Embed Size (px)

Citation preview

A Study of Impact of Financial Inclusion on Rural Development Page 1

Chapter –I

Introduction and Conceptual Framework

1.0 Introduction:

The meaning of finance starts where there is a general acceptance of what

is being offered as services. The World Bank financial access (2009)

looked at the financial access from the view point of differences between

developed and under-developed countries. Their findings were very

distinctive and explorative. They discovered that the developed European

countries were better exposed to financial services and accounts ownership.

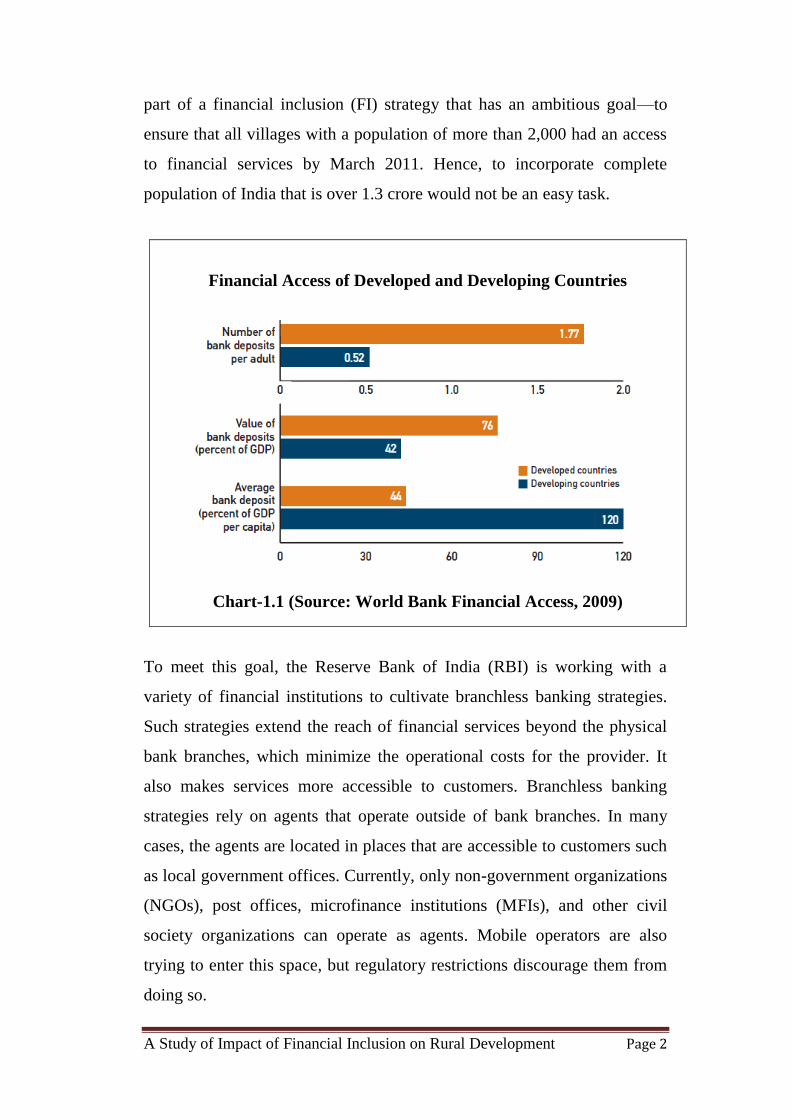

They collected some set of indicators of financial access in countries

around the world (Refer Chart 1.1). Such indicators included the number

of deposit accounts and loans, the number of deposit clients and borrowers,

and the number of financial access points, such as branches, agents, and

automated teller machines (ATMs).

The Italians studied, with the use of a survey on their different territories, it

was to better understand the new typology of customer who could be more

effectively integrated into society and the ordinary financial system. It is

also seen as a policy objective for national policymakers, multilateral

institutions, and others in the economic development field. According to

Mitchell, (2003), a developed financial system on its own cannot bring

about economic growth but it can contribute to it.

The Indian government has undertaken a social banking program as part of

its development efforts that has two main objectives. The first is to extend

formal credit and savings opportunities to the poor and marginalized

segments of the population. The second is to displace informal service

providers such as moneylenders. More recently, the opening of no-frills

savings accounts, with zero balances and low maintenance fees, has been a

crucial policy initiative. Such accounts are being offered at scale, and are

A Study of Impact of Financial Inclusion on Rural Development Page 2

part of a financial inclusion (FI) strategy that has an ambitious goal—to

ensure that all villages with a population of more than 2,000 had an access

to financial services by March 2011. Hence, to incorporate complete

population of India that is over 1.3 crore would not be an easy task.

To meet this goal, the Reserve Bank of India (RBI) is working with a

variety of financial institutions to cultivate branchless banking strategies.

Such strategies extend the reach of financial services beyond the physical

bank branches, which minimize the operational costs for the provider. It

also makes services more accessible to customers. Branchless banking

strategies rely on agents that operate outside of bank branches. In many

cases, the agents are located in places that are accessible to customers such

as local government offices. Currently, only non-government organizations

(NGOs), post offices, microfinance institutions (MFIs), and other civil

society organizations can operate as agents. Mobile operators are also

trying to enter this space, but regulatory restrictions discourage them from

doing so.

Financial Access of Developed and Developing Countries

Chart-1.1 (Source: World Bank Financial Access, 2009)

A Study of Impact of Financial Inclusion on Rural Development Page 3

By late 2000s, the significance of an inclusive financial system has been

extensively recognized, leading to becoming a priority policy in many

countries. Initiatives for building inclusive financial systems have come

from the financial regulators, the governments and the banking industry.

Several countries have initiated legislative measures, for example, The

Community Reinvestment; Act, 1997 of the United States of America

requires banks to offer credit throughout their area of operation and

prohibits them from targeting only the rich neighborhoods. The French law

against exclusion (Loi du, Juillet 1998 contre exclusion) emphasizes an

individual‘s right to have a bank account. In the United Kingdom, a

Financial Inclusion Task Force was constituted by the government in 2005

in order to monitor the development on financial inclusion.

Among several initiatives of the banking sector in promoting financial

inclusion are The German Bankers Association‟s Voluntary Codes,

1996 to provide for everyman a current banking account that facilitates

basic banking transactions, introduction of Mzansi, a low cost bank

account, in 2004 for financially excluded people by the South African

Banking Association and initiatives by the RBI to achieve greater

financial inclusion, such as facilitating no-frills accounts and ―General

Credit Cards‖ for low deposit and credit. Alternative financial institutions,

such as micro-finance institutions and Self-Help Groups are also promoted

in many countries in order to provide financial services to the excluded.

Multilateral organizations such as the World Bank (WB) and the

International Monetary Fund (IMF) have also paid focused attention to the

issue of financial inclusion through policy prescriptions and guidelines. In

addition, the IMF has recently initiated ―Financial Access Survey‖ in an

endeavor to put together cross country data and information relating to the

issue of financial inclusion.

A Study of Impact of Financial Inclusion on Rural Development Page 4

Technology service providers such as FINO and A Little World (ALW) are

key facilitators in this financial inclusion (FI) effort. These companies

provide the platform on which the remote transactions are processed and

they work with banks to open accounts at scale. The companies also have a

mandate to handle government to person (G2P) payments in certain areas.

As part of the G2P efforts, they are providing no-frills savings accounts to

millions of unbanked individuals.

Such FI efforts have been successful in terms of enrollment. Nearly 60% of

the adult population has a bank account. This is high when compared with

other developing countries such as South Africa (32%), Tanzania (6%) or

Colombia (39%) but low when compared with Denmark (99%), the UK

(88%) or the US (91%). An additional 584 million accounts, however,

must be added for India to reach its 100% inclusion target.

Technologies such as debit and credit cards, telephone and Internet

banking, automatic teller machines (ATMs), and biometric point of

transaction (POT) terminals have been vital to such success. They enable

remote accessibility to financial services and enhance security for

associated transactions. This has extended and accelerated the FI drive.

However, despite this success, evidence suggests that access has not

translated into usage. A study in Tamil Nadu found that 72% of poor

individuals had zero or minimum balances after holding their no-frills

accounts for one year. A study of G2P recipients found this number to be

even higher, with 85% of these accounts being dormant. The study further

noted that only 5% of G2P recipients made deposits into their no-frills

accounts. The remainder withdrew all funds and thereafter funneled their

wages into informal savings mechanisms.

Accessibility was noted as a major issue. Recipients paid nearly 50% of

their daily wage to travel to the bank. The queues were also long: 70% said

A Study of Impact of Financial Inclusion on Rural Development Page 5

that visiting a bank caused them to lose an entire work day. A lack of

attention from formal financial institutions also posed a barrier. 85% of

respondents said the benefits of the account were not explained by bank

staff during enrollment. Another 87% claimed the features of the account

were not made clear. A variety of other reasons have been given for such

low levels of usage, from lack of interest by the poor to inadequate design

of financial services .

