Embed Size (px)

DESCRIPTION

Chapter Four. Cost Volume Profit Analysis. Cost Behavior. A cost is classified as either fixed or variable, according to whether the total amount of the cost changes as activity changes. - PowerPoint PPT Presentation

Citation preview

Chapter Four

Cost Volume Profit Analysis

Cost BehaviorA cost is classified as either fixed or variable, according to whether the total amount of the cost changes as activity changes.

Activity is a general term denoting anything that the company does; examples: units of product sold or produced, hours worked, invoices prepared, and parts inspected.

Volume is a common measure of activity.

Definitions

Variable costs change, in total, in direct proportion to changes in volume.

Fixed costs remain the same in total over a wide range of volume.

Total Costs = Fixed costs + Variable costs

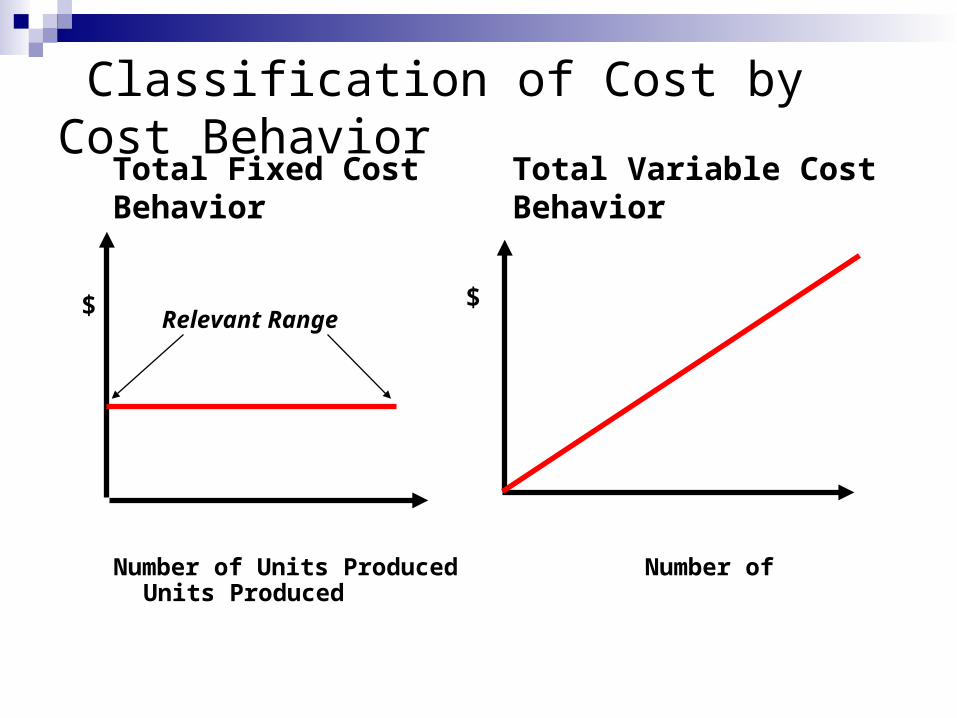

Classification of Cost by Cost BehaviorTotal Fixed Cost Behavior

Total Variable Cost Behavior

$$ Relevant Range

Number of Units Produced Number of Units Produced

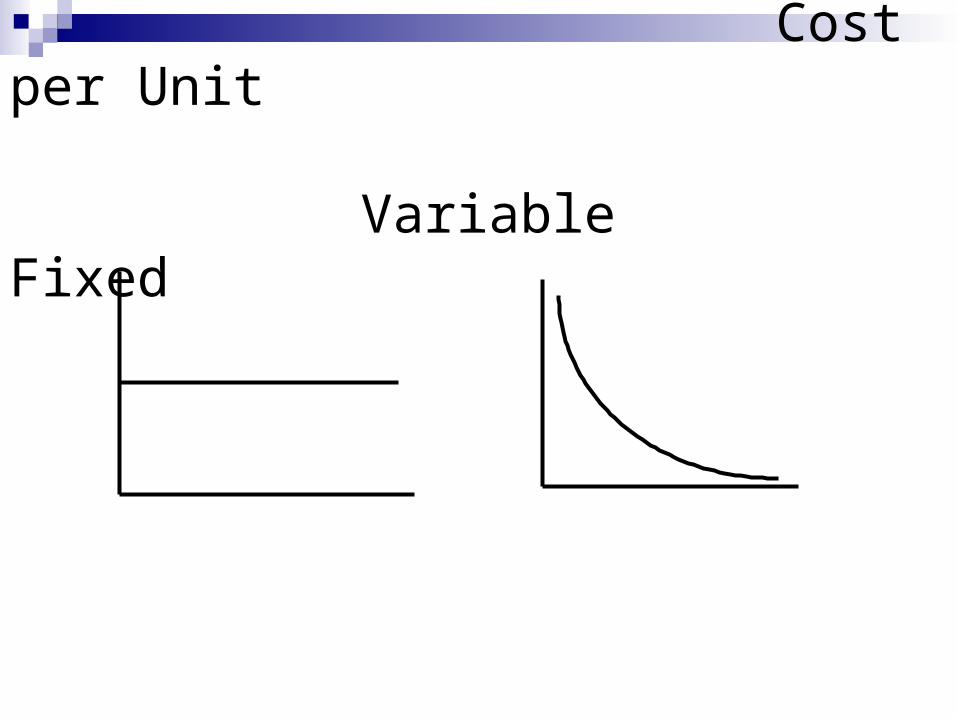

Cost per Unit

Variable Fixed

Mixed Cost A mixed cost is a cost that has a fixed and

a variable element Example would be utilities in a factory Can separate mixed costs into fixed and

variable by:RegressionScatter DiagramAccount analysisHigh-low method

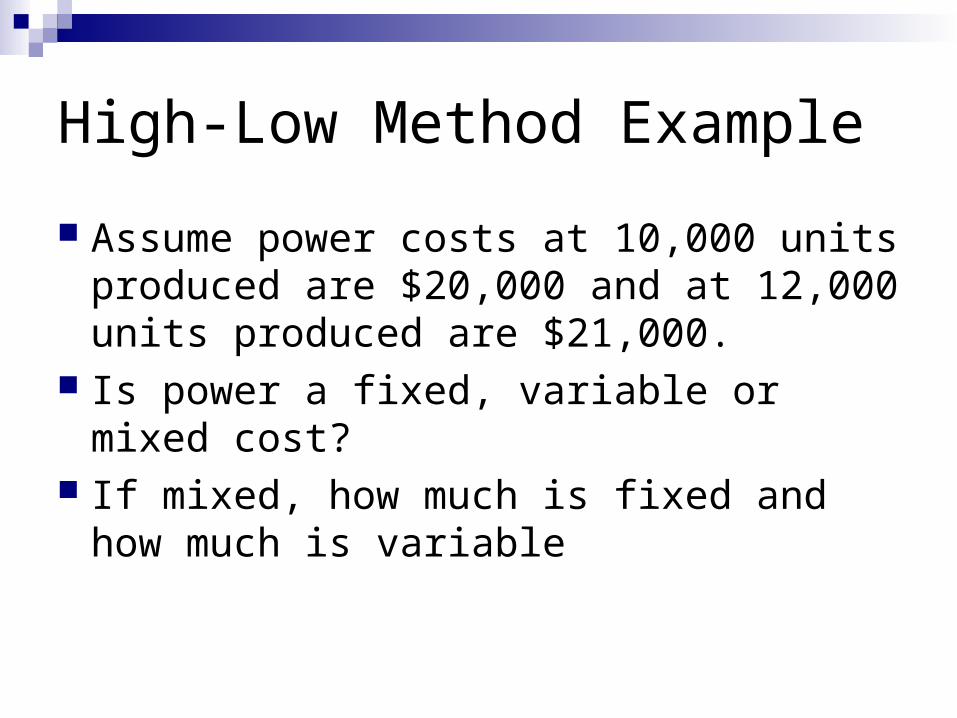

High-Low Method Example

Assume power costs at 10,000 units produced are $20,000 and at 12,000 units produced are $21,000.

