Embed Size (px)

Citation preview

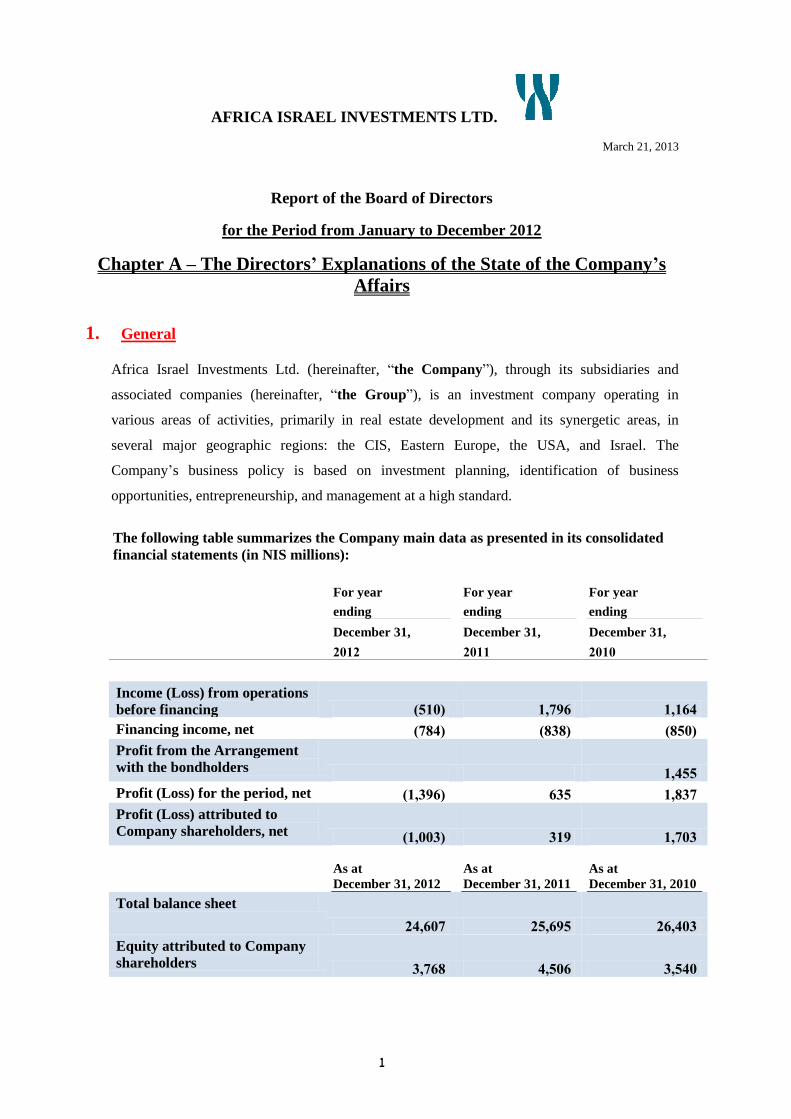

1

AFRICA ISRAEL INVESTMENTS LTD.

March 21, 2013

Report of the Board of Directors

for the Period from January to December 2012

Chapter A – The Directors’ Explanations of the State of the Company’s

Affairs

1. General

Africa Israel Investments Ltd. (hereinafter, ―the Company‖), through its subsidiaries and

associated companies (hereinafter, ―the Group‖), is an investment company operating in

various areas of activities, primarily in real estate development and its synergetic areas, in

several major geographic regions: the CIS, Eastern Europe, the USA, and Israel. The

Company’s business policy is based on investment planning, identification of business

opportunities, entrepreneurship, and management at a high standard.

The following table summarizes the Company main data as presented in its consolidated

financial statements (in NIS millions):

For year For year For year

ending ending ending

December 31, December 31, December 31,

1021 1022 1020

Income (Loss) from operations

before financing (020) 29241 29211

Financing income, net (231) (333) (300)

Profit from the Arrangement

with the bondholders 29100

Profit (Loss) for the period, net (29341) 130 29332

Profit (Loss) attributed to

Company shareholders, net (29003) 324 29203

As at

December 31, 2012

As at

December 31, 2011

As at

December 31, 2010

Total balance sheet

119102 109140 119103

Equity attributed to Company

shareholders 39213 19001 39010

2

The following revaluations/depreciations were recorded in 2012:

In 2012, the Company recorded net depreciation of NIS 1,108 million (of which, NIS 21 million

in respect of appreciation recorded in the fourth quarter of 2012). The depreciations stemmed

from the following reasons:

(a) Decline in fair value of investment property under construction in the amount of NIS 835

million (of which, NIS 40 million recorded in the fourth quarter of 2012), stemming mainly

from a decline in the fair value of four AFI Development projects involving real estate

development and rental properties in the CIS due to changes in municipal planning policies and

development policies of Moscow municipality;

(b) Revaluation of a provision for impairment of inventory of building and land, especially in

AFI Development, in the amount of NIS 266 million (NIS 14 million in respect of recovered

value recorded in the fourth quarter of 2012), stemming mainly from a depreciation of land in an

AFI Development projects resulting from a liquidation suit filed against the project’s primary

investor;

(c) Net decline in the fair value of investment property in the amount of NIS 21 million (of

which, a depreciation in the amount of NIS 20 million was recorded in the fourth quarter of

2012);

(d) Revaluation gains from associated companies item in the amount of NIS 143 million of

which, NIS 98 was recorded as revaluation gains in the fourth quarter of 2012), stemming

mainly from the revaluation of the Times Building in the USA and revaluation of investment

property in AFI Development’s Four Winds project (a property whose sale was concluded after

the date of the statement of financial position);

(e) Depreciation of associated companies, which was recorded in other expenses, in the amount

of NIS 128 million (of which a decline in value in the amount of NIS 31 million was recorded in

the fourth quarter of 2012), stemming mainly from a depreciation of Africa Properties in respect

of an associated company in Poland in the amount of NIS 97 million in the third quarter of 2012.

The following revaluations/depreciations were recorded in 2011:

In 2011, the Company recorded a net appreciation of NIS 1,262 million (of which, revaluation

of NIS 376 million was recorded in the fourth quarter of 2011). The appreciation stemmed

mainly from the following reasons:

(a) Revaluation in respect of investment property in the amount of NIS 856 million (of which,

NIS 166 million was recorded in the fourth quarter of 2011);

(B) Revaluation of investment property under construction of NIS 65 million (of which, NIS 74

million was recorded in the fourth quarter of 2011);

(c) Revaluation gains from associated companies in the amount of NIS 290 million (of which,

NIS 117 million were recorded as revaluation gains in the fourth quarter of 2012);

(d) Elimination of a provision for impairment mainly in a residential project in the United States,

in the amount of NIS 82 million (of which NIS 21 million was recorded in the fourth quarter of

3

2011) less a deduction for impairment of NIS 20 million stemming from a provision recorded

for loss on an investment in a jointly controlled company presented at book value and recorded

in the fourth quarter of 2011.

2. The Group’s Segments of Operation

Through its subsidiaries and associated companies (above and hereinafter, ―the Group‖), the

Company is engaged in holdings and investments in a variety of areas in and outside of Israel.

The Company’s main operations are the development and construction of real estate projects

designated for residential, industrial, office, and commercial uses, where the Company focuses

on the rental and operation of non-residential projects after construction has been completed.

The Group operates mainly in the CIS (mainly in Russia), Eastern Europe, the USA, and Israel.

The Company also has operations in areas that are synergetic with its real estate operations,

such as operations in the sector of construction contracting and infrastructure contracting, and

operations in the steel (in Israel) and ceramics sectors.

The Company has four publicly traded subsidiaries, and one publicly traded subsidiary listed on

the London Stock Exchange.

The Group has 10 activity sectors that are reported as primary operating segments in the

Company’s Financial Statements, as described below:

a. Real estate development in Israel;

b. Rental properties in Israel;

c. Development of real estate and rental properties in Europe – Central and Eastern Europe;

d. Development of real estate and rental properties in the USA;

e. Development of real estate and rental properties in the CIS;

f. Construction contracting;

g. Infrastructure contracting;

h. Steel in Israel;

i. Steel in Russia1;

j. Ceramics.

In addition to the segments of operation listed above, the Group operates in the hotel industry

and in the communications industry (Channel 9). These operations do not constitute a segment

of operations due to their limited scope. The Group performs various other activities through

associated companies:

1 Until December 6, 2012, the Group was also active in the steel industry in Russia. In view of the conclusion of Africa

Industries’ holdings (65%) in its subsidiary on December 6, 2012, as stated in Section 15.1(A) to the Description of the

Company’s Business, the steel sector in Russia is presented in the Company’s financial statements as at December 31, 2012

as a discontinued operation.

4

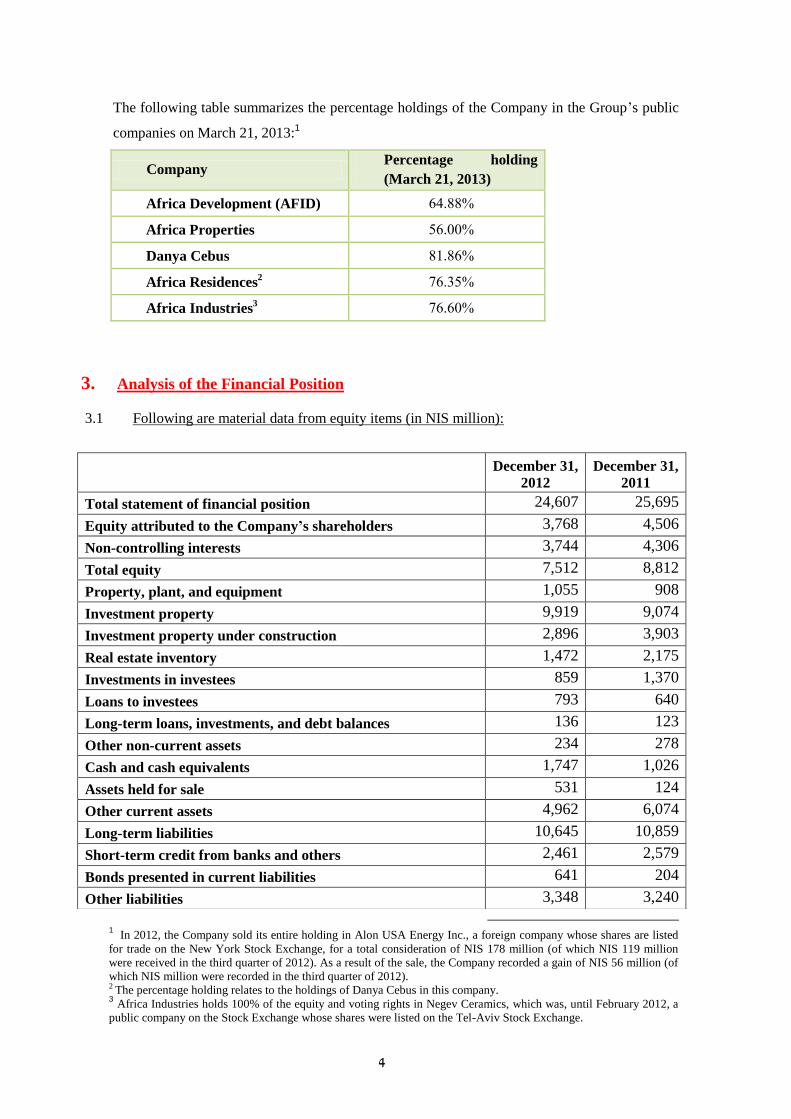

The following table summarizes the percentage holdings of the Company in the Group’s public

companies on March 21, 2013:1

Company Percentage holding

(March 21, 2013)