The academic literature has adequately discussed the close relation

between financial development and economic growth. However, there has

not been much discussion on whether financial development implies

financial inclusion. It has been observed that even well-developed financial

systems have not succeeded to be all-inclusive and certain segments of the

population remain outside the formal financial systems. The importance of

an inclusive financial system is widely recognized in the policy circle and

financial inclusion is seen as a policy priority in many countries.

An inclusive financial system is desirable for many reasons. First, it

facilitates efficient allocation of productive resources. Second, access to

appropriate financial services can significantly improve the day-to-day

management of finances. And third, an all-inclusive financial system can

help reduce the growth of informal sources of credit (such as

moneylenders) which often tend to be exploitative. Thus, an all-inclusive

financial system enhances efficiency and welfare by providing avenues for

secure and safe saving practices and by facilitating a whole range of

efficient financial services.

In banking worldwide, the service environment is becoming very

competitive and is featured by many demanding customers and banks are

seeking various ways of getting more unreached areas. Even so, many parts

of the underdeveloped world do not share a similar view in terms of the

A Study of Impact of Financial Inclusion on Rural Development Page 6

availability of banking services at their disposal. Africa has been at the

center of attraction in terms of this. In some areas of concern, there is the

issue of long distances between communities and bank branches and also

the unavailability of cheaper banking facilities. Some of them incur some

amount of cost on wanting to have access to ATMs or other banking

services. Sometimes, the issue could be that some people do not see the

need for these services and so banks have to device several means of

easing off the pressures of accessing these services. Therefore, the quality

of service becomes an integral part of the financial institutions attempt to

reach the unbanked. The attitude of banks and non-banking institutions

should be channeled towards seeing these unreached areas as a competitive

edge as they constitute a majority of the population in underdeveloped

areas. There is a need to further look into the matter of financial

exclusion/inclusion, service quality and strategies that would help in

customer outreaching.

1.1 Understanding Financial Exclusion:

Financial products play an important part in today‘s society, being able to

access and use a wide range of financial products and services is now

necessary ‗to lead a normal social life‘ (Gloukoviezoff, 2007). This

‗financialisation‘ of British society entails significant consequences for

those who find it difficult to access and/or use these products. For example,

private service provision can be more expensive for those who pay utility

bills in cash and a bank account is now generally required for receiving

wages (Kempson, 1994; Kempson & Whyley, 1998). The requirement for

financial products also needs to be understood against the decline of social

welfare provision, which makes it increasingly necessary for individuals to

make their own provision against risk (Anderloni et. al., 2008) estimate

that while in the 15 ‗older‘ European Union countries, two out of ten of the

adult population do not have access to transaction banking services; three

in ten have no savings and four in ten have no credit facilities, this rises

A Study of Impact of Financial Inclusion on Rural Development Page 7

significantly in the new member states where more than half do not have

transaction accounts, a similar proportion have no savings and almost three

quarters have no immediate access to credit. Furthermore, there are

increasing fears that the current economic downturn has intensified levels

of exclusion partly attributable to a new phase of risk aversion and reduced

outreach by financial institutions, which has restricted the flow of

affordable credit particularly to those on lower incomes.

Certain social groups are especially vulnerable to financial exclusion

including the low paid, unemployed, the elderly, young people not in

education, training or employment and people with disabilities (Anderloni

et. al., 2008). The concept of financial exclusion, then, refers to this

inability of individuals to access and/or effectively use financial products

that help them to participate in the range of activities that constitute social

life.

Financial exclusion is a relatively new concept which was first used in

1994 to describe the process of withdrawal of financial institutions

predominantly from deprived areas (Leyshon, 1994). While this body of

literature refers to the spatial dimension of the financial exclusion process,

other publications have concentrated on different aspects of the

phenomenon including individual factors and preferences. Financial

exclusion is a phenomenon that often affects a significant minority of

predominantly vulnerable and otherwise disadvantaged people, such as

single parents, social tenants, the long-term unemployed, members of some

minority ethnic communities and those living on persistent low incomes

(Kempson & Whyley, 1999b).

According to the analysis of Kempson & Whyley (1999b), seven per cent

of households in Britain (around 1.5 million) were without any mainstream

financial products in the mid-1990s. In addition, 19% were only marginally

A Study of Impact of Financial Inclusion on Rural Development Page 8

included, having only one or two financial products. In terms of banking,

nearly two million adults were still without a bank account in 2006

(Treasury, 2007b). Some studies also give evidence of regional variations

in financial exclusion, for example, higher levels of banking exclusion in

Northern Ireland and Scotland (Kempson, 1994) and areas of deprivation

(Leyshon & Thrift, 1997). While these studies show that disadvantaged

individuals and households and deprived areas are more likely to be

affected by exclusion from the financial system, it is also associated with

both economic and social costs for those affected. Financial exclusion can

thus both contribute and be the outcome of processes of social exclusion.

Financial inclusion (or, alternatively, financial exclusion) has been defined

in the literature in the context of a larger issue of social inclusion (or

exclusion) in a society. One of the early attempts by Leyshon & Thrift

(1995) defined financial exclusion as referring to those processes that serve

to prevent certain social groups and individuals from gaining access to the

formal financial system. According to Sinclair (2001), financial exclusion

means the inability to access necessary financial services in an appropriate

form.

Exclusion can come about as a result of problems with access, conditions,

prices, marketing or self-exclusion in response to negative experiences or

perceptions. Carbo, et. al., (2005) have defined financial exclusion as

broadly the inability of some societal groups to access the financial system.

The Government of India‘s Committee on Financial Inclusion in India

began its report by defining financial inclusion as the process of ensuring

access to financial services and timely and adequate credit where needed

by vulnerable groups such as the weaker sections and low income groups at

an affordable cost (Rangarajan Committee Report, 2008).

A Study of Impact of Financial Inclusion on Rural Development Page 9

Thus, most definitions indicate that financial exclusion is manifestation of

a much broader issue of social exclusion of certain societal groups such as

the poor and the disadvantaged. For the purpose of this thesis, we define

financial inclusion ‗as a process that ensures the ease of access, availability

and usage of the formal financial system for all members of an economy‘.

This definition emphasizes several dimensions of financial inclusion, viz.,

accessibility, availability and usage of the financial system. These

dimensions together build an inclusive financial system. As banks are the

gateway to the most basic forms of financial services, banking

inclusion/exclusion is often used as analogous to financial

inclusion/exclusion.

1.1.1 Types of Financial Exclusion:

Kempson & Whyley (2000), in their study, established six types of

financial exclusion:

Physical Access Exclusion: It is brought about by the closure of

local banks or building societies and lack of reliable transport to

reach alternatives.

Access Exclusion: This type of access is restricted through risk

assessment, with people being denied a product or service as they

are perceived to be high risks.

Condition Exclusion: This is when conditions are attached to

products or services thereby making them inaccessible to some.

Price Exclusion: This occurs when products are available but at a

price that is unaffordable.

Marketing Exclusion: Where sales and marketing activity is

targeted on some groups, or areas, at the expense of others.

A Study of Impact of Financial Inclusion on Rural Development Page 10

Self Exclusion: When individuals do not seek financial products

and services for reasons including fear of failure, fear of temptation

or lack of awareness.

1.1.2 Causes of Financial Exclusion:

According to the World Bank, (cited in Honohan & King, (2009), the

causes of financial exclusion were broken down into: insufficient income;

discrimination; contractual/information framework; and price and product

features. In their research, they looked to see the reasons that none

financial user give for not using financial products. He asked if it could be

fixed by the financial providers in terms of quality of service, location or

relevance of product.

Kempson (2006) gave some explanations to the reasons why people are

financially excluded. He said that these reasons could vary from country to

country. He stated the importance of bank required identification and

documents, the terms and conditions of bank accounts, levels of bank

charges, physical access and cultural barriers in financial inclusion.

1.1.2.1 Required Identification

Kempson (2006) stated that various types of people with the right means

of identifying themselves fail to meet the banks requirements to open an

account. People like the homeless and unemployed. Everywhere around the

world, banks require a certain proof of identity before some kinds of

services could be offered.

Leyshon & Thrift (1995, cited in the European Commission, 2008)

stated that people with limited income and with some disabilities represent

a high risk to the financial institutions, who then avoid such geographical

locations where these people reside.

A Study of Impact of Financial Inclusion on Rural Development Page 11

1.1.2.2 Financial Liberalization and Over-complexity:

Kempson et. al., (2000, cited in, The European Commission 2008) gave

financial liberalization as one of the societal factors that limits financial

inclusion. Shehzad & De Haan (2008) argued that financial liberalization

reduces the likelihood of financial crises. Contrary to this, it was stated in

the European Commission (2008) that financial liberalization has led to

an increase in the complexity of financial products and providers.

The liberalization of the financial system is comprised of high levels of

administrations of financial institutions, which according to Shehza d &De

Haan (2008) is measured with the presence of interest rate controls, credit

controls, entry barriers, capital account restrictions and supervision of the

banking sector.

