Embed Size (px)

Citation preview

Chapter 4Completing the

Accounting Cycle

高立翰

Study Objectives

1. Prepare a worksheet.

2. Explain the process of closing the books.

3. Describe the content and purpose of a post-closing trial balance.

4. State the required steps in the accounting cycle.

5. Explain the approaches to preparing correcting entries.

6. Identify the sections of a classified statement of financial position.

會計學(一) http://ppt.cc/mJFq 2

PREVIEW OF CHAPTER 4

會計學(一) http://ppt.cc/mJFq 3

Using A Worksheet (1/2)Worksheet (工作底稿)

A multiple-column form used in preparing financial statements.Not a permanent accounting record.May be a computerized worksheet using an electronic spreadsheet program such as Excel.Five step process.Use of worksheet is optional.

會計學(一) http://ppt.cc/mJFq 4

Using A Worksheet (2/2) Illustration: pp. 162-164

會計學(一) http://ppt.cc/mJFq 5

Illustration 4-1

Steps in Preparing a Worksheet (1/5)1. Prepare a Trial Balance on the Worksheet

會計學(一) http://ppt.cc/mJFq 6

Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.Cash 15,200 Advertising Supplies 2,500 Prepaid Insurance 600 Office Equipment 5,000 Notes Payable 5,000 Accounts Payable 2,500 Unearned Revenue 1,200 Share Capital 10,000 Dividends 500 Service Revenue 10,000

Salaries Expense 4,000 Rent 900

Totals 28,700 28,700

Financial PositionAdjusted Income

Trial Balance Adjustments Trial Balance StatementStatement of

Trial balance amounts come directly from ledger accounts.

Include all accounts with balances.

Steps in Preparing a WorksheetAdjusting

Journal Entries in Chapter 3

會計學(一) http://ppt.cc/mJFq 7

Illustration 3-23General journal showing adjusting entries

Steps in Preparing a Worksheet (2/5)2. Enter the Adjustments in the Adjustments Columns

會計學(一) http://ppt.cc/mJFq 8

Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.Cash 15,200 Advertising Supplies 2,500 1,500 Prepaid Insurance 600 50 Office Equipment 5,000 Notes Payable 5,000 Accounts Payable 2,500 Unearned Revenue 1,200 400 Share Capital 10,000 Dividends 500 Service Revenue 10,000 400

200 Salaries Expense 4,000 1,200 Rent 900

Totals 28,700 28,700 Advertising Supplies Expense 1,500 Insurance Expense 50 Accumulated Depreciation 40 Depreciation Expense 40 Accounts Receivable 200 Interest Expense 50 Interest Payable 50 Salaries Payable 1,200

Totals 3,440 3,440

Financial PositionAdjusted Income

Trial Balance Adjustments Trial Balance StatementStatement of

(a)(b)

(a)

(g)

(c)

(d)

(d)

(e)

(b)

(e)(f)

(f)(g)

(c)

Enter adjustment amounts, total adjustments columns,and check for equality.

Add additional accounts as needed.

Adjustments Key:(a) Supplies Used.(b) Insurance Expired.(c) Depreciation Expensed.(d) Service Revenue Earned.(e) Service Revenue Accrued.(f) Interest Accrued.(g) Salaries Accrued.

Steps in Preparing a Worksheet (3/5)3. Complete the Adjusted Trial Balance Columns

會計學(一) http://ppt.cc/mJFq 9

Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.Cash 15,200 15,200 Advertising Supplies 2,500 1,500 1,000 Prepaid Insurance 600 50 550 Office Equipment 5,000 5,000 Notes Payable 5,000 5,000 Accounts Payable 2,500 2,500 Unearned Revenue 1,200 400 800 Share Capital 10,000 10,000 Dividends 500 500 Service Revenue 10,000 400 10,600

200 Salaries Expense 4,000 1,200 5,200 Rent 900 900

Totals 28,700 28,700 Advertising Supplies Expense 1,500 1,500 Insurance Expense 50 50 Accumulated Depreciation 40 40 Depreciation Expense 40 40 Accounts Receivable 200 200 Interest Expense 50 50 Interest Payable 50 50 Salaries Payable 1,200 1,200

Totals 3,440 3,440 30,190 30,190

Financial PositionAdjusted Income

Trial Balance Adjustments Trial Balance StatementStatement of

(a)(b)

(a)

(g)

(c)

(d)

(d)

(e)

(b)

(e)(f)

(f)(g)

(c)

Total the adjusted trial balance columns and check for equality.

