Embed Size (px)

Citation preview

Chapter Eight Strategies for Short- and Long-Term Financing Options SHORT-TERM FINANCING ......................................................................................... 8-1 Long-Term Financing COST OF CAPITAL ....................................................................................................... 8-2 RISK TERMS .................................................................................................................. 8-5 Derivatives

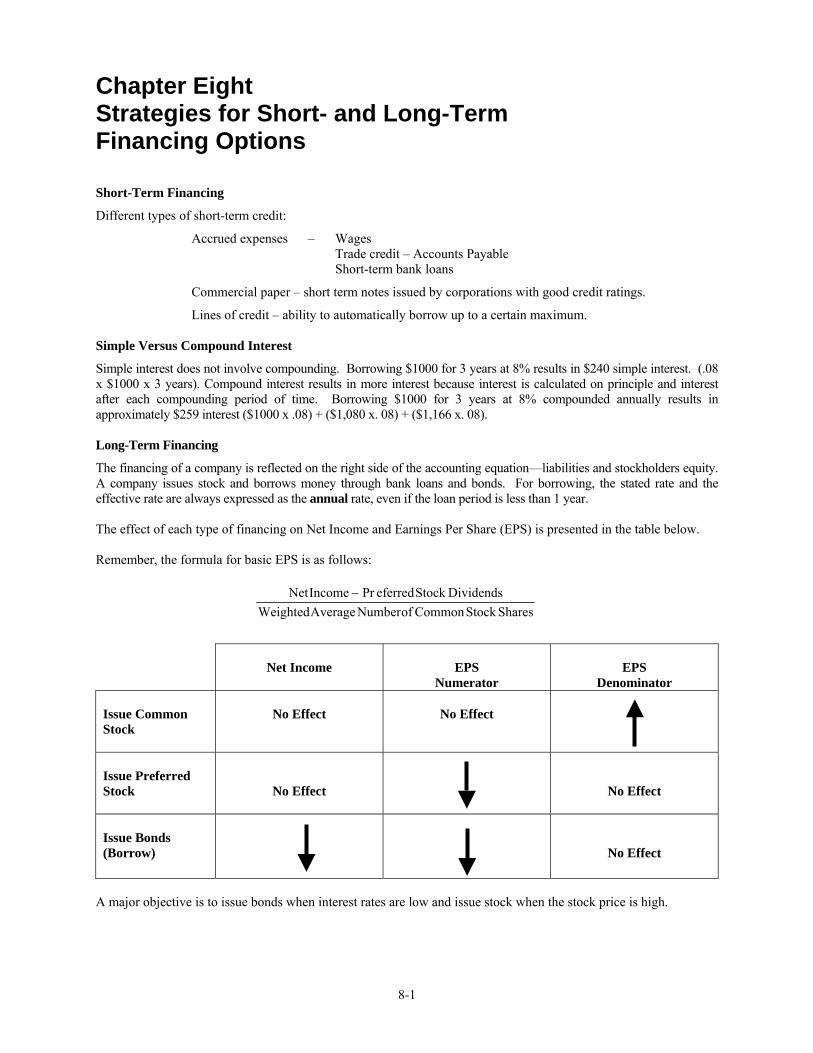

Chapter Eight Strategies for Short- and Long-Term Financing Options Short-Term Financing

Different types of short-term credit:

Accrued expenses – Wages Trade credit – Accounts Payable

Short-term bank loans

Commercial paper – short term notes issued by corporations with good credit ratings.

Lines of credit – ability to automatically borrow up to a certain maximum. Simple Versus Compound Interest

Simple interest does not involve compounding. Borrowing $1000 for 3 years at 8% results in $240 simple interest. (.08 x $1000 x 3 years). Compound interest results in more interest because interest is calculated on principle and interest after each compounding period of time. Borrowing $1000 for 3 years at 8% compounded annually results in approximately $259 interest ($1000 x .08) + ($1,080 x. 08) + ($1,166 x. 08). Long-Term Financing

The financing of a company is reflected on the right side of the accounting equation—liabilities and stockholders equity. A company issues stock and borrows money through bank loans and bonds. For borrowing, the stated rate and the effective rate are always expressed as the annual rate, even if the loan period is less than 1 year. The effect of each type of financing on Net Income and Earnings Per Share (EPS) is presented in the table below. Remember, the formula for basic EPS is as follows:

SharesStockCommonofNumberAverageWeightedDividendsStockeferredPrIncomeNet −

Net Income

EPS

Numerator

EPS

Denominator Issue Common Stock

No Effect

No Effect

Issue Preferred Stock

No Effect

No Effect

Issue Bonds (Borrow)

No Effect

A major objective is to issue bonds when interest rates are low and issue stock when the stock price is high.