Financial liberalization has brought about a striking shift in banking policy

in India and has led to changes in the regional and sectoral pattern of

banking in the country and there has been:

(a) a large-scale closure of commercial bank branches in rural areas;

(b) a widening of inter-State inequality in credit provision,

accompanied by a fall in the proportion of bank credit directed

towards rural areas as well as regions where banking has historically

been underdeveloped;

(c) a sharp fall in the growth of credit flow to agriculture followed by a

revival in the 2000s, but with a changed pattern of distribution of

agricultural credit in favour of urban-based borrowers and corporate

and institutional groups;

(d) the relative exclusion of the disadvantaged and dispossessed

sections of the rural population from the formal financial system;

and

A Study of Impact of Financial Inclusion on Rural Development Page 12

(e) the strengthening of money lending in the countryside

[Ramachandran & Swaminathan (2005), Shetty (2004),

Ramakumar & Chavan (2007), and Chavan (2005 & 2010)]

It is in the period of financial liberalization that the new term ―financial

inclusion‖ has been coined. Financial inclusion may appear similar in name

to the policy of social and development banking, but is inherently different

with respect to policy essentials. ―Financial inclusion‖ has been defined as

the provision of affordable financial services to those who have been left

unattended or under-attended by the formal agencies of the financial

system without compromising on commercial and profitability

considerations in order to ensure the ―long-term sustainability‖ of such

services (RBI, 2008).

The recent approach to financial inclusion is more individual-specific than

previous policy. It incorporates two main instruments: firstly, a no-frills

basic saving bank deposit account facility (including a small overdraft

facility); and secondly, a collateral-free small borrower facility under

microfinance at market-determined rates of interest (RBI, 2006b). Both

these instruments have been used rather rigorously by banks in the 2000s,

either directly or through intermediaries. Banks‘ intermediaries mainly

include Business Correspondents (BCs) and Micro-Finance Institutions

(including non-banking financial companies, trusts, and cooperative

societies). Further, there has been a growing emphasis on the introduction

of advanced technological solutions by banks and their intermediaries.

These solutions include hand-held devices and mobile phones, measures

intended to bring down the costs of administering the large numbers of

small-volume transactions required under financial inclusion. The RBI also

emphasized on designing market-based regulatory incentives for banks for

financial inclusion. The RBI has set targets of providing, by 2012, banking

A Study of Impact of Financial Inclusion on Rural Development Page 13

services through a banking outlet to every village with a population of over

2,000.

1.1.2.3 Terms and Conditions of Bank Accounts:

Different banks across the world have different terms and conditions for

opening accounts with them. Such terms as amount of money to open with,

the amount of minimum/maximum balance etc. This goes a long way to

having an effect on the extent of financial inclusion. Kempson (2006)

explained that these different types of terms and conditions can deter or

prevent people with low incomes to open an account. Some accounts come

with certain contracts that establish the rules on which the accounts are

controlled.

1.1.2.4 Income Inequality and Unemployment:

Kempson (2006) stated that countries with low levels of income inequality

tend to have lower levels of financial exclusion, whereas high financial

exclusion is found in least equal countries. In most areas of the world, a

person who is unemployed and with no source of income is most likely to

be excluded from the use of financial facilities. It is also likely that this will

be due to self-exclusion.

1.1.2.5 Levels of Bank Charges:

OFT (1999, cited in Wallace & Quilgars, 2005) stated that the fear of

getting overdrawn and incurring high bank charges was a major

discouraging factor for many people on low or modest incomes to

obtaining an account. Kempson et. al., (2000, cited in Wallace &

Quilgars, 2005) supported by saying that low income earners prefer bank

services that complies with the needs of low income households.

A Study of Impact of Financial Inclusion on Rural Development Page 14

1.1.2.6 Lack of Physical Access:

The inability to have access to certain financial services could be due to

various reasons like; travel distance, disabilities, or level of knowhow.

According to Kempson (2006), it can also be caused by bank closures

which are due to the intense level of competition and economics in

international banking. The World Bank financial access (2009) stated that

the main barrier to financial inclusion in rural areas is the great distances

that rural residents must travel to reach a bank branch.

1.1.2.7 Cultural Barriers:

―In countries with high levels of financial exclusion, self exclusion by

individuals with low or no income is more of the reason for lack of access

to banking services than direct exclusion by the banks refusing to open

accounts‖ (Kempson, 2006). Help the aged noted that cultural and

language barriers are one of the issues that minority community dwellers

face in accessing financial services.

1.1.2.8 Lack of Effective demand for Services:

Sinclair et. al., (2009) explained that low income means a lack of adequate

demand for services. He stated that such a lack of demand can be attributed

to the failures and limitations of services from current providers of such

services. According to The House of Commons Treasury Committee

2005-06, banking services are central to the challenge of financial

inclusion.

1.1.2.9 Lack of Financial Education:

―A credit union also has an obligation to educate their members in effective

and responsible management of money, and credit unions offer debt and

money advice to their members alongside financial goods and services and

insurance products‖ (Credit Unions Act, 1979 - cited in Commission of

A Study of Impact of Financial Inclusion on Rural Development Page 15

Rural Communities, 2007). The absence of this will inevitably lead to an

exclusion from financial facilities and services.

1.1.3 „Financial Exclusion‟ in Rural Areas:

Financial exclusion has been high on the Government agenda since 2004,

and has gained added impetus following high-profile cases such as the

collapse of the Farepak Christmas savings club and recent turmoil in the

financial markets.

There is much evidence (and many recent reports) to show relative income

poverty (including, but not limited to, low wages) in rural areas,

particularly in sparse rural areas and coastal areas. At the same time,

expenditure on everyday commodities and services (such as heating fuel

and power, and transport) is demonstrably higher for rural residents and

there is evidence to suggest that the accessibility of banks and building

societies has reduced in rural areas8 alongside a trend towards fee-charging

cash machines in rural areas.

The term ‗financial exclusion‘ is used to encapsulate the issues around

financial disadvantage that reach beyond a simple focus on incomes,

although those on low incomes tend to be at particular risk of other forms

of financial disadvantage. For example those on low incomes are more

likely to borrow from ‗alternative lenders‘, incurring high rates of interest,

whilst on the other hand any savings made by those on low incomes are

likely to attract only the lowest tiers of interest rates and be subject to fixed

transaction costs.

A characteristic feature of rural life is a reluctance to seek help among the

rural population, which could mean that indebtedness amongst rural

residents is more difficult to detect. However, what is clear is that face-to-

face advice (which could be more effective than other forms of advice for

A Study of Impact of Financial Inclusion on Rural Development Page 16

the financially excluded) is likely to be harder to access for those in rural

areas, and that the accessibility of banks and building societies has reduced

still further in recent years. Nonetheless, the focus of many schemes and

policy initiatives to tackle financial exclusion to date has been on specific

(mostly urban) areas, at least in the initial stages.

1.2 Understanding Financial Inclusion:

In simple terms, Financial Inclusion means provision of banking services at

an affordable cost to the vast sections of disadvantaged and low-income

groups. These include access to savings, credit, insurance, payments and

remittance facilities by the formal financial system to those who tend to be

excluded. As banking services are viewed as services in public good, the

term financial inclusion means availability of banking services to the entire

population without discrimination. In short, financial inclusion means to

provide access to financial services to all the people in a fair, transparent

and equitable manner at an affordable cost.

A World Bank report states, ―Financial Inclusion, or broad access to

financial services, is defined as an absence of price or non price barrier in

the use of financial services.‖ It recognizes the fact that the financial

inclusion does not imply that all households and firms should be able to

borrow unlimited amounts or transmit funds across the world for some fee.

It makes the point that creditworthiness of the customer is critical in

providing financial services. The report also stresses that the distinction

between ‗access to‘ and ‗use of‘ financial services as it has implication for

policymakers. ‗Access‘ essentially refers to the supply of services, whereas

use is determined by demand and supply. Among the non- users of formal

financial services a clear distinction needs to be made between voluntary

and involuntary exclusion. The problem of financial inclusion addresses

the ‗involuntary excluded‘, as they are the ones who, despite demanding

financial services, do not have access to them.

