Embed Size (px)

Citation preview

LEARNING OUTCOME

Making awarehow to Avail and Utilize

CENVAT Credit

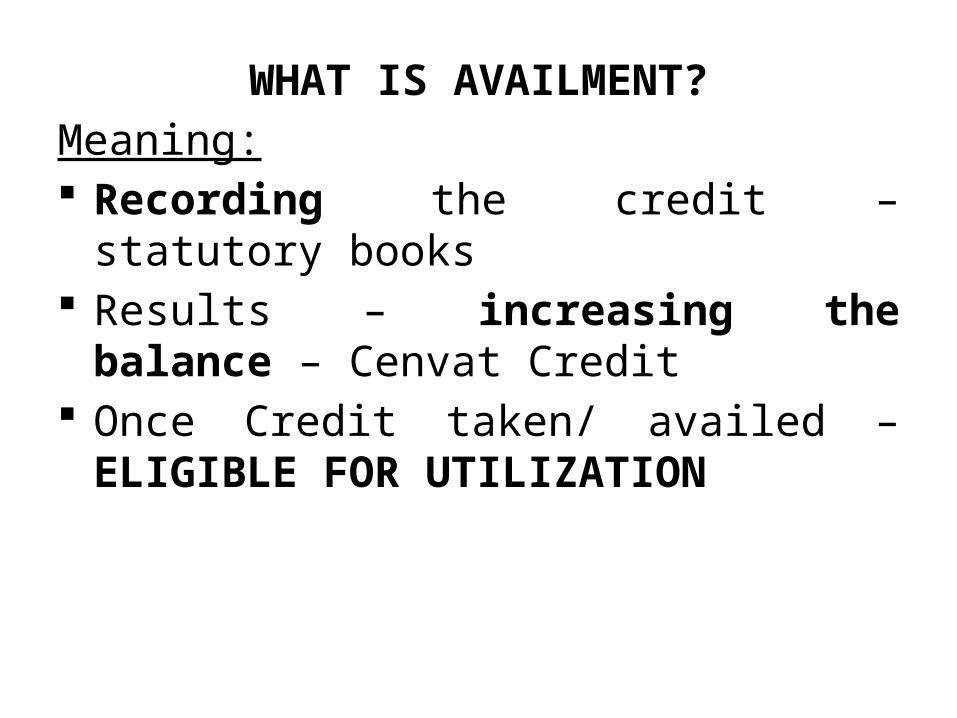

WHAT IS AVAILMENT?Meaning: Recording the credit – statutory books Results – increasing the balance – Cenvat

Credit Once Credit taken/ availed – ELIGIBLE FOR

UTILIZATION

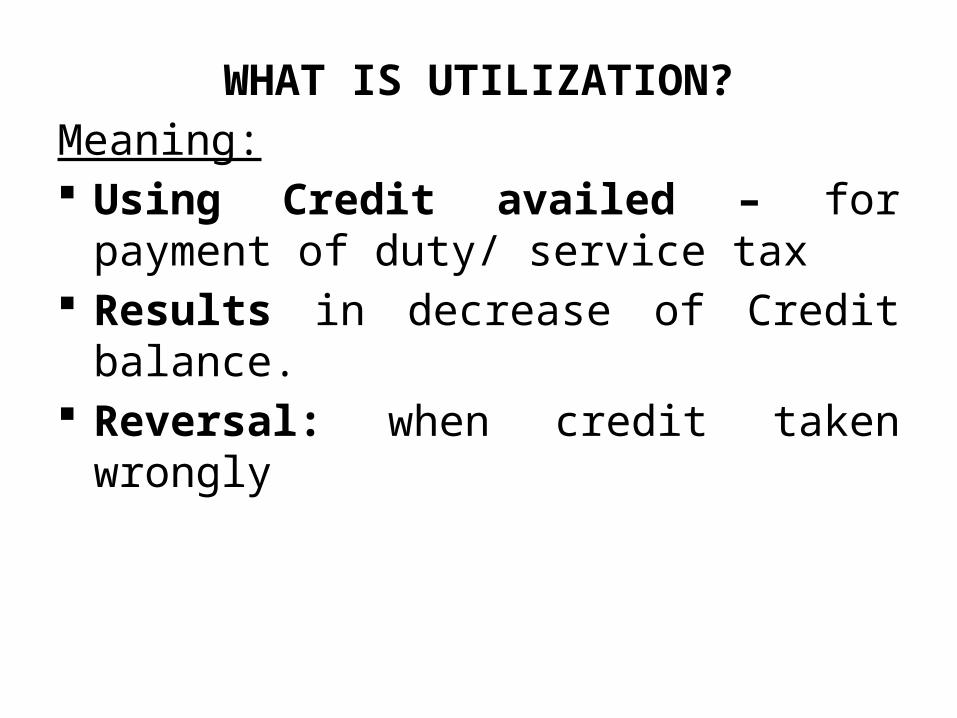

WHAT IS UTILIZATION?Meaning: Using Credit availed – for payment of duty/

service tax Results in decrease of Credit balance. Reversal: when credit taken wrongly