Steps in Preparing a Worksheet (4/5)4. Extend Amounts to Financial Statement Columns

會計學(一) http://ppt.cc/mJFq 10

Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.Cash 15,200 15,200 Advertising Supplies 2,500 1,500 1,000 Prepaid Insurance 600 50 550 Office Equipment 5,000 5,000 Notes Payable 5,000 5,000 Accounts Payable 2,500 2,500 Unearned Revenue 1,200 400 800 Share Capital 10,000 10,000 Dividends 500 500 Service Revenue 10,000 400 10,600 10,600

200 Salaries Expense 4,000 1,200 5,200 5,200 Rent 900 900 900

Totals 28,700 28,700 Advertising Supplies Expense 1,500 1,500 1,500 Insurance Expense 50 50 50 Accumulated Depreciation 40 40 Depreciation Expense 40 40 40 Accounts Receivable 200 200 Interest Expense 50 50 50 Interest Payable 50 50 Salaries Payable 1,200 1,200

Totals 3,440 3,440 30,190 30,190 7,740 10,600

Statement of Adjusted IncomeTrial Balance Adjustments Trial Balance Statement Financial Position

(a)(b)

(a)

(g)

(c)

(d)

(d)

(e)

(b)

(e)(f)

(f)(g)

(c)

Extend all revenue and expense account balances to the income statement columns.

Steps in Preparing a Worksheet (5/5)5. Total Columns, Compute Net Income (Loss)

11

Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.Cash 15,200 15,200 15,200 Advertising Supplies 2,500 1,500 1,000 1,000 Prepaid Insurance 600 50 550 550 Office Equipment 5,000 5,000 5,000 Notes Payable 5,000 5,000 5,000 Accounts Payable 2,500 2,500 2,500 Unearned Revenue 1,200 400 800 800 Share Capital 10,000 10,000 10,000 Dividends 500 500 500 Service Revenue 10,000 400 10,600 10,600

200 Salaries Expense 4,000 1,200 5,200 5,200 Rent 900 900 900

Totals 28,700 28,700 Advertising Supplies Expense 1,500 1,500 1,500 Insurance Expense 50 50 50 Accumulated Depreciation 40 40 40 Depreciation Expense 40 40 40 Accounts Receivable 200 200 200 Interest Expense 50 50 50 Interest Payable 50 50 50 Salaries Payable 1,200 1,200 1,200

Totals 3,440 3,440 30,190 30,190 7,740 10,600 22,450 19,590 Net income 2,860 2,860

Totals 10,600 10,600 22,450 22,450

Financial Position Adjusted Income

Trial Balance Adjustments Trial Balance Statement Statement of

(a)(b)

(a)

(g)

(c)

(d)

(d)

(e)

(b)

(e)(f)

(f)(g)

(c)

Compute Net Income or Net Loss.

Q4‐1.

Preparing Financial Statements from a Worksheet

Income Statement is prepared from the income statement columns.

Statement of Financial Position and Retained Earnings Statement are prepared from the Statement of Financial Position columns.

Companies can prepare financial statements before they journalize and post adjusting entries.