A Study of Impact of Financial Inclusion on Rural Development Page 17

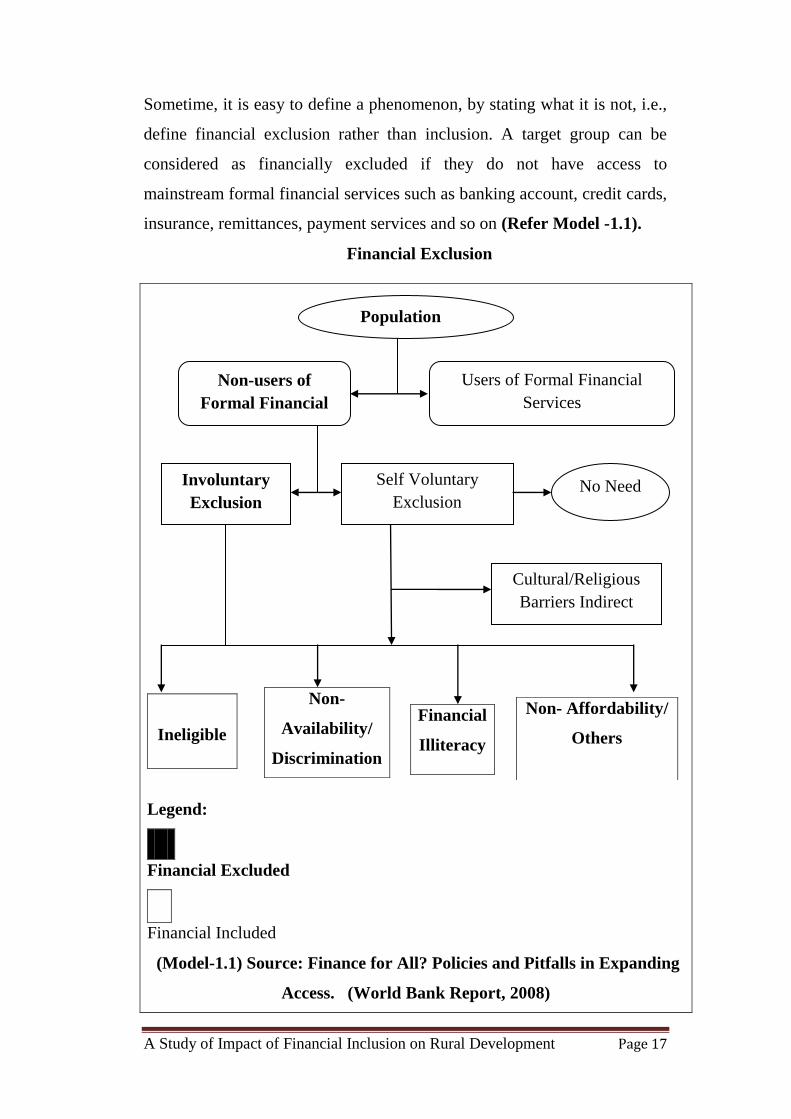

Sometime, it is easy to define a phenomenon, by stating what it is not, i.e.,

define financial exclusion rather than inclusion. A target group can be

considered as financially excluded if they do not have access to

mainstream formal financial services such as banking account, credit cards,

insurance, remittances, payment services and so on (Refer Model -1.1).

Financial Exclusion

Ineligible

Non-

Availability/

Discrimination

Financial

Illiteracy

Non- Affordability/

Others

Legend:

Financial Excluded

Financial Included

(Model-1.1) Source: Finance for All? Policies and Pitfalls in Expanding

Access. (World Bank Report, 2008)

Non-users of

Formal Financial

Services

Users of Formal Financial

Services

No Need

Population

Involuntary

Exclusion

Self Voluntary

Exclusion

Cultural/Religious

Barriers Indirect

access

A Study of Impact of Financial Inclusion on Rural Development Page 18

The financial inclusion needs to be interpreted in a relative dimension.

Depending on the stage of development, the degree of financial inclusion

differs among countries. For example, in a developed country non-payment

of utility bills through banks may be considered as a case of financial

exclusion, however, the same may not be considered as financial exclusion

in an underdeveloped nation as the financial system is not yet developed to

provide sophisticated services. Hence, while making any cross country

comparison due care need to be taken.

Financial Inclusion as defined by RBI, ―Financial Inclusion is the process

of ensuring access to appropriate financial products and services needed by

vulnerable groups such as weaker sections and low income groups at an

affordable cost in a fair and transparent manner by mainstream Institutional

players‖. Financial inclusion is the availability of banking services at an

affordable cost to disadvantaged and low-income groups. In India, the

basic concept of financial inclusion is having a savings or current account

with any bank. In reality, it includes loans, insurance services, and much

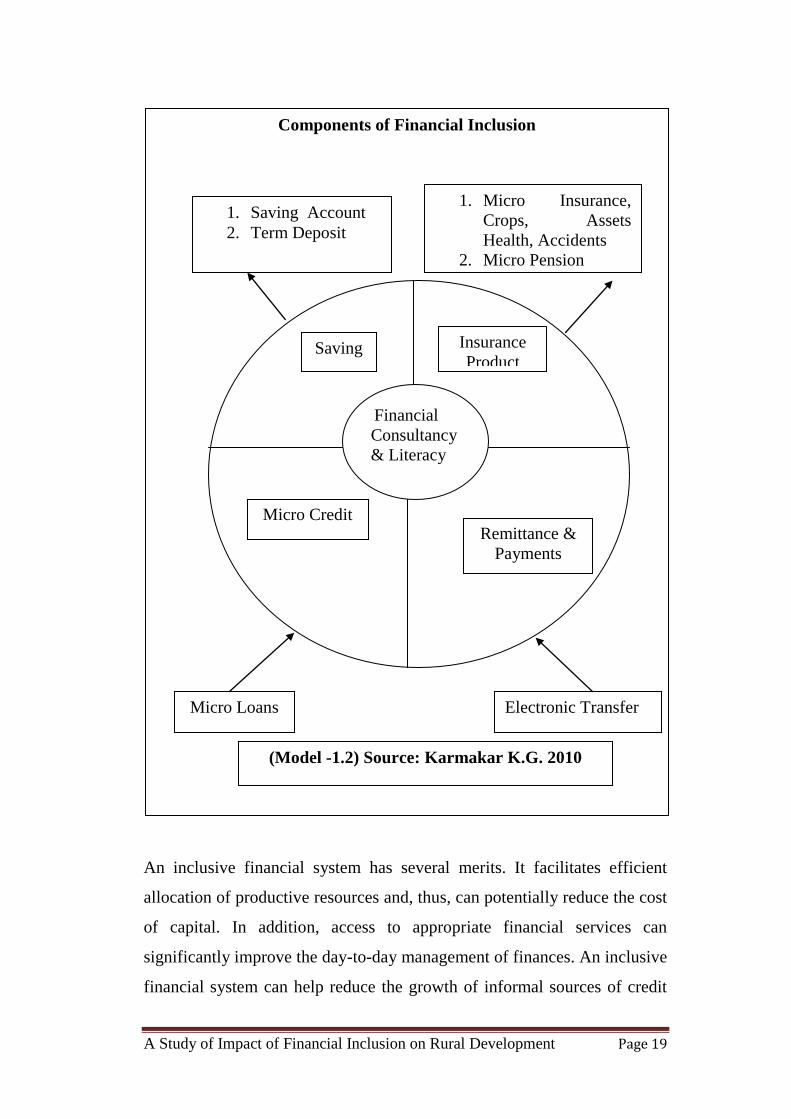

more (Refer Model -1.2).

The importance of an inclusive financial system is widely recognized in the

policy circle and recently, financial inclusion has become a policy priority

in many countries. Initiatives for financial inclusion have come from the

financial regulators, the governments, and the banking industry. Legislative

measures have been initiated in some countries.

The Indian banking system will have to deliver on the plan for financial

inclusion, the system, which demonstrated its resilience in the face of the

recent global financial crisis, should adopt strong and urgent measures to

reach the unbanked segment of society and unlock their savings and

investment potentials.

A Study of Impact of Financial Inclusion on Rural Development Page 19

An inclusive financial system has several merits. It facilitates efficient

allocation of productive resources and, thus, can potentially reduce the cost

of capital. In addition, access to appropriate financial services can

significantly improve the day-to-day management of finances. An inclusive

financial system can help reduce the growth of informal sources of credit

Components of Financial Inclusion

Financial

Consultancy

& Literacy

Saving

Insurance

Product

Micro Credit

Remittance &

Payments

1. Micro Insurance,

Crops, Assets

Health, Accidents

2. Micro Pension

1. Saving Account

2. Term Deposit

Micro Loans

Electronic Transfer

(Model -1.2) Source: Karmakar K.G. 2010

A Study of Impact of Financial Inclusion on Rural Development Page 20

(such as money lenders), which are often found to be exploitative. Thus, an

all-inclusive financial system would enhance efficiency and welfare by

providing avenues for secure and safe saving practices and by facilitating a

whole range of efficient financial services.

In this context, it is imperative that any programme of financial inclusion

must include steps to remove most factors helping exclusion. As a first

step, the RBI devised guidelines exhorting banks to offer a basic ―no-frills‖

account scheme to the public as a step towards empowering the have-nots

and create awareness among them about banking. The very knowledge

about the existence and operation of such a scheme is bound to enthuse a

large number of people among the target sector to access banking and be

aware of the benefits available from banks. Basically, the thrust on

empowerment depends on the stage of development of a society. No-frills

accounts are persuasive initiatives aimed at empowering the excluded lot to

have access to bank accounts and facilitate their participation. In the

meantime, Reserve Bank is also laying significant stress on the expansion

of banking network in un-banked and under-banked areas in its efforts

towards empowerment.