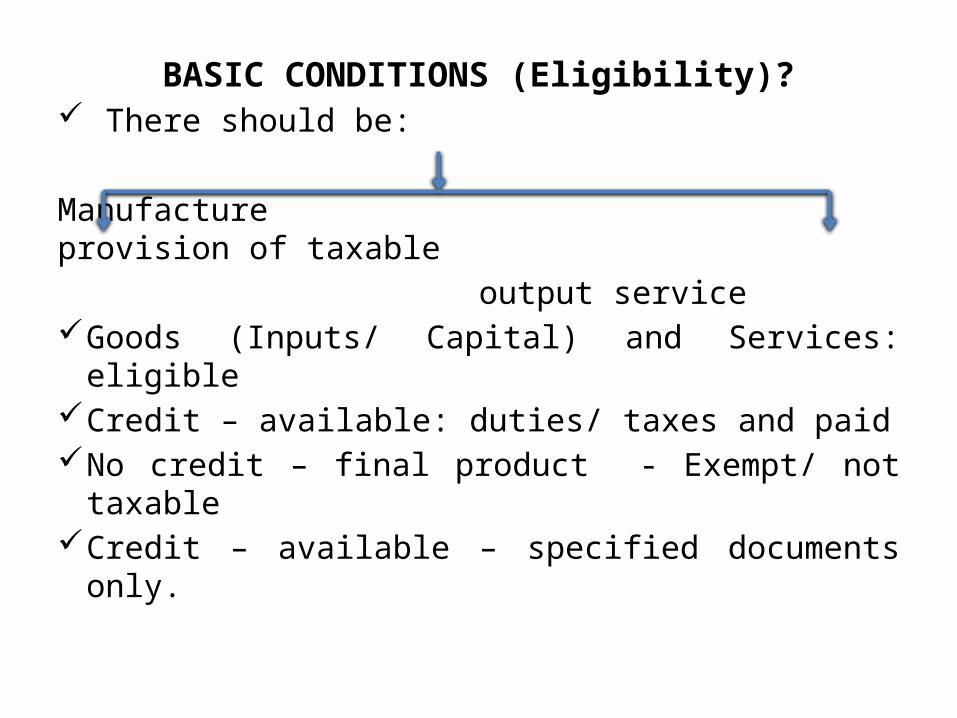

BASIC CONDITIONS (Eligibility)? There should be:

Manufacture provision of taxable output service

Goods (Inputs/ Capital) and Services: eligibleCredit – available: duties/ taxes and paidNo credit – final product - Exempt/ not taxableCredit – available – specified documents only.

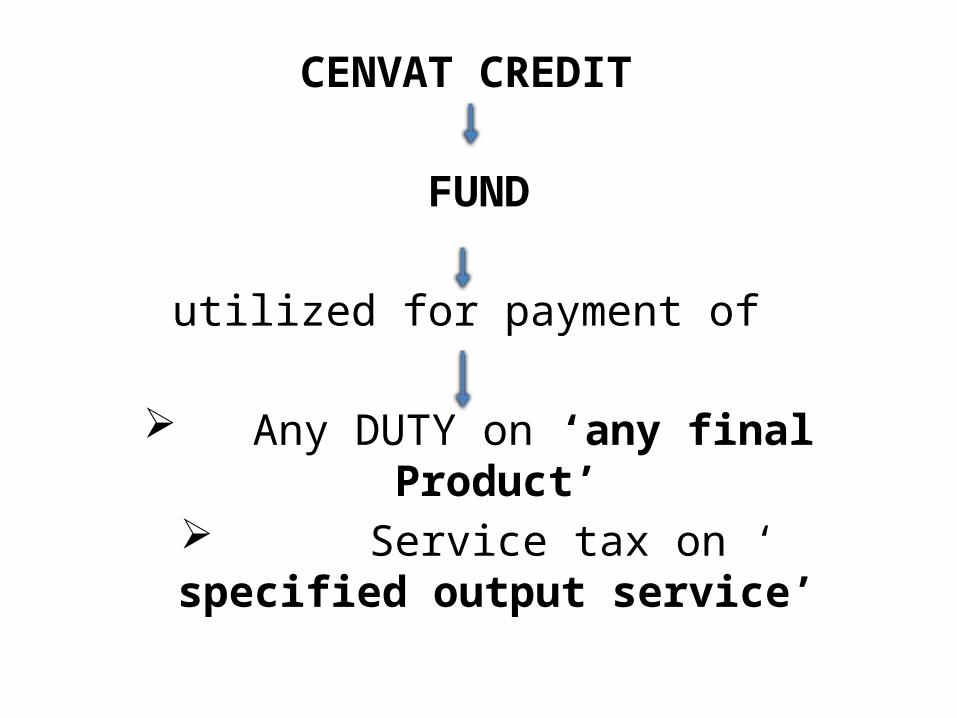

CENVAT CREDIT

FUND

utilized for payment of

Any DUTY on ‘any final Product’ Service tax on ‘ specified output service’

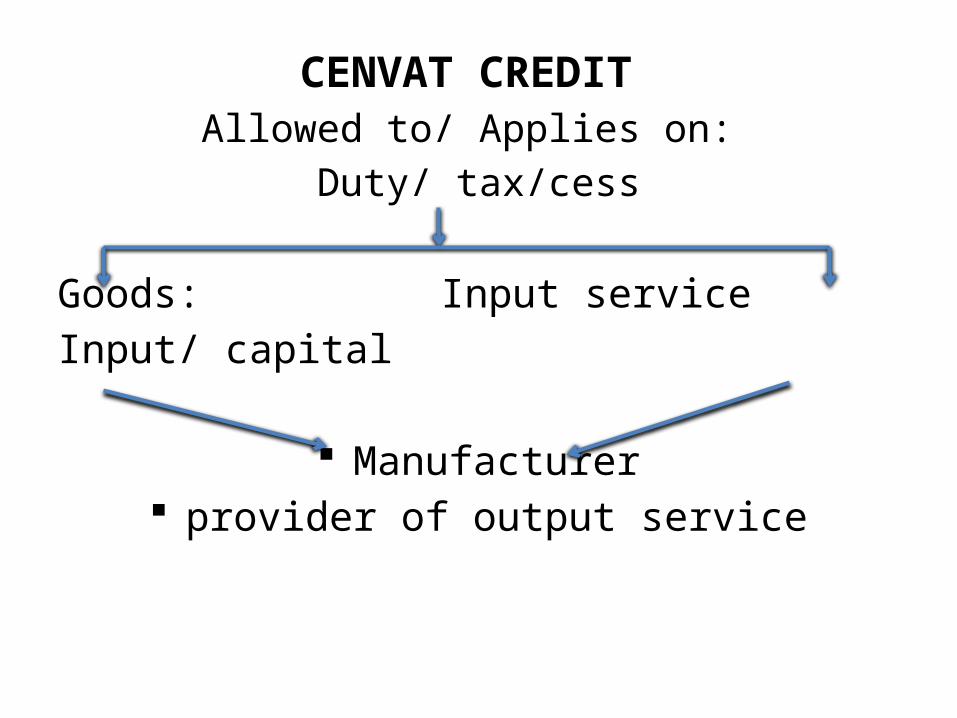

CENVAT CREDIT Allowed to/ Applies on:

Duty/ tax/cess

Goods: Input serviceInput/ capital

Manufacturer provider of output service

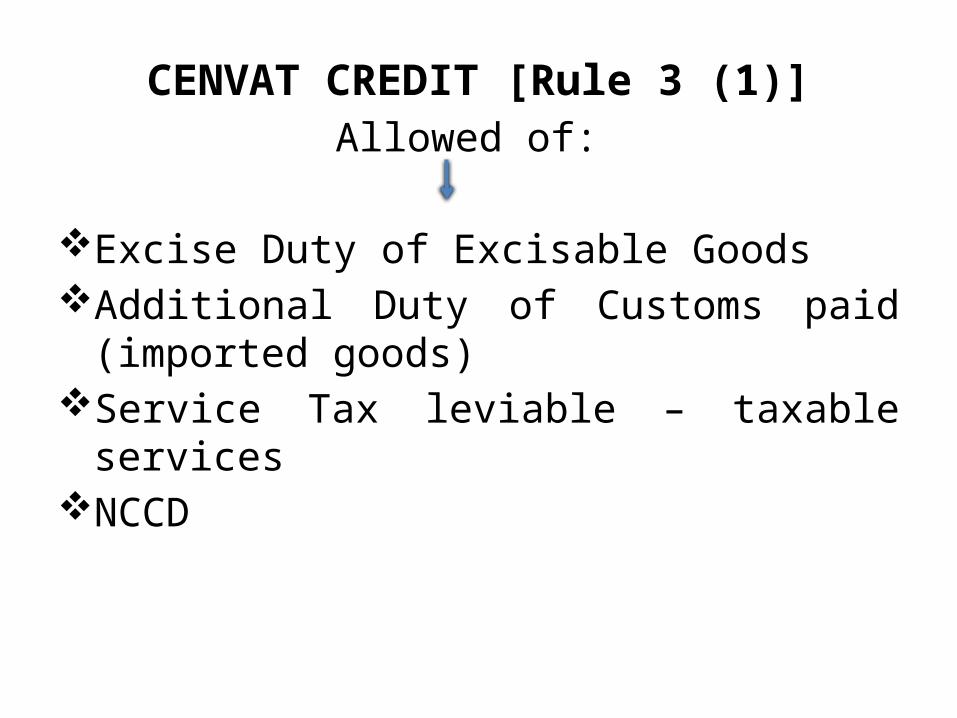

CENVAT CREDIT [Rule 3 (1)]Allowed of:

Excise Duty of Excisable GoodsAdditional Duty of Customs paid (imported

goods)Service Tax leviable – taxable servicesNCCD

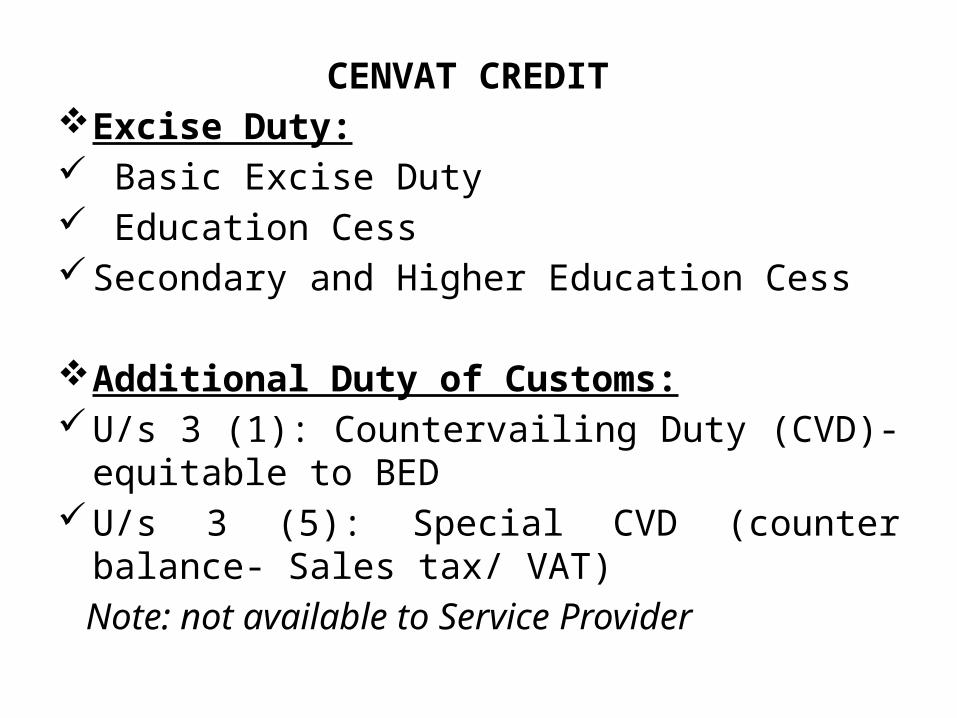

CENVAT CREDIT Excise Duty: Basic Excise Duty Education CessSecondary and Higher Education Cess

