Embed Size (px)

Citation preview

Chapter – 5

Analysis and Interpretation

Chapter-5: Analysis and

Interpretation

5.1 Introduction

5.2 Growth Rate Analysis of Major Financial

Components of Selected Municipal Corporations

5.3 Ratio Analysis

5.4 Analysis of Variance

5.5 Regression Analysis

5. Analysis and Interpretation

5.1 Introduction

To ensure transparency and give a correct picture of assets

and liabilities, municipal corporations has introduced the accrual

based accounting system; presently, a mix of cash based system

and accrual based sys tem is being followed. The system involves

the revenue function (receipt of taxes, charges, loans and grants)

and the expenditure function (release of funds against

establishment, works and supplies).

The corporation maintains its accounts in the form of funds;

the income and expenditure items are indicated under each fund

account. There is a municipal general fund under which the normal

income and expenditure (revenue and capital) items are listed.

Apart from this, there are separate fund accounts for the loans,

anamat (public deposits), capital grants including contributions

from the corporation and tasalmaat (advances). Additionally, the

gas project is maintained as an individual entity and accounting

for the same is maintained separately with that of th e corporation.

The corporation maintains its assets in the form of fixed assets,

deposits, capital works-in-progress, investments in sinking fund

etc.; these are accounted under the anamat fund. The corporation

also holds a record of its current assets inc luding stores and spares

in hand, bank balance and cash balance. The loans and advances

paid to the employees and other parties are also accounted for as

assets.

As part of their liabilities, municipal corporations maintain a

tasalmat fund, consisting of revolving funds for specific purposes.

The reserves and surpluses contained by the corporation include

income from capital receipts and credit balance from revenue

income. In addition to these, there are current liabilities in the

form of sundry creditors , deposits received, employee related

liabilities and other liabilities.

Municipal finances hold the key to the overall status and

progress of service delivery in right direction. Poor finances of

municipal corporation results in poor basic services, low capital

investment, low credibility of municipal corporation, poor revenue

collection efficiency, corruption and the lack of innovation in

resource mobilization. This vicious cycle leads to poor delivery

and low quality of services, which will hamper the g rowth

potential of Municipal Corporation. Here, understanding the

structure or pattern of finance of Municipal Corporation and its

growth holds greater promise in the move towards improving the

municipal revenue.

The analysis of municipal finances first l ooks at the current

financial status of municipal bodies in providing civic amenities,

which is carried out in terms of current spending vis -à-vis the

standard/norm. The revenue of expenditure sides of municipal

finance are then analysed in terms of the gr owth and their

normalized indicators are used to benchmark the cities. The

performance is also measured through relative analysis of the

Municipal Corporations in a cross section in terms of absolute

figures and their growth. Although, the debt/borrowed fu nds can

play an important role, it is not examined here as only few of them

actually have gone to market and made borrowings. Therefore,

debt sustainability of the local governments is not looked upon in

this study.

5.2 Growth Rate Analysis of Major Financial

Components of Selected Municipal

Corporations

Following tables indicates the growth rates of study

indicators of all three Municipal Corporations for the period of ten

years i.e. from 1999-2000 to 2008-2009.

Municipal Corporations are expected to render a minimum

level of services to citizens in order to ensure providing a

minimum standard of living to citizens. To understand the above

situation, per capita revenue and expenditure are compared with

growth in total receipts and expenditures to see whet her there are

any inherent constraints to the provision of services before the

Municipal Corporations.

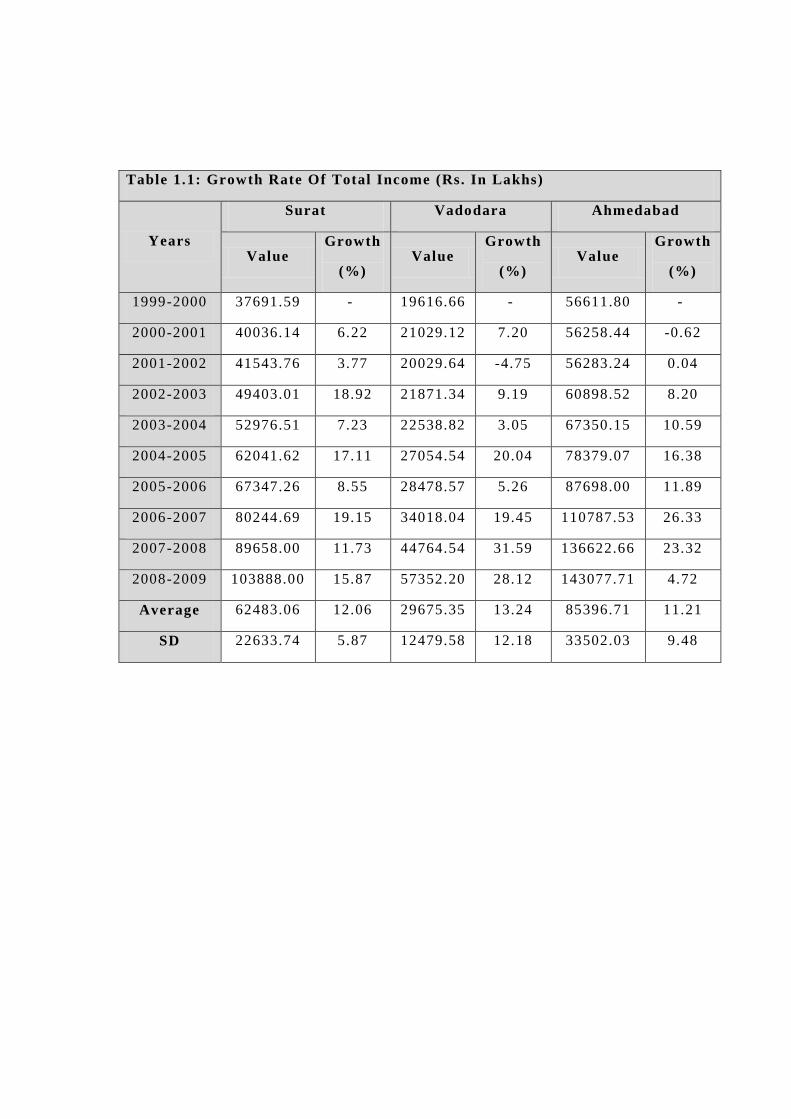

Table 1.1: Growth Rate Of Total Income (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 37691.59 - 19616.66 - 56611.80 -

2000-2001 40036.14 6.22 21029.12 7.20 56258.44 -0.62

2001-2002 41543.76 3.77 20029.64 -4.75 56283.24 0.04

2002-2003 49403.01 18.92 21871.34 9.19 60898.52 8.20

2003-2004 52976.51 7.23 22538.82 3.05 67350.15 10.59

2004-2005 62041.62 17.11 27054.54 20.04 78379.07 16.38

2005-2006 67347.26 8.55 28478.57 5.26 87698.00 11.89

2006-2007 80244.69 19.15 34018.04 19.45 110787.53 26.33

2007-2008 89658.00 11.73 44764.54 31.59 136622.66 23.32

2008-2009 103888.00 15.87 57352.20 28.12 143077.71 4.72

Average 62483.06 12.06 29675.35 13.24 85396.71 11.21

SD 22633.74 5.87 12479.58 12.18 33502.03 9.48

Above table indicate growth rate of total income of all three

Municipal Corporations for the period of ten years data fro m

1999-2000 to 2008-2009. Overall growth rate, during this period

has been shown by taking average growth rate of all consecutive

years.

In the Surat Municipal Corporations growth rate is vary from

3.77 percent in the year 2001-2002 to 19.15 percent in the year

2006-2007 with an average growth rate 12.06 percentage. Standard

deviation (5.87) indicates consistency in the growth rates during

the taken period of time.

The variation in the growth rates for Vadodara Municipal

Corporation is found -4.75 percent in the year 2001-2002 to 28.12

percent in the year 2008-2009. Standard deviation (12.18)

indicates non-homogeneity in the growth rate of total income in

Chart 1.1: Growth Rate Of Total Income

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Ra

te

Surat Vadodara Ahmedabad

Vadodara Municipal Corporation. Looking to the growth rate data

average growth rate is calculated 13 .24 percentages during of the

year 1999-2000 to 2008-2009.

According to the data of Ahmedabad Municipal Corporation

growth rate of total income, -2.82 percent found in the year 2000-

2001 and maximum growth rate found 23.58 percent in the year

2006-2007 with an average growth rate 8.75 percentages. Standard

deviation 9.27 of growth rate of total income indicate high

inconsistency during define period.

Table 1.2: Growth Rate of Per Capita Income (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 1659.53 1542.34 1644.62

2000-2001 1644.98 -0.88 1609.91 4.38 1598.21 -2.82

2001-2002 1592.88 -3.17 1493.07 -7.26 1563.55 -2.17

2002-2003 1767.67 10.97 1587.47 6.32 1654.35 5.81

2003-2004 1768.88 0.07 1592.90 0.34 1789.15 8.15

2004-2005 1933.16 9.29 1861.75 16.88 2036.08 13.80

2005-2006 1958.28 1.30 1908.20 2.50 2227.78 9.41

2006-2007 2177.40 11.19 2219.42 16.31 2752.07 23.53

2007-2008 2270.29 4.27 2843.74 28.13 3318.78 20.59

2008-2009 2454.86 8.13 3547.57 24.75 3398.72 2.41

Average 1922.79 4.57 2020.64 10.26 2198.33 8.75

SD 293.09 5.48 677.64 11.86 712.05 9.27

Above table shows the per capita income of Surat, Vadodara

and Ahmedabad Municipal Corporations for the define period of

ten years using the projected Population from the year 1999 -2000

to 2008-2009 by taking the reference of Census of India.

In the year 2000-2001 and 2001-2002 the per capita income

is found to be negative and highest 11.19 percentage in the year

2006-2007. Average per capita income for the period 1999-2000 to

2008-2009 was 4.57 percentages with absolute figure of Rs

1922.79. The lowest per capita income was Rs. 1592 in the year

2001-2002 and highest Rs. 2454.86 in the year 2008 -2009.

According to per capita income growth rate, in Vadodara

Municipal Corporation the variation is found -7.26 percent to

28.13 percent in the year 2001-2002 & 2007-2008 respectively.

The lowest per capita income Rs 1493.07 was found in the year

Chart 1.2: Growth Rate of Per Capita Income

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Ra

te

Surat Vadodara Ahmedabad

2001-2002 and highest was found Rs. 3547 .57 in the year 2008-

2009. The average per capita income is Rs. 2020.64 with average

growth rate 10.26 percent in Vadodara Municipal Corporation.

