goals and objectives are each used to convey a special meaning, with goals being the lessspecific and more encompassing concept. Most authors follow this usage; however, some use the twowords interchangeably, while others reverse the usage.

Strategic managers recognize that short-run profit maximization is rarely the best approachto achieving sustained corporate growth and profitability. An often repeated adage statesthat if impoverished people are given food, they will eat it and remain impoverished; how-ever, if they are given seeds and tools and shown how to grow crops, they will be able toimprove their condition permanently. A parallel choice confronts strategic decision makers:

1. Should they eat the seeds to improve the near-term profit picture and make large divi-dend payments through cost-saving measures such as laying off workers during periodsof slack demand, selling off inventories, or cutting back on research and development?

2. Or should they sow the seeds in the effort to reap long-term rewards by reinvesting prof-its in growth opportunities, committing resources to employee training, or increasingadvertising expenditures?

For most strategic managers, the solution is clear—distribute a small amount of profitnow but sow most of it to increase the likelihood of a long-term supply. This is the most fre-quently used rationale in selecting objectives.

To achieve long-term prosperity, strategic planners commonly establish long-term ob-jectives in seven areas:

Profitability The ability of any firm to operate in the long run depends on attaining an ac-ceptable level of profits. Strategically managed firms characteristically have a profit ob-jective, usually expressed in earnings per share or return on equity.

Productivity Strategic managers constantly try to increase the productivity of their sys-tems. Firms that can improve the input-output relationship normally increase profitability.Thus, firms almost always state an objective for productivity. Commonly used productivityobjectives are the number of items produced or the number of services rendered per unit of

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

192 Part Two Strategy Formulation

input. However, productivity objectives sometimes are stated in terms of desired cost de-creases. For example, objectives may be set for reducing defective items, customer com-plaints leading to litigation, or overtime. Achieving such objectives increases profitabilityif unit output is maintained.

Competitive Position One measure of corporate success is relative dominance in the mar-ketplace. Larger firms commonly establish an objective in terms of competitive position,often using total sales or market share as measures of their competitive position. An objec-tive with regard to competitive position may indicate a firm’s long-term priorities. For ex-ample, Gulf Oil set a five-year objective of moving from third to second place as a producerof high-density polypropylene. Total sales were the measure.

Employee Development Employees value education and training, in part because theylead to increased compensation and job security. Providing such opportunities often in-creases productivity and decreases turnover. Therefore, strategic decision makers fre-quently include an employee development objective in their long-range plans. For example,PPG has declared an objective of developing highly skilled and flexible employees and,thus, providing steady employment for a reduced number of workers.

Employee Relations Whether or not they are bound by union contracts, firms activelyseek good employee relations. In fact, proactive steps in anticipation of employee needs andexpectations are characteristic of strategic managers. Strategic managers believe that pro-ductivity is linked to employee loyalty and to appreciation of managers’ interest in em-ployee welfare. They, therefore, set objectives to improve employee relations. Among theoutgrowths of such objectives are safety programs, worker representation on managementcommittees, and employee stock option plans.

Technological Leadership Firms must decide whether to lead or follow in the market-place. Either approach can be successful, but each requires a different strategic posture.Therefore, many firms state an objective with regard to technological leadership. For ex-ample, Caterpillar Tractor Company established its early reputation and dominant positionin its industry by being in the forefront of technological innovation in the manufacture oflarge earthmovers. E-commerce technology officers will have more of a strategic role in themanagement hierarchy of the future, demonstrating that the Internet has become an integralaspect of corporate long-term objective setting. In offering an e-technology managerhigher-level responsibilities, a firm is pursuing a leadership position in terms of innovationin computer networks and systems. Officers of e-commerce technology at GE and Delta Airhave shown their ability to increase profits by driving down transaction-related costs withWeb-based technologies that seamlessly integrate their firms’ supply chains. These tech-nologies have the potential to “lock in” certain suppliers and customers and heighten com-petitive position through supply chain efficiency.

Public Responsibility Managers recognize their responsibilities to their customers and tosociety at large. In fact, many firms seek to exceed government requirements. They worknot only to develop reputations for fairly priced products and services but also to establishthemselves as responsible corporate citizens. For example, they may establish objectives forcharitable and educational contributions, minority training, public or political activity, com-munity welfare, or urban revitalization. In an attempt to exhibit their public responsibilityin the United States, Japanese companies, such as Toyota, Hitachi, and Matsushita, con-tribute more than $500 million annually to American educational projects, charities, andnonprofit organizations.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 193

Qualities of Long-Term ObjectivesWhat distinguishes a good objective from a bad one? What qualities of an objective improveits chances of being attained? These questions are best answered in relation to seven crite-ria that should be used in preparing long-term objectives: acceptable, flexible, measurableover time, motivating, suitable, understandable, and achievable.

Acceptable Managers are most likely to pursue objectives that are consistent with theirpreferences. They may ignore or even obstruct the achievement of objectives that offendthem (e.g., promoting a high-sodium food product) or that they believe to be inappropriateor unfair (e.g., reducing spoilage to offset a disproportionate allocation of fixed overhead).In addition, long-term corporate objectives frequently are designed to be acceptable togroups external to the firm. An example is efforts to abate air pollution that are undertakenat the insistence of the Environmental Protection Agency.

Flexible Objectives should be adaptable to unforeseen or extraordinary changes in thefirm’s competitive or environmental forecasts. Unfortunately, such flexibility usually is in-creased at the expense of specificity. One way of providing flexibility while minimizing itsnegative effects is to allow for adjustments in the level, rather than in the nature, of objectives.For example, the personnel department objective of providing managerial development train-ing for 15 supervisors per year over the next five-year period might be adjusted by changingthe number of people to be trained. In contrast, changing the personnel department’s objec-tive of “assisting production supervisors in reducing job-related injuries by 10 percent peryear” after three months had gone by would understandably create dissatisfaction.

Measurable Objectives must clearly and concretely state what will be achieved and whenit will be achieved. Thus, objectives should be measurable over time. For example, the ob-jective of “substantially improving our return on investment” would be better stated as “in-creasing the return on investment on our line of paper products by a minimum of 1 percenta year and a total of 5 percent over the next three years.”

Motivating People are most productive when objectives are set at a motivating level—onehigh enough to challenge but not so high as to frustrate or so low as to be easily attained. Theproblem is that individuals and groups differ in their perceptions of what is high enough. Abroad objective that challenges one group frustrates another and minimally interests a third.One valuable recommendation is that objectives be tailored to specific groups. Developingsuch objectives requires time and effort, but objectives of this kind are more likely to motivate.

Suitable Objectives must be suited to the broad aims of the firm, which are expressed inits mission statement. Each objective should be a step toward the attainment of overallgoals. In fact, objectives that are inconsistent with the company mission can subvert thefirm’s aims. For example, if the mission is growth oriented, the objective of reducing thedebt-to-equity ratio to 1.00 would probably be unsuitable and counterproductive.

Understandable Strategic managers at all levels must understand what is to be achieved.They also must understand the major criteria by which their performance will be evaluated.Thus, objectives must be so stated that they are as understandable to the recipient as they areto the giver. Consider the misunderstandings that might arise over the objective of “increas-ing the productivity of the credit card department by 20 percent within two years.” What doesthis objective mean? Increase the number of outstanding cards? Increase the use of outstand-ing cards? Increase the employee workload? Make productivity gains each year? Or hope thatthe new computer-assisted system, which should improve productivity, is approved by year 2?As this simple example illustrates, objectives must be clear, meaningful, and unambiguous.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