Additional Duty of Customs:U/s 3 (1): Countervailing Duty (CVD)- equitable to

BED U/s 3 (5): Special CVD (counter balance- Sales tax/

VAT) Note: not available to Service Provider

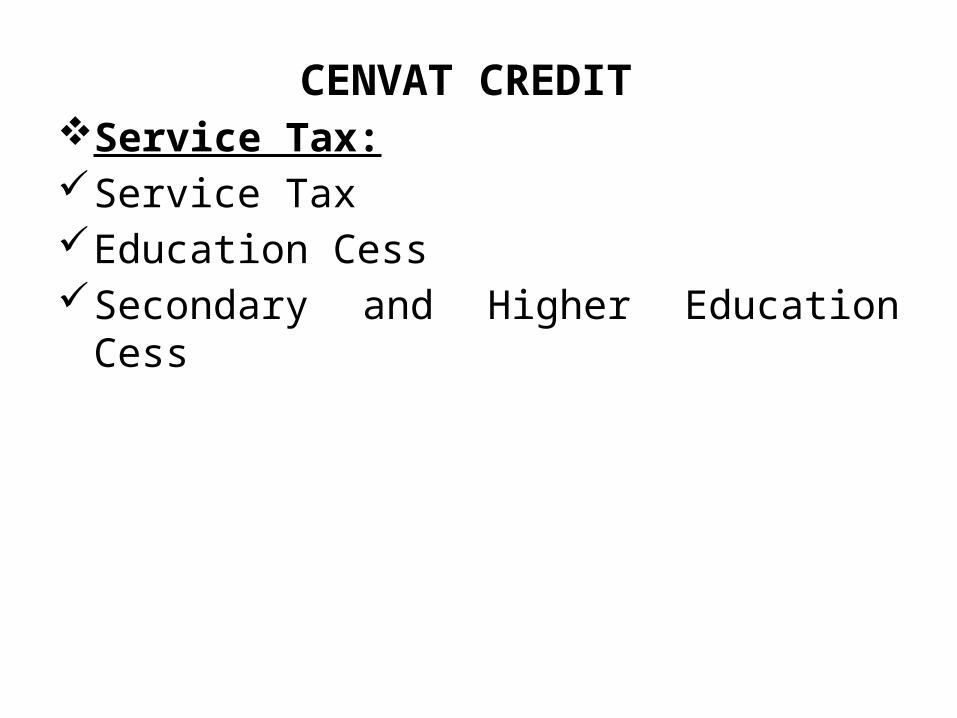

CENVAT CREDIT Service Tax:Service TaxEducation CessSecondary and Higher Education Cess

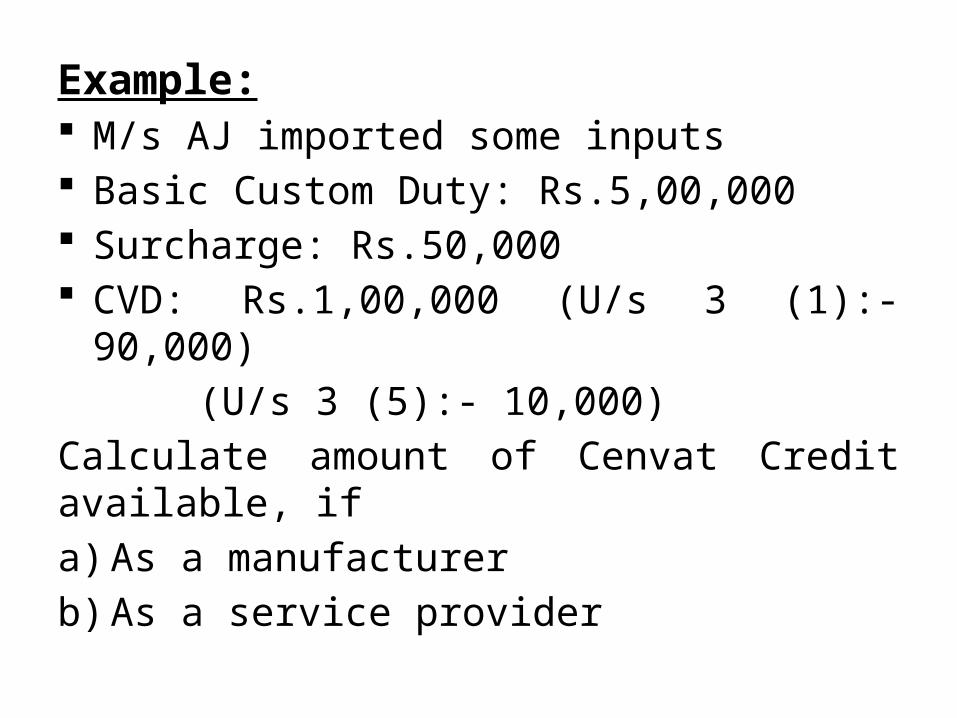

Example: M/s AJ imported some inputs Basic Custom Duty: Rs.5,00,000 Surcharge: Rs.50,000 CVD: Rs.1,00,000 (U/s 3 (1):- 90,000)

(U/s 3 (5):- 10,000)Calculate amount of Cenvat Credit available, ifa) As a manufacturerb) As a service provider