8-1

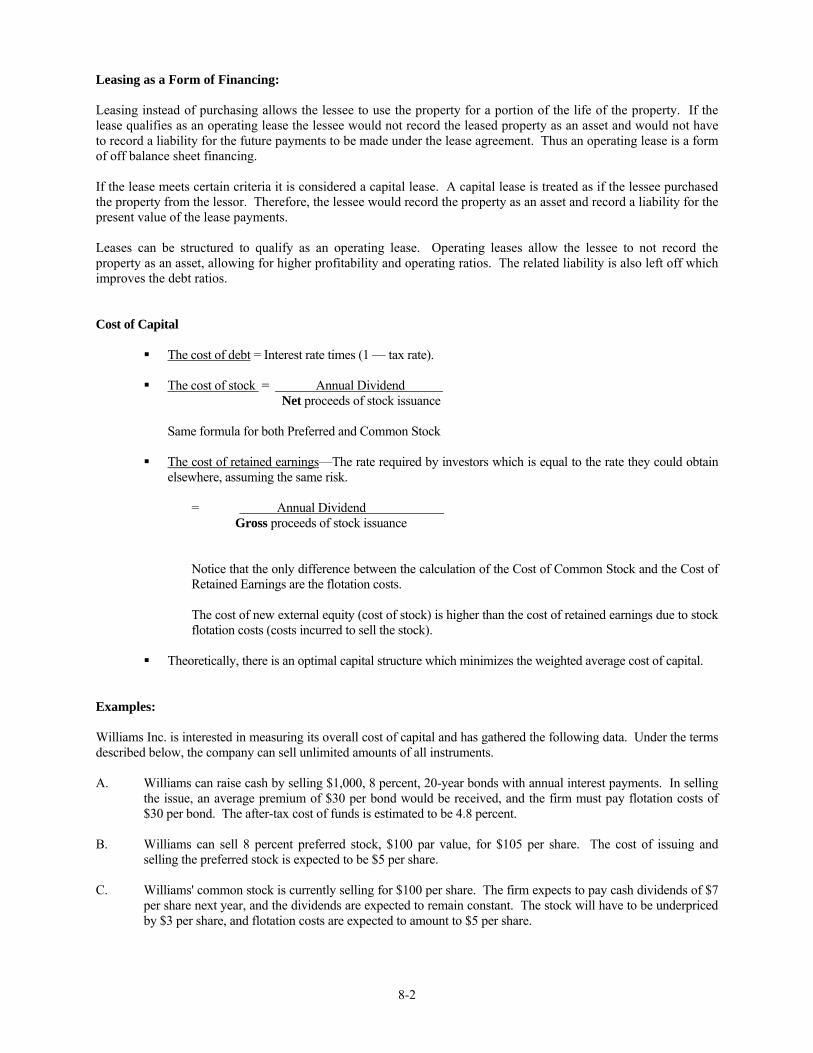

Leasing as a Form of Financing: Leasing instead of purchasing allows the lessee to use the property for a portion of the life of the property. If the lease qualifies as an operating lease the lessee would not record the leased property as an asset and would not have to record a liability for the future payments to be made under the lease agreement. Thus an operating lease is a form of off balance sheet financing. If the lease meets certain criteria it is considered a capital lease. A capital lease is treated as if the lessee purchased the property from the lessor. Therefore, the lessee would record the property as an asset and record a liability for the present value of the lease payments. Leases can be structured to qualify as an operating lease. Operating leases allow the lessee to not record the property as an asset, allowing for higher profitability and operating ratios. The related liability is also left off which improves the debt ratios. Cost of Capital

The cost of debt = Interest rate times (1 — tax rate). The cost of stock = Annual Dividend

Net proceeds of stock issuance

Same formula for both Preferred and Common Stock The cost of retained earnings—The rate required by investors which is equal to the rate they could obtain

elsewhere, assuming the same risk. = Annual Dividend Gross proceeds of stock issuance Notice that the only difference between the calculation of the Cost of Common Stock and the Cost of Retained Earnings are the flotation costs. The cost of new external equity (cost of stock) is higher than the cost of retained earnings due to stock flotation costs (costs incurred to sell the stock). Theoretically, there is an optimal capital structure which minimizes the weighted average cost of capital.

Examples: Williams Inc. is interested in measuring its overall cost of capital and has gathered the following data. Under the terms described below, the company can sell unlimited amounts of all instruments.

A. Williams can raise cash by selling $1,000, 8 percent, 20-year bonds with annual interest payments. In selling

the issue, an average premium of $30 per bond would be received, and the firm must pay flotation costs of $30 per bond. The after-tax cost of funds is estimated to be 4.8 percent.

B. Williams can sell 8 percent preferred stock, $100 par value, for $105 per share. The cost of issuing and

selling the preferred stock is expected to be $5 per share. C. Williams' common stock is currently selling for $100 per share. The firm expects to pay cash dividends of $7

per share next year, and the dividends are expected to remain constant. The stock will have to be underpriced by $3 per share, and flotation costs are expected to amount to $5 per share.

8-2

D. Williams expects to have available $100,000 of retained earnings in the coming year; once these retained earnings are exhausted, the firm will use new common stock as the form of common stock equity financing.

E. Williams' preferred capital structure is:

Long-term debt 30% Preferred stock 20 Common stock 50

Question 1: The cost of funds from common stock for Williams Inc. is: a. 7.0 percent. b. 7.6 percent. c. 7.4 percent. d. 8.1 percent. e. 7.8 percent.

1. Answer: (b) is correct Using the information from section C above, we can complete the formula for the cost of issuing common stock:

7.6% .076$92$7

$5– $3– $100$7

Net

StockCommon of Issue from Proceeds Dividend Annual

Williams Inc. is interested in measuring its overall cost of capital and has gathered the following data. Under the terms described below, the company can sell unlimited amounts of all instruments.

A. Williams can raise cash by selling $1,000, 8 percent, 20-year bonds with annual interest payments. In selling the

issue, an average premium of $30 per bond would be received, and the firm must pay flotation costs of $30 per bond. The after-tax cost of funds is estimated to be 4.8 percent.