The average per capita income during the period from 1999 -

2000 to 2008-2009 is Rs. 2198.33 and average growt h rate is 8.75

in Ahmedabad Municipal Corporation. Looking to the lowest and

highest value of per capita income and growth rate, per capita

income was found Rs. 1563.55 as a lowest in the year 2001 -2002

and Rs. 3398.72 as a highest in the year 2008 -2009. As per growth

rate -2.82 percent as a lowest in the year 2000-2001 and 23.53

percent highest in the year 2006-2007.

Looking to the standard deviation value of all three

Municipal Corporations, consistent increase was found in per

capita income.

The level of expenditure is, to some extent, reflective of the

level of services rendered by Municipal Corporations. While the

trend in per capita expenditure would provide first approximation

of the level as services rendered by a municipal government, a

further segregation into discretionary and non-discretionary

components, relative share of revenue and capital expenditure,

share of establishment, administrative, wages -salaries as a

proportion of total revenue expenditure would reveal the quality of

expenditure and ability of local bodies to meet its stated

objectives.

Following tables indicates the year wise expenditure

growth rates as well as per capita expenditure growth rates.

Table 1.3: Growth Rate of Expenditure (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value Growth

(%)

Value Growth

(%)

1999-2000 23512.02 18268.41 43299.25

2000-2001 22995.83 -2.20 18294.21 0.14 47898.55 10.62

2001-2002 23355.66 1.56 18395.89 0.56 47261.93 -1.33

2002-2003 23904.11 2.35 19167.73 4.20 47406.43 0.31

2003-2004 25139.38 5.17 19535.85 1.92 47168.50 -0.50

2004-2005 26392.43 4.98 20195.36 3.38 49875.97 5.74

2005-2006 28816.07 9.18 20962.12 3.80 53737.70 7.74

2006-2007 34910.61 21.15 28483.90 35.88 68420.36 27.32

2007-2008 40811.53 16.90 29919.44 5.04 76675.34 12.07

2008-2009 48936.00 19.91 38237.29 27.80 78672.91 2.61

Average 29877.36 8.78 23146.02 9.19 56041.69 7.17

SD 8881.48 8.55 6785.19 13.10 13306.40 8.97

Chart 1.3: Growth Rate of Expenditure

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Table indicates the growth rates of Revenue Expenditure for

the period of ten years from 1999-2000 to 2008-2009 for Surat,

Vadodara and Ahmedabad Municipal Corporations.

In Surat compared to 1999-2000 expenditure was low

indicated by -2.20 percent negative growth rate, and heights

percentage growth rates 21.15 percent in the year 200 6-2007

compare to the previous year. With the average growth rate 8.78

percent, Surat municipal corporations found consistent in last few

years compare to beginning years of the duration.

For the Vadodara municipal corporations, growth rate found

to consistent except the year 2006-2007 and 2008-2009. In the

year mentioned with heights growth rates, there was a tremendous

rise found in expenditure with 35.88 and 27.80 percent of growth.

The average growth rate of expenditure is 9.19 percents.

Ahmedabad Municipal Corporation was not that consistent in

expenditure during the period. With the variation, -1.33 percent in

the year 2001-2002 to 27.22 percent in the year 2006 -2007. The

average growth rate of expenditure is 7.17 percent form the period

999-2000 to 2008-2009.

The Standard deviations overall growth rates for all three

municipal corporations can not be predicted.

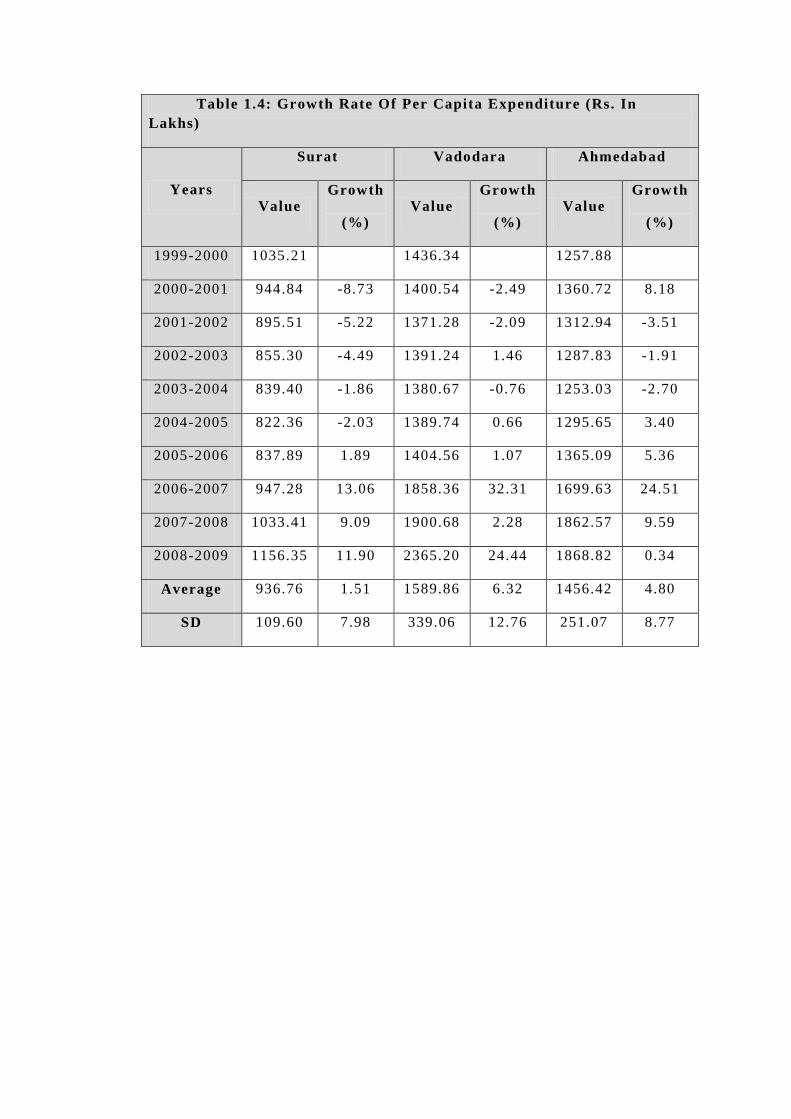

Table 1.4: Growth Rate Of Per Capita Expenditure (Rs. In

Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 1035.21 1436.34 1257.88

2000-2001 944.84 -8.73 1400.54 -2.49 1360.72 8.18

2001-2002 895.51 -5.22 1371.28 -2.09 1312.94 -3.51

2002-2003 855.30 -4.49 1391.24 1.46 1287.83 -1.91

2003-2004 839.40 -1.86 1380.67 -0.76 1253.03 -2.70

2004-2005 822.36 -2.03 1389.74 0.66 1295.65 3.40

2005-2006 837.89 1.89 1404.56 1.07 1365.09 5.36

2006-2007 947.28 13.06 1858.36 32.31 1699.63 24.51

2007-2008 1033.41 9.09 1900.68 2.28 1862.57 9.59

2008-2009 1156.35 11.90 2365.20 24.44 1868.82 0.34

Average 936.76 1.51 1589.86 6.32 1456.42 4.80

SD 109.60 7.98 339.06 12.76 251.07 8.77

In the table above shows the per capita expenditure by

respective Municipal Corporations.

There is a high variation found in growth rate of per capita

expenditure in Surat Municipal Corporation. Per capita

expenditure varies from Rs. 822.36 to Rs. 1156.35. The average

per capita expenditure is Rs. 936.76 with an average growth rate

1.51 percent.

In the Vadodara, the per capita expenditure varies from Rs.

1371.28 during the year 2001-2002 to Rs. 2365.23 in the year

2008-2009. Again there was no linear increase found in the per

capita expenditure growth rate. The average per capita expenditure

of Vadodara Municipal Corporation is Rs. 1589.86 with average

growth rate 6.32 percent.

Chart 1.4: Growth Rate Of Per Capita Expenditure

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

In the Ahmedabad, the per capita expenditure varies from

Rs. 1257.88 during the year 1999-2000 to Rs. 1868.82 in the year

2008-2009. Again there was no linear increase found in the per

capita expenditure growth rate. The average per c apita expenditure

of Ahmedabad Municipal Corporation is Rs. 1456.42 with average

growth rate 4.80 percent.

The high Standard Deviation value indicate that there was no

consistency in the per capital expenditure growth rates amongst

the all three Municipal Corporations.

Table 1.5: Growth Rate of Income over Expenditure (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 14179.56 1348.25 13312.55

2000-2001 17040.31 20.18 2734.91 102.85 8359.90 -37.20

2001-2002 18188.10 6.74 1633.74 -40.26 9021.31 7.91

2002-2003 25498.90 40.20 2703.61 65.49 13492.09 49.56

2003-2004 27837.13 9.17 3002.97 11.07 20181.65 49.58

2004-2005 35649.18 28.06 6859.17 128.41 28503.10 41.23

2005-2006 38531.19 8.08 7516.45 9.58 33960.30 19.15

2006-2007 45334.08 17.66 5534.14 -26.37 42367.17 24.75

2007-2008 -39914.95 -188.05 14845.10 168.25 59947.32 41.49

2008-2009 -47897.12 20.00 19114.92 28.76 64404.80 7.44

Average 13444.64 -4.22 6529.33 49.75 29355.02 22.66

SD 31863.93 69.75 5980.54 71.36 20556.22 27.83

Table shows the growth rate of Income over Expenditure for

the period from 1999-2000 to 2008-2009.

Growth rate varies from -188.05 percent to 40.20 percent in

Surat municipal corporations in the year 2007 -2008 and 2002-2003

respectively.

Growth rate varies from -40.26 percent to 168.25 percent in

Vadodara municipal corporations in the year 2001 -2002 and 2007-

2008 respectively.

Growth rate varies from -37.20 percent to 49.58 percent in

Ahmedabad municipal corporations in the year 2000-2001 and

2003-2004 respectively.

Chart 1.5: Growth Rate of Income over Expenditure

-250.00

-200.00

-150.00

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 69.75, 71.36 and 27.83 percent

respectively.

The revenue performance of a municipal corporation can be

observed in terms of growth of tax revenue, growth of total (tax

and non-tax) revenue, composition of tax and non -tax performers

amongst the municipal corporations, shared revenue to total

revenue (decentralization) and transfers from state government to

total revenue receipts (dependency).

Growth of tax revenue is an important indicator which

reflects the strength of a municipal corporation to undertake

service provisioning responsibilities.