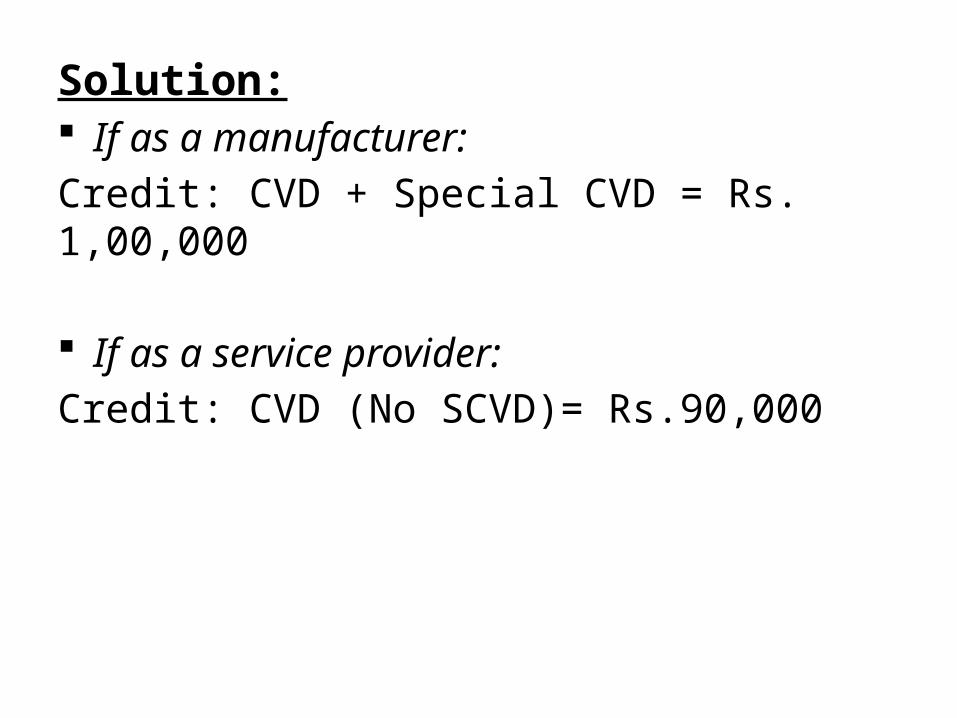

Solution: If as a manufacturer: Credit: CVD + Special CVD = Rs. 1,00,000

If as a service provider:Credit: CVD (No SCVD)= Rs.90,000

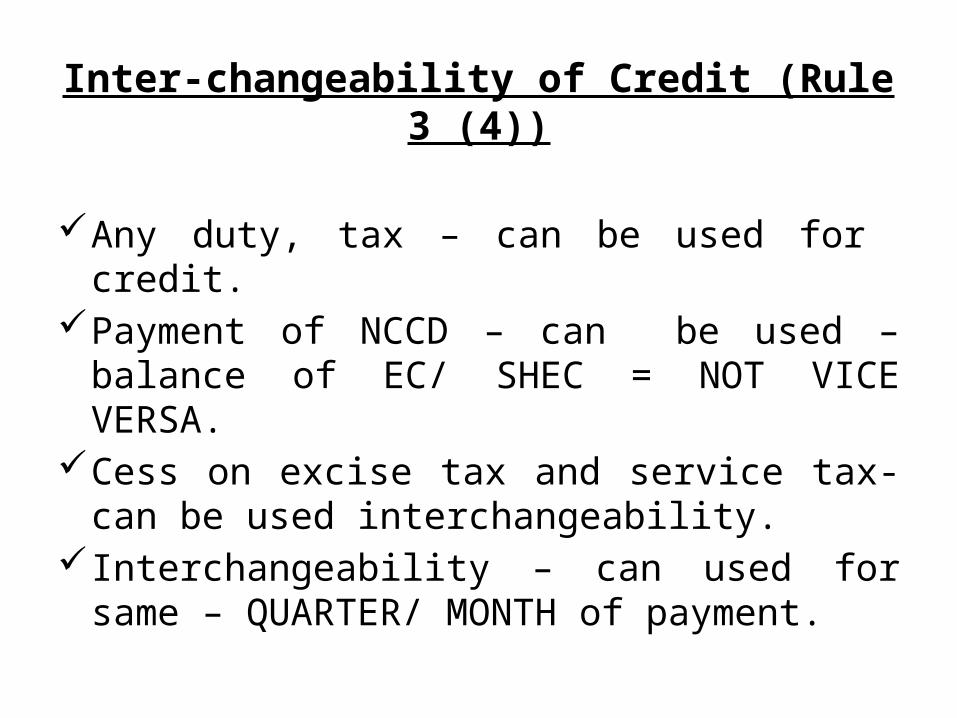

Inter-changeability of Credit (Rule 3 (4))

Any duty, tax – can be used for credit.Payment of NCCD – can be used – balance of EC/

SHEC = NOT VICE VERSA.Cess on excise tax and service tax- can be used

interchangeability.Interchangeability – can used for same –

QUARTER/ MONTH of payment.

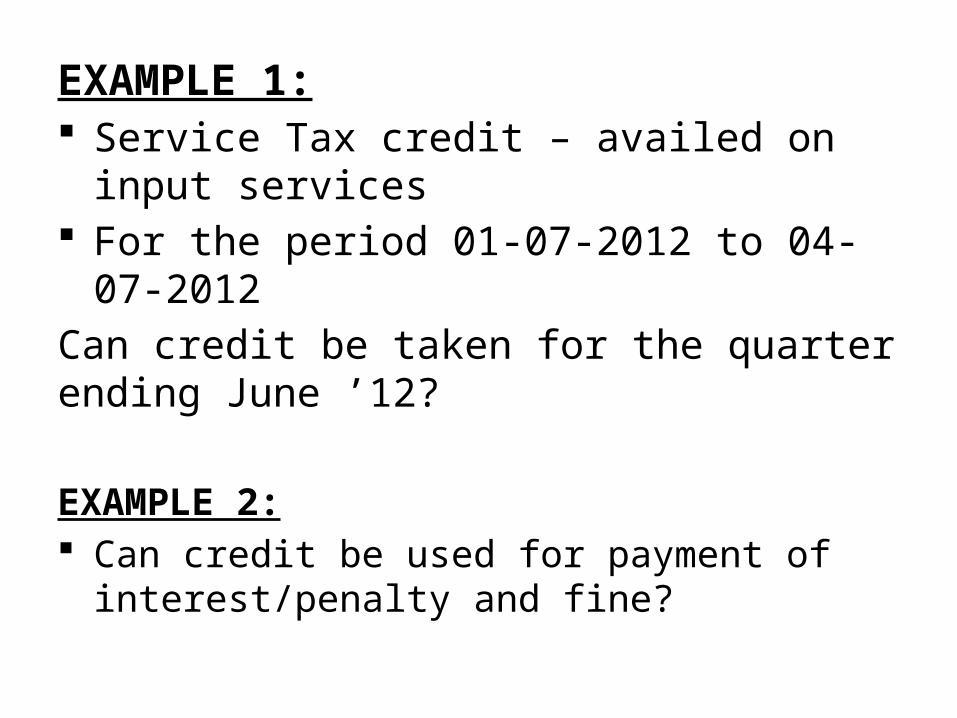

EXAMPLE 1: Service Tax credit – availed on input services For the period 01-07-2012 to 04-07-2012Can credit be taken for the quarter ending June ’12?

EXAMPLE 2: Can credit be used for payment of interest/penalty

and fine?