194 Part Two Strategy Formulation

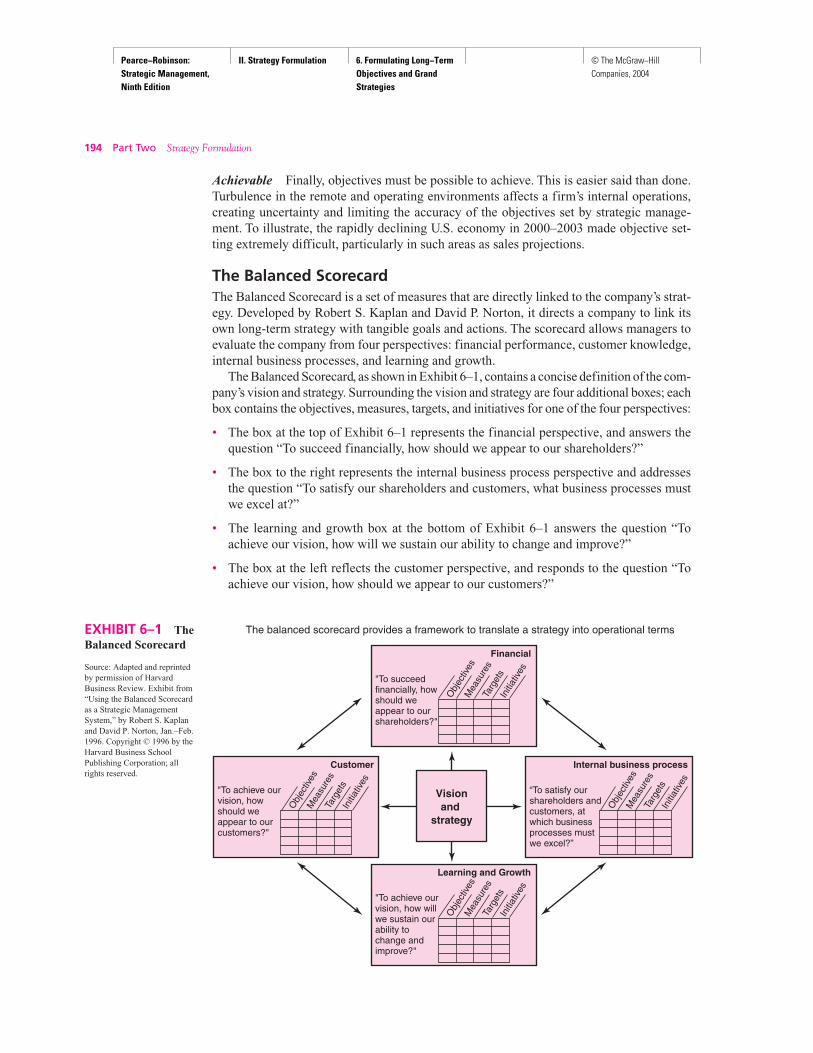

EXHIBIT 6–1 TheBalanced Scorecard

Source: Adapted and reprintedby permission of HarvardBusiness Review. Exhibit from“Using the Balanced Scorecardas a Strategic ManagementSystem,” by Robert S. Kaplanand David P. Norton, Jan.–Feb.1996. Copyright © 1996 by theHarvard Business SchoolPublishing Corporation; allrights reserved.

The balanced scorecard provides a framework to translate a strategy into operational terms

Financial

Obj

ectiv

esM

easu

res

Targ

ets

Initi

ativ

es

"To succeedfinancially, howshould we appear to our shareholders?"

Internal business process

Obj

ectiv

esM

easu

res

Targ

ets

Initi

ativ

es

“To satisfy our shareholders and customers, at which business processes mustwe excel?”

Customer

Obj

ectiv

esM

easu

res

Targ

ets

Initi

ativ

es

"To achieve ourvision, howshould weappear to ourcustomers?"

Learning and Growth

Obj

ectiv

esM

easu

res

Targ

ets

Initi

ativ

es

"To achieve our vision, how willwe sustain ourability tochange and improve?"

Visionand

strategy

Achievable Finally, objectives must be possible to achieve. This is easier said than done.Turbulence in the remote and operating environments affects a firm’s internal operations,creating uncertainty and limiting the accuracy of the objectives set by strategic manage-ment. To illustrate, the rapidly declining U.S. economy in 2000–2003 made objective set-ting extremely difficult, particularly in such areas as sales projections.

The Balanced ScorecardThe Balanced Scorecard is a set of measures that are directly linked to the company’s strat-egy. Developed by Robert S. Kaplan and David P. Norton, it directs a company to link itsown long-term strategy with tangible goals and actions. The scorecard allows managers toevaluate the company from four perspectives: financial performance, customer knowledge,internal business processes, and learning and growth.

The Balanced Scorecard, as shown in Exhibit 6–1, contains a concise definition of the com-pany’s vision and strategy. Surrounding the vision and strategy are four additional boxes; eachbox contains the objectives, measures, targets, and initiatives for one of the four perspectives:

• The box at the top of Exhibit 6–1 represents the financial perspective, and answers thequestion “To succeed financially, how should we appear to our shareholders?”

• The box to the right represents the internal business process perspective and addressesthe question “To satisfy our shareholders and customers, what business processes mustwe excel at?”

• The learning and growth box at the bottom of Exhibit 6–1 answers the question “Toachieve our vision, how will we sustain our ability to change and improve?”

• The box at the left reflects the customer perspective, and responds to the question “Toachieve our vision, how should we appear to our customers?”

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 195

All of the boxes are connected by arrows to illustrate that the objectives and measures ofthe four perspectives are linked by cause-and-effect relationships that lead to the success-ful implementation of the strategy. Achieving one perspective’s targets should lead to de-sired improvements in the next perspective, and so on, until the company’s performanceincreases overall.

A properly constructed scorecard is balanced between short- and long-term measures;financial and nonfinancial measures; and internal and external performance perspectives.

The Balanced Scorecard is a management system that can be used as the central organ-izing framework for key managerial processes. Chemical Bank, Mobil Corporation’s USMarketing and Refining Division, and CIGNA Property and Casualty Insurance have usedthe Balanced Scorecard approach to assist in individual and team goal setting, compensa-tion, resource allocation, budgeting and planning, and strategic feedback and learning.

GENERIC STRATEGIES

Many planning experts believe that the general philosophy of doing business declared bythe firm in the mission statement must be translated into a holistic statement of the firm’sstrategic orientation before it can be further defined in terms of a specific long-term strat-egy. In other words, a long-term or grand strategy must be based on a core idea about howthe firm can best compete in the marketplace.

The popular term for this core idea is generic strategy. From a scheme developed byMichael Porter, many planners believe that any long-term strategy should derive from afirm’s attempt to seek a competitive advantage based on one of three generic strategies:

1. Striving for overall low-cost leadership in the industry.

2. Striving to create and market unique products for varied customer groups throughdifferentiation.

3. Striving to have special appeal to one or more groups of consumer or industrial buyers,focusing on their cost or differentiation concerns.

Advocates of generic strategies believe that each of these options can produce above-average returns for a firm in an industry. However, they are successful for very differentreasons.

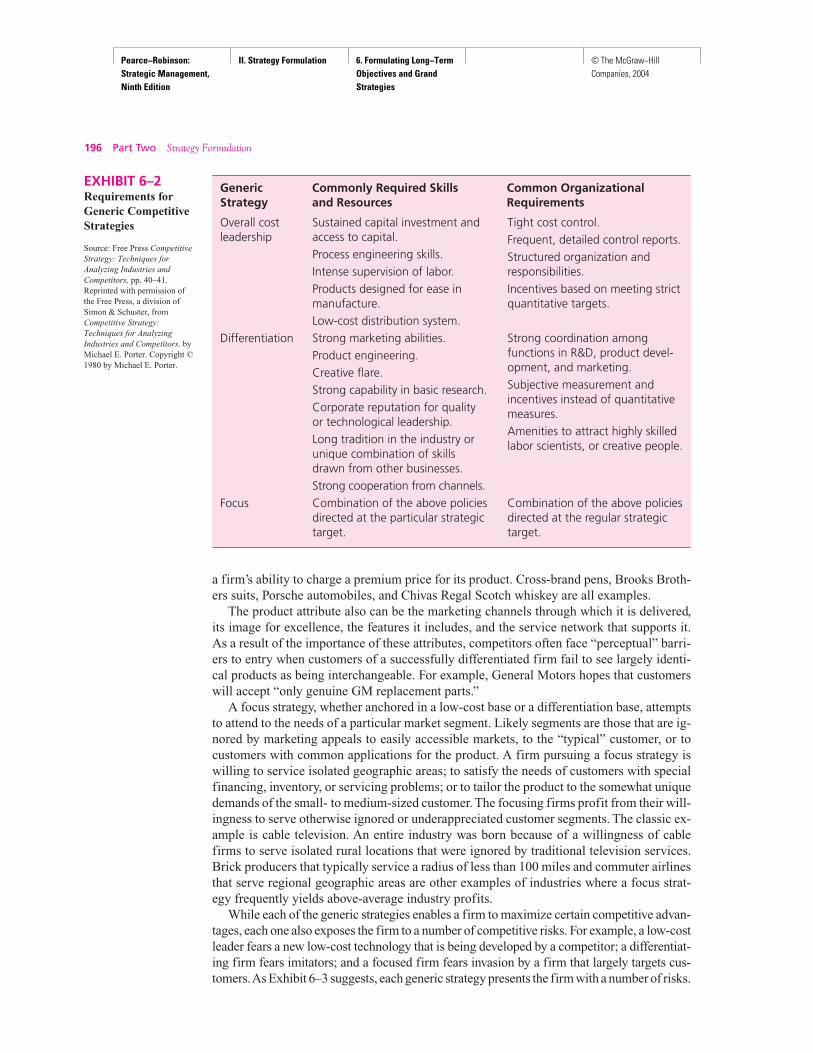

Low-cost leaders depend on some fairly unique capabilities to achieve and sustain theirlow-cost position. Examples of such capabilities are: having secured suppliers of scarce rawmaterials, being in a dominant market share position, or having a high degree of capitaliza-tion. Low-cost producers usually excel at cost reductions and efficiencies. They maximizeeconomies of scale, implement cost-cutting technologies, stress reductions in overhead andin administrative expenses, and use volume sales techniques to propel themselves up theearning curve. The commonly accepted requirements for successful implementation of thelow-cost and the other two generic strategies are overviewed in Exhibit 6–2.