Table 1.6: Growth Rate of Income from Tax (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 29770.78 14817.88 42584.04

2000-2001 31638.85 6.27 16349.95 10.34 42235.01 -0.82

2001-2002 33324.30 5.33 15551.19 -4.89 42964.96 1.73

2002-2003 39488.40 18.50 17878.11 14.96 47586.51 10.76

2003-2004 42066.87 6.53 19158.41 7.16 52056.57 9.39

2004-2005 49423.06 17.49 23899.66 24.75 61251.79 17.66

2005-2006 52179.01 5.58 25029.28 4.73 72686.18 18.67

2006-2007 62127.32 19.07 29045.94 16.05 91249.94 25.54

2007-2008 69415.33 11.73 24575.74 -15.39 103427.29 13.35

2008-2009 80432.53 15.87 31486.37 28.12 105282.30 1.79

Average 48986.65 11.82 21779.25 9.54 66132.46 10.90

SD 17136.18 5.97 5856.87 13.73 25442.11 8.90

Table shows the growth rate of Income from Tax for the

period from 1999-2000 to 2008-2009.

Growth rate varies from 5.33 percent to 19.07 percent in

Surat municipal corporations in the year 2001 -2002 and 2006-2007

respectively.

Growth rate varies from -15.39 percent to 28.12 percent in

Vadodara municipal corporations in the year 2007-2008 and 2008-

2009 respectively.

Chart 1.6: Growth Rate of Income from Tax

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Growth rate varies from -0.82 percent to 25.54 percent in

Ahmedabad municipal corporations in the year 2000 -2001 and

2006-2007 respectively.

Surat, Vadodara and Ahmedabad municipal corpora tions

having average growth rate 5.97, 13.73 and 8.90 percent

respectively.

Growth rate of revenue receipts is an indication of healthy

state of finances of municipal corporations.

Table 1.7: Growth Rate of Total revenue (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 36287.92 16176.26 46711.45

2000-2001 38715.02 6.69 17970.21 11.09 46054.70 -1.41

2001-2002 40168.91 3.76 17196.69 -4.30 47346.56 2.81

2002-2003 47593.32 18.48 18659.87 8.51 51980.45 9.79

2003-2004 51242.63 7.67 19969.28 7.02 59116.07 13.73

2004-2005 60352.46 17.78 24705.54 23.72 69255.75 17.15

2005-2006 65496.03 8.52 25940.38 5.00 79360.17 14.59

2006-2007 78746.90 20.23 30518.33 17.65 101317.54 27.67

2007-2008 87984.51 11.73 31175.19 2.15 124855.62 23.23

2008-2009 101948.90 15.87 39941.57 28.12 128687.25 3.07

Average 60853.66 12.30 24225.33 10.99 75468.56 12.29

SD 22500.70 5.96 7749.40 10.43 32137.40 9.72

Table shows the growth rate of total revenue for the per iod

from 1999-2000 to 2008-2009.

Growth rate varies from 6.69 percent to 20.23 percent in

Surat municipal corporations in the year 2000 -2001 and 2006-2007

respectively.

Growth rate varies from -4.30 percent to 28.12 percent in

Vadodara municipal corpora tions in the year 2001-2002 and 2008-

2009 respectively.

Growth rate varies from -1.41 percent to 27.67 percent in

Ahmedabad municipal corporations in the year 2000 -2001 and

2006-2007 respectively.

Char 1.7: Growth Rate of Total Revenue

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 5.96, 10.43 and 9.72 percent

respectively.

Growth rate of composition of tax and non-tax revenue

indicates one way of establishing creditworthiness.

Table 1.8: Growth Rate of Total (Tax and Non -tax) Revenue (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 32104.04 15321.97 44651.06

2000-2001 34052.33 6.07 16781.86 9.53 44702.78 0.12

2001-2002 36111.91 6.05 15786.63 -5.93 46112.04 3.15

2002-2003 42595.88 17.96 18214.41 15.38 50556.22 9.64

2003-2004 45717.89 7.33 19564.60 7.41 57153.15 13.05

2004-2005 53657.98 17.37 24343.85 24.43 66712.73 16.73

2005-2006 56679.92 5.63 25533.13 4.89 77068.19 15.52

2006-2007 66424.18 17.19 29957.04 17.33 96724.75 25.51

2007-2008 74216.24 11.73 25267.06 -15.66 110886.61 14.64

2008-2009 85995.42 15.87 32372.09 28.12 116168.88 4.76

Average 52755.58 11.69 22314.26 9.50 71073.64 11.46

SD 18179.81 5.46 6048.42 13.97 27814.84 7.91

Table shows the growth rate of total revenue i. e. composite

of tax and non tax for the period from 1999-2000 to 2008-2009.

Growth rate varies from 6.05 percent to 15.87 percent in

Surat municipal corporations in the year 2000 -2001 and 2008-2009

respectively.

Growth rate varies from -15.66 percent to 28.12 percent in

Vadodara municipal corporations in the year 2000 -2001 and 2006-

2007 respectively.

Growth rate varies from 0.12 percent to 25.51 percent in

Ahmedabad municipal corporations in the year 2000 -2001 and

2008-2009 respectively.

Chart 1.8: Growth Rate of Total (Tax and Non-tax) Revenue

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 11.69, 13.97 and 11.46 percent

respectively.

Apart from the measures of revenue growth and composition,

the revenue performance of municipal corporations can be gauged

through other than tax income.

Table 1.9: Growth Rate of other Revenue Income (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 4183.88 854.29 2060.39

2000-2001 4662.69 11.44 1188.36 39.10 1351.92 -34.39

2001-2002 4057.00 -12.99 1410.06 18.66 1234.52 -8.68

2002-2003 4997.44 23.18 445.46 -68.41 1424.23 15.37

2003-2004 5524.74 10.55 404.68 -9.16 1962.92 37.82

2004-2005 6694.48 21.17 361.70 -10.62 2543.02 29.55

2005-2006 8816.11 31.69 407.25 12.59 2291.98 -9.87

2006-2007 12322.72 39.77 561.26 37.82 4592.79 100.39

2007-2008 13768.26 11.73 5908.13 952.66 13969.01 204.15

2008-2009 15953.48 15.87 7569.48 28.12 12518.37 -10.38

Average 8098.08 16.94 1911.07 111.20 4394.92 35.99

SD 4395.46 14.96 2598.84 317.29 4772.40 74.24

Table shows the growth rate of other revenue income for the

period from 1999-2000 to 2008-2009.

Growth rate varies -12.99 percent to 39.77 percent in Surat

municipal corporations in the year 2001-2002 and 2006-2007

respectively.

Growth rate varies -68.41 percent to 952.66 percent in

Vadodara municipal corporations in the year 2002 -2003 and 2007-

2008 respectively.

Chart 1.9: Growth Rate of other Revenue Income

-200.00

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Growth rate varies -34.39 percent to 204.15 percent in

Ahmedabad municipal corporations in the year 2000 -2001 and

2007-2008 respectively.

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 16.94, 111.20 and 35.99 percent

respectively.

Establishment expenditure includes salary & wages,

allowances, reimbursements, employee welfare, terminal bene fits

and other employee costs.

Table 1.10: Growth Rate of Establishment (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 15507.64 10098.12 28540.52

2000-2001 14150.24 -8.75 9392.68 -6.99 31395.10 10.00

2001-2002 14850.10 4.95 9470.13 0.82 30389.77 -3.20

2002-2003 15800.40 6.40 9793.56 3.42 30548.59 0.52

2003-2004 16759.23 6.07 10093.70 3.06 31222.08 2.20

2004-2005 17693.26 5.57 10339.06 2.43 30936.31 -0.92

2005-2006 19270.66 8.92 11289.24 9.19 32924.35 6.43

2006-2007 21638.98 12.29 14927.19 32.22 46285.60 40.58

2007-2008 26366.01 21.84 16265.56 8.97 47329.18 2.25

2008-2009 32126.00 21.85 20787.52 27.80 44917.94 -5.09

Average 19416.25 8.79 12245.68 8.99 35448.94 5.86

SD 5790.41 9.35 3829.16 12.87 7502.65 13.81

Table shows the growth rate of establishment expenditure for

the period from 1999-2000 to 2008-2009.

Growth rate varies from -8.75 percent to 21.85 percent in

Surat municipal corporations in the year 2000 -2001 and 2008-2009

respectively.

Growth rate varies from -6.99 percent to 32.22 percent in

Vadodara municipal corporations in the year 2000 -2001 and 2006-

2007 respectively.

Growth rate varies from -5.09 percent to 40.58 percent in

Ahmedabad municipal corporations in the year 2000-2001 and

2007-2008 respectively.

Chart 1.10: Growth Rate of Establishment

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 8.79, 8.99 and 5.86 percent

respectively.

Administrative expense is one of the major expenses of total

expenditure.

Table 1.11: Growth Rate of Administrative Expenses (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value

Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 4722.18 256.08 899.04

2000-2001 6352.90 34.53 322.03 25.76 1029.63 14.53

2001-2002 6622.05 4.24 274.80 -14.67 917.14 -10.93

2002-2003 6616.59 -0.08 175.80 -36.03 1535.37 67.41

2003-2004 7558.60 14.24 184.66 5.04 1109.68 -27.73

2004-2005 8176.12 8.17 132.42 -28.29 1046.49 -5.69

2005-2006 9010.93 10.21 171.74 29.70 1315.89 25.74

2006-2007 10482.07 16.33 668.03 288.97 1843.22 40.07

2007-2008 10992.21 4.87 998.08 49.41 2144.85 16.36

2008-2009 13800.00 25.54 1275.56 27.80 2378.69 10.90

Average 8433.37 13.12 445.92 38.63 1422.00 14.52

SD 2695.54 11.06 399.70 98.21 533.35 28.36

Table shows the growth rate of Administrative expense for

the period from 1999-2000 to 2008-2009.

Growth rate varies from -0.08 percent to 34.53 percent in

Surat municipal corporations in the year 2002 -2003 and 2001-2002

respectively.

Growth rate varies from -36.03 percent to 288.97 percent in

Vadodara municipal corporations in the year 2002 -2003 and 2006-

2007 respectively.

Growth rate varies from -27.73 percent to 67.41 percent in

Ahmedabad municipal corporations in the year 2003 -2004 and

2002-2003 respectively.

Chart 1.11: Growth Rate of Administrative Expenses

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 13.12, 38.63 and 14.52 percent

respectively.