B. Williams can sell 8 percent preferred stock, $100 par value, for $105 per share. The cost of issuing and selling

the preferred stock is expected to be $5 per share. C. Williams' common stock is currently selling for $100 per share. The firm expects to pay cash dividends of $7

per share next year, and the dividends are expected to remain constant. The stock will have to be underpriced by $3 per share, and flotation costs are expected to amount to $5 per share.

D. Williams expects to have available $100,000 of retained earnings in the coming year; once these retained

earnings are exhausted, the firm will use new common stock as the form of common stock equity financing. E. Williams' preferred capital structure is:

Long-term debt 30% Preferred stock 20 Common stock 50

Question 2: The cost of funds from retained earnings for Williams Inc. is: a. 7.0 percent.

b. 7.6 percent. c. 7.4 percent. d. 8.1 percent. e. 7.8 percent.

2. Answer: (a) is correct.

8-3

Using the same information from Section C above, we complete the formula for the cost of retained earnings:

%.$

$StockCommon Issuing from Proceeds

Dividend Annual 707100

7===

Gross Williams Inc. is interested in measuring its overall cost of capital and has gathered the following data. Under the terms described below, the company can sell unlimited amounts of all instruments.

A. Williams can raise cash by selling $1,000, 8 percent, 20-year bonds with annual interest payments. In selling the issue, an average premium of $30 per bond would be received, and the firm must pay flotation costs of $30 per bond. The after-tax cost of funds is estimated to be 4.8 percent. B. Williams can sell 8 percent preferred stock, $100 par value, for $105 per share. The cost of issuing and selling the preferred stock is expected to be $5 per share. C. Williams' common stock is currently selling for $100 per share. The firm expects to pay cash dividends of $7 per share next year, and the dividends are expected to remain constant. The stock will have to be underpriced by $3 per share, and flotation costs are expected to amount to $5 per share. D. Williams expects to have available $100,000 of retained earnings in the coming year; once these retained earnings are exhausted, the firm will use new common stock as the form of common stock equity financing. E. Williams' preferred capital structure is:

i. Long-term debt 30% ii. Preferred stock 20

iii. Common stock 50

Question 3. If Williams Inc. needs a total of $200,000, the firm’s weighted average cost is a. 19.8 percent. b. 4.8 percent. c. 6.5 percent. d. 6.8 percent. e. 7.3 percent. Answer: (c) is correct.

Williams preferred capital structure is shown in section E. So if Williams needs $200,000 they will get $100,000 (50%) from Common Stock, $40,000 (20%) from Preferred Stock and $60,000 (30%) from Long-Term debt. So the weighted average cost of capital formula would be as follows:

50% (Cost of Common Stock Financing) + 20% (Cost of Preferred Stock Financing) + 30% (Cost of Long-term debt financing)

Remember, internally generated funds from retained earnings are considered part of Common Stock financing. Therefore, the $100,000 from Common Stock financing comes from Retained Earnings because in Section D the problem tells us Williams expects $100,000 from new retained earnings this coming year. So the formula is now:

50% (7 %) + 20% (Cost of Preferred Stock Financing) + 30% (Cost of Long-term Debt Financing)

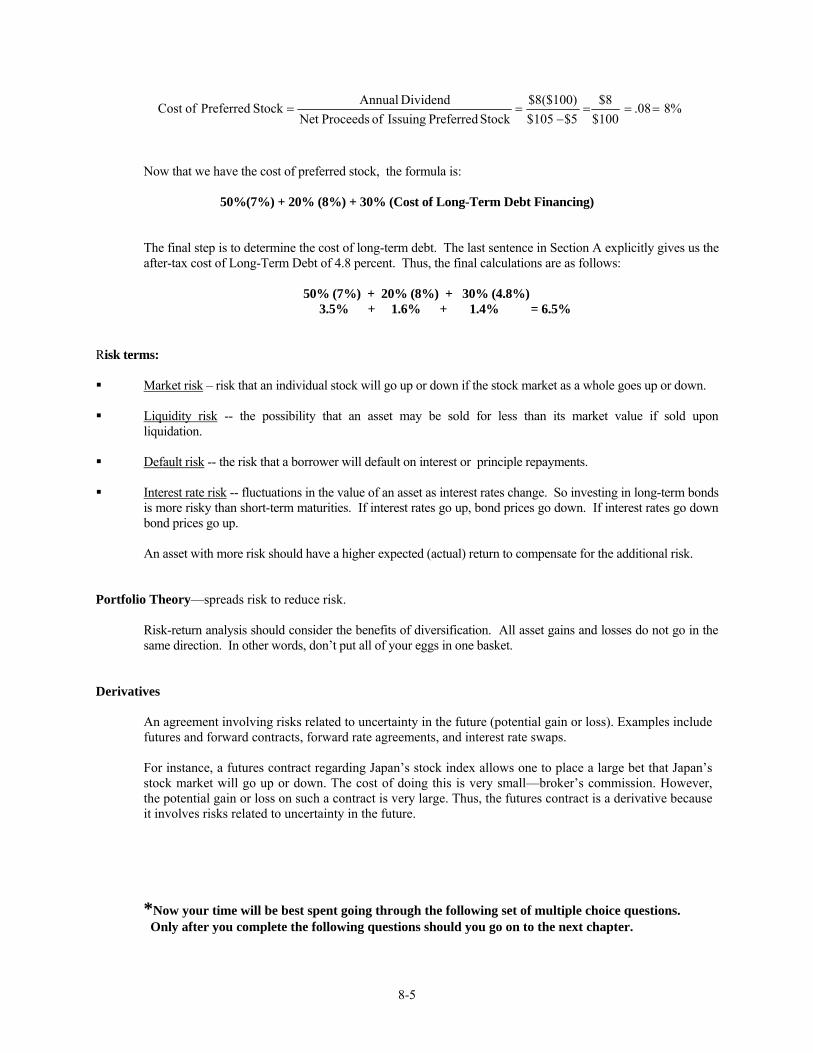

Next, the cost of Preferred Stock Financing must be calculated using the same formula as Cost of Common Stock Financing. Obtaining information from Section B, we have the following:

8-4

%808.100$

8$5$105$)100($8$

Stock Preferred Issuing of ProceedsNet Dividend AnnualStockPreferred ofCost ===

−==

Now that we have the cost of preferred stock, the formula is:

50%(7%) + 20% (8%) + 30% (Cost of Long-Term Debt Financing) The final step is to determine the cost of long-term debt. The last sentence in Section A explicitly gives us the after-tax cost of Long-Term Debt of 4.8 percent. Thus, the final calculations are as follows: 50% (7%) + 20% (8%) + 30% (4.8%) 3.5% + 1.6% + 1.4% = 6.5%

Risk terms: Market risk – risk that an individual stock will go up or down if the stock market as a whole goes up or down.

Liquidity risk -- the possibility that an asset may be sold for less than its market value if sold upon

liquidation. Default risk -- the risk that a borrower will default on interest or principle repayments.

Interest rate risk -- fluctuations in the value of an asset as interest rates change. So investing in long-term bonds

is more risky than short-term maturities. If interest rates go up, bond prices go down. If interest rates go down bond prices go up. An asset with more risk should have a higher expected (actual) return to compensate for the additional risk.

Portfolio Theory—spreads risk to reduce risk.

Risk-return analysis should consider the benefits of diversification. All asset gains and losses do not go in the same direction. In other words, don’t put all of your eggs in one basket.

Derivatives

An agreement involving risks related to uncertainty in the future (potential gain or loss). Examples include futures and forward contracts, forward rate agreements, and interest rate swaps.

For instance, a futures contract regarding Japan’s stock index allows one to place a large bet that Japan’s stock market will go up or down. The cost of doing this is very small—broker’s commission. However, the potential gain or loss on such a contract is very large. Thus, the futures contract is a derivative because it involves risks related to uncertainty in the future. *Now your time will be best spent going through the following set of multiple choice questions. Only after you complete the following questions should you go on to the next chapter.

8-5

8Q-1

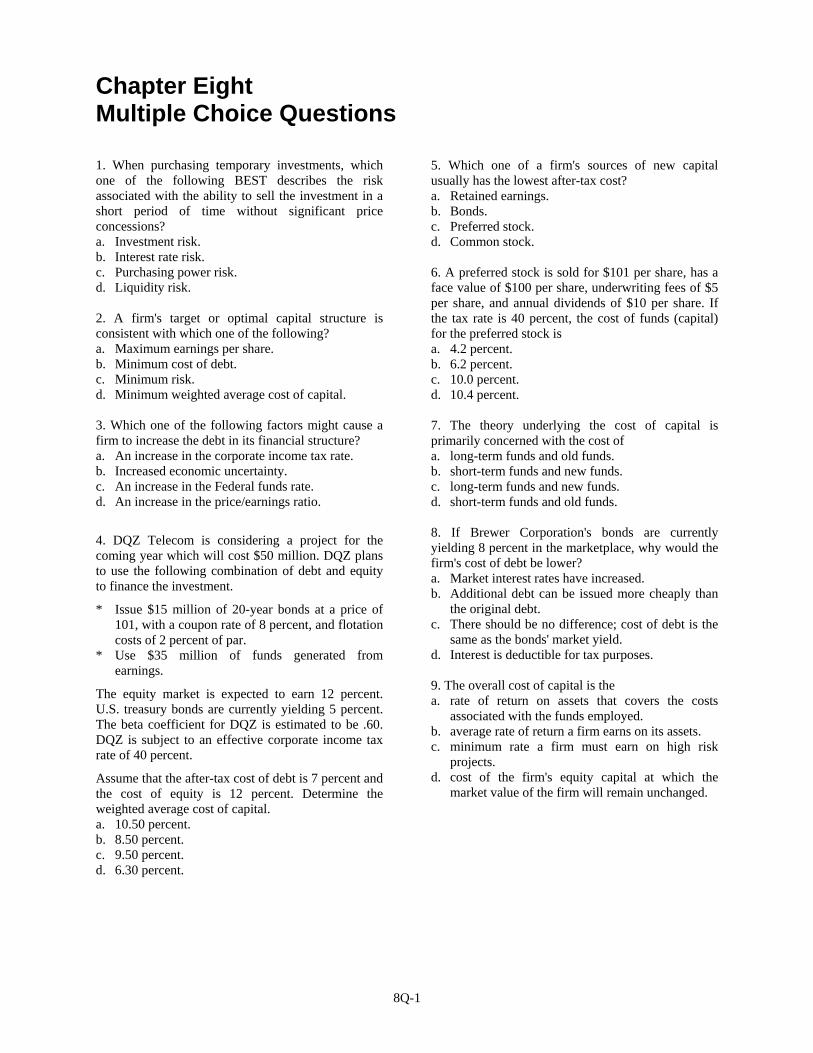

Chapter Eight Multiple Choice Questions 1. When purchasing temporary investments, which one of the following BEST describes the risk associated with the ability to sell the investment in a short period of time without significant price concessions? a. Investment risk. b. Interest rate risk. c. Purchasing power risk. d. Liquidity risk. 2. A firm's target or optimal capital structure is consistent with which one of the following? a. Maximum earnings per share. b. Minimum cost of debt. c. Minimum risk. d. Minimum weighted average cost of capital. 3. Which one of the following factors might cause a firm to increase the debt in its financial structure? a. An increase in the corporate income tax rate. b. Increased economic uncertainty. c. An increase in the Federal funds rate. d. An increase in the price/earnings ratio.