Africa Development (AFID) 68.44%

Africa Properties 66...%

Danya Cebus 48.46%

Africa Residences2 56.66%

Africa Industries3 56.6.%

3. Analysis of the Financial Position

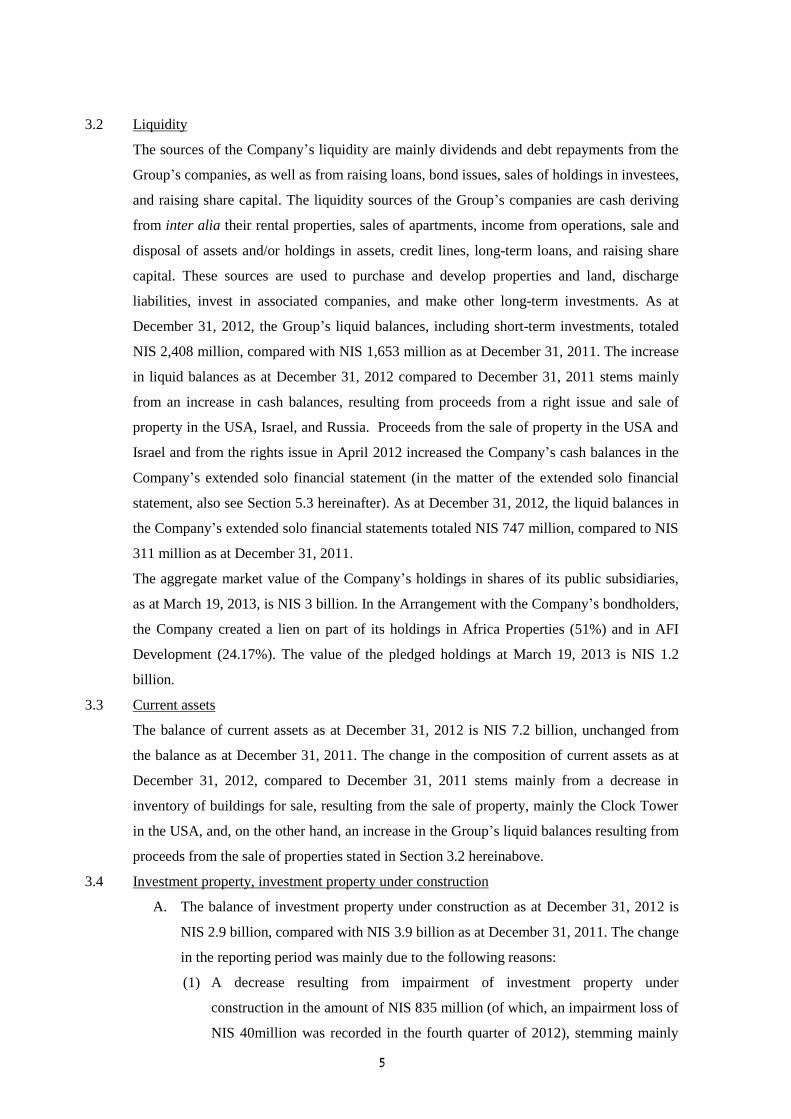

3.1 Following are material data from equity items (in NIS million):

1 In 2012, the Company sold its entire holding in Alon USA Energy Inc., a foreign company whose shares are listed

for trade on the New York Stock Exchange, for a total consideration of NIS 178 million (of which NIS 119 million

were received in the third quarter of 2012). As a result of the sale, the Company recorded a gain of NIS 56 million (of

which NIS million were recorded in the third quarter of 2012). 2

The percentage holding relates to the holdings of Danya Cebus in this company. 3 Africa Industries holds 100% of the equity and voting rights in Negev Ceramics, which was, until February 2012, a

public company on the Stock Exchange whose shares were listed on the Tel-Aviv Stock Exchange.

December 31,

2012

December 31,

2011

Total statement of financial position 24,607 25,695

Equity attributed to the Company’s shareholders 3,768 4,506

Non-controlling interests 3,744 4,306

Total equity 7,512 8,812

Property, plant, and equipment 1,055 908

Investment property 9,919 9,074

Investment property under construction 2,896 3,903

Real estate inventory 1,472 2,175

Investments in investees 859 1,370

Loans to investees 793 640

Long-term loans, investments, and debt balances 136 123

Other non-current assets 234 278

Cash and cash equivalents 1,747 1,026

Assets held for sale 531 124

Other current assets 4,962 6,074

Long-term liabilities 10,645 10,859

Short-term credit from banks and others 2,461 2,579

Bonds presented in current liabilities 641 204

Other liabilities 3,348 3,240

5

3.2 Liquidity

The sources of the Company’s liquidity are mainly dividends and debt repayments from the

Group’s companies, as well as from raising loans, bond issues, sales of holdings in investees,

and raising share capital. The liquidity sources of the Group’s companies are cash deriving

from inter alia their rental properties, sales of apartments, income from operations, sale and

disposal of assets and/or holdings in assets, credit lines, long-term loans, and raising share

capital. These sources are used to purchase and develop properties and land, discharge

liabilities, invest in associated companies, and make other long-term investments. As at

December 31, 2012, the Group’s liquid balances, including short-term investments, totaled

NIS 2,408 million, compared with NIS 1,653 million as at December 31, 2011. The increase

in liquid balances as at December 31, 2012 compared to December 31, 2011 stems mainly

from an increase in cash balances, resulting from proceeds from a right issue and sale of

property in the USA, Israel, and Russia. Proceeds from the sale of property in the USA and

Israel and from the rights issue in April 2012 increased the Company’s cash balances in the

Company’s extended solo financial statement (in the matter of the extended solo financial

statement, also see Section 5.3 hereinafter). As at December 31, 2012, the liquid balances in

the Company’s extended solo financial statements totaled NIS 747 million, compared to NIS

311 million as at December 31, 2011.

The aggregate market value of the Company’s holdings in shares of its public subsidiaries,

as at March 19, 2013, is NIS 3 billion. In the Arrangement with the Company’s bondholders,

the Company created a lien on part of its holdings in Africa Properties (51%) and in AFI

Development (24.17%). The value of the pledged holdings at March 19, 2013 is NIS 1.2

billion.

3.3 Current assets

The balance of current assets as at December 31, 2012 is NIS 7.2 billion, unchanged from

the balance as at December 31, 2011. The change in the composition of current assets as at

December 31, 2012, compared to December 31, 2011 stems mainly from a decrease in

inventory of buildings for sale, resulting from the sale of property, mainly the Clock Tower

in the USA, and, on the other hand, an increase in the Group’s liquid balances resulting from

proceeds from the sale of properties stated in Section 3.2 hereinabove.

3.4 Investment property, investment property under construction

A. The balance of investment property under construction as at December 31, 2012 is

NIS 2.9 billion, compared with NIS 3.9 billion as at December 31, 2011. The change

in the reporting period was mainly due to the following reasons:

(1) A decrease resulting from impairment of investment property under

construction in the amount of NIS 835 million (of which, an impairment loss of

NIS 40million was recorded in the fourth quarter of 2012), stemming mainly

6

from a decrease in AFI Development’s rights in four projects in Russia due to

changes in the municipal planning policy and development policy of Moscow

municipality. For additional details, also see Section 4.3.2 hereinafter.

(2) A decrease resulting from the first-time classification in the second quarter of

2012, of the Tverskaya Plaza II and Tverskaya Plaza Ib projects, from

investment property under construction to investment property, in the amount

of NIS 159 million in total. For additional information see Note 7(A)(2)(C) of

the Company’s Financial Statements as at December 31, 2012.

(3) A decrease following the first-time classification to investment property

performed by Africa Properties of an office building adjacent to the AFI Palace

Cotroceni mall in Bucharest, stage B of Classic 7 project in Prague, and the

Beit Psagot House project in Tel Aviv (following construction completion in

the reporting period), of a total amount of NIS 251 million;

(4) Increase following additional costs invested in 2012 in the amount of NIS 240

million, mainly in respect of AFI Europe’s projects and AFI Development’s

projects.

B. The balance of investment property as at December 31, 2012 totaled NIS 9.9 billion,

compared to NIS 9.1 billion as at December 31, 2011. The change from December

31, 2011 to December 31, 2012 stemmed mainly from the following reasons:

(1) A decrease due to impairment of investment property in the amount of NIS 21

million (of which, an impairment loss in the amount of NIS 20 million was

recorded in the fourth quarter of 2012).

(2) An increase due to the first-time classification, in the second quarter of 2012,

from investment property under construction to investment property of the

Tverskaya Plaza II and Tverskaya Plaza Ib projects in the total amount of NIS

159 million. For additional information see Note 7(A)(2)(B) of the Company’s

Financial Statements as at December 31, 2012.

(3) An increase following the first-time classification from investment property

under construction to investment property of an office building adjacent to the

AFI Palace Cotroceni mall in Bucharest, stage B of Classic 7 project in Prague,

and the Beit Psagot House project in Tel Aviv (following construction

completion in the reporting period), of a total amount of NIS 251 million.

(4) An increase following the first-time consolidation of real estate properties in

Germany owned by AFI Europe in the amount of NIS 480 million.

(5) An increase following the strengthening of the euro and the ruble relative to the

shekel in the reporting period in the amount of NIS 43 million.

C. Following is a geographic breakdown of the Group’s investment property and

investment property under construction as at December 31, 2012:

7

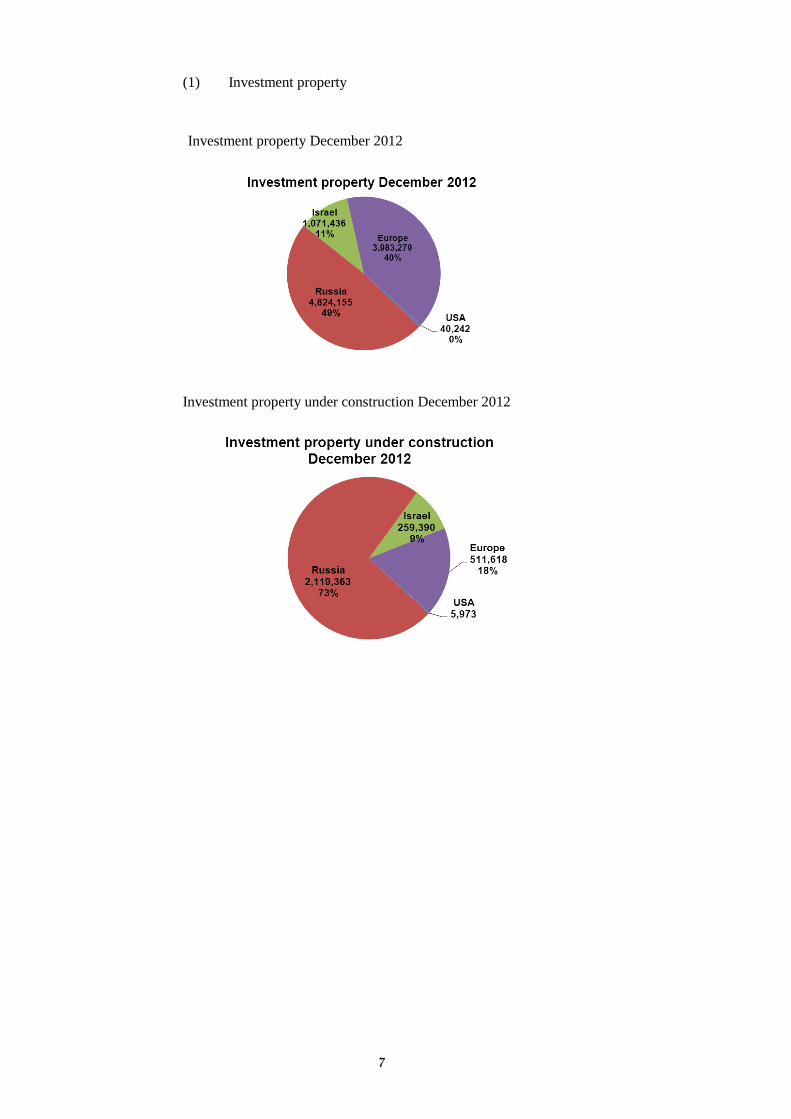

(1) Investment property

Investment property December 2012

Investment property under construction December 2012

8

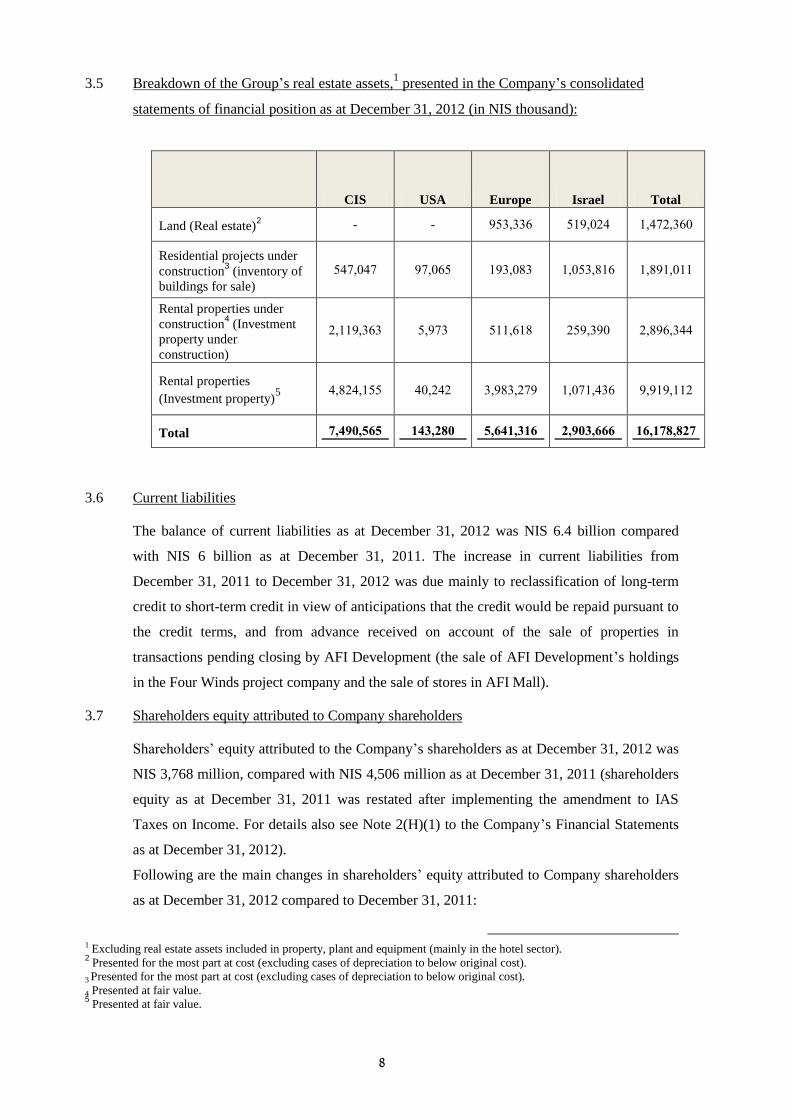

3.5 Breakdown of the Group’s real estate assets,1 presented in the Company’s consolidated

statements of financial position as at December 31, 2012 (in NIS thousand):

CIS USA Europe Israel Total

Land (Real estate)2 - - 666,666 686,.18 8,851,66.

Residential projects under

construction3 (inventory of

buildings for sale)

685,.85 65,.66 866,.46 8,.66,486 8,468,.88

Rental properties under

construction4 (Investment

property under

construction)

1,886,666 6,656 688,684 166,66. 1,466,688

Rental properties

(Investment property)5

8,418,866 8.,181 6,646,156 8,.58,866 6,686,881

Total 291409010 2139130 091129321 194039111 2192239312

3.6 Current liabilities

The balance of current liabilities as at December 31, 2012 was NIS 6.4 billion compared

with NIS 6 billion as at December 31, 2011. The increase in current liabilities from

December 31, 2011 to December 31, 2012 was due mainly to reclassification of long-term

credit to short-term credit in view of anticipations that the credit would be repaid pursuant to

the credit terms, and from advance received on account of the sale of properties in

transactions pending closing by AFI Development (the sale of AFI Development’s holdings

in the Four Winds project company and the sale of stores in AFI Mall).

3.7 Shareholders equity attributed to Company shareholders

Shareholders’ equity attributed to the Company’s shareholders as at December 31, 2012 was

NIS 3,768 million, compared with NIS 4,506 million as at December 31, 2011 (shareholders

equity as at December 31, 2011 was restated after implementing the amendment to IAS

Taxes on Income. For details also see Note 2(H)(1) to the Company’s Financial Statements

as at December 31, 2012).

Following are the main changes in shareholders’ equity attributed to Company shareholders

as at December 31, 2012 compared to December 31, 2011:

1 Excluding real estate assets included in property, plant and equipment (mainly in the hotel sector). 2 Presented for the most part at cost (excluding cases of depreciation to below original cost).

3 Presented for the most part at cost (excluding cases of depreciation to below original cost).

4 Presented at fair value. 5 Presented at fair value.

9

The Company’s loss in 2012 totaled NIS 1,003 million.

Increase of NIS 15 million in capital reserves from translation differences

(adjustments stemming from the translation of financial statements of foreign

operations).

Net proceeds of NIS 213 million from a rights issue the Company made in April

2012.

Increase in net capital reserves from transactions with non-controlling interests in the

amount of NIS 38 million, reflecting mainly the difference between the

consideration paid in respect of AFI Development shares and Danya Cebus shares

(for additional details see Note 6(C)(2)(3) to the Company’s Financial Statements as

at December 31, 2012) and the decrease in non-controlling interests.

Shareholders’ equity per share (including non-controlling interests) as at December 31, 2012

was NIS 51.17 compared with NIS 67.37 per share as at December 31, 2011.

Shareholders’ equity per share (excluding non-controlling interests) as at December 31, 2012

was NIS 25.62 compared with NIS 34.45 per share as at December 31, 2011.

3.8 Restatement of earnings (loss) per share:

The data on loss per share for the years 2011 and 2010 were restated in view of the rights

issue the Company made during the reporting period (for details also see Note 1(C)(2) to the

Company’s Financial Statements as at December 31, 2012) and due to the retrospective

implementation of an amendment to an accounting standard (for details also see Note

2(H)(1) to the Company’s Financial Statements as at December 31, 2012).

The effect of the restatement on the basic and diluted loss per share is as follows:

For year ended December 31, 2011

In NIS

As

previously

reported

Effect of the

restatement

retroactively

As reported in

these Financial

Statements

Basic earnings per share 2.52 0.01 2.53

Diluted earnings per share 2.52 - 2.52

For year ended December 31, 2010

In NIS

As

previously

reported

Effect of the

restatement

retroactively

As reported in

these Financial

Statements

Basic earnings per share 17.37 (0.15) 17.22

Diluted earnings per share 17.35 (0.15) 17.20

11

4. Results of Business Operations

4.1 Set forth below are significant items from the statement of income (in NIS millions):

For the year ended December 31

2012 2011 2010

Income from construction and real estate transactions 247 277 344

Sale of properties 77 102 (8)

Update of provision for decline in value of

inventory of land and buildings (266) 82 60

Increase (decrease) in fair value of investment

property under construction, net (835) 65 (20)

Increase in fair value of investment property, net (21) 856 221

Total income (loss) from real estate initiations (798) 1,382 597

Income from rental and operation of properties 518 406 332

Income from industry 135 184 126

Income (loss) from other activities (12) 1 (11)

Other income 71 107 287

Income from associated companies, net 81 155 367

Administrative and general (287) (326) (287)

Amortization of other assets and other expenses (218) (113) (247)

Operating income (loss) (510) 1,796 1,164

Financing income 361 272 1,729

Financing expenses (1,145) (1,110) (1,124)

Financing income (expenses), net (784) (838) 605

Taxes on income (73) (401) (152)

Income (loss ) from continuing operations (1,387) 557 1,617

Income (loss) from discontinued operations, after

taxes (29) 78 220

Income (loss) for the period (1,396) 635 1,837

Attributable to:

The equity holders of the Company (1,003) 319 1,703

Non-controlling interests (393) 316 134

The Company’s results may experience wide fluctuations between different reporting

periods, mainly as a result of the timing of realizations made by the Company and the Group

companies, from time to time, the timing of revaluations and write-downs of investment

property and investment property under construction, and changes in the financing expenses

(net) incurred by the Company and the Group companies, the scope of which is affected by

the amount of the net debt, the debt’s linkage channels and the net monetary assets and rate

of change in the Consumer Price Index and the exchange rates of the various foreign

currencies against the shekel in the periods reported.

11

8.1 Income (loss) from real estate development

8.1.8 The income (losses) from real estate development derive from the following sources:

A. Income (losses) from sale of residential units.

B. Sale of properties.

C. Income (losses) from contracting work.

D. Update of the provision for decline in value of the inventory of land and buildings.

E. Income (losses) from increase (decrease) in the fair value of investment property, net.

F. Income (losses) from increase (decrease) in the fair value of investment property under

construction, net.

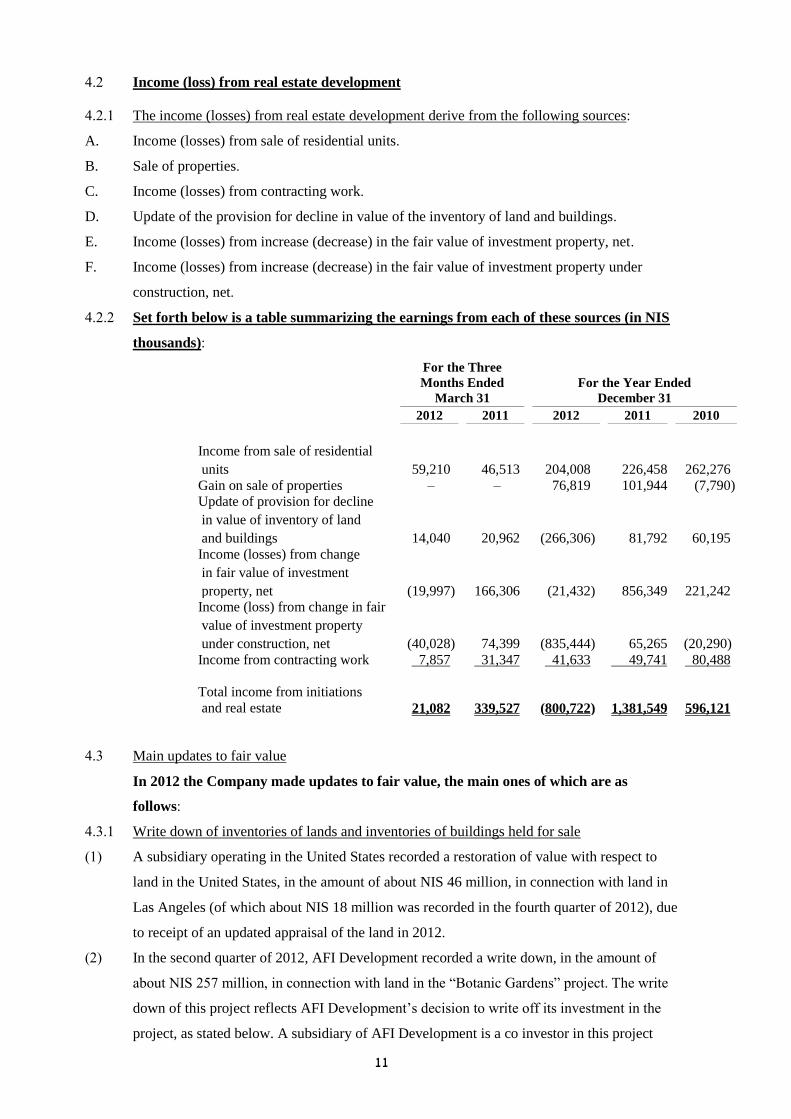

8.1.1 Set forth below is a table summarizing the earnings from each of these sources (in NIS

thousands):

For the Three

Months Ended For the Year Ended

March 31 December 31

2012 2011 2012 2011 2010

Income from sale of residential units 59,210 46,513 204,008 226,458 262,276 Gain on sale of properties – – 76,819 101,944 (7,790) Update of provision for decline in value of inventory of land and buildings 14,040 20,962 (266,306) 81,792 60,195 Income (losses) from change in fair value of investment property, net (19,997) 166,306 (21,432) 856,349 221,242 Income (loss) from change in fair value of investment property under construction, net (40,028) 74,399 (835,444) 65,265 (20,290) Income from contracting work 7,857 31,347 41,633 49,741 80,488

Total income from initiations

and real estate 21,082 339,527 )800,722( 1,381,549 596,121

8.6 Main updates to fair value

In 2012 the Company made updates to fair value, the main ones of which are as

follows:

8.6.8 Write down of inventories of lands and inventories of buildings held for sale

(8) A subsidiary operating in the United States recorded a restoration of value with respect to

land in the United States, in the amount of about NIS 46 million, in connection with land in

Las Angeles (of which about NIS 18 million was recorded in the fourth quarter of 2012), due

to receipt of an updated appraisal of the land in 2012.