Due to no small part to the stimulus provided by the United Nations Year

of Micro Credit 2005, policymakers across the world have begun to pay

closer attention to increasing financial inclusion. Financial inclusion herein

refers to the timely delivery of financial services to disadvantaged sections

of society. Research in the last decade led us to believe that a well-

functioning and inclusive financial system was linked to faster and

equitable growth (Honohan, 2004). However, despite the attention paid to

financial inclusion and policies devoted to enhancing access to finance,

there was a dearth of information regarding access to finance. The problem

of inadequate information was compounded by the fact that access did not

A Study of Impact of Financial Inclusion on Rural Development Page 21

always lead to usage. This knowledge gap posed a significant challenge in

designing effective policy interventions.

Since 2005, the RBI has promulgated a drive for financial inclusion,

whereby banks promote the participation of every household at the district-

level via savings accounts for the ‗unbanked.‘ This study was an attempt to

arrive at a deeper understanding of the processes behind financial

inclusion. Namely, it proposed to uncover perceptions and dynamics

behind financial inclusion, such as those within unbanked households, as

well as study whether financial inclusion led to usage and/or influences

financial behavior.

It would demonstrate the on-the-ground realities and results of current

initiatives and provide evidence that informs future policies for law

makers. This information would also facilitate the design of appropriate

products driven by client needs to financial institutes. In the case of

microfinance institutions, the evidence herein may help them increase

outreach and hence, financial viability.

The opening of ‗No-frills Accounts‘ is fast emerging as a crucial policy

initiative. The Committee on Financial Inclusion, headed by Dr. C.

Rangarajan, Chairman of the Prime Minister‘s Economic Advisory

Committee, recommended that each semi-urban/rural bank branch opened

roughly 250 bank accounts annually which, if successful, would result in

approximately 11.5 million accounts across the country. As of September

2008, approximately 15.8 million bank accounts have already been opened

as part of the drive. To achieve 100% financial inclusion, however, an

additional 584 million accounts would need to be opened (‗RBI asks banks

to offer credit through no-frill accounts‘, The Economic Times, 12 Sep

2008). Given these developments, it is both timely and pertinent to

A Study of Impact of Financial Inclusion on Rural Development Page 22

examine the implementation of the drive, the utility of accounts to users,

and levels of usage.

The Report viewed financial inclusion as a comprehensive and holistic

process of ensuring access to financial services and timely and adequate

credit, particularly by vulnerable groups such as weaker sections and low

income groups at an affordable cost. Financial inclusion, therefore,

according to the Committee, should include access to mainstream financial

products such as bank accounts, credit, remittances and payment services,

financial advisory services and insurance facilities. Several steps have been

taken by the various banks, NGOs and government to bring the financially

excluded people to the fold of the formal banking services. The cent per

cent financial inclusion drive is progressing all over the country. The

financial inclusion in rural areas is necessary and profitable for banking

sectors.

No doubt, the banking sector in the country is playing its role in reducing

the disparities and is geared up to meet the challenges faced from financial

exclusion. But in future, the bankers need to shoulder more responsibility

because of the challenge to bring all the disadvantaged section of people to

the mainstream of development. The bankers have to pool all available

resources including technology and expertise to take banking to the bottom

of the pyramid, as there are big opportunities to be exploited. In this

background, the present study is an attempt towards evaluating the

outreach of bankers and their level of involvement in promoting financial

inclusion in the district of Indore in Madhya Pradesh.

1.3 Financial Reforms and Rural Credit:

Finance is an extraordinary effective tool in spreading economic

opportunity and fighting against poverty. Wider access to finance helps

both the producers as well as consumers in raising their welfare status.

A Study of Impact of Financial Inclusion on Rural Development Page 23

Access to finance allows the poor to use their rich talents or opens avenue

for greater opportunities. A composite set of services like credit, savings,

and insurance protects from the unexpected shocks or fluctuations.

Therefore, the role of finance has been critical in economic growth and

development as observed in many of the countries over the years. In one of

the early expositions, Schumpeter (1911) argued that the functions and

role of finance are essential for technological innovation and economic

development. A number of studies have found that the poor need financial

services to help them, manage their lives and livelihoods that are complex,

diverse, dynamic and vulnerable, and the poor want their financial services

to respond by being reliable, flexible, continuous and convenient

(Morduch & Rutherford, 2003). Financial system affects growth by

altering the savings rate sometimes by their allocation of savings for capital

producing technologies (Romer, 1986). Credit or other resource allocation

processes of financial institutions can, in principle, lead to efficient

financial management and enhanced growth. Provision of finance

facilitates entrepreneurship, innovation, and improvement of economic

productivity and thus finally contributes to both economic development

and growth.

In India, in the pre-reform period, the commercial banks were nationalized

(between 1969 and 1980) with an objective of extending the financial

services to rural areas. These banks played a vital role in providing

financial services to the rural areas for long period. However, the

introduction of financial reforms had an instantaneous, direct and

remarkable effect on rural credit system. The policies of liberalization have

generated shocks to financial sector and there has been a decline in rural

banking in general, and in priority sector and preferential lending to the

poor in particular (Ramachandran & Swaminathan, 2002). These

changes in pre- and post-economic reforms are explained through

indicators such as the number of rural bank offices, the rural credit

A Study of Impact of Financial Inclusion on Rural Development Page 24

outstanding and deposits, Credit-Deposit (C-D) ratio, credit share in favor

of agriculture and small-scale industries, and credit to the priority sectors.

In the post-reform period, banks were allowed to convert their non-viable

rural branches into satellite offices, or to close down branches at rural

centers served by two or more commercial banks. At the same time, the

regional rural banks were allowed to relocate their loss-making branches to

new places that may be outside the rural areas (Shetty, 2004). It is relevant

here to look at the RBI's (1997) policy on this subject-"Banks were given

the operational freedom to open and relocate branches at semi-urban, urban

and metropolitan centers subject to the approval of respective Boards and

ensuring track record of profit in the last three years‖. The entire scheduled

commercial banking sector was reluctant to opening of rural branches and

the new policy in banking totally arrested the growth of banking in rural

areas. Thus, branch network in rural areas was downsized after the

commencement of financial liberalization.

In the pre-reform period (1991), in India, the percentage of rural bank

branches to the total bank branches was as high as 56.92%. However, in

the post-reform period, there was an ongoing decline in the share of the

rural bank offices which fell below 50% in 1998 and thereafter. In fact, the

present share (percent) of rural bank offices to total bank offices was equal

to that of the 1980s, i.e., 45.69% in 2005 and 45.72% in 1980s. It was clear

that more than 10% of rural bank offices were either closed down or

shifted to more 'profitable' zones for several reasons. However, 'poor

repayment' was cited as the root cause for relocating many rural banks. The

tendency to shift from rural areas had an adverse effect on vulnerable

sector in obtaining credit. This gave an opportunity to the MFIs to feed the

thinning financial services in the rural areas.

There was a sluggish growth of rural deposits and credit in the pre- and

post-reforms period. Before the liberalization of banking sector in India,

A Study of Impact of Financial Inclusion on Rural Development Page 25

the share of rural deposits to the total credit was as high as 15.46% in 1991,

which declined steadily after the reforms to as low as 12.20% in 2005

(relatively deposits in 2005 and 1980 were the same). The C-D ratios have

fallen sharply since the beginning of 1991, both in terms of the amount

sanctioned and amount utilized (Ramachandran & Swaminathan, 2005).

There was a steady decline in the C-D ratios in rural branches from over

73% to around 61% in 1984 and 1991, respectively. After 1991, there was

a sharp decline in the ratio for the rural branches, i.e., as low as 39% in

2001. This was the most miserable facet of banking development in the

past decade (Shetty, 2005). Decline in the C-D ratio was the result of

slowdown of banking activity (low profitability with high non-performing

assets) by the public sector commercial banks in rural areas. There was

relatively a sharp decline in the number of rural and semi-urban bank

offices and in the credit disbursed in the pre- and post-reform periods.

Similar trends were true of total commercial bank credit to agriculture

(Chavan, 2001).

One of the prime objectives of bank nationalization (1969 and 1980) was to

inflate the flow of credit to agriculture and small industries, or this

direction of lending was termed as 'priority sector' lending

(Ramachandran & Swaminathan, 2002 & 2005). The share of these

sectors in the total advances of scheduled commercial banks rose from

14% in 1969 to 33% in 1980. In the mid-1980s, the RBI had set a target of

40% for priority sector lending and this target was over achieved during the

period 1986-89. From 1991 to 1996, the share of priority sector advances

fell in line with the recommendations of the Narasimham Committee.

From 1990-91 to 1996-97, loan accounts to agriculture fell by 5 million

(Narayana, 2000). While 52% of bank credit in rural areas went towards

agriculture in 1985, the proportion fell to 38% in 1998 (Nair, 1999). In the

post-economic reform period, there was a sharp decline in the priority

sector lending, and the same trend continued until the end of March 2003.

A Study of Impact of Financial Inclusion on Rural Development Page 26

However, the situation changed after 2004; there was a slight increase in

the priority sector advances. It is interesting to observe that the reforms

introduced since 1991 in the banking system have had a heavy toll on small

borrowers. The spread of banking credit facilities has not only halted but

the number of small borrowers getting financial facilities too sharply

declined in the post-liberalization period.