4. DQZ Telecom is considering a project for the coming year which will cost $50 million. DQZ plans to use the following combination of debt and equity to finance the investment.

* Issue $15 million of 20-year bonds at a price of 101, with a coupon rate of 8 percent, and flotation costs of 2 percent of par.

* Use $35 million of funds generated from earnings.

The equity market is expected to earn 12 percent. U.S. treasury bonds are currently yielding 5 percent. The beta coefficient for DQZ is estimated to be .60. DQZ is subject to an effective corporate income tax rate of 40 percent.

Assume that the after-tax cost of debt is 7 percent and the cost of equity is 12 percent. Determine the weighted average cost of capital. a. 10.50 percent. b. 8.50 percent. c. 9.50 percent. d. 6.30 percent.

5. Which one of a firm's sources of new capital usually has the lowest after-tax cost? a. Retained earnings. b. Bonds. c. Preferred stock. d. Common stock. 6. A preferred stock is sold for $101 per share, has a face value of $100 per share, underwriting fees of $5 per share, and annual dividends of $10 per share. If the tax rate is 40 percent, the cost of funds (capital) for the preferred stock is a. 4.2 percent. b. 6.2 percent. c. 10.0 percent. d. 10.4 percent. 7. The theory underlying the cost of capital is primarily concerned with the cost of a. long-term funds and old funds. b. short-term funds and new funds. c. long-term funds and new funds. d. short-term funds and old funds. 8. If Brewer Corporation's bonds are currently yielding 8 percent in the marketplace, why would the firm's cost of debt be lower? a. Market interest rates have increased. b. Additional debt can be issued more cheaply than

the original debt. c. There should be no difference; cost of debt is the

same as the bonds' market yield. d. Interest is deductible for tax purposes. 9. The overall cost of capital is the a. rate of return on assets that covers the costs

associated with the funds employed. b. average rate of return a firm earns on its assets. c. minimum rate a firm must earn on high risk

projects. d. cost of the firm's equity capital at which the

market value of the firm will remain unchanged.

8Q-2

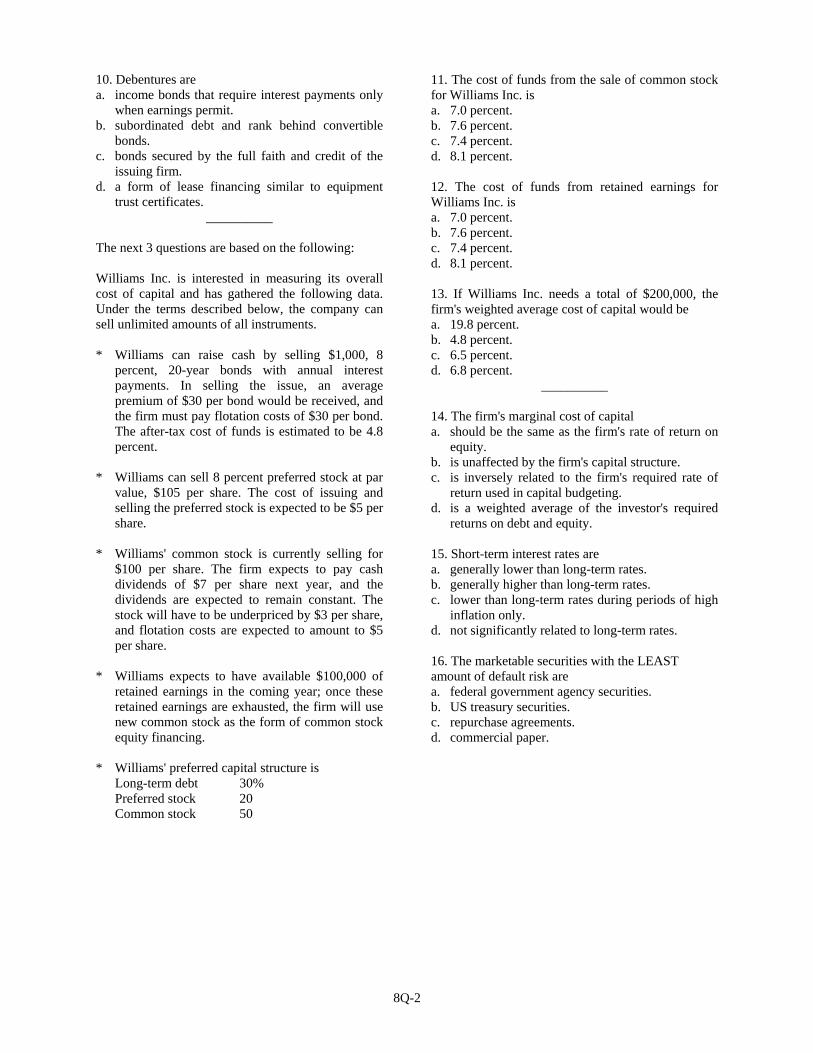

10. Debentures are a. income bonds that require interest payments only

when earnings permit. b. subordinated debt and rank behind convertible

bonds. c. bonds secured by the full faith and credit of the

issuing firm. d. a form of lease financing similar to equipment

trust certificates. __________

The next 3 questions are based on the following: Williams Inc. is interested in measuring its overall cost of capital and has gathered the following data. Under the terms described below, the company can sell unlimited amounts of all instruments. * Williams can raise cash by selling $1,000, 8

percent, 20-year bonds with annual interest payments. In selling the issue, an average premium of $30 per bond would be received, and the firm must pay flotation costs of $30 per bond. The after-tax cost of funds is estimated to be 4.8 percent.