Is power a fixed, variable or mixed cost? If mixed, how much is fixed and how much

is variable

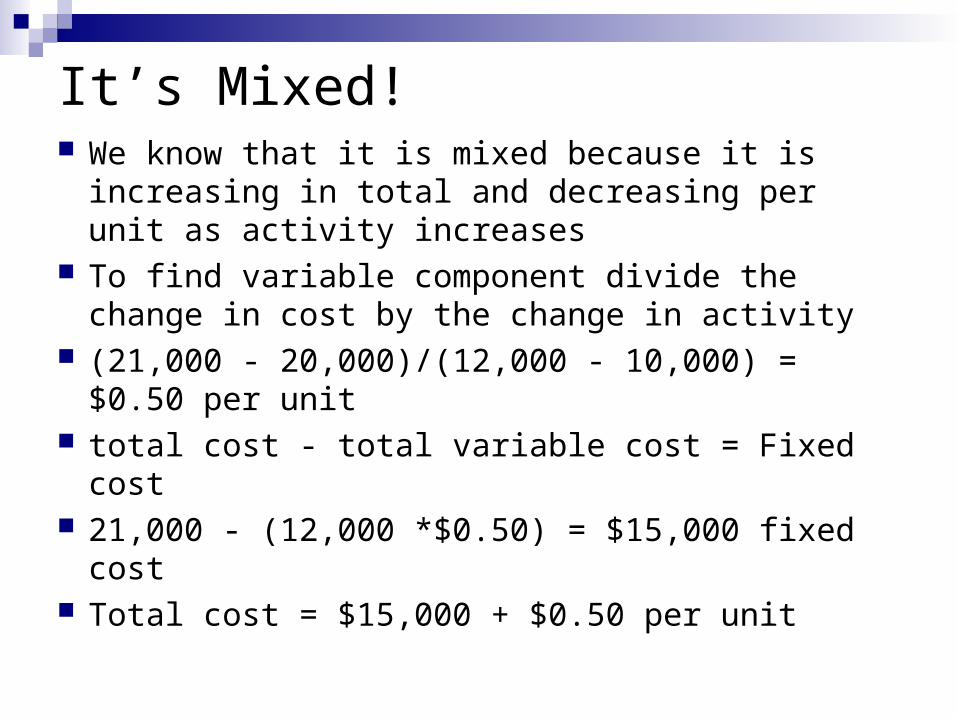

It’s Mixed! We know that it is mixed because it is increasing

in total and decreasing per unit as activity increases

To find variable component divide the change in cost by the change in activity

(21,000 - 20,000)/(12,000 - 10,000) = $0.50 per unit

total cost - total variable cost = Fixed cost 21,000 - (12,000 *$0.50) = $15,000 fixed cost Total cost = $15,000 + $0.50 per unit

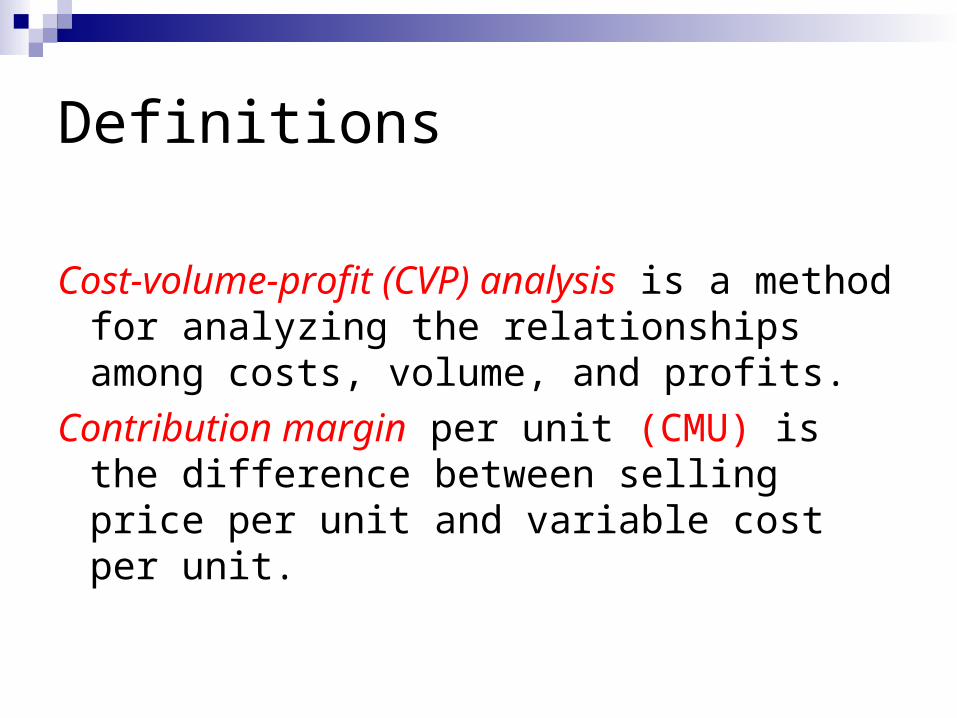

Definitions

Cost-volume-profit (CVP) analysis is a method for analyzing the relationships among costs, volume, and profits.

Contribution margin per unit (CMU) is the difference between selling price per unit and variable cost per unit.

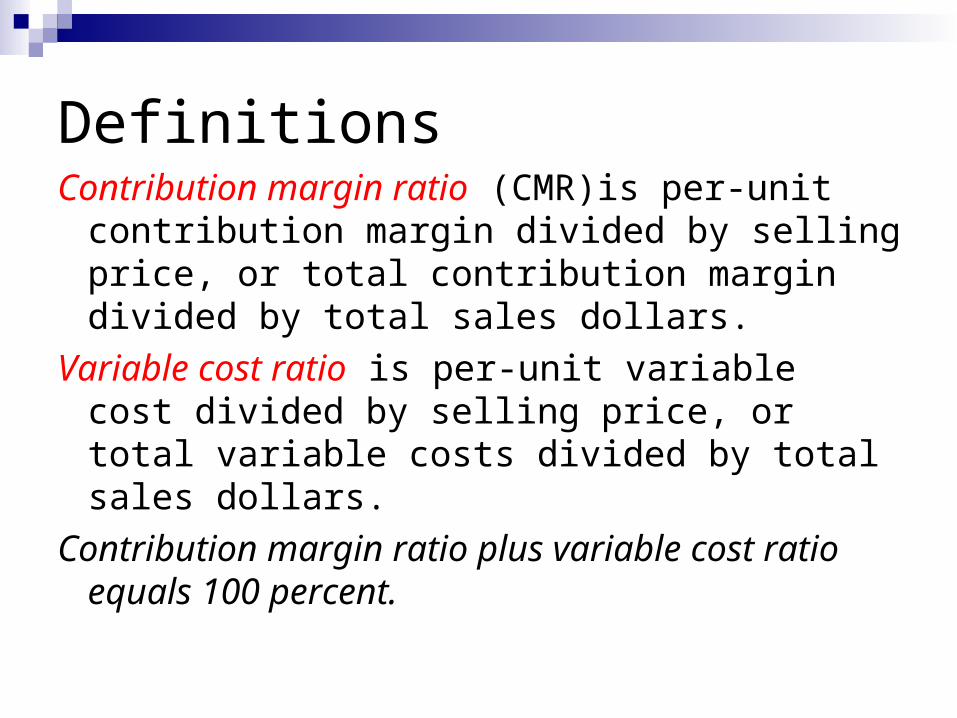

DefinitionsContribution margin ratio (CMR)is per-unit

contribution margin divided by selling price, or total contribution margin divided by total sales dollars.