(1) In the second quarter of 2012, AFI Development recorded a write down, in the amount of

about NIS 257 million, in connection with land in the ―Botanic Gardens‖ project. The write

down of this project reflects AFI Development’s decision to write off its investment in the

project, as stated below. A subsidiary of AFI Development is a co investor in this project

12

together with a private company wholly owned by the City of Moscow, which is the main

investor in the project (hereinafter – ―the Main Investor‖), and which is entitled under the

investment agreement with the City of Moscow to receive the lease rights therein. On

August 2, 2012, a request was filed in the Court in Moscow on behalf of a third party

creditor to declare that the Main Investor is bankrupt, further to a foreclosure imposed on its

assets in favor of that creditor. AFI Development estimates, based on an outside legal

opinion, that the chances of recovering its investments in this project are not probable.

Taking into account the circumstances of the matter, AFI Development decided to write off

its investment in this project in its financial statements for the second quarter of 2012.

Nonetheless, AFI Development announced its intention to continue the efforts to recover its

investments in this project and/or to receive the development rights therein. On February 5,

2013, AFI Development announced that further to contacts it carried on with the City, the

parties signed an addendum to the investment agreement (hereinafter – ―the Addendum‖)

whereby the rights of AFI Development in the project were recognized (through a wholly

controlled subsidiary, hereafter – ―the Project Company‖). Pursuant to the Addendum, the

Main Investor will have no contentions with respect to the AFI Development’s investments

in the project and the Project Company will become the sole investor in the project pursuant

to the investment agreement. Further to this, the City approved assignment of the short term

lease agreement covering the project’s lands from the name of the Main Investor to the name

of the Project Company. After an in depth evaluation of the risks to the rights of the Project

Company in the project, against the background of the insolvency of the Main Investor, the

Project Company decided to make the required payments to the City pursuant to the

Addendum in exchange for additional development rights. The total payments under the

Addendum amount to about US$18.5 million, which were paid in a number of installments.

The decision was made on the basis of the opinion of AFI Development’s outside legal

advisors, whereby in a case where the Addendum is declared null and void or is cancelled

(due to claims of creditors of the Main Investor), the Project Company will be entitled to

return of the amounts paid to the City of Moscow. In light of maintenance of the insolvency

proceedings, and based on an opinion of AFI Development’s outside legal advisors, there is

uncertainty regarding the period of the Addendum and/or the possibility of maintaining

grounds for its cancellation. Due to that stated above, at this stage the provision recorded, as

stated above, with respect to write off of the investment in the project, was not cancelled.

(6) In the third quarter of 2012, AFI Europe made a write down for decline in value of an

inventory of lands relating to projects in Romania, in the aggregate amount of NIS 54

million.

8.6.1 Write down of investment property under construction

(8) In the second quarter of 2012, AFI Development recorded a decline in fair value, in the

amount of about NIS 282 million, in respect of the Putchotovo project. During 2012, the

13

City of Moscow acted to apply across the board changes in the urban planning and

development policies in Moscow, the main ones of which being reduction of the

construction density and a cutback of zoning changes of lands designated for commercial use

within the boundaries of the City of Moscow. Further to that stated above, AFI Development

carried on contacts with the authorities of the City of Moscow, with reference to the City’s

intention to also implement changes, as stated, with respect to the project and its surrounding

areas. In the beginning of August 2012, an internal document from the City’s planning

authorities came to AFI Development’s attention (which was not directed to AFI

Development), that the built up area in this project is to be significantly reduced. In reliance

on this decision and further to additional conversations with City parties, AFI

Development’s management decided to agree to reduction of the building density and,

accordingly, to re plan the project. The significant reduction in the building rights in the

project is the main reason for the decline in the fair value of the project compared with its

estimated value as at December 31, 2011. The decline in value was made based on an

external valuation received from the office of JLL, as at June 30, 2012. The valuation

performed by the office of Cushman & Wakefield, as at December 31, 2012 is attached to

the Company’s financial statements as at December 31, 2012.

(1) In the second quarter of 2012, AFI Development recorded a decline in fair value, in the

amount of about NIS 191 million, in respect of the Kosinskaya project. On July 1, 2012, the

borders of the City of Moscow were officially expanded in the southwest direction (an area

known as ―New Moscow‖). Prior to this, the President of Russia initiated a plan for gradual

transfer of the State authorities to New Moscow. As a result, a trend is visible of re-routing

the business activities, in a gradual manner, from the City center to the southwest direction.

In the estimation of the project’s appraiser, this trend is expected to make marketing of

offices located on the east side of the City – such as the project – more difficult. Taking into

account the aforesaid trends, in order to maintain a competitive advantage and a level of

revenues as previously planned for the project, AFI Development was forced to update the

project concept and to improve the specifications of the property designated to be built in the

framework thereof. Update of the concept along with addition of elevators and allotment of

larger public areas resulted in a contraction of the area planned for rental. Along with this

impact, this update also triggered an increase in the budget for the balance of the project’s

construction costs. Most of the increase in the budget relates to additional adaptations (―fit

outs‖) for the public areas, external infrastructures and additional approvals for these needs.

Furthermore, costs were added to the updated budget (such as permits, approvals and others)

for purposes of adding direct access from the project to Moscow’s circular highway

(MKAD), as well as in order to prepare an additional land area for outside parking in an

attempt to improve the relative number of parking spaces in the project. Update of the

planning in order to make the most favorable use of the project due to identification of the

14

change in the market trend as a result of expansion of the City’s borders, which led to a

decline in the project’s income producing areas, along with an increase in the construction

costs, are the basis for the decline in the fair value of this project. The decline in value was

made based on an external appraisal received from the office of JLL, which was attached to

the Company’s quarterly report for the period ended June 30, 2012. The valuation performed

by the office of Cushman & Wakefield, as at December 31, 2012 is attached to the

Company’s financial statements as at December 31, 2012.

(6) In the second quarter of 2012, AFI Development recorded a decline in value, in the amount

of about NIS 231 million, in connection with the Tverskia Zestava project – stages II and Ib.

As part of implementation of ―across the board‖ changes in the urban planning and

development policies by the City of Moscow, the City’s authorities are advancing a move

toward reducing the scope of the construction in the City’s center. Further to that stated

above, in 2011 and 2012 AFI Development held discussions with the City of Moscow’s

authorities addressing the continued development of a number of projects in the Tverskia

Zestava area.

With respect to some of the projects in this area (the Tverskia Zestava shopping mall, Plaza

1C, Plaza 2A and Plaza 4), AFI Development reached non-binding understandings with City

of Moscow in connection with discontinuance of development of shopping mall and receipt

of additional rights in the surrounding area. Concurrent with and further to these

understandings, the parties continued the discussions regarding development of the Plaza 2

and Plaza 1B projects. During the period of the discussions, AFI Development’s

management encountered publications and information releases (sometimes contradicting),

in connection with, among other things, decisions of the City with respect to the rights of

AFI Development in Plaza 2, Plaza 2A and Plaza 1B, which according to its understanding

needed to be clarified, and to the extent necessary, the possibility of taking steps to change

or cancel these decisions needed to be examined. Against the background of that stated

above, AFI Development sent a letter to the Deputy Mayor of the City of Moscow, wherein

the City was request to clarify the development possibilities in connection with these

projects. In response to this letter and after additional discussions were held, in August 2012,

AFI Development received a letter from the City of Moscow whereby the City of Moscow’s

authorities will approve development of the areas/buildings in these projects only within the

existing areas. In light of that stated above, AFI Development views these two projects as

properties designated for improvement within the existing areas and not as projects for new

development. Accordingly, in the second quarter of 2012, the classification of these projects

was changed from investment property under construction to investment property.

Abandonment of the development plans for these projects, including the possibility of

increasing their areas, is the basis for the decline in the fair value of the projects compared

with their values estimated as at December 31, 2011. The decline in value was made based

15

on an external appraisal received from the office of JLL, which was attached to the

Company’s quarterly report for the period ended June 30, 2012.

(8) In 2012, Africa Properties recorded a decline in fair value with respect to land in the area of

Ramle, Gezer and Modi’in, in the amount of about NIS 11 million, deriving from the fact

that the Subcommittee for Objections of the Central District Committee made a decision

with respect to land in the area of Ramle, Gezer and Modi’in, concerning cancellation of a

prior decision of the plenary Central District Committee, regarding change of the stages in

the land area in which it is planned, among other things, to construct a logistics park. As a

practical result of the decision of the Subcommittee, as stated, the commencement date of

development of the logistics park was postponed. In addition, Africa Properties recorded a

decline in the fair value in respect of land in area of Petah Tiqwa, in the amount of about

NIS 4.9 million, due to a provision recorded by Africa Properties in respect of taxes

expected to apply to the land and a decline in the fair value of land of Africa Properties in

Bulgaria, in the amount of about NIS 15 million. On the other hand, Africa Properties

recorded an increase in fair value of investment property under construction in connection

with a project of Africa Properties in the Czech Republic, in the amount of about NIS 4.5

million, and in respect of a building Africa Properties is constructing in the Science Park in

Nes Ziona, in the amount of about NIS 5.5 million.

8.6.6 Income from increase in fair value of investment property, net

(8) In 2012, AFI Development recorded a decline in fair value, in the amount of about NIS 202

million, in respect of the ―AFI Mall‖ shopping center (of which about NIS 48 million was

recorded in the fourth quarter of 2012). The source of the above mentioned reduction is the

strengthening of the ruble against the U.S. dollar in 2012 at the rate of about 5.6%. The value

of the property as at December 31, 2012, was determined based on an external valuation

received from the office of Cushman & Wakefield. The valuation is attached to the

Company’s financial statements as at December 31, 2012.

(2) In 2012, Africa Properties recorded an increase in fair value stemming mainly from a

revaluation, in the amount of about NIS 63.6 million, in respect of properties of Africa

Properties in the Czech Republic (mainly the Parducheva shopping mall), a revaluation, in

the amount of about NIS 88.7 million, in respect of properties of Africa Properties in

Romania (the Cotroceni shopping mall and the office tower adjacent thereto), and a

revaluation, in the amount of about NIS 62 million, in respect of properties of Africa

Properties in Israel including, among others, a revaluation, in the amount of about NIS 17

million, in respect of the Global Park project in Lod and a revaluation, in the amount of

about NIS 27 million, in respect of the Weitzman Park project in Nes Ziona. The increase in

the fair value was offset by a decline in fair value, in the amount of about NIS 21.3 million,

in respect of a property in Bulgaria, and a decline in fair value, in the amount of about NIS

13.6 million, in respect of a property in Serbia.

16

In 2011, the Company made the following adjustments to fair value:

4.3.4 Write-down of inventory of land and inventory of buildings for sale

(1) A subsidiary operating in the USA recorded recovery of the value of its inventory in the

USA in the amount of NIS 14 million in respect of land in Gowanus. This adjustment was

recorded in the first quarter of 2011 following the receipt of a revised appraisal for a number

of plots of land and an indication from a transaction that was concluded in the period of

report of the financial position in respect of one specific plot.

(2) A subsidiary operating in the USA recorded recovery of value of NIS 112 million in respect

of building inventory in the Marquis and 20 Pine projects in the USA (of which NIS 21

million was recorded in the fourth quarter of 2011). This adjustment was recorded following

the receipt of a revised appraisal of the project.

