Embed Size (px)

Citation preview

LEARNING OUTCOME

Making aware and enable how to

Utilize CENVAT Credit on Exempted Goods & Services

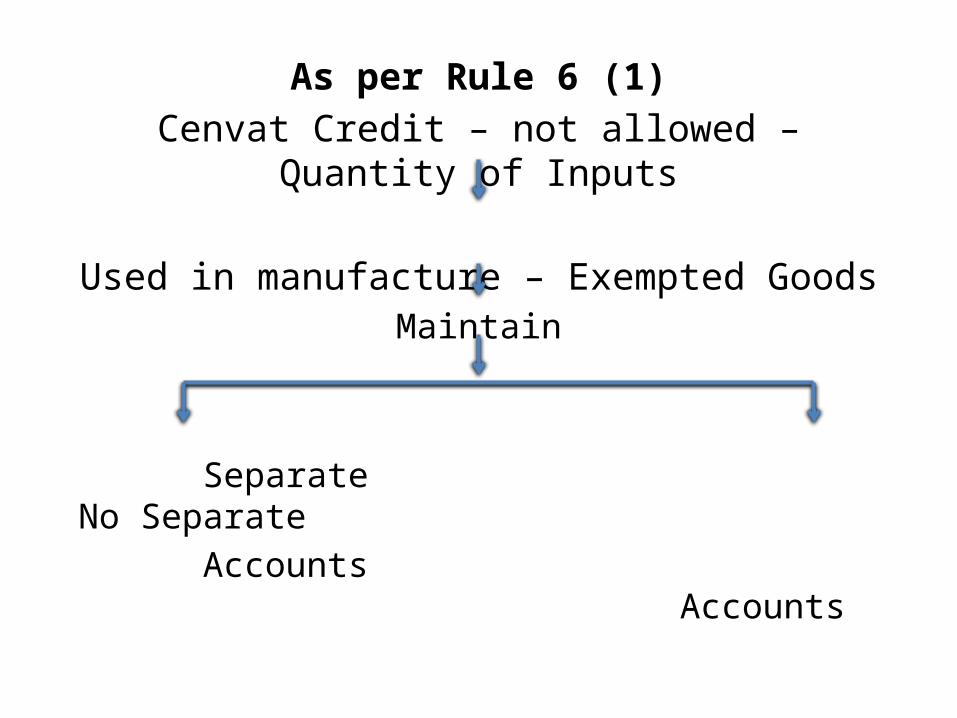

As per Rule 6 (1)Cenvat Credit – not allowed – Quantity of Inputs

Used in manufacture – Exempted GoodsMaintain

Separate No Separate Accounts Accounts

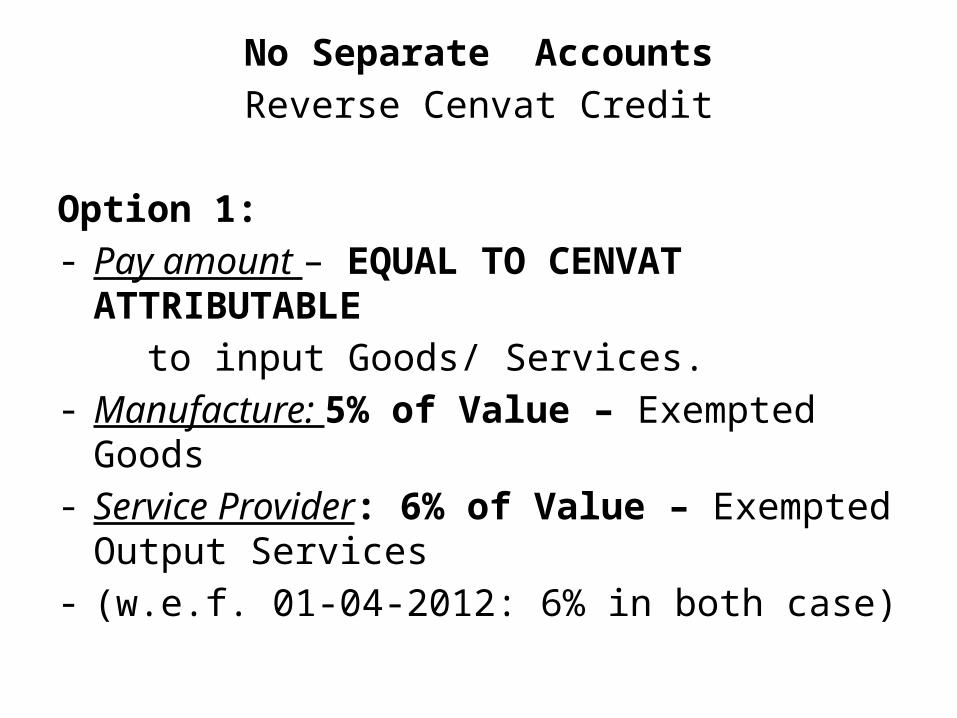

No Separate AccountsReverse Cenvat Credit

Option 1: - Pay amount – EQUAL TO CENVAT ATTRIBUTABLE to input Goods/ Services.- Manufacture: 5% of Value – Exempted Goods- Service Provider: 6% of Value – Exempted Output

Services- (w.e.f. 01-04-2012: 6% in both case)