Variable cost ratio is per-unit variable cost divided by selling price, or total variable costs divided by total sales dollars.

Contribution margin ratio plus variable cost ratio equals 100 percent.

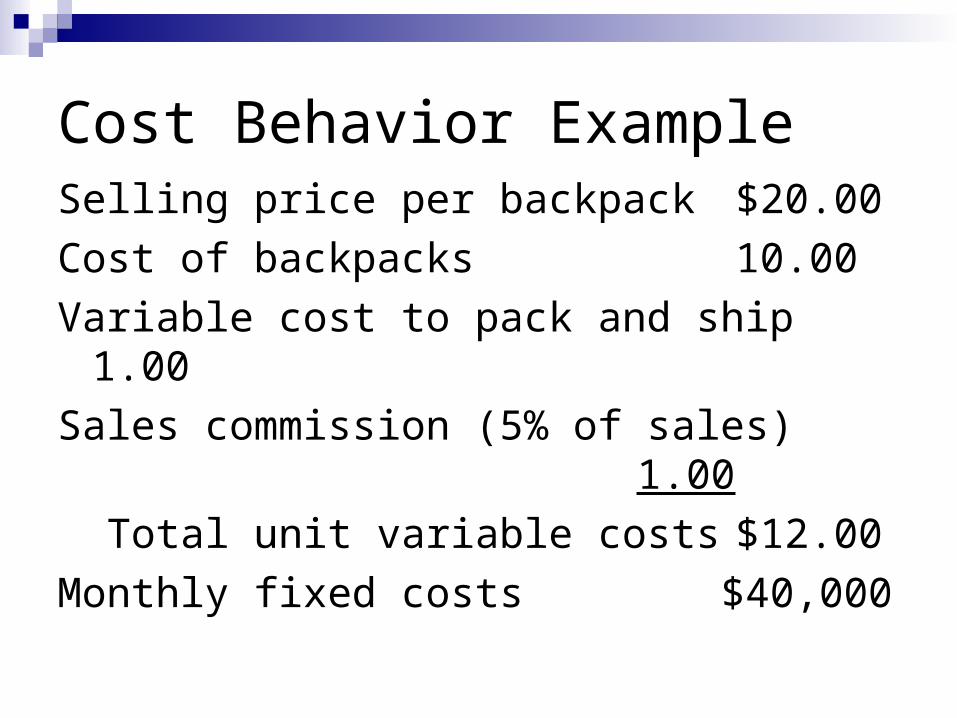

Cost Behavior ExampleSelling price per backpack $20.00

Cost of backpacks 10.00

Variable cost to pack and ship 1.00

Sales commission (5% of sales) 1.00

Total unit variable costs $12.00

Monthly fixed costs $40,000

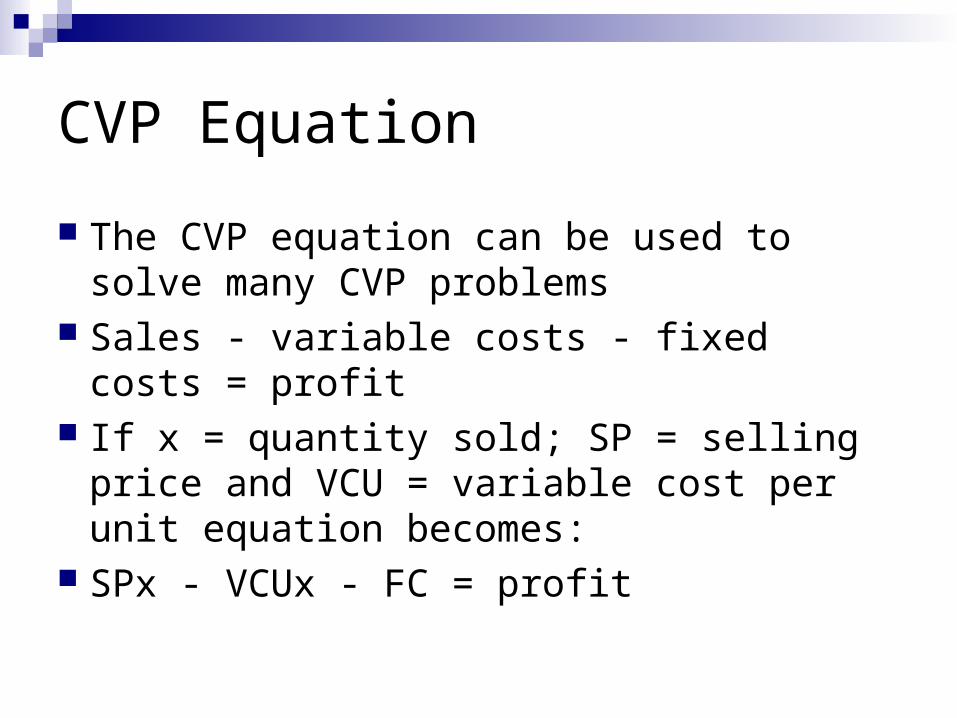

CVP Equation

The CVP equation can be used to solve many CVP problems

Sales - variable costs - fixed costs = profit If x = quantity sold; SP = selling price and

VCU = variable cost per unit equation becomes:

SPx - VCUx - FC = profit

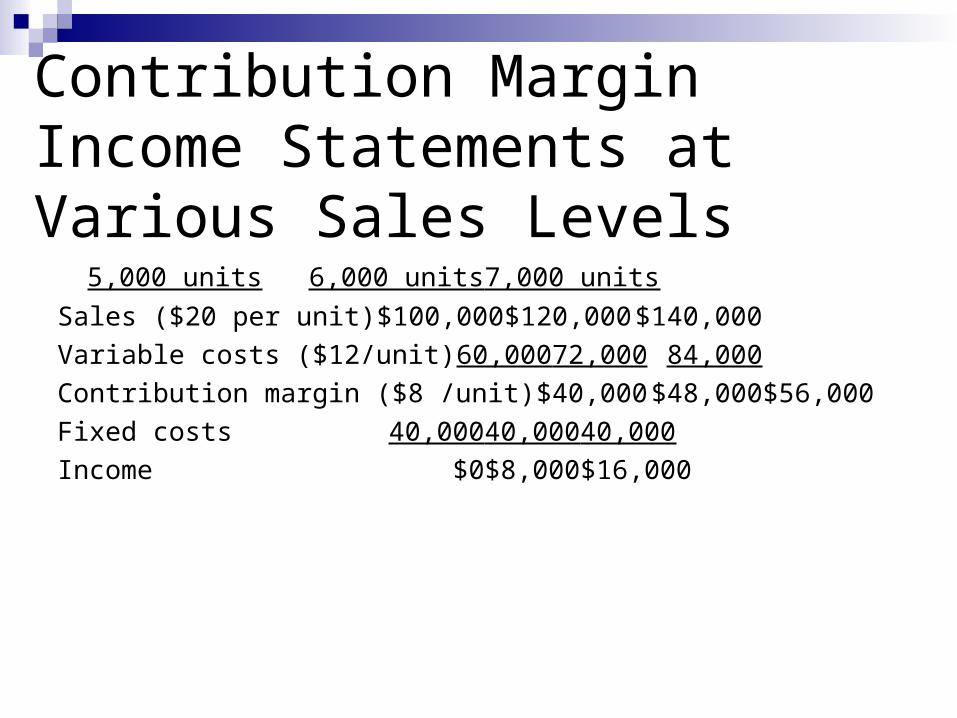

Contribution Margin Income Statements at Various Sales Levels

5,000 units 6,000 units 7,000 units

Sales ($20 per unit) $100,000 $120,000 $140,000

Variable costs ($12/unit) 60,000 72,000 84,000

Contribution margin ($8 /unit)$40,000 $48,000 $56,000

Fixed costs 40,000 40,000 40,000

Income $0 $8,000 $16,000

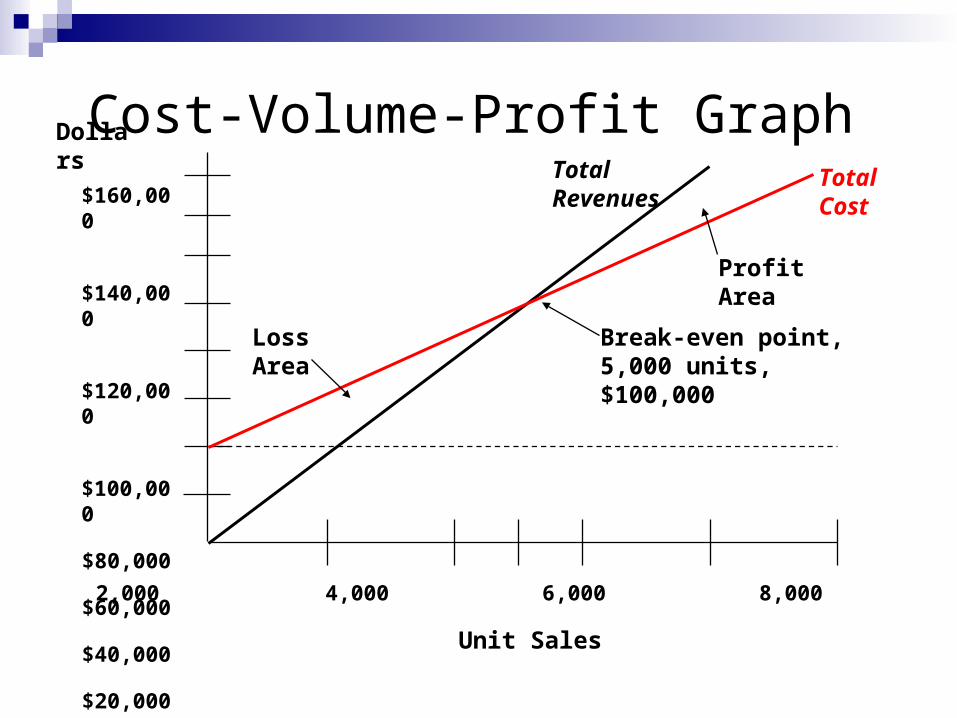

Cost-Volume-Profit Graph$160,000

$140,000

$120,000

$100,000

$80,000

$60,000

$40,000

$20,000

$0

2,000 4,000 6,000 8,000 10,000

Unit Sales

Dollars

Break-even point,5,000 units, $100,000

TotalCost

TotalRevenues

LossArea

Profit Area

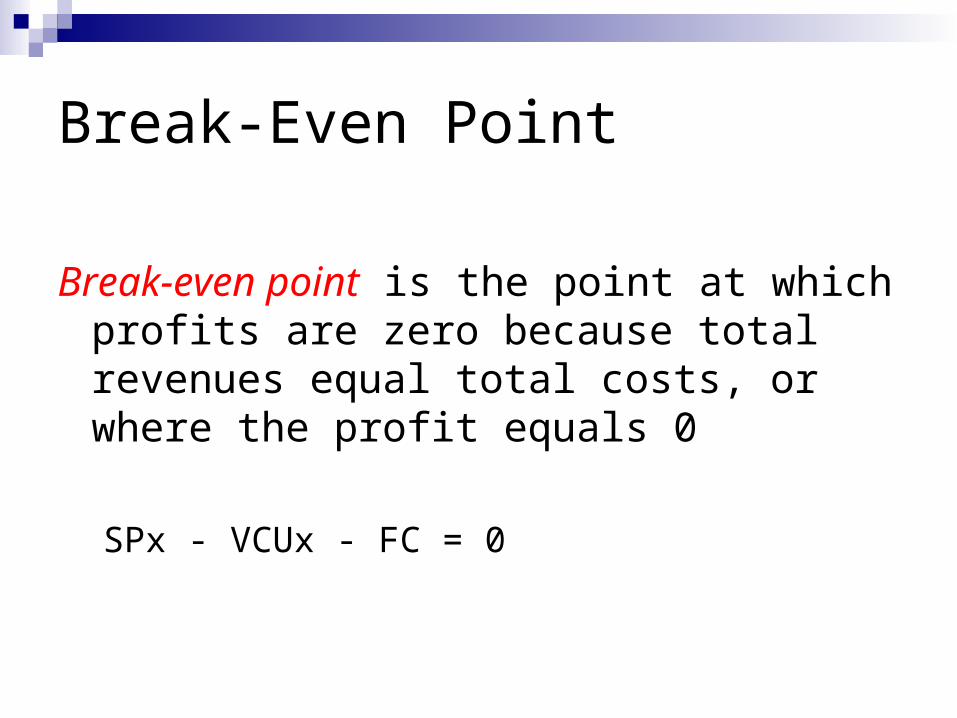

Break-Even Point

Break-even point is the point at which profits are zero because total revenues equal total costs, or where the profit equals 0