Table 1.12: Growth Rate of Repair & Maintenance Expense (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 3652.15 3800.46 1905.96

2000-2001 4249.63 16.36 4405.69 15.92 1604.40 -15.82

2001-2002 3427.02 -19.36 4218.59 -4.25 2070.77 29.07

2002-2003 3075.35 -10.26 4763.58 12.92 2331.26 12.58

2003-2004 3353.20 9.03 5208.53 9.34 1888.42 -19.00

2004-2005 4017.97 19.82 5796.71 11.29 3308.16 75.18

2005-2006 4540.00 12.99 5725.93 -1.22 3149.98 -4.78

2006-2007 7006.57 54.33 8668.78 51.40 3875.61 23.04

2007-2008 7570.52 8.05 8715.69 0.54 3548.26 -8.45

2008-2009 8604.00 13.65 11138.72 27.80 4958.78 39.75

Average 4949.64 11.62 6244.27 13.75 2864.16 14.62

SD 2001.21 20.55 2429.72 17.20 1081.56 30.72

Table shows the growth rate of Repair & Maintenance

Expense for the period from 1999-2000 to 2008-2009.

Growth rate varies from -19.36 percent to 54.33 percent in

Surat municipal corporations in the year 2001 -2002 and 2006-2007

respectively.

Growth rate varies from -4.25 percent to 51.40 percent in

Vadodara municipal corporations in the year 2001 -2002 and 2006-

2007 respectively.

Chart 1.12: Growth Rate of Repair & Maintenance Expense

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Growth rate varies from -19.00 percent to 75.18 percent in

Ahmedabad municipal corporations in the year 2003 -2004 and

2004-2005 respectively.

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 20.55, 17.20 and 30.72 percent

respectively.

Table 1.13: Growth Rate of Services related direct expense (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value

Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 923.50 3080.76 1288.06

2000-2001 1328.08 43.81 3046.13 -1.12 1381.42 7.25

2001-2002 1438.40 8.31 3049.38 0.11 1504.47 8.91

2002-2003 1434.38 -0.28 3209.16 5.24 1717.94 14.19

2003-2004 1615.09 12.60 3188.66 -0.64 1429.23 -16.81

2004-2005 2218.13 37.34 3444.07 8.01 1984.05 38.82

2005-2006 2589.31 16.73 3597.90 4.47 3004.31 51.42

2006-2007 3531.72 36.40 4434.94 23.26 3564.92 18.66

2007-2008 3670.79 3.94 4827.01 8.84 4421.58 24.03

2008-2009 4284.59 16.72 6168.95 27.80 4841.94 9.51

Average 2303.40 19.51 3804.70 8.44 2513.79 17.33

SD 1165.49 15.88 1033.28 10.39 1345.74 19.62

Table shows the growth rate of Services related direct

expense for the period from 1999-2000 to 2008-2009.

Growth rate varies from -0.28 percent to 37.34 percent in

Surat municipal corporations in the year 2002 -2003 and 2004-2005

respectively.

Growth rate varies from -1.12 percent to 27.80 percent in

Vadodara municipal corporations in the year 2000 -2001 and 2008-

2009 respectively.

Growth rate varies from -16.81 percent to 51.42 percent in

Ahmedabad municipal corporations in the year 2003-2004 and

2005-2006 respectively. Surat, Vadodara and Ahmedabad

Chart 1.13: Growth Rate of Services related direct expense

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

rate

Surat Vadodara Ahmedabad

municipal corporations having average growth rate 15.88, 10.39

and 19.62 percent respectively.

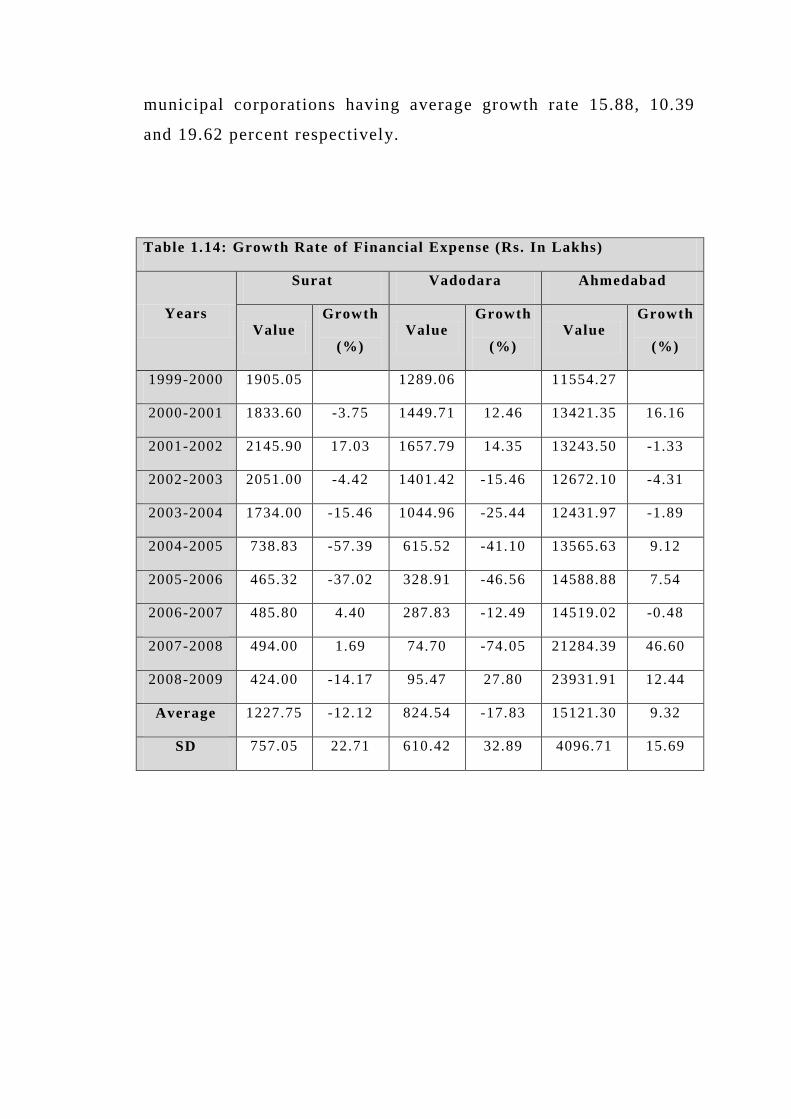

Table 1.14: Growth Rate of Financial Expense (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 1905.05 1289.06 11554.27

2000-2001 1833.60 -3.75 1449.71 12.46 13421.35 16.16

2001-2002 2145.90 17.03 1657.79 14.35 13243.50 -1.33

2002-2003 2051.00 -4.42 1401.42 -15.46 12672.10 -4.31

2003-2004 1734.00 -15.46 1044.96 -25.44 12431.97 -1.89

2004-2005 738.83 -57.39 615.52 -41.10 13565.63 9.12

2005-2006 465.32 -37.02 328.91 -46.56 14588.88 7.54

2006-2007 485.80 4.40 287.83 -12.49 14519.02 -0.48

2007-2008 494.00 1.69 74.70 -74.05 21284.39 46.60

2008-2009 424.00 -14.17 95.47 27.80 23931.91 12.44

Average 1227.75 -12.12 824.54 -17.83 15121.30 9.32

SD 757.05 22.71 610.42 32.89 4096.71 15.69

Table shows the growth rate of Financial Expense for the

period from 1999-2000 to 2008-2009.

Growth rate varies from -57.39 percent to 17.03 percent in

Surat municipal corporations in the year 2004 -2005 and 2001-2002

respectively.

Growth rate varies from -46.56 percent to 27.80 percent in

Vadodara municipal corporations in the year 2005 -2006 and 2008-

2009 respectively.

Growth rate varies from -4.31 percent to 46.60 percent in

Ahmedabad municipal corporations in the year 2002 -2003 and

2007-2008 respectively.

Chart 1.14: Growth Rate of Financial Expense

-100.00

-80.00

-60.00

-40.00

-20.00

0.00

20.00

40.00

60.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 22.71, 32.89 and 15.69 percent

respectively.

Table 1.15: Growth Rate of Salary and Wages (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 9280.63 4458.94 9509.21

2000-2001 7500.65 -19.18 4513.89 1.23 10460.31 10.00

2001-2002 7571.36 0.94 4528.52 0.32 14273.74 36.46

2002-2003 7608.56 0.49 4210.21 -7.03 14471.23 1.38

2003-2004 7728.81 1.58 4147.39 -1.49 15603.71 7.83

2004-2005 8214.13 6.28 4089.41 -1.40 15757.43 0.99

2005-2006 11090.32 35.02 5517.63 34.92 17404.26 10.45

2006-2007 12685.48 14.38 8373.74 51.76 25559.02 46.85

2007-2008 13236.10 4.34 7162.45 -14.47 26246.02 2.69

2008-2009 16237.20 22.67 12811.31 78.87 26558.06 1.19

Average 10115.32 7.39 5981.35 15.86 17584.30 13.09

SD 3061.80 15.35 2801.66 31.86 6351.31 16.82

Table shows the growth rate of Salary and Wages for the

period from 1999-2000 to 2008-2009.

Growth rate varies from -19.18 percent to 35.02 percent in

Surat municipal corporations in the year 2000 -2001 and 2005-2006

respectively.

Growth rate varies from -14.47 percent to 78.87 percent in

Vadodara municipal corporations in the year 2007 -2008 and 2008-

2009 respectively.

Growth rate varies from 0.99 percent to 46.85 percent in

Ahmedabad municipal corporations in the year 2004-2005 and

2006-2007 respectively.

Chart 1.15: Growth Rate of Salary and Wages

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

100.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 15.35, 31.86 and 16.82 percent

respectively.

Table 1.16: Growth Rate of Other than Salary and Wages (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 6227.01 5639.18 19031.31

2000-2001 6651.39 6.82 4878.80 -13.48 20934.78 10.00

2001-2002 7278.74 9.43 4941.61 1.29 16116.03 -23.02

2002-2003 8191.84 12.54 5583.35 12.99 16077.36 -0.24

2003-2004 9030.42 10.24 5946.31 6.50 15618.37 -2.85

2004-2005 9479.13 4.97 6249.65 5.10 15178.88 -2.81

2005-2006 8180.34 -13.70 5771.61 -7.65 15520.09 2.25

2006-2007 8953.50 9.45 6553.44 13.55 20726.58 33.55

2007-2008 12767.19 42.59 9103.11 38.91 21083.16 1.72

2008-2009 15888.80 24.45 7976.21 -12.38 18359.88 -12.92

Average 9264.84 11.87 6264.33 4.98 17864.64 0.63

SD 2956.57 15.18 1330.86 16.23 2440.17 15.58

Table shows the growth rate of Other than Salary and Wages

for the period from 1999-2000 to 2008-2009.