4.3.5 Income in respect of increase (decline) in the fair value of investment property under

construction, net:

(1) In 2011, a positive revaluation was recorded of investment property under construction of

NIS 26 million (of which NIS 4 million was recorded in the fourth quarter of 2011). This

amount is due to interim income generated to Danya Cebus in respect of investment property

projects under construction that are being executed for the Group.

(2) A subsidiary of AFI Development recorded an increase in fair value in the second quarter of

2011 of NIS 45 million in respect of Stage 2 of the Paveletskaya project. The cost of the

project was depreciated in 2008 and 2009, in view of the situation in the Russian real estate

market and uncertainty about the continued development of the project. Due to the recovery

in the real estate market in Moscow in 2010 and 2011, AFI Development intends to develop

the project and it is now in the early stages of development and therefore an increase in fair

value was recorded, based on an external opinion received from JLL.

(3) In November 2011 a decision was taken by Moscow municipality according to which the

Tverskaya Zastava Mall (part of the Tverskaya Zastava project; hereinafter, ―Tverskaya‖) in

Moscow will be returned to the Municipality and as compensation, Moscow municipality

will ratify and renew AFI Development’s development and lease rights in the other stages of

the project. Among other things, the Municipality will not charge AFI Development with the

costs of municipal development it was due to pay in the project. The write-off of the

Tverskaya project from AFI Development’s books and the recording of the remaining stages

of the project in accordance with the understanding reached had no material effect on the

results for the period. As at December 31, 2011, external valuations were received from JLL

for Tverskaya in accordance with the understanding reached.

(4) In 2011 Africa Properties recorded an increase in fair value due mainly to an increase in fair

value of assets in Israel in the amount of NIS 52.7 million (mainly in respect of the land

purchased in Ramleh, Gezer, Modi’in, and Africa Properties’ rights in the Ahad Ha’am

Project in Tel Aviv) and due to an increase of approximately NIS 6.8 million in the fair

17

value of the Classic 7 Project Stage B in the Czech Republic. The increase was set off by a

decline in fair value of NIS 25.3 million in respect of the Varna Business Park in Bulgaria,

and a decline of NIS 6.5 million in respect of land owned by Africa Properties land in Lod.

4.3.6 Income in respect of increase (decrease) in the fair value of investment property, net:

(1) A subsidiary of Africa Development recorded an increase of NIS 365 million in fair value in

2011 in respect of the AFI Mall project in Moscow (of which NIS 155 million was recorded

in the fourth quarter of 2011). The increase in the fourth quarter of 2011 was made on the

basis of an external appraisal received from JLL as at December 31, 2011. The adjustments

in the fourth quarter of 2011 include NIS USD 21 million in respect of a value added tax

refund received in February 2012 which reduced the estimated Project costs and increased

revaluation income in the fourth quarter of 2011.

(2) AFI Development also recorded income of NIS 417 million from the purchase of the

Municipality’s share (25%) of the AFI Mall project in the third quarter of 2011.

(3) A subsidiary of AFI Development recorded an increase in fair value of NIS 45 million in the

second quarter of 2011 in respect of Stage 2 of the Paveletskaya project. The cost of the

project was depreciated in 2008 and 2009 in view of the situation in the Russian real estate

market and uncertainty about the continued development of the project. Due to the recovery

in the real estate market in Moscow in 2010 and 2011, AFI Development intends to develop

the project and it is now in the early stages of development and therefore an appreciation

was recorded in fair value based on an external opinion received from JLL.

(4) In 2011, Africa Properties recorded a net impairment of NIS 1.1 million in fair value of

investment property. The impairment in fair value in 2011 was due mainly to an impairment

in fair value of NIS 46.2 million in respect of the Varna Business Park project in Bulgaria

(due mainly to the departure of a major tenant) and impairment in fair value of NIS 16.9

million in respect of the Airport City project in Belgrade. The impairment was partly set off

by an appreciation of NIS 41.5 million in respect of Africa Properties’ assets in the Czech

Republic and an appreciation of NIS 25 million in respect of properties in Israel.

4.4 Property operations and rental

4.4.1 In 2012, the Company’s income from property operations and rentals totaled NIS 732

million, compared to NIS 672 million in 2011. The increase from 2011 to 2012 stemmed

mainly from the opening of the AFI Mall in Moscow in March 2011. Since the opening date,

income of USD 65 million was recorded in 2011, compared with USD 65 million in 2012.

4.4.2 The Company’s income from property operation and rental in 2011 was NIS 672 million,

compared with NIS 440 million in 2010. Growth in income stemmed mainly from the

opening of AFI Mall in Moscow, as stated above.

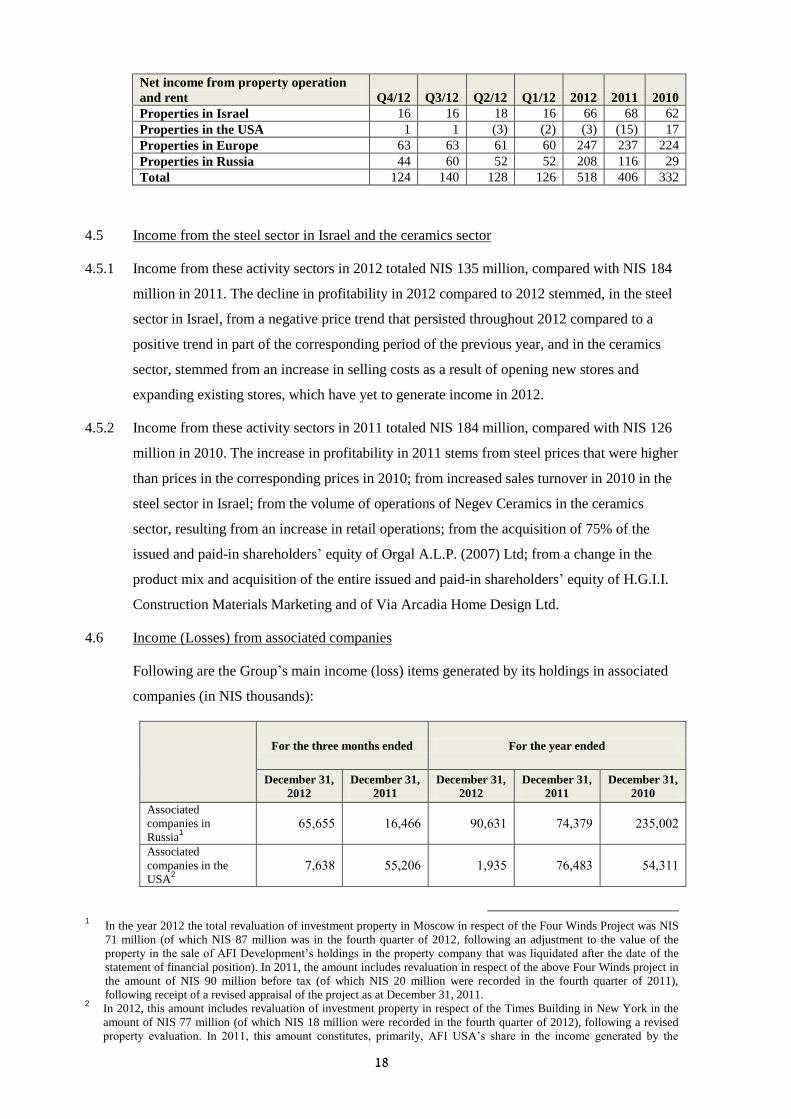

4.4.3 Following is a breakdown of the net income in respect of property operation and rentals

(NOI) by geographic location (in NIS millions):

18

Net income from property operation

and rent Q4/12 Q3/12 Q2/12 Q1/12 2012 2011 2010

Properties in Israel 16 16 18 16 66 68 62

Properties in the USA 1 1 (3) (2) (3) (15) 17

Properties in Europe 63 63 61 60 247 237 224

Properties in Russia 44 60 52 52 208 116 29

Total 124 140 128 126 518 406 332

4.5 Income from the steel sector in Israel and the ceramics sector

4.5.1 Income from these activity sectors in 2012 totaled NIS 135 million, compared with NIS 184

million in 2011. The decline in profitability in 2012 compared to 2012 stemmed, in the steel

sector in Israel, from a negative price trend that persisted throughout 2012 compared to a

positive trend in part of the corresponding period of the previous year, and in the ceramics

sector, stemmed from an increase in selling costs as a result of opening new stores and

expanding existing stores, which have yet to generate income in 2012.

4.5.2 Income from these activity sectors in 2011 totaled NIS 184 million, compared with NIS 126

million in 2010. The increase in profitability in 2011 stems from steel prices that were higher

than prices in the corresponding prices in 2010; from increased sales turnover in 2010 in the

steel sector in Israel; from the volume of operations of Negev Ceramics in the ceramics

sector, resulting from an increase in retail operations; from the acquisition of 75% of the

issued and paid-in shareholders’ equity of Orgal A.L.P. (2007) Ltd; from a change in the

product mix and acquisition of the entire issued and paid-in shareholders’ equity of H.G.I.I.

Construction Materials Marketing and of Via Arcadia Home Design Ltd.

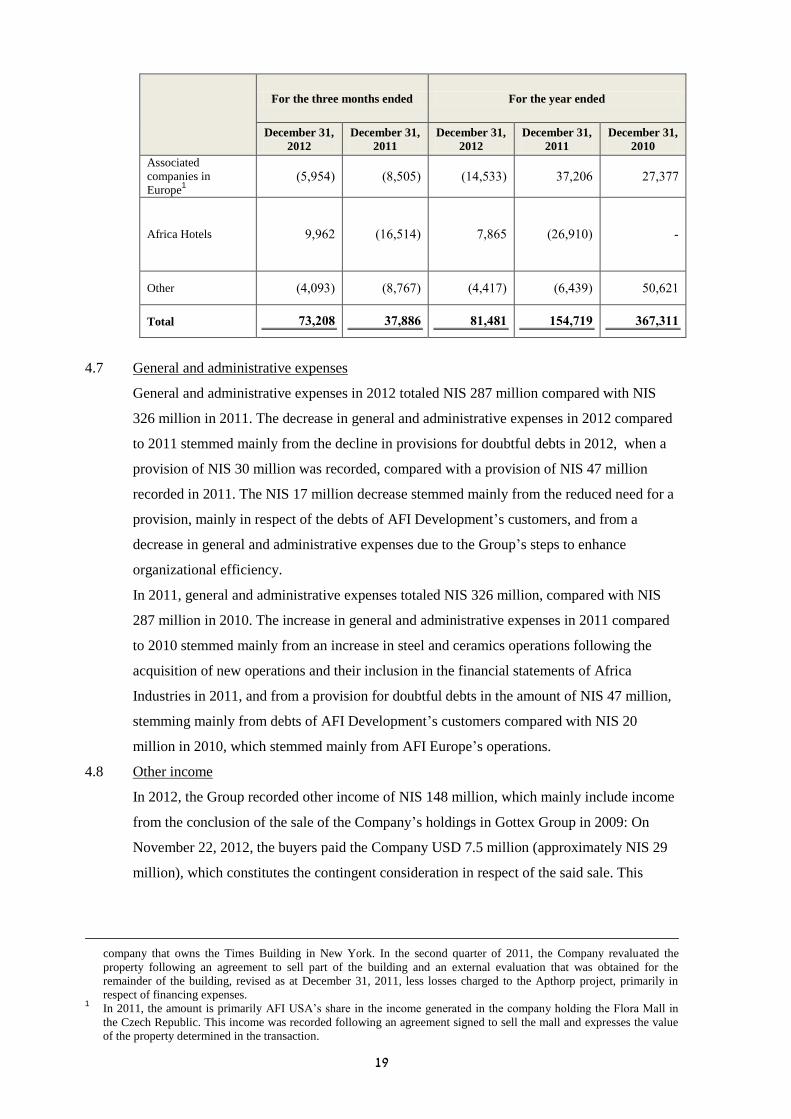

4.6 Income (Losses) from associated companies

Following are the Group’s main income (loss) items generated by its holdings in associated

companies (in NIS thousands):