會計學(一) http://ppt.cc/mJFq 12

Income Statement from a Worksheet

會計學(一) http://ppt.cc/mJFq 13

Illustration 4-3

Retained Earnings Statement from a Worksheet

會計學(一) http://ppt.cc/mJFq 14

Illustration 4-3

Statement of Financial Position from a Worksheet

會計學(一) http://ppt.cc/mJFq 15

Illustration 4-3

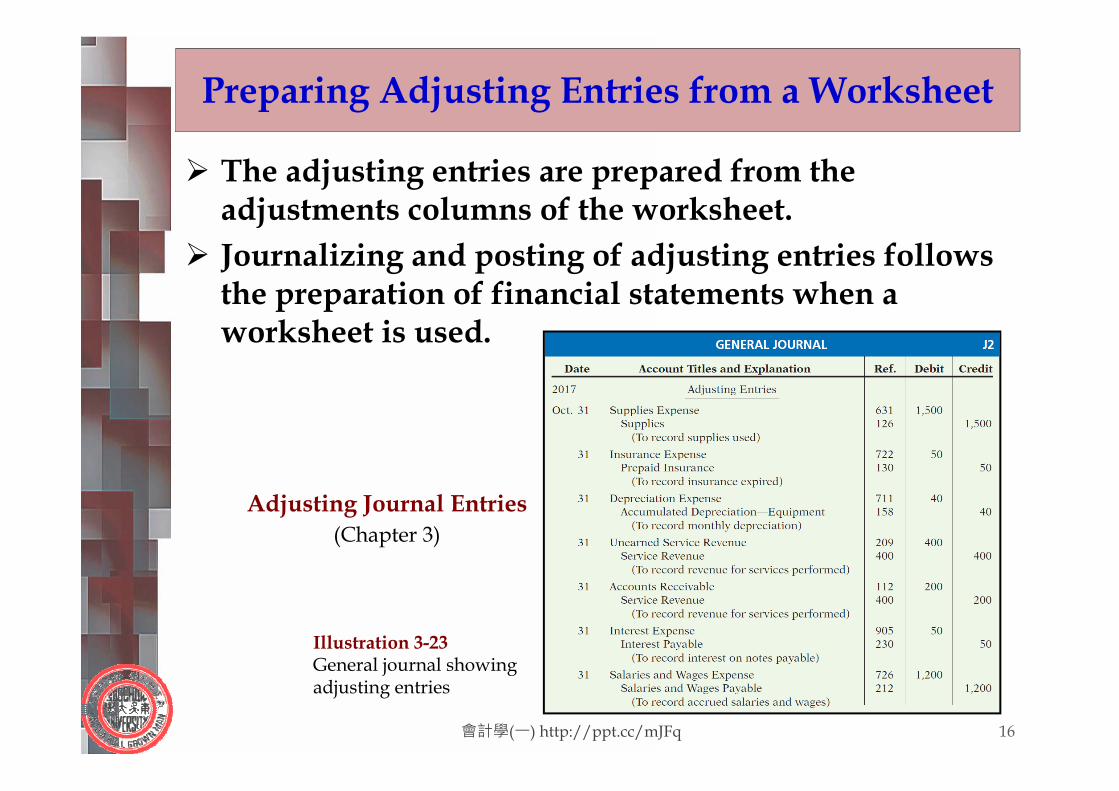

Preparing Adjusting Entries from a Worksheet

The adjusting entries are prepared from the adjustments columns of the worksheet.

Journalizing and posting of adjusting entries follows the preparation of financial statements when a worksheet is used.

會計學(一) http://ppt.cc/mJFq 16

Adjusting Journal Entries (Chapter 3)

Illustration 3-23General journal showing adjusting entries

Closing the Books (1/4) At the end of the accounting period, the company

makes the accounts ready for the next period.

Temporary (暫時性) and Permanent (永久性) accounts

會計學(一) http://ppt.cc/mJFq 17

Closing the Books (2/4)Closing Entries (結帳分錄) formally recognize,

in the general ledger, the transfer of Net Income (or Net Loss), andDividends

to Retained Earnings.

Closing entries are only journalized and posted at the end of the annual accounting period.

Closing entries produce a zero balance in each temporary account.

會計學(一) http://ppt.cc/mJFq 18Q4‐2.

會計學(一) http://ppt.cc/mJFq 19

Dividends are closed directly to Retained Earnings and notto Income Summary because Dividends are not an expense.

Note:

Closing the Books (3/4)Closing entries need to be posted

會計學(一) http://ppt.cc/mJFq 20

Illustration 4-6Closing entries journalized

Closing the Books (4/4)Posting closing entries

會計學(一) http://ppt.cc/mJFq 21

Illustration 4-7Posting of closing entries

Preparing a Post-Closing Trial Balance

“Post-Closing Trial Balance” (結帳後試算表)Lists permanent accounts and their balances after the journalizing and posting of closing entries.

To prove the equality of the permanent account balances after journalizing and posting of closing entries.

Only contains balances for permanent—statement of financial position—accounts.

All temporary accounts will have zero balances.

會計學(一) http://ppt.cc/mJFq 22Q4‐3.

會計學(一) http://ppt.cc/mJFq 23

Illustration 4-8Post-closing trial balance

Summary of the Accounting Cycle

會計學(一) http://ppt.cc/mJFq 24

1. Analyze business transactions

2. Journalize the transactions

6. Prepare an adjusted trial balance

7. Prepare financial statements

8. Journalize and post closing entries

9. Prepare a post-closing trial balance

4. Prepare a trial balance

3. Post to ledger accounts

5. Journalize and post adjusting entries

Illustration 4-11

Q4‐4.