Growth rate varies from -13.70 percent to 42.59 percent in

Surat municipal corporations in the year 2005 -2006 and 2007-2008

respectively.

Growth rate varies from -13.48 percent to 38.91 percent in

Vadodara municipal corporations in the year 2000-2001 and 2007-

2008 respectively.

Growth rate varies from -23.02 percent to 33.55 percent in

Ahmedabad municipal corporations in the year 2001 -2002 and

2006-2007 respectively.

Chart 1.16: Growth Rate of Other than Salary and Wages

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal co rporations

having average growth rate 11.87, 4.98 and 0.63 percent

respectively.

Table 1.17: Growth Rate of Octroi and Toll (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 22259.85 9672.19 30918.72

2000-2001 23003.10 3.34 11321.95 17.06 32451.10 4.96

2001-2002 23495.29 2.14 10458.90 -7.62 30806.73 -5.07

2002-2003 28502.80 21.31 11991.35 14.65 36130.57 17.28

2003-2004 30135.03 5.73 13489.09 12.49 40093.84 10.97

2004-2005 35417.50 17.53 15994.42 18.57 46204.73 15.24

2005-2006 40520.73 14.41 18451.98 15.37 55150.39 19.36

2006-2007 48559.48 19.84 22489.07 21.88 70815.00 28.40

2007-2008 34734.55 -28.47 16157.67 -28.15 51200.93 -27.70

2008-2009 0.00 -100.00 26.43 -99.84 0.00 -100.00

Average 28662.83 -4.91 13005.30 -3.96 39377.20 -4.06

SD 13091.40 38.74 6042.64 39.37 18791.64 39.53

Table shows the growth rate of Octroi and Toll for the

period from 1999-2000 to 2008-2009.

Growth rate varies from -100.00 percent to 21.31 percent in

Surat municipal corporations in the year 2008 -2009 and 2002-2003

respectively.

Growth rate varies from -99.84 percent to 21.88 percent in

Vadodara municipal corporations in the year 2008 -2009 and 2006-

2007 respectively.

Growth rate varies from -100.00 percent to 28.40 percent in

Ahmedabad municipal corporations in the year 2008 -2009 and

2006-2007 respectively.

Chart 1.17: Growth Rate of Octroi and Toll

-120.00

-100.00

-80.00

-60.00

-40.00

-20.00

0.00

20.00

40.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 38.74, 39.37 and 39.53 percent

respectively.

Table 1.18: Growth Rate of Property Tax (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 7503.06 5003.98 11665.32

2000-2001 8625.18 14.96 4987.93 -0.32 9783.91 -16.13

2001-2002 9821.29 13.87 5055.04 1.35 12158.23 24.27

2002-2003 10978.40 11.78 5350.72 5.85 11455.94 -5.78

2003-2004 11817.36 7.64 5141.38 -3.91 11992.73 4.69

2004-2005 13453.36 13.84 7307.88 42.14 15047.07 25.47

2005-2006 10973.57 -18.43 6030.00 -17.49 17535.79 16.54

2006-2007 12417.06 13.15 5862.54 -2.78 20434.94 16.53

2007-2008 34084.00 174.49 6497.04 10.82 21372.31 4.59

2008-2009 79742.40 133.96 24280.67 273.72 22610.86 5.80

Average 19941.57 40.58 7551.72 34.38 15405.71 8.44

SD 22327.92 66.04 5926.87 91.20 4724.22 13.75

Table shows the growth rate of Property Tax for the period

from 1999-2000 to 2008-2009.

Growth rate varies from -18.43 percent to 174.49 percent in

Surat municipal corporations in the year 2005 -2006 and 2007-2008

respectively.

Growth rate varies from -17.49 percent to 273.72 percent in

Vadodara municipal corporations in the year 2005 -2006 and 2008-

2009 respectively.

Growth rate varies from -16.13 percent to 25.47 percent in

Ahmedabad municipal corporations in the year 2000 -2001 and

2004-2005 respectively.

Chart 1.18: Growth Rate of Property Tax

-50.00

0.00

50.00

100.00

150.00

200.00

250.00

300.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 66.04, 91.20 and 13.75 percent

respectively.

Table 1.19: Growth Rate of Reserved & Surplus (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 18515.48 1092.18 14208.68

2000-2001 30311.19 63.71 2442.43 123.63 13551.75 -4.62

2001-2002 40911.29 34.97 1358.95 -44.36 2601.00 -80.81

2002-2003 46549.74 13.78 2661.12 95.82 2701.00 3.84

2003-2004 60821.21 30.66 2818.30 5.91 11301.00 318.40

2004-2005 80234.31 31.92 6726.69 138.68 11301.00 0.00

2005-2006 92896.50 15.78 7344.70 9.19 21101.00 86.72

2006-2007 237647.88 155.82 5160.34 -29.74 31201.00 47.87

2007-2008 254503.62 7.09 24561.28 375.96 42800.20 37.18

2008-2009 279953.98 10.00 25484.69 3.76 78901.00 84.35

Average 114234.52 40.41 7965.07 75.43 22966.77 54.77

SD 101650.99 46.65 9238.53 130.78 23229.00 111.39

Table shows the growth rate of Reserved & Surplace for the

period from 1999-2000 to 2008-2009.

Growth rate varies from 7.09 percent to 155.82 percent in

Surat municipal corporations in the year 2007 -2008 and 2006-2007

respectively.

Growth rate varies from -44.36 percent to 375.96 percent in

Vadodara municipal corporations in the year 2001 -2002 and 2007-

2008 respectively.

Growth rate varies from -80.81 percent to 318.40 percent in

Ahmedabad municipal corporations in the year 2001 -2002 and

2003-2004 respectively.

Chart 1.19: Growth Rate of Reserved & Surplus

-200.00

-100.00

0.00

100.00

200.00

300.00

400.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 46.65, 130.78 and 111.39 percent

respectively.

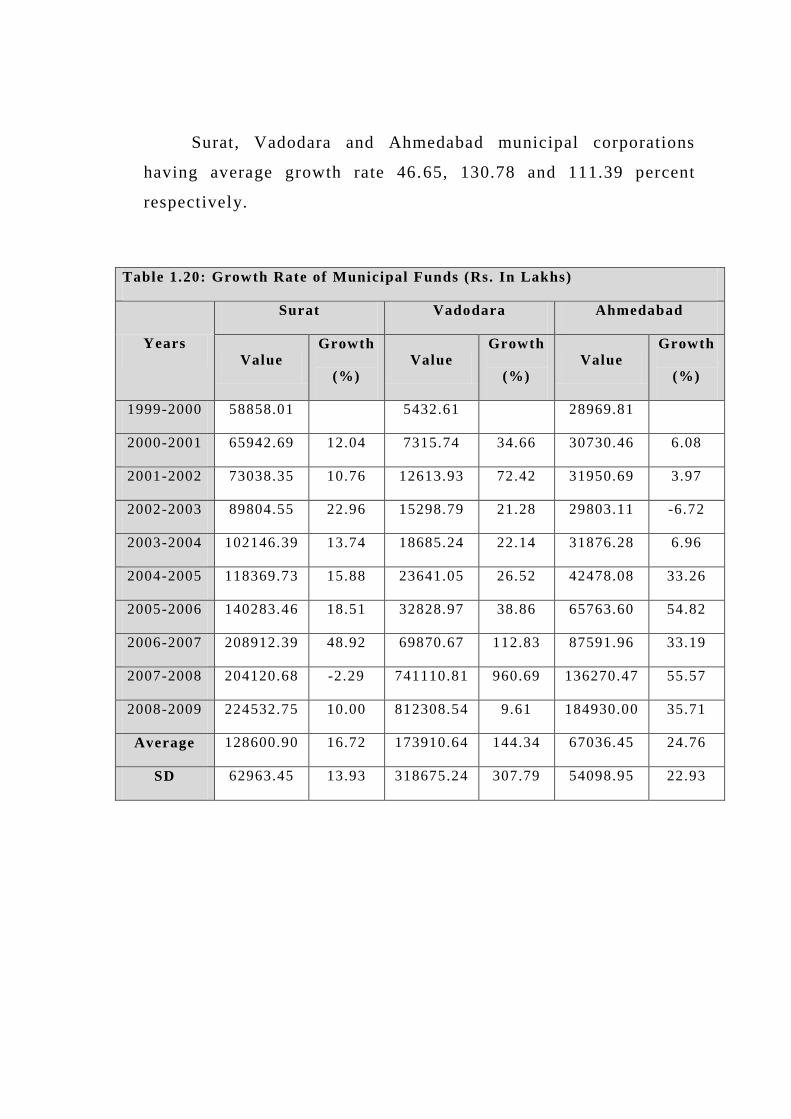

Table 1.20: Growth Rate of Municipal Funds (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 58858.01 5432.61 28969.81

2000-2001 65942.69 12.04 7315.74 34.66 30730.46 6.08

2001-2002 73038.35 10.76 12613.93 72.42 31950.69 3.97

2002-2003 89804.55 22.96 15298.79 21.28 29803.11 -6.72

2003-2004 102146.39 13.74 18685.24 22.14 31876.28 6.96

2004-2005 118369.73 15.88 23641.05 26.52 42478.08 33.26

2005-2006 140283.46 18.51 32828.97 38.86 65763.60 54.82

2006-2007 208912.39 48.92 69870.67 112.83 87591.96 33.19

2007-2008 204120.68 -2.29 741110.81 960.69 136270.47 55.57

2008-2009 224532.75 10.00 812308.54 9.61 184930.00 35.71

Average 128600.90 16.72 173910.64 144.34 67036.45 24.76

SD 62963.45 13.93 318675.24 307.79 54098.95 22.93

Table shows the growth rate of Municipal Funds for the

period from 1999-2000 to 2008-2009.

Growth rate varies from -2.29 percent to 48.92 percent in

Surat municipal corporations in the year 2007-2008 and 2006-2007

respectively.

Growth rate varies from 9.61 percent to 960.69 percent in

Vadodara municipal corporations in the year 2008 -2009 and 2007-

2008 respectively.

Growth rate varies from -6.72 percent to 55.57 percent in

Ahmedabad municipal corporations in the year 2002 -2003 and

2007-2008 respectively.

Chart 1.20: Growth Rate of Municipal Funds

-200.00

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 13.93, 307.79 and 22.93 percent

respectively.