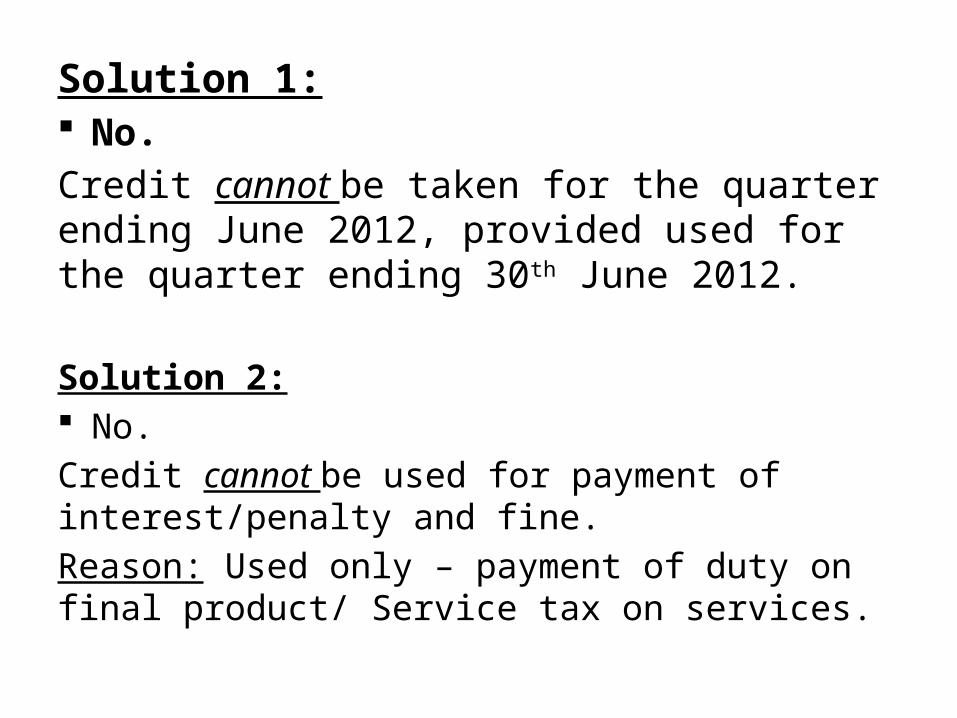

Solution 1: No.Credit cannot be taken for the quarter ending June 2012, provided used for the quarter ending 30th June 2012.

Solution 2: No.Credit cannot be used for payment of interest/penalty and fine.Reason: Used only – payment of duty on final product/ Service tax on services.

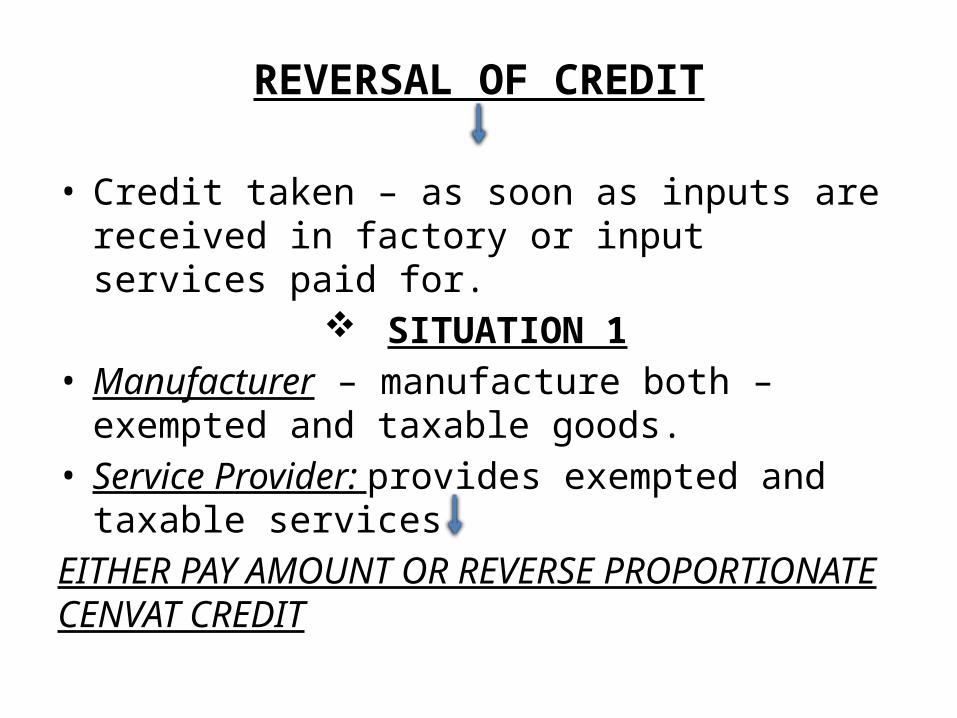

REVERSAL OF CREDIT

• Credit taken – as soon as inputs are received in factory or input services paid for.