Correcting Entries – An Avoidable Step

Correcting Entries (更正分錄)are unnecessary if the records are error-freeare made whenever an error is discoveredmust be posted before closing entries

Instead of preparing a correcting entry, it is possible to reverse the incorrect entry and then prepare the correct entry

會計學(一) http://ppt.cc/mJFq 25

Closing Entries – Illustration (1/2) Case 1

On May 10, Bai Co. journalized and posted a NT$500 cash collection on account from a customer as a debit to Cash NT$500 and a credit to Service Revenue NT$500. The company discovered the error on May 20, when the customer paid the remaining balance in full.

會計學(一) http://ppt.cc/mJFq 26

Cash 500Incorrect entry Service Revenue 500

Cash 500Correct entry Accounts Receivable 500

Service Revenue 500Correcting entry Accounts Receivable 500

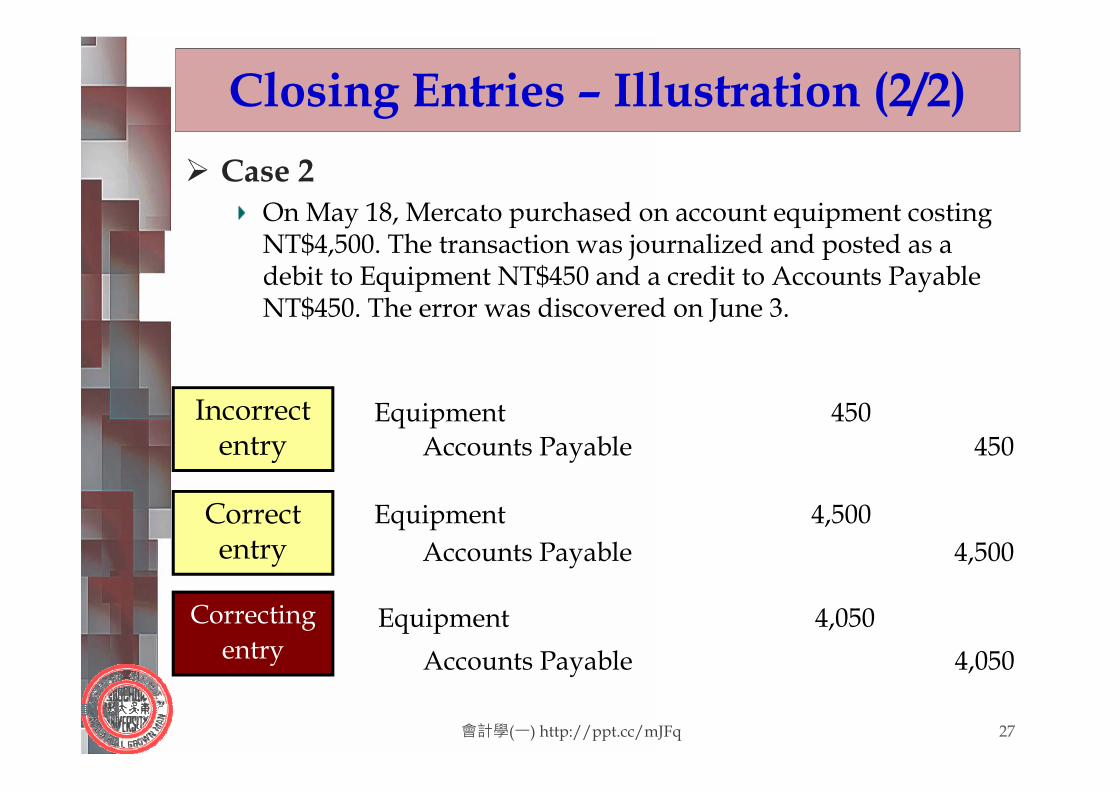

Closing Entries – Illustration (2/2) Case 2

On May 18, Mercato purchased on account equipment costing NT$4,500. The transaction was journalized and posted as a debit to Equipment NT$450 and a credit to Accounts Payable NT$450. The error was discovered on June 3.