A low-cost leader is able to use its cost advantage to charge lower prices or to enjoyhigher profit margins. By so doing, the firm effectively can defend itself in price wars, at-tack competitors on price to gain market share, or, if already dominant in the industry, sim-ply benefit from exceptional returns. As an extreme case, it has been argued that NationalCan Company, a corporation in an essentially stagnant industry, is able to generate attrac-tive and improving profits by being the low-cost producer.

Strategies dependent on differentiation are designed to appeal to customers with a spe-cial sensitivity for a particular product attribute. By stressing the attribute above other prod-uct qualities, the firm attempts to build customer loyalty. Often such loyalty translates into

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

196 Part Two Strategy Formulation

EXHIBIT 6–2Requirements forGeneric CompetitiveStrategies

Source: Free Press CompetitiveStrategy: Techniques forAnalyzing Industries andCompetitors, pp. 40–41.Reprinted with permission ofthe Free Press, a division ofSimon & Schuster, fromCompetitive Strategy:Techniques for AnalyzingIndustries and Competitors, byMichael E. Porter. Copyright ©1980 by Michael E. Porter.

Generic Commonly Required Skills Common OrganizationalStrategy and Resources Requirements

Overall cost leadership

Differentiation

Focus

Sustained capital investment andaccess to capital.Process engineering skills.Intense supervision of labor.Products designed for ease inmanufacture.Low-cost distribution system.Strong marketing abilities.Product engineering.Creative flare.Strong capability in basic research.Corporate reputation for qualityor technological leadership.Long tradition in the industry orunique combination of skillsdrawn from other businesses.Strong cooperation from channels.Combination of the above policiesdirected at the particular strategictarget.

Tight cost control.Frequent, detailed control reports.Structured organization andresponsibilities.Incentives based on meeting strictquantitative targets.

Strong coordination amongfunctions in R&D, product devel-opment, and marketing.Subjective measurement andincentives instead of quantitativemeasures.Amenities to attract highly skilledlabor scientists, or creative people.

Combination of the above policiesdirected at the regular strategictarget.

a firm’s ability to charge a premium price for its product. Cross-brand pens, Brooks Broth-ers suits, Porsche automobiles, and Chivas Regal Scotch whiskey are all examples.

The product attribute also can be the marketing channels through which it is delivered,its image for excellence, the features it includes, and the service network that supports it.As a result of the importance of these attributes, competitors often face “perceptual” barri-ers to entry when customers of a successfully differentiated firm fail to see largely identi-cal products as being interchangeable. For example, General Motors hopes that customerswill accept “only genuine GM replacement parts.”

A focus strategy, whether anchored in a low-cost base or a differentiation base, attemptsto attend to the needs of a particular market segment. Likely segments are those that are ig-nored by marketing appeals to easily accessible markets, to the “typical” customer, or tocustomers with common applications for the product. A firm pursuing a focus strategy iswilling to service isolated geographic areas; to satisfy the needs of customers with specialfinancing, inventory, or servicing problems; or to tailor the product to the somewhat uniquedemands of the small- to medium-sized customer. The focusing firms profit from their will-ingness to serve otherwise ignored or underappreciated customer segments. The classic ex-ample is cable television. An entire industry was born because of a willingness of cablefirms to serve isolated rural locations that were ignored by traditional television services.Brick producers that typically service a radius of less than 100 miles and commuter airlinesthat serve regional geographic areas are other examples of industries where a focus strat-egy frequently yields above-average industry profits.

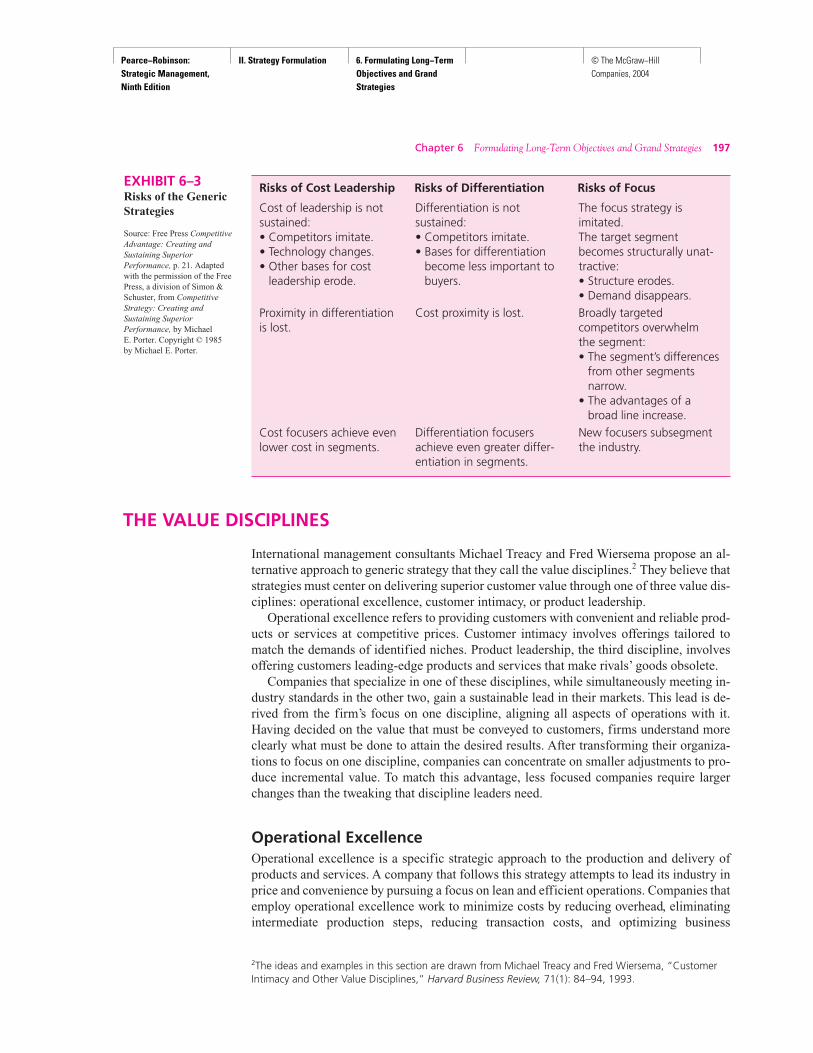

While each of the generic strategies enables a firm to maximize certain competitive advan-tages, each one also exposes the firm to a number of competitive risks. For example, a low-costleader fears a new low-cost technology that is being developed by a competitor; a differentiat-ing firm fears imitators; and a focused firm fears invasion by a firm that largely targets cus-tomers.As Exhibit 6–3 suggests, each generic strategy presents the firm with a number of risks.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 197

EXHIBIT 6–3Risks of the GenericStrategies

Source: Free Press CompetitiveAdvantage: Creating andSustaining SuperiorPerformance, p. 21. Adaptedwith the permission of the FreePress, a division of Simon &Schuster, from CompetitiveStrategy: Creating andSustaining SuperiorPerformance, by MichaelE. Porter. Copyright © 1985by Michael E. Porter.

Risks of Cost Leadership Risks of Differentiation Risks of Focus

Cost of leadership is not sustained:• Competitors imitate.• Technology changes.• Other bases for cost

leadership erode.

Proximity in differentiation is lost.

Cost focusers achieve even lower cost in segments.

Differentiation is notsustained:• Competitors imitate.• Bases for differentiation

become less important tobuyers.

Cost proximity is lost.

Differentiation focusersachieve even greater differ-entiation in segments.

The focus strategy isimitated.The target segmentbecomes structurally unat-tractive:• Structure erodes.• Demand disappears.Broadly targetedcompetitors overwhelm the segment:• The segment’s differences

from other segmentsnarrow.

• The advantages of abroad line increase.

New focusers subsegmentthe industry.

THE VALUE DISCIPLINES

2The ideas and examples in this section are drawn from Michael Treacy and Fred Wiersema, “CustomerIntimacy and Other Value Disciplines,” Harvard Business Review, 71(1): 84–94, 1993.

International management consultants Michael Treacy and Fred Wiersema propose an al-ternative approach to generic strategy that they call the value disciplines.2 They believe thatstrategies must center on delivering superior customer value through one of three value dis-ciplines: operational excellence, customer intimacy, or product leadership.

Operational excellence refers to providing customers with convenient and reliable prod-ucts or services at competitive prices. Customer intimacy involves offerings tailored tomatch the demands of identified niches. Product leadership, the third discipline, involvesoffering customers leading-edge products and services that make rivals’ goods obsolete.

Companies that specialize in one of these disciplines, while simultaneously meeting in-dustry standards in the other two, gain a sustainable lead in their markets. This lead is de-rived from the firm’s focus on one discipline, aligning all aspects of operations with it.Having decided on the value that must be conveyed to customers, firms understand moreclearly what must be done to attain the desired results. After transforming their organiza-tions to focus on one discipline, companies can concentrate on smaller adjustments to pro-duce incremental value. To match this advantage, less focused companies require largerchanges than the tweaking that discipline leaders need.