The World Bank indicated that no official survey of rural access to finance

had been conducted since 1991. However, a survey conducted jointly by

the World Bank and the National Council of Applied Economic

Research (NCAER), the Rural Finance Access Survey (RFAS) 2003

allowed for analysis of some trends between 1991 and 2003 (World Bank,

2004; and Basu & Srivastava, 2005). Following bank nationalization, the

share of banks in rural household debt increased to approximately 61.2% in

1991. Despite these achievements, there still had been little progress in

providing the rural poor with access to formal finance. Rural banks served

primarily the needs of well-off rural borrowers with around 66% of large

farmers having a deposit account and 44% with access to credit, in contrast

to 70% of marginal/landless farmers who did not have a bank account and

87% who are without access to credit. Access to other financial services

like insurance was even more limited for the rural poor. Inadequacies and

incompetence in access to formal financial institutions and the seemingly

extort terms of informal finance for the poor provide a strong need and

ample space for innovative approaches to serve the financial needs of

India's poor. Over the past decade, government, financial institutions and

NGOs have made efforts in partnership, to develop novel financial delivery

approaches. These microfinance approaches have been designed to

combine the safety and reliability of formal finance with the convenience

and flexibility that are typically associated with informal finance (Basu &

Srivastava, 2005).

A Study of Impact of Financial Inclusion on Rural Development Page 27

Against this backdrop, the present study made an attempt to examine the

nature and type of new institutions that have emerged in the Indian

financial system to include the excluded poor. The study also analyzed the

outreach of two dominant microfinance models in India, viz., SHG-Bank

Linkage Program (SBLP) and private MFIs. The study analyzed the

financial inclusion in terms of credit outstanding as well as the number of

clients served over the years, by the new institutions. The major source of

secondary data included the RBI publications, National Bank for

Agriculture and Rural Development (NABARD), MIX (Microfinance

Information exchange) market, Sa-Dhan used for analyzing the outreach

of microfinance models, over the years.

Financial inclusion in developing economies is different than that of

developed economies. In latter where inclusion is a minority, informer it

could be a majority. Elaine Kempson in his research (2006) showed that

in Sweden lower than two per cent of adults did not have an account in

2000 and in Germany, the figure was around three per cent. Another

research by (Buckland et. al., 2005) showed that less than four per cent of

adults in Canada and five per cent in Belgium lacked a bank account.

Therefore, it was also mentioned in academia that a better way to analyze

financial inclusion in developing economies is to actually see financial

exclusion.

1.4 Financial Inclusion in India:

In India, the focus of the financial inclusion at present is confined to

ensuring a bare minimum access to a savings bank account without frills,

to all. Internationally, the financial inclusion has been viewed in a much

wider perspective. Having a current account / savings account on its own,

is not regarded as an accurate indicator of financial inclusion.

A Study of Impact of Financial Inclusion on Rural Development Page 28

'Financial Inclusion' efforts should offer at a minimum, access to a range

of financial services including savings, long and short term credit,

insurance, pensions, mortgages, money transfers, etc. and all this at a

reasonable cost. Out of 19.9 crore households in India, only 6.82 crore

households have access to banking services. As far as rural areas are

concerned; out of 13.83 crore rural households in India, only 4.16 crore

rural households have access to basic banking services. In respect of urban

areas, only 49.52% of urban households have access to banking services.

Over 41% of adult population in India did not have bank account.

The Report Committee on Financial Inclusion headed by Dr. C.

Rangarajan (2008) has observed that financial inclusion must be taken up

in a mission mode and suggested a National Mission on Financial Inclusion

(NMFI) comprising representation of all stakeholders for suggesting the

overall policy changes required, and supporting stakeholders in the domain

of public, private and NGO sectors in undertaking promotional initiatives.

A sample study carried out by the Banking Codes and Standards Board

of India in Mumbai revealed the poor awareness about ‗no-frills‘ accounts

and relaxed Know Your Customers (KYC) norms amongst the bank staff

itself, a general unwillingness by the bank staff to open ‗no-frills‘ accounts

for persons of small means, the account opening forms were not simplified

and did not contain any information about the required documents under

simplified KYC norms and none of the branches the staff were in a

position to offer any guidance in case the prospective customer was not in

a position to produce required documents in proof of identity and address.

As a result, the weaker sections of India hesitate to take part in financial

inclusion and help to increase economic growth of the country.

A Study of Impact of Financial Inclusion on Rural Development Page 29

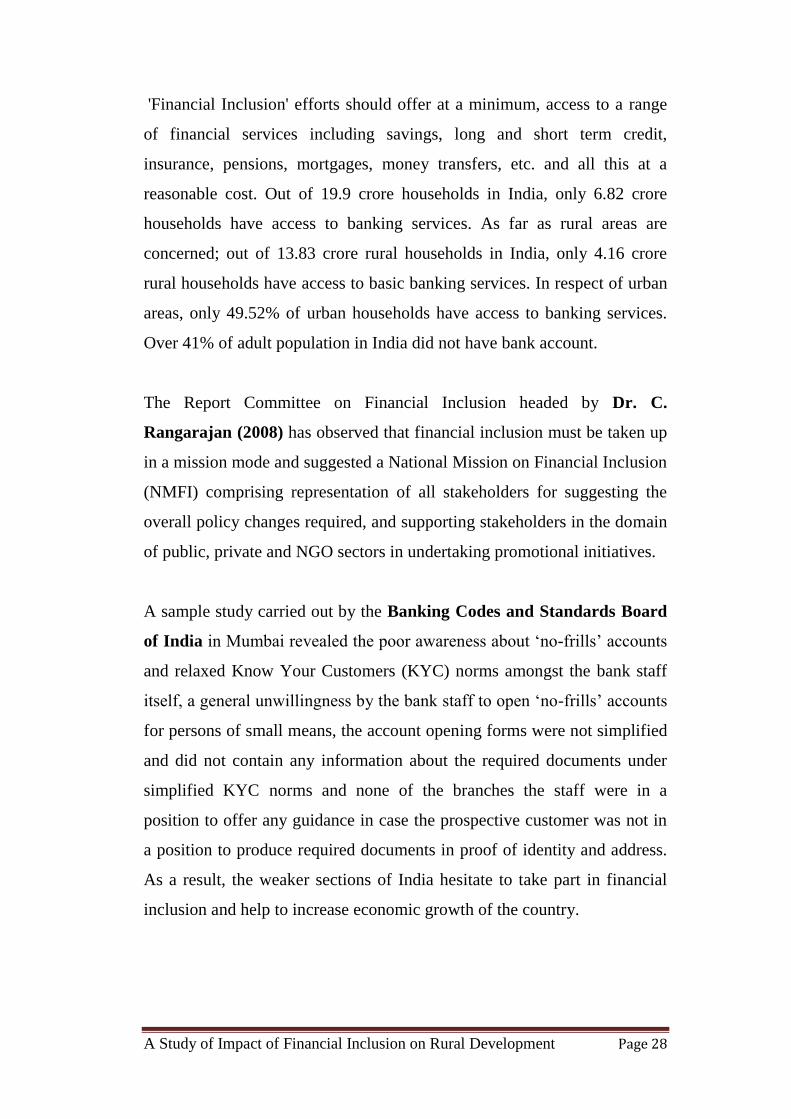

All India level: Chart.-1.2 shows that rural and Semi-urban offices

constitute a majority of the Commercial Bank offices in India. Rural bank

offices total have increased from 2011 to 2012. This is mainly because of

the inclusive focus of the policymakers mentioned above.