SITUATION 1• Manufacturer – manufacture both – exempted and

taxable goods.• Service Provider: provides exempted and taxable

servicesEITHER PAY AMOUNT OR REVERSE PROPORTIONATE CENVAT CREDIT

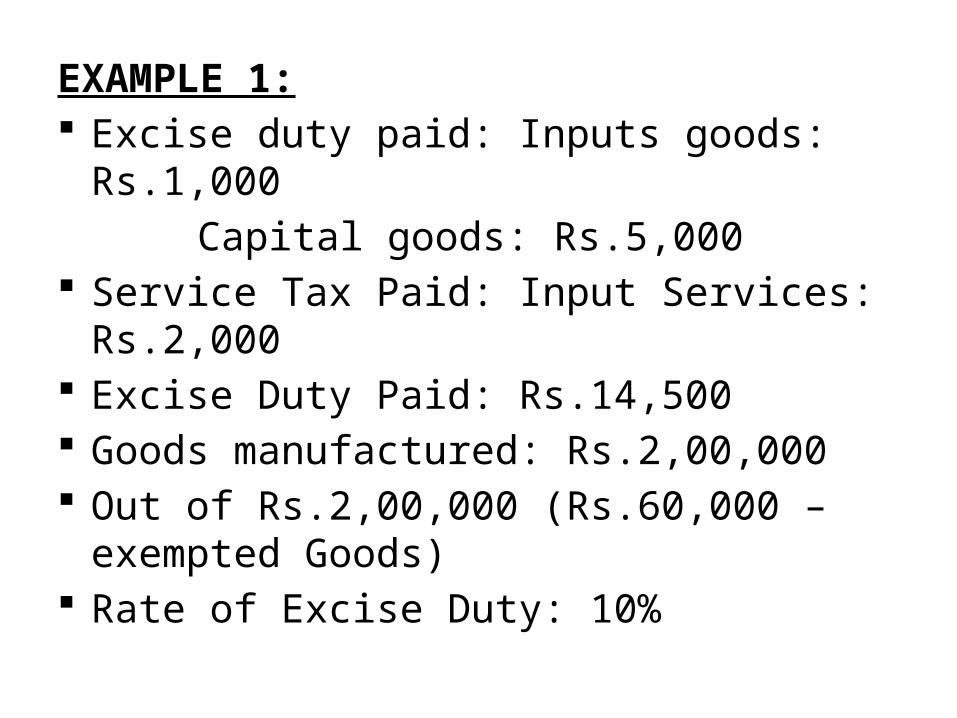

EXAMPLE 1: Excise duty paid: Inputs goods: Rs.1,000

Capital goods: Rs.5,000 Service Tax Paid: Input Services: Rs.2,000 Excise Duty Paid: Rs.14,500 Goods manufactured: Rs.2,00,000 Out of Rs.2,00,000 (Rs.60,000 – exempted

Goods) Rate of Excise Duty: 10%

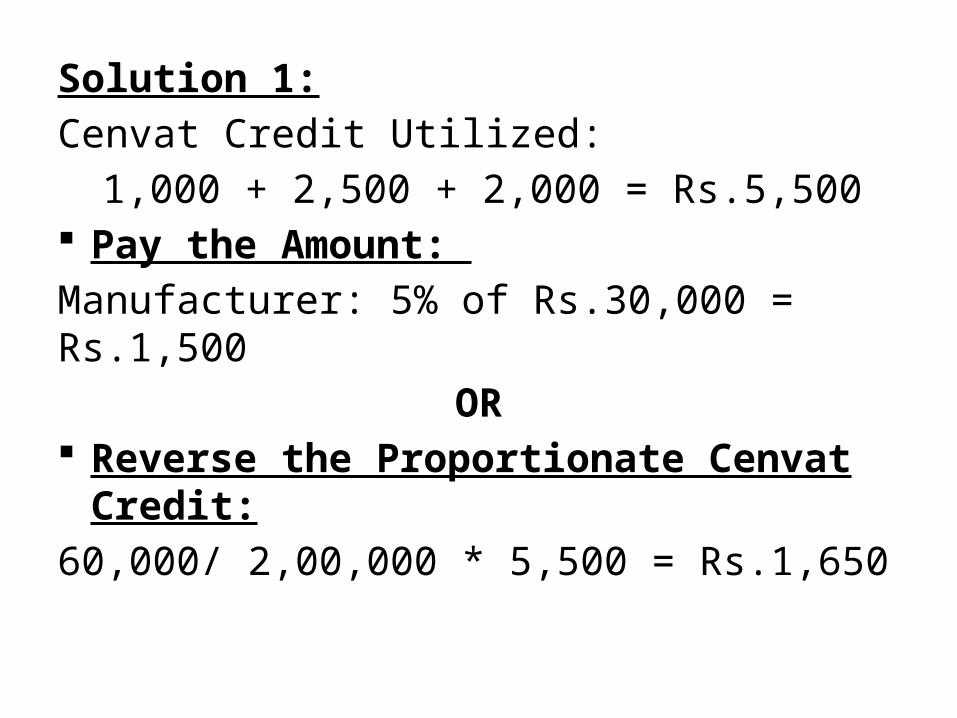

Solution 1:Cenvat Credit Utilized:

1,000 + 2,500 + 2,000 = Rs.5,500 Pay the Amount: Manufacturer: 5% of Rs.30,000 = Rs.1,500