Operational ExcellenceOperational excellence is a specific strategic approach to the production and delivery ofproducts and services. A company that follows this strategy attempts to lead its industry inprice and convenience by pursuing a focus on lean and efficient operations. Companies thatemploy operational excellence work to minimize costs by reducing overhead, eliminatingintermediate production steps, reducing transaction costs, and optimizing business

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

198 Part Two Strategy Formulation

processes across functional and organizational boundaries. The focus is on delivering prod-ucts or services to customers at competitive prices with minimal inconvenience.

Through its focus on operational excellence, Dell Computer has shown PC buyers thatthey do not have to sacrifice quality of state-of-the art technology in order to buy personalcomputers easily and inexpensively. Dell recognized the opportunity to cut retail dealers outof the industry’s traditional distribution process. Through this approach—which includesdirect sales, building to order, and creating a disciplined, extremely low-cost culture—Dellhas been able to undercut other PC makers in price yet provide high-quality products andservice.

Operational excellence is also the strategic focus of General Electric’s large appliancebusiness. Historically, the distribution strategy for large appliances was based on requiringthat dealers maintain large inventories. Price breaks for dealers were based on order quan-tities. However, as the marketplace became more competitive, principally as a result of com-petition for multibrand dealers like Sears, GE recognized the need to adjust its productionand distribution plans.

The GE system addresses the delivery of products. As a step toward organizational ex-cellence, GE created a computer-based logistics system to replace its in-store inventoriesmodel. Retailers use this software to access a 24-hour on-line order processing system thatguarantees GE’s best price. This system allows dealers to better meet customer needs, withinstantaneous access to a warehouse of goods and accurate shipping and production infor-mation. GE benefits from the deal as well. Efficiency is increased since manufacturing nowoccurs in response to customer sales. Additionally, warehousing and distribution systemshave been streamlined to create the capability of delivering to 90 percent of destinations inthe continental United States within one business day.

Firms that implement the strategy of operational excellence typically restructure theirdelivery processes to focus on efficiency and reliability, and use state-of-the art informa-tion systems that emphasize integration and low-cost transactions.

Customer IntimacyCompanies that implement a strategy of customer intimacy continually tailor and shapeproducts and services to fit an increasingly refined definition of the customer. Companiesexcelling in customer intimacy combine detailed customer knowledge with operationalflexibility. They respond quickly to almost any need, from customizing a product to fulfill-ing special requests to create customer loyalty.

Customer-intimate companies are willing to spend money now to build customer loyaltyfor the long term, considering each customer’s lifetime value to the company, not the profitof any single transaction. Consequently, employees in customer-intimate companies go togreat lengths to ensure customer satisfaction with low regard for initial cost.

Home Depot implements the discipline of customer intimacy. Home Depot clerks spendthe necessary time with customers to determine the product that best suits their needs, be-cause the company’s business strategy is built around selling information and service in ad-dition to home-repair and improvement items. Consequently, consumers concerned solelywith price fall outside Home Depot’s core market.

Companies engaged in customer intimacy understand the difference between the prof-itability of a single transaction and the profitability of a lifetime relationship with a singlecustomer. The company’s profitability depends in part on its maintaining a system that dif-ferentiates quickly and accurately the degree of service that customers require and the rev-enues their patronage is likely to generate. Firms using this approach recognize that notevery customer is equally profitable. For example, a financial services company installed a

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 199

telephone-computer system capable of recognizing individual clients by their telephonenumbers when they call. The system routes customers with large accounts and frequenttransactions to their own senior account representative. Other customers may be routed toa trainee or junior representative. In any case, the customer’s file appears on the represen-tative’s screen before the phone is answered.

The new system allows the firm to segment its services with great efficiency. If the com-pany has clients who are interested in trading in a particular financial instrument, it cangroup them under the one account representative who specializes in that instrument. Thissaves the firm the expense of training every representative in every facet of financial serv-ices. Additionally, the company can direct certain value-added services or products to a spe-cific group of clients that would have interest in them.

Businesses that select a customer intimacy strategy have decided to stress flexibilityand responsiveness. They collect and analyze data from many sources. Their organiza-tional structure emphasizes empowerment of employees close to customers. Additionally,hiring and training programs stress the creative decision-making skills required to meet in-dividual customer needs. Management systems recognize and utilize such concepts as cus-tomer lifetime value, and norms among employees are consistent with a “have it your way”mind set.

Product LeadershipCompanies that pursue the discipline of product leadership strive to produce a continuousstream of state-of-the-art products and services. Three challenges must be met to attain thatgoal. Creativity is the first challenge. Creativity is recognizing and embracing ideas usuallyoriginating outside the company. Second, innovative companies must commercialize ideasquickly. Thus, their business and management processes need to be engineered for speed.Product leaders relentlessly pursue new solutions to problems. Finally, firms utilizing thisdiscipline prefer to release their own improvements rather than wait for competitors to en-ter. Consequently, product leaders do not stop for self-congratulation; they focus on con-tinual improvement.

For example, Johnson & Johnson’s organizational design brings good ideas in, developsthem quickly, and looks for ways to improve them. In 1983, the president of J&J’s Vistakon,Inc., a maker of specialty contact lenses, received a tip concerning an ophthalmologist whohad conceived of a method to manufacture disposable contact lenses inexpensively.Vistakon’s president received this tip from a J&J employee from a different subsidiarywhom he had never met. Rather than dismiss the tip, the executives purchased the rights tothe technology, assembled a management team to oversee the product’s development teamto oversee the product’s development, and built a state-of-the-art facility in Florida to man-ufacture disposable contact lenses called Acuvue. Vistakon and its parent, J&J, were will-ing to incur high manufacturing and inventory costs before a single lens was sold. Ahigh-speed production facility helped give Vistakon a six-month head start over the com-petition that, taken off guard, never caught up.

Like other product leaders, J&J creates and maintains an environment that encouragesemployees to share ideas. Additionally, product leaders continually scan the environmentfor new product or service possibilities and rush to capitalize them. Product leaders alsoavoid bureaucracy because it slows commercialization of their ideas. In a product leader-ship company, a wrong decision often is less damaging than one made late. As a result,managers make decisions quickly, their companies encouraging them to decide today andimplement tomorrow. Product leaders continually look for new methods to shorten their cy-cle times.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

200 Part Two Strategy Formulation

The strength of product leaders lies in reacting to situations as they occur. Shorter reactiontimes serve as an advantage in dealings with the unknown. For example, when competitorschallenged the safety of Acuvue lenses, the firm responded quickly and distributed data com-bating the charges to eye-care professionals.This reaction created goodwill in the marketplace.

Product leaders act as their own competition. These firms continually make the productsand services they have created obsolete. Product leaders believe that if they do not developa successor, a competitor will. So, although Acuvue is successful in the marketplace, Vis-takon continues to investigate new material that will extend the wearability of contact lensesand technologies that will make current lenses obsolete. J&J and other innovators recognizethat the long-run profitability of an existing product or service is less important to the com-pany’s future than maintaining its product leadership edge and momentum.

GRAND STRATEGIES

While the need for firms to develop generic strategies remains an unresolved debate, de-signers of planning systems agree about the critical role of grand strategies. Grand strate-gies, often called master or business strategies, provide basic direction for strategic actions.They are the basis of coordinated and sustained efforts directed toward achieving long-termbusiness objectives.

The purpose of this section is twofold: (1) to list, describe, and discuss 15 grand strate-gies that strategic managers should consider and (2) to present approaches to the selectionof an optimal grand strategy from the available alternatives.

Grand strategies indicate the time period over which long-range objectives are to beachieved. Thus, a grand strategy can be defined as a comprehensive general approach thatguides a firm’s major actions.

The 15 principal grand strategies are: concentrated growth, market development, prod-uct development, innovation, horizontal integration, vertical integration, concentric diver-sification, conglomerate diversification, turnaround, divestiture, liquidation, bankruptcy,joint ventures, strategic alliances, and consortia. Any one of these strategies could serve asthe basis for achieving the major long-term objectives of a single firm. But a firm involvedwith multiple industries, businesses, product lines, or customer groups—as many firmsare—usually combines several grand strategies. For clarity, however, each of the principalgrand strategies is described independently in this section, with examples to indicate someof its relative strengths and weaknesses.

Concentrated GrowthMany of the firms that fell victim to merger mania were once mistakenly convinced that thebest way to achieve their objectives was to pursue unrelated diversification in the search forfinancial opportunity and synergy. By rejecting that “conventional wisdom,” such firms asMartin-Marietta, KFC, Compaq,Avon, Hyatt Legal Services, andTenant have demonstratedthe advantages of what is increasingly proving to be sound business strategy. A firm that hasenjoyed special success through a strategic emphasis on increasing market share throughconcentration is Chemlawn. With headquarters in Columbus, Ohio, Chemlawn is the NorthAmerican leader in professional lawn care. Like others in the lawn-care industry, Chemlawnis experiencing a steadily declining customer base. Market analysis shows that the declineis fueled by negative environmental publicity, perceptions of poor customer service, andconcern about the price versus the value of the company’s services, given the wide array ofdo-it-yourself alternatives. Chemlawn’s approach to increasing market share hinges on ad-dressing quality, price, and value issues; discontinuing products that the public or environ-mental authorities perceive as unsafe; and improving the quality of its workforce.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 201

These firms are just a few of the majority of American firms that pursue a concentratedgrowth strategy by focusing on a specific product and market combination. Concentratedgrowth is the strategy of the firm that directs its resources to the profitable growth of a sin-gle product, in a single market, with a single dominant technology. The main rationale forthis approach, sometimes called a market penetration or concentration strategy, is that thefirm thoroughly develops and exploits its expertise in a delimited competitive arena.