(Chart-1.2) Source: Reserve Bank of India

0

5000

10000

15000

20000

25000

30000

35000

40000

Rural Semi Urban Urban Metropolitan

POPULATION GROUP WISE DISTRIBUTION OF NUMBER OF OFFICES OF COMMERCIAL BANK - 2011 and 2012 As on

March 31

2011

2012

A Study of Impact of Financial Inclusion on Rural Development Page 30

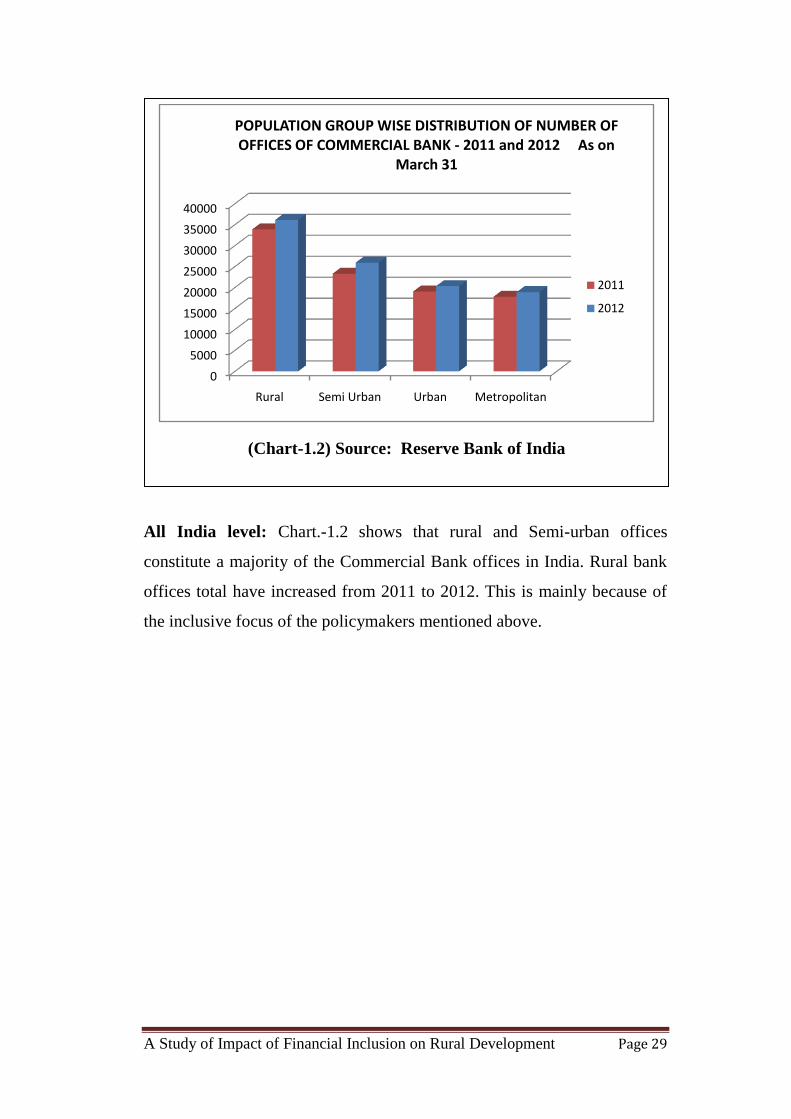

Population Group-Wise Distribution of Deposits and Credit of

Scheduled

Commercial Banks - 2008 to 2012

(Amount in ` Billion)

Popul

-ation

Grou

p

As on March 31

8-Mar 9-Mar 10-Mar 11-Mar 12-Mar

D C D C D C D C D C

-1 -2 -3 -4 -5 -6 -7 -8 -9 -10

Rural 3030.3 1831 3654.9 2087 4235.02 2498 4968.6 2941 5782.11 4182

-9.4 -7.6 -9.3 -7.3 -9.2 -7.5 -9.2 -7.2 -9.4 -8.7

Semi-

Urban 4293.8 2306 5319.4 2667 6182.07 3204 7212 3831 8484.46 4569

-13.3 -9.6 -13.5 -9.6 -13.4 -9.6 -13.3 -9.4 -13.7 -9.5

Urban 6576.2 3836 8244.6 4619 9511.16 5593 11164 6850 12809 7809

-20.4 -16 -20.9 -16.2 -20.7

-

16.7 -20.6

-

16.8 -20.7 -16.2

Metro

polita

n 18388 15973 22154 19202 26091

2216

1 30921

2714

7 34665.9 31654

-56.9 -66.7 -56.3 -67.2 -56.7

-

66.2 -57

-

66.6 -56.1 -65.7

All

India 32288 23946 39373 28575 46019.3

3345

6 54265

4076

9 61741.5 48215

-100 -100 -100 -100 -100 -100 -100 -100 -100 -100

Note: Figures in bracket indicate percent share in All-India total.

(Table 1.1) Source: Quarterly Statistics on Deposits and Credit of

Scheduled Commercial Banks, RBI

Table 1.1, provides further clarity providing a break-up of the deposit

accounts. Both the deposit and credit accounts are lower in rural

households than urban households. Hence despite the rural-push, the rural

population has not come forward and avail even basic banking services.

A Study of Impact of Financial Inclusion on Rural Development Page 31

Key Statistics on Financial Inclusion in India: A Survey

(Per cent)

Share with an

account at a

formal

financial

institution

Adults saving

in the past

year

Adults

originating a

new loan in

the past year

Adults

with a

credit

card

Adults

with

an

outsta

nding

mortg

age

Adults

paying

personall

y for

health

insurance

Al

l

ad

ul

ts

Poor

est

inco

me

quint

ile

W

o

m

en

Usi

ng a

for

mal

a/c

Using

a

comm

unity-

based

metho

d

Fro

m a

form

al

finan

cial

instit

ution

From

famil

y or

friend

s

1 2 3 4 5 6 7 8 9 10 11

India 35 21 26 12 3 8 20 2 2 7

World 50 38 47 22 5 9 23 15 7 17

(Table-1.2) Source: Asli Demirguc - Kunt and Klapper, L. (2012):

„Measuring Financial Inclusion‟, Policy Research Working Paper, 6025,

World Bank, April.

A financial inclusion survey was conducted by World Bank team in India

between April-June, 2011 which included face to face interviews of 3,518

respondents. The sample excluded the North-Eastern states and remote

islands representing approximately 10 per cent of the total adult

population. The results of the survey suggest that India lags behind

developing countries in opening bank accounts, but is much closer to the

global average when it comes to borrowing from formal institutions. In

India, 35 per cent of people had formal accounts versus the global average

of 50 per cent and the average of 41 per cent in developing economies. The

survey also points to the ‗slow growth of mobile money in India, where

only 4 per cent of adults in the Global Index sample report having used a

mobile phone in the past 12 months to pay bills or send or receive money‘.

The RBI recently came up with a State-wise Index of Financial Inclusion.

RBI considered three basic dimensions of an inclusive financial system --

A Study of Impact of Financial Inclusion on Rural Development Page 32

banking penetration, availability of the banking services and usage of the

banking system. In the group of 23 states for which a 3-dimensional IFI

(Index of Financial Inclusion) has been estimated by using data on three

dimensions of financial inclusion, Kerala led with the highest value of IFI

followed by Maharashtra and Karnataka. Gujarat lagged behind at 11th

place. In an Index of Financial Inclusion, India has been ranked 50 out of

100 countries. At present, only 34% of the India‘s population has access to

basic banking services. The latest National Sample Survey Organisation

survey reports that there are over 80 million poor people living in the cities

and towns of India and they lack access to the most basic banking services

(Refer table 1.2).

1.5 Financial Inclusion in India – Policy Perspective:

Financial Inclusion has become a buzzword now but in India it has been

practiced for quite some time. RBI has made endeavor to make commercial

banks to open branches in rural areas. Priority sector lending was instituted

to provide loans to small and medium enterprises and agricultural sector.

Further, special banks were set up for rural areas like Rural Cooperative

Banks, Regional Rural Banks. The government also set up national level

institutions like NABARD, SIDBI to empower credit to rural areas and

small and medium enterprises.

Despite the rural policy-push, above statistics suggest majority of the

population continues to be financially excluded. The efforts were further

intensified by RBI and its Annual Policy (2005-06) mentioned:

RBI will implement policies to encourage banks which provide

extensive services while dis-incentivising those which are not

responsive to the banking needs of the community, including the

underprivileged.

A Study of Impact of Financial Inclusion on Rural Development Page 33

The nature, scope and cost of services will be monitored to assess

whether there is any denial, implicit or explicit, of basic banking

services to the common person.

Banks are urged to review their existing practices to align them with

the objective of financial inclusion.

Thus RBI focus led to a few key developments:

No-Frill Accounts: In November 2005, RBI asked banks to offer

no-frills savings account which enables excluded people to open a

savings account. Normally, the savings account requires people to

maintain a minimum balance and most banks now even offer

various facilities with the same. No-frills account requires no (or

negligible) balance and is without any other facilities leading to

lower costs both for the bank and the individual. The number of no-

frills account increased mainly in public sector banks from about 0.4

million to 6 million between March 2006 and March 2007. The

number of No-frill accounts in private sector banks also increased

from 0.2 million to 1 million in the same period. No significant

increases were there in foreign banks. This is understandably so as

majority of rural and sub-urban bank offices are in public sector

banks.

Usage of Regional Language: The Banks were required to provide

all the material related to opening accounts, disclosures etc. in the

regional languages.

Simple KYC Norms: In order to ensure that persons belonging to

low income group both in urban and rural areas do not face

difficulty in opening the bank accounts due to the procedural

hassles, the Know Your Customer procedure for opening accounts

has been simplified for those persons who intend to keep balances

A Study of Impact of Financial Inclusion on Rural Development Page 34

not exceeding rupees fifty thousand (Rs. 50,000/-) in all their

accounts taken together and the total credit in all the accounts taken

together is not expected to exceed rupees one lakh (Rs.1, 00,000/-)

in a year.

Easier Credit Facilities: Banks have been asked to consider

introducing General Purpose Credit Card (GCC) facility up to Rs.

25,000/- at their rural and semi urban branches. GCC is in the nature

of revolving credit entitling the holder to withdraw up to the limit

sanctioned. The limit for the purpose can be set based on assessment

of household cash flows; the limits are sanctioned without insistence

on security or purpose. The interest rate on the facility is completely

deregulated. A simplified mechanism for one-time settlement of

overdue loans up to Rs.25,000/- has been suggested for adoption.