For the three months ended For the year ended

December 31,

2012

December 31,

2011

December 31,

2012

December 31,

2011

December 31,

2010

Associated

companies in

Russia1

66,666 86,866 6.,668 58,656 166,..1

Associated

companies in the

USA2

5,664 66,1.6 8,666 56,846 68,688

1 In the year 2012 the total revaluation of investment property in Moscow in respect of the Four Winds Project was NIS

71 million (of which NIS 87 million was in the fourth quarter of 2012, following an adjustment to the value of the

property in the sale of AFI Development’s holdings in the property company that was liquidated after the date of the

statement of financial position). In 2011, the amount includes revaluation in respect of the above Four Winds project in

the amount of NIS 90 million before tax (of which NIS 20 million were recorded in the fourth quarter of 2011),

following receipt of a revised appraisal of the project as at December 31, 2011. 2 In 2012, this amount includes revaluation of investment property in respect of the Times Building in New York in the

amount of NIS 77 million (of which NIS 18 million were recorded in the fourth quarter of 2012), following a revised

property evaluation. In 2011, this amount constitutes, primarily, AFI USA’s share in the income generated by the

19

For the three months ended For the year ended

December 31,

2012

December 31,

2011

December 31,

2012

December 31,

2011

December 31,

2010

Associated

companies in

Europe1

(6,668) (4,6.6) (88,666) 65,1.6 15,655

Africa Hotels 6,661 (86,688) 5,466 (16,68.) -

Other (8,.66) (4,565) (8,885) (6,866) 6.,618

Total 239103 329331 329132 2019224 3129322

4.7 General and administrative expenses

General and administrative expenses in 2012 totaled NIS 287 million compared with NIS

326 million in 2011. The decrease in general and administrative expenses in 2012 compared

to 2011 stemmed mainly from the decline in provisions for doubtful debts in 2012, when a

provision of NIS 30 million was recorded, compared with a provision of NIS 47 million

recorded in 2011. The NIS 17 million decrease stemmed mainly from the reduced need for a

provision, mainly in respect of the debts of AFI Development’s customers, and from a

decrease in general and administrative expenses due to the Group’s steps to enhance

organizational efficiency.

In 2011, general and administrative expenses totaled NIS 326 million, compared with NIS

287 million in 2010. The increase in general and administrative expenses in 2011 compared

to 2010 stemmed mainly from an increase in steel and ceramics operations following the

acquisition of new operations and their inclusion in the financial statements of Africa

Industries in 2011, and from a provision for doubtful debts in the amount of NIS 47 million,

stemming mainly from debts of AFI Development’s customers compared with NIS 20

million in 2010, which stemmed mainly from AFI Europe’s operations.

4.8 Other income

In 2012, the Group recorded other income of NIS 148 million, which mainly include income

from the conclusion of the sale of the Company’s holdings in Gottex Group in 2009: On

November 22, 2012, the buyers paid the Company USD 7.5 million (approximately NIS 29

million), which constitutes the contingent consideration in respect of the said sale. This

company that owns the Times Building in New York. In the second quarter of 2011, the Company revaluated the

property following an agreement to sell part of the building and an external evaluation that was obtained for the

remainder of the building, revised as at December 31, 2011, less losses charged to the Apthorp project, primarily in

respect of financing expenses. 1 In 2011, the amount is primarily AFI USA’s share in the income generated in the company holding the Flora Mall in

the Czech Republic. This income was recorded following an agreement signed to sell the mall and expresses the value

of the property determined in the transaction.

21

amount was recorded in the Company’s financial statements for the third quarter of 2012 as

income under other income.

In March 2012, the sale of the Company’s (100%) holdings in a subsidiary, Cebus Rimon

Building Industries and Development Ltd, which owns real estate in the industrial zone, was

for a consideration of NIS 76.2 million (and VAT) was concluded. Total income in respect

of the sale was NIS 68 million, which was recorded in the first quarter of 2012.

4.9 Depreciation of other assets and other expenses

Other expenses in 2012 mainly included:

4.9.1 The main expense included in this item is the impairment of an investment in an associated

company in Poland, in which Africa Properties holds 30% of the rights (hereinafter, ―the

Associated Company‖). The Associated Company owns land in Warsaw on which it had

planned to construct a large residential neighborhood and shopping center (mall). The

assessment of an impairment was conducted, among other reasons, in view of a certain

slowdown recently recorded in the residential market in Poland; legal and planning

difficulties that the Associated Company encountered in constructing the shopping center;

and in view of the uncertainty of the continued development of the project due to the

partner’s intention to take steps to sell the land owned by the Associated Company.

Although no decision to sell the land owned by the Associated Company has been made,

Africa Properties decided to depreciate the investment by an amount of NIS 97 million,

based on the estimated consideration that Africa Properties expects to receive in the event

that the Associated Company disposes of the land.

4.9.2 A write-down on an investment in an associated property company of AFI USA, following a

revision to the projected consideration that the property will generate. Total depreciation

recorded was NIS 31 million.

Other expenses in 2011 mainly included:

4.9.3 An impairment recorded in the first quarter of 2011 in respect of a jointly controlled

company presented at book value, in the amount of NIS 20 million.

4.9.4 Impairments of NIS 12 million in respect of hotel properties in AFI Development following

receipt of revised property evaluations performed in 2011.

4.9.5 A provision made by Africa Properties in respect of a settlement with the owner of land in

Romania in the third quarter of 2011.

4.10 Financing income/expenses

4.10.1 In 2012, the Group’s financing expenses totaled NIS 1,145 million compared with NIS 1,110

million in 2011.

Most of the Group’s financing expenses in 2012 were in respect of the Group’s index-linked

liabilities, mainly those of the Company. In 2012, the known CPI rose by 1.44% compared

with an increase of 2.55% in 2011. In contrast, the Group’s financing income in 2012 totaled

NIS 362 million, compared with NIS 272 million in the previous year. Financing income in

21

2012 included income of NIS 56million from the sale of shares in Alon USA, compared with

NIS 91 million in the previous year.

Accordingly, in 2012, financing expenses (net) totaled NIS 784 million, compared with

financing income (net) of NIS 838 million in 2011.

4.10.2 In 2011, the Group’s financing expenses totaled NIS 1,110 million compared with NIS 1,124

million in 2010.

Most of the Group’s financing expenses in 2011 were in respect of the Group’s index-linked

liabilities, mainly those of the Company. In 2011, the known CPI rose by 2.55% compared

with an increase of 2.28% in 2010. In contrast, the Group’s financing income in 2011 totaled

NIS 272 million, compared with NIS 1,729 million in 2010. The Group’s financing income

in 2010 includes income from the conclusion of the Company’s Arrangement with its

bondholders, in the amount of NIS 1.45billion (For details, also see Note 1(C) to the

Company’s Financial Statements as at December 31, 2012). Excluding this income, the

Group’s financing income in 2010 totaled a mere NIS 280 million.

Accordingly, total financing expenses (net) in 2011 totaled NIS 838 million, compared with

financing expenses (net) of NIS 606 million in 2010.

4.11 Taxes on income

4.11.1 In 2012, tax expenses totaled NIS 73 million. Pre-tax loss , excluding equity income in this

period totaled NIS 1,374 million. The reason for the low amount of tax is financing expenses

in the Company in respect of which no deferred taxes were recorded, stemming from the

Company’s accumulated losses. Tax expenses for 2012 include a one-time expense

following the change in the tax rate in Serbia in the amount of NIS 25 million.

4.11.2 In 2011, tax expenses were NIS 401 million. Income before tax, after controlling for equity

income in the aforesaid period was NIS 803 million. The statutory tax rate in this period is

24% and the effective tax rate for the period was 41.8%. The reason for the high tax rate was

financing expenses in the Company in respect of which deferred tax was not recognized as a

result of losses accumulated in the Company. In 2011, additional tax expenses of NIS 45

million (including the company’s share of taxes recognized in companies presented on an

equity basis) were recognized in the reporting period in respect of the Taxation Section of

the recommendations of the committee headed by Professor Trachtenberg, the main effect of

which on the Group is the suspension of the tax cuts and increase of corporate tax to 25%

beginning in 2012.

4.12 Income (Loss) from discontinued operations

Losses from discontinued operations in 2012 constitute the loss recorded by Africa

Industries in the steel sector in Russia, which is presented in Africa Industries’ financial

statements, beginning from the financial statements as at December 31, 2012 as

―discontinued operation‖ following the sale of Africa Industries’ sale of its holdings in

22

Cloudwalk (that owned the company through which the Group operated in the steel sector in

Russia). According to GAAP, the results of the sold company’s operations that stem from

and are related to the discontinued operation are not presented as consolidated results of

Africa Industries. Africa Industries’ loss from the discontinued operation in 2012 totaled NIS

28.8 million, comprising a current loss from the discontinued operation in the amount of NIS

18.4 million and a loss from the sale of the discontinued operation in the amount of NIS 10.4

million.

In 2011, Africa Industries recorded income of NIS 3 million from the discontinued

operation. The Company’s total income from the discontinued operation in 2011 totaled NIS

78, net after tax, of which NIS 71 million constitutes the income from the sale of 75% of

Danya Cebus’ holdings in Nitivei Hayoval Ltd.

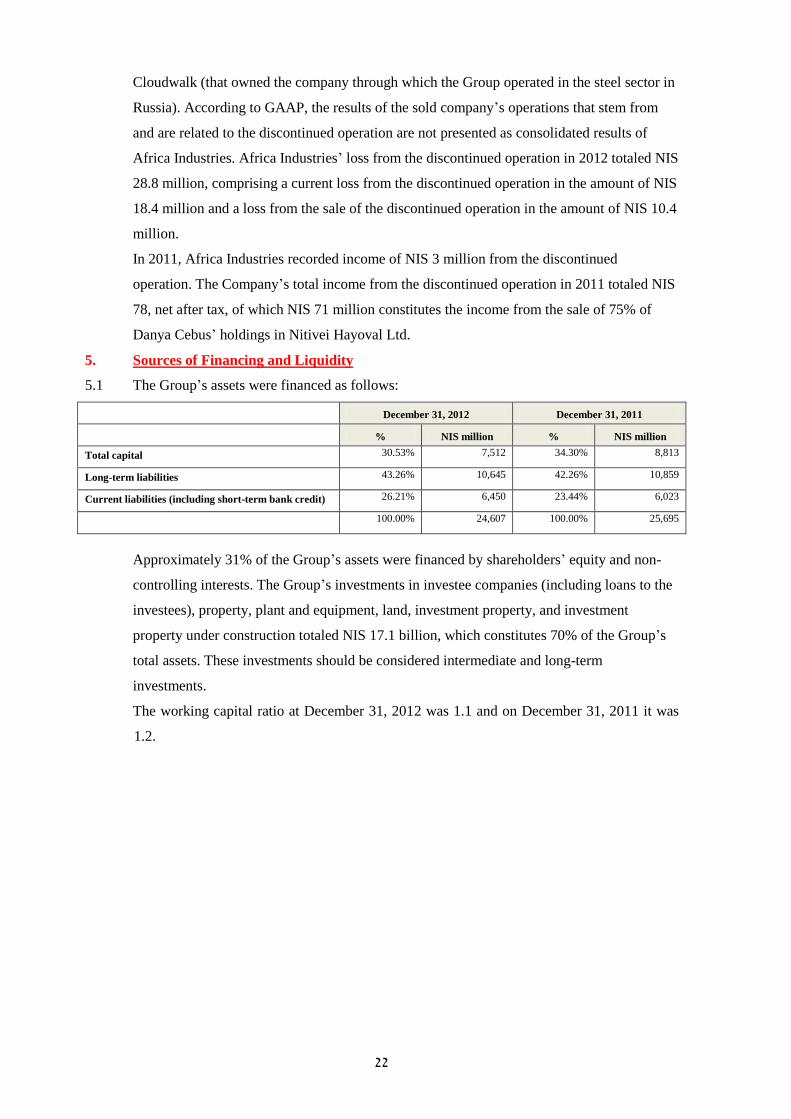

5. Sources of Financing and Liquidity

5.1 The Group’s assets were financed as follows:

December 31, 2012 December 31, 2011

% NIS million % NIS million

Total capital 30.53% 7,512 34.30% 8,813

Long-term liabilities 43.26% 10,645 42.26% 10,859

Current liabilities (including short-term bank credit) 26.21% 6,450 23.44% 6,023

100.00% 24,607 100.00% 25,695

Approximately 31% of the Group’s assets were financed by shareholders’ equity and non-

controlling interests. The Group’s investments in investee companies (including loans to the

investees), property, plant and equipment, land, investment property, and investment

property under construction totaled NIS 17.1 billion, which constitutes 70% of the Group’s

total assets. These investments should be considered intermediate and long-term

investments.