Rationale for Superior Performance

Concentrated growth strategies lead to enhanced performance. The ability to assess marketneeds, knowledge of buyer behavior, customer price sensitivity, and effectiveness of pro-motion are characteristics of a concentrated growth strategy. Such core capabilities are amore important determinant of competitive market success than are the environmentalforces faced by the firm. The high success rates of new products also are tied to avoidingsituations that require undeveloped skills, such as serving new customers and markets, ac-quiring new technology, building new channels, developing new promotional abilities, andfacing new competition.

A major misconception about the concentrated growth strategy is that the firm practic-ing it will settle for little or no growth. This is certainly not true for a firm that correctly uti-lizes the strategy. A firm employing concentrated growth grows by building on itscompetences, and it achieves a competitive edge by concentrating in the product-marketsegment it knows best. A firm employing this strategy is aiming for the growth that resultsfrom increased productivity, better coverage of its actual product-market segment, and moreefficient use of its technology.

Conditions That Favor Concentrated Growth

Specific conditions in the firm’s environment are favorable to the concentrated growth strat-egy. The first is a condition in which the firm’s industry is resistant to major technologicaladvancements. This is usually the case in the late growth and maturity stages of the prod-uct life cycle and in product markets where product demand is stable and industry barriers,such as capitalization, are high. Machinery for the paper manufacturing industry, in whichthe basic technology has not changed for more than a century, is a good example.

An especially favorable condition is one in which the firm’s targeted markets are notproduct saturated. Markets with competitive gaps leave the firm with alternatives forgrowth, other than taking market share away from competitors. The successful introductionof traveler services by Allstate and Amoco demonstrates that even an organization as en-trenched and powerful as the AAA could not build a defensible presence in all segments ofthe automobile club market.

A third condition that favors concentrated growth exists when the firm’s product mar-kets are sufficiently distinctive to dissuade competitors in adjacent product markets fromtrying to invade the firm’s segment. John Deere scrapped its plans for growth in the con-struction machinery business when mighty Caterpillar threatened to enter Deere’s mainstay,the farm machinery business, in retaliation. Rather than risk a costly price war on its ownturf, Deere scrapped these plans.

A fourth favorable condition exists when the firm’s inputs are stable in price and quan-tity and are available in the amounts and at the times needed. Maryland-based Giant Foodsis able to concentrate in the grocery business largely due to its stable long-term arrange-ments with suppliers of its private-label products. Most of these suppliers are makers of thenational brands that compete against the Giant labels. With a high market share and ag-gressive retail distribution, Giant controls the access of these brands to the consumer. Con-sequently, its suppliers have considerable incentive to honor verbal agreements, called

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

202 Part Two Strategy Formulation

bookings, in which they commit themselves for a one-year period with regard to the price,quality, and timing of their shipments to Giant.

The pursuit of concentrated growth also is favored by a stable market—a market with-out the seasonal or cyclical swings that would encourage a firm to diversify. Night Owl Se-curity, the District of Columbia market leader in home security services, commits itscustomers to initial four-year contracts. In a city where affluent consumers tend to be quitetransient, the length of this relationship is remarkable. Night Owl’s concentrated growthstrategy has been reinforced by its success in getting subsequent owners of its customers’homes to extend and renew the security service contracts. In a similar way, Lands’ End re-inforced its growth strategy by asking customers for names and addresses of friends and rel-atives living overseas who would like to receive Lands’ End catalogs.

A firm also can grow while concentrating, if it enjoys competitive advantages based onefficient production or distribution channels. These advantages enable the firm to formu-late advantageous pricing policies. More efficient production methods and better handlingof distribution also enable the firm to achieve greater economies of scale or, in conjunc-tion with marketing, result in a product that is differentiated in the mind of the consumer.Graniteville Company, a large South Carolina textile manufacturer, enjoyed decades ofgrowth and profitability by adopting a “follower” tactic as part of its concentrated growthstrategy. By producing fabrics only after market demand had been well established, and byfeaturing products that reflected its expertise in adopting manufacturing innovations and inmaintaining highly efficient long production runs, Graniteville prospered through concen-trated growth.

Finally, the success of market generalists creates conditions favorable to concentratedgrowth. When generalists succeed by using universal appeals, they avoid making special ap-peals to particular groups of customers. The net result is that many small pockets are leftopen in the markets dominated by generalists, and that specialists emerge and thrive in thesepockets. For example, hardware store chains, such as Home Depot, focus primarily on rou-tine household repair problems and offer solutions that can be easily sold on a self-service,do-it-yourself basis. This approach leaves gaps at both the “semiprofessional” and “neo-phyte” ends of the market—in terms of the purchaser’s skill at household repairs and the ex-tent to which available merchandise matches the requirements of individual homeowners.

Risk and Rewards of Concentrated Growth

Under stable conditions, concentrated growth poses lower risk than any other grand strat-egy; but, in a changing environment, a firm committed to concentrated growth faces highrisks. The greatest risk is that concentrating in a single product market makes a firm par-ticularly vulnerable to changes in that segment. Slowed growth in the segment would jeop-ardize the firm because its investment, competitive edge, and technology are deeplyentrenched in a specific offering. It is difficult for the firm to attempt sudden changes if itsproduct is threatened by near-term obsolescence, a faltering market, new substitutes, orchanges in technology or customer needs. For example, the manufacturers of IBM clonesfaced such a problem when IBM adopted the OS/2 operating system for its personal com-puter line. That change made existing clones out of date.

The concentrating firm’s entrenchment in a specific industry makes it particularly sus-ceptible to changes in the economic environment of that industry. For example, MackTruck, the second-largest truck maker in America, lost $20 million as a result of an 18-month slump in the truck industry.

Entrenchment in a specific product market tends to make a concentrating firm moreadept than competitors at detecting new trends. However, any failure of such a firm to prop-erly forecast major changes in its industry can result in extraordinary losses. Numerous

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 203

makers of inexpensive digital watches were forced to declare bankruptcy because theyfailed to anticipate the competition posed by Swatch, Guess, and other trendy watches thatemerged from the fashion industry.

A firm pursuing a concentrated growth strategy is vulnerable also to the high opportu-nity costs that result from remaining in a specific product market and ignoring other op-tions that could employ the firm’s resources more profitably. Overcommitment to a specifictechnology and product market can hinder a firm’s ability to enter a new or growing prod-uct market that offers more attractive cost-benefit trade-offs. Had Apple Computers main-tained its policy of making equipment that did not interface with IBM equipment, it wouldhave missed out on what have proved to be its most profitable strategic options.

Concentrated Growth Is Often the Most Viable Option

Examples abound of firms that have enjoyed exceptional returns on the concentratedgrowth strategy. Such firms as McDonald’s, Goodyear, and Apple Computers have usedfirsthand knowledge and deep involvement with specific product segments to become pow-erful competitors in their markets. The strategy is associated even more often with suc-cessful smaller firms that have steadily and doggedly improved their market position.

The limited additional resources necessary to implement concentrated growth, coupledwith the limited risk involved, also make this strategy desirable for a firm with limited funds.For example, through a carefully devised concentrated growth strategy, medium-sized JohnDeere & Company was able to become a major force in the agricultural machinery businesseven when competing with such firms as Ford Motor Company. While other firms were try-ing to exit or diversify from the farm machinery business, Deere spent $2 billion in up-grading its machinery, boosting its efficiency, and engaging in a program to strengthen itsdealership system. This concentrated growth strategy enabled it to become the leader in thefarm machinery business despite the fact that Ford was more than 10 times its size.

The firm that chooses a concentrated growth strategy directs its resources to the prof-itable growth of a narrowly defined product and market, focusing on a dominant technol-ogy. Firms that remain within their chosen product market are able to extract the most fromtheir technology and market knowledge and, thus, are able to minimize the risk associatedwith unrelated diversification. The success of a concentration strategy is founded on thefirm’s use of superior insights into its technology, product, and customer to obtain a sus-tainable competitive advantage. Superior performance on these aspects of corporate strat-egy has been shown to have a substantial positive effect on market success.

A grand strategy of concentrated growth allows for a considerable range of action.Broadly speaking, the firm can attempt to capture a larger market share by increasing theusage rates of present customers, by attracting competitors’ customers, or by selling tononusers. In turn, each of these options suggests more specific options, some of which arelisted in the top section of Exhibit 6–4.

When strategic managers forecast that their current products and their markets will notprovide the basis for achieving the company mission, they have two options that involvemoderate costs and risk: market development and product development.