SPx - VCUx - FC = 0

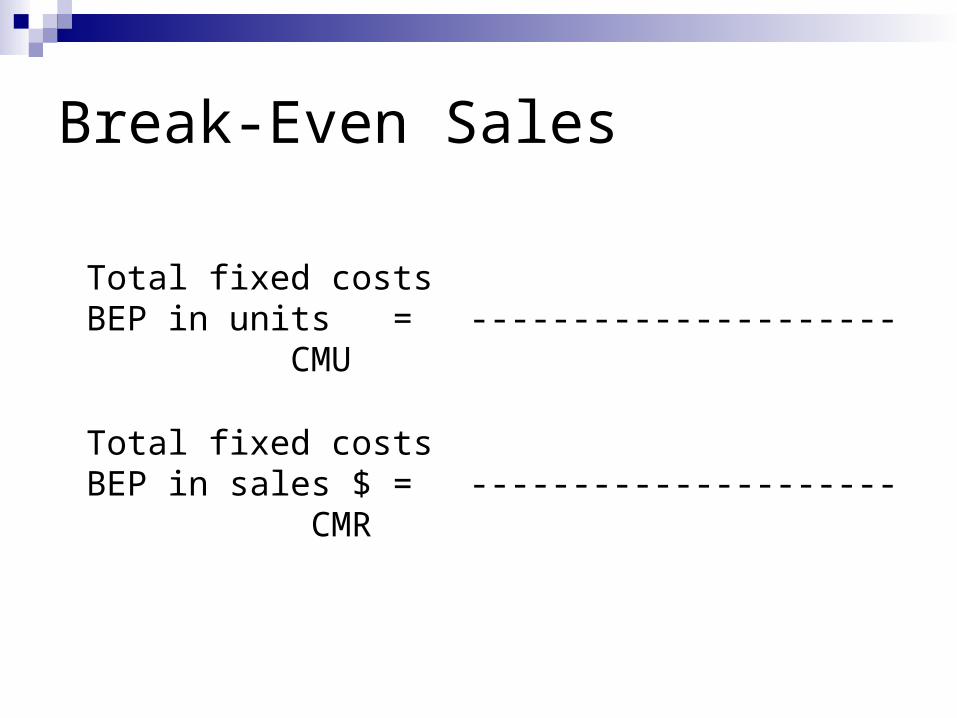

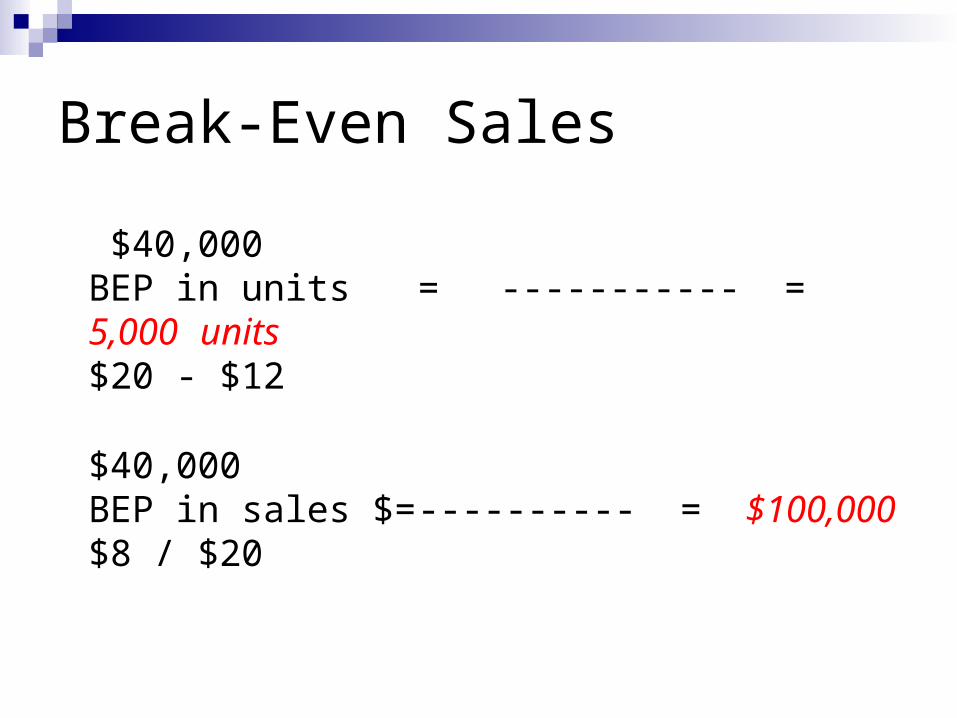

Break-Even Sales

Total fixed costsBEP in units = ---------------------

CMU

Total fixed costsBEP in sales $ = ---------------------

CMR

Break-Even Sales

$40,000BEP in units = ----------- = 5,000 units$20 - $12

$40,000BEP in sales $= ---------- = $100,000$8 / $20

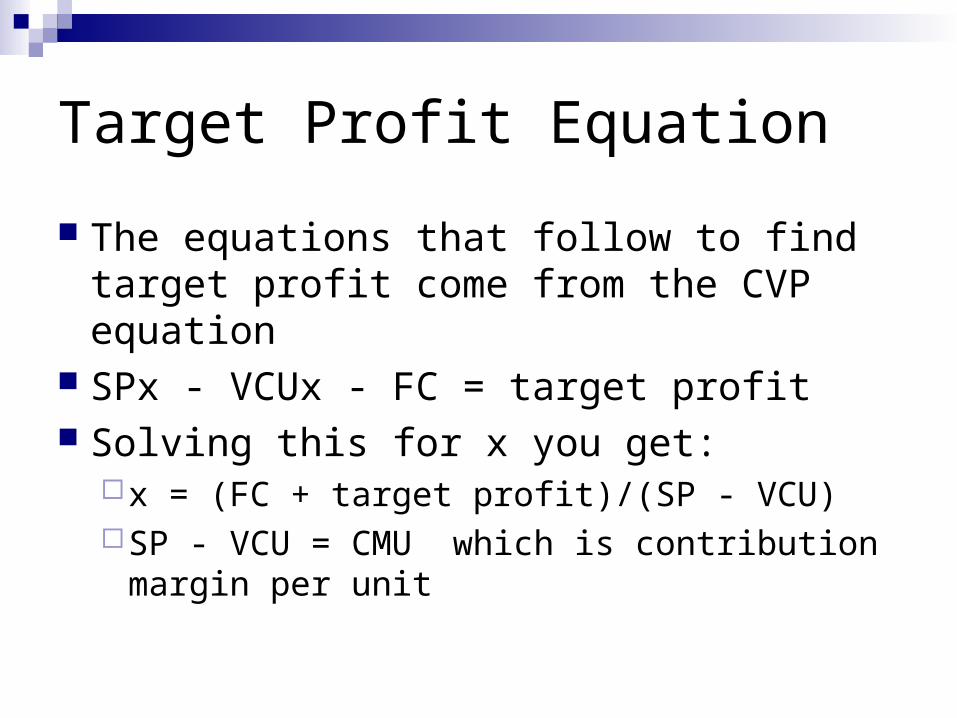

Target Profit Equation

The equations that follow to find target profit come from the CVP equation

SPx - VCUx - FC = target profit Solving this for x you get:

x = (FC + target profit)/(SP - VCU)SP - VCU = CMU which is contribution

margin per unit

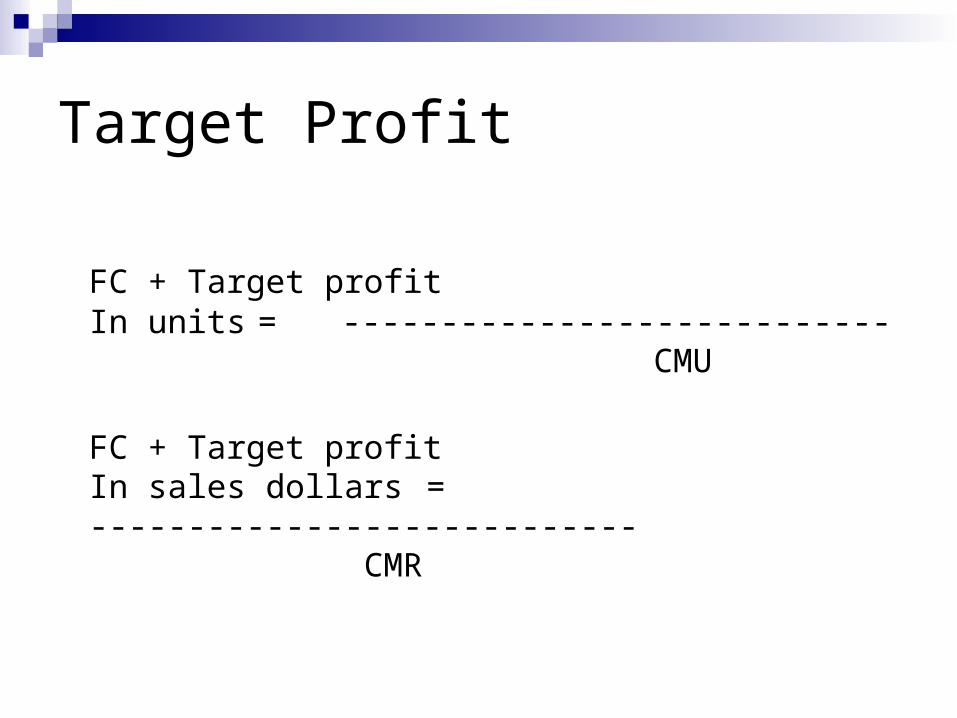

Target Profit

FC + Target profitIn units = ----------------------------

CMU

FC + Target profitIn sales dollars = ----------------------------

CMR

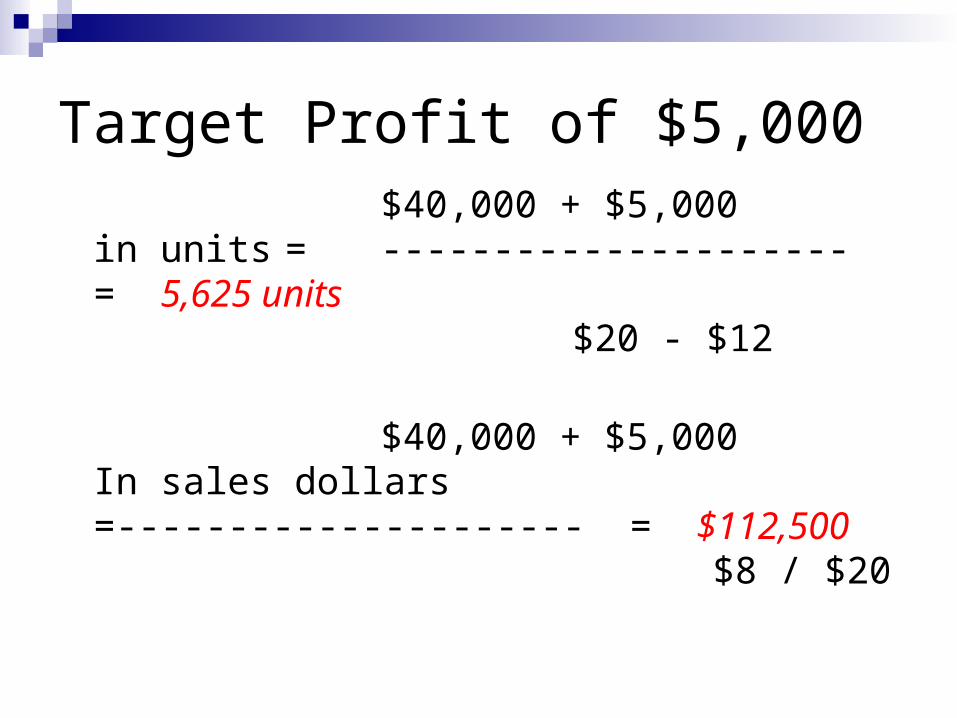

Target Profit of $5,000$40,000 + $5,000

in units = --------------------- = 5,625 units $20 - $12

$40,000 + $5,000In sales dollars =--------------------- = $112,500

$8 / $20

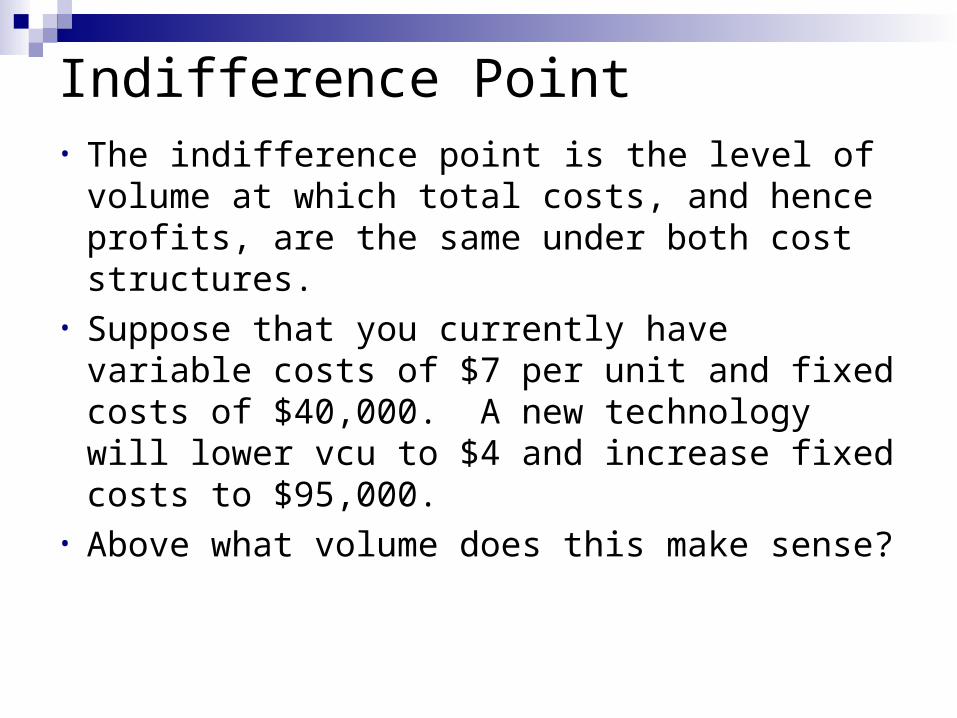

Indifference Point• The indifference point is the level of volume

at which total costs, and hence profits, are the same under both cost structures.

• Suppose that you currently have variable costs of $7 per unit and fixed costs of $40,000. A new technology will lower vcu to $4 and increase fixed costs to $95,000.

• Above what volume does this make sense?

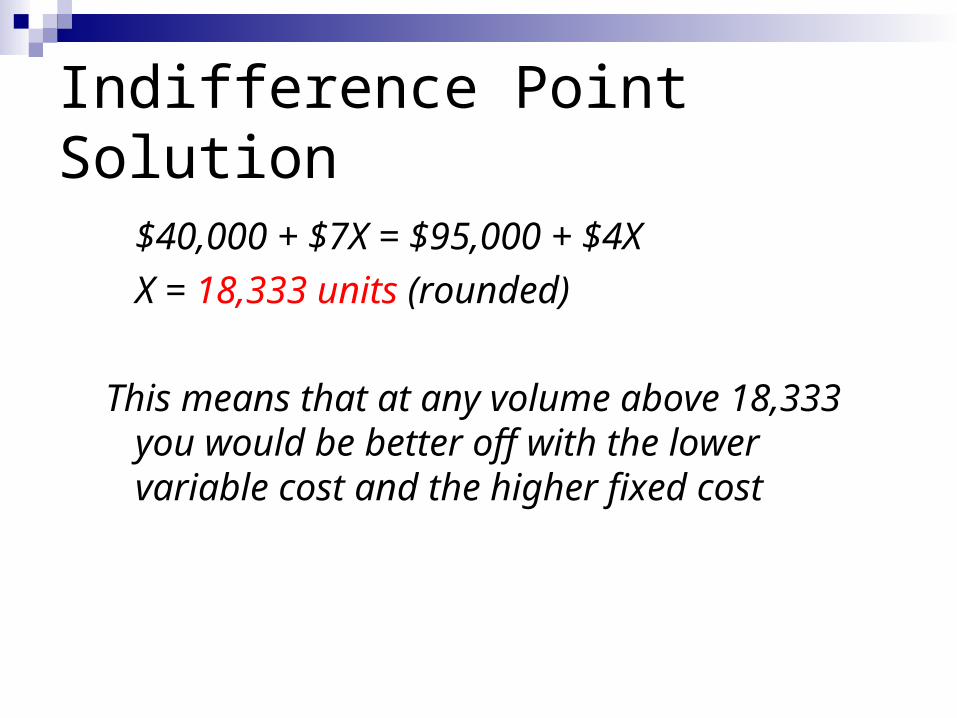

Indifference Point Solution

$40,000 + $7X = $95,000 + $4X

X = 18,333 units (rounded)