* Williams can sell 8 percent preferred stock at par

value, $105 per share. The cost of issuing and selling the preferred stock is expected to be $5 per share.

* Williams' common stock is currently selling for

$100 per share. The firm expects to pay cash dividends of $7 per share next year, and the dividends are expected to remain constant. The stock will have to be underpriced by $3 per share, and flotation costs are expected to amount to $5 per share.

* Williams expects to have available $100,000 of

retained earnings in the coming year; once these retained earnings are exhausted, the firm will use new common stock as the form of common stock equity financing.

* Williams' preferred capital structure is Long-term debt 30% Preferred stock 20 Common stock 50

11. The cost of funds from the sale of common stock for Williams Inc. is a. 7.0 percent. b. 7.6 percent. c. 7.4 percent. d. 8.1 percent. 12. The cost of funds from retained earnings for Williams Inc. is a. 7.0 percent. b. 7.6 percent. c. 7.4 percent. d. 8.1 percent. 13. If Williams Inc. needs a total of $200,000, the firm's weighted average cost of capital would be a. 19.8 percent. b. 4.8 percent. c. 6.5 percent. d. 6.8 percent.

__________ 14. The firm's marginal cost of capital a. should be the same as the firm's rate of return on

equity. b. is unaffected by the firm's capital structure. c. is inversely related to the firm's required rate of

return used in capital budgeting. d. is a weighted average of the investor's required

returns on debt and equity. 15. Short-term interest rates are a. generally lower than long-term rates. b. generally higher than long-term rates. c. lower than long-term rates during periods of high

inflation only. d. not significantly related to long-term rates. 16. The marketable securities with the LEAST amount of default risk are a. federal government agency securities. b. US treasury securities. c. repurchase agreements. d. commercial paper.

8Q-3

17. Commercial paper a. has a maturity date greater than one year. b. is generally sold only through investment banking

dealers. c. generally does not have an active secondary

market. d. has an interest rate lower than treasury bills. 18. The working capital financing policy that subjects the firm to the GREATEST risk of being unable to meet the firm's maturing obligations is the policy that finances a. fluctuating current assets with long-term debt. b. permanent current assets with long-term debt. c. permanent current assets with short-term debt. d. all current assets with long-term debt. 19. Which one of the following financial instruments generally provides the largest source of short-term credit for small firms a. Installment loans. b. Commercial paper. c. Trade credit. d. Mortgage bonds. 20. Which one of the following provides a spontaneous source of financing for a firm? a. Accounts payable. b. Mortgage bonds. c. Accounts receivable. d. Debentures. 21. Which one of the following responses is NOT an advantage to a corporation that uses the commercial paper market for short-term financing? a. This market provides more funds at lower rates

than other methods provide. b. The borrower avoids the expense of maintaining a

compensating balance with a commercial bank. c. There are no restrictions as to the type of

corporation that can enter into this market. d. This market provides a broad distribution for

borrowing. 22. Which one of the following statements about trade credit is correct? Trade credit is a. not an important source of financing for small

firms. b. a source of long-term financing to the seller. c. subject to risk of buyer default. d. usually an inexpensive source of external

financing.

23. The treasury analyst for Garth Manufacturing has estimated the cash flows for the first half of next year (ignoring any short-term borrowings) as follows.

Cash (millions) Inflows Outflows January $2 $1 February 2 4 March 2 5 April 2 3 May 4 2 June 5 3 Garth has a line of credit of up to $4 million on which it pays interest monthly at a rate of 1 percent of the amount utilized. Garth is expected to have a cash balance of $2 million on January 1 and no amount utilized on its line of credit. Assuming all cash flows occur at the end of the month, approximately how much will Garth pay in interest during the first half of the year? a. Zero. b. $61,000. c. $80,000. d. $132,000. 24. A put is an option that gives its owner the right to do which of the following? a. Sell a specific security at fixed conditions of price and time. b. Sell a specific security at a fixed price for an indefinite time period. c. Buy a specific security at fixed conditions of price and time. d. Buy a specific security at a fixed price for an indefinite time period. 25. A company has several long-term floating-rate bonds outstanding. The company's cash flows have stabilized, and the company is considering hedging interest rate risk. Which of the following derivative instruments is recommended for this purpose? a. Structured short-term note b. Forward contract on a commodity c. Futures contract on a stock d. Swap agreement