Table 1.21: Growth Rate of Secured Loa n (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 12963.52 5469.64 31252.13

2000-2001 15633.89 20.60 4857.31 -11.20 26447.42 -15.37

2001-2002 17616.77 12.68 3964.71 -18.38 51702.61 95.49

2002-2003 14670.05 -16.73 2655.95 -33.01 51698.25 -0.01

2003-2004 11987.21 -18.29 2655.95 0.00 64490.17 24.74

2004-2005 2565.40 -78.60 785.07 -70.44 74492.20 15.51

2005-2006 2458.90 -4.15 1137.65 44.91 74494.48 0.00

2006-2007 2352.40 -4.33 949.50 -16.54 74494.67 0.00

2007-2008 1875.90 -20.26 1137.65 19.82 74494.67 0.00

2008-2009 2063.49 10.00 1262.59 10.98 74494.67 0.00

Average 8418.75 -11.01 2487.60 -8.21 59806.13 13.37

SD 6657.58 29.23 1737.06 33.00 18738.45 32.78

Table shows the growth ra te of Secured Loan for the period

from 1999-2000 to 2008-2009.

Growth rate varies from -78.60 percent to 20.60 percent in

Surat municipal corporations in the year 2004 -2005 and 2000-2001

respectively.

Growth rate varies from -70.44 percent to 44.91 percent in

Vadodara municipal corporations in the year 2004 -2005 and 2005-

2006 respectively.

Growth rate varies from -15.37 percent to 95.49 percent in

Ahmedabad municipal corporations in the year 2000 -2001 and

2001-2002 respectively.

Chart 1.21: Growth Rate of Secured Loan

-100.00

-80.00

-60.00

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

100.00

120.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 29.23, 33.00 and 32.78 percent

respectively.

Table 1.22: Growth Rate of Liability (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 98331.90 16357.00 172571.99

2000-2001 119851.63 21.88 21588.79 31.99 101380.24 -41.25

2001-2002 140536.76 17.26 25797.09 19.49 204363.38 101.58

2002-2003 164491.71 17.05 26742.22 3.66 123669.03 -39.49

2003-2004 189120.96 14.97 29924.84 11.90 159561.78 29.02

2004-2005 216746.46 14.61 34827.17 16.38 184629.45 15.71

2005-2006 253047.10 16.75 41494.36 19.14 222871.27 20.71

2006-2007 470629.66 85.99 77960.19 87.88 261631.76 17.39

2007-2008 460500.20 -2.15 769115.66 886.55 347780.70 32.93

2008-2009 506550.22 10.00 841376.80 9.40 456639.78 31.30

Average 261980.66 21.82 188518.41 120.71 223509.94 18.66

SD 156853.60 25.00 325931.86 288.28 107854.13 42.33

Table shows the growth rate of l iability for the period from

1999-2000 to 2008-2009.

Growth rate varies from -2.15 percent to 85.99 percent in

Surat municipal corporations in the year 2007 -2008 and 2006-2007

respectively.

Growth rate varies from 3.66 percent to 886.55 percent in

Vadodara municipal corporations in the year 2002 -2003 and 2007-

2008 respectively.

Growth rate varies from -39.49 percent to 101.58 percent in

Ahmedabad municipal corporations in the year 2002 -2003 and

2001-2002 respectively.

Chart 1.22: Growth Rate of Liability

-200.00

0.00

200.00

400.00

600.00

800.00

1000.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 25.00, 288.28 and 42.33 percent

respectively.

Table 1.23: Growth Rate of Capital work in progress (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%) Value

Growth

(%) Value

Growth

(%)

1999-2000 82749.97 8401.76 20324.28

2000-2001 103489.25 25.06 16047.02 91.00 15487.43 -23.80

2001-2002 119417.72 15.39 19513.54 21.60 40068.61 158.72

2002-2003 136058.21 13.93 22104.96 13.28 17308.66 -56.80

2003-2004 153328.27 12.69 23653.30 7.00 49009.57 183.15

2004-2005 170714.93 11.34 29592.13 25.11 55483.00 13.21

2005-2006 203277.73 19.07 36550.19 23.51 61295.38 10.48

2006-2007 94904.57 -53.31 3958.00 -89.17 73754.10 20.33

2007-2008 120643.96 27.12 13787.96 248.36 99736.66 35.23

2008-2009 132708.36 10.00 18453.21 33.84 115490.90 15.80

Average 131729.30 9.03 19206.21 41.61 54795.86 39.59

SD 36442.14 24.12 9580.67 90.38 34148.04 79.54

Table shows the growth rate of Capital work in progress for

the period from 1999-2000 to 2008-2009.

Growth rate varies from -53.31 percent to 27.12 percent in

Surat municipal corporations in the year 2006-2007 and 2007-2008

respectively.

Growth rate varies from -89.17 percent to 248.36 percent in

Vadodara municipal corporations in the year 2006 -2007 and 2007-

2008 respectively.

Growth rate varies from -56.80 percent to 183.15 percent in

Ahmedabad municipal corporations in the year 2002 -2003 and

2003-2004 respectively.

Chart 1.23: Growth Rate of Capital work in progress

-150.00

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

250.00

300.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 24.12, 90.38 and 79.54 percent

respectively.

Table 1.24: Growth Rate of Unsecured Loan (Rs. In Lakhs)

Years

Surat Vadodara Ahmedabad

Value Growth

(%)

Value Growth

(%)

Value Growth

(%)

1999-2000 7984.93 4362.57 8492.32

2000-2001 7951.57 -0.42 6973.31 59.84 8904.92 4.86

2001-2002 8956.78 12.64 7859.50 12.71 88552.96 894.43

2002-2003 13466.44 50.35 6126.36 -22.05 9696.43 -89.05

2003-2004 14166.11 5.20 5765.35 -5.89 9892.09 2.02

2004-2005 15576.98 9.96 3674.37 -36.27 10804.63 9.22

2005-2006 17408.25 11.76 183.03 -95.02 11525.48 6.67

2006-2007 21716.98 24.75 591.12 222.96 12558.23 8.96

2007-2008 0.00 -100.00 183.03 -69.04 14430.83 14.91

2008-2009 0.00 - 186.87 2.10 17825.26 23.52

Average 10722.80 1.78 3590.55 7.71 19268.31 97.28

SD 7124.03 43.99 3077.41 92.57 24507.40 300.78

Table shows the growth rate of Unsecured Loan for the

period from 1999-2000 to 2008-2009.

Growth rate varies from -100.00 percent to 50.35 percent in

Surat municipal corporations in the year 2007 -2008 and 2002-2003

respectively.

Growth rate varies from -95.02 percent to 222.96 percent in

Vadodara municipal corporations in the year 2005 -2006 and 2006-

2007 respectively.

Growth rate varies from -89.05 percent to 894.43 percent in

Ahmedabad municipal corporations in the year 2002 -2003 and

2001-2002 respectively.

Chart 1.24: Growth Rate of Unsecured Loan

-200.00

0.00

200.00

400.00

600.00

800.00

1000.00

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Years

Gro

wth

Rate

Surat Vadodara Ahmedabad

Surat, Vadodara and Ahmedabad municipal corporations

having average growth rate 43.99, 92.57 and 300.78 percent

respectively.

5.3 Ratio Analysis

With rapid urbanization and the pressure on urban areas for

service delivery, the role of urban local governments is

undoubtedly becoming important and, here, their financial

capacity can hold the key. At the same time, there are several

issues in urban governance that need to be addressed yet.

Delegation of decision making powers to urban local bodies

(ULBs), which are traditionally considered as a part of the system

of State government and acting on behalf of it, is one of them. The

constitutional mechanisms like inter -governmental fiscal transfers

were an attempt to reduce the ground. It has become imperative

now to understand the financial position of ULBs in order to move

forward with the new means of fund flow. Performing cross -

sectional analysis of the finances of Surat, Vadodara and

Ahmedabad Municipal Corporations in terms of their financial

base and its adequacy vis-à-vis norms, and their revenue and

expenditure performance. Using certain ratios, the relative

performance of municipalities on decentralization and dependency

measures was also assessed. The implications to the finances of

ULBs, in terms of raising resources, improv ing inter-governmental

transfers and charting new mechanisms are also discussed.

Revenue performance depend upon the ability of

municipality to generate revenue depends upon an array of factors:

(i) the level of economic activity in the region; (ii) fisc al powers

delegated to local government; (iii) tax efforts of municipal

government itself; and (iv) transfers out of sharable pool of

revenue by the state government to local government. The revenue

performance of the municipality/ Municipal Corporation ca n be

gauged by computing following two groups of indicators:

An Expenditure performance depend upon the level of

expenditure is, to some extent, reflective of the level of services

rendered by an urban local body. While the trend in per capita

expenditure would provide first approximation of the level of

services rendered by a municipal government, a further

segregation into discretionary and non-discretionary components,

relative share of revenue and capital expenditure, share of

establishment/ administra tive/ wages salaries as a proportion of

total/ revenue expenditure would reveal the quality of expenditure

and ability of the local bodies to meet is stated objectives.

Achieving a good proportion of own revenue to total revenue

receipts is one way of establishing creditworthiness, and a greater

share of tax revenue in it is desirable as it is a reliable revenue

source.

Apart from the measures of revenue growth and composition,

the revenue performance of Municipal Corporations can be gauged

through decentralization and dependency. Decentralization

measure is defined as the proportion of shared tax in the tax

revenue, which underscores the importance of share revenue as

opposed to own revenue. The dependency measure is the

proportion of total grants in a id in total expenditure.

The level and structure of expenditure has some major

implications to the finances of the Municipal Corporations. The

revenue expenditure, comprising expenditures on establishment

(staff salaries and administration) and maintenance, assumes

importance, as it relates to the provision of civic services and their

maintenance.

The expenditure structure of municipal corporations also

throws some lights on the relative importance assigned to each

component in the total expenditure and it has bearing on the

financial position and service delivery.

Various ratios has been calculated on the basis of various

financial terms using the data for the duration of ten years i.e.

from 1999-2000 to 2008-2009.