The working capital ratio at December 31, 2012 was 1.1 and on December 31, 2011 it was

1.2.

23

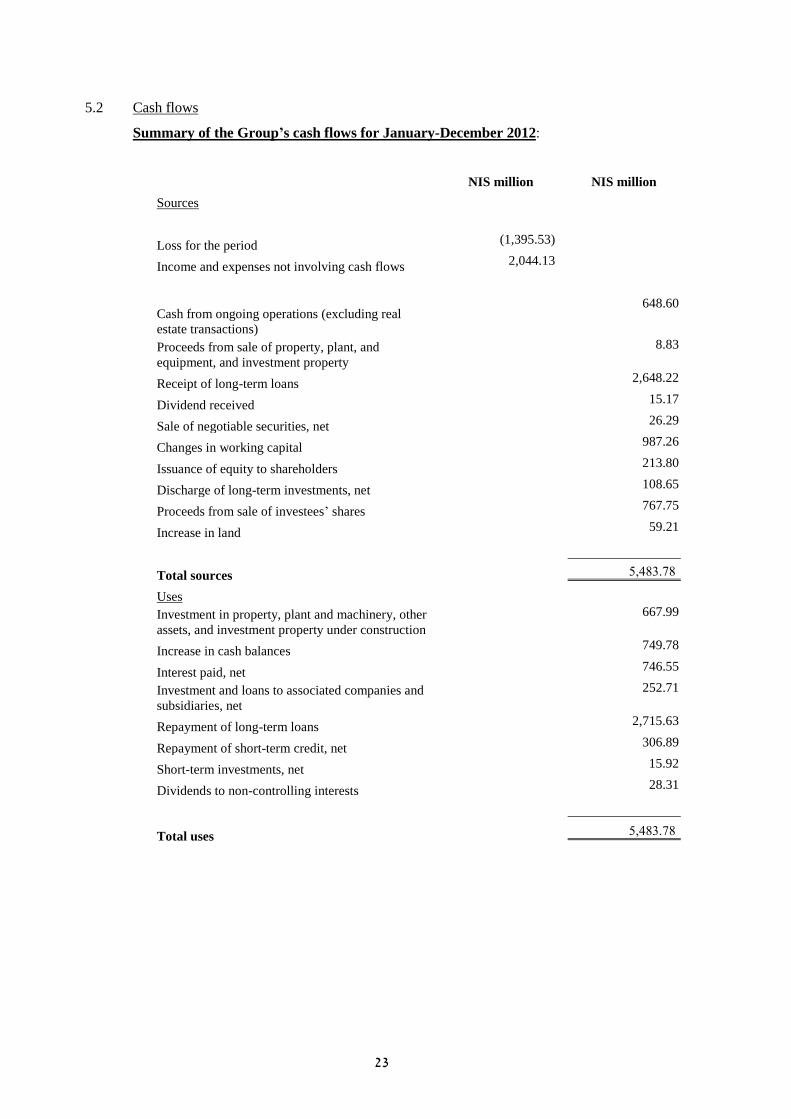

5.2 Cash flows

Summary of the Group’s cash flows for January-December 2012:

NIS million NIS million

Sources

Loss for the period (1,395.53)

Income and expenses not involving cash flows 2,044.13

Cash from ongoing operations (excluding real

estate transactions)

648.60

Proceeds from sale of property, plant, and

equipment, and investment property

8.83

Receipt of long-term loans

2,648.22

Dividend received

15.17

Sale of negotiable securities, net

26.29

Changes in working capital

987.26

Issuance of equity to shareholders

213.80

Discharge of long-term investments, net

108.65

Proceeds from sale of investees’ shares 767.75

Increase in land 59.21

Total sources

6,846.54

Uses

Investment in property, plant and machinery, other

assets, and investment property under construction

667.99

Increase in cash balances

749.78

Interest paid, net

746.55

Investment and loans to associated companies and

subsidiaries, net

252.71

Repayment of long-term loans

2,715.63

Repayment of short-term credit, net

306.89

Short-term investments, net

15.92

Dividends to non-controlling interests

28.31

Total uses

6,846.54

24

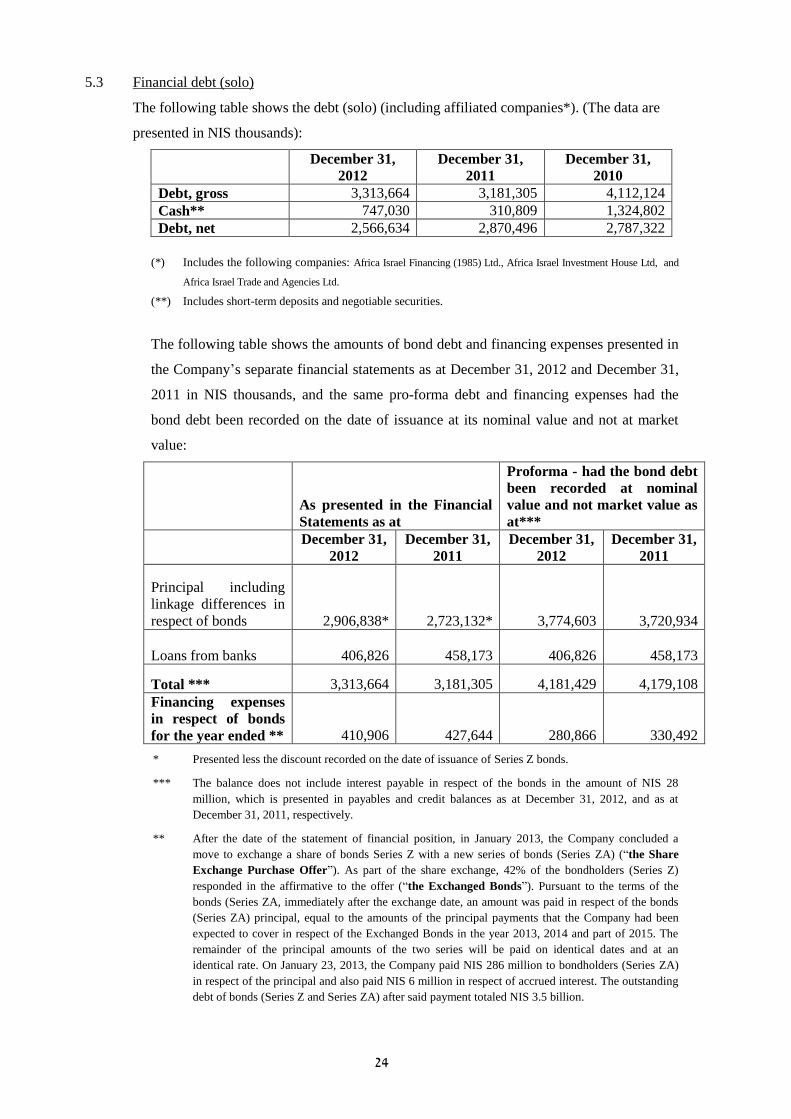

5.3 Financial debt (solo)

The following table shows the debt (solo) (including affiliated companies*). (The data are

presented in NIS thousands):

December 31,

2012

December 31,

2011

December 31,

2010

Debt, gross 3,313,664 3,181,305 4,112,124

Cash** 747,030 310,809 1,324,802

Debt, net 2,566,634 2,870,496 2,787,322

(*) Includes the following companies: Africa Israel Financing (1985) Ltd., Africa Israel Investment House Ltd, and

Africa Israel Trade and Agencies Ltd.

(**) Includes short-term deposits and negotiable securities.

The following table shows the amounts of bond debt and financing expenses presented in

the Company’s separate financial statements as at December 31, 2012 and December 31,

2011 in NIS thousands, and the same pro-forma debt and financing expenses had the

bond debt been recorded on the date of issuance at its nominal value and not at market

value:

As presented in the Financial

Statements as at

Proforma - had the bond debt

been recorded at nominal

value and not market value as

at***

December 31,

2012

December 31,

2011

December 31,

2012

December 31,

2011

Principal including

linkage differences in

respect of bonds 2,906,838* 2,723,132* 3,774,603 3,720,934

Loans from banks 406,826 458,173 406,826 458,173

Total *** 3,313,664 3,181,305 4,181,429 4,179,108

Financing expenses

in respect of bonds

for the year ended ** 410,906 427,644 280,866 330,492

* Presented less the discount recorded on the date of issuance of Series Z bonds.

*** The balance does not include interest payable in respect of the bonds in the amount of NIS 28

million, which is presented in payables and credit balances as at December 31, 2012, and as at

December 31, 2011, respectively.

** After the date of the statement of financial position, in January 2013, the Company concluded a

move to exchange a share of bonds Series Z with a new series of bonds (Series ZA) (―the Share

Exchange Purchase Offer‖). As part of the share exchange, 42% of the bondholders (Series Z)

responded in the affirmative to the offer (―the Exchanged Bonds‖). Pursuant to the terms of the

bonds (Series ZA, immediately after the exchange date, an amount was paid in respect of the bonds

(Series ZA) principal, equal to the amounts of the principal payments that the Company had been

expected to cover in respect of the Exchanged Bonds in the year 2013, 2014 and part of 2015. The

remainder of the principal amounts of the two series will be paid on identical dates and at an

identical rate. On January 23, 2013, the Company paid NIS 286 million to bondholders (Series ZA)

in respect of the principal and also paid NIS 6 million in respect of accrued interest. The outstanding

debt of bonds (Series Z and Series ZA) after said payment totaled NIS 3.5 billion.

25

5.4 Compliance with financial covenants

Regarding compliance by the Group Companies with financial covenants – see Note 22(D)

to the Company’s Financial Statements as at December 31, 2012. Under the Arrangement,

the Company was required to maintain to a maximum net solo debt to CAP ratio of 70%.1

As

at December 31, 2012, the net solo debt to CAP ratio was 36.83%,2

compared with 37.86%

as at December 31, 2011.

5.5 Projected cash flows to finance repayment of the Company’s liabilities

Pursuant to Regulation 10(B)(14) of the Securities Regulations (Periodic and Immediate

Reports) 1970, in the event of warning signs as defined in these Regulations, the company

must attach a statement of projected cash flows including details of the company’s existing

and anticipated liabilities in the two-year period after the publication date of the financial

statement (hereinafter, ―the Projected Cash Flow Statement‖). One of these warning signs is

negative cash flow or a negative cash flow for a period of 12 months, or a persistent negative

cash flow from ordinary operations, unless the Company’s Board of Directors determines

that they do not indicate any liquidity concerns.

Pursuant to the Company’s solo financial statements as at December 31, 2012, the Company

has a negative cash flow from ordinary operations of NIS 19 million in 2012.Nonetheless, it

should be noted that the cash flow from ordinary operations in the fourth quarter of 2012

was positive.

It is the assessment of the Company’s Board of Directors, in view of the fact that the

Company’s ability to service its debt, as a holding company, relies mainly on cash flows

from investing operations and cash flows from financing operations, and to a lesser extent on

cash flows from ordinary operations (which are in any case limited in holding

companies).Taking into consideration that the Company’s solo liquid balances as at

December 31, 2012 were NIS 747 million (see Section 5.3 million), and in view of the scope

of the Company’s short-term liabilities, the Company’s Board of Directors determined that

the solo negative cash flows from ordinary operations do not indicate a liquidity concern and

therefore none of the warning signs exist with respect to the Company.

1 For full details on the manner in which the calculation was made and the specific conditions, the Arrangement

documents (Reference No. 2010-01-379929). 2 Before controlling for accounting deductions in respect of assets against which loans granted exceeded the amount of

the right of recourse to the borrower, which would have reduced this ratio even further.

26

6. Significant Data from the Description of the Company’s Business and Events in

the Reporting Period

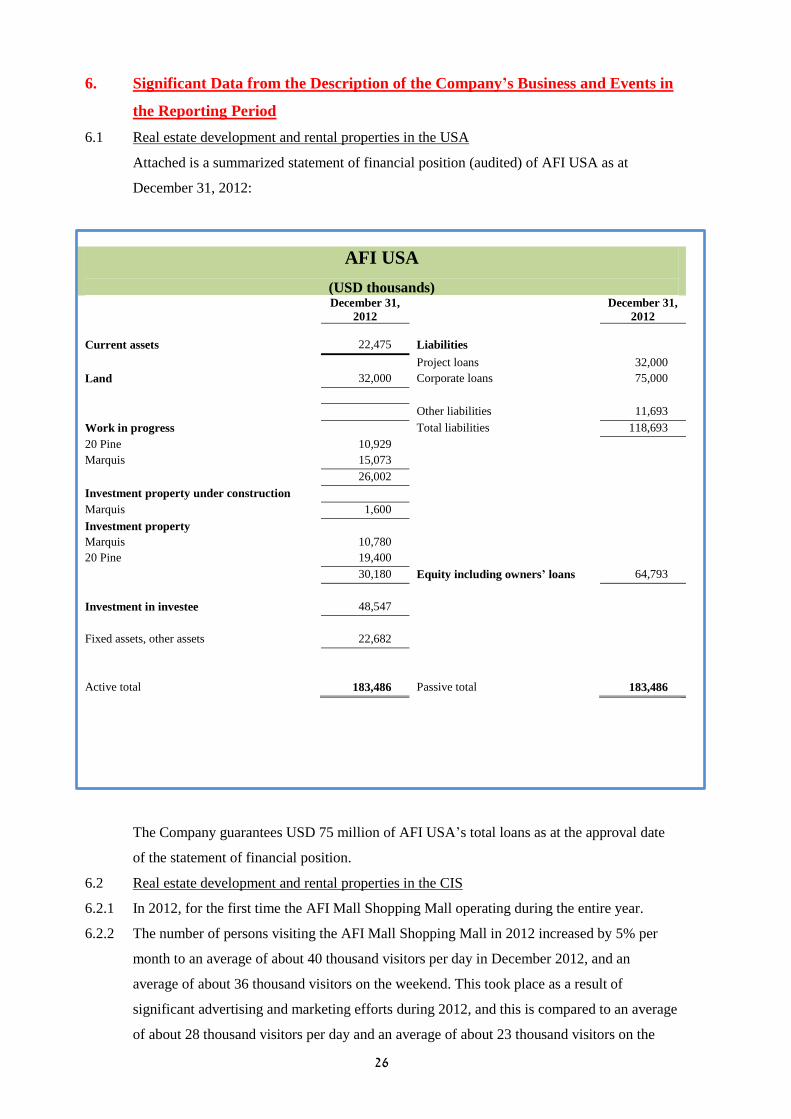

6.1 Real estate development and rental properties in the USA

Attached is a summarized statement of financial position (audited) of AFI USA as at

December 31, 2012:

AFI USA

(USD thousands) December 31,

2012

December 31,

2012

Current assets 22,475 Liabilities

Project loans 32,000

Land 32,000 Corporate loans 75,000

Other liabilities 11,693

Work in progress Total liabilities 118,693

20 Pine 10,929

Marquis 15,073

26,002

Investment property under construction

Marquis 1,600

Investment property

Marquis 10,780

20 Pine 19,400

30,180 Equity including owners’ loans 64,793

Investment in investee 48,547

Fixed assets, other assets 22,682

Active total 183,486 Passive total 183,486

The Company guarantees USD 75 million of AFI USA’s total loans as at the approval date

of the statement of financial position.

6.2 Real estate development and rental properties in the CIS

6.2.1 In 2012, for the first time the AFI Mall Shopping Mall operating during the entire year.

6.2.2 The number of persons visiting the AFI Mall Shopping Mall in 2012 increased by 5% per

month to an average of about 40 thousand visitors per day in December 2012, and an

average of about 36 thousand visitors on the weekend. This took place as a result of

significant advertising and marketing efforts during 2012, and this is compared to an average

of about 28 thousand visitors per day and an average of about 23 thousand visitors on the

27

weekend, in the corresponding period last year, that is an increase in the rates of about 36%

and about 57%, respectively. This increase in the number of visitors stems from among other

things, significant advertising and marketing efforts made by the Group in 2012, as well as

from full operation of the underground parking facility towards the end of 2012, which

offers over 2,000 parking spaces to persons visiting the AFI Mall Shopping Mall.

6.2.3 In addition, during 2012 the Group made efforts with respect to improvement of the

composition of its shopping-mall tenants, collection of rents and to improvement of the

overall profitability. Nonetheless, the occupancy rate remained at the same level as last year

at the rate of about 77%, however the NOI, revenues and collections increased significantly

during 2012.

6.2.4 In 2012, the NOI of the AFI Mall Shopping Mall, in the amount of about US 48.2 million,

compared with about $35.5 million in 2011, wherein the AFI Mall Shopping Mall operated

only starting from March 2011.

6.2.5 As part of the Group’s strategy to improve the credit terms in connection with rental

properties after their completion, in 2012 AFI Development executed a refinancing for the

AFI Mall Shopping Mall, whereby the aggregate credit framework will be US$666 million

(about 21 billion rubles), and the average interest for each loan will be reduced from an

average rate of about 9.62% to an average rate of about 8.22%. The amount of the credit

framework and its terms indicate the confidence of one of the large banks in the Russian

banking system in AFI Development, in general, and in the AFI Mall Shopping Mall, in

particular.

6.2.6 During 2012, the work continued with respect to construction of the new metro station,

which will create direct access to the AFI Mall Shopping Mall from the eastern part of

Moscow as well as from the northwest Moscow. Based on the official information published

by Moscow Metro, the new station is expected to enter into service by the end of 2013, and

thus to continue to improve the access roads to the Shopping Mall.

6.2.7 In addition, to the best of the Company’s knowledge, there has been progress with respect to

construction of the towers in the Moscow City site (on which the Shopping Mall is located)

and up to the end of 2012 construction of about 500 thousand square meters of office space

had been completed. Based on a report prepared by the appraisers Jones Lang LaSalle, up to

the end of 2013 construction of the buildings is expected to be completed on an aggregate

rentable area of about 308 thousand square meters. It is noted that the employees of the

office tower presently constitute a significant percentage of the total number of persons

visiting the AFI Mall Shopping Mall in the middle of the week and, therefore, completion of

entry of tenants into additional office areas on the site is expected to increase the number of

persons visiting the Shopping Mall.

6.2.8 In December 2012, AFI Development replaced the appraisers Jones Lang LaSalle,

(hereinafter – ―JLL‖) with Cushman & Wakefield (hereinafter, ―C&W‖). This replacement

28

was made as part of a rotation the Group makes of its outside advisors, after JLL served in

the position for 7 years. It is noted that to the best of the Company’s knowledge, two

international real estate consulting companies are involved, where in prior periods wherein

JLL performed the valuations of AFI Development’s properties C&W made a sample survey

and provided a second opinion for some of the properties. The valuations performed as at

December 31, 2012 were performed by C&W, whereas a sample survey and second opinion

for some of the properties was made/issued by JLL. C&W, similar to its predecessor JLL,

uses the ―discounted cash flows‖ (DCF) method in the valuations. Nonetheless, there are a

number of differences between the approaches of C&W and JLL. Among other things, the

differences between them are as follows: (1) forecast horizon – while the forecasted time

range up to theoretical realization in JLL’s models is between one year and 5 years, in

C&W’s models the range is between about 4 years and 7 years; (2) over the forecast years,

JLL used fixed prices whereas C&W assumed an annual growth rate in the price (lease/sale)

of between 2.5% and 5%, based on the market forecast for the upcoming years; (3) with

reference to properties under construction, C&W does not consider the initiator’s profit

separately as JLL did but, rather, they add it to the relevant risk factors for the project when

determining its discount rate; and (4) in light of the fact that C&W assumes a higher level of

risk for the anticipated cash flows (as stated, assumption of increase in price and the

initiator’s profit), the discount rate it adopts is significantly higher compared with the

discount rate used by JLL. It is noted that the differences in approach are reflected in the

discount rate and do not affect the yield rate assumptions in the representative year.

Notwithstanding the differences in approach, there is no significant difference in the value of

the properties, as at December 31, 2012, as determined in the valuations performed by

C&W, compared with the values of the properties determined in the valuations performed by

JLL, as at June 30, 2012.

7. Discussion and Examination of Remuneration to Parties at Interest and Senior

Executives

7.1 Following are details of the examination conducted into the connection between

remuneration paid to the Group’s senior executives and managers, and to parties at interest

in the Company (hereinafter jointly, ―the Executives‖) pursuant to the requirements of

Regulation 21 of the Securities Regulations (Periodic and Immediate Reports) 1970, and the

contribution of each of them to the Company in 2012.

7.2 How the remuneration is examined:

Prior to the discussion by the Company’s Board of Directors, a detailed discussion was held

on the remuneration for each of the Company’s executives and managers, noted in said

Regulation 21, by the Company’s Remuneration Committee (hereinafter, ―the

Remuneration Committee‖), which drafted its recommendations on the subject and

presented them to the Company’s Board of Directors.

29

The Remuneration Committee is a Board of Directors’ committee set up specially to

coordinate the matter of remuneration to the Company’s senior executives, which includes

the Company’s two external directors and an additional director in the Company (who is also

an independent director).

As part of the background material for discussions on the matter by members of the

Remuneration Committee, the main points of the conditions of employment of the

Executives and the remuneration paid to Company officers in 2012 were reviewed,

explanations were presented concerning the connection between the amount of remuneration

and the contribution of each of the Executives to the Company in the reporting period

(including data presented concerning the various aspects of the results of the Company’s

operations in the areas of responsibility of the Company’s officers.

This included a presentation to the members of the Remuneration Committee of the

employment terms of the officers in AFI Development (Mssrs. Lev Leviev, Mark Groisman,

and Ms. Tzvia Leviev-Alazarov), a public subsidiary whose shares are listed for train on the

main market of the London Stock Exchange (LSE) and officers in Africa Industries (Mssrs.

Abraham Novogrotzsky in respect of his term as CEO of Africa Industries, and Avi Motola),

a public subsidiary of the Company, as well as the main points of the discussions on

employment terms conducted by the Remuneration Committee and the Board of Directors of

AFI Development and AFI Industries, respectively, and their conclusions. In view of the

public nature of these companies, which have independent boards of directors that comply

with regulatory requirements in London and Israel, as the case may be, and in view of the

fact that a discussion of the remuneration of these officers was conducted in meetings of the

remuneration committees and boards of directors of AFI Development and AFI Industries,

the Company’s Board of Directors determined that it does not consider itself in a proper

position to examine this issue and that it is convinced that there is no justification for

intervening in the determinations made by the boards of these subsidiaries regarding the

remuneration of these officers.

After the discussion by the Remunerations Committee and the drafting of its

recommendations, the background material described above was also distributed to members

of the Company’s Board of Directors. During the discussion by the Board of Directors,

members of the board were shown the main points of the discussion by the Remuneration

Committee and its recommendations on the subject. Further to the above, after the topic was

discussed, the Company’s Board of Directors decided to adopt the recommendations of the

Remuneration Committee and determined its position regarding the fairness and

reasonableness of said remuneration.

7.3 Summary of the Board of Directors’ Explanations

A. Mark Groisman

31

For details of the remuneration paid to Mr. Groisman for 2012 see Regulation 21 of the