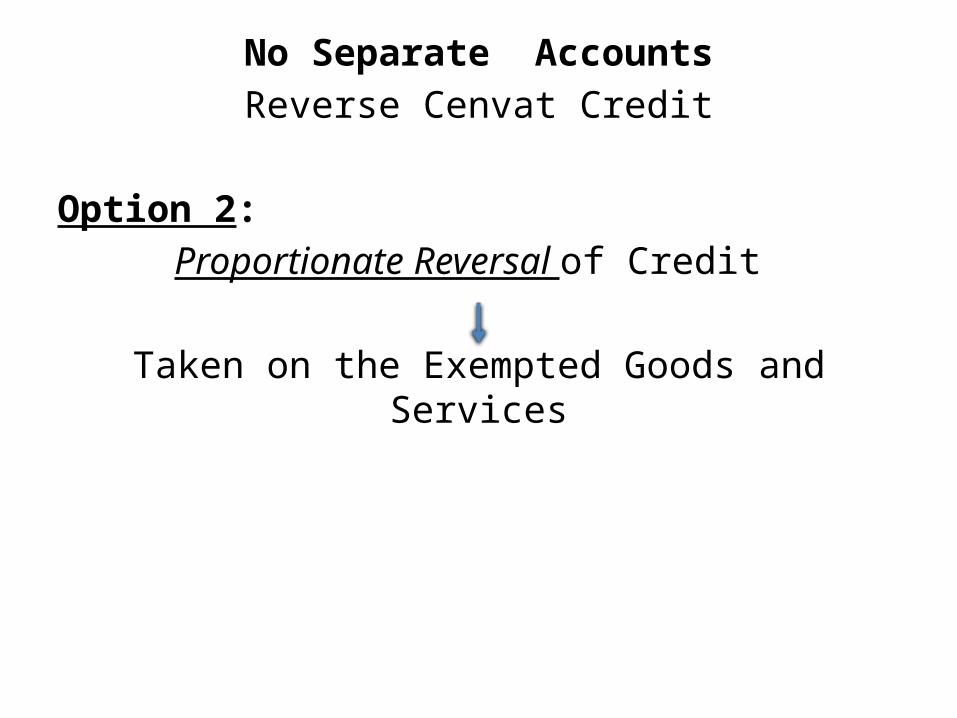

No Separate AccountsReverse Cenvat Credit

Option 2:Proportionate Reversal of Credit

Taken on the Exempted Goods and Services

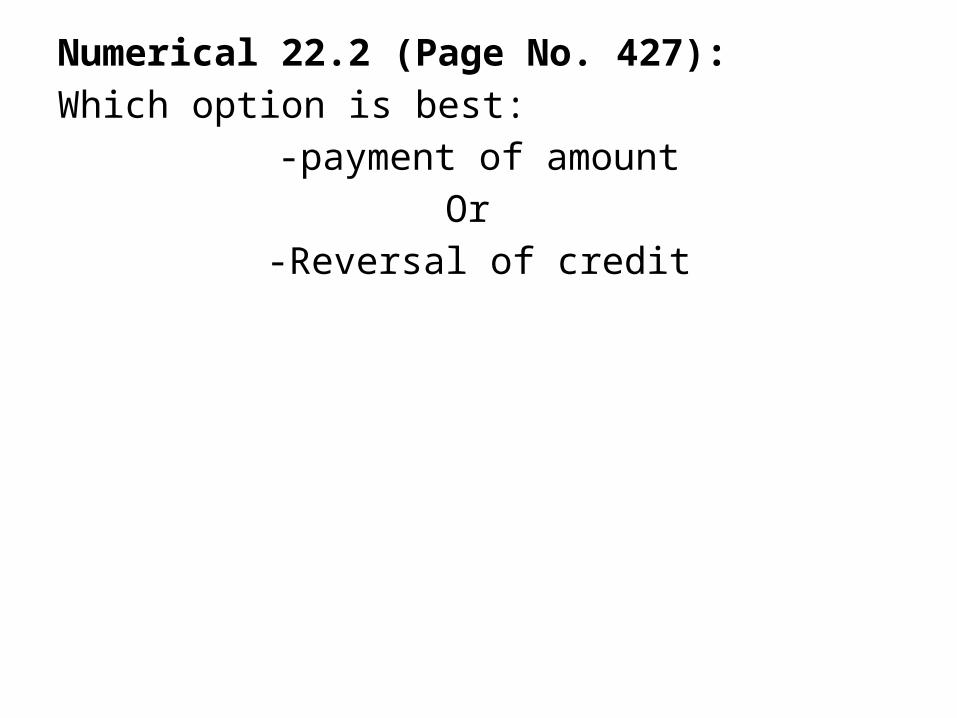

Numerical 22.2 (Page No. 427):Which option is best:

-payment of amountOr

-Reversal of credit

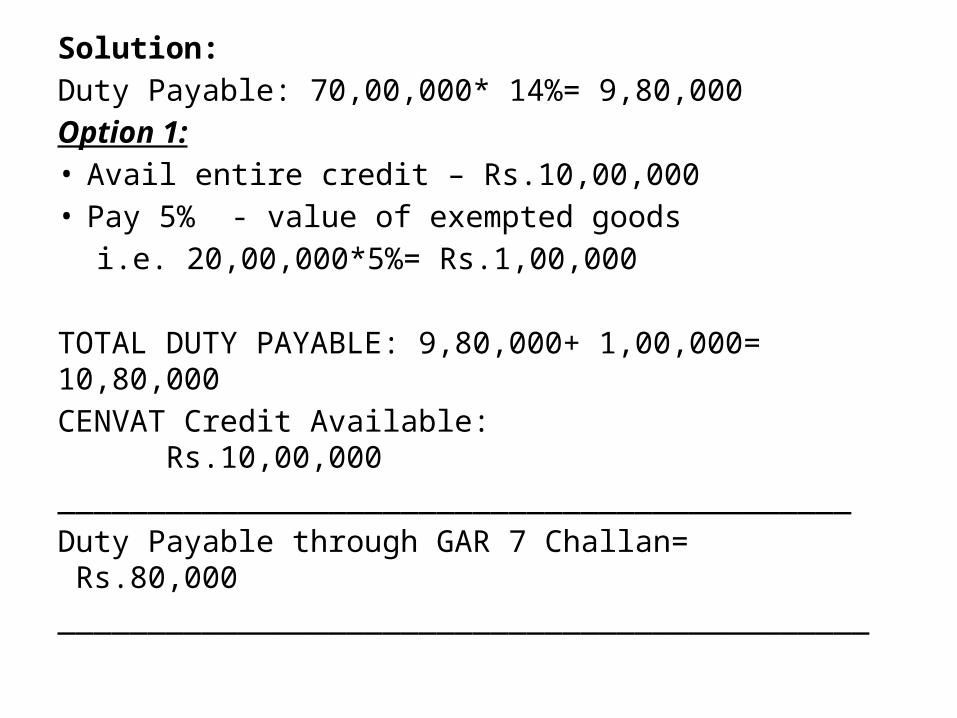

Solution:Duty Payable: 70,00,000* 14%= 9,80,000Option 1:• Avail entire credit – Rs.10,00,000• Pay 5% - value of exempted goods

i.e. 20,00,000*5%= Rs.1,00,000

TOTAL DUTY PAYABLE: 9,80,000+ 1,00,000= 10,80,000CENVAT Credit Available: Rs.10,00,000____________________________________________Duty Payable through GAR 7 Challan= Rs.80,000_____________________________________________