會計學(一) http://ppt.cc/mJFq 27

Equipment 450Incorrect entry Accounts Payable 450

Equipment 4,500Accounts Payable 4,500

Equipment 4,050Correcting entry Accounts Payable 4,050

Correct entry

The Classified Statement of Financial Position

Presents a snapshot at a point in timeTo improve understanding, companies group

similar assets and similar liabilities togetherAssets accounts are listed by the reverse order

of their liquidity

會計學(一) http://ppt.cc/mJFq 28

Assets Equity and LiabilitiesIntangible assets EquityProperty, plant, and equipment Non-current liabilities Long-term investments Current liabilitiesCurrent assets

Illustration 4-16Standard Classifications

Q4‐5.

Classified statement of financial position

會計學(一) http://ppt.cc/mJFq 29

Classified Statement of Financial Position (1/7)

Intangible Assets (無形資產)Assets that do not have physical substance.

– Goodwill (商譽)– Franchises (特許權)– Trademark (商標)

會計學(一) http://ppt.cc/mJFq 30

Illustration 4-18Intangible assets section

Classified Statement of Financial Position (2/7)

Property, Plant, and Equipment (固定資產,PP&E)Long useful livesCurrently used in operationsDepreciation

– allocating the cost of assets to a number of yearsAccumulated depreciation

– total amount of depreciation expensed thus far in the asset’s life

會計學(一) http://ppt.cc/mJFq 31

Classified Statement of Financial Position (3/7)

Long-term investments (長期投資)Investments in stocks and bonds of other companiesInvestments in long-term assets such as land or buildings that a company is not currently using in its operating activities

會計學(一) http://ppt.cc/mJFq 32

房地產投資關聯企業投資

Classified Statement of Financial Position (4/7)

Current Assets (流動資產)Assets that a company expects to convert to cash or use up within one year or the operating cycle, whichever is longerOperating cycle is the average time it takes from the purchase of inventory to the collection of cash from customers

會計學(一) http://ppt.cc/mJFq 33

流動性

低

高

Q4‐6.

Classified Statement of Financial Position (5/7)

Equity (權益)Proprietorship - one capital account (Owner’s Equity)Partnership - capital account for each partnerCorporation – Share Capital and Retained Earnings

會計學(一) http://ppt.cc/mJFq 34

Classified Statement of Financial Position (6/7)

Non-current Liabilities (非流動負債)Obligations a company expects to pay after one year.

會計學(一) http://ppt.cc/mJFq 35

Classified Statement of Financial Position (7/7)

Current Liabilities (流動負債)Obligations the company is to pay within the coming yearUsually list notes payable first, followed by accounts payable. Other items follow in order of magnitudeLiquidity (流動性)

– ability to pay obligations expected to be due within the next year

會計學(一) http://ppt.cc/mJFq 36

Appx. 4A: Reversing Entries (不考)Reversing Entries (迴轉分錄)

It is often helpful to reverse some of the adjusting entries before recording the regular transactions of the next periodCompanies make a reversing entry at the beginning of the next accounting periodEach reversing entry is the exact opposite of the adjusting entry made in the previous periodThe use of reversing entries does not change the amounts reported in the financial statements

會計學(一) http://ppt.cc/mJFq 37

Reversing Entries Example Illustration: To illustrate the optional use of

reversing entries for accrued expenses, we will use the salaries expense transactions for YaziciAdvertising A.S. 1. October 26 (initial salary entry): Pioneer pays ₺4,000 of

salaries and wages earned between October 15 and October 26.

2. October 31 (adjusting entry): Salaries and wages earned between October 29 and October 31 are ₺1,200. The company will pay these in the November 9 payroll.

3. November 9 (subsequent salary entry): Salaries and wages paid are ₺4,000. Of this amount, ₺1,200 applied to accrued salaries and wages payable and ₺2,800 was earned between November 1 and November 9.

會計學(一) http://ppt.cc/mJFq 38

會計學(一) http://ppt.cc/mJFq 39

Salaries and Wages Expense 4,000

Salaries and Wages Payable 1,200

Reversing Entry

With Reversing Entries (per appendix)

Initial Salary EntryOct. 26 Same entry

Adjusting Entry

Closing Entry

Salaries and Wages Expense 1,200

Subsequent Salary Entry

Oct. 31 Same entry

Oct. 31 Same entry

Nov. 1

Cash 4,000Nov. 9

會計學(一) http://ppt.cc/mJFq 40