Market DevelopmentMarket development commonly ranks second only to concentration as the least costly andleast risky of the 15 grand strategies. It consists of marketing present products, often withonly cosmetic modifications, to customers in related market areas by adding channels ofdistribution or by changing the content of advertising or promotion. Several specific mar-ket development approaches are listed in Exhibit 6–4. Thus, as suggested by the figure,

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

204 Part Two Strategy Formulation

EXHIBIT 6–4Specific Optionsunder the GrandStrategies ofConcentration,Market Development,and ProductDevelopment

Source: Adapted from PhilipKotler, Marketing ManagementAnalysis, Planning, andControl, 11th ed., 2002.Reprinted by permission ofPrentice Hall, Inc., UpperSaddle River, NJ.

Concentration (increasing use of present products in present markets):

1. Increasing present customers’ rate of use:a. Increasing the size of purchase.b. Increasing the rate of product obsolescence.c. Advertising other uses.d. Giving price incentives for increased use.

2. Attracting competitors’ customers:a. Establishing sharper brand differentiation.b. Increasing promotional effort.c. Initiating price cuts.

3. Attracting nonusers to buy the product:a. Inducing trial use through sampling, price incentives, and so on.b. Pricing up or down.c. Advertising new uses.

Market development (selling present products in new markets):

1. Opening additional geographic markets:a. Regional expansion.b. National expansion.c. International expansion.

2. Attracting other market segments:a. Developing product versions to appeal to other segments.b. Entering other channels of distribution.c. Advertising in other media.

Product development (developing new products for present markets):

1. Developing new product features:a. Adapt (to other ideas, developments).b. Modify (change color, motion, sound, odor, form, shape).c. Magnify (stronger, longer, thicker, extra value).d. Minify (smaller, shorter, lighter).e. Substitute (other ingredients, process, power).f. Rearrange (other patterns, layout, sequence, components).g. Reverse (inside out).h. Combine (blend, alloy, assortment, ensemble; combine units, purposes, appeals, ideas).

2. Developing quality variations.3. Developing additional models and sizes (product proliferation).

firms that open branch offices in new cities, states, or countries are practicing market de-velopment. Likewise, firms are practicing market development if they switch from ad-vertising in trade publications to advertising in newspapers or if they add jobbers tosupplement their mail-order sales efforts. Kmart pursued market development with its re-cent emphasis on increasing market share among Hispanics as described in Strategy inAction Exhibit 6–5.

Market development allows firms to practice a form of concentrated growth by identi-fying new uses for existing products and new demographically, psychographically, or ge-ographically defined markets. Frequently, changes in media selection, promotionalappeals, and distribution are used to initiate this approach. Du Pont used market develop-ment when it found a new application for Kevlar, an organic material that police, security,and military personnel had used primarily for bulletproofing. Kevlar now is being used to

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

205

Move over, Martha. Here comesThalia. The sexy Mexico-born pop staris about to add some sizzle to Kmart

Corp.’s tired image. Industry sources say the queen of Latin popwill lend her name to a new line of clothing, shoes, and cos-metics for Kmart. Although unknown to many English-speakingAmericans, Thalia (pronounced Tah-lee-ah) has a big followingamong Hispanics in the United States. The exclusive apparel lineis part of a new strategy to woo Hispanic shoppers that may beKmart’s best hope for reviving its flagging business.

For years, Kmart has struggled to find a niche betweenWal-Mart’s low prices and Target’s cheap chic. Kmart’s biggestfailure, last year’s price war with Wal-Mart, helped land thecompany in bankruptcy court. Now, in its bid to survive, Kmartis latching on to the one advantage it has over its discount ri-vals: stores in heavily populated urban areas. That meanscatering more to multicultural consumers, who already makeup nearly 40 percent of Kmart’s sales.

Thalia’s line is just the start. Kmart says it hopes to an-nounce a similar deal with an African American celebrity byyear-end. Meanwhile, it is adding more Hispanic merchandiseto its stores and reaching out to Hispanics with new Spanish-language ads and publications. “It’s a very strong step Kmartis taking,” says Kurt Barnard, publisher of Barnard’s RetailTrend Report. “It’s going to pay big dividends.”

The strategy isn’t risk-free. Kmart could alienate its existingcustomers if it swings too far toward the Hispanic market. AndWal-Mart, already targeting Hispanics, plans to open more ur-ban stores. “There’s a window of opportunity for Kmart,” saysIra Kalish, chief economist at Columbus (Ohio) consultant Re-tail Forward, Inc., “But it’s going to close quickly.”

Kmart is coming late to this party. Wal-Mart and Sears,Roebuck & Co. several years ago began letting local managersbuy products suited to their communities. Kmart’s previousmanagement thought it more efficient for buyers at head-quarters to purchase for stores nationwide. But, says CEOJames B. Adamson, who took over in March, “people sittingin Troy, Mich., can’t understand the difference between storesin Los Angeles, New York, Texas, or Miami.”

That’s why Adamson is giving store managers more sayover what goes on their shelves. For Frank Gonzales, managerof a San Jose (Calif.) Kmart, that means selling tortilla warm-ers, tamale pots, and such produce as avocados, mangoes,and cilantro. “We were missing a lot of those sales,” saysGonzales.

Kmart knows its Hispanic focus must not be seen as pan-dering. “They’ve got to know you’re not giving them lip serv-ice,” says Adamson, who is credited with turning around theDenny’s restaurant chain after complaints of racial discrimina-tion tarnished its image. In an effort to build loyalty, Kmart islaunching on Sept. 15 La Vida, a four-page weekly magazinein Spanish to go out with a new Spanish ad circular. It will fea-ture celebrities and lifestyle articles.

With Hispanics expected to outnumber African Americansby 2009, this may be Kmart’s best chance. But it will take morethan Hispanic shoppers to save the company. Its problems—ranging from poor inventory controls to lousy distribution—are deep-seated and can’t be fixed overnight. But gettingshoppers back is a start. And Thalia may help.

Source: By Joann Muller in Troy, Mich., with Wendy Zellner in Dallas.BusinessWeek, September 9, 2002, p. 46.

Strategy in ActionKmart Con Salsa: Will It Be Enough? Exhibit 6–5

refit and maintain wooden-hulled boats, since it is lighter and stronger than glass fibersand has 11 times the strength of steel.

The medical industry provides other examples of new markets for existing products. TheNational Institutes of Health’s report of a study showing that the use of aspirin may lowerthe incidence of heart attacks was expected to boost sales in the $2.2 billion analgesic mar-ket. It was predicted that the expansion of this market would lower the market share ofnonaspirin brands, such as industry leaders Tylenol and Advil. Product extensions currentlyplanned include Bayer Calendar Pack, 28-day packaging to fit the once-a-day prescriptionfor the prevention of a second heart attack.

Another example is Chesebrough-Ponds, a major producer of health and beauty aids,which decided several years ago to expand its market by repacking its Vaseline PetroleumJelly in pocket-size squeeze tubes as Vaseline “Lip Therapy.” The corporation decided toplace a strategic emphasis on market development, because it knew from market studiesthat its petroleum-jelly customers already were using the product to prevent chapped lips.Company leaders reasoned that their market could be expanded significantly if the productwere repackaged to fit conveniently in consumers’ pockets and purses.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

206

PepsiCo Corp. diverted some of itsadvertising attention away from itsflagship cola toward newer and nar-

rower brands like Sierra Mist and Pepsi Twist. It was the latestsign of how the soft-drink giant had reformulated its missionfrom bolstering core brands like Pepsi-Cola and MountainDew to peppering the market with niche products and brandextensions. Pepsi’s market had splintered and big brands nolonger had universal appeal. To attract a younger, less cohesivegeneration, Purchase (N.Y.)-based Pepsi had to rethink theway it developed and marketed its wares. “The era of the massbrand has been over for a long time,” said David Burwick,chief marketing officer of Pepsi-Cola North America.

Pepsi’s response had been a raft of new products, mostbearing the Pepsi or Mountain Dew names. Its biggest hit hadbeen cherry-flavored, caffeine-loaded Mountain Dew CodeRed. Pepsi Twist and berry-flavored Pepsi Blue had developedmore modest followings. Sierra Mist was a youth-skewed chal-lenger to Cadbury Schweppes PLC’s 7 Up.

Code Red, Twist, Blue, and Mist accounted for barely 5 per-cent of Pepsi’s soft-drink sales. In the past, Pepsi might nothave bothered with such small fry. In 2003, though, it waslooking for products that could crack a hard-to-reach demo-graphic group. Code Red, for example, had reeled in urban-ites, women, and African Americans who had not previouslyshown any impulse to do the Dew. That could have helped off-set flagship Pepsi’s 2 percent volume sales decline in 2002.

Because these new drinks were more narrowly targeted,Pepsi had to refine its marketing techniques. To launch CodeRed in 2001, the company handed out a million samples atyouth magnets like the Winter X Games and the NCAA FinalFour basketball tourney before the brand was available instores. That helped create a buzz that got Code Red off to abrisk start. For teen-oriented Pepsi Blue last fall, Pepsi went be-yond hiring rock stars to appear in ads. Instead, it worked outan innovative deal with Universal Music Group.

Source: Excerpted from Gerry Khermouch, “Call It the Pepsi BlueGeneration.” BusinessWeek, February 3, 2003, p. 96.