8Q-4

26. A company uses its company-wide cost of capital to evaluate new capital investments. What is the implication of this policy when the company has multiple operating divisions, each having unique risk attributes and capital costs? a. High-risk divisions will over-invest in new projects and low risk divisions will under-invest in new projects. b. High-risk divisions will under-invest in high-risk projects. c. Low-risk divisions will over-invest in low-risk projects. d. Low-risk divisions will over-invest in new projects and high risk divisions will under-invest in new projects. 27. A company has cash of $100 million, accounts receivable of $600 million, current assets of $1.2 billion, accounts payable of $400 million, and current liabilities of $900 million. What is its acid-test (quick) ratio? a. 0.11 b. 0.78 c. 1.75 d. 2.11 28. The stock of Fargo Co. is selling for $85. The next annual dividend is expected to be $4.25 and is expected to grow at a rate of 7%. The corporate tax rate is 30%. What percentage represents the firm's cost of common equity? a. 12.0% b. 8.4% c. 7.0% d. 5.0% 29. The following information is available on market interest rates: The risk-free rate of interest 2% Inflation premium 1% Default risk premium 3% Liquidity premium 2% Maturity risk premium 1% What is the market rate of interest on a one-year U.S. Treasury bill? a. 3% b. 5% c. 6% d. 7%

8S-1

Chapter Eight Answers to Multiple Choice Questions 1. (d) Liquidity risk relates to the risk of selling an investment in a short period of time without significant price concessions. Answer (a) is not correct. Investment risk relates to the investment, not the ability to sell an investment in a short period of time without significant price concessions. Answer (b) is not correct. Interest rate risks relates to the risk of interest rate changes affecting the value of the investments. Answer (c) is not correct. Purchasing power risk relates to the risk of changes in the value of the U.S. dollar. 2. (d) is the correct answer. Answer (a) is incorrect. A firm's target or optimal capital structure is not consistent with maximum earnings per share. A firm's target or optimal capital structure minimizes the cost of capital, not the overall maximum earnings per share. Answer (b) is incorrect. A firm's target or optimal capital structure is not consistent with minimum cost of debt. A firm's target or optimal capital structure is concerned with minimizing the cost of debt and equity, not just debt. Answer (c) is incorrect. A firm's target or optimal capital structure is not consistent with minimum risk because the optimum capital structure minimizes cost, not risk. 3. (a) is the correct answer. An increase in the corporate income tax rate might cause a firm to increase the debt in its financial structure. Answer (b) is incorrect. Increased economic uncertainty would not cause a firm to increase the debt in its financial structure. Answer (c) is incorrect. An increase in the Federal funds rate would not cause a firm to increase the debt in its financial structure. Answer (d) is incorrect. An increase in the price/earnings ratio would not cause a firm to increase the debt in its financial structure. 4. (a) is the correct answer. The weighted average cost of capital is 10.50 percent.

debtpercent 30.30million $50

million $15==

debtpercent 70.70million $50

million $35==

70% X 12% = .084 30% X 7% = .021 .105 = 10.5 percent 5. (b) is the correct answer. The source of new capital that has the lowest after-tax cost is bonds because the interest is tax deductible for the organization. 6. (d) is the correct answer. The cost of capital for preferred stock is the dividends per year divided by the net amount received upon stock issuance. Thus, the cost of capital for the preferred stock is 10.4% ($10 / $96). 7. (c) is the correct answer. The theory underlying the cost of capital is primarily concerned with the cost of long-term funds and new funds. Answer (a) is incorrect because the cost of capital is primarily concerned with new funds, not old funds. Answer (b) is incorrect because the cost of capital is primarily concerned with long-term funds rather than short-term funds. Answer (d) is incorrect because short-term funds and old funds are not the primary focus of cost of capital. 8. (d) is the correct answer. Interest is tax deductible; therefore, the firm's cost of debt would be the percentage cost of the bonds less the tax effect. 9. (a) is the correct answer. The overall cost of capital is the rate of return on assets that covers the cost associated with the funds employed. The overall cost of capital is the weighted average cost of capital which includes both debt and equity. Answer (b) is incorrect because the overall cost of capital is not the average rate of return a firm earns on

8S-2

its assets. Hopefully, a firm earns a higher rate of return than the overall cost of capital. Answer (c) is incorrect because the minimum rate a firm must earn on any project is not related to the overall cost of capital. Answer (d) is incorrect because the overall cost of capital is not related to the cost of a firm's equity capital at which the market value of the firm will remain unchanged. 10. (c) is the correct answer. Debentures are bonds secured by the full faith and credit of the issuing firm. Answer (a) is incorrect because debentures are not income bonds that require interest payments only earnings permit. Answer (b) is incorrect because debentures are not subordinated debt and ranked behind convertible bonds. Answer (d) is incorrect because debentures are not a form of lease financing similar to equipment trust certificates. 11. (b) is the correct answer.

%6.792$5$–3$

7$–100$

7$issuancestock from proceeds

dividendyearly ===

12. (a) is the correct answer.

%707.100$7$

stock of price sellingcurrent dividendyearly

===

13. (c) is the correct answer. The company wishes to maintain a capital structure of 30 percent debt, 20 percent preferred stock, and 50 percent common stock (includes retained earnings).