This means that at any volume above 18,333 you would be better off with the lower variable cost and the higher fixed cost

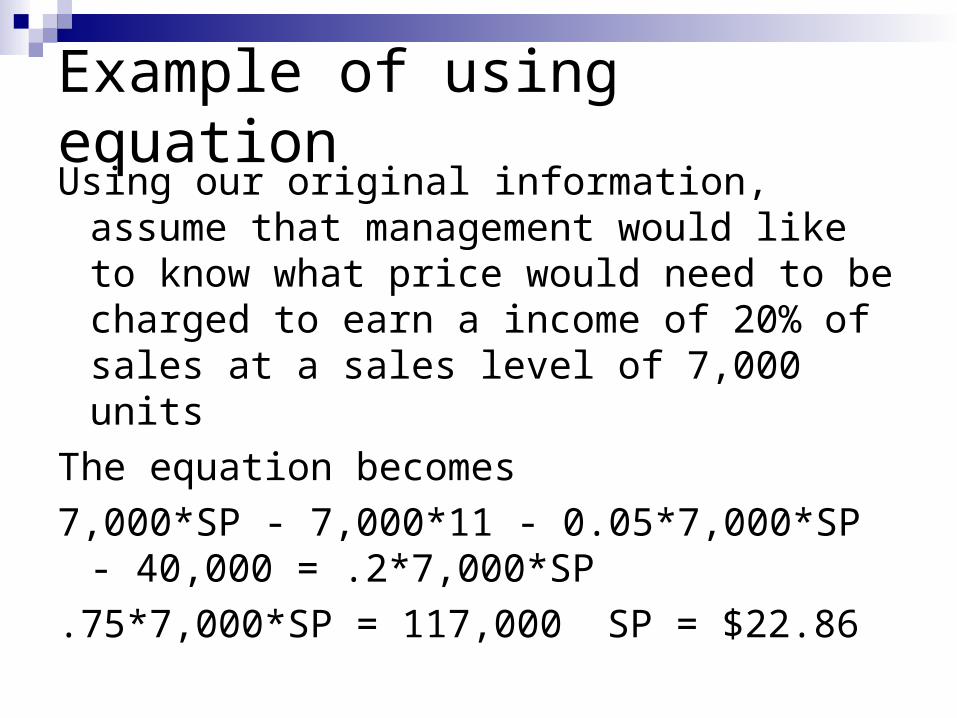

Example of using equationUsing our original information, assume that

management would like to know what price would need to be charged to earn a income of 20% of sales at a sales level of 7,000 units

The equation becomes

7,000*SP - 7,000*11 - 0.05*7,000*SP - 40,000 = .2*7,000*SP

.75*7,000*SP = 117,000 SP = $22.86

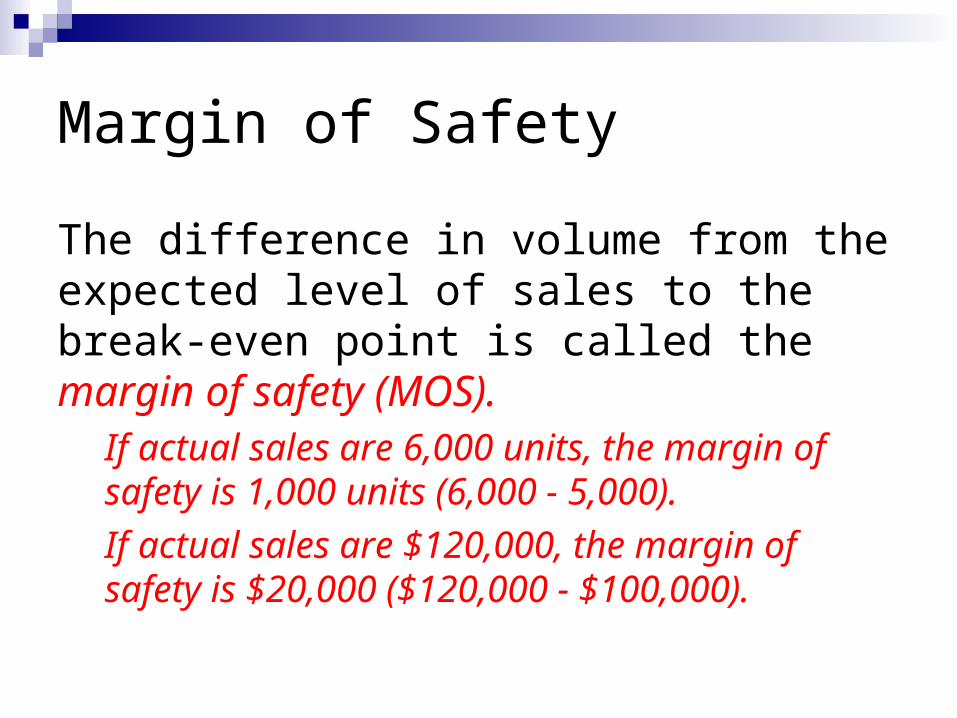

Margin of Safety

The difference in volume from the expected level of sales to the break-even point is called the margin of safety (MOS).

If actual sales are 6,000 units, the margin of safety is 1,000 units (6,000 - 5,000).

If actual sales are $120,000, the margin of safety is $20,000 ($120,000 - $100,000).

Multiple Products

For multiple products, must assume that they are sold in a constant mix to do CVP

Calculate a weighted average contribution margin per unit or contribution margin ratio and then proceed with CVP as normal.

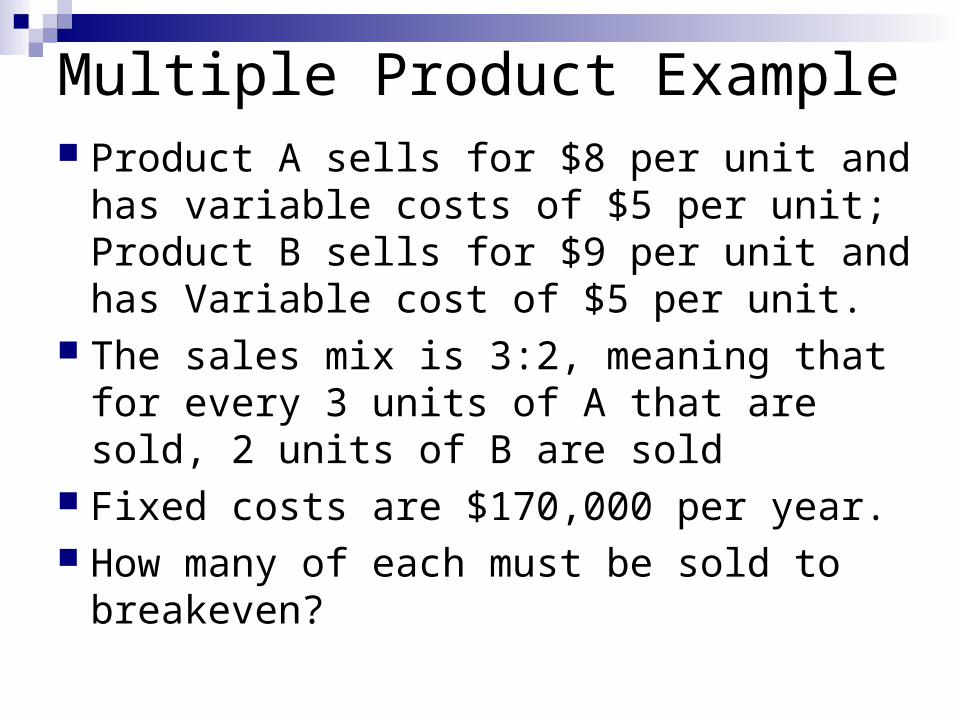

Multiple Product Example Product A sells for $8 per unit and has

variable costs of $5 per unit; Product B sells for $9 per unit and has Variable cost of $5 per unit.