Strategy in ActionCall It the Pepsi Blue Generation Exhibit 6–6

Product DevelopmentProduct development involves the substantial modification of existing products or the cre-ation of new but related products that can be marketed to current customers through estab-lished channels. The product development strategy often is adopted either to prolong thelife cycle of current products or to take advantage of a favorite reputation or brand name.The idea is to attract satisfied customers to new products as a result of their positive expe-rience with the firm’s initial offering. The bottom section in Exhibit 6–4 lists some of theoptions available to firms undertaking product development. A revised edition of a collegetextbook, a new car style, and a second formula of shampoo for oily hair are examples ofthe product development strategy.

A detailed example of Pepsi’s product development activities is provided in Exhibit 6–6,Strategy in Action. In 2001, Pepsi changed its strategy on beverage products by creating newproducts to follow the industry movement away from mass branding. This new movement wasdesigned to attract a younger, hipper customer segment. Pepsi’s new products include a versionof Mountain Dew, called Code Red, and new Pepsi brands, called Pepsi Twist and Pepsi Blue.

The product development strategy is based on the penetration of existing markets by in-corporating product modifications into existing items or by developing new products witha clear connection to the existing product line. The telecommunications industry providesan example of product extension based on product modification. To increase its estimated8 to 10 percent share of the $5 to $6 billion corporate user market, MCI CommunicationCorporation extended its direct-dial service to 146 countries, the same as those serviced byAT&T, at lower average rates than those of AT&T. MCI’s addition of 79 countries to its net-work underscores its belief in this market, which it expects to grow 15 to 20 percent annu-ally. Another example of expansions linked to existing lines is Gerber’s decision to engagein general merchandise marketing. Gerber’s recent introduction included 52 items thatranged from feeding accessories to toys and children’s wear. Likewise, Nabisco Brandsseeks competitive advantage by placing its strategic emphasis on product development.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 207

With headquarters in Parsippany, New Jersey, the company is one of three operating unitsof RJR Nabisco. It is the leading producer of biscuits, confections, snacks, shredded cere-als, and processed fruits and vegetables. To maintain its position as leader, Nabisco pursuesa strategy of developing and introducing new products and expanding its existing productline. Spoon Size Shredded Wheat and Ritz Bits crackers are two examples of new productsthat are variations on existing products.

InnovationIn many industries, it has become increasingly risky not to innovate. Both consumer and in-dustrial markets have come to expect periodic changes and improvements in the productsoffered. As a result, some firms find it profitable to make innovation their grand strategy.They seek to reap the initially high profits associated with customer acceptance of a new orgreatly improved product. Then, rather than face stiffening competition as the basis of prof-itability shifts from innovation to production or marketing competence, they search forother original or novel ideas. The underlying rationale of the grand strategy of innovationis to create a new product life cycle and thereby make similar existing products obsolete.Thus, this strategy differs from the product development strategy of extending an existingproduct’s life cycle. For example, Intel, a leader in the semiconductor industry, pursues ex-pansion through a strategic emphasis on innovation. With headquarters in California, thecompany is a designer and manufacturer of semiconductor components and related com-puters, of microcomputer systems, and of software. Its Pentium microprocessor gives adesktop computer the capability of a mainframe.

While most growth-oriented firms appreciate the need to be innovative occasionally, afew firms use it as their fundamental way of relating to their markets. An outstanding ex-ample is Polaroid, which heavily promotes each of its new cameras until competitors areable to match its technological innovation; by this time, Polaroid normally is prepared to in-troduce a dramatically new or improved product. For example, it introduced consumers inquick succession to the Swinger, the SX-70, the One Step, and the Sun Camera 660.

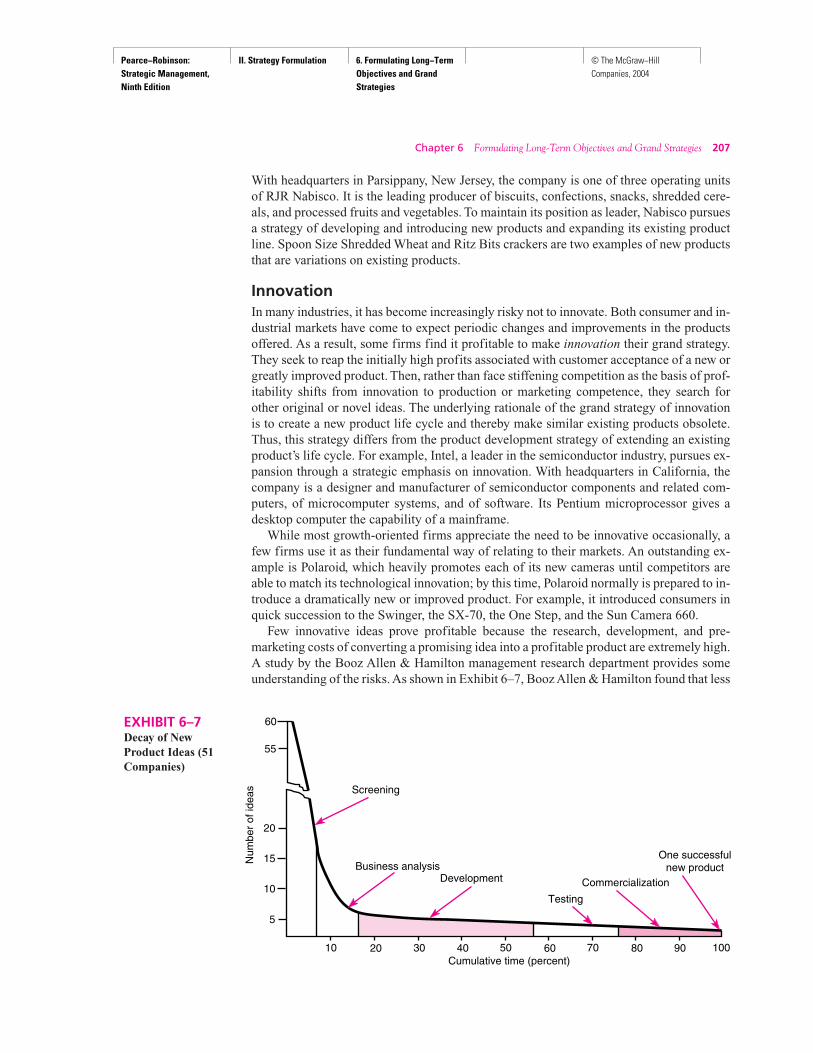

Few innovative ideas prove profitable because the research, development, and pre-marketing costs of converting a promising idea into a profitable product are extremely high.A study by the Booz Allen & Hamilton management research department provides someunderstanding of the risks. As shown in Exhibit 6–7, Booz Allen & Hamilton found that less

EXHIBIT 6–7Decay of NewProduct Ideas (51Companies)

10 20 30 40 50 60 70 80 90 100

20

10

5

15

60

55

Num

ber

of id

eas Screening

Business analysisDevelopment

Testing

Commercialization

One successfulnew product

Cumulative time (percent)

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

208

Measured against the nation’s wire-less giants, VoiceStream WirelessCorp. has been a bit of a pipsqueak.

So why would Germany’s Deutsche Telekom pay an eye-popping $21,639 per subscriber for the little Bellevue, Wash-ington, cell phone company? Simply put, Deutsche Telekomis not buying subscribers in the United States. It’s buying po-tential—in this case, the potential to become a dominantplayer—not just in the United States, but globally. By the endof 2000, only about 32.5 percent of the U.S. population wasusing some form of wireless compared with 52 percent in Eu-rope and 60 percent in Japan. Growth prospects in such a rel-atively undeveloped market, the German executives reckon,are so high that their company will emerge almost immedi-ately as a formidable rival. U.S. telecom execs say a DT-VoiceStream link will force U.S. players to step up efforts toprovide wireless Net service to a broader market, includingoverseas.

To gain this kind of sway over the lucrative U.S. market andthe global market, Deutsche Telekom felt it was worth signifi-cantly besting the $4,390 per subscriber Britain’s Vodafonepaid for AirTouch in 1999 or the estimated $12,400 that thecombined Vodafone-AirTouch paid for Mannesmann earlier

this year. That has set off a torrent of criticism that it has wildlyoverpaid for its position. However, Deutsche Telekom’s CEOSommer is confident. Here’s what he considered when heagreed to the price: VoiceStream owns licenses in 23 of thetop 25 U.S. markets. In wireless lingo, its licenses cover areaswith a 220 million subscriber base. Though it has relatively fewsubscribers signed up and currently does not actually provideservice to many of the locales where it holds licenses, it isadding subscribers at a sizzling pace—an 18.5 percent growthrate that is among the top in the industry.

Wireless companies across the country are taking note,given DT’s deep pockets and promise to make a starting in-vestment of at least $5 billion in VoiceStream. With the $5 bil-lion, VoiceStream can accelerate construction of wirelesssystems in places like California and Ohio. Stanton estimatesthat the cash infusion will help him push up the roll-out of hisservice by 6 to 18 months. Also, Deutsche Telekom’s cash is ex-pected to allow VoiceStream to participate in a major way inthe upcoming auction of more spectrum licenses by the FCC.