Banks have been specifically advised that borrowers with loans

settled under the one time settlement scheme will be eligible to re-

access the formal financial system for fresh credit.

Other Rural Intermediaries: Banks were permitted in January

2006, to use other rural organizations like Nongovernmental

organizations, self-help groups, micro-finance institutions etc for

furthering the cause of financial inclusion.

Using Information Technology: A few Pilot projects have been

initiated to test how technology can be used to increase financial

inclusion. Usha Thorat in her speech (June 19, 2007) pointed to a

few measures: Smart cards for opening bank accounts with

biometric identification. Link to mobile or hand held connectivity

devices ensure that the transactions are recorded in the bank's books

on real time basis. Some State Governments are routing social

security payments as also payments under the National Rural

A Study of Impact of Financial Inclusion on Rural Development Page 35

Employment Guarantee Scheme through such smart cards. The

same delivery channel can be used to provide other financial

services like low cost remittances and insurance. The use of IT also

enables banks to handle the enormous increase in the volume of

transactions for millions of households for processing, credit

scoring, credit record and follow up.

Financial Education: RBI has taken number of measures to

increase financial literacy in the country. It has set up a multilingual

website in 13 languages explaining about banking, money etc. It has

started putting up comic strips to explain various difficult subjects

like importance of saving, RBI's functions and so on. These comics

explain myriad and complex concepts in an entertaining manner.

1.6 Committee on Financial Inclusion (CFI):

Government of India constituted a Committee to enhance financial

inclusion in India on 22 June 2006. The Committee presented its report in

January 2008. The report has analyzed financial inclusion in detail and

confirms the statistics presented below in (Table-1.3)

Financial Inclusion Statistics in India

(a) General :

51.4% of farmer households are financially excluded from both

formal/ informal sources.

Of the total farmer households, only 27% access formal sources of

credit; one third of this group also borrows from non-formal

sources.

Overall, 73% of farmer households have no access to formal

sources of credit.

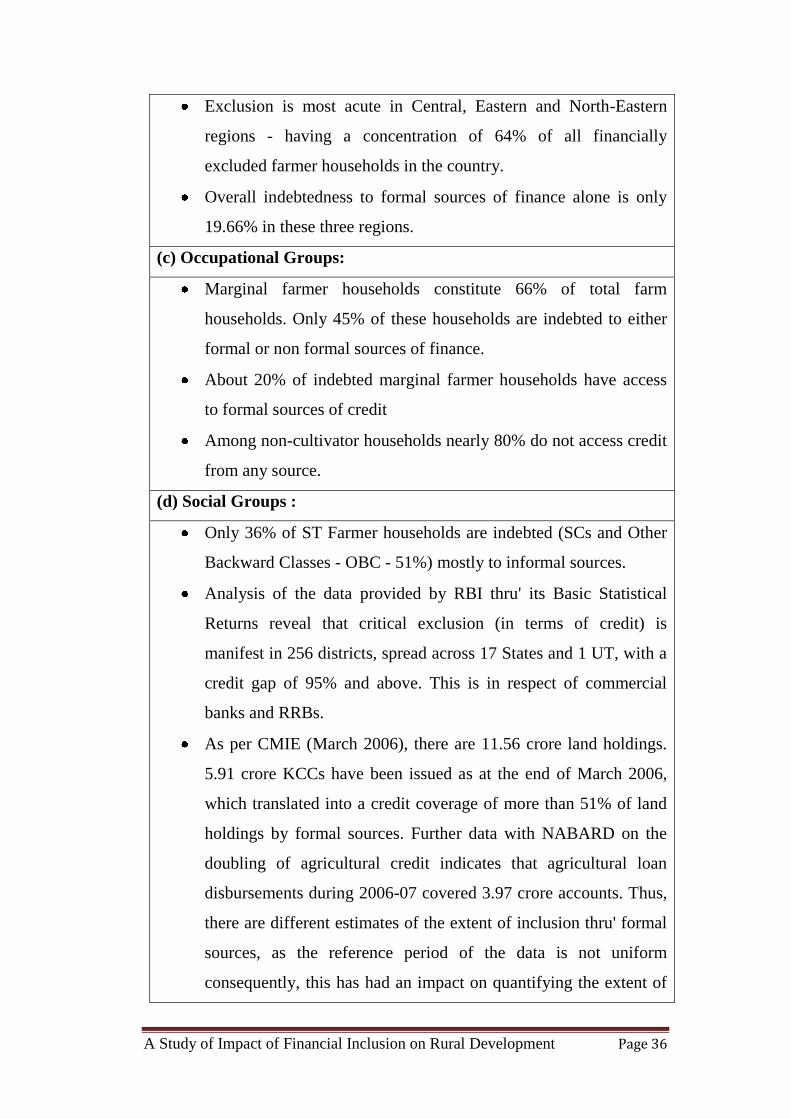

(b) Region-wise :

A Study of Impact of Financial Inclusion on Rural Development Page 36

Exclusion is most acute in Central, Eastern and North-Eastern

regions - having a concentration of 64% of all financially

excluded farmer households in the country.

Overall indebtedness to formal sources of finance alone is only

19.66% in these three regions.

(c) Occupational Groups:

Marginal farmer households constitute 66% of total farm

households. Only 45% of these households are indebted to either

formal or non formal sources of finance.

About 20% of indebted marginal farmer households have access

to formal sources of credit

Among non-cultivator households nearly 80% do not access credit

from any source.

(d) Social Groups :

Only 36% of ST Farmer households are indebted (SCs and Other

Backward Classes - OBC - 51%) mostly to informal sources.

Analysis of the data provided by RBI thru' its Basic Statistical

Returns reveal that critical exclusion (in terms of credit) is

manifest in 256 districts, spread across 17 States and 1 UT, with a

credit gap of 95% and above. This is in respect of commercial

banks and RRBs.

As per CMIE (March 2006), there are 11.56 crore land holdings.

5.91 crore KCCs have been issued as at the end of March 2006,

which translated into a credit coverage of more than 51% of land

holdings by formal sources. Further data with NABARD on the

doubling of agricultural credit indicates that agricultural loan

disbursements during 2006-07 covered 3.97 crore accounts. Thus,

there are different estimates of the extent of inclusion thru' formal

sources, as the reference period of the data is not uniform

consequently, this has had an impact on quantifying the extent of

A Study of Impact of Financial Inclusion on Rural Development Page 37

levels of exclusion.

(Table-1.3) Source: Committee on Financial Inclusion, IDBI Gilts Ltd

CFI has initiated a mission called National Rural Financial Inclusion plan.

It has set targets to increase FI in the country across regions and across

institutions (banks, rural regional banks etc.). It has suggested measures to

address both, supply and demand constraints in increasing financial

inclusion. The measures to address supply constraints aim to provide

finance (via banks, micro-finance etc). Demand constraints imply that

despite the supply people do not come forward because of number of

factors.

The report says:

It is widely recognized in economic literature that there are at least

five different types of capitals - Physical (roads, buildings, plant and

machinery, infrastructure), Natural (land, water, forests, livestock,

and weather), Human (nutrition, health, education, skills, and

competencies), Social (kinship groups, associations, trust, norms,

institutions) and Financial. One of the causes as well as

consequences of poverty and backwardness is inadequate access to

all these forms of capital. Thus, to look at financial inclusion in an

isolated way is problematic.

The report also suggests measures to address demand constraints in

all the other forms of capital as well. To address human capital it

stresses on health and education; for natural capital - enhance access

to land which could provide collateral; for physical capital- improve

infrastructure; social capital- develop institutions like gram

panchayats etc. The interim report was presented before the Budget

(2007-08). The Finance Minister in the Budget decided to

implement, immediately, two recommendations. The first was to

A Study of Impact of Financial Inclusion on Rural Development Page 38

establish a Financial Inclusion Fund with NABARD for meeting the

cost of developmental and promotional interventions. The second

was to establish a Financial Inclusion Technology Fund to meet the

costs of technology adoption. The overall corpus for each fund was

Rs.500 crore, with initial funding to be contributed by the Central

Government, RBI and NABARD.

In the 2008-09-budget statement, the Finance Minister proposed two

more measures: one to add at least 250 rural household accounts

every year at each of their rural and semi-urban branches of

commercial banks (including regional rural banks) and two, to allow

individuals such as retired bank officers, ex-servicemen etc to be

appointed as business facilitator or business correspondent or credit

counselor. The Finance Minister also proposed to expand the reach

of NABARD, SIDBI and NHB.

1.7 Research Structure:

The research is structured in the following format for better

comprehensiveness of the study. Chapter one is to give a general

introduction and conceptual framework to the topic by defining terms and

explaining topics. Chapter two is a capture of literatures on the topic to

further validate the study. Chapter three is for rationale, objective and

hypothesis for the study. Chapter four is an outline of the methods and

analytical approach of the research. Chapter five is data analysis and

a description of the findings and discussion, and chapter six is for

summary, conclusions and recommendations. Finally, chapter seven is for

the implication of the study.