Following are the ratios for three Municipals Corporations

i.e. Surat, Vadodara and Ahmedabad, listed below:

1. Year wise Per Capita Income, Expenditure Ratio

2. Ratio Percentage of Financial Expense by Loan

(Secured+Unsecured)

3. Ratio Percentage of Expenditure by Income

4. Ratio Percentage of Establishment Expenditure by total

Revenue Income

5. Ratio Percentage of Administrative Expense by total

Revenue Income

6. Ratio Percentage of Repair & Maintains Expense by Total

Revenue Income

7. Ratio Percentage of Direct Expense by Total Revenue

Income

8. Ratio Percentage of Financial Expense by Total Revenue

Income

9. Ratio Percentage of Other Expense by Total Revenue

Income

10. Ratio Percentage of Income over Expenditure by Total

Revenue Income

11. Ratio Percentage of Income over Expenditure by

Municipal Fund & Reserve & Surplus

12. Ratio Percentage of Salary, Wages & allowances by Total

Income

13. Ratio Percentage of Salary, Wages & allowances by

Establishment Expenditure

14. Ratio Percentage of Direct Expenditure for Service &

Programs by Total Income

15. Ratio Percentage of Terminal Benefits by Establishment

Expenditure

16. Ratio Percentage of Octrio & Toll by Income from Tax

17. Ratio Percentage of Property Tax & Toll by Income from

Tax

18. Ratio Percentage of Other direct Tax & Toll by Income

from Tax

Table 2.0: Year wise Per Capita Income, Expenditur e Ratio for Surat, Vadodara and Ahmedabad

Year

Per Capita Income (in Rs.) Per Capita Expenditure (in Rs.) Ratio (Income over Expenditure)

Surat Vadodara Ahmedabad Surat Vadodara Ahmedabad Surat Vadodara Ahmedabad

2000 1659.53 1542.34 1644.62 1035.21 1436.34 1257.88 1.60 1.07 1.31

2001 1644.98 1609.91 1598.21 944.84 1400.54 1360.72 1.74 1.15 1.17

2002 1592.88 1493.07 1563.55 895.51 1371.28 1312.94 1.78 1.09 1.19

2003 1767.67 1587.47 1654.35 855.30 1391.24 1287.83 2.07 1.14 1.28

2004 1768.88 1592.90 1789.15 839.40 1380.67 1253.03 2.11 1.15 1.43

2005 1933.16 1861.75 2036.08 822.36 1389.74 1295.65 2.35 1.34 1.57

2006 1958.28 1908.20 2227.78 837.89 1404.56 1365.09 2.34 1.36 1.63

2007 2177.40 2219.42 2752.07 947.28 1858.36 1699.63 2.30 1.19 1.62

2008 2270.29 2843.74 3318.78 1033.41 1900.68 1862.57 2.20 1.50 1.78

2009 2454.86 3547.57 3398.72 1156.35 2365.20 1868.82 2.12 1.50 1.82

Average 1922.79 2020.64 2198.33 936.76 1589.86 1456.42 2.06 1.25 1.48

SD 293.09 677.64 712.05 109.60 339.06 251.07 0.27 0.16 0.24

Table(2.0) indicate the percentage ratio of Per Capita Income

over Expenditure. To calculate the per capita income and

expenditure projected population has been calculated using the

exponential growth rate and census population data for 1991 and

2001 for Surat, Vadodara and Ahmedabad.

Looking to the ratio percentage, for Surat Municipal

Corporations percentage varies from 1.60 percent in the year 2000

to 2.35 percent in the year 2005. Average percentage of this ratio

is 2.06 for define period. Also per capita income and expenditure

is Rs. 1922.79 and Rs. 936.76 respectively.

Looking to the ratio percentage, for Vadodara Municipal

Corporations percentage varies from 1.07 percent in the year 2000

to 1.50 percent in the year 2008 and 2009. Av erage percentage of

this ratio is 1.25 for define period. Also per capita income and

expenditure is Rs. 2020.64 and Rs. 1589.86 respectively.

Looking to the ratio percentage, for Ahmedabad Municipal

Corporations percent varies from 1.17 percent in the yea r 2001 to

1.82 percentage in the year 2009. Average percentage of this ratio

is 1.48 for define period. Also per capita income and expenditure

is Rs. 2198.33 and Rs. 1456.42 respectively.

Table 2.1: Ratio Percentage of Financial Expense by Loan (Secured+ Unsecured) for all three cities (In Rs. Lakhs)

Years

Surat Vadodara Ahmedabad

Financial

Expense

Secured

loan &

Unsecured

loan

Ratio

%

Financial

Expense

Secured

loan &

Unsecured

loan

Ratio

%

Financial

Expense

Secured

loan &

Unsecured

loan

Ratio

%

1999-2000 1905.05 20948.44 9.09 1289.06 9832.21 13.11 11554.27 111744.45 10.34

2000-2001 1833.60 23585.47 7.77 1449.71 11830.62 12.25 13421.35 35352.34 37.96

2001-2002 2145.90 26573.55 8.08 1657.79 11824.21 14.02 13243.50 140255.58 9.44

2002-2003 2051.00 28136.49 7.29 1401.42 8782.31 15.96 12672.10 61394.68 20.64

2003-2004 1734.00 26153.32 6.63 1044.96 8421.30 12.41 12431.97 74382.26 16.71

2004-2005 738.83 18142.38 4.07 615.52 4459.44 13.80 13565.63 85296.83 15.90

2005-2006 465.32 19867.15 2.34 328.91 1320.69 24.90 14588.88 86019.96 16.96

2006-2007 485.80 24069.38 2.02 287.83 1540.62 18.68 14519.02 87052.90 16.68

2007-2008 494.00 1875.90 26.33 74.70 1320.69 5.66 21284.39 88925.50 23.94

2008-2009 424.00 2063.49 20.55 95.47 1449.46 6.59 23931.91 92319.93 25.92

Average 1227.75 19141.56 9.42 824.54 6078.15 13.74 15121.30 86274.44 19.45

SD 757.05 9567.85 7.89 610.42 4508.08 5.53 4096.71 27811.62 8.32

Table(2.1) indicate the percentage ratio of financial charges to

Loan including secured and unsecured loan both. To under stand

the variation of this percentage ratio ten years value of financial

expense and loan amount has been taken for the periods 1999 -2000

to 2008-2009.

Looking to the ratio percentage, for Surat Municipal

Corporations percentage varies from 2.02 percentage (2006-2007)

to 26.33 percentage (2007-2008) on loan amount. The ratio pattern

indicates that on an average Surat Municipal Corporation paid

9.42 percentages as financial charges.

Chart 2.1: Ratio Percentage of Financial Expense by Loan (Secured+Unsecured)

for all three cities

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

1999-

2000

2000-

2001

2001-

2002

2002-

2003

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

2008-

2009

Years

Ra

tio

(%

)

Surat Vadodara Ahmedabad

For Vadodara Municipal Corporations the above percentage

ratio is varies from 5.66 percentage (2007-2008) to 24.90

percentages (2005-2006). Vadodara Municipal Corporations paid

on an average 13.74 percentage financial charges on loan

amount.For Ahmedabad Municipal Corporations the above

percentages ratio is varies from 9.44 percentage (2001 -2002) to

37.96 percentages (2000-2001). Ahmedabad Municipal

Corporations paid on an average 19.45 percentage financial

charges on loan amount.

Table 2.2: Ratio Percentage of Expenditure by Income for all t hree cities (In Rs. Lakhs)

Years

Surat Vadodara Ahmedabad

Expenditure Income Ratio

% Expenditure Income

Ratio

% Expenditure Income

Ratio

%

1999-2000 28234.20 36287.92 77.81 18268.41 16176.26 112.93 44198.29 46711.45 94.62

2000-2001 29348.74 38715.02 75.81 18294.21 17970.21 101.80 48928.17 46054.70 106.24

2001-2002 29977.71 40168.91 74.63 18395.89 17196.69 106.97 48179.07 47346.56 101.76

2002-2003 30520.69 47593.32 64.13 19167.73 18659.87 102.72 48941.80 51980.45 94.15

2003-2004 32697.98 51242.63 63.81 19535.85 19969.28 97.83 48278.18 59116.07 81.67

2004-2005 34568.56 60352.46 57.28 20195.36 24705.54 81.74 50922.46 69255.75 73.53

2005-2006 37827.00 65496.03 57.75 20962.12 25940.38 80.81 55053.59 79360.17 69.37

2006-2007 45392.68 78746.90 57.64 28483.90 30518.33 93.33 70263.58 101317.54 69.35

2007-2008 51803.74 87984.51 58.88 29919.44 31175.19 95.97 78820.19 124855.62 63.13

2008-2009 62736.00 101948.90 61.54 38237.29 39941.57 95.73 81051.60 128687.25 62.98

Average 38310.73 60853.66 64.93 23146.02 24225.33 96.99 57463.69 75468.56 81.68

SD 11482.00 22500.70 8.11 6785.19 7749.40 10.12 13812.03 32137.40 16.31

Table(2.2) indicate the percentage ratio of Expenditure by

income. To under stand the variation of this percentage ratio ten

years value of expenditure and income amount has been taken for

the periods 1999-2000 to 2008-2009.

Looking to the ratio percentage, for Surat Municipal

Corporations percentage varies from 57.28 percentage (2004 -2005)

to 77.81 percentage (1999-2000) on income amount. The average

of the ratio is found to be 64.93 percent during the ten years of

period.

Chart 2.2: Ratio Percentage of Expenditure by Income for all three cities

0.00

20.00

40.00

60.00

80.00

100.00

120.00

1999-

2000

2000-

2001

2001-

2002

2002-

2003

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

2008-

2009

Years

Ra

tio

(%

)

Surat Vadodara Ahmedabad

For Vadodara Municipal Corporations percentage varies from

80.81 percentage (2005-2006) to 112.93 percentage (1999-2000)

on income amount. The average of the ratio is found to be 96.99

percent during the ten years of period.

For Ahmedabad Municipal Corporations percentage varies

from 62.98 percentage (2008-2009) to 106.24 percentage (2000-

2001) on income amount. The average of the ratio is found to be

81.68 percent during the ten years of period.