Source: Excerpted from R. O. Crockett and D. Fairlamb, August 7,2000, “Deutsche Telekom’s Wireless Wager,” BusinessWeek (3693),pp. 30–32.

Global Strategy in ActionDeutsche Telekom Growth Strategy of Horizontal Acquisition Exhibit 6–8

than 2 percent of the innovative projects initially considered by 51 companies eventuallyreached the marketplace. Specifically, out of every 58 new product ideas, only 12 pass aninitial screening test that finds them compatible with the firm’s mission and long-term ob-jectives, only 7 remain after an evaluation of their potential, and only 3 survive develop-ment attempts. Of the three survivors, two appear to have profit potential after testmarketing and only one is commercially successful.

Horizontal IntegrationWhen a firm’s long-term strategy is based on growth through the acquisition of one or moresimilar firms operating at the same stage of the production-marketing chain, its grand strat-egy is called horizontal integration. Such acquisitions eliminate competitors and providethe acquiring firm with access to new markets. One example is Warner-Lambert’s acquisi-tion of Parke Davis, which reduced competition in the ethical drugs field for Chilcott Lab-oratories, a firm that Warner-Lambert previously had acquired. Another example is thelong-range acquisition pattern of White Consolidated Industries, which expanded in the re-frigerator and freezer market through a grand strategy of horizontal integration, by acquir-ing Kelvinator Appliance, the Refrigerator Products Division of Bendix WestinghouseAutomotive Air Brake, and Frigidaire Appliance from General Motors. Nike’s acquisitionin the dress shoes business and N. V. Homes’s purchase of Ryan Homes have vividly ex-emplified the success that horizontal integration strategies can bring.

Exhibit 6–8, Global Strategy in Action, describes Deutsche Telekom growth strategy ofhorizontal acquisition. Deutsche Telekom was a dominant player in the European wirelessservices market, but without a presence in the fast-growing U.S. market. To correct this lim-

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

Chapter 6 Formulating Long-Term Objectives and Grand Strategies 209

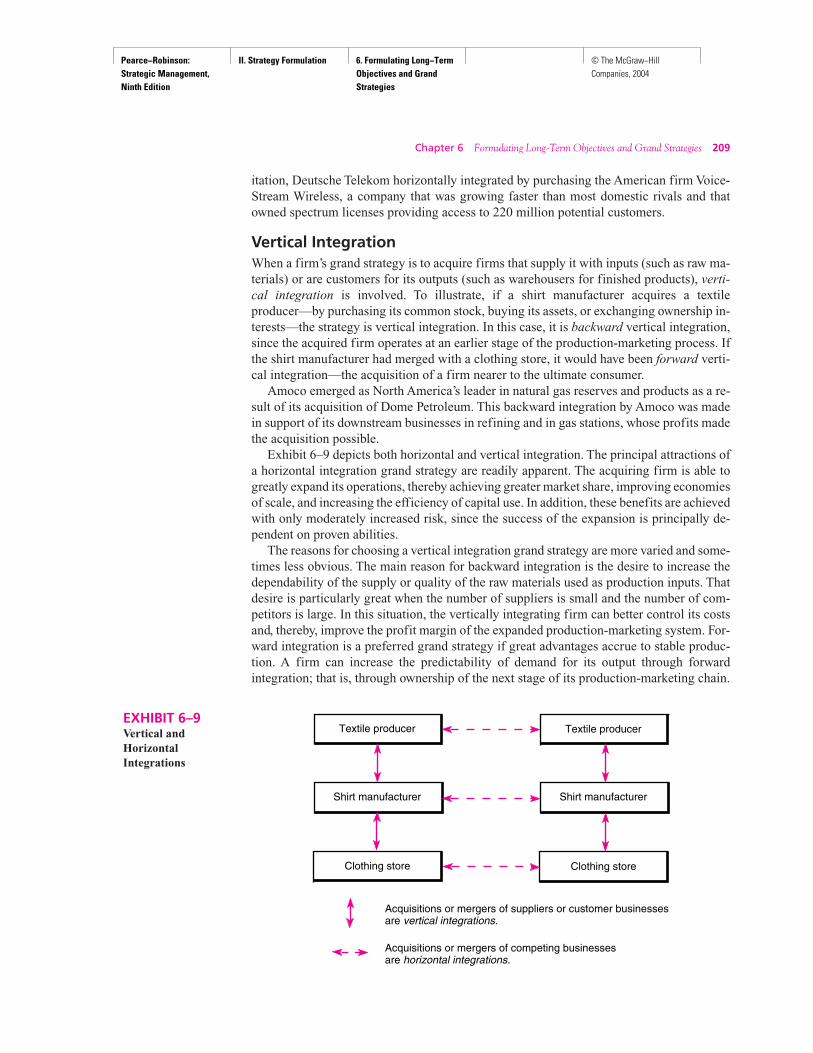

EXHIBIT 6–9Vertical andHorizontalIntegrations

Textile producer

Shirt manufacturer

Clothing store

Textile producer

Shirt manufacturer

Clothing store

Acquisitions or mergers of suppliers or customer businessesare vertical integrations.

Acquisitions or mergers of competing businessesare horizontal integrations.

itation, Deutsche Telekom horizontally integrated by purchasing the American firm Voice-Stream Wireless, a company that was growing faster than most domestic rivals and thatowned spectrum licenses providing access to 220 million potential customers.

Vertical IntegrationWhen a firm’s grand strategy is to acquire firms that supply it with inputs (such as raw ma-terials) or are customers for its outputs (such as warehousers for finished products), verti-cal integration is involved. To illustrate, if a shirt manufacturer acquires a textileproducer—by purchasing its common stock, buying its assets, or exchanging ownership in-terests—the strategy is vertical integration. In this case, it is backward vertical integration,since the acquired firm operates at an earlier stage of the production-marketing process. Ifthe shirt manufacturer had merged with a clothing store, it would have been forward verti-cal integration—the acquisition of a firm nearer to the ultimate consumer.

Amoco emerged as North America’s leader in natural gas reserves and products as a re-sult of its acquisition of Dome Petroleum. This backward integration by Amoco was madein support of its downstream businesses in refining and in gas stations, whose profits madethe acquisition possible.

Exhibit 6–9 depicts both horizontal and vertical integration. The principal attractions ofa horizontal integration grand strategy are readily apparent. The acquiring firm is able togreatly expand its operations, thereby achieving greater market share, improving economiesof scale, and increasing the efficiency of capital use. In addition, these benefits are achievedwith only moderately increased risk, since the success of the expansion is principally de-pendent on proven abilities.

The reasons for choosing a vertical integration grand strategy are more varied and some-times less obvious. The main reason for backward integration is the desire to increase thedependability of the supply or quality of the raw materials used as production inputs. Thatdesire is particularly great when the number of suppliers is small and the number of com-petitors is large. In this situation, the vertically integrating firm can better control its costsand, thereby, improve the profit margin of the expanded production-marketing system. For-ward integration is a preferred grand strategy if great advantages accrue to stable produc-tion. A firm can increase the predictability of demand for its output through forwardintegration; that is, through ownership of the next stage of its production-marketing chain.

Pearce−Robinson: Strategic Management, Ninth Edition

II. Strategy Formulation 6. Formulating Long−Term Objectives and Grand Strategies

© The McGraw−Hill Companies, 2004

210 Part Two Strategy Formulation

3Godfrey Devlin and Mark Bleackley, “Strategic Alliances—Guidelines for Success,” Long Range Planning,October 1988, pp. 18–23.

Some increased risks are associated with both types of integration. For horizontally inte-grated firms, the risks stem from increased commitment to one type of business. For verti-cally integrated firms, the risks result from the firm’s expansion into areas requiring strategicmanagers to broaden the base of their competences and to assume additional responsibilities.

Concentric DiversificationGrand strategies involving diversification represent distinctive departures from a firm’s ex-isting base of operations, typically the acquisition or internal generation (spin-off) of a sep-arate business with synergistic possibilities counterbalancing the strengths and weaknessesof the two businesses. For example, Head Ski initially sought to diversify into summersporting goods and clothing to offset the seasonality of its “snow” business. However, di-versifications occasionally are undertaken as unrelated investments, because of their highprofit potential and their otherwise minimal resource demands.

Regardless of the approach taken, the motivations of the acquiring firms are the same:

• Increase the firm’s stock value. In the past, mergers often have led to increases in thestock price or the price-earnings ratio.

• Increase the growth rate of the firm.

• Make an investment that represents better use of funds than plowing them into inter-nal growth.

• Improve the stability of earnings and sales by acquiring firms whose earnings and salescomplement the firm’s peaks and valleys.

• Balance or fill out the product line.

• Diversify the product line when the life cycle of current products has peaked.

• Acquire a needed resource quickly (e.g., high-quality technology or highly innovativemanagement).

• Achieve tax savings by purchasing a firm whose tax losses will offset current or futureearnings.

• Increase efficiency and profitability, especially if there is synergy between the acquiringfirm and the acquired firm.3