retained earnings 50% X 7% = 3.50% preferred stock 20% X 8% = 1.60% debt 30% X 4.8% = 1.44% 6.54% 14. (d) is the correct answer. A firm's marginal cost of capital is a weighted average of the investor's required returns on debt and equity. The marginal cost of capital is the weighted average cost of additional debt and equity which is the return that investors in the debt and investors in the equity require. Answers (a), (b), and (c) are incorrect because the firm's marginal cost of capital is the weighted average of the investor's required returns on debt and equity. 15. (a) is the correct answer because short-term interest rates are generally lower than long-term interest rates. Answer (d) is incorrect because short-term interest rates are related to long-term rates. 16. (b) is correct. The marketable securities with the least amount of default risk are U.S. Treasury securities. Answer (a) is incorrect because federal government agencies securities do not have the least amount of default risk. Answer (c) is incorrect because repurchase agreements do not have the least amount of default risk. Answer (d) is incorrect because commercial paper does not have the least amount of default risk. 17. (c) is correct. Commercial paper generally does not have an active secondary market. Answer (a) is incorrect because commercial paper does not always have to have a maturity date greater than one year. Answer (b) is incorrect because commercial paper is not generally sold only through investment banking dealers. Answer (d) is incorrect because commercial paper does not have an interest rate lower than treasury bills. 18. (c) is the correct answer. The working capital financing policy that subjects the firm to the greatest risk of being unable to meet the firm's maturing obligations is the policy that finances permanent current assets with short-term debt. Permanent current assets should be financed with long-term liabilities. Answer (a) is incorrect. The working capital financing policy that subjects the firm to the greatest risk of being unable to meet the firm's maturing obligations is not the policy that finances fluctuating current assets with long-term debt. Answer (b) is incorrect. The working capital financing policy that subjects the firm to the greatest risk of being unable to meet the firm's maturing obligations is not the policy that finances permanent current assets with long-term debt. Answer (d) is incorrect. The working capital financing policy that subjects the firm to the greatest risk of being unable to meet the firm's maturing obligations is not the policy that finances all current assets with long-term debt. This is the least risky among the alternatives.

8S-3

19. (c) is the correct answer. Trade credit generally provides the largest source of short-term credit for small firms. Answer (a) is incorrect. Installment loans do not generally provide the largest source of short-term credit for small firms although installment loans can be a source of short term credit. Answer (b) is incorrect. Commercial paper does not generally provide the largest source of short-term credit for small firms. Large, well-known firms can find a market for their own short term unsecured notes (commercial paper) but small firms can not. Answer (d) is incorrect. Mortgage bonds do not generally provide the largest source of short-term credit for small firms. Mortgage bonds are normally long-term credit. 20. (a) is the correct answer. Accounts payable provides a spontaneous source of financing for a firm. Answer (b) is incorrect. Given mortgage bonds link to real estate and its long term nature, mortgage bonds do not provide a spontaneous source of financing for a firm. Answer (c) is incorrect. Accounts receivable do not provide a spontaneous source of financing for a firm. Accounts receivable is when others owe us, not a source of financing for a firm. Answer (d) is incorrect. Debentures do not provide a spontaneous source of financing for a firm. Debentures are unsecured bonds used for long-term financing. 21. (c) is the correct answer. The fact that "there are no restrictions as to the type of corporation who can enter the market" is not an advantage to the borrower. Answer (a) is incorrect since obtaining funds at a lower rate is one of the advantages commercial paper provides. Answer (b) is incorrect since borrowing through the commercial paper market avoids the expense of maintaining a compensating balance and is therefore an advantage. Answer (d) is incorrect since it is an advantage to have a broad distribution for borrowing. 22. (c) is the correct answer since trade credit is subject to the risk of buyer default. This arises as a part of the purchase transaction on account -- seller runs risk of buyer not paying. Choice (a) is incorrect since trade credit is an important source of financing for small firms. Choice (b) is incorrect since trade credit is not long-term financing to the seller. Choice (d) is incorrect since trade credit is an expensive source of external financing. 23. (b) The cash balances for each month are as follows:

Starting balance 2,000,000 End of January 3,000,000 End of February 1,000,000 End of March –2,000,000 End of April –3,000,000 End of May –1,000,000 End of June 1,000,000 Thus, we would need to borrow 2,000,000 for one month, 3,000,000 for one month, and 1,000,000 for one month. The cost is = 1% per month; therefore, approximately $60,000 is the answer. 24. (a) A put option gives the owner the right to sell a specific security at fixed conditions of price and time. "Buy a specific security at fixed conditions of price and time." and "Buy a specific security at a fixed price for an indefinite time period." are incorrect because they use the word "buy". "Sell a specific security at a fixed price for an indefinite time period." is incorrect because a put option does not allow the owner to sell a security for an indefinite period of time. 25. (d) Since the company is trying to hedge the interest on long-term bonds, the best approach would be to have an interest rate swap agreement. These are agreements to exchange interest payments based on one interest structure for payments based on another structure. For example, the company may want to swap for a fixed interest rate to hedge against the floating interest rate. 26. (a) High-risk divisions by their nature will take more risk and over-invest in new projects and low risk divisions by their nature will under-invest in new projects. "High-risk divisions will under-invest in high-risk projects." is incorrect because high-risk divisions will over-invest not under-invest. "Low-risk divisions will over-invest in low-risk projects." is incorrect because low-risk divisions will under-invest not over-invest. 27. (b) The acid-test ration is "quick" assets divided by current liabilities. The quick assets are cash of $100 million plus accounts receivables of $600 million for a total of quick assets of $700 million divided by current liabilities of $900 million for an acid test ratio of .78 rounded.

8S-4

28. (a) In order to arrive at this answer the Return on Equity can be used. 29. (a) Approx nominal rate = real rate + expected inflation rate. Real rate can also be called the risk-free rate on very short term risk free debt. So approx. nominal rate = 2% + 1 So approx. nominal rate = 3% Exact rate can be found using the Fisher Effect

![ExperimentalInvestigationonSeismicBehavioursofReinforced ... · 2019. 12. 29. · seismic loading tests of eight full-size corroded RC short columns,VuandLi[19] ... load-bearing and](https://img.pdfslide.us/doc/110x75/60a8b5614824376307010f0c/experimentalinvestigationonseismicbehavioursofreinforced-2019-12-29-seismic.jpg)