OR Reverse the Proportionate Cenvat Credit:60,000/ 2,00,000 * 5,500 = Rs.1,650

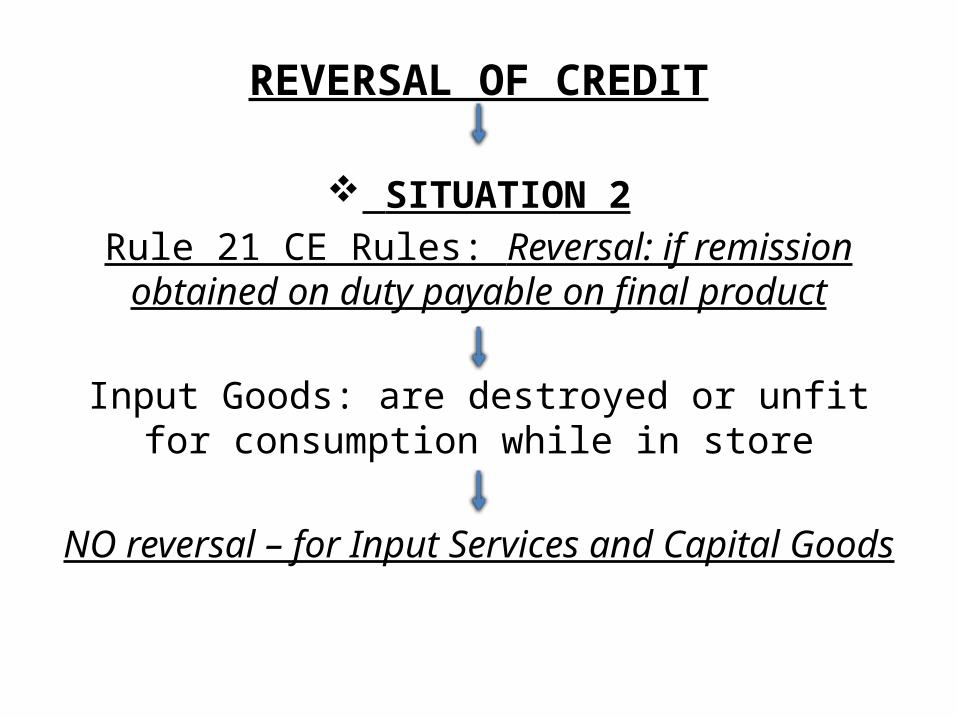

REVERSAL OF CREDIT

SITUATION 2Rule 21 CE Rules: Reversal: if remission obtained on

duty payable on final product

Input Goods: are destroyed or unfit for consumption while in store

NO reversal – for Input Services and Capital Goods

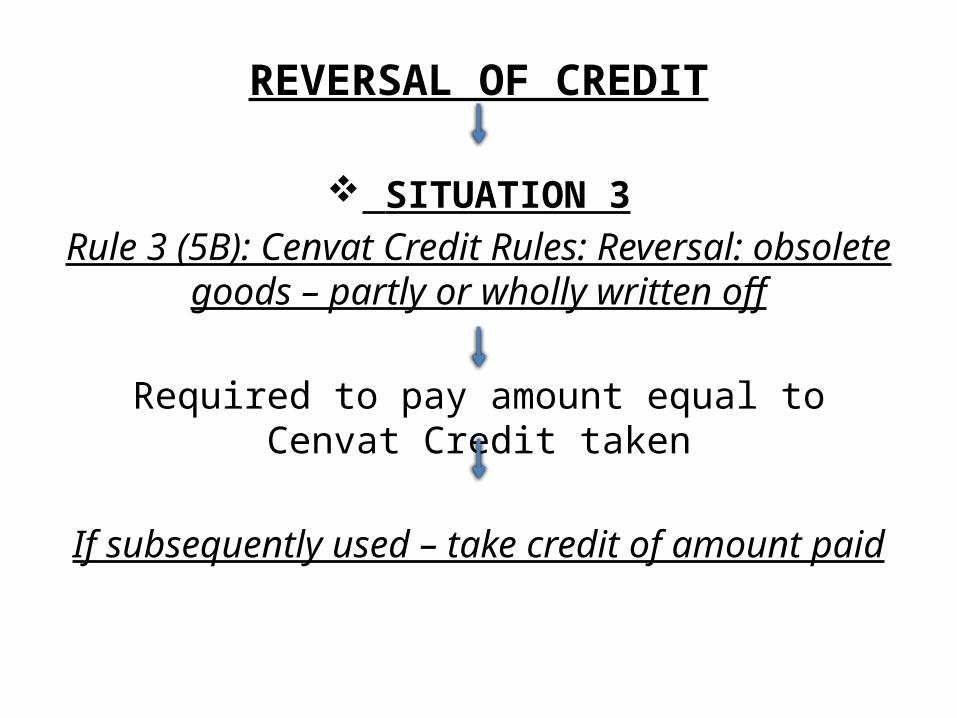

REVERSAL OF CREDIT

SITUATION 3Rule 3 (5B): Cenvat Credit Rules: Reversal: obsolete

goods – partly or wholly written off

Required to pay amount equal to Cenvat Credit taken

If subsequently used – take credit of amount paid

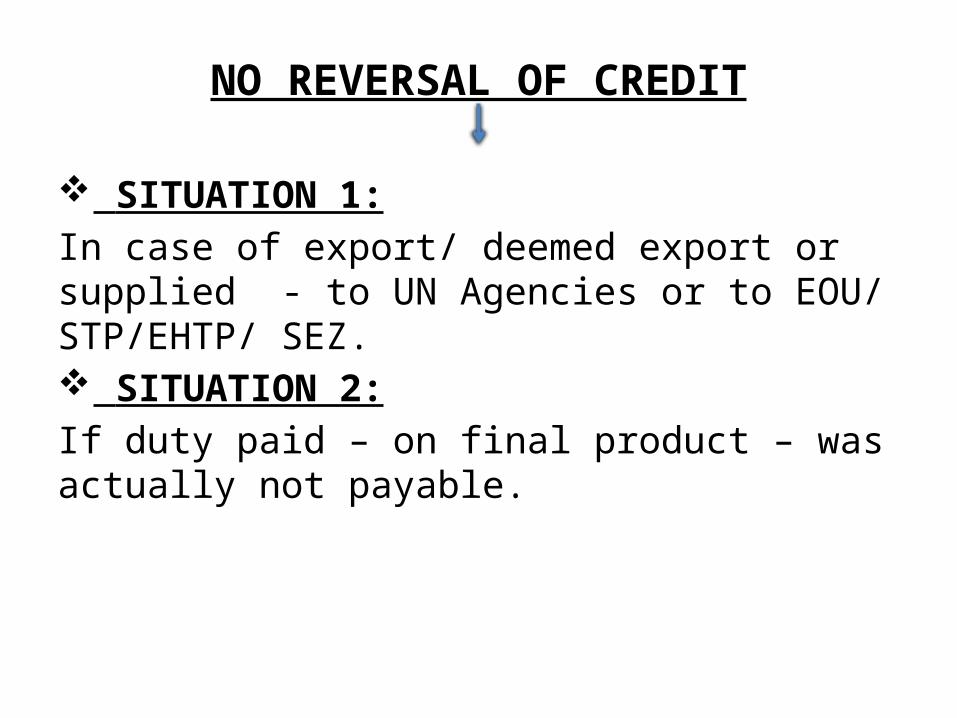

NO REVERSAL OF CREDIT

SITUATION 1:In case of export/ deemed export or supplied - to UN Agencies or to EOU/ STP/EHTP/ SEZ. SITUATION 2:If duty paid – on final product – was actually not payable.

Numerical No. 22.1 (Page No. 423)

Read:who is/ are:

- First Stage dealer- Second Stage dealer on (Page No. 409)

Duty paying documents for cenvat (Page Nos. 406 to 408)

Responsibility of person taking cenvat credit (Page No. 410)