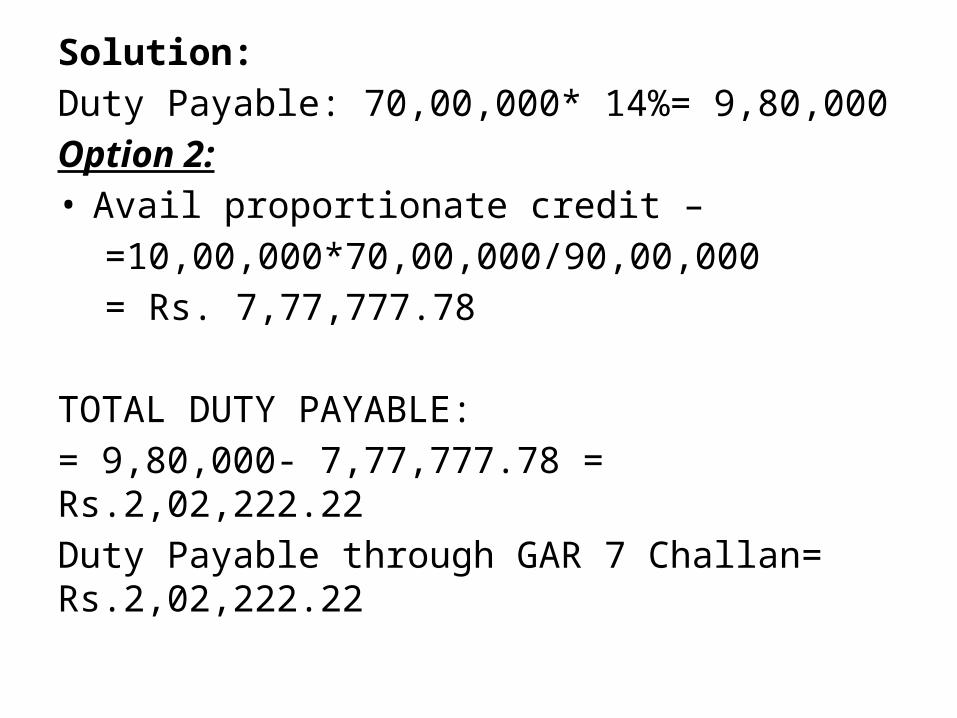

Solution:Duty Payable: 70,00,000* 14%= 9,80,000Option 2:• Avail proportionate credit –

=10,00,000*70,00,000/90,00,000= Rs. 7,77,777.78

TOTAL DUTY PAYABLE: = 9,80,000- 7,77,777.78 = Rs.2,02,222.22Duty Payable through GAR 7 Challan= Rs.2,02,222.22

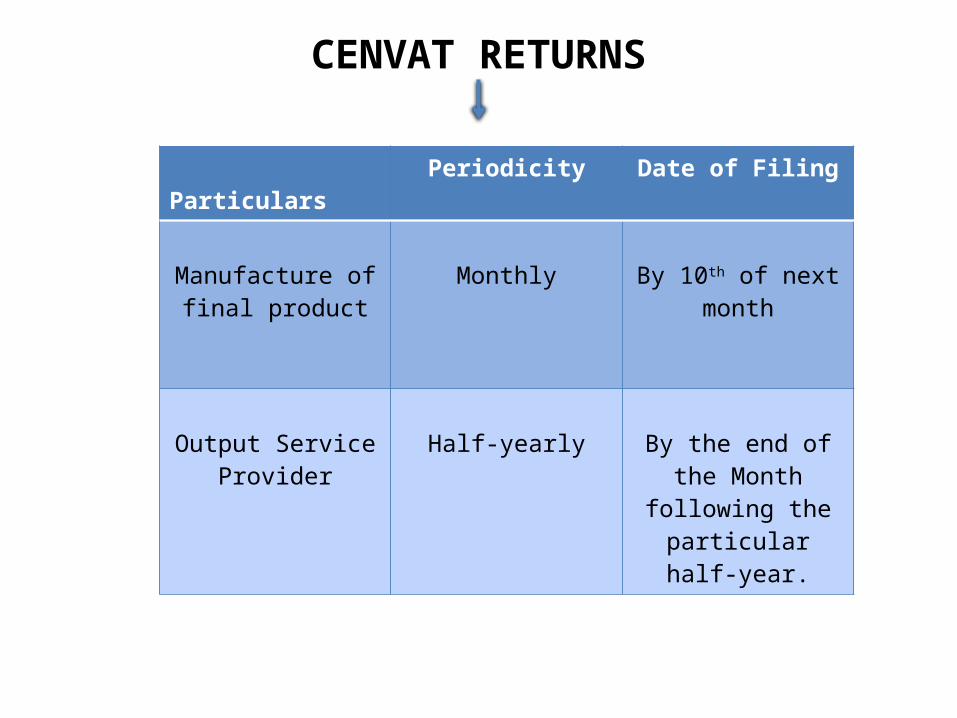

CENVAT RETURNS

Particulars Periodicity Date of Filing

Manufacture of final product

Monthly By 10th of next month

Output Service Provider

Half-yearly By the end of the Month following the particular half-year.