Table 2.3: Ratio Percentage of Establishment Expenditure by total Revenue Income for all three cities (In Rs. Lakhs)

Years

Surat Vadodara Ahmedabad

Expenditure Income Ratio

% Expenditure Income

Ratio

% Expenditure Income

Ratio

%

1999-2000 15507.64 37691.59 41.14 10098.12 19616.66 51.48 28540.52 56611.80 50.41

2000-2001 14150.24 40036.14 35.34 9392.68 21029.12 44.67 31395.10 56258.44 55.81

2001-2002 14850.10 41543.76 35.75 9470.13 20029.64 47.28 30389.77 56283.24 53.99

2002-2003 15800.40 49403.01 31.98 9793.56 21871.34 44.78 30548.59 60898.52 50.16

2003-2004 16759.23 52976.51 31.64 10093.70 22538.82 44.78 31222.08 67350.15 46.36

2004-2005 17693.26 62041.62 28.52 10339.06 27054.54 38.22 30936.31 78379.07 39.47

2005-2006 19270.66 67347.26 28.61 11289.24 28478.57 39.64 32924.35 87698.00 37.54

2006-2007 21638.98 80244.69 26.97 14927.19 34018.04 43.88 46285.60 110787.53 41.78

2007-2008 26366.01 89658.00 29.41 16265.56 44764.54 36.34 47329.18 136622.66 34.64

2008-2009 32126.00 103888.00 30.92 20787.52 57352.20 36.25 44917.94 143077.71 31.39

Average 19416.25 62483.06 32.03 12245.68 29675.35 42.73 35448.94 85396.71 44.16

SD 5790.41 22633.74 4.29 3829.16 12479.58 4.98 7502.65 33502.03 8.42

Table(2.3) indicate the percentage ratio of Establishment

Expenditure by Total Revenue Income. To under stand the

variation of this percentage ratio ten years value of establishment

expenditure and total revenue income amount has been taken for

the periods 1999-2000 to 2008-2009.

Looking to the ratio percentage, for Surat Municipal

Corporations percentage varies from 28.52 percentage (2004 -2005)

to 41.14 percentage (1999-2000) on total revenue income amount.

The average of the ratio is found to be 32.03 percent d uring the

ten years of period.

Chart 2.3: Ratio Percentage of Establishment Expenditure by total Revenue

Income for all three cities

0.00

10.00

20.00

30.00

40.00

50.00

60.00

1999-

2000

2000-

2001

2001-

2002

2002-

2003

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

2008-

2009

Years

Ra

tio

(%

)

Surat Vadodara Ahmedabad

For Vadodara Municipal Corporations percentage varies from

36.25 percentage (2008-2009) to 51.48 percentage (1999-2000) on

total revenue income amount. The average of the ratio is found to

be 42.73 percent during the ten yea rs of period.

For Ahmedabad Municipal Corporations percentage varies

from 31.39 percentage (2008-2009) to 55.81 percentage (2000-

2001) on total revenue income amount. The average of the ratio is

found to be 44.16 percent during the ten years of period.

Table 2.4: Ratio Percentage of Administrative Expense by total Revenue Income for all three cities (In Rs. Lakhs)

Years

Surat Vadodara Ahmedabad

Ad.

Expense Income

Ratio

%

Ad.

Expense Income

Ratio

%

Ad.

Expense Income

Ratio

%

1999-2000 4722.18 37691.59 12.53 256.08 19616.66 1.31 899.04 56611.80 1.59

2000-2001 6352.90 40036.14 15.87 322.03 21029.12 1.53 1029.63 56258.44 1.83

2001-2002 6622.05 41543.76 15.94 274.80 20029.64 1.37 917.14 56283.24 1.63

2002-2003 6616.59 49403.01 13.39 175.80 21871.34 0.80 1535.37 60898.52 2.52

2003-2004 7558.60 52976.51 14.27 184.66 22538.82 0.82 1109.68 67350.15 1.65

2004-2005 8176.12 62041.62 13.18 132.42 27054.54 0.49 1046.49 78379.07 1.34

2005-2006 9010.93 67347.26 13.38 171.74 28478.57 0.60 1315.89 87698.00 1.50

2006-2007 10482.07 80244.69 13.06 668.03 34018.04 1.96 1843.22 110787.53 1.66

2007-2008 10992.21 89658.00 12.26 998.08 44764.54 2.23 2144.85 136622.66 1.57

2008-2009 13800.00 103888.00 13.28 1275.56 57352.20 2.22 2378.69 143077.71 1.66

Average 8433.37 62483.06 13.72 445.92 29675.35 1.33 1422.00 85396.71 1.69

SD 2695.54 22633.74 1.27 399.70 12479.58 0.65 533.35 33502.03 0.32

Table(2.4) indicate the percentage ratio of Administrative

Expenditure by Total Revenue Income. To under stand the

variation of this percentage ratio ten years value of administrative

expenditure and total revenue income amount has been taken for

the periods 1999-2000 to 2008-2009.

Looking to the ratio percentage, for Surat Municipal

Corporations percentage varies from 12.53 percentage (1999-2000]

to 15.94 percentage (2001-2002) on total revenue income amount.

The average of the ratio is found to be 13.72 percent during the

ten years of period.

Chart 2.4: Ratio Percentage of Administrative Expense by total Revenue Income

for all three cities

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

1999-

2000

2000-

2001

2001-

2002

2002-

2003

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

2008-

2009

Years

Rati

o (

%)

Surat Vadodara Ahmedabad

For Vadodara Municipal Corporations percentage varies from

0.49 percentage (2004-2005) to 2.23 percentage (2007-2008) on

total revenue income amount. The average of the ratio is found to

be 1.33 percent during the ten years of period.

For Ahmedabad Municipal Corporations percentage varies

from 1.34 percentage (2004-2005) to 2.52 percentage (2002-2003)

on total revenue income amount. The average of the ratio is found

to be 1.69 percent during the ten years of period.

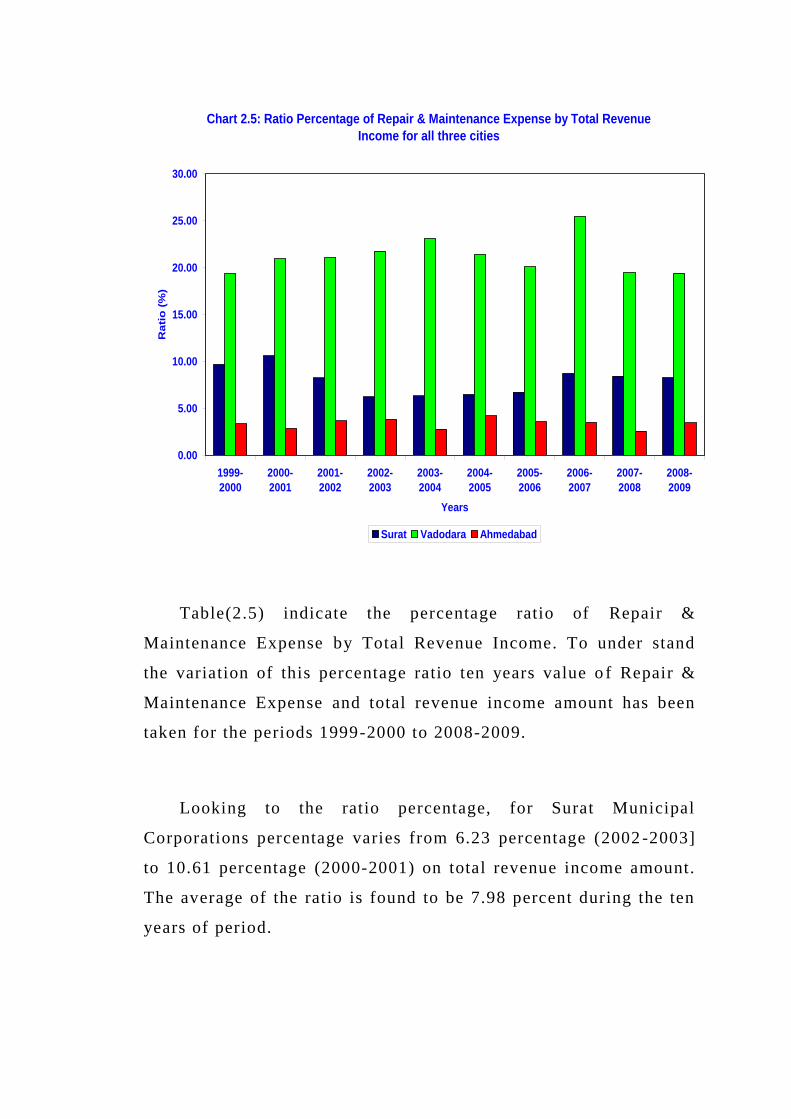

Table 2.5: Ratio Percentage of Repair & Maintenance Expense by Total Revenue Income for all three cities (In Rs.

Lakhs)

Years

Surat Vadodara Ahmedabad

Repair &

Maintenance Income

Ratio

%

Repair &

Maintenance Income

Ratio

%

Repair &

Maintenance Income

Ratio

%

1999-2000 3652.15 37691.59 9.69 3800.46 19616.66 19.37 1905.96 56611.80 3.37

2000-2001 4249.63 40036.14 10.61 4405.69 21029.12 20.95 1604.40 56258.44 2.85

2001-2002 3427.02 41543.76 8.25 4218.59 20029.64 21.06 2070.77 56283.24 3.68

2002-2003 3075.35 49403.01 6.23 4763.58 21871.34 21.78 2331.26 60898.52 3.83

2003-2004 3353.20 52976.51 6.33 5208.53 22538.82 23.11 1888.42 67350.15 2.80

2004-2005 4017.97 62041.62 6.48 5796.71 27054.54 21.43 3308.16 78379.07 4.22

2005-2006 4540.00 67347.26 6.74 5725.93 28478.57 20.11 3149.98 87698.00 3.59

2006-2007 7006.57 80244.69 8.73 8668.78 34018.04 25.48 3875.61 110787.53 3.50

2007-2008 7570.52 89658.00 8.44 8715.69 44764.54 19.47 3548.26 136622.66 2.60

2008-2009 8604.00 103888.00 8.28 11138.72 57352.20 19.42 4958.78 143077.71 3.47

Average 4949.64 62483.06 7.98 6244.27 29675.35 21.22 2864.16 85396.71 3.39

SD 2001.21 22633.74 1.51 2429.72 12479.58 1.92 1081.56 33502.03 0.50

Table(2.5) indicate the percentage ratio of Repair &

Maintenance Expense by Total Revenue Income. To under stand

the variation of this percentage ratio ten years value o f Repair &

Maintenance Expense and total revenue income amount has been

taken for the periods 1999-2000 to 2008-2009.

Looking to the ratio percentage, for Surat Municipal

Corporations percentage varies from 6.23 percentage (2002 -2003]

to 10.61 percentage (2000-2001) on total revenue income amount.

The average of the ratio is found to be 7.98 percent during the ten

years of period.

Chart 2.5: Ratio Percentage of Repair & Maintenance Expense by Total Revenue

Income for all three cities

0.00

5.00

10.00

15.00

20.00

25.00

30.00

1999-

2000

2000-

2001

2001-

2002

2002-

2003

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

2008-

2009

Years

Ra

tio

(%

)

Surat Vadodara Ahmedabad

For Vadodara Municipal Corporations percentage varies from