The sales mix is 3:2, meaning that for every 3 units of A that are sold, 2 units of B are sold

Fixed costs are $170,000 per year. How many of each must be sold to

breakeven?

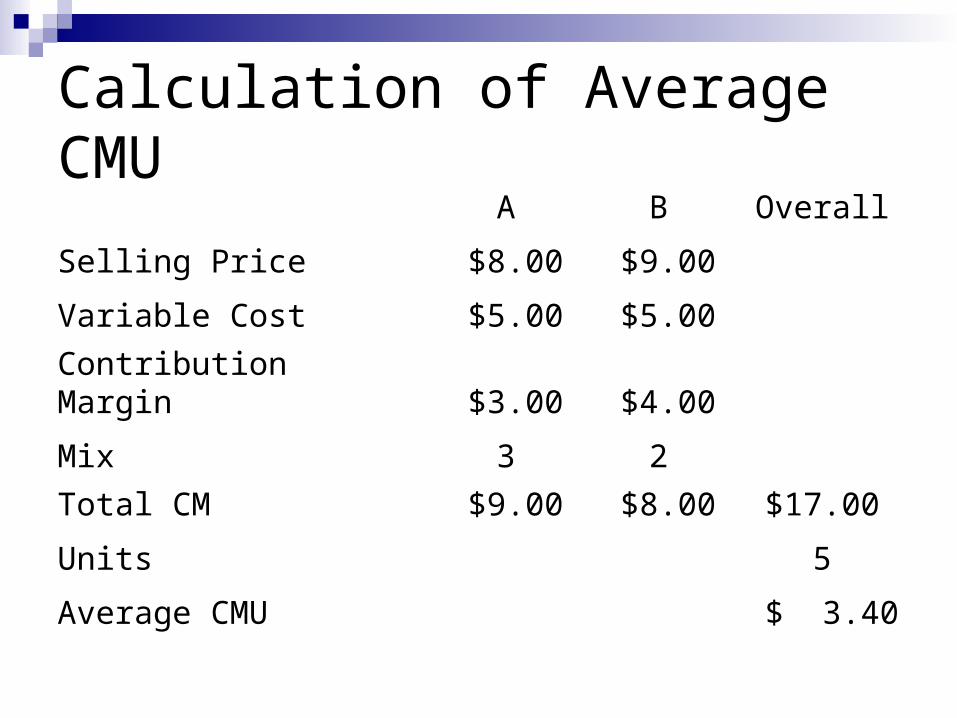

Calculation of Average CMUA B Overall

Selling Price $8.00 $9.00

Variable Cost $5.00 $5.00

Contribution Margin $3.00 $4.00

Mix 3 2

Total CM $9.00 $8.00 $17.00

Units 5

Average CMU $ 3.40

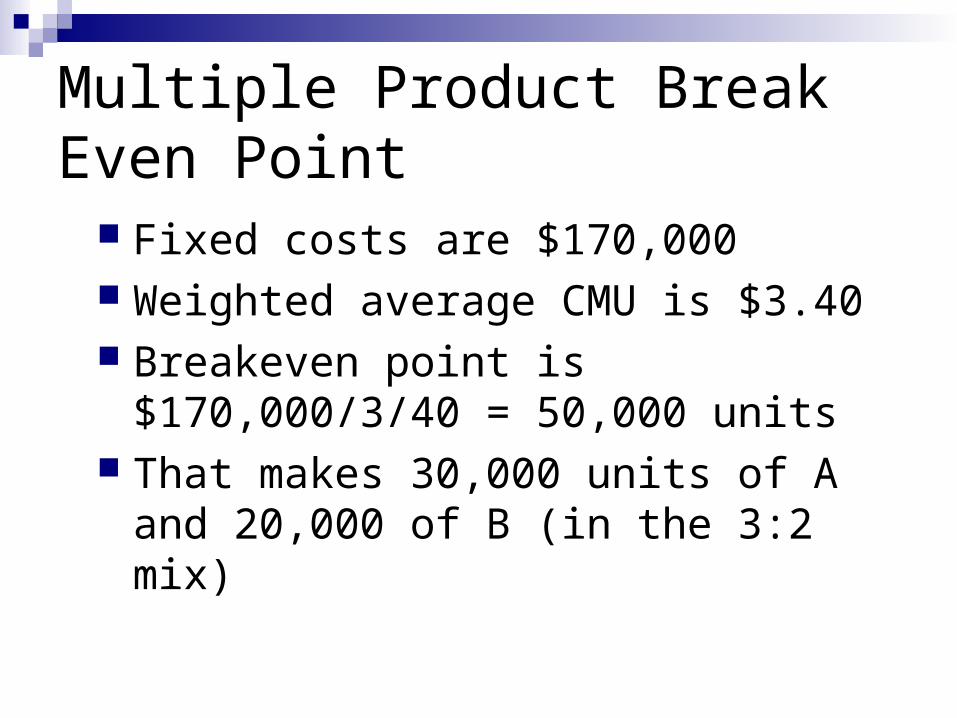

Multiple Product Break Even Point

Fixed costs are $170,000 Weighted average CMU is $3.40 Breakeven point is $170,000/3/40 =

50,000 units That makes 30,000 units of A and

20,000 of B (in the 3:2 mix)

Assumptions and Limitations ofCVP Analysis Selling price, per-unit variable cost, and total

fixed costs must be constant throughout the relevant range.

The company sells only one product, or the sales of each product in a multiproduct company are a constant percentage of sales.

Production equals sales in units.

Relevant Range

Relevant range is the range of volume over which it can reasonably expect selling price, per-unit variable cost, and total fixed costs to be constant.

Do Fixed Costs Add Risk?

Fixed costs cannot be reduced quickly When sales fall off, fixed costs remain When sales rise, fixed costs also remain

the same Do fixed costs add risk?

Operating Leverage Firm’s with high levels of fixed costs are said to

have high operating leverage. Their profit will move faster (up or down) in

response to a change in sales. The ratio of CM/profit will tell you how many

multiples a % change in sales will have on profits

For example if a firm has CM of 30,000 and profit of 10,000, a 10% increase in sales gives a 30% increase in profits!! Try it out.

Constraints A constraint exists when a supply of a

resource (labor, material, processing time) is inadequate to meet demand

Demand itself is also a constraint Need to get the most out of each unit of a

constrained input Do this by calculating a contribution

margin per unit of the constrained resource

Constraints Example

Assume that there are only 800 labor hours available, product A needs 2 hours per unit, product B needs 3 hours per unit.

Product A has a CMU of $5.00, B is $6.00 Demand for each product is 200 units How many units of